Embed Size (px)

Citation preview

Academic paperMaking the most of corporate socialresponsibility reporting: disclosurestructure and its impact on performance

Clodia Vurro and Francesco Perrini

Abstract

Purpose – Examining a three-year disclosure experience of a sample of Fortune 100 global companies,

the paper aims to propose and test a model that relates the structure of CSR disclosure to corporate

social performance. Based on the results obtained, it proposes to draw implications for emerging

economies.

Design/methodology/approach – Combining content analysis of CSR reports and corporate social

performance data, the paper built a longitudinal dataset starting from the population of worldwide

companies included in the AccountAbility Rating between 2004 and 2007. Longitudinal regression

analysis is performed on a final sample size of 114 firm-year observations involving 38 firms over a

three-year period.

Findings – The paper finds evidence that the level of disclosure does not improve firm ability to manage

stakeholders. However, a finer-grained analysis of the structure of disclosure shows that better social

performers are those who increased the breadth of their disclosure to stakeholders and uniformly

distributed disclosure across stakeholders.

Research limitations/implications – Results provide an empirical test for the theories describing true

responsible economic actors as those who are able to combine high engagement with the social context

of reference and balanced coverage of diversified interests. However, the study suffers the usual

limitations of content analysis-based research, as well as exclusively relying on CSR disclosure by large

corporations.

Practical implications – Findings suggest not only the importance of structuring the report in a

comprehensive way, and extending coverage to multiple stakeholders and related issues, but also the

need for balance between informative needs, thus avoiding concentrated structures. Accordingly,

companies that report on more themes, presenting a balanced and comprehensive product, develop a

better ability to manage their stakeholder network, thus gaining higher corporate social performance.

Originality/value – The study seeks to revisit the relation between CSR disclosure and corporate social

performance, answering the request for more rigorous measures. It goes beyond the level of disclosure

as a comprehensive proxy of firm-stakeholder dialogue and demonstrates how a finer-grained analysis

of the structure of disclosure can be a better predictor of superior performance.

Keywords CSR disclosure and reporting, Corporate social responsibility, Social responsibility,Corporate social performance, Emerging markets

Paper type Research paper

Introduction

With the renewed expectations of corporate conduct within a global stakeholder society and

the Global Reporting Initiative (GRI) publishing the third version of its Sustainability

Reporting Guidelines in 2006, recent years have witnessed a substantial shift in corporate

practices, with disclosure on corporate social responsibility (CSR) becoming the norm

instead of the exception across industries and regions.

DOI 10.1108/14720701111159280 VOL. 11 NO. 4 2011, pp. 459-474, Q Emerald Group Publishing Limited, ISSN 1472-0701 j CORPORATE GOVERNANCE j PAGE 459

Clodia Vurro and

Francesco Perrini are

based in the Department of

Management and

Technology, Universita

Commerciale ‘‘Luigi

Bocconi’’, Milan, Italy.

Both the design and implementation of CSR reporting procedures[1] have definitely become

the cornerstone of the CSR movement, a result of the growing awareness, shared by both

research and practice, of the competitive benefits enjoyed by firms that integrate wider

economic, environmental, and societal concerns into their ongoing operations and

interaction with stakeholders, on a voluntary basis and beyond legal prescriptions (Vogel,

2005).

A means of understanding and tracking social and environmental impacts, by creating a

platform for stakeholder dialogue, effective CSR reporting is intended in and of itself to

improve stakeholder-related performance (corporate social performance, CSP). In fact, CSR

reporting is a source of information vital to internal decision making, enabling companies to

identify strengths and weaknesses across the whole corporate responsibility spectrum that

in turn measure the value of long-term relationships and assets. In addition to strengthening

internal systems and decision making, effective measuring through CSR reports helps

companies to manage external relationships as well, attracting stakeholders who favor

socially responsible business and have the power to reward it (Waddock and Bodwell,

2004). In fact, CSR disclosure and reporting actively supports stakeholder dialogue by

mapping, measuring, systematizing, and communicating what firms accomplish in the area

of stakeholder-related CSR (Nitkin and Brooks, 1998).

While the broad focus on measurement has raised both awareness of the importance of CSR

reporting and excitement about its potential, accountability and reporting standards have

also increased exponentially. With such a burgeoning supply of more or less authoritative

advice, companies face the daunting challenge of how to optimize standard selection and

implementation. In particular, has the structure of disclosure through social, environmental

and sustainability reports an impact on the ability of firms to manage the dialogue with

stakeholders, thus leading to improved CSP?

Though recognizing CSR disclosure and reporting as the natural operationalization of CSR,

that is, the managerial effort to understand and track social and environmental impacts while

contributing to an ongoing stakeholder dialogue (Cooper and Owen, 2007; Greenwood,

2007), whether and how CSR reporting has an impact on CSP are still open to debate. If CSR

reporting improves the management of stakeholders’ concerns and requests, then

investigating its performance consequences is vitally important.

To empirically address the research question above, we reviewed the three-year CSR

reporting experience of a sample of Fortune 100 global companies, relating the level and

structure of social and environmental disclosure to CSP. We adopted a stakeholder-based

framework to formalize and test a set of hypotheses, and we found evidence that the mere

level of disclosure does not translate into CSP improvement, as much as its structure.

According to the theoretical basis of stakeholder engagement and accountability (Freeman,

1984; Rasche and Esser, 2006), the best social performers broaden the scope of their

disclosure beyond the narrow set of critical areas (e.g. environmental impacts and health

and safety in human resource management) to the various external stakeholders. Moreover,

the extent to which disclosure is concentrated or uniformly distributed across stakeholders is

key to CSP, with negative impacts associated to more concentrated structures.

Beyond testing the effectiveness of the CSR disclosure level and structure in improving CSP,

our study provides hints that can be potentially extended to accountability approaches in

emerging markets. In fact, recent studies show how, despite different in emphasizing

motivations to disclose and engage in stakeholder dialogue, emerging economies tend to

be generally aligned with their western counterparts in approaches and types of CSR

activities (Alon et al., 2010; Muller and Kolk, 2009; OECD, 2005). In this context, international

surveys and academic researches highlight the growing importance of emerging

economies as adopters of tools and methodologies to manage stakeholder dialogue, both

to respond to pressing requests from western and local large buyers and international

institutions (KPMG, 2008; Min Foo, 2007).

Based on existing literature, we highlight the contributions of our framework, research

hypotheses and results to the debate on the dynamics and use of CSR reporting in emerging

PAGE 460 jCORPORATE GOVERNANCEj VOL. 11 NO. 4 2011

economies. In particular, though we relied on a sample of Fortune 100 global companies, we

point out to the relevance of our findings given an increasing convergence between the

practice of reporting in emerging economies and that of western countries. In particular,

structuring CSR reporting in a way that improves firm ability to manage its stakeholder

network is even more important in emerging markets, in that the main motivations to engage

in social and environmental accountability processes is strictly related to the need to answer

to the requests of influential global actors, such as multinational corporations operating

abroad, NGOs and international institutions and local governments. Finally, our findings

suggest how to fill the reporting gaps between emerging and developing countries in

managing stakeholder consensus in an increasingly global competitive arena.

In the sections that follow, we first locate our research within the most relevant literature on

CSR reporting and develop specific hypotheses. In so doing, the relevance of CSR reporting

in emerging economies is highlighted. Then, we present our methodology and related

results, to end up with discussion and implication.

Theoretical background and hypothesis development

Born of the so-called social accounting movement in the 1970s and aimed at broadening the

scope of accountability to various internal and external stakeholders, CSR reporting have

become key in discussions of the relationship between business and society.

This tendency is the most direct outgrowth of the changing social ethos that has redefined

the notion of a corporation’s social responsibilities in a stakeholder society (Post et al., 2002).

The related call for increased stakeholder engagement aimed at both enhancing company’s

sensitivity to its context of reference and the context’s understanding of the dilemmas facing

the organizations has produced a need for new ways of identifying, measuring and reporting

on social and environmental impacts. In the search for a fit between company behavior and

the demands of the relevant stakeholders, the development of CSR reporting practices have

attempted to satisfy that need while maximizing companies’ chance for survival.

Over time, theoretical and empirical investigations have converged on identifying multiple

underlying drivers of the impact of CSR disclosure on corporate social performance. First of

all, superior performers are expected to have an incentive to disclose their commitments and

attainments in fields other than the relationships with shareholders (Verrecchia, 1983).

Disclosure through ad hoc reports acts as a signaling exercise aimed at differentiating the

company in the eye of interested stakeholders, thus avoiding potential adverse selection

risks and the exposure to future social costs (Dye, 1985).

At the same time, acting within social contexts made of changing, reciprocal expectations,

companies face social and political pressures to act in ways that are socially desirable

(Abbott and Monsen, 1979). In this sense, disclosure and reporting function as legitimacy

devices realigning stakeholder perceptions and expectations about actual changes in

corporate behavior, highlighting accomplishments in critical areas, justifying intentions, acts

and omissions (Patten, 2002). In other words, CSR disclosure allows firms to control for

potential legitimacy threats, thus improving CSP by means of its favorable impact on

stakeholder perceptions. Since stakeholders will favor the company they view as legitimate,

appropriate disclosure and reporting contribute to make stakeholders aware that corporate

procedures are fair.

Finally, beyond cost-benefit analysis and the pressures coming from the context, the

practices of CSR disclosure mirror certain adaptive managerial styles to dealing with an

increasingly dynamic environment (Bowman and Haire, 1975). Accordingly, reporting is a

tool to improve managerial awareness of and control over the social impact of corporate

activities, a vehicle toward the development of a better ability to manage stakeholder

relationships turning into improved CSP.

Though research has disproportionally addressed CSR reporting practices in developed

countries, attention has recently grown for CSR in emerging countries (Alon et al., 2010;

Belal and Momin, 2009), mostly Brazil, Russia, India and China (BRIC). In fact, pressures

VOL. 11 NO. 4 2011 jCORPORATE GOVERNANCEj PAGE 461

from international lending agencies (such as the World Bank), government regulations and

the desire to achieve listing on the international stock markets have brought large local

companies to adopt CSR disclosure and reporting practices as legitimacy tools to

addressed changing institutional requests (Islam and Deegan, 2008; Rahaman et al., 2004).

At the same time, influential stakeholder groups, such as international non-governmental

organizations, have started asking multinational corporations operating in emerging

countries to be accountable for the practices of their local subsidiaries, thus fostering the

diffusion and adoption of Western practices (Husted and Allen, 2006). As a result, a growing

number of empirical studies is supporting an increasing convergence between developed

and emerging economies on considering CSR reports as a managerial tool to support

firm-stakeholder dialogue (Muller and Kolk, 2009; Tencati et al., 2008).

Yet, despite increasing theoretical recognition of the importance of investigating the impact

of CSR reporting on the aggregate ability of an organization to respond to anticipated or

existing social demands (i.e. CSP), the questions whether CSR disclosure contributes to

improved CSP and how best to structure accountability processes behind CSR disclosure to

improve performance both deserve further investigation (Clarkson et al., 2008).

As a whole, existing research implicitly converge on the following conclusion. If companies

want to succeed in improving stakeholder management and social responsibility, they have

to measure and communicate their commitment to CSR systematically. In this sense, CSR

disclosure is expected to predict corporate social performance in that the former mirrors the

latter, that is, CSR disclosure is a transparent representation of firms’ CSR accomplishments,

impacts, and expected results (Orlitzky et al., 2003). If the above is true, then the more an

organization engages with its stakeholders, the stronger the need is to be accountable

toward them in disclosing non-financial information and the larger the impact on social

performance becomes.

Accordingly, an increase in the quantity of information disclosed through non-financial

reports – what we call disclosure depth – should represent a stronger commitment to CSR

(Gelb and Strawser, 2001) and thus lead to better performance.

Our hypothesis follows:

H1. The higher the depth of non-financial disclosure by firm i at time t, the higher the

corporate social performance at time t þ 1.

But is it just the level of disclosure (i.e. disclosure depth) that influences performance,

supporting the empirical, simplistic ‘‘the more the better’’ maxim? Aggregate measures of

CSR disclosure quantity miss the opportunity to distinguish between companies that differ in

the extent to which they include different stakeholders and stakeholder-related areas. On the

contrary, if we view CSR disclosure and reporting as a management process with the goal of

improving social performance, the more firms are able to extend their social responsibilities

over a broad set of stakeholders and related issues – what we call disclosure breadth – the

higher their social performance. Thus we hypothesize:

H2. The larger the breadth of non-financial disclosure by firm i at time t, the higher the

corporate social performance at time t þ 1.

What distinguishes stakeholder theory from other theories of the firm is its reliance on the

crucial assumption that the interests of all legitimate stakeholders have to be considered

equally, because of their intrinsic value (Donaldson and Preston, 1995) for a firm to be truly

responsible. However, the above assumption does not imply that stakeholders behave in the

same way toward each firm, nor that all firms treat relationships the same way. Even though

the interests of all stakeholders are normatively legitimated, firms have to be able to develop

a balance between often conflicting, costly interests, in light of the respective contributions,

costs, and risks of each stakeholder group (Mitchell et al., 1997). Unavoidably, firms will

prioritize some stakeholder claims over others. As a result, given the same disclosure

volume and coverage, a firm that concentrates on a single or few stakeholders is not

PAGE 462 jCORPORATE GOVERNANCEj VOL. 11 NO. 4 2011

necessarily similar to a firm that can distribute its attention more equally to a broader set of

stakeholders. Thus we hypothesize:

H3. The less homogeneous the distribution of non-financial disclosure by firm i at time t

among stakeholders, the lower the corporate social performance at time t þ 1.

Methodology

Sample

Since the purpose of the research is to assess the extent to which disclosure level and

structure are predictors of corporate social performance, we needed to focus on a sample of

companies for which it was possible to measure all the variables consistently. Accordingly,

we built a longitudinal dataset, employing data from the population of worldwide companies

included in the accountability rating between 2004 and 2007 and publishing a CSR report.

Merging the accountability rating database used for the dependent variable (corporate

social performance) with published reports used for the independent variables (disclosure

breadth, disclosure depth, and disclosure concentration), yielded a final sample size of 114

firm-year observations involving 38 firms. The remainder of the section describes the details

of variable operationalization.

Dependent variable

Corporate social performance. To explore the causal relationship between disclosure level,

disclosure structure, and performance, an external measure of corporate social

performance was required. Many previous studies of social and environmental

performance relied on scores provided by external rating agencies (see for example

Clarkson et al., 2008; Hughes et al., 2001; Waddock and Graves, 1997). Accordingly, we

operationalized corporate social performance as the score provided by AccountAbility

Rating from 2004 and 2007. A note is due on the potential endogeneity risk arising from the

way disclosure structure and corporate social performance was respectively measured. We

cannot completely exclude that rating assigned by the agency to firms may have relied upon

information disclosed through CSR reports. If this was the case, one could ask herself

whether disclosure measures and performance are actually the same. In order to minimize

this risk, we first referred to previous studies using rating scores as measures of

performance (Abbott and Monsen, 1979; Waddock and Graves, 1997). They converge on

recognizing rating as the most reliable secondary source to measure social or environmental

performance. Moreover, we went into the details of AccountAbility’s rating process. In

particular, though reporting is one of the source used by the agency to formulate its rating, it

is not the only one. AccountAbility enriches the evaluation process with self-produced

information, direct interviews with firms under evaluation, other secondary sources (e.g.

reports released by NGOs and other third-party organizations), and direct engagement with

stakeholders to triangulate company owned information. As such, the whole process is

deeper and richer than exclusive reliance upon disclosure released by firms through CSR

reports.

Finally, to reduce the endogeneity bias, we lagged this variable so that the impact of CSR

disclosure by firm i at time t was assessed on performance at time t þ 1. Finally, to reduce

variability and improve the significance of our regression analysis, we took the logarithm of

corporate social performance.

Independent variables

Consistent with previous literature (Abbott and Monsen, 1979; Guthrie and Parker, 1989), the

variables related to the level and structure of CSR disclosure were operationalized on the

basis of a content analysis of non-financial reports published by the Fortune 100 companies

included in the Accountability Rating between 2004 and 2006.

Differing from previous research on the effects of disclosure on performance, our study goes

beyond aggregate measures of disclosure level (disclosure depth), providing a

finer-grained analysis of its structure, namely, disclosure breadth and disclosure

VOL. 11 NO. 4 2011 jCORPORATE GOVERNANCEj PAGE 463

concentration. Toward this goal, it was necessary to develop an interrogation instrument to

record the typology and amount of disclosure in different CSR-related categories. Such an

instrument was developed on the basis of a previous comparative analysis of the standard

reporting frameworks available on the markets (author ref) and records disclosure based

both on stakeholders (eight categories considered: human resources, shareholders,

financial partners, customers, suppliers, public authorities and institutions, communities and

environment) and on a checklist of disclosure themes for each stakeholder. The

stakeholder-related themes included into the interrogation instrument are presented in

Table I.

Given the interrogation instrument, we developed three measures representing various

aspects of non-financial disclosure.

Disclosure depth. Disclosure depth corresponds to the volume of disclosure offered by firm i

at time t. Disclosure depth, measured as the number of sentences referring to each theme, is

an indication of the importance assigned to an issue by a reporting entity (Krippendorf,

1980). Though the themes in the recording instrument have been selected on the basis of a

comparative analysis of existing standards to reduce subjectivity (Clarkson et al., 2008), the

final number of themes can still be considered arbitrary. To reduce this bias, we decided to

measure disclosure depth with a weighted index, summing the number of sentences for

each stakeholder and multiplying the ratio between the total number of sentences written

about that stakeholder by the whole sample and the total number of sentences in the

sample. Accordingly, the disclosure depth index is equal to:

disclosure depth index ¼Xm

j¼1

stkjit

Pni¼1 stkjitPm

j¼1

Pni stkjit

where: stkjit is the number of sentences disclosed by firm i for stakeholder j at time t, with m

equal to the number of stakeholders included in the analysis (i.e. the eight stakeholders

considered) and n equal to the number of sampled firms. The number of sentences by each

firm for each stakeholder is weighted by the ratio between the total number of sentences for

that stakeholder in the sample at time t and the total number of sentences at time t.

In other words, the disclosure depth index measures the average volume of disclosure by

firm i at time t in relative terms, that is, relative to what all the others in the sample do. The

underlying ratio remains the same: though non-financial reports are increasingly

standardized, neither a unique standard nor common language exists. There is great

variability between disclosing firms, so that relative measures are more appropriate than

sums or simple arithmetic averages.

Disclosure breadth. Disclosure breadth measures variety of stakeholder-related themes

included in the non-financial reports released by firm i at time t. To calculate the score of

disclosure breadth, the total number of themes mentioned in the non-financial report was

summed and divided by the total number of reportable themes. In other words, disclosure

breadth is an index equal to the share of themes disclosed in the report. The use of indices to

measure the extent of disclosure has a long tradition in the accounting literature (see for a

review Ahmed and Courtis, 1999; Marston and Shrives, 1991) and, in part, in the studies on

social and environmental disclosure (Clarkson et al., 2008).

To calculate disclosure breadth, the total number of stakeholder-related themes mentioned

in the CSR reports was summed in each stakeholder category. Given that the final number of

themes within each category could be considered arbitrary, the number of reported areas for

each stakeholder was divided by the total number of possible issues for that stakeholder. For

example, if a firm satisfied five of the 14 themes for human resources, one of the seven

themes for shareholders, and two of the seven themes for customers, its disclosure breadth

score would be (5=14 þ 1=7 þ 2=7).

Disclosure concentration. We captured disclosure concentration using the ‘‘Gini’’

coefficient. Recently, management researchers have suggested (Pfarrer et al., 2008) and

employed these statistics for investigating pay dispersion (Bloom, 1999) or to measure the

disproportionate weight of culpability in top executives versus employees in analyses of

PAGE 464 jCORPORATE GOVERNANCEj VOL. 11 NO. 4 2011

Table

ITheinterrogationinstrument

Sta

kehold

ers

Hum

an

reso

urc

es

Share

hold

ers

Fin

ancia

lp

art

ners

Cust

om

ers

Sup

plie

rsP

ub

licse

cto

rC

om

munity

Envi

ronm

ent

Sta

kehold

er-

rela

ted

them

es

Sta

ffcom

posi

tion

Em

plo

yment

polic

yand

turn

ove

rE

qualit

yof

treatm

ent

Train

ing

Work

ing

hours

Schem

es

of

wag

es

and

incentiv

es

Ab

sente

eis

mE

mp

loye

es’

benefit

sIn

dust

rial

rela

tions

Inte

rnal

com

munic

atio

ns

Health

and

safe

tyP

ers

onnel’s

satis

factio

nP

rote

ctio

nof

work

ers

’rig

hts

Dis

cip

linary

measu

res

and

litig

atio

n

Cap

italst

ock

com

posi

tion

Share

hold

ers

’re

munera

tion

Fin

ancia

lhig

hlig

hts

Ratin

gC

orp

ora

teg

ove

rnance

Benefit

sand

serv

ices

for

share

hold

ers

Inve

stor

rela

tions

Rela

tionsh

ips

with

banks

Rela

tionsh

ips

with

insu

rance

com

panie

sR

ela

tionsh

ips

with

oth

er

financia

lp

art

ners

Genera

lchara

cte

rist

ics

Mark

et

deve

lop

ment

Cust

om

er

satis

factio

nand

loya

ltyP

rod

uct

info

rmatio

nand

lab

elin

gE

thic

aland

envi

ronm

enta

lp

rod

ucts

Pro

motio

nal

polic

ies

Priva

cy

pro

tectio

n

Genera

lC

hara

cte

rist

ics

Sup

plie

rse

lectio

nC

om

munic

atio

n,

aw

are

ness

cre

atio

nand

info

rmatio

nC

ontr

actu

alte

rms

Taxe

sand

dutie

sR

ela

tions

with

localauth

oritie

sC

od

es

ofc

ond

uct

and

com

plia

nce

with

law

Confo

rmity

verific

atio

nand

insp

ectio

nC

ontr

ibutio

ns,

benefit

s,easy

-term

financin

g

Corp

ora

teg

ivin

gD

irect

invo

lvem

ent

Sta

kehold

er

eng

ag

em

ent

Rela

tions

with

the

med

iaV

irtu

alcom

munity

Corr

up

tion

pre

ventio

n

Energ

yand

mate

rials

consu

mp

tion,

em

issi

ons

Envi

ronm

enta

lst

rate

gy

VOL. 11 NO. 4 2011 jCORPORATE GOVERNANCEj PAGE 465

corporate crime. By analogy, the Gini coefficient has been suggested as useful to capture

the disproportionate attention paid by firms to stakeholders (Pfarrer et al., 2008). The Gini

coefficient can be calculated with individual- or subpopulation-level data (Brown et al.,

2003). For this study, we followed the subpopulation approach to calculation and used

average disclosure levels at the stakeholder level. In other words, we calculated a separate

Gini coefficient for each firm for each year, following the formula presented in Bloom (1999):

gini coefficient ¼ 1

m2

2

m 2 �y

� �y1 þ 2y2 þ . . . þ mymð Þ

where y1. . .ym is a sequence of disclosure levels for the stakeholders covered by firm i in

decreasing order of size, �y is the average disclosure level for each stakeholder in firm i, and

m is the number of stakeholders included in the analysis. Gini coefficients can theoretically

range from 0 (indicating a total egalitarian stakeholder coverage) to 1 (for a totally

concentrated/hierarchical disclosure structure).

Control variables

Several studies indicate that voluntary disclosure is not uniform but depends on different

dimensions – from the industry each firm belongs to, to the organizational context in which

the responsible behavior takes place (Gray et al., 1995a, b; Patten, 2002).

Accordingly, controls have been classified as organizational and environmental affecting

factors that can influence the level of corporate social performance, the number and

relevance associated with stakeholders, and the propensity to report voluntarily on social

and environmental issues.

Organizational affecting factors. First of all, we controlled for the presence of a supportive

internal organizational environment. In particular, we controlled for the presence of

supportive organizational arrangements, introducing a dummy variable for the presence of a

dedicated CSR division in the firm. The dummy is equal to 1 if a CSR division exists, 0

otherwise. The presence of a CSR division indicates not only a stronger commitment to CSR

but also can be considered a proxy of the ease of recognizing, collecting, reporting, and

communicating relevant information on CSR-related activities and behavior (Weaver et al.,

1999). The presence of a CSR division has been checked via the company website and

other publicly available information. Moreover, we controlled for firm experience in reporting

(reporting experience) in that again this affects both the firm’s ability to disclose relevant

information depending on the amount of its experience in interacting with stakeholders and,

potentially, the level of corporate social performance, in that firms with more experience in

CSR also have longer track records in external evaluation processes (Gond and Herrbach,

2006). Reporting experience is equal to the number of years a firm has been publishing a

non-financial report. Data were collected through company reports themselves and

triangulated with data provided by CorporateRegister (www.corporateregister.com), an

online archive of non-financial reports.

We also controlled for the use of reporting standard, introducing a dummy equal to 1 if a

standard was adopted (e.g. the Global Reporting Initiative standard or the

AccountAbility1000 process) and 0 otherwise, and for the reliance on third party audit,

introducing a dummy equal to 1 if the report was audited and 0 otherwise. Data relevant to

both of the above were drawn from company reports and checked through

CorporateRegister. They facilitated control for variables that could have affected the

structure of disclosure and the quality of released information (Dando and Swift, 2003).

Finally, according to previous studies, we controlled for firm size, measured as the natural

logarithm of employees and for firm profitability, measured as the return on equity index.

Environmental affecting factors. Previous studies have highlighted the importance of

industry effect on the level of disclosure and the impact on corporate social performance

(Patten, 2002). At the same time, industry effect can be relevant in that the more pervasive

CSR behavior is among firms the greater the incentive to adhere to the responsible

paradigm to maintain a competitive position. To capture the two combined effects, we

controlled for industry relying on industry CSR ratings as a measure of industry-level

PAGE 466 jCORPORATE GOVERNANCEj VOL. 11 NO. 4 2011

commitment to CSR, as provided by KPMG in the International Survey of Corporate

Responsibility Reporting and checked with the AccountAbility surveys. Dividing into three

intervals the 0 to 100 score provided by KPMG, we introduced a categorical variable

distinguishing between low-, medium-, and high-performing industries. We also controlled

for the country effect, classifying countries in Europe, the US, and others, depending on the

country of a firm’s headquarters.

Year effects. Given the longitudinal nature of our dataset, we included a dummy variable for

the year 2005 to pick up any effects specific to the years in the analysis.

Estimation method

We performed a pooled OLS estimation regression. We used the Cook-Weisberg and the

White test statistics to check the homoskedasticity assumption and found the presence of

heteroskedasticity (Cook and Weisberg, 1983; White, 1980). To correct for

heteroskedasticity, we used a robust-cluster estimator of the standard errors in our

regressions. The robust-cluster variance estimator is a variant of the Huber-White robust

estimator, which provides correct standard errors in the presence of any pattern of

heteroskedasticity. It also remains valid and provides correct coverage in the presence of

any pattern of correlation among errors within units. This estimator allowed us to relax the

assumption of independence of errors in the regression. Since we used a pooled time-series

approach, repeated observations may create correlated error terms and inflate t-statistics

without using this correction. In fact, the robust-standard errors are unaffected by the

presence of unmeasured firm-specific factors causing correlation among errors of

observations for the same firms, or for that matter any other form of within-unit error

correlation. Thus, the robust-cluster estimator produces correct standard errors even when

the observations are correlated within clusters (STATA, 2005).

Results

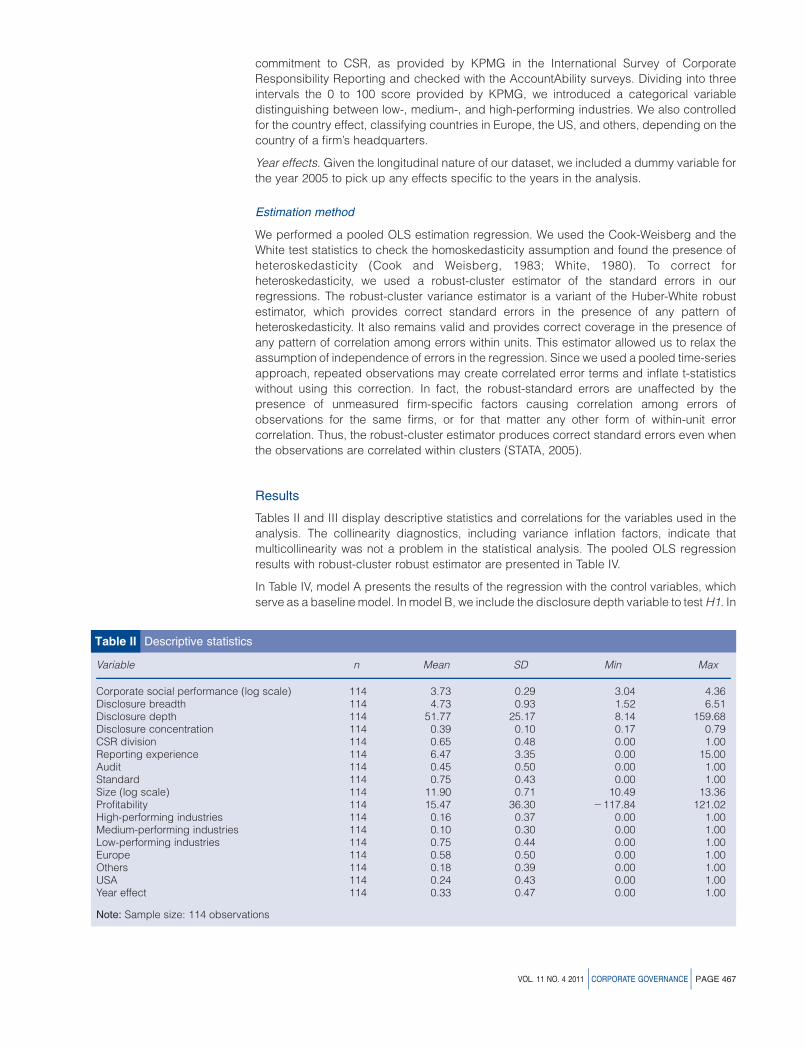

Tables II and III display descriptive statistics and correlations for the variables used in the

analysis. The collinearity diagnostics, including variance inflation factors, indicate that

multicollinearity was not a problem in the statistical analysis. The pooled OLS regression

results with robust-cluster robust estimator are presented in Table IV.

In Table IV, model A presents the results of the regression with the control variables, which

serve as a baseline model. In model B, we include the disclosure depth variable to test H1. In

Table II Descriptive statistics

Variable n Mean SD Min Max

Corporate social performance (log scale) 114 3.73 0.29 3.04 4.36Disclosure breadth 114 4.73 0.93 1.52 6.51Disclosure depth 114 51.77 25.17 8.14 159.68Disclosure concentration 114 0.39 0.10 0.17 0.79CSR division 114 0.65 0.48 0.00 1.00Reporting experience 114 6.47 3.35 0.00 15.00Audit 114 0.45 0.50 0.00 1.00Standard 114 0.75 0.43 0.00 1.00Size (log scale) 114 11.90 0.71 10.49 13.36Profitability 114 15.47 36.30 2117.84 121.02High-performing industries 114 0.16 0.37 0.00 1.00Medium-performing industries 114 0.10 0.30 0.00 1.00Low-performing industries 114 0.75 0.44 0.00 1.00Europe 114 0.58 0.50 0.00 1.00Others 114 0.18 0.39 0.00 1.00USA 114 0.24 0.43 0.00 1.00Year effect 114 0.33 0.47 0.00 1.00

Note: Sample size: 114 observations

VOL. 11 NO. 4 2011 jCORPORATE GOVERNANCEj PAGE 467

Table

IIICorrelationsmatrix

12

34

56

78

910

11

12

13

14

15

16

17

18

19

1.

Corp

ora

teso

cia

lp

erf

orm

ance

(log

scale

)1.0

02.

Dis

clo

sure

bre

ad

th0.2

8**

1.0

03.

Dis

clo

sure

dep

th0.1

9*0.2

7**

1.0

04.

Dis

clo

sure

concentr

atio

n2

0.3

1***

20.6

1***

20.0

21.0

05.

CS

Rd

ivis

ion

0.2

6**

0.1

50.1

32

0.0

21.0

06.

Rep

ort

ing

exp

erience

0.2

8**

20.0

80.2

1*0.1

12

0.0

21.0

07.

Aud

it0.4

4***

0.2

6**

20.0

22

0.1

20.3

7***

0.1

31.0

08.

Sta

nd

ard

0.2

6**

0.0

60.0

72

0.0

60.1

40.1

00.1

41.0

09.

Siz

e(log

scale

)0.0

12

0.1

70.1

22

0.0

00.0

50.1

92

0.1

8*0.0

41.0

010.

Pro

fitab

ility

0.0

32

0.0

32

0.1

62

0.0

70.0

22

0.1

60.0

92

0.0

82

0.2

2*1.0

011.

Hig

h-p

erf

orm

ing

ind

ust

ries

0.2

7**

0.0

22

0.0

12

0.1

22

0.2

3*0.1

70.1

40.0

22

0.3

5***

0.2

5**

1.0

012.

Med

ium

-p

erf

orm

ing

ind

ust

ries

20.0

60.0

32

0.1

8*2

0.0

40.1

22

0.2

6**

20.0

60.0

52

0.1

00.1

02

0.1

41.0

013.

Low

-perf

orm

ing

ind

ust

ries

20.1

8*2

0.0

40.1

30.1

30.1

20.0

32

0.1

62

0.0

50.3

6***

20.2

7**

20.7

4***

20.5

5***

1.0

014.

Euro

pe

0.2

3*0.1

42

0.2

5**

0.0

50.1

50.0

70.5

2***

0.1

32

0.1

40.1

20.0

80.2

22

0.2

1*1.0

015.

Oth

ers

20.4

4***

20.1

72

0.0

30.1

22

0.0

32

0.0

32

0.3

4***

20.2

5**

0.0

82

0.0

32

0.2

12

0.1

60.2

8**

20.5

6***

1.0

016.

US

A0.1

32

0.0

10.3

2***

20.1

62

0.1

52

0.0

62

0.2

9**

0.0

80.0

92

0.1

20.1

02

0.1

12

0.0

12

0.6

5***

20.2

6**

1.0

017

2004

20.0

92

0.2

7**

20.0

90.1

30.0

52

0.2

1*2

0.1

10.0

62

0.0

30.0

72

0.2

6**

0.4

6***

20.1

00.0

00.0

00.0

01.0

018

2005

20.1

50.1

00.0

52

0.1

12

0.0

30.0

00.0

40.0

12

0.0

02

0.0

20.1

02

0.2

3*0.0

30.0

00.0

00.0

02

0.5

0***

1.0

019.

2006

20.1

50.1

00.0

52

0.1

02

0.0

20.0

00.0

40.0

12

0.0

02

0.0

20.1

02

0.2

30.0

70.0

00.0

00.0

02

0.5

0***

20.5

0***

1.0

0

Notes:

*p,

0.0

5;

**p,

0.0

1;

***p

,0.0

01;

n¼

114

PAGE 468 jCORPORATE GOVERNANCEj VOL. 11 NO. 4 2011

model C, we test H2 by including the disclosure breadth variable to the baseline model. In

model D, we test H3 including the disclosure concentration variable.

Different from what was predicted, the coefficient of the variable representing the weighted

volume of disclosure per stakeholder-related theme is positive but not significant (model B).

A higher number of sentences on a theme does not necessarily translate into an additional

piece of useful information on company activities in those areas. In other words, though CSR

reports are increasingly standardized, a common language still does not exist, thus

complicating the comparison across companies based on the quantity of disclosure.

We find that the coefficient of the variable representing the breadth of stakeholder-related

themes disclosed by firms that release a non-financial report is positive and significant at the

1 percent level, thus supporting H2. In our sample, the more themes a firm covers in its CSR

report, the higher its performance in the next year. Firms that present more extensive CSR

reporting are more able both to manage their responsible relationships with stakeholders

better and to strengthen its image as a socially responsible company among other

stakeholders.

The coefficient for the variable capturing the extent to which disclosure is concentrated or

homogeneously distributed across stakeholders is negative and significant at the 1 percent

level. As predicted by H3, disclosing more but in favor of a limited set of stakeholders is more

likely to decrease the level of corporate social performance in the next year.

Several other variables representing organizational and environmental affecting factors are

positive and significant at the 1-10 percent level. The presence of a CSR division is positive

and significant in all the models, indicating that an internal formal commitment within the

organizational boundaries improves the ability of firms to manage CSR, thus improving

performance in the next year. Having a longer reporting experience has a positive and

significant impact on performance in all the models but B, thus indicating the presence of a

learning-by-doing effect on CSR management. Moreover, the coefficient representing

whether or not a CSR report was audited has a positive, significant impact on performance in

Table IV Pooled regression results

(A) (B) (C) (D) (E)

Disclosure depth 0.000 (0.000) 0.022 (0.037)Disclosure breadth 0.066 (0.023)** 0.000 (0.000)Disclosure concentration 20.741 (0.261) ** 20.937 (0.385)*CSR division 0.130 (0.062)* 0.123 (0.062)† 0.120 (0.063)† 0.132 (0.060)* 0.131 (0.058)*Reporting experience 0.014 (0.008)† 0.013 (0.008) 0.016 (0.008)* 0.017 (0.007)* 0.019 (0.007)**Audit 0.164 (0.074)* 0.163 (0.075)* 0.144 (0.076)† 0.138 (0.076)† 0.129 (0.079)Standard 0.076 (0.053) 0.075 (0.054) 0.071 (0.054) 0.067 (0.048) 0.078 (0.048)Size (log scale) 0.037 (0.052) 0.037 (0.053) 0.051 (0.050) 0.027 (0.049) 0.015 (0.053)Profitability 0.000 (0.001) 0.000 (0.000) 0.000 (0.000) 0.000 (0.000) 0.000 (0.000)High-performing industries – – 0.275 (0.126)* – –Medium-performingindustries 20.234 (0.128)† 20.229 (0.127)† 2 20.240 (0.129) 20.225 (0.141)Low-performing industries 20.165 (0.098) † 20.167 (0.098)† 0.092 (0.089) 0.144 (0.090) 20.149 (0.098)Europe 0.182 (0.083)* 0.186 (0.084)* 0.169 (0.085)* 0.189 (0.085)* 0.179 (0.085)*Others – – – – –USA 0.288 (0.077)*** 0.274 (0.073)*** 0.267 (0.769)*** 0.258 (0.077)** 0.232 (0.072)**Year 2004 – 20.049 (0.056) – – 20.034 (0.054)Year 2005 20.098 (0.046)* 20.146 (0.035) 20.14 (0.048)** 20.127 (0.047)** 20.155 (0.033)***Year 2006 0.05 (0.056) – 20.003 (0.054) 0.024 (0.049) –Constant 2.976 (0.581)*** 3.001 (0.598)*** 2.285 (0.579)*** 3.387 (0.587)*** 3.465 (0.734)***Observations 114 114 114 114 114R 2 0.481 0.484 0.515 0.536 0.563F 9.24 9.98 12.12 11.43 14.06p, 0.000 0.000 0.000 0.000 0.000

Notes: *p , 0.05; **p , 0.01; ***p , 0.001; †p , 0.1; Dependent variable: corporate social performance (log scale)

VOL. 11 NO. 4 2011 jCORPORATE GOVERNANCEj PAGE 469

models B through D, indicating the usefulness of relying on external advisors to strengthen a

firm’s ability to interact with stakeholders and improving social performance. Finally,

belonging to a well-rated CSR industry contributes more positively to corporate social

performance than does belonging to a medium-low rated industry.

Discussion and conclusion

Starting from an attempt to test the soundness of ‘‘the more the better’’ assumption, this

study adds to our understanding of the performance consequences of CSR disclosure and

demonstrates the impact of disclosure level and structure on corporate social performance.

Our results supported most of the hypotheses and the general notion that a finer-grained

analysis of the practice of CSR disclosure is needed to go beyond the ‘‘what should

companies disclose’’ question to the ‘‘how should companies disclose information’’

question, both regarding their responsible relationship with stakeholders.

Different from what anecdotal evidence and theoretical accounts suggest, the level of

disclosure does not have a significant impact on social performance. This result seems to

support the critique of CSR disclosure because it masks poor performance (Hughes et al.,

2001), and the critique that poor performers provide more extensive disclosure than good

performers do, and the conclusion by Ingram and Frazier (1980) about the poor quality of

voluntary non-financial information disclosed by the firms.

On the contrary and in light of the other findings in our study, the failure to find a positive,

significant relationship between the amount of disclosure (i.e. disclosure depth) and

performance could be explained by the fact that, although CSR disclosure increasingly

relies on third-party standards (e.g. the Global Reporting Initiative guidelines), it remains

voluntary, so that neither a unique common format nor a universal reporting language, style,

and practice exists to create simpler and more comparable company reports. In this sense,

one can hardly conclude that a firm has a higher probability of being a good performer just

because it discloses more than the others do.

Going beyond empirical claims that disclosure is a univocal construct, our findings provide a

preliminary answer to the question of how disclosure should be organized to improve

performance. Our findings support theoretical claims that CSR cannot be understood

separately from the dependence relationships between companies and their social context

(Post et al., 2002), such that the detection and scanning of, and response to the social

demand become fundamental to achieving social legitimacy, greater social acceptance,

and prestige. In this sense, an active company involvement in CSR has to go beyond a

generic responsiveness toward society at large, focusing rather on the importance of

identifying stakeholder and related areas of responsibility. If so, regardless of the level of

disclosure, the more firms are able to extend their systematizing and communicating efforts

to a wider range of stakeholders and stakeholder-related CSR programs, the stronger their

ability to achieve superior social performance, especially if accompanied by the

determination to maintain an appropriate balance between different, often contrasting

interests (Ogden and Watson, 1999).

Though not testing it directly through a comparison between company CSR disclosure and

stakeholder perceptions regarding the usefulness of released data and information, results

point out to the relevance of materiality in refining the content and structure of reporting

(Rasche and Esser, 2006). Showing the social performance consequences of broadening

the scope of stakeholders, while treating the different categories as equally crucial for firm

survival, findings highlight the need to make CSR reporting mirroring the heterogeneity,

complexity and multiplicity that characterize the stakeholder network firms are embedded in

(Deegan and Rankin, 1997). In other words, in order to have a direct impact on the ability to

manage multiple relationships, enlightened companies seem to be aware of the importance

to communicate information that is relevant to stakeholders in their efforts to make coherent

decisions according to their expectations (Cooper and Owen, 2007).

PAGE 470 jCORPORATE GOVERNANCEj VOL. 11 NO. 4 2011

Findings are even more relevant in an emerging market context. In fact, as companies

increasingly adopt CSR disclosure moved by the desire to answer the requests of powerful

stakeholder groups, via parent company instructions, pressure from international buyers

and the government (Islam and Deegan, 2008; Williams and Pei, 1999), giving a proper

structure to reports can strengthen their materiality and turn into a better ability to manage

the dialogue with stakeholders. Partly related to the previous point, recent studies show how

large firms in emerging economies tend to be more sensitive to global expectations rather

than the information needs in their home countries (Newson and Deegan, 2002). In this

context, our findings suggest how to better bridge the gaps in the reporting practice in order

to be aligned with global competitors and have equally access to stakeholder consensus

and legitimacy to operate (Min Foo, 2007; Tencati et al., 2008), especially for those

companies having an increasingly international profile (Muller and Kolk, 2009). In other

words, because of greater integration in the global economy and concomitant increases in

attention from international organizations and institutions, pressures can be expected to

lead to a similar CSR implementation path both in Western and emerging economies.

Though advancing theoretical and empirical debate on CSR disclosure structure and its

impact, the study suffers of methodological limitations of both relying on content analysis

and using secondary sources to measure CSP are well-known. Judicious attempts were

made to mitigate their effects. First of all, our study ignores sources of disclosure other than

CSR reports (e.g., corporate web sites, annual reports, and press releases). There may be

companies that have programs consistent with the CSR paradigm but have not used a report

to disclose such information. Our research does not capture this information. Yet, the choice

to focus the analysis solely on CSR reports was supported by the need to enhance

traceability, comparability over time, and reliability of disclosed information. In addition, the

study suffers the usual limitations of content analysis-based research. Though supported by

previous literature (Gray et al., 1995a, b), the choice to rely on sentence as the unit of

analysis to score disclosure level remains subjective. Given our need to measure the volume

of disclosure in certain behavior-related areas, using sentences has been more natural and

less subjective than counting words and not as aggregated as counting paragraphs.

Moreover, this study explicitly addresses CSR disclosure by large corporations who in

general have a high resource availability devoted to CSR and the formalization of a

disclosure procedure. At the same time, large corporations are extremely visible, and

visibility may motivate them to behave responsibly, so that the intrinsic characteristics of the

sample under observation may have made disclosure dynamics more visible than

elsewhere.

Note

1. CSR disclosure includes social, environmental and sustainability disclosures.

References

Abbott, W.F. and Monsen, R.J. (1979), ‘‘On the measurement of corporate social responsibility:

self-reported disclosures as a method of measuring corporate social involvement’’, Academy of

Management Journal, Vol. 22 No. 3, pp. 501-15.

Ahmed, K. and Courtis, J.K. (1999), ‘‘Associations between corporate characteristics and disclosure

levels in annual reports: a meta-analysis’’, British Accounting Review, Vol. 31 No. 1, pp. 35-61.

Alon, I., Lattemann, C., Fetscherin, M., Li, S. and Schneider, A.-M. (2010), ‘‘Usage of public corporate

communications of social responsibility in Brazil, Russia, India and China (BRIC)’’, International Journal

of Emerging Markets, Vol. 5 No. 1, pp. 6-22.

Belal, A.R. and Momin, M. (2009), ‘‘Corporate social reporting (CSR) in emerging economies: a review

and future direction’’, in Tsamenyi, M. and Uddin, S. (Eds), Accounting in Emerging Economies, Vol. 9,

Emerald Group Publishing, Bingley, pp. 119-43.

Bloom, M.C. (1999), ‘‘The performance effects of pay dispersion on individuals and organizations’’,

Academy of Management Journal, Vol. 42 No. 1, pp. 25-40.

VOL. 11 NO. 4 2011 jCORPORATE GOVERNANCEj PAGE 471

Bowman, E.H. and Haire, M. (1975), ‘‘A strategic posture toward corporate social responsibility’’,

California Management Review, Vol. 18 No. 2, pp. 49-58.

Brown, M.P., Sturman, M.C. and Simmering, M.J. (2003), ‘‘Compensation policy and organizational

performance: the efficiency, operational, and financial implications of pay levels and pay structure’’,

Academy of Management Journal, Vol. 46 No. 6, pp. 752-62.

Clarkson, P.M., Li, Y., Richardson, G.D. and Vasvari, F.P. (2008), ‘‘Revisiting the relation between

environmental performance and environmental disclosure’’, Accounting, Organizations and Society,

Vol. 33 Nos 4/5, pp. 303-27.

Cook, R.D. and Weisberg, S. (1983), ‘‘Diagnostic for heteroskedasticity in regression’’, Biometrika,

Vol. 70 No. 1, pp. 1-10.

Cooper, S.M. and Owen, D.L. (2007), ‘‘Corporate social reporting and accountability: the missing link’’,

Accounting, Organizations and Society, Vol. 32 Nos 7/8, pp. 649-67.

Dando, N. and Swift, T. (2003), ‘‘Transparency and assurance: minding the credibility gap’’, Journal of

Business Ethics, Vol. 44 Nos 2/3, pp. 195-200.

Deegan, C. and Rankin, M. (1997), ‘‘The materiality of environmental information to users of annual

reports’’, Accounting, Auditing & Accountability Journal, Vol. 10 No. 4, pp. 562-83.

Donaldson, T. and Preston, L.E. (1995), ‘‘The stakeholder theory of the corporation: concepts, evidence,

and implications’’, Academy of Management Review, Vol. 20 No. 1, pp. 65-91.

Dye, R.A. (1985), ‘‘Disclosure of non-proprietary information’’, Journal of Accounting Research, Vol. 23

No. 1, pp. 123-45.

Freeman, E.R. (1984), Strategic Management: A Stakeholder Approach, Pitman, Boston, MA.

Gelb, D.S. and Strawser, J.A. (2001), ‘‘Corporate social responsibility and financial disclosures:

an alternative explanation for increased disclosure’’, Journal of Business Ethics, Vol. 33 No. 1, pp. 1-13.

Gond, J.-P. and Herrbach, O. (2006), ‘‘Social reporting as an organizational learning tool? A theoretical

framework’’, Journal of Business Ethics, Vol. 65 No. 4, pp. 359-71.

Gray, R., Kouhy, R. and Lavers, S. (1995a), ‘‘Corporate social and environmental reporting: a review of

the literature and a longitudinal study of UK disclosure’’, Accounting, Auditing & Accountability Journal,

Vol. 8 No. 2, pp. 47-77.

Gray, R., Kouhy, R. and Lavers, S. (1995b), ‘‘Methodological themes: constructing a research database

of social and environmental reporting by UK companies’’, Accounting, Auditing & Accountability

Journal, Vol. 8 No. 2, pp. 78-101.

Greenwood, M. (2007), ‘‘Stakeholder engagement: beyond the myth of corporate responsibility’’,

Journal of Business Ethics, Vol. 74 No. 4, pp. 315-27.

Guthrie, J. and Parker, L.D. (1989), ‘‘Corporate social disclosure practice: a comparative international

analysis’’, Advances in Public Interest Accounting, Vol. 3, pp. 159-75.

Hughes, S.B., Anderson, A. and Golden, S. (2001), ‘‘Corporate environmental disclosure: are they useful

in determining environmental performance?’’, Journal of Accounting and Public Policy, Vol. 20 No. 3,

pp. 217-40.

Husted, B. and Allen, D. (2006), ‘‘Corporate social responsibility in the multinational enterprise: strategic

and institutional approaches’’, Journal of International Business Studies, Vol. 37 No. 6, pp. 838-49.

Ingram, R.W. and Frazier, K. (1980), ‘‘Environmental performance and corporate disclosure’’, Journal of

Accounting Research, Vol. 18 No. 2, pp. 614-22.

Islam, M.A. and Deegan, C. (2008), ‘‘Motivation for an organization within a developing country to report

social responsibility information: evidence from Bangladesh’’, Accounting, Auditing & Accountability

Journal, Vol. 21 No. 6, pp. 850-74.

KPMG (2008), International Survey of Corporate Responsibility Reporting 2008, KPMG International.

Krippendorf, K. (1980), Content Analysis: An Introduction to its Methodology, Sage, New York, NY.

Marston, C.L. and Shrives, P.J. (1991), ‘‘The use of disclosure indices in accounting research: a review

article’’, British Accounting Review, Vol. 23, pp. 195-210.

PAGE 472 jCORPORATE GOVERNANCEj VOL. 11 NO. 4 2011

Min Foo, L. (2007), ‘‘Stakeholder engagement in emerging economies: considering the strategic

benefits of stakeholder management in a cross-cultural and geopolitical context’’, Corporate

Governance: The International Journal of Business in Society, Vol. 7 No. 4, pp. 379-87.

Mitchell, R.K., Agle, B.R. and Wood, D.J. (1997), ‘‘Toward a theory of stakeholder identification and

salience: defining the principle of who and what really counts’’, Academy of Management Review, Vol. 22

No. 4, pp. 853-86.

Muller, A. and Kolk, A. (2009), ‘‘CSR performance in emerging markets: evidence from Mexico’’, Journal

of Business Ethics, Vol. 85 No. 2, pp. 325-37.

Newson, M. and Deegan, C. (2002), ‘‘Global expectations and their association with corporate social

disclosure practices in Australia, Singapore, and South Korea’’, The International Journal of Accounting,

Vol. 37 No. 2, pp. 183-213.

Nitkin, D. and Brooks, L.J. (1998), ‘‘Sustainability auditing and reporting: the Canadian experience’’,

Journal of Business Ethics, Vol. 17 No. 13, pp. 1499-507.

OECD (2005), Corporate Responsibility Practices of Emerging Market Companies: A Fact-Finding

Study, OECD, Paris.

Ogden, S. and Watson, R. (1999), ‘‘Corporate performance and stakeholder management: balancing

shareholders’ and customers’ interests in the UK privatized water industry’’, Academy of Management

Journal, Vol. 42 No. 5, pp. 526-38.

Orlitzky, M., Schmidt, F.L. and Rynes, S.L. (2003), ‘‘Corporate social and financial performance:

a meta-analysis’’, Organization Studies, Vol. 24 No. 3, pp. 403-41.

Patten, D.M. (2002), ‘‘The relation between environmental performance and environmental disclosure:

a research note’’, Accounting, Organizations and Society, Vol. 27 No. 8, pp. 763-73.

Pfarrer, M.D., Decelles, K.A., Smith, K.G. and Taylor, M.S. (2008), ‘‘After the fall: reintegrating the corrupt

organization’’, Academy of Management Review, Vol. 33 No. 3, pp. 730-49.

Post, J.E., Preston, L.E. and Sachs, S. (2002), Redefining the Corporation: Stakeholder Management

and Organizational Wealth, Stanford University Press, Stanford, CA.

Rahaman, A.S., Lawrence, S. and Roper, J. (2004), ‘‘Social and environmental reporting at VRA:

institutional legitimacy or legitimation crisis?’’, Critical Perspectives on Accounting, Vol. 15 No. 1,

pp. 35-56.

Rasche, A. and Esser, D.E. (2006), ‘‘From stakeholder management to stakeholder accountability’’,

Journal of Business Ethics, Vol. 65 No. 3, pp. 251-67.

STATA (2005), Stata User’s Guide (STATA Release 9), Stata Press, College Station, TX.

Tencati, A., Russo, A. and Quaglia, V. (2008), ‘‘Unintended consequences of CSR: protectionism and

collateral damage in global supply chains: the case of Vietnam’’, Corporate Governance:

The International Journal of Business in Society, Vol. 8 No. 4, pp. 518-31.

Verrecchia, R.E. (1983), ‘‘Discretionary disclosure’’, Journal of Accounting and Economics, Vol. 5 No. 3,

pp. 179-94.

Vogel, D. (2005), The Market for Virtue: The Potential and Limits of Corporate Social Responsibility,

Brookings Institution Press, Washington, DC.

Waddock, S. and Bodwell, C. (2004), ‘‘Managing responsibility: what can be learned from the quality

movement?’’, California Management Review, Vol. 47 No. 1, pp. 25-37.

Waddock, S. and Graves, S.B. (1997), ‘‘The corporate social performance-financial performance link’’,

Strategic Management Journal, Vol. 18 No. 4, pp. 303-19.

Weaver, G.R., Trevino, L.K. and Cochran, P.L. (1999), ‘‘Integrated and decoupled corporate social

performance: management commitments, external pressures, and corporate ethics practices’’,

Academy of Management Journal, Vol. 42 No. 5, pp. 539-52.

White, H. (1980), ‘‘A heteroskedasticity-consistent covariance matrix estimator and a direct test for

heteroskedasticity’’, Econometrica, Vol. 48 No. 4, pp. 817-38.

Williams, S. and Pei, C. (1999), ‘‘Corporate social disclosures by listed companies on their web sites:

an international comparison’’, The International Journal of Accounting, Vol. 34 No. 3, pp. 389-419.

VOL. 11 NO. 4 2011 jCORPORATE GOVERNANCEj PAGE 473

About the authors

Clodia Vurro is post-doctoral fellow of Business Administration and Management at theInstitute of Strategy, Department of Management and Technology, Bocconi University (Milan,Italy). She is assistant to the SIF Chair of Social Entrepreneurship and Research Fellow at theResearch Center for Sustainability and Value (CReSV) at Bocconi University. Her researchinterests include strategic change, organizational learning, corporate social responsibilityand sustainability, and social entrepreneurship. Clodia Vurro is the corresponding authorand can be contacted at: [email protected]

Francesco Perrini is Full Professor of Management and CSR at the Institute of Strategy,Department of Management and Technology, Bocconi University (Milan, Italy). He is also SIFChair of Social Entrepreneurship and Senior Professor of Corporate Finance in the Corporateand Real Estate Finance Department, SDA Bocconi School of Management (Milan, Italy).He is currently Director of the Research Center for Sustainability and Value (CReSV) andCSR Unit at Bocconi University. His research interests include management of corporatedevelopment processes, social and environmental issues in management, corporatesustainability and social entrepreneurship.

PAGE 474 jCORPORATE GOVERNANCEj VOL. 11 NO. 4 2011

To purchase reprints of this article please e-mail: [email protected]

Or visit our web site for further details: www.emeraldinsight.com/reprints