Embed Size (px)

Citation preview

Making Fiscal

Policy ‘Work’ CAN FISCAL POLICY DO MORE TO ADDRESS POVERTY, INEQUALITY,

GROWTH & JOBS IN AUSTERE TIMES?

MACROECONOMIC & FISCAL MANAGEMENT

Triple Challenges Are Center Stage

Poverty Every night 12 million South Africans go to bed without food

Inequality 1 in every 17 individuals in Sandhurst have wealth in excess of US$30 million (R400 million)

Alexandra’s average household income is < R2 700 a month

Unemployment

There are more people unemployed (expanded definition) in South Africa than the combined population of

Botswana, Namibia, and Lesotho

MACROECONOMIC & FISCAL MANAGEMENT

Challenge 1: Poverty

High For A Middle Income Country

South Africa

35%

17%

Poverty Headcount Ratio at $3.10 a day (2011 PPP) (% of Population)

Poverty Headcount Ratio at $1.90 a day (2011 PPP) (% of Population)

Upper Middle

Income

5%

1%

MACROECONOMIC & FISCAL MANAGEMENT

Challenge 2: Inequality

World’s Most Unequal Country

0.69

0.43

South Africa

Upper middle

income country

average

UMIC

comparison:

MACROECONOMIC & FISCAL MANAGEMENT

Challenge 3: Unemployment

Is High By Global Standards

Youth Unemployment Rate Unemployment Rate in 2019

MACROECONOMIC & FISCAL MANAGEMENT

Demographic Change

Implies Jobs Challenge Will Grow

The working age

population is 65% of the total population

MACROECONOMIC & FISCAL MANAGEMENT

Source: South African Economic Update 7

As South Africa Currently Fails to

Generate Enough Jobs

Source: Statistics South Africa, Labor Force Surveys

Since 2000

Only 2.8 million out of the

8.3 million extra working age

population found jobs

Today

Only 40% of the

working age

population work

Manufacturing

Agriculture

Mining

MACROECONOMIC & FISCAL MANAGEMENT

Job Creation Has Become More

Skilled

Source: Statistics South Africa, Labor Force Surveys Source: Statistics South Africa, Labor Force Surveys

MACROECONOMIC & FISCAL MANAGEMENT

Leaving Many Unskilled Youth Facing

The Prospect Of Unemployment

Source: Statistics South Africa, Labor Force Surveys

South Africa Unemployment Rate 25.5%

Upper Middle Income Countries Average 11%

MACROECONOMIC & FISCAL MANAGEMENT

Source: Statistics South Africa, Labor Force Surveys

Absent Job Creation

Growth Dividend Missed

Inequality & Poverty Remain By 2030:

MACROECONOMIC & FISCAL MANAGEMENT

Source: South African Economic Update 7

How Can Fiscal Policy Address The

Triple Challenges In Austere Times?

MACROECONOMIC & FISCAL MANAGEMENT

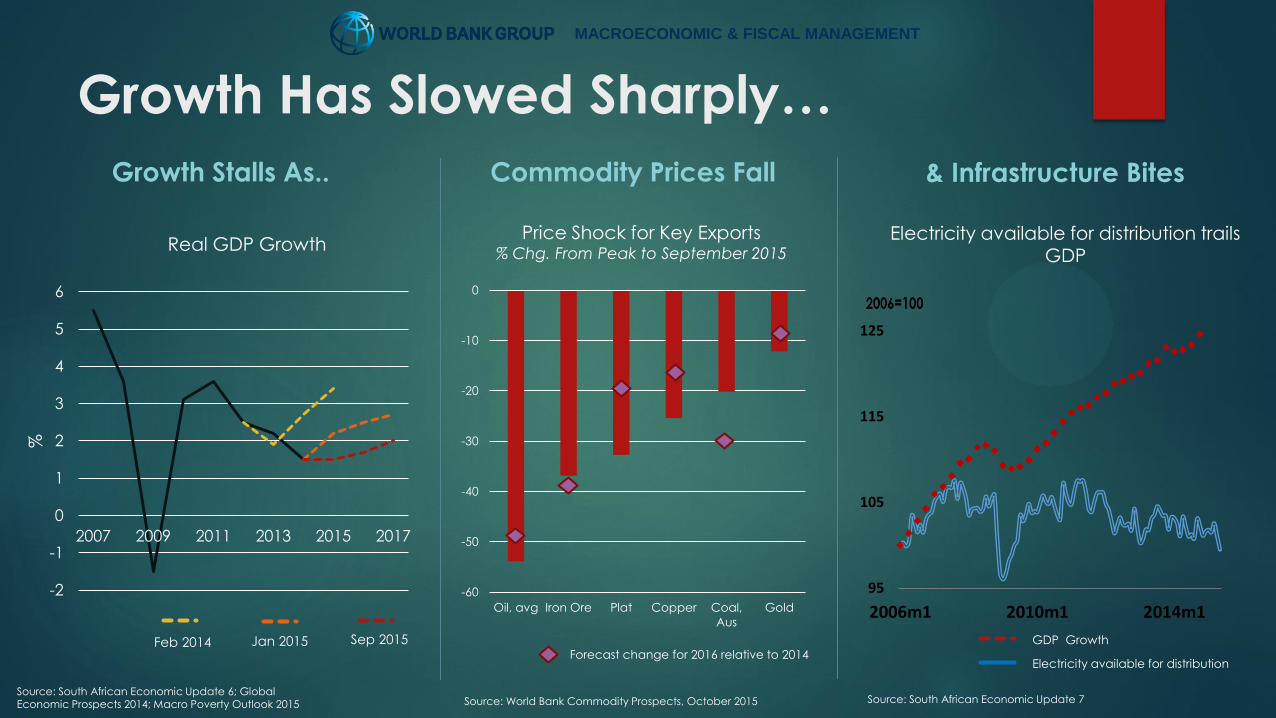

Growth Has Slowed Sharply…

& Infrastructure Bites

95

105

115

125

2006m1 2010m1 2014m1

Commodity Prices Fall

-60

-50

-40

-30

-20

-10

0

Oil, avg Iron Ore Plat Copper Coal,

Aus

Gold

Growth Stalls As..

-2

-1

0

1

2

3

4

5

6

2007 2009 2011 2013 2015 2017

%

Feb 2014 Jan 2015 Sep 2015

Source: South African Economic Update 6; Global Economic Prospects 2014; Macro Poverty Outlook 2015

Real GDP Growth

Price Shock for Key Exports % Chg. From Peak to September 2015

Electricity available for distribution trails GDP

Source: World Bank Commodity Prospects, October 2015 Source: South African Economic Update 7

Forecast change for 2016 relative to 2014

GDP Growth

Electricity available for distribution

MACROECONOMIC & FISCAL MANAGEMENT

….Exhausting Fiscal Space

Adjustment Will Imply Hard Choices

25

30

35

40

45

50

FY08/09 FY09/10 FY10/11 FY11/12 FY12/13 FY13/14 FY14/15 FY15/16 FY16/17 FY17/18

Gross Debt/GDP

2009 Budget 2010 Budget 2011 Budget 2012 Budget

2013 Budget 2014 Budget 2015 MTBPS

Source: South African National Treasury Budget Review 2009-2015

MACROECONOMIC & FISCAL MANAGEMENT

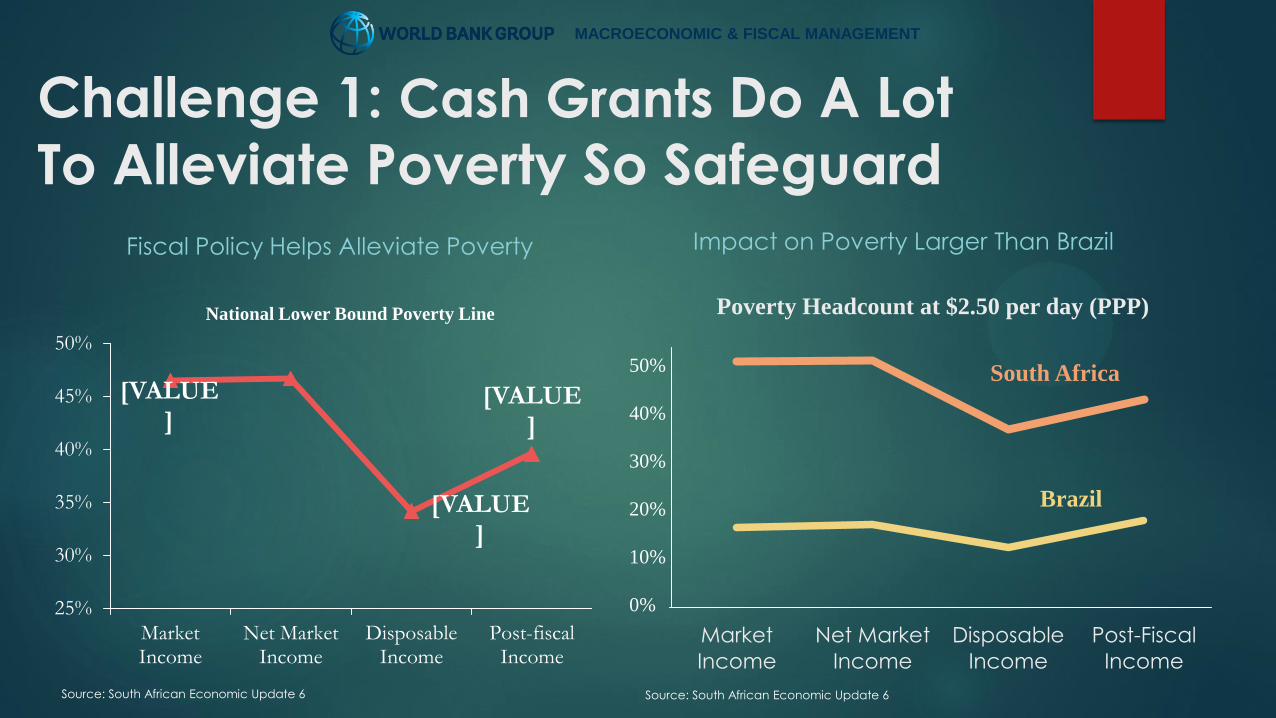

Challenge 1: Cash Grants Do A Lot

To Alleviate Poverty So Safeguard

Fiscal Policy Helps Alleviate Poverty Impact on Poverty Larger Than Brazil

[VALUE]

[VALUE]

[VALUE]

25%

30%

35%

40%

45%

50%

MarketIncome

Net MarketIncome

DisposableIncome

Post-fiscalIncome

Market

Income

Net Market

Income

Disposable

Income

Post-Fiscal

Income

Poverty Headcount at $2.50 per day (PPP)

Brazil

South Africa 50%

40%

30%

20%

10%

0%

National Lower Bound Poverty Line

Source: South African Economic Update 6 Source: South African Economic Update 6

MACROECONOMIC & FISCAL MANAGEMENT

Challenge 2: Taxes & Cash Grants Narrow Income Gap But 0.77 Gini Requires Jobs

Taxes & Spending Lower Gini Reduction Large But Gini Is Still Higher

Than Elsewhere

0.771 0.75

0.694 0.695

0.25

0.35

0.45

0.55

0.65

0.75

Market

Income

Net

Market

Income

Disposable

Income

Post-Fiscal

Income

Final

Income

Gini Coefficient

0.579

0.771

0.694

0.25

0.35

0.45

0.55

0.65

0.75

Market

Income

Net Market

Income

Disposable

Income

Post-Fiscal

Income

Final Income

Gini Coefficient

0.4

South Africa (2010)

Brazil (2009)

Mexico (2010)

Indonesia (2012)

MACROECONOMIC & FISCAL MANAGEMENT

Challenge 3: How Does Fiscal

Policy Support Growth and Jobs?

ASSESSING GROWTH & JOB IMPACT OF FISCAL INTERVENTIONS

MACROECONOMIC & FISCAL MANAGEMENT

Fiscal Instruments & Private Sector

Taxes

•Corporate

•Labor

• Indirect

Infrastructure

•Raises Demand

•A Public Good

•Expands Productive Capacity Private

Social Benefits

•Social Benefits (Health and Education)

•Pensions

•ALMP

•Education

•Health

MACROECONOMIC & FISCAL MANAGEMENT

Just One Example:

How The Corporate Tax System Works IS THE CORPORATE TAX SYSTEM SUPPORTING INVESTMENT AND JOB

CREATION?

MACROECONOMIC & FISCAL MANAGEMENT

What Is A Marginal Effective Tax Rate?

A Tool That Measures Burden of Tax On The Marginal Investment

With Taxes Rate Of Return Has To Rise So After Tax Investor Can Still Pay Cost of

Finance + Depreciation

METR: Return On Marginal Investment Equal Return on Risk Free Investment

METR=0 But Revenue Collections Are Positive: Tax Is Collected On All

Investments Earning Above Normal Returns

METR Can Be Negative Implying Marginal Investment is Subsidized

Finding 1: Effective Corporate Tax

On Manufacturing Is Competitive

MACROECONOMIC & FISCAL MANAGEMENT

Effective Corporate Tax Rates By Country, 2014

South Africa

-20

-10

0

10

20

30

40

50

60

Arg

en

tin

aC

ha

dU

zbe

kis

tan

Co

lom

bia

Fra

nc

eU

rug

ua

yB

razi

lC

ost

a R

ica

U.S

.R

uss

iaS.

Ko

rea

Ve

ne

zue

laP

eru

Ind

iaJa

pa

nG

uya

na

Pa

kis

tan

Eth

iop

iaB

oliv

iaA

ust

ralia

Ita

lyD

om

inic

an

R.

Ge

rma

ny

Au

stria

Rw

an

da

Ka

zakh

sta

nSp

ain

Ph

ilip

pin

es

Ira

nEc

ua

do

rZa

mb

iaIn

do

ne

sia

U.K

.N

ew

Ze

ala

nd

No

rwa

yC

hin

aP

an

am

aG

eo

rgia

Po

rtu

ga

lD

en

ma

rkTu

nis

iaN

ige

ria

Slo

va

k R

ep

ub

licM

exic

oLu

xe

mb

ou

rgM

ala

ysi

aSa

ud

i Ara

bia

Be

lgiu

m Fiji

Hu

ng

ary

Est

on

iaV

ietn

am

Mo

roc

co

Sw

itze

rla

nd

Ma

da

ga

sca

rN

eth

erla

nd

sFin

lan

dSo

uth

Afr

ica

Sw

ed

en

Gh

an

aIs

rae

lP

ola

nd

Eg

yp

tTa

nza

nia

Gre

ec

eC

zec

h R

ep

ub

licTa

iwa

nB

an

gla

de

shLe

soth

oTh

aila

nd

Ukra

ine

Ice

lan

dC

roa

tia

Sie

rra

Le

on

eR

om

an

iaJo

rda

nP

ara

gu

ay

Ja

ma

ica

Slo

ve

nia

Ku

wa

itIre

lan

dB

ots

wa

na

Ma

uritiu

sC

hile

Ug

an

da

Ca

na

da

Latv

iaSin

ga

po

reQ

ata

rTr

inid

ad

Bu

lga

ria

Turk

ey

Ho

ng

Ko

ng

Se

rbia

Ke

nya

Source: Chin and Mintz, 2014

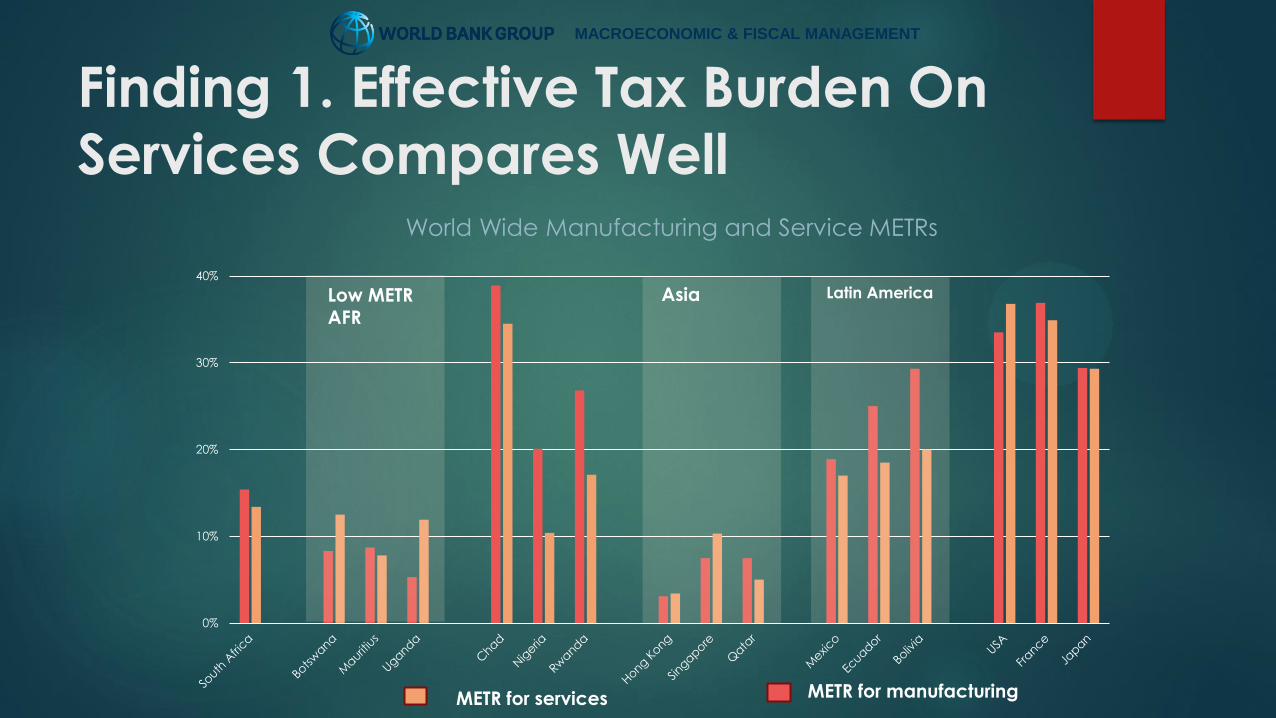

Finding 1. Effective Tax Burden On

Services Compares Well

MACROECONOMIC & FISCAL MANAGEMENT

0%

10%

20%

30%

40%

World Wide Manufacturing and Service METRs

METR for manufacturing METR for services

Low METR AFR

Asia Latin America

Finding 2. Depreciation Allowances

Work To Reduce Effective Tax Burden

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

Statutory 28% CIT Rate

Marginal Effective Tax Rate on Capital By Sector

MACROECONOMIC & FISCAL MANAGEMENT

Finding 3. Interest Deductibility

Reduces Effective Burden Further

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

De

bt-

to-A

sse

t R

atio

Ma

rgin

al Eff

ec

tiv

e T

ax R

ate

Marginal Effective Tax Rate Using Actual Debt-Asset Ratio of Each Sector

MACROECONOMIC & FISCAL MANAGEMENT

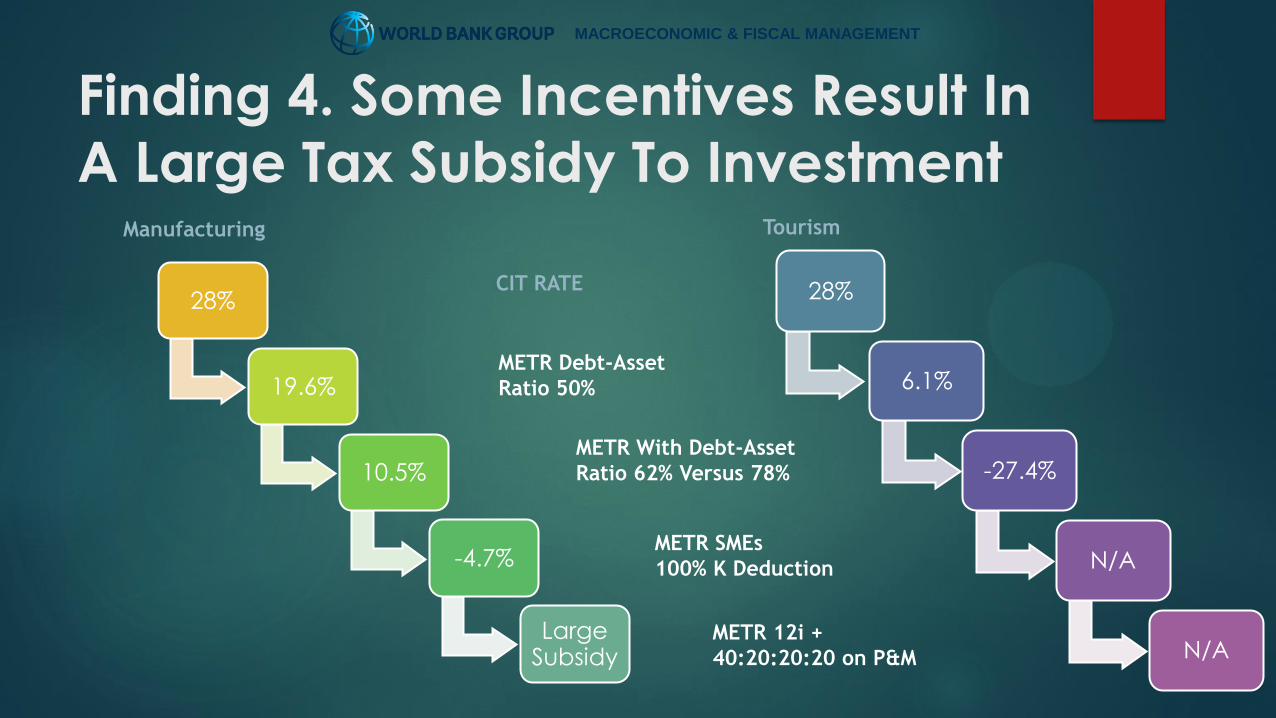

Finding 4. Some Incentives Result In

A Large Tax Subsidy To Investment

28%

19.6%

10.5%

-4.7%

Large Subsidy

CIT RATE

METR Debt-Asset

Ratio 50%

METR With Debt-Asset

Ratio 62% Versus 78%

METR SMEs

100% K Deduction

28%

6.1%

-27.4%

N/A

N/A

Manufacturing Tourism

METR 12i +

40:20:20:20 on P&M

MACROECONOMIC & FISCAL MANAGEMENT

But Does It Work? HAVE FIRMS THAT BENEFITTED FROM ACCELERATED DEPRECATION

ALLOWANCES & OTHER TAX BENEFITS INVESTED MORE?

MACROECONOMIC & FISCAL MANAGEMENT

Is Corporate Tax System

Encouraging Investment? 344,000 Firms With 2 Million Observations From 2009 to 2012

Reduced To A Sample Of 201,687 Observations Covering 74,515 Firms

MACROECONOMIC & FISCAL MANAGEMENT

3 Sectors Received 73% Of Tax

Forgone From R72 bn in Deductions

MACROECONOMIC & FISCAL MANAGEMENT

- 2.0 4.0 6.0 8.0 10.0 12.0

PUBLICHOUSE

EXTSPORT

ART-RECEDUC

RESCHHEALTHTRADE

HOTL-RESTSERV

FINREALPROF

TRANSCONST

AGRIICT

MININGUTIL

MANF

Foregone Tax From Incentives Claimed 2009-12

In Rand Billion

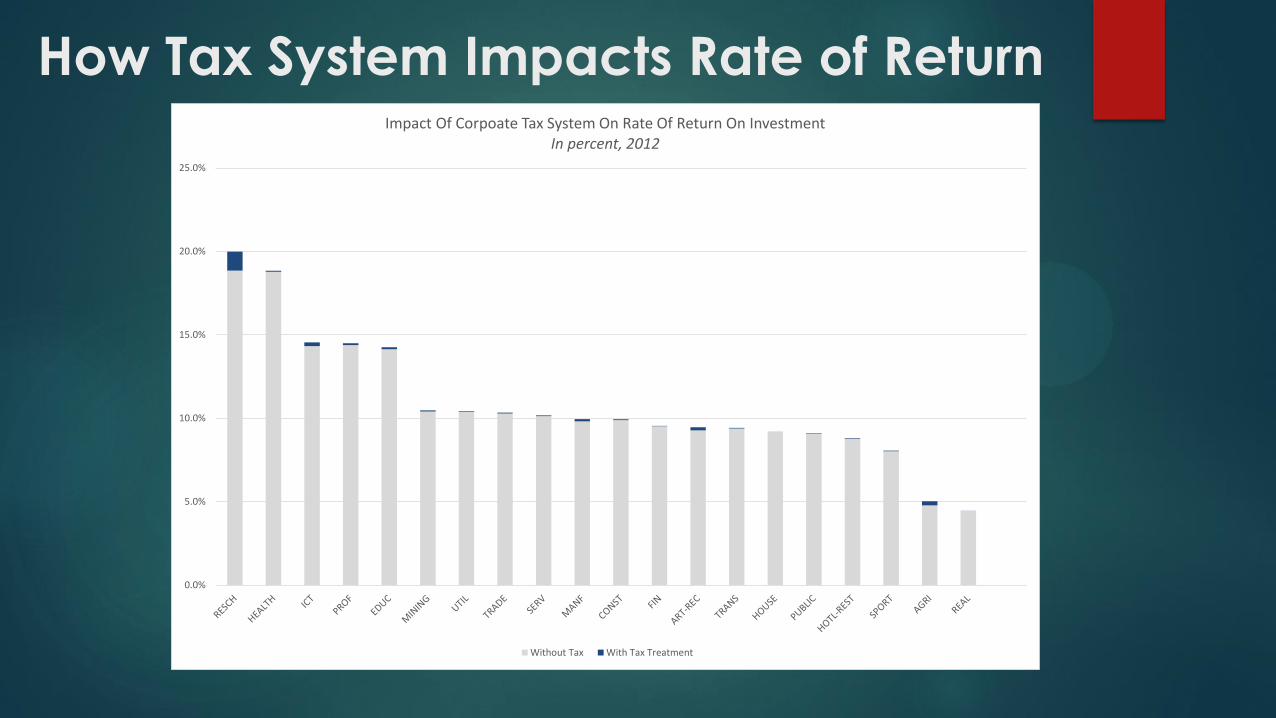

How Tax System Impacts Rate of Return

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Impact Of Corpoate Tax System On Rate Of Return On Investment In percent, 2012

Without Tax With Tax Treatment

Tax Factors That Impact Firm’s Cost Of Capital

Asset Structure

• Buildings (64.5% of Total Assets)

• Plant & Machinery (24.5% of Total Assets)

• Other Assets (11.0% of Total Assets)

Standard Allowances

• Building: 5% depreciation over 20 years

• Plant and Machinery: Straight Line Depreciation Over 5 years

• Wear & Tear Allowance On Plant & Machinery

Additional Incentives

• Manufacturing Accelerated Depreciation Allowance (12 bc) (40:20: 20:20)

• SME Accelerated Depreciation 12e (100% Year 1)

• Machinery, Ship, Aircraft Allowance

• Urban Development Zone Deduction

Leverage

• Actual Debt-Asset Ratio Reported in Tax Return

…Causes User Cost Of Capital To Vary

Example: Metals, Machinery, Equipment

User Cost of Capital Ranges From A Low Of 6% To A High of 20%

No allowance

SMEs

Wear and tear

Machinery, ship or

aircraft

Depreciable asset

Urban development

zones

“ ”

Investment Rises by 2.8%

For Every 1 PP Drop In

Firm’s Cost Of Capital EVIDENCE FROM FIXED EFFECTS REGRESSION BASED ON 201,687 OBSERVATIONS COVERING 74,515 FIRMS.

Investment Response By Sector To Tax

Induced Changes in Cost of Capital

•Agriculture

•Manufacturing

•Services (Private & Public)

High Response

(Coefficient > 1.5%)

•Construction

•Utilities

Medium Response

(Coefficient < 1.5%)

•Mining No Significant

Response

(At 5% level)

Is The Corporate Tax System

Helping Job Creation? Supplement Cost of Capital by Firm From CIT Tax Returns

With Formal Sector Jobs Impact From PIT Tax Returns

MACROECONOMIC & FISCAL MANAGEMENT

How Are Tax Benefits Targeted?

Investment Returns + Jobs Potential

MACROECONOMIC & FISCAL MANAGEMENT

There are a few job

intensive sectors where

incentives could help raise

returns on investment

Clear Case? Agriculture

On Boundary?

Transport

Construction

Hotels

Low Jobs

Low Return

Low Jobs

High Return

We Just Assessed The Corporate

Tax System

Fiscal Spent R4.2 bn in 2011/12

MACROECONOMIC & FISCAL MANAGEMENT

Customs Incentives For The Motor Vehicles Sector

Fiscal Spent R16.3 bn in 2011/12

Evidence Suggests

Tax System Lowers Marginal Effective Tax Burden On Investment

Impact Of Tax System On Rate of Return Is Minimal: Other Economic Factors Matter

More

Investment Does Respond Strongly To Tax Induced Changes in Cost of Capital

But Benefits In The Corporate Tax System Not Necessarily Going To Most Labor

Intensive Sectors

Conclusion

In Times Of Austerity Evidence Based Analysis Can:

Help Evaluate If Policies Have Intended Impacts

Can Help Shed Light On Potential Trade-Offs Between Policies That Aim To

Address Poverty, Inequality and Unemployment

Thank You

We Would Like Thank You All Who Contributed and Supported This Effort

SARs

DTC

National Treasury