Embed Size (px)

Citation preview

Dept of Real Estate and Construction Management Master of Science Thesis no. 501 Div of Building and Real Estate Economics

Macroeconomic Overview and the Correlations Between Selected Real Estate Markets

Stockholm – London – New York

Author: Supervisor: Johan Edenström Mats Wilhelmsson Olof Johnson

Stockholm 2010

2

Master of Science thesis

Title: Macroeconomic Overview and the Correlations

Between Selected Real Estate Markets

Stockholm – London – New York

Authors Johan Edenström and Olof Johnson

Department Department of Real Estate and Construction

Management

Division of Building and Real Estate Economics

Master Thesis number 501

Supervisor Mats Wilhelmsson

Keywords Real Estate, Correlation, Co-Movements, Time Lag

Abstract: Statements such as “there could be a time lag between real estate markets all over the globe” or that “there might be a correlation between different real estate markets” has been present for a long time. We are to investigate if there is some reality in these assumptions focusing on studying if there is a significant presence of correlations and co-movements between three selected real estate office markets. The following markets are undertaken in our study; Stockholm (Sweden), London (United Kingdom) and New York (United States) The first part of this thesis discusses the Fisher-Di Pasquale-Wheaton (FDW) model in order to give a greater understanding of the different market interactions between the real estate- and the financial market. The ripple effect theory discusses how the behavior of one market can come to affect the outcome for its surrounding (sub) markets. The second part provides an overall picture on both the macro economic outlook in each country and also for their individual real estate markets. A great number of aggregated real estate data from several international companies where collected and then converting it into a homogeneous form making it comparable to each other. The information gathered stretches over the time period Q1, 1990 to Q4, 2009. The adjusted database where then used in the econometric software, STATA, in order to investigate the correlations and time lags in between these markets. The correlation tests are undertaken in three different ways during the entire time period of 1990-2009. Our first correlation model is based on the whole time period from 1990-2009. In our second model we divided the time series into two shorter intervals, 1990-1999 and 2000-2009. This re-structure was undertaken in order to be able to investigate if the globalization factor has had an impact on our results. In the third model we compare the differences in correlation and time lag during periods of economic decline versus economic upswing.

Summarizing the results from the STATA correlation tests for all three markets, London stands out as the trendsetter compared to both New York and Stockholm. This is indeed a bit surprising as we thought at first that the trend line should be New York – London - Stockholm. The most reliable interpretation that can be made from all the correlations is that Stockholm (the smallest market) is one quarter behind the two larger ones, New York and London.

3

Acknowledgement This Master Thesis has been conducted at the Division of Building and Real Estate Economics at KTH

Royal Institute of Technology, Stockholm.

First, we would like to express our gratitude to all those who helped us accomplish this thesis with

their support and knowledge. Sotiris Tsolacos (Director European Research, PPR), Tom Francis (Real

Estate Analyst, PPR), Joseph A. Mannina Jr (Executive Vice President, RCA), Jessica Ruderman (Senior

Analyst, RCA), Morris Cox (Quantitative Analyst, RCA), Jeroen Vreeker (Senior Analyst, GPR), Urban

Edenström (CEO, Stronghold) et al.

In addition, great thanks to Newsec AB for helping us with a workplace and their extensive

knowledge.

We would also like to thank our supervisor Mats Wilhelmsson, Professor of Applied Financial

Economics, for his guidance and valuable comments throughout the writing of this thesis.

Finally we would like to thank our families for all their support and feedback.

Many thanks!

Stockholm, 2010-03-21

Johan Edenström and Olof Johnson

4

Table of Contents 1. Introduction ......................................................................................................................................... 6

1.1 Background .................................................................................................................................... 6

1.2 Purpose .......................................................................................................................................... 6

1.3 Method .......................................................................................................................................... 7

1.4 Disposition ..................................................................................................................................... 8

1.5 Limitations and Definitions............................................................................................................ 8

2. Theory and Basic Definitions ............................................................................................................... 9

2.1 4Q – Real Estate Market Model .................................................................................................... 9

2.2 Selected Theories ........................................................................................................................ 11

2.2.1 The Ripple Effect ................................................................................................................... 11

2.2.2 Time Lag and the Correlation Between Markets.................................................................. 11

2.3 Hypothesis ................................................................................................................................... 11

3. Correlation Methods ......................................................................................................................... 12

3.1 Correlation ................................................................................................................................... 12

3.2 XCorrelation Function.................................................................................................................. 12

3.3 Correlation Model ....................................................................................................................... 12

3.4 STATA Outline .............................................................................................................................. 13

4. Data and Variables............................................................................................................................. 14

4.1 Macroeconomic Variables ........................................................................................................... 14

4.2 Real Estate Market Variables ...................................................................................................... 14

4.3 Variables used in STATA .............................................................................................................. 15

5. Market and Region Overview ............................................................................................................ 17

5.1 Market Analysis ........................................................................................................................... 17

5.1.1 Macroeconomic Overview – Sweden ................................................................................... 17

5.1.2 Real Estate Market Overview – Stockholm .......................................................................... 21

5.1.3 Macroeconomic Overview – UK ........................................................................................... 25

5.1.4 Real Estate Market Overview – London ............................................................................... 28

5.1.5 Macroeconomic Overview – US ........................................................................................... 34

5.1.6 Real Estate Market Overview – NYC ..................................................................................... 37

5

6. Correlation and Co-Movement Results ............................................................................................. 42

6.1 Rents ............................................................................................................................................ 42

6.2 Vacancy ........................................................................................................................................ 45

6.3 Yield / Cap Rate ........................................................................................................................... 47

6.4 Business Cycle Correlation .......................................................................................................... 49

7. Analysis .............................................................................................................................................. 50

7.1 RE Market Correlation for New York - London - Stockholm ........................................................ 50

7.2 RE Market Correlation for London’s Submarkets ........................................................................ 52

8. Conclusions ........................................................................................................................................ 53

9. References ......................................................................................................................................... 56

Appendix A. Correlation Outline used in STATA

Appendix B. Correlation Results

6

1. Introduction

1.1 Background

Statements such as “there could be a time lag between real estate markets all over the globe” or that

“there might be a correlation between different real estate markets” has been present for a long

time. We are to investigate if there is some reality in these assumptions focusing on studying if there

is a significant presence of correlations and co-movements between three selected real estate

markets. The current financial turmoil and the major economic setback that has hit the global

economy have made even more immediate to investigate these statements in order to obtain a

higher understanding of how the next real estate related business cycle is to develop.

A more globalized market and a higher awareness of its actors could be one factor affecting the

faster dissemination of the market information flow. Diversified investors acting on several real

estate markets are preparing to get out there again and enter the next business cycle with the best

timing possible on the basis of their individual investment strategies. Obtaining some additional

knowledge of how the real estate markets has developed and had an effect on each other in the past

could give the players some additional understanding before entering the next cycle.

This market correlation awareness could come to improve the timing and behavior among these

investors in the future and enable them to accomplish more favorable pull-outs and obtain higher

returns on their investments. The constantly growing real estate related distress is an alarming factor

all across the globe although at the same time it is presenting opportunities for the investors with

equity to invest.

1.2 Purpose

The main objective of this thesis is to investigate if there is a significant presence of correlation and

co-movements between certain selected real estate markets. The reader is also to be given a more

overall macroeconomic view of these individual markets in the aspect of some historical

development, the current situation and a forecast of the near future.

The historical recap will for the most part extend from 1997 (with the exception of some data going

back to Q1, 1990) until the end of 2009 based on aggregated data on a monthly, quarterly or

annually basis. A more detailed study of the individual market’s business and real estate cycles will

then be the foundation for the search of a possible presence of market correlation and co-movement

among the selected variables. The information dataset in our study will be in the form of both

standard macro variables and also a few chosen real estate variables systematically arranged for

each country and region.

7

1.3 Method

The first stage of the thesis is to provide an overall picture of the real estate market and the variables

affecting its development and possible outcomes. The 4Q- model was used to describe the basic

concepts and the complete market interactions between the real estate- and the financial market.

The selected and significant variables were then to be defined and illustrated in the matter on how

they are collaborating and affecting each other.

A comprehensive data gathering was undertaken in order to obtain all valuable macro data needed

to analyze and present the regional economic development in each region. The regions and markets

selected for this thesis are; Sweden and Stockholm, United Kingdom and London, finally United

States and New York (Manhattan). The macro data gathered for these markets established the base

for the comprehensive market analysis created for each region and where used to describe the

historical development and the current situation within these.

The most difficult part of the research was to find solid and reliable aggregated data on the selected

real estate variables for each market. This was solved by gathering a lot of statistical data from

several companies which we analyzed and then converted into a homogeneous form in order to

make them comparable to each other.

The next step was to investigate the magnitude of correlation and the presence of time lags between

then real estate variables of the selected markets. The converted homogeneous data where then

used in the econometric software, STATA, used to investigate the correlations and time lags in these

markets. The current programming language used in our study paper and the programming code can

be found in appendix A.

The result is then to be analyzed and we will also include some external work and assumptions from

other papers and articles. We will investigate if the “ripple-effect” can be established based on our

correlations and how they might come to affect the current markets in the near future.

8

1.4 Disposition

Chapter 2 presents the theoretical framework, literature review, basic definitions and description of

the different macro economic variables, related theories and our hypothesis.

Chapter 3 contains the econometric correlation model used in this thesis and our programming

code.

Chapter 4 describes the actual data and variables used in this study. The macro- and real estate

variables are first presented in their fundamental structure (local currency and measurement) and

then as the converted homogeneous data used in the STATA software.

Chapter 5 presents a macroeconomic overview for the three countries (United States, United

Kingdom and Sweden), followed by a real estate market overview over the respective main region

and city for each country (New York, London and Stockholm).

Chapter 6 displays the selected results from our correlations which are divided into categories on

the basis of the variable type. Comments and interpretations are also added under each chart in

order to facilitate the results for the reader.

Chapter 7 presents an analysis of the results obtained in the previous chapter.

Chapter 8 contains discussion and a concluding summary of the results.

1.5 Limitations and Definitions

This master thesis main focus lays on the real estate office market in New York, London and

Stockholm. We have chosen the central business district (CBD) in each city as our area to examine. In

these markets we have selected three main variables: rent, vacancy and yield/cap rate for our

correlation model. All variables used in the econometric methods are adjusted in order to be

comparable against each other.

Currency: daily exchange rates converted into a quarterly mean value acting as a quarterly local currency coefficient. The coefficient has then been used to transform all data into one consistent currency, USD.

Area/Space: all office space is transformed into square feet (sqf).

Only the London market has been inspected more closely as a domestic market, consisting of the

three submarkets that are defined below.

The time period stretches over 20 years from January 1990 until December 2009.

CBD in New York and London are defined as followed:

CBD New York – Manhattan (Downtown, Midtown South and Midtown)

CBD London – London City, West End and Docklands/Canary Wharf

9

2. Theory and Basic Definitions

2.1 4Q – Real Estate Market Model

The Fisher-Di Pasquale-Wheaton (FDW) model

Figure 1- The Fisher Di Pasquale Wheaton model

The FDW model is a constructive tool to use when explaining the basic concepts and interactions

between the real estate- and the financial market. The complete market interactions are illustrated

as a four-panel graph and are used as an interactive pedagogical instrument that facilitates the

comprehension of the simultaneous market movements affecting the whole industry. The four

quadrants are used to explain the interactions between urban markets (such as employment and

required space), capital markets, annual construction and annual stock adjustment.1 The correlations

between the real estate market, capital market (the real economy) and the construction sector all

leads to a long-run equilibrium and is represented by the rather thick square in the panel graph

above.

Quadrant One (Q1) – The Demand Function on the Market for Space

The first quadrant (Q1) represents the total demand on the office rental market. Given a certain

stock a specific rent is being offered.

Variables that are affecting the outcome of the first panel are the ones related to demand and

supply. In our case the unemployment rate and the vacancy level are relevant thus its effect on the

demand and supply function for office space.

1 Geltner D, Miller N (2006)

10

Quadrant Two (Q2) – The Valuation Function

The second quadrant (Q2) corresponds with the asset valuation. In this quadrant the given market

rent is transformed into a present market value by discounting at the cap rate or yield. The current

rent and yield level provides the equilibrium asset value or price that investors are willing to pay.

The variables being used in this thesis that are of interest to this panel are; prime rent, average rent,

asking rent, inflation, bank rate, GDP* and yield/cap rate. * Note: Real estate prices are found to be significantly influenced by GDP growth rates and provide a good long-term hedge

against inflation but a poor year –to-year hedge.

Quadrant Three (Q3) – The Construction Function

The third quadrant (Q3) shows how the construction sector reacts on the investments being

undertaken on the open market. By studying the current market price (asset values) that investors

are offering for the existing real estate stock, the construction sector can decide on whether to

invest in new construction or not. Construction will take place when the market prices are above the

construction costs.

A variable that could come to affect the outcome of this panel and that is being used in this thesis are

the transaction/investment volumes (indicates the current price that the investors are offering).

Quadrant Four (Q4) – The Adjustment Supply

This fourth quadrant displays how the depreciation factor is developing, on the basis of the annual

difference between the volumes of construction opposed to the decrease in the existing stock. There

are no significant variables used in our study that directly could affect this panel. On a more

generalized level, variables such as a region’s economic development could come to affect its

attractiveness and there for the level of construction undertaken and the volume of depreciation.

11

2.2 Selected Theories

2.2.1 The Ripple Effect

The Ripple Effect is a term taken from the ever expanding ripples across the water surface when an

object is dropped into it, where an effect from an initial state (origin) can be followed outwards

incrementally. The effect is indirect and spreads out from the direct or main effect to reach areas or

populations far away from its origin. This term is often used in economical expressions to explain the

time lag after a major financial event, e.g. the collapse of Lehman that came to spread huge ripples

all over the world’s stock exchanges. An easier way of describing the Ripple Effect is for example

when a person decides to cut down on his/hers expenses which reduces the income of those who are

gaining from this persons spending pattern. This will cause an indirect effect on the second party’s

spending capacity due to the behavior of the first person.

In the paper “the Convergence of Regional House Prices in the UK”,2 the Ripple Effect is discussed of

being present within the UK housing market. The article is stating that the house prices increase

initially in the South East region before it spreads to other regions. When the global market is

growing stronger and more foreign companies are able to invest with the same knowledge and rules

as the domestic actors, the Ripple Effect hypothesis should be applicable on a global level as it is on

the smaller domestic markets. London is for example the financial centre in Europe and has one of

the largest real estate markets within this region. A development in the UK domestic yield should in

turn as an indirect effect gradually spread to the other main real estate markets in Europe.

2.2.2 Time Lag and the Correlation Between Markets

The word lag or lagging is defined as a measurable economic factor that changes after the economy

has already begun to follow a particular pattern or trend. Time lag could then be described as the

measurable time period of this factor and could also be interpreted as the time difference between

two co-moving markets. One way to statistically prove that two markets are co-moving is through

correlation testing (see 3.1 Correlation). In the article “Global Real Estate Markets: Cycles and

Fundamentals”3 the writers perform a correlation between several global real estate returns and

then studying how they are affected by world GDP. As they say in there abstract “international

property returns move together in dramatic fashion”, our assumption is that additional real estate

variables (not merely the return) are moving together but no evidence of a actual time lag has yet

been proven.

2.3 Hypothesis Our hypothesis is that we believe there is a significant correlation and presence of time lag between

the three selected markets. The globalization factor has had a direct affect on the transparency of

the real estate market and there for influenced the information flow considerably. With more

international investors and real estate portfolios functioning on several markets this statement

should get additional support due to the larger amount of activity and available real estate related

information. It is our belief that one possible outcome from this transparency factor will be visible in

stronger correlation values and a decreasing time lag development between the selected markets.

2 Cook (2003)

3 Case B, Goetzmann W, Rouwenhorst K.G (1999)

12

3. Correlation Methods

3.1 Correlation Correlation measures the degree to which two series are moving together and is expressed as a value between 1.0 and -1.0. A value near 1.0 explains a close positive movement between the two series where on a value near -1.0 is of the opposite. For example; if product A on a market is highly positive correlated (close to 1.0) with product B, then we could say that the two products A and B are moving together in the same direction with a significant co-movement. If the correlation value between the two products is close to -1.0 they are instead moving very strongly in different directions.4 Theoretical definition:

𝐶𝑜𝑟𝑟 𝑋, 𝑌 = 𝑐𝑜𝑣 (𝑋 ,𝑌)

𝑠𝑑 𝑋 ×𝑠𝑑 (𝑌)=

𝐸 𝑋−𝜇𝑋 𝑌−𝜇𝑌

𝑠𝑑 𝑋 ×𝑠𝑑 (𝑌)

3.2 XCorrelation Function Xcorrelation or “xcorr” as the function is written in the STATA programming language is the only

function used in all of the correlations that has been undertaken. The “xcorr” function is taking the

autocorrelation in the time series into consideration and makes the series constant. If we would have

used a normal correlation function such as “corr” we would have had a problem with the

interference of the autocorrelation between the two time series. By using the “xcorr” function we

are instead avoiding this problem and making the autocorrelation constant. The “xcorr” is there for

presenting us with a more moderate and true value correlation coefficient then of the normal “corr”

function. The “xcorr” function is also presenting a graph or a table (depending on your choosing) that

shows the correlation development over a selected time interval.

3.3 Correlation Model In this thesis we are using our values in three different ways during the entire time period of 1990-

2009. All models have the ground purpose to find the most significant time lag in possession of the

strongest correlation value between the two variables that we are running against each other. The

first correlation model is based on the whole time interval of 1990-2009. In our second model the

complete time interval is divided into two time series consisting of ten years each i.e. 1990-1999 and

2000-2009. The reason for dividing up the whole interval into a pre 2000 and after 2000 is to become

able of observing whether the globalization factor has had an impact on both the correlation and a

possible time lag. In our third model we compare the differences in correlation and time lag during

an economic decline versus and upswing.5

4 Wooldridge J M (2006)

5 The comprehensive correlation model can be found in appendix A

13

3.4 STATA Outline The STATA outline for the three different models is presented in short below:6

Principal Outline:

1. General Correlation

xcorr var1 var2 xcorr var1 var2, table Discerns the highest correlation value at a certain time lag

2. Periodically (per 10- years) Correlation

xcorr var1 var2 if obs<41, lag(10) [obs<41 gives the interval 1990-1999] xcorr var1 var2 if obs<41, lag(10) table xcorr var1 var2 if obs>40, lag(10) [obs>40 gives the interval 2000-2009] xcorr var1 var2 if obs>40, lag(10) table Determines if the time lag has changed and also how the correlation coefficient is developed

3. Business Cycle (GDP based) Correlation

xcorr varX1 varY2 if BCX_Y==0, lag(4) xcorr varX1 varY2 if BCX_Y==0, lag(4) table [==0 economic decline] xcorr varX1 varY2 if BCX_Y==1, lag(4) corr varX1 varY2 if BCX_Y==1, lag(4) table [==1 economic upswing] Determines if there is any difference in time lag and the correlation value depending on the

appearance of the business cycle, i.e. in an economic decline or an upswing.

6 The comprehensive correlation model can be found in appendix A

14

4. Data and Variables

4.1 Macroeconomic Variables

GDP Development (percent)

The annual percentage GDP change (delta) for each country, between the time-period 1991-

2009 (in fixed prices)

Source: The Swedish National Institute of Economic Research (NIER)

Inflation (percent)

The annual average percentage change (delta) for each country, between the time-period

1997-2009.

Source: The Swedish National Institute of Economic Research (NIER)

Unemployment Rate (percent)

The year-end unemployment rate in percentage for each country, between the time-period

1997-2009.

Sources: The European Central Bank (ECB) and the Bureau of Labour Statistics (BLS)

Bank Rate (percent)

The second quarter bank rate is given in the month of July between the time-period 1997-

2009.

Sources: The Swedish Riksbank, the Bank of England and the Federal Reserve

4.2 Real Estate Market Variables

Prime Rent (excluding NYC)*

The nominal prime rent per square meter and year, in local currency within the time period

1990-2009.

Source: PPR

Average Rent (excluding NYC)*

The nominal prime rent per square meter and year, in local currency within the time period

1990-2009.

Source: PPR

Asking Rent (only for NYC)*

The asking rent level in the gross USD per square feet and year.

Source: PPR

Vacancy (percent)*

The overall vacancy rate in percentage of total unoccupied space in the local market

(occupied square meter or square feet / inventory)

Source: PPR

15

Yield and Cap Rate*

The yield is provided for the UK and the Swedish market and is defined as the initial yield.

The Cape Rate is provided for the U.S. market and is calculated by dividing forecast NOI (Net

operating Income) over the next year by today's modeled value.

Note: The cap rate has a slightly different calculation to the European Yield, but they are

virtually the same and in our econometric model in STATA they are used interchangeably.

Source: PPR

Transactions / Investment Volumes (cross-border and domestic)*

The transaction volume for Sweden is in billion SEK, on a quarterly basis and only covers

transactions ≥ 100 MSEK. The volumes for New York and London are on a monthly basis,

transformed to a quarterly amount in order to make it more comparable with the aggregated

data. All volumes are in million USD and are also only covering deals ≥ USD 10 million.

Sources: RCA (Real Capital Analytics) and Newsec

The Historical Performance of the Listed RE-Companies in Specific Regions

The index is a is a free floating weighted index that tracks the performance of all the

domestic property companies on the stock exchange with a market capitalization over USD

50 million.

Source: GPR (Global Property Research)

* (only for office properties)

4.3 Variables used in STATA

PRX = Prime Rent for City X

Prime Rent for London (London City, West End, and Docklands/Canary Wharf) and

Stockholm. The converted homogenous unit is: U.S. dollars per square feet.

Source: PPR

ARX = Average/Asking Rent for City X

Average Rent for London (London City, West End, and Docklands/Canary Wharf) and

Stockholm, Asking rent for New York. The converted homogenous unit is: U.S. dollars per

square feet.

Source: PPR

VACANCYX = Vacancy Rate for City X

Vacancy rate for New York, London (London City, West End, Docklands/Canary Wharf) and

Stockholm. The overall vacancy rate in percentage of total unoccupied space in the local

market (occupied square meter or square feet / inventory).

Source: PPR

16

YIELDX =Yield/Cap Rate for City X

The yield is provided for London (London City, West End, Docklands/Canary Wharf) and

Stockholm, and is defined as the initial yield. The Cape Rate is provided for New York and is

calculated by dividing forecast NOI (Net operating Income) over the next year by today's

modeled value.

Note: The cap rate has a slightly different calculation to the European Yield, but they are

virtually the same and in our econometric model in STATA they are used interchangeably

Source: PPR

BCX_Y = Business Cycle for Country X vs. Y

This is a dummy variable based on a comparison between the gross domestic product (GDP)

in country X and Y. If the GDP value for country X is larger than its mean value during the

given time period a variable with value 1 is generated. If it on the other hand is minor than

the mean value the generated variable is given a value = 0. The value 1 stands for an

economic upswing and the value 0 for an economic decline. When combining the business

cycle for country X and Y the variables need to match, e.g. Q1, 1999 country X = 1 and

country Y= 1 leads to a combined business cycle showing = 1. If the variables do not match a

blank post is created and excluding that time period in order to only use corresponding

variables in the business cycle tests.

17

5. Market and Region Overview

5.1 Market Analysis

5.1.1 Macroeconomic Overview – Sweden

Diagram 1 - Macroeconomic Indicators Sweden

Since the last economic set-back in the beginning of the year 2000, Sweden has had a long period of

sustained economic upswing, intensified by growth in domestic demand and solid exports.

Regardless of the stable and strong historical development of the Swedish market and underlying

fundamentals it to came to a halt in the third quarter of 2008.7 The financial crisis that hit the global

economy and led to the historically severe synchronized economic depression has been the fuel in

the steep downturn that has been present in the Swedish market. The demand for both investment

items and consumer goods has dropped considerably with a long period of substantial decreasing

GDP. The deteriorating global conditions have affected the Swedish industry quite hard in the form

of reduced export demand and consumption. The Swedish export industries generate more than half

of the country’s GDP and has had a major setback due to that these markets and industries initially

registered the majority of the dramatic changes.8,9

7 Newsec

8 NIER

9 The Swedish Riksbank

-6

-4

-2

0

2

4

6

8

10

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Macroeconomic Indicators - Sweden

Sweden-GDP Sweden-Inflation Sweden-Unemployment rate Sweden-Bank rate

Source: NIER, ECB, Riksbanken

18

The policy interest rates are currently at historic lows and the fiscal policy measures that have been

implemented has begun to improve the conditions on the Swedish financial market. In the spring

there were various accounts of risk premiums (RP’s) dropping back where it seemed to be somewhat

easier for the players to get financing. The Swedish krona grew stronger again, the stock market

prices increased and the market has upon today continued to normalize. This first rise could be the

first part of a “double dip” cycle which is yet to be determined.10

The sharp drop in Sweden’s GDP has stopped and the overall assessment is that the GDP will be

down by 5.0 percent at the end of 2009 which is the weakest since the beginning of the 90’s. The

forecast for 2010 is that the GDP growth will pick-up (might be some temporary drops along the way)

due to a domestic rise in output and demand. The tendency in other countries will also improve

which will result in an increase in demand for Swedish exports. All factors taken into account the

forecast for the GDP at the end of 2010 is 1.5 percent and it will continue to rise along with the

international recovery.11

As a result from the rescue package for the banking sector and the low interest rates, the household

consumption will continue to increase but with some resistance due to the rising unemployment. The

major drop in the GDP has directly affected the labour market and since last year the unemployment

rate has climbed from 5.9 percent to 8.3 percent (see diagram 1). The forecast is that the

unemployment will continue to rise further with almost 12 percent at the end of 2011.12

The current financial situation has forced firms to implement efficiency programs to improve their

productivity in order to counteract the falling demand. There is a significant increase in the number

of personnel lay off’s followed by a declining demand of office space. The manufacturing and

construction industries lie in an early part of the economic cycle which has had a significant effect on

the domestic labour market. Employment trends normally follow GDP trends with a six-to-twelve

month lag and therefore the employment growth rate is forecast to stabilize in late 2011.

The inflation forecast for the next few years is set at about 1 percent at the end of 2011 and any

additional stimulation packages (fiscal policy measures) that the Swedish Government might produce

could come to affect the inflation forecast. The repo rate is predicted to remain at the current all-

time low of 0.25 percent the first two quarters of 2010. The Swedish Riksbank will then slowly begin

increasing interest rates and by the end of 2011 the forecast is that the repo rate will be 1.5 percent.

Long-term rates are predicted to increase to some extent due to the bottoming out of the economic

cycle and expectations of increasing future growth rates. However, there is currently an endogenous

tightening in the credit market, and the bank’s interest-rate margins are high due to expected credit

losses and consolidations in their balance sheets. 13,14

10

The Swedish Riksbank 11

NIER 12

NIER 13

The Swedish Riksbank 14

NIER

19

Diagram 2 - Transaction Volume Sweden

The transaction side came to a halt in the second quarter of 2008 due to the financial economic set-

back which directly affected the investors operating on the Swedish market. After almost a decade of

steadily increasing transaction volumes the financial turmoil all of a sudden made it almost

impossible to get a satisfying financing from the banks which came to affect the IRR calculations.

Capital values were hit by a two-fold impact of adverse rent and yield development leading to a

decrease of market values. Non-distressed property owners were reluctant to sell at the yield levels

being offered by the investors, resulting in a price disagreement between the two parties. The few

transactions that took place in the first quarter of 2009 were made by low leverage funds,

institutions, municipal housing, equity-financed property companies and family owned property

companies. The cross-border capital flow has been very weak during 2009 and the foreign investors

are assumed to stay within their home market for some time to come. The overall transaction

activity on the Swedish market is forecast to continue on a very low level for a period of time.15

15

Newsec

0

20

40

60

80

100

120

140

160

Transaction Volume - Sweden

Domestic Buyers International Buyers

Billion SEK

Source: Newsec

20

Diagram 3 - GPR Index Sweden

The real estate crash in the beginning of the 90’s came to set a very slow positive development pace

when the Swedish market finally turned. Startled and cautious banks sitting on distressed assets that

they’ve confiscate due to different actor’s bankruptcy, were now regulating the tempo of the market

growth. The development of the public real estate companies got its real upswing after the IT crash

in the beginning of 2002 when the Swedish economy got back on its feet.

When comparing the GPR Index for the Swedish market with the Index for UK and U.S. a major value

decrease is a shared trend. The Swedish index has gone down approx. a third from its top value in

2006, which can be compared with the UK and U.S. index that has gone down two thirds respectively

half its value within the same time period.

0

50

100

150

200

250

300

350

GPR Index - SwedenSource: GPR

21

5.1.2 Real Estate Market Overview – Stockholm

Stockholm is the economic centre of Scandinavia and is ranked as the most attractive Scandinavian

location for business and investments by the European regional Growth Index (E-REGI). Stockholm

has amongst its neighboring capitals, the highest GRP (Gross Regional Product) and growth. The

average economic growth for Stockholm during the period 1994 and 2006 were at 4.1 percent which

can be compared to 3.2 percent for the country as a whole. 16,17

The population of Stockholm has for the last three decades increased faster than the population of

Sweden itself. The forecast for the capital’s population growth during the years to come is at 1.2

percent a year.18

Diagram 4 - Annual Population Growth

The service sector is dominant in the Stockholm region and the large financial sector was therefore

rather late to be affected by the financial turmoil due to its late position in the economic cycle. The

region is expected to be less affected by the global recession than Sweden as a hole due to

expectations of generally smaller drops in demand in the service sector that in other industries.19,20

16

The City of Stockholm 17

Eurostat 18

SCB 19

Newsec 20

Jones Lang LaSalle

0,0%

0,2%

0,4%

0,6%

0,8%

1,0%

1,2%

1,4%

1,6%

1,8%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Annual Population Growth

Stockholm Sweden

Source: Datscha

22

Stockholm CBD has an office stock of approx. 1.8 million square meters, mainly situated in the

different sections of the city shown within the CBD polygon. The main commercial office blocks are

located around and in between the outer CBD sections such as Sergels Torg (the Central Station),

Hötorget and Stureplan. If you were to include the prime submarkets of Marievik, Kista, Solna

Business Park etc. the total combined office stock would land at about 12 million square meters.

During 2009 approx. 70 000 square meters of new office space entered the market and almost a

third of it is located within the CBD. The vacancy in these new office premises are in fact close to zero

showing a solid demand in prime office space.21,22

Map 1 - Stockholm CBD

21

Newsec 22

Jones Lang LaSalle

23

Diagram 5 - Prime Rent Stockholm

The rents have after a couple of years of steadily increasing growth finally come to a halt and we are

now seeing falling rents in all submarkets. Since the middle of 2008 there has been a decrease of 5-

10 percent in the submarkets (outside the CBD) and for prime office space, rents have fallen by 10-15

percent. A more common factor on the rental market is the “rental discount” which is forecast to be

more present for some time to come. The submarkets are predicted to register ongoing falling rents

throughout the rest of the year and far into 2010. The rental fall is expected to be more severe for

prime office space due to several projects entering the market during this period which will put

additional pressure on the rental levels.

Diagram 6- Prime Yield Stockholm

After almost half a decade of increasing yields it all came to a turning-point at the end of 2002. The

solid economic development in the years that followed led to decreasing yields and causing the gap

between prime CBD properties and long-term government bonds to almost disappear.

The rapid yield growth that has been present for the last period has finally started to stabilize. This is

mainly a result of decreasing interest rates and that the demand for prime and modern properties

are picking up, combined with a relatively low supply. The major problem on today’s market is still

the trouble of getting the banks on reasonable terms due to their current lending policies. The

forecast for the rest of 2009 is that the yields are to continue rising due to aversion for lower rental

levels and rising vacancies.

2 500

3 000

3 500

4 000

4 500

5 000

Prime Rent Source: Newsec

SEK /sqm

3,5%

4,0%

4,5%

5,0%

5,5%

6,0%

6,5%

7,0%

Prime YieldSource: Newsec

24

Diagram 7 - Vacancy Rate Stockholm

Vacancies have been on a rather constant level for the last years but since the financial crisis started

the demand for office space has decrease. The difficulties in signing new lease agreements during the

end of 2008 caused the vacancy rate to stabilize but due to major layoffs during 2009 and the new

office space coming out on the market, the vacancies are currently rising in all submarkets. The

forecast for Greater Stockholm is that the vacancy is going to continue rising for some time to come

due to falling employment and other factors affecting the demand.

Diagram 8 - Transaction Volume Sweden

The transaction volumes are to pick up during 2010 and the demand for investing in real estate is

expected to increase further as the general economy is stabilizing. One major factor that could come

to set the pace on the transaction market, is the fact that financing most likely will continue to be

very difficult to negotiate and remain restrictive among banks. One theory about this statement is

that the banks were in severe panic during the crisis in the beginning of the 90’s were a lot of

liquidations took place. Today they are in possession of more knowledge and experience and are

there for in a holding mode that could be present for some time to come.

0%1%2%3%4%5%6%7%8%9%

10%

Vacancy RateSource: Newsec

0

20

40

60

80

100

120

140

160

Transaction Volume - SwedenBillionSEK

Source: Newsec

25

5.1.3 Macroeconomic Overview – UK

Diagram 9 - Macroeconomic Indicators UK

Since the last financial setback which was created by the real estate crises in the 90’s UK have had a long turn of economic expansion, with a temporary decline during 2000 and the beginning of 2001. The expansion of the UK economy had an abrupt end in 2007 when the global financial crises had its impact on the UK market. With a steep fall in GDP, quick rising unemployment rates, severe losses for the banks and the real and nominal spending falling at record rates, the financial system crumpled. The Bank of England used both monetary and fiscal programs such as “the asset purchase program”23 and a historical low policy interest rate (bank rate) as tools to ease the fall. The UK economy is currently in a more stable phase but the recovery period is anticipated to be rather long.

23

Bank Of England (2009)

-6

-4

-2

0

2

4

6

8

10

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Macroeconomic Indicators - UK

UK-GDP UK-Inflation UK-Unemployment rate UK-Bank rate

Source: NIER, ECB, Bank of England

26

The UK has as many other western countries started to develop into a more service focused economy and away from its dependence on heavy industry which was once the aorta in economy. The main service sectors such as banking, insurance and business services are some of the largest contributors to the UK GDP.24 Since the financial crisis the UK exports has declined very sharply and there has also been a large dip in import which came to affect the GDP outcome considerably. The pound sterling (GBP) has seen a huge drop against other main currencies, especially compared to the strong Euro. This could lead to a larger export volume due to the lower prices than of the surrounding countries. The low pound sterling has together with the falling real estate prices drawn overseas money to the UK real estate market. The UK GDP dropped 7 percent from the second quarter 2007 until same period in 2009 (see diagram 9),25 this is the lowest GDP figure since 1991.26 Two of the main reasons for such a huge drop are the large fall in private consumption and in business investment. The monetary and fiscal politics has now managed to ease its fall and the GDP is predicted to start growing again in the beginning of 2010.27 Since 2000 the unemployment rate has been stable at around 5 percent. With a steady stream of

foreign labour force, the UK people have been able to raise their living standard and develop an even

stronger service sector. This positive pattern did come to a change due to the crisis. The

unemployment rate started to grow rapidly in the end of 2007 and have continued since that. Today

the unemployment rate has risen up to almost 8 percent of the population. Only during Q3 2009

unemployment increased with 88,000 people to a total of 2.47 million people.28

The Bank of England inflation goal is set to 2 percent and the overall inflation between 1997 and

2007 was slightly below that goal. During 2008 we could see that the inflation rate grew rapidly as a

consequence to a rise in the bank rate the previous year. The preceding year inflation level was

corrected when Bank of England lowered the bank rate once more. Figures for 2009 shows the

inflation at 1.9 percent and the predicted value for 2010 shows 1.7 percent. The current bank rate at

0.5 percent is historically low and the prediction for 2010 is an increase up to 1.5 percent.29

The UK investment market was the first in Europe to see commercial real estate values being

corrected substantially. Between the market peak in the summer 2007 and December 2008,

commercial real estate values went down with 35 percent according to IPD. Today’s problems are

still a tight consumer credit policy as banks continue to repair their own balance sheets. The high

levels of lend out money and the large fall on asset pricing has put many banks in a really tight spot.

One of the main problems is that a large group of foreign lenders have left the UK market entirely

too instead focus on their domestic market. A combination of this deserted foreign lenders and

constrained real estate market with companies that needs to be refinance when their existing loans

runs out puts the domestic banks in problems. As a result from this, there will be a shortage of

liquidity for many banks. As recoil to the current market situation a large number of foreign

opportunistic investors have started to invest in UK real estate, for and most in central London.

24

CIA 25

HM Treasury 26

BBC News (2008) 27

Bank of England (2010) 28

Bank of England (2009) 29

Bank of England (2010)

27

Diagram 10 - GPR Index UK

The listed RE- stocks on the LSE (London Stock Exchange) have as many public real estate companies

worldwide seen a really positive development for their stocks during the beginning of the 21’st

century. The strong development in RE-stock value seen on LSE from 2002 until 2007 is now more or

less gone as the stocks are purchased in the same level as in 2003.

0

100

200

300

400

500

600

700

GPR Index - UKSource: GPR

28

5.1.4 Real Estate Market Overview – London

London is the city in Western Europe with the largest population, more than 7.56 million inhabitants

and as many as 50 different ethnic groups populates the city. London is the major financial centre in

Europe. According to PriceWaterhouseCoopers London qualifies as the 5th largest city economy in

the world (2008). The city economy stands alone for 17 percent of UK’s total GDP. One fifth of

Europe’s largest companies have their headquarters situated in London.30

Diagram 11 - Annual Population Growth

The population growth during the years to come is at 2.5 percent per year (UK as a total is expected

to grow 0.7 percent, London by its own stands for 48 percent of this growth). London’s largest sector

of employment is the service sector where 9 out 10 people are working.

The RE-market of London CBD (Central Business District) is divided into three major zones.31 The first

zone is London West End (see the orange color in map 2). The main tenants in office space in this

area are companies active in Management Consultation and Accounting, West End are also a

workplace for more than 60,000 people in retail and restaurants. The second zone is The City of

London (see the red color in map 2) which is Europe's largest central business - and financial district

with a daily working population of over 300,000 people. The third zone is Docklands/Canary Wharf

(see the blue color in map 2) which is the smallest and newest business district in London. Tenants in

this area are mostly operative in banking, law and media.

30

Greater London Authority 31

Jones Lang LaSalle (2009)

0,0%

0,2%

0,4%

0,6%

0,8%

1,0%

1,2%

1,4%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Annual Population Growth

London UK

Source: UK National Statistics

29

Map 2 - London CBD

UK Lease model

UK Leases has been different from other countries with longer and more stable leases, this is

changing more and more in to a Europe standard accept for one characteristic called the upward-

only rent review (UORR) clause. The purpose of this clause is to ensure a stable minimum rental

income for the real estate owners by making it impossible to lower the rent, only increasing it or

letting it be on the same level. The lengths of the leases are changing dramatically in the 90’s with 60

percent of all lettings were on 20- or 25 years leases with rent reviews every fifth year. Today over 60

percent of all new leases signed is less than 5 years.32

32

PPR (2009)

30

Diagram 12 - Prime Rent London

Diagram 13 - Average Rent London

The rents in London CBD are currently a bit lower than in the beginning of 2000. During the last ten

years the rent development has been quiet different between the three submarkets. London City

and Docklands/Canary Wharf has followed each other but at different ground levels. The stabile

tenants and long contracts (see UK lease model page no. 29) have made this area less volatile with

moderate developed rents. The West End had a huge upswing in rents between 2003 and 2008

followed by a major fall with over 50 percent to today’s levels. The London office market has been

among those to show the greatest effects of the downturn worldwide. Active demand has fallen as

many occupiers put their requirements on hold in light of the economic climate.33

33

Jones Lang LaSalle (2009)

0

200

400

600

800

1 000

1 200

1 400

Prime Rent

City (office) Docklands (office) West End (office)

Source: PPRGBP/sqm

200

250

300

350

400

450

500

Average Rent

City (office) Docklands (office) West End (office)

Source: PPRGBP/sqm

31

Diagram 14 - Prime Yield London

The Prime Yield in London during the last 13 years differs between Docklands/Canary Wharf and

City/West End. The Docklands area have seen a steady downward Yield curve from 1997 until 2007,

at the same time the yield curve for City and West End are considerable more volatile, as the where

more affected by the .com bubble. After that crises in the beginning of 2000 the yields where

effected negative for a couple of years, this changed in 2004 when the economic upswing started to

forced the Yields for all three markets down to historical low levels in 2007. In the mark of the

financial crises many investors have been forced to sell their assets which have lead to a large

correction in real estate prices. Yields are forecasted to reach its peak during 2010.

4%

5%

6%

7%

8%

9%

10%

Prime Yield

City (office) Docklands (office) West End (office)

Source: PPR

32

Diagram 15 –Vacancy Rate London

Vacancy rate in London saw a huge rise in the beginning of 2001 until the break point of 2004. A large

amount of office space was built to fill all the new and upcoming .com business, but the bubble burst

and many of the companies went bankrupt. The new office space that was build for .com businesses

where added to the already large amount of vacant space for the property owners and builders.

Since 2004 the vacancy rate has slowly been pushed down by the economical upswing. In the

beginning of 2007 the overall vacancy rate where around 4-5 percent for all submarkets in London

CBD. When Lehman Brother collapses in the fall of 2008 we could see a huge rise in vacancy rate for

all submarkets. Today’s market seems too been stabilized with an overall vacancy rate at 11 percent

for central London (see diagram 15).

0%

5%

10%

15%

20%

Vacancy Rate

City (office) Docklands (office) West End (office)

Source: PPR

33

Diagram 16 - Transaction Volume London

As the financial crises hit the UK in 2007, the real estate transaction market felt its magnitude very

hard. The banks all of a sudden changed their leveraged value of all transactions and some even

choked all possible ways to loan money. In less than a year the transaction volume was back into the

same level as in 2002 (see diagram 16). As the yields reached higher levels and the GBP where

weakened this opened up possibilities to foreign investor and the transaction market are now slowly

recovering.

5

10

15

20

25

30

35

40

45

Transaction Volume - LondonBillionUSD

Source: RCA

34

5.1.5 Macroeconomic Overview – US

Diagram 17 - Macroeconomic Indicators US

The United States is the main reason to today’s global financial crises that has made an impact on the

global market. As a result of the subprime mortgage crises leading to investment bank failures, falling

home prices as so forth, the American economy went into a recession in middle of 2008. As an

answer to these crises the U.S. government established different programs in order to help stabilized

the domestic and global economy. One of their most successful ones is the Troubled Asset Relief

Program (TARP) which has helped to steady the financial market.34 This particular program allows

the Treasury to purchase or insure illiquid, difficult-to-value assets from financial institutions such as

banks, to improve the institutions liquidity, save them from further losses and stabilize their balance

sheets.

34

CIA

-6

-4

-2

0

2

4

6

8

10

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Macroeconomic Indicators - US

US-GDP US-Inflation US Unemployment US-Bank rate

Source: NIER, BLS, Federal Reserve

35

The U.S. budget deficit ended at 1.417 trillion dollars for the budget year 2009, which is more than

three times the budget amount from the preceding year. The budget of 1.417 trillion dollars is

equivalent to 10 percent of the U.S. GDP and it is the largest figure since the end of World War II.

The U.S. Bank rate is the main tool and the key interest rate in U.S. monetary policy. Since December

2008 it’s made a major drop from 5 percent to the current zero level. This magnitude of a fall in the

U.S. interest rate has not been present since the beginning of 2000 and this time around it will

probably be left buoyant at zero for a longer period of time.

According to Bloomberg.com the U.S. economy started growing in the 3rd quarter of 2009 at the

fastest rate in two years. Before the upswing the GDP had been decreasing for four straight quarters

with 3.8 percent which was the worst performance since the 1930’s recession. The U.S. economy is

forecasted to keep on growing, but in a slower pace than of the end of 2009. One problem that the

United States now stands before is how the country will act without the government stimulus

program for consumer spending, which is the backbone in their economy. The credit conditions are

still very tight which makes it hard for both companies to grow and also for the consumers to spend

more money. One main hazard for the GDP development is the rising unemployment as without

work, people need government benefits to survive which in turn will come to hollow out the

governments funds.

Looking back in the mirror the U.S. inflation rate has been stable around 2-3 percent since 1997. This

came to change dramatically in 2008 when de inflation rate became a deflation rate. Figures are

indicating that the U.S. economy will manage to navigate out of this deflation period during 2010.

The future inflation rate is really hard to predict as the public dept is nearly as high as during the

aftermath of World War 2. In an historical point of view this could lead to really high inflation rates as

it “eats up” the dept. This economic outcome would in turn open up for some other economical

problems that might lead to one major down-going economical spiral. Morgan Stanley’s economist

says in his article Economics: The Return of Debtflation? ” it's as if the economy has just gone through

World War 3”.35

Since the recession started the United States has lost more the 6.5 million jobs, only during this year

(2009) almost half of these were lost. The official unemployment rate in June where at 9.5 percent,

but the real numbers (including unemployment, underemployment and discouraged workers) the

figures are as high as 16,5 percent . Almost all sectors are affected by the job losses with only a few

exceptions in the area of education, health service and the government sectors. The outlook for the

unemployment sector is that the unemployment rate will keep growing up to 11 percent during

2010.36

If we look back to the beginning of 21’st century, the U.S. real estate market was more of a solid

market suitable for long-term investments. In the beginning of 2003 this slowly came to change and

the number of transaction started to grow. At its highest in 2007 over 3700 office properties changed

owner which can be compared with 2001 when only about 850 office properties were sold. Today’s

number of properties in the transaction market is on a historical low, with only 290 office properties

have been sold for the first three quarters 2009.

35

Morgan Stanley 36

Jones Lang LaSalle (2009)

36

Diagram 18 - GPR Index US

The listed real estate stocks on the Dow Jones stock exchange had an extreme development, at

almost 900 points between 1990 to January 2007. This came to a halt at the end of 2006 and then

took a major drop during the following year. The market is finally starting to make a slow recovery

and is currently back on the same level as in 2004 (see diagram 18).

0

100

200

300

400

500

600

700

800

900

GPR Index - USSource: GPR

37

5.1.6 Real Estate Market Overview – NYC

New York City is the largest city in the United States with 8.3 million inhabitants and a rather low

population growth at around 0.5 percent. PriceWaterhouse Coopers rates New York as the 2nd largest

city economy in the world, Tokyo in Japan is the only one ranked higher (2008). New York has been

struck hard by the layoffs and according to the New York City Office of Management and Budget

(OMB), the city has lost a total of 14.500 jobs per month since September 2008. Positive signals

during the last months are that numbers of layoffs have declined. But even if this number could be

interpreted positive, the employments forecasts will possible not show any growth until the end of

2010.37

Diagram 19 - Annual Population Growth

Note: The 2000 Census (2000-2008) showed significant improvements in coverage compared to the 1990 Census (1990-

2000). The high amplitude around the year 2000 is a result of these improvements and is not to be misleading as a very

large population increase.

37

Jones Lang LaSalle (2009)

0,0%

1,0%

2,0%

3,0%

4,0%

5,0%

6,0%

7,0%

8,0%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Annual Population Growth

NYC US

Source: the US Bureau of the Census

38

Manhattan CBD is divided into three submarkets major submarkets38 Downtown, Midtown South

and Midtown. Downtown is the central financial district with Wall Street and the New York Stock

exchange (NYSE) and NASDAQ. It is also home to the city hall and the future new World Trade Center

“the Freedom Tower”. Downtown has a real estate stock of 96 million sqf (see the red color in map

3). Midtown is the largest single business district in the U.S. with a real estate stock of 269 million

sqf. The majority of the largest and tallest skyscrapers in NYC are located in midtown, such as the

Rockefeller Centre and the Empire State Building. In Midtown you have large retail establishments

especially around Fifth Avenue and Times Square (see the orange color in map 3). Midtown South is

the smallest district if measured in real estate stock with its 61 million sqf. This area could in turn be

narrowed down to five smaller submarkets, Chelsea, Gramercy Park, Greenwich Village, Hudson

Square Park and SoHo. This district is home to many media and advertisement companies (see the

blue color in map 3).

Map 3 – Manhattan (New York) Submarkets

38

Jones Lang LaSalle (2009)

Manhattan

Midtown: Grand Central, Times

Square, Columbus circle, Plaza

District and Penn Plaza/Garment

Midtown South: Chelsea, Hudson

Square, Gramercy Park, SoHo and

Greenwich Village

Downtown: WTC, Financial District

and City Hall

39

Diagram 20 - Asking Rents New York

The average asking rent on Manhattans has been very depended on the market situation. With a

steady growth in the end of the 90’s, led by the strong demand in office space by the IT pioneers, the

growth ended with the .com bubble in 2000. In 2004 a strong recovery period started and rents

climbed again, this continued until the event of today’s financial crisis. New York’s average asking

rents are now back at the same level as in 2003-2004 but it seems like the steep curve are about to

peter out and a positive trend is now predicted to lead the way to higher rent levels.

Diagram 21 - Cap Rate New York

Office cap rate for New York saw a steady fall from 1997 until 2007. A more lending friendly

environment gave opportunities to a new group of investor which in turn led to lower Cap Rates.

Even if we could see falling rents during 2001 until 2004 there were no larger impact on the Cap

Rates as it kept on falling during this period. In the beginning of 2008 until today we have seen a

huge correction in commercial Real Estate Cap Rates and today’s rates are back at the same levels as

in 2003.

30

35

40

45

50

55

60

Asking RentUSD/sqfSource: PPR

5,0%

5,5%

6,0%

6,5%

7,0%

7,5%

8,0%

8,5%

Cap RateSource: PPR

40

Diagram 22 - Vacancy Rate New York

The vacancy rates in New York can explain the asking average rate as the two more or less follows

each other. We can clearly see that the dot.com crash in 2000 has had a huge impact on the vacancy

rates and also that the latest financial crises is believed to generate even higher levels of vacancy

rates in the coming two years. The downtown market, with Wall Street as its heart, has had a low

vacancy rate compared to the rest of Manhattan. In this area a large number of new spaces are

under construction such as the new World Trade Center Building, this could come to constrain the

recovery of the vacancy rate. The Midtown and south midtown has no major space under

construction so there is no new space of major importance that is going into today’s vacancy stock.39

According to JLL, a real balance between the supply and demand for space will first be possible when

New York recovers and have job growth instead of job losses; this scenario is possible first in 2012.

39

Jones Lang LaSalle (2009)

7%

9%

11%

13%

15%

17%

19%

Vacancy RateSource: PPR

41

Diagram 23 - Transaction Volume New York

The transaction volume during the previous year was extremely low and one of its reasons is due to

the large amount of equity that’s disappeared in the large price correction on the real estate- and the

financial market. The price correction could easiest be described through looking at the market Cap

rate (see diagram 21) development which has increased these last couple of years. A fall from 40

billion USD in 2007 to less the 5 billion 2009 shows the reality in figures (see diagram 23). Transaction

volumes all over the U.S. are currently back at the same level as they were during 2001.

0

5

10

15

20

25

30

35

40

45

Transaction Volume - NYCSource: RCA Billion

USD

42

6. Correlation and Co-Movement Results

6.1 Rents

Comments:

The three results for the Stockholm - London Prime Rent market could be summarized by very high

correlation values. A time lag is present between the two markets indicating that the Prime Rent for

the London office market is one quarter ahead of Stockholm.

[The comprehensive correlation results concerning Prime Rent can be found in appendix B]

43

Comments:

In the London CBD market we could see stronger correlations values between the submarkets during

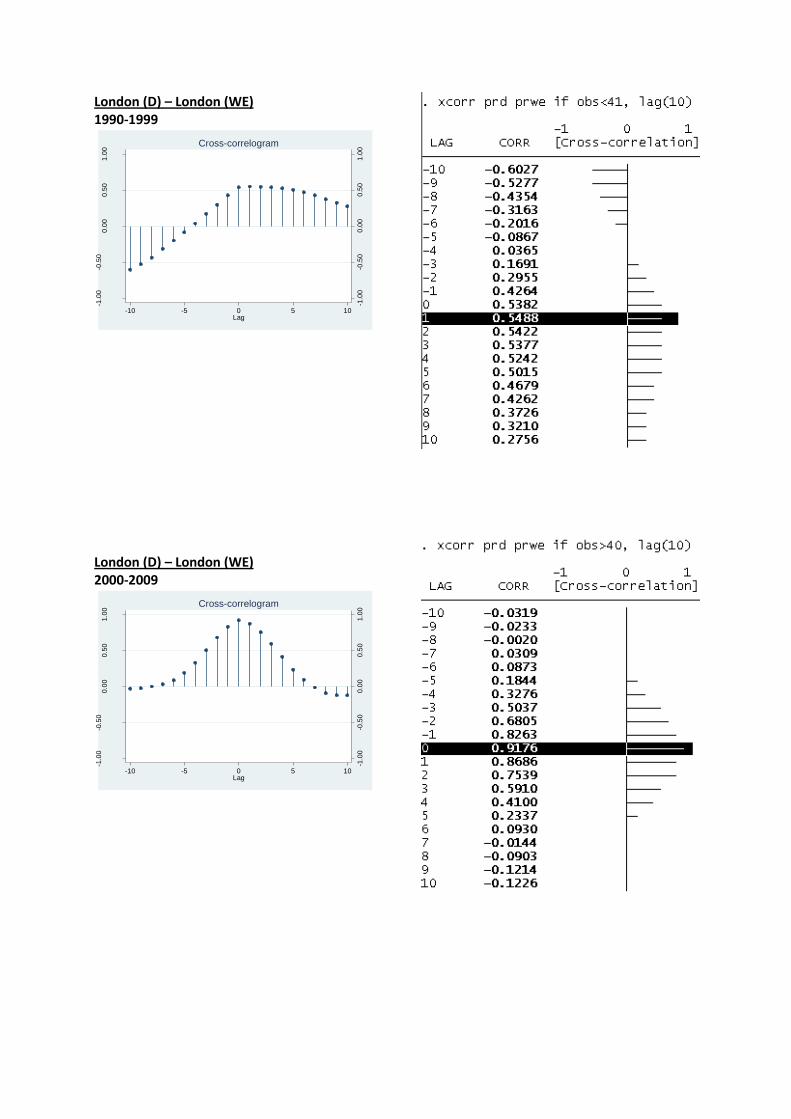

2000-2009 (ΔPR2) then 1990-1999 (ΔPR1). The results are also indicating that an internal time lag is

present in CBD, where Docklands/Canary Wharf and London City are one quarter ahead of West End

during the 90’s. [The comprehensive correlation results concerning Prime Rent can be found in appendix B]

Comments:

The Average Rent between Stockholm and London City is not showing any trace of a possible time lag

between the two cities. The correlation values are on the other hand very strong for the entire time

series. [The comprehensive correlation results concerning Average Rent can be found in appendix B]

44

Comments:

The Average Rent in London CBD has the same outcome in correlation as the Prime Rent when

studying the actual correlation values for these two variables. The AR shows higher values in 2000-

2009 (ΔPR2) then 1990-1999 (ΔPR1). Time Lag is present in both correlation models during the 90’s

(ΔPR1) and is indicating that Docklands/Canary Wharf is one quarter ahead of both London City and

West End. [The comprehensive correlation results concerning Average Rent can be found in appendix B]

45

6.2 Vacancy

Comments:

The Vacancy correlation is showing medium values over the whole time period with a presence of a

three quarter time lag between London City and Stockholm. When we divide the time series into two

parts, the correlation values are increasing and the time lag between the two cities are decreasing

from four quarters in the 90’s (ΔPR1) to one quarter in 00’s (ΔPR2). London City is ahead of

Stockholm during the entire correlation test.

[The comprehensive correlation results concerning Vacancy can be found in appendix B]

Comments:

The correlation between Stockholm and New York shows medium to high correlation values over the

entire time period. A time lag is present over the complete time series with New York ahead of

Stockholm, in the 90’s (ΔPR1) the time lag is four quarters, this decreases into only one quarter in the

last decade (ΔPR2). [The comprehensive correlation results concerning Vacancy can be found in appendix B]

46

Comments:

The correlation during the whole time period shows a strong correlation between the two markets

and that New York is one quarter ahead of London City. When we divide the interval into two series

we are still getting high correlation values but the time lag is no longer present. This result indicates

that Stockholm is currently one quarter behind both New York and London City.

[The comprehensive correlation results concerning Vacancy can be found in appendix B]

47

6.3 Yield / Cap Rate

Comments:

When performing the correlation tests between the Yield variable for Stockholm and London City, we

observe a stronger correlation over time and a decrease in time lag. The present time lag shows that

during the 90’s (ΔPR1), London was ahead with three quarters, and during 00’s (ΔPR2) this lag

decrease down to only one quarter. This time lag development could also be seen in our vacancy

correlation between these two markets.

[The comprehensive correlation results concerning Yields/Cap Rate can be found in appendix B]

Comments:

The Yield/Cap Rate correlation model between Stockholm and New York City is showing strong

correlation values. There were no presence of a possible time lag in the 90’s (ΔPR1) and the last ten

years shows a strong but a bit lower correlation value then during the 90’s (ΔPR1). During the 00’s

(ΔPR2) a time lag becomes visible and indicates that New York is one quarter ahead of Stockholm.

[The comprehensive correlation results concerning Yields/Cap Rate can be found in appendix B]

48

Comments:

Over the entire time period we could see a strong correlation and that London City is four quarters

ahead of New York. Dividing the time period into the 90’s (ΔPR1) and the 00’s (ΔPR2), we notice that

the correlation values are on a significant lower level and a time lag development becomes apparent,

with four quarters in the 90’s (ΔPR1) and one quarter in 00’s (ΔPR2).

[The comprehensive correlation results concerning Yields/Cap Rate can be found in appendix B]

49

6.4 Business Cycle Correlation

Comments:

Summarizing the global business cycle correlation we could see that during an economic upswing our

correlation values are significant stronger then during an economic decline. There is no sign of any

time lag in neither of the correlations. Only one test stands out from the others which is the London

City – New York Yield/Cap Rate correlation. This test is showing a higher correlation value during an

economic decline then in an upswing.

[The comprehensive correlation results concerning Business Cycle Correlation can be found in appendix B]

50

7. Analysis The aim of this thesis is to analyze and find statistical proof that there is a common movement

between selected countries and their specific markets. The study focuses on the Swedish, UK and

U.S. market on both a more comprehensive macro economical level and also on a real estate variable

related economic perspective. The delimitation is set to only focus on the office real estate markets

in Stockholm, London and New York. A domestic analyze were also undertaken for London’s three

submarkets; London City, West End and Docklands/Canary Wharf.

The macroeconomic overview is supposed to give the reader a market update on the economical

situation in the selected country from 1997 until today. The following variables analyzed and

discussed in the macroeconomic overview are as followed; GDP, Inflation rate, Bank rate and the

Unemployment rate. When analyzing the office real estate markets for the different cities we

decided on the following variables as a limitation of these markets; yield/cap rate, rent

(prime/average/asking) and vacancy rate. The complete market interactions between the real estate-

and the financial market are illustrated with the help of the FDW model (4Q) which will facilitate the

reader’s comprehension of this thesis.

7.1 RE Market Correlation for New York - London - Stockholm When analyzing the office rental market between the different cities, a clear pattern of high

correlation values between London and Stockholm indicates strong co-movements between the two

cities. One major reason for the solid results when comparing these two markets was due to the

dependable relationship in the obtained data set for these two cities. The similarity in the real estate

variables such as the same rent classification, the similar yield definition etc. came to smooth the