Embed Size (px)

Citation preview

Macro & FICC Research

Week Ahead Friday 20 July 2018

Key Economic Indicators & Events: 23 – 29 Jul, 2018

Date CET Country Event Period SEB forecast* Consensus* Last*

Mon 23 Reports: Google/Alphabet, Ryanair. Speeches: BOE’s Broadbent (19.00).

08:00 DEN Consumer confidence Jul --- 10.6

16:00 EMU Consumer confidence Jul A -0.7 -0.5

16:00 US Existing home sales | mom change Jun 5.45m | 0.3% 5.43m | -0.4%

Tue 24 Govt. auctions: UK to sell 6y bonds (11.30), US to sell 4w bills (17.30) & 2y notes (19.00). Reports: UBS (06.45), Intrum (07.00), Sanoma (07.30), Outokumpu

(11.00), Verizon (13.30), AT&T. Other: ECB Bank Lending survey (10.00), Hungary Central Bank rate decision (14.00).

02:30 JAP PMI manufacturing (Nikkei) Jul P --- 53.0

08:00 NOR Business tendency survey Q2 7.5 --- 6.3

09:30 GER PMI manufacturing | services | composite (Markit) Jul P 55.5 | 54.4 | 54.8 55.9 | 54.5 | 54.8

10:00 EMU PMI manufacturing | services | composite (Markit) Jul P 54.6 | 55.0 | 54.7 54.9 | 55.2 | 54.9

15:00 US FHFA house price index mom May 0.4 0.1

15:45 US PMI manufacturing | services | composite (Markit) Jul P 55.1 | 56.5 |--- 55.4 | 56.5 | 56.2

Wed 25 Govt. auctions: Germany to sell 5y bonds (11.30), US to sell 2y FRNs, reopening (17.30) & 5y notes (19.00). Reports: Caverion (08.00), Indutrade (13.00), GM

(13.00), Boeing (13.30), Deutsche Bank, Ford (23.30). Other: DOE US Crude Oil Inventories (16.30).

03.30 AUS CPI qoq/yoy | trimmed mean qoq/yoy Q2 0.5/2.2 | 0.5/1.9 0.4/1.9 | 0.5/1.9

09:30 SWE PPI | consumer goods Jun 0.5/7.7 | 0.2/2.0 --- 1.4/6.3 | 1.5/2.1

10:00 GER IFO bus. climate | expect. | current assessment Jul 101.8 | 98.1 | 105.5 101.5 |98.3 | 104.8 101.8 | 98.6 | 105.1

10:00 EMU M3 money supply yoy Jun 3.8 4.0 4.0

16:00 US New home sales |mom change Jun 670k | -2.8 689k | 6.7

Thu 26 Govt. auctions: US to sell 7y notes (19.00). Reports: Nokia (07.00), YIT (07.00), Daimler (07.30), Astra Zeneca (08.00), Attendo (08.00), Metso (08.00), Spotify

(before US markets open), Amazon (22.01). Speeches: ECB’s Draghi holds press conference on policy decision (14.30). Other: Swedish National Financial

Management Authority publishes government budget outcome (09.00).

08:00 DEN Retail sales Jun --- 0.9/3.9

08:00 NOR LFS unemployment rate May 3.7 3.7 3.7

08:00 GER GfK consumer confidence Aug 10.7 10.7

09:00 SWE Consumer confidence | inflation expectations Jul 96.5 | 3.4 --- 96.8 | 3.4

09:00 SWE Manufacturing conf. | service | econ. tendency Jul 115.0 | 105.0 | 108.0 --- 116.1 | 104.0 |108.7

09:30 SWE Unemployment rate | trend | SA Jun 6.8 | --- | 6.0 6.8 | --- | 6.1 6.5 | 6.2 | 6.1

09:30 SWE Household lending yoy Jun 6.6 --- 6.6

13:45 EMU ECB rate decision main |marg. lending | deposit 0.00 | 0.25 | -0.40 0.00 | 0.25 | -0.40 0.00 | 0.25 | -0.40

13.45 EMU ECB asset purchases target EUR 30bn/m EUR 30bn/m EUR 30bn/m

14:30 US Advance goods trade balance Jun USD -67.1bn USD -64.8bn

14:30 US Initial jobless claims | continuing claims 215k | 1730k 207k | 1751k

14:30 US Durable goods orders | ex. transportation Jun P 2.8 | 0.5 -0.4 | 0.0

Fri 27 Reports: Poolia (07.00), Mekonomen (07.30), Veoneer (11.00), Autoliv (12.00), Securitas (13.00), Twitter (13.00). Other: Russia’s Central Bank rate decision

(12.30), Sweden’s Sovereign Debt to be rated by Fitch.

09:30 SWE Trade balance Jun SEK 4.0bn --- SEK -2.6bn

09:30 SWE Retail sales Jun -0.7/2.1 --- 0.2/3.1

14:30 US GDP AR qoq | personal consumption Q2 A 4.1 | 3.9 4.1 | 2.9 2.0 | 0.9

14:30 US GDP price index | core PCE qoq Q2 A 2.4 | 2.2 2.2 | 2.3

16:00 US U. of Mich. Sentiment Jul F 97.1 97.1

* % MoM/YoY unless otherwise stated. Felix Ewert, [email protected]

The Week Ahead

Key Events 23 – 29 Jul, 2018

Tuesday 24, 08.00

NOR: Business Tendency Survey (Q2)

• The quarterly manufacturing sentiment index (Business Tendency Survey) remained roughly unchanged in Q1 and continues to signal that actual manufacturing output should increase in the period ahead.

• Sentiment among Norwegian manufacturers has been depressed in recent years, with the index bottoming out in approximately late 2015, roughly one year after oil prices collapsed. Since then, the indicator has recovered to its long-term average driven by the upswing in both the global industrial cycle and the petroleum sector.

• Oil investments are likely to have bottomed out and the predicted rebound higher in coming years should support the oil-focused capital goods sector. Moreover, the NOK remains weak and external demand is decent, which should push the export-orientated intermediate goods sector higher.

• We forecast an increase in the main index to 7.5 in Q2. Further escalations of the trade conflict between the US and China remains a downside risk to the outlook.

2

Net balance SEB Cons. Prev.

Manufacturing sentiment (S.A.) 7.5 --- 6.3

Wednesday 25, 09.30

SWE: PPI (Jun)

• After a temporary slowdown last year producer prices have accelerated significantly, driven by a combination of weak exchange rate and higher commodity prices (primarily on energy products). The upward pressure is expected to continue in June with a major upturn in electricity prices as the key driver.

• A weak exchange rate has also contributed to an acceleration in prices on consumer goods, although the upturn is more moderate.

• In 2017 PPI on consumer goods increased by 3% y/y on average. The upturn this year is expected to be only 1.5-2%.

• In 2017 higher prices on food commodities contributed to the upturn. Prices on food commodities are expected to decline this year.

• Drought in Sweden is an upside risk to food prices, although the near term impact is likely to be small (prices could even come under downward pressure over the next couple of months).

% mom/yoy SEB Cons. Prev.

Headline 0.5/7.7 --- 1.4/6.3

Consumer goods 0.2/2.0 --- 1.5/2.1

3

Wednesday 25, 10.00

EMU: Money supply M3 (June)

Growth of money supply M3 has fluctuated between 4.3% and 5.3% y/y for three years. In February it dropped below this range, but rose back to 4.0% in May

Aggregate loan dynamics (“Credit to EZ Residents”) continued to rebound in May as the slowdown of growth in “Credit to General Government” came to a halt at its 37-months’ low. At the same time, private sector loan growth accelerated to 3.0% in May.

Private sector loan growth so far is maintaining its ~1pp lag vs. M3 growth. With ongoing progress in banks’ NPL reduction this gap should gradually narrow in coming quarters when we expect M3 growth to settle in a 3.5-4% range.

% yoy SEB Cons. Prev.

M3, SA 3.8 4.0 4.0

Credit to EZ residents 2.9 --- 3.2

Loans to private sector 2.8 --- 3.0

4

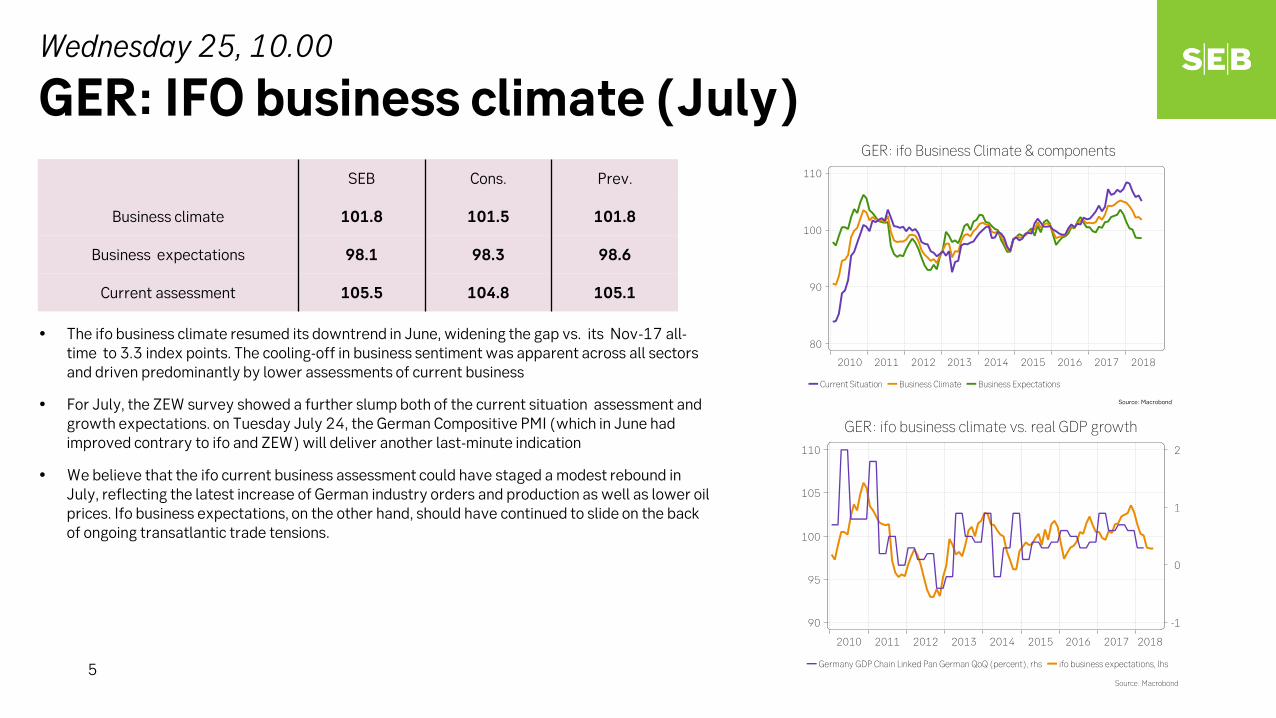

Wednesday 25, 10.00

GER: IFO business climate (July)

The ifo business climate resumed its downtrend in June, widening the gap vs. its Nov-17 all-time to 3.3 index points. The cooling-off in business sentiment was apparent across all sectors and driven predominantly by lower assessments of current business

For July, the ZEW survey showed a further slump both of the current situation assessment and growth expectations. on Tuesday July 24, the German Compositive PMI (which in June had improved contrary to ifo and ZEW) will deliver another last-minute indication

We believe that the ifo current business assessment could have staged a modest rebound in July, reflecting the latest increase of German industry orders and production as well as lower oil prices. Ifo business expectations, on the other hand, should have continued to slide on the back of ongoing transatlantic trade tensions.

SEB Cons. Prev.

Business climate 101.8 101.5 101.8

Business expectations 98.1 98.3 98.6

Current assessment 105.5 104.8 105.1

5

Thursday 26, 08.00

NOR: LFS unemployment (May)

The Labour Force (LFS) unemployment rate continued on its downward trend in March-May (officially reported as April), declining 0.2ppt to 3.7%.

In recent months, both growth in employment and the labour force has picked up, and the acceleration in employment motivated the central bank to revise its employment forecasts higher in the June MPR.

The strong developments in the labour market support our forecast of a first hike from Norges Bank in September, which also is the central bank’s forecast.

According to Norges Bank, the trajectory for the key rate after Sep-18 depends on the effect on indebted households. Hence, labour market data will be important ahead, as strong employment is expected to underpin consumption growth.

Fresh forecasts from Norges Bank’s June MPR indicate an average unemployment rate of 3.7% in 2018, which is in line with our forecast. The bank projects a gradual decline for the unemployment rate to 3.2% at the end of the forecast horizon (2021).

6

% of labour force SEB Cons. Prev.

Unemployment rate 3.7 3.7 3.7

Thursday 26, 09.00

SWE: Consumer confidence (Jul)

• After increasing at the end of last year consumer confidence has gradually deteriorated during 2018. In May confidence declined below the historical average for the first time since 2016 and the decline continued in June.

• The outlook for confidence going forward is mixed. • The labour market is strong but there are signs of a slowdown in job growth from the

current firm pace. • Upward pressure on consumer prices from energy and earlier SEK depreciation is denting

household incomes. • Home prices appears to be stabilizing but as shown by the graph over confidence and

home price expectations (SEB housing price indicator), home price trends do not appear to have been of major importance for confidence.

• We expect the confidence to continue to edge lower in July.

SEB Cons. Prev.

CCI 96.5 --- 96.8

Inflation expectations 3.4 --- 3.4

7

Thursday 26, 09.00

SWE: Business confidence (Jul)

• Outlook for the manufacturing sector is mixed with a marked decline in PMI since the end of last year, but with manufacturing sentiment remaining at high levels. PMI often leads NEIR sentiment and we expect the manufacturing confidence indicator to decline in July.

• The outlook for the domestic sectors is mixed with sentiment in services and retail sectors recovering in June, but with the trend in both sectors having stabilized slightly above their historical averages.

• Sentiment in construction has declined since the middle of last year, but with some signs of stabilization over the last couple of months. Sentiment is still above the historical average, but weaker housing starts imply that sentiment will come under renewed downward pressure in the second half of this year.

• The July survey is the quarterly one with special questions regarding capacity utilization and labour shortage. The share of companies reporting labour shortage has stabilized at cyclical peak levels over the last 6 months. Signs of slightly weaker employment growth suggest that labour shortage will ease slightly in the second half of this year.

• The quarterly NIER survey is the most important input for the Riksbank’s capacity utilization indicator. This indicator is also showing signs of turning lower from a high level.

SEB Cons. Prev.

Manufacturing 115.0 --- 116.1

Service sector 105.0 --- 104.4

Tendency indicator 108.0 --- 108.7

8

Thursday 26, 09.30

SWE: Household lending (Jun)

• After being largely stable since the middle of last year household lending has slowed over the last 3 months.

• Declining home prices imply that the growth rate will slow, but on the contrary high completions of new homes suggest that the slowdown will be more gradual than indicated by the last 3 months.

• Higher amortizations are also expected to contribute to a slowdown in lending going forward. • Household lending has to slow to 4.5-5% y/y in order to stabilize household debt to income-

ratio.

% yoy SEB Cons. Prev.

Household lending 6.6 --- 6.6

Non financial corporations --- --- 6.9

9

Thursday 26, 09.30

SWE: Unemployment (Jun)

• Unemployment continued to decline in May driven by strong employment growth. • Despite a fall in the forward looking indicator we predict employment growth to be sufficiently

strong to continue to push unemployment lower. • We expect unemployment rate to drop below 6% in the second half of this year. • The Riksbank predicts that the lower unemployment rate in May is temporary and expects a

gradual upward trend to start in June and continue over the next 3 years.

% SEB Cons. Prev.

Seas. adj. 6.0 6.1 6.1

Actual 6.8 6.8 6.5

Empl. 1000s/% yoy 85/1.6 --- 119/2.4

10

Thursday 26, 13.45/14.30

EMU: ECB Governing Council Meeting

11

Rate announcement at 13.45:

• policy rates unchanged • QE parameters unchanged • forward guidance unchanged

Q&A session at 14.30:

• QE unchanged pace & composition until Q4 • Inflation ECB strongly confident regarding inflation convergence towards target, will look

through s/t fluctuations, closely watch fx developments. • Growth EZ expansion is broad-based and solid; strong growth momentum and gradual

absorption of labour market slack to continue in H2-18. Downside risks relate predominantly to global factors (protectionism) and geopolitical tensions.

• ECB outlook repeat of “confidence, patience & persistence” mantra; call for swift structural reform, completion of EMU. Expected intra-day market impact neutral for EUR rates and the euro

• Forecast risk: None; a policy change is most unlikely after the June decision

ECB staff projections

SEB Cons. Prev.

Marginal Lending Rate (%) 0.25 0.25 0.25

Main Refinancing Rate (%) 0.00 0.00 0.00

Deposit Facility Rate (%) -0.40 -0.40 -0.40

APP target (€ bn/month) 30 30 30

% yoy Year June March

Inflation

2018 1.7 1.4

2019 1.7 1.4

2020 1.7 1.7

GDP

2018 2.1 2.4

2019 1.9 1.9

2020 1.7 1.7

Friday 27, 09.30

SWE: Trade balance (Jun)

• The trade balance has stabilised over the last 12 months after trending lower since 2006. • Strong imports is the main driver of the smaller trade surplus, while exports have been rising at

a moderate pace. • We predict that exports will become a more important driver of growth while at the same time

domestic demand is seen to slow. This suggests that the trade balance will continue to recover going forward.

• The trade surplus according to national accounts, which also includes services and merchanting is still showing a significant surplus (approximately 4% of GDP).

• June is a seasonally strong month and the seasonality is perhaps the most important reason for predicting a surplus this month.

SEK bn SEB Cons. Prev.

Actual 4.0 --- -2.6

12

Friday 27, 09.30

SWE: Retail sales (Jun)

Retail sales have been strong over the past 3 months after starting the year on a weaker footing.

Sentiment among retailers has recovered slightly over the last quarter but remains at moderate levels and do not support the recent upturn in sales.

Firm employment growth should be supportive for consumption going forward. Falling real income due to high energy prices and a weak krona, however, implies that we should not expect any strong recovery for consumption.

Weak sentiment among households imply that household consumption will continue to struggle in the second half of this year.

Strong retail sales of mostly food has been an important driver behind the strong retail sales outcomes during the spring. We do not see any particular underlying reason for this upturn, which suggests it will rebound lower.

In 2107, a pattern emerged where initially strong retail sales were revised significantly lower after 2-3 months. As the reason was uncertain, there is a risk that the surge in recent months will be revised lower as well.

% mom/yoy SEB Cons. Prev.

Retail sales -0.7/2.1 --- 0.2/3.1

13

Friday 27, 14.30

US: GDP (Q2, advanced)

• Q1 GDP growth disappointed by decelerating to 2.0% annualised. The main culprit was consumption growth which slumped to only 0.9% annualised. Investment was the main contributor to Q1 activity, contributing 1.22 percentage points to growth.

• However, GDP growth has accelerated in Q2 as personal consumption has recovered. The strong labour market, tax cuts and household net wealth at record levels support consumption.

• Net exports detracted slightly from growth in Q1 but are set for a positive contribution in Q2. Exports got a temporary boost due to US exporters trying to beat imposition of Chinese import tariffs on soybeans and corn. The positive effect will reverse in Q3.

• Atlanta Fed’s growth tracker suggests that growth was close to 3.9% in Q2, New York Fed’s tracker indicates 2.8% (July 13).

• We forecast 4.1% real GDP growth and 3.9% consumer spending growth in Q2. • The Fed has confirmed that the economy is doing well (“already very strong” according to the

June meeting minutes). However, the central bank has communicated that escalating trade tensions are a downside risk.

• We expect activity in the economy to accelerate in Q2 and forecast GDP to grow 2.8% in 2018.

% SEB Cons. Prev.

GDP annualized qoq 4.1 4.1 2.0

Personal consumption 3.9 2.9 0.9

14

Category Contribution to per cent change in Q1 GDP

Personal consumption 0.60

Investment 1.22

Net exports -0.04

Government consumption and

investment 0.22

Q1 GDP 2.00

European Sovereign Rating Reviews

Source: Bloomberg

15

Upcoming rating reviews Friday, 20 July 2018 Agency Rating / Outlook last change Change?Austria Fitch AA+ / Stable 02/13/2015 no

Czech Republic S&P AA- / Stable 08/24/2011 no

Estonia Moody's A1 / Stable 03/31/2010 outlook to Positive?

Finland DBRS AA H / Stable 09/09/2016 no

France Fitch AA / Stable 12/12/2014 no

Greece S&P B / Positive 01/19/2018 no

Friday, 27 July 2018 Agency Rating / Outlook last change Change?Cyprus Moody's Ba3 / Positive 07/28/2017 rating upgrade 1 notch?

EFSF DBRS AAA / Stable 07/27/2012 no

ESM DBRS AAA / Stable 04/04/2014 no

Netherlands Moody's Aaa / Stable 03/07/2014 no

Slovakia Fitch A+ / Stable 07/08/2008 no

Slovakia S&P A+ / Stable 07/31/2015 no

Sweden Fitch Aaa / Stable 12/18/2007 no