Embed Size (px)

Citation preview

MACRO ECONOMIC INDICATORS AND FMCG

SALES-A CASE STUDY

Submitted by:Ayan Adhikari

University of Calcutta

Department of Statistics

We are given data on FMCG Sales, which is a function of mainly 4 macro economic indicators ,

namely:

• GDP(Gross Domestic Product)

• CPI(Consumer Price Index)

• PPI(Producer Prices Index)

• IPI(Industrial Production Index) Along with them the FMCG Sales is also affected by Crude Oil Prices and Sugar Prices and the

distribution of all the above mentioned factors.

In this Case Study our objective is two fold:

1. To determine how FMCG sales gets impacted by the movement of all the above

mentioned factors

2. To predict the sales for next 3 quarters. So to achieve our objectives we carry out a statistical analysis on the data we are provided with.

A.Description of the data

The data that is provided, gives us information on FMCG Sales,which is the response

variable. The FMCG Sales however is a two dimensional vector ,consisting of the components

Value Offtake (in 00,000 Rs) and the Number of Stores .The data on FMCG Sales is given for

each month , spanning from January 2012 to June 2014. Hence,necessarily it is a Time Series

Data.

The data on the Macroeconomic Indicators,Crude Oil Prices and Sugar Prices are also

given on a monthly basis,although the data on all the covariates are not supplied for the span

January 2012 to June 2014,as in the case of the response.

The data on GDP is provided for each of the 10 quarters(There are 10 quarters from

January 2012 to June 2014).

The data on CPI(prices paid by consumers for a basket of goods and services)is given for

the span August 2013 to July 2014.Similarly the data provided on PPI(measuring the average

change in price of goods and services sold by manufacturers) and IPI(measuring changes in

output for the manufacturing,mining and utilities)are for the same time span as CPI.

So,the consolidated data may look somewhat like as below:

Month Value Offtake Number of Stores Crude Oil Sugar Pric GDP CPI PPI IPI

JAN13 1,778,946 8,756,249 5475.7 8

FEB12 1,460,671 8,373,696 5540.8 8

MAR12 1,674,358 8,370,395 5927.6 8

APR12 1,569,027 8,365,588 5892.6 6.7

MAY12 1,673,478 8,358,634 5659.7 24.3 6.7

JUN12 1,618,560 8,364,721 5083.6 24.9 6.7

JUL12 1,687,376 8,368,860 5372.2 27.9 6.1

AUG12 1,729,846 8,380,458 5849.3 25.2 6.1

SEP12 1,702,726 8,387,885 5800.7 24.3 6.1

OCT12 1,729,722 8,382,093 5475.4 23.8 5.3

NOV12 1,722,802 8,378,245 5536 23.3 5.3

DEC12 1,805,808 8,385,347 5525.5 23.2 5.3

JAN13 1,778,946 8,756,249 5705.1 22.6 5.5

FEB13 1,647,682 8,758,686 5786 21.6 5.5

MAR13 1,870,267 8,760,601 5580.7 22 5.5

APR13 1,767,852 8,766,108 5375 21.2 4.4

MAY13 1,888,606 8,765,700 5467.6 21.2 4.4

JUN13 1,810,826 8,765,753 5817.7 21.8 4.4

JUL13 1,873,960 8,765,790 6289.4 22.6 4.8

AUG13 1,907,894 8,766,110 6830.4 24.1 4.8 134.6 177.5 2.63

SEP13 1,845,721 8,770,102 6928.1 24.8 4.8 136.2 179.7 0.43

OCT13 1,909,556 8,770,151 6499.6 25.6 4.7 137.6 180.3 2.76

B.Completion of the Data Set

As it is seen from the snapshot,we mainly face 3 constraints while modeling the

impact of the movement of all the factors on FMCG Sales.They are:

A. The data contains a number of missing values in the columns of the

Covariates:Sugar Prices,IPI,CPI and PPI.

B. Moreover,the data on GDP was given on a quarterly basis.

C. However the main problem in the data was that, we were provided with the data

on FMCG Sales of January 2013 in the place of January 2012.So we have actually

treated the response data corresponding to January 2012 missing as well.

i. To overcome these problems we first consider the Response variable-FMCG Sales.

As a single value is missing among all the 30 observed data points,we replace the

values(both of Value Offtake and Number of Shops) corresponding to January 2012 by the

mean of the remaining observed data points.

Thus we obtain a dataset where we have responses corresponding to all the

observed thirty months.

Again,as the response FMCG Sales contains of two components Value Offtake and

Number of Shops,we have to actually analyse how both of them are affected by the movement

of the given Macroeconomic Factors.Or else,we can actually obtain a new response variable

Value Offtake per Shop(00,000Rs) = value offtake(00,000)/ no. of shops Here in this case study analysis,the single response variable,Value Offtake per Shop has been

considered.Thus we address one of the three constraints.

ii. Next we try to obtain the GDP values on monthly basis

For addressing this problem we first plot the GDP data given on a quarterly basis.

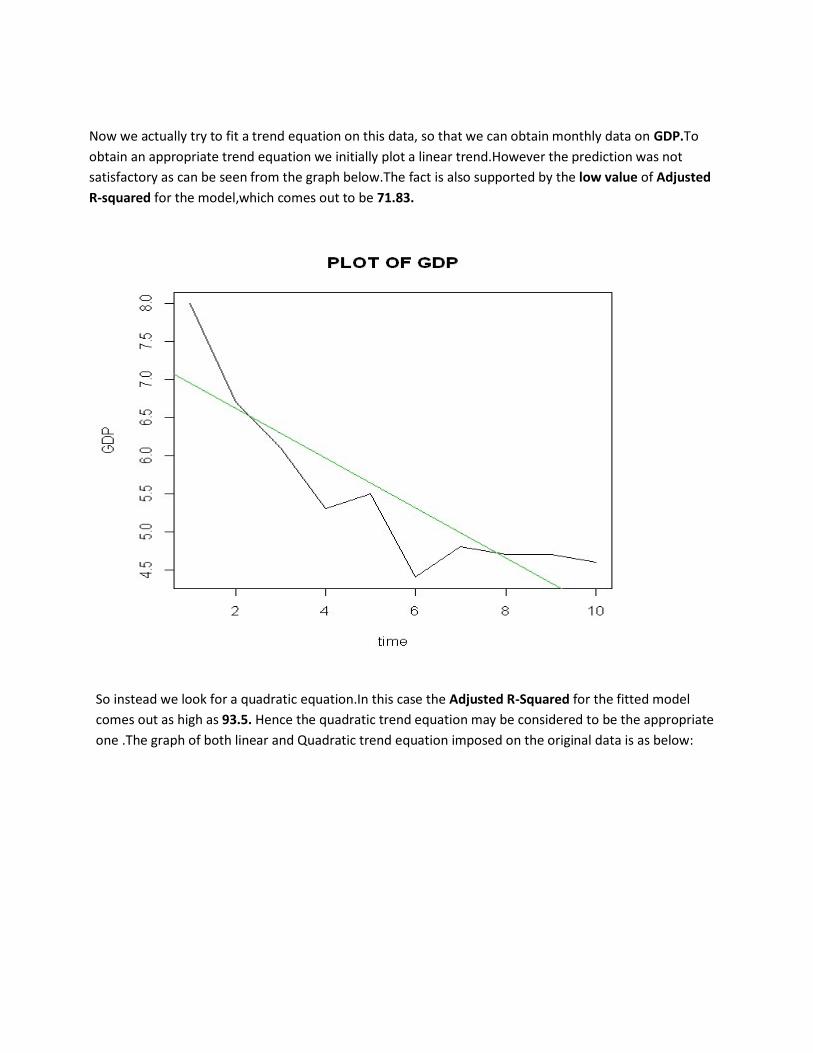

Now we actually try to fit a trend equation on this data, so that we can obtain monthly data on GDP.To

obtain an appropriate trend equation we initially plot a linear trend.However the prediction was not

satisfactory as can be seen from the graph below.The fact is also supported by the low value of Adjusted

R-squared for the model,which comes out to be 71.83.

So instead we look for a quadratic equation.In this case the Adjusted R-Squared for the fitted model

comes out as high as 93.5. Hence the quadratic trend equation may be considered to be the appropriate

one .The graph of both linear and Quadratic trend equation imposed on the original data is as below:

So we obtain a quarterly trend equation for GDP.Then we carry out the necessary

transformations and adjustments to obtain the monthly trend equation for GDP.

Quarterly Trend Equation: Yt= 8.76167-1.06598*t+0.06705*t2……….(1)

Unit:1 quarter Origin:1st quarter of 2012 Monthly Trend Equation: Yt=8.76167-((1.06598/3)*(t-(1/3)))+((0.06705/9)*((t-(1/3))2)…..(2)

Unit:1 month Origin: January 2012 In monthly trend Equation all the coefficients of time are divided by the appropriate

constants(divided by 3 as 1 quarter contains 3 months) and then properly centred.

Thus we obtain the GDP values for all the months spanning from January 2012 to June

2014from equation (2).

iii. Now,we impute the missing values in Sugar Prices,IPI,CPI,PPI

For this purpose we actually make use of the mi package(multiple imputation) in R.

Here we actually generate multiple imputations for incomplete data using iterative regression

imputation. If the variables with missingness are a matrix Y with columns Y(1), . . . , Y(K) and the

fully observed predictors are X, this entails first imputing all the missing Y values using some

crude approach (for example, choosing imputed values for each variable by randomly selecting

from the observed outcomes of that variable); and then imputing Y(1) given Y(2), . . . , Y(K) and

X; imputing Y(2) given Y(1), Y(3), . . . , Y(K) and X (using the newly imputed values for Y(1)), and

so forth, randomly imputing each variable and looping through until approximate convergence.

As we wish to impute the values of Sugar Prices,IPI,CPI and PPI,we treat them

as the Y values with missingness as mentioned in the above paragraph.To circumnavigate any

problem of Multicollinearity that may arise in future,we ignore the Oil Prices and GDP

values(both of which by now are fully observed) but take the Value Offtake per Shop only as

the fully observed predictor X,based on which the imputation is carried out.

Thus we outdo all the three initial problems that were faced at the beginning and obtain a fully

completed dataset;a snapshot of which looks as below:

Y Time Oil Sugar GDP IPI CPI PPI

0.208611 1 5475.7 25.35579 8.528097 -1.67502 140.9283 185.0866

0.174436 2 5540.8 25.25792 8.190153 1.228825 137.7208 180.3033

0.200033 3 5927.6 25.42624 7.86711 1.002539 137.9063 177.2557

0.187557 4 5892.6 25.56207 7.558967 -4.21778 139.2061 180.1868

0.20021 5 5659.7 24.3 7.265723 -0.18116 141.0971 179.4309

0.193498 6 5083.6 24.9 6.98738 -4.02633 140.6432 182.5184

0.201626 7 5372.2 27.9 6.723937 -2.08461 139.7622 180.7297

0.206414 8 5849.3 25.2 6.475393 -4.75091 138.9687 179.5387

0.202998 9 5800.7 24.3 6.24175 0.732328 132.476 182.077

0.206359 10 5475.4 23.8 6.023007 0.424546 140.9178 183.2025

0.205628 11 5536 23.3 5.819163 0.981606 137.6504 179.1849

0.215353 12 5525.5 23.2 5.63022 -4.34836 141.4364 181.2235

0.203163 13 5705.1 22.6 5.456177 -2.59397 132.5132 180.946

0.18812 14 5786 21.6 5.297033 0.257167 138.1901 179.6825

0.213486 15 5580.7 22 5.15279 1.938265 137.8538 183.4112

0.201669 16 5375 21.2 5.023447 0.219639 137.7525 182.6066

0.215454 17 5467.6 21.2 4.909003 0.529774 138.2674 181.5117

C.Analysis of the Completed dataset and fitting an

Appropriate Model Once we obtain the fully completed dataset we can actually analyse the data and study

the impact of the movement of the Macroeconomic Indicators on the FMCG Sales. We firstly plot all the Time Series data i.e, the response variables along with the six covariates.

From the above graph and the graph attached below it is evident that all the six covariates and

the response variable shows movements along time,though may not be in the same

direction.The graph of the response variable clearly shows an increasing trend with seasonality

present(presence of seasonality is natural as it is a monthly data).

Similarly the plot of OIL Prices,CPI,IPI and PPI also shows an increasing trend in the last few

quarters with certain fluctuations p resent.Also the plot of GDP clearly states that it is

decreasing over time,that is, it might affect the response negatively.The plot of Sugar Prices

also indicates of a decreasing trend with fluctuations in between.Hence Sugar Prices may also

affect the FMCG Sales negatively.

However, nothing can be said with certainty about the impact of the movement of each covariate on

FMCG Sales without carrying out a proper statistical analysis of the data. Hence to come to a concrete

conclusion we must carry out a regression analysis.

Now we check using qqplot whether the response variable can be assumed to

follow a Normal distribution or not.Here we actually compare the sample quantiles with the

theoretical quantiles.Looking at the graph below we conclude that Value Offtake per Shop

maybe well assumed to follow a Normal Distribution as all the points lie on the qqline with a

few exceptions.

Similarly we check the normality assumption for all the six Covariates.

Coefficients Estimate Standard Error p-value Decision taken

Intercept 0.6681 0.179 0.00123 Reject H0

GDP 0.1131 0.03588 0.00482 Reject H0

Value Offtake per

Shop(preeding time

point)

-0.4719 0.1387 0.00268 Reject H0

GDP(preceding time

point)

-0.1165 0.03338 0.00219 Reject H0

Sugarprices(Preceding

time point)

0.003514 0.0009913 0.00192 Reject H0

PPI -0.002009 0.0009601 0.4867 Accept H0

IPI -0.001435 .000766 0.07503 Accept H0

Oil Prices(preceding

time poiny)

-0.000007861 .000004268 0.07962 Accept H0

So it may be assumed that all the covariates as well follow approximately a Normal Distribution

as is evident from the above Q-Q Plots.

As the response follows a Normal Distribution,we may carry out a Generalized Linear

Model with the Identity Link function. However as all the data under consideration are Time

Series data we consider the Time Series regression model and use the dyn package(dynamic

regression) to carry outour necessary analysis.

"dyn" enables regression functions that were not written to handle time series to

handle them. Both the dependent and independent variables may be time series and they may

have different time indexes (in which case they are automatically aligned).

We go on adding one variable at a time to obtain the most parsimonious model,that might

explain the impact of the movement of the covariates on the response.

But we do face a problem in our pursuit to seek for the best predictive equation.The

best model that we obtain in terms of minimum AIC and residual deviance does not include all

the factors,but is a function of GDP,Response of the preceding time point,GDP of the

preceding time point , Sugar Prices of the preceding time point,PPI,IPI and Oil Prices of the

preceding time point.

The best model obtained by incorporating all the covariates do also admit a low AIC but it

is greater than the above mentioned model.

A statistical table of the following two models is presented here:

I. The best model:Model I

Here the null hypothesis states that H0:the particular coefficient is 0.So we conclude from the

above table that all the covariates except PPI,IPI and Oil Prices at the preceding time point are

significant,at 5% level of significance.The measures of Goodness of fit is provided by AIC and

residual deviance.They comes out to be as

AIC:-203.22 Residual Deviance: 0.00082608 on 21 df Hence the model comes out to be :

Yt=0.6681+0.1131*GDPt-0.4719*Yt-1-0.1165*GDPt-1+0.003514*Sugart-1-0.002009*PPIt-

0.001435*IPIt-0.000007861*Oilt-1

II. The best model including all the covariates:Model II

Coefficients Estimate Standard Error p-Value Decision

Intercept 0.6267 0.2048 0.00617 Reject H0

GDP .1075 .03868 0.01158 Reject H0

Value Offtake per

Shop(preceding

time point)

-0.4833 .1437 0.00309 Reject H0

GDP(preceding

time point)

-.1112 .03606 0.00587 Reject H0

CPI 0.0004369 0.0009795 0.66037 AcceptH0

PPI -.002113 .001006 0.04859 Reject H0

Sugar

Prices(Preceding

time point)

.003419 0.001033 0.00349 Reject H0

Oil Prices(Preceding

time point)

-.000006989 .00000477 0.15843 Accept H0

IPI -0.001431 .0007811 0.08193 AcceptH0

Here the null hypothesis states that H0:the particular coefficient is 0.So we conclude from the

above table that all the covariates except CPI,Oil Prices at the preceding time point and IPI are

significant,at 5% level of significance.The measures of Goodness of fit is provided by AIC and

residual deviance.They comes out to be as

AIC:-201.51 Residual Deviance: 0.0008179on 20 df Hence the model comes out to be :

Yt=0.6267+.1075*GDPt-0.4833*Yt-1-.1112*GDPt-1+0.0004369*CPIt- .002113*PPIt

+.003419*Sugar t-1-.000006989*Oil t-1-0.001431*IPIt

D.The Conclusion

The graph of the actual and the fitted values are shown below:

So from the graph we can conclude that the fitted model do serve as a good prediction formula

at the beginning and end of the time span,though may fail to do so accurately in the

middle.However both the fitted models can actually predict the rises and declines in the FMCG

Sales over time.As there is not much deviation between the best model and the best model

obtained by using all the Covariate values,we will consider model II as the desired model as it

accurately gives the impact of movement of all the covariates on the FMCG Sales.

The model which is given as :

Yt=0.6267+.1075*GDPt-0.4833*Yt-1-.1112*GDPt-1+0.0004369*CPIt- .002113*PPIt

+.003419*Sugar t-1-.000006989*Oil t-1-0.001431*IPIt

may be interpreted as below.

We see from the above model that the Value Offtake per shop is positively correlated

with GDP,CPI and Sugar Price(of the preceding year).The interpretation may be as follows:

The FMCG Sales increases as the GDP for that particular time point increases, i.e., as

there is growth in the economy,the Sales increases.Also as CPI increases,or in other words the

amount of money paid by a consumer for a basket of goods and services increases,so does

FMCG Sales ,as is very evident from the increased spending power of the consumers.The Sugar

price of the preceding time point also do positively affect the FMCG Sales.

On the other hand the response is negatively affected by the Value Offtake per shop of

the preceding time point,GDP of the preceding time point,PPI,Oil Price of the preceding time

point and IPI.

That both the Value Offtake per shop of the preceding time point and GDP of the

preceding time point affect the response negatively,well establishes the fact that the response

at a particular time point is indeed positively affected by the GDP at that time point.However

if the Sales is one month is low it may result in increased Sale during the successive month.On

the other hand as PPI increases, i,e., the producer’s price increases the demand decreases and

hence it results in decreased Sales.

The value of the fitted and actual response variables are also provided herewith:

ACTUAL DATA FITTED DATA

0.174436 0.1761853

0.200033 0.1977128

0.187557 0.1846241

0.20021 0.2062007

0.193498 0.1911048

0.201626 0.2035335

0.206414 0.2062317

0.202998 0.1995788

0.206359 0.2055571

0.205628 0.2065550

0.215353 0.2064828

0.203163 0.2030951

0.18812 0.2058080

0.213486 0.2115194

0.201669 0.2028833

0.215454 0.2129214

0.20658 0.2055969

0.213781 0.2162724

0.217644 0.2117013

0.210456 0.2122387

0.217734 0.2152377

0.218895 0.2230590

0.230446 0.2253755

0.221738 0.2125913

0.202495 0.2121646

0.232641 0.2306643

0.212545 0.2199740

0.22655 0.2248898

0.217588 0.2153383

Thus we have achieved our 1st objective of assessing the impact of the movement of the

Macroeconomic Indicators on the FMCG Sales .

Now we move onto our second objective:Predict the sales for the next 3 quarters.

To achieve this objective,we actually make use of the model that we have proposed in

the earlier section.

Yt=0.6267+.1075*GDPt-0.4833*Yt-1-.1112*GDPt-1+0.0004369*CPIt- .002113*PPIt

+.003419*Sugar t-1-.000006989*Oil t-1-0.001431*IPIt

But here the covariate values are unknown as well.But as all the variables are necessarily Time

Series data,we may make use of the different Time Series tools to actually predict their future

values,and then replace them in the model to obtain the predicted sales for the upcoming 3

quarters.

In R we use the tseries package to carry out the DICKEY FULLER TEST to find out the

appropriate value of the differencing operator d or the number of times the given data set has

to be differenced to obtain a stationary Time Series.Then we use the forecast package to find

out the appropriate ARIMA model that needs to be fitted to the data.Once we obtain the

appropriate model,the value of the upcoming 9 months can be predicted.

However incase of CPI,PPI and IPI we were already provided with the data of July 2014,so we

need to predict only the upcoming 8 values.

As in case of GDP although we make use of the monthly trend equation to obtain the future

values.

The appropriate models:

• Oil Prices: Here we find the appropriate value of d=2 and an ARIMA(0,2,0) model is most suitable for the

given data.

The AIC of the fitted model is 404.44.The completed dataset is: Jan Feb Mar Apr May Jun Jul Aug Sep Oct N ov

5475.7 5540.8 5927.6 5892.6 5659.7 5083.6 5372.2 5849.3 5800.7 5475.4 5536.0

5705.1 5786.0 5580.7 5375.0 5467.6 5817.7 6289.4 6830.4 6928.1 6499.6 6432.7

6683.9 6777.2 6548.5 6333.8 6274.3 6471.1 6667.9 6864.7 7061.5 7258.3 7455.1

7848.7 8045.5 8242.3

Dec

5525.5

6534.9

7651.9

• Sugar Prices

Here we find the appropriate value of d=2 and an ARIMA(2,2,0) model is most suitable for the

given data.

The model is given as

Xt+0.5624*Xt-1+0.5533*Xt-2=εt

The AIC of the fitted model is 104.42.The completed dataset is:

Jan Feb Mar Apr May Jun Jul Aug

25.04605

23.58084

24.21894

26.11498

24.30000

24.90000

27.90000

25.20000

22.60000 21.60000 22.00000 21.20000 21.20000 21.80000 22.60000 24.10000

21.40000

23.20000

24.10000

24.30000

23.90000

23.90000

24.00702

23.83255

23.59418

23.53607

23.46656

Sep

Oct

Nov

Dec

24.30000 23.80000 23.30000 23.20000

24.80000

25.60000

24.50000

22.50000

23.75716

•

23.78180

IPI

23.69536

23.61605

Here we find the appropriate value of d=2 and an ARIMA(0,2,2) model is most suitable for the

given data.

The model is given as

Xt=εt +1.5547*ε t-1- 0.6115* εt-2

The AIC of the fitted model is 142.94.The completed dataset is:

Jan Feb Mar Apr May Jun Jul

1.1746550 7.3972661 3.7072634 2.8963077 4.4504296 4.0884881 3.9991053

2.4120624 0.5958998 0.6001720 0.2831000 -1.0973953 3.5172673 -0.6028610

-0.1600000 0.8000000 -1.8000000 -0.5000000 3.4000000 4.7000000 3.4000000

5.0022741 5.3438301 5.6853862 6.0269422

Aug Sep Oct Nov Dec

5.8232911 2.3769340 3.9591879 3.4029745 -0.9656482

2.6300000 0.4300000 2.7600000 -1.1600000 -1.3200000

3.4000000 3.6360501 3.9776061 4.3191621 4.6607181

• CPI

Here we find the appropriate value of d=2 and an ARIMA(3,2,1) model is most suitable for the

given data.

The model is given as

Xt+0.2641*Xt-1+0.4580*Xt-2+0.52*Xt-3=εt +0.7508*ε t-1

The AIC of the fitted model is 120.2.The completed dataset is:

Jan Feb Mar Apr May Jun Jul Aug

138.2053 138.7676 136.1041 136.7705 138.4375 136.9388 136.7875 137.8282

139.5952 137.3964 136.6392 136.3946 140.7071 140.5282 138.1013 134.6000

137.4000 137.3000 138.1000 139.1000 139.9000 141.2000 143.7000 143.7000

147.1355 147.3322 148.1754 149.3200

Sep Oct Nov Dec

140.5583 137.9624 137.3509 138.4425

136.2000 137.6000 139.4000 138.0000

143.5506 143.9616 145.5932 146.7234

• PPI

Here we find the appropriate value of d=1 and a SARIMA model is most suitable for the

given data.

The AIC of the fitted model is 119.16.The completed dataset is:

Jan Feb Mar Apr May Jun Jul Au g 177.8320 179.4753 177.8159 179.9181 176.3337 179.6239 179.4277 180.3901

179.0016 180.7789 180.5083 181.2937 181.4430 179.2461 179.2569 177.5000

178.9000 178.9000 179.8000 180.2000 181.7000 182.6000 184.6000 184.6000

185.0593 185.2501 185.4410 185.6318

Sep Oct Nov Dec

180.5875

176.8029

177.2197

180.7103

179.7000

180.3000 181.5000 179.2000

184.2959

184.4867

184.6776

184.8684

•

GDP

The GDP is calculated from the monthly trend equation and the completed dataset is as

follows:

8.528097 8.190153 7.867110 7.558967 7.265723 6.987380 6.723937 6.475393

6.241750 6.023007 5.819163 5.630220 5.456177 5.297033 5.152790 5.023447

4.909003

4.809460

4.724817

4.655073

4.600230

4.560287

4.535243

4.525100

4.529857

4.549513

4.584070

4.633527

4.697883

4.777140

4.871297

4.980353

5.104310

5.243167

5.396923

5.565580

5.749137

5.947593

6.160950

As soon as all the Covariates are obtained,we obtain the Predictes sales value of the

upcoming3 quarters using the model

Yt=0.6267+.1075*GDPt-0.4833*Yt-1-.1112*GDPt-1+0.0004369*CPIt-

.002113*PPIt+.003419*Sugar t-1-.000006989*Oil t-1-0.001431*IPIt

They are as follows:

Month Value Offtake per Stores(Predicted)

July 2014 0.218195

Aug 2014 0.2399177

Sep 2014 0.2223075

Oct 2014 0.2269519

Nov 2014 0.2184703

Dec 2014 0.2263709

Jan 2015 0.2227174

Feb 2015 0.2202478

Mar 2015 0.2196627

The graph of the total Sales is as given below:

Thus we have achieved our 2nd objective as well.