Embed Size (px)

Citation preview

Macquarie S

uper and Pension M

anager M

acquarie Super A

ccumulator

Macquarie Super and Pension Manager

Macquarie Super AccumulatorAnnual report to investors Year ended 30 June 2008

Macquarie Superannuation Plan Smart administration solutions made simple

Macquarie Investment Management Limited ABN 66 002 867 003 AFSL 237492 RSEL L0001281

Contents01 Welcome

02 The year in review

04 Investment returns to 30 June 2008

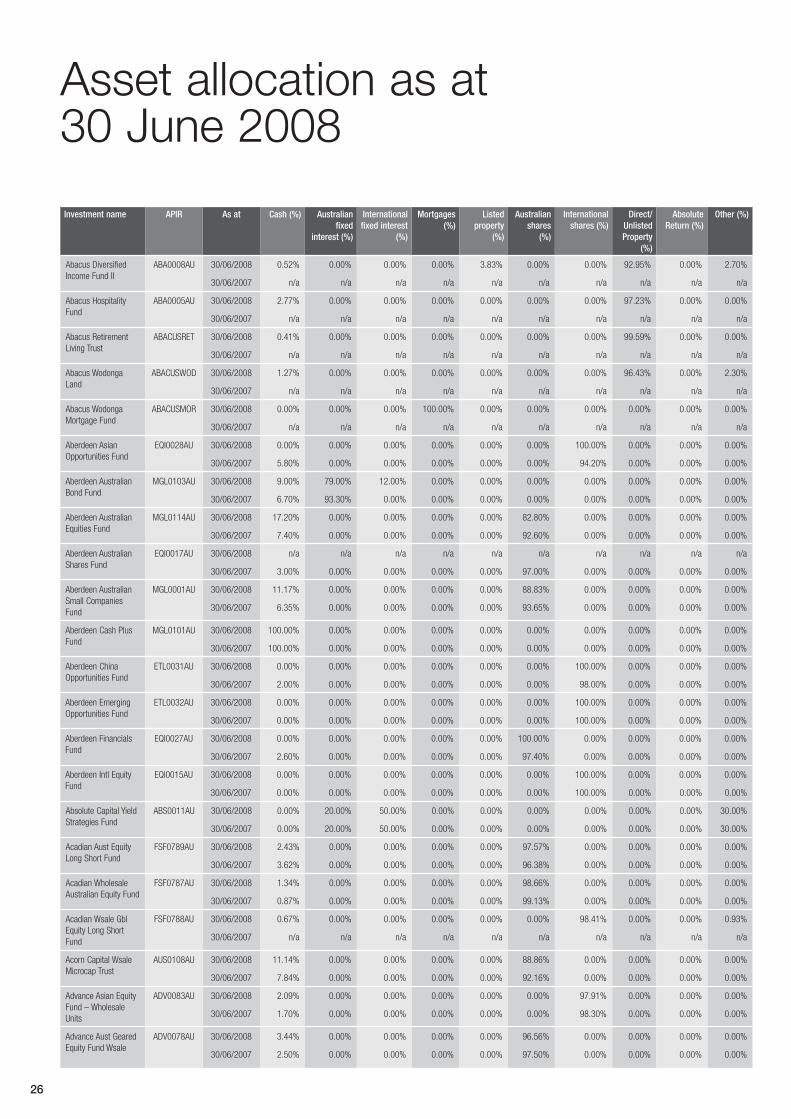

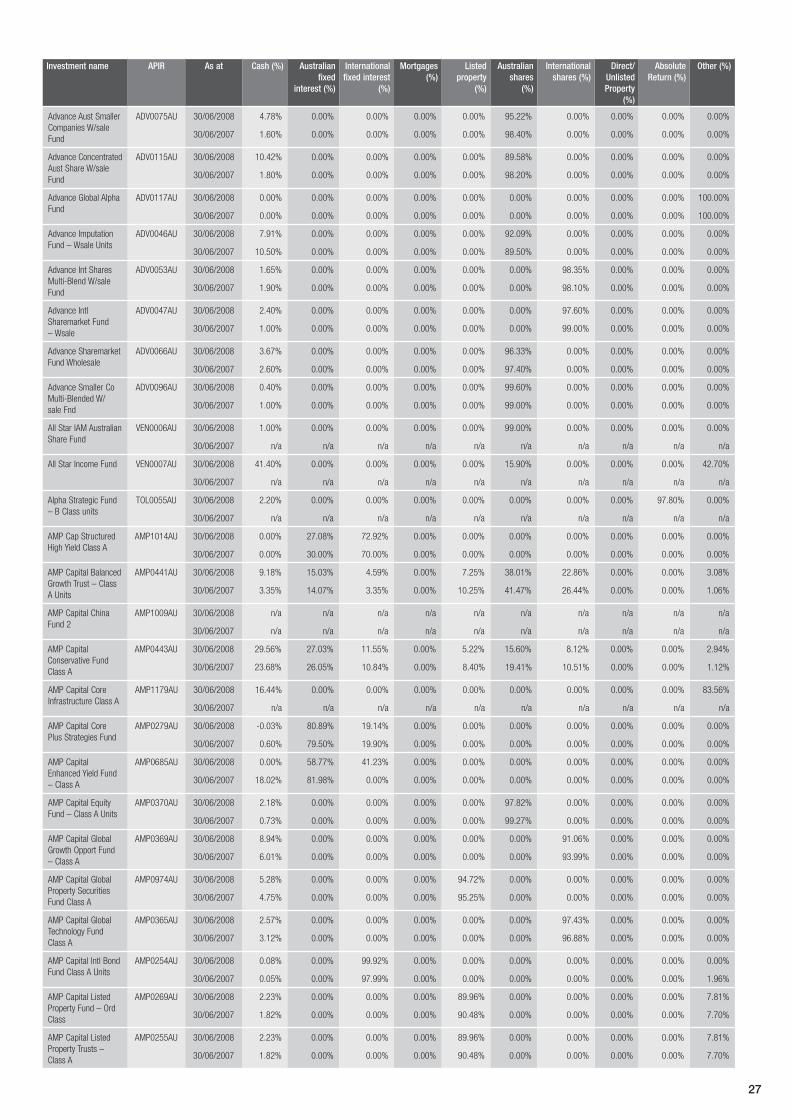

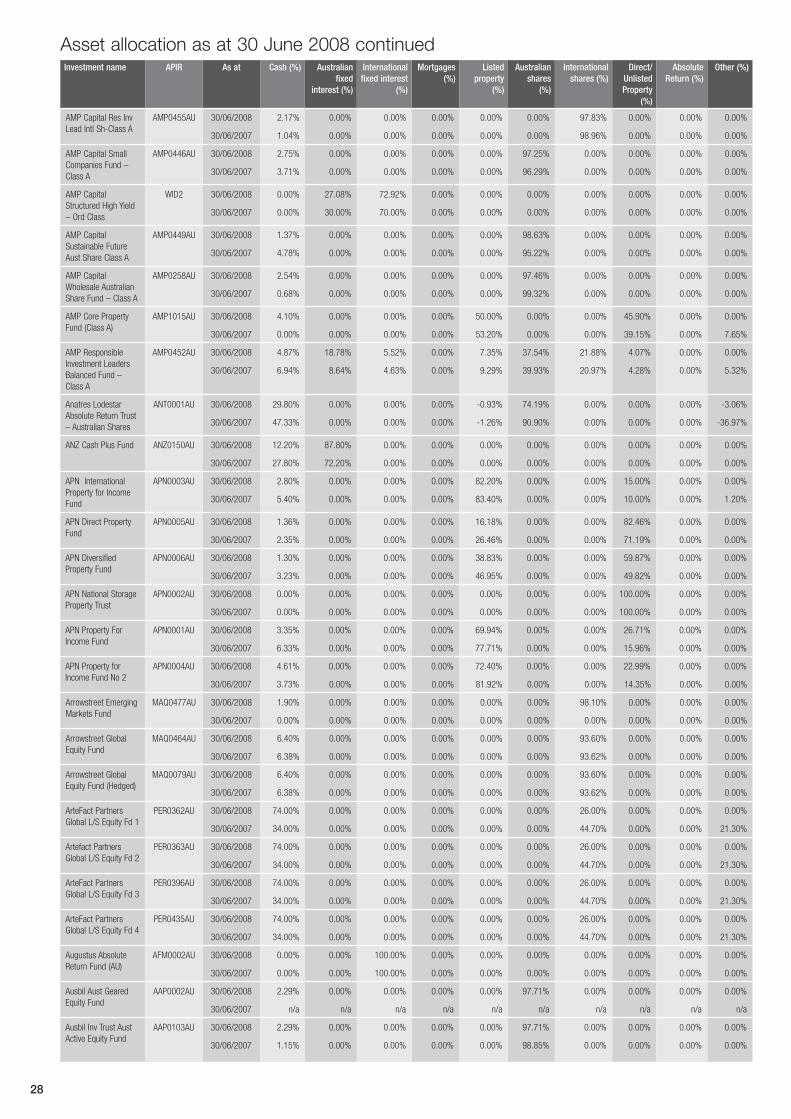

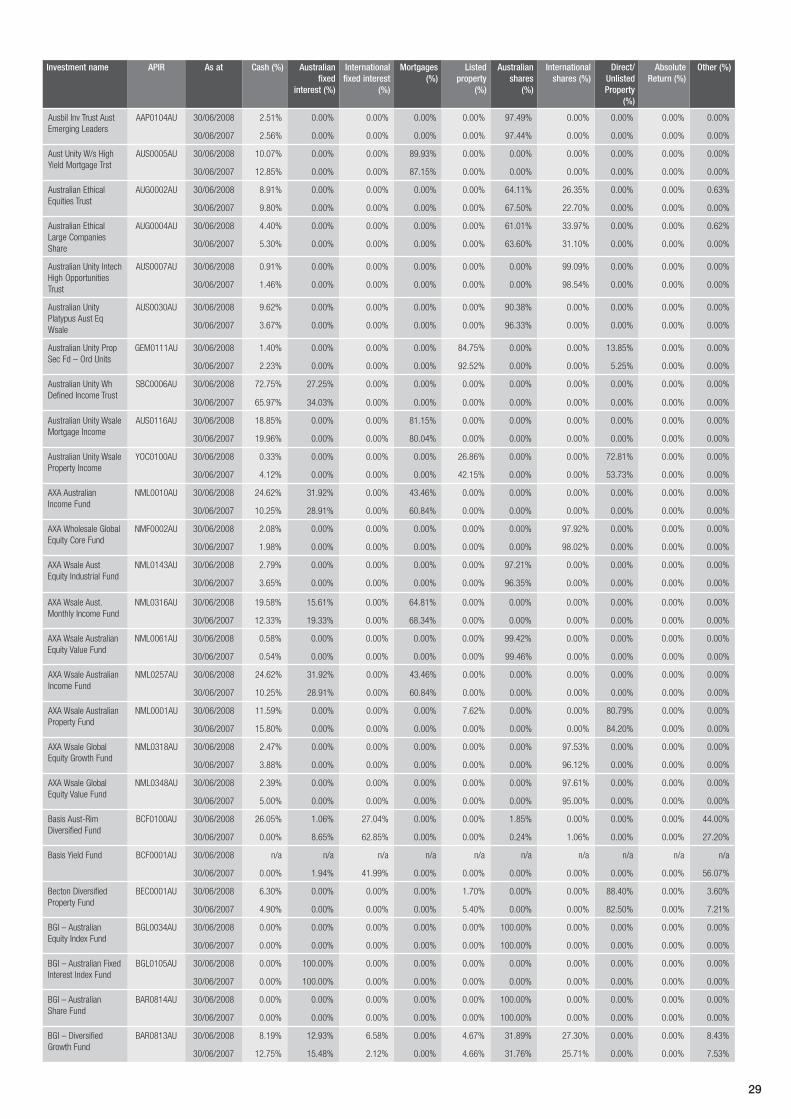

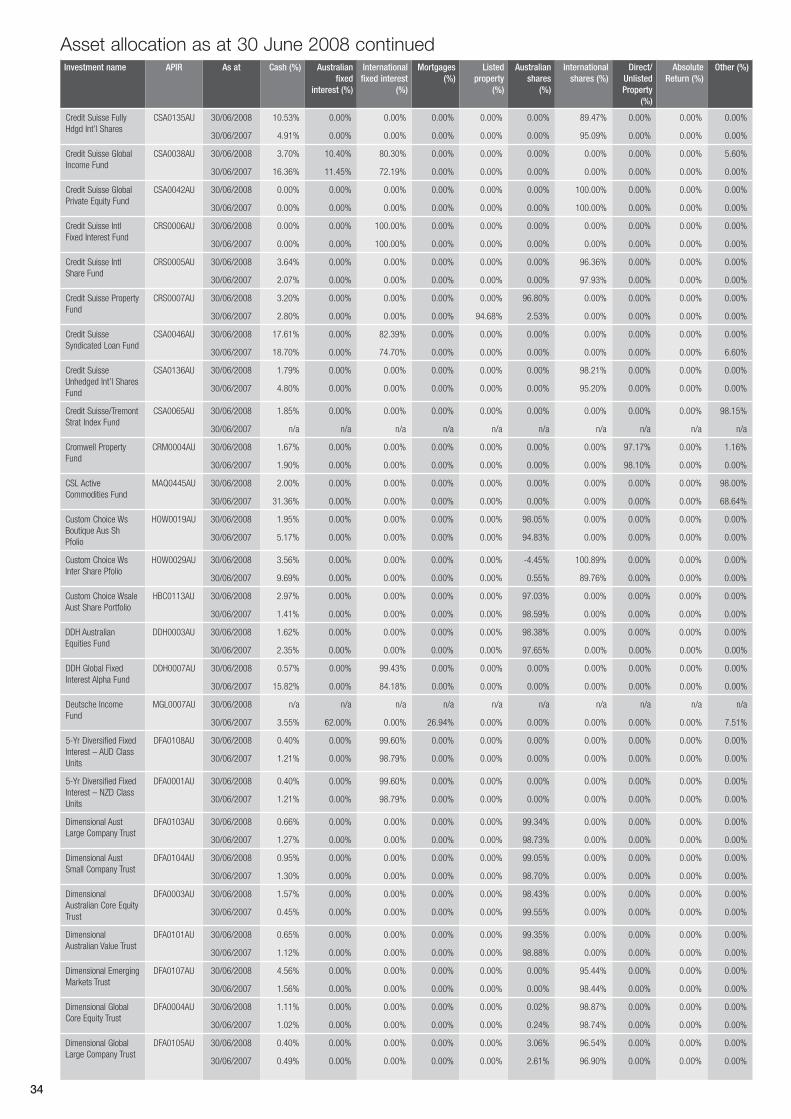

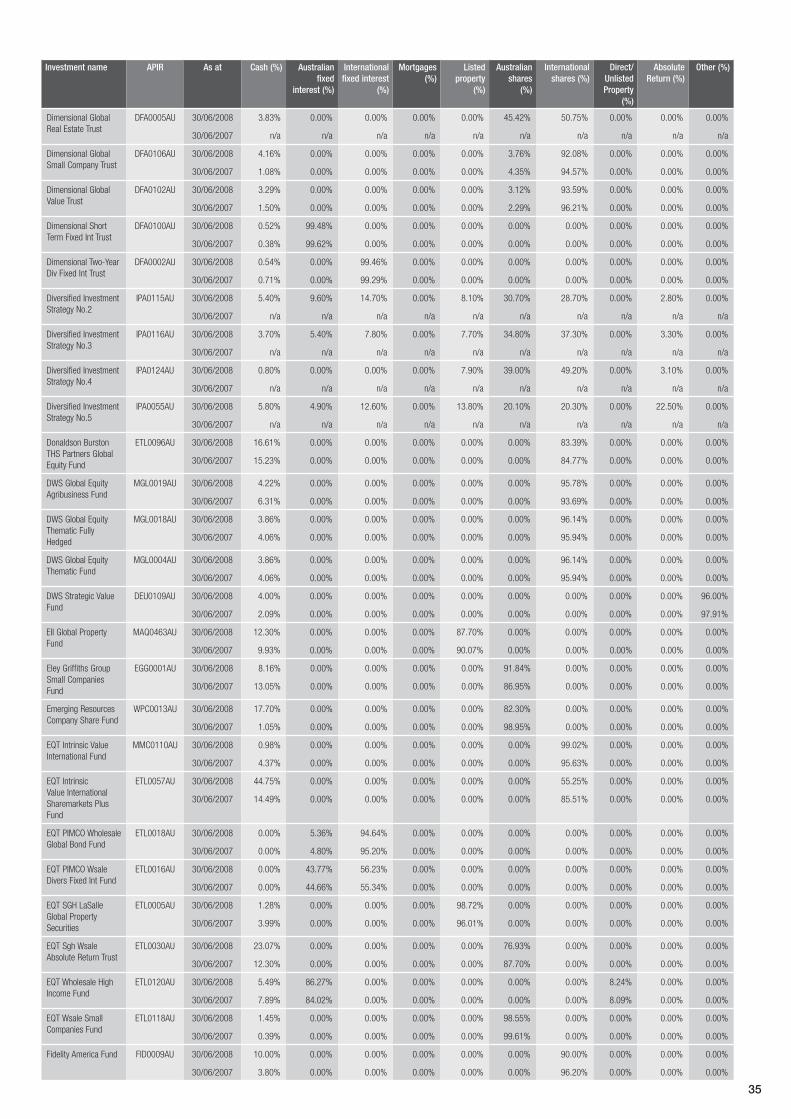

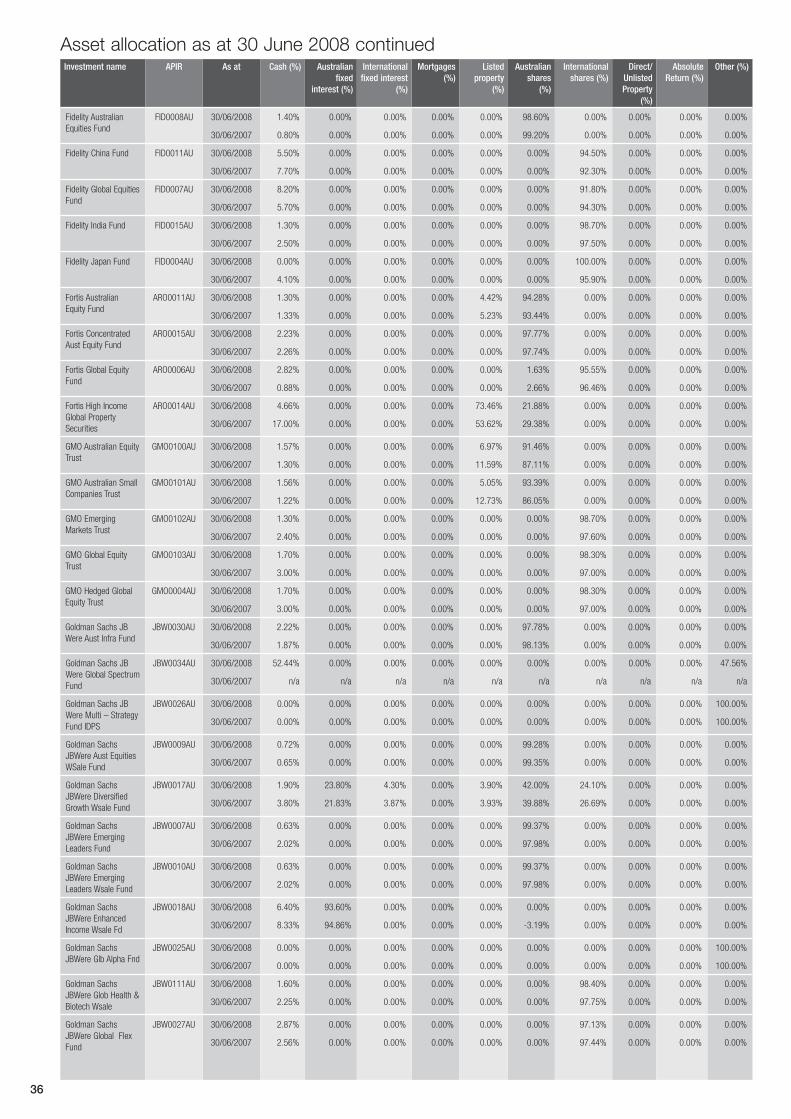

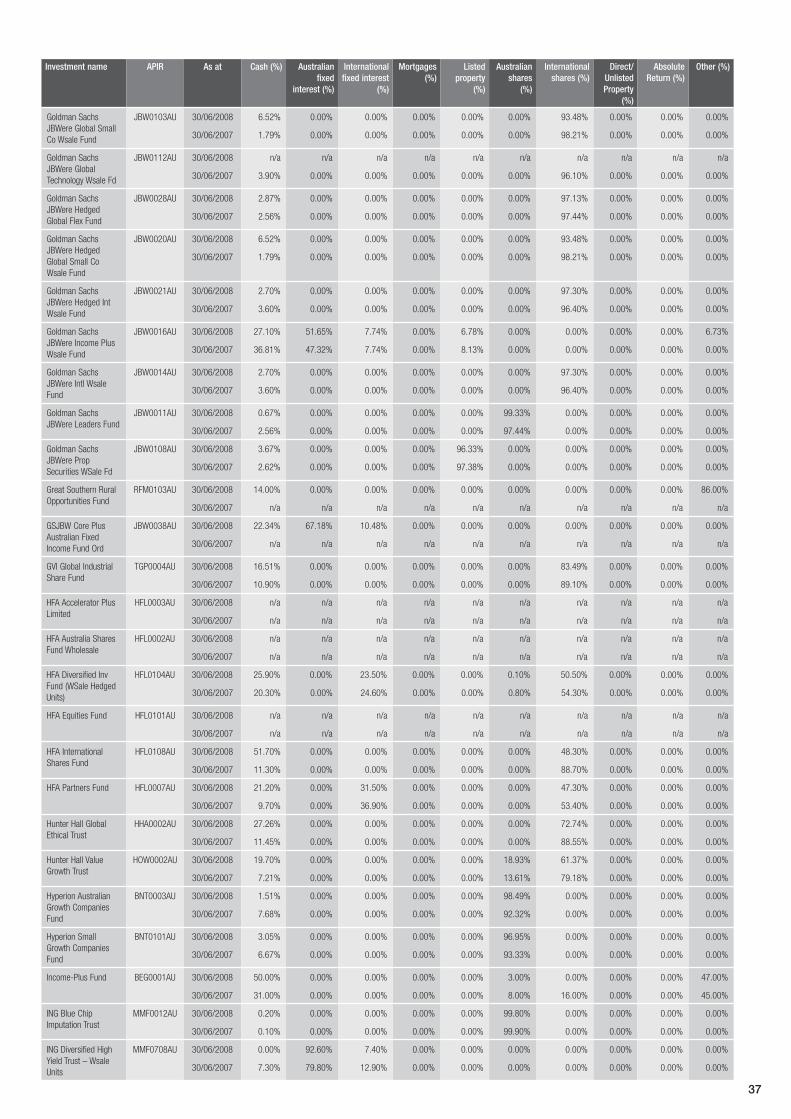

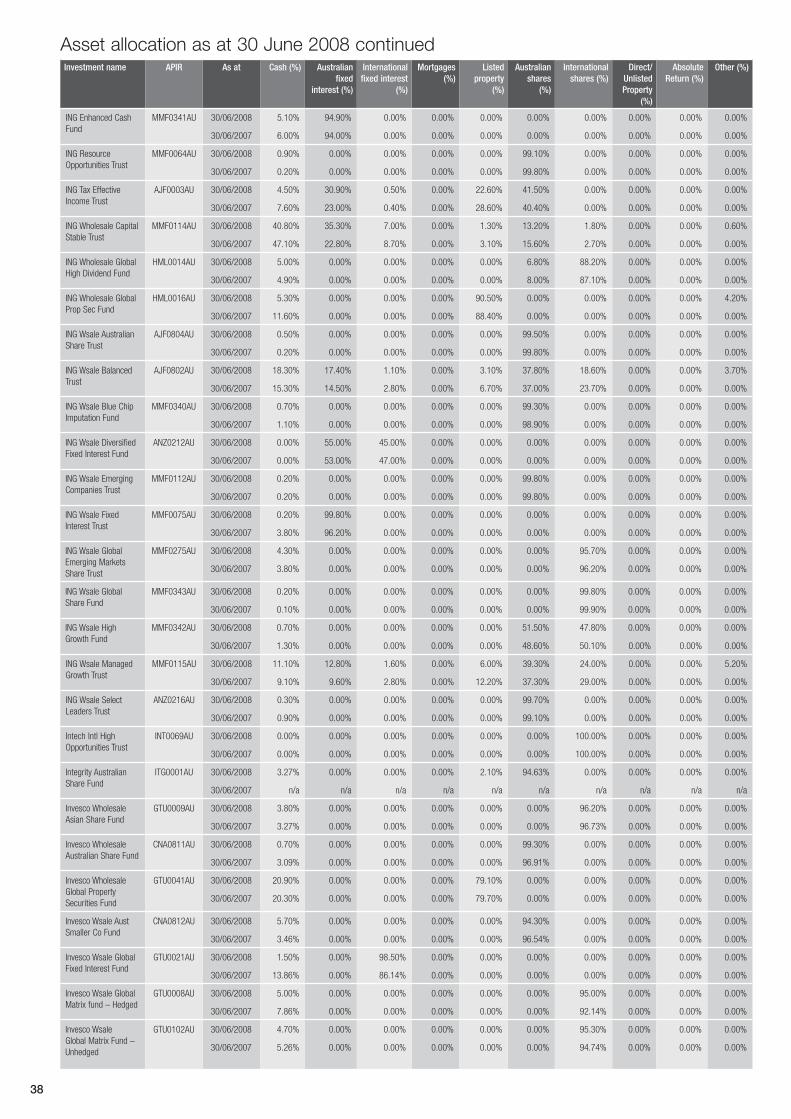

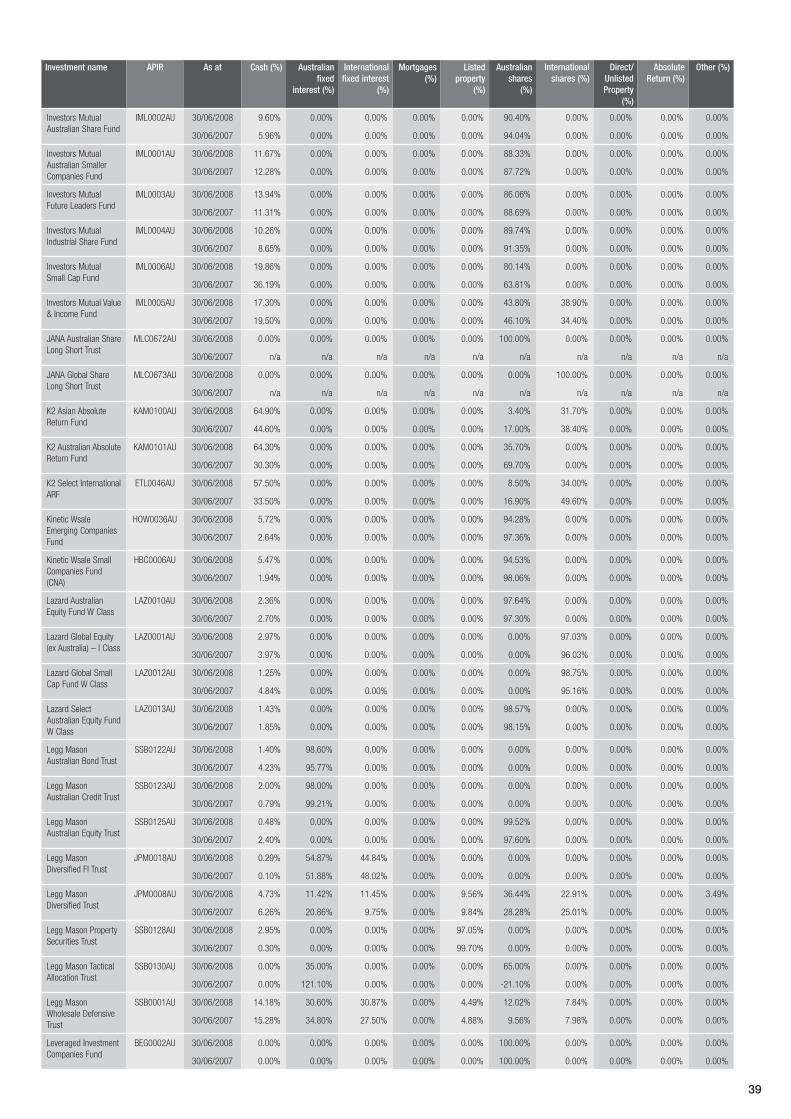

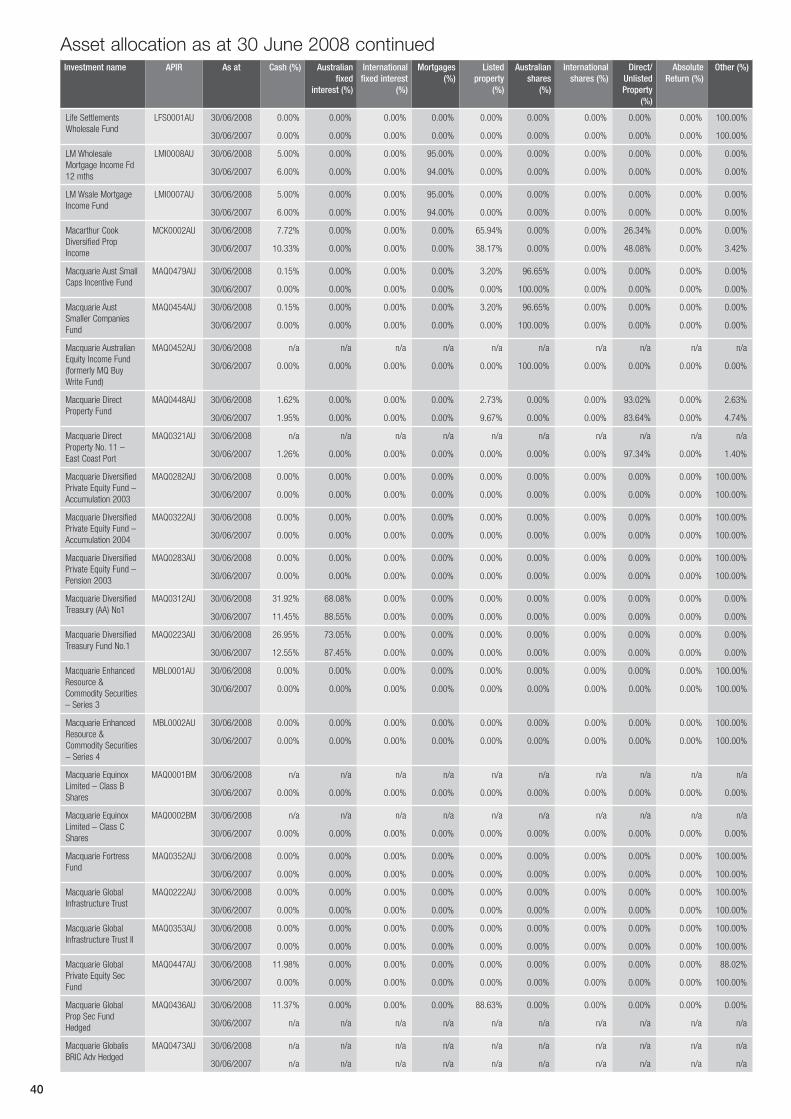

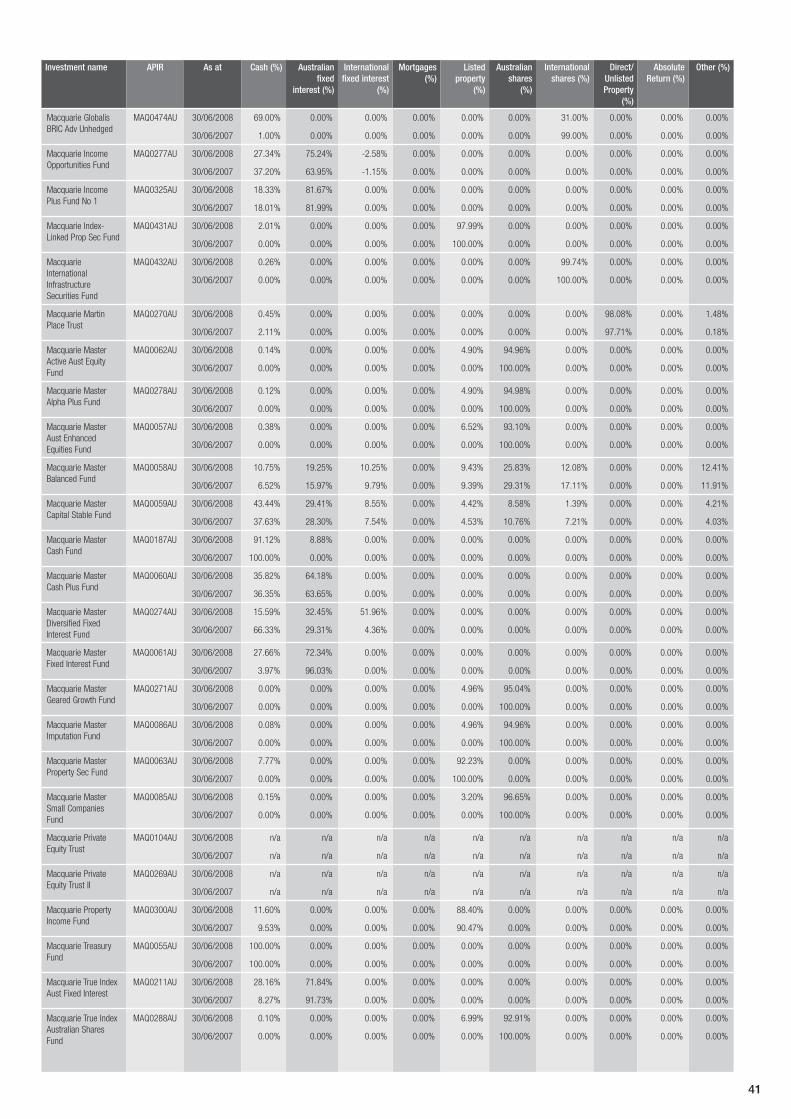

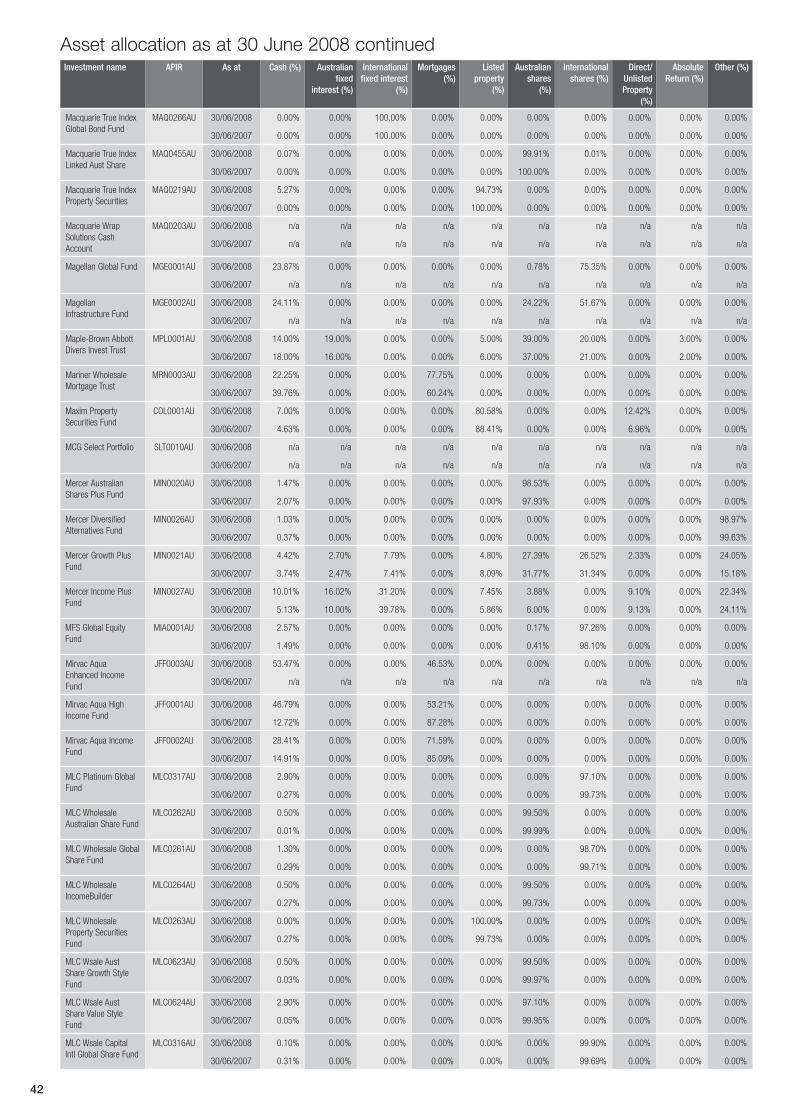

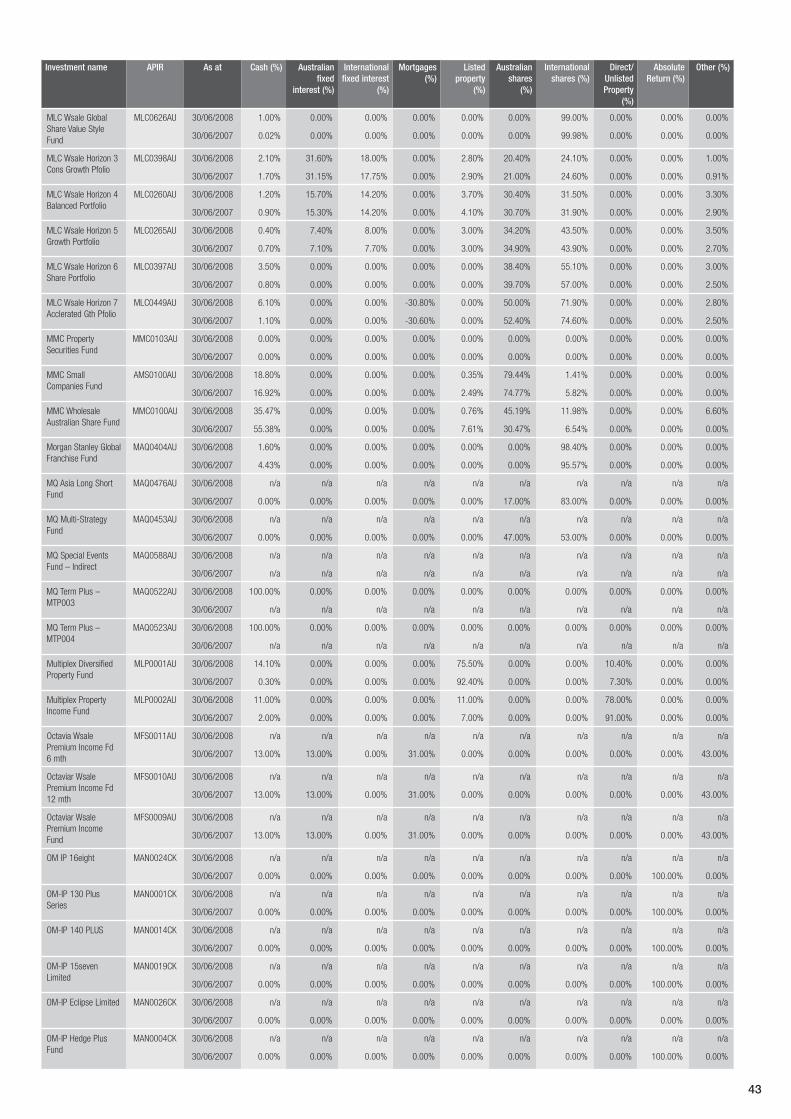

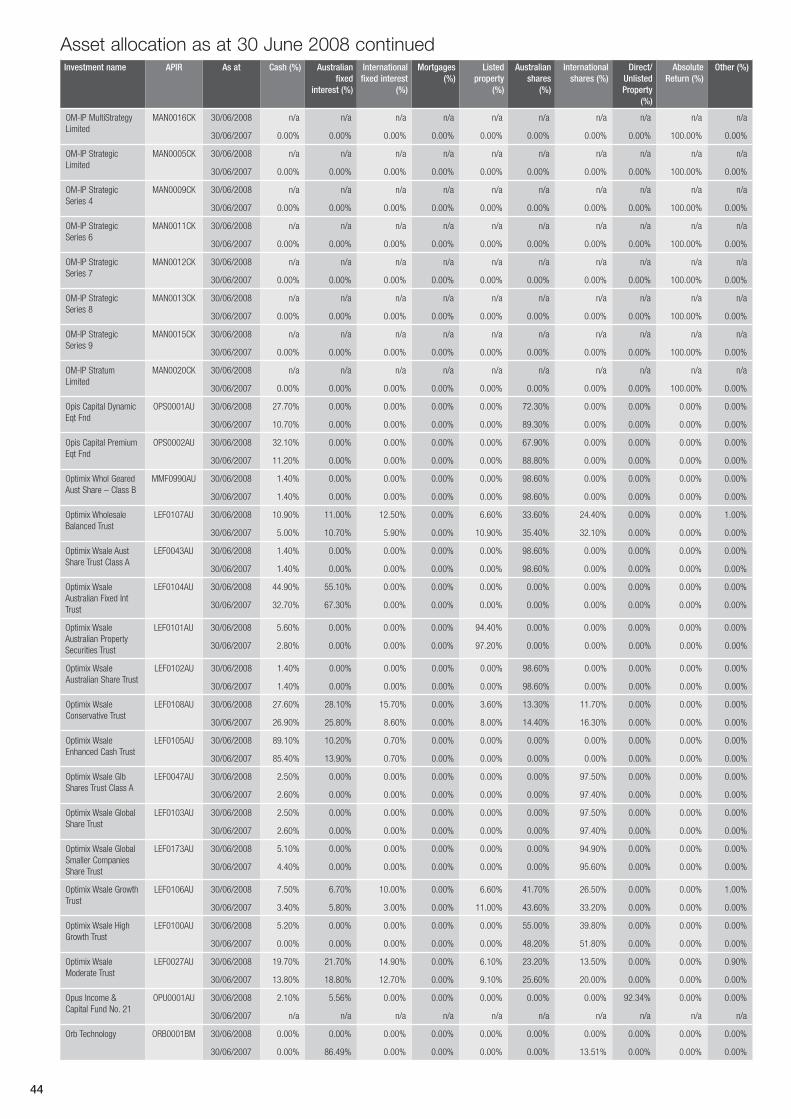

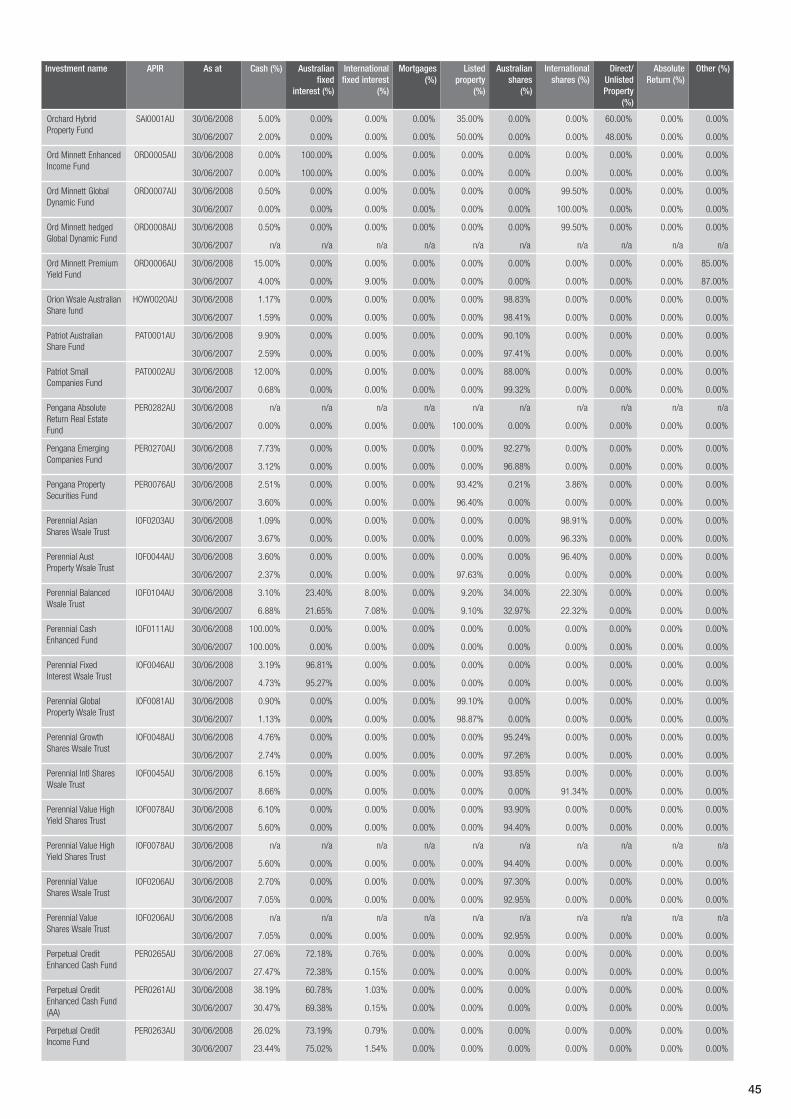

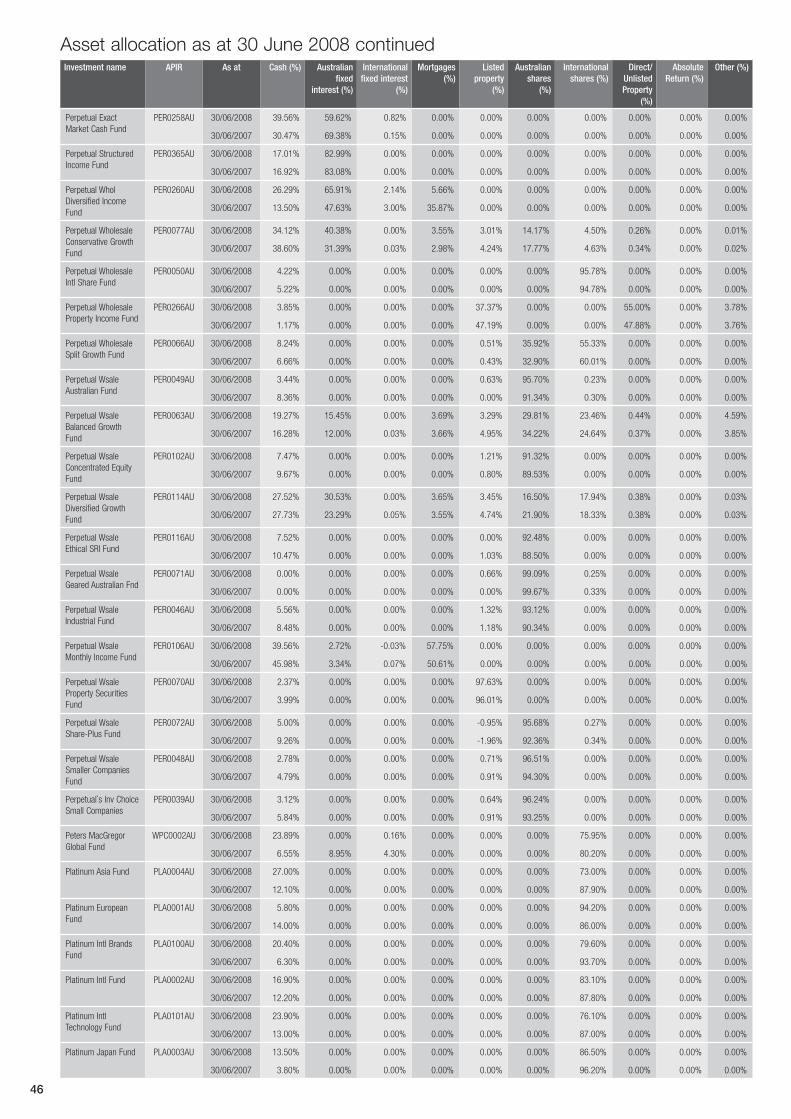

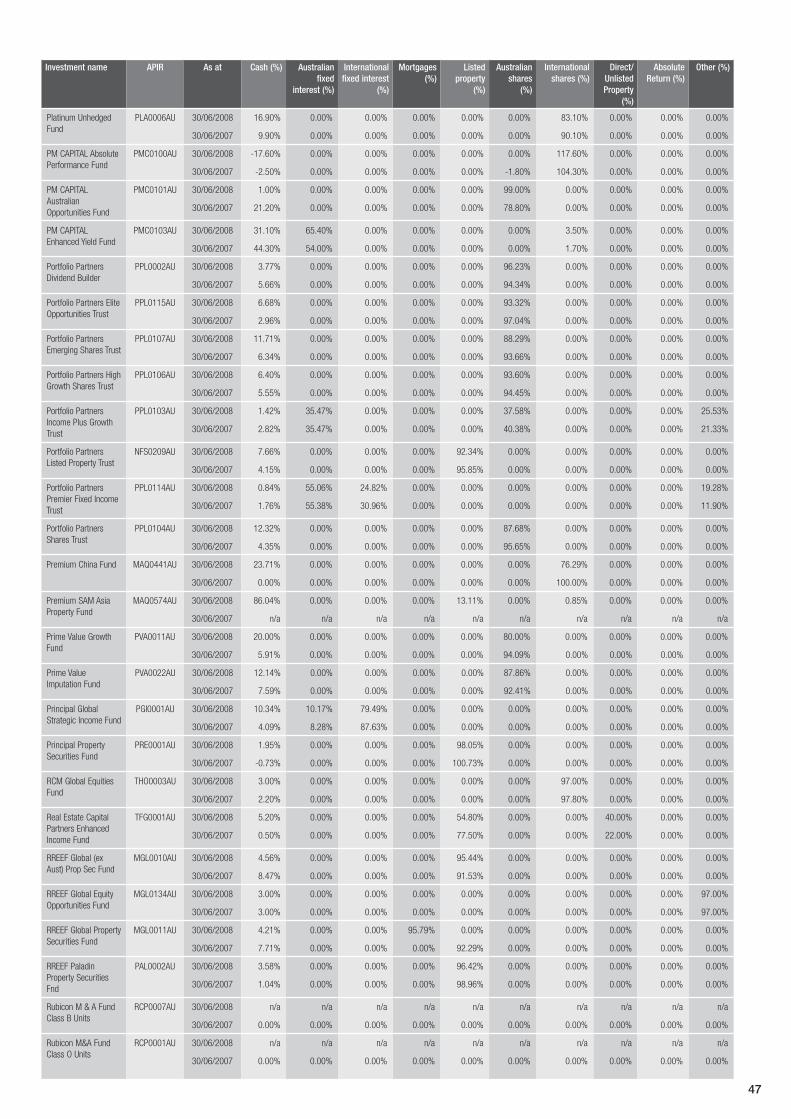

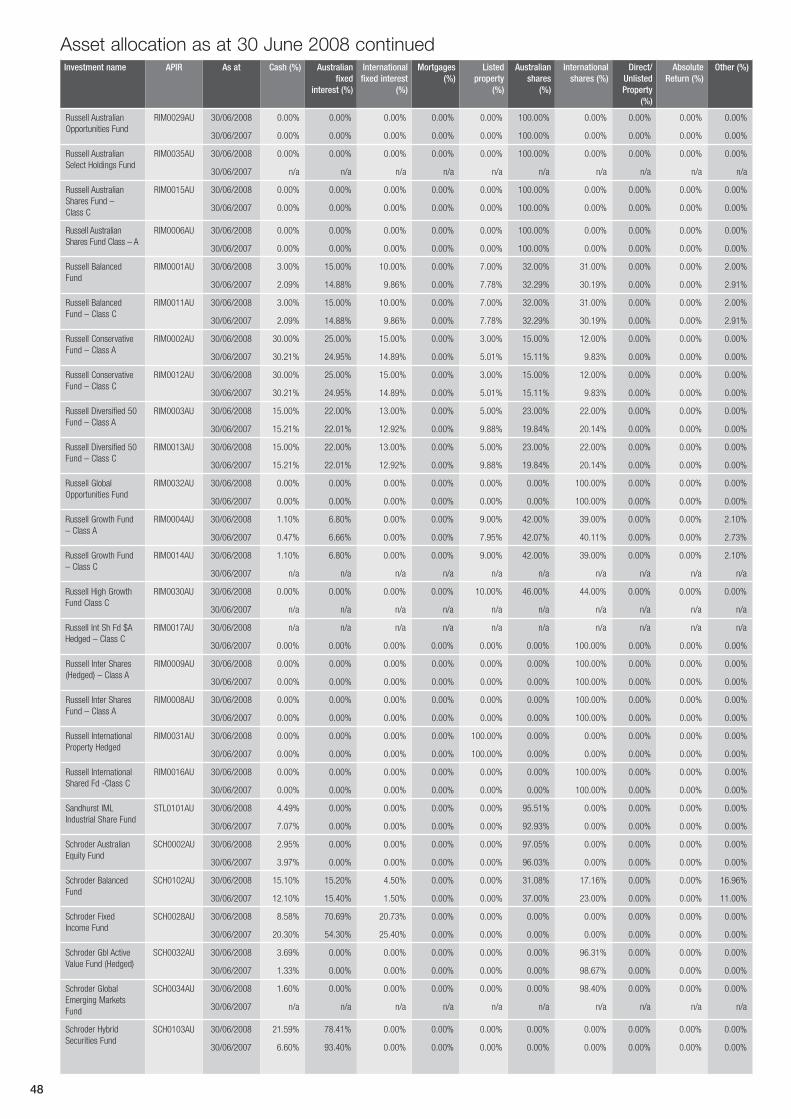

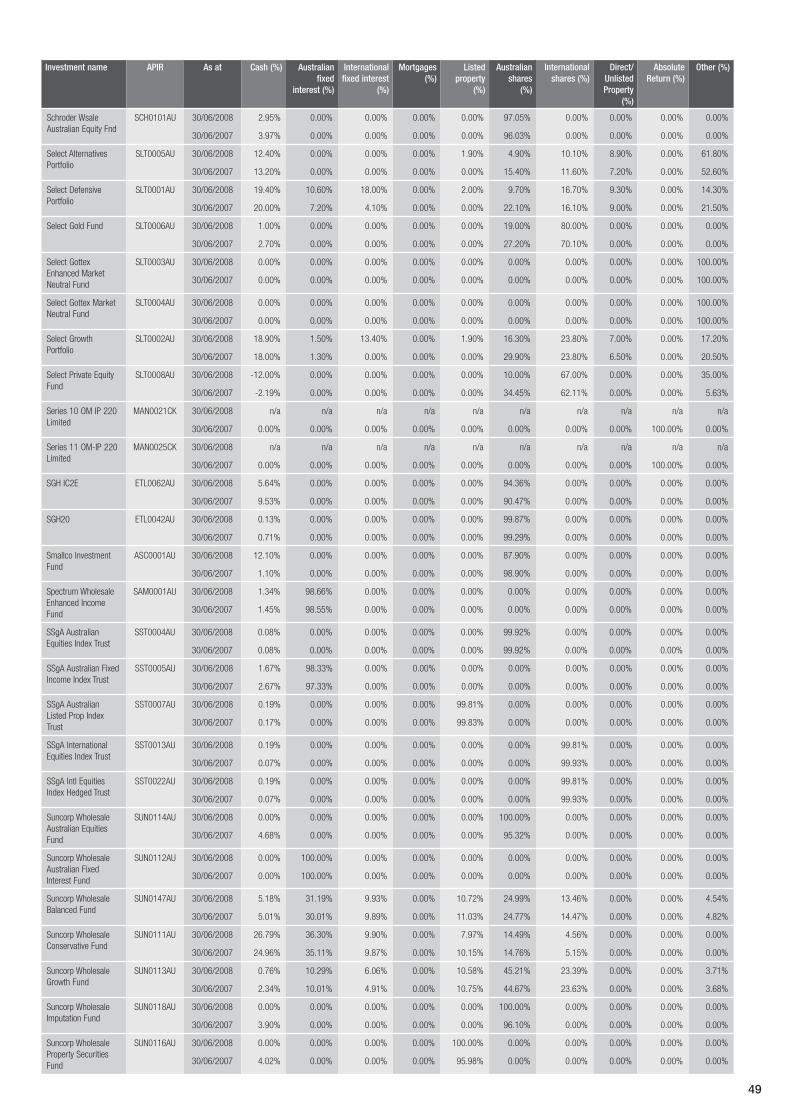

26 Asset allocation as at 30 June 2008

53 Investment strategies

56 Important information

59 Financial statements

62 Notes to and forming part of the financial statements

70 Trustee’s statement

71 Independent report by approved auditor to trustee and members

Macquarie Super and Pension Manager (Super and Pension Manager) together with Macquarie Super Accumulator (Super Accumulator) form part of a superannuation fund known as the Macquarie Superannuation Plan RSE R1004496. The trustee for the superannuation fund is Macquarie Investment Management Limited ABN 66 002 867 003 AFSL 237 492 RSEL L0001281 (MIML, Macquarie, the trustee, we, us).

MIML has appointed Bond Street Custodians Limited (BSCL) ABN 57 008 607 065 AFSL 237 489 to hold the fund’s investments in custody. BSCL and MIML are wholly owned subsidiaries of Macquarie Bank Limited ABN 46 008 583 542.

MIML is not an authorised deposit-taking institution for the purposes of the Banking Act (Cth) 1959, and MIML’s obligations do not represent deposits or other liabilities of Macquarie Bank Limited. Macquarie Bank Limited does not guarantee or otherwise provide assurance in respect of the obligations of MIML.

Investments in Super and Pension Manager and Super Accumulator are not deposits with or other liabilities of Macquarie Bank Limited or of any Macquarie Group company, and are subject to investment risk, including possible delays in repayment and loss of income or principal invested. Neither Macquarie Bank Limited, MIML, Macquarie Life Limited ABN 56 003 963 773 AFSL 237 497, Macquarie Equities Limited ABN 41 002 574 923, any other investment managers referred to in this annual report, nor any other member company of the Macquarie Group guarantees the performance of Super and Pension Manager or Super Accumulator or the repayment of capital from Super and Pension Manager or Super Accumulator.

The information contained in this annual report is dated 22 December 2008 and is general information only. We have not taken into account your objectives, financial situation or needs. You should consider the appropriateness of this information, taking into account your objectives, financial situation and needs and the applicable PDS available from us or your adviser, before acting on any of the information in this annual report.

1

Welcome

22 December 2008

Dear Investor,

Welcome to the annual report for Super and Pension Manager and Super Accumulator for the year ended 30 June 2008.

The 2007–08 financial year saw the successful implementation of the Government’s Better Super reforms. Key among the changes were new limits on the amount of contributions you can make, tax free benefits after reaching the age of 60 and modified pension payment rules.

It has also proven to be an extraordinary year in a number of ways. The pace of change in the outlook for growth, commodity prices, equity markets, interest rates and government policy has been so dramatic that even the most astute analysts and investors have been barely able to keep up.

Given the amazing developments of the past couple of months, it is easy to forget there has been not one but two once in a lifetime phenomena in 2008. The first half of the year was characterised by an incredible divergence between the fortunes of credit and commodity markets, followed by the fallout in financial markets from the subprime mortgage debacle that gained increasing traction in early 2008.

To help you make sense of the year’s events, we have included ‘The year in review’ section on the following pages.

If you have any questions about this annual report, Super and Pension Manager or Super Accumulator in general, please contact your adviser.

Yours sincerely,

Neil Roderick Executive Director

Macquarie Investment Management Limited

This annual report includes information on:

Super Manager ■■ and Super Accumulator, accumulation superannuation products

Pension Manager■■ , a retirement income solution incorporating an account based pension and Term Allocated Pension.

References to Pension Manager can be interpreted as references to both Pension Manager and Term Allocated Pension Manager.

The financial statements relate to the entire Macquarie Superannuation Plan which includes Macquarie Super and Pension Manager, Macquarie Super Accumulator, Macquarie SuperOptions and FutureWise Super – a risk only superannuation fund.

2

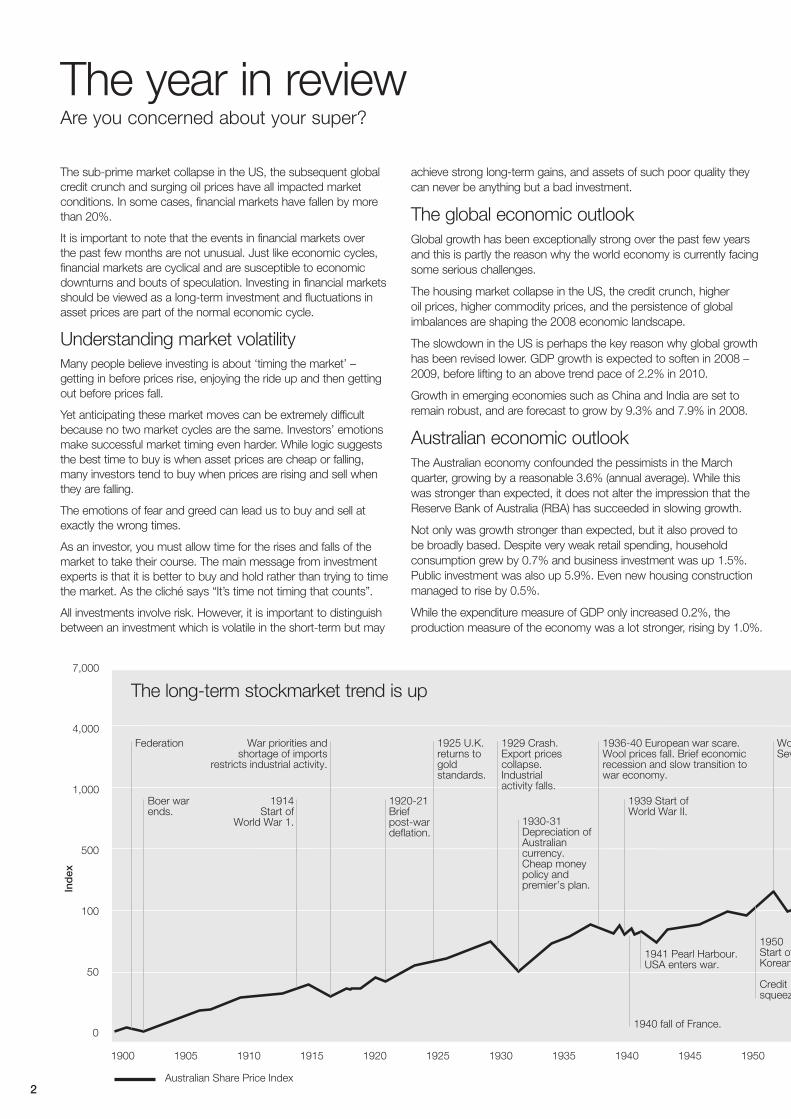

The sub-prime market collapse in the US, the subsequent global credit crunch and surging oil prices have all impacted market conditions. In some cases, financial markets have fallen by more than 20%.

It is important to note that the events in financial markets over the past few months are not unusual. Just like economic cycles, financial markets are cyclical and are susceptible to economic downturns and bouts of speculation. Investing in financial markets should be viewed as a long-term investment and fluctuations in asset prices are part of the normal economic cycle.

Understanding market volatilityMany people believe investing is about ‘timing the market’ – getting in before prices rise, enjoying the ride up and then getting out before prices fall.

Yet anticipating these market moves can be extremely difficult because no two market cycles are the same. Investors’ emotions make successful market timing even harder. While logic suggests the best time to buy is when asset prices are cheap or falling, many investors tend to buy when prices are rising and sell when they are falling.

The emotions of fear and greed can lead us to buy and sell at exactly the wrong times.

As an investor, you must allow time for the rises and falls of the market to take their course. The main message from investment experts is that it is better to buy and hold rather than trying to time the market. As the cliché says “It’s time not timing that counts”.

All investments involve risk. However, it is important to distinguish between an investment which is volatile in the short-term but may

achieve strong long-term gains, and assets of such poor quality they can never be anything but a bad investment.

The global economic outlookGlobal growth has been exceptionally strong over the past few years and this is partly the reason why the world economy is currently facing some serious challenges.

The housing market collapse in the US, the credit crunch, higher oil prices, higher commodity prices, and the persistence of global imbalances are shaping the 2008 economic landscape.

The slowdown in the US is perhaps the key reason why global growth has been revised lower. GDP growth is expected to soften in 2008 – 2009, before lifting to an above trend pace of 2.2% in 2010.

Growth in emerging economies such as China and India are set to remain robust, and are forecast to grow by 9.3% and 7.9% in 2008.

Australian economic outlookThe Australian economy confounded the pessimists in the March quarter, growing by a reasonable 3.6% (annual average). While this was stronger than expected, it does not alter the impression that the Reserve Bank of Australia (RBA) has succeeded in slowing growth.

Not only was growth stronger than expected, but it also proved to be broadly based. Despite very weak retail spending, household consumption grew by 0.7% and business investment was up 1.5%. Public investment was also up 5.9%. Even new housing construction managed to rise by 0.5%.

While the expenditure measure of GDP only increased 0.2%, the production measure of the economy was a lot stronger, rising by 1.0%.

The year in reviewAre you concerned about your super?

4,000

0

100

1,000

7,000

500

50

Federation

Boer war ends.

1914Start of

World War 1.

War priorities andshortage of imports

restricts industrial activity.

1920-21Briefpost-wardeflation.

1925 U.K.returns togold standards.

1929 Crash. Export pricescollapse. Industrialactivity falls.

1930-31Depreciation ofAustralian currency.Cheap moneypolicy andpremier’s plan.

1936-40 European war scare. Wool prices fall. Brief economicrecession and slow transition towar economy.

1939 Start ofWorld War II.

1940 fall of France.

1941 Pearl Harbour.USA enters war.

Suezcrisis

Strong overseasinvestment, scrip shortage and property boom.

1950Start of Korean War.

Credit squeeze.

Oil, gas andnickel discoveries.

Iron ore andbauxite developed.

Industrial andproperty boom. First labourgovernment since 1949.

OPEC oil crisis.Inflation,credit squeeze.Property company failures.

Inflation down,industrials recover, commodities weak. $A fallattracts overseasinvestors.

Worldshareprice

collapse.Bankcreditfuels

propertyboom.

Cold War ends. CBD property crash hits banks. Major recession. Interest rates and inflation fall. Privatisation starts.

CPI rise under 2%.Bond yields at 20 year low. Gold price up.

World interest rates rise then falls. S&P up 70% in 2 years.

World TradeCentre attacks

US deflationscare

Subprimemortgage

crisis

Oil found inBass Strait.

Wool prices peak.Severe but brief inflation.

Oil, mining andPoseidon booms.

Energy and metalsharesboom.

Commodities plunge,interest rates peak,

severe recession,rising deficit.

The ‘87Crash

The ‘00Dot.comCrash

The ‘94 BondMarket Crisis

Australian Share Price Index

Ind

ex

1900 1905 1910 1915 1920 1925 1930 1935 1940 1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2008

The long-term stockmarket trend is up

3

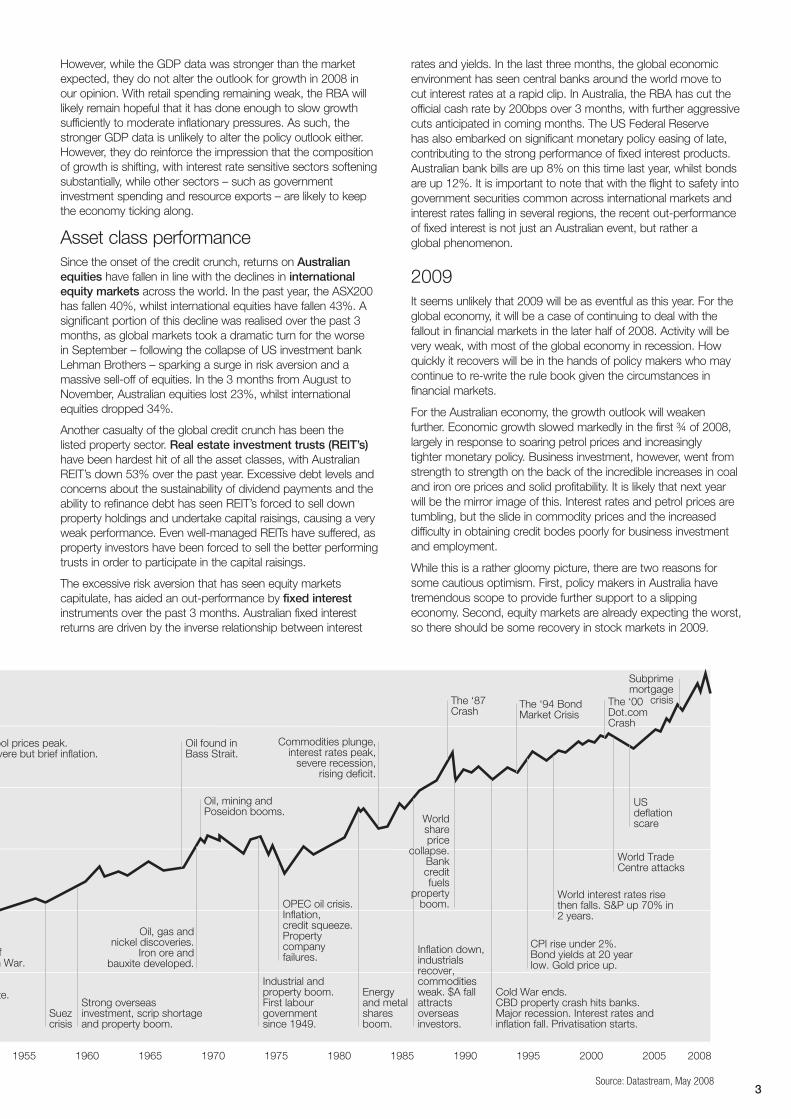

However, while the GDP data was stronger than the market expected, they do not alter the outlook for growth in 2008 in our opinion. With retail spending remaining weak, the RBA will likely remain hopeful that it has done enough to slow growth sufficiently to moderate inflationary pressures. As such, the stronger GDP data is unlikely to alter the policy outlook either. However, they do reinforce the impression that the composition of growth is shifting, with interest rate sensitive sectors softening substantially, while other sectors – such as government investment spending and resource exports – are likely to keep the economy ticking along.

Asset class performanceSince the onset of the credit crunch, returns on Australian equities have fallen in line with the declines in international equity markets across the world. In the past year, the ASX200 has fallen 40%, whilst international equities have fallen 43%. A significant portion of this decline was realised over the past 3 months, as global markets took a dramatic turn for the worse in September – following the collapse of US investment bank Lehman Brothers – sparking a surge in risk aversion and a massive sell-off of equities. In the 3 months from August to November, Australian equities lost 23%, whilst international equities dropped 34%.

Another casualty of the global credit crunch has been the listed property sector. Real estate investment trusts (REIT’s) have been hardest hit of all the asset classes, with Australian REIT’s down 53% over the past year. Excessive debt levels and concerns about the sustainability of dividend payments and the ability to refinance debt has seen REIT’s forced to sell down property holdings and undertake capital raisings, causing a very weak performance. Even well-managed REITs have suffered, as property investors have been forced to sell the better performing trusts in order to participate in the capital raisings.

The excessive risk aversion that has seen equity markets capitulate, has aided an out-performance by fixed interest instruments over the past 3 months. Australian fixed interest returns are driven by the inverse relationship between interest

rates and yields. In the last three months, the global economic environment has seen central banks around the world move to cut interest rates at a rapid clip. In Australia, the RBA has cut the official cash rate by 200bps over 3 months, with further aggressive cuts anticipated in coming months. The US Federal Reserve has also embarked on significant monetary policy easing of late, contributing to the strong performance of fixed interest products. Australian bank bills are up 8% on this time last year, whilst bonds are up 12%. It is important to note that with the flight to safety into government securities common across international markets and interest rates falling in several regions, the recent out-performance of fixed interest is not just an Australian event, but rather a global phenomenon.

2009It seems unlikely that 2009 will be as eventful as this year. For the global economy, it will be a case of continuing to deal with the fallout in financial markets in the later half of 2008. Activity will be very weak, with most of the global economy in recession. How quickly it recovers will be in the hands of policy makers who may continue to re-write the rule book given the circumstances in financial markets.

For the Australian economy, the growth outlook will weaken further. Economic growth slowed markedly in the first ¾ of 2008, largely in response to soaring petrol prices and increasingly tighter monetary policy. Business investment, however, went from strength to strength on the back of the incredible increases in coal and iron ore prices and solid profitability. It is likely that next year will be the mirror image of this. Interest rates and petrol prices are tumbling, but the slide in commodity prices and the increased difficulty in obtaining credit bodes poorly for business investment and employment.

While this is a rather gloomy picture, there are two reasons for some cautious optimism. First, policy makers in Australia have tremendous scope to provide further support to a slipping economy. Second, equity markets are already expecting the worst, so there should be some recovery in stock markets in 2009.

4,000

0

100

1,000

7,000

500

50

Federation

Boer war ends.

1914Start of

World War 1.

War priorities andshortage of imports

restricts industrial activity.

1920-21Briefpost-wardeflation.

1925 U.K.returns togold standards.

1929 Crash. Export pricescollapse. Industrialactivity falls.

1930-31Depreciation ofAustralian currency.Cheap moneypolicy andpremier’s plan.

1936-40 European war scare. Wool prices fall. Brief economicrecession and slow transition towar economy.

1939 Start ofWorld War II.

1940 fall of France.

1941 Pearl Harbour.USA enters war.

Suezcrisis

Strong overseasinvestment, scrip shortage and property boom.

1950Start of Korean War.

Credit squeeze.

Oil, gas andnickel discoveries.

Iron ore andbauxite developed.

Industrial andproperty boom. First labourgovernment since 1949.

OPEC oil crisis.Inflation,credit squeeze.Property company failures.

Inflation down,industrials recover, commodities weak. $A fallattracts overseasinvestors.

Worldshareprice

collapse.Bankcreditfuels

propertyboom.

Cold War ends. CBD property crash hits banks. Major recession. Interest rates and inflation fall. Privatisation starts.

CPI rise under 2%.Bond yields at 20 year low. Gold price up.

World interest rates rise then falls. S&P up 70% in 2 years.

World TradeCentre attacks

US deflationscare

Subprimemortgage

crisis

Oil found inBass Strait.

Wool prices peak.Severe but brief inflation.

Oil, mining andPoseidon booms.

Energy and metalsharesboom.

Commodities plunge,interest rates peak,

severe recession,rising deficit.

The ‘87Crash

The ‘00Dot.comCrash

The ‘94 BondMarket Crisis

Australian Share Price Index

Ind

ex

1900 1905 1910 1915 1920 1925 1930 1935 1940 1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2008

Source: Datastream, May 2008

4

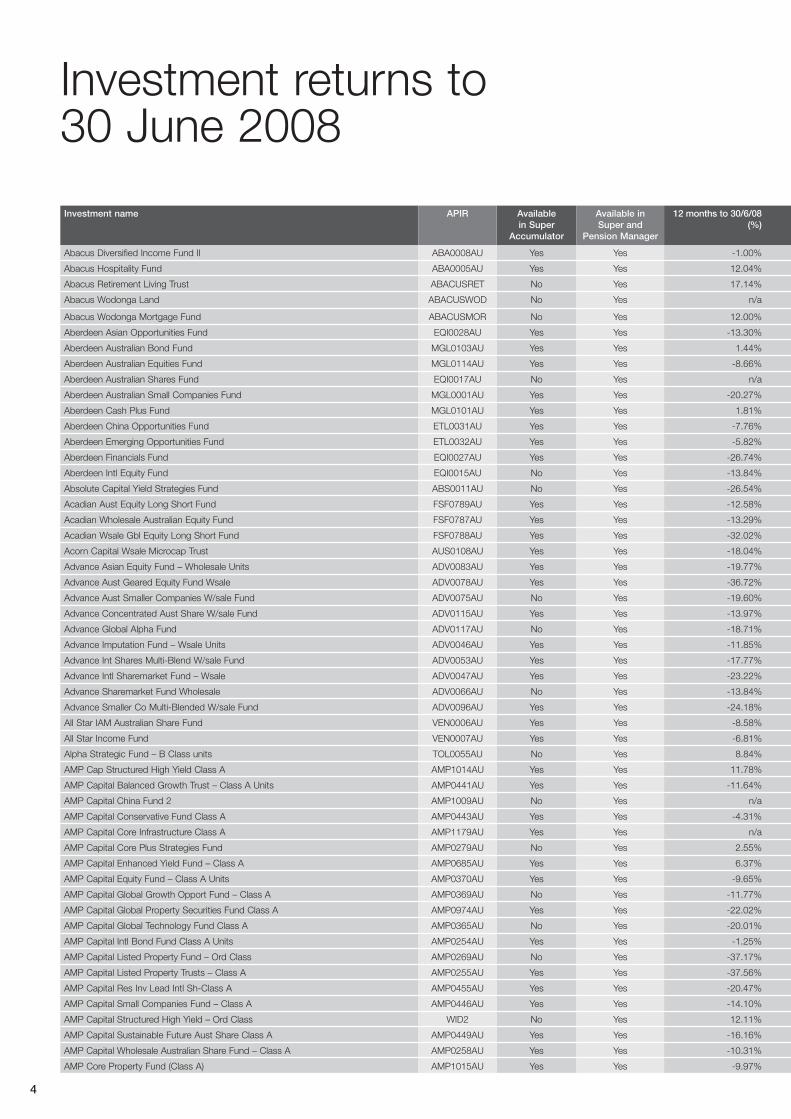

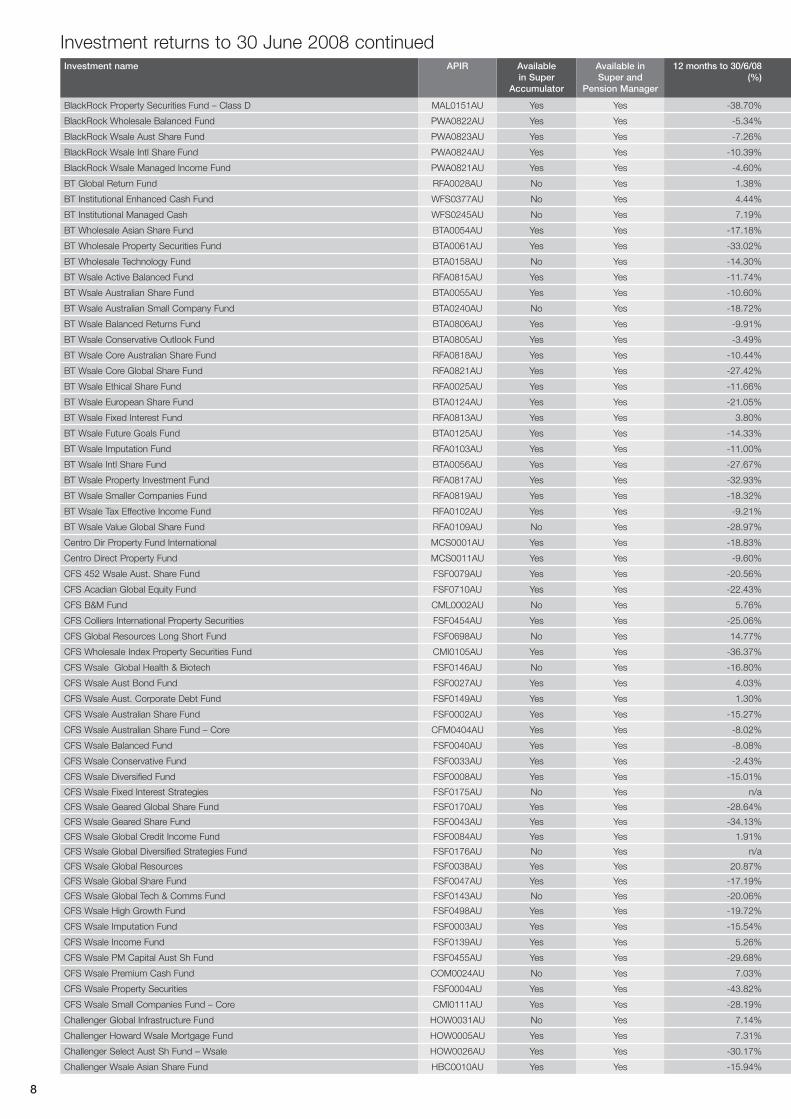

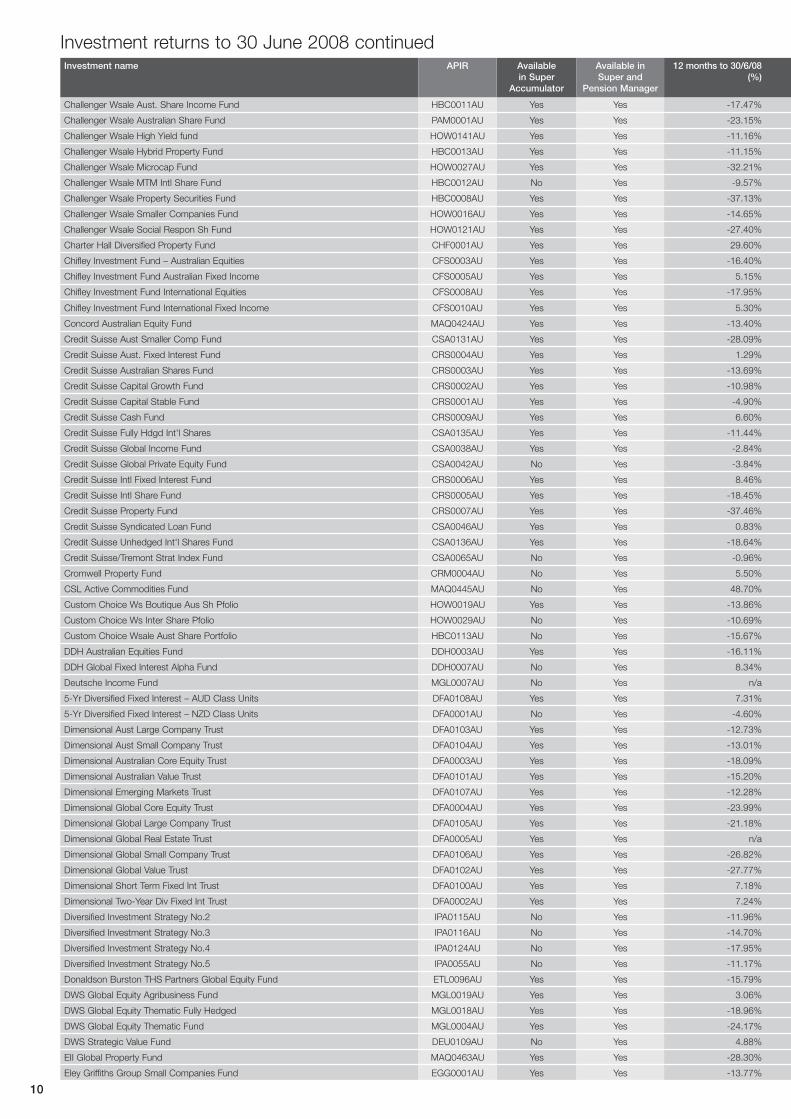

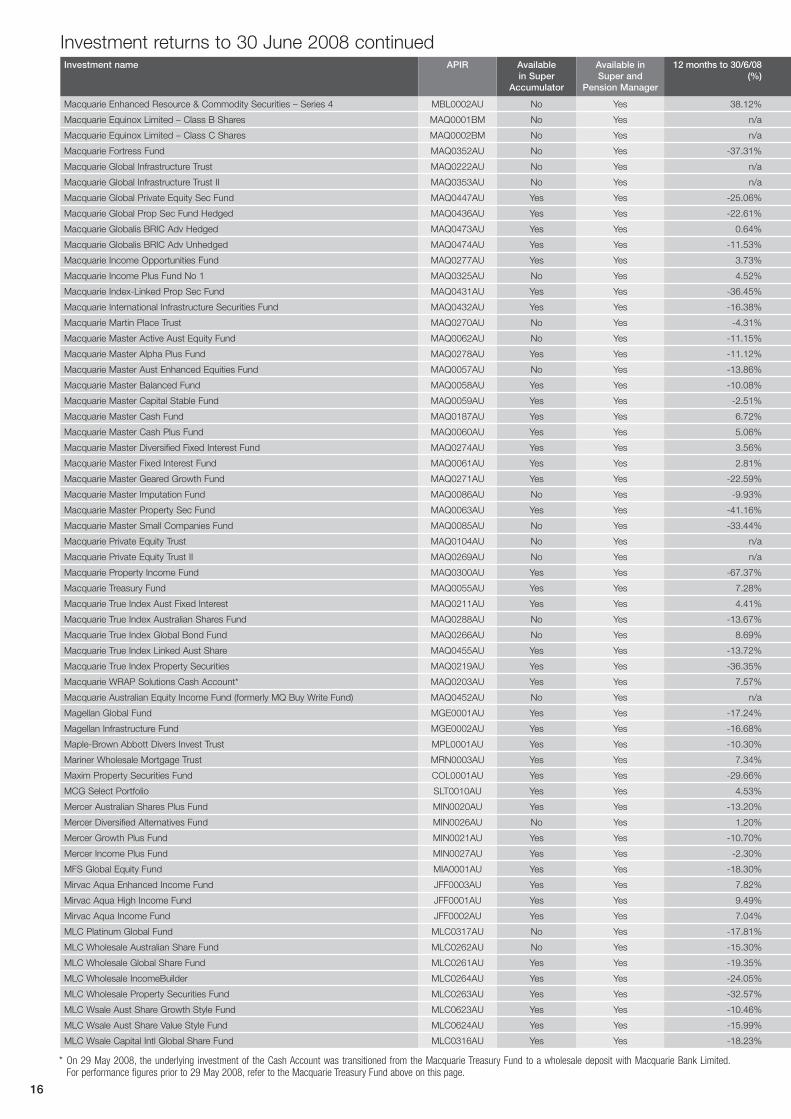

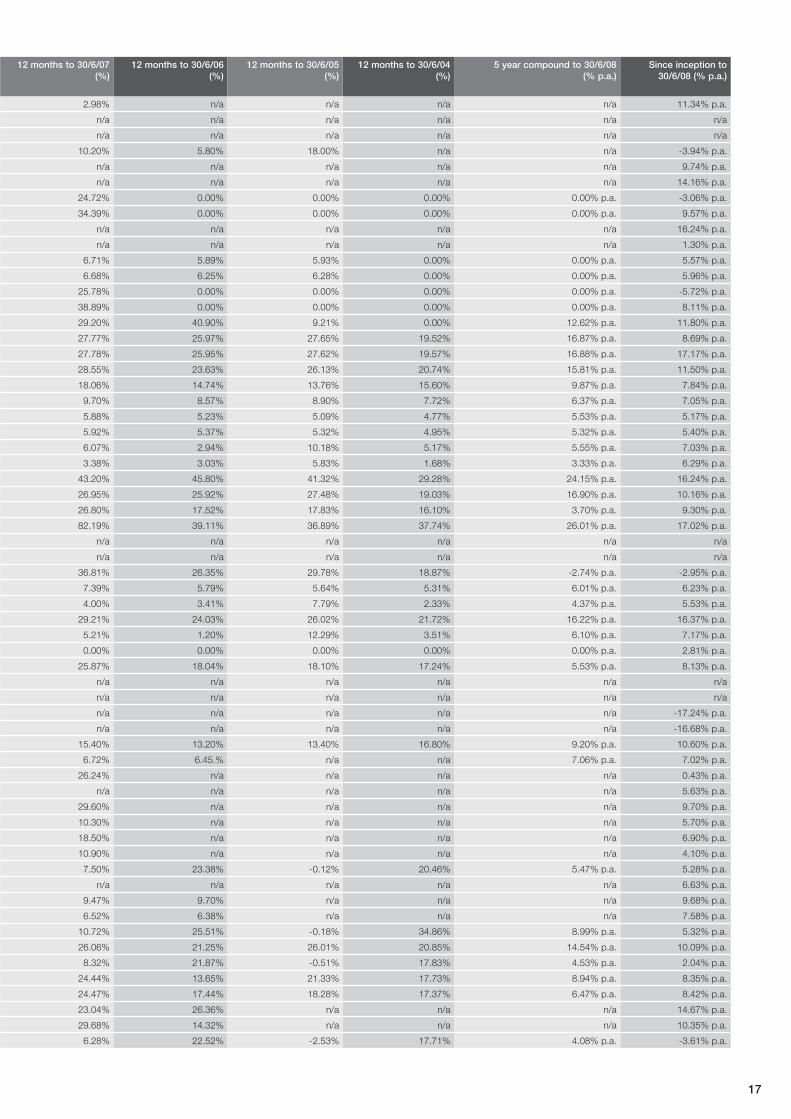

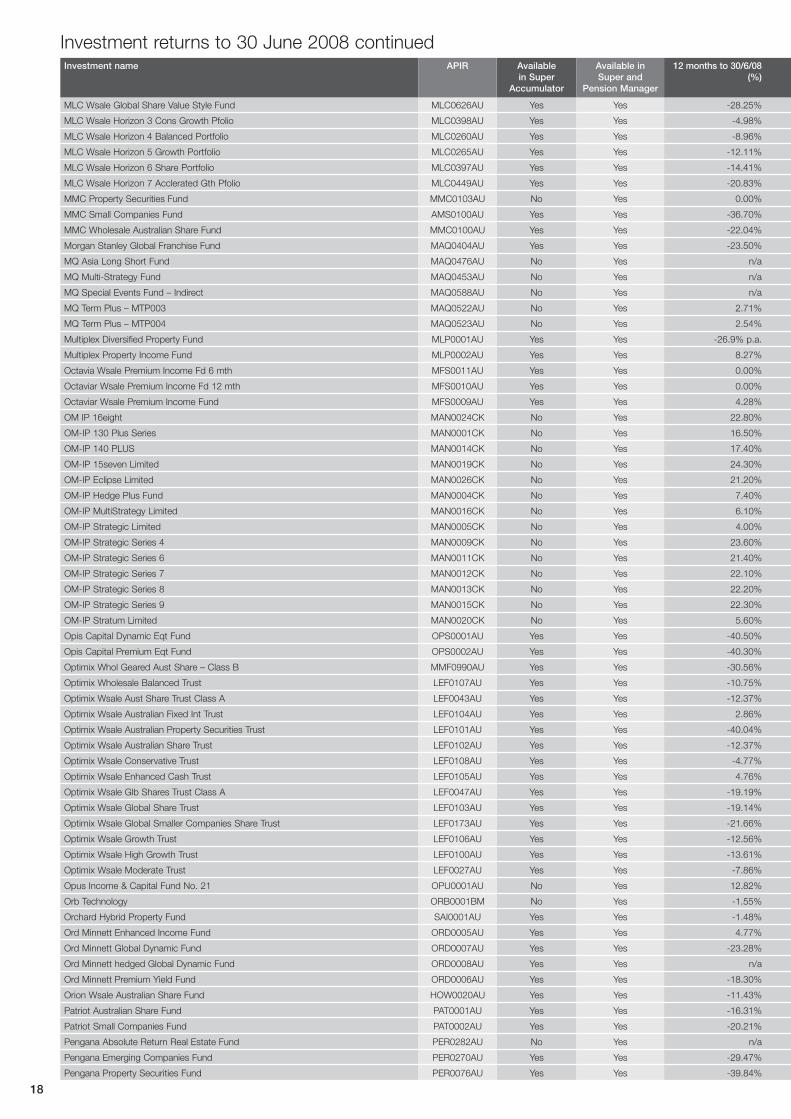

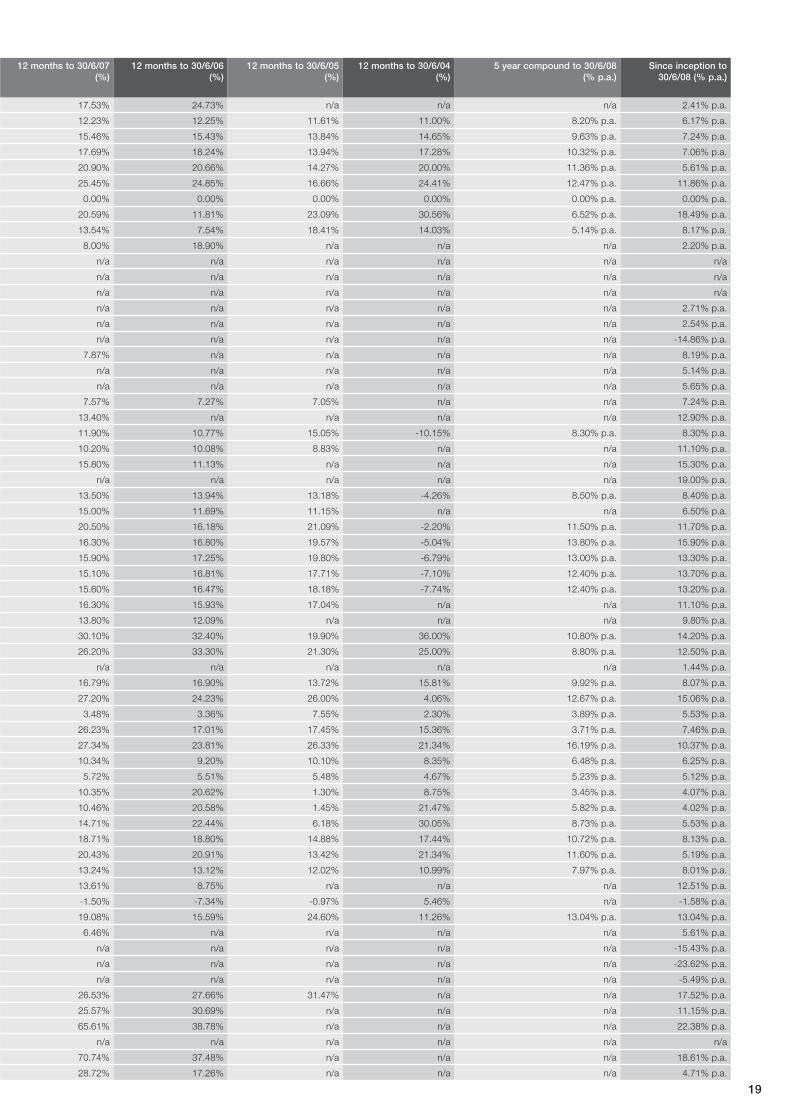

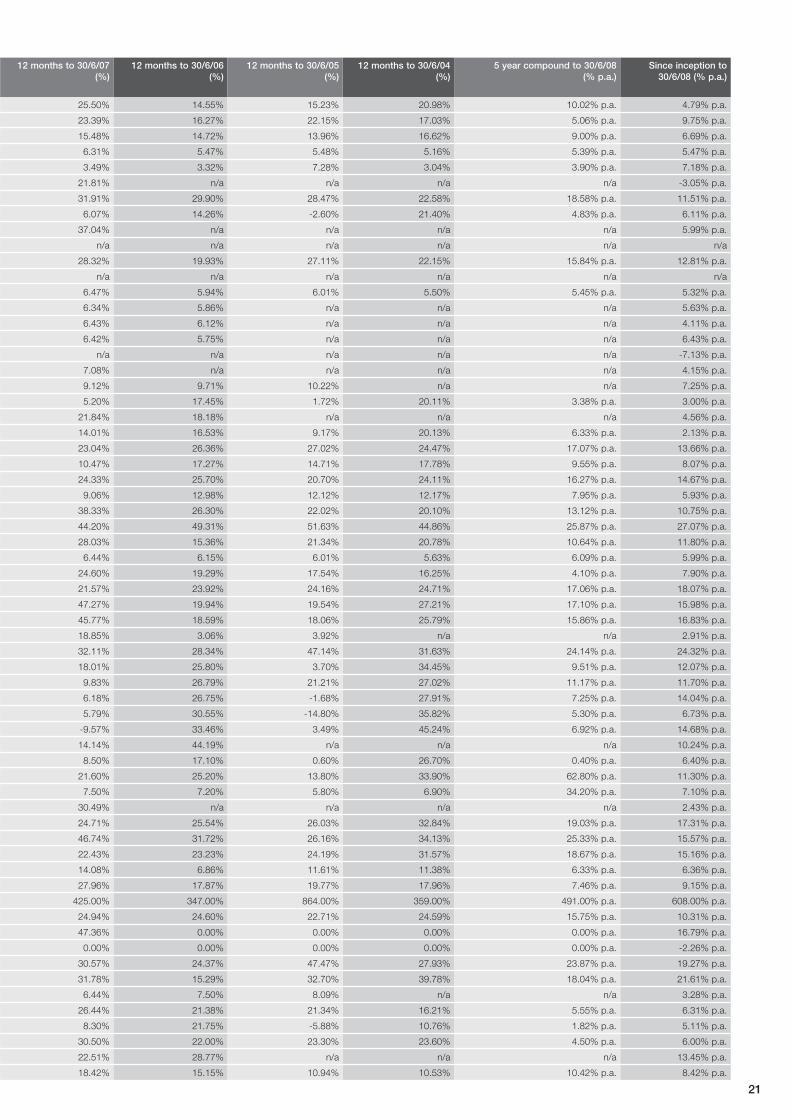

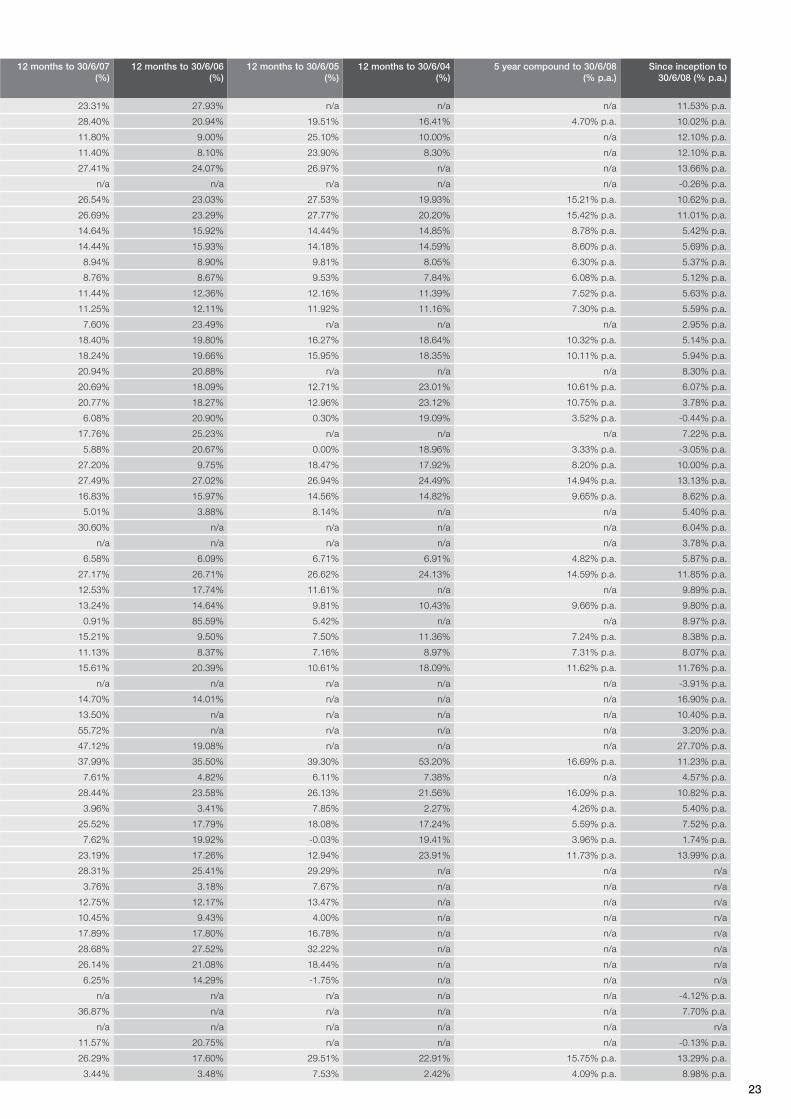

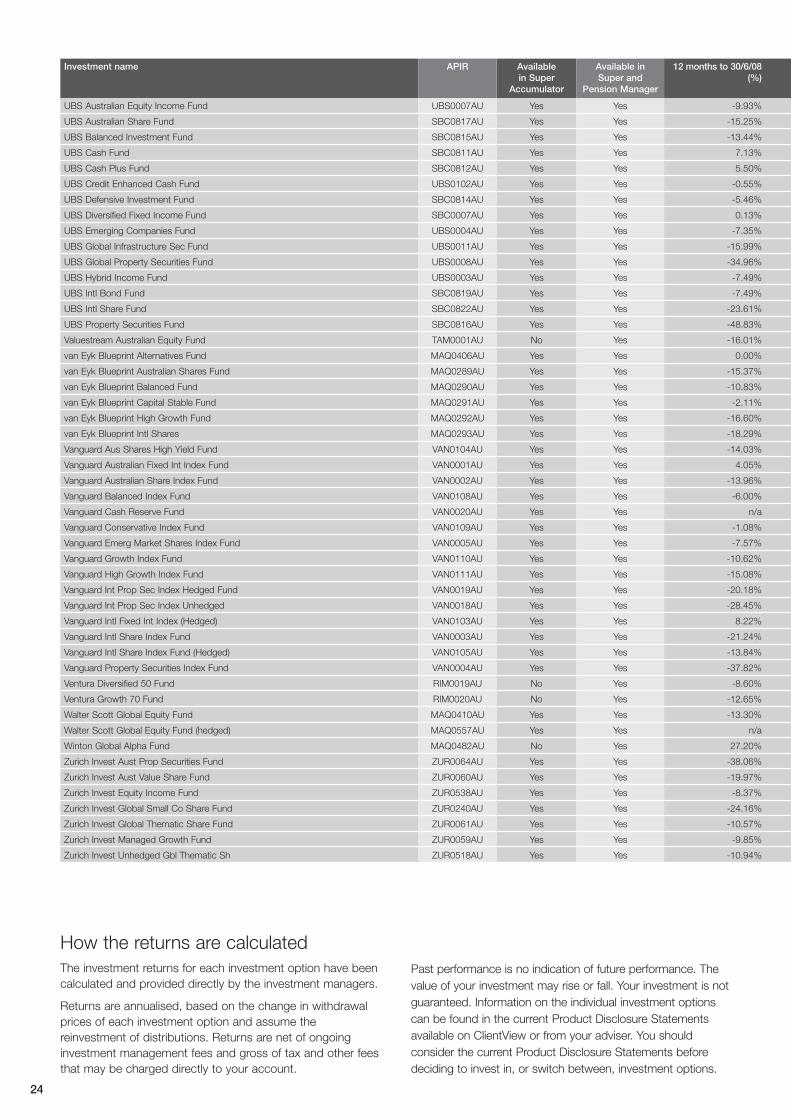

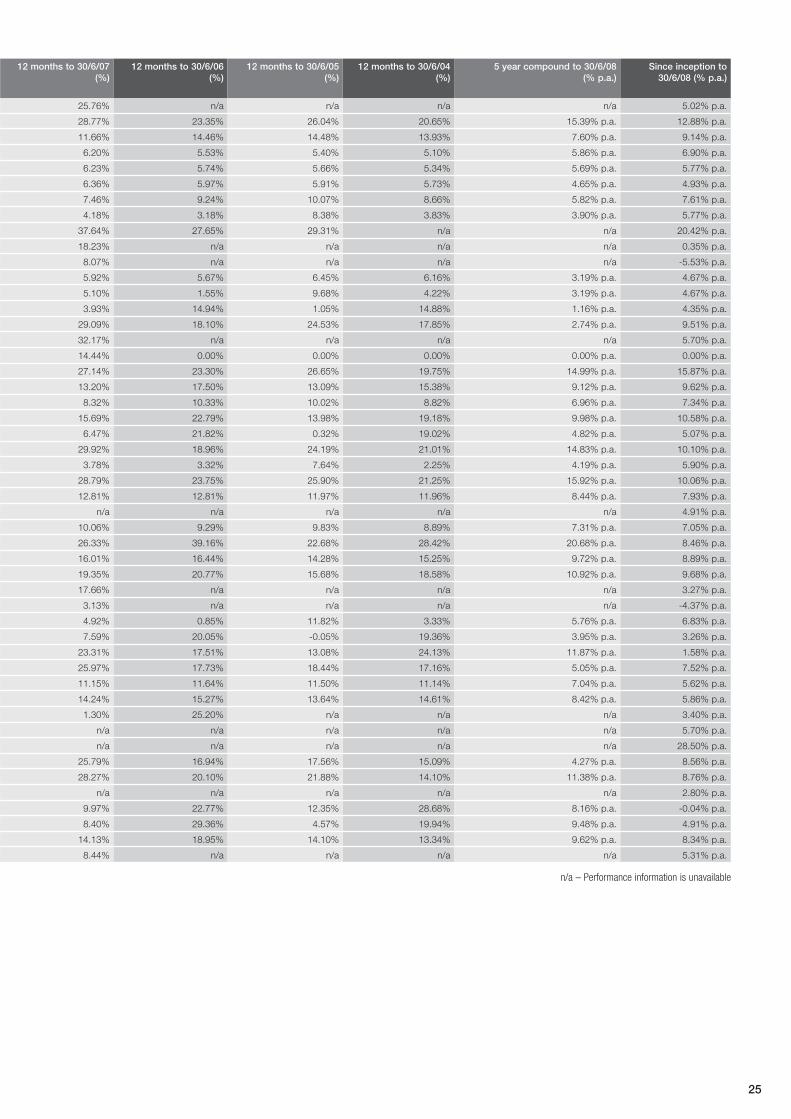

Investment returns to 30 June 2008

Investment name APIR Available in Super

Accumulator

Available in Super and

Pension Manager

12 months to 30/6/08 (%)

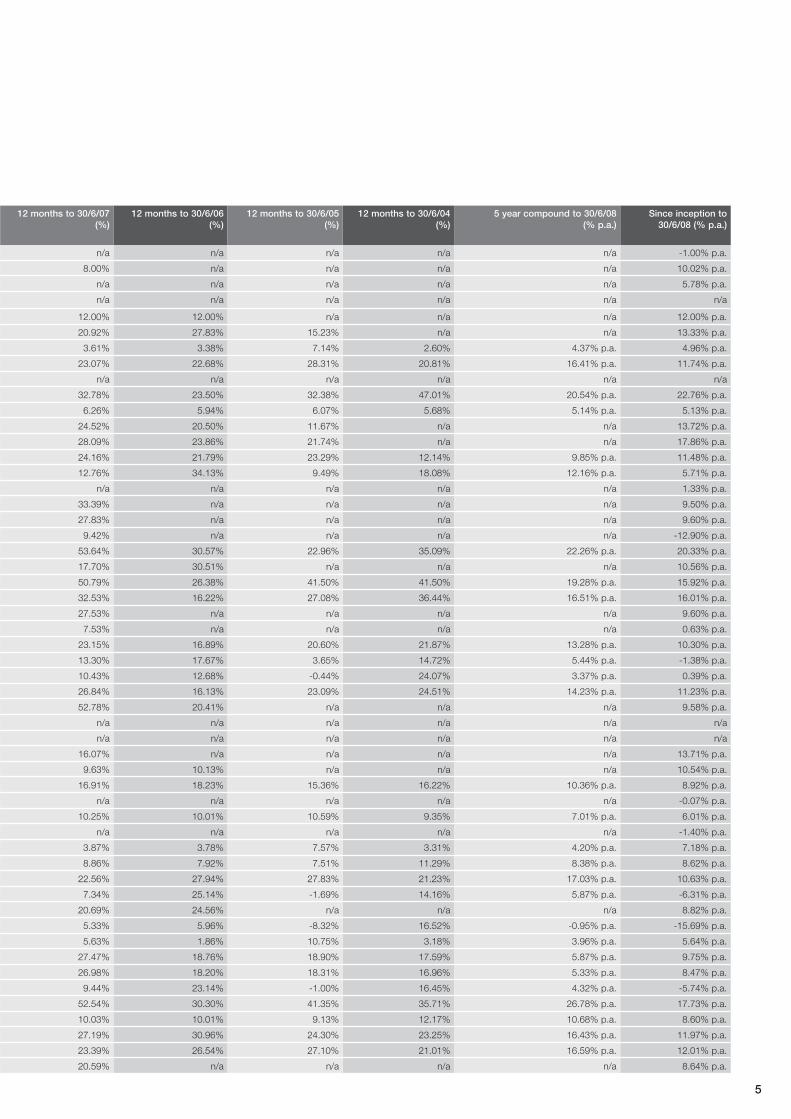

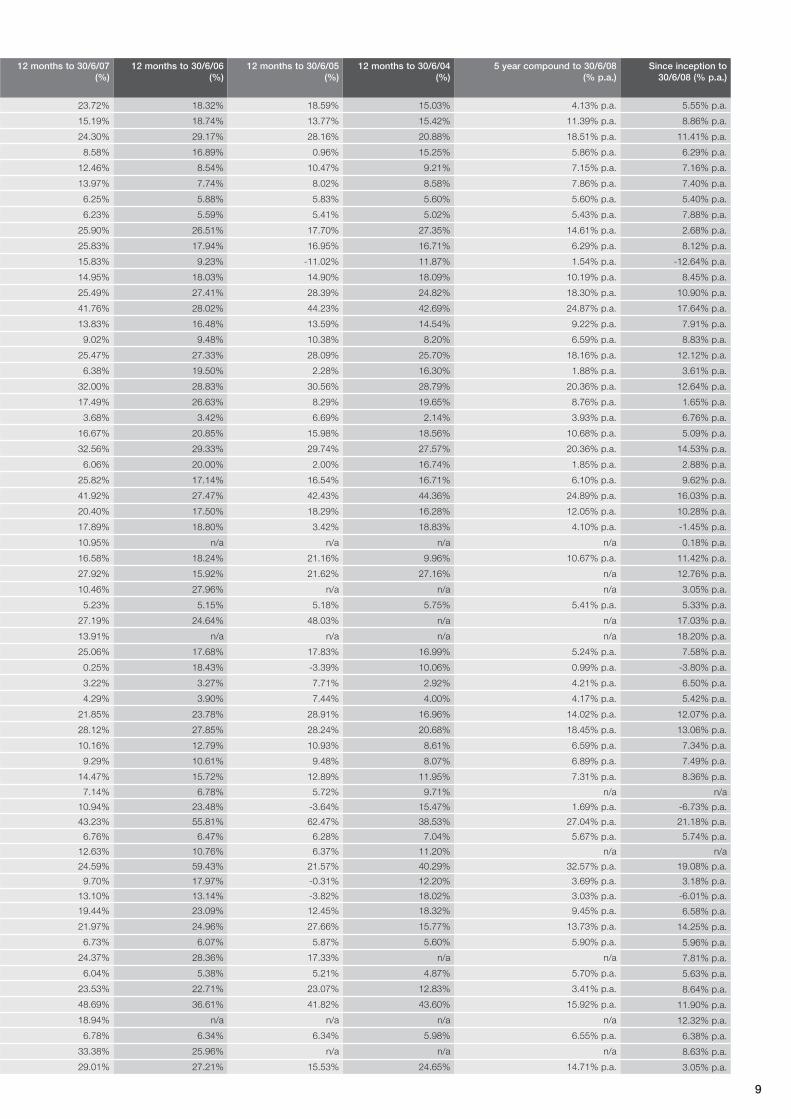

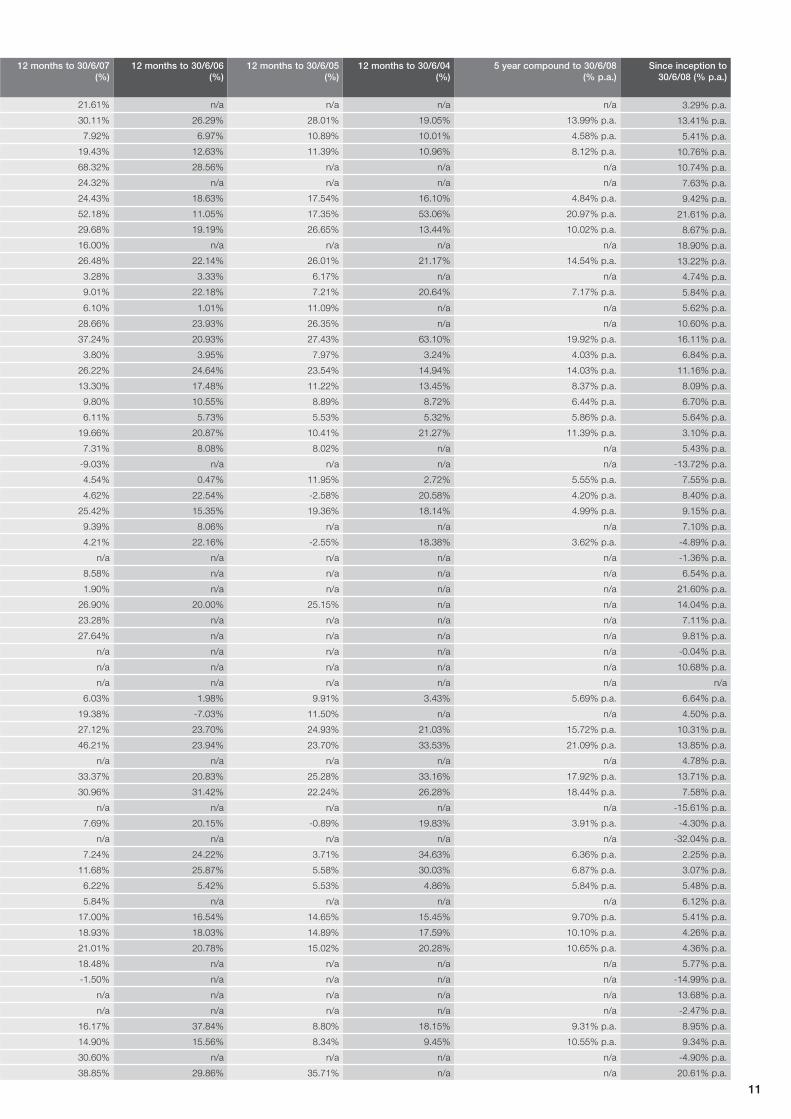

12 months to 30/6/07 (%)

12 months to 30/6/06 (%)

12 months to 30/6/05 (%)

12 months to 30/6/04 (%)

5 year compound to 30/6/08 (% p.a.)

Since inception to 30/6/08 (% p.a.)

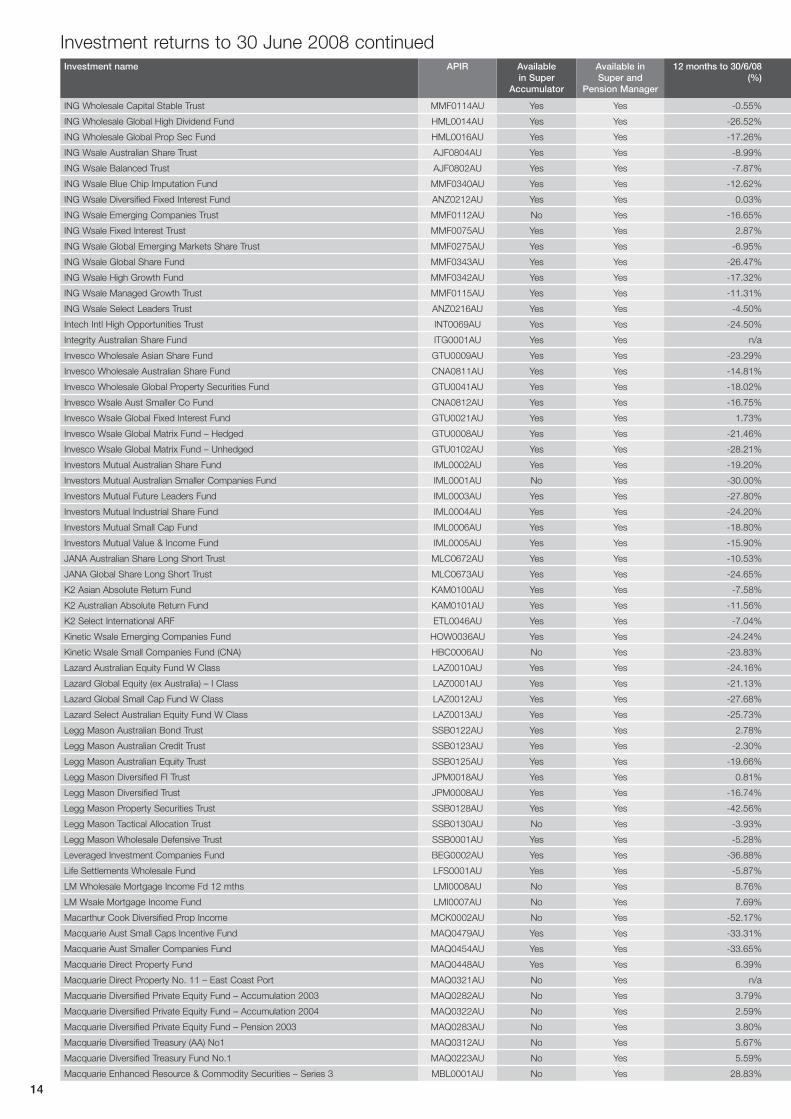

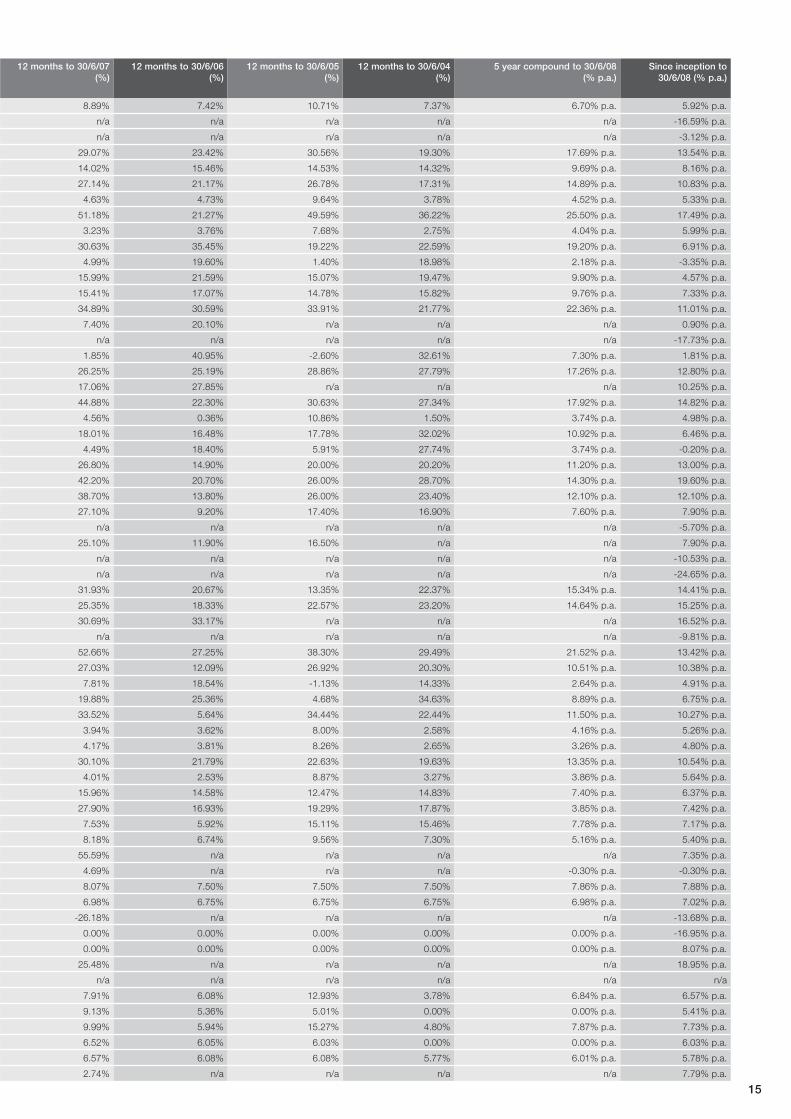

Abacus Diversified Income Fund II ABA0008AU Yes Yes -1.00% n/a n/a n/a n/a n/a -1.00% p.a.

Abacus Hospitality Fund ABA0005AU Yes Yes 12.04% 8.00% n/a n/a n/a n/a 10.02% p.a.

Abacus Retirement Living Trust ABACUSRET No Yes 17.14% n/a n/a n/a n/a n/a 5.78% p.a.

Abacus Wodonga Land ABACUSWOD No Yes n/a n/a n/a n/a n/a n/a n/a

Abacus Wodonga Mortgage Fund ABACUSMOR No Yes 12.00% 12.00% 12.00% n/a n/a n/a 12.00% p.a.

Aberdeen Asian Opportunities Fund EQI0028AU Yes Yes -13.30% 20.92% 27.83% 15.23% n/a n/a 13.33% p.a.

Aberdeen Australian Bond Fund MGL0103AU Yes Yes 1.44% 3.61% 3.38% 7.14% 2.60% 4.37% p.a. 4.96% p.a.

Aberdeen Australian Equities Fund MGL0114AU Yes Yes -8.66% 23.07% 22.68% 28.31% 20.81% 16.41% p.a. 11.74% p.a.

Aberdeen Australian Shares Fund EQI0017AU No Yes n/a n/a n/a n/a n/a n/a n/a

Aberdeen Australian Small Companies Fund MGL0001AU Yes Yes -20.27% 32.78% 23.50% 32.38% 47.01% 20.54% p.a. 22.76% p.a.

Aberdeen Cash Plus Fund MGL0101AU Yes Yes 1.81% 6.26% 5.94% 6.07% 5.68% 5.14% p.a. 5.13% p.a.

Aberdeen China Opportunities Fund ETL0031AU Yes Yes -7.76% 24.52% 20.50% 11.67% n/a n/a 13.72% p.a.

Aberdeen Emerging Opportunities Fund ETL0032AU Yes Yes -5.82% 28.09% 23.86% 21.74% n/a n/a 17.86% p.a.

Aberdeen Financials Fund EQI0027AU Yes Yes -26.74% 24.16% 21.79% 23.29% 12.14% 9.85% p.a. 11.48% p.a.

Aberdeen Intl Equity Fund EQI0015AU No Yes -13.84% 12.76% 34.13% 9.49% 18.08% 12.16% p.a. 5.71% p.a.

Absolute Capital Yield Strategies Fund ABS0011AU No Yes -26.54% n/a n/a n/a n/a n/a 1.33% p.a.

Acadian Aust Equity Long Short Fund FSF0789AU Yes Yes -12.58% 33.39% n/a n/a n/a n/a 9.50% p.a.

Acadian Wholesale Australian Equity Fund FSF0787AU Yes Yes -13.29% 27.83% n/a n/a n/a n/a 9.60% p.a.

Acadian Wsale Gbl Equity Long Short Fund FSF0788AU Yes Yes -32.02% 9.42% n/a n/a n/a n/a -12.90% p.a.

Acorn Capital Wsale Microcap Trust AUS0108AU Yes Yes -18.04% 53.64% 30.57% 22.96% 35.09% 22.26% p.a. 20.33% p.a.

Advance Asian Equity Fund – Wholesale Units ADV0083AU Yes Yes -19.77% 17.70% 30.51% n/a n/a n/a 10.56% p.a.

Advance Aust Geared Equity Fund Wsale ADV0078AU Yes Yes -36.72% 50.79% 26.38% 41.50% 41.50% 19.28% p.a. 15.92% p.a.

Advance Aust Smaller Companies W/sale Fund ADV0075AU No Yes -19.60% 32.53% 16.22% 27.08% 36.44% 16.51% p.a. 16.01% p.a.

Advance Concentrated Aust Share W/sale Fund ADV0115AU Yes Yes -13.97% 27.53% n/a n/a n/a n/a 9.60% p.a.

Advance Global Alpha Fund ADV0117AU No Yes -18.71% 7.53% n/a n/a n/a n/a 0.63% p.a.

Advance Imputation Fund – Wsale Units ADV0046AU Yes Yes -11.85% 23.15% 16.89% 20.60% 21.87% 13.28% p.a. 10.30% p.a.

Advance Int Shares Multi-Blend W/sale Fund ADV0053AU Yes Yes -17.77% 13.30% 17.67% 3.65% 14.72% 5.44% p.a. -1.38% p.a.

Advance Intl Sharemarket Fund – Wsale ADV0047AU Yes Yes -23.22% 10.43% 12.68% -0.44% 24.07% 3.37% p.a. 0.39% p.a.

Advance Sharemarket Fund Wholesale ADV0066AU No Yes -13.84% 26.84% 16.13% 23.09% 24.51% 14.23% p.a. 11.23% p.a.

Advance Smaller Co Multi-Blended W/sale Fund ADV0096AU Yes Yes -24.18% 52.78% 20.41% n/a n/a n/a 9.58% p.a.

All Star IAM Australian Share Fund VEN0006AU Yes Yes -8.58% n/a n/a n/a n/a n/a n/a

All Star Income Fund VEN0007AU Yes Yes -6.81% n/a n/a n/a n/a n/a n/a

Alpha Strategic Fund – B Class units TOL0055AU No Yes 8.84% 16.07% n/a n/a n/a n/a 13.71% p.a.

AMP Cap Structured High Yield Class A AMP1014AU Yes Yes 11.78% 9.63% 10.13% n/a n/a n/a 10.54% p.a.

AMP Capital Balanced Growth Trust – Class A Units AMP0441AU Yes Yes -11.64% 16.91% 18.23% 15.36% 16.22% 10.36% p.a. 8.92% p.a.

AMP Capital China Fund 2 AMP1009AU No Yes n/a n/a n/a n/a n/a n/a -0.07% p.a.

AMP Capital Conservative Fund Class A AMP0443AU Yes Yes -4.31% 10.25% 10.01% 10.59% 9.35% 7.01% p.a. 6.01% p.a.

AMP Capital Core Infrastructure Class A AMP1179AU Yes Yes n/a n/a n/a n/a n/a n/a -1.40% p.a.

AMP Capital Core Plus Strategies Fund AMP0279AU No Yes 2.55% 3.87% 3.78% 7.57% 3.31% 4.20% p.a. 7.18% p.a.

AMP Capital Enhanced Yield Fund – Class A AMP0685AU Yes Yes 6.37% 8.86% 7.92% 7.51% 11.29% 8.38% p.a. 8.62% p.a.

AMP Capital Equity Fund – Class A Units AMP0370AU Yes Yes -9.65% 22.56% 27.94% 27.83% 21.23% 17.03% p.a. 10.63% p.a.

AMP Capital Global Growth Opport Fund – Class A AMP0369AU No Yes -11.77% 7.34% 25.14% -1.69% 14.16% 5.87% p.a. -6.31% p.a.

AMP Capital Global Property Securities Fund Class A AMP0974AU Yes Yes -22.02% 20.69% 24.56% n/a n/a n/a 8.82% p.a.

AMP Capital Global Technology Fund Class A AMP0365AU No Yes -20.01% 5.33% 5.96% -8.32% 16.52% -0.95% p.a. -15.69% p.a.

AMP Capital Intl Bond Fund Class A Units AMP0254AU Yes Yes -1.25% 5.63% 1.86% 10.75% 3.18% 3.96% p.a. 5.64% p.a.

AMP Capital Listed Property Fund – Ord Class AMP0269AU No Yes -37.17% 27.47% 18.76% 18.90% 17.59% 5.87% p.a. 9.75% p.a.

AMP Capital Listed Property Trusts – Class A AMP0255AU Yes Yes -37.56% 26.98% 18.20% 18.31% 16.96% 5.33% p.a. 8.47% p.a.

AMP Capital Res Inv Lead Intl Sh-Class A AMP0455AU Yes Yes -20.47% 9.44% 23.14% -1.00% 16.45% 4.32% p.a. -5.74% p.a.

AMP Capital Small Companies Fund – Class A AMP0446AU Yes Yes -14.10% 52.54% 30.30% 41.35% 35.71% 26.78% p.a. 17.73% p.a.

AMP Capital Structured High Yield – Ord Class WID2 No Yes 12.11% 10.03% 10.01% 9.13% 12.17% 10.68% p.a. 8.60% p.a.

AMP Capital Sustainable Future Aust Share Class A AMP0449AU Yes Yes -16.16% 27.19% 30.96% 24.30% 23.25% 16.43% p.a. 11.97% p.a.

AMP Capital Wholesale Australian Share Fund – Class A AMP0258AU Yes Yes -10.31% 23.39% 26.54% 27.10% 21.01% 16.59% p.a. 12.01% p.a.

AMP Core Property Fund (Class A) AMP1015AU Yes Yes -9.97% 20.59% n/a n/a n/a n/a 8.64% p.a.

5

Investment name APIR Available in Super

Accumulator

Available in Super and

Pension Manager

12 months to 30/6/08 (%)

12 months to 30/6/07 (%)

12 months to 30/6/06 (%)

12 months to 30/6/05 (%)

12 months to 30/6/04 (%)

5 year compound to 30/6/08 (% p.a.)

Since inception to 30/6/08 (% p.a.)

Abacus Diversified Income Fund II ABA0008AU Yes Yes -1.00% n/a n/a n/a n/a n/a -1.00% p.a.

Abacus Hospitality Fund ABA0005AU Yes Yes 12.04% 8.00% n/a n/a n/a n/a 10.02% p.a.

Abacus Retirement Living Trust ABACUSRET No Yes 17.14% n/a n/a n/a n/a n/a 5.78% p.a.

Abacus Wodonga Land ABACUSWOD No Yes n/a n/a n/a n/a n/a n/a n/a

Abacus Wodonga Mortgage Fund ABACUSMOR No Yes 12.00% 12.00% 12.00% n/a n/a n/a 12.00% p.a.

Aberdeen Asian Opportunities Fund EQI0028AU Yes Yes -13.30% 20.92% 27.83% 15.23% n/a n/a 13.33% p.a.

Aberdeen Australian Bond Fund MGL0103AU Yes Yes 1.44% 3.61% 3.38% 7.14% 2.60% 4.37% p.a. 4.96% p.a.

Aberdeen Australian Equities Fund MGL0114AU Yes Yes -8.66% 23.07% 22.68% 28.31% 20.81% 16.41% p.a. 11.74% p.a.

Aberdeen Australian Shares Fund EQI0017AU No Yes n/a n/a n/a n/a n/a n/a n/a

Aberdeen Australian Small Companies Fund MGL0001AU Yes Yes -20.27% 32.78% 23.50% 32.38% 47.01% 20.54% p.a. 22.76% p.a.

Aberdeen Cash Plus Fund MGL0101AU Yes Yes 1.81% 6.26% 5.94% 6.07% 5.68% 5.14% p.a. 5.13% p.a.

Aberdeen China Opportunities Fund ETL0031AU Yes Yes -7.76% 24.52% 20.50% 11.67% n/a n/a 13.72% p.a.

Aberdeen Emerging Opportunities Fund ETL0032AU Yes Yes -5.82% 28.09% 23.86% 21.74% n/a n/a 17.86% p.a.

Aberdeen Financials Fund EQI0027AU Yes Yes -26.74% 24.16% 21.79% 23.29% 12.14% 9.85% p.a. 11.48% p.a.

Aberdeen Intl Equity Fund EQI0015AU No Yes -13.84% 12.76% 34.13% 9.49% 18.08% 12.16% p.a. 5.71% p.a.

Absolute Capital Yield Strategies Fund ABS0011AU No Yes -26.54% n/a n/a n/a n/a n/a 1.33% p.a.

Acadian Aust Equity Long Short Fund FSF0789AU Yes Yes -12.58% 33.39% n/a n/a n/a n/a 9.50% p.a.

Acadian Wholesale Australian Equity Fund FSF0787AU Yes Yes -13.29% 27.83% n/a n/a n/a n/a 9.60% p.a.

Acadian Wsale Gbl Equity Long Short Fund FSF0788AU Yes Yes -32.02% 9.42% n/a n/a n/a n/a -12.90% p.a.

Acorn Capital Wsale Microcap Trust AUS0108AU Yes Yes -18.04% 53.64% 30.57% 22.96% 35.09% 22.26% p.a. 20.33% p.a.

Advance Asian Equity Fund – Wholesale Units ADV0083AU Yes Yes -19.77% 17.70% 30.51% n/a n/a n/a 10.56% p.a.

Advance Aust Geared Equity Fund Wsale ADV0078AU Yes Yes -36.72% 50.79% 26.38% 41.50% 41.50% 19.28% p.a. 15.92% p.a.

Advance Aust Smaller Companies W/sale Fund ADV0075AU No Yes -19.60% 32.53% 16.22% 27.08% 36.44% 16.51% p.a. 16.01% p.a.

Advance Concentrated Aust Share W/sale Fund ADV0115AU Yes Yes -13.97% 27.53% n/a n/a n/a n/a 9.60% p.a.

Advance Global Alpha Fund ADV0117AU No Yes -18.71% 7.53% n/a n/a n/a n/a 0.63% p.a.

Advance Imputation Fund – Wsale Units ADV0046AU Yes Yes -11.85% 23.15% 16.89% 20.60% 21.87% 13.28% p.a. 10.30% p.a.

Advance Int Shares Multi-Blend W/sale Fund ADV0053AU Yes Yes -17.77% 13.30% 17.67% 3.65% 14.72% 5.44% p.a. -1.38% p.a.

Advance Intl Sharemarket Fund – Wsale ADV0047AU Yes Yes -23.22% 10.43% 12.68% -0.44% 24.07% 3.37% p.a. 0.39% p.a.

Advance Sharemarket Fund Wholesale ADV0066AU No Yes -13.84% 26.84% 16.13% 23.09% 24.51% 14.23% p.a. 11.23% p.a.

Advance Smaller Co Multi-Blended W/sale Fund ADV0096AU Yes Yes -24.18% 52.78% 20.41% n/a n/a n/a 9.58% p.a.

All Star IAM Australian Share Fund VEN0006AU Yes Yes -8.58% n/a n/a n/a n/a n/a n/a

All Star Income Fund VEN0007AU Yes Yes -6.81% n/a n/a n/a n/a n/a n/a

Alpha Strategic Fund – B Class units TOL0055AU No Yes 8.84% 16.07% n/a n/a n/a n/a 13.71% p.a.

AMP Cap Structured High Yield Class A AMP1014AU Yes Yes 11.78% 9.63% 10.13% n/a n/a n/a 10.54% p.a.

AMP Capital Balanced Growth Trust – Class A Units AMP0441AU Yes Yes -11.64% 16.91% 18.23% 15.36% 16.22% 10.36% p.a. 8.92% p.a.

AMP Capital China Fund 2 AMP1009AU No Yes n/a n/a n/a n/a n/a n/a -0.07% p.a.

AMP Capital Conservative Fund Class A AMP0443AU Yes Yes -4.31% 10.25% 10.01% 10.59% 9.35% 7.01% p.a. 6.01% p.a.

AMP Capital Core Infrastructure Class A AMP1179AU Yes Yes n/a n/a n/a n/a n/a n/a -1.40% p.a.

AMP Capital Core Plus Strategies Fund AMP0279AU No Yes 2.55% 3.87% 3.78% 7.57% 3.31% 4.20% p.a. 7.18% p.a.

AMP Capital Enhanced Yield Fund – Class A AMP0685AU Yes Yes 6.37% 8.86% 7.92% 7.51% 11.29% 8.38% p.a. 8.62% p.a.

AMP Capital Equity Fund – Class A Units AMP0370AU Yes Yes -9.65% 22.56% 27.94% 27.83% 21.23% 17.03% p.a. 10.63% p.a.

AMP Capital Global Growth Opport Fund – Class A AMP0369AU No Yes -11.77% 7.34% 25.14% -1.69% 14.16% 5.87% p.a. -6.31% p.a.

AMP Capital Global Property Securities Fund Class A AMP0974AU Yes Yes -22.02% 20.69% 24.56% n/a n/a n/a 8.82% p.a.

AMP Capital Global Technology Fund Class A AMP0365AU No Yes -20.01% 5.33% 5.96% -8.32% 16.52% -0.95% p.a. -15.69% p.a.

AMP Capital Intl Bond Fund Class A Units AMP0254AU Yes Yes -1.25% 5.63% 1.86% 10.75% 3.18% 3.96% p.a. 5.64% p.a.

AMP Capital Listed Property Fund – Ord Class AMP0269AU No Yes -37.17% 27.47% 18.76% 18.90% 17.59% 5.87% p.a. 9.75% p.a.

AMP Capital Listed Property Trusts – Class A AMP0255AU Yes Yes -37.56% 26.98% 18.20% 18.31% 16.96% 5.33% p.a. 8.47% p.a.

AMP Capital Res Inv Lead Intl Sh-Class A AMP0455AU Yes Yes -20.47% 9.44% 23.14% -1.00% 16.45% 4.32% p.a. -5.74% p.a.

AMP Capital Small Companies Fund – Class A AMP0446AU Yes Yes -14.10% 52.54% 30.30% 41.35% 35.71% 26.78% p.a. 17.73% p.a.

AMP Capital Structured High Yield – Ord Class WID2 No Yes 12.11% 10.03% 10.01% 9.13% 12.17% 10.68% p.a. 8.60% p.a.

AMP Capital Sustainable Future Aust Share Class A AMP0449AU Yes Yes -16.16% 27.19% 30.96% 24.30% 23.25% 16.43% p.a. 11.97% p.a.

AMP Capital Wholesale Australian Share Fund – Class A AMP0258AU Yes Yes -10.31% 23.39% 26.54% 27.10% 21.01% 16.59% p.a. 12.01% p.a.

AMP Core Property Fund (Class A) AMP1015AU Yes Yes -9.97% 20.59% n/a n/a n/a n/a 8.64% p.a.

6

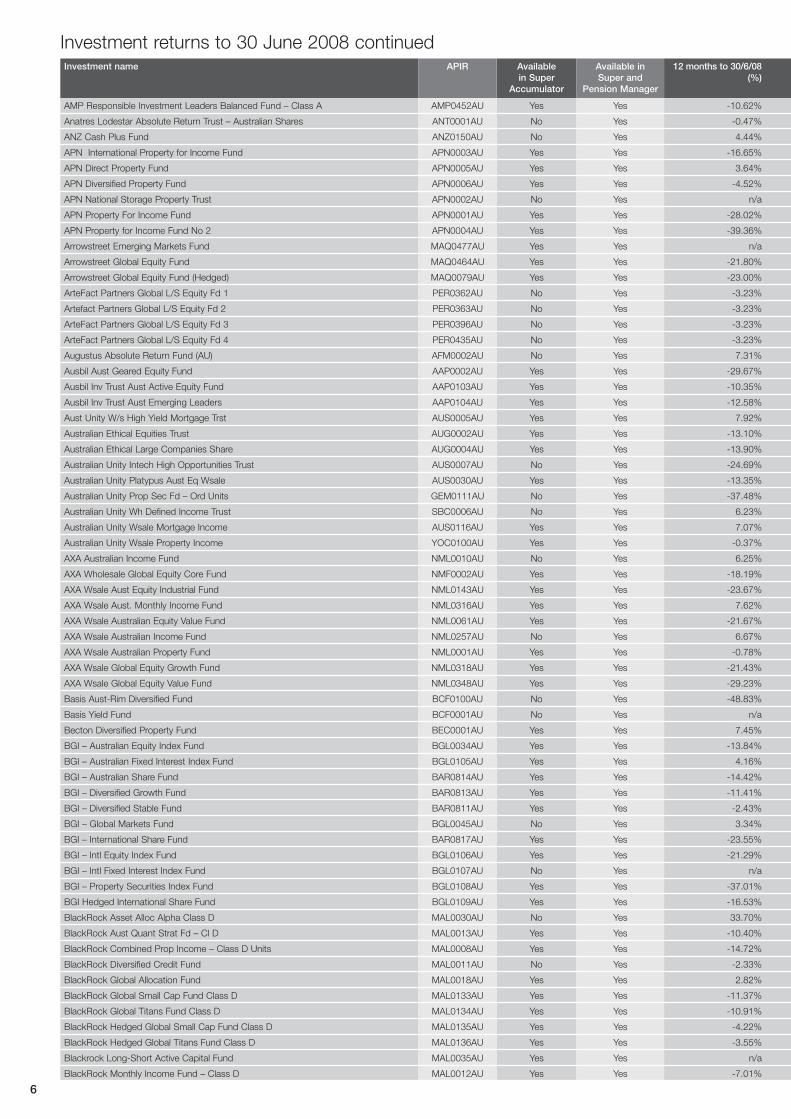

Investment returns to 30 June 2008 continuedInvestment name APIR Available

in Super Accumulator

Available in Super and

Pension Manager

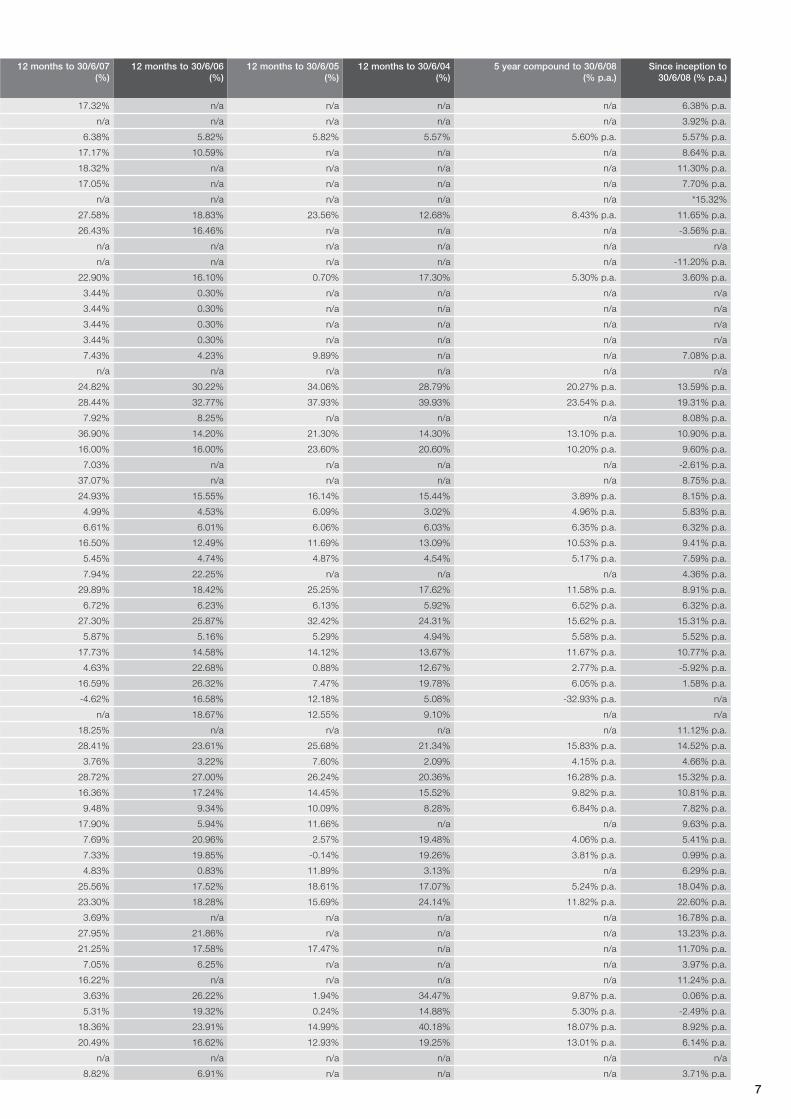

12 months to 30/6/08 (%)

12 months to 30/6/07 (%)

12 months to 30/6/06 (%)

12 months to 30/6/05 (%)

12 months to 30/6/04 (%)

5 year compound to 30/6/08 (% p.a.)

Since inception to 30/6/08 (% p.a.)

AMP Responsible Investment Leaders Balanced Fund – Class A AMP0452AU Yes Yes -10.62% 17.32% n/a n/a n/a n/a 6.38% p.a.

Anatres Lodestar Absolute Return Trust – Australian Shares ANT0001AU No Yes -0.47% n/a n/a n/a n/a n/a 3.92% p.a.

ANZ Cash Plus Fund ANZ0150AU No Yes 4.44% 6.38% 5.82% 5.82% 5.57% 5.60% p.a. 5.57% p.a.

APN International Property for Income Fund APN0003AU Yes Yes -16.65% 17.17% 10.59% n/a n/a n/a 8.64% p.a.

APN Direct Property Fund APN0005AU Yes Yes 3.64% 18.32% n/a n/a n/a n/a 11.30% p.a.

APN Diversified Property Fund APN0006AU Yes Yes -4.52% 17.05% n/a n/a n/a n/a 7.70% p.a.

APN National Storage Property Trust APN0002AU No Yes n/a n/a n/a n/a n/a n/a *15.32%

APN Property For Income Fund APN0001AU Yes Yes -28.02% 27.58% 18.83% 23.56% 12.68% 8.43% p.a. 11.65% p.a.

APN Property for Income Fund No 2 APN0004AU Yes Yes -39.36% 26.43% 16.46% n/a n/a n/a -3.56% p.a.

Arrowstreet Emerging Markets Fund MAQ0477AU Yes Yes n/a n/a n/a n/a n/a n/a n/a

Arrowstreet Global Equity Fund MAQ0464AU Yes Yes -21.80% n/a n/a n/a n/a n/a -11.20% p.a.

Arrowstreet Global Equity Fund (Hedged) MAQ0079AU Yes Yes -23.00% 22.90% 16.10% 0.70% 17.30% 5.30% p.a. 3.60% p.a.

ArteFact Partners Global L/S Equity Fd 1 PER0362AU No Yes -3.23% 3.44% 0.30% n/a n/a n/a n/a

Artefact Partners Global L/S Equity Fd 2 PER0363AU No Yes -3.23% 3.44% 0.30% n/a n/a n/a n/a

ArteFact Partners Global L/S Equity Fd 3 PER0396AU No Yes -3.23% 3.44% 0.30% n/a n/a n/a n/a

ArteFact Partners Global L/S Equity Fd 4 PER0435AU No Yes -3.23% 3.44% 0.30% n/a n/a n/a n/a

Augustus Absolute Return Fund (AU) AFM0002AU No Yes 7.31% 7.43% 4.23% 9.89% n/a n/a 7.08% p.a.

Ausbil Aust Geared Equity Fund AAP0002AU Yes Yes -29.67% n/a n/a n/a n/a n/a n/a

Ausbil Inv Trust Aust Active Equity Fund AAP0103AU Yes Yes -10.35% 24.82% 30.22% 34.06% 28.79% 20.27% p.a. 13.59% p.a.

Ausbil Inv Trust Aust Emerging Leaders AAP0104AU Yes Yes -12.58% 28.44% 32.77% 37.93% 39.93% 23.54% p.a. 19.31% p.a.

Aust Unity W/s High Yield Mortgage Trst AUS0005AU Yes Yes 7.92% 7.92% 8.25% n/a n/a n/a 8.08% p.a.

Australian Ethical Equities Trust AUG0002AU Yes Yes -13.10% 36.90% 14.20% 21.30% 14.30% 13.10% p.a. 10.90% p.a.

Australian Ethical Large Companies Share AUG0004AU Yes Yes -13.90% 16.00% 16.00% 23.60% 20.60% 10.20% p.a. 9.60% p.a.

Australian Unity Intech High Opportunities Trust AUS0007AU No Yes -24.69% 7.03% n/a n/a n/a n/a -2.61% p.a.

Australian Unity Platypus Aust Eq Wsale AUS0030AU Yes Yes -13.35% 37.07% n/a n/a n/a n/a 8.75% p.a.

Australian Unity Prop Sec Fd – Ord Units GEM0111AU No Yes -37.48% 24.93% 15.55% 16.14% 15.44% 3.89% p.a. 8.15% p.a.

Australian Unity Wh Defined Income Trust SBC0006AU No Yes 6.23% 4.99% 4.53% 6.09% 3.02% 4.96% p.a. 5.83% p.a.

Australian Unity Wsale Mortgage Income AUS0116AU Yes Yes 7.07% 6.61% 6.01% 6.06% 6.03% 6.35% p.a. 6.32% p.a.

Australian Unity Wsale Property Income YOC0100AU Yes Yes -0.37% 16.50% 12.49% 11.69% 13.09% 10.53% p.a. 9.41% p.a.

AXA Australian Income Fund NML0010AU No Yes 6.25% 5.45% 4.74% 4.87% 4.54% 5.17% p.a. 7.59% p.a.

AXA Wholesale Global Equity Core Fund NMF0002AU Yes Yes -18.19% 7.94% 22.25% n/a n/a n/a 4.36% p.a.

AXA Wsale Aust Equity Industrial Fund NML0143AU Yes Yes -23.67% 29.89% 18.42% 25.25% 17.62% 11.58% p.a. 8.91% p.a.

AXA Wsale Aust. Monthly Income Fund NML0316AU Yes Yes 7.62% 6.72% 6.23% 6.13% 5.92% 6.52% p.a. 6.32% p.a.

AXA Wsale Australian Equity Value Fund NML0061AU Yes Yes -21.67% 27.30% 25.87% 32.42% 24.31% 15.62% p.a. 15.31% p.a.

AXA Wsale Australian Income Fund NML0257AU No Yes 6.67% 5.87% 5.16% 5.29% 4.94% 5.58% p.a. 5.52% p.a.

AXA Wsale Australian Property Fund NML0001AU Yes Yes -0.78% 17.73% 14.58% 14.12% 13.67% 11.67% p.a. 10.77% p.a.

AXA Wsale Global Equity Growth Fund NML0318AU Yes Yes -21.43% 4.63% 22.68% 0.88% 12.67% 2.77% p.a. -5.92% p.a.

AXA Wsale Global Equity Value Fund NML0348AU Yes Yes -29.23% 16.59% 26.32% 7.47% 19.78% 6.05% p.a. 1.58% p.a.

Basis Aust-Rim Diversified Fund BCF0100AU No Yes -48.83% -4.62% 16.58% 12.18% 5.08% -32.93% p.a. n/a

Basis Yield Fund BCF0001AU No Yes n/a n/a 18.67% 12.55% 9.10% n/a n/a

Becton Diversified Property Fund BEC0001AU Yes Yes 7.45% 18.25% n/a n/a n/a n/a 11.12% p.a.

BGI – Australian Equity Index Fund BGL0034AU Yes Yes -13.84% 28.41% 23.61% 25.68% 21.34% 15.83% p.a. 14.52% p.a.

BGI – Australian Fixed Interest Index Fund BGL0105AU Yes Yes 4.16% 3.76% 3.22% 7.60% 2.09% 4.15% p.a. 4.66% p.a.

BGI – Australian Share Fund BAR0814AU Yes Yes -14.42% 28.72% 27.00% 26.24% 20.36% 16.28% p.a. 15.32% p.a.

BGI – Diversified Growth Fund BAR0813AU Yes Yes -11.41% 16.36% 17.24% 14.45% 15.52% 9.82% p.a. 10.81% p.a.

BGI – Diversified Stable Fund BAR0811AU Yes Yes -2.43% 9.48% 9.34% 10.09% 8.28% 6.84% p.a. 7.82% p.a.

BGI – Global Markets Fund BGL0045AU No Yes 3.34% 17.90% 5.94% 11.66% n/a n/a 9.63% p.a.

BGI – International Share Fund BAR0817AU Yes Yes -23.55% 7.69% 20.96% 2.57% 19.48% 4.06% p.a. 5.41% p.a.

BGI – Intl Equity Index Fund BGL0106AU Yes Yes -21.29% 7.33% 19.85% -0.14% 19.26% 3.81% p.a. 0.99% p.a.

BGI – Intl Fixed Interest Index Fund BGL0107AU No Yes n/a 4.83% 0.83% 11.89% 3.13% n/a 6.29% p.a.

BGI – Property Securities Index Fund BGL0108AU Yes Yes -37.01% 25.56% 17.52% 18.61% 17.07% 5.24% p.a. 18.04% p.a.

BGI Hedged International Share Fund BGL0109AU Yes Yes -16.53% 23.30% 18.28% 15.69% 24.14% 11.82% p.a. 22.60% p.a.

BlackRock Asset Alloc Alpha Class D MAL0030AU No Yes 33.70% 3.69% n/a n/a n/a n/a 16.78% p.a.

BlackRock Aust Quant Strat Fd – Cl D MAL0013AU Yes Yes -10.40% 27.95% 21.86% n/a n/a n/a 13.23% p.a.

BlackRock Combined Prop Income – Class D Units MAL0008AU Yes Yes -14.72% 21.25% 17.58% 17.47% n/a n/a 11.70% p.a.

BlackRock Diversified Credit Fund MAL0011AU No Yes -2.33% 7.05% 6.25% n/a n/a n/a 3.97% p.a.

BlackRock Global Allocation Fund MAL0018AU Yes Yes 2.82% 16.22% n/a n/a n/a n/a 11.24% p.a.

BlackRock Global Small Cap Fund Class D MAL0133AU Yes Yes -11.37% 3.63% 26.22% 1.94% 34.47% 9.87% p.a. 0.06% p.a.

BlackRock Global Titans Fund Class D MAL0134AU Yes Yes -10.91% 5.31% 19.32% 0.24% 14.88% 5.30% p.a. -2.49% p.a.

BlackRock Hedged Global Small Cap Fund Class D MAL0135AU Yes Yes -4.22% 18.36% 23.91% 14.99% 40.18% 18.07% p.a. 8.92% p.a.

BlackRock Hedged Global Titans Fund Class D MAL0136AU Yes Yes -3.55% 20.49% 16.62% 12.93% 19.25% 13.01% p.a. 6.14% p.a.

Blackrock Long-Short Active Capital Fund MAL0035AU Yes Yes n/a n/a n/a n/a n/a n/a n/a

BlackRock Monthly Income Fund – Class D MAL0012AU Yes Yes -7.01% 8.82% 6.91% n/a n/a n/a 3.71% p.a.

7

Investment name APIR Available in Super

Accumulator

Available in Super and

Pension Manager

12 months to 30/6/08 (%)

12 months to 30/6/07 (%)

12 months to 30/6/06 (%)

12 months to 30/6/05 (%)

12 months to 30/6/04 (%)

5 year compound to 30/6/08 (% p.a.)

Since inception to 30/6/08 (% p.a.)

AMP Responsible Investment Leaders Balanced Fund – Class A AMP0452AU Yes Yes -10.62% 17.32% n/a n/a n/a n/a 6.38% p.a.

Anatres Lodestar Absolute Return Trust – Australian Shares ANT0001AU No Yes -0.47% n/a n/a n/a n/a n/a 3.92% p.a.

ANZ Cash Plus Fund ANZ0150AU No Yes 4.44% 6.38% 5.82% 5.82% 5.57% 5.60% p.a. 5.57% p.a.

APN International Property for Income Fund APN0003AU Yes Yes -16.65% 17.17% 10.59% n/a n/a n/a 8.64% p.a.

APN Direct Property Fund APN0005AU Yes Yes 3.64% 18.32% n/a n/a n/a n/a 11.30% p.a.

APN Diversified Property Fund APN0006AU Yes Yes -4.52% 17.05% n/a n/a n/a n/a 7.70% p.a.

APN National Storage Property Trust APN0002AU No Yes n/a n/a n/a n/a n/a n/a *15.32%

APN Property For Income Fund APN0001AU Yes Yes -28.02% 27.58% 18.83% 23.56% 12.68% 8.43% p.a. 11.65% p.a.

APN Property for Income Fund No 2 APN0004AU Yes Yes -39.36% 26.43% 16.46% n/a n/a n/a -3.56% p.a.

Arrowstreet Emerging Markets Fund MAQ0477AU Yes Yes n/a n/a n/a n/a n/a n/a n/a

Arrowstreet Global Equity Fund MAQ0464AU Yes Yes -21.80% n/a n/a n/a n/a n/a -11.20% p.a.

Arrowstreet Global Equity Fund (Hedged) MAQ0079AU Yes Yes -23.00% 22.90% 16.10% 0.70% 17.30% 5.30% p.a. 3.60% p.a.

ArteFact Partners Global L/S Equity Fd 1 PER0362AU No Yes -3.23% 3.44% 0.30% n/a n/a n/a n/a

Artefact Partners Global L/S Equity Fd 2 PER0363AU No Yes -3.23% 3.44% 0.30% n/a n/a n/a n/a

ArteFact Partners Global L/S Equity Fd 3 PER0396AU No Yes -3.23% 3.44% 0.30% n/a n/a n/a n/a

ArteFact Partners Global L/S Equity Fd 4 PER0435AU No Yes -3.23% 3.44% 0.30% n/a n/a n/a n/a

Augustus Absolute Return Fund (AU) AFM0002AU No Yes 7.31% 7.43% 4.23% 9.89% n/a n/a 7.08% p.a.

Ausbil Aust Geared Equity Fund AAP0002AU Yes Yes -29.67% n/a n/a n/a n/a n/a n/a

Ausbil Inv Trust Aust Active Equity Fund AAP0103AU Yes Yes -10.35% 24.82% 30.22% 34.06% 28.79% 20.27% p.a. 13.59% p.a.

Ausbil Inv Trust Aust Emerging Leaders AAP0104AU Yes Yes -12.58% 28.44% 32.77% 37.93% 39.93% 23.54% p.a. 19.31% p.a.

Aust Unity W/s High Yield Mortgage Trst AUS0005AU Yes Yes 7.92% 7.92% 8.25% n/a n/a n/a 8.08% p.a.

Australian Ethical Equities Trust AUG0002AU Yes Yes -13.10% 36.90% 14.20% 21.30% 14.30% 13.10% p.a. 10.90% p.a.

Australian Ethical Large Companies Share AUG0004AU Yes Yes -13.90% 16.00% 16.00% 23.60% 20.60% 10.20% p.a. 9.60% p.a.

Australian Unity Intech High Opportunities Trust AUS0007AU No Yes -24.69% 7.03% n/a n/a n/a n/a -2.61% p.a.

Australian Unity Platypus Aust Eq Wsale AUS0030AU Yes Yes -13.35% 37.07% n/a n/a n/a n/a 8.75% p.a.

Australian Unity Prop Sec Fd – Ord Units GEM0111AU No Yes -37.48% 24.93% 15.55% 16.14% 15.44% 3.89% p.a. 8.15% p.a.

Australian Unity Wh Defined Income Trust SBC0006AU No Yes 6.23% 4.99% 4.53% 6.09% 3.02% 4.96% p.a. 5.83% p.a.

Australian Unity Wsale Mortgage Income AUS0116AU Yes Yes 7.07% 6.61% 6.01% 6.06% 6.03% 6.35% p.a. 6.32% p.a.

Australian Unity Wsale Property Income YOC0100AU Yes Yes -0.37% 16.50% 12.49% 11.69% 13.09% 10.53% p.a. 9.41% p.a.

AXA Australian Income Fund NML0010AU No Yes 6.25% 5.45% 4.74% 4.87% 4.54% 5.17% p.a. 7.59% p.a.

AXA Wholesale Global Equity Core Fund NMF0002AU Yes Yes -18.19% 7.94% 22.25% n/a n/a n/a 4.36% p.a.

AXA Wsale Aust Equity Industrial Fund NML0143AU Yes Yes -23.67% 29.89% 18.42% 25.25% 17.62% 11.58% p.a. 8.91% p.a.

AXA Wsale Aust. Monthly Income Fund NML0316AU Yes Yes 7.62% 6.72% 6.23% 6.13% 5.92% 6.52% p.a. 6.32% p.a.

AXA Wsale Australian Equity Value Fund NML0061AU Yes Yes -21.67% 27.30% 25.87% 32.42% 24.31% 15.62% p.a. 15.31% p.a.

AXA Wsale Australian Income Fund NML0257AU No Yes 6.67% 5.87% 5.16% 5.29% 4.94% 5.58% p.a. 5.52% p.a.

AXA Wsale Australian Property Fund NML0001AU Yes Yes -0.78% 17.73% 14.58% 14.12% 13.67% 11.67% p.a. 10.77% p.a.

AXA Wsale Global Equity Growth Fund NML0318AU Yes Yes -21.43% 4.63% 22.68% 0.88% 12.67% 2.77% p.a. -5.92% p.a.

AXA Wsale Global Equity Value Fund NML0348AU Yes Yes -29.23% 16.59% 26.32% 7.47% 19.78% 6.05% p.a. 1.58% p.a.

Basis Aust-Rim Diversified Fund BCF0100AU No Yes -48.83% -4.62% 16.58% 12.18% 5.08% -32.93% p.a. n/a

Basis Yield Fund BCF0001AU No Yes n/a n/a 18.67% 12.55% 9.10% n/a n/a

Becton Diversified Property Fund BEC0001AU Yes Yes 7.45% 18.25% n/a n/a n/a n/a 11.12% p.a.

BGI – Australian Equity Index Fund BGL0034AU Yes Yes -13.84% 28.41% 23.61% 25.68% 21.34% 15.83% p.a. 14.52% p.a.

BGI – Australian Fixed Interest Index Fund BGL0105AU Yes Yes 4.16% 3.76% 3.22% 7.60% 2.09% 4.15% p.a. 4.66% p.a.

BGI – Australian Share Fund BAR0814AU Yes Yes -14.42% 28.72% 27.00% 26.24% 20.36% 16.28% p.a. 15.32% p.a.

BGI – Diversified Growth Fund BAR0813AU Yes Yes -11.41% 16.36% 17.24% 14.45% 15.52% 9.82% p.a. 10.81% p.a.

BGI – Diversified Stable Fund BAR0811AU Yes Yes -2.43% 9.48% 9.34% 10.09% 8.28% 6.84% p.a. 7.82% p.a.

BGI – Global Markets Fund BGL0045AU No Yes 3.34% 17.90% 5.94% 11.66% n/a n/a 9.63% p.a.

BGI – International Share Fund BAR0817AU Yes Yes -23.55% 7.69% 20.96% 2.57% 19.48% 4.06% p.a. 5.41% p.a.

BGI – Intl Equity Index Fund BGL0106AU Yes Yes -21.29% 7.33% 19.85% -0.14% 19.26% 3.81% p.a. 0.99% p.a.

BGI – Intl Fixed Interest Index Fund BGL0107AU No Yes n/a 4.83% 0.83% 11.89% 3.13% n/a 6.29% p.a.

BGI – Property Securities Index Fund BGL0108AU Yes Yes -37.01% 25.56% 17.52% 18.61% 17.07% 5.24% p.a. 18.04% p.a.

BGI Hedged International Share Fund BGL0109AU Yes Yes -16.53% 23.30% 18.28% 15.69% 24.14% 11.82% p.a. 22.60% p.a.

BlackRock Asset Alloc Alpha Class D MAL0030AU No Yes 33.70% 3.69% n/a n/a n/a n/a 16.78% p.a.

BlackRock Aust Quant Strat Fd – Cl D MAL0013AU Yes Yes -10.40% 27.95% 21.86% n/a n/a n/a 13.23% p.a.

BlackRock Combined Prop Income – Class D Units MAL0008AU Yes Yes -14.72% 21.25% 17.58% 17.47% n/a n/a 11.70% p.a.

BlackRock Diversified Credit Fund MAL0011AU No Yes -2.33% 7.05% 6.25% n/a n/a n/a 3.97% p.a.

BlackRock Global Allocation Fund MAL0018AU Yes Yes 2.82% 16.22% n/a n/a n/a n/a 11.24% p.a.

BlackRock Global Small Cap Fund Class D MAL0133AU Yes Yes -11.37% 3.63% 26.22% 1.94% 34.47% 9.87% p.a. 0.06% p.a.

BlackRock Global Titans Fund Class D MAL0134AU Yes Yes -10.91% 5.31% 19.32% 0.24% 14.88% 5.30% p.a. -2.49% p.a.

BlackRock Hedged Global Small Cap Fund Class D MAL0135AU Yes Yes -4.22% 18.36% 23.91% 14.99% 40.18% 18.07% p.a. 8.92% p.a.

BlackRock Hedged Global Titans Fund Class D MAL0136AU Yes Yes -3.55% 20.49% 16.62% 12.93% 19.25% 13.01% p.a. 6.14% p.a.

Blackrock Long-Short Active Capital Fund MAL0035AU Yes Yes n/a n/a n/a n/a n/a n/a n/a

BlackRock Monthly Income Fund – Class D MAL0012AU Yes Yes -7.01% 8.82% 6.91% n/a n/a n/a 3.71% p.a.

8

Investment name APIR Available in Super

Accumulator

Available in Super and

Pension Manager

12 months to 30/6/08 (%)

12 months to 30/6/07 (%)

12 months to 30/6/06 (%)

12 months to 30/6/05 (%)

12 months to 30/6/04 (%)

5 year compound to 30/6/08 (% p.a.)

Since inception to 30/6/08 (% p.a.)

BlackRock Property Securities Fund – Class D MAL0151AU Yes Yes -38.70% 23.72% 18.32% 18.59% 15.03% 4.13% p.a. 5.55% p.a.

BlackRock Wholesale Balanced Fund PWA0822AU Yes Yes -5.34% 15.19% 18.74% 13.77% 15.42% 11.39% p.a. 8.86% p.a.

BlackRock Wsale Aust Share Fund PWA0823AU Yes Yes -7.26% 24.30% 29.17% 28.16% 20.88% 18.51% p.a. 11.41% p.a.

BlackRock Wsale Intl Share Fund PWA0824AU Yes Yes -10.39% 8.58% 16.89% 0.96% 15.25% 5.86% p.a. 6.29% p.a.

BlackRock Wsale Managed Income Fund PWA0821AU Yes Yes -4.60% 12.46% 8.54% 10.47% 9.21% 7.15% p.a. 7.16% p.a.

BT Global Return Fund RFA0028AU No Yes 1.38% 13.97% 7.74% 8.02% 8.58% 7.86% p.a. 7.40% p.a.

BT Institutional Enhanced Cash Fund WFS0377AU No Yes 4.44% 6.25% 5.88% 5.83% 5.60% 5.60% p.a. 5.40% p.a.

BT Institutional Managed Cash WFS0245AU No Yes 7.19% 6.23% 5.59% 5.41% 5.02% 5.43% p.a. 7.88% p.a.

BT Wholesale Asian Share Fund BTA0054AU Yes Yes -17.18% 25.90% 26.51% 17.70% 27.35% 14.61% p.a. 2.68% p.a.

BT Wholesale Property Securities Fund BTA0061AU Yes Yes -33.02% 25.83% 17.94% 16.95% 16.71% 6.29% p.a. 8.12% p.a.

BT Wholesale Technology Fund BTA0158AU No Yes -14.30% 15.83% 9.23% -11.02% 11.87% 1.54% p.a. -12.64% p.a.

BT Wsale Active Balanced Fund RFA0815AU Yes Yes -11.74% 14.95% 18.03% 14.90% 18.09% 10.19% p.a. 8.45% p.a.

BT Wsale Australian Share Fund BTA0055AU Yes Yes -10.60% 25.49% 27.41% 28.39% 24.82% 18.30% p.a. 10.90% p.a.

BT Wsale Australian Small Company Fund BTA0240AU No Yes -18.72% 41.76% 28.02% 44.23% 42.69% 24.87% p.a. 17.64% p.a.

BT Wsale Balanced Returns Fund BTA0806AU Yes Yes -9.91% 13.83% 16.48% 13.59% 14.54% 9.22% p.a. 7.91% p.a.

BT Wsale Conservative Outlook Fund BTA0805AU Yes Yes -3.49% 9.02% 9.48% 10.38% 8.20% 6.59% p.a. 8.83% p.a.

BT Wsale Core Australian Share Fund RFA0818AU Yes Yes -10.44% 25.47% 27.33% 28.09% 25.70% 18.16% p.a. 12.12% p.a.

BT Wsale Core Global Share Fund RFA0821AU Yes Yes -27.42% 6.38% 19.50% 2.28% 16.30% 1.88% p.a. 3.61% p.a.

BT Wsale Ethical Share Fund RFA0025AU Yes Yes -11.66% 32.00% 28.83% 30.56% 28.79% 20.36% p.a. 12.64% p.a.

BT Wsale European Share Fund BTA0124AU Yes Yes -21.05% 17.49% 26.63% 8.29% 19.65% 8.76% p.a. 1.65% p.a.

BT Wsale Fixed Interest Fund RFA0813AU Yes Yes 3.80% 3.68% 3.42% 6.69% 2.14% 3.93% p.a. 6.76% p.a.

BT Wsale Future Goals Fund BTA0125AU Yes Yes -14.33% 16.67% 20.85% 15.98% 18.56% 10.68% p.a. 5.09% p.a.

BT Wsale Imputation Fund RFA0103AU Yes Yes -11.00% 32.56% 29.33% 29.74% 27.57% 20.36% p.a. 14.53% p.a.

BT Wsale Intl Share Fund BTA0056AU Yes Yes -27.67% 6.06% 20.00% 2.00% 16.74% 1.85% p.a. 2.88% p.a.

BT Wsale Property Investment Fund RFA0817AU Yes Yes -32.93% 25.82% 17.14% 16.54% 16.71% 6.10% p.a. 9.62% p.a.

BT Wsale Smaller Companies Fund RFA0819AU Yes Yes -18.32% 41.92% 27.47% 42.43% 44.36% 24.89% p.a. 16.03% p.a.

BT Wsale Tax Effective Income Fund RFA0102AU Yes Yes -9.21% 20.40% 17.50% 18.29% 16.28% 12.05% p.a. 10.28% p.a.

BT Wsale Value Global Share Fund RFA0109AU No Yes -28.97% 17.89% 18.80% 3.42% 18.83% 4.10% p.a. -1.45% p.a.

Centro Dir Property Fund International MCS0001AU Yes Yes -18.83% 10.95% n/a n/a n/a n/a 0.18% p.a.

Centro Direct Property Fund MCS0011AU Yes Yes -9.60% 16.58% 18.24% 21.16% 9.96% 10.67% p.a. 11.42% p.a.

CFS 452 Wsale Aust. Share Fund FSF0079AU Yes Yes -20.56% 27.92% 15.92% 21.62% 27.16% n/a 12.76% p.a.

CFS Acadian Global Equity Fund FSF0710AU Yes Yes -22.43% 10.46% 27.96% n/a n/a n/a 3.05% p.a.

CFS B&M Fund CML0002AU No Yes 5.76% 5.23% 5.15% 5.18% 5.75% 5.41% p.a. 5.33% p.a.

CFS Colliers International Property Securities FSF0454AU Yes Yes -25.06% 27.19% 24.64% 48.03% n/a n/a 17.03% p.a.

CFS Global Resources Long Short Fund FSF0698AU No Yes 14.77% 13.91% n/a n/a n/a n/a 18.20% p.a.

CFS Wholesale Index Property Securities Fund CMI0105AU Yes Yes -36.37% 25.06% 17.68% 17.83% 16.99% 5.24% p.a. 7.58% p.a.

CFS Wsale Global Health & Biotech FSF0146AU No Yes -16.80% 0.25% 18.43% -3.39% 10.06% 0.99% p.a. -3.80% p.a.

CFS Wsale Aust Bond Fund FSF0027AU Yes Yes 4.03% 3.22% 3.27% 7.71% 2.92% 4.21% p.a. 6.50% p.a.

CFS Wsale Aust. Corporate Debt Fund FSF0149AU Yes Yes 1.30% 4.29% 3.90% 7.44% 4.00% 4.17% p.a. 5.42% p.a.

CFS Wsale Australian Share Fund FSF0002AU Yes Yes -15.27% 21.85% 23.78% 28.91% 16.96% 14.02% p.a. 12.07% p.a.

CFS Wsale Australian Share Fund – Core CFM0404AU Yes Yes -8.02% 28.12% 27.85% 28.24% 20.68% 18.45% p.a. 13.06% p.a.

CFS Wsale Balanced Fund FSF0040AU Yes Yes -8.08% 10.16% 12.79% 10.93% 8.61% 6.59% p.a. 7.34% p.a.

CFS Wsale Conservative Fund FSF0033AU Yes Yes -2.43% 9.29% 10.61% 9.48% 8.07% 6.89% p.a. 7.49% p.a.

CFS Wsale Diversified Fund FSF0008AU Yes Yes -15.01% 14.47% 15.72% 12.89% 11.95% 7.31% p.a. 8.36% p.a.

CFS Wsale Fixed Interest Strategies FSF0175AU No Yes n/a 7.14% 6.78% 5.72% 9.71% n/a n/a

CFS Wsale Geared Global Share Fund FSF0170AU Yes Yes -28.64% 10.94% 23.48% -3.64% 15.47% 1.69% p.a. -6.73% p.a.

CFS Wsale Geared Share Fund FSF0043AU Yes Yes -34.13% 43.23% 55.81% 62.47% 38.53% 27.04% p.a. 21.18% p.a.

CFS Wsale Global Credit Income Fund FSF0084AU Yes Yes 1.91% 6.76% 6.47% 6.28% 7.04% 5.67% p.a. 5.74% p.a.

CFS Wsale Global Diversified Strategies Fund FSF0176AU No Yes n/a 12.63% 10.76% 6.37% 11.20% n/a n/a

CFS Wsale Global Resources FSF0038AU Yes Yes 20.87% 24.59% 59.43% 21.57% 40.29% 32.57% p.a. 19.08% p.a.

CFS Wsale Global Share Fund FSF0047AU Yes Yes -17.19% 9.70% 17.97% -0.31% 12.20% 3.69% p.a. 3.18% p.a.

CFS Wsale Global Tech & Comms Fund FSF0143AU No Yes -20.06% 13.10% 13.14% -3.82% 18.02% 3.03% p.a. -6.01% p.a.

CFS Wsale High Growth Fund FSF0498AU Yes Yes -19.72% 19.44% 23.09% 12.45% 18.32% 9.45% p.a. 6.58% p.a.

CFS Wsale Imputation Fund FSF0003AU Yes Yes -15.54% 21.97% 24.96% 27.66% 15.77% 13.73% p.a. 14.25% p.a.

CFS Wsale Income Fund FSF0139AU Yes Yes 5.26% 6.73% 6.07% 5.87% 5.60% 5.90% p.a. 5.96% p.a.

CFS Wsale PM Capital Aust Sh Fund FSF0455AU Yes Yes -29.68% 24.37% 28.36% 17.33% n/a n/a 7.81% p.a.

CFS Wsale Premium Cash Fund COM0024AU No Yes 7.03% 6.04% 5.38% 5.21% 4.87% 5.70% p.a. 5.63% p.a.

CFS Wsale Property Securities FSF0004AU Yes Yes -43.82% 23.53% 22.71% 23.07% 12.83% 3.41% p.a. 8.64% p.a.

CFS Wsale Small Companies Fund – Core CMI0111AU Yes Yes -28.19% 48.69% 36.61% 41.82% 43.60% 15.92% p.a. 11.90% p.a.

Challenger Global Infrastructure Fund HOW0031AU No Yes 7.14% 18.94% n/a n/a n/a n/a 12.32% p.a.

Challenger Howard Wsale Mortgage Fund HOW0005AU Yes Yes 7.31% 6.78% 6.34% 6.34% 5.98% 6.55% p.a. 6.38% p.a.

Challenger Select Aust Sh Fund – Wsale HOW0026AU Yes Yes -30.17% 33.38% 25.96% n/a n/a n/a 8.63% p.a.

Challenger Wsale Asian Share Fund HBC0010AU Yes Yes -15.94% 29.01% 27.21% 15.53% 24.65% 14.71% p.a. 3.05% p.a.

Investment returns to 30 June 2008 continued

9

Investment name APIR Available in Super

Accumulator

Available in Super and

Pension Manager

12 months to 30/6/08 (%)

12 months to 30/6/07 (%)

12 months to 30/6/06 (%)

12 months to 30/6/05 (%)

12 months to 30/6/04 (%)

5 year compound to 30/6/08 (% p.a.)

Since inception to 30/6/08 (% p.a.)

BlackRock Property Securities Fund – Class D MAL0151AU Yes Yes -38.70% 23.72% 18.32% 18.59% 15.03% 4.13% p.a. 5.55% p.a.

BlackRock Wholesale Balanced Fund PWA0822AU Yes Yes -5.34% 15.19% 18.74% 13.77% 15.42% 11.39% p.a. 8.86% p.a.

BlackRock Wsale Aust Share Fund PWA0823AU Yes Yes -7.26% 24.30% 29.17% 28.16% 20.88% 18.51% p.a. 11.41% p.a.

BlackRock Wsale Intl Share Fund PWA0824AU Yes Yes -10.39% 8.58% 16.89% 0.96% 15.25% 5.86% p.a. 6.29% p.a.

BlackRock Wsale Managed Income Fund PWA0821AU Yes Yes -4.60% 12.46% 8.54% 10.47% 9.21% 7.15% p.a. 7.16% p.a.

BT Global Return Fund RFA0028AU No Yes 1.38% 13.97% 7.74% 8.02% 8.58% 7.86% p.a. 7.40% p.a.

BT Institutional Enhanced Cash Fund WFS0377AU No Yes 4.44% 6.25% 5.88% 5.83% 5.60% 5.60% p.a. 5.40% p.a.

BT Institutional Managed Cash WFS0245AU No Yes 7.19% 6.23% 5.59% 5.41% 5.02% 5.43% p.a. 7.88% p.a.

BT Wholesale Asian Share Fund BTA0054AU Yes Yes -17.18% 25.90% 26.51% 17.70% 27.35% 14.61% p.a. 2.68% p.a.

BT Wholesale Property Securities Fund BTA0061AU Yes Yes -33.02% 25.83% 17.94% 16.95% 16.71% 6.29% p.a. 8.12% p.a.

BT Wholesale Technology Fund BTA0158AU No Yes -14.30% 15.83% 9.23% -11.02% 11.87% 1.54% p.a. -12.64% p.a.

BT Wsale Active Balanced Fund RFA0815AU Yes Yes -11.74% 14.95% 18.03% 14.90% 18.09% 10.19% p.a. 8.45% p.a.

BT Wsale Australian Share Fund BTA0055AU Yes Yes -10.60% 25.49% 27.41% 28.39% 24.82% 18.30% p.a. 10.90% p.a.

BT Wsale Australian Small Company Fund BTA0240AU No Yes -18.72% 41.76% 28.02% 44.23% 42.69% 24.87% p.a. 17.64% p.a.

BT Wsale Balanced Returns Fund BTA0806AU Yes Yes -9.91% 13.83% 16.48% 13.59% 14.54% 9.22% p.a. 7.91% p.a.

BT Wsale Conservative Outlook Fund BTA0805AU Yes Yes -3.49% 9.02% 9.48% 10.38% 8.20% 6.59% p.a. 8.83% p.a.

BT Wsale Core Australian Share Fund RFA0818AU Yes Yes -10.44% 25.47% 27.33% 28.09% 25.70% 18.16% p.a. 12.12% p.a.

BT Wsale Core Global Share Fund RFA0821AU Yes Yes -27.42% 6.38% 19.50% 2.28% 16.30% 1.88% p.a. 3.61% p.a.

BT Wsale Ethical Share Fund RFA0025AU Yes Yes -11.66% 32.00% 28.83% 30.56% 28.79% 20.36% p.a. 12.64% p.a.

BT Wsale European Share Fund BTA0124AU Yes Yes -21.05% 17.49% 26.63% 8.29% 19.65% 8.76% p.a. 1.65% p.a.

BT Wsale Fixed Interest Fund RFA0813AU Yes Yes 3.80% 3.68% 3.42% 6.69% 2.14% 3.93% p.a. 6.76% p.a.

BT Wsale Future Goals Fund BTA0125AU Yes Yes -14.33% 16.67% 20.85% 15.98% 18.56% 10.68% p.a. 5.09% p.a.

BT Wsale Imputation Fund RFA0103AU Yes Yes -11.00% 32.56% 29.33% 29.74% 27.57% 20.36% p.a. 14.53% p.a.

BT Wsale Intl Share Fund BTA0056AU Yes Yes -27.67% 6.06% 20.00% 2.00% 16.74% 1.85% p.a. 2.88% p.a.

BT Wsale Property Investment Fund RFA0817AU Yes Yes -32.93% 25.82% 17.14% 16.54% 16.71% 6.10% p.a. 9.62% p.a.

BT Wsale Smaller Companies Fund RFA0819AU Yes Yes -18.32% 41.92% 27.47% 42.43% 44.36% 24.89% p.a. 16.03% p.a.

BT Wsale Tax Effective Income Fund RFA0102AU Yes Yes -9.21% 20.40% 17.50% 18.29% 16.28% 12.05% p.a. 10.28% p.a.

BT Wsale Value Global Share Fund RFA0109AU No Yes -28.97% 17.89% 18.80% 3.42% 18.83% 4.10% p.a. -1.45% p.a.

Centro Dir Property Fund International MCS0001AU Yes Yes -18.83% 10.95% n/a n/a n/a n/a 0.18% p.a.

Centro Direct Property Fund MCS0011AU Yes Yes -9.60% 16.58% 18.24% 21.16% 9.96% 10.67% p.a. 11.42% p.a.

CFS 452 Wsale Aust. Share Fund FSF0079AU Yes Yes -20.56% 27.92% 15.92% 21.62% 27.16% n/a 12.76% p.a.

CFS Acadian Global Equity Fund FSF0710AU Yes Yes -22.43% 10.46% 27.96% n/a n/a n/a 3.05% p.a.

CFS B&M Fund CML0002AU No Yes 5.76% 5.23% 5.15% 5.18% 5.75% 5.41% p.a. 5.33% p.a.

CFS Colliers International Property Securities FSF0454AU Yes Yes -25.06% 27.19% 24.64% 48.03% n/a n/a 17.03% p.a.

CFS Global Resources Long Short Fund FSF0698AU No Yes 14.77% 13.91% n/a n/a n/a n/a 18.20% p.a.

CFS Wholesale Index Property Securities Fund CMI0105AU Yes Yes -36.37% 25.06% 17.68% 17.83% 16.99% 5.24% p.a. 7.58% p.a.

CFS Wsale Global Health & Biotech FSF0146AU No Yes -16.80% 0.25% 18.43% -3.39% 10.06% 0.99% p.a. -3.80% p.a.

CFS Wsale Aust Bond Fund FSF0027AU Yes Yes 4.03% 3.22% 3.27% 7.71% 2.92% 4.21% p.a. 6.50% p.a.

CFS Wsale Aust. Corporate Debt Fund FSF0149AU Yes Yes 1.30% 4.29% 3.90% 7.44% 4.00% 4.17% p.a. 5.42% p.a.

CFS Wsale Australian Share Fund FSF0002AU Yes Yes -15.27% 21.85% 23.78% 28.91% 16.96% 14.02% p.a. 12.07% p.a.

CFS Wsale Australian Share Fund – Core CFM0404AU Yes Yes -8.02% 28.12% 27.85% 28.24% 20.68% 18.45% p.a. 13.06% p.a.

CFS Wsale Balanced Fund FSF0040AU Yes Yes -8.08% 10.16% 12.79% 10.93% 8.61% 6.59% p.a. 7.34% p.a.

CFS Wsale Conservative Fund FSF0033AU Yes Yes -2.43% 9.29% 10.61% 9.48% 8.07% 6.89% p.a. 7.49% p.a.

CFS Wsale Diversified Fund FSF0008AU Yes Yes -15.01% 14.47% 15.72% 12.89% 11.95% 7.31% p.a. 8.36% p.a.

CFS Wsale Fixed Interest Strategies FSF0175AU No Yes n/a 7.14% 6.78% 5.72% 9.71% n/a n/a

CFS Wsale Geared Global Share Fund FSF0170AU Yes Yes -28.64% 10.94% 23.48% -3.64% 15.47% 1.69% p.a. -6.73% p.a.

CFS Wsale Geared Share Fund FSF0043AU Yes Yes -34.13% 43.23% 55.81% 62.47% 38.53% 27.04% p.a. 21.18% p.a.

CFS Wsale Global Credit Income Fund FSF0084AU Yes Yes 1.91% 6.76% 6.47% 6.28% 7.04% 5.67% p.a. 5.74% p.a.

CFS Wsale Global Diversified Strategies Fund FSF0176AU No Yes n/a 12.63% 10.76% 6.37% 11.20% n/a n/a

CFS Wsale Global Resources FSF0038AU Yes Yes 20.87% 24.59% 59.43% 21.57% 40.29% 32.57% p.a. 19.08% p.a.

CFS Wsale Global Share Fund FSF0047AU Yes Yes -17.19% 9.70% 17.97% -0.31% 12.20% 3.69% p.a. 3.18% p.a.

CFS Wsale Global Tech & Comms Fund FSF0143AU No Yes -20.06% 13.10% 13.14% -3.82% 18.02% 3.03% p.a. -6.01% p.a.

CFS Wsale High Growth Fund FSF0498AU Yes Yes -19.72% 19.44% 23.09% 12.45% 18.32% 9.45% p.a. 6.58% p.a.

CFS Wsale Imputation Fund FSF0003AU Yes Yes -15.54% 21.97% 24.96% 27.66% 15.77% 13.73% p.a. 14.25% p.a.

CFS Wsale Income Fund FSF0139AU Yes Yes 5.26% 6.73% 6.07% 5.87% 5.60% 5.90% p.a. 5.96% p.a.

CFS Wsale PM Capital Aust Sh Fund FSF0455AU Yes Yes -29.68% 24.37% 28.36% 17.33% n/a n/a 7.81% p.a.

CFS Wsale Premium Cash Fund COM0024AU No Yes 7.03% 6.04% 5.38% 5.21% 4.87% 5.70% p.a. 5.63% p.a.

CFS Wsale Property Securities FSF0004AU Yes Yes -43.82% 23.53% 22.71% 23.07% 12.83% 3.41% p.a. 8.64% p.a.

CFS Wsale Small Companies Fund – Core CMI0111AU Yes Yes -28.19% 48.69% 36.61% 41.82% 43.60% 15.92% p.a. 11.90% p.a.

Challenger Global Infrastructure Fund HOW0031AU No Yes 7.14% 18.94% n/a n/a n/a n/a 12.32% p.a.

Challenger Howard Wsale Mortgage Fund HOW0005AU Yes Yes 7.31% 6.78% 6.34% 6.34% 5.98% 6.55% p.a. 6.38% p.a.

Challenger Select Aust Sh Fund – Wsale HOW0026AU Yes Yes -30.17% 33.38% 25.96% n/a n/a n/a 8.63% p.a.

Challenger Wsale Asian Share Fund HBC0010AU Yes Yes -15.94% 29.01% 27.21% 15.53% 24.65% 14.71% p.a. 3.05% p.a.

10

Investment name APIR Available in Super

Accumulator

Available in Super and

Pension Manager

12 months to 30/6/08 (%)

12 months to 30/6/07 (%)

12 months to 30/6/06 (%)

12 months to 30/6/05 (%)

12 months to 30/6/04 (%)

5 year compound to 30/6/08 (% p.a.)

Since inception to 30/6/08 (% p.a.)

Challenger Wsale Aust. Share Income Fund HBC0011AU Yes Yes -17.47% 21.61% n/a n/a n/a n/a 3.29% p.a.

Challenger Wsale Australian Share Fund PAM0001AU Yes Yes -23.15% 30.11% 26.29% 28.01% 19.05% 13.99% p.a. 13.41% p.a.

Challenger Wsale High Yield fund HOW0141AU Yes Yes -11.16% 7.92% 6.97% 10.89% 10.01% 4.58% p.a. 5.41% p.a.

Challenger Wsale Hybrid Property Fund HBC0013AU Yes Yes -11.15% 19.43% 12.63% 11.39% 10.96% 8.12% p.a. 10.76% p.a.

Challenger Wsale Microcap Fund HOW0027AU Yes Yes -32.21% 68.32% 28.56% n/a n/a n/a 10.74% p.a.

Challenger Wsale MTM Intl Share Fund HBC0012AU No Yes -9.57% 24.32% n/a n/a n/a n/a 7.63% p.a.

Challenger Wsale Property Securities Fund HBC0008AU Yes Yes -37.13% 24.43% 18.63% 17.54% 16.10% 4.84% p.a. 9.42% p.a.

Challenger Wsale Smaller Companies Fund HOW0016AU Yes Yes -14.65% 52.18% 11.05% 17.35% 53.06% 20.97% p.a. 21.61% p.a.

Challenger Wsale Social Respon Sh Fund HOW0121AU Yes Yes -27.40% 29.68% 19.19% 26.65% 13.44% 10.02% p.a. 8.67% p.a.

Charter Hall Diversified Property Fund CHF0001AU Yes Yes 29.60% 16.00% n/a n/a n/a n/a 18.90% p.a.

Chifley Investment Fund – Australian Equities CFS0003AU Yes Yes -16.40% 26.48% 22.14% 26.01% 21.17% 14.54% p.a. 13.22% p.a.

Chifley Investment Fund Australian Fixed Income CFS0005AU Yes Yes 5.15% 3.28% 3.33% 6.17% n/a n/a 4.74% p.a.

Chifley Investment Fund International Equities CFS0008AU Yes Yes -17.95% 9.01% 22.18% 7.21% 20.64% 7.17% p.a. 5.84% p.a.

Chifley Investment Fund International Fixed Income CFS0010AU Yes Yes 5.30% 6.10% 1.01% 11.09% n/a n/a 5.62% p.a.

Concord Australian Equity Fund MAQ0424AU Yes Yes -13.40% 28.66% 23.93% 26.35% n/a n/a 10.60% p.a.

Credit Suisse Aust Smaller Comp Fund CSA0131AU Yes Yes -28.09% 37.24% 20.93% 27.43% 63.10% 19.92% p.a. 16.11% p.a.

Credit Suisse Aust. Fixed Interest Fund CRS0004AU Yes Yes 1.29% 3.80% 3.95% 7.97% 3.24% 4.03% p.a. 6.84% p.a.

Credit Suisse Australian Shares Fund CRS0003AU Yes Yes -13.69% 26.22% 24.64% 23.54% 14.94% 14.03% p.a. 11.16% p.a.

Credit Suisse Capital Growth Fund CRS0002AU Yes Yes -10.98% 13.30% 17.48% 11.22% 13.45% 8.37% p.a. 8.09% p.a.

Credit Suisse Capital Stable Fund CRS0001AU Yes Yes -4.90% 9.80% 10.55% 8.89% 8.72% 6.44% p.a. 6.70% p.a.

Credit Suisse Cash Fund CRS0009AU Yes Yes 6.60% 6.11% 5.73% 5.53% 5.32% 5.86% p.a. 5.64% p.a.

Credit Suisse Fully Hdgd Int'l Shares CSA0135AU Yes Yes -11.44% 19.66% 20.87% 10.41% 21.27% 11.39% p.a. 3.10% p.a.

Credit Suisse Global Income Fund CSA0038AU Yes Yes -2.84% 7.31% 8.08% 8.02% n/a n/a 5.43% p.a.

Credit Suisse Global Private Equity Fund CSA0042AU No Yes -3.84% -9.03% n/a n/a n/a n/a -13.72% p.a.

Credit Suisse Intl Fixed Interest Fund CRS0006AU Yes Yes 8.46% 4.54% 0.47% 11.95% 2.72% 5.55% p.a. 7.55% p.a.

Credit Suisse Intl Share Fund CRS0005AU Yes Yes -18.45% 4.62% 22.54% -2.58% 20.58% 4.20% p.a. 8.40% p.a.

Credit Suisse Property Fund CRS0007AU Yes Yes -37.46% 25.42% 15.35% 19.36% 18.14% 4.99% p.a. 9.15% p.a.

Credit Suisse Syndicated Loan Fund CSA0046AU Yes Yes 0.83% 9.39% 8.06% n/a n/a n/a 7.10% p.a.

Credit Suisse Unhedged Int'l Shares Fund CSA0136AU Yes Yes -18.64% 4.21% 22.16% -2.55% 18.38% 3.62% p.a. -4.89% p.a.

Credit Suisse/Tremont Strat Index Fund CSA0065AU No Yes -0.96% n/a n/a n/a n/a n/a -1.36% p.a.

Cromwell Property Fund CRM0004AU No Yes 5.50% 8.58% n/a n/a n/a n/a 6.54% p.a.

CSL Active Commodities Fund MAQ0445AU No Yes 48.70% 1.90% n/a n/a n/a n/a 21.60% p.a.

Custom Choice Ws Boutique Aus Sh Pfolio HOW0019AU Yes Yes -13.86% 26.90% 20.00% 25.15% n/a n/a 14.04% p.a.

Custom Choice Ws Inter Share Pfolio HOW0029AU No Yes -10.69% 23.28% n/a n/a n/a n/a 7.11% p.a.

Custom Choice Wsale Aust Share Portfolio HBC0113AU No Yes -15.67% 27.64% n/a n/a n/a n/a 9.81% p.a.

DDH Australian Equities Fund DDH0003AU Yes Yes -16.11% n/a n/a n/a n/a n/a -0.04% p.a.

DDH Global Fixed Interest Alpha Fund DDH0007AU No Yes 8.34% n/a n/a n/a n/a n/a 10.68% p.a.

Deutsche Income Fund MGL0007AU No Yes n/a n/a n/a n/a n/a n/a n/a

5-Yr Diversified Fixed Interest – AUD Class Units DFA0108AU Yes Yes 7.31% 6.03% 1.98% 9.91% 3.43% 5.69% p.a. 6.64% p.a.

5-Yr Diversified Fixed Interest – NZD Class Units DFA0001AU No Yes -4.60% 19.38% -7.03% 11.50% n/a n/a 4.50% p.a.

Dimensional Aust Large Company Trust DFA0103AU Yes Yes -12.73% 27.12% 23.70% 24.93% 21.03% 15.72% p.a. 10.31% p.a.

Dimensional Aust Small Company Trust DFA0104AU Yes Yes -13.01% 46.21% 23.94% 23.70% 33.53% 21.09% p.a. 13.85% p.a.

Dimensional Australian Core Equity Trust DFA0003AU Yes Yes -18.09% n/a n/a n/a n/a n/a 4.78% p.a.

Dimensional Australian Value Trust DFA0101AU Yes Yes -15.20% 33.37% 20.83% 25.28% 33.16% 17.92% p.a. 13.71% p.a.

Dimensional Emerging Markets Trust DFA0107AU Yes Yes -12.28% 30.96% 31.42% 22.24% 26.28% 18.44% p.a. 7.58% p.a.

Dimensional Global Core Equity Trust DFA0004AU Yes Yes -23.99% n/a n/a n/a n/a n/a -15.61% p.a.

Dimensional Global Large Company Trust DFA0105AU Yes Yes -21.18% 7.69% 20.15% -0.89% 19.83% 3.91% p.a. -4.30% p.a.

Dimensional Global Real Estate Trust DFA0005AU Yes Yes n/a n/a n/a n/a n/a n/a -32.04% p.a.

Dimensional Global Small Company Trust DFA0106AU Yes Yes -26.82% 7.24% 24.22% 3.71% 34.63% 6.36% p.a. 2.25% p.a.

Dimensional Global Value Trust DFA0102AU Yes Yes -27.77% 11.68% 25.87% 5.58% 30.03% 6.87% p.a. 3.07% p.a.

Dimensional Short Term Fixed Int Trust DFA0100AU Yes Yes 7.18% 6.22% 5.42% 5.53% 4.86% 5.84% p.a. 5.48% p.a.

Dimensional Two-Year Div Fixed Int Trust DFA0002AU Yes Yes 7.24% 5.84% n/a n/a n/a n/a 6.12% p.a.

Diversified Investment Strategy No.2 IPA0115AU No Yes -11.96% 17.00% 16.54% 14.65% 15.45% 9.70% p.a. 5.41% p.a.

Diversified Investment Strategy No.3 IPA0116AU No Yes -14.70% 18.93% 18.03% 14.89% 17.59% 10.10% p.a. 4.26% p.a.

Diversified Investment Strategy No.4 IPA0124AU No Yes -17.95% 21.01% 20.78% 15.02% 20.28% 10.65% p.a. 4.36% p.a.

Diversified Investment Strategy No.5 IPA0055AU No Yes -11.17% 18.48% n/a n/a n/a n/a 5.77% p.a.

Donaldson Burston THS Partners Global Equity Fund ETL0096AU Yes Yes -15.79% -1.50% n/a n/a n/a n/a -14.99% p.a.

DWS Global Equity Agribusiness Fund MGL0019AU Yes Yes 3.06% n/a n/a n/a n/a n/a 13.68% p.a.

DWS Global Equity Thematic Fully Hedged MGL0018AU Yes Yes -18.96% n/a n/a n/a n/a n/a -2.47% p.a.

DWS Global Equity Thematic Fund MGL0004AU Yes Yes -24.17% 16.17% 37.84% 8.80% 18.15% 9.31% p.a. 8.95% p.a.

DWS Strategic Value Fund DEU0109AU No Yes 4.88% 14.90% 15.56% 8.34% 9.45% 10.55% p.a. 9.34% p.a.

EII Global Property Fund MAQ0463AU Yes Yes -28.30% 30.60% n/a n/a n/a n/a -4.90% p.a.

Eley Griffiths Group Small Companies Fund EGG0001AU Yes Yes -13.77% 38.85% 29.86% 35.71% n/a n/a 20.61% p.a.

Investment returns to 30 June 2008 continued

11

Investment name APIR Available in Super

Accumulator

Available in Super and

Pension Manager

12 months to 30/6/08 (%)

12 months to 30/6/07 (%)

12 months to 30/6/06 (%)

12 months to 30/6/05 (%)

12 months to 30/6/04 (%)

5 year compound to 30/6/08 (% p.a.)

Since inception to 30/6/08 (% p.a.)

Challenger Wsale Aust. Share Income Fund HBC0011AU Yes Yes -17.47% 21.61% n/a n/a n/a n/a 3.29% p.a.

Challenger Wsale Australian Share Fund PAM0001AU Yes Yes -23.15% 30.11% 26.29% 28.01% 19.05% 13.99% p.a. 13.41% p.a.

Challenger Wsale High Yield fund HOW0141AU Yes Yes -11.16% 7.92% 6.97% 10.89% 10.01% 4.58% p.a. 5.41% p.a.

Challenger Wsale Hybrid Property Fund HBC0013AU Yes Yes -11.15% 19.43% 12.63% 11.39% 10.96% 8.12% p.a. 10.76% p.a.

Challenger Wsale Microcap Fund HOW0027AU Yes Yes -32.21% 68.32% 28.56% n/a n/a n/a 10.74% p.a.

Challenger Wsale MTM Intl Share Fund HBC0012AU No Yes -9.57% 24.32% n/a n/a n/a n/a 7.63% p.a.

Challenger Wsale Property Securities Fund HBC0008AU Yes Yes -37.13% 24.43% 18.63% 17.54% 16.10% 4.84% p.a. 9.42% p.a.

Challenger Wsale Smaller Companies Fund HOW0016AU Yes Yes -14.65% 52.18% 11.05% 17.35% 53.06% 20.97% p.a. 21.61% p.a.

Challenger Wsale Social Respon Sh Fund HOW0121AU Yes Yes -27.40% 29.68% 19.19% 26.65% 13.44% 10.02% p.a. 8.67% p.a.

Charter Hall Diversified Property Fund CHF0001AU Yes Yes 29.60% 16.00% n/a n/a n/a n/a 18.90% p.a.

Chifley Investment Fund – Australian Equities CFS0003AU Yes Yes -16.40% 26.48% 22.14% 26.01% 21.17% 14.54% p.a. 13.22% p.a.

Chifley Investment Fund Australian Fixed Income CFS0005AU Yes Yes 5.15% 3.28% 3.33% 6.17% n/a n/a 4.74% p.a.

Chifley Investment Fund International Equities CFS0008AU Yes Yes -17.95% 9.01% 22.18% 7.21% 20.64% 7.17% p.a. 5.84% p.a.

Chifley Investment Fund International Fixed Income CFS0010AU Yes Yes 5.30% 6.10% 1.01% 11.09% n/a n/a 5.62% p.a.

Concord Australian Equity Fund MAQ0424AU Yes Yes -13.40% 28.66% 23.93% 26.35% n/a n/a 10.60% p.a.

Credit Suisse Aust Smaller Comp Fund CSA0131AU Yes Yes -28.09% 37.24% 20.93% 27.43% 63.10% 19.92% p.a. 16.11% p.a.

Credit Suisse Aust. Fixed Interest Fund CRS0004AU Yes Yes 1.29% 3.80% 3.95% 7.97% 3.24% 4.03% p.a. 6.84% p.a.

Credit Suisse Australian Shares Fund CRS0003AU Yes Yes -13.69% 26.22% 24.64% 23.54% 14.94% 14.03% p.a. 11.16% p.a.

Credit Suisse Capital Growth Fund CRS0002AU Yes Yes -10.98% 13.30% 17.48% 11.22% 13.45% 8.37% p.a. 8.09% p.a.

Credit Suisse Capital Stable Fund CRS0001AU Yes Yes -4.90% 9.80% 10.55% 8.89% 8.72% 6.44% p.a. 6.70% p.a.

Credit Suisse Cash Fund CRS0009AU Yes Yes 6.60% 6.11% 5.73% 5.53% 5.32% 5.86% p.a. 5.64% p.a.

Credit Suisse Fully Hdgd Int'l Shares CSA0135AU Yes Yes -11.44% 19.66% 20.87% 10.41% 21.27% 11.39% p.a. 3.10% p.a.

Credit Suisse Global Income Fund CSA0038AU Yes Yes -2.84% 7.31% 8.08% 8.02% n/a n/a 5.43% p.a.

Credit Suisse Global Private Equity Fund CSA0042AU No Yes -3.84% -9.03% n/a n/a n/a n/a -13.72% p.a.

Credit Suisse Intl Fixed Interest Fund CRS0006AU Yes Yes 8.46% 4.54% 0.47% 11.95% 2.72% 5.55% p.a. 7.55% p.a.

Credit Suisse Intl Share Fund CRS0005AU Yes Yes -18.45% 4.62% 22.54% -2.58% 20.58% 4.20% p.a. 8.40% p.a.

Credit Suisse Property Fund CRS0007AU Yes Yes -37.46% 25.42% 15.35% 19.36% 18.14% 4.99% p.a. 9.15% p.a.

Credit Suisse Syndicated Loan Fund CSA0046AU Yes Yes 0.83% 9.39% 8.06% n/a n/a n/a 7.10% p.a.

Credit Suisse Unhedged Int'l Shares Fund CSA0136AU Yes Yes -18.64% 4.21% 22.16% -2.55% 18.38% 3.62% p.a. -4.89% p.a.

Credit Suisse/Tremont Strat Index Fund CSA0065AU No Yes -0.96% n/a n/a n/a n/a n/a -1.36% p.a.

Cromwell Property Fund CRM0004AU No Yes 5.50% 8.58% n/a n/a n/a n/a 6.54% p.a.

CSL Active Commodities Fund MAQ0445AU No Yes 48.70% 1.90% n/a n/a n/a n/a 21.60% p.a.

Custom Choice Ws Boutique Aus Sh Pfolio HOW0019AU Yes Yes -13.86% 26.90% 20.00% 25.15% n/a n/a 14.04% p.a.

Custom Choice Ws Inter Share Pfolio HOW0029AU No Yes -10.69% 23.28% n/a n/a n/a n/a 7.11% p.a.

Custom Choice Wsale Aust Share Portfolio HBC0113AU No Yes -15.67% 27.64% n/a n/a n/a n/a 9.81% p.a.

DDH Australian Equities Fund DDH0003AU Yes Yes -16.11% n/a n/a n/a n/a n/a -0.04% p.a.

DDH Global Fixed Interest Alpha Fund DDH0007AU No Yes 8.34% n/a n/a n/a n/a n/a 10.68% p.a.

Deutsche Income Fund MGL0007AU No Yes n/a n/a n/a n/a n/a n/a n/a

5-Yr Diversified Fixed Interest – AUD Class Units DFA0108AU Yes Yes 7.31% 6.03% 1.98% 9.91% 3.43% 5.69% p.a. 6.64% p.a.

5-Yr Diversified Fixed Interest – NZD Class Units DFA0001AU No Yes -4.60% 19.38% -7.03% 11.50% n/a n/a 4.50% p.a.

Dimensional Aust Large Company Trust DFA0103AU Yes Yes -12.73% 27.12% 23.70% 24.93% 21.03% 15.72% p.a. 10.31% p.a.

Dimensional Aust Small Company Trust DFA0104AU Yes Yes -13.01% 46.21% 23.94% 23.70% 33.53% 21.09% p.a. 13.85% p.a.

Dimensional Australian Core Equity Trust DFA0003AU Yes Yes -18.09% n/a n/a n/a n/a n/a 4.78% p.a.

Dimensional Australian Value Trust DFA0101AU Yes Yes -15.20% 33.37% 20.83% 25.28% 33.16% 17.92% p.a. 13.71% p.a.

Dimensional Emerging Markets Trust DFA0107AU Yes Yes -12.28% 30.96% 31.42% 22.24% 26.28% 18.44% p.a. 7.58% p.a.

Dimensional Global Core Equity Trust DFA0004AU Yes Yes -23.99% n/a n/a n/a n/a n/a -15.61% p.a.

Dimensional Global Large Company Trust DFA0105AU Yes Yes -21.18% 7.69% 20.15% -0.89% 19.83% 3.91% p.a. -4.30% p.a.

Dimensional Global Real Estate Trust DFA0005AU Yes Yes n/a n/a n/a n/a n/a n/a -32.04% p.a.

Dimensional Global Small Company Trust DFA0106AU Yes Yes -26.82% 7.24% 24.22% 3.71% 34.63% 6.36% p.a. 2.25% p.a.

Dimensional Global Value Trust DFA0102AU Yes Yes -27.77% 11.68% 25.87% 5.58% 30.03% 6.87% p.a. 3.07% p.a.

Dimensional Short Term Fixed Int Trust DFA0100AU Yes Yes 7.18% 6.22% 5.42% 5.53% 4.86% 5.84% p.a. 5.48% p.a.

Dimensional Two-Year Div Fixed Int Trust DFA0002AU Yes Yes 7.24% 5.84% n/a n/a n/a n/a 6.12% p.a.

Diversified Investment Strategy No.2 IPA0115AU No Yes -11.96% 17.00% 16.54% 14.65% 15.45% 9.70% p.a. 5.41% p.a.

Diversified Investment Strategy No.3 IPA0116AU No Yes -14.70% 18.93% 18.03% 14.89% 17.59% 10.10% p.a. 4.26% p.a.

Diversified Investment Strategy No.4 IPA0124AU No Yes -17.95% 21.01% 20.78% 15.02% 20.28% 10.65% p.a. 4.36% p.a.

Diversified Investment Strategy No.5 IPA0055AU No Yes -11.17% 18.48% n/a n/a n/a n/a 5.77% p.a.

Donaldson Burston THS Partners Global Equity Fund ETL0096AU Yes Yes -15.79% -1.50% n/a n/a n/a n/a -14.99% p.a.

DWS Global Equity Agribusiness Fund MGL0019AU Yes Yes 3.06% n/a n/a n/a n/a n/a 13.68% p.a.

DWS Global Equity Thematic Fully Hedged MGL0018AU Yes Yes -18.96% n/a n/a n/a n/a n/a -2.47% p.a.

DWS Global Equity Thematic Fund MGL0004AU Yes Yes -24.17% 16.17% 37.84% 8.80% 18.15% 9.31% p.a. 8.95% p.a.

DWS Strategic Value Fund DEU0109AU No Yes 4.88% 14.90% 15.56% 8.34% 9.45% 10.55% p.a. 9.34% p.a.

EII Global Property Fund MAQ0463AU Yes Yes -28.30% 30.60% n/a n/a n/a n/a -4.90% p.a.

Eley Griffiths Group Small Companies Fund EGG0001AU Yes Yes -13.77% 38.85% 29.86% 35.71% n/a n/a 20.61% p.a.

12

Investment name APIR Available in Super

Accumulator

Available in Super and

Pension Manager

12 months to 30/6/08 (%)

12 months to 30/6/07 (%)

12 months to 30/6/06 (%)

12 months to 30/6/05 (%)

12 months to 30/6/04 (%)

5 year compound to 30/6/08 (% p.a.)

Since inception to 30/6/08 (% p.a.)

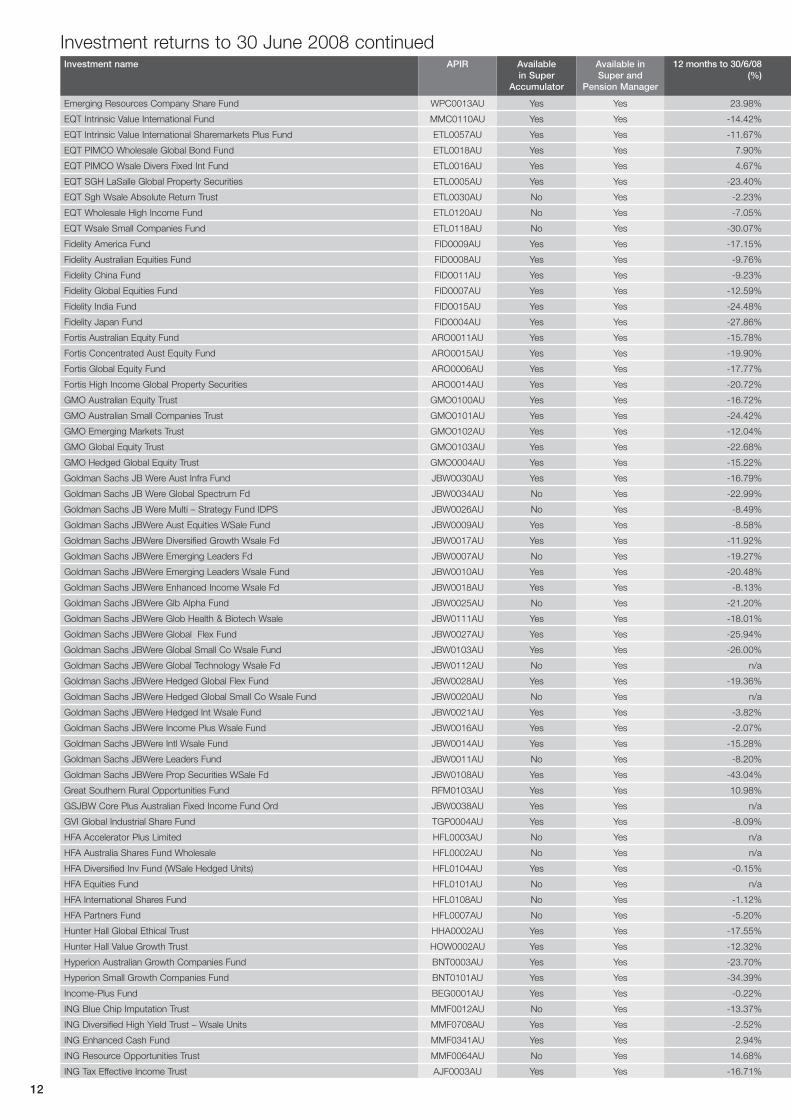

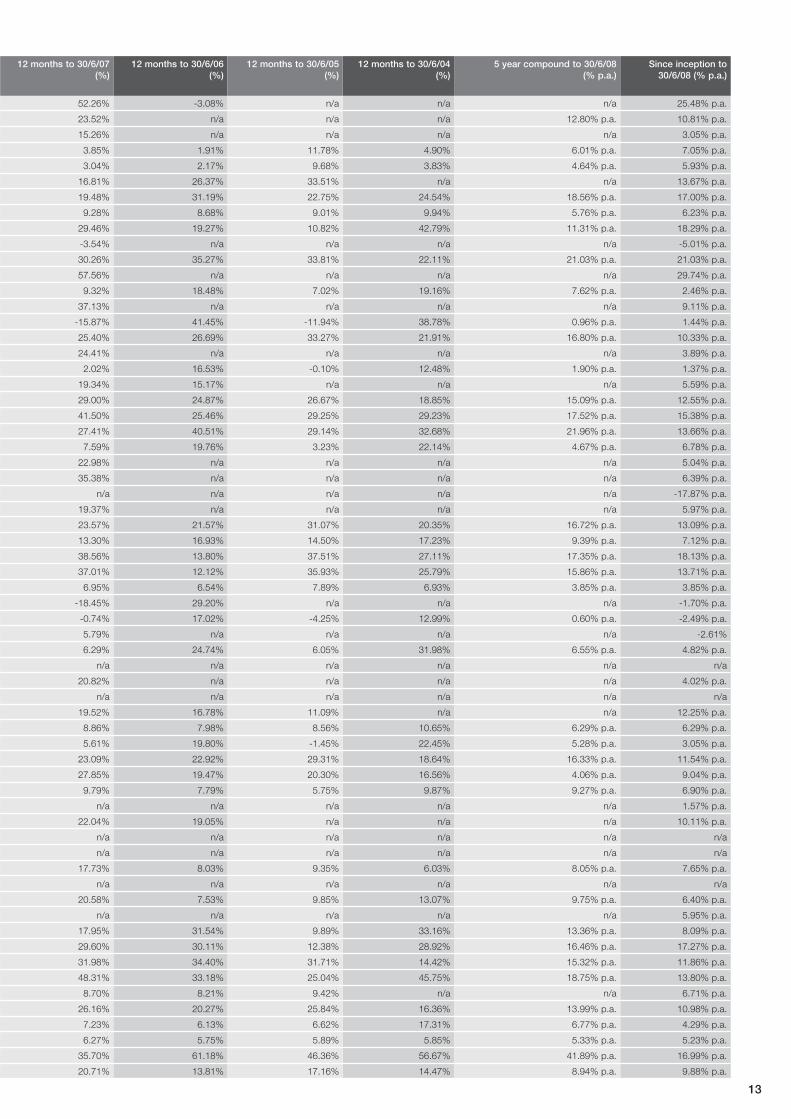

Emerging Resources Company Share Fund WPC0013AU Yes Yes 23.98% 52.26% -3.08% n/a n/a n/a 25.48% p.a.

EQT Intrinsic Value International Fund MMC0110AU Yes Yes -14.42% 23.52% n/a n/a n/a 12.80% p.a. 10.81% p.a.

EQT Intrinsic Value International Sharemarkets Plus Fund ETL0057AU Yes Yes -11.67% 15.26% n/a n/a n/a n/a 3.05% p.a.

EQT PIMCO Wholesale Global Bond Fund ETL0018AU Yes Yes 7.90% 3.85% 1.91% 11.78% 4.90% 6.01% p.a. 7.05% p.a.

EQT PIMCO Wsale Divers Fixed Int Fund ETL0016AU Yes Yes 4.67% 3.04% 2.17% 9.68% 3.83% 4.64% p.a. 5.93% p.a.

EQT SGH LaSalle Global Property Securities ETL0005AU Yes Yes -23.40% 16.81% 26.37% 33.51% n/a n/a 13.67% p.a.

EQT Sgh Wsale Absolute Return Trust ETL0030AU No Yes -2.23% 19.48% 31.19% 22.75% 24.54% 18.56% p.a. 17.00% p.a.

EQT Wholesale High Income Fund ETL0120AU No Yes -7.05% 9.28% 8.68% 9.01% 9.94% 5.76% p.a. 6.23% p.a.

EQT Wsale Small Companies Fund ETL0118AU No Yes -30.07% 29.46% 19.27% 10.82% 42.79% 11.31% p.a. 18.29% p.a.

Fidelity America Fund FID0009AU Yes Yes -17.15% -3.54% n/a n/a n/a n/a -5.01% p.a.

Fidelity Australian Equities Fund FID0008AU Yes Yes -9.76% 30.26% 35.27% 33.81% 22.11% 21.03% p.a. 21.03% p.a.

Fidelity China Fund FID0011AU Yes Yes -9.23% 57.56% n/a n/a n/a n/a 29.74% p.a.

Fidelity Global Equities Fund FID0007AU Yes Yes -12.59% 9.32% 18.48% 7.02% 19.16% 7.62% p.a. 2.46% p.a.

Fidelity India Fund FID0015AU Yes Yes -24.48% 37.13% n/a n/a n/a n/a 9.11% p.a.

Fidelity Japan Fund FID0004AU Yes Yes -27.86% -15.87% 41.45% -11.94% 38.78% 0.96% p.a. 1.44% p.a.

Fortis Australian Equity Fund ARO0011AU Yes Yes -15.78% 25.40% 26.69% 33.27% 21.91% 16.80% p.a. 10.33% p.a.

Fortis Concentrated Aust Equity Fund ARO0015AU Yes Yes -19.90% 24.41% n/a n/a n/a n/a 3.89% p.a.

Fortis Global Equity Fund ARO0006AU Yes Yes -17.77% 2.02% 16.53% -0.10% 12.48% 1.90% p.a. 1.37% p.a.

Fortis High Income Global Property Securities ARO0014AU Yes Yes -20.72% 19.34% 15.17% n/a n/a n/a 5.59% p.a.

GMO Australian Equity Trust GMO0100AU Yes Yes -16.72% 29.00% 24.87% 26.67% 18.85% 15.09% p.a. 12.55% p.a.

GMO Australian Small Companies Trust GMO0101AU Yes Yes -24.42% 41.50% 25.46% 29.25% 29.23% 17.52% p.a. 15.38% p.a.

GMO Emerging Markets Trust GMO0102AU Yes Yes -12.04% 27.41% 40.51% 29.14% 32.68% 21.96% p.a. 13.66% p.a.

GMO Global Equity Trust GMO0103AU Yes Yes -22.68% 7.59% 19.76% 3.23% 22.14% 4.67% p.a. 6.78% p.a.

GMO Hedged Global Equity Trust GMO0004AU Yes Yes -15.22% 22.98% n/a n/a n/a n/a 5.04% p.a.

Goldman Sachs JB Were Aust Infra Fund JBW0030AU Yes Yes -16.79% 35.38% n/a n/a n/a n/a 6.39% p.a.

Goldman Sachs JB Were Global Spectrum Fd JBW0034AU No Yes -22.99% n/a n/a n/a n/a n/a -17.87% p.a.

Goldman Sachs JB Were Multi – Strategy Fund IDPS JBW0026AU No Yes -8.49% 19.37% n/a n/a n/a n/a 5.97% p.a.

Goldman Sachs JBWere Aust Equities WSale Fund JBW0009AU Yes Yes -8.58% 23.57% 21.57% 31.07% 20.35% 16.72% p.a. 13.09% p.a.

Goldman Sachs JBWere Diversified Growth Wsale Fd JBW0017AU Yes Yes -11.92% 13.30% 16.93% 14.50% 17.23% 9.39% p.a. 7.12% p.a.

Goldman Sachs JBWere Emerging Leaders Fd JBW0007AU No Yes -19.27% 38.56% 13.80% 37.51% 27.11% 17.35% p.a. 18.13% p.a.

Goldman Sachs JBWere Emerging Leaders Wsale Fund JBW0010AU Yes Yes -20.48% 37.01% 12.12% 35.93% 25.79% 15.86% p.a. 13.71% p.a.

Goldman Sachs JBWere Enhanced Income Wsale Fd JBW0018AU Yes Yes -8.13% 6.95% 6.54% 7.89% 6.93% 3.85% p.a. 3.85% p.a.

Goldman Sachs JBWere Glb Alpha Fund JBW0025AU No Yes -21.20% -18.45% 29.20% n/a n/a n/a -1.70% p.a.

Goldman Sachs JBWere Glob Health & Biotech Wsale JBW0111AU Yes Yes -18.01% -0.74% 17.02% -4.25% 12.99% 0.60% p.a. -2.49% p.a.

Goldman Sachs JBWere Global Flex Fund JBW0027AU Yes Yes -25.94% 5.79% n/a n/a n/a n/a -2.61%

Goldman Sachs JBWere Global Small Co Wsale Fund JBW0103AU Yes Yes -26.00% 6.29% 24.74% 6.05% 31.98% 6.55% p.a. 4.82% p.a.

Goldman Sachs JBWere Global Technology Wsale Fd JBW0112AU No Yes n/a n/a n/a n/a n/a n/a n/a

Goldman Sachs JBWere Hedged Global Flex Fund JBW0028AU Yes Yes -19.36% 20.82% n/a n/a n/a n/a 4.02% p.a.

Goldman Sachs JBWere Hedged Global Small Co Wsale Fund JBW0020AU No Yes n/a n/a n/a n/a n/a n/a n/a

Goldman Sachs JBWere Hedged Int Wsale Fund JBW0021AU Yes Yes -3.82% 19.52% 16.78% 11.09% n/a n/a 12.25% p.a.

Goldman Sachs JBWere Income Plus Wsale Fund JBW0016AU Yes Yes -2.07% 8.86% 7.98% 8.56% 10.65% 6.29% p.a. 6.29% p.a.

Goldman Sachs JBWere Intl Wsale Fund JBW0014AU Yes Yes -15.28% 5.61% 19.80% -1.45% 22.45% 5.28% p.a. 3.05% p.a.

Goldman Sachs JBWere Leaders Fund JBW0011AU No Yes -8.20% 23.09% 22.92% 29.31% 18.64% 16.33% p.a. 11.54% p.a.

Goldman Sachs JBWere Prop Securities WSale Fd JBW0108AU Yes Yes -43.04% 27.85% 19.47% 20.30% 16.56% 4.06% p.a. 9.04% p.a.

Great Southern Rural Opportunities Fund RFM0103AU Yes Yes 10.98% 9.79% 7.79% 5.75% 9.87% 9.27% p.a. 6.90% p.a.

GSJBW Core Plus Australian Fixed Income Fund Ord JBW0038AU Yes Yes n/a n/a n/a n/a n/a n/a 1.57% p.a.

GVI Global Industrial Share Fund TGP0004AU Yes Yes -8.09% 22.04% 19.05% n/a n/a n/a 10.11% p.a.

HFA Accelerator Plus Limited HFL0003AU No Yes n/a n/a n/a n/a n/a n/a n/a

HFA Australia Shares Fund Wholesale HFL0002AU No Yes n/a n/a n/a n/a n/a n/a n/a

HFA Diversified Inv Fund (WSale Hedged Units) HFL0104AU Yes Yes -0.15% 17.73% 8.03% 9.35% 6.03% 8.05% p.a. 7.65% p.a.

HFA Equities Fund HFL0101AU No Yes n/a n/a n/a n/a n/a n/a n/a

HFA International Shares Fund HFL0108AU No Yes -1.12% 20.58% 7.53% 9.85% 13.07% 9.75% p.a. 6.40% p.a.

HFA Partners Fund HFL0007AU No Yes -5.20% n/a n/a n/a n/a n/a 5.95% p.a.

Hunter Hall Global Ethical Trust HHA0002AU Yes Yes -17.55% 17.95% 31.54% 9.89% 33.16% 13.36% p.a. 8.09% p.a.

Hunter Hall Value Growth Trust HOW0002AU Yes Yes -12.32% 29.60% 30.11% 12.38% 28.92% 16.46% p.a. 17.27% p.a.

Hyperion Australian Growth Companies Fund BNT0003AU Yes Yes -23.70% 31.98% 34.40% 31.71% 14.42% 15.32% p.a. 11.86% p.a.

Hyperion Small Growth Companies Fund BNT0101AU Yes Yes -34.39% 48.31% 33.18% 25.04% 45.75% 18.75% p.a. 13.80% p.a.

Income-Plus Fund BEG0001AU Yes Yes -0.22% 8.70% 8.21% 9.42% n/a n/a 6.71% p.a.