Embed Size (px)

Citation preview

1

Macau Gaming Sector Report

September 25, 2012

Angela Han Lee—Analyst

(852) 3698-6318

John Mulcahy—Head of Research

(852) 3698-6889

“A rising tide lifts all boats” - secular growth remains intact SECTOR DESERVES RE-RATING FOR SHIFT TO MASS-MARKET

We believe the Macau gaming sector investment story is shifting from its VIP orientation

to a mass-market emphasis. As we believe the mass market is driven by supply, the

53% increase in hotel supply by 2015/2016 is a cornerstone of our view.

On the demand side, only 23% of China’s population currently qualifies for the Individual

Visit Scheme (IVS) to Hong Kong and Macau, and the pent-up demand from even a

modest proportion will underwrite mass-market growth. Further relaxation in visa policy

should unlock substantial growth in visitor arrivals to Macau.

To translate into fundamentals, we project the mass-market to grow at a 31.4% CAGR

during 2011-2014, while VIP gaming is expected to grow at a 10.8% CAGR. As a whole,

we forecast Macau’s gross gaming revenue (GGR) to grow at a 16.5% CAGR.

As mass-market produces c.3.7 times EBITDA margin than the VIP segment, the shift

will become visible in earnings, which we expect to enjoy CAGR of 37.7% from 2011 to

2014.

MARKET CONCERN IS OVERDONE AND UNDER-ESTIMATES MASS-MARKET PHE-

NOMENON

The market is estimating 12.8% year-on-year (YoY) growth in GRR in 2013 and 11.4%

in 2014, which we believe is too pessimistic. Compared to the market consensus, our

GGR estimate is 8.8% higher for 2013 at HK$333.6bn and 10.2% higher for 2014 at

HK$376.2bn.

Our earnings projections are similarly more optimistic: we expect net profit of six major

gaming operators to reach HK$58.7bn and HK$74.6bn in 2013 and 2014, which is

30.7% and 42.3% above the market consensus.

The consensus concern is overdone and the sector is regaining positive momentum: we

expect September GGR growth to be c.20% vs. 5.5% in August, inducing more confi-

dence into the sector.

TIME TO CHASE DEEP VALUE PLAYERS WITH NEAR-TERM CATALYSTS

Galaxy Entertainment (GEG) is our top pick for its consistently outperforming operating

figures.

Valuation laggards MGM China and SJM are also recommended. They are trading at

7.2% and 8.3% yield with net cash providing limited downside risk, while their upcoming

Cotai projects leave room for upside.

Wynn Macau also offers good value for its strong brand name and good operating effi-

ciency, and its YTD price underperformance provides scope for short-term catch-up in

valuation.

Figure 1: Coverage Summary

Target Upside

Ticker Rating Price Potential

(HK$) (%)

0880 HK BUY 18.30 12.1

1928 HK HOLD 29.20 2.1

0027 HK BUY 27.60 10.8

1128 HK BUY 23.90 14.9

6883 HK HOLD 35.20 5.7

2282 HK BUY 14.90 13.6

2013

Ticker PER EV/EBITDA Yield

(x) (x) (%)

0880 HK 9.1 6.7 8.3

1928 HK 11.1 10.1 6.3

0027 HK 11.7 9.4 -

1128 HK 12.8 10.1 4.8

6883 HK 11.9 8.1 -

2282 HK 8.4 7.0 7.2

Source: Bloomberg, CGIHK Research

September 25, 2012

Macau Gaming Sector

2

Figure 2: YTD share price performance

Source: Bloomberg, CGIHK Research, As of September 24, 2012

Figure 3: Comparable valuation table

Source: Bloomberg, CGIHK Research, As of September 24, 2012

Figure 4: Market share movement during the past five years

Source: Macau Business, CGIHK Research

3

Industry background

Macau, Las Vegas of the Orient, is the world’s largest gaming city with GGR of

MOP267.9bn in 2011, five times that of the Vegas Strip. One of the differences from

Las Vegas is Macau’s revenue composition, which is largely biased towards VIP table

gaming (2011: 73.2%, 1H12: 70.5%), followed by mass market table gaming and slot

machines. Baccarat is the most popular game in Macau.

Macau’s gambling history originates from 1847, when the Portuguese government

legalized gambling to generate more revenues from its colony. 90 years later, the gov-

ernment granted the monopoly casino concession to the Tai Xing Company in 1937,

which was taken over by Sociedade de Turismo e Diversoes de Macau (STDM) in

1962. STDM was then owned by Stanley Ho, Teddy Ip, Ip Hon and Henry Fok. The

company is now controlled by the Ho family.

The major breakthrough to create the modern Macau gaming sector occurred in 2001,

with the partial deregulation of the industry, when gaming concessions and sub-

concessions were granted to six operators, including a number of companies tracing

their origins to STDM. The extension of additional gaming rights has dramatically

transformed Macau from a VIP-focused gaming center to a more diverse location with

attractions for mass-market gamblers and tourists. With more mega-sized integrated

gaming resorts to be built in Macau, we believe mass market gaming will flourish,

supported by continuously increasing visitor arrivals from China - more cities under

the individual visit scheme (IVS) and infrastructure improvement - and increasing

disposable income (2007-2011 11.4% CAGR in urban households).

Figure 5: Macau gaming concessionaires and sub-concessionaires

Source: MGM China IPO Prospectus, CGIHK Research

Strong growth in mass market along

with increasing visitor arrivals due to:

1) more cities to be covered by IVS

2) Infrastructure improvement

4

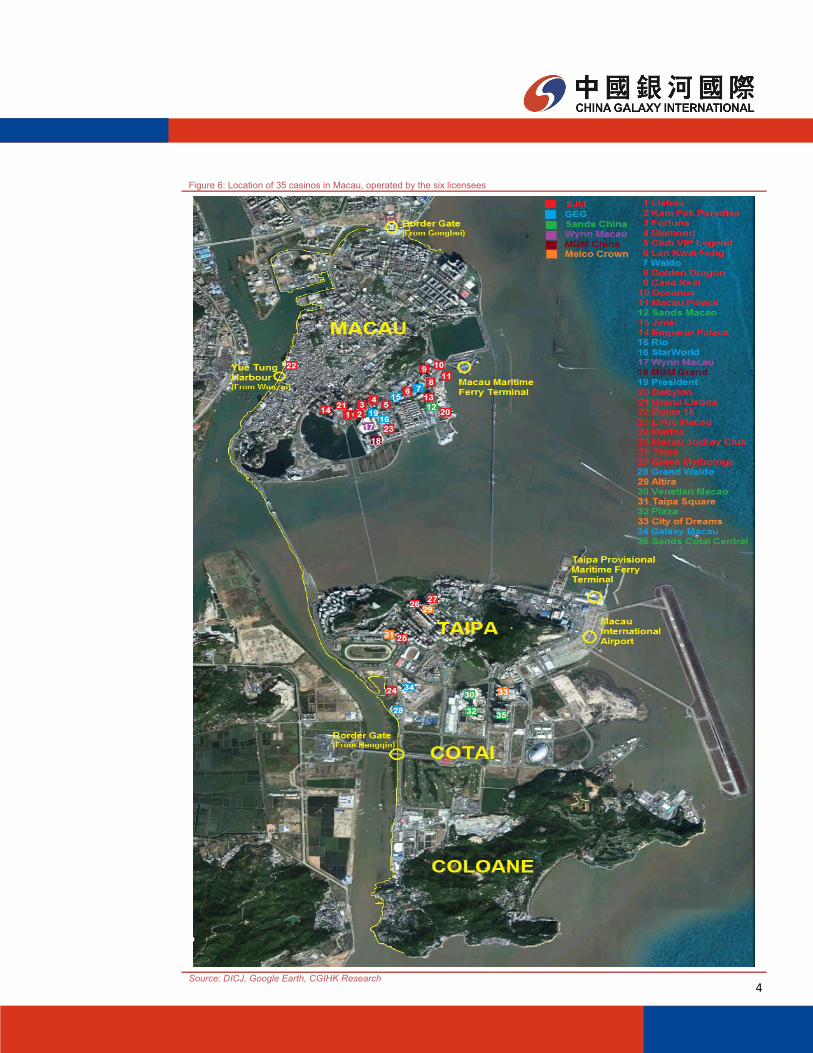

Figure 6: Location of 35 casinos in Macau, operated by the six licensees

Source: DICJ, Google Earth, CGIHK Research

Ho

w d

oe

s t

he

in

du

str

y w

ork

?

6

Market is cautious about the ever-growing Macau,

but we see such concern is overdone

In Macau, supply drives demand. Sands Macao, Wynn Macau, the Venetian Macao

and Galaxy Macau were milestones in the evolution of the Macau gaming industry. A

transformation in visitor arrivals and GGR followed the opening of new casinos. We

believe this was not merely good timing or coincidence, but the execution of a meticu-

lous strategy which led to sustained growth in gaming revenue. During 2000-2011

visitor arrivals to Macau grew at 11.8% CAGR and GGR increased much faster at

32.7% CAGR, or 17-fold to MOP268bn, which was five times of Macau’s nominal

GDP in 2000. Significant demand is created by supply of new casinos with diversified

service, in our view, and steady casino supply in long term in Cotai should continue

driving demand. This is not supply-side theory, but the reality of infrastructure and

capacity needed to absorb a continuously expanding volume of visitors. Without ac-

commodation, or distractions to attract them, visitors would not choose Macau as a

destination. The gaming industry has recognized that it must create capacity/supply so

that increasing numbers of Chinese tourists are attracted.

Opening of new casinos historically

drove visitor arrivals and GGR, and...

...Macau’s GGR in 2011 was 5x Macau’s

nominal GDP in 2000.

Supply constraint should be eased, driving demand

Figure 7: New casino openings drive visitor arrivals Figure 8: Macau GGR surges with increased supply

Source: DSEC, CGIHK Research Source: DICJ, CGIHK Research

7

Macau is suffering from supply constraints. Macau’s accommodation industry is

running at an unsustainably high occupancy rate, compared with other Asian regions

except Hong Kong and Singapore. Average hotel occupancy rate in 2011 was at a

historic high of 84.1%, while affordably good four-star and three-star hotels generated

even higher occupancy of 89.2% and 86.0%. Hotels in Macau are running at almost

100% occupancy in peak periods such as the Chinese New Year season, imposing a

cap on visitor arrivals and length of stay. Occupancy rates showed a sign of easing to

83.3% and 80% in 1Q12 and 2Q12, with c.10% increased hotel room supply from the

opening of Sands Cotai Central (SCC) Phase 1. We believe a c.7.5% increase in

rooms with Sands Cotai Central Phase 2 opening this month (September) will further

ease Macau’s occupancy level, but still not sufficient to cater to increasing visitor arri-

vals during peak seasons.

Hotel occupancy rate in Macau is one

of the highest, proving supply con-

straint.

Figure 9: Room supply and occupancy rate Figure 10: Regional hotel occupancy rates

Source: DSEC, CGIHK Research Source: DSEC, Wind, Bloomberg, CGIHK Research

More hotel rooms to be built in medium term. Several projects are in the pipeline to

be completed by 2016, which will add c.14,250 new rooms in Cotai. It will effectively

increase the hotel rooms supply by 53% from the current level of 26,800 rooms, fur-

ther easing the pressure in accommodating incoming tourists in Macau and effectively

enlarging their length of stay from the current low level of 1.3 nights. We believe that it

will be beneficial to the growth of the high-margin mass market gaming.

Hotel room supply will increase by 53%

with new properties opening in

2015/2016.

Fig

ure

11

: C

ota

i w

ith e

xis

ting a

nd in p

ipelin

e c

asin

os

Fig

ure

12

:Sch

ed

ule

of u

pcom

ing h

ote

ls/r

esort

s

Sourc

e:

Go

ogle

Eart

h,

CG

IHK

Researc

h

Sourc

e: C

om

pa

ny, C

GIH

K R

ese

arc

h

9

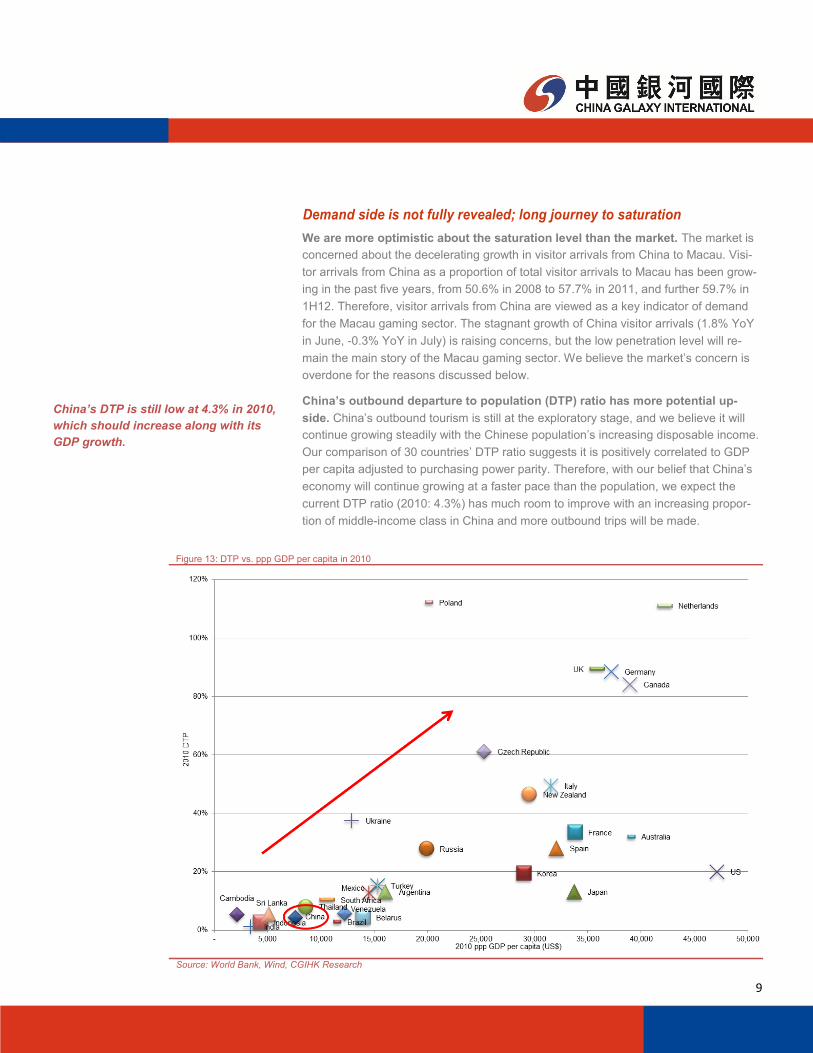

We are more optimistic about the saturation level than the market. The market is

concerned about the decelerating growth in visitor arrivals from China to Macau. Visi-

tor arrivals from China as a proportion of total visitor arrivals to Macau has been grow-

ing in the past five years, from 50.6% in 2008 to 57.7% in 2011, and further 59.7% in

1H12. Therefore, visitor arrivals from China are viewed as a key indicator of demand

for the Macau gaming sector. The stagnant growth of China visitor arrivals (1.8% YoY

in June, -0.3% YoY in July) is raising concerns, but the low penetration level will re-

main the main story of the Macau gaming sector. We believe the market’s concern is

overdone for the reasons discussed below.

China’s outbound departure to population (DTP) ratio has more potential up-

side. China’s outbound tourism is still at the exploratory stage, and we believe it will

continue growing steadily with the Chinese population’s increasing disposable income.

Our comparison of 30 countries’ DTP ratio suggests it is positively correlated to GDP

per capita adjusted to purchasing power parity. Therefore, with our belief that China’s

economy will continue growing at a faster pace than the population, we expect the

current DTP ratio (2010: 4.3%) has much room to improve with an increasing propor-

tion of middle-income class in China and more outbound trips will be made.

China’s DTP is still low at 4.3% in 2010,

which should increase along with its

GDP growth.

Demand side is not fully revealed; long journey to saturation

Figure 13: DTP vs. ppp GDP per capita in 2010

Source: World Bank, Wind, CGIHK Research

10

China’s DTP ratio to Macau is rising steadily. We believe Hong Kong and Macau

are the main beneficiaries of rising outbound tourism from China. Hong Kong and Ma-

cau are the main destinations for first-time outbound trippers, for the geographical and

cultural proximity, and Hong Kong and Macau respectively accounted for 40% and

28% of total departures to international destinations in China in 2011. The trend in the

number of trips is showing continuing improvement, proven by consistently increasing

DTP ratio for both Hong Kong and Macau from China during 2002-2011. In our view,

first-time travellers will support a continued increase in the DTP ratio to Hong Kong

and Macau, while re-visitors will be a further key to drive the Macau gaming industry in

the future.

Hong Kong and Macau are the first

destinations for China’s outbound tour-

ists.

Further easing visa policy should unlock more tourist flow. Only 300m Chinese

citizens are covered under the individual visit scheme (IVS) to Hong Kong and Macau.

As highlighted in the map (in purple), some tier-2 cities are not under IVS yet and only

23% of population are allowed to visit individually. With tightening economic and politi-

cal ties between China, Hong Kong and Macau, we do not expect further tightening

visa policies. But we do see considerable room for improvement in the future, when

the central government allows citizens of all tier-2 cities and wealthy tier-3 cities to

apply for visas directly without involving travel agencies.

Only 23% of Chinese citizens are under

IVS, and we expect further travel eas-

ing policy in long term.

Figure 14: China’s outbound departures Figure 15: China’s DTP to major destinations

Source: China National Tourism Administration, CGIHK Research Source: China National Tourism Administration, CGIHK Research

11

The Chinese government is relaxing the visa

application process in six cities (four tier-1

cities, Tianjin and Chongqing). Non-local

residents of those cities can apply visa or

passport directly in cities where they reside,

while previously they had to go back to their

original hometown, where they had Hukou

(residency permit) to make application. It will

save money and time for non-local residents

to get travel documents, with a positive effect

on tourist inflow to Macau and on gaming

revenue. Although the new policy has not yet

been activated, we see it as government’s

message to encourage interaction between

China, Hong Kong and Macau, supporting

our view of continuing visa policy relaxation.

Improving infrastructure should help mass market. With the railway system be-

coming more sophisticated in China, we expect traveling convenience will be en-

hanced. Guangzhou-Zhuhai Intercity Rail Transit’s Zhuhai Station will be available

from December 2012. It is situated next to the Gongbei border gate to Macau. We

believe this will shorten the traveling time from Guangzhou to Macau from 90min by

bus to 45min by train, and Guangzhou is one of China’s main transportation hubs.

In our view, the main beneficiary to the Macau gaming sector is the mass market seg-

ment. With lower time and travel cost from inner provinces to Zhuhai/Macau, we ex-

pect to see increases in visitor arrivals to Macau, along with improving connectivity of

Macau to other cities in China. Especially, it would effectively encourage re-visitors to

Macau, who have more sophisticated knowledge of gambling, directly contributing to

the growth of mass market gaming.

Improving infrastructure has positive

impact on mass market gaming, en-

couraging re-visitors to travel to Ma-

cau.

Figure 16: Regions and cities under IVS

Source: Google Earth, CGIHK Research

12

In the longer term, Macau is building a light rail transit (LRT) system covering the Ma-

cau Peninsula, Taipa and Cotai, linking all tourist attractions and major casinos in Ma-

cau. It is scheduled to launch in late 2015, and one of its terminals will be Gongbei

border gate, facilitating inbound tourists from Zhuhai. When all these railways are con-

nected we believe Macau will be capable of accommodating increasing numbers of

tourists. It confirms our view that Macau has much work to do on the supply side to

unlock the potential demand.

Macau’s LRT Phase 1 will be completed

in late 2015, adjacent to Gongbei bor-

der gate.

Figure 17: High speed railway network in China and Zhuhai Station Figure 18: Macau LRT route map (planned)

Source: SJM Presentation, CGIHK Research Source: DICJ, Google Earth, CGIHK Research

13

Still a cyclical play?

Historically, Macau gaming has been cyclical. The in-

dustry is commonly considered to be recession-proof, be-

cause gambling is an addictive habit and not income-

elastic. There is a presumption that the current weak eco-

nomic situation should have no impact on Macau and that

Macau’s current slow growth should be attributed to other

reasons, such as saturation.

We disagree with this argument. Data for the last five years

suggests the growth of the Macau gaming sector is posi-

tively correlated to the China’s GDP growth

(correlation=0.60). We believe the relatively mild GGR

growth in 2012 is a reflection of the slower growth in China,

and that it should accelerate with the recovery of the econ-

omy.

Figure 19: YoY growth of Macau GGR and China GDP

Source: DICJ, Wind, CGIHK Research

VIP gaming segment is cyclical. The VIP gaming segment is making a c.70% contri-

bution to the Macau gaming sector, and its volatile characteristics influence the cycli-

cality of the whole Macau gaming sector. For the same five-year period, the VIP seg-

ment YoY growth had a higher correlation of 0.63 to China GDP growth than the

whole Macau sector growth.

VIP gaming growth is positively corre-

lated to China’s GDP growth because:

Figure 20: YoY growth of VIP GGR and China GDP Figure 21: YoY growth of VIP GGR and Guangdong export

Source: DICJ, Wind, CGIHK Research Source: DICJ, Wind, CGIHK Research

14

The VIP gaming segment is mainly driven by Chinese VIP patrons, half of whom are

from Guangdong Province. It is estimated that most players from Guangdong Prov-

ince are business owners exporting manufactured products. Their time and inclination

to gamble is logically affected by their business performance. As a result, VIP gaming

growth and Guangdong export growth showed an even higher positive correlation of

0.75.

During hard times junket operators tend to be more careful in extending credit to VIP

players. VIP players play on credit in Macau and repay junket operators after they

return home. With a deteriorating economic environment and tight liquidity, it is to be

expected that junket operators would tighten their credit policy.

We believe the current slowdown in the VIP gaming segment is compounded by other

factors. A considerable portion (c.30%) of VIP players are government officials and

SOE managers. We consider they are seeking a low profile during the sensitive gov-

ernment transition period and demand from this segment could pick up late this year

or in 2013, when the political transition is completed.

1) Most VIP patrons are business

owners …

2) Junket operators tighten credit

policy for safer play …

3) Some SOE managers and officials

become more cautious during tran-

sition period.

Mass market gaming is more resilient to economic cycles. Its growth has a much

weaker correlation with China’s GDP growth (correlation=0.38), while it showed

stronger positive relationship with mainland visitor arrivals to Macau

(correlation=0.54). We believe the number could be even higher if the most recent

growth numbers were factored in, pointing to a significant boom after several integrat-

ed casinos opened in 2007.

Mass market is less correlated to GDP

growth but visitor arrivals.

Figure 22: YoY growth of mass market GGR and China GDP Figure 22: YoY growth of mass market GGR and China visitor arrivals

Source: DICJ, Wind, CGIHK Research Source: DICJ, DSEC, CGIHK Research

15

The resilience to the economic cycle can be easily explained: the trip to Hong Kong

and Macau is typically planned for a long time and budgets are mostly from savings.

The traveling cost to Hong Kong and Macau is generally considered not expensive

and people believe they can recover their transportation cost by purchasing luxury or

daily products at lower prices than in China. Therefore, we believe the decision to

travel to Macau is not directly influenced by short-term fears of reduced income, ex-

plaining why the mass gaming market has been growing fast at 43.3% and 35.1% in

1Q12 and 2Q12, while VIP gaming only grew at 23.7% and 7.5% YoY.

People’s trip plan to Hong Kong and

Macau is less sensitive to economic

environment.

The sector will become less cyclical in the future. So far, the VIP gaming segment

has been the Macau gaming sector’s main growth driver, but the picture is changing

gradually. From 4Q11, the mass market gaming segment delivered faster growth than

the VIP gaming segment due to 1) VIP segment was impacted by a weaker economy,

and 2) positive momentum in mass market gaming sustained with more visitor inflows

to mega integrated resorts such as Galaxy Macau. With faster growth in the latter we

expect increasing contribution from more cycle-resistant mass market gaming seg-

ment, and the whole sector will be less vulnerable to economic cycles. The planned

new integrated resorts in Cotai, to be commissioned in 2015-2016, will attract more

visitor arrivals to those properties, driving up the sector’s growth in the long term.

Contribution from more resilient mass

market segment is increasing.

Figure 23: YoY growth of Macau GGR and China GDP

Source: DICJ, CGIHK Research

16

VIP gaming recovery is happening. We expect the bottoming of China’s economy

will leave scope for the VIP gaming segment to regain growth momentum soon, given

the trend among international and domestic governments to kick-start their econo-

mies. China has taken some fiscal and monetary action, but more is expected after

the political transition is completed. Junket operators are normalizing their credit poli-

cies based on expectations of further easing policies, providing more liquidity to VIP

gamblers. VIP gaming’s pick-up in the last few weeks has already been confirmed by

some casino operators, and we expect the positive trend to be sustained, with full

recovery next year when the political and economic situations stabilise.

Limited risk from putative regional competitors. Several regions are trying to de-

velop casino businesses in attempts to replicate Macau’s gaming success. But we see

that it is unlikely to happen for the following reasons:

Matsu Islands (Taiwan): Geographical proximity from China (1.5hour from Fuzhou

on ferry) and famous for good natural environment. Currently no infrastructure or

reputation to attract gamblers. Still needs c.5 years to build a casino.

Vladivostok (Russia): Geographical proximity (1-1.5hour flight from Haerbin), and

easier to hire Chinese-speaking labor. Still under reviewing period and as yet no

firm plan. Extreme weather conditions and no tourist infrastructure are disad-

vantages.

Singapore, Cambodia and Philippines: Relatively far from Greater China, and

normally catering to wealthy individuals in South-East Asia such as Singapore,

Malaysia and Indonesia.

Korea and Japan: non-Chinese speaking would be a disadvantage in catering to

the needs of Chinese gamblers.

We are bullish on the sector’s long-term prospects, and valuation is attractive.

All Macau gaming companies are now profitable after huge capital expenditure for

casino property construction, and PER valuation methodology is gaining more traction

than EV/EBITDA multiples. We also take PER as our primary metric for valuation

combined with DCF methodology. The Macau gaming sector is trading at 11.1x PER

on our 2013 forecast, at the historically low range valuation level, despite our view that

growth potential remains intact with 37.7% earnings CAGR during 2011-2014. Gaming

companies are also offering relatively high yield of 4.8% on average, providing down-

side protection. In an environment of concerns about long-term growth stability, we

see upside risk based on likely earnings upgrades, and we recommend investors ac-

cumulate to benefit from eventual re-rating.

Some casino operators confirmed VIP

gaming segment is picking up.

Macau is still the king in Asia as a gam-

bling center; competitiveness of other

regions is limited.

Secular growth in long term and the

sector valuation is attractive.

Recommendation

17

Galaxy Entertainment [0027.HK, TP: HK$27.60, BUY] GEG’s execution capability was well proven by the successful opening of Galaxy Ma-

cau and its consistently outperforming StarWorld compared with other Macau Penin-

sula casinos. We like the company for its strong operation and large landbank, already

approved for casino building. Its large revenue exposure to VIP gaming implies more

room for margin improvement in the future during the transition from a VIP-centric

model to mass-market focus. Given its strong earnings growth, the 11.7x 2013 PER

offers more upside potential.

SJM [0880.HK, TP: HK$18.30, BUY] Despite its loss in market share, Macau gaming doyen Dr. Stanley Ho’s SJM is still the

market leader with the longest gaming history in Macau. Its self-operated casinos are

outperforming the market, while third-party casinos are underperforming. The contri-

bution from self-operated casinos will increase, with another casino to be built in Cotai

and SJM can relocate gaming tables from third-party casinos to self-operated casinos.

It is also considering an application for Parcels 7&8 in Cotai in the future. Its 9.1x

PER, 8.3% yield and strong cash position limits the downside, and its market-leading

position qualifies SJM as a Macau proxy and income source from dividends.

MGM China [2282.HK, TP: HK$14.90, BUY] MGM is “small but beautiful”. Although the market has discounted the stock consist-

ently after its IPO in June 2011, we believe this is not justified. It has the smallest mar-

ket share but it generates good returns. The market should realize this superior earn-

ings track record in due course and the expected Cotai land approval should spark a

re-rating. It is also trading as cheaply as SJM at 8.4x PER and 7.2% yield.

Top pick of the sector

Largest operator with high yield

Small but high operating efficiency,

decent yield

18

Wynn Macau [1128.HK, TP: HK$23.90, BUY] Good operator with unquestionable brand name. It is preferred by VIP and premium

mass gamblers. Its earnings underperformed the sector recently but we see upside in

its Cotai property opening in 2016. It is the underperformer in terms of YTD share

price movement, although it has historically been trading at premium to its peers with

the highest ROE. We expect the company will catch up to enjoy sector re-rating in

near term. The company is trading at 12.8x PER and 4.8% yield.

Sands China [1928.HK, TP: HK$29.20, HOLD] With the largest exposure to the mass-market segment, Sands China will be the first

beneficiary of our mass market growth story. But it is trading at 11.1x PER, in line with

the industry average, while we doubt SCC can become as iconic as Galaxy Macau,

due to the lack of speciality either design or service: it is large but not special. Current

valuation appears fair, in our view, while the next catalyst will be the Parcel 3 opening

– its success depending on the uniqueness of its property.

Melco Crown [6883.HK, MPEL.US, TP: HK$35.20, HOLD] Relatively new company taking modern culture concept into the gaming industry. City

of Dreams and the House of Dancing Water have become firm tourist attractions. But

Macao Studio City has not yet obtained a gaming license and this will be difficult to

achieve given all other operators are still queuing. We are sceptical about their future

plans to expand to the Philippines, Matsu Islands and Russia, since we believe Macau

still offers the best opportunity for gaming growth. Additionally, its zero-dividend policy

and 15% net debt:equity ratio by the end of 2012 do not look attractive compared with

other gaming companies. It is trading at 11.9x PER and we believe the current valua-

tion is too rich.

Good brand catering to wealthy individ-

uals.

Focuses on high-margin mass market

gaming, but already priced in.

Its new property might not have casino,

no much catalyst from Macau, valua-

tion looks rich.

19

Galaxy Entertainment [0027.HK]

We reiterate our BUY rating on GEG with a target price of HK$27.60.

Outperforming 1H12. Net profit was up from HK$378m in 1H11 to HK$3.45bn in

1H12, on a 107.2% YoY growth in revenue to HK$28.3bn. Growth of 290.9% YoY in

high-margin mass market revenue to HK$4.4bn (vs. 99.1% growth in VIP segment to

HK$21.3bn) contributed to net margin improvement from 2.8% in 1H11 to 12.2% in

1H12. No dividend was recommended.

Expect strong growth in 2012E. We forecast 2012 revenue to grow by 43.2% to

HK$58.99bn and net profit rose 103.6% YoY to and HK$6.12bn, due mainly to the full

-year contribution from Galaxy Macau. With strong operating cash flow, we expect

GEG to be in a net cash position by the end of 2012, from 31.1% net debt:equity ratio

at the end of 2011. With projects in pipeline such as Galaxy Macau Phase 2, we ex-

pect no dividend payout for the foreseeable future.

Earnings growth to remain resilient in longer term. On the transition from VIP

gaming model to mass-market focus, we expect margins to keep improving in the long

term from 7.3% in 2011 to 16% in 2014. During this period we expect EPS to grow at

a 58.6% CAGR. Apart from the strong performance in Galaxy Macau and StarWorld,

we see most upside potential in new properties coming from 2015, such as Galaxy

Macau Phase 2, 3 and 4.

Target price maintained at HK$27.60. We keep our target price unchanged, which

implies 13x PER and 10.7x EV/EBITDA for 2013. Given our DCF-derived value of

HK$32.30 per share, we are convinced that GEG is deeply undervalued at present,

with further upside when factoring in Galaxy Macau Phase 3 and 4 projects.

Maintain BUY, undemanding valuation. GEG is trading at 11.7x PER and 9.4x EV/

EBITDA on our 2013 forecast, at historical mid-range trading level. Backed by its

strong fundamentals, GEG has led the recent rally in gaming stocks, and we expect

the momentum to be sustained in the long term for its continuous margin improve-

ment. We expect the immediate catalysts are 1) strong 3Q11 results and 2) the sale

of Permira’s 5.95% holding, which is an overhang. Permira has reduced its holding,

and the residual stake is likely to be sold at some point, as the private equity group

has owned the stake in GEG for five years, with an entry level of HK$8.42.

BUY

Close: HK$24.90 (Sept 25, 2012)

Target Price: HK$27.60 (+11%)

Price Performance

Market Cap US$13,452.9m

Shares Outstanding 4,192.5m

Auditor PWC

Free Float 47.8%

52W range HK$8.69-25.95

3M average daily T/O US$46.7m

Major Shareholding Management (48.0%)

Source: Company, Bloomberg

Angela Han Lee—Analyst

(852) 3698-6318

John Mulcahy—Head of Research

(852) 3698 6889

2010 2011 2012E 2013E 2014E

Turnover (HK$m) 19,262 41,186 58,991 67,771 76,337

Net profit (HK$m) 898 3,004 6,116 8,974 12,229

Net margin (%) 4.7 7.3 10.4 13.2 16.0

EPS (HK$) 0.23 0.73 1.45 2.13 2.90

Change (%) (21.9) 219.3 99.3 46.7 36.3

PER (x) 109.2 34.2 17.2 11.7 8.6

Yield (%) - - - - -

Source: Company, CGIHK Research

Macau Gaming Sector

20

Valuation assumptions.

In our DCF model we included our projection for free cash flow from existing properties until 2022, when the current gaming li-

cense expires.

We included the net present value of Galaxy Macau Phase 2 until 2022, which is HK$7.34 per share. Galaxy Macau Phase 2 is

still under construction to open in mid-2015.

We did not include the value of Galaxy Macau Phase 3 and 4, which has not yet broken ground.

Figure 24: GEG’s ownership

Source: Company, Capital IQ, CGIHK Research

Ownership structure

21

Key financials

22

Key valuation metrics

Figure 25: Revenue/Operating profit/Net profit Figure 26: Revenue Breakdown

Source: Company, CGIHK Research Source: Company, CGIHK Research Figure 27: Margins Figure 28: ROE/ROA

Source: Company, CGIHK Research Source: Company, CGIHK Research Figure 29: PER band Figure 30: PBR band

Source: Company, Bloomberg, CGIHK Research Source: Company, Bloomberg, CGIHK Research

23

SJM Holdings [0880.HK]

We initiate coverage with a BUY rating on SJM and a target price of HK$18.30.

Relatively weak 1H12 because of third party casinos. Net profit was up by 28%

YoY to HK$3.41bn in 1H12, while revenue grew at 3.9% YoY to HK$39.26bn. Gaming

revenue was only up by 3.8% YoY to HK$38.96bn, dragged down by underperforming

third-party casinos, although Grand Lisboa outperformed the industry with 22.2% YoY

growth in revenue and 37.6% YoY growth in net profit. HK$0.10 interim dividend per

share was announced, up by 25% YoY, translating into a 16.2% payout ratio.

Some pick-up in 2H12 but little surprise expected. With scandals in the New Cen-

tury Hotel, SJM has moved 40 tables from Greek Mythology, the third-party casino

operated in the hotel. The 40 tables were to be allocated to Grand Lisboa’s VIP gam-

ing area, which has consistently outperformed the industry. We believe this will im-

prove the company’s gaming volume, but our outlook for third party casinos remains

cautious for 2H12 , given increased competition from SCC Phase 2. For 2012, we

expect revenue to grow at 7.8% to HK$81.98bn and net profit to rise 30.7% YoY to

HK$6.93bn.

Still the long-term leader. Despite the increasing competition from Cotai players,

SJM remains the market leader with 25-26% share, and Dr. Stanley Ho retains his

powerful influence in Macau. Its self-promoted casinos have delivered satisfactory

results so far and Grand Lisboa still has a particularly strong reputation in China. The

contribution from self-promoted casinos will gradually increase in the long term, since

upcoming projects will be self-promoted. Also, SJM holds 30% of total gaming tables

in Macau, which implies more room for improvement in table yields, with tables more

productively relocated to outperforming casinos in the future.

Sites 1&2, Parcels 7&8 for approval. SJM’s main disadvantage is its lack of a Cotai

presence. However, this obstacle will be eliminated when its Cotai land grants are

approved. Site 2, next to Macau Dome and Wynn Cotai, is expected to be approved

soon, in late 2012 or early 2013, for which we estimate the NPV at HK$4.60 per

share. Site 1 is also queuing for the approval after Site 2, and the management has

indicated an interest in applying for Parcels 7&8. Although the contribution from these

projects is beyond our forecast horizon, we view them as long-term revenue and profit

drivers.

BUY

Close: HK$16.32 (Sept 25, 2012)

Target Price: HK$18.30 (+12%)

Price Performance

Market Cap US$11,665.0m

Shares Outstanding 5,546.6m

Auditor Deloitte

Free Float 32.9%

52W range HK$10.08-17.61

3M average daily T/O US$12.6m

Major Shareholding STDM (55.0%)

Source: Company, Bloomberg

Angela Han Lee—Analyst

(852) 3698-6318

John Mulcahy—Head of Research

(852) 3698 6889

2010 2011 2012E 2013E 2014E

Turnover (HK$m) 57,585 76,058 81,975 90,635 99,732

Net profit (HK$m) 3,559 5,308 6,934 9,893 12,772

Net margin (%) 6.2 7.0 8.5 10.9 12.8

EPS (HK$) 0.69 0.96 1.26 1.80 2.32

Change (%) 281.5 39.4 30.7 42.7 29.1

PER (x) 23.6 16.9 13.0 9.1 7.0

Yield (%) 2.1 4.5 5.8 8.3 10.7

Source: Company, CGIHK Research

Macau Gaming Sector

24

Target price at HK$18.30. We used our DCF model to derive our target price, implying 10.2x PER and 8.4x EV/EBITDA for 2013.

Our projection for the target price does not include the potential value of upcoming projects such as Sites 1&2, leaving scope for up-

grading in medium term when there is more clarity on the projects.

Initiate with BUY, dividend play. SJM is trading at 9.1x PER and 6.7x EV/EBITDA on our 2013 forecast, a c.20% discount to the

industry average, implying limited downside risk. Beyond its attractive valuation, the 8.3% forward yield provides a good return for

long-term dividend investors. SJM’s balance sheet is the strongest in the sector with a cash cushion of HK$14.9bn with all debt paid

back by the end of this year. Management confirmed the current payout ratio is sustainable, which we assume to be 75%, as in 2011.

SJM has been trading at a discount to its peers, due mainly to the perceived lack of catalysts. Backed by the government’s imminent

land grant, we believe SJM’s valuation will gradually pick up further and the value of new projects leaves scope for re-rating in the

long term.

Valuation assumptions.

In our DCF model, we included our projection for free cash flow from existing properties until 2020, when the current gaming li-

cense expires.

We did not include the value of Sites 1&2, which has not yet been approved.

Our Site 2 NPV estimation of HK$4.60 per share will be an accretion to our target price, to be included when SJM obtains its land

grant.

Ownership structure

Figure 31: SJM’s ownership

Source: Company, HKEx, Capital IQ, CGIHK Research

25

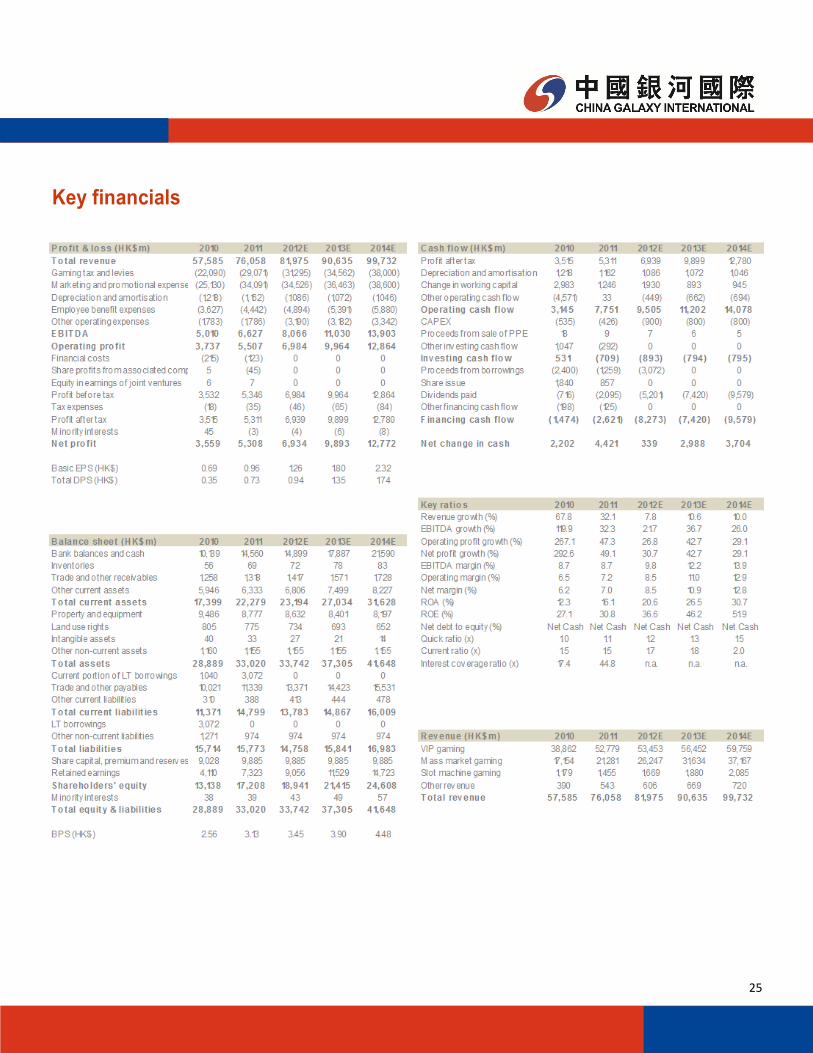

Key financials

26

Key valuation metrics

Figure 32: Revenue/Operating profit/Net profit Figure 33: Revenue Breakdown

Source: Company, CGIHK Research Source: Company, CGIHK Research

Figure 34: Margins Figure 35: ROE/ROA

Source: Company, CGIHK Research Source: Company, CGIHK Research

Figure 36: PER band Figure 37: PBR band

Source: Company, Bloomberg, CGIHK Research Source: Company, Bloomberg, CGIHK Research

27

MGM China [2282.HK] We reiterate our BUY rating on MGM China with a target price of HK$14.90.

Strong 1H12, outperformer in revenue and earnings after GEG. Net profit was up

by 37.7% YoY to HK$2.63bn in 1H12. Its revenue (after charging junket commission)

grew by 11.2% YoY to HK$10.79bn, maintaining its market share at c.10%. Strong

revenue growth (16.4%) in the mass market segment was the key to the margin im-

provement, from 17.8% in 1H11 to 22.2% in 1H12. No dividend was recommended.

Further pick-up in 2H12 due to expansion. We expect its topline growth to remain

strong and the VIP gaming area expansion on Level Two should further consolidate

its strong position in serving wealthy individuals. We believe an additional 40 VIP ta-

bles with new junkets should protect its market share from the opening of SCC Phase

2. For 2012 we expect revenue to grow by 17.1% YoY to HK$32.45bn and net profit

by 51.1% to HK$4.96bn, in line with management guidance of 15-20% revenue

growth. For the longer term we project 29% EPS CAGR during 2011-2014.

Long-term catalyst on the way. Wynn Macau obtained a land grant for Cotai in May

2012, and MGM China is next in line. This is likely by the end of 2012 and the man-

agement expects to break ground by then with a plan to complete by late 2015.

Target price at HK$14.90. We maintain an unchanged target price, driven by our

DCF model for the existing property, MGM Macau. It implies 9.3x PER and 7.4x EV/

EBITDA for 2013. Our projection for the target price does not include the potential

value of its Cotai project, leaving scope for upgrading by its NPV of HK$3.10 per

share after it obtains land grant.

Maintain BUY, compelling value play. MGM China is trading at 8.4x PER and 7.0x

EV/EBITDA on our 2013 forecast, a c.30% discount to Wynn Macau, which we be-

lieve is the closest comparable. They both have their sole casino in Macau Peninsula

with a strong focus on premium service, and seeking exposure in Cotai. However,

MGM China has often been overlooked by the market since listing in June 2011 be-

cause of its small market share. We believe the market will begin paying more atten-

tion in future to its small but solid growth outperforming the industry, narrowing the

valuation gap in the long term. As a catalyst, we expect the land grant in Cotai to trig-

ger a re-rating, once the value of the new property is factored into its target price. In

addition, the 7.2% forward yield provides a good return, for which we assume 60%

payout ratio in 2012 (2011: 95%) backed by its net cash position from 2011.

BUY

Close: HK$13.12 (Sept 25, 2012)

Target Price: HK$14.90 (+14%)

Price Performance

Market Cap US$6,424.7m

Shares Outstanding 3,800.0m

Auditor Deloitte

Free Float 21.6%

52W range HK$7.60-14.76

3M average daily T/O US$4.1m

Major Shareholding MGM Resorts

(51.0%)

Source: Company, Bloomberg

Angela Han Lee—Analyst

(852) 3698-6318

John Mulcahy—Head of Research

(852) 3698 6889

2010 2011 2012E 2013E 2014E

Turnover (HK$m) 16,608 27,719 32,450 36,686 41,133

Net profit (HK$m) 1,566 3,279 4,955 5,954 7,040

Net margin (%) 9.4 11.8 15.3 16.2 17.1

EPS (HK$) 0.41 0.86 1.30 1.57 1.85

Change (%) N.A. 109.4 51.1 20.2 18.2

PER (x) 31.8 15.2 10.1 8.4 7.1

Yield (%) 0.0 6.2 6.0 7.2 8.5

Source: Company, CGIHK Research

Macau Gaming Sector

28

Valuation assumptions.

In our DCF model we included our projection for free cash flow from existing property until 2020, when the current gaming li-

cense expires.

We did not include the value of its Cotai project, which has not yet been approved.

Our estimate of the Cotai project’s NPV of HK$3.10 per share will be an accretion to our target price, to be included when MGM

China obtains its land grant.

Ownership structure

Figure 38: MGM China’s ownership

Source: Company, HKEx CGIHK Research

29

Key financials

30

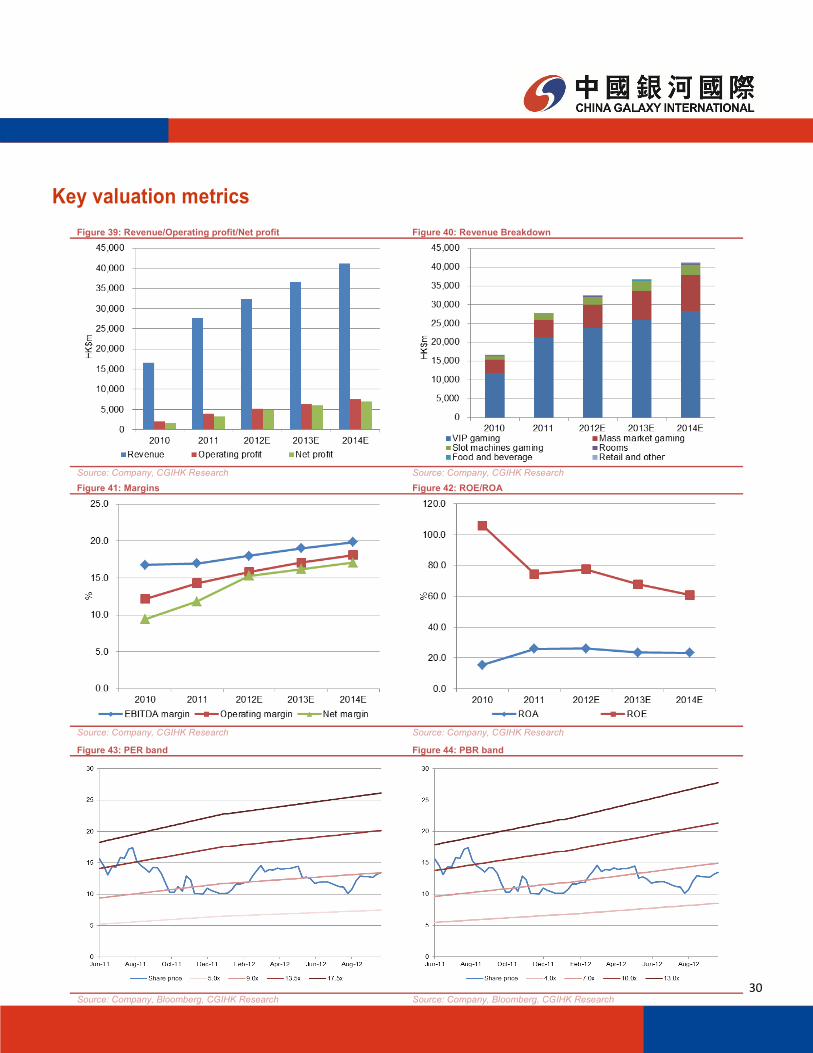

Key valuation metrics

Figure 39: Revenue/Operating profit/Net profit Figure 40: Revenue Breakdown

Source: Company, CGIHK Research Source: Company, CGIHK Research Figure 41: Margins Figure 42: ROE/ROA

Source: Company, CGIHK Research Source: Company, CGIHK Research

Figure 43: PER band Figure 44: PBR band

Source: Company, Bloomberg, CGIHK Research Source: Company, Bloomberg, CGIHK Research

31

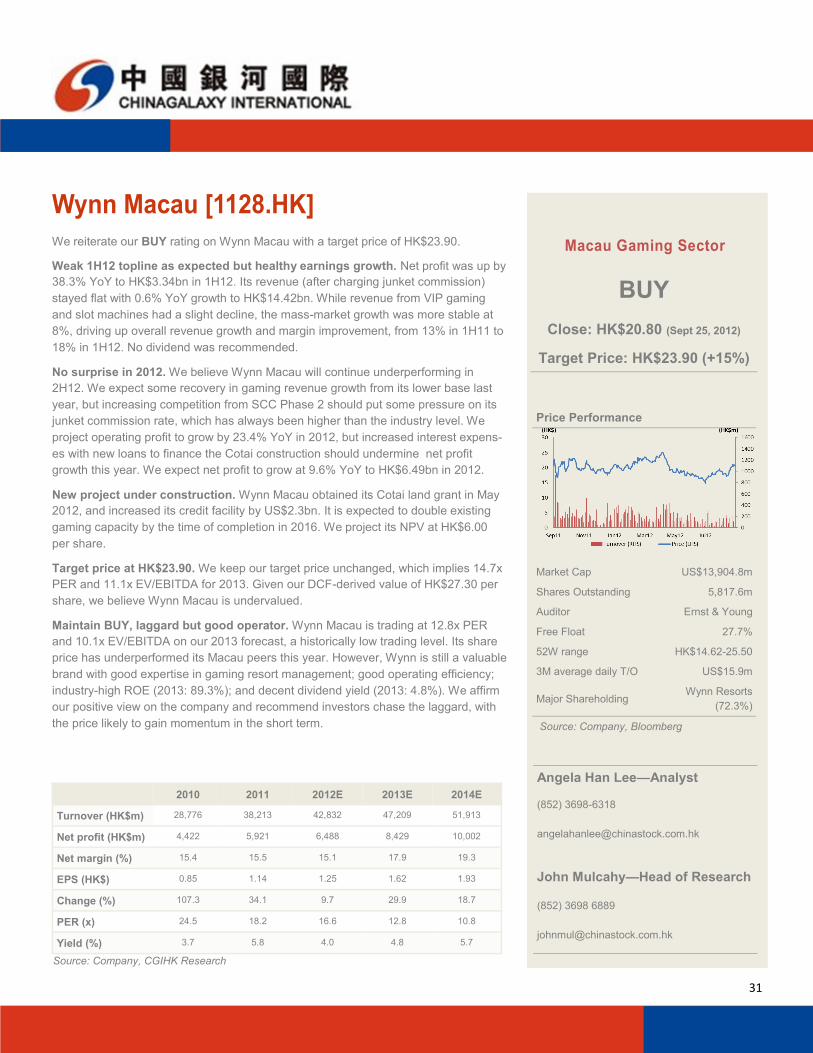

Wynn Macau [1128.HK]

We reiterate our BUY rating on Wynn Macau with a target price of HK$23.90.

Weak 1H12 topline as expected but healthy earnings growth. Net profit was up by

38.3% YoY to HK$3.34bn in 1H12. Its revenue (after charging junket commission)

stayed flat with 0.6% YoY growth to HK$14.42bn. While revenue from VIP gaming

and slot machines had a slight decline, the mass-market growth was more stable at

8%, driving up overall revenue growth and margin improvement, from 13% in 1H11 to

18% in 1H12. No dividend was recommended.

No surprise in 2012. We believe Wynn Macau will continue underperforming in

2H12. We expect some recovery in gaming revenue growth from its lower base last

year, but increasing competition from SCC Phase 2 should put some pressure on its

junket commission rate, which has always been higher than the industry level. We

project operating profit to grow by 23.4% YoY in 2012, but increased interest expens-

es with new loans to finance the Cotai construction should undermine net profit

growth this year. We expect net profit to grow at 9.6% YoY to HK$6.49bn in 2012.

New project under construction. Wynn Macau obtained its Cotai land grant in May

2012, and increased its credit facility by US$2.3bn. It is expected to double existing

gaming capacity by the time of completion in 2016. We project its NPV at HK$6.00

per share.

Target price at HK$23.90. We keep our target price unchanged, which implies 14.7x

PER and 11.1x EV/EBITDA for 2013. Given our DCF-derived value of HK$27.30 per

share, we believe Wynn Macau is undervalued.

Maintain BUY, laggard but good operator. Wynn Macau is trading at 12.8x PER

and 10.1x EV/EBITDA on our 2013 forecast, a historically low trading level. Its share

price has underperformed its Macau peers this year. However, Wynn is still a valuable

brand with good expertise in gaming resort management; good operating efficiency;

industry-high ROE (2013: 89.3%); and decent dividend yield (2013: 4.8%). We affirm

our positive view on the company and recommend investors chase the laggard, with

the price likely to gain momentum in the short term.

BUY

Close: HK$20.80 (Sept 25, 2012)

Target Price: HK$23.90 (+15%)

Price Performance

Market Cap US$13,904.8m

Shares Outstanding 5,817.6m

Auditor Ernst & Young

Free Float 27.7%

52W range HK$14.62-25.50

3M average daily T/O US$15.9m

Major Shareholding Wynn Resorts

(72.3%)

Source: Company, Bloomberg

Angela Han Lee—Analyst

(852) 3698-6318

John Mulcahy—Head of Research

(852) 3698 6889

2010 2011 2012E 2013E 2014E

Turnover (HK$m) 28,776 38,213 42,832 47,209 51,913

Net profit (HK$m) 4,422 5,921 6,488 8,429 10,002

Net margin (%) 15.4 15.5 15.1 17.9 19.3

EPS (HK$) 0.85 1.14 1.25 1.62 1.93

Change (%) 107.3 34.1 9.7 29.9 18.7

PER (x) 24.5 18.2 16.6 12.8 10.8

Yield (%) 3.7 5.8 4.0 4.8 5.7

Source: Company, CGIHK Research

Macau Gaming Sector

32

Valuation assumptions.

In our DCF model, we included our projection for free cash flow from existing property until 2022, when the current gaming li-

cense expires.

We included the net present value of Cotai project until 2022, which is HK$6.00 per share. Its Cotai project is still under construc-

tion to open in 2016.

Ownership structure

Figure 45: Wynn Macau’s ownership

Source: Company, HKEx, CGIHK Research

33

Key financials

34

Key valuation metrics

Figure 46: Revenue/Operating profit/Net profit Figure 47: Revenue Breakdown

Source: Company, CGIHK Research Source: Company, CGIHK Research Figure 48: Margins Figure 49: ROE/ROA

Source: Company, CGIHK Research Source: Company, CGIHK Research Figure 50: PER band Figure 51: PBR band

Source: Company, Bloomberg, CGIHK Research Source: Company, Bloomberg, CGIHK Research

35

Sands China [1928.HK]

We initiate coverage with a HOLD rating on Sands China with target price of

HK$29.20.

Weak 1H12 mainly for one-off item. Net profit was down by 18.5% YoY to

US$439.8m in 1H12. Its revenue grew faster than the industry with 23.7% YoY growth

to US$2.92bn, due to its strategy of expanding VIP gaming segment in the Plaza Ma-

cao. However, one-off impairment charge of US$143.7m occurred, because of 1) the

capitalized construction cost on Parcels 7&8 which was not approved for Sands Chi-

na’s use, and 2) the closure of the Cirque du Soleil “ZAiA” show at the Venetian Ma-

cao. As a result, net margin deteriorated from 22.9% in 1H11 to 15.1% in 1H12. No

dividend was recommended.

SCC Phase 2 opened in September, but we expect no surprise. SCC Phase 1

opening was not as impressive as Galaxy Macau’s, and we see SCC as a big but not

attractive property. With more casino properties being built in Macau the uniqueness

(“WOW Factor”) of those properties is important in capturing the flow of mass-market

players. With no iconic features we expect SCC to take longer to ramp-up than the

market had expected. We forecast 38.2% revenue growth and 36.2% net profit growth

in 2012.

Good mass market player with Parcel 3 under construction. Although its 2012

margins will be under pressure for one-off items, Sands China is a good operator with

more focus on mass market. Even though the company has gained some market

share in the VIP gaming segment, we still project it to generate around 65% of its

gaming revenue from the VIP segment, compared with the 70% industry level. The

next catalyst for Sands China is its Parcel 3 project, which will break ground in No-

vember and a completion deadline of April 2016. Parcel 3 will be known as “The Pa-

risian” and will have a replica of Eiffel Tower, which should differentiate it as a tourist

attraction.

Target price at HK$29.20. We used our DCF model to derive our target price, imply-

ing 11.3x PER and 10.2x EV/EBITDA for 2013. Our projection for the target price

does not include the potential value of Parcel 3, leaving scope for upgrading in the

medium term when there is more clarity on the Cotai project.

HOLD

Close: HK$28.60 (Sept 25, 2012)

Target Price: HK$29.20 (+2%)

Price Performance

Market Cap US$29,675.5m

Shares Outstanding 8,051.8m

Auditor PWC

Free Float 29.7%

52W range HK$14.90-33.05

3M average daily T/O US$49.1m

Major Shareholding Las Vegas Sands

(70.3%)

Source: Company, Bloomberg

Angela Han Lee—Analyst

(852) 3698-6318

John Mulcahy—Head of Research

(852) 3698 6889

2010 2011 2012E 2013E 2014E

Turnover (US$m) 4,142 4,881 6,746 9,921 11,825

Net profit (US$m) 666 1,133 1,543 2,672 3,369

Net margin (%) 16.1 23.2 22.9 26.9 28.5

EPS (HK$) 0.64 1.09 1.49 2.58 3.25

Change (%) 150.1 69.7 36.0 73.2 26.1

PER (x) 44.4 26.1 19.2 11.1 8.8

Yield (%) 0.0 4.1 3.6 6.3 7.9

Source: Company, CGIHK Research

Macau Gaming Sector

36

Initiate with HOLD, fairly valued with no near-term catalyst. Sands China is trading at 11.1x PER and 10.1x EV/EBITDA on our

2013 forecast, at a slight premium to the industry average. For its brand name with experience in gaming resort management, the

stock has always traded at a premium. However, our DCF model suggests the current share price has factored in the upside. There is

no basis for an extremely negative view, as we see Parcel 3 as a potential long-term catalyst and SCC should ramp-up gradually, so

we recommend long-term investors to hold.

Valuation assumptions.

In our DCF model, we included our projection for free cash flow from existing property including SCC until 2022, when the current

gaming license expires.

We did not include the value of Parcel 3 project, which is still preparing for construction to open in 2016, as SCC Phase 2B and

Phase 3 are still in progress.

Ownership structure

Figure 52: Sands China’s ownership

Source: Company, HKEx, CGIHK Research

37

Key financials

38

Key valuation metrics

Figure 53: Revenue/Operating profit/Net profit Figure 54: Revenue Breakdown

Source: Company, CGIHK Research Source: Company, CGIHK Research Figure 55: Margins Figure 56: ROE/ROA

Source: Company, CGIHK Research Source: Company, CGIHK Research Figure 57: PER band Figure 58: PBR band

Source: Company, Bloomberg, CGIHK Research Source: Company, Bloomberg, CGIHK Research

39

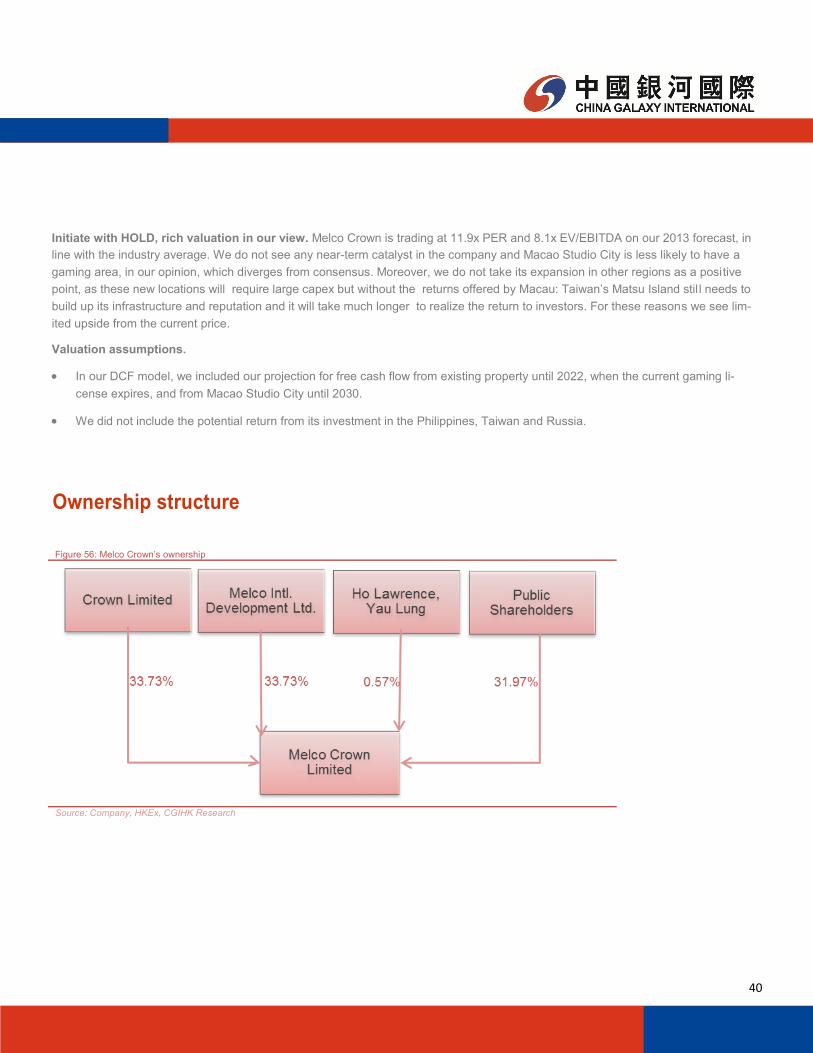

Melco Crown [6883.HK]

We initiate coverage with a HOLD rating on Melco Crown and a target price of

HK$35.20.

In line 1H12. Net profit was up from US$73.8m in 1H11 to US$204.4m in 1H12, while

revenue (after charging junket commission) was up by 11.3% YoY to US$1.97bn.

Stronger growth in earnings is due to the rising operating leverage, after turning a net

loss into net profit in 2011. It is relocating tables from Altira to City of Dreams, which

has a higher table yield, optimizing facility efficiency. No dividend was recommended.

No surprise in 2H12. We expect 2H12 performance will be in line with 1H12, and

project revenue growth at 9.1% to US$5.62bn and net profit to grow 50.8% YoY to

US$444m. Slower YoY growth in earnings is attributable to increasing construction

cost for Macao Studio City.

Uncertainty in Macao Studio City and its future plan. In July 2012, Macau Studio

City received a permit to restart construction of the project, in which Melco Crown has

60% equity interest. Despite the management’s promise the land grant was approved

without a gaming license. Although the management is confident of obtaining it, we

are less optimistic, and rate the chances quite low. The Macau government said all

casino operators will own a casino in Cotai, and MGM China and SJM are still queu-

ing after the approval to Wynn Macau. Melco Crown already runs City of Dreams in

Cotai, so we believe the licensing priority will go to MGM China and SJM. Outside

Macau, Melco Crown is actively working to open casinos in the Philippines, Taiwan

and Russia. Although these could be good businesses, we prefer operators focusing

in Macau, which is the regional/global centre of casino gambling and an established

reputation and infrastructure.

Target price at HK$35.20. Our DCF-driven target price implies 12.6x PER and 8.3x

EV/EBITDA for 2013. The target price includes the potential value of the non-gaming

Macau Studio City until 2030, which is independent from the expiry date of gaming

sub-concession.

HOLD

Close: HK$33.30 (Sept 25, 2012)

Target Price: HK$35.20 (+6%)

Price Performance

Market Cap US$7,115.1m

Shares Outstanding 1,658.1m

Auditor Deloitte

Free Float 32.0%

52W range HK$22.40-43.00

3M average daily T/O US$34,137.7

Major Shareholding Crown (33.7%)

Melco (33.7%)

Source: Company, Bloomberg

Angela Han Lee—Analyst

(852) 3698-6318

John Mulcahy—Head of Research

(852) 3698 6889

2010 2011 2012E 2013E 2014E

Turnover (US$m) 3,601 5,153 5,619 6,106 6,688

Net profit (US$m) (11) 295 444 593 826

Net margin (%) (0.3) 5.7 7.9 9.7 12.4

EPS (HK$) (0.05) 1.43 2.10 2.80 3.90

Change (%) n.a. n.a. 47.2 33.3 39.5

PER (x) (648.9) 23.4 15.9 11.9 8.5

Yield (%) 0.0 0.0 0.0 0.0 0.0

Source: Company, CGIHK Research

Macau Gaming Sector

40

Initiate with HOLD, rich valuation in our view. Melco Crown is trading at 11.9x PER and 8.1x EV/EBITDA on our 2013 forecast, in

line with the industry average. We do not see any near-term catalyst in the company and Macao Studio City is less likely to have a

gaming area, in our opinion, which diverges from consensus. Moreover, we do not take its expansion in other regions as a positive

point, as these new locations will require large capex but without the returns offered by Macau: Taiwan’s Matsu Island stil l needs to

build up its infrastructure and reputation and it will take much longer to realize the return to investors. For these reasons we see lim-

ited upside from the current price.

Valuation assumptions.

In our DCF model, we included our projection for free cash flow from existing property until 2022, when the current gaming li-

cense expires, and from Macao Studio City until 2030.

We did not include the potential return from its investment in the Philippines, Taiwan and Russia.

Ownership structure

Figure 56: Melco Crown’s ownership

Source: Company, HKEx, CGIHK Research

41

Key financials

42

Key valuation metrics

Figure 57: Revenue/Operating profit/Net profit Figure 58: Revenue Breakdown

Source: Company, CGIHK Research Source: Company, CGIHK Research

Figure 59: Margins Figure 60: ROE/ROA

Source: Company, CGIHK Research Source: Company, CGIHK Research

Figure 61: PER band Figure 62: PBR band

Source: Company, Bloomberg, CGIHK Research Source: Company, Bloomberg, CGIHK Research

43

DISCLAIMER

For private perusal only. This report (including any information attached) is issued by China Galaxy International Securities (Hong Kong) Co.,

Limited, one of the subsidiaries of the China Galaxy International Financial Holdings Limited, to individual addressee whether they are pro-

fessional investor, institutional client or otherwise, in good faith from sources believed to be reliable but no representation or warranty

(expressly or implied) is made as to their accuracy, correctness and/or completeness. Where any part of the information, opinions or esti-

mates contained herein reflects the personal views and opinions of the analyst who prepared this report, such views and opinions may not

correspond to the published view of China Galaxy International Financial Holdings Limited and any of its subsidiaries. This report shall not be

construed as an offer, invitation or solicitation to buy or sell any securities of the company or companies referred to herein. All opinions and

estimates reflect the judgment of the analyst on the date of this report and are subject to change without notice.

Please take note that member companies of China Galaxy International Financial Holdings Limited (including but not limited to China Galaxy

International Securities (Hong Kong) Co., Ltd) and/or their directors, officers, agents and employees (“the Relevant Parties”) may have an

interest in securities of the company or companies referred to in this report. The Relevant Parties hereby disclaim any of their liabilities aris-

ing from the inaccuracy, incorrectness and incompleteness of this report and its attachment(s) and/or any action or omission made in reli-

ance thereof. Accordingly, this report must be read in conjunction with this disclaimer.

COPYRIGHT RESERVED

China Galaxy International Securities (Hong Kong) Co. Limited, CE No.AXM459, Room 3501-3507, 35/F, Cosco Tower, Grand Millennium

Plaza, 183 Queen’s Road Central, Sheung Wan, Hong Kong. General line: 3698-6888.

Analyst Certification The research analyst who is primarily responsible for the content of this research report, in whole or in part, certifies that with respect to the

securities or issuer covered in this report: (1) all of the views expressed accurately reflect his or her personal views about the subject, securi-

ties or issuer; and (2) no part of his or her compensation was, is, or will be, directly or indirectly, related to the specific views expressed by the

analyst in this report.

Besides, the analyst confirms that neither the analyst nor his/her associates (as defined in the code of conduct issued by The Hong Kong

Securities and Futures Commission) (1) have dealt in or traded in the stock(s) covered in this research report within 30 calendar days prior to

the date of issue of this report; (2) will deal in or trade in the stock(s) covered in this research report three business days after the date of issue

of this report; (3) serve as an officer of any of the Hong Kong listed companies covered in this report; and (4) have any financial interests in

the Hong Kong listed companies covered in this report.

Explanation on Equity Ratings

BUY: We expect the total return on the stock to exceed 20% over a 12 to 18 month horizon.

HOLD: We expect the total return on the stock will be between 0% to 20% over a 12 to 18 month horizon.

SELL: We expect the total return on the stock will be less than 0% over a 12 to 18 month horizon.