Embed Size (px)

Citation preview

38th

Floor, One Corporate Centre Julia Vargas corner Meralco Avenue Ortigas Center, Pasig 1605 Tel: +63 (2) 667-7332 / +63(2) 755-2332 Fax: +63 (2) 982-2141

May 14, 2012

MA. CONCEPCION M. MAGDARAOG

Market Regulatory Services Group

Philippine Dealing & Exchange Corp.

37/F, Tower 1, The Enterprise Center

6766 Ayala Ave. cor. Paseo de Roxas

Makati City

Dear Ms. Magdaraog:

In compliance with the disclosure requirements of the PSE, we submit the attached

Energy Development Corporation (Consolidated) Quarterly Report for the period ended

March 31, 2012 (SEC Form 17-Q)

SEC Form 17Q – 1Q 2012

SEC Number 66381

File Number _____

ENERGY DEVELOPMENT CORPORATION

(Company’s full Name)

One Corporate Centre Julia Vargas cor. Meralco Ave., Ortigas Center, Pasig City

(Company’s Address)

(632) 755-2332

(Telephone Number)

March 31, 2012

(Quarter Ending)

SEC FORM 17-Q

(Form Type)

SEC Form 17Q – 1Q 2012

PART 1 FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

Our unaudited consolidated financial statements for the quarter ended March 31, 2012

have been prepared in accordance with Philippine Financial Reporting Standards (PFRS)

and are filed as Annex I of this report.

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS (“MD & A”) The following is a discussion and analysis of the Company’s consolidated financial

performance for the quarter ended March 31, 2012. The prime objective of this MD&A

is to help the readers understand the dynamics of our Company’s business and the key

factors underlying our financial results. Hence, our MD&A is comprised of a discussion of

our core business and an analysis of the results of operations. This section also focuses on

key statistics from the unaudited financial statements and pertains to risks and uncertainties

relating to the geothermal power industry in the Philippines where we operate up to the

stated reporting period. However, our MD&A should not be considered all inclusive, as it

excludes unknown risks, uncertainties and changes that may occur in the general economic,

political and environment condition after the stated reporting date.

Our MD&A should be read in conjunction with our unaudited consolidated financial

statements and the accompanying notes. All financial information is reported in Philippine

Pesos (PhP) unless otherwise stated.

Any references in this MD&A to “we”, “us”, “our”, “Company” means the Energy

Development Corporation and its subsidiaries.

Additional information about the Company can be found on our corporate website

www.energy.com.ph.

SEC Form 17Q – 1Q 2012 4

The following is a summary of the key sections of this MD&A:

OVERVIEW OF OUR BUSINESS ..............................................................................................5 Principal Products or Services ........................................................................................................ 5

Percentage of sales or revenues contributed by foreign sales ......................................................... 5

Distribution methods of products or services ................................................................................. 6

Competition..................................................................................................................................... 6

Dependence on one or a few major customers and identity of any such major customers ............ 7

KEY PERFORMANCE INDICATORS ......................................................................................8

FINANCIAL HIGHLIGHTS .........................................................................................................9

RESULTS OF OPERATIONS ...................................................................................................10

Net Income ....................................................................................................................................13 CAPITAL AND LIQUIDITY RESOURCES ............................................................................14 FINANCIAL POSITION ............................................................................................................15

Horizontal and Vertical Analysis of Material Changes as of March 31, 2012 and December

31, 2011..................................................................................................................................... 15

Horizontal and Vertical Analysis of Material Changes as of March 31, 2012 and 2011. ........ 19

CASH FLOW ...............................................................................................................................24 DISCUSSION ON THE SUBSIDIARIES .................................................................................25

FG Hydro .................................................................................................................................. 25 Green Core Geothermal Inc. ..................................................................................................... 26

Bac-Man Geothermal Inc. ......................................................................................................... 27

FOREIGN EXCHANGE AND INTEREST RATE EXPOSURE ...........................................28 OTHER MATTERS ....................................................................................................................28

MAJOR STOCKHOLDERS ......................................................................................................29 BOARD OF DIRECTORS ..........................................................................................................30

OFFICERS ...................................................................................................................................30

SEC Form 17Q – 1Q 2012 5

OVERVIEW OF OUR BUSINESS

Principal Products or Services

As of March 31, 2012, the Company operates twelve geothermal steam fields in the five

geothermal service contract areas where it is principally involved in:

i. the production of geothermal steam for sale to National Power Corporation (NPC)

pursuant to Steam Sales Agreements (SSAs) and

ii. the generation and sale of electricity through Company-owned geothermal power plants

to NPC and privately-owned distribution utilities (DUs), pursuant to Power Purchase

Agreements (PPAs) and Electricity Sales Agreements (ESAs), respectively.

Starting September 3, 2010, on account of the extended waiver, the Company ceased billing to

NPC after Bacman Geothermal Inc’s (BGI) successful acquisition of the plants from NPC.

Through its 60% equity interest in First Gen Hydro Power Corporation (FG Hydro), the

Company indirectly operates the 120 MW Pantabangan and 12 MW Masiway Hydroelectric

Power Plants, located in Pantabangan, Nueva Ecija Province, Central Luzon. The power plants

supply electricity into the Luzon grid to service the consumption of its customers which include

the Wholesale Electricity Spot Market (WESM), distribution utilities covered by bilateral

contract quantities (BCQ) and the National Grid Corporation of the Philippines (NGCP) for

ancillary services.

For the Company’s third business segment, Energy Development Corporation (EDC) provides

drilling services to the Lihir Gold Limited in Papua New Guinea.

The Company has evolved into being the country’s premier pure renewable energy play,

possessing interests in geothermal energy and hydro power. For geothermal energy, its expertise

spans the entire geothermal value chain, i.e., from geothermal energy exploration and

development, reservoir engineering and management, engineering design and construction,

environmental management and energy research and development. With FG Hydro, the

Company has not only acquired expertise in hydropower operation and maintenance, but also the

capability to sell power on a merchant basis.

Percentage of sales or revenues contributed by foreign sales

The Company generated P167.6 million from the contract it entered into with Lihir Gold Limited

(LGL) in Papua, New Guinea. This represents 2.2% of the Company’s P7,704.3 million gross

revenues for the first quarter of 2012. For the fifth consecutive time, the Company’s contract

with LGL was once again renewed and extended up to December 31, 2012.

SEC Form 17Q – 1Q 2012 6

Distribution methods of products or services

The Company’s 1,866.4 GWh total sales volume comprised of 1,627.1 GWh coming from

electricity production in Leyte, Mindanao, Tongonan I and Palinpinon geothermal power plants;

148.9 GWh in Bac-Man geothermal power plants (BMGPP) and 90.4 GWh from FG Hydro’s

Pantabangan-Masiway hydro power plants. About 60.0% or 1,119.2 GWh generated by Leyte

and Mindanao was sold to NPC. The 1,627.1 GWh generated by Tongonan I, Palinpinon I and II

was sold to electric cooperatives and industrial customers in the Visayas region and the

Wholesale Electricity Spot Market (WESM). BGI purchased 148.9 GWh to serve its contractual

obligations to BATELEC and Linde Philippines. Electricity production of about 90.4 GWh, by

FG Hydro’s power plants, was sold to the distribution utility clients comprised of electric

cooperatives in the province of Nueva Ecija, the WESM and NGCP for ancillary services.

The electricity generated by the Company’s geothermal power plants is transmitted to customers

i.e., distribution utilities, electric cooperatives or bulk power customers by the NGCP through its

high voltage backbone system.

FG Hydro generated 90.4 GWh of electricity as of first quarter of 2012, of which 68% or

61.1 GWh was delivered to its contracted customers and 32% or 14.8 GWh was sold to the

WESM.

Competition

The Company competes with other energy sources used for the production of power, particularly

coal, gas and oil, substantially all of which is imported.

Under the Company’s Geothermal Renewable Energy Service Contracts (GRESCs), it has long-

term exclusive rights to explore, develop, and utilize geothermal steam resources in specific

areas. Substantially all of the Company’s power capacity is sold through various offtake

agreements, such as PPAs for the supply of electricity to NPC and ESAs with DUs. Since most

these agreements provide for take-or-pay quantities, the Company is not subject to direct

competition. Furthermore, the supply of steam is location-specific, such that each power plant

can only source its fuel from a dedicated nearby steam field.

On May 5, 2010, BGI, the Company’s wholly-owned subsidiary through EDC Geothermal

Corporation, submitted the winning bid of US$28.25 million for PSALM’s auction of the 150

MW BMGPP located in the towns of Bacon, Sorsogon Province and Manito, Albay Province.

The power plants were turned over to BGI in September 2010, and are currently under

rehabilitation to restore capacity and reliability.

The only other Philippine company engaged in the production of steam is Chevron Geothermal

Philippines Holdings. Aboitiz Power Corporation, a power distribution and generation company,

successfully bid for the 747 MW Tiwi-Makban geothermal power plant. Multinationals that

currently operate in the Philippines include Korea Electric Power Corporation, Marubeni,

CalEnergy, Tokyo Electric Power Company, AES and Sumitomo.

SEC Form 17Q – 1Q 2012 7

Dependence on one or a few major customers and identity of any such major customers

Close to 43.0% of the Company’s total revenues are derived from existing long-term PPAs with

NPC.

Concessions and government share payments

The five geothermal service contract areas where the EDC’s geothermal production steam fields

are located are:

• Tongonan Geothermal Project (expiring in 2031)

• Southern Negros Geothermal Project (expiring in 2031)

• Bacon-Manito Geothermal Project (expiring in 2031)

• Mt. Apo Geothermal Project (expiring in 2042)

Northern Negros Geothermal Project (expiring in 2044)

The Company also holds service contracts for the following prospect areas:

Geothermal Resource

1. Mt Cabalian Geothermal Project (expiring by 2034)

2. Mt. Labo Geothermal Project (with a five-year pre-development period expiring in 2015,

25-year contract period expiring in 2035)

3. Mainit Geothermal Project (with a five-year pre-development period expiring in 2015,

25-year contract period expiring in 2035)

Wind Resource

1. Burgos Wind Project (WESC assigned by EDC to EDC Burgos Wind Power

Corporation)

Under DOE Certificate of Registration No. WESC 2009-09-004 (pre-development stage

expiring in 2012, 25-year contract period expiring in 2034)

2. Pagudpud Wind Project,

Under DOE Certificate of Registration No. WESC 2010-02-040 (pre-development stage

expiring in 2013, 25-year contract period expiring in 2035)

3. Camiguin Wind Project,

Under DOE Certificate of Registration No. WESC 2010-02-041 (pre-development stage

expiring in 2013, 25-year contract period expiring in 2035)

SEC Form 17Q – 1Q 2012 8

KEY PERFORMANCE INDICATORS

The top five (5) key performance indicators are set forth below:

Ratio

Mar – 12

Mar – 11

Current Ratio 1.89:1 2.44:1

Debt-to-Equity Ratio 1.63:1 1.75:1

Net Debt-to-Equity Ratio 1.21:1 1.10:1

Return on Assets (%) 2.45 2.28

Return on Equity (%) 7.48 6.67

Current Ratio – Total current assets divided by total current liabilities

This ratio is a rough indication of a company’s ability to pay its short-term obligations.

Generally, a current ratio above 1.00 is indicative of a company’s greater capability to settle

its current obligations.

Debt-to-Equity Ratio – Total interest-bearing debts divided by stockholders’ equity

This ratio expresses the relationship between capital contributed by the creditors and the

owners. The higher the ratio, the greater the risk being assumed by the creditors. A lower

ratio generally indicates greater long-term financial safety.

Net-Debt-to-Equity Ratio – Total interest-bearing debts less cash & cash equivalents

divided by stockholders’ equity

This ratio measures the company’s financial leverage and stability. A negative net debt-to-equity

ratio means that the total of cash and cash equivalents exceeds interest-bearing

liabilities.

Return on Assets – Net income (annual basis) divided by total assets (average)

This ratio indicates how profitable a company is relative to its total assets. This also gives an

idea as to how efficient management is at using its assets to generate earnings.

Return on Equity – Net income (annual basis) divided by total stockholders’ equity (average)

This ratio reveals how much profit a company earned in comparison to the total amount of

shareholder equity found on the balance sheet. A business that has a high return on equity is

more likely to be one that is capable of internally generating cash. For the most part, the

company’s return on equity is compared with an industry average. The company is

considered superior if its return on equity is greater than the industry average.

SEC Form 17Q – 1Q 2012 9

OPERATING REVENUES AND EXPENSES

FINANCIAL HIGHLIGHTS

The recurring net income generated in the first quarter of 2012 increased by 126.1% or

P1,557.1 million to P2,792.2 million from the P1,235.1 million posted during the same

period in 2011. This was mainly due to P642.5 million Green Core Geothermal Inc’s

(GCGI) higher revenues from Tongonan I and Palinpinon power plants as per GCGI’s

agreed contracts that became effective in mid-2011; and FG Hydro’s P596.9 million

revenues from contingency and dispatchable reserves.

Recurring net income attributable to equity holders of the parent was posted at

P2,344.5 million, up by 102.8%, as compared to the P1,155.9 billion for the first quarter

of 2011.

Net income is equivalent to 40.8% of total revenues in 2012 as compared to the 24.5%

from the same period in 2011. It increased by 115.4% or P1,686.1 million to

P3,146.9 million as of March 31, 2012 from P1,460.8 million during the same period in

2011.

Factors contributing to these were the following:

P1,738.6 million increase in sale of electricity due to fresh contribution of BGI’s

revenues, increase in GCGI’s sales and FG Hydro’s revenues from contingency and

dispatchable reserves; and

P149.4 million Foreign exchange gains due to appreciation of the peso against the US

dollar.

Net income attributable to equity holders of the parent at P2,699.3 million for the first

quarter of 2012, increased by 95.3% as compared to the P1,381.8 million during the same

period in 2011.

Cash and cash equivalents increased by 5.0% or P630.0 million to P13,123.4 million as

of March 31, 2012 from the P12,493.4 million December 31, 2011 balance. The increase

was mainly accounted for by the P798.9 million regular long-term debt servicing offset

by the P132.7 million dividend received from FG Hydro.

SEC Form 17Q – 1Q 2012 10

RESULTS OF OPERATIONS

The following table details the results of operations for EDC for the first quarter of

2012 and 2011.

INCOME STATEMENT

Horizontal Analysis of Material Changes as of March 31, 2012 and 2011

Favorable (Unfavorable) Variance

(Amounts in PHP millions) March 2012 March 2011 Amount % 2012 2011

REVENUES

Sale of electricity 7,536.8 5,798.2 1,738.6 30.0% 97.8% 97.4%

Revenue from drilling services 167.6 154.6 13.0 8.4% 2.2% 2.6%

7,704.4 5,952.8 1,751.6 29.4% 100.0% 100.0%

COST OF SALES AND SERVICES*

Cost of sales of electricity and steam (2,741.3) (2,762.7) 21.4 -0.8% -35.6% -46.4%

Cost of drilling services (95.4) (108.3) 12.9 -11.9% -1.2% -1.8%

(2,836.7) (2,871.0) 34.3 -1.2% -36.8% -48.2%

GENERAL AND ADMINISTRATIVE EXPENSES* (919.6) (888.9) (30.7) 3.5% -11.9% -14.9%

FINANCIAL INCOME (EXPENSE)

Interest income 93.9 123.9 (30.0) -24.2% 1.2% 2.1%

Interest expense (1,015.4) (1,038.9) 23.5 -2.3% -13.2% -17.5%

(921.5) (915.0) (6.5) 0.7% -12.0% -15.4%

OTHER INCOME (CHARGES)

Foreign exchange gains (losses), net 338.0 188.6 149.4 79.2% 4.4% 3.2%

Derivatives gains (losses), net - 37.6 (37.6) -100.0% 0.0% 0.6%

Miscellaneous, net* 59.3 30.7 28.6 93.2% 0.8% 0.5%

397.3 256.9 140.4 54.7% 5.2% 4.3%

INCOME BEFORE INCOME TAX 3,423.9 1,534.8 1,889.1 123.1% 44.4% 25.8%

BENEFIT FROM (PROVISION FOR) INCOME TAX

Current (187.9) (168.4) (19.5) 11.6% -2.4% -2.8%

Deferred (89.1) 94.4 (183.5) -194.4% -1.2% 1.6%

(277.0) (74.0) (203.0) 274.3% -3.6% -1.2%

NET INCOME 3,146.9 1,460.8 1,686.1 115.4% 40.8% 24.5%

Net income (loss) attributable to:

Equity holders of the Parent Company 2,699.3 1,381.8 1,317.5 95.3% 35.0% 23.2%

Non-controlling interest 447.6 79.0 368.6 466.6% 5.8% 1.3%

EBITDA 4,863.2 3,166.7 1,696.5 53.6% 63.1% 53.2%

RECURRING NET INCOME 2,792.2 1,235.1 1,557.1 126.1% 36.2% 20.7%

Recurring net income attributable to:

Equity holders of the Parent Company 2,344.5 1,155.9 1,188.6 102.8% 30.4% 19.4%

Non-controlling interest 447.7 79.2 368.5 465.3% 5.8% 1.3%

HORIZONTAL ANALYSIS VERTICAL ANALYSIS

*New presentation based on SRC Rule 68 issued by Philippine SEC last October 20, 2011 – As amended effective for audited financial statements covering periods ending December 31, 2011 and onwards, and for interim financial statements starting the first quarter of 2012, and

thereafter.

SEC Form 17Q – 1Q 2012 11

YTD March 31, 2012 vs. YTD March 31, 2011

Revenues

Total revenues for the period ended March 31, 2012 increased by 29.4% or P1,751.6 million to

P7,704.4 million from P5,952.8 million in 2011.

Sale of Electricity

Revenues from sale of electricity increased by 30.0% or P1,738.6 million to

P7,536.8 million in the first quarter of 2012 from P5,798.2 million during the same

period in 2011. The increase in revenue was primarily due to the following:

P738.9 million fresh contribution of BGI’s revenues coming from its PSAs with

BATELEC and Linde Philippines;

P642.5 million GCGI’s higher revenues from Tongonan I and Palinpinon power

plants as per agreed contracts that became effective in mid-2011; and

P596.9 million FG Hydro’s revenues from contingency and dispatchable reserves.

Revenue from Drilling Services

Revenue from drilling services increased by 8.4% or P13.0 million to P167.6 million in

the first quarter of 2012 from P154.6 million during the same period in 2011. The

favorable variance was attributed to higher dollar revenues in 2012 as there was 15 non-

revenue days reported in 2011 for the repair of Rig 11. Total dollar revenues as of

March 2012 was US$3.9 million against the US$3.5 million as of March 2011.

This was offset by lower average exchange rate by P0.952/US$1 (YTD March

2012=P42.832/US$1 vs. YTD March 2011=P43.784/US$1) due to the appreciation of the

peso against the US dollar.

Cost of Sales and Services

Cost of sales and services decreased by 1.2% or P34.3 million to P2,836.7 million in the first

quarter of 2012 from P2,871.0 million during the same period in 2011. Cost of drilling services

decreased by 11.9% or P12.9 million to P95.4 million in the first quarter of 2012 from

P108.3 million during the same period in 2011 mainly due to the repair of Rig 11 undertaken in

the first quarter of 2011. Total cost of sales of electricity and steam includes replacement power

cost amounting to P706.5 million.

Financial Income (Expenses)

Interest income decreased by 24.2% or P30.0 million to P93.9 million in the first quarter of 2012

from P123.9 million during the same period in 2011 due to lower monthly average investible

funds cushioned by higher weighted average interest rates on peso placements.

SEC Form 17Q – 1Q 2012 12

Other Income (Charges)

Other income–net increased by 54.7% or P140.4 million to P397.3 million in the first quarter of

2012 from P256.9 million during the same period in 2011.

Foreign Exchange Gains (Losses) - net

Net foreign exchange gains increased by P149.4 million, or 79.2%, to P338.0 million

from P188.6 million in 2011. The favorable variance was brought about by appreciation

of the peso against the US dollar.

The comparative foreign exchange rates against the USD were as follows:

JPY:US$ PHP:US$

December 31, 2010 81.659 43.840

March 31, 2011 82.871 43.390

December 31, 2011 77.912 43.840

March 31, 2012 82.420 42.920

Derivatives Gain (Loss) - Net

Derivative gain - net decreased by 100% from the P37.6 million balance in

March 31, 2011. The derivative gain pertained to various swap transactions for US dollar

and Japanese yen currencies entered into with various banks in February 2011, maturing

in March 2011 and April 2011.

Miscellaneous – Net

Miscellaneous income increased by 93.5% or P28.7 million to P59.4 million in the first

quarter of 2012 from P30.7 million during the same period in 2011. This was mainly

caused by P63.6 million reversal of NNGP power plant impairment.

Provision for Income Tax

Current tax expense increased by P19.5 million, or 11.6%, to P187.9 million from P168.4 million

during the same period in 2011. The unfavorable variance was on account of the following:

P31.0 million increase caused by taxable income in 2012 for the drilling operations in

Lihir, Papua, New Guinea versus taxable loss (NOLCO) in 2011; and

P43.7 million Fresh contribution of income taxes from BGI’s taxable income in 2012.

These were offset by P55.3 million lower taxable income on steam and electricity operations

mainly contributed by the absence of NNGP's revenues in 2012 coupled with higher finance cost

on new loans.

SEC Form 17Q – 1Q 2012 13

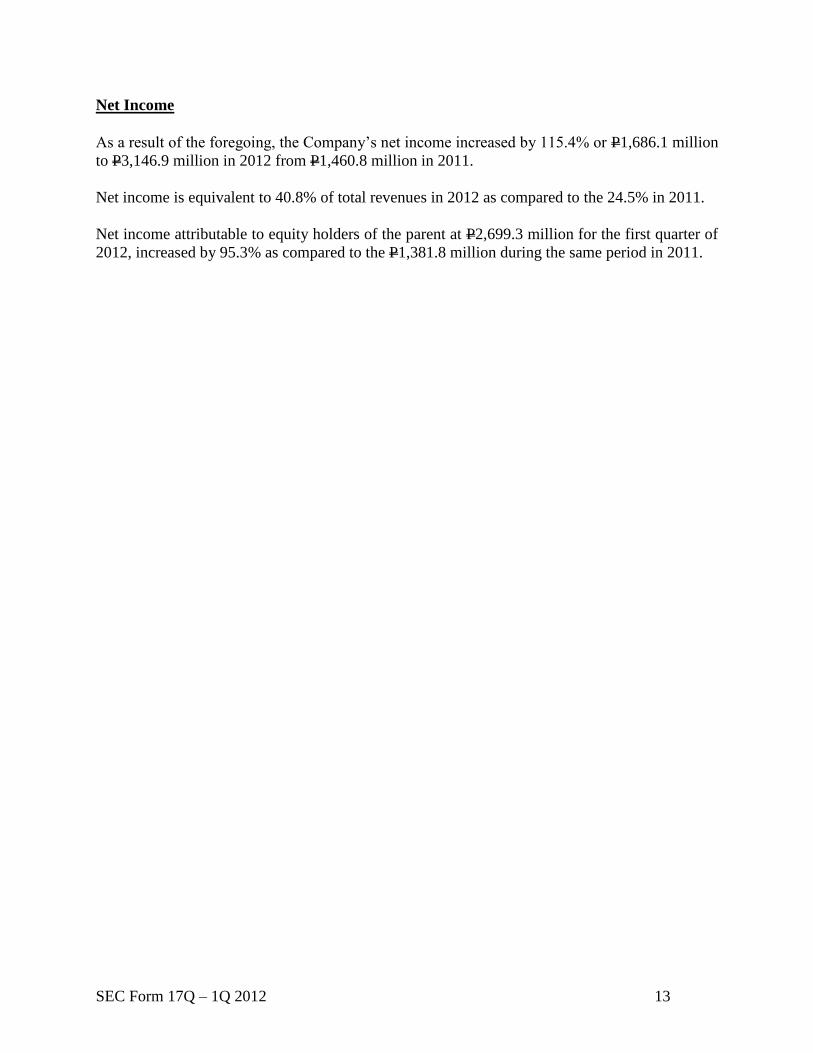

Net Income

As a result of the foregoing, the Company’s net income increased by 115.4% or P1,686.1 million

to P3,146.9 million in 2012 from P1,460.8 million in 2011.

Net income is equivalent to 40.8% of total revenues in 2012 as compared to the 24.5% in 2011.

Net income attributable to equity holders of the parent at P2,699.3 million for the first quarter of

2012, increased by 95.3% as compared to the P1,381.8 million during the same period in 2011.

SEC Form 17Q – 1Q 2012 14

CAPITAL AND LIQUIDITY RESOURCES

As of the quarter ended

(in millions of pesos)

Q1

2012

Q1

2011 YoY change

Balance Sheet Data

Total Assets …………………………… 92,151.1 95,326.7 3.3%

Total Liabilities………………………... 61,340.2 64,642.0 5.1%

Total Stockholder’s Equity …………… 30,810.9 30,684.7 0.4%

The Company’s assets as of March 31, 2012 amounted to P92,151.1 million, 3.3% higher as

compared to the P95,326.7 million level as of March 31, 2011.

SEC Form 17Q – 1Q 2012 15

FINANCIAL POSITION

Horizontal and Vertical Analysis of Material Changes as of March 31, 2012 and

December 31, 2011.

(Amounts In PHP millions) March 2012 Dec. 2011 Amount % 2012 2011

ASSETS

Current Assets

Cash and cash equivalents 13,123.4 12,493.4 630.0 5.0% 14.2% 13.9%

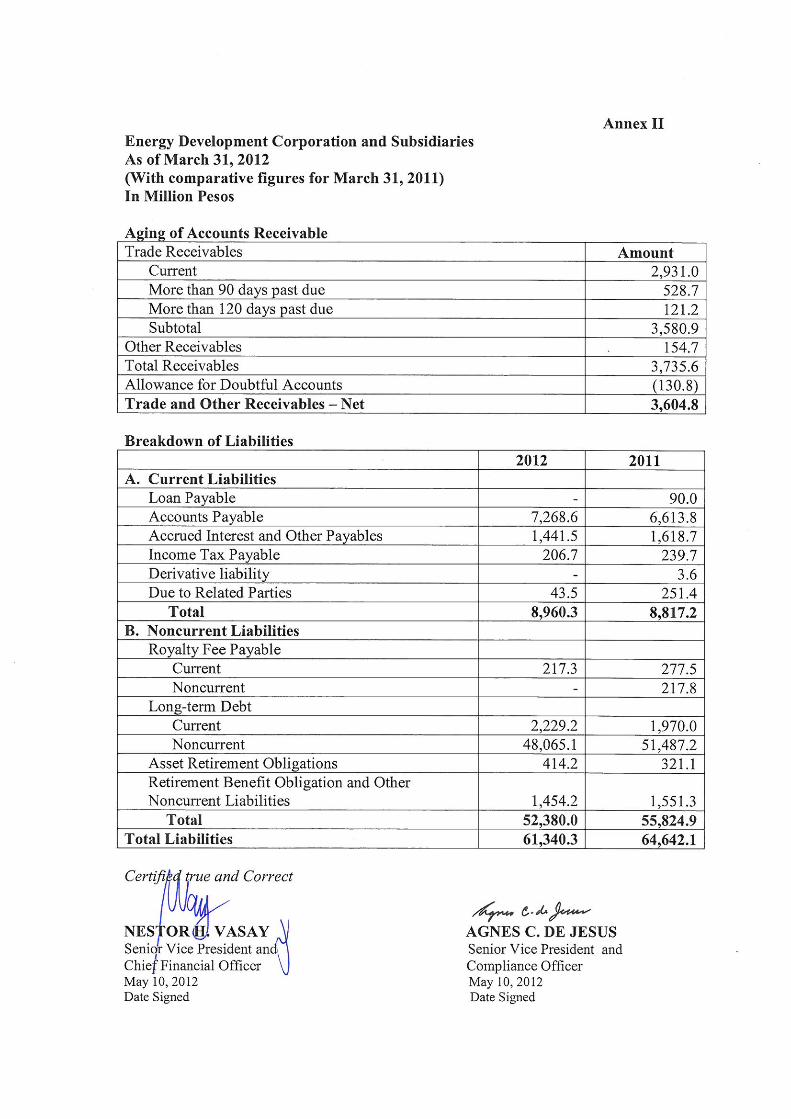

Trade and other receivables 3,604.8 3,411.3 193.5 5.7% 3.9% 3.8%

Available-for-sale (AFS) investments 649.8 673.9 (24.1) -3.6% 0.7% 0.7%

Parts and supplies inventories 3,244.9 3,355.8 (110.9) -3.3% 3.5% 3.7%

Other current assets 980.4 741.9 238.5 32.1% 1.1% 0.8%

Total Current Assets 21,603.3 20,676.3 927.0 4.5% 23.4% 23.0%

Noncurrent Assets

Property, plant and equipment 58,256.5 57,676.9 579.6 1.0% 63.2% 64.1%

Intangible assets 4,714.0 4,705.2 8.8 0.2% 5.1% 5.2%

Deferred tax assets 1,331.6 1,420.7 (89.1) -6.3% 1.4% 1.6%

Exploration and evaluation assets 1,505.5 1,087.1 418.4 38.5% 1.6% 1.2%

Other noncurrent assets 4,740.2 4,451.6 288.6 6.5% 5.1% 4.9%

Total Noncurrent Assets 70,547.8 69,341.5 1,206.3 1.7% 76.4% 77.0%

TOTAL ASSETS 92,151.1 90,017.8 2,133.3 2.4% 99.8% 100.0%

LIABILITIES AND EQUITY

LIABILITIES

Current Liabilities

Trade and other payables 8,710.1 6,704.1 2,006.0 29.9% 9.5% 7.4%

Income tax payable 206.7 18.7 188.0 1005.3% 0.2% 0.0%

Due to related parties 43.5 60.1 (16.6) -27.6% 0.0% 0.1%

Current portion of:

Long-term debts 2,229.2 2,249.5 (20.3) -0.9% 2.4% 2.5%

Royalty fee payable 217.3 287.6 (70.3) -24.4% 0.2% 0.3%

Total Current Liabilities 11,406.8 9,320.0 2,086.8 22.4% 12.3% 10.4%

Noncurrent Liabilities

Long-term debts - net of current portion 48,065.1 49,240.1 (1,175.0) -2.4% 52.2% 54.7%

Net retirement and other post-employment

benefits 1,144.5 1,054.2 90.3 8.6% 1.2% 1.2%

Provisions and other long-term liabilities 723.8 756.8 (33.0) -4.4% 0.8% 0.9%

Total Noncurrent Liabilities 49,933.4 51,051.1 (1,117.7) -2.2% 54.2% 56.8%

EQUITY

Equity Attributable to Equity Holders of the Parent

Preferred stock 93.8 93.8 - 0.0% 0.1% 0.1%

Common stock 18,750.0 18,750.0 - 0.0% 20.3% 20.8%

Common stock in employee trust account (372.3) (372.3) - 0.0% -0.3% -0.4%

Additional paid-in capital 6,267.0 6,267.0 - 0.0% 6.8% 7.0%

Equity reserve (3,706.4) (3,706.4) - 0.0% -3.9% -4.1%

Net accumulated unrealized gain on AFS

investments 80.1 91.8 (11.7) -12.7% 0.1% 0.1%

Retained earnings 7,121.5 6,304.7 816.8 13.0% 7.7% 7.0%

Cumulative translation adjustment 0.6 0.6 - 0.0% 0.0% 0.0%

28,234.3 27,429.2 805.1 2.9% 30.7% 30.4%

Non-controlling interest 2,576.6 2,217.5 359.1 16.2% 2.8% 2.5%

Total Equity 30,810.9 29,646.7 1,164.2 3.9% 33.5% 32.8%

TOTAL LIABILITIES AND EQUITY 92,151.1 90,017.8 2,133.3 2.4% 100.0% 100.0%

HORIZONTAL

ANALYSIS

VERTICAL

ANALYSIS

Increase (Decrease)

SEC Form 17Q – 1Q 2012 16

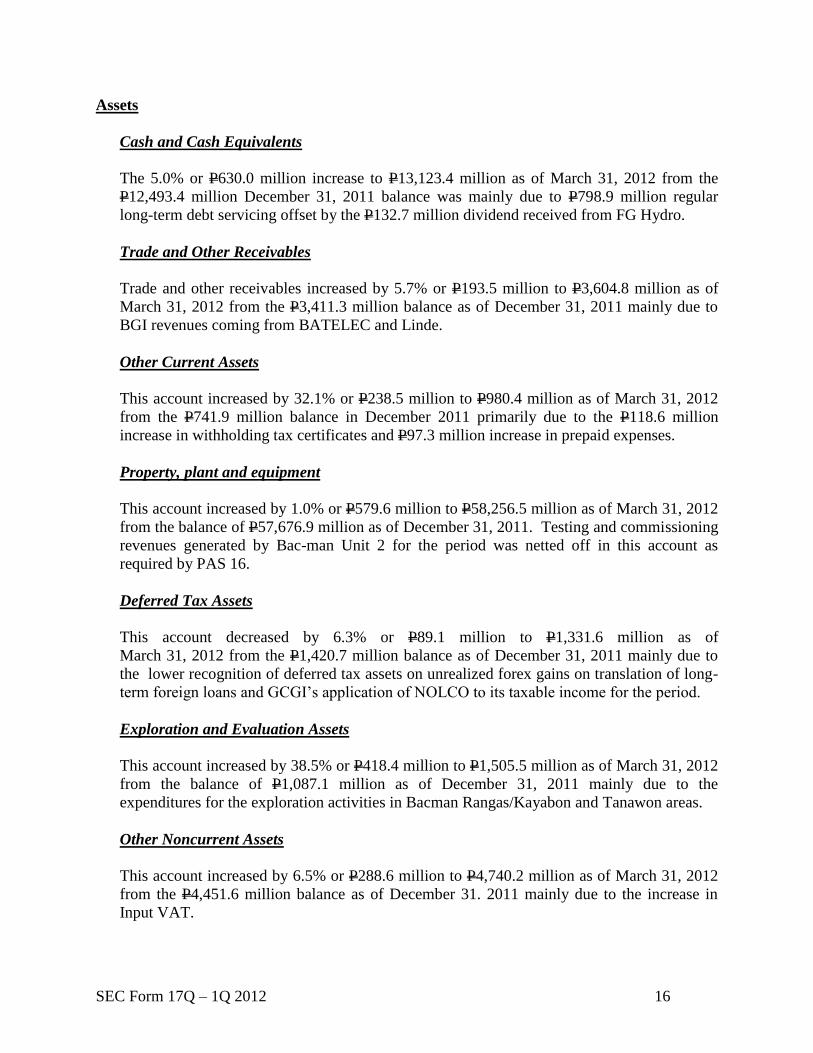

Assets

Cash and Cash Equivalents

The 5.0% or P630.0 million increase to P13,123.4 million as of March 31, 2012 from the

P12,493.4 million December 31, 2011 balance was mainly due to P798.9 million regular

long-term debt servicing offset by the P132.7 million dividend received from FG Hydro.

Trade and Other Receivables

Trade and other receivables increased by 5.7% or P193.5 million to P3,604.8 million as of

March 31, 2012 from the P3,411.3 million balance as of December 31, 2011 mainly due to

BGI revenues coming from BATELEC and Linde.

Other Current Assets

This account increased by 32.1% or P238.5 million to P980.4 million as of March 31, 2012

from the P741.9 million balance in December 2011 primarily due to the P118.6 million

increase in withholding tax certificates and P97.3 million increase in prepaid expenses.

Property, plant and equipment

This account increased by 1.0% or P579.6 million to P58,256.5 million as of March 31, 2012

from the balance of P57,676.9 million as of December 31, 2011. Testing and commissioning

revenues generated by Bac-man Unit 2 for the period was netted off in this account as

required by PAS 16.

Deferred Tax Assets

This account decreased by 6.3% or P89.1 million to P1,331.6 million as of

March 31, 2012 from the P1,420.7 million balance as of December 31, 2011 mainly due to

the lower recognition of deferred tax assets on unrealized forex gains on translation of long-

term foreign loans and GCGI’s application of NOLCO to its taxable income for the period.

Exploration and Evaluation Assets

This account increased by 38.5% or P418.4 million to P1,505.5 million as of March 31, 2012

from the balance of P1,087.1 million as of December 31, 2011 mainly due to the

expenditures for the exploration activities in Bacman Rangas/Kayabon and Tanawon areas.

Other Noncurrent Assets

This account increased by 6.5% or P288.6 million to P4,740.2 million as of March 31, 2012

from the P4,451.6 million balance as of December 31. 2011 mainly due to the increase in

Input VAT.

SEC Form 17Q – 1Q 2012 17

Liabilities

Trade and other payables

This account increased by 29.9% or P2,006.0 million to P8,710.1 million as of

March 31, 2012 from the P6,704.1 million balance as of December 31. 2011 due to the

P1,882.5 million accrual of cash dividend declared on March 13, 2012.

Income Tax payable

This account increased by 1005.3% or P188.0 million, to P206.7 million as of

March 31, 2012 from the P18.7 million balance as of December 31, 2011 arising from the

Parent Company’s taxable income for the period and the testing and commissioning revenues

generated by Bac-man Unit 2 for the period.

Due to related parties

This account decreased by 27.6% or P16.6 million to P43.5 million as of March 31, 2012

from the P60.1 million balance as of December 31, 2011 mainly due to partial settlement of

liabilities by the Parent Company.

Royalty fee payable - current portion

Royalty fee payable decreased by 24.4% or P70.3 million, to P217.3 million as of

March 31, 2012 from the P287.6 million balance at year-end 2011 was due to the payment of

royalty fee for the period.

Net retirement and other post-employment benefits

This account increased by 8.6% or P90.3 million to P1,144.5 million as of March 31, 2012

from the P1,054.2 million balance as of December 31, 2011 due to the accrual of retirement

benefits for the period.

Net accumulated unrealized gain on AFS investments

This account decreased by 12.7% or P11.7 million to P80.1 million as of March 31, 2012

from P91.8 million as of December 31, 2011 mainly due to the decrease in fair value of the

investments for the period.

Retained Earnings

Retained Earnings increased by 13.0% or P816.8 million, to P7,121.5 million as of

March 31, 2012 from P6,304.7 million as of December 31, 2011 mainly due to the

P2,699.3 million net income for the first quarter of 2012 offset by the P1,882.5 million

payment of cash dividend.

SEC Form 17Q – 1Q 2012 18

Non-controlling Interest

Non-controlling Interest increased by 16.2% or P359.1 million to P2,576.6 million as of

March 31, 2012 from P2,217.5 million balance as of December 31, 2011 mainly due to the

P447.6 million net income for the first quarter of 2012 offset by the P88.5 million payment of

cash dividend.

SEC Form 17Q – 1Q 2012 19

Horizontal and Vertical Analysis of Material Changes as of March 31, 2012 and 2011.

BALANCE SHEET

Analysis of Material Changes as of March 31, 2012 and 2011

(Amounts In PHP millions) March 2012 March 2011 Amount % 2012 2011

ASSETS

Current Assets

Cash and cash equivalents 13,123.4 19,814.6 (6,691.2) -33.8% 14.2% 20.8%

Trade and other receivables 3,604.8 2,922.3 682.5 23.4% 3.9% 3.1%

Available-for-sale (AFS) investments 649.8 690.3 (40.5) -5.9% 0.7% 0.7%

Parts and supplies inventories 3,244.9 2,717.2 527.7 19.4% 3.5% 2.9%

Derivative assets - 11.8 (11.8) -100.0% 0.0% 0.0%

Other current assets 980.4 853.6 126.8 14.9% 1.1% 0.9%

Total Current Assets 21,603.3 27,009.8 (5,406.5) -20.0% 23.4% 28.3%

Noncurrent Assets

Property, plant and equipment 58,256.5 58,084.8 171.7 0.3% 63.2% 60.9%

Intangible assets 4,714.0 4,519.0 195.0 4.3% 5.1% 4.7%

Deferred tax assets 1,331.6 987.9 343.7 34.8% 1.4% 1.0%

Exploration and evaluation assets 1,505.5 1,201.5 304.0 25.3% 1.6% 1.3%

Other noncurrent assets 4,740.2 3,523.8 1,216.4 34.5% 5.1% 3.7%

Total Noncurrent Assets 70,547.8 68,317.0 2,230.8 3.3% 76.4% 71.7%

TOTAL ASSETS 92,151.1 95,326.8 (3,175.7) -3.3% 99.8% 100.0%

LIABILITIES AND EQUITY

LIABILITIES

Current Liabilities

Loan payable - 90.0 (90.0) -100.0% 0.0% 0.1%

Trade and other payables 8,710.1 8,232.5 477.6 5.8% 9.5% 8.6%

Income tax payable 206.7 239.7 (33.0) -13.8% 0.2% 0.3%

Due to related parties 43.5 251.4 (207.9) -82.7% 0.0% 0.3%

Derivative liabilities - 3.6 (3.6) -100.0% 0.0% 0.0%

Current portion of:

Long-term debts 2,229.2 1,970.0 259.2 13.2% 2.4% 2.1%

Royalty fee payable 217.3 277.5 (60.2) -21.7% 0.2% 0.3%

Total Current Liabilities 11,406.8 11,064.7 342.1 3.1% 12.3% 11.6%

Noncurrent Liabilities

Long-term debts - net of current portion 48,065.1 51,487.2 (3,422.1) -6.6% 52.2% 54.0%

Royalty fee payable - net of current portion - 217.8 (217.8) -100.0% 0.0% 0.2%

Net retirement and other post-employment benefits 1,144.5 1,298.6 (154.1) -11.9% 1.2% 1.4%

Provisions and other long-term liabilities 723.8 573.8 150.0 26.1% 0.8% 0.7%

Total Noncurrent Liabilities 49,933.4 53,577.4 (3,644.0) -6.8% 54.2% 56.3%

EQUITY

Equity Attributable to Equity Holders of the Parent

Preferred stock 93.8 93.8 - 0.0% 0.1% 0.1%

Common stock 18,750.0 18,750.0 - 0.0% 20.3% 19.7%

Common stock in employee trust account (372.3) (377.5) 5.2 -1.4% -0.3% -0.4%

Additional paid-in capital 6,267.0 6,266.3 0.7 0.0% 6.8% 6.6%

Equity reserve (3,706.4) (3,706.4) - 0.0% -3.9% -3.9%

Net accumulated unrealized gain on AFS investments 80.1 110.3 (30.2) -27.4% 0.1% 0.1%

Retained earnings 7,121.5 7,898.8 (777.3) -9.8% 7.7% 8.3%

Cumulative translation adjustment 0.6 1.4 (0.8) -57.1% 0.0% 0.0%

28,234.3 29,036.7 (802.4) -2.8% 30.7% 30.4%

Non-controlling Interest 2,576.6 1,648.0 928.6 56.3% 2.8% 1.7%

Total Equity 30,810.9 30,684.7 126.2 0.4% 33.5% 32.1%

TOTAL LIABILITIES AND EQUITY 92,151.1 95,326.8 (3,175.7) -3.3% 100.0% 100.0%

HORIZONTAL

ANALYSIS

VERTICAL

ANALYSIS

Increase

SEC Form 17Q – 1Q 2012 20

Assets

Cash and Cash Equivalents

This account decreased by 33.8% or P6,691.2 million to P13,123.4 million as of

March 31, 2012 from the P19,814.6 million balance as of March 31, 2011 primarily due to

the following:

P5,215.2 million pre payment of OECF 9th, 18th, 19th and 21st Yen and regular debt

servicing in 2011;

P798.9 million settlement of regular long-term debt servicing in 2012;

P3,007.5 million cash dividends paid by the parent company in 2011; and

P175.0 million payment of short-term borrowings.

These were offset by the P3,262.5 million proceeds from IFC 2.

Trade and Other Receivables

This account increased by 23.4% or P682.5 million to P3,604.8 million as of March 31, 2012

from the P2,922.3 million balance as of March 31, 2011. The increase is mainly due to the

BGI revenues coming from BATELEC and Linde and GCGI’s higher revenues.

Available-For-Sale (AFS) Investments

AFS Investments decreased by 5.9% or P40.5 million to P649.8 million as of March 31, 2012

from the P690.3 million balance as of March 31, 2011 due to foreign exchange losses

sustained in translating the placements to the continued appreciation of the Peso versus the

US Dollar exchange rate.

Parts and Supplies Inventories

This account increased by 19.4% or P527.7 million to P3,244.9 million balance as of

March 31, 2012 from the P2,717.2 million balance for the same period in 2011 due to the

increase , net of withdrawals, on various materials and supplies for drilling, maintenance and

rehabilitation activities in 2011.

Derivative assets

The derivative assets P11.8 million balance as of March 31, 2011 pertains to the fair value of

the outstanding foreign currency forward and foreign exchange swap contracts.

Other Current Assets

Other current assets increased by 14.9% or P126.8 million to P980.4 million as of

March 31, 2012 from the P853.6 million posted for the same period in 2011 is attributable to

the P248.7 million increase in prepaid expenses offset by P115.6 million decrease in

withholding taxes.

SEC Form 17Q – 1Q 2012 21

Deferred Tax Assets

This account increased by 34.8% or P343.7 million to P1,331.6 million as of March 31, 2012

from the balance of P987.9 million as of March 31, 2011 mainly due to the recognition of

deferred tax assets on the provision for full impairment of NNGP’s assets amounting to

P4,998.6 million and unrealized forex loss on dollar denominated loans in 2011.

Exploration and Evaluation Assets

This account increased by 25.3% or P304.0 million to P1,505.5 million as of March 31, 2012

from the balance of P1,201.5 million as of March 31, 2011 primarily due to the expenses of

Mindanao, Bacman Rangas/Kayabon, and Tanawon areas.

Other Noncurrent Assets

This account increased by 34.5% or P1,216.4 million, to P4,740.2 million as of

March 31, 2012 from the P3,523.8 million as of March 31, 2011 mainly due to the

P934.4 million increase in input VAT and P579.8 million increase long term receivables.

These were offset by the increase in allowance for doubtful accounts of P298.3 million.

Liabilities

Loan payable

This account decreased by 100.0%, or P90.0 million as of March 31, 2012 due to the

settlement of the loan.

Trade and other payables

This account increased by 5.8%, or P477.6 million, to P8,710.1 million as of March 31, 2012

from the balance of P8,232.5 million in the same period of 2011 mainly due to the

P654.7 million increase in accounts payable and offset by the P232.2 million decrease in

accrued interest and guarantee fee and other payables.

Income tax payable

Income tax payable decreased by 13.8% or P33.0 million to P206.7 million as of

March 31, 2012 from P239.7 million for the same period in 2011 mainly due to the

application of withholding tax certificates in the payment of income tax due for the 4th qtr of

2010 and 1st qtr. to 3rd qtr of 2011.

SEC Form 17Q – 1Q 2012 22

Due to related parties

This account decreased by 82.7% or P207.9 million to P43.5 million as of March 31, 2012

from the balance of P251.4 million as of March 31, 2011 primarily due to the settlement of

advances from First Gen of P235.0 million offset by increase in consultancy fee of

P28.6 million.

Derivative liabilities

The P3.6 million balance as of March 31, 2011 pertains to the fair value of the outstanding

foreign currency forward and foreign exchange swap contracts with various counterparties.

Long-term debts (current portion)

This account increased by 13.2% or P259.2 million to P2,229.2 million as of March 31, 2012

from the balance of P1,970.0 million as of March 31, 2011 mainly due to the P687.5 million

reclassification of the current portion of maturing IFC, FRCN and PNB debt obligation in

2012. These were offset by the P402.6 million settlement maturing debt obligation and

prepayment of current portion of OECF 9th, 18th, 19th and 21st Yen loan in 2011.

Royalty fee payable (current portion )

This account decreased by 21.7 % or P60.2 million to P217.3 million as of March 31, 2012

from the balance of P277.5 million as of March 31, 2011 mainly due to P80.3 million

payment to DOE and LGU’s offset by P20.1 million accretion on Day 1 gain recognized

from April 1, 2011 to March 31, 2012.

Long-term debt (net of current portion)

Long-term debts, consisting of JPY, US$ and PHP loans, decreased by 6.6% or

P3,422.1 million to P48,065.1 million as of March 31, 2012 from P51,487.2 million as of

March 31, 2011 due to the following:

Settlement of P4,260.6 million OECF 21st Yen loan and P128.0 million OECF 8th, 9th,

18th and 19th Yen loan,

P1,532.2 million and P496.8 million reclassification to current portion of obligation

due in 2012 of FRCN and IFC Loan, respectively.

These were offset by P3,262.5 million proceeds from of IFC loan 2.

Royalty fee payable (net of current portion )

This account decreased by 100.0% or P217.8 million as of March 31, 2012 primarily due to

the reclassification to current portion of outstanding royalty fees payable to 2012.

SEC Form 17Q – 1Q 2012 23

Net retirement and other post-retirement benefits

This account decreased by 11.9% or P154.1 million to P1,144.5 million as of March 31, 2012

from P1,298.6 million balance as of March 31, 2011 mainly due to contribution to the fund in

2011 offset by the accrual of retirement benefits for the period.

Provisions and other long-term liabilities

This account increased by 26.1% or P150.0 million to P723.8 million as of March 31, 2012

from P573.8 million balance as of March 31, 2011 mainly due to the P64.4 million asset

retirement obligation recognized in 2011, P28.7 million accretion for the period and

P54.1 million accrual of sick leave and vacation leave for the period net of payment of the

10 days monetized vacation leave.

Net accumulated unrealized gain on AFS investments

This account decreased by 27.4% or P30.2 million to P80.1 million as of March 31, 2012

from P110.3 million as of March 31, 2011 mainly due to the decrease in fair value of the

investments for the period.

Retained Earnings

Retained Earnings decreased by 9.8% or P777.3 million to P7,121.5 million as of

March 31, 2012 from P7,898.8 million balance as of March 31, 2011 mainly due to the net

loss of P1,548.9 million posted from March 31, 2011 to December 31, 2011 and

P1,882.5 million payment of cash dividend for the year offset by P2,699.3 million net income

for the first quarter of 2012.

Non-controlling Interest

Non-controlling Interest increased by 56.3% or P928.6 million to P2,576.6 million as of

March 31, 2012 from P1,648.0 million balance as of March 31, 2011 mainly due to the net

income of P703.1 million posted from March 31, 2011 to December 31, 2011 and

P447.6 million net income for the first quarter of 2012. This was offset by P88.5 million

payment of cash dividend this year.

SEC Form 17Q – 1Q 2012 24

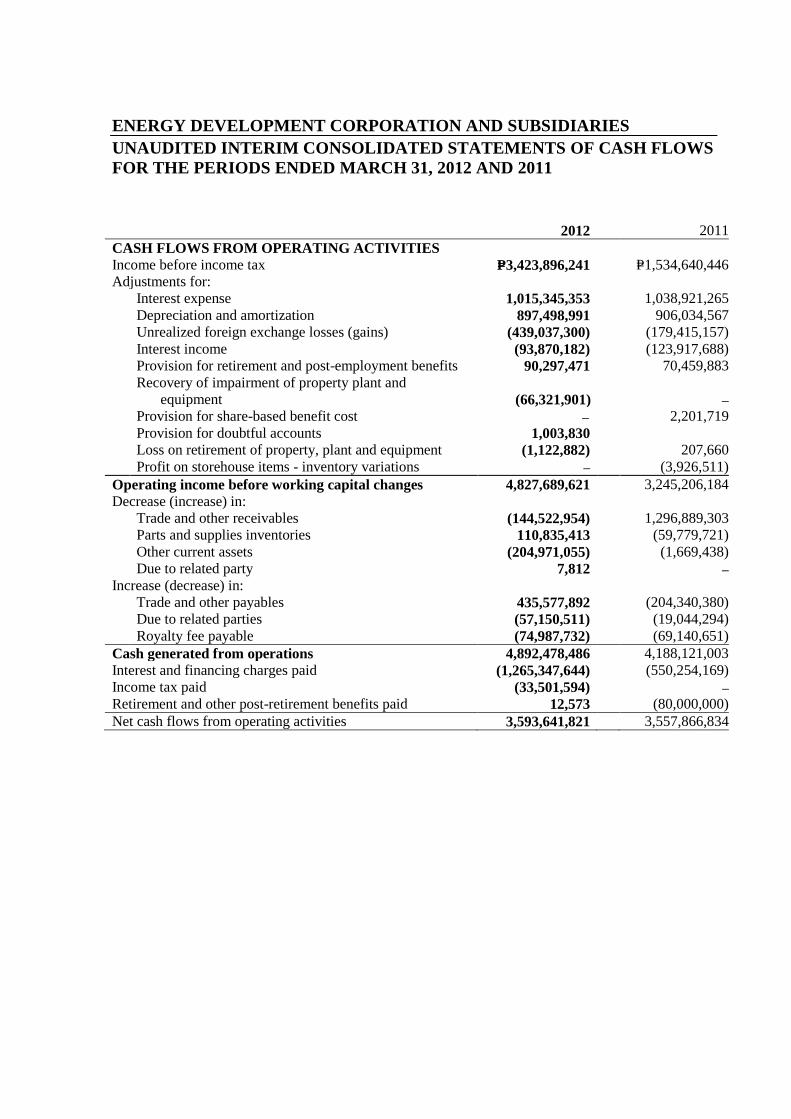

CASH FLOW

March 31, 2012 vs. March 31, 2011

Net cash flows from operating activities increased by 1.0% or P35.8 million to P3,593.6 million

in the first quarter of 2012 from P3,557.9 million during the same period in 2011 mainly due to

the P704.4 million improved cash generation from operations due to increased revenues and

P80.0 million decrease in retirement and other post-retirement benefits paid. These were offset

by the P715.1 million increase in interest and financing charges paid and P33.5 million increase

in withholding tax certificates.

Net cash flows used in investing activities decreased by 10.4% or P236.9 million to

P2,042.0 million in March 2012 as compared to the P2,278.9 million during the same period in

2011 primarily due to the decrease in acquisition of property, plant and equipment by

P689.2 million. This was offset by the P416.5 million increase in exploration and evaluation

assets.

The movement of P13,536.1 million, to P927.9 million on net cash flows used in financing

activities in March 2012 from the P12,608.2 million net cash flows from financing activities

during the same period in 2011 was mainly due to the P13,350 million proceeds from the

US$300M notes in 2011.

SEC Form 17Q – 1Q 2012 25

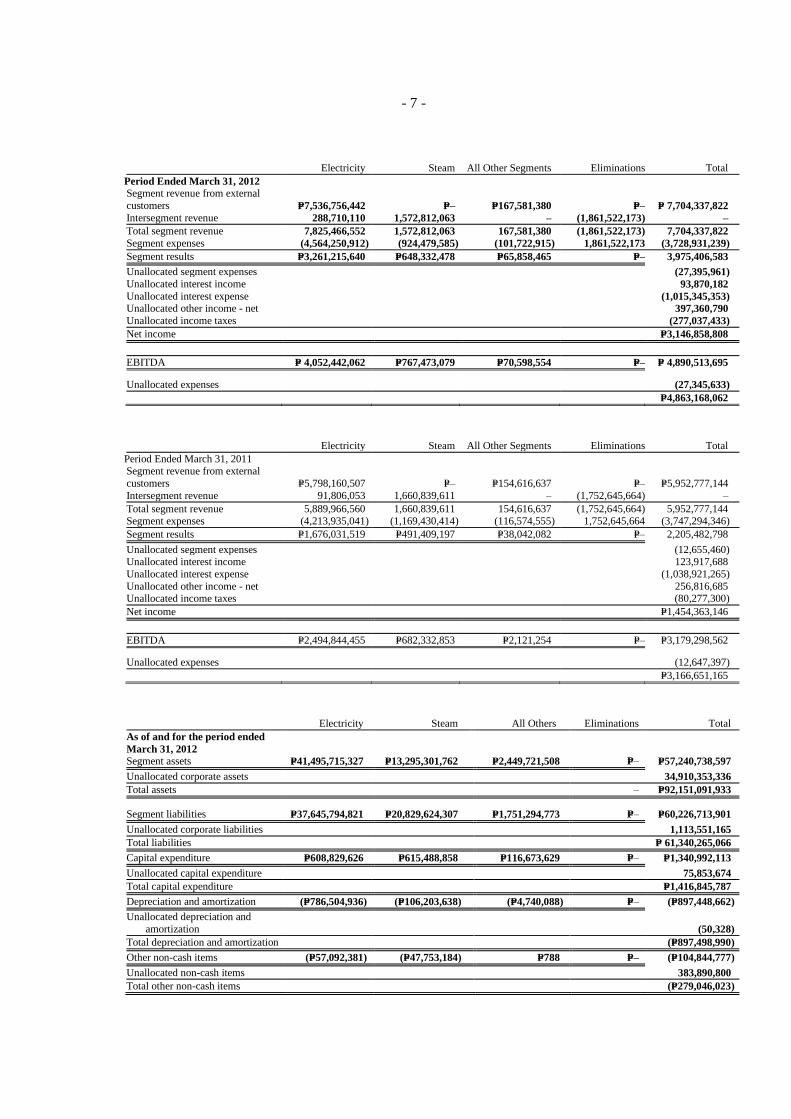

DISCUSSION ON THE SUBSIDIARIES

FG Hydro

(Amounts in PHP millions)

As of and for the periods ended

March 31

2012 2011

Operating revenues 1,411.1 517.2

Operating expenses 198.5 225.4

Other expenses – net 93.6 100.7

Income before tax 1,119.0 191.1

Provision for (benefit from) income tax - -

Net income 1,119.0 191.1

Total current assets 3,414.0 1,822.2

Total noncurrent assets 7,156.1 7,364.3

Total current liabilities 650.4 491.9

Total noncurrent liabilities 4,219.2 4,574.6

Total equity 5,700.5 4,120.0

FG Hydro generated revenues of P1,411.1 million for the period ended March 31, 2012, almost thrice the

revenues of P517.2 million for the same period in 2011. The favorable variance was mainly on account of

revenues earned from sale of electricity, as ancillary services to National Grid Corporation of the

Philippines (“NGCP”), amounting to P596.9 million, and the temporary assumption of BGI’s Power

Supply Agreements (PSAs) with Batangas Electric Cooperative II (“BATELEC II”) 48MW and Linde

Philippines 6MW amounting to P288.7 million. There were no revenues from the said entities for the

same period in 2011.

The favorable variance in operating expenses is mainly on account of lower depreciation, operations and

maintenance expenses and taxes and licenses in 2012. Higher interest income from short-term deposits of

P16.8 million in 2012 versus P9.1 million in 2011 further contributed to the favorable variance. Overall,

FG Hydro posted a net income of P1,119.0 million for the period ended March 31, 2012, P927.9 million

or 485.6% higher than the P191.1 million reported income for the same period in 2011.

Total assets as of March 31, 2012 stood at P10,570.1 million, P1,383.6 million or 15.1% higher than the

2011 level of P9,186.5 million. The favorable variance was mainly due to higher cash and accounts

receivable trade balances in 2012. As compared with the same period in 2011, there were no electricity

sales for ancillary services yet.

As of March 31, 2012, total liabilities stood at P4,869.6 million, P196.9 million or 3.9% lower than the

2011 level of P5,066.5 million. The decrease in liabilities was mainly due to the continuous pay-out of the

scheduled semi-annual loan repayments.

Total equity as of March 31, 2012 of P5,700.5 million is P1,580.5 million or 38.4% higher compared to

the March 31, 2011 level of P4,120.0 million.

SEC Form 17Q – 1Q 2012 26

Green Core Geothermal Inc.

(Amounts in PHP millions)

As of and for the periods ended

March 31 2012 2011

Revenues 2,365.4 1,814.7 Operating expenses* (1,901.8) (2,072.5) Other income (charges) - net 23.9 (107.9) Income (loss) before income tax 487.5 (365.7) Benefit from (provision for) income tax –

deferred (48.6) 36.6

Net income (loss) 438.9 (329.1)

Total Current Assets 1,729.2 1,249.4 Total Non-Current Assets 9,963.7 9,727.0 Total Liabilities 2,442.0 7,593.6 Total Equity 9,250.9 3,382.8

*Includes Cost of Sale of Electricity and General and Administrative Expenses

GCGI’s revenues increased by 30.3% or P550.7 million, to P2,365.4 million for the three-month period

ended March 31, 2012 from P1,814.7 million for the same period in 2011 due to higher revenues from the

sale of electricity as per agreed contracts that became effective in mid-2011.

Operating expenses decreased by 8.2% or P170.7 million, to P1,901.8 million in 2012 from

P2,072.5 million in 2011 due to lower cost of steam by an average of P0.19/kWh (P88.0 million). The

decrease is also due to lower operations & maintenance of P84.2 million and purchased services &

utilities of P28.8 million offset by higher general & administrative expenses of P29.8 million.

This period’s other income of P23.9 million consisted mainly of foreign exchange gains and the absence

in 2012 of interest expense.

Provision for income tax - deferred of P48.6 million in 2012 was a reversal of P36.6 million benefit from

income tax - deferred in 2011.

Total current assets increased by 38.4% or P479.8 million, to P1,729.2 million in 2012 from

P1,249.4 million in 2011 largely due to higher trade & other receivables of P301.1 million and other

current assets of P175.5 million.

Total noncurrent assets increased by 2.4% or P236.7 million, to P9,963.7 million in 2012 from

P9,727.0 million in 2011 due to higher property, plant and equipment of P190.8 million and other

noncurrent assets of P91.5 million reduced by lower deferred tax asset of P45.6 million.

Total liabilities decreased by 67.8% or P5,151.6 million, to P2,442.0 million in 2012 from

P7,593.6 million in 2011 while total equity increased by 173.5% or P5,868.1 million, to P9,250.9 million

in 2012 from P3,382.8 million in 2011 due mainly to the conversion of the P5,452.5 million advances

from EDC to equity coupled with the net income for the period April 1, 2011 to March 31, 2012

amoutning to P415.6 million.

SEC Form 17Q – 1Q 2012 27

Bac-Man Geothermal Inc.

(Amounts in PHP millions)

As of and for the periods ended

March 2012

March 2011

(Restated)

Revenues 738,935.3 –

Expenses (716,913.3) (2,135.8)

Other income 834.5 691.8

Operating income (loss) 22,856.5 (1,444.0)

Benefit from (provision for) income tax (36,208.1) 145.7

Net loss (13,351.6) (1,298.3)

Total Current Assets 484.9 134.4

Total Non-Current Assets 3,449.5 1,733.2

Total Current Liabilities 821.5 1,901.1

Total Equity 3,112.9 (33.5) *BGI was incorporated in the Philippines on April 7, 2010.

As of March 31, 2012, BGI has yet to start commercial operations.

Revenues earned result from electricity sales for the period pursuant to the signed PSAs with BATELEC

and Linde Philippines effective December 26, 2011.

The increase in expenses pertains primarily due to the cost of replacement power amounting to

P706.5 million.

The increase in current assets by 260.7% or P=350.5 million is due mainly to the increase in trade and

other receivables amounting to P=360.7 million partially offset by issuances of parts and supplies

inventories amounting to P=17.9 million.

Non-current asset increased by 99.0% or P=1,716.2 million resulting mainly from capitalized costs for the

on-going rehabilitation of the power plants of P=1,529.0 million. Testing and commissioning revenues

generated by Bac-man Unit 2 for the period was netted off in this account as required by PAS 16.

The decrease in liabilities and corresponding increase in equity results from the conversion of payables to

related parties into equity as capital infusion in December 2011.

SEC Form 17Q – 1Q 2012 28

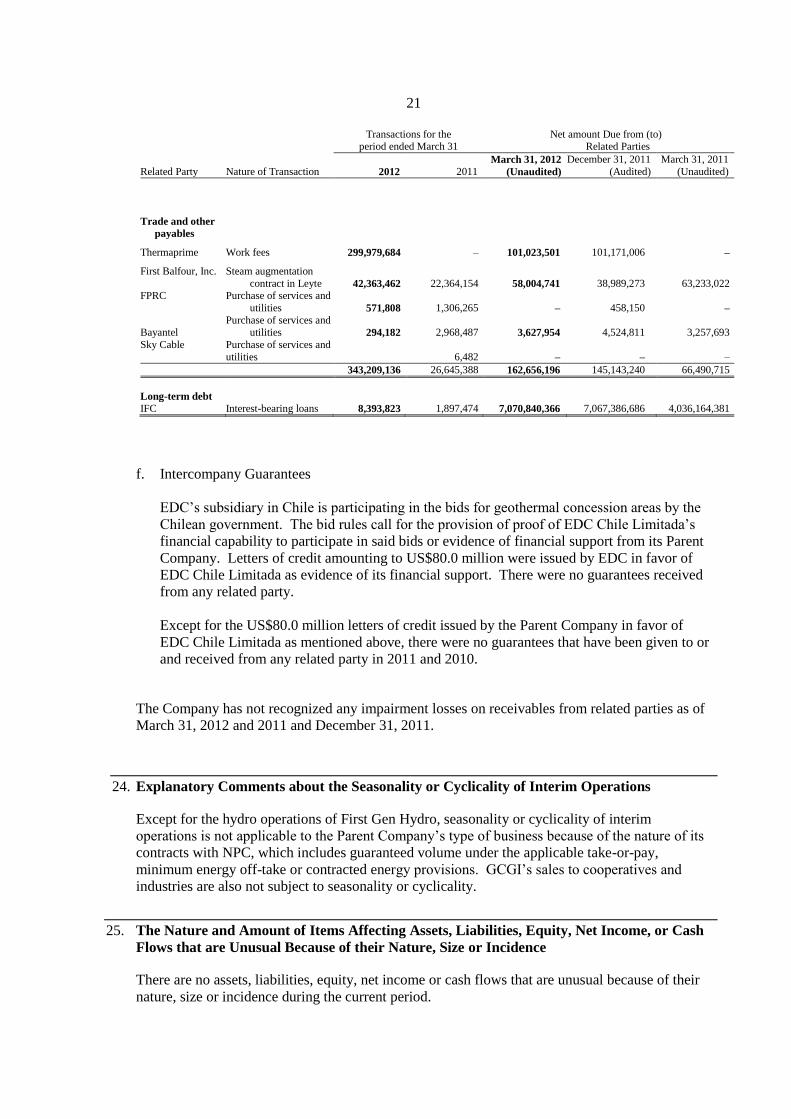

Commitments that will have an impact on the issuer’s liquidity

As of March 31, 2012, the company has unserved purchase orders and awarded contracts for the

purchase of various capital goods in the total amount of P155.7 million.

Other than these, we are not aware of any other material commitments that should impact the

Company’s liquidity.

Legal proceedings

There are no other material changes in the contingent liabilities since the last annual balance

sheet date.

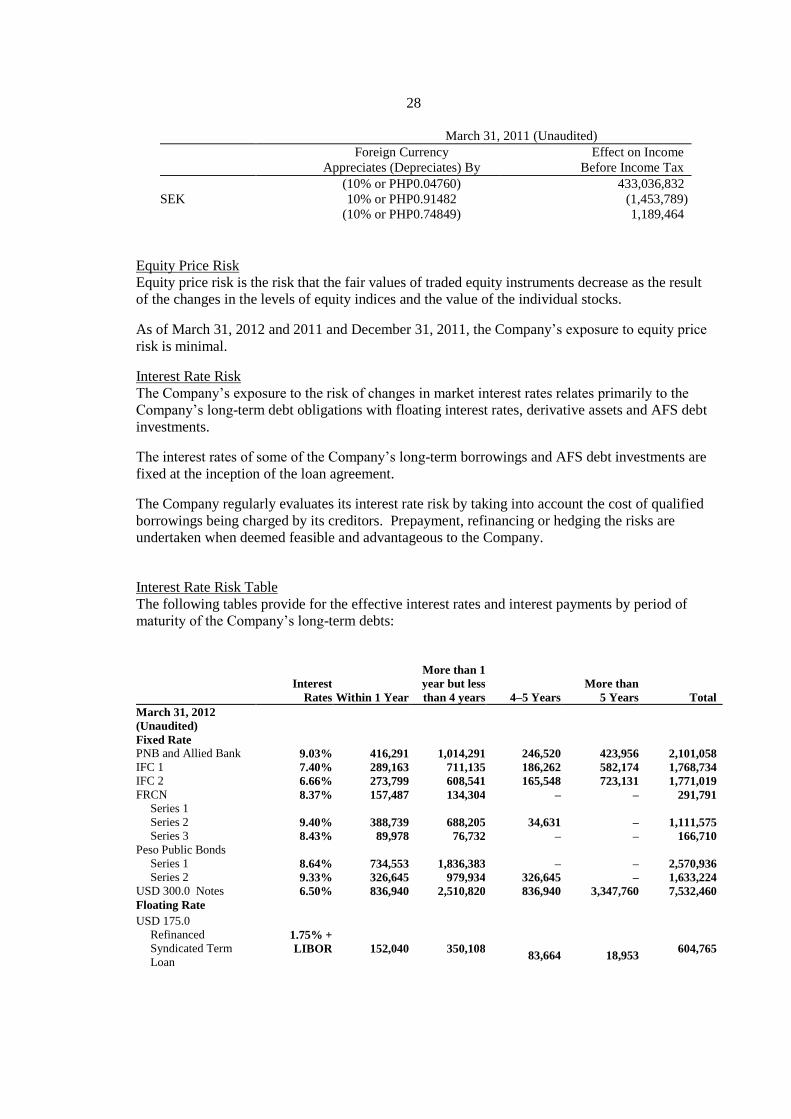

FOREIGN EXCHANGE AND INTEREST RATE EXPOSURE

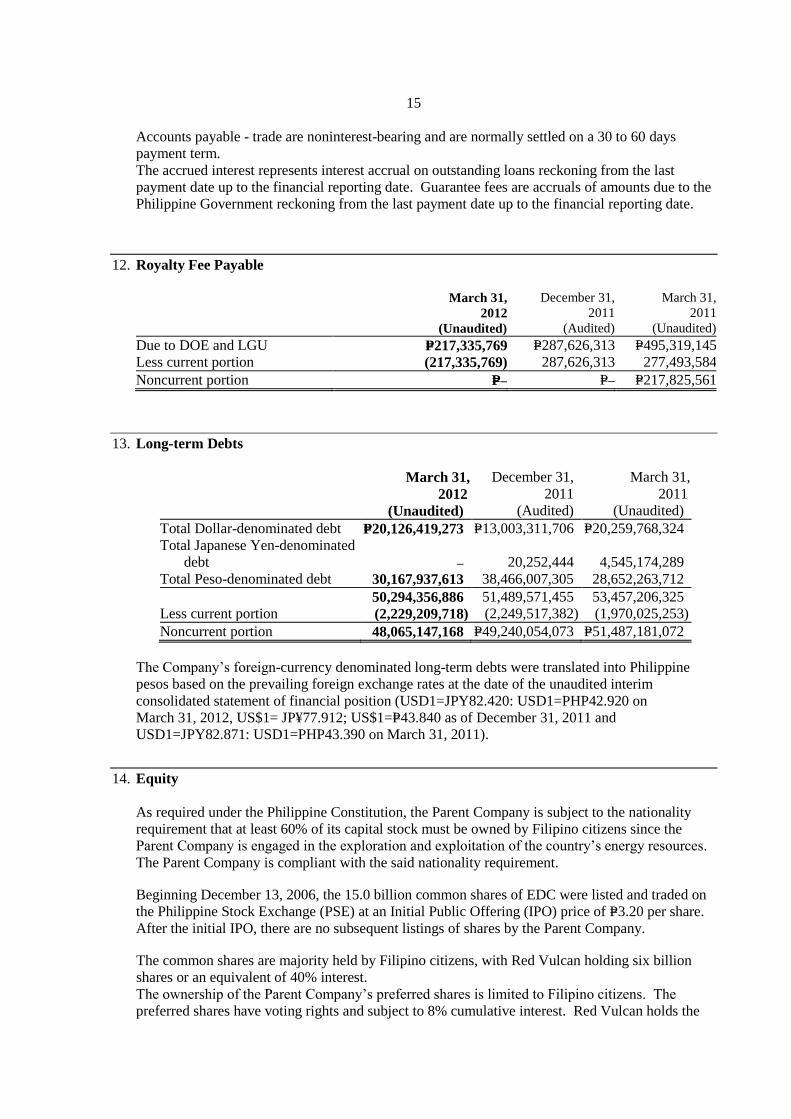

The Company has P=20,126.42 million in long-term US dollar denominated loans as of

March 31, 2012 which is 44.01% of the total company’s long-term loans.

OTHER MATTERS

CASH DIVIDEND

On March 13 2012, the BOD of the Parent Company approved the following cash dividends

in favor of all stockholders of record as of March 28, 2012 and payable on or before

April 24, 2012:

cash dividend of P=0.0008 per share on the preferred shares

regular cash dividend of P=0.10 per share on the common shares.

SEC Form 17Q – 1Q 2012 29

MAJOR STOCKHOLDERS

As of March 31, 2012, the total number of stockholders was 702 and price was P6.00 per share.

The public float level was at 52.79% (or 9,897,713,964 common shares).

List of Top 20 Stockholders as of March 31, 2012

Rank Name Nationality

Number of Shares

% Preferred Common Total

1

Red Vulcan Holdings

Corporation Filipino 9,375,000,000 7,500,000,000 16,875,000,000 60.00

2 PCD Nominee Corporation Foreign - 6,736,468,952 6,736,468,952 23.95

3 PCD Nominee Corporation Filipino - 3,147,041,711 3,147,041,711 11.19

4 First Gen Corporation Filipino - 991,782,700 991,782,700 3.53

5

Northern Terracotta Power

Corporation Filipino - 324,522,900 324,522,900 1.15

6 Federico R. Lopez Filipino - 6,092,501 6,092,501 0.02

7 Ernesto B. Rufino, Jr. Filipino - 5,694,700 5,694,700 0.02

8 Peter D. Garrucho, Jr. Filipino - 5,670,000 5,670,000 0.02

9 Benjamin K. Liboro Filipino - 3,525,500 3,525,500 0.01

10 Arthur A. De Guia Filipino - 2,200,000 2,200,000 0.01

11 CROSLO Holdings Corporation Filipino - 1,600,000 1,600,000 0.01

12 Hi-Light Corporation Filipino - 1,577,500 1,577,500 0.01

13 Mapazon Corporation Filipino - 1,470,000 1,470,000 0.01

14 Ronaldo C. Sabella Filipino - 1,100,000 1,100,000 0.00

15 ALG Holdings Corporation Filipino - 875,000 875,000 0.00

16 Raul I. Macatangay Filipino - 725,000 725,000 0.00

17 Rosalind Camara Filipino - 663,750 663,750 0.00

18 Rodolfo R. Waga, Jr. Filipino - 658,750 658,750 0.00

19 Emelita D. Sabella Filipino - 521,000 521,000 0.00

20

Rodolfo R. Waga, Jr. &/or Grace

B. Waga Filipino - 501,200 501,200 0.00

SEC Form 17Q – 1Q 2012 30

BOARD OF DIRECTORS

As of March 31, 2012, the members of Board of Directors of EDC are as follows:

Oscar M. Lopez Chairman Emeritus

Federico R. Lopez Chairman and Chief Executive Officer

Peter D. Garrucho, Jr. Director

Elpidio L. Ibañez Director

Ernesto B. Pantangco Director and Executive Vice President

Francis Giles B. Puno Director

Richard B. Tantoco Director, President and Chief Operating Officer

Jonathan C. Russell Director

Edgar O. Chua Independent Director

Francis Ed. Lim Independent Director

Arturo T. Valdez Independent Director

OFFICERS

As of March 31, 2012, the officers of EDC are as follows:

Name Position

Federico R. Lopez Chief Executive Officer

Richard B. Tantoco President and Chief Operating Officer

Ernesto B. Pantangco Executive Vice President

Agnes C. de Jesus Senior Vice President for Environment and

External Relations, and Compliance Officer

Nestor H. Vasay Senior Vice President, Chief Financial

Officer and Treasurer

Marcelino M. Tongco Senior Vice President

Manuel S. Ogena Senior Vice President for Technical Services

Dominic M. Camu Senior Vice President for Power Generation

Danilo C. Catigtig Senior Vice President for Strategic Initiatives

Office

Ernesto G. Espinosa Vice President for Human Resource

Management

Vincent Martin C. Villegas Vice President for Business Development

Erwin O. Avante Vice President for Corporate Finance

Rico G. Bersamin Vice President for Steam Field Operations

Ferdinand B. Poblete Vice President, Chief Information Officer

Ariel Arman V. Lapus Vice President/Project Development Officer

of EDC International

Ellsworth R. Lucero Vice President - Power

Dwight A. Maxino Vice President - So. Negros Geothermal

SEC Form 17Q – 1Q 2012 31

Name Position

Project

Manuel C. Paete Vice President - Leyte Geothermal Project

Liberato S. Virata Vice President - Bacon-Manito Geothermal

Project

Wilfredo A. Malonzo Vice President for Supply Chain

Management

Maribel A. Manlapaz Comptroller

Teodorico Jose R. Delfin Corporate Secretary

Ana Maria A. Katigbak-Lim Assistant Corporate Secretary

Glenn L. Tee Senior Manager, Internal Audit

Erudito S. Recio Senior Manager, Investor Relations

Annex I

Energy Development Corporation and Subsidiaries A Subsidiary of Red Vulcan Holdings Corporation

Unaudited Interim Condensed Consolidated Financial Statements March 31, 2012 and 2011 (With Comparative Figures as of December 31, 2011 )

ENERGY DEVELOPMENT CORPORATION AND SUBSIDIARIES

UNAUDITED INTERIM CONSOLIDATED

STATEMENTS OF FINANCIAL POSITION

MARCH 31, 2012 AND 2011

(With Comparative Figures as of December 31, 2011)

March 31,

2012

(Unaudited)

December 31,

2011

(Audited)

March 31,

2011

(Unaudited)

ASSETS

Current Assets

Cash and cash equivalents (Notes 5 and 32) P=13,123,430,591 P=12,493,406,963 P=19,814,618,839

Trade and other receivables (Notes 6 and 32) 3,604,793,410 3,411,309,528 2,922,268,849

Available-for-sale (AFS) investments (Note 32) 649,830,260 673,853,680 690,344,012

Parts and supplies inventories (Note 7) 3,244,932,240 3,355,767,653 2,641,149,059

Derivative assets (Note 32) – – 11,789,416

Due from related parties (Notes 23 and 32) – 7,812 – Other current assets 980,383,906 741,911,257 853,618,425

Total Current Assets 21,603,370,407 20,676,256,893 26,933,788,600

Noncurrent Assets

Property, plant and equipment – net (Note 8) 58,256,469,805 57,676,929,006 58,160,864,628

Intangible assets (Note 9) 4,713,967,976 4,705,245,708 4,518,994,137

Deferred tax assets – net (Note 22) 1,331,550,748 1,420,656,657 987,867,438

Exploration and evaluation assets 1,505,532,721 1,087,079,413 1,201,456,358

Other noncurrent assets – net (Note 10) 4,740,200,276 4,451,649,107 3,523,767,037

Total Noncurrent Assets 70,547,721,526 69,341,559,891 68,392,949,598

TOTAL ASSETS P=92,151,091,933 P=90,017,816,784 P=95,326,738,198

LIABILITIES AND EQUITY

Current Liabilities

Loan payable (Note 32) P=– P=– P=90,000,000

Trade and other payables (Notes 11 and 32) 8,710,058,490 6,704,075,261 8,232,463,833

Income tax payable 206,667,979 18,736,456 239,681,571

Due to related parties (Notes 23 and 32) 43,505,312 60,090,825 251,353,422

Derivative liabilities (Note 32) – – 3,641,161

Current portion of:

Long-term debts (Notes 13 and 32) 2,229,209,718 2,249,517,382 1,970,025,253

Royalty fee payable (Notes 12 and 32) 217,335,769 287,626,313 277,493,584

Total Current Liabilities 11,406,777,268 9,320,046,237 11,064,658,824

March 31,

2012

(Unaudited)

December 31,

2011

(Audited)

March 31,

2011

(Unaudited)

Noncurrent Liabilities

Long-term debts - net of current portion

(Notes 13 and 32) 48,065,147,168 49,240,054,073 51,487,181,072

Royalty fee payable - net of current

portion (Notes 12 and 32) – – 217,825,561

Net retirement and other post-

employment benefits 1,144,547,300 1,054,237,256 1,298,609,476

Provisions and other long-term

liabilities (Note 8) 723,793,331 756,877,725 573,836,850

Total Noncurrent Liabilities 49,933,487,799 51,051,169,054 53,577,452,959

Total Liabilities 61,340,265,067 60,371,215,291 64,642,111,783

Equity (Note 14)

Attributable to Equity Holders of the

Parent Company:

Preferred stock 93,750,000 93,750,000 93,750,000

Common stock 18,750,000,000 18,750,000,000 18,750,000,000

Common shares in employee trust

account (372,272,723) (372,272,723) (377,483,019)

Additional paid-in capital 6,266,966,828 6,266,966,828 6,266,341,978

Equity reserve (3,706,430,769) (3,706,430,769) (3,706,430,769)

Net accumulated unrealized gain on

AFS investments 80,075,239 91,758,915 110,290,794

Cumulative translation adjustment 633,539 592,534 1,370,000

Retained earnings 7,121,471,769 6,304,695,114 7,898,784,383

28,234,193,883 27,429,059,899 29,036,623,367

Non-controlling interest 2,576,632,983 2,217,541,594 1,648,003,048

Total Equity 30,810,826,866 29,646,601,493 30,684,626,415

TOTAL LIABILITIES AND

EQUITY P=92,151,091,933 P=90,017,816,784 P=95,326,738,198

See accompanying Notes to Unaudited Interim Condensed Consolidated Financial Statements.

ENERGY DEVELOPMENT CORPORATION AND SUBSIDIARIES

UNAUDITED INTERIM CONSOLIDATED STATEMENTS OF INCOME

FOR THE PERIODS ENDED MARCH 31, 2012 AND 2011

2012 2011

REVENUES (Note 4)

Sale of electricity P=7,536,756,442 P=5,798,160,507

Revenue from drilling services 167,581,380 154,616,637

7,704,337,822 5,952,777,144

COSTS OF SALES AND SERVICES

Costs of sales of electricity and steam (Note 15) (2,741,304,687) (2,762,726,562)

Cost of drilling services (Note 16) (95,439,340) (108,323,427)

(2,836,744,027) (2,871,049,989)

GENERAL AND ADMINISTRATIVE

EXPENSES (Note 17)

(919,583,173)

(888,899,817)

FINANCIAL INCOME (EXPENSES)

Interest income (Notes 4 and 20) 93,870,182 123,917,688

Interest expense (Notes 4 and 19) (1,015,345,353) (1,038,921,265)

(921,475,171) (915,003,577)

OTHER INCOME (CHARGES) (Note 4)

Foreign exchange gains - net (Note 18) 337,953,506 188,561,127

Derivatives gain (loss) – net – 37,553,046

Miscellaneous – net 59,407,284 30,702,512

397,360,790 256,816,685

INCOME BEFORE INCOME TAX 3,423,896,241 1,534,640,446

PROVISION FOR INCOME TAX

Current (187,931,523) (168,434,061)

Deferred (89,105,910) 94,387,514

(277,037,433) (74,046,547)

NET INCOME P=3,146,858,808 P=1,460,593,899

Net income attributable to:

Equity Holders of the Parent Company P=2,699,276,655 P=1,381,680,572

Non-controlling interest 447,582,153 78,913,327

P=3,146,858,808 P=1,460,593,899

Basic/Diluted Earnings Per Share for Net

Income Attributable to Equity Holders of

the Parent Company (Note 21) P=0.144 P=0.073

See accompanying Notes to Unaudited Interim Condensed Consolidated Financial Statements.

ENERGY DEVELOPMENT CORPORATION AND SUBSIDIARIES

UNAUDITED INTERIM CONSOLIDATED

STATEMENTS OF COMPREHENSIVE INCOME

FOR THE PERIODS ENDED MARCH 31, 2012 AND 2011

2012 2011

Net Income P=3,146,858,808 P=1,460,593,899

Other comprehensive income

Unrealized gain (loss) on AFS investments (11,683,676) (9,428,003)

Total comprehensive income P=3,135,175,132 P=1,451,165,896

Total comprehensive income attributable to:

Equity Holders of the Parent Company P=2,687,592,979 P=1,372,252,569

Non-controlling interest 447,582,153 78,913,327

P=3,135,175,132 P=1,451,165,896

See accompanying Notes to Unaudited Interim Condensed Consolidated Financial Statements.

ENERGY DEVELOPMENT CORPORATION AND SUBSIDIARIES

UNAUDITED INTERIM CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY

FOR THE PERIODS ENDED MARCH 31, 2012 AND 2011

Equity Attributable to Equity Holders of the Parent Company

Preferred

Stock

Common

Stock

Common

Shares in

Employee

Trust Account

Additional

Paid-in

Capital

Equity

Reserve

Net

Accumulated

Unrealized

Gain on AFS

Investments

Retained

Earnings Subtotal

Non-controlling

Interest Total Equity

Cumulative

Translation

Adjustment

Balances, December 31, 2010, as

previously reported P=93,750,000 P=18,750,000,000 (P=379,219,785) P=6,266,099,283 (P=3,706,430,769) P=119,718,797

P=1,370,000 P=9,524,603,810 P=30,669,891,336 P=1,569,089,721 P=32,238,981,057

Total comprehensive income:

Net income – – – – – – – 1,381,680,572 1,381,680,572 78,913,327 1,460,593,899

Changes in fair value of AFS investments recognized in equity

–

–

–

–

– (9,428,003)

–

– (9,428,003)

– (9,428,003)

– – – – – (9,428,003) – 1,381,680,572 1,372,252,569 78,913,327 1,451,165,896

Cash dividend (Note 28) – – – – – – – (3,007,500,000) (3,007,500,000) (3,007,500,000) Share-based payment – – 1,736,766 464,953 – – – – 2,201,719 – 2,201,719

Deferred tax effect of share-based payment – – – (222,257) – – – – (222,257) – (222,257)

Balances, March 31, 2011 P=93,750,000 P=18,750,000,000 (P=377,483,019) P=6,266,341,979 (P=3,706,430,769) P=110,290,794 P=1,370,000 P=7,898,784,382 P=29,036,623,367 P=1,648,003,048 P=30,684,626,415

Balances, December 31, 2011 P=93,750,000 P=18,750,000,000 (P=372,272,723) P=6,266,966,828 (P=3,706,430,769) P=91,758,915 P=592,534 P=6,304,695,114 P=27,429,059,899 P=2,217,541,594 P=29,646,601,493

Total comprehensive income:

Net income – – – – – – – 2,699,276,655 2,699,276,655 447,582,153 3,146,858,808

Changes in fair value of AFS

investments recognized in equity

–

–

–

–

– (11,683,676)

–

– (11,683,676)

– (11,683,676) Cumulative translation adjustment – – – – – – 41,005 – 41,005 – 41,005

– – – – – (11,683,676) 41,005 2,699,276,655 2,687,633,984 447,582,153 3,135,216,137

Cash dividend (Note 28) – – – – – – – (1,882,500,000) (1,882,500,000) (88,490,764) (1,970,990,764)

Balances, March 31, 2012 P=93,750,000 P=18,750,000,000 (P=372,272,723) P=6,266,966,828 (P=3,706,430,769) P=80,075,239 P=633,539 P=7,121,471,769 P=28,234,193,883 P=2,576,632,983 P=30,810,826,866

See accompanying Notes to Unaudited Interim Condensed Consolidated Financial Statements.

ENERGY DEVELOPMENT CORPORATION AND SUBSIDIARIES

UNAUDITED INTERIM CONSOLIDATED STATEMENTS OF CASH FLOWS

FOR THE PERIODS ENDED MARCH 31, 2012 AND 2011

2012 2011

CASH FLOWS FROM OPERATING ACTIVITIES

Income before income tax P=3,423,896,241

P=1,534,640,446

Adjustments for:

Interest expense 1,015,345,353

1,038,921,265

Depreciation and amortization 897,498,991

906,034,567

Unrealized foreign exchange losses (gains) (439,037,300)

(179,415,157)

Interest income (93,870,182)

(123,917,688)

Provision for retirement and post-employment benefits 90,297,471

70,459,883

Recovery of impairment of property plant and

equipment (66,321,901)

–

Provision for share-based benefit cost –

2,201,719

Provision for doubtful accounts 1,003,830

Loss on retirement of property, plant and equipment (1,122,882)

207,660

Profit on storehouse items - inventory variations –

(3,926,511)

Operating income before working capital changes 4,827,689,621

3,245,206,184

Decrease (increase) in:

Trade and other receivables (144,522,954)

1,296,889,303

Parts and supplies inventories 110,835,413

(59,779,721)

Other current assets (204,971,055)

(1,669,438)

Due to related party 7,812

– Increase (decrease) in:

Trade and other payables 435,577,892

(204,340,380)

Due to related parties (57,150,511)

(19,044,294)

Royalty fee payable (74,987,732) (69,140,651)

Cash generated from operations 4,892,478,486

4,188,121,003

Interest and financing charges paid (1,265,347,644)

(550,254,169)

Income tax paid (33,501,594)

– Retirement and other post-retirement benefits paid 12,573

(80,000,000)

Net cash flows from operating activities 3,593,641,821 3,557,866,834

2012 2011

CASH FLOWS FROM INVESTING ACTIVITIES

Acquisition of property, plant and equipment (1,416,845,788)

(2,106,030,465)

Proceeds from sale of property and equipment 71,863,569

Interest received 45,189,497

129,296,048

Decrease (increase) in:

Exploration and evaluation assets (418,453,308)

(2,044,119)

Other noncurrent assets (323,791,575)

(300,127,644)

Net cash flows from (used in) investing activities (2,042,037,605) (2,278,906,180)

CASH FLOWS FROM FINANCING ACTIVITIES

Proceeds from:

Long-term debts –

13,350,000,000

Payments of:

Short-term loans –

(85,000,000)

Long-term debts (798,852,453)

(618,105,082)

Cash dividends (88,490,765)

–

Increase in other long-term liabilities (40,508,508)

(38,664,359)

Net cash flows (used in) financing activities (927,851,726) 12,608,230,559

NET INCREASE IN CASH AND CASH EQUIVALENTS 623,752,490

13,887,191,213

EFFECT OF FOREIGN EXCHANGE RATE CHANGES

ON CASH AND CASH EQUIVALENTS 6,271,137

(230,497,506)

CASH AND CASH EQUIVALENTS AT BEGINNING OF

PERIOD 12,493,406,964 6,157,925,132

CASH AND CASH EQUIVALENTS AT END OF

PERIOD P=13,123,430,591 P=19,814,618,839

See accompanying Notes to Unaudited Interim Condensed Consolidated Financial Statements.

ENERGY DEVELOPMENT (EDC) CORPORATION AND SUBSIDIARIES A Subsidiary of Red Vulcan Holdings Corporation

SELECTED NOTES TO THE UNAUDITED INTERIM CONDENSED

CONSOLIDATED FINANCIAL STATEMENTS

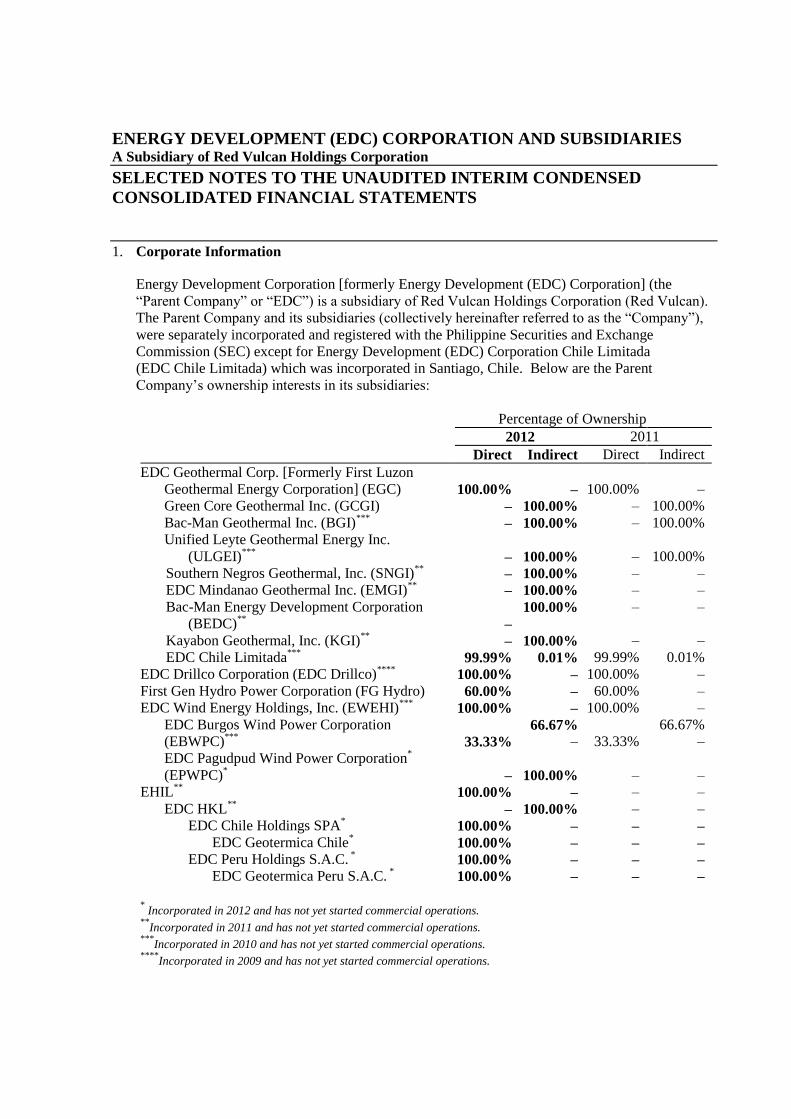

1. Corporate Information

Energy Development Corporation [formerly Energy Development (EDC) Corporation] (the

“Parent Company” or “EDC”) is a subsidiary of Red Vulcan Holdings Corporation (Red Vulcan).

The Parent Company and its subsidiaries (collectively hereinafter referred to as the “Company”),

were separately incorporated and registered with the Philippine Securities and Exchange

Commission (SEC) except for Energy Development (EDC) Corporation Chile Limitada

(EDC Chile Limitada) which was incorporated in Santiago, Chile. Below are the Parent

Company’s ownership interests in its subsidiaries:

Percentage of Ownership

2012 2011

Direct Indirect Direct Indirect

EDC Geothermal Corp. [Formerly First Luzon

Geothermal Energy Corporation] (EGC) 100.00%

– 100.00%

–

Green Core Geothermal Inc. (GCGI) – 100.00% – 100.00%

Bac-Man Geothermal Inc. (BGI)***

– 100.00% – 100.00%

Unified Leyte Geothermal Energy Inc.

(ULGEI)***

– 100.00% – 100.00%

Southern Negros Geothermal, Inc. (SNGI)**

– 100.00% – –

EDC Mindanao Geothermal Inc. (EMGI)**

– 100.00% – –

Bac-Man Energy Development Corporation

(BEDC)**

–

100.00% – –

Kayabon Geothermal, Inc. (KGI)**

– 100.00% – –

EDC Chile Limitada***

99.99% 0.01% 99.99% 0.01%

EDC Drillco Corporation (EDC Drillco)****

100.00% – 100.00% –

First Gen Hydro Power Corporation (FG Hydro) 60.00% – 60.00% –

EDC Wind Energy Holdings, Inc. (EWEHI)***

100.00% – 100.00% –

EDC Burgos Wind Power Corporation

(EBWPC)***

33.33%

66.67%

– 33.33%

66.67%

–

EDC Pagudpud Wind Power Corporation*

(EPWPC)* –

100.00% –

–

EHIL**

100.00% – – –

EDC HKL**

– 100.00% – –

EDC Chile Holdings SPA* 100.00% – – –

EDC Geotermica Chile* 100.00% – – –

EDC Peru Holdings S.A.C. * 100.00% – – –

EDC Geotermica Peru S.A.C. * 100.00% – – –

* Incorporated in 2012 and has not yet started commercial operations.

**Incorporated in 2011 and has not yet started commercial operations.

***Incorporated in 2010 and has not yet started commercial operations.

****Incorporated in 2009 and has not yet started commercial operations.

- 2 -

History of Ownership

Beginning December 13, 2006, the common shares of EDC were listed and traded on the

Philippine Stock Exchange (PSE). Up to November 2007, EDC was controlled by the Philippine

National Oil Company (PNOC), a government-owned and controlled corporation, and the

PNOC EDC Retirement Fund.

On November 29, 2007, PNOC and PNOC EDC Retirement Fund sold their combined interests in

EDC to Red Vulcan (a Philippine corporation). Red Vulcan was then a wholly owned subsidiary

of First Gen Corporation (First Gen, a publicly listed Philippine corporation) through Prime

Terracota Holdings Corporation (Prime Terracota). First Gen’s indirect interest in EDC consists

of 6.0 billion common shares and 7.5 billion preferred shares. Control was then established

through First Gen’s 60% indirect voting interest in EDC. Meanwhile, First Philippine Holdings

Corporation (First Holdings) directly owns 66.2% of the common shares of First Gen.

Accordingly, First Holdings became then the ultimate parent of the Company.

On May 12, 2009, First Gen’s indirect voting interest in Red Vulcan was reduced to 45% with the

balance taken up by Lopez Inc. Retirement Fund (40%) and Quialex Realty Corporation (15%)

through the issuance of preferred shares by Prime Terracota. As a result of this transaction, Prime

Terracota replaced First Holdings as the ultimate parent of EDC effective May 12, 2009.

Nature of Operations

The Parent Company operates 12 geothermal projects in five geothermal service contract areas,

namely Tongonan Geothermal Project (TGP), Southern Negros Geothermal Project (SNGP),

Bacon-Manito Geothermal Project (BMGP), Mt. Apo Geothermal Project (MGP) and Northern

Negros Geothermal Project (NNGP) under the Geothermal Service Contracts (GSCs) entered into

with the Department of Energy (DOE) pursuant to the provisions of Presidential Decree (P.D.)

1442. These GSCs were replaced by Geothermal Renewable Energy Service Contracts (GRESCs)

on October 23, 2009.

Geothermal steam produced is delivered to the company-owned power plants to produce

electricity. EDC sells power to National Power Corporation (NPC), privately-owned distribution

utilities (DUs) and large industrial customers, pursuant to Power Purchase Agreements (PPAs) and

Power Supply Agreements (PSAs). Separately, it also has drilling activities in Papua New

Guinea.

Change in Corporate Name

On the July 29, 2010 annual stockholders meeting, the stockholders approved the amendment of

the Parent Company’s name from Energy Development (EDC) Corporation to Energy

Development Corporation. The Philippine SEC approved the change of the Parent Company’s

name on November 5, 2010.

Subsidiaries

On October 20 and November 17, 2008, in line with its objective of focusing on renewable

energy, the Parent Company acquired a total of 60% interest in FG Hydro from First Gen. FG

Hydro operates the 132 Megawatt (MW) Pantabangan and Masiway Hydro-Electric Power Plants

(PAHEP/MAHEP) located in Nueva Ecija, Philippines. FG Hydro buys from and sells electricity

to the Wholesale Electricity Spot Market (WESM) and to various DUs under the Transition Power

Supply Contracts (TPSCs).

EGC is a special-purpose company incorporated on April 9, 2008 to participate in the bid for

another local power plant. The bid was won by and awarded to another local entity. Thereafter,

there has been no business activity yet as far as EGC is concerned other than being the investment

- 3 -

holding company of its wholly owned subsidiaries, namely GCGI, BGI, ULGEI, SNGI, EMGI,

BEDC and KGI. EGC also has a 0.01% stake in EDC Chile Limitada.

On March 8, 2011, the Philippine SEC approved the change of First Luzon Geothermal Energy

Corporation’s corporate name to EGC.

GCGI was incorporated on June 22, 2009 with primary activities on power generation,

transmission, distribution, and other energy related businesses. GCGI is currently operating the

192.5 MW Palinpinon and 112.5 MW Tongonan 1 geothermal power plants in Negros Oriental

and Leyte, respectively, following its successful acquisition from the Power Sector Assets and

Liabilities Management Corporation (PSALM) in 2009.

EDC Drillco is a company incorporated on September 28, 2009 to act as an independent service