Embed Size (px)

Citation preview

LPL FINANCIAL RESEARCH

Outlook

2

2009 OUTLOOK

How We Got Here

Industry changes that led to a lack of oversight and regulation over a number of major financial institutions.

Drastically lowering lending standards without recalibrating risk assessment tools.

Financial institutions increasing leverage to inappropriate levels and their dependence on the capital markets.

3

2009 OUTLOOK

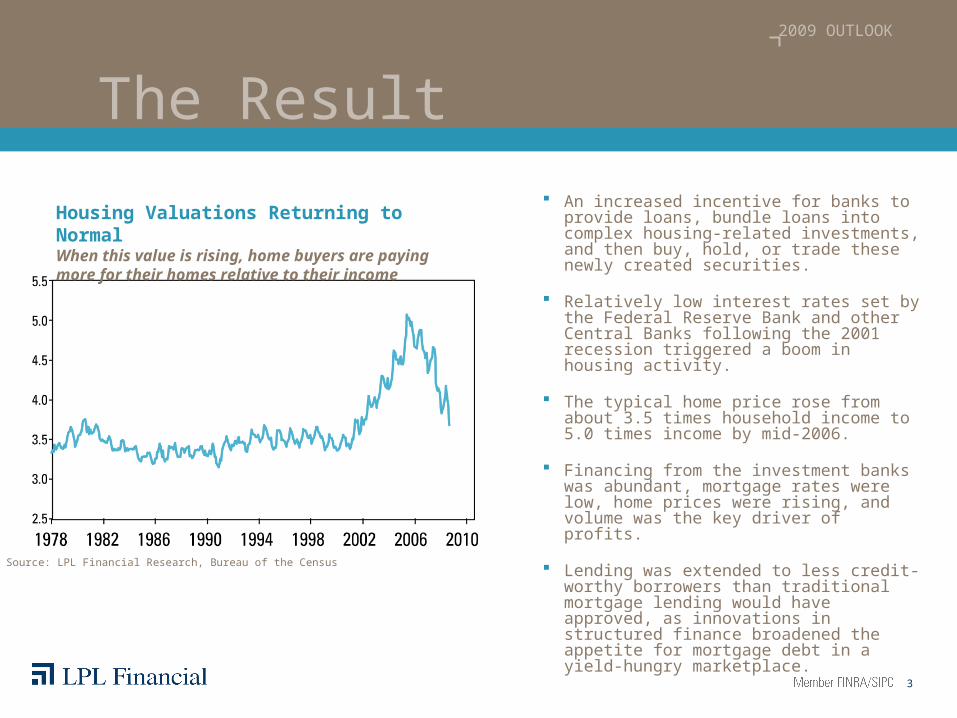

The Result

An increased incentive for banks to provide loans, bundle loans into complex housing-related investments, and then buy, hold, or trade these newly created securities.

Relatively low interest rates set by the Federal Reserve Bank and other Central Banks following the 2001 recession triggered a boom in housing activity.

The typical home price rose from about 3.5 times household income to 5.0 times income by mid-2006.

Financing from the investment banks was abundant, mortgage rates were low, home prices were rising, and volume was the key driver of profits.

Lending was extended to less credit-worthy borrowers than traditional mortgage lending would have approved, as innovations in structured finance broadened the appetite for mortgage debt in a yield-hungry marketplace.

Housing Valuations Returning to NormalWhen this value is rising, home buyers are paying more for their homes relative to their income

Source: LPL Financial Research, Bureau of the Census

4

2009 OUTLOOK

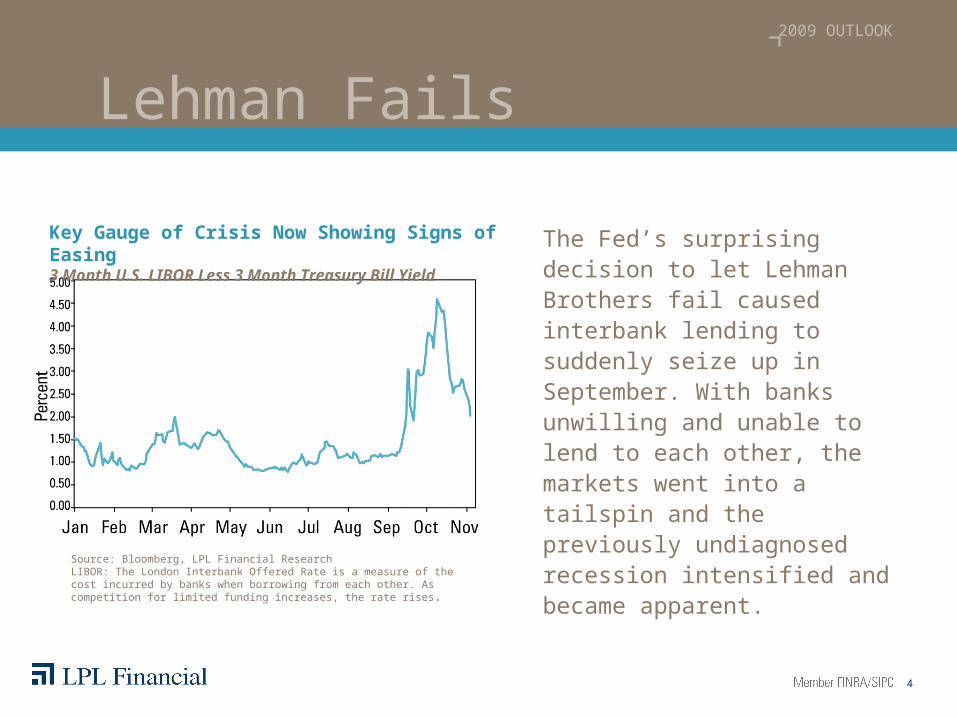

Lehman Fails

The Fed’s surprising decision to let Lehman Brothers fail caused interbank lending to suddenly seize up in September. With banks unwilling and unable to lend to each other, the markets went into a tailspin and the previously undiagnosed recession intensified and became apparent.

Key Gauge of Crisis Now Showing Signs of Easing3 Month U.S. LIBOR Less 3 Month Treasury Bill Yield

Source: Bloomberg, LPL Financial ResearchLIBOR: The London Interbank Offered Rate is a measure of the cost incurred by banks when borrowing from each other. As competition for limited funding increases, the rate rises.

5

2009 OUTLOOK

As a result, we present three scenarios for 2009:

Our base case

A bear case

And bull case

What’s on the Horizon

The heightened uncertainty and conditional nature of the current macroeconomic and policy backdrop generated a wider range of possibilities for 2009 than for most years.

6

2009 OUTLOOK

Base Case The financial panic that began in September 2008 will subside in early 2009 allowing a normalization of financial markets by mid-year 2009.

Scenario:

Economy emerges from recession in second half of 2009

Inflation turns negative early in 2009, but rises by year end

The S&P 500 posts a mid-teen return. Volatility gives way to earnings/sentiment consistency in Q3/4. S&P finishes around 1000-1050.

The Barclays Aggregate Bond Index posts a mid- to high-single digit return.

Alternatives “volatility strategy” investments continue to benefit returns in first part of ’09.

Alternative investments may not be suitable for all investors and should be considered as an investment for the risk capital portion of the investor's portfolio. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

7

2009 OUTLOOK

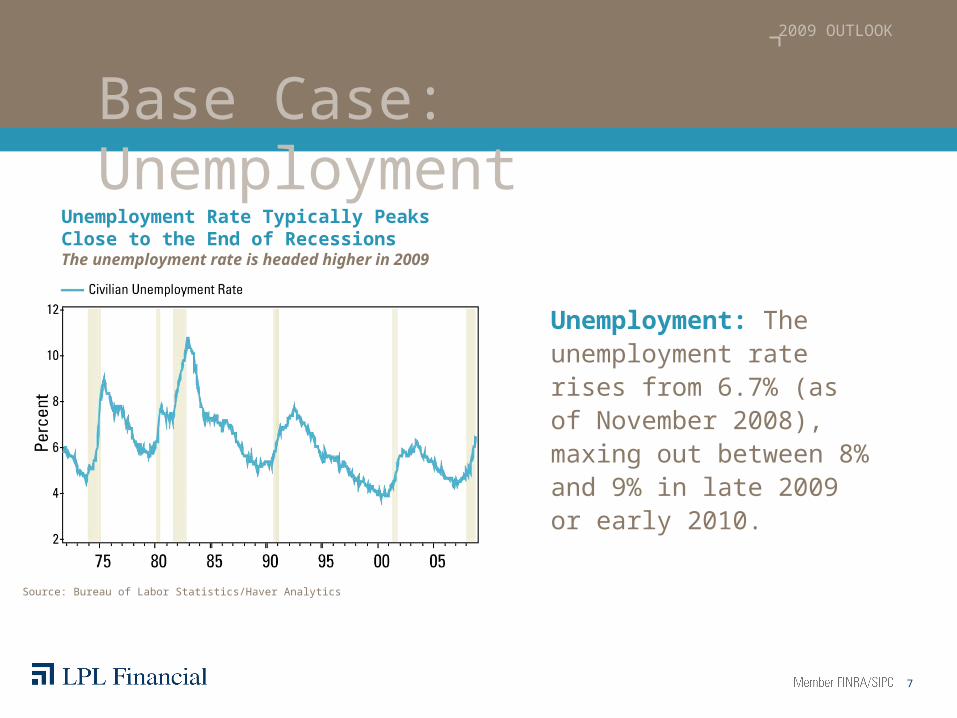

Base Case: Unemployment

Unemployment: The unemployment rate rises from 6.7% (as of November 2008), maxing out between 8% and 9% in late 2009 or early 2010.

Unemployment Rate Typically Peaks Close to the End of RecessionsThe unemployment rate is headed higher in 2009

Source: Bureau of Labor Statistics/Haver Analytics

8

2009 OUTLOOK

Base Case: P/E

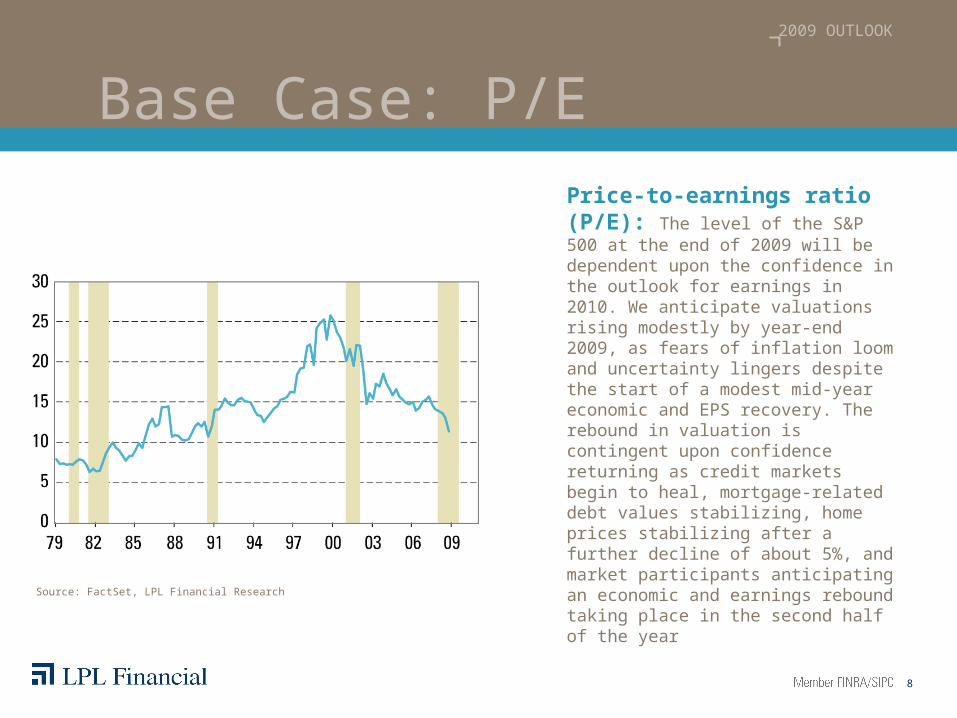

Price-to-earnings ratio (P/E): The level of the S&P 500 at the end of 2009 will be dependent upon the confidence in the outlook for earnings in 2010. We anticipate valuations rising modestly by year-end 2009, as fears of inflation loom and uncertainty lingers despite the start of a modest mid-year economic and EPS recovery. The rebound in valuation is contingent upon confidence returning as credit markets begin to heal, mortgage-related debt values stabilizing, home prices stabilizing after a further decline of about 5%, and market participants anticipating an economic and earnings rebound taking place in the second half of the year

Source: FactSet, LPL Financial Research

9

2009 OUTLOOK

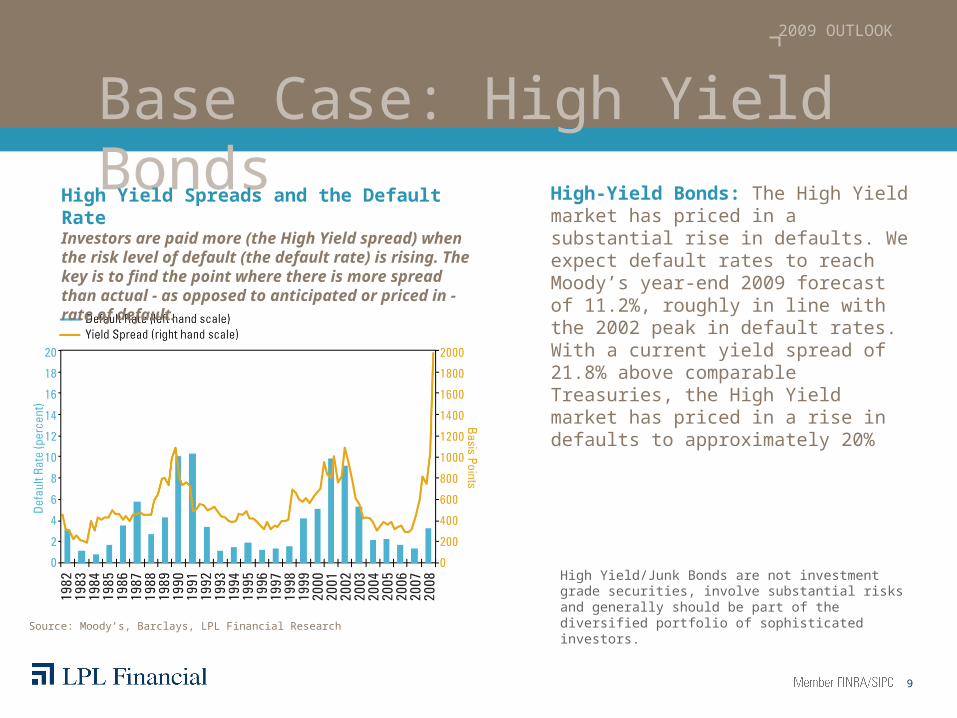

Base Case: High Yield BondsHigh-Yield Bonds: The High Yield market has priced in a substantial rise in defaults. We expect default rates to reach Moody’s year-end 2009 forecast of 11.2%, roughly in line with the 2002 peak in default rates. With a current yield spread of 21.8% above comparable Treasuries, the High Yield market has priced in a rise in defaults to approximately 20%

High Yield Spreads and the Default RateInvestors are paid more (the High Yield spread) when the risk level of default (the default rate) is rising. The key is to find the point where there is more spread than actual - as opposed to anticipated or priced in - rate of default.

Source: Moody’s, Barclays, LPL Financial Research

High Yield/Junk Bonds are not investment grade securities, involve substantial risks and generally should be part of the diversified portfolio of sophisticated investors.

10

2009 OUTLOOK

Base Case: What Investors Can Do

Continue to favor U.S. markets over International and Emerging Markets.

Favor Growth over Value among Large Cap stocks.

Look to yield advantages of Corporate Bonds, Agency Bonds, Preferred Stocks, and Mortgage-Backed Securities relative to Treasuries are at or beyond the biggest ever witnessed in the bond market.

Throughout 2009, shift from mutual fund strategies that help with volatility, like Covered Calls and Global Macro, to investments that search for value in credit and stocks.

Alternative investments may not be suitable for all investors and should be considered as an investment for the risk capital portion of the investor's portfolio. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and are subject to availability and change in price.

11

2009 OUTLOOK

Bear Case The financial panic lingers well into 2010, and financial markets do not normalize at all over the course of 2009.

Scenario:

Economy lingers in a recession throughout 2009 into 2010 with a lending frozen market

The S&P 500 posts returns similar to 2008 with a possible 35% decline as confidence fails and earnings tumble20%. The S&P 500 finishes around 560

The Barclays Aggregate Bond Index return low to mid-single digit returns with additional Treasury gains offset by price weakness in non-Treasury sectors: Corporate, Bonds, Mortgage-Backed Securities (MBS), and Agency Bonds

Alternative investment “volatility strategy” opportunities: Long/Short, Covered Calls, Managed Futures, Global Macro, Absolute Return, and Market Neutral

Alternative investments may not be suitable for all investors and should be considered as an investment for the risk capital portion of the investor's portfolio. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

12

2009 OUTLOOK

Bear Case: What Investors Can Do

Adopt a defensive posture by underweighting the stock market and favoring the safest investments, such as cash equivalents

Be aware, the outlook for deflation in this bearish scenario means that gold, a traditional safe haven, may also suffer

Focus stock market exposure on Large Cap Growth defensive sectors like Consumer Staples and Healthcare and underweight cyclical stocks in the Financials, Consumer Discretionary, and Information Technology sectors

Consider alternative strategies that emphasize short positions that may also provide a hedge against further stock market declines

In the fixed income market overweight long maturity TreasuriesAlternative investments may not be suitable for all investors and should be considered as an investment for the risk capital portion of the investor's portfolio. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

Long positions may decline as short positions rise, thereby accelerating potential losses to the investor.

13

2009 OUTLOOK

Bull Case The financial panic that began in September 2008 dissipates at the very start of 2009, and financial markets begin to normalize early in the year.

Scenario:

Economy experiences a quick rebound from the recession and a rebound in the credit markets as confidence is restored

Stocks rebound up to 50%; both earnings and valuations snap back as a mountain of cash is returned to the capital markets. The year-end S&P 500 close would be about 1365

The bond market returns high-single digits as income and price appreciation, from Corporate Bonds in particular, more than offsets Treasury weakness

Most alternative strategies provide positive results but trail the strong stock market in this bullish scenario

14

2009 OUTLOOK

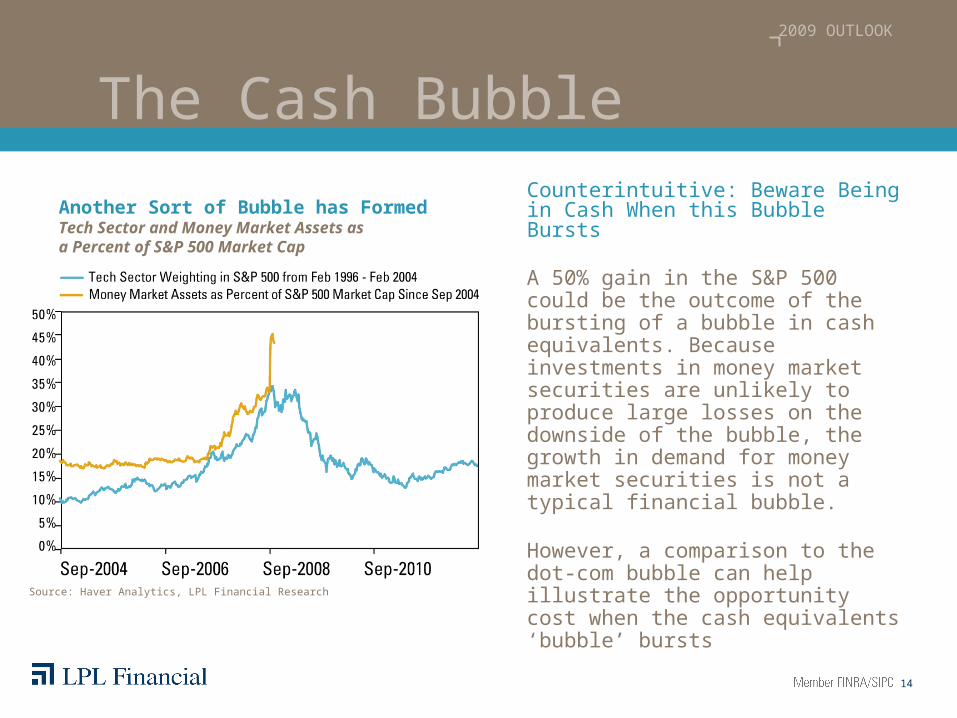

The Cash BubbleCounterintuitive: Beware Being in Cash When this Bubble Bursts

A 50% gain in the S&P 500 could be the outcome of the bursting of a bubble in cash equivalents. Because investments in money market securities are unlikely to produce large losses on the downside of the bubble, the growth in demand for money market securities is not a typical financial bubble.

However, a comparison to the dot-com bubble can help illustrate the opportunity cost when the cash equivalents ‘bubble’ bursts

Another Sort of Bubble has FormedTech Sector and Money Market Assets as a Percent of S&P 500 Market Cap

Source: Haver Analytics, LPL Financial Research

15

2009 OUTLOOK

Bull Case: What Investors Can Do

Overweight stocks and underweight high quality bonds

Overweight the most cyclical stocks in the Financials and Consumer Discretionary sectors along with the high beta Information Technology sector, while underweighting the defensive Utilities and Consumer Staples sectors

Domestic equity asset class, Small Cap Value, tends to perform the best as the credit markets and economy rebound from recession

In the fixed income, underweight Treasuries and overweight High Yield Bonds, investment grade Corporate Bonds and Preferred Stocks

Reduce the overall portfolio allocation to alternative asset classes

Small Cap stocks maybe subject to higher degree of risk than more established companies' securities. The illiquidity of the Small Cap market may adversely affect the value of these investments.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and are subject to availability and change in price.

16

2009 OUTLOOK

Great Depression II?

Why it is Highly Unlikely

The Great Depression came about because of serious economic and monetary policy errors that compounded what was already a serious recession. Actually, according to the National Bureau of Economic Research (NBER), the official date setter of U.S. recessions, there were two major back- to- back recessions in the 1930s, with a significant recovery in the middle. The economy and regulatory environment of the 1930s are a far cry from today’s, but can a great

depression occur again? We believe it cannot.

17

2009 OUTLOOK

Great Depression II - Policy

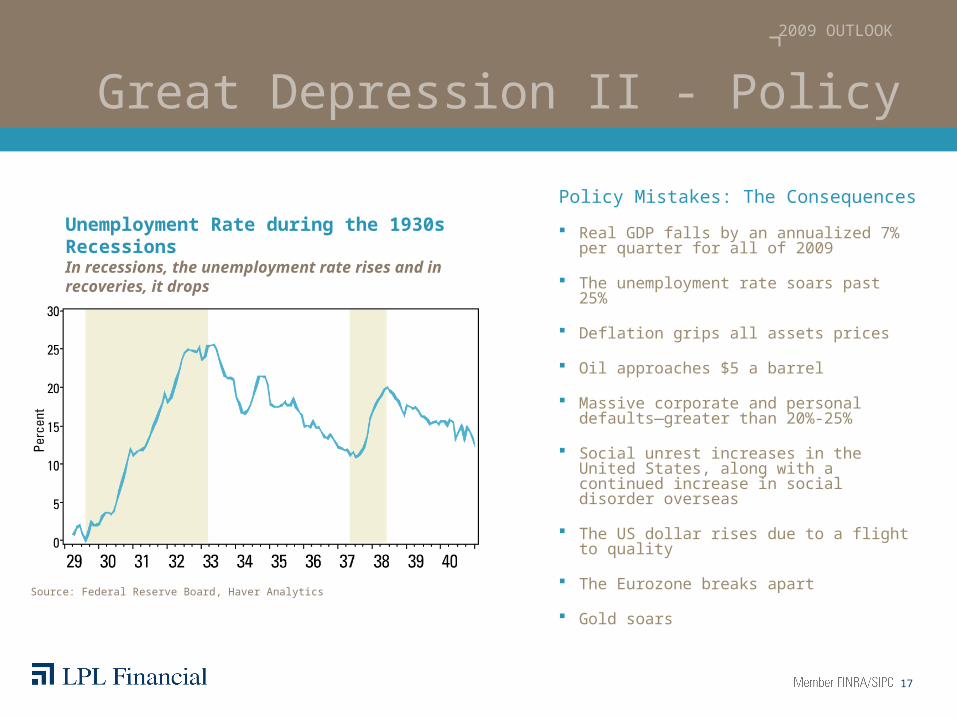

Unemployment Rate during the 1930s RecessionsIn recessions, the unemployment rate rises and in recoveries, it drops

Source: Federal Reserve Board, Haver Analytics

Policy Mistakes: The Consequences

Real GDP falls by an annualized 7% per quarter for all of 2009

The unemployment rate soars past 25%

Deflation grips all assets prices

Oil approaches $5 a barrel

Massive corporate and personal defaults—greater than 20%-25%

Social unrest increases in the United States, along with a continued increase in social disorder overseas

The US dollar rises due to a flight to quality

The Eurozone breaks apart

Gold soars

18

2009 OUTLOOK

Great Depression II – Highly Unlikely

The Fed reversing course and increasing rates over the course of 2009

The Fed raising bank reserve requirements

The Fed abruptly discontinuing the reflation program that it has already begun

A wave of global protectionism

The elimination of the TARP and related housing and bank rescue measures

Not Repeating the 1930s

In order to enter a depression like the 1930s, huge policy mistakes would have to be made. We do not think these mistakes will occur, but want to outline what they might be and how they would impact the economy and markets. Policy mistakes would include:

19

2009 OUTLOOK

The Impact of Washington

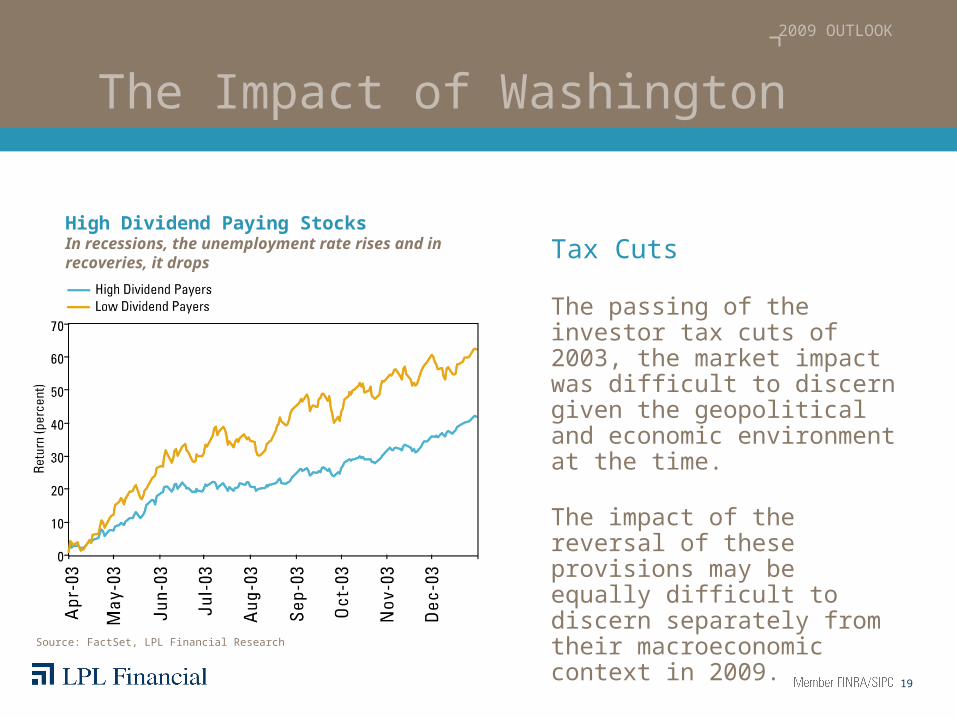

Tax Cuts

The passing of the investor tax cuts of 2003, the market impact was difficult to discern given the geopolitical and economic environment at the time.

The impact of the reversal of these provisions may be equally difficult to discern separately from their macroeconomic context in 2009.

High Dividend Paying Stocks In recessions, the unemployment rate rises and in recoveries, it drops

Source: FactSet, LPL Financial Research

20

2009 OUTLOOK

The Impact of Washington

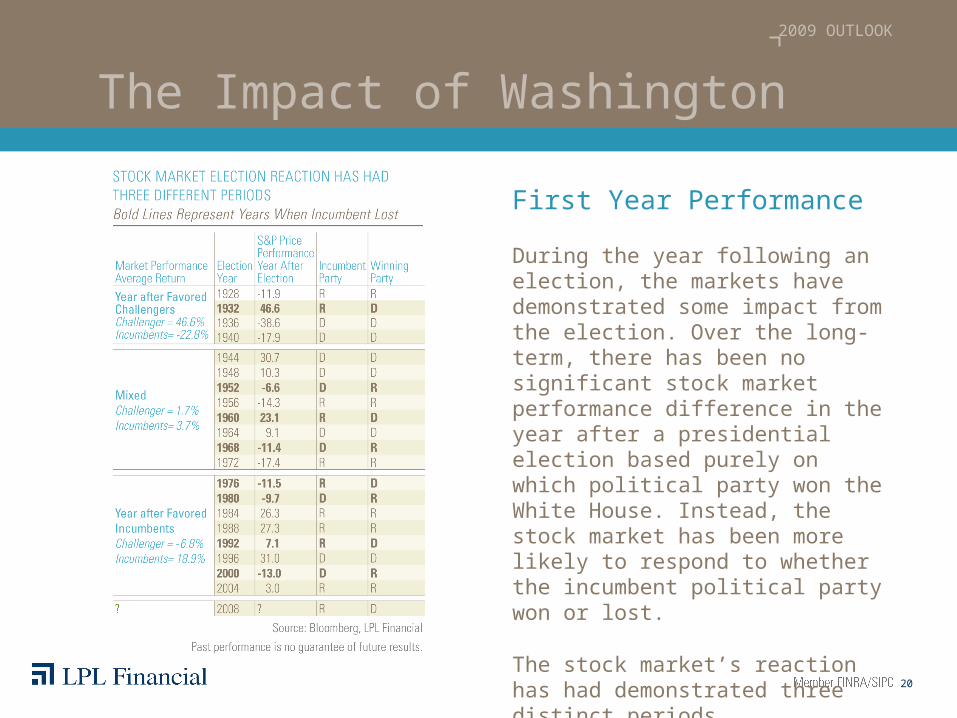

First Year Performance

During the year following an election, the markets have demonstrated some impact from the election. Over the long-term, there has been no significant stock market performance difference in the year after a presidential election based purely on which political party won the White House. Instead, the stock market has been more likely to respond to whether the incumbent political party won or lost.

The stock market’s reaction has had demonstrated three distinct periods.

21

2009 OUTLOOK

Important DisclosuresThe opinions voiced in this material are for general information only and are not intended to provide or be construed as providing specific investment advice or recommendations for any individual. To determine which investments may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and are subject to availability and change in price.

Stock investing involves risk including loss of principal.

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors.

Small cap stocks maybe subject to higher degree of risk than more established companies’ securities. The illiquidity of the small-cap market may adversely affect the value of these investments.

High yield/junk bonds are not investment grade securities, involve substantial risks and generally should be part of the diversified portfolio of sophisticated investors.

Municipal bonds are subject availability and change in price. Subject to market and interest rate risk is sold prior to maturity. Bond values will decline as interest rate rise. Interest income may be subject to the alternative tax. Federally tax-free but other state and local taxed may apply.

Government bonds and Treasury Bills are guaranteed by the US government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value.

Investing in alternative investments may not be suitable for all investors and involve special risks such as risk associated with leveraging the investment, potential adverse market forces, regulatory changes, potentially illiquidity. There is no assurance that the investment objective will be attained.

Investing in real estate/REITs involves special risks such as potential illiquidity and may not be suitable for all investors. There is no assurance that the investment objectives of this program will be attained.

Investing in mutual funds involve risk, including possible loss of principal. Investments in specialized industry sectors have additional risks, which are outlines in the prospectus.

The market value of corporate bonds will fluctuate, and if the bond is sold prior to maturity, the investor’s yield may differ from the advertised yield.

An investment in a money fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Although the Fed seeks to preserve the value of your investments at $1.00 per share, it is possible to lose money investing in the Fund.

The Barclays Aggregate Bond Index is composed of securities from the Barclays Government/Credit Bond Index, Mortgage-Backed Securities Index and Asset-Backed Securities Index

The Standard & Poor’s 500 Stock Index (S&P 500) is an unmanaged index generally representative of the U.S. Stock Market, without regard to company size.

Covered Call mutual fund strategies typically hold a long portfolio of stocks and then sell covered calls. Some covered call strategies then buy puts to further protect against downside risk. The net result is a portfolio that is correlated to the broader markets, but with significantly less volatility and increased risk due to the use of derivatives.

Global Macro funds use fundamental inputs (focused on broad global economic themes) in their models as well as technical (or price related) inputs. Global Macro funds may also be less systematic than the typical managed futures fund. Historically, the benefit of global macro has been solid long-term returns with very low correlation to equities and fixed income securities.

22

2009 OUTLOOK

Important DisclosuresLong/short funds focus on managers who go long and hedge against the market through options or shorting equity securities with the goal of outperforming the market while limiting volatility. These funds tend to have a higher correlation to equities than other alternative strategies and, therefore, are most appropriate for more aggressive portfolios.

Consumer Discretionary: Companies that tend to be the most sensitive to economic cycles. Its manufacturing segment includes automotive, household durable goods, textiles and apparel, and leisure equipment. The service segment includes hotels, restaurants and other leisure facilities, media production and services, consumer retailing and services and education services.

Consumer Staples: Companies whose businesses are less sensitive to economic cycles. It includes manufacturers and distributors of food, beverages and tobacco, and producers of non-durable household goods and personal products. It also includes food and drug retailing companies.

Energy: Companies whose businesses are dominated by either of the following activities: The construction or provision of oil rigs, drilling equipment and other energy-related service and equipment, including seismic data collection. The exploration, production, marketing, refining and/or transportation of oil and gas products, coal and consumable fuels.

Financials: Companies involved in activities such as banking, consumer finance, investment banking and brokerage, asset management, insurance and investment, and real estate, including REITs.

Healthcare: Companies in two main industry groups: Healthcare equipment and supplies or companies that provide health care-related services, including distributors of health care products, providers of basic healthcare services, and owners and operators of healthcare facilities and organizations. Companies primarily involved in the research, development, production and marketing of pharmaceuticals and biotechnology products.

Industrials: Companies whose businesses: Manufacture and distribute capital goods, including aerospace and defense, construction, engineering and building products, electrical equipment and industrial machinery. Provide commercial services and supplies, including printing, employment, environmental and office services. Provide transportation services, including airlines, couriers, marine, road and rail, and transportation infrastructure.

Technology Software & Services, including companies that primarily develop software in various fields such as the Internet, applications, systems and/or database management and companies that provide information technology consulting and services. Technology Hardware & Equipment, including manufacturers and distributors of communications equipment, computers and peripherals, electronic equipment and related instruments, and semiconductor equipment and products.

Materials: Companies that are engaged in a wide range of commodity-related manufacturing. Included in this sector are companies that manufacture chemicals, construction materials, glass, paper, forest products and related packaging products, metals, minerals and mining companies, including producers of steel.

Telecommunications Services: Companies that provide communications services primarily through a fixed line, cellular, wireless, high bandwidth and/or fiber-optic cable network.

Utilities: Companies considered electric, gas or water utilities, or companies that operate as independent producers and/or distributors of power.

This research material has been prepared by LPL Financial.

The LPL Financial family of affiliated companies includes LPL Financial, UVEST Financial Services Group, Inc., Mutual Service Corporation, Waterstone Financial Group, Inc., and Associated Securities Corp., each of which is a member of FINRA/SIPC.

Not FDIC/NCUA Insured | Not Bank/Credit Union Guaranteed | May Lose Value | Not Guaranteed by any Government Agency | Not a Bank/Credit Union Deposit

Tracking #510470 (Exp. 1/11) |