Embed Size (px)

Citation preview

LOTUS CAPITAL HALAL INVESTMENT FUND ANNUAL REPORT AND ACCOUNTS, 2012

The Lotus Halal Investment Fund is managed by:Lotus Capital Limited

1THE LOTUS HALAL INVESTMENT FUND IS MANAGED BY LOTUS CAPITAL LIMITED

LOTUS CAPITAL HALAL INVESTMENT FUND

Managed by

LOTUS CAPITAL LIMITED

FINANCIAL STATEMENTS

for the year ended

31st DECEMBER, 2012

Horwath Dafinone, Chartered Accountants, Ceddi Towers, 16 Wharf Road, Apapa,P. O. Box 2151, Marina, Lagos

2 THE LOTUS HALAL INVESTMENT FUND IS MANAGED BY LOTUS CAPITAL LIMITED

CONTENTS Pages

1. Notice of the Annual General Meeting 3

2. Corporate information 6

3. Report of the Trustees 7

4. Report of the Fund Manager 10

5. Report of the Shari’ah Supervisory Board 13

6. Report of the Auditors 14

7. Statement of Financial Position 16

8. Statement of Comprehensive Income 17

9. Statement of Changes in Equity 18

10. Statement of Cash Flows 19

11. Notes to the Financial Statements 20

12. Proxy Form 57

13. Admission Card 59

14. Electronic Delivery Mandate Form 60

3THE LOTUS HALAL INVESTMENT FUND IS MANAGED BY LOTUS CAPITAL LIMITED

NOTICE OF ANNUAL GENERAL MEETINGNOTICE IS HEREBY GIVEN that the 4th Annual General Meeting of Lotus Capital Halal Investment Fund will be held at The Daisy Management Centre Ltd, 5, Babatunde Jose Street ( former Festival Road), Victoria Island, Lagos on Thursday the 24th day of October, 2013 at 9:00am to transact the following business:

ORDINARY BUSINESS

1. To receive the Audited Financial Statements for the year ended 31st December, 2012 and the Reports of the Trustees, Manager and Auditors.

2. To consider and if thought fit authorize the Manager to fix the remuneration payable to the Auditors for the ensuing year.

SPECIAL BUSINESS

To consider and if thought fit, pass the following resolutions as special resolutions:

1. That the Trust Deed dated 31st January, 2008 (“Trust Deed”) between Lotus Capital Limited (as Manager) and First Trustees Nigeria Limited (as Trustee), as amended by the First Supplemental Trust Deed dated August 25, 2010 and the Second Supplemental Trust Deed dated November 2, 2011 be supplemented and amended in the manner described below and that a third supplemental deed to the Trust Deed be prepared and executed to record these amendments.

I. Amendments to Clause 1

Amendment to Clause 1.1

The definition of “asset backed investments” as contained in section 8.4.2 of the Trust Deed including, but not limited to, Musharaka, Mudaraba, Murabaha, Ijara, Istisna and Wakala are now expressly defined in clause 1.1.

Insertion of Proviso to clause 1.1

NOTWITHSTANDING ANYTHING CONTAINED HEREIN, the Fund Manager shall not be restricted from utilizing any other Shari’ah compliant structure by virtue of the fact that it is not expressly defined above.

Amendment to Clause 1.1.2

Clause 1.1.2 of the Trust Deed shall be deleted and replaced with the following:

“Authorized Investment” means any investment selected by the Manager from time to time which is Shariah compliant and authorized by the Fund’s Trust Deed as well as any applicable law in force whether or not listed, quoted or dealt in on any securities exchange.

II. Insertion of a new Clause 8.4.5

A new clause 8.4.5 of the Trust Deed is hereby included as follows:

“The asset allocation policy of the Fund shall be invested at the discretion of the Manager in investments which are Shari’ah Compliant and authorized for purchase in the proportions specified below:

4 THE LOTUS HALAL INVESTMENT FUND IS MANAGED BY LOTUS CAPITAL LIMITED

ASSETCLASS RANGE

8.4.5 Unlisted Securities - 0% - 30%”

III. Amendment to Clause 9

Clause 9.1 of the Trust Deed shall be deleted and replaced with the following: -

“Subject to clauses 8.4 and 13, the Fund shall be invested in specially screened securities and asset-backed investments including but not limited to equity instruments (listed and unlisted) and debt instruments approved by the Commission and which are Shari’ah Compliant. Where the Fund invests in unlisted securities, the Manager shall take full responsibility for such investment. The Fund Manager shall also submit a valuation of the portfolio of unlisted securities quarterly to the Commission and the Trustees".

IV. Amendment to Clause 13 (1)

Clause 13.1 of the Trust Deed which was amended by Clause 2.1.4 of the First Supplemental Trust Deed is hereby reinstated while the amendment in Clause 2.1.4 of the First Supplemental Trust Deed is hereby deleted. Clause 13.1 shall now read as follows:

”where such investment would result in either the value or the aggregate of the values of any investment in any one company or body or in any one security exceeding one-tenth of the value of the Fund”

V. Amendment to Clause 31

Clauses 31.1 of the Trust Deed shall be deleted and replaced with the following:-

“It shall be the duty of the Registrar to prepare all Certificates and to prepare and pay all cheques, warrants and electronic dividends.”

VI. Amendment to Clause 39 (1)

Clause 39.1 of the Trust Deed shall be deleted completely and clause 39.2 renumbered accordingly.

VII. Amendment to Clause 42

Clause 42.1 of the Trust Deed shall be deleted and replaced with the following:-

"Any monies payable by the Trustee or by the Manager to a Holder or former Holder under the provisions of these presents may be paid by crossed-cheque, warrant or electronic payment (via wire transfer or any other means) made payable to the registered address or bank account of such Holder. Every cheque, warrant or electronic payment shall be sent at the risk of the Holder or former Holder and payment of any such cheque, warrant or electronic payment shall be satisfaction of the monies payable thereby and shall be a good discharge of the Trustee and Manager. Where an authority in writing, to pay a specified banker, agent or nominee, shall have been received by the Trustee or Manager from the Holder or former Holder in such form and signed or sealed in such manner as the Trustee or Manager shall direct, the Trustee, Manager or Registrar shall pay the moneys payable to the Holder as the case may be in the same manner and with the same effect as hereinbefore provided as if such banker, agent or nominee were the Holder".

Clause 42.2 of the Trust Deed shall be deleted and replaced with the following:-

“Without prejudice to the application of sub-clause 42.1 above, a receipt signed or purported to be signed by the Holder or former Holder for any moneys payable in respect of Units held or formerly held by him or an automatic delivery receipt or electronic payment notification by a third-party/vendor shall be a good discharge to the Trustee and Manager.”

5THE LOTUS HALAL INVESTMENT FUND IS MANAGED BY LOTUS CAPITAL LIMITED

VIII. Amendments to the First Schedule

Clause 1 of Schedule 1 (Rules for Meetings of Holders) of the Trust Deed is hereby deleted.

Clause 14(b) of Schedule 1 shall be deleted and replaced with the following:-

“The quorum for a Meeting of the Fund shall be formed by five (5) Unit Holders holding not less than 25% of the entire outstanding units of the Fund present in person or by proxy.”

NOTES:

Proxy

1. Only Unitholders are entitled to attend the meeting. A Unitholder entitled to attend and vote may appoint a proxy to attend and vote instead of him/her/itself. A proxy need not be a Unitholder of the Fund.

2. To be valid, the proxy form attached to this Notice must be stamped to the value of N50 as duty thereon and should be deposited at the office of The Registrar, Unity Registrars at Unity Bank Building, 94, Agege Motor Road, Idi Oro, Lagos not later than 48 (Forty – eight) hours before the time fixed for the meeting.

Dated this 30th day of September, 2013

BY ORDER OF THE MANAGER

LOTUS CAPITAL LIMITED

MAS’UD BALOGUN

COMPANY SECRETARY

IB UDI STREET

OSBORNE FORESHORE ESTATE

IKOYI, LAGOS.

6 THE LOTUS HALAL INVESTMENT FUND IS MANAGED BY LOTUS CAPITAL LIMITED

Corporate information

Fund Manager Lotus Capital Limited 1b, Udi Street Osborne Foreshore Estate Osborne Road Lagos

Directors of the Fund Manager Mr. Fola Adeola Mrs. Hajara Adeola Mrs. Lateefah Okunnu Mrs. Amina Oyagbola Mr. Nuruddeen Lemu

Registered office 1b, Udi Street(Fund Manager) Osborne Foreshore Estate Osborne Road Lagos

Trustees to the Fund First Trustees Nigeria Limited AG Leventis Building 2nd Floor, 42/43 Marina Lagos

Auditors to the Fund Horwath Dafinone Chartered Accountants

Custodian to the Fund Citibank Nigeria Limited

Registrar to the Fund Unity Registrars Limited Unity Bank Building

94, Agege Motor Road Idi Oro Lagos

7THE LOTUS HALAL INVESTMENT FUND IS MANAGED BY LOTUS CAPITAL LIMITED

Report of the Trustees

The Trustees present their report on the affairs of the Lotus Capital Halal Investment Fund, together with the audited financial statements for the year ended 31st December, 2012.

Principal Activity: The principal activity of the Lotus Capital Halal Investment Fund is the pooling of funds from individual members of the public and companies and the investment of such funds in equities listed on the Nigerian Stock Exchange, Asset Backed Investments and other sharia-compliant investments.

During the year under review, the Fund was administered in accordance with the Trustees Investment Act, CAP T22 LFN, 2004, the Investments and Securities Act, 2007, the provisions of the Trust Deed and any supplemental thereto, together with the rules and regulations set out by the regulatory bodies established pursuant to the legislation referred to within this paragraph (“Applicable Regulations”), taking into cognisance prevailing market conditions as well as preserving of (and minimising possible losses to) Unitholders’ funds. The Fund was also administered in accordance with Shari’ah Rules and Principles.

Results: The results for the year are set out on Pages 17.

Distribution: While the Trust Deed constituting the Fund empowers the Fund to distribute any part of its income to its members, such distribution has to be approved by the Trustee on the recommendation of the Fund Manager.

Directors: The directors of the Fund Manager who served on the board of the Fund Manager during the period under review and up to the date of approving these financial statements were:

Mr. Fola Adeola (Chairman)Mrs. Hajara Adeola (Managing Director/ Chief Executive Officer)Mrs. Lateefah Okunnu Mrs. Amina Oyagbola Mr. Nuruddeen Lemu

Directors’ and related The Directors of Lotus Capital Limited who held direct andparties interest in the indirect beneficial interest in the units of the Fund as at 31stunits of the Fund: December, 2012 are: Units held as at 31st December, 2012

Mr. Fola Adeola 5,000,000Mrs. Hajara Adeola 3,916,074Mr. Nuruddeen Lemu 3,274,756Mrs. Lateefah Okunnu 10,459,227Mrs. Amina Oyagbola 339,987

None of the directors of First Trustees Nigeria Limited has any direct or indirect beneficial interest in the units of the Fund.

8 THE LOTUS HALAL INVESTMENT FUND IS MANAGED BY LOTUS CAPITAL LIMITED

Report of the Trustees (continued)

Responsibilities of the The Investments and Securities Act, 2007 requires the Fund ManagerFund Manager: to keep proper books of account and prepare annual financial statements

which give a true and fair view of the state of affairs of the unit trust scheme during the period covered by the financial statements.In our opinion, the Fund Manager has in preparing the financial statements:

• selected suitable accounting policies and applied them consistently;

• made judgments and estimates that were reasonable and prudent;

• ensured that the applicable accounting standards have been followed, and in the case of any material departure, that it was fully disclosed and explained in the financial statements; and

• prepared the financial statements on a going concern basis; since it was appropriate to assume that the Fund shall continue to exist.

The Fund Manager was responsible for keeping proper accounting records, which disclose with reasonable accuracy, at any point in time, the financial position of the Fund, and enable the Fund Manager to ensure that the financial statements comply with the Applicable Regulations.

The Fund Manager is also responsible for maintaining adequate financial resources to meet its commitments and to manage the risks to which the Fund is exposed.

Responsibilities of the The responsibilities of the Trustee as provided by the Securities andTrustee: Exchange Commission’s Rules and Regulations made pursuant to the

Investments and Securities Act, 2007 are as stated below:• Monitoring the activities of the Fund Manager and the custodian on

behalf of and in the interest of the Unit Holders;

• Ensuring that the Custodian takes into custody all of the scheme’s assets and holds it in trust for the holders in accordance with the Trust Deed and the Custodial Agreement;

• Monitoring the register of Unitholders or contributors;

• Ascertaining the Fund Manager’s compliance with the Applicable Regulations;

• Ascertaining that the monthly and other periodic returns/reports relating to the Fund are sent by the Fund Manager to the Commission;

• Exercising any right of voting conferred on it as the registered holder of any investment and/or forward to the fund manager within a

9THE LOTUS HALAL INVESTMENT FUND IS MANAGED BY LOTUS CAPITAL LIMITED

Report of the Trustees (continued)reasonable time all notices of meetings, reports, circulars, proxy solicitations and any other document of a like nature for necessary action;

• Ensuring that fees and expenses of the fund is within the prescribed limits; and

• Acting at all times in the interest and for the benefit of unit holders of the scheme.

Administration of the Fund: During the year under review, the Fund was administered in accordance with the Applicable Regulations, taking into cognisance prevailing market conditions as well as preserving of (and minimising possible losses to) Unitholders’ funds.

Charitable Donations: The Fund did not make any charitable donations during the period. (2011: nil)

Auditors: Messrs Horwath Dafinone, Chartered Accountants, having indicated their willingness to continue in office, shall do so in accordance with Section 169(1) of the Investments and Securities Act, 2007.

By Order of the Trustees

Adekunle Awojobi,

Ag. Managing Director

First Trustees Nigeria Limited

Lagos, Nigeria

9th July, 2013

10 THE LOTUS HALAL INVESTMENT FUND IS MANAGED BY LOTUS CAPITAL LIMITED

Report of the Fund Manager

Dear Investor,

This report provides an overview of the performance of the Lotus Capital Halal Investment Fund from January 1, 2012 to the financial year ended December 31, 2012.

INVESTMENT OBJECTIVESThe primary objective of the Fund is to optimize total returns of investors (i.e. dividend and investment profits as well as capital appreciation on assets held) by seeking high quality investments whilst adhering to the strictest code of ethics in line with our Islamic finance investment philosophy.

MACROECONOMIC REVIEWComing on the heels of a muted global economic landscape in 2011, economic indicators reflect that 2012 was more positive despite a rollercoaster performance. On the local scene, data from the National Bureau of Statistics (“NBS”) showed that the economy grew respectively by 6.17%, 6.28% and 6.48% in the first, second and third quarter as against 7.13%, 7.61 and 7.37% in the corresponding quarters of 2011. Overall, Gross Domestic Product (“GDP”) growth rate of 6.77% for 2012 was forecast compared to an earlier forecast of 6.5%. Furthermore, the economy showed impressive resilience against a backdrop of economic challenges witnessed during the year such as the uncertain international economic environment and internal economic shocks, including economic losses instigated from the January nati Nigeria’s foreign exchange reserves, the establishment of a Sovereign Wealth Fund as well as the productive reforms in the banking and power sector.A number of noteworthy events occurred during the year that had an impact on the macro economy: -The Federal Government launched a Sovereign Wealth Fund (“SWF”). The SWF is expected to improve fiscal consolidation, safeguard oil revenues and cushion the economy against external shocks.

• Driven by improved proceeds from crude oil and gas sales, crude oil related taxes, as well as increased inflow from foreign direct investment; Nigeria’s foreign exchange reserves grew by 34.22% from USD32.9 billion at the start of the year to USD44.17 billion in December, 2012.

• The first Shari’ah compliant equity Islamic index was introduced into the Nigerian capital market. The index, known as the NSE-Lotus Islamic Index (NSE LII), was created via a partnership between Lotus Capital and the Nigerian Stock Exchange (“NSE”). This Index is expected to track the performance of 15 selected ethical stocks listed on the floor of the Exchange. The NSE-Lotus Islamic Index was the second best performing Index on the Nigerian Stock Exchange with a 44.21% return for 2012.

• The Federal Government granted a forbearance package of about N22.6 billion to 84 stockbrokers, to relieve them of the effects of the margin loans incurred since 2008. However, the relief came with a number of sanctions to discourage excessive borrowing by capital market operators in the future.

11THE LOTUS HALAL INVESTMENT FUND IS MANAGED BY LOTUS CAPITAL LIMITED

Report of the Fund Manager (continued)

• In the period under review, 10 capital market operators commenced market making activities for 36 stocks listed on the Nigerian Stock Exchange. This is expected to improve liquidity and depth in the capital market by providing a two-way quote for each of the selected stocks.

• 3 Federal Government of Nigeria (FGN) Bonds were included in the JP Morgan Government Bond Index-Emerging Markets and this resulted in the decline of yields in the fixed income market towards the end of the year.

NIGERIAN CAPITAL MARKET REVIEWFollowing a weak performance during the first quarter of 2012, which yielded a negative return of 0.38%, the market witnessed a rebound in the second quarter returning 4.59%. The uptrend was buoyed by the impressive score cards released by listed companies for the 2011 financial year end. This brought about improved confidence as investors took up equity positions.The rally was sustained in the third quarter as the equities market returned a significant 20.43%. The All Share Index, which measures the general performance of the entire equities market in the third quarter opened at 21,599.57 points and closed at 26,011.63 points, breaking through the traditional 25,000 and 26,000 investor resistance levels. The market sustained its performance during the fourth quarter as it rallied 7.95% to close year 2012 at 28,078.80 points. Furthermore, market capitalization gained N692.168 billion to close the last quarter at N8.28 trillion, representing an 8.36% return.

Generally, 2012 was a good year for equity investors. The Nigerian Stock Exchange ended the year with a return of 35.45%; the highest the market has witnessed since the stock market crisis of 2008 and 2009. This impressive performance was largely supported by the strong quarterly results released by some companies, relatively softening yields in the fixed income market, a stable foreign exchange market, improved investor confidence in the equities market as well as the initiatives of various regulatory bodies, particularly the NSE and the CBN.

HALAL FUND ASSET ALLOCATIONAs stipulated in the Trust deed, the Fund invested in equities, asset-backed investments and cash, in the period under review. Over the course of the year, the Fund Manager adequately managed liquidity and re-balanced the portfolio. As at December 31, 2012, the Fund was 47% (2011:41%) invested in equities, 52% (2011:54%) in asset-backed investments and 1% (2011:5%) in cash.

12 THE LOTUS HALAL INVESTMENT FUND IS MANAGED BY LOTUS CAPITAL LIMITED

Report of the Fund Manager (continued)

Cash Available 1%

Securities47%

Asset Backed Investments

52%

ASSET ALLOCATION AS AT 31 DECEMBER 2012

Cash Available 5%

Securities41%

Asset Backed Investments

54%

ASSET ALLOCATION AS AT DECEMBER 2011

HALAL FUND PERFORMANCE The Fund opened the year at N0.73K and closed at N0.78K, which translates into an annual return of 6.85%. As a balanced fund, maintaining stable returns over a period of time and being less volatile than the market is an essential feature of the Halal Fund. This means that when the market goes down, the fund will not fall by as much as the market. Likewise, when the market goes up, the fund will not rise by as much. Nevertheless, the equity portion of the Fund performed considerably well by returning 18.6% in the period. The Fund Manager adopted a robust credit management structure to improve the quality of asset backed transactions. These strategies were also followed through providing a good buffer to the equities portfolio. The fund valuation remained impaired by provisions made on certain asset backed investments, in line with prudential guidelines. Nevertheless, the Fund Manager have taken due actions to facilitate recovery of such investments and expect that the provisions made, will be written back in the immediate term.

STRATEGY AND OUTLOOK FOR 2013While we anticipate that the Nigerian economy would gather momentum and exceed the growth witnessed in 2012, this is hinged on stable crude oil prices as well as growth in non-oil sectors particularly agriculture, telecommunications, wholesale/retail trade, and services. According to the International Monetary Fund (IMF), the Nigerian economy is projected to grow by 6.6% in 2013, given the prevailing macroeconomic indications. The National budget for 2013 has been passed and the bulk of the capital expenditure allocation is expected to fund the power, healthcare, works, security and the education sectors among others. Nevertheless, successful implementation remains a key issue as witnessed in the past. In the fixed income market, the recent upgrade in Nigeria’s credit rating, inclusion of Nigerian Bonds in the JP Morgan and Barclays Bond Indices would temper yields. Consequently, as confidence is renewed in the equities market, we believe the market will continue to witness strong growth though at a lower pace than in 2012. This expected growth is premised on expected good financial performance of quoted companies and lower anticipated yields in the fixed income market. In the coming year, the Fund Manager is poised to continuously re-balance the portfolio by overweighting investments in high income, value based stocks with strong fundamentals through a top-down approach. Furthermore key focus for the asset backed investment would be to seek high quality financial contracts which would yield impressive fixed returns and diversify portfolio risk in the immediate term. We wish you a prosperous 2013.

13THE LOTUS HALAL INVESTMENT FUND IS MANAGED BY LOTUS CAPITAL LIMITED

Report of the Shari’ah Supervisory Board

Shari’ah Report & Shari’ah Supervisory BoardLotus Capital Halal Investment Fund

Shari’ah Report for the fiscal year ending December 31, 2012In the name of Allah, the Most Beneficent, Most Merciful. Alhamdu Lillahi Rabbi al Alamin, wa al Salatu wa al Salamu ‘ala SayyidinaMuhammad, wa ala Aalihi wa Sahbihi Ajma’inTo the unitholders of the Lotus Capital Halal Investment Fund (“the Halal Fund”)Assalamu Alaikum Wa Rahmat Allah Wa Barakatuh

We have reviewed the principles and the form-contracts relating to the transactions and applications utilized by Lotus Capital Limited (“the Fund Manager”) during the year under review. We have also received assurance from the Lotus Capital Management that all procedures of investment and Shari’ah compliant contract templates only have been used in all investment of the Halal Fund as approved and instructed by us the Shari’ah Supervisory Board. This allows us to form an opinion as to whether the Fund Manager has complied with Shari‘ah Rules and Principles and with the rulings set by the Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI).

The Fund Manager is responsible for ensuring that the company conducts the business of the Halal Fund in accordance with Islamic Rules and Principles. It is the Shari‘ah Supervisory Board‘s responsibility to form an independent opinion on Shari‘ah compliance based on its review of the operations and activities of the Fund. The Fund Manager has assumed the responsibility to pay the total non -permissible income to charity in accordance with the guidance of the Shari‘ah Supervisory Board. The company has not been given the authority to pay Zakaat on behalf of unitholders or depositors. This is the responsibility of the shareholders and depositors themselves.

We report that the Shari‘ah Supervisory Board (SSB) conducted the review by examining the form contracts and formal procedures for each type of transaction utilized by the Fund Manager. The SSB was assured by the Fund Manager that all transactions have specifically been conducted and concluded by using these form contracts with no additional or other conditions. Accordingly, in our opinion the contracts, transactions and dealings entered into by the Fund Manager during the period under review are generally in compliance with Shari‘ah Rules and Principles. However, the Shari’ah Supervisory Board will continue to work with the Fund Manager to perfect their operations from a Shari’ah standpoint.

We beg Almighty Allah to grant us all wisdom to understand His religion and follow its teaching and to bestow on us success in this worldly life and in the life after.

Wassalamu Alaikum Wa Rahmat Allah Wa Barakatuh.

_________________________________ ___________________________________

Prof. Dr. Monzer Kahf Professor Muhammad Lawal Bashar Chairman Shari’ah Board Member Shari’ah Board Lotus Capital Limited Lotus Capital Limited

REPORT OF THE INDEPENDENT AUDITORS TO THE UNIT HOLDERS OF LOTUS CAPITAL HALAL INVESTMENT FUND

We have audited the financial statements of Lotus Capital Halal Investment Fund which comprise, the statements of financial position as at 31st December 2012, the statements of comprehensive income, statement of changes in equity attributable to holders of the redeemable units, statements of cash flows for the year then ended, and notes comprising the principal accounting policies, other explanatory notes. These financial statements are set out on pages 16 to 56 and have been prepared using the accounting policies set out on page 20 to 44.

Fund Manager and Trustees’ responsibilities for the financial statements

The Fund Manager is responsible for the preparation and fair presentation of the financial statements in accordance with the International Financial Reporting Standards and the requirements of the Investment and securities Act, 2007, whilst the Trustee is responsible for ascertaining compliance with the provision of the Trust Deed and other relevant laws. The responsibility of the Fund Manager includes the designing, implementing and maintaining internal controls that are relevant to the preparation and fair presentation of the financial statements that are free from material misstatement, whether due to fraud or error as well as selecting and applying appropriate accounting policies and making accounting estimates that are reasonable in the circumstances.

Auditor’s responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with International Standards on Auditing and Nigerian Standards on Auditing issued by the Institute of Chartered Accountants of Nigeria. The standards require that we comply with ethical requirements and plan and perform the audit so as to obtain reasonable assurance as to whether the financial statements are free from material misstatement.

Basis of our opinion

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgement, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal controls relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements

14

15

16 THE LOTUS HALAL INVESTMENT FUND IS MANAGED BY LOTUS CAPITAL LIMITED

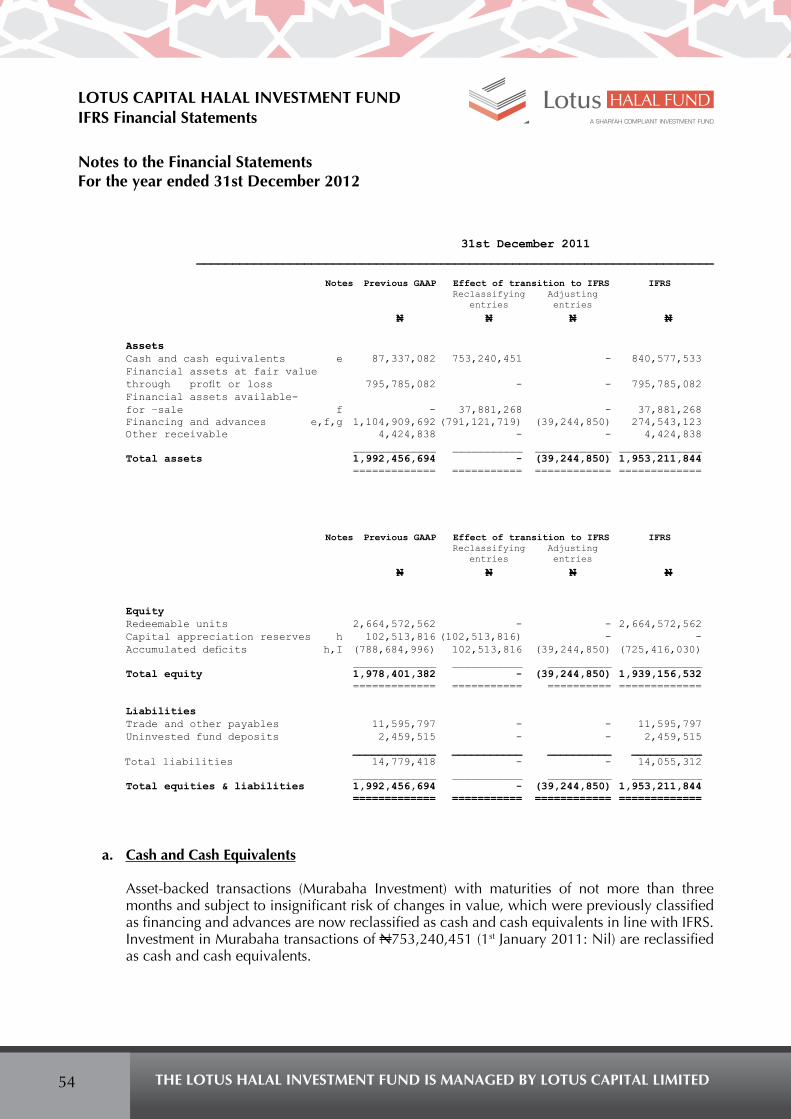

LOTUS CAPITAL HALAL INVESTMENT FUNDIFRS Financial Statements

Statement of Financial Positionfor the year ended 31st December, 2012 31 December 31 December 1 January Notes 2012 2011 2011

N N N Assets

Cash and cash equivalents 12 550,670,465 840,577,533 938,741,783 Financial assets at fair valuethrough profit or loss 13 903,068,093 795,785,082 930,201,210 Financial assets available-for-sale 14 5,000,000 37,881,268 37,938,831 Financing and advances 15 488,313,220 274,543,123 281,052,191 Other receivables 16 6,200,384 4,424,838 5,516,543 ______________ _____________ _____________

Total assets 1,953,252,162 1,953,211,844 2,193,450,558 ______________ _____________ _____________

Equity

Redeemable units 2,419,284,920 2,664,572,562 2,815,124,163Accumulated deficit (512,062,832) (725,416,030) (635,453,023) ______________ _____________ _____________ Total equity 1,907,222,088 1,939,156,532 2,179,671,140 _____________ _____________ _____________ Liabilities

Uninvested fund deposits 1,747,265 2,459,515 4,804,354 Trade and other payables 17 44,282,808 11,595,797 8,975,064 ______________ _____________ _____________

Total liabilities 46,030,073 14,055,312 13,779,418 ______________ _____________ _____________

Total equity & liabilities 1,953,252,161 1,953,211,844 2,193,450,558 ============== ============= =============

9th July, 2013

The statement of the principal accounting policies set out on pages 20 to 44 and the notes on pages 44 to 56 form an integral part of these financial statements.

17THE LOTUS HALAL INVESTMENT FUND IS MANAGED BY LOTUS CAPITAL LIMITED

LOTUS CAPITAL HALAL INVESTMENT FUNDIFRS Financial Statements

Statement of Comprehensive Incomefor the year ended 31st December, 2012

31 December 31 December Notes 2012 2011 N N

Income from financing and advances 7 124,679,055 110,051,678

Dividend income 40,727,216 40,087,063

Other income 36,000 880,628

___________ ___________

Total revenue 165,442,271 151,019,369

___________ ___________

Net impairment gain/(loss) on financial assets 8 24,151,748 (75,311,330)

Net gain/(loss) from financial assets at

fair value through profit or loss 9 107,283,011 (192,236,240)

Other operating expenses 10 (96,899,696) (10,683,056)

___________ ___________

Total operating expenses 34,535,063 (278,230,626)

___________ ___________

Profit/(loss) before tax 199,977,334 (127,211,257)

___________ _____________

Withholding tax expense 11 (3,935,222) (3,763,706)

Profit / loss for the year 196,042,112 (130,974,963)

=========== =============

The statement of the principal accounting policies set out on pages 20 to 44 and the notes on pages 44 to 56 form an integral part of these financial statements.

18 THE LOTUS HALAL INVESTMENT FUND IS MANAGED BY LOTUS CAPITAL LIMITED

LOTUS CAPITAL HALAL INVESTMENT FUNDIFRS Financial Statements

Statement of Changes in Equityas at 31st December, 2012

Redeemable Accumulated Total units deficit equity N N N

Balance at 1st January 2012 2,664,572,562 (725,416,030) 1,939,156,532

Total comprehensive income for the year: Profit or loss - 196,042,113 196,042,113 _____________ ___________ ____________

Transactions with unit holders, recognised directly in equity

Contributions, redemptions and distributions to unit holders:

Issue of redeemable units 5,107,609 5,107,609 Redemption of redeemable units (250,395,251) 49,361,799 (201,033,452) Fair value through equity (32,050,714) (32,050,714) _____________ ___________ ____________

Total transactions with unit holders (245,287,642) 17,311,085 (227,976,557) _____________ ___________ ____________

Balance at 31 December 2012 2,419,284,920 (512,062,832) 1,907,222,088 ============= =========== =============

Statement of changes in equity as at 31st December, 2011

Redeemable Accumulated Total units deficit equity N N N

Balance at 1st January 2011 2,815,124,163 (635,453,023) 2,179,671,140

Total comprehensive income for the year: Profit or loss - (130,974,963) (130,974,963) _____________ ___________ ____________

Transactions with unit holders, recognised directly in equity

Contributions, redemptions and distributions to unit holders:

Issue of redeemable units 123,181,492 - 123,181,492 Redemption of redeemable units (273,733,093) 52,059,114 (221,673,979) Fair value through equity - (11,047,158) (11,047,158) ______________ _____________ _____________

Total transactions with unit holders (150,551,601) 41,011,956 (109,539,645) ______________ _____________ _____________

Balance at 31 December 2011 2,664,572,562 (725,416,030) 1,939,156,532 ============== ============= =============

The statement of the principal accounting policies set out on pages 20 to 44 and the notes on pages 44 to 56 form an integral part of these financial statements.

19THE LOTUS HALAL INVESTMENT FUND IS MANAGED BY LOTUS CAPITAL LIMITED

LOTUS CAPITAL HALAL INVESTMENT FUNDIFRS Financial Statements

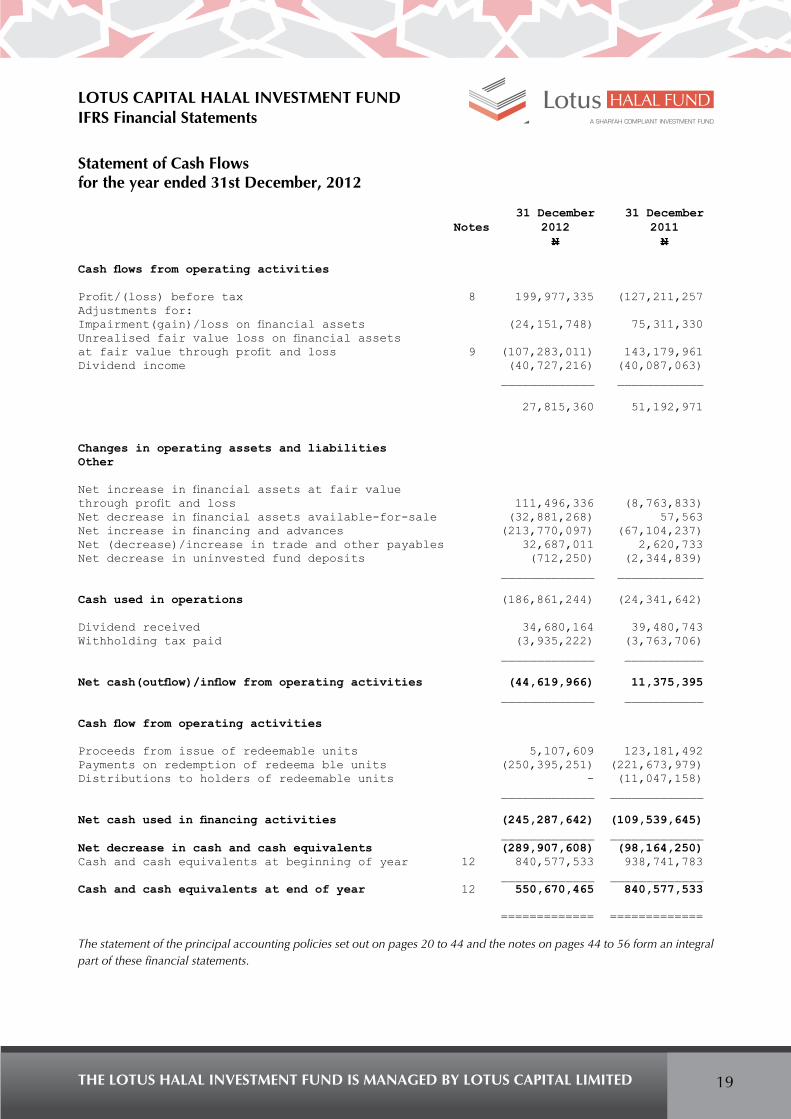

Statement of Cash Flows for the year ended 31st December, 2012

31 December 31 December Notes 2012 2011 N N

Cash flows from operating activities

Profit/(loss) before tax 8 199,977,335 (127,211,257Adjustments for:Impairment(gain)/loss on financial assets (24,151,748) 75,311,330Unrealised fair value loss on financial assetsat fair value through profit and loss 9 (107,283,011) 143,179,961Dividend income (40,727,216) (40,087,063) _____________ ____________

27,815,360 51,192,971

Changes in operating assets and liabilities Other

Net increase in financial assets at fair valuethrough profit and loss 111,496,336 (8,763,833)Net decrease in financial assets available-for-sale (32,881,268) 57,563Net increase in financing and advances (213,770,097) (67,104,237)Net (decrease)/increase in trade and other payables 32,687,011 2,620,733Net decrease in uninvested fund deposits (712,250) (2,344,839) _____________ ____________

Cash used in operations (186,861,244) (24,341,642)

Dividend received 34,680,164 39,480,743Withholding tax paid (3,935,222) (3,763,706) _____________ ___________

Net cash(outflow)/inflow from operating activities (44,619,966) 11,375,395 _____________ ___________

Cash flow from operating activities

Proceeds from issue of redeemable units 5,107,609 123,181,492Payments on redemption of redeema ble units (250,395,251) (221,673,979)Distributions to holders of redeemable units - (11,047,158) _____________ _____________ Net cash used in financing activities (245,287,642) (109,539,645) _____________ _____________ Net decrease in cash and cash equivalents (289,907,608) (98,164,250)Cash and cash equivalents at beginning of year 12 840,577,533 938,741,783 _____________ _____________Cash and cash equivalents at end of year 12 550,670,465 840,577,533 ============= ============= The statement of the principal accounting policies set out on pages 20 to 44 and the notes on pages 44 to 56 form an integral part of these financial statements.

20 THE LOTUS HALAL INVESTMENT FUND IS MANAGED BY LOTUS CAPITAL LIMITED

LOTUS CAPITAL HALAL INVESTMENT FUNDIFRS Financial Statements

Notes to the Financial StatementsFor the year ended 31st December 2012

1. Reporting Entity

Lotus Capital Halal Investment Fund (“the Fund”) is an open-ended Unit Trust Scheme authorised and registered by the Securities and Exchange Commission. The Fund’s principal office is located at Lotus Capital Limited, 1b Udi Street, Osborne Foreshore Estate, Ikoyi, Lagos, Nigeria.The Fund is primarily involved in investments in well-diversified portfolio comprised of high quality equities listed on the Nigerian Stock Exchange, real estate and asset-backed investments in accordance with the principles of Islamic finance.The Fund is managed by Lotus Capital Limited (“the Fund Manager”) and the trustees to the Fund are First Trustees Nigeria Limited (“the Trustees”).

2. Basis of Preparation

2.1 Statement of ComplianceThe financial statements have been prepared in accordance with International Financial Reporting Standards (IFRSs). These are the Fund’s first financial statements prepared in accordance with IFRSs, and IFRS 1 First-time adoption of International Financial Reporting Standards has been applied.An explanation of how the transition to IFRSs has affected the reported financial position, financial performance and cash flows of the Fund is provided in note 19. This note includes reconciliation of profit or loss for comparative periods reported under Nigerian GAAP (previous GAAP) to those reported for this year under IFRS.The financial statements were authorised for issue by the Trustees and Fund Manager on 9th July, 2013.

2.2 Functional and Presentation CurrencyThese financial statements are presented in Nigerian Naira, which is the Fund’s functional currency. Except as otherwise indicated, financial information presented in Naira has been rounded to the nearest thousand.

2.3 Basis of MeasurementThese financial statements are prepared on the historical cost basis except for the following:

• Financial instruments at fair value through profit or loss are measured at fair value;• Available-for-sale financial assets are measured at fair value;

• Loans and receivables, held to maturity financial assets and financial liabilities are measured at amortized cost.

2.4 Use of Estimates and Judgments

The preparation of financial statements in conformity with IFRSs requires management

21THE LOTUS HALAL INVESTMENT FUND IS MANAGED BY LOTUS CAPITAL LIMITED

LOTUS CAPITAL HALAL INVESTMENT FUNDIFRS Financial Statements

Notes to the Financial StatementsFor the year ended 31st December 2012

to make judgments, estimates and assumptions that affect the application of policies and reported amounts of assets and liabilities, income and expenses. The estimates and associated assumptions are based on historical experience and various other factors that are believed to be reasonable under the circumstances, the results of which form the basis of making the judgments about carrying values of assets and liabilities that are not readily apparent from other sources. Actual results may differ from these estimates.

The estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognised in the year in which the estimates are revised and in any future years affected.

Judgements made by management in the application of IFRSs that have significant effect on the financial statements and estimates with a significant risk of material adjustments are discussed in note 5.

3. Significant Accounting P olicies

Significant accounting policies are defined as those that are reflective of significant judgements and uncertainties, and potentially give rise to different results under different assumptions and conditions.

The accounting policies set out below have been consistently applied to all years presented in these financial statements and in preparing an opening IFRS balance sheet at 1 January 2011 for purposes of the transition to IFRS.

3.1 Definition

(i) Murabaha

An agreement whereby the Fund sells to a customer a commodity which the Fund has purchased and acquired based on a promise received from customer to buy the item purchased according to specific terms and conditions. The selling price comprises the cost of the commodity and an agreed profit margin.

(ii) Mudaraba

An agreement between the Fund and a customer whereby the Fund would invest in a specific enterprise or activity, managed by the customer for a specific share in the profit. The customer would bear the loss in the case of default, negligence or violation of any of the terms and conditions of the Mudaraba.

(iii) Musharaka

An agreement between the Fund and a customer to contribute to a certain investment enterprise, whether existing or new, or the ownership of a certain property, either permanently or according to a diminishing arrangement ending with the acquisition by the customer of the

22 THE LOTUS HALAL INVESTMENT FUND IS MANAGED BY LOTUS CAPITAL LIMITED

LOTUS CAPITAL HALAL INVESTMENT FUNDIFRS Financial Statements

Notes to the Financial StatementsFor the year ended 31st December 2012

Fund’s share in the enterprise or property. The profit is shared as per the agreement set between both parties while the loss is shared in the proportion in which capital was contributed.

(iv) Ijara

An agreement whereby the Fund (lessor) purchases or leases an asset according to the customer’s requirements (lessee) based on his promise to lease the assets for a specific period and against certain rent instalments. Ijara could end by transferring the ownership of the asset to the lessee or not.

3.2 Foreign Currency Transactions

Transactions denominated in foreign currencies are recorded in Naira at the rate of exchange ruling at the date of each transaction. Any gain or loss arising from a change in exchange rates subsequent to the date of the transaction is included in the income statement.

Monetary assets and liabilities denominated in foreign currencies are translated using the exchange rate ruling at the balance sheet date; the resulting foreign exchange gain or loss is recognised in the income statement while those on non-monetary items are recognised in other comprehensive income. For non-monetary financial investments available-for-sale, unrealised exchange differences are recorded directly in equity until the asset is disposed or impaired.

3.3 Income from Financing and Advances

Income from financing and advances (financial contracts) such as Ijara, Murabaha, Mudaraba and Musharaka, are recognised in profit or loss using the effective return method. The effective return rate is the rate that exactly discounts the estimated future cash payments and receipts through the expected life of the financial asset or liability (or, where appropriate, a shorter period) to the carrying amount of the financial asset or liability. When calculating the effective return rate, the Fund estimates future cash flows considering all contractual terms of the financial instruments but not future credit losses. The effective return rate is calculated on initial recognition of the financial asset and liability and is not revised subsequently.

The calculation of the effective return rate includes contractual fees and points paid or received transaction costs, and discounts or premiums that are an integral part of the effective return rate. Transaction costs are incremental costs that are directly attributable to the acquisition, issue or disposal of a financial asset or liability.

Income from financing and advances presented in the statement of comprehensive income include returns on financial assets and liabilities measured at amortised cost calculated on an effective return rate basis.

Fair value changes on other financial assets and liabilities carried at fair value through profit or loss, are presented in net trading income from other financial instruments at fair value through profit and loss in the statement of comprehensive income.

23THE LOTUS HALAL INVESTMENT FUND IS MANAGED BY LOTUS CAPITAL LIMITED

LOTUS CAPITAL HALAL INVESTMENT FUNDIFRS Financial Statements

Notes to the Financial StatementsFor the year ended 31st December 2012

3.4 Net Gain/Loss from Financial Instruments at Fair Value through Profit or Loss

Net gain/loss from financial instruments at fair value through profit or loss includes all realised and unrealised fair value changes and foreign exchange differences, but excludes finance and dividend income.

3.5 Dividend Income

Dividend income is recognised when the right to receive income is established. Dividend income from equity securities designated at fair value through profit or loss and available-for-sale is recognised in the “dividend income” line in the statement of comprehensive income.

3.6 Fees, Commission and other Expenses

Fees, commission and other expenses are recognised in the statement of comprehensive income on an accrual basis.

3.7 Taxation

Dividend income and income from financing and advances received by the Fund is subject to withholding tax. Dividend income and income from financing and investing are therefore recorded gross of such taxes and the corresponding withholding tax is recognised as tax expense.

3.8 Financial Assets and Liabilities

(i) Recognition

The Fund classifies its financial instruments into the following categories: at fair value through profit or loss, available for sale, held to maturity, and financing and advances.

Management determines the classification at initial recognition.

All financial instruments are initially recognised at fair value, which includes transaction costs for financial instruments not classified as at fair value through profit and loss. Financial instruments are derecognised when the rights to receive cash flows from the financial instruments have expired or where the Fund has transferred substantially all risks and rewards of ownership.

(ii) Subsequent Measurement

Subsequent to initial measurement, financial instruments are measured either at fair value or amortised cost, depending on their classification:

24 THE LOTUS HALAL INVESTMENT FUND IS MANAGED BY LOTUS CAPITAL LIMITED

LOTUS CAPITAL HALAL INVESTMENT FUNDIFRS Financial Statements

Notes to the Financial StatementsFor the year ended 31st December 2012

(a) Held-to-Maturity

Held-to-maturity investments are non-derivative financial assets with fixed determinable payments and fixed maturities that management has both the positive intent and ability to hold to maturity, and which are not designated at fair value through profit or loss or as available for sale. Where the Fund sells more than an insignificant amount of held-to-maturity assets, the entire category would be tainted and reclassified as available-for-sale assets and the difference between amortised cost and fair value will be accounted for in equity. Held-to-maturity investments are carried at amortised cost, using the effective return method, less any provisions for impairment.

(b) Financial Assets Held at Fair Value through Profit or Loss

This category has two sub-categories; financial assets held for trading, and those designated at fair value through profit or loss at inception. A financial asset is classified as trading if acquired principally for the purpose of selling in the short term. Financial assets may be designated at fair value through profit or loss when the designation eliminates or significantly reduces measurement or recognition inconsistency that would otherwise arise from measuring assets or liabilities on different basis, or when a group of financial assets is managed and its performance evaluated on a fair value basis.

Subsequent to initial recognition, the fair values are re-measured at each reporting date. All gains or losses arising from changes therein are recognised in the income statement in ‘net trading income’ for trading assets, and in ‘net income from other financial instruments carried at fair value’ for financial assets designated at fair value through profit or loss at inception. The Fund’s investments in equities quoted on the Nigerian Stock Exchange are currently classified as financial assets held at fair value through profit or loss.

(c) Available-for-Sale

This category has two sub-categories; Available-for-sale financial assets are subsequently carried at fair value. Unrealised gains or losses arising from changes in the fair value of available-for-sale financial assets are recognised in net assets attributable to redeemable unit holders until the financial asset is derecognised or impaired. When available-for-sale financial assets are disposed of, the fair value adjustments accumulated in net assets attributable to redeemable unit holders are recognised in the income statement.

Dividends received on available-for-sale instruments are recognised in income statement when the Fund’s right to receive payment has been established.

The Fund’s investments in unquoted equities are currently classified as available-for-sale financial assets.

(d) Financing and Advances

Financing and advances are non-derivative financial assets with fixed or determinable

25THE LOTUS HALAL INVESTMENT FUND IS MANAGED BY LOTUS CAPITAL LIMITED

LOTUS CAPITAL HALAL INVESTMENT FUNDIFRS Financial Statements

Notes to the Financial StatementsFor the year ended 31st December 2012

payments that are not quoted in an active market, other than those classified by the Fund as at fair value through profit or loss or available-for-sale.

Financing and advances are measured at amortised cost using the effective return method, less any impairment losses. Origination transaction costs and origination fees received that are integral to the effective rate are capitalised to the value of the loan and receivable and amortised through finance income as part of the effective return rate.

The Fund’s investments in Ijara, Murabaha, Mudaraba and Musharaka contracts are currently classified as financing and advances.

(iii) Fair Value Measurement

Fair value is the amount for which an asset could be exchanged, or liability settled, between knowledgeable, willing parties in an arm’s length transaction on the measurement date. The best evidence of the fair value of a financial instrument on initial recognition is the transaction price, i.e. the fair value of the consideration paid or received, unless the fair value is evidenced by comparison with other observable current market transactions in the same instrument, without modification or repackaging, or based on discounted cash flow models and option pricing valuation techniques whose variables include only data from observable markets.

Subsequent to initial recognition, the fair values of financial instruments are based on quoted market prices or dealer price quotations for financial instruments traded in active markets. If the market for a financial asset is not active or the instrument is an unlisted instrument, the fair value is determined by using applicable valuation techniques. These include the use of recent arm’s length transactions, discounted cash flow analyses, pricing models and valuation techniques commonly used by market participants.

Where discounted cash flow analyses are used, estimated cash flows are based on management’s best estimates and the discount rate is a market-related rate at the financial position date from a financial asset with similar terms and conditions. Where pricing models are used, inputs are based on observable market indicators at the financial position date and profits or losses are only recognised to the extent that they relate to changes in factors that market participants will consider in setting the price.

(iv) Impairment of Financial Assets

(a) Assets Carried at Amortised Cost

The Fund assesses at each financial position date whether there is objective evidence that a financial asset or group of financial assets is impaired.

A financial asset or a group of financial assets is impaired and impairment losses are incurred if, and only if, there is objective evidence of impairment as a result of one or more events that occurred after the initial recognition of the assets (a ‘loss event’), and that loss event (or events) has an impact on the estimated future cash flows of the financial asset or group of financial assets that can be reliably estimated.

26 THE LOTUS HALAL INVESTMENT FUND IS MANAGED BY LOTUS CAPITAL LIMITED

LOTUS CAPITAL HALAL INVESTMENT FUNDIFRS Financial Statements

Notes to the Financial StatementsFor the year ended 31st December 2012

Objective evidence that financial assets (including equity securities) are impaired may include; default or delinquency by a debtor, restructuring of a financing account or advance by the Fund on terms that the Fund would not otherwise consider, indications that a customer or issuer will enter bankruptcy, the disappearance of an active market for a security, or other observable data relating to a group of assets such as adverse changes in the payment status of customers or issuers in the group, or economic conditions that correlate with defaults in the group.

The Fund first assesses whether objective evidence of impairment exists individually for financial assets that are individually significant, and individually or collectively for financial assets that are not individually significant.

If the Fund determines that no objective evidence of impairment exists for an individually assessed financial asset, whether significant or not, it includes the asset in a group of financial assets with similar credit risk characteristics and collectively assesses them for impairment. Assets that are individually assessed for impairment and for which an impairment loss is or continues to be recognised, are not included in a collective assessment of impairment.

For the purposes of a collective evaluation of impairment, financial assets are grouped on the basis of similar credit risk characteristics (i.e. on the basis of the Fund’s grading process which considers asset type, industry, geographic location, collateral type, past-due status and other relevant factors). These characteristics are relevant to the estimation of future cash flows for groups of such assets being indicative of the debtors’ ability to pay all amounts due according to the contractual terms of the assets being evaluated.

In assessing collective impairment, the Fund uses statistical modelling of historical trends of the probability of default, timing of recoveries and the amount of loss incurred, adjusted for management’s judgment as to whether current economic and credit conditions are such that actual losses are likely to be greater or less than suggested by historical modelling. Default rates, loss rates and the expected timing of future recoveries are regularly benchmarked against actual outcomes to ensure that they remain appropriate.

If there is objective evidence that an impairment loss on receivable or a held-to-maturity asset has been incurred, the amount of the loss is measured as the difference between the asset’s carrying amount and the present value of estimated future cash flows (excluding future credit losses that have not been incurred), discounted at the asset’s original effective return rate. Losses are recognised in profit or loss and reflected in an allowance account against loans and receivables. Finance income on the impaired asset continues to be recognised through the unwinding of the discount. The carrying amount of the asset is reduced through the use of an allowance account.

The calculation of the present value of the estimated future cash flows of a collateralized financial asset reflects the cash flows that may result from foreclosure less costs for obtaining and selling the collateral, whether or not foreclosure is probable. Future cash flows in a group of financial assets that are collectively evaluated for impairment are estimated on the basis of the historical loss experience for assets with credit risk characteristics similar to those in the group. Historical loss experience is adjusted on the basis of current observable data to reflect the effects off current conditions that did not affect the period on which the historical loss experience is based, and to remove the effects of conditions in the historical period that do not exist currently.

27THE LOTUS HALAL INVESTMENT FUND IS MANAGED BY LOTUS CAPITAL LIMITED

LOTUS CAPITAL HALAL INVESTMENT FUNDIFRS Financial Statements

Notes to the Financial StatementsFor the year ended 31st December 2012

To the extent a receivable is irrecoverable, it is written off against the related allowance for impairment. Such receivables are written off after all the necessary procedures have been completed and the amount of the loss has been determined. Subsequent recoveries of amounts previously written of decrease the amount of the allowance for impairment in profit or loss. If, in a subsequent period, the amount of the impairment loss decreases and the decrease can be related objectively to an event occurring after the impairment was recognised (such as an improvement in the debtor’s credit rating), the previously recognized impairment loss is reversed by adjusting the allowance account. The amount of the reversal is recognised in profit or loss.

(b) Available-for-Sale Financial Assets

Available-for-sale financial assets are impaired if there is objective evidence of impairment, resulting from one or more loss events that occurred after initial recognition but before the financial position date, that have an impact on the future cash flows of the asset. In addition, an available-for-sale equity instrument is generally considered impaired if a significant or prolonged decline in the fair value of the instrument below its cost has occurred. Where an available-for-sale asset, which has been re-measured to fair value directly through net assets available to redeemable unit holder, is impaired, the impairment loss is recognised in profit or loss. If any loss on the financial asset was previously recognised directly in equity as a reduction in fair value, the cumulative net loss that had been recognised in net assets available to redeemable unit holders is transferred to profit or loss and is recognised as part of the impairment loss. The amount of the loss recognised in profit or loss is the difference between the acquisition cost and the current fair value, less any previously recognised impairment loss.

If, in a subsequent period, the amount relating to an impairment loss decreases and the decrease can be linked objectively to an event occurring after the impairment loss was recognised in the income statement, where the instrument is a debt instrument, the impairment loss is reversed through profit or loss. An impairment loss in respect of an equity instrument classified as available-for-sale is not reversed through profit or loss but accounted for directly in net assets available to redeemable unit holders.

(v) Offsetting Financial Instrument

Financial assets and liabilities are set off and the net amount presented in the statement of financial position when, and only when, the Fund has a legal right to set off the amounts and intends either to settle on a net basis or to realise the asset and settle the liability simultaneously.

Income and expenses are presented on a net basis only when permitted by accounting standards, or for gains and losses arising from a group of similar transactions such as in the Fund’s trading activity.

28 THE LOTUS HALAL INVESTMENT FUND IS MANAGED BY LOTUS CAPITAL LIMITED

LOTUS CAPITAL HALAL INVESTMENT FUNDIFRS Financial Statements

Notes to the Financial StatementsFor the year ended 31st December 2012

(vi) Derecognition of Financial Instruments

The Fund derecognises a financial asset when the contractual rights to the cash flows from the asset expire, or it transfers the rights to receive the contractual cash flows on the financial asset in a transaction in which substantially all the risks and rewards of ownership of the financial asset are transferred, or has assumed an obligation to pay those cash flows to one or more recipients, subject to certain criteria.

Any interest in transferred financial assets that is created or retained by the Fund is recognised as a separate asset or liability.

The Fund derecognises a financial liability when its contractual obligations are discharged or cancelled or expire. The Fund enters into transactions whereby it transfers assets recognised on its balance sheet, but retains either all risks or rewards of the transferred assets or a portion of them. If all or substantially all the risks and rewards are retained, then the transferred assets are not derecognised from the statement of financial position. In transactions where the Fund neither retains nor transfers substantially all the risks and rewards of ownership of a financial asset, it derecognises the asset if control over the asset is lost.

The rights and obligations retained in the transfer are recognised separately as assets and liabilities as appropriate. In transfers where control over the asset is retained, the Fund continues to recognise the asset to the extent of its continuing involvement, determined by the extent to which it is exposed to changes in the value of the transferred asset.

3.9 Cash and Cash Equivalents

Cash and cash equivalents include notes and coins in hand, operating accounts with banks and highly liquid financial assets with original maturities of three months or less from the acquisition date, which are subject to insignificant risk of changes in their fair value, and are used by the Fund in the management of its short-term commitments.

Cash and cash equivalents are carried at amortised cost in the statement of financial position.

3.10 Provisions

A provision is recognised if, as a result of a past event, the Fund has a present legal or constructive obligation that can be estimated reliably, and it is provable that an outflow of economic benefits will be required to settle the obligation. Provisions are determined by discounting the expected future cash flows at a pre-tax rate that reflects current market assessments of the time value of money and, where appropriate, the risks specific to the liability.

A provision for restructuring is recognised when the Fund has approved a detailed and formal restructuring plan, and the restructuring either has commenced or has been announced publicly. Future operating costs are not provided for.

A provision for onerous contracts is recognised when the expected benefits to be derived by the Fund from a contract are lower than the unavoidable cost of meeting the obligations under the contract. The provision is measured at the present value of the lower of the expected cost of terminating the contract and the expected net cost of continuing with the contract. Before

29THE LOTUS HALAL INVESTMENT FUND IS MANAGED BY LOTUS CAPITAL LIMITED

LOTUS CAPITAL HALAL INVESTMENT FUNDIFRS Financial Statements

Notes to the Financial StatementsFor the year ended 31st December 2012

a provision is established, the Fund recognises any impairment loss on the assets associated with that contract.

3.11 Contingencies

(i) Contingent Asset

Contingent Asset is a possible asset that arises from past events and whose existence will be confirmed only by the occurrence or non-occurrence of one or more uncertain future events not wholly within the control of the entity.

A contingent asset is disclosed when an inflow of economic benefit is probable. When the realisation of income is virtually certain, then the related asset is not contingent and its recognition is appropriate. Contingent assets are assessed continually to ensure that developments are appropriately reflected in the financial statements.

(ii) Contingent Liability

Contingent liability is a possible obligation that arises from past event and whose existence will be confirmed only by the occurrence or non-occurrence of one or more uncertain future events not wholly within the control of the entity; or a present obligation that arises from past events but is not recognised because it is not probable that an outflow of resources embodying economic benefits will be required to settle the obligation; or the amount of the obligation cannot be measured with sufficient reliability.

Contingent liability is disclosed unless the probability of an outflow of resources embodying economic benefit is remote. A provision for the part of the obligation for which an outflow of resources embodying economic benefit is recognised; except in the extremely rare circumstances where no reliable estimate can be made.

Contingent liabilities are assessed continually to determine whether an outflow of economic benefit has become probable.

3.12 Redeemable Units

The Fund classifies financial instruments issued as financial liabilities or equity instruments in accordance with the substance of the contractual terms of the instruments.

The Fund has only one class of redeemable units in issue. The redeemable units provide investors with the right to require redemption for cash at a value proportionate to the investor’s share in the Fund’s net assets at the time of redemption and also in the event of the Fund’s liquidation.

A puttable financial instrument that includes a contractual obligation for the Fund to repurchase or redeem that instrument for cash or another financial asset is classified as equity if it meets all the following conditions.

• It entitles the holder to a pro rata share of the Fund’s net assets in the event of the Fund’s liquidation;

30 THE LOTUS HALAL INVESTMENT FUND IS MANAGED BY LOTUS CAPITAL LIMITED

LOTUS CAPITAL HALAL INVESTMENT FUNDIFRS Financial Statements

Notes to the Financial StatementsFor the year ended 31st December 2012

• It is in the class of instruments that is subordinate to all other classes of instruments;

• All financial instruments in the class of instruments that is subordinate to all other classes of instruments have identical features;

• Apart from the contractual obligation for the Fund to repurchase or redeem the instrument for cash or another financial asset, the instrument does not include any other feature that would require classification as a liability; and

• The total expected cash flows attributable to the instrument over its life are based substantially on the profit or loss, the change in the recognised net assets or the change in the fair value of the recognised and unrecognised net assets of the Fund over the life of the instrument.

The Fund’s redeemable units meet these conditions and are classified as equity.

All transactions relating to the issue and redemption of redeemable units as well as distributions to holders of redeemable units are recognised in equity.

3.13 New Standards and Interpretations Not Yet Adopted

A number of new standards, amendments to standards and interpretations, are not yet effective for the year ended 31st December, 2012, and have not been applied in preparing these financial statements. None of these will have an effect on the financial statements of the Fund, with the possible exception of the following:

• IFRS 9 Financial Instruments: Classification and Measurement

IFRS 9 deals with classification and measurement of financial assets and its requirements represent a significant change from the existing requirements in IAS 39 in respect of financial assets. The standard contains two primary measurement categories for financial assets: amortised cost and fair value. A financial asset would be measured at amortised cost if it is held within a business model whose objective is to hold assets in order to collect contractual cash flows, and the asset’s contractual terms give rise on specified dates to cash flows that are solely payments of principal and interest on the principal outstanding. All other financial assets would be measured at fair value. The standard eliminates the existing IAS 39 categories of held to maturity, available for sale and loans and receivables.

For an investment in an equity instrument which is not held for trading, the standard permits an irrevocable election, on initial recognition, on an individual share-by- share basis, to present all fair value changes from the investment in other comprehensive income. No amount recognised in other comprehensive income would ever be reclassified to profit or loss. However, dividends on such investments are recognised in profit or loss, rather than other comprehensive income unless they clearly represent a partial recovery of the cost of the investment. Investments in equity instruments in respect of which an entity does not elect to present fair value changes in other comprehensive income would be measured at fair value with changes in fair value recognised in profit or loss. IFRS 9 is effective for annual periods beginning on or after 1st January 2015 with early adoption permitted. The Fund is currently in the process of evaluating the potential effect of this standard. The standard is not expected to have a significant impact on the financial statements since the majority of the Fund’s financial assets are measure at amortised cost.

31THE LOTUS HALAL INVESTMENT FUND IS MANAGED BY LOTUS CAPITAL LIMITED

LOTUS CAPITAL HALAL INVESTMENT FUNDIFRS Financial Statements

Notes to the Financial StatementsFor the year ended 31st December 2012

• IFRS 13 Fair Value Measurement

IFRS 13 defines fair value, provides guidance on its determination and introduces consistent requirements for disclosure on fair value measurements. It is applicable for all assets and liabilities that require a fair value based on IFRS. Disclosures for fair value are extended. The Fund will assess whether this new standard has any impact on existing fair value policies and disclosures. IFRS 13 is effective for annual periods beginning on or after 1st January 2013 with early adoption permitted. The Fund has not adopted IFRS 13 early.

4 Financial Risk Management

(a) Introduction and Overview

Lotus Capital Halal Investment Fund has exposure to the following risks from financial instruments.

i. Credit risk;ii. Liquidity risk;iii. Market risk; andiv. Operational risk.

Risk Management Framework

Lotus Capital Halal Investment Fund maintains positions in a variety of financial instruments in accordance with its investment management strategy as stated below:

“The Fund shall be invested in securities screened for Shari’ah compliance and asset-backed investments including but not limited to equity and non-interest debt instruments approved by the Securities and Exchange Commission of Nigeria. Furthermore, the Fund can invest in real estate transactions which are Shari’ah compliant. The Trust Deed allows maximum of 80% of the Fund to be invested in selected equities of Nigerian quoted companies, 60% in other investments and 30% in Real Estate. The Fund Manager shall not alter the investment policy of the Fund without the prior approval of the Securities and Exchange Commission and approval of the Trustee with a special resolution of a meeting of holders duly convened and held in accordance with the provisions in the Trust Deed.”

The Fund’s investment portfolio comprises investments in equities, investments in asset-backed contracts and real estate. The asset-backed contracts and real estate investments are classified as financing and advances in the statement of financial position.

Asset purchases and sales are determined by the Fund’s Portfolio Manager, who has been given discretionary authority to manage the distribution of the assets to achieve the Fund’s investment objectives subject to the approval of the Chief Investment Officer. Compliance with the target asset allocations and the composition of the portfolio is monitored by the Investment and Risk Management Committee on a weekly basis. In instances where the portfolio has deviated from target asset allocations, the Fund’s Portfolio Manager is obliged to take such actions as may be approved by the Investment Committee to rebalance the portfolio in line with the asset allocation as prescribed by the Trust Deed, within the reasonable time limits.

32 THE LOTUS HALAL INVESTMENT FUND IS MANAGED BY LOTUS CAPITAL LIMITED

LOTUS CAPITAL HALAL INVESTMENT FUNDIFRS Financial Statements

Notes to the Financial StatementsFor the year ended 31st December 2012

(b) Credit Risk

Credit risk is the risk that a counter party to a financial instrument will fail to discharge an obligation or commitment that it has entered into with the Fund, resulting in a financial loss to the Fund. It arises principally from financing and advances and cash and cash equivalents.

For risk management reporting purposes the Fund considers and consolidates all elements of credit risk exposure (such as individual obligor default risk, country and sector risk).

Management of Credit Risk

Lotus Capital Halal Investment Fund’s policy in respect of credit risk is to minimize its exposure to clients with perceived higher risk of default by dealing only with clients that meet the requirements of the risk management policy as set out in the Fund’s prospectus. The risk is also managed by evaluating the client and assigning a credit rating to each client which serves as a trigger and also suggests the action to be taken in case of first default. Other ways of managing the credit risk include; identifying and mitigating transaction risk, reviewing industry position, managing global credit exposure to a counter party, taking collateral and monitoring disbursement/repayment.

The Fund’s credit risks are monitored on a weekly basis by the Investment and Risk Management Committee which is led by the Chief Investment Officer. Where the credit risks are not in accordance with the investment policy or guidelines of the Fund, the Portfolio Manager is obliged to reject and/or rebalance the portfolio as approved by the Investment and Risk Management Committee when the portfolio is not in compliance with the stated investment objectives.

Single Obligor Limit

At every point in time, the total exposure of the Fund to any single entity or group of related borrowers shall not exceed 10% of the Fund’s net asset value. The portfolio manager also considers and monitors the limit each time there is a new or restructured investment.

Exposure to Credit Risk

The Fund’s maximum credit risk exposure (before collateral and other credit enhancements) at the statement of financial position date is represented by the respective carrying amounts of the financial assets in the statement of financial position. The risks on some of these exposures, such as receivables from financing and advance, are mitigated by collateral securities held.

Cash and Cash Equivalents

The Fund’s cash balances are held mainly with the custodian Citibank Nigeria Limited which is rated Aa+ by Agusto & Co. However, the fund also maintains a certain portion of the Fund’s assets in Murabaha investment contracts which are fully guaranteed by banker’s acceptances issued by a reputable bank in Nigeria. Due to the nature of this type of transaction and its maturity, the investment is classified as cash equivalent.

The Portfolio Manager monitors the Fund’s liquidity position with the custodian on a daily basis.

Financing and Advances

In order to secure commitment and prevent possible diversion of funds by the counter party

33THE LOTUS HALAL INVESTMENT FUND IS MANAGED BY LOTUS CAPITAL LIMITED

LOTUS CAPITAL HALAL INVESTMENT FUNDIFRS Financial Statements

Notes to the Financial StatementsFor the year ended 31st December 2012

requesting for financing and advances, the Portfolio Manager demands for post-dated cheques for the value of the assets being financed and or an account domiciliation of the deposit if the payment is coming from a third party. In addition to the measures above, the fund manager has also set up a process that flags the possible risk of impairment in the value of the receivables.

Credit Quality of Gross Financing and Advances

Collateral

The main types of collateral obtained by the Fund to mitigate the credit risk are as follows:

• Ijara financing and advances – ownership claims over the assets financed;

• Murabaha financing and advances- charges over other liquid assets provided by the client;

• For other financing and advances – charges over business assets such as premises, inventories, trade receivables, investment deposits or residential properties.

Gross financing and advances are classified as follows:

Neither Past Due Nor Impaired Financing and Advances

Financing and advances in which the borrower has not missed a contractual payment (profit or principal) when contractually due and is not impaired as there is no objective evidence of impairment.

Past due but not impaired financing and advances

Financing and advances in which the contractual profit or principal payments are past due, but the Fund believe that impairment is not appropriate on the basis of the level of collateral available and/or the stage of collection amounts owed to the Fund.

Impaired Financing and Advances

Financing and advances are classified as impaired when the principal or profit or both are past due for three months or more, or where a financing is in arrears for less than three months, but the financing exhibits indications of significant credit weakness.

34 THE LOTUS HALAL INVESTMENT FUND IS MANAGED BY LOTUS CAPITAL LIMITED

LOTUS CAPITAL HALAL INVESTMENT FUNDIFRS Financial Statements

Notes to the Financial StatementsFor the year ended 31st December 2012