Embed Size (px)

Citation preview

Lost Profits in Construction Litigation:

Proving and Defending Damages

Speakers:Jeffrey W. Spilker, JD, CPA/ABVJared C. Jordan, CFE

Presented to:

Speakers

Jeff Spilker is an Owner of Hill Schwartz Spilker Keller LLC (“HSSK”), a business valuation and

litigation consulting firm in Houston, Texas. Jeff leads the HSSK’s real estate consulting and

construction advisory practice.

Previously, Jeff was with a national accounting and consulting firm. He has also served as the

CFO of an engineering/construction company and Vice President/General Manager of a

construction and real estate development firm. Jeff has provided a wide range of financial and

economic consulting and financial forensics services to attorneys in matters involving intellectual

property and patent infringement claims, health care and professional practices, oil & gas issues,

construction disputes, professional liability claims, partnership disputes, real estate and business

valuation issues, environmental issues, personal injury and employment claims, lost profits

analyzes, fraud investigations and lender liability claims. He has provided expert testimony in

over 100 of these matters.

Jeff is a Certified Public Accountant, licensed attorney in the Commonwealth of Virginia and a

Texas State Certified General Real Estate Appraiser.

Jeffrey W. Spilker, JD, CPA/ABV

Speakers

Jared Jordan serves as Managing Director in the Litigation Consulting practice and is the leader of

HSSK’s Austin office. He is a Certified Fraud Examiner with over 14 years of experience assisting

clients with the financial and accounting aspects of disputes and investigations including serving

as an expert witness in litigation matters.

Jared’s experience includes developing and analyzing damage claims, conducting fraud and

financial forensics investigations, examining and assessing corporate governance practices and

internal controls, and evaluating complex data sets resulting from allegations of breach of

contract, financial misrepresentation, fraud, director and officer misconduct, misuse of corporate

funds and breach of fiduciary duty.

Jared previously served in a Director level position in the Disputes and Investigations practice of

an international publicly-traded consulting firm. He currently serves on the Advisory Council for

the Association of Certified Fraud Examiners. Jared also regularly presents on a wide range of

topics including conducting fraud, forensic and special investigations in and out of the litigation

setting.

Jared C. Jordan, CFE

Today’s Program

I. Lost Profits Damages – Overview

II. Evidence & Documentation – What do You Need?

III. Quantification of Lost Profits – Methods & Issues

IV. Defending Against Lost Profits – Areas of Focus

V. Daubert Expert Challenges – Historical Trends

Types of Construction Damages

• Types of construction damages

Direct Damages

Consequential Damages

• Today’s presentation is focused on lost profits

What are “lost profits”?

• Lost profits are damages for the loss of net income to a

business.

• The claim is for income from lost

business activity, less expenses that

would have been attributable to that

activity.

Permanent or Temporary

• Permanent Loss means no resumption of operations. The

measure of damages for a permanent loss is diminished

value:

Value at Event

- Value After the Event

Damages

Permanent or Temporary (cont.)

• Temporary Loss means that the business will resume

normal operations in the future.

• There can be cases of mixed loss, i.e., loss of profits until

business terminates.

Permanent or Temporary (cont.)

• “Damage Period” defines the time it will take Plaintiff to

be put back into the position prior to the wrongful event.

• Facts: Contract period, historical relationships, historical

retention rates, etc. If no case facts establish a damage

period, future losses become more speculative.

Simple Lost Profits Example

0

100

200

300

400

500

600

700

Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13

Expected Profit

Actual profit

Loss Period

Lost Profits

Event Recovery

Lost Profits Model – Delay Claim

$

Series1 Series2

1 Year 2 Years 3 Years

Excess Costs

Lost Profits

10 ½ Month Damage PeriodStabilized

NOI

10 ½ Month Delay Period

September 15, 2010July 31, 2011● ●

Expected Profit Actual Profit

Reasonable Certainty

• You must “prove” something that never happened

"I'd shut [Apple] down and give the

money back to the shareholders."—

Michael Dell, founder and CEO of Dell,

Inc., 1997

Apple’s stock price:

January 7, 2007 -- $ 21.12/share.

March 3, 2014 -- $ 523.42/share.

Reasonable Certainty (cont.)

• There are almost no law review articles

that discuss it other than student notes

• For an exhaustive analysis –

Robert M. Lloyd, Professor

at Univ. of Tennessee

Reasonable Certainty – Examples

Southwest Battery Corp. v. Owen, 115 S.W.2d (Tex. 1938)

• “The amount of the loss must be shown by competent

evidence with reasonable certainty” (at 1097, 1098-99)

• Industry was well established -- Sale of car batteries not

uncertain or speculative

• A short history of profits combined with an established

industry was sufficient

• However, the court referred to the “new business” rule

Texas Instruments, Inc. v. Teletron Energy Management,

Inc., 877 S.W.2d (Tex. 1994).

• “New business” rule clarified –

• The enterprise is the “activity” not the entity. “The focus is

on the experience of the persons involved in the enterprise

and the nature of the business activity, and the relevant

market.” (at 276, 279-280)

Reasonable Certainty – Examples (cont.)

Evidence & Documentation…

What do You Need?

It’s the facts…

• Look at the activity. Is it an established activity? Yes! –fried chicken, car batteries, hotel door key/credit card readers

No! – voice prompted thermostats

• What are the facts of the entity/activity? Things your expert

needs to “drill down into.” Management Expertise and Experience

Availability of labor

Availability of capital

The Business Plan

Competition and Markets

Types of Evidence / Documentation

• Business Records … Literally

• Business financial forecasts –

Management budgets (New Business)

• Historical Financial Statements

(for every entity, subsidiary, etc.)

Types of Evidence / Documentation (cont.)

• Tax Returns for the same period as Financials – Request all the

schedules

Types of Evidence / Documentation (cont.)

• Debt and credit documentation -- Subpoena third-party

banks

Contracts – (customer, equipment, facilities, long term obligations)

Corporate Formation Documents / operating capacity limits

Meetings with management

Deposition testimony

Industry trade publications/professional associations

Federal and government economic data

Public company and competitive resources

Economic / market / local events

Quantification of Lost Profits –

Methods & Issues

• Causation is often assumed by the expert

Proof of causation is on the lawyer

Proof of foresee ability too

• Demonstrate Lost Profits with Discounted Cash Flow

Damages = Liability + Causation

Methods

• Before and After

• Yardstick

• Market Share or Specific Contract

Before and After Approach

$0

$100

$200

$300

$400

$500

$600

1995 1996 1997 1998 1999 2000 2001 2002

Before After

Lost Sales

$0

$100

$200

$300

$400

$500

$600

1995 1996 1997 1998 1999 2000 2001 2002

Before Projected (but-for) After (Actual)

Lost Sales

Before and After Approach (cont.)

$0

$100

$200

$300

$400

$500

$600

$700

1995 1996 1997 1998 1999 2000 2001 2002

Before After (but-for) After (Actual) Like Company Index

Lost Sales

Yardstick Approach

Determining But-For Costs

• Incremental costing

• Some methods for

determining but-for costs:

Fully allocated costs

Comparative costs

Line item classification

Cost engineering

Regression analysis

0

10

20

30

40

1998 1999 2000 2001 2002

Lost Sales

Incremental Costs

Lost Profits

Discount Period

Projecting Costs

• Variable, Semi-variable

and Fixed can vary

with location

Stabilized Earnings

“The first step in a delay study for an income-

producing property is for the appraiser or

analyst to be provided with an extraordinary

assumption that the subject property

sustained a delay. This information should be

based on calculations by a qualified

construction expert. The change in timeline

then supplies the analyst with the foundation

for the number of days, weeks, or months that

will form the basis for the ultimate damage

calculation.”

Stabilized Earnings (cont.)

“The appraiser or analyst must then establish pro forma income and

expense statement, which would include market-based income, vacancy

rates, and fixed and variable expenses from which adjusted daily lost

revenues can be derived. The analyst should be aware that it is not

appropriate to use the initial absorption period for calculating the

damage estimate. Revenues relating to stabilized occupancy should be

used instead. Ultimately, the estimated daily lost revenue is multiplied by

the total number of days of delay, as provided by the construction expert,

to form an opinion of damages.”

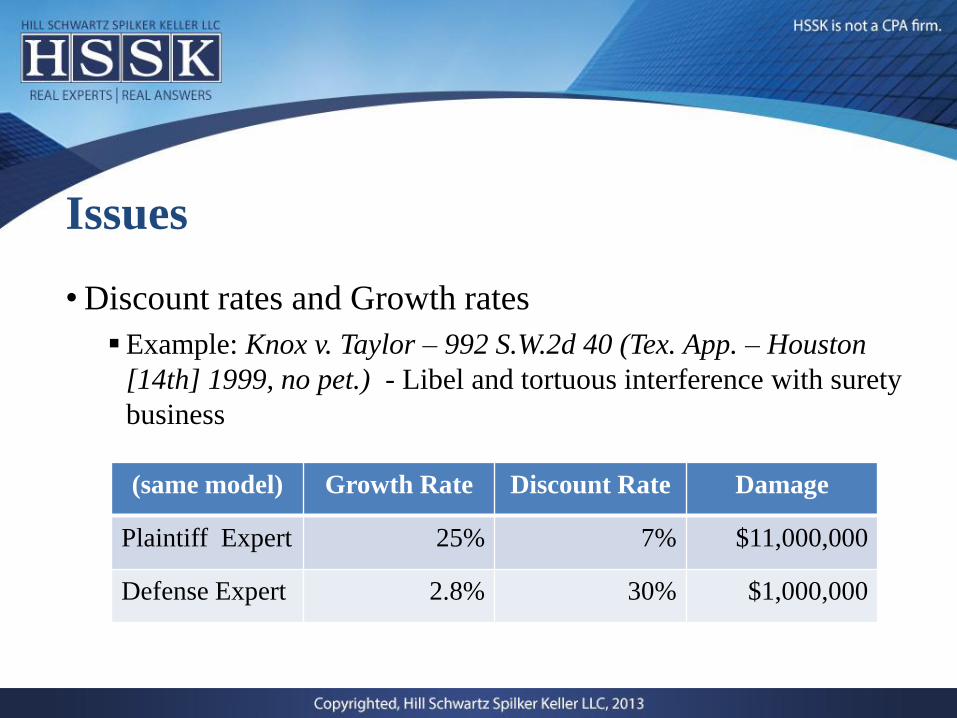

Issues

• Discount rates and Growth rates

Example: Knox v. Taylor – 992 S.W.2d 40 (Tex. App. – Houston

[14th] 1999, no pet.) - Libel and tortuous interference with surety

business

(same model) Growth Rate Discount Rate Damage

Plaintiff Expert 25% 7% $11,000,000

Defense Expert 2.8% 30% $1,000,000

Defending Against Lost Profits –

Areas of Focus

Qualified, Relevant & Reliable

• The Expert

• The Data

• The Assumptions

• The Methodology

• The Opinions

• The Report

• The Disclosure/ Designation

Analytical gap…Capital Metro v. Central Tennessee

• Freight service provider on rail line; contract terminated,

counterclaim

Analytical gap…(cont.)Capital Metro v. Central Tennessee (cont.)

• Plaintiff’s expert -- $6.6 million Historical revenues;

Estimate of carloads and charges;

Projection of costs

• Court -- $0 History of losses;

No identifiable contracts;

Forecasts based on “old” contract with

Capital Metro;

No independent confirmation of 7,550

carloads he assumed;

No evidence they could even do that many;

No verification of revenue per carload;

No investigation of management practices;

whether it had a business plan;

Admitted that variable costs were running

160% of revenue;

And other problems

Apartment Complex Example

• Water loss delays opening of new apartment complex

• Case brought by subrogating insurance carrier

• Complex sues for its uninsured losses, including business

interruption claim arising out of delayed opening

Apartment Complex Example (cont.) Expert Qualifications

• Not a CPA

• No education or classes in school regarding lost profit

claims

• No real estate specialization or designation

• Only one other lost profit model, totally unrelated to losses

in this case

• Was “surprised” to learn that there are generally accepted

models within the industry

Apartment Complex Example (cont.) Saved ExpensesQ. Okay. It's also your belief that

there are no saved expenses.

Is that correct?

A. That's right.

Q. All right. But just so that the jury understands your—the

model that you've created and the approach you've taken,

you have not undertaken to determine if there are any

saved expenses. Correct?

A. In this model. Right.

Apartment Complex Example (cont.) Absorption

• Number of apartments rented per month.

• Loss related to water event vs. loss due to other factors?

Speculation!

• Absorption rate: 20

• The higher the rate,

the higher the damages

i.e., apartments would

have leased more quickly.

Apartment Complex Example (cont.) Absorption (cont.)Q. Okay. So when you told me earlier that the number 20 came out of the pro

forma that was put together with GE at the time that y'all went to get

financing and do all that financial stuff, that was an incorrect statement.

Correct?

A. It was related to -- you know, it was -- that does not match this pro forma.

That's right.

Q. Okay. Well --

A. Yeah, that's fair. And this pro forma that was provided was the originally

approved pro forma and we -- again, I guess I had assumed they were kind of

going through --and we -- well, I'd assumed that this schedule was what --

Q. Okay. But it's not.

A. Right. You're right.

Apartment Complex Example (cont.) Absorption (cont.)

The alternate source for absorption rate was a

database compiled by the company to track

occupancy rates at other properties.

Red River Roberston 404 Rio Amli Amli on Gables 300 N. Greystar The The

Week ended Flats Hill Grande Downtown 2nd West Avenue Lamar South Congess Monarch Crescent Comments

April 7, 2008 0 7 1 3 0 3 3 0 5

April 14, 2008 0 0 0 0 0 0 0 0 0 No information on sheet

April 21, 2008 0 0 0 0 0 0 0 0 0 No information on sheet

April 28, 2008 0 0 0 0 0 0 0 0 0 No information on sheet

May 5, 2008 0 0 0 0 0 0 0 0 0 No information on sheet

May 12, 2008 0 7 1 3 0 3 3 0 5

May 19, 2008 2 8 2 6 6 4 5 0 5

May 26, 2008 2 8 2 4 6 0 2 2 11

June 2, 2008 0 0 0 0 0 0 0 0 0

June 9, 2008 1 8 0 5 471 3 4 5 10 Unusually high number.

June 16, 2008 0 8 2 7 6 5 2 0 13

June 23, 2008 0 0 0 0 0 0 0 0 0 No information on sheet

June 30, 2008 0 0 0 0 0 0 0 0 0 No information on sheet

July 7, 2008 0 1 3 6 2 5 5 2 8

July 14, 2008 3 2 2 5 3 7 7 5 11

July 21, 2008 4 10 5 2 11 6 4 9 3

July 28, 2008 4 10 5 2 11 6 4 9 3 Same as prior month?

August 4, 2008 3 3 6 7 6 5 4 2 2 5

August 11, 2008 0 0 0 0 0 0 0 0 0 No information on sheet

August 18, 2008 0 0 0 0 0 0 0 0 0 No information on sheet

August 25, 2008 10 4 2 3 5 4 3 7 4

September 1, 2008 1 4 1 4 3 5 2 3 2 1

September 8, 2008 0 0 0 0 0 0 0 0 0 No information on sheet

September 15, 2008 0 0 0 0 0 0 0 0 0 No information on sheet

September 22, 2008 0 0 0 0 0 0 0 0 0 No information on sheet

September 29, 2008 0 0 0 0 0 0 0 0 0 No information on sheet

October 6, 2008 0 0 0 0 0 0 0 0 0 No information on sheet

October 13, 2008 0 0 0 0 0 0 0 0 0 No information on sheet

October 20, 2008 0 0 0 0 0 0 0 0 0 No information on sheet

October 27, 2008 0 0 0 0 0 0 0 0 0 No information on sheet

November 3, 2008 0 0 0 0 0 0 0 0 0 No information on sheet

November 10, 2008 0 0 0 0 0 0 0 0 0 No information on sheet

November 17, 2008 0 0 0 0 0 0 0 0 0 No information on sheet

November 24, 2008 0 0 0 0 0 0 0 0 0 No information on sheet

December 1, 2008 0 0 0 0 0 0 0 0 0 No information on sheet

December 8, 2008 0 0 0 0 0 0 0 0 0 No information on sheet

December 15, 2008 0 0 0 0 0 0 0 0 0 No information on sheet

December 22, 2008 0 0 0 0 0 0 0 0 0 No information on sheet

December 29, 2008 0 0 0 0 0 0 0 0 0 No information on sheet

Daubert Expert Challenges –

Historical Trends

PWC’s Daubert Challenges to

Financial Experts • 14-year trend w/ cases citing Daubert/Kumho Tire

• Economists, accountants, and appraisers challenged the most

• Economists and accountants most likely to survive.

• Case type affects the frequency and outcome

• Lack of Reliability is the top reason to exclude financial experts

• Exclusions more common due to the misuse of accepted

methodologies than from the introduction of unusual or untested

analytical methods

PWC’s Daubert Challenges to

Financial Experts (cont.)• Challenges raised every year from 2000-2013.

• Plaintiff’s experts are challenged approx. three times as often as

defense experts, but their exclusions rates were lower in eight of

the past 14 years.

• The Circuit Court matters, with 57% of all Daubert challenges

being adjudicated in the Second, Fifth, Sixth, Seventh, & Ninth

circuits.

Questions?