Embed Size (px)

Citation preview

Fast Close: A Guide to Rapid Month-End and Year-End Reporting

by David Parmenter

This document breaches copyright if it has not been received directly from David Parmenter

Fast Close: A Guide to Rapid Month-End & Year-End Reporting ©2018 Page 2 David Parmenter [email protected] www.davidparmenter.com

Contents 1. Introduction .............................................................................................................. 5

1.1. Importance of abandonment .............................................................................. 5

1.2. The importance of challenging the status quo .................................................... 6

1.3. Ranking guide .................................................................................................... 6

2. The burning platform ................................................................................................ 7

2.1. Benefits of quick monthly reporting to management and the Finance team ....... 7

2.2. The impact of quick reporting on the Finance team and the organisation ........... 8

3. Lean best practice for your next month-end ............................................................. 9

3.1. Get the CEO supporting fast month-end reporting ............................................. 9

3.2. Establish month-end reporting rules within the finance team ........................... 10

3.3. Catch all adjustments in an ‘overs and unders' schedule ................................. 11

3.4. Avoid a huge wave of AP invoices at month-end ............................................. 11

3.5. Early closing of the accounts payable ledger ................................................... 12

3.6. Close accruals before the accounts payable cut-off ......................................... 12

3.7. Stop reconciling to suppliers’ statements ......................................................... 13

3.8. Avoid inter-company adjustments .................................................................... 13

3.9. Early closing-off of accounts receivables ......................................................... 13

3.10. Early capital expenditure cut-off ..................................................................... 14

3.11. Early inventory cut-off .................................................................................... 14

3.12. The critical first 24 hours ................................................................................ 14

3.13. Deliver a flash report at the end of day 1........................................................ 15

3.14. Stop monthly reforecasting of year-end.......................................................... 16

3.15. The key month-end activities on a day three month-end ................................ 17

4. Winning agile practices to improve month-end ....................................................... 18

4.1. Adopting Peter Drucker’s abandonment .......................................................... 18

4.2. Run a workshop to “post-it” re-engineering month-end reporting processes .... 18

4.3. Introducing daily scrums to the month-end process ......................................... 24

4.4. Introducing a Kanban progress board to the month-end process ..................... 25

4.5. Applying Kaizen to all finance team processes ................................................ 26

5. Major quality assurance tasks after day+1 ............................................................. 28

5.1. Ban all late changes to the month-end report .................................................. 28

5.2. Check numbers for internal consistency .......................................................... 28

5.3. The two person read through ........................................................................... 29

5.4. Text to voice facility ......................................................................................... 29

5.5. The final check for the “two gremlins” .............................................................. 29

6. Further steps you can implement within six months ............................................... 30

This document breaches copyright if it has not been received directly from David Parmenter

Fast Close: A Guide to Rapid Month-End & Year-End Reporting ©2018 Page 3 David Parmenter [email protected] www.davidparmenter.com

6.1. Move to a paperless accounts payable operation ............................................ 30

6.2. Introduce a purchase card for high volume low value transactions .................. 33

6.3. Have a closer relationship with your main suppliers ......................................... 35

6.4. Avoid late time sheets ...................................................................................... 36

6.5. Monthly targets set, a quarter ahead, by a quarterly rolling process ................ 36

6.6. Limit your account codes for the P/L to less than 60 ........................................ 38

6.7. Minimise budget holders’ month-end reporting ................................................ 38

6.8. Avoid rewriting the board report ....................................................................... 39

6.9. Improve budget holders’ co-operation .............................................................. 40

6.10. Close on the same day each month ............................................................... 41

7. Technology you need to embrace .......................................................................... 43

7.1. Banning spreadsheets from core finance routines ........................................... 43

7.2. The technologies you need to understand and evaluate .................................. 45

7.3. Planning and forecasting tools ......................................................................... 46

7.4. Upgrade accounts payable systems ................................................................ 50

7.5. Using a reporting tool ....................................................................................... 52

7.6. Turbo your G/L with a friendly front end ........................................................... 52

7.7. Consolidation and intercompany software ....................................................... 53

7.8. Fast Close Applications ................................................................................... 54

7.9. Collaborative disclosure management ............................................................. 55

7.10. Paperless board meetings ............................................................................. 56

7.11. Project planning software using Trello ........................................................... 57

8. Lean one-page reporting ........................................................................................ 58

8.1. Minimise budget holders’ month-end reporting ................................................ 58

8.2. A3 page summary report for the CEO .............................................................. 58

8.3. A3 dashboard for the Board ............................................................................. 58

8.4. The Toyota A3 investment proposal ................................................................ 63

8.5. Monthly sales report from Stephen Few ........................................................... 63

8.6. More emphasis on daily and weekly reporting ................................................. 64

8.7. Heads up email in week 4 ................................................................................ 69

8.8. Value stream reporting .................................................................................... 70

8.9. Costing of a product group by rate of flow ........................................................ 71

8.10. One off deal analysis using the lean approach ............................................... 72

8.11. Designing graphs by Stephen Few, an expert based in the USA ................... 73

9. Quick annual reporting – within 15 working days post year end! ............................ 75

9.1. The costs of a slow year-end ........................................................................... 75

9.2. Cost to the annual accounts process ............................................................... 75

9.3. A quick year-end is a good year-end ............................................................... 76

This document breaches copyright if it has not been received directly from David Parmenter

Fast Close: A Guide to Rapid Month-End & Year-End Reporting ©2018 Page 4 David Parmenter [email protected] www.davidparmenter.com

9.4. Establish year-end reporting rules within the finance team .............................. 77

9.5. Help get the auditors organised ....................................................................... 78

9.6. Appoint an audit coordinator ............................................................................ 78

9.7. Complete the drafting of the annual report before year-end! ............................ 79

9.8. Set up an “overs and unders” schedule and limit when changes can be made 79

9.9. Negotiate and plan for a sign-off by the auditors within 15 working days! ........ 80

9.10. Have a month 10 or 11 hard close ................................................................. 80

9.11. Effective stock takes ...................................................................................... 80

9.12. Estimating “added value” in WIP and finished goods ..................................... 81

9.13. Effective fixed assets verification ................................................................... 81

9.14. Extract More Value from The Management Letter .......................................... 81

9.15. Derive More Value From The Interim Audit .................................................... 82

9.16. Restrict Access Of Confidential Information To The Audit Partner ................. 82

9.17. Run a workshop to “post-it” re-engineer year-end reporting ........................... 82

9.18. Checklist for speeding-up the annual accounts process ................................. 82

9.19. Data Capture From Reporting Entities ........................................................... 82

9.20. Mapping To Group Systems and Control ....................................................... 83

9.21. “Last Mile” Information Handling .................................................................... 83

10. Selling and leading change ................................................................................. 85

10.1. Steve Zaffron and Dave Logan ...................................................................... 85

10.2. Harry Mills ...................................................................................................... 85

10.3. John Kotter .................................................................................................... 86

10.4. Selling to the senior management team ......................................................... 88

10.5. The elevator speech ...................................................................................... 89

10.6. Deliver a compelling burning platform presentation ........................................ 90

10.7. Pre-selling to an influential member of the decision team .............................. 91

10.8. Practise, practise, practise ............................................................................. 91

11. Immediate Steps ................................................................................................. 92

12. Writer’s biography ............................................................................................... 94

Appendix 1 Month-end reporting checklist ..................................................................... 95

Appendix 2 Draft Set of Month-End Rules for the Finance team .................................... 97

Appendix 3 Useful letters and memos .......................................................................... 100

Appendix 4 Suggested Rules for The Year-End Processes ......................................... 105

Appendix 5 Annual accounts checklist ......................................................................... 108

This document breaches copyright if it has not been received directly from David Parmenter

Fast Close: A Guide to Rapid Month-End & Year-End Reporting ©2018 Page 5 David Parmenter [email protected] www.davidparmenter.com

1. Introduction Is your team one of the many who are sucked-in by processes that have more in common with the Charles Dicken’s era than the 21st century? When I was a corporate accountant each period end was a disaster waiting to happen. Each month-end had a life of its own. You never knew when and where the next problem was going to come from. Always two or three days away we appeared to have it under control and yet each month we were faxing (email was not on the scene then!!) the result five minutes before the deadline. Our fingers were crossed as a series of late adjustments had meant that the quality assurance work we had done was invalid and we did not have the luxury of doing it again. Does this sound familiar?

If so, this white paper will show you a way forward, a pathway blazed by some of your far-seeing peers. This white paper is based on the collective wisdoms of over 2,000 corporate accountants, to them we owe a great gratitude.

How do you fare on these questions?

Does it take longer than three business days for your Finance team to complete the monthly reporting package to the CEO and to the Board?

Yes No

Do your staff burn the midnight oil to achieve this? Yes No

Are you finding that each month-end is a drama? Yes No

Do the monthly reports have a high error rate? Yes No

Do the month-end reports go through endless rewrites? Yes No

Is the month-end reporting process seen as a negative task for staff and management?

Yes No

If you answer “no” to all of these questions you are one of the small minority who have got to grips with timely month-end reporting.

1.1. Importance of abandonment

Management guru Peter Drucker1 who I consider to be the Leonardo de Vinci of management, frequently used the word ‘abandonment’. I think it is one of the top ten gifts Drucker gave us all. He said

“Don’t tell me what you’re doing, tell me what you’ve stopped doing.”

He frequently said that abandonment is the key to innovation, in other words, the key to a fast month-end.

Peter Drucker observed in one organisation that the first Monday of every month is set aside for “abandonment meetings at every management level.” Each session targets a different area so that in the course of a year everything is given the once-over. This process would work well in the finance team except we should meet once a week to discuss at least two abandonments each week!

The act of abandonment gives a tremendous sense of relief to the finance team for it stops the past from haunting the future. It takes courage and conviction from the CFO. Knowing when to abandon and having the courage to do so are

This document breaches copyright if it has not been received directly from David Parmenter

Fast Close: A Guide to Rapid Month-End & Year-End Reporting ©2018 Page 6 David Parmenter [email protected] www.davidparmenter.com

important leadership attributes. In order for these processes in this white paper to work there needs to be an adoption of:

an abandonment of processes and procedures a letting go of the past a commitment to change the rules

1.2. The importance of challenging the status quo

Far too often we have accepted antiquated and anti lean practices within the corporate accounting repertoire as the status quo. If the medical profession used our approach they would probably still be using leeches (well actually they still do I understand in special cases). The medical profession have breakthrough conferences on a regular basis and all the practicing surgeons, in that field attend, and adopt the new procedure. This should be the corporate finance model. The problem with corporate finance is that the surgeon “the CFO” is often too busy to attend, caught in the aforementioned “Catch-22”.

In an interview, called the lost Interview, Steve Jobs, was asked, “As 22-year-old worth $10m, and a 25 year old worth $100m, how did he get his business acumen.” He said that over time he realized that most business was pretty straight forward. He talked about when Apple had their first computerized manufacturing plant for the Apple II and the accountant sent Steve Jobs his first standard costing report.

Jobs asked, “why do we have a standard cost and not an actual cost” The responses was “that just the way it’s done”. He soon realized that the reason was the accounting system. When that was fixed, standard costing reports vanished. In business Jobs believes that few in management thinks deeply about why things are done. He came up with this quote I want to share with you. Your time is limited, so don’t waste it living someone else’s life. Don’t be trapped into living with the results of other people’s thinking. Don’t let the noise of other’s opinions drown your own inner voice” Steve Jobs

1.3. Ranking guide

The following rating scale, see Exhibit 1.1, shows the time frames of month - end reporting across the 5,000 corporate accountants I have presented to in the past 20 years.

Exhibit 1.1: Speed of month-end reporting ranking

Exceptional Outstanding Above average

Average

One working day

Two to three working days

Four working days

Five working days

This document breaches copyright if it has not been received directly from David Parmenter

Fast Close: A Guide to Rapid Month-End & Year-End Reporting ©2018 Page 7 David Parmenter [email protected] www.davidparmenter.com

2. The burning platform There is a burning platform and the finance team needs to jump. Your month-end: Does not create much value the horse has bolted, is part of trifecta of lost

opportunities (the other two activities to re-engineer are annual planning and annual reporting)

Forces you to invest too much time and effort as a processing centre instead of advisory time

Is slower than your peers who are reporting quickly (some are even reporting in one day)

2.1. Benefits of quick monthly reporting to management and the Finance team

As a good friend of mine, who is a CFO of a tertiary institution, said “Every day spent producing reports is a day less spent on analysis and projects”. There are many benefits to management and the Finance team of quick reporting, and these are set out in Exhibit 2.1 below.

Exhibit 2.1: Table of benefits

Benefits to management Benefits to the finance team

Reporting plays a bigger part in the decision - making process.

Staff are more productive as efficiencies are locked in and bottlenecks are tackled.

Reduction in detail and length of reports.

Many month - end traditional processes are out of date and inefficient, and these are removed.

Reduced cost to organization of month - end reporting.

Happier staff with higher morale and increased job satisfaction.

More time spent analyzing trends.

Finance staff focus is now on being a business partner to the budget holder, helping them to shape the future.

More time spent on achieving results.

The team has time to be involved in more rewarding activities, such as quarterly rolling forecasts, project work, and so forth.

Greater budget holder ownership (accruals, variance analysis, coding, corrections during month, better understanding, etc.).

More professionally qualified finance staff.

Less senior management time invested in month - end.

Less senior finance team time invested in month – end the change also leads to a very quick year - end.

This document breaches copyright if it has not been received directly from David Parmenter

Fast Close: A Guide to Rapid Month-End & Year-End Reporting ©2018 Page 8 David Parmenter [email protected] www.davidparmenter.com

2.2. The impact of quick reporting on the Finance team and the organisation

The impact of quick month-end reporting is a redistribution of work moving out of the low value processing activities of month-end, annual accounts to the more future focused activities such as rolling forecasting, systems implementation and advisory, as shown in Exhibit 2.2. This is often accompanied by a change in the mix of the finance team, with a higher percentage of qualified staff, which is good news for qualified accountants.

Exhibit 2.2: Changing the focus of our work

The significance of month-end reporting can be seen from this comparison of three reporting timeframes. Quick reporting accounting teams are far more advanced in many other areas. They should be, as they have much more time on their hands, as shown in Exhibit 2.3.

Exhibit 2.3: Impact of a quick month-ends on a 22 working day month

Non-lean Lean

Advisory

System implementation

Annual budgeting and

planning

System implementation, adoption of new lean processes

Rolling forecasting &

planningMonth-end and annual

reporting Month-end and annual

reporting

Advisory

wor

king

hou

rs

75%

fut

ure

focu

s

Tasks Day 1 Quick m/e Slow m/e

Month-end reporting 1 4 9

Remaining days 21 18 13

Percentage of extra time for project work & daily routines

60% more time

40% more time

Based on a 22 working day month

No. of working days a month

This document breaches copyright if it has not been received directly from David Parmenter

Fast Close: A Guide to Rapid Month-End & Year-End Reporting ©2018 Page 9 David Parmenter [email protected] www.davidparmenter.com

3. Lean best practice for your next month-end

3.1. Get the CEO supporting fast month-end reporting

It is important to get the CEO behind a fast month-end. You start by costing out to management and the Board the month-end reporting process.

Such an analysis can be easily performed by a management accountant in 30 minutes, and will be valuable in the sale process of changing month-end reporting time frames.

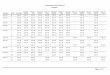

Exhibit 3.1 Shows the time invested in an organisation with 40 budget holders with around 500 full time staff. The cost estimate is between £0.6m to £1m.

Exhibit 3.1 Costing out the current month-end reporting process

When doing this exercise, remember that senior management barely have 32 weeks of productive time when you remove holidays, sick leave, travelling time,

Accounting team

BHs Direct reports

SMT

Accounts payable cut-offAccounts receivable cut-offCapex, inventory etcAccrualsAdjustmentsFirst run of GL 2 to 3 Researching variances by staff 0.5Drafting papers 0.5 to 1 0.5 to 1Flash reportReview and redrafting 0.5 to 1 0.5Second run of GLPreparing consolidated accounts commentary 2 to 3 Review by CFO and Financial Controller 0.5 to 1Presentation to SMT (senior management team) 0.5 to 1

5.5 to 9 1.5 to 2 0.5 to 140 budget holder reports 60 to 80100 direct reports reporting progress by way of a written monthly report

50 to 100

Board papersPreparing board financial report 2 to 3 1 to 1.5Review reports before they go to BoardPreparing business unit progress reports to the Board

4 to 6

Review by CEO 0.5 to 1Preparing one-off board reports 10 to 20 6 to 10

Working days per month 7.5 to 12 70 to 100 50 to 100 11.5 to 18.5

Average salary cost $65,000 $80,000 $55,000 $200,000Average productive weeks 42 42 42 32

Low High

Average personnel cost $600,000 $1,100,000

Consultants reports $100,000 $200,000

Estimated annual cost of monthly reporting to managers, SMT and Board

$700,000 $1,300,000

500 FTE organisation with monthly management and Board reports

This document breaches copyright if it has not been received directly from David Parmenter

Fast Close: A Guide to Rapid Month-End & Year-End Reporting ©2018 Page 10 David Parmenter [email protected] www.davidparmenter.com

and routine management meetings. Thus a cost of £800-£1,000 per senior management day is not unrealistic. The Excel on which this costing was based is available to all readers of this white paper.

Having performed the calculation I would then approach the CEO with a 30 second elevator speech to catch their attention.

“We have just done some calculations that estimate that we will spend between £8m-£10m over the next 10 years reporting monthly results well and truly after the ‘horse has bolted’. I want to undertake a project to speed up month-end reporting, giving you access to numbers inside three working days and saving over £5m in the next ten years. Could I have 15 minutes of your time to outline the project, its benefits and your role in helping make it happen?”

There is not a CEO on this planet who will not say “I am with you, how can I assist?” Many things happen with the CEO’s total co-operation. All communiqués about changes to processes or requests to attend training sessions on the new regime should be sent out by the CEO instead of by the finance team.

Major breaches of procedures should be listed weekly (invoices over £10,000 with no raised order, no receipting of receipt of goods and services over £10,000, budget holders with over three months of outstanding purchase card receipts etc) and the CEO asked to phone the culprits and give a one-minute reprimand making it clear that full cooperation is expected and non-compliance will be career limiting.

3.2. Establish month-end reporting rules within the finance team

I always point out to accountants that we are all artists. Every month we sculpt a month-end result and it can never be the right number, as there is no such thing as a ‘right’ number, it can only be a “true and fair “number. If 10 accounting teams prepared the month-end numbers for one company for five years there would be 10 different results each month. Each accounting team will have made different judgement calls, yet over the five years the cumulative result will be very similar.

The finance team has to realise that they only need to do enough work to arrive at a ‘true and fair’ view. All work done after this point that has been reached will thus not be adding value. We therefore need some rules that the month-end financial report should: not be delayed for detail be consistent between months, e.g., same judgment calls, same format be a true and fair view and error free e.g. hunting for the perfect number is

now unacceptable and the final report will have extensive quality assurance checks to ensure it is free from any report writing errors

be concise - less than a 10-page finance pack e.g., only include a one-page report on each major business with minor businesses being reviewed by the CFO and omitted from the pack

be a merging of numbers, trend graphs and bullet point comments all on one page

Not be changed for adjustments that are likely to be set off by others yet to be found - allowing adjustments to offset each other on an “overs and unders” schedule

See Appendix 2 for the draft set of rules I have prepared for your finance team. These rules are also in the accompanying electronic media.

This document breaches copyright if it has not been received directly from David Parmenter

Fast Close: A Guide to Rapid Month-End & Year-End Reporting ©2018 Page 11 David Parmenter [email protected] www.davidparmenter.com

3.3. Catch all adjustments in an ‘overs and unders' schedule

Month-end reporting is not the time for spring cleaning no matter how tempting it can be. This requires a re-education within the finance team and with budget holders.

All miscoding, unless resulting in a material misstatement of the P/L, are processed during the following month. Budget holders are educated to review their cost centre numbers via on-line access to the G/L during the month and are requested to highlight any discrepancies immediately with the finance team.

We want to have a regime where we catch all material adjustments and see the net result of them before any decision is made to adjust e.g. only a material month-end misstatement will result in processing an adjustment. Set up two ‘overs and unders’ spreadsheets, see Exhibit 3.2, at the close of the last working day. One spreadsheet is to trap major adjustments, say over £5,000, £20,000 or £50,000 depending on the size of the organisation, and the other for smaller items. If they find adjustments, the accountants will enter them on the appropriate spreadsheets that reside on a shared drive on the local area network. More often than not you will note that adjustments have a tendency to net each other off.

If there is a material misstatement of the net result we will process one or two appropriate adjustments and then remove them from this schedule. This will bring the total of the overs and unders to an acceptable figure. We then process all the other adjustments during the quiet time in the following mid-month

Exhibit 3.2: Maintaining an ‘overs and unders’ schedule

3.4. Avoid a huge wave of AP invoices at month-end

The last thing the AP team needs is to receive a tsunami of invoices on the last day of cut-off, as shown in Exhibit 3.3. It is important to push processing back from month-end by avoiding a payment run at month-end. It is a better practice is to have weekly or daily direct credit payment runs with none happening within the last and first two days of month-end.

Source Raised by JV #

Dr Cr Dr Crxxxxx Pat 1 Dr xxxxxxxxx xxxxx xxxx 45

Cr xxxx xxxxx xxxxx 45

xxxxx John 2 Dr xxxx xxxx 10Cr xx x x xxxxxxxxx 10

xxxxx Jean 3 Dr xxxx xxxx 25Cr xx x x xxxxxxxxx 25

xxxxx Dave 4 Dr xxxx xxxx 15Cr xx x x xxxxxxxxx 15

etc80 70-70

Net impact on P/L 10

P/L impact B/S impactAdjustment

This document breaches copyright if it has not been received directly from David Parmenter

Fast Close: A Guide to Rapid Month-End & Year-End Reporting ©2018 Page 18 David Parmenter [email protected] www.davidparmenter.com

4. Winning agile practices to improve month-end There are five agile techniques to adopt for this month-end.

4.1. Adopting Peter Drucker’s abandonment

As mentioned abandonment needs to be incorporated into this process. Common abandonments include: Spring cleaning at month-end Supplier reconciliations Small accruals Delayed cut-offs Large spreadsheets Endless small adjustments

4.2. Run a workshop to “post-it” re-engineering month-end reporting processes

This can be a complex and expensive task or a relatively easy one, the choice is yours. Many organisations start off by bringing in consultants to process map the existing procedures. This is a futile exercise as why spend a lot of money documenting a process you are about to radically alter and when it is done only the consultants will understand the resulting data-flow diagrams.

The answer is to “Post-it” re-engineer your month-end procedures in an in-workshop.

There are seven stages.

Stage 1 Invitation

Having set the date, get the CEO on board and ask them to send out the invites, see Appendix 3 for a draft. The finance team needs to send out instructions, a week or so prior workshop, outlining how each team is to prepare their post-it stickers, see Exhibit 4.1.

Suggested attendees include all those involved in month-end including accounts payable, financial and management accountants, representatives from teams interface with month-end routines, e.g. someone from IT, payroll etc)

This document breaches copyright if it has not been received directly from David Parmenter

Fast Close: A Guide to Rapid Month-End & Year-End Reporting ©2018 Page 28 David Parmenter [email protected] www.davidparmenter.com

5. Major quality assurance tasks after day+1 When the flash report is done and has been discussed with the CEO, we need to focus on the reporting back. The important issue to remember here is that the month-end can never be right; it can only be a true and fair view.

5.1. Ban all late changes to the month-end report

Once the flash report has been issued, at the close of business on the first working day, teams should continue with recording any adjustment found in the relevant “ overs and unders ” spreadsheet.

No changes are permitted to the numbers reported in the flash report until the entire review has been completed. The accounting team can then assess which adjustments are worthy of processing. As many have no P & L impact, they would be held back for adjustment in the following month.

Once the reporting pack is prepared, no adjustments are allowed unless they are very material. There is nothing worse for the finance team than to submit a finance report to the CEO that is inconsistent. This is frequently caused by a late change not being processed properly through the report. As night follows day, the CEO will be sure to find it. I am sure many readers have been guilty of this one.

It is far better to hold back the adjustments. If the CEO says to you, “I thought the sales were higher, ” you can say, “ Pat, it is a pleasure working for such an astute CEO. You are right, the sales are understated by $30,000; however, there are adjustments totalling $27,000 going the opposite way, so I have not booked the adjustments as the net difference is immaterial. I am booking these through this month. However, if you like I will adjust this month’s report. ” Most CEOs will feel pleased with themselves for spotting the shortfall and then move on to another issue.

5.2. Check numbers for internal consistency

Mark all pages with a number, e.g., for a five page report mark 1 of 5, 2 of 5, see Exhibit 5.1. For every number that appears elsewhere, either in a box, table or graph write the page reference where it appears again, by the page number, and initial to indicate that you have checked this number in the subsequent page and it is right.

Exhibit 5.1: Checking for consistency

This document breaches copyright if it has not been received directly from David Parmenter

Fast Close: A Guide to Rapid Month-End & Year-End Reporting ©2018 Page 30 David Parmenter [email protected] www.davidparmenter.com

6. Further steps you can implement within six months

6.1. Move to a paperless accounts payable operation

Many accounts payable processing procedures are more akin to the Charles Dickens era than the 21st century. Why do we go from an electronic transaction in the suppliers accounting system to a Charles Dickens paper based invoice? Surely we should be able to change this easily with our major suppliers.

Many American multinationals have achieved this already. It requires an investment, skilled A/P staff and retraining of the budget holders. The rewards are immense. To appreciate the benefits I suggest the A/P team regularly visit www.theaccountspayablenetwork.com website of The Accounts Payable Network.

There have been major advancements in technology for accounts payable teams. The return on investment in AP technology is, I believe, greater than any other equivalent investment in other service departments within a business. Why then are some AP teams so under invested? I believe it is due to:

Lack of understanding by the CFO of the technologies and their benefits The AP team not researching the AP technologies Poor selling of the AP technologies to the executive team

It is safe to say that there is a technology suitable for SMEs and large enterprises that will make them paperless. In a recent study the winds of change were shown in Exhibits 6.1 & 6.2. As can be seen, if you are not using electronic payments and purchasing cards you are already behind the eight ball.

Exhibit 6.1: Technology in use or planned to be in use in next six months

Source: Automating Payables for the SME market – A Big bang for the Buck PayStream Advisors 2015

This document breaches copyright if it has not been received directly from David Parmenter

Fast Close: A Guide to Rapid Month-End & Year-End Reporting ©2018 Page 31 David Parmenter [email protected] www.davidparmenter.com

Exhibit 6.2: The major components of payables automation

Source: Automating Payables for the SME market – A Big bang for the Buck PayStream Advisors 2015

This document breaches copyright if it has not been received directly from David Parmenter

Fast Close: A Guide to Rapid Month-End & Year-End Reporting ©2018 Page 32 David Parmenter [email protected] www.davidparmenter.com

In their paper Paystream Advisors point out:

Once an invoice or other payables data is captured electronically, the question to ask is: Does this invoice need to be approved? The ability to derive an automated answer by using business rules, which in turn trigger appropriate workflows, is the centrepiece of an automated AP environment. If the answer to the question is no, the system will move the invoice into the payment process. If the answer is yes, the system will route it to the approving party along with any necessary decision support documents and information. Business rules, flexible workflow and transactional transparency are essential.2

Here are some of the ways to work towards a paperless accounts payable function.

Electronic ordering system

Most accounting systems come with an integrated purchase order system. Getting the electronic ordering system to work effectively is a major exercise, and one that should be researched immediately. There will be an organization that uses the same accounting system and where the purchase order system is working well. Visit that organization and learn how to implement the system.

Purchase card Introduce the purchase card to all staff with delegated authority so all small value items can be purchased through the purchase card thereby saving thousands of hours of processing time by both budget holders and the accounts payable teams, see separate purchase card section below.

Electronic supplier feeds

Invest in liaison time with all major suppliers to organise electronic feeds of the invoices which will include the general ledger account codes – this requires liaison between the two IT teams, yours and the suppliers!

Web based expense claim

Acquire an integrated web based expense claim system so employees, wherever they are, can process their claims. These systems are now linked to the user’s mobile phone so pictures of the transaction dockets are photographed and uploaded into the system, doing away with the requirement that all expense receipts are to be sent to, and stored by, the AP team. Some purchase cards can also accommodate cash expense items.

Eliminate all cheques

Eliminate all cheque payments, framing the last cheque on the CEO’s wall. With a plaque saying, “This is the last check and is a symbol of our drive to end all Charles Dickens processes.” The CEO will

This document breaches copyright if it has not been received directly from David Parmenter

Fast Close: A Guide to Rapid Month-End & Year-End Reporting ©2018 Page 52 David Parmenter [email protected] www.davidparmenter.com

7.5. Using a reporting tool

The advancement of reporting tools has meant that the G/L is used merely as a collecting area for financial data for the month. A better practice today is to have a reporting tool collect this data from the G/L overnight, or in some cases weekly, so that the budget holders can drill into their revenues and costs during the month. Management accountants also will use this reporting tool when analyzing costs because it contains prior months’ figures in a continuous stream, enabling them to do cross - year financial comparisons seamlessly. Exhibit 7.3 outlines some reporting tools offered by application providers.

Excel has no place as a reporting tool. Again, it is too prone to disaster. There is no problem where the system automatically downloads to Excel, with all the programming logic being resident in the system and basically bombproof. The problem arises when the system has been built in - house, often by someone who has now left the company, with the accuracy of formatting the G/L download relying on Excel formulas reading the imported file. This is simply a disaster waiting to happen.

Exhibit 7.3 Reporting Tools Offered By Application Providers

Reporting Tool Suppliers Website

Caspio www.caspio.com

Combit Software www.combit.net

Devexpress www.devexpress.com

Dundas Data Visualization www.dundas.com

Qlikview www.Qlik.com

Megalytic www.megalytic.com

Phocas www.phocassoftware.com

Power BI Powerbi.microsoft.com

SAP BusinessObjects www.sap.com

SAP Crystal Reports www.sap.com

Sisense.com www.sisense.com

Spotlightreporting.com/ www.spotlightreporting.com

SQL Server Reporting Services www.msdn.microsoft.com

Tableau www.tableau.com

Targit.com www.targit.com

7.6. Turbo your G/L with a friendly front end

It is important that budget holders take ownership of their part of the G/L. To this end we need to offer them a user - friendly interface to their part of the G/L. There are a number of tools that can make an old G/L feel like a 21st - century version. In Exhibit 7.4 I have outlined some front-end tools for General ledgers.

This document breaches copyright if it has not been received directly from David Parmenter

Fast Close: A Guide to Rapid Month-End & Year-End Reporting ©2018 Page 53 David Parmenter [email protected] www.davidparmenter.com

Companies are reporting that they have had great success by downloading transactions (daily or weekly) from the G/L into these drill-down tools, allowing read - only access to budget holders.

With a drill-down tool, budget holders never look at the G/L. Management accountants and budget holders also will use this reporting tool when analyzing costs. The drill-down tool offers trend analysis that transcends the year - end, enabling budget holders to look at the last 18-or 24-month trend seamlessly.

A byproduct of these reporting tools is that CFOs are now questioning why they need to invest in the first-tier accounting systems. In Australia, one CFO is running the G/L of an organization with 400 full-time employees on the mind-your-own-business (MYOB) accounting G/L. As he said, “Why invest thousands when all the G/L does is to hold the historic numbers and only a couple of accountants access it? In our company, all the reporting against budget and drill-down access used by budget holders is performed in auxiliary systems.”

Exhibit 7.4 Front-end tools for general ledgers

Supplier Website

AccountMate Software Corporation

www.accountmate.com/source.asp

Combit www.combit.net

Infor F9 www.infor.com

Praxinet Drillanywhere www.praxinet.com

SQL Power Group www.sqlpower.ca/

7.7. Consolidation and intercompany software

Performing a consolidation in a spreadsheet is inappropriate, or put more bluntly, is stupid. There are now excellent systems that organize this for you and enable the subsidiaries to have their own general ledger and account code structure. Their trail balance is simply mapped into the consolidated entity’s account codes. An exploration of any search engine will also find some freeware, robust older versions available at no cost. Try this search consolidation+software. Using this search I soon found the solutions outlined in Exhibit 7.5.

Exhibit 7.5 Consolidation tool offerings

Supplier Website

Adaptive Consolidation www.adaptiveinsights.com

BlackLine Consolidation Integrity Manager www.blackline.com

Board International www.board.com

Host Analytics Inc hwww.hostanalytics.com

Hyperion Financial Management www.oracle.com

Intacct www.intacct.com

Mona Group Reporting www.sigmaconso.com

Netsuite www.netsuite.com

This document breaches copyright if it has not been received directly from David Parmenter

Fast Close: A Guide to Rapid Month-End & Year-End Reporting ©2018 Page 75 David Parmenter [email protected] www.davidparmenter.com

9. Quick annual reporting – within 15 working days post year end!

The annual reporting activity is part of the “trifecta” of lost opportunities. Whilst annual reporting is an important legal requirement, it does not create any value within your organisation and thus seldom is it a task where your team has received any form of gratitude. Accounting functions therefore need to find ways to extract value from the process while, at the same time, bringing it down into a tight time-frame.

Before you can have a quick year-end you need to speed up month-end reporting so staff are disciplined to a tight month-end. Your goal should be reporting numbers and comments by Day Three, see earlier section on quick month-end reporting.

9.1. The costs of a slow year-end

The costs of a slow year-end include: Months where the accounting team are simply doing annual and monthly

reporting – thus little added value is created by the finance team in that time period.

Too much time goes into the annual report as we lose sight of Pareto’s 80/20 Little or no client management during this time and thus bad habits are picked

up by budget holders

“Accounting teams are often hijacked by the annual reporting process”

Quote from a CFO with blue chip international experience

“Given the amount of time this activity takes, the 80/20 rule still applies. Most organisations look at the annual report financials as being “special” numbers that they have reworked many times. There is absolutely no reason, in 99% of the cases, why the “first cut” of year-end for internal reporting should not be the same as the last cut for external reporting. Most adjustments are trivial and result in printing delays. The annual report comes out so late virtually nobody reads it anyway!”

Quote from a CFO with blue chip international experience

There are many ways in which we can improve the way we do year-end, and they can all be grouped around three words, organisation, communication and pre-work. Organisation - establishing an audit coordinator, the working paper files, the

deadlines etc. Communication - communicating with both the auditors and staff Pre year-end work – bring forward many year-end routines earlier, such as

cutting off at month 10 or 11 and rolling forward. This also includes preparing a comprehensive auditors’ file, saving the audit team considerable audit time.

9.2. Cost to the annual accounts process

In order to create a change in the way the SMT, Board and management address the annual accounts you need to establish what is the full cost of the annual accounts process including all Board, management and staff time and all those external costs (audit fees, printing costs, PR and legal fees etc).

This document breaches copyright if it has not been received directly from David Parmenter

Fast Close: A Guide to Rapid Month-End & Year-End Reporting ©2018 Page 76 David Parmenter [email protected] www.davidparmenter.com

Exhibit 9.1 Shows how to calculate the costs of an annual accounts process. The times are estimates and show what a 300-to-500 full-time employee (FTE) public company may be investing in their annual report preparation. It does not include investor relations and so forth. The senior management team (SMT) has lower productive weeks in a year because you have to take out, in addition to holidays, training, and sick leave, the time they spend travelling and in general meetings.

Exhibit 9.1: Cost of the annual accounts process

9.3. A quick year-end is a good year-end

A fast year-end involves all business units within the group playing ‘the same score’. At site level, top performers are managing a close within 4 elapsed days as shown in exhibit 1.4.

Exhibit 1.4 annual close at site level ( Source: APQC)

In the US companies for a long time have been achieving very fast audited account deadlines. With great team work between the finance team and the auditors reported results inside 20 elapsed days post year end have been achieved. The following companies are famed for this achievement: Cisco Dell Computers Hewlett-Packard IBM Motorola

Accounting team

BHs SMT

Liaison with auditors throughout audit 3 to 5 1 to 2Planning audit 1 to 3Interim audit assistance 4 to 6 20 to 40Preparing annual accounts 2 to 5 Preparing audit schedules 2 to 5 Extra work finalising year-end numbers 20 to 30Final audit visit assistance 10 to 20 20 to 40Finalising annual report 10 to 20 5 to 8

Total weeks of effort 52 to 94 40 to 80 6 to 10Average salary cost $80,000 $55,000 $200,000Average productive weeks 42 42 32

Low HighAverage personnel cost $190,000 $350,000Printing costs 45,000 75,000Audit Fees 45,000 65,000Estimated cost $280,000 $490,000

This document breaches copyright if it has not been received directly from David Parmenter

Fast Close: A Guide to Rapid Month-End & Year-End Reporting ©2018 Page 77 David Parmenter [email protected] www.davidparmenter.com

General Electric

Compare this with the best in the UK where Imperial tobacco manage their audited year-end in 32 elapsed days (over 60% more time).

In addition to being quicker, the Hackett Group's studies show that world-class companies spend 45% less on their closing and reporting efforts than other companies, which the Hackett Group states saves, on average, $US5.5 million per $US1 billion in revenue. These savings come largely from needing fewer people and systems to scrub data.

Another benefit these organizations get is better compliance. PricewaterhouseCoopers report that “Consistent, self-auditing processes help companies more easily conform to regulatory mandates such as Sarbanes-Oxley by reducing the risk of errors”.

Exhibit 9.2 shows a rating scale for the timeframe to have an audited and signed annual report (time from year-end date).

Exhibit 9.2 year-end reporting timeframes (from the year-end to signed annual report)

Exceptional Outstanding Above average

Average

Less than 15 elapsed days

15-25 elapsed days

26-35 elapsed days

36-45 elapsed

days

Many top American companies report very quickly to the stock exchange, in my days as an auditor IBM was well known for its speed of reporting.

There are a number of benefits of a quick year-end and these include:

better value from the interim and final audit visits improved data quality through improved processing reduced costs of both the audit and accounting teams time more time for finance staff to devote to critical activities such as analysis,

decision-making and forecasting improved investor relations

“A fast close builds investor confidence. Investors are right to make the inference, that if the close is slow it means processes are broken. And if the processes are broken, chances are the data is broken.”

Source CIO

9.4. Establish year-end reporting rules within the finance team

I always point out to accountants that we are all artists. Each year-end we sculpt the result and it can never be the right number, as there is no such thing as a ‘right’ number, it can only be a “true and fair “number. If ten accounting teams prepared the year-end numbers for one company there would be ten different results. Each accounting team will have made different judgement calls, different calls on materiality, accruals and accounting treatments.

The finance team has to realise that they only need to do enough work to arrive at a ‘true and fair’ view. All work done after this point has been reached will thus not be adding value. We therefore need some rules that the year-end reporting (YER) should adhere to. YER should not be delayed for detail

This document breaches copyright if it has not been received directly from David Parmenter

Fast Close: A Guide to Rapid Month-End & Year-End Reporting ©2018 Page 78 David Parmenter [email protected] www.davidparmenter.com

Month 12 numbers are the year end numbers YER can only be a true and fair view e.g. hunting for the perfect number is

now unacceptable. The final year-end report will have extensive quality assurance checks to

ensure it is free from any report writing errors Ban spring cleaning at year-end and allow adjustments offset each other

“overs and unders” Spreadsheets will not be used for key routines, such as the consolidation

Year-end reporting is not the time for spring cleaning no matter how tempting it can be. This requires a re-education within the finance team and with budget holders.

We want to have a regime where we catch all material adjustments and see the net result of them before any decision is made to adjust e.g. only a material month-end misstatement will result in processing an adjustment.

See Appendix 4 for a draft finance team rules for you and these are in the accompanying electronic media.

9.5. Help get the auditors organised

An audit can very easily get disorganised. The audit firm will more than likely have a change in either the audit senior or audit staff, and their first year staff will know little about what they are trying to audit, no matter what training they have had.

So, in order to aid the audit team, it is beneficial for both parties to: Allocate appropriate facilities for the audit room (desks, phones, security) Provide an induction session for new audit staff as up to 40% of junior audit

time is wasted in an unknown environment Prepare a financial statement file and hand it over on day one of the final visit

( this file will contain papers supporting all numbers in the financial statements, including completed audit lead schedules ready for their papers, 12 months of monthly reports etc.)

Advise staff to assist the auditors and having a specific person in every section who should be contacted in first instance should the auditors need further explanation

Hold meetings at key times with the auditors e.g. the planning meeting, the interim meeting and the meetings to discuss the final results.

9.6. Appoint an audit coordinator

The first step to improving communication between staff and the audit team is to have a full time audit coordinator. This person should be a staff member, not necessarily in finance, who knows most people in the company and knows where everything is, in other words “an oracle”.

You may find the ideal person is someone in accounts payable or someone who has recently retired. The important point is that they should have no other duties during the audit visits (both interim and final visits) other than helping the audit team. Give them an agreeable room and say “When not helping the audit team you can simply put your feet up.” Do not get tempted to give them additional duties. Their tasks include: Providing an induction session for new audit staff Gathering any vouchers and so forth that the auditors need

This document breaches copyright if it has not been received directly from David Parmenter

Fast Close: A Guide to Rapid Month-End & Year-End Reporting ©2018 Page 79 David Parmenter [email protected] www.davidparmenter.com

Responding to information requests the auditors have made that are still outstanding

Setting up designated contact points in every function (e.g., who to speak to in the marketing department)

Organising meetings with the designated person in the section they need to visit

Arranging meetings at key times between CFO and the auditors.

9.7. Complete the drafting of the annual report before year-end!

It is desirable to complete the annual report, other than the final year’s result, by the middle of month 12. This will require co-ordination with the PR consultant who drafts the written commentary in the annual accounts, discussions with the Chairman of the Board and with the CEO. Your last month’s numbers will not greatly impact the commentary!!

Also remember that nobody, I mean nobody reads the annual report. If you are a public listed company, the stock broker analysts rely on the more in-depth briefing you give them, shareholders in the main do not understand them, and the accounting profession just skim them.

9.8. Set up an “overs and unders” schedule and limit when changes can be made

Year-end is not a time for spring cleaning. We will apply the rules already mentioned. We will make the month 12 numbers the final – year numbers. The “overs and unders” schedule as shown in Exhibit 3.1, will be maintained, and we will record any major adjustments on this schedule. When the auditors arrive we had over the schedule and ask that it now contain all their and any other subsequent ones we find.

You will often find that adjustments have a tendency to offset each other. If the auditors find a major adjustment, look in the opposite direction and you no doubt will find another to offset it.

The changes for year-end should be as follows:

Stage 1: Close of first working day (part of preparing the flash report for month 12)

Stage 2: Day 3 when we finally issue month 12 results Stage 3: The morning when final audit starts so auditors have the bottom line

number Stage 4: Final Tax entries Stage 5: Final audit agreement

This document breaches copyright if it has not been received directly from David Parmenter

Fast Close: A Guide to Rapid Month-End & Year-End Reporting ©2018 Page 95 David Parmenter [email protected] www.davidparmenter.com

Appendix 1 Month-end reporting checklist There are a wide range of steps that can be taken for tackling month-end processing. The following checklist allows you to see if you are utilizing all of them.

Key Task Tick if covered

All management aware of the problem with a slow m/e Yes No

Buy-in obtained from CEO and senior management team (SMT)

Yes No

Have held a “post-its” re-engineering workshop where all relevant people have attended .

Yes No

Adopted Scrum and Kanban agile techniques. Yes No

Mandate made by SMT that all service operations are to adhere to new deadlines issued by the QMERT .

Yes No

Rigorously apply the Pareto principle (80/20), focusing on the big numbers and establish materiality levels ( e.g., >$_____ for any debit entry in an accrual list, >$____ for any accrual total from a department etc) .

Yes No

Manual journal entry line items reduced by over 50% (80% has been achieved).

Yes No

Eliminated all interdepartmental corrections at m/e. Yes No

Eliminated management review of budget holder’s numbers as budget holders now have responsibility to resolve issues.

Yes No

Estimates used to avoid slowing down process. Yes No

Eliminated all spreadsheets over 100 rows from month-end Yes No

Set up an “overs and unders” schedule to catch material adjustments (this allows the natural set-off to occur reducing the processed adjustments). Only process those that lead to a material misstatement

Yes No

Set up an “overs and unders” schedule to catch minor errors. Do not post these. Simply investigate reasons and give training so they will not happen again.

Yes No

Budget holders tracked activity throughout the month eliminating the usual surprises found during the close process.

Yes No

Allocations, if used, are now processed without seeing departmental spending.

Yes No

Preparations for m/e close moved before period end instead of after.

Yes No

Moved all month-end cut-offs to the last working day (Day -One) or the day preceding day (Day-Two) (e.g., AP cut-off, accruals cut-off).

Yes No

Developed concise one page reports. Yes No

This document breaches copyright if it has not been received directly from David Parmenter

Fast Close: A Guide to Rapid Month-End & Year-End Reporting ©2018 Page 96 David Parmenter [email protected] www.davidparmenter.com

All key systems upgraded to be on-line real time. Yes No

Removed duplicate data entry. Yes No

Ceased to perform reconciliations of suppliers’ statements Yes No

Management accountants assigned to budget holders. Yes No

Closing-off capital projects one week before month-end. Yes No

In last week only essential operating entries are processed. Yes No

Issuing a flash report by end of first working day. Yes No

Final number and commentary ready by at least close of business Day Three.

Yes No

Bring management meetings to the third working day after month end, effectively locking in the benefit.

Yes No

Adopted a continual focus on process improvement e.g. every month some new change is implemented to improve processing by adopting Kaizen meetings

Yes No

Set up league tables allowing natural competition between sectors to reduce errors (nobody likes being on the bottom).

Yes No

Set up listings of process breaches for the CEO to follow-up with errant budget holders.

Yes No

Started counting errors e.g. Motorola went from 10k errors for 700,000 to 1000 per 2m events

Yes No

Using a consolidation tool rather than Excel Yes No

Map different chart of accounts to a consolidated summary set in the consolidation tool (thus allowing subsidiaries to keep their own accounting systems and chart of accounts)

Yes No

Closing on the same day each month (4,4,5 reporting periods per quarter).

Yes No

Pushing processing back from month end by avoiding having payment runs, inter-company adjustments etc. at month-end.

Yes No

Re-focus of “variance to budget” reporting to YTD variances which are more stable, or better still to latest forecast for the month.

Yes No

Limit budget holder’s reports to one page (about ten lines of numbers, a couple of graphs and a third of a page for commentary).

Yes No

Banned all late changes to the reports once the flash report has been sent to the CEO unless a material misstatement.

Yes No

Performing a call through on the final report. One person reads the report out aloud to another person who is reading it simultaneously. This will help find all grammatical and spelling errors.

Yes No

Letting the financial report, written by the management accountant, go unaltered to the CEO and the Board.

Yes No

This document breaches copyright if it has not been received directly from David Parmenter

Fast Close: A Guide to Rapid Month-End & Year-End Reporting ©2018 Page 97 David Parmenter [email protected] www.davidparmenter.com

Appendix 2 Draft Set of Month-End Rules for the Finance team Based on better practice from around the world our finance team is going to complete its month-end reporting radically quicker. Instead of reporting in ____ days to the CEO we are targeting ___ days next month.

This change is only possible when we adopt new practices and discard processes that are broken, time consuming and of questionable benefit. We need as Peter Drucker preached, to embrace “Abandonment”.

As an accountants are all artists: we sculpt a month-end result and there is no such thing as a ‘right’ number, only a ‘true and fair ‘number. The finance team need only do enough to arrive at a ‘true and fair’ view. All work done after this point has been reached will thus not be adding value. The new rules for the finance team during month-end reporting are:

We will not delay for detail. If we have not got a final number by the last working day we will estimate, or cut-off the last days transactions and include them in the next month’s activities.

Materiality for a misstatement to any month-end result is ______. To this end we need to limit the number of journals posted as many are immaterial. From now on I propose that :

o no department is to raise accruals if the total accrual is less than ________

o no one debit in an accrual listing can be for less than _______

o no journal voucher is to be raised at month-end for less than _______

There is a ban on spring cleaning at month-end. Month-end reporting is not the time for spring cleaning no matter how tempting it can be. All miscoding, unless resulting in a material misstatement of the P/L, are processed during the following month. Budget holders are to be educated to review their cost centre numbers via on-line access to the G/L during the month and are requested to highlight any discrepancies immediately with the finance team.

We want to have a regime where we catch all material adjustments and see the net result of them before any decision is made to adjust. All adjustments are to be processed first on two ‘overs and unders’ spreadsheets, see Exhibit 1, at the close of the last working day. One to trap major adjustments, say over ______, and one for smaller items. If we find adjustments we are to enter them on the appropriate spreadsheets that reside on a shared drive on the local area network. I am expecting that the adjustments will have a tendency to net each other off.

If there is a material misstatement of the net result we will process one or two appropriate adjustments and then remove them from this schedule. This will bring the total of the overs and unders to an acceptable figure. We then process all the other adjustments during the quiet time in the following mid month.