Embed Size (px)

Citation preview

Long Term Financing

of the European

Economy

HyperVolatility

Do not limit your risk, trade it

1 | P a g e

1) Do you agree with the analysis out above regarding the

supply and characteristics of long term financing?

1.b) Generally speaking, the introductory part of the green paper presents and

defines long – term financing in a satisfactory manner. Nevertheless, terms such

as economic and social infrastructures should have been defined with more

accuracy in order to provide the reader with a more tangible and concrete

understanding of what falls under those definitions. Furthermore, short – lived

capital goods such as computers, mobile phones or vehicles are becoming far

more important to companies’ growth than the traditional long term – lived

capital goods. The reason the second category will, in all likelihood, overtakes

the second one lies in the fact that computers, mobile phones and short – lived

technology based capital goods are re – shaping the market. Specifically,

economic and social infrastructures need a lot of time before being implemented

because the financing of such activities is often in the hands of governments or

local authorities which are far from being time efficient entities. The education

and innovation industries have been irremediably re – configured by computers

and mobile phones or technology in general, in fact, many universities or high

education providers have been forced to offer web – based courses in order to

address the increased demand for online knowledge. On the other hand, the car

industry will probably see an irreversible decline since practices such as car

sharing are becoming a lot more popular amongst individuals (particularly those

below 35 years old) who have no longer access to stable jobs or decent salaries.

It is important to point out that, given the current economic conditions, cars

should not be considered short – lived goods anymore. If we consider that

people in the 28 – 35 age interval will soon become the engine of the actual

economy is not difficult to figure out that their precarious conditions will

remarkably affect the car industry. An article of the Guardian newspaper dated

18th of June 2013 reports the following: “The slump in European car sales has

2 | P a g e

reached a fresh nadir with the worst figures for May in 20 years, eroding

manufacturers' faint hopes of a recovery after more than five years of decline.

The European Automobile Manufacturers' Association said demand for new

cars in the European Union was down 5.9% on the same month last year. Just

over a million cars were registered in the lowest total since 1993 – a blow to the

industry after a slight, unexpected upturn in April.

Amid negative economic growth across the Euro–zone, France, Germany and

Italy all showed big declines in sales, with only the UK among the largest

national markets bucking that trend. British car sales rose 11% in May.

Car manufacturers have been struggling with ever more consumers unwilling or

unable to afford new vehicles as unemployment rises. Several manufacturers

have announced factory closures or deferred launching new models”. The next

chart (source: Automotive News) displays fairly well the worldwide scenario

for the car industry:

3 | P a g e

The housing market is definitely not in better shape so even the construction

industry is suffering from the tight economic conditions. House sharing is

becoming the most popular choice for many individuals because difficulties in

obtaining mortgages are forcing many people and families to adopt alternative

lifestyle options. The next chart (source: Knight Frank Residential Research)

shows the trend in the housing industry worldwide:

4 | P a g e

The 12 month change is the most important column to examine because it

quantifies the long term trend. It is easy to notice that, if we exclude London

with +8.1% and Monaco (+12.2%), home prices in the largest European cities

have been all declining in 2012: Zurich (-2.5%), Vienna (-2.8%), Geneva (-

6.8%), Rome (-7.7%), Madrid (-13%), Paris (-13.6%). The current trend will

continue to depress house prices as long as the job market will remain weak.

Short term contracts, unpaid work and low – paying positions will continue to

keep low the demand for new houses in Europe. Specifically, an unstable

5 | P a g e

contractual agreement with an employer or an insecure job position will

discourage individuals from purchasing new houses and will inevitably augment

the mortgage rejection rate.

2) Do you have a view on the most appropriate definition of

long-term financing?

2.b) Long term financing can be defined as the satisfaction of long – term

corporate liabilities via the acquisition of fixed streams of cash flows or equities

over a period of time not inferior to 5 years

3) Given the evolving nature of the banking sector, going

forward, what role do you see for banks in the channelling

of financing to long-term investments?

3.b) The role of banks in Europe will probably remain crucial in the next 3 to 5

years. However, in the last 3 – 4 years the banking sector failed to fulfil its

important social role: facilitating the circulation of cash amongst individuals

and businesses. Since this paragraph is primarily concentrated on commercial

banks the discussion field will be principally restricted to loans and mortgages.

Commercial banks have for years implemented a substantially “risk – free

arbitrage” between the interest rates paid for deposits and the interest rates

charged for loans and mortgages. The only risk commercial banks had is credit

risk or default risk, however, the credit risk exposure has been greatly reduced

by the fact that many insurance companies started to provide adequate insurance

policies against potential defaults of non – prime customers. The role the

banking sector will play in financing long – term investments will probably

change remarkably in the upcoming future. The ever – increasing rejection rate

and the tightening of loans/mortgages requirements are becoming a major

source of discontentment amongst micro and small business owners as well as

households. The next table (source: Eurostat) proves the point just made:

6 | P a g e

The table report the success rate in obtaining bank loans by country (%). The

figures clearly show a net increase in unsuccessful claims in 2010 with respect

to the 2007. Recent data are not available yet but the quantification of short

term trends offered by the mainstream economic and financial data providers

display non – comforting figures. The unsuccessful applications rate in 2010 in

large economies was dangerously high: United Kingdom (20.8% against 5.6%

in 2007), Germany (8.2% against 6.7% in 2007), Spain (13.2% against 3% in

2007), France (7% against 2% in 2007) and Italy (4.9% against 1.2% in 2007).

This situation will likely push many business owners, households, entrepreneurs

and start–uppers to seek alternative forms of long term financing such as crowd

funding or peer–to–peer lending (often family, friends or acquaintances). These

alternative types of fund raising are already popular in the United States and

7 | P a g e

they will keep increasing in popularity in Europe too. There are different

reasons which can augment the attractiveness of crowd funding solutions but

amongst the most cited motives, without a doubt, we have:

1) The face–to–face contact between cash lenders and loan/ mortgage

receivers

2) Lenders know perfectly well how their money are being used while in a

bank depositors are unaware of whom the bank is lending money to

3) The requirements for accessing funds can be more easily negotiated and

they can be shaped ad–hoc for a specific investment

4) There are many online platforms, social media groups, small financial

institutions or companies acting as intermediaries between demand and

offer but at a lower cost

Crowd funding or peer–to–peer funding solutions can have a significant impact

on the future of European financial scenario. In fact, these measures will be

largely adopted by freelancers, sole traders, micro or small business owners

which are, by far, the largest business segment in the whole Europe. The next

table (source: Eurostat) will help clarifying the aforementioned concept:

8 | P a g e

The data refers to the 2009 but the figures are self – explanatory. Micro

enterprises constitute the 92.2% of the total businesses in Europe and if we add

micro and small businesses the percentage increases to 98.7% of the total. Now,

micro or small businesses will definitely encounter more difficulty in raising

finance in traditional ways (bank loans) due to shaky or low cash flows, to low

creditworthiness or to the fact that business is not well established yet in terms

of productive process. All these factors will increase the propensity for

alternative types of financing in the upcoming years.

9 | P a g e

4) How could the role of national and multilateral

development banks best support the financing of long-term

investment? Is there scope for greater coordination between

these banks in the pursuit of EU policy goals? How could

financial instruments under the EU budget better support

the financing of long-term investment in sustainable

growth?

4.b) Development banks should respond more quickly to the needs of modern

economies. Nowadays, the traditional structure of the economic apparatus has

been completely reshaped and twisted by the crisis. Europe entered a new

economic and financial paradigm; hence, a more flexible approach is needed in

order to tackle the existing byzantine bureaucracy and the obsolete requirements

for project funding. Development banks should focus on smaller entities such as

freelancer, micro or small businesses because these realities are going to be the

only one who will be able to create stable growth. The only way for national or

multilateral development banks to support, in a sustainable manner, long – term

investment is to channel their resources towards small businesses and to finance

up to 55% of the total project costs. The recent crisis, which is still ongoing,

proved to be a hard wake – up call for many market players. The motto in the

upcoming years should be: let’s get back to basics. The largest companies

proved to be too slow when responding to market changes and sustainable

growth can only be achieved by allowing more competitions.

4.c) The interconnectivity amongst these banks can greatly help the EU towards

reaching its goals. A larger co–operation amongst development and national

banks could allow for the creation of preferential lending rates for virtuous

businesses (sustainable growth, low debt). A bigger collaboration could increase

the propensity to open start – ups and small businesses which would directly

benefit the job market by creating new vacancies.

10 | P a g e

4.d) Financial instruments could benefit the European budget as long as 2 rules

will be closely observed and respected: responsible risk management and

portfolio diversification achieved via the combination of different maturities.

Specifically, European short or medium term liabilities could be

counterbalanced and financed via the bond market. Consequently, investing in

triple A ranked government debt securities could help European institutions to

offset medium term liabilities. In fact, the relatively safe nature of these

instruments would avoid the loss of the notional principal amount and the bearer

of the bond would benefit from the returns provided by the coupon.

Nevertheless, an appropriate combination of medium term maturing bonds (3 to

5 years) and long term expiring instruments would also manage to balance the

portfolio volatility. In fact, the low variance of the yields in long term bonds (10

or 30 years maturity) would compensate for the higher degree of fluctuations

experienced by medium term expiring bonds. Consequently, an appropriate yet

well managed investment over the entire yield curve would provide sufficient

financing for short and medium term liabilities promoting growth and

sustainable expansion.

5) Are there other public policy tools and frameworks that

can support the financing of long term investment?

5.b) There are numerous policies that can help the financing of long term

investments such as

1) Diminished bureaucracy

2) Fiscal credit for start – ups, free lancers or micro businesses,

3) Channelling funds for financing projects proposed by young entrepreneurs or

professionals

11 | P a g e

4) Attractive interest rates for businesses loans or loans repayment spanned on

an increased period of time for virtuous businesses which manage to keep the

debt/equity ratio to a decent minimum

5) Low fiscal pressure for start – ups or businesses employing young graduates

These are only some of the measures that could be adopted in order to promote

sustainable growth. However, any policy which would increase the

entrepreneurial spirit amongst young Europeans would strongly benefit

economic expansion and prosperity in the long term.

6) To what extent and how can institutional investors play a

greater role in the changing landscape of long-term

financing?

6.b) Institutional investors such as insurance companies, mutual funds or

pension funds are obviously the largest market players when it comes to long

term financing. They, more than everybody else, provide liquidity on long term

expiring maturities since their liabilities are in the long term. However, given

the decreasing importance of state pensions and social security bodies, it is

reasonable to expect that their exposure to the back end of the yield curve will

increase in the next 5 to 7 years. In order to engage more institutional investors,

policies such as a low capital gain tax for longer holding periods could be

introduced or a fiscal credit measures for venture capitalists financing long –

term projects promoted by start – ups or young entrepreneurs/professionals

could be supported. Furthermore, more publicity could be given to green energy

investments channelling the attention of pension funds towards new energy

sources and “forcing” them to inject fresh capital towards industries which have

a large social impact and that would improve the living standards of European

cities. The recent data suggests an increased attention of pension funds and asset

12 | P a g e

management companies towards non – liquid type of investments and private

equity ranging from high – tech companies to renewable energy, from housing

projects to biotechnologies so policies which give public exposure to small

businesses could be a great source to meet demand and supply.

7) How can prudential objectives and the desire to support

long-term financing best be balanced in the design and

implementation of the respective prudential rules for

insurers, reinsurers and pension funds, such as IORPs?

7.b) Probably the best way to preserve customers ‘investments as well as

ensuring solvency without harming long–term support is to increase risk

monitoring techniques and promote lower taxation rates on long term asset

holdings. The monitoring of the risk should be based more on statistical facts

than accounting procedures because portfolio volatility and yields variance are

more objective quantitative measures than accounting standards that can be

manipulated at any time. Besides, the expansive fiscal incentives would increase

the attention on the back of the yield curve which has less volatile yields. These

measures should decrease portfolio risk but they would boost the investment

predisposition in the long term.

8) What are the barriers to creating pooled investment

vehicles? Could platforms be developed at the EU level?

8.b) There already many pooled investment vehicles but the barriers have not

changed in the last years. The main problem is that pooled investment vehicles

are restricted to a limited amount of people given their expensive nature. The

credit crunch decreased the tendency to invest in financial markets or in other

forms of investment therefore some of the barriers could be eliminated by

promoting pooled investment vehicles on a more public scale. Also,

13 | P a g e

deregulating and facilitating the creation of smaller yet competent asset

management firms would certainly facilitate the spreading of such vehicles.

8.c) Platforms at EU level could be developed. However, the change should

really happen at a private level. European institutions should monitor the

industry and deregulate it. Flexibility will be a key issue in the future and failure

to meet these requirements would probably result in both financial and human

capital losses

9) What other options and instruments could be considered

to enhance the capacity of banks and institutional investors

to channel long-term finance?

9) The channelling of long – term finance is useful as long as funds and

investments are redirected towards new sources of businesses or the

establishment of new companies. By this logic, banks, given the fact that they

are mere intermediaries, should promote new business opportunities to potential

investors (not necessarily institutional entities). The instruments could be of

diverse nature; however, the establishment of a start–up rating scale could be

introduced and proposed to interested parties. Performance – bounded

certificates with different maturities could be created by banks or financial

institutions and subsequently sold over to venture capitalists, institutional

investors, etc. This mechanism would create new business for the banking

sector but it would benefit entrepreneurs, start – uppers and professionals

because it would provide them with fresh capital to employ. Furthermore,

expansive fiscal measures for those investing in long term projects, businesses

or ideas are definitely the best tool to shift public’s attention towards long –

term financing.

14 | P a g e

10) Are there any cumulative impacts of current and

planned prudential reforms on the level and cyclicality of

aggregate long-term investment and how significant are

they? How could any impact be best addressed?

10.b) The current scenario forces banks to increase their reserves which means

that less capital will be invested in short, medium or long term instruments or

projects. Furthermore, a potential augment of the fiscal pressure on market

instruments (stocks and derivatives including government bonds) could have a

depressive effect on long – term financing and market liquidity. The volatility

of government bond yields could remarkably change because a diminished

investment in long – term instruments would imply an increased variance in the

back end of the yield curve. Such phenomenon would alter the mortgage

market, whose interest rates are based on 10 and 30 years bond rates, and re –

financing operations. The private equity sector and small companies, whose

shares are far from being liquid, could be heavily influenced by the cumulative

effect of prudential reforms. In fact, a tightening of fiscal or prudential activities

will force banks, financial institutions, insurers and institutional investors to re –

direct their funds towards heavily traded stocks creating a great imbalance in

market equilibrium

10.c) Expansive fiscal measures are still the best way to increase the attention

towards the long term and alleviate the impact on the real economy.

15 | P a g e

11) How could capital market financing of long-term

investment be improved in Europe?

11.b) Financial asset classes, such as equities or bonds, tend to respect a sort of

long term correlation. Government bond markets will always be used by market

players as a hedging tool to diversify risk in their portfolios. Hence, it is

absolutely normal to see negative correlation between bond markets and the so

called risky assets at least in the short term. This phenomenon explains why the

yields on triple A rated bonds, such as the 10 year German Bund, are fluctuating

around 1.5% and some auctions for shorter term debt securities issued on

German sovereign debt have registered negative rates. Nevertheless, regular

bond markets are still more attractive, despite the historically low returns, than

covered bonds or asset – backed securities. The popularity of covered bonds or

asset – backed securities is definitely diminishing amongst sophisticated

investors which are now looking at different ways to invest their funds. The

other source of financing is the equity market which is preferred by many

companies because it does not involve debt. However, SMEs still have to face

rather high costs for IPOs and long – term financing through equity capital

remains predominantly a practice adopted by well established and mature

businesses which account for less than 1% of the total number of businesses in

Europe. Capital market financing of long – term investment can be improved by

lowering the costs for IPOs and by introducing a lower fiscal pressure on those

companies which prefer equity financing to debt financing.

16 | P a g e

12) How can capital markets help fill the equity gap in

Europe? What should change in the way market-based

intermediation operates to ensure that the financing can

better flow to long-term investments, better support the

financing of long-term investment in economically-,socially-

and environmentally-sustainable growth and ensuring

adequate protection for investors and consumers?

12.b) Capital markets have helped to fill the equity gap since the end of the

80s,however, these practices are much more established in the United States

than Europe where many companies prefer conducting business the “old way”.

The benefits of capital markets on the equity gap are obvious: more

transparency, injection of fresh capital into the business and flexibility.

12.c) Intermediation should happen at more affordable costs. Usually IPOs are

conducted by investment banks which charge very high fees and therefore only

large businesses can afford to adopt this source of financing. The establishment

of independent consultancy firms would definitely lower the costs and would

allow SMEs to get exposure to capital markets. The co – operation of European

stock exchanges could lead to the creation of a European equity index for

smaller businesses and less liquid stocks (like the Russell Index in the USA).

This equity index would increase the exposure of SMEs to the public and would

help to improve the capitalisation and liquidity of the European financial

markets which is still rather acerb in terms of development.

17 | P a g e

13) What are the pros and cons of developing a more

harmonised framework for covered bonds? What elements

could compose this framework?

13.b) The benefits are a potential increased liquidity over the long term, a more

accurate assessment of companies’ liabilities in terms of accounting standards

and business book valuation a more harmonised and less fragmented

synchronization amongst European stock exchanges and capital markets in

general. The drawbacks are clearly connected to the risks that the issuer would

incur in case of credit event, credit risk in case of default of the counterparty

and, given by the large numbers of mortgages associated with each covered

bond, the miscalculation of the risk associated to the single instrument

13.c) Increased monitoring over covered bond issuing procedures, limited

number of mortgages assigned to each instrument, the mortgages underlying

instrument should strictly be assigned to prime ranked customers, risk

monitoring based on credit risk model valuation and volatility rather than

merely on accounting standards, the listing of covered bonds on the secondary

market or product publicity conducted by European stock exchanges to Over –

the – Counter clients

14) How could the securitisation market in the EU be

revived in order to achieve the right balance between

financial stability and the need to improve maturity

transformation by the financial system?

14.b) The securitisation market is probably exhausted in Europe. In the United

States, where financial markets are more mature and better capitalised than

European ones, many sophisticated investors and OTC clients are not interested

in such instruments anymore. Maturity in financial system cannot necessarily be

18 | P a g e

achieved via securitising debt. Nevertheless, monitoring market credit risk using

appropriate valuation models and credit event techniques is certainly a more

accurate way to assess the volatility associated with the investment in

securitised debt. These measures could potentially restore confidence and

investors’ appetite towards this market

15) What are the merits of the various models for a specific

savings account available within the EU level? Could an EU

model be designed?

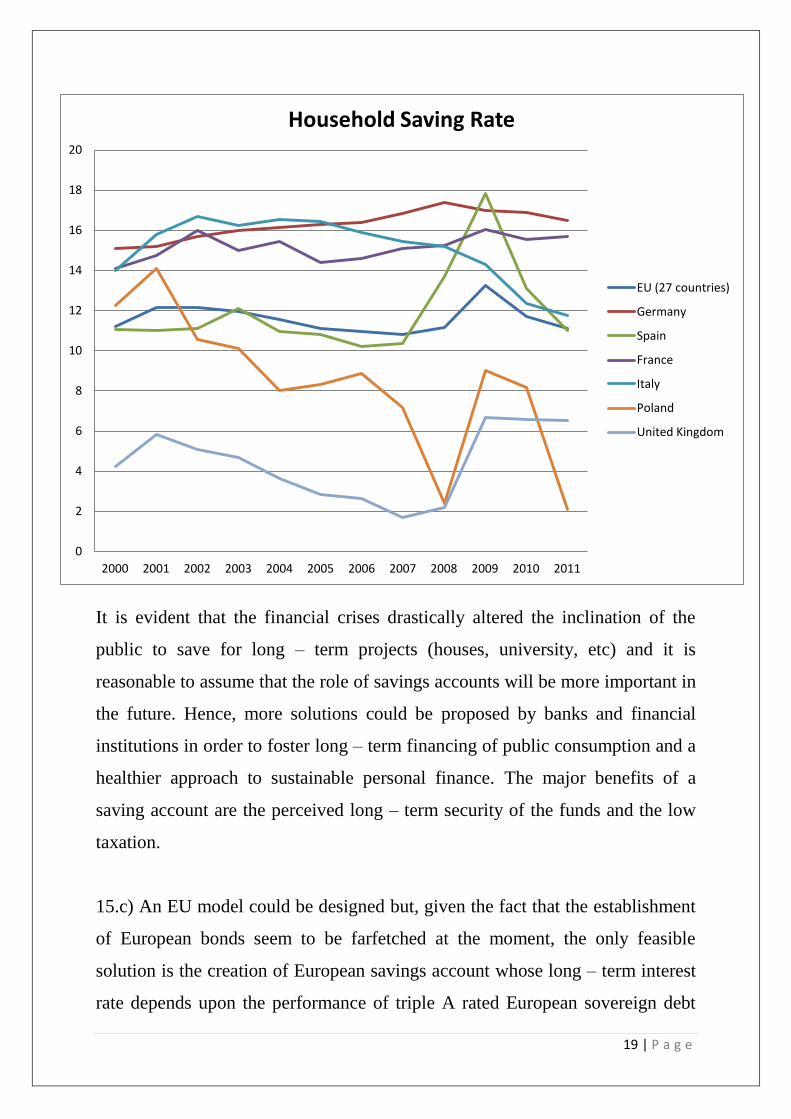

15.b) Household propensity to saving for the long – term it is almost entirely

dependent upon economic conditions. The next chart (source: Eurostat)

provides a quantification of household predisposition towards saving in the

largest European economies

19 | P a g e

It is evident that the financial crises drastically altered the inclination of the

public to save for long – term projects (houses, university, etc) and it is

reasonable to assume that the role of savings accounts will be more important in

the future. Hence, more solutions could be proposed by banks and financial

institutions in order to foster long – term financing of public consumption and a

healthier approach to sustainable personal finance. The major benefits of a

saving account are the perceived long – term security of the funds and the low

taxation.

15.c) An EU model could be designed but, given the fact that the establishment

of European bonds seem to be farfetched at the moment, the only feasible

solution is the creation of European savings account whose long – term interest

rate depends upon the performance of triple A rated European sovereign debt

0

2

4

6

8

10

12

14

16

18

20

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Household Saving Rate

EU (27 countries)

Germany

Spain

France

Italy

Poland

United Kingdom

20 | P a g e

securities. These types of saving accounts would certainly encourage

investments in the long term but they would also allow households and non –

sophisticated investors to access indirectly financial markets and to gain decent

profits. Furthermore, the invested capital would still be protected because, as

previously mentioned, the notional value would be redeemed at expiration.

Financial institutions could also charge customers a marginal fee, a premium, to

pay not higher than the 3% of the return generated by each coupon.

16) What type of CIT reforms could improve investment

conditions by removing distortions between debt and equity?

16.b) Equity capital is more subject to taxation so investment decisions are

clearly biased towards the issuing of debt securities. However, the leverage

created by these form of investments, if not correctly addressed, is not always

beneficial because it could increase the exposure to market risk and challenge

corporate cash flows in the medium to long term. On the other hand, a

softening of the fiscal pressure on equity capital could help SMEs to meet

medium term liabilities and remove any exogenous distortions

17) What considerations should be taken into account for

setting the right incentives at national level for long-term

saving? In particular, how should tax incentives be used to

encourage long-term saving in a balanced way?

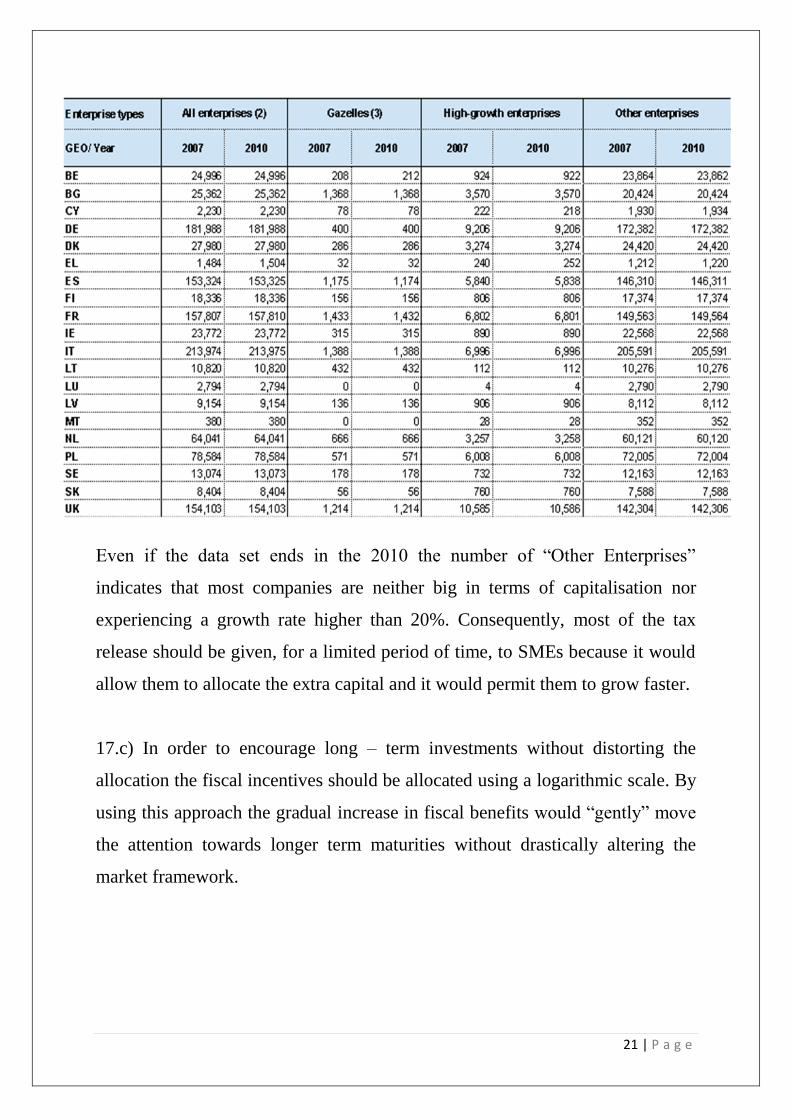

17.b) There are numerous factors to take into account when setting policies at a

national level. Nevertheless, all incentives should be allocated in a way that

benefits the largest segment of companies in a country. The next table (source:

Eurostat) displays the number of enterprises in Europe and it classifies them for

size and growth rate:

21 | P a g e

Even if the data set ends in the 2010 the number of “Other Enterprises”

indicates that most companies are neither big in terms of capitalisation nor

experiencing a growth rate higher than 20%. Consequently, most of the tax

release should be given, for a limited period of time, to SMEs because it would

allow them to allocate the extra capital and it would permit them to grow faster.

17.c) In order to encourage long – term investments without distorting the

allocation the fiscal incentives should be allocated using a logarithmic scale. By

using this approach the gradual increase in fiscal benefits would “gently” move

the attention towards longer term maturities without drastically altering the

market framework.

22 | P a g e

18) Which types of corporate tax incentives are beneficial?

What measures could be used to deal with the risks of

arbitrage when exemptions/incentives are granted for

specific activities?

18.b) Corporate tax incentives should be allowed for small companies in the

first 1 – 2 years, for companies operating in socially relevant fields

(environment, health care or assistance, etc), for companies where a large

working capital is needed or for companies offering long – term contracts.

18.c) Arbitrage risk is very difficult to identify and even harder to eliminate.

However, a tight monitoring of the investment procedures employed by the

companies which are benefiting from the expansive fiscal measures would

certainly help.

19) Would deeper tax coordination in the EU support the

financing of long-term investment?

19.b) Yes. Deeper coordination within fiscal activities could certainly diminish

bureaucracy, lower costs and barriers

23 | P a g e

20) To what extent do you consider that the use of fair value

accounting principles has led to short-termism in investor

behaviour? What alternatives or other ways to compensate

for such effects could be suggested?

20.b) Accounting principles have largely influenced companies’ performances

because many old style investors based their decisions on book valuation.

Accounting standards do not account for portfolio risk and volatility which are

factors that should always be considered while deciding how and where allocate

funds. Furthermore, the reduction in equity allocation and the augment of

investment towards government bond futures proves that volatility and portfolio

risk are crucial factors to account for. The next char plots the volatilities of

Eurostoxx futures, FTSE/MIB futures, DAX futures against German Bund

futures:

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

50.00%

Volatilities: European Equities vs German Bund

Bund Futures Eurostoxx Futures DAX Futures FTSE/MIB Futures

24 | P a g e

The chart above reported clearly highlights the fact that equity markets (here we

used the German DAX and the Italian FTSE/MIB as proxies) have an average

volatility oscillating around the 15% – 20% interval whilst futures contracts on

10 years German sovereign debt fluctuates around the 5% – 6% range.

Volatility is risk and investors should know about it when investing in either

short or long term horizons.

20.c) “Short – Termism” in investment decision and performances is a typical

case of principal – agent problem. The management (executives, board of

directors, etc) are incentivised to boost performance in the short term because

their bonuses are tied to quarterly results while investors prefer long term and

stable performances. There are numerous studies in the field of corporate

governance which are trying to address this issue but bonding executives’

salaries and bonuses to stock LEAPS options with biennial or triennial maturity

could probably force a change towards the “Long – Termism”.

21) What kind of incentives could help promote better long-

term shareholder engagement?

21.b) Expansive fiscal measure applied on dividends for investors who engage

in long – term investments could certainly be the way to go

22) How can the mandates and incentives given to asset

managers be developed to support long-term investment

strategies and relationships?

22.b) Asset managers have to control and limit portfolio risk while creating

added value for their customers. Hence, the only incentives that could

empirically be effective are more attractive interest rates for 10, 20 or 30 years

25 | P a g e

government bonds, a further decrease in long term yields which could help

stabilise even more portfolio risk or expansive fiscal measures for institutional

investors engaging significant amount of capital in long – term maturities

23) Is there a need to revisit the definition of fiduciary duty

in the context of long-term financing?

23.b) This is a measure of secondary importance.

24) To what extent can increased integration of financial

and non-financial information help provide a clearer

overview of a company’s long-term performance, and

contribute to better investment decision-making?

24.b) Financial information should not be limited to accounting figures but

portfolio volatility and correlation should be included in the information

publicly disclosed by asset managers. Furthermore, credit rating or benchmarks,

given the actual market volatility, should be based on annual performance. In

fact, any credit rating or benchmark based upon less than 9 months data

responds to an obsolete market paradigm. On the other hand, non – financial

information can benefit companies or businesses operating outside the financial

arena (particularly if the aforementioned businesses operate in social or

environmental fields)

26 | P a g e

25) Is there a need to develop specific long-term

benchmarks?

25.b) Yes. Long – term benchmarks would create a minimum target to achieve

for asset managers but at the same time they would provide investors with a

quantitative standard or scale against which they can contrast real life figures.

The creation of long – term benchmarks would help investors in understanding

financial figures or companies’ performances allowing them to make better

informed decisions

26) What further steps could be envisaged, in terms of EU

regulation or other reforms, to facilitate SME access to

alternative sources of finance?

26.b) Other than applying expansive fiscal policies or reducing bureaucratic

measures for SMEs, the creation of a financial index tracking the performance

of the stock issued by small or less capitalized companies (the European

equivalent of the Russell Index in USA) would promote investment in these

entities. Crowd funding will become one of the most popular financing sources

for many SMEs in the upcoming years so regulating in a flexible and not

oppressive manner these aspects would definitely help their growth. The major

problem SMEs encounter when raising finance is public exposure. Therefore,

European institutions could create a way to promote or foster the virtuous SMEs

which distinguish themselves for high growth / low debt ratios or for their

engagement in social activities such as preservation of the environment or social

responsibility at a local level. The ways to promote these companies are

different but most of the work should involve the issuing of EU newsletters to

investors, the creation of an online portal where investors could find potential

companies and where interviews to the most virtuous managers, executives,

27 | P a g e

employees could be reported and read. In other words, anything that would

provide SMEs with an increased public exposure would definitely help them

grow

27) How could securitisation instruments for SMEs be

designed? What are the best ways to use securitisation in

order to mobilise financial intermediaries' capital for

additional lending/investments to SMEs?

27.b) The re – designing should involve fiscal credit incentives for investors

purchasing instruments issued by SMEs and the securitised instruments should

have a lower number of underlying assets so that investors will feel more

comfortable when monitoring or managing their risk

27.c) The best way is to make securitisation a practice accessible to most SMEs.

Financial intermediaries will lend more and more often to SMEs if these

companies will use securitised instruments to increase liquidity. In fact, if SMEs

will start to see securitisation as a feasible channel for long – term finance they

will have to work with banks in order to issue the aforementioned instruments.

Consequently, banks will be more willing to lend extra cash to companies that

already provided them with a profit via customer’s commissions. Furthermore,

the selling of securitised instruments would allow SMEs to accumulate a higher

amount of capital so banks and financial institutions would probably charge a

lower rate for business loans because the proceeds coming from the selling of

asset – backed securities could be used as collateral and limit credit risk.

28 | P a g e

28) Would there be merit in creating a fully separate and

distinct approach for SME markets? How and by whom

could a market be developed for SMEs, including for

securitised products specifically designed for SMEs’

financing needs?

28.b) Yes, the creation of an ad – hoc platform for SME markets would channel

the attention towards them and consequently increase the number of

investments

28.c) A platform for SMEs could be created by allowing a greater co –

operation between exchanges, financial brokers and banks under the supervision

of the EU. The European bodies should, at first, create the legal framework in

order to delineate the general rules which should be based on the principles

listed in the answer to the question number 27. The second step would involve

the intervention of major financial institutions which would assist the EU in

creating the platform and promote the product amongst customers and contacts

29) Would an EU regulatory framework help or hinder the

development of these alternative non-bank sources of

finance for SMEs? What reforms could help support their

continued growth?

29.b) An efficient regulatory framework for alternative non – bank sources is

necessary to protect customers and to advertise the existence of a SMEs market.

However, policy makers should not regulate heavily the sector and should not

introduce too many barriers because the majority of the SMEs have to be able to

access this market at affordable costs.

29.c) Lower fiscal pressure, decreased bureaucracy, flexible regulation for

SMEs

29 | P a g e

30) In addition to the analysis and potential measures set out

in this Green Paper, what else could contribute to the long-

term financing of the European economy?

30.b) The most important measures and potential reforms have been extensively

discussed in the paper. However, increasing the exposure to financial education

as well as expanding public awareness towards the benefits of long – term

financing are important aspects to consider.