Embed Size (px)

Citation preview

18Long-Term Debt Financing

Multinational corporations (MNCs) typically use long-term sources offunds to finance long-term projects. They have access to both domestic andforeign sources of funds. It is worthwhile for MNCs to consider all possibleforms of financing before making their final decisions. Financial managersmust be aware of their sources of long-term funds so that they can financeinternational projects in a manner that maximizes the wealth of the MNC.

TheMNC’s cost of debt affects its required rate of returnwhen it assessesproposed projects. Features of debt such as currency of denomination,maturity, and whether the rate is fixed or floating can affect the cost of debt,and therefore affect the feasibility of projects that are supported with thedebt. Thus, MNCs can enhance their value by determining specific featuresof debt that can reduce their cost of debt.

FINANCING TO MATCH THE INFLOW CURRENCYSubsidiaries of MNCs commonly finance their operations with the currency in whichthey invoice their products. This matching strategy can reduce the subsidiary’s exposureto exchange rate movements because it allows the subsidiary to use a portion of its cashinflows to cover the cash outflows to repay its debt. In this way, the amount of the sub-sidiary’s funds that will ultimately be remitted to the parent (and converted into the par-ent’s currency) is reduced.

Many MNCs, including Honeywell and The Coca-Cola Co., issue bonds in some of the foreign curren-cies they receive from operations. PepsiCo issues bonds in several foreign currencies and uses pro-ceeds in those same currencies resulting from foreign operations to make interest and principalpayments. IBM and Nike have issued bonds denominated in yen at low-interest rates and use yen-denominated revenue to make the interest payments.

General Electric has issued bonds denominated in Australian dollars, British pounds, Japanese yen,New Zealand dollars, and Polish zloty to finance its foreign operations. Its subsidiaries in Australia useAustralian dollar inflows to pay off their Australian debt. Its subsidiaries in Japan use Japanese yeninflows to pay off their yen-denominated debt. By using various debt markets, General Electric canmatch its cash inflows and outflows in a particular currency. The decision to obtain debt in currencieswhere it receives cash inflows reduces the company’s exposure to exchange rate risk.•EXAMPLE

The matching strategy described above is especially desirable when the foreignsubsidiaries are based in countries where interest rates are relatively low. The MNCachieves a low financing rate and also reduces its exchange rate risk by matching its

CHAPTEROBJECTIVES

The specificobjectives of thischapter are to:

■ explainhowanMNCuses debt financingin a manner thatminimizes itsexposure toexchange rate risk,

■ explain how anMNC may assessthe potentialbenefits fromfinancing with alow-interest ratecurrency thatdiffers from itscash inflowcurrency,

■ explainhowanMNCmay determine theoptimal maturitywhen obtainingdebt, and

■ explainhowanMNCmay decidebetween usingfixed rate versusfloating rate debt.

531

© C

enga

ge L

earn

ing.

All

right

s re

serv

ed. N

o di

strib

utio

n al

low

ed w

ithou

t exp

ress

aut

horiz

atio

n.

debt outflow payments with the currency denominating its cash inflows. This can help tostabilize the firm’s cash flow.

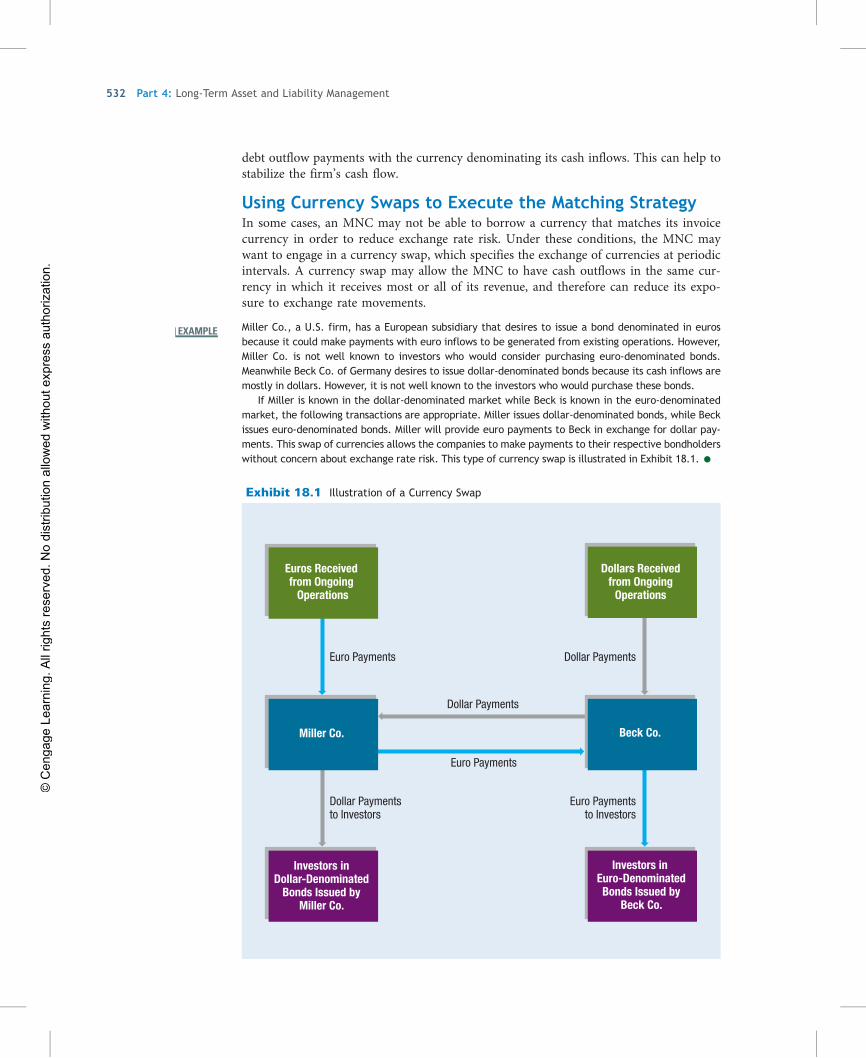

Using Currency Swaps to Execute the Matching StrategyIn some cases, an MNC may not be able to borrow a currency that matches its invoicecurrency in order to reduce exchange rate risk. Under these conditions, the MNC maywant to engage in a currency swap, which specifies the exchange of currencies at periodicintervals. A currency swap may allow the MNC to have cash outflows in the same cur-rency in which it receives most or all of its revenue, and therefore can reduce its expo-sure to exchange rate movements.

EXAMPLE Miller Co., a U.S. firm, has a European subsidiary that desires to issue a bond denominated in eurosbecause it could make payments with euro inflows to be generated from existing operations. However,Miller Co. is not well known to investors who would consider purchasing euro-denominated bonds.Meanwhile Beck Co. of Germany desires to issue dollar-denominated bonds because its cash inflows aremostly in dollars. However, it is not well known to the investors who would purchase these bonds.

If Miller is known in the dollar-denominated market while Beck is known in the euro-denominatedmarket, the following transactions are appropriate. Miller issues dollar-denominated bonds, while Beckissues euro-denominated bonds. Miller will provide euro payments to Beck in exchange for dollar pay-ments. This swap of currencies allows the companies to make payments to their respective bondholderswithout concern about exchange rate risk. This type of currency swap is illustrated in Exhibit 18.1.•

Exhibit 18.1 Illustration of a Currency Swap

Euro Payments

Euros Received from Ongoing

Operations

Dollar Payments

Beck Co.

Dollar Payments

Euro Payments

Investors inDollar-Denominated

Bonds Issued byMiller Co.

Investors in Euro-DenominatedBonds Issued by

Beck Co.

Miller Co.

Dollar Paymentsto Investors

Euro Paymentsto Investors

Dollars Receivedfrom Ongoing

Operations

532 Part 4: Long-Term Asset and Liability Management

© C

enga

ge L

earn

ing.

All

right

s re

serv

ed. N

o di

strib

utio

n al

low

ed w

ithou

t exp

ress

aut

horiz

atio

n.

The swap just described eliminates exchange rate risk for both Miller Co. and BeckCo. because both firms are able to match their cash outflow currency with the cashinflow currency. Miller essentially passes the euros it receives from ongoing operationsthrough to Beck and passes the dollars it receives from Beck through to the investors inthe dollar-denominated bonds. Thus, even though Miller receives euros from its ongoingoperations, the currency swap allows it to make dollar payments to the investors withouthaving to be concerned about exchange rate risk.

Ford Motor Co., Johnson & Johnson, and many other MNCs use currency swaps.Many MNCs simultaneously swap interest payments and currencies. The Gillette Co.engaged in swap agreements that converted $500 million in fixed rate dollar-denominated debt into multiple currency variable rate debt. PepsiCo enters into interestrate swaps and currency swaps to reduce borrowing costs. The large commercial banksthat serve as financial intermediaries for currency swaps sometimes take positions. Thatis, they may agree to swap currencies with firms, rather than simply search for suitableswap candidates.

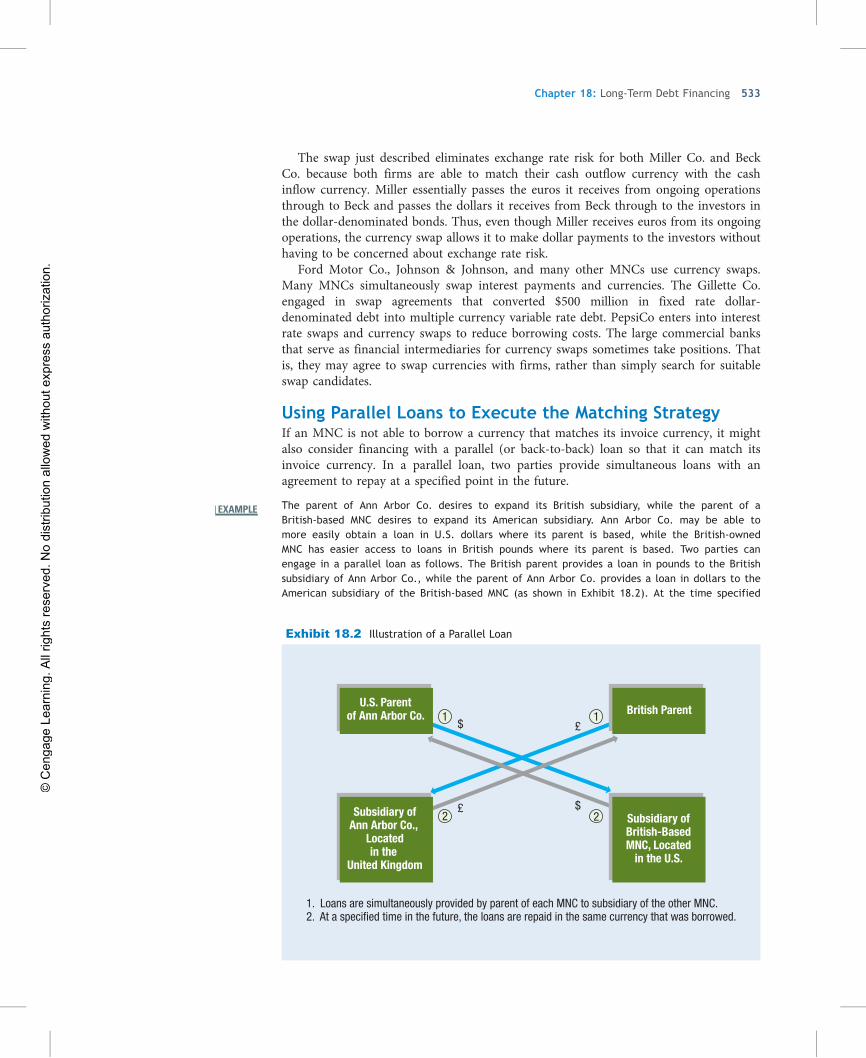

Using Parallel Loans to Execute the Matching StrategyIf an MNC is not able to borrow a currency that matches its invoice currency, it mightalso consider financing with a parallel (or back-to-back) loan so that it can match itsinvoice currency. In a parallel loan, two parties provide simultaneous loans with anagreement to repay at a specified point in the future.

EXAMPLE The parent of Ann Arbor Co. desires to expand its British subsidiary, while the parent of aBritish-based MNC desires to expand its American subsidiary. Ann Arbor Co. may be able tomore easily obtain a loan in U.S. dollars where its parent is based, while the British-ownedMNC has easier access to loans in British pounds where its parent is based. Two parties canengage in a parallel loan as follows. The British parent provides a loan in pounds to the Britishsubsidiary of Ann Arbor Co., while the parent of Ann Arbor Co. provides a loan in dollars to theAmerican subsidiary of the British-based MNC (as shown in Exhibit 18.2). At the time specified

Exhibit 18.2 Illustration of a Parallel Loan

1 1

2 2

1. Loans are simultaneously provided by parent of each MNC to subsidiary of the other MNC.2. At a specified time in the future, the loans are repaid in the same currency that was borrowed.

$

$£

£

U.S. Parentof Ann Arbor Co. British Parent

Subsidiary ofAnn Arbor Co.,

Locatedin the

United Kingdom

Subsidiary ofBritish-BasedMNC, Located

in the U.S.

Chapter 18: Long-Term Debt Financing 533

© C

enga

ge L

earn

ing.

All

right

s re

serv

ed. N

o di

strib

utio

n al

low

ed w

ithou

t exp

ress

aut

horiz

atio

n.

by the loan contract, the loans are repaid. The British subsidiary of Ann Arbor Co. uses pound-denominated revenues to repay the British company that provided the loan. At the same time,the American subsidiary of the British-based MNC uses dollar-denominated revenues to repaythe loan from the parent of Ann Arbor Co.•

The use of parallel loans is particularly attractive if the MNC is conducting a projectin a foreign country, will receive the cash flows in the foreign currency, and is worriedthat the foreign currency will depreciate substantially. If the foreign currency is notheavily traded, other hedging alternatives, such as forward or futures contracts, may notbe available, and the project may have a negative net present value (NPV) if the cashflows remain unhedged.

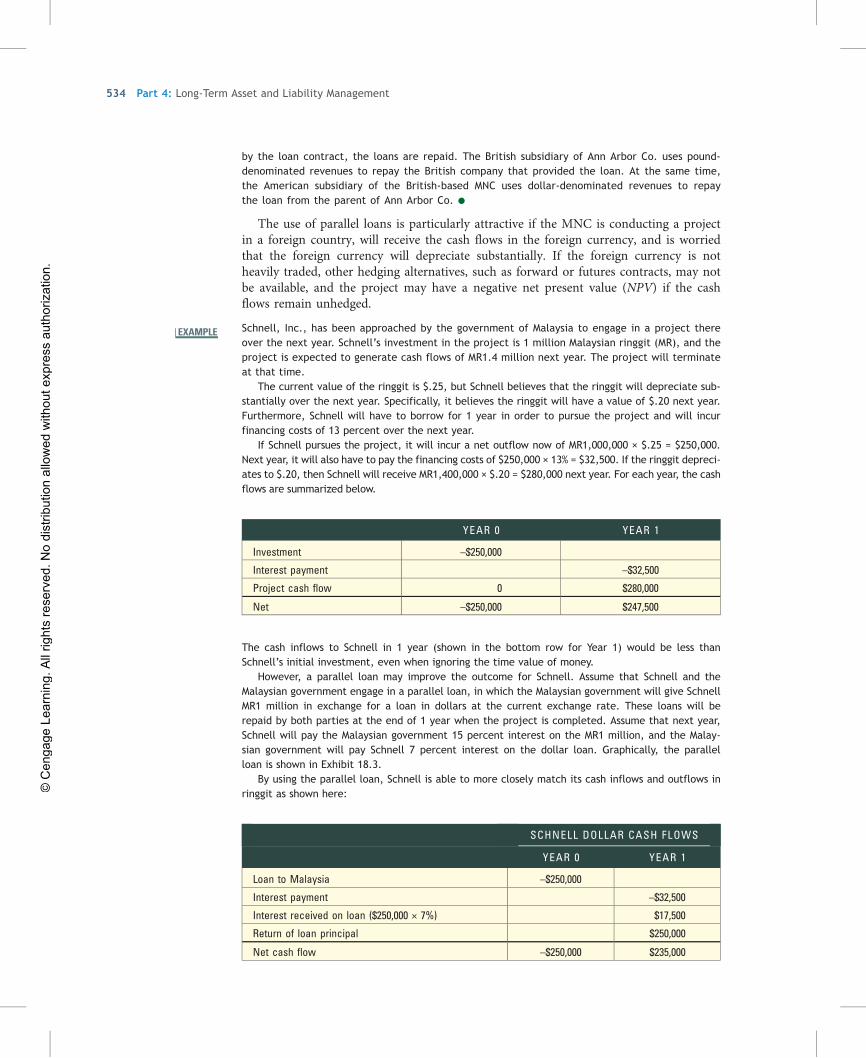

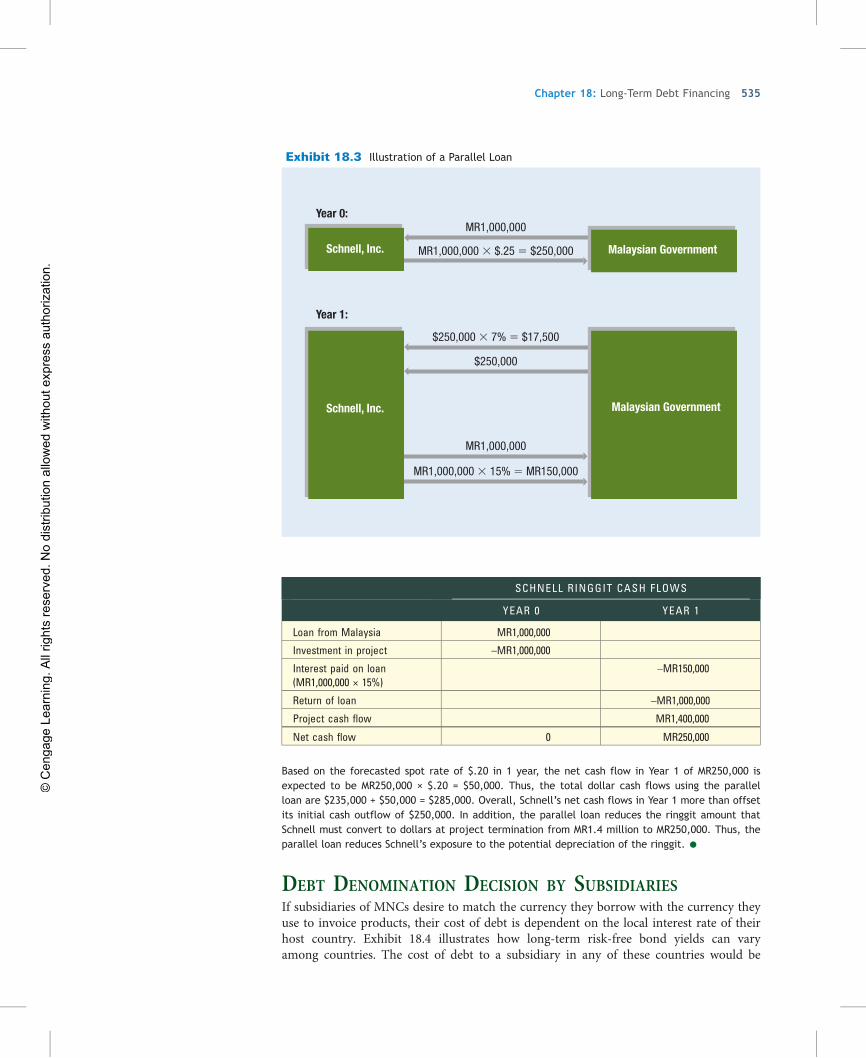

EXAMPLE Schnell, Inc., has been approached by the government of Malaysia to engage in a project thereover the next year. Schnell’s investment in the project is 1 million Malaysian ringgit (MR), and theproject is expected to generate cash flows of MR1.4 million next year. The project will terminateat that time.

The current value of the ringgit is $.25, but Schnell believes that the ringgit will depreciate sub-stantially over the next year. Specifically, it believes the ringgit will have a value of $.20 next year.Furthermore, Schnell will have to borrow for 1 year in order to pursue the project and will incurfinancing costs of 13 percent over the next year.

If Schnell pursues the project, it will incur a net outflow now of MR1,000,000 × $.25 = $250,000.Next year, it will also have to pay the financing costs of $250,000 × 13% = $32,500. If the ringgit depreci-ates to $.20, then Schnell will receive MR1,400,000 × $.20 = $280,000 next year. For each year, the cashflows are summarized below.

YEAR 0 YEAR 1

Investment –$250,000

Interest payment –$32,500

Project cash flow 0 $280,000

Net –$250,000 $247,500

The cash inflows to Schnell in 1 year (shown in the bottom row for Year 1) would be less thanSchnell’s initial investment, even when ignoring the time value of money.

However, a parallel loan may improve the outcome for Schnell. Assume that Schnell and theMalaysian government engage in a parallel loan, in which the Malaysian government will give SchnellMR1 million in exchange for a loan in dollars at the current exchange rate. These loans will berepaid by both parties at the end of 1 year when the project is completed. Assume that next year,Schnell will pay the Malaysian government 15 percent interest on the MR1 million, and the Malay-sian government will pay Schnell 7 percent interest on the dollar loan. Graphically, the parallelloan is shown in Exhibit 18.3.

By using the parallel loan, Schnell is able to more closely match its cash inflows and outflows inringgit as shown here:

SCHNELL DOLLAR CASH FLOWS

YEAR 0 YEAR 1

Loan to Malaysia –$250,000

Interest payment –$32,500

Interest received on loan ($250,000 × 7%) $17,500

Return of loan principal $250,000

Net cash flow –$250,000 $235,000

534 Part 4: Long-Term Asset and Liability Management

© C

enga

ge L

earn

ing.

All

right

s re

serv

ed. N

o di

strib

utio

n al

low

ed w

ithou

t exp

ress

aut

horiz

atio

n.

SCHNELL RINGGIT CASH FLOWS

YEAR 0 YEAR 1

Loan from Malaysia MR1,000,000

Investment in project –MR1,000,000

Interest paid on loan(MR1,000,000 × 15%)

–MR150,000

Return of loan –MR1,000,000

Project cash flow MR1,400,000

Net cash flow 0 MR250,000

Based on the forecasted spot rate of $.20 in 1 year, the net cash flow in Year 1 of MR250,000 isexpected to be MR250,000 × $.20 = $50,000. Thus, the total dollar cash flows using the parallelloan are $235,000 + $50,000 = $285,000. Overall, Schnell’s net cash flows in Year 1 more than offsetits initial cash outflow of $250,000. In addition, the parallel loan reduces the ringgit amount thatSchnell must convert to dollars at project termination from MR1.4 million to MR250,000. Thus, theparallel loan reduces Schnell’s exposure to the potential depreciation of the ringgit.•

DEBT DENOMINATION DECISION BY SUBSIDIARIESIf subsidiaries of MNCs desire to match the currency they borrow with the currency theyuse to invoice products, their cost of debt is dependent on the local interest rate of theirhost country. Exhibit 18.4 illustrates how long-term risk-free bond yields can varyamong countries. The cost of debt to a subsidiary in any of these countries would be

Exhibit 18.3 Illustration of a Parallel Loan

Year 0:

Schnell, Inc. Malaysian Government

MR1,000,000

MR1,000,000 � $.25 � $250,000

Year 1:

Schnell, Inc. Malaysian Government

$250,000 � 7% � $17,500

$250,000

MR1,000,000

MR1,000,000 � 15% � MR150,000

Chapter 18: Long-Term Debt Financing 535

© C

enga

ge L

earn

ing.

All

right

s re

serv

ed. N

o di

strib

utio

n al

low

ed w

ithou

t exp

ress

aut

horiz

atio

n.

slightly higher than the risk-free rates shown here because it would contain a credit riskpremium. The cost of debt financing in Japan is typically low because the risk-free bondrate there is low. Conversely, the cost of debt financing in Brazil (as shown here) andsome other countries can be very high. A subsidiary in a host country where interestrates are high might consider borrowing in a different currency in order to avoid thehigh cost of local debt. The analysis used to determine which currency to borrow isexplained in the following section.

Debt Decision in Host Countries with High Interest RatesWhen an MNC’s subsidiaries are based in developing countries such as Brazil, Indonesia,Malaysia, Mexico, and Thailand, they may be subject to relatively high interest rates.Thus, while the matching strategy described earlier reduces exchange rate risk, it wouldforce MNC subsidiaries in developing countries to incur a high cost of debt. The parentof a U.S.–based MNC may consider providing a loan in dollars to finance the subsidiaryso the subsidiary can avoid the high cost of local debt. However, this will force the sub-sidiary to convert some of its funds to dollars in order to repay the loan. Recall thatcountries where interest rates are high tend to have high expected inflation (the Fishereffect, explained in Chapter 8) and that currencies of countries with relatively high infla-tion tend to weaken over time (as suggested by purchasing power parity, explained inChapter 8). Thus, by attempting to avoid the high cost of debt in one currency, the sub-sidiary of a U.S.–based MNC becomes more highly exposed to exchange rate risk.

EXAMPLE Boise Co. (a U.S. company) has a Mexican subsidiary that will need about 200 million Mexican pesosfor 3 years to finance its Mexican operations. While the Mexican subsidiary will continue to existeven after 3 years, the focus here on a 3-year period is sufficient to illustrate a common subsidiaryfinancing dilemma when the host country interest rate is high. Assume the peso’s spot rate is $.10;the financing represents $20 million (computed as MXP200 million × $.10). To finance its operations,Boise’s parent considers two possible financing alternatives:

1. Peso Loan. Boise’s parent can instruct its Mexican subsidiary to borrow Mexican pesos to financethe Mexican operations. The interest rate on a 3-year fixed rate peso-denominated loan is12 percent.

2. Dollar Loan. Boise’s parent can borrow dollars and extend a loan to the Mexican subsidiary tofinance the Mexican operations. Boise can obtain a 3-year fixed rate dollar-denominated loanat an interest rate 7 percent.•

Exhibit 18.4 Annualized Bond Yields among Countries (as of January 2009)

JapaneseYen

U.S.Dollar

EuroCanadianDollar

BritishPound

AustralianDollar

BrazilianReal

Annu

aliz

ed B

ond

Yiel

d

16

12

4

0

8

536 Part 4: Long-Term Asset and Liability Management

© C

enga

ge L

earn

ing.

All

right

s re

serv

ed. N

o di

strib

utio

n al

low

ed w

ithou

t exp

ress

aut

horiz

atio

n.

If the Mexican subsidiary borrows Mexican pesos, it is matching its cash outflow cur-rency (when making interest payments) to its cash inflow currency. Thus, it can use aportion of its peso inflows to periodically make payments on the peso-denominatedloan before remitting any earnings to the parent. Consequently, it has less cash availableto periodically remit to the parent convertible into dollars, and it does not have any loanrepayments to the parent. This situation reflects a relatively low exposure of Boise toexchange rate risk. Even if the Mexican peso depreciates substantially over time, theadverse impact is less pronounced because there is a smaller amount of pesos periodi-cally converted into U.S. dollars over time. However, the disadvantage of borrowingpesos is that the interest rate is high.

The potential advantage of the Mexican subsidiary borrowing dollars is that it resultsin a lower interest rate. However, the potential disadvantage of borrowing in dollars isthat there is more of a mismatch between the cash flows, as illustrated in Exhibit 18.5.If the Mexican subsidiary borrows dollars, it does not have debt in pesos, so it will peri-odically remit a larger amount of pesos to the parent (so that it can repay the loan fromthe parent), convertible into dollars. This situation reflects a high exposure of Boise toexchange rate risk. If the Mexican peso depreciates substantially over time, the subsidiarywill need more pesos to repay the dollar-denominated loan over time. For this reason, itis possible that the subsidiary will need more pesos to pay off the 7 percent dollar-denominated loan than the 12 percent peso-denominated loan.

Combining Debt Financing with Forward Hedging While a subsidiary ismore exposed to exchange rate risk if it borrows a currency other than that of its hostcountry, it might consider hedging that risk. Forward contracts may be available on somecurrencies for 5 years or longer, which may allow the subsidiary to hedge its future loanpayments in a particular currency. However, this hedging strategy may not allow the

Exhibit 18.5 Comparison of Subsidiary Financing with Its Local Currency versus Borrowing from Parent

Parent Mexican Subsidiary

Local Bank inMexico

InterestPaymentsLoans

Alternative 1: Mexican Subsidiary Borrows Pesos at Interest Rate of 12 Percent

Small Amount of Remitted Funds

Parent Mexican Subsidiary

Large Loan in $ Provided by Parent

Alternative 2: Mexican Subsidiary Borrows Dollars at Interest Rate of 7 Percent

Much Remitted Funds Needed to Pay Off Loan

Chapter 18: Long-Term Debt Financing 537

© C

enga

ge L

earn

ing.

All

right

s re

serv

ed. N

o di

strib

utio

n al

low

ed w

ithou

t exp

ress

aut

horiz

atio

n.

subsidiary to achieve a lower debt financing rate than it could achieve by borrowing itshost country currency, as illustrated here.

EXAMPLE Recall that the Mexican subsidiary of Boise Co. wants to borrow 200 million Mexican pesos for3 years to support its operations, but the prevailing fixed interest rate on peso-denominated debtis 12 percent versus 7 percent on dollar-denominated debt. The Mexican subsidiary considers bor-rowing $20 million and converting them to pesos to support its operations. It would need to convertpesos to dollars to make interest payments of $2,100,000 (computed as 7% × $20,000,000) for eachof the next 3 years. It is concerned that the Mexican peso could depreciate against the dollar overtime, which could increase the amount of pesos needed to cover the loan payments. So it wants tohedge its loan payments with forward sales of pesos in exchange for $2,100,000 over each of thenext 3 years. However, even if Boise Co. is able to find a financial institution that is willing toaccommodate this request with forward contracts over the next 3 years, it will not benefit fromthis strategy. Recall from Chapter 7 that from a U.S. perspective, interest rate parity causes the for-ward rate of a foreign currency to exhibit a discount that reflects the differential between theinterest rate of that currency versus the interest rate on dollars. In this example, the interest ratefrom borrowing pesos is much higher than the interest rate from borrowing U.S. dollars. Thus, theforward rate of the Mexican peso will contain a substantial discount, which means that the Mexicansubsidiary of Boise Co. would be selling pesos forward at a substantial discount in order to obtaindollars so that it could make loan payments. Consequently, the discount would offset the interestrate advantage of borrowing dollars, so Boise Co. would not be able to reduce its financing costswith this forward hedge strategy.•

Even if a subsidiary cannot effectively hedge its financing position, it might stillconsider financing with a currency that differs from its host country. Its final debtdenomination decision will likely be based on its forecasts of exchange rates, as isillustrated in the following section.

Comparing Financing Costs between Debt Denominations If an MNCparent considers financing subsidiary operations in a host country where interest ratesare high, it must estimate the financing costs for both financing alternatives.

EXAMPLE Recall that the Mexican subsidiary of Boise Co. could obtain a MXP200 million loan at an annualizedinterest rate of 12 percent over 3 years, or can borrow $20 million from its parent at an annualizedinterest rate of 7 percent over 3 years. Assume that all loan principal is repaid at the end of3 years. The annualized cost of each financing alternative is shown in Exhibit 18.6. The subsidiary’spayments on the peso-denominated loan is simply based on the interest rate (12 percent) applied tothe loan amount, as there is no exchange rate risk to the Mexican subsidiary if it borrows its local cur-rency. Next, the annualized cost of financing of the dollar loan is the discount rate that equates thepayments to the loan proceeds (MXP200 million) at the time the loan is created, and is estimated tobe 12.00 percent (the same as the interest rate because there is no exchange rate risk).

The estimated cost of financing with dollars requires forecasts of exchange rates at the intervalswhen loan payments are made to the U.S. parent, as shown in Exhibit 18.6. Assume that the subsid-iary forecasts that the peso’s spot rate will be $.10 in 1 year, $.09 in 2 years, and $.09 in 3 years.Given the required loan repayments in dollars and the forecasted exchange rate of the peso, the

Exhibit 18.6 Comparison of Two Alternative Loans with Different Debt Denominations for the Foreign Subsidiary

YEAR 1 YEAR 2 YEAR 3

PESO LOAN OF MXP 200,000,000 at 12%: MXP24,000,000 MXP24,000,000 MXP24,000,000 + loan principalrepayment of MXP200,000,000

U.S. DOLLAR LOAN OF $20,000,000 at 7%:Loan repayment in U.S. Dollars

$1,400,000 $1,400,000 $1,400,000 + loan principal repaymentof $20,000,000

Forecasted Exchange Rate of Peso $.10 $.09 $.09

Pesos Needed to Repay Dollar Loan MXP14,000,000 MXP15,555,556 MXP237,777,778

538 Part 4: Long-Term Asset and Liability Management

© C

enga

ge L

earn

ing.

All

right

s re

serv

ed. N

o di

strib

utio

n al

low

ed w

ithou

t exp

ress

aut

horiz

atio

n.

amount of pesos needed to repay the loan per year can be estimated, as shown in Exhibit 18.6.Next, the annualized cost of financing of the Mexican subsidiary with a dollar loan can be deter-mined. It is the discount rate that equates the payments to the loan proceeds ($20 million) atthe time the loan is created, and can be calculated with the use of many calculators. It is esti-mated to be 10.82 percent when financing with a U.S. dollar loan, versus 12 percent for the Mexi-can peso loan.•

While the annualized cost of financing is slightly lower when financing the Mexicansubsidiary with dollars, the cost is subject to exchange rate forecasts, and therefore isuncertain. Conversely, the cost of financing with the peso-denominated loan is certainfor the Mexican subsidiary. Thus, Boise Co. will only decide to finance the Mexicansubsidiary with dollar-denominated debt if it is confident that the peso will not weakenany more than its prevailing forecasts over the next 3 years.

Accounting for Uncertainty of Financing Costs The estimated cost of debtfinancing by the subsidiary when it borrows a different currency than that of its hostcountry is highly sensitive to the forecasted exchange rates. If the subsidiary usesinaccurate exchange rate forecasts, it could make the wrong decision regarding thecurrency to denominate its debt. It can at least account for the uncertainty surround-ing its point estimate exchange rate forecasts by using sensitivity analysis, in which itcan develop alternative forecasts for the exchange rate for each period in which aloan payment will be provided. It might initially use its best guess for each periodto estimate the cost of financing. Then, it can repeat the process based on unfavor-able conditions. Finally, it can repeat the process under more favorable conditions.For each set of exchange rate forecasts, the MNC can estimate the cost of financing.This process results in a different estimate of the cost of financing for each of thethree sets of forecasts that it used.

Alternatively, an MNC can apply simulation, in which it develops a probabilitydistribution for the exchange rate for each period in which an outflow payment will beprovided. It can feed those probability distributions into a computer simulationprogram. The program will randomly draw one possible value from the exchange ratedistribution for the end of each year and determine the outflow payments based on thoseexchange rates. Consequently, the cost of financing is determined. The proceduredescribed up to this point represents one iteration.

Next, the program will repeat the procedure by again randomly drawing one possiblevalue from the exchange rate distribution at the end of each year. This will provide a newschedule of outflow payments reflecting those randomly selected exchange rates. Thecost of financing for this second iteration is also determined. The simulation programcontinually repeats this procedure as many times as desired, perhaps 100 times or so.

Every iteration provides a possible scenario of future exchange rates, which is thenused to determine the annual cost of financing if that scenario occurs. Thus, thesimulation generates a probability distribution of annual financing costs that can then becompared with the known cost of financing if the subsidiary borrows its local currency.Through this comparison, the MNC can determine the probability that borrowinga currency other than its local currency (of its host country) will achieve a lowerannualized cost of financing than if it borrows its local currency.

Debt Denomination to Finance a ProjectWhen an MNC considers a new project, it must consider what currency to borrow whenfinancing the project. This decision is related to the previous section in which an MNC’ssubsidiary decides how to finance its operations. However, it is more specific in that it isfocused on financing a specific project, as illustrated in the example below.

Chapter 18: Long-Term Debt Financing 539

© C

enga

ge L

earn

ing.

All

right

s re

serv

ed. N

o di

strib

utio

n al

low

ed w

ithou

t exp

ress

aut

horiz

atio

n.

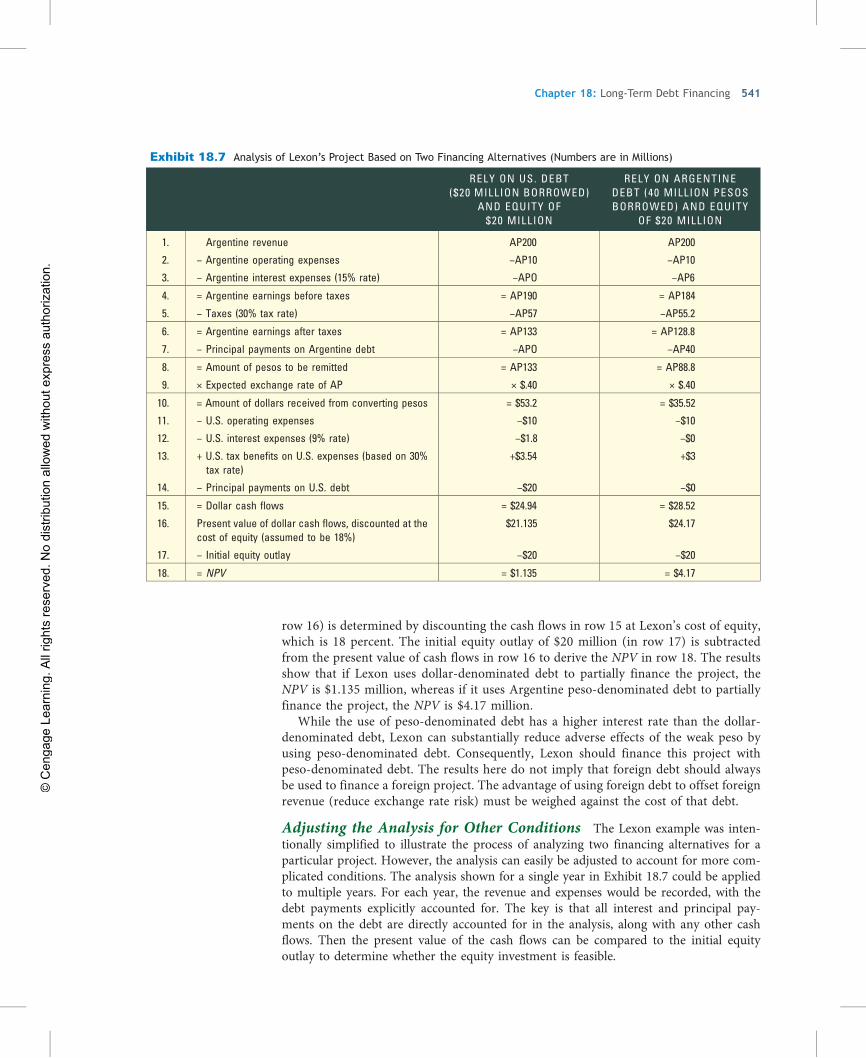

Input Necessary to Conduct an Analysis Consider the case of Lexon Co.(a U.S. firm), which considers a new project that would require an investment of80 million Argentine pesos (AP). Because the spot rate of the Argentine peso is presently$.50, the project’s initial outlay requires the equivalent of $40 million. If Lexon imple-ments this project, it will use equity to finance half of the investment, or $20 million. Itwill use debt to finance the remainder. For its debt financing, Lexon will either borrow$20 million (and convert those funds into pesos), or it will borrow AP40 million. Thus,the focus of this problem is on the currency to borrow to support the project. Lexon willpay an annualized interest rate of 9 percent if it borrows U.S. dollars or 15 percent if itborrows Argentine pesos. The project will be terminated in 1 year. At that time, the debtwill be repaid, and any earnings generated by the project will be remitted to Lexon in theUnited States. The project is expected to generate revenue of AP200 million at the end of1 year, and operating expenses in Argentina will be AP10 million payable at the end of1 year. Lexon expects that the Argentine peso will be valued at $.40 in 1 year. This projectwill not generate any revenue in the United States, but Lexon does expect to incur operatingexpenses of $10 million in the United States. Lexon’s cost of equity is 18 percent.

Analysis of Financing Alternatives for the Project By applying capital bud-geting analysis to each possible financing mix, Lexon can determine which financing mixwill result in a higher net present value. As explained in Chapter 14, an MNC canaccount for exchange rate effects due to debt financing by directly estimating the debtpayment cash flows along with all other cash flows in the capital budgeting process.Because the debt payments are completely accounted for within the cash flow estimates,the initial outlay represents the parent’s equity investment, and the capital budgetinganalysis determines the net present value of the parent’s equity investment. If neitheralternative has a positive NPV, the proposed project will not be undertaken. If both alter-natives have positive NPVs, the project will be financed with the financing mix that isexpected to generate a higher NPV.

The analysis of the two financing alternatives is provided in Exhibit 18.7. Rows 1 and2 show the expected revenue and operating expenses in Argentina, and are the same forboth alternatives. Row 3 shows that borrowing dollars results in zero Argentine interestexpenses, while the alternative of borrowing pesos results in interest expenses of AP6million pesos (15% × 40 million pesos). Row 4 shows Argentine earnings before taxes,which is computed as row 1 minus rows 2 and 3. The tax rate is applied to the Argentineearnings before taxes (row 4) in order to derive the taxes paid in Argentina (row 5) andArgentine earnings after taxes (row 6).

Row 7 accounts for the repayment of Argentine debt. This is a key difference betweenthe two financing alternatives, and is why the amount of pesos remitted to Lexon in row8 is so much larger if dollar-denominated debt is used instead of peso-denominateddebt. The expected exchange rate of the peso in row 9 is applied to the amount of pesosto be remitted in row 8 in order to determine the amount of dollars received in row 10.The U.S. operating expenses are shown in row 11. The U.S. interest expenses are shownin row 12 and computed as 9% × $20 million = $1.8 million if dollar-denominated debtis used. Row 13 accounts for tax savings to Lexon from incurring expenses in the UnitedStates due to the project, which are estimated as the 30 percent U.S. tax rate multipliedby the U.S. expenses shown in rows 11 and 12. The principal payment of U.S. dollar-denominated debt is shown in row 14.

Dollar cash flows resulting from the project in row 15 can be estimated as the amountof dollars received from Argentina (row 10) minus the U.S. expenses (rows 11 and 12)plus tax benefits due to U.S. expenses (row 13) minus the principal payment on U.S. debt(row 14). The present value of the dollar cash flows resulting from the project (shown in

540 Part 4: Long-Term Asset and Liability Management

© C

enga

ge L

earn

ing.

All

right

s re

serv

ed. N

o di

strib

utio

n al

low

ed w

ithou

t exp

ress

aut

horiz

atio

n.

row 16) is determined by discounting the cash flows in row 15 at Lexon’s cost of equity,which is 18 percent. The initial equity outlay of $20 million (in row 17) is subtractedfrom the present value of cash flows in row 16 to derive the NPV in row 18. The resultsshow that if Lexon uses dollar-denominated debt to partially finance the project, theNPV is $1.135 million, whereas if it uses Argentine peso-denominated debt to partiallyfinance the project, the NPV is $4.17 million.

While the use of peso-denominated debt has a higher interest rate than the dollar-denominated debt, Lexon can substantially reduce adverse effects of the weak peso byusing peso-denominated debt. Consequently, Lexon should finance this project withpeso-denominated debt. The results here do not imply that foreign debt should alwaysbe used to finance a foreign project. The advantage of using foreign debt to offset foreignrevenue (reduce exchange rate risk) must be weighed against the cost of that debt.

Adjusting the Analysis for Other Conditions The Lexon example was inten-tionally simplified to illustrate the process of analyzing two financing alternatives for aparticular project. However, the analysis can easily be adjusted to account for more com-plicated conditions. The analysis shown for a single year in Exhibit 18.7 could be appliedto multiple years. For each year, the revenue and expenses would be recorded, with thedebt payments explicitly accounted for. The key is that all interest and principal pay-ments on the debt are directly accounted for in the analysis, along with any other cashflows. Then the present value of the cash flows can be compared to the initial equityoutlay to determine whether the equity investment is feasible.

Exhibit 18.7 Analysis of Lexon’s Project Based on Two Financing Alternatives (Numbers are in Millions)

RELY ON US. DEBT($20 MILLION BORROWED)

AND EQUITY OF$20 MILLION

RELY ON ARGENTINEDEBT (40 MILLION PESOSBORROWED) AND EQUITY

OF $20 MILLION

1. Argentine revenue AP200 AP200

2. − Argentine operating expenses −AP10 −AP10

3. − Argentine interest expenses (15% rate) −APO −AP6

4. = Argentine earnings before taxes = AP190 = AP184

5. − Taxes (30% tax rate) −AP57 −AP55.2

6. = Argentine earnings after taxes = AP133 = AP128.8

7. − Principal payments on Argentine debt −APO −AP40

8. = Amount of pesos to be remitted = AP133 = AP88.8

9. × Expected exchange rate of AP × $.40 × $.40

10. = Amount of dollars received from converting pesos = $53.2 = $35.52

11. − U.S. operating expenses −$10 −$10

12. − U.S. interest expenses (9% rate) −$1.8 −$0

13. + U.S. tax benefits on U.S. expenses (based on 30%tax rate)

+$3.54 +$3

14. − Principal payments on U.S. debt −$20 −$0

15. = Dollar cash flows = $24.94 = $28.52

16. Present value of dollar cash flows, discounted at thecost of equity (assumed to be 18%)

$21.135 $24.17

17. − Initial equity outlay −$20 −$20

18. = NPV = $1.135 = $4.17

Chapter 18: Long-Term Debt Financing 541

© C

enga

ge L

earn

ing.

All

right

s re

serv

ed. N

o di

strib

utio

n al

low

ed w

ithou

t exp

ress

aut

horiz

atio

n.

DEBT MATURITY DECISIONRegardless of the currency that an MNC uses to finance its international operations, itmust also decide on the maturity that it should use for its debt. Normally, an MNCmay use a long-term maturity for financing subsidiary operations that will continue for along-term period. But it might consider a maturity that is shorter than the time period inwhich it will need funds, especially when it notices that annualized interest rates on debtare relatively low for particular maturities.

Assessment of Yield CurveBefore making the debt maturity decision, MNCs assess the yield curve of the country inwhich they need funds.

The shape of the yield curve (relationship between annualized yield and debt matu-rity) can vary among countries. Some countries tend to have an upward-sloping yieldcurve, which means that the annualized yields are lower for short-term debt maturitiesthan for long-term debt maturities. One argument for the upward slope is that investorsmay require a higher rate of return on long-term debt as compensation for lower liquid-ity (tying up their funds for a longer period of time). Put another way, an upward-sloping yield curve suggests that more creditors prefer to loan funds for shorter loanmaturities, and therefore charge a lower annualized interest rate for these maturities.

Financing Costs of Loans with Different MaturitiesWhen there is an upward-sloping yield curve, the MNC may be tempted to finance theproject with debt over a shorter maturity in order to achieve a lower cost of debt financ-ing, even if means that it will need funding beyond the life of the loan. However, theMNC may incur higher financing costs when it attempts to obtain additional fundingafter the existing loan matures if market interest rates are higher at that time. It mustdecide whether to obtain a loan with a maturity that perfectly fits its needs, or one witha shorter maturity if it has a more favorable interest rate and then additional financingwhen this loan matures.

EXAMPLE Scottsdale Co. (a U.S. firm) has a Swiss subsidiary that needs debt financing in Swiss francs for5 years. It plans to borrow SF40 million. A Swiss bank offers a loan that would require annual inter-est payments of 8 percent for a 5-year period, which results in interest expenses of SF3,200,000 peryear (computed as SF40,000,000 × .08). Assume that the subsidiary could achieve an annualized costof debt of only 6 percent if it borrows for a period of 3 years instead of 5 years. In this case, itsinterest expenses would be SF2,400,000 per year (computed as SF40,000,000 × .06) over the first3 years. Thus, it can reduce its interest expenses by SF80,000 per year over the first 3 years if itpursues the 3-year loan. If Scottsdale accepts a 3-year loan, it would be able to extend its loan in3 years for 2 additional years, but the loan rate for those remaining years would be based on theprevailing market interest rate of Swiss francs at the time. Scottsdale believes that the interestrate on Swiss francs in years 4 and 5 will be 9 percent. In this case, it would pay SF3,600,000 inannual interest expenses in Years 4 and 5.

The payments of the two financing alternatives are shown in Exhibit 18.8 Row 1 shows thepayments that would be required for the 5-year loan, while row 2 shows the payments for the3-year loan plus the estimated payments for the loan extension (in years 4 and 5). The annual-ized cost of financing for the two alternative loans can be measured as the discount rate thatequates the payments to the loan proceeds of SF40 million. This discount rate is 8.00 percentfor the 5-year loan versus 7.08 percent for the 3-year loan plus the loan extension. Since theannualized cost of financing is expected to be lower for the 3-year loan plus loan extension,Scottsdale prefers that loan.•

542 Part 4: Long-Term Asset and Liability Management

© C

enga

ge L

earn

ing.

All

right

s re

serv

ed. N

o di

strib

utio

n al

low

ed w

ithou

t exp

ress

aut

horiz

atio

n.

When Scottsdale Co. assesses the annualized cost of financing for the 3-year loan plusthe loan extension, there is uncertainty surrounding the interest rate to be paid duringthe loan extension (in years 4 and 5). It could have considered alternative possible inter-est rates that may exist over that period, and estimated the annualized cost of financingbased on those scenarios. In this way, it could develop a probability distribution for theannualized cost of financing and compare that to the known annualized cost of financingif it pursues the fixed rate 5-year loan.

FIXED VERSUS FLOATING RATE DEBT DECISIONMNCs that wish to use a long-term maturity but wish to avoid paying the prevailing fixedrate on long-term bonds may consider floating rate bonds or loans. In this case, the couponrate on bonds (or interest rate on loans) will fluctuate over time in accordance with marketinterest rates. For example, the coupon rate on a floating rate bond is frequently tied to theLondon Interbank Offer Rate (LIBOR), which is a rate at which banks lend funds to eachother. As LIBOR increases, so does the coupon rate of a floating rate bond. A floating cou-pon rate can be an advantage to the bond issuer during periods of decreasing interest rates,when otherwise the firm would be locked in at a higher coupon rate over the life of thebond. It can be a disadvantage during periods of rising interest rates. In some countries,such as those in South America, most long-term debt has a floating interest rate.

Financing Costs of Fixed versus Floating Rate LoansIf an MNC considers financing with floating-rate loans whose rate is tied to the LIBOR,it can first forecast the LIBOR for each year, and that would determine the expectedinterest rate it would pay per year. This would allow it to derive forecasted interest pay-ments for all years of the loan. Then, it could estimate the annualized cost of financingbased on the anticipated loan interest payments and repayment of loan principal.

EXAMPLE Reconsider the case of Scottsdale Co., which plans to borrow SF40 million at a fixed rate of 3 years,and obtain a loan extension for two additional years. It is now considering one alternative financingarrangement in which it obtains a floating-rate loan from a bank at an interest rate set at LIBOR + 3percent. Its analysis of this loan is provided in Exhibit 18.9 To forecast the interest payments paidon the floating rate loan, Scottsdale must first forecast the LIBOR for each year. Assume the fore-casts as shown in the first row. The interest rate applied to its loan each year is LIBOR + 3 percent,as shown in row 2. Row 3 discloses the results when the loan amount of SF40,000,000 is multipliedby this interest rate in order to estimate the interest expenses each year, and the repayment ofprincipal is also included in Year 5. The annualized cost of financing is determined as the discountrate that equates the payments to the loan proceeds of SF40,000,000. For the floating-rate loan,the annualized cost of financing is 7.48 percent. While this cost is lower than the 8 percent annual-ized cost of the 5-year fixed rate loan in the previous example, it is higher than the 7.08 percentannualized cost of the 3-year fixed rate loan and loan extension in the previous example. Based onthis comparison, Scottsdale decides to obtain the 3-year fixed rate loan with the loan extension.•

Exhibit 18.8 Comparison of Two Alternative Loans with Different Maturities for the Foreign Subsidiary

YEAR 1 YEAR 2 YEAR 3 YEAR 4 YEAR 5

5-Year Loan: Repayments Based onFixed Rate Loan of 8% for 5 Years

SF3,200,000 SF3,200,000 SF3,200,000 SF3,200,000 SF3,200,000 + Repayment ofSF40,000,000 in loan principal.

3-Year Loan Plus Extension:Repayments Based on Fixed RateLoan of 6% for 3 Years + ForecastedInterest Rate of 9% in Years 4 and 5

SF2,400,000 SF2,400,000 SF2,400,000 SF3,600,000 SF3,600,000 + Repayment ofSF40,000,000 in loan principal

Chapter 18: Long-Term Debt Financing 543

© C

enga

ge L

earn

ing.

All

right

s re

serv

ed. N

o di

strib

utio

n al

low

ed w

ithou

t exp

ress

aut

horiz

atio

n.

Hedging Interest Payments with Interest Rate SwapsIn some cases, MNCs may finance with floating rather than fixed rate debt because theprevailing floating rate debt terms offered at the time of the debt offering were morefavorable. However, if the MNCs are concerned that interest rates will rise over time,they may complement their floating rate debt with interest rate swaps to hedge the riskof rising interest rates. The interest rate swaps allow them to reconfigure their futurecash flows in a manner that offsets their outflow payments to creditors (lenders or bond-holders). In this way, MNCs can reduce their exposure to interest rate movements. ManyMNCs commonly use interest rate swaps, including Ashland, Inc., Campbell Soup Co.,Intel Corp., Johnson Controls, and Union Carbide.

Financial institutions such as commercial and investment banks and insurance com-panies often act as dealers in interest rate swaps. Financial institutions can also act asbrokers in the interest rate swap market. As a broker, the financial institution simplyarranges an interest rate swap between two parties, charging a fee for the service, butdoes not actually take a position in the swap.

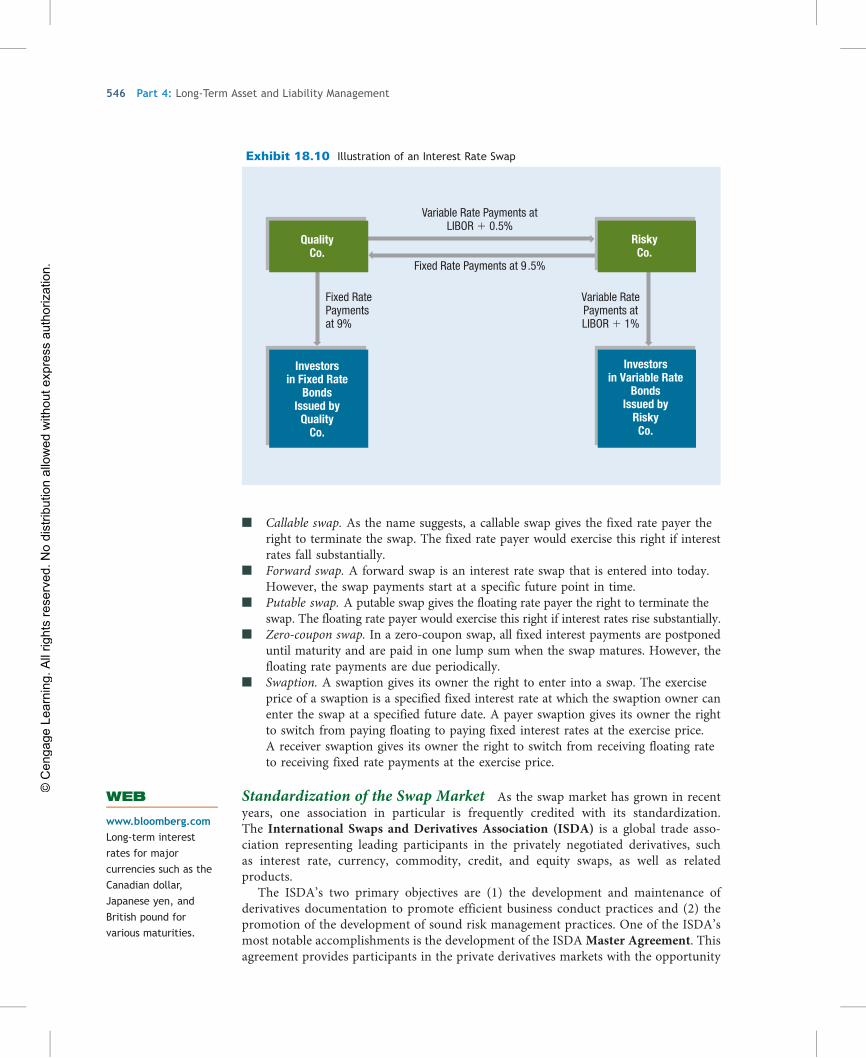

In a “plain vanilla” interest rate swap, one participating firm makes fixed rate pay-ments periodically (every 6 months or year) in exchange for floating rate payments.The fixed rate payments remain fixed over the life of the contract. The floating interestrate payment per period is based on a prevailing interest rate such as LIBOR at thattime. The payments in an interest rate swap are typically determined using some notionalvalue agreed upon by the parties to the swap in order to determine the swap payments.

The fixed rate payer is typically concerned that interest rates may rise in the future.Perhaps it recently issued a floating rate bond and is worried that its coupon paymentswill rise in the future if interest rates increase. Thus, it can benefit from swapping fixedinterest payments in exchange for floating rate payments if its expectations are correct,and the gains from the interest rate swap can offset its higher expenses from having topay higher coupon payments on the bonds it issued. Conversely, the floating rate payerexpects that interest rates may decline over time, and it can benefit from swapping floatinginterest payments in exchange for fixed interest payments if its expectations are correct.

EXAMPLE Two firms plan to issue bonds:

Exhibit 18.9 Alternative Financing Arrangement Using a Floating-Rate Loan

YEAR 1 YEAR 2 YEAR 3 YEAR 4 YEAR 5

Forecast of LIBOR 3% 4% 4% 6% 6%

Forecast of Interest Rate Applied tothe Floating Rate Loan

6% 7% 7% 9% 9%

5-Year Floating Rate Loan:Repayments Based on Floating-Rate Loan of LIBOR + 3%

SF2,400,000 SF2,800,000 SF2,800,000 SF3,600,000 SF3,600,000 + Repayment ofSF40,000,000 in loan principal.

■ Quality Co. is a highly rated firm that prefers to borrow at a variable (floating) interest rate,because it expects that interest rates will decline over time.

■ Risky Co. is a low-rated firm that prefers to borrow at a fixed interest rate.Assume that the rates these companies would pay for issuing either floating rate or fixed ratebonds are as follows:

FIXED RATE BOND FLOATING RATE BOND

Quality Co. 9% LIBOR + 0.5%

Risky Co. 10.5% LIBOR + 1.0%

WEB

www.bloomberg.com

Information about

international financing,

including the issuance

of debt in international

markets.

544 Part 4: Long-Term Asset and Liability Management

© C

enga

ge L

earn

ing.

All

right

s re

serv

ed. N

o di

strib

utio

n al

low

ed w

ithou

t exp

ress

aut

horiz

atio

n.

Based on the information given, Quality Co. has an advantage when issuing either fixed rate orfloating rate bonds but more of an advantage with fixed rate bonds. Yet Quality Co. wanted toissue floating rate bonds because it anticipates that interest rates will decline over time. QualityCo. could issue fixed rate bonds while Risky Co. issues floating rate bonds. Then, Quality could pro-vide floating rate payments to Risky in exchange for fixed rate payments.

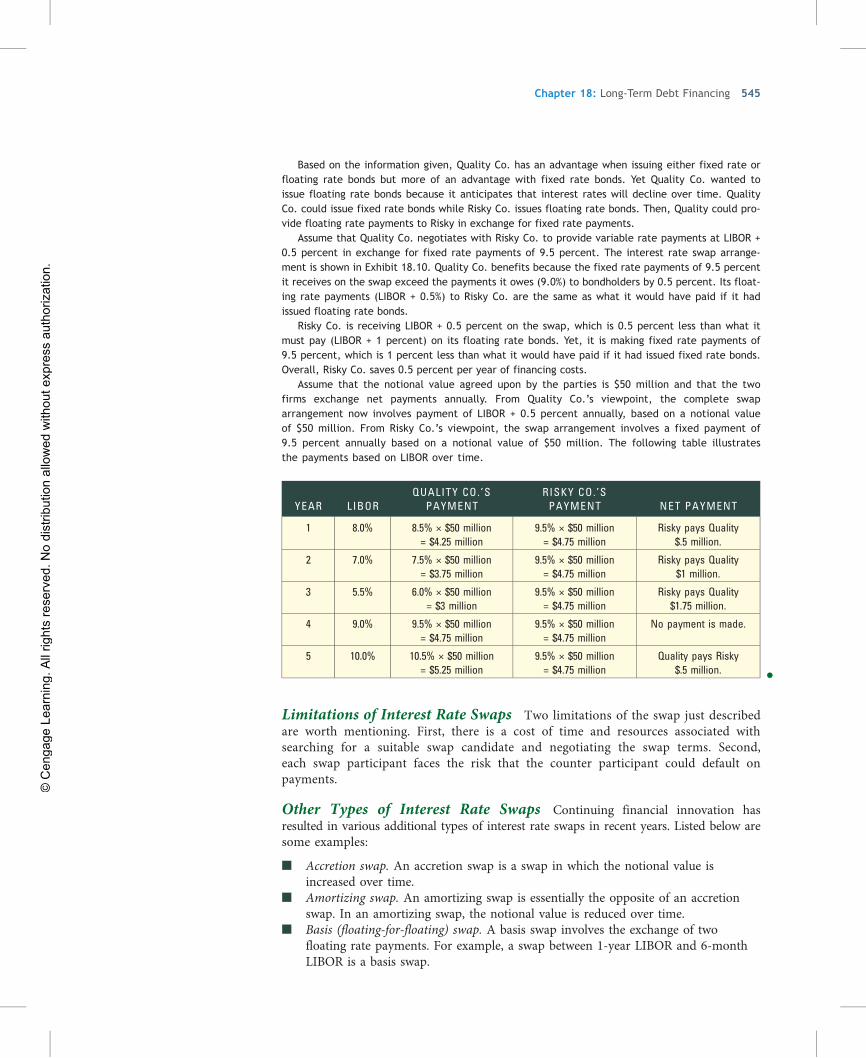

Assume that Quality Co. negotiates with Risky Co. to provide variable rate payments at LIBOR +0.5 percent in exchange for fixed rate payments of 9.5 percent. The interest rate swap arrange-ment is shown in Exhibit 18.10. Quality Co. benefits because the fixed rate payments of 9.5 percentit receives on the swap exceed the payments it owes (9.0%) to bondholders by 0.5 percent. Its float-ing rate payments (LIBOR + 0.5%) to Risky Co. are the same as what it would have paid if it hadissued floating rate bonds.

Risky Co. is receiving LIBOR + 0.5 percent on the swap, which is 0.5 percent less than what itmust pay (LIBOR + 1 percent) on its floating rate bonds. Yet, it is making fixed rate payments of9.5 percent, which is 1 percent less than what it would have paid if it had issued fixed rate bonds.Overall, Risky Co. saves 0.5 percent per year of financing costs.

Assume that the notional value agreed upon by the parties is $50 million and that the twofirms exchange net payments annually. From Quality Co.’s viewpoint, the complete swaparrangement now involves payment of LIBOR + 0.5 percent annually, based on a notional valueof $50 million. From Risky Co.’s viewpoint, the swap arrangement involves a fixed payment of9.5 percent annually based on a notional value of $50 million. The following table illustratesthe payments based on LIBOR over time.

YEAR LIBORQUALITY CO. ’S

PAYMENTRISKY CO. ’SPAYMENT NET PAYMENT

1 8.0% 8.5% × $50 million= $4.25 million

9.5% × $50 million= $4.75 million

Risky pays Quality$.5 million.

2 7.0% 7.5% × $50 million= $3.75 million

9.5% × $50 million= $4.75 million

Risky pays Quality$1 million.

3 5.5% 6.0% × $50 million= $3 million

9.5% × $50 million= $4.75 million

Risky pays Quality$1.75 million.

4 9.0% 9.5% × $50 million= $4.75 million

9.5% × $50 million= $4.75 million

No payment is made.

5 10.0% 10.5% × $50 million= $5.25 million

9.5% × $50 million= $4.75 million

Quality pays Risky$.5 million. •

Limitations of Interest Rate Swaps Two limitations of the swap just describedare worth mentioning. First, there is a cost of time and resources associated withsearching for a suitable swap candidate and negotiating the swap terms. Second,each swap participant faces the risk that the counter participant could default onpayments.

Other Types of Interest Rate Swaps Continuing financial innovation hasresulted in various additional types of interest rate swaps in recent years. Listed below aresome examples:

■ Accretion swap. An accretion swap is a swap in which the notional value isincreased over time.

■ Amortizing swap. An amortizing swap is essentially the opposite of an accretionswap. In an amortizing swap, the notional value is reduced over time.

■ Basis (floating-for-floating) swap. A basis swap involves the exchange of twofloating rate payments. For example, a swap between 1-year LIBOR and 6-monthLIBOR is a basis swap.

Chapter 18: Long-Term Debt Financing 545

© C

enga

ge L

earn

ing.

All

right

s re

serv

ed. N

o di

strib

utio

n al

low

ed w

ithou

t exp

ress

aut

horiz

atio

n.

■ Callable swap. As the name suggests, a callable swap gives the fixed rate payer theright to terminate the swap. The fixed rate payer would exercise this right if interestrates fall substantially.

■ Forward swap. A forward swap is an interest rate swap that is entered into today.However, the swap payments start at a specific future point in time.

■ Putable swap. A putable swap gives the floating rate payer the right to terminate theswap. The floating rate payer would exercise this right if interest rates rise substantially.

■ Zero-coupon swap. In a zero-coupon swap, all fixed interest payments are postponeduntil maturity and are paid in one lump sum when the swap matures. However, thefloating rate payments are due periodically.

■ Swaption. A swaption gives its owner the right to enter into a swap. The exerciseprice of a swaption is a specified fixed interest rate at which the swaption owner canenter the swap at a specified future date. A payer swaption gives its owner the rightto switch from paying floating to paying fixed interest rates at the exercise price.A receiver swaption gives its owner the right to switch from receiving floating rateto receiving fixed rate payments at the exercise price.

Standardization of the Swap Market As the swap market has grown in recentyears, one association in particular is frequently credited with its standardization.The International Swaps and Derivatives Association (ISDA) is a global trade asso-ciation representing leading participants in the privately negotiated derivatives, suchas interest rate, currency, commodity, credit, and equity swaps, as well as relatedproducts.

The ISDA’s two primary objectives are (1) the development and maintenance ofderivatives documentation to promote efficient business conduct practices and (2) thepromotion of the development of sound risk management practices. One of the ISDA’smost notable accomplishments is the development of the ISDA Master Agreement. Thisagreement provides participants in the private derivatives markets with the opportunity

Exhibit 18.10 Illustration of an Interest Rate Swap

Variable Rate Payments atLIBOR � 0.5%

Fixed Rate Payments at 9 .5%

Fixed RatePaymentsat 9%

QualityCo.

Investorsin Fixed Rate

BondsIssued by

QualityCo.

Investorsin Variable Rate

BondsIssued by

RiskyCo.

Variable RatePayments atLIBOR � 1%

RiskyCo.

WEB

www.bloomberg.com

Long-term interest

rates for major

currencies such as the

Canadian dollar,

Japanese yen, and

British pound for

various maturities.

546 Part 4: Long-Term Asset and Liability Management

© C

enga

ge L

earn

ing.

All

right

s re

serv

ed. N

o di

strib

utio

n al

low

ed w

ithou

t exp

ress

aut

horiz

atio

n.

to establish the legal and credit terms between them for an ongoing businessrelationship. The key advantage of such an agreement is that the general legal and creditterms do not have to be renegotiated each time the parties enter into a transaction.Consequently, the ISDA Master Agreement has contributed greatly to the standardiza-tion of the derivatives market.1

SUMMARY

■ AnMNC’s subsidiary may prefer to use debt financingin a currency that matches the currency it receivesfrom cash inflows. The cash inflows can be used tocover its interest payments on its existing loans.When MNCs issue debt in a foreign currency that dif-fers from the currency they receive from sales, theymay use currency swaps or parallel loans to hedge theexchange rate risk resulting from the debt financing.

■ An MNC’s subsidiary may consider long-termfinancing in a foreign currency different from itslocal (host country) currency in order to reducefinancing costs. It can forecast the exchange ratesfor the periods in which it will make loan pay-ments, and then can estimate the annualized costof financing in that currency.

When determining the debt denomination tofinance a specific project, an MNC can conductthe capital budgeting by deriving the NPV basedon the equity investment, and the cash flows fromthe debt can be directly accounted for within theestimated cash flows. This allows for explicit consid-eration of the exchange rate effects on all cash flowsafter considering debt payments. By applying this

method (which was developed in Chapter 14), anMNC can assess the feasibility of a particular proj-ect based on various debt financing alternatives.

■ An MNC’s subsidiary can select among variousavailable debt maturities when financing its opera-tions. It can estimate the annualized cost of financ-ing for alternative maturities, and determine whichmaturity will result in the lowest expected annual-ized cost of financing.

■ For debt that has floating interest rates, the interest(or coupon) payment to be paid to investors isdependent on the future LIBOR, and is thereforeuncertain. An MNC can forecast LIBOR so it canderive expected interest rates it would be chargedon the loan in future periods. It can apply theseexpected interest rates to estimate expected loan pay-ments, and can then derive the expected annualizedcost of financing of the floating rate loan. Finally, itcan compare the expected cost of financing on afloating rate loan to the known cost of financing ona fixed rate loan. In some cases, an MNC may engagein a floating rate loan, and use interest rate swaps tohedge the interest rate risk.

POINT COUNTER-POINTWill Currency Swaps Result in Low Financing Costs?Point Yes. Currency swaps have created greaterparticipation by firms that need to exchange theircurrencies in the future. Thus, firms that finance in alow interest rate currency can more easily establish anagreement to obtain the currency that has the lowinterest rate.

Counter-Point No. Currency swaps will establishan exchange rate that is based on market forces. If aforward rate exists for a future period, the swap rateshould be somewhat similar to the forward rate. If itwas not as attractive as the forward rate, theparticipants would use the forward market instead.

If a forward market does not exist for the currency, theswap rate should still reflect market forces. Theexchange rate at which a low-interest currency could bepurchased will be higher than the prevailing spot ratesince otherwise MNCs would borrow the low-interestcurrency and simultaneously purchase the currencyforward so that they could hedge their future interestpayments.

Who Is Correct? Use the Internet to learn moreabout this issue. Which argument do you support?Offer your own opinion on this issue.

1For more information about interest rate swaps, see the following: Robert A. Strong, Derivatives: An Introduction, 2e (Mason, Ohio: South-Western,2005); and the ISDA, at www.isda.org.

Chapter 18: Long-Term Debt Financing 547

© C

enga

ge L

earn

ing.

All

right

s re

serv

ed. N

o di

strib

utio

n al

low

ed w

ithou

t exp

ress

aut

horiz

atio

n.

SELF-TESTAnswers are provided in Appendix A at the back of the text.

1. Explain why a firm may issue a bond denominatedin a currency different from its home currency tofinance local operations. Explain the risk involved.

2. Tulane, Inc. (based in Louisiana), is consideringissuing a 20-year Swiss franc-denominated bond. Theproceeds are to be converted to British pounds tosupport the firm’s British operations. Tulane, Inc., hasno Swiss operations but prefers to issue the bond infrancs rather than pounds because the coupon rate is2 percentage points lower. Explain the risk involved inthis strategy. Do you think the risk here is greater orless than it would be if the bond proceeds were used tofinance U.S. operations? Why?

3. Some large companies based in Latin Americancountries could borrow funds (through issuing bondsor borrowing from U.S. banks) at an interest rate thatwould be substantially less than the interest rates intheir own countries. Assuming that they are perceived

to be creditworthy in the United States, why might theystill prefer to borrow in their local countries whenfinancing local projects (even if they incur interest ratesof 80 percent or more)?

4. A respected economist recently predicted that eventhough Japanese inflation would not rise, Japaneseinterest rates would rise consistently over the next 5 years.Paxson Co., a U.S. firm with no foreign operations, hasrecently issued a Japanese yen-denominated bond tofinance U.S. operations. It chose the yen denominationbecause the coupon rate was low. Its vice president stated,“I’m not concerned about the prediction because weissued fixed rate bonds and are therefore insulated fromrisk.” Do you agree? Explain.

5. Long-term interest rates in some Latin Americancountries tend to be much higher than those ofindustrialized countries. Why do you think someprojects in these countries are feasible for local firms,even though the cost of funding the projects is so high?

QUESTIONS AND APPLICATIONS

1. Floating Rate Bonds

a. What factors should be considered by a U.S. firmthat plans to issue a floating rate bond denominated ina foreign currency?

b. Is the risk of issuing a floating rate bond higher orlower than the risk of issuing a fixed rate bond? Explain.

c. How would an investing firm differ from a bor-rowing firm in the features (i.e., interest rate and cur-rency’s future exchange rates) it would prefer a floatingrate foreign currency-denominated bond to exhibit?

2. Risk from Issuing Foreign Currency-Denominated Bonds What is the advantage of usingsimulation to assess the bond financing position?

3. Exchange Rate Effects

a. Explain the difference in the cost of financing withforeign currencies during a strong-dollar period versusa weak-dollar period for a U.S. firm.

b. Explain how a U.S.–based MNC issuing bondsdenominated in euros may be able to offset a portion ofits exchange rate risk.

4. Bond Offering Decision Columbia Corp. is aU.S. company with no foreign currency cash flows. It

plans to issue either a bond denominated in euros witha fixed interest rate or a bond denominated in U.S.dollars with a floating interest rate. It estimates itsperiodic dollar cash flows for each bond. Which bonddo you think would have greater uncertaintysurrounding these future dollar cash flows? Explain.

5. Borrowing Combined with Forward HedgingCedar Falls Co. has a subsidiary in Brazil, where localinterest rates are high. It considers borrowing dollarsand hedging the exchange rate risk by selling theBrazilian real forward in exchange for dollars for theperiods in which it would need to make loan paymentsin dollars. Assume that forward contracts on the realare available. What is the limitation of this strategy?

6. Financing That Reduces Exchange Rate RiskKerr, Inc., a major U.S. exporter of products to Japan,denominates its exports in dollars and has no otherinternational business. It can borrow dollars at 9 percentto finance its operations or borrow yen at 3 percent. If itborrows yen, it will be exposed to exchange rate risk. Howcan Kerr borrow yen and possibly reduce its economicexposure to exchange rate risk?

7. Exchange Rate Effects Katina, Inc., is a U.S.firm that plans to finance with bonds denominated in

548 Part 4: Long-Term Asset and Liability Management

© C

enga

ge L

earn

ing.

All

right

s re

serv

ed. N

o di

strib

utio

n al

low

ed w

ithou

t exp

ress

aut

horiz

atio

n.

euros to obtain a lower interest rate than is available ondollar-denominated bonds. What is the most criticalpoint in time when the exchange rate will have thegreatest impact?

8. Financing Decision Cuanto Corp. is a U.S. drugcompany that has attempted to capitalize on newopportunities to expand in Eastern Europe. Theproduction costs in most Eastern European countriesare very low, often less than one-fourth of the cost inGermany or Switzerland. Furthermore, there is a strongdemand for drugs in Eastern Europe. Cuantopenetrated Eastern Europe by purchasing a 60 percentstake in Galena, a Czech firm that produces drugs.

a. Should Cuanto finance its investment in the Czechfirm by borrowing dollars from a U.S. bank that wouldthen be converted into koruna (the Czech currency) orby borrowing koruna from a local Czech bank? Whatinformation do you need to know to answer thisquestion?

b. How can borrowing koruna locally from a Czechbank reduce the exposure of Cuanto to exchange raterisk?

c. How can borrowing koruna locally from a Czechbank reduce the exposure of Cuanto to political riskcaused by government regulations?

Advanced Questions9. Bond Financing Analysis Sambuka, Inc., canissue bonds in either U.S. dollars or in Swiss francs.Dollar-denominated bonds would have a coupon rateof 15 percent; Swiss franc-denominated bonds wouldhave a coupon rate of 12 percent. Assuming thatSambuka can issue bonds worth $10 million in eithercurrency, that the current exchange rate of the Swissfranc is $.70, and that the forecasted exchange rate ofthe franc in each of the next 3 years is $.75, what is theannual cost of financing for the franc-denominatedbonds? Which type of bond should Sambuka issue?

10. Bond Financing Analysis Hawaii Co. justagreed to a long-term deal in which it will exportproducts to Japan. It needs funds to finance theproduction of the products that it will export. Theproducts will be denominated in dollars. Theprevailing U.S. long-term interest rate is 9 percentversus 3 percent in Japan. Assume that interest rateparity exists and that Hawaii Co. believes that theinternational Fisher effect holds.

a. Should Hawaii Co. finance its production with yenand leave itself open to exchange rate risk? Explain.

b. Should Hawaii Co. finance its production with yenand simultaneously engage in forward contracts tohedge its exposure to exchange rate risk?

c. How could Hawaii Co. achieve low-costfinancing while eliminating its exposure to exchangerate risk?

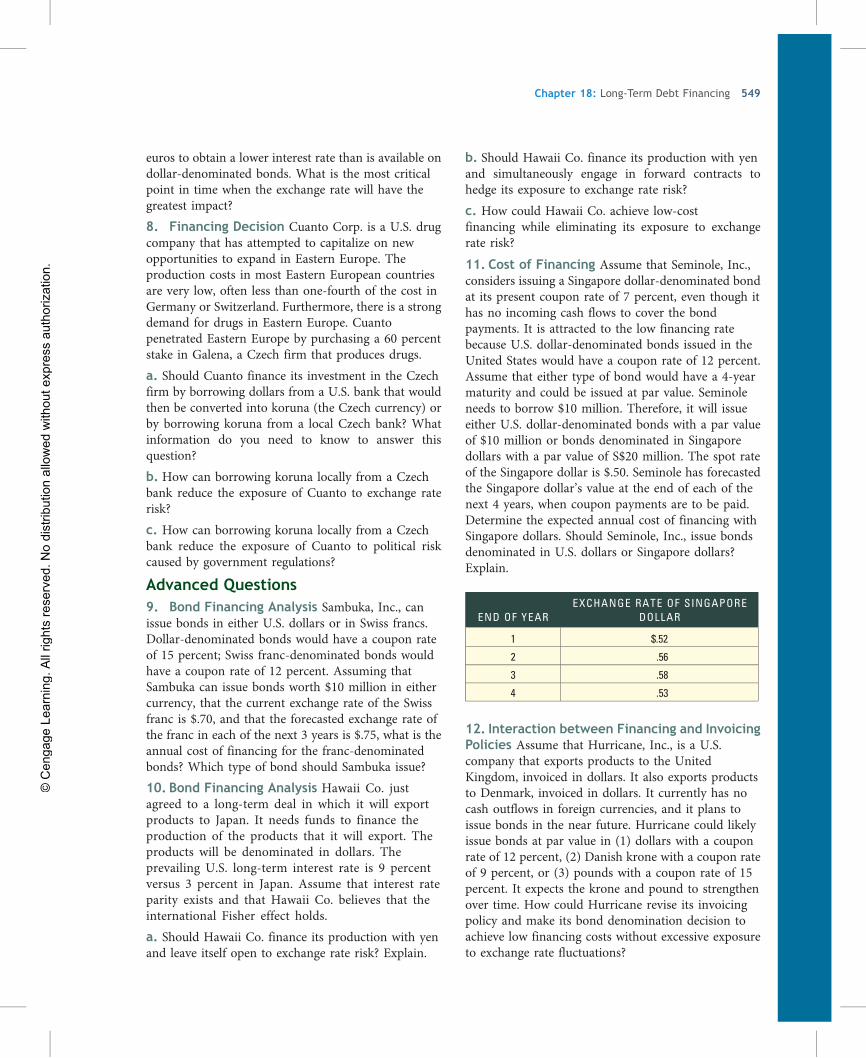

11. Cost of Financing Assume that Seminole, Inc.,considers issuing a Singapore dollar-denominated bondat its present coupon rate of 7 percent, even though ithas no incoming cash flows to cover the bondpayments. It is attracted to the low financing ratebecause U.S. dollar-denominated bonds issued in theUnited States would have a coupon rate of 12 percent.Assume that either type of bond would have a 4-yearmaturity and could be issued at par value. Seminoleneeds to borrow $10 million. Therefore, it will issueeither U.S. dollar-denominated bonds with a par valueof $10 million or bonds denominated in Singaporedollars with a par value of S$20 million. The spot rateof the Singapore dollar is $.50. Seminole has forecastedthe Singapore dollar’s value at the end of each of thenext 4 years, when coupon payments are to be paid.Determine the expected annual cost of financing withSingapore dollars. Should Seminole, Inc., issue bondsdenominated in U.S. dollars or Singapore dollars?Explain.

END OF YEAREXCHANGE RATE OF SINGAPORE

DOLLAR

1 $.52

2 .56

3 .58

4 .53

12. Interaction between Financing and InvoicingPolicies Assume that Hurricane, Inc., is a U.S.company that exports products to the UnitedKingdom, invoiced in dollars. It also exports productsto Denmark, invoiced in dollars. It currently has nocash outflows in foreign currencies, and it plans toissue bonds in the near future. Hurricane could likelyissue bonds at par value in (1) dollars with a couponrate of 12 percent, (2) Danish krone with a coupon rateof 9 percent, or (3) pounds with a coupon rate of 15percent. It expects the krone and pound to strengthenover time. How could Hurricane revise its invoicingpolicy and make its bond denomination decision toachieve low financing costs without excessive exposureto exchange rate fluctuations?

Chapter 18: Long-Term Debt Financing 549

© C

enga

ge L

earn

ing.

All

right

s re

serv

ed. N

o di

strib

utio

n al

low

ed w

ithou

t exp

ress

aut

horiz

atio

n.

13. Swap Agreement Grant, Inc., is a well-knownU.S. firm that needs to borrow 10 million Britishpounds to support a new business in the UnitedKingdom. However, it cannot obtain financing fromBritish banks because it is not yet established withinthe United Kingdom. It decides to issue dollar-denominated debt (at par value) in the United States,for which it will pay an annual coupon rate of 10 percent. It then will convert the dollar proceeds from thedebt issue into British pounds at the prevailing spotrate (the prevailing spot rate is one pound = $1.70).Over each of the next 3 years, it plans to use therevenue in pounds from the new business in theUnited Kingdom to make its annual debt payment.Grant, Inc., engages in a currency swap in which itwill convert pounds to dollars at an exchange rate of$1.70 per pound at the end of each of the next 3years. How many dollars must be borrowed initiallyto support the new business in the United Kingdom?How many pounds should Grant, Inc., specify in theswap agreement that it will swap over each of thenext 3 years in exchange for dollars so that it canmake its annual coupon payments to the U.S.creditors?

14. Interest Rate Swap Janutis Co. has just issuedfixed rate debt at 10 percent. Yet, it prefers to convertits financing to incur a floating rate on its debt. Itengages in an interest rate swap in which it swapsvariable rate payments of LIBOR plus 1 percent inexchange for payments of 10 percent. The interest ratesare applied to an amount that represents the principalfrom its recent debt issue in order to determine theinterest payments due at the end of each year for thenext 3 years. Janutis Co. expects that the LIBOR will be9 percent at the end of the first year, 8.5 percent at theend of the second year, and 7 percent at the end of thethird year. Determine the financing rate that JanutisCo. expects to pay on its debt after considering theeffect of the interest rate swap.

15. Financing and the Currency Swap DecisionBradenton Co. is considering a project in which it willexport special contact lenses to Mexico. It expects thatit will receive 1 million pesos after taxes at the end ofeach year for the next 4 years and after that time itsbusiness in Mexico will end as its special patent will beterminated. The peso’s spot rate is presently $.20. TheU.S. annual risk-free interest rate is 6 percent, whileMexico’s annual risk-free interest rate is 11 percent.Interest rate parity exists. Bradenton Co. uses the1-year forward rate as a predictor of the exchange rate

in 1 year. Bradenton Co. also presumes the exchangerates in each of years 2 through 4 will also change bythe same percentage as it predicts for year 1. Bradentonsearches for a firm with which it can swap pesos fordollars over each of the next 4 years. Briggs Co. is animporter of Mexican products. It is willing to take the1 million pesos per year from Bradenton Co. and willprovide Bradenton Co. with dollars at an exchange rateof $.17 per peso. Ignore tax effects.

Bradenton Co. has a capital structure of 60 percentdebt and 40 percent equity. Its corporate tax rate is 30percent. It borrows funds from a bank and pays 10percent interest on its debt. It expects that the U.S.annual stock market return will be 18 percent per year.Its beta is .9. Bradenton would use its cost of capital asthe required return for this project.

a. Determine the NPV of this project if Bradentonengages in the currency swap.

b. Determine the NPV of this project if Bradenton doesnot hedge the future cash flows.

16. Financing and Exchange Rate Risk The parentof Nester Co. (a U.S. firm) has no internationalbusiness but plans to invest $20 million in a business inSwitzerland. Because the operating costs of thisbusiness are very low, Nester Co. expects this businessto generate large cash flows in Swiss francs that will beremitted to the parent each year. Nester will financehalf of this project with debt. It has these choices forfinancing the project:

■ obtain half of the funds needed from parentequity and the other half by borrowing dollars,

■ obtain half of the funds needed from parent equityand the other half by borrowing Swiss francs, or

■ obtain half of the funds that are needed from parentequity and obtain the remainder by borrowingan equal amount of dollars and Swiss francs.

The interest rate on dollars is the same as theinterest rate on Swiss francs.

a. Which choice will result in the most exchange rateexposure?

b. Which choice will result in the least exchange rateexposure?

c. If the Swiss franc were expected to appreciateover time, which financing choice would result inthe highest expected net present value?

17. Financing and Exchange Rate Risk Vix Co.(a U.S firm) presently serves as a distributor of

550 Part 4: Long-Term Asset and Liability Management

© C

enga

ge L

earn

ing.

All

right

s re

serv

ed. N

o di

strib

utio

n al

low

ed w

ithou

t exp

ress

aut

horiz

atio

n.

products by purchasing them from other U.S. firmsand selling them in Europe. It wants to purchase amanufacturer in Thailand that could produce similarproducts at a low cost (due to low labor costs inThailand) and export the products to Europe. Theoperating expenses would be denominated in Thaicurrency (the baht). The products would be invoiced ineuros. If Vix Co. can acquire a manufacturer, it willdiscontinue its existing distributor business. If Vix Co.purchases a company in Thailand, it expects that itsrevenue might not be sufficient to cover its operatingexpenses during the first 8 years. It will need to borrowfunds for an 8-year term to ensure that it has enoughfunds to pay all of its operating expenses in Thailand. Itcan borrow funds denominated in U.S. dollars, in Thaibaht, or in euros. Assuming that its financing decisionwill be primarily intended to minimize its exposure toexchange rate risk, which currency should it borrow?Briefly explain.

18. Financing and Exchange Rate Risk ComptonCo. has a subsidiary in Thailand that producescomputer components. The subsidiary sells thecomponents to manufacturers in the United States.The components are invoiced in U.S. dollars.Compton pays employees of the subsidiary in Thaibaht and makes a large monthly lease payment inThai baht. Compton financed the investment in theThai subsidiary by borrowing dollars borrowed froma U.S. bank. Compton has no other internationalbusiness.

a. Given the conditions, is Compton affected favor-ably, unfavorably, or not at all by depreciation of theThai baht? Briefly explain.

b. Assume that interest rates in Thailand declinedrecently, so the Compton subsidiary considers obtain-ing a new loan in Thai baht. Compton would use theproceeds to pay off its existing loan from a U.S. bank.Will this form of financing increase, reduce, or notimpact its economic exposure to exchange rate move-ments? Briefly explain.

19. Selecting a Loan Maturity Omaha Co. has asubsidiary in Chile that wants to borrow from a localbank at a fixed rate over the next 10 years.

a. Explain why Chile’s term structure of interest rates(as reflected in its yield curve) might cause the subsidi-ary to borrow for a different term to maturity.

b. If Omaha is offered a more favorable interest ratefor a term of 6 years, explain the potential disadvantagecompared to a 10-year loan.

c. Explain how the subsidiary can determine whetherto select the 6-year loan or the 10-year loan.

20. Project Financing Dryden Co. is a U.S. firm thatplans a foreign project in which it needs $8,000,000 asan initial investment. The project is expected togenerate cash flows of 10 million euros in 1 year afterthe complete repayment of the loan (including the loaninterest and principal). The project has zero salvagevalue and is terminated at the end of 1 year. Drydenconsiders financing this project with:

■ all U.S. equity,■ all U.S. debt (loans) denominated in dollars

provided by U.S. banks,■ all debt (loans) denominated in euros provided

by European banks, or■ half of funds obtained from loans denominated

in euros, and half obtained from loans denominatedin dollars.

Which form of financing will cause the project’sNPV to be the least sensitive to exchange rate risk?

Discussion in the BoardroomThis exercise can be found in Appendix E at the backof this textbook.

Running Your Own MNCThis exercise can be found on the International Finan-cial Management text companion website. Go to www.cengagebrain.com (students) or login.cengage.com(instructors) and search using ISBN 9781133435174.

BLADES, INC. CASE

Use of Long-Term FinancingRecall that Blades, Inc., is considering the establish-ment of a subsidiary in Thailand to manufactureSpeedos, Blades’ primary roller blade product. Alterna-

tively, Blades could acquire an existing manufacturer ofroller blades in Thailand, Skates’n’Stuff. At the mostrecent meeting of the board of directors of Blades,

Chapter 18: Long-Term Debt Financing 551

© C

enga

ge L

earn

ing.

All

right

s re

serv

ed. N

o di

strib

utio

n al

low

ed w

ithou

t exp

ress

aut

horiz

atio

n.

Inc., the directors voted to establish a subsidiary inThailand because of the relatively high level of controlit would afford Blades.