Embed Size (px)

Citation preview

Local TV Stations and Digital Advertising Executive Interviews with Buyers and Sellers

Confidential Report for TVB

November 9, 2016

©2016, All Rights Reserved, BIA/Kelsey, Chantilly, VA.

Contents Executive Summary ....................................................................................................................................... 2

Part 1: Setting the Stage: BIA/Kelsey's Local Ad Market Insights ................................................................. 4

Part 2: BIA/Kelsey Study of Local TV Sellers and Buyers ............................................................................... 8

Part 3: Perception versus Reality .................................................................................................................. 9

Part 4: A Deeper Dive into Our Interviews.................................................................................................. 12

Part 5: Recommendations .......................................................................................................................... 26

Appendix A: Interviewees ........................................................................................................................... 29

Appendix B: BIA/Kelsey’s Local TV and Digital Offerings SWOT Analysis ................................................... 30

List of Figures

Figure 1. Top 5 Local Ad Media in 2017 (Source: BIA/Kelsey, 2016) ............................................................ 4

Figure 2. Digital to Account for 43.6% of Total Local Ad Spend by 2021 (Source: BIA/Kelsey, 2016) .......... 4

Figure 3. Ad Revenue by Media Platforms Delivering Local Audiences (Source: BIA/Kelsey, 2016) ............ 5

Figure 4. Shift Toward Digital in Local Ad Spending (Source: BIA/Kelsey, 2016) .......................................... 5

Figure 5. Local Video Ad Growth 2016-2012 by Segment (Source: BIA/Kelsey, 2016) ................................. 6

List of Tables

Table 1. Top Ten Ad Billers in New York Television Market (Source: BIA/Kelsey, 2016) .............................. 6

Table 2. Sellers and Buyers: Perception versus Reality (Source: BIA/Kelsey, 2016) ..................................... 9

Table 3. SWOT Analysis of Local TV Station Digital Sales (Source: BIA/Kelsey, 2016) ................................ 30

Local TV Stations and Digital Advertising

Confidential 2 BIA/Kelsey

Executive Summary In the dynamic local advertising market, local TV stations of course are major players. As these stations

further expand into the adjacent digital advertising marketplace, we expect to see new market

dynamics. To assess the relative merits of local TV's digital offerings and how stations might improve

their digital revenue growth opportunities, TVB commissioned BIA/Kelsey to interview local TV sellers

and buyers.

TVB's overall goals of the study were to identify:

Key strengths of broadcast stations’ digital offerings including stations own website, mobile, and

digital ad networks our stations sell.

Significant and appreciable differences between local broadcast assets and competitors’ assets

to inform sales.

Perceived barriers/challenges to using broadcast TV stations digital assets in order to find

solutions.

Local TV Sellers

Based on our interviews with TV sellers, we've identified a core set of value propositions for digital

products and services that sellers feel they offer the marketplace:

Local TV Offers Digital Premium Content

Local TV Offers Trusted Relationships

Integrated solutions

Unique Inventory

Audience Targeting

Validating Local Audiences

Local TV Buyers

There is concurrence but also some gaps in perception versus reality between sellers and buyers.

Agencies and marketers are more driven than sellers by data and cost-efficiency and looking for

more integrated cross-platform video impressions.

Local TV sellers are offering digital as a value add to broadcast in what buyers sometimes

perceive as half-hearted selling efforts.

Increased spend on local TV's digital offerings sometimes comes as a reallocation of the TV

budget across linear and digital offerings.

Measurement services and confusing rules surrounding metrics create adverse confusion. With

more market education on the buyer and seller sides, better measurement and reporting, and a

commitment to developing and servicing quality digital solutions, we see significant upside for

local TV and their digital offerings. However, the competition in digital will increase.

Local TV Stations and Digital Advertising

Confidential 3 BIA/Kelsey

Based on this study and key learnings, BIA/Kelsey offers these recommendations for local TV sellers:

1. Increase Digital Knowledge, Skills, Experience: Continuing to educate local TV sales team and

clients on digital but also work on building capabilities to distinguish some key products that

make sense for the client in question.

2. Clearly Differentiate Benefits of Local TV Premium Content. Buyers concur that local stations

offer unique and valuable content. What they'd like to see more of is what quantifiable value

this can offer to them in terms of delivering audiences over-indexing in their target segments or

how this high value content delivers more engaged audiences that can benefit marketers.

3. Develop Digital Packages that Are Measurable and Sustainable: Selling integrated broadcast

and a wide variety of digital offers may not be a profitable option for TV sellers in the long term.

It is important to select a package of digital services that both address buyers' needs and that

make good business sense for the stations. Margins should be examined to determine if low

ticket sales are worth the effort.

4. Audience Extension Can be a Double-Edged Sword: Often digital buyers require a larger volume

of digital video impressions than the Local Station can deliver, and Local TV stations may extend

their own digital audiences by going to ad networks and programmatic exchanges. While

servicing buyer’s immediate needs, long term this may impact station’s digital profits and make

them more vulnerable to defection.

5. Digital Packages Should Be Based on and Fulfill Client Needs: Local TV can become more

systematic in offering a set of digital offers that are both more curated and focuses on clients'

needs and their ability to fulfill and service these products. There is a perception that some

sellers are simply trying to be all things to clients to make a sale. This could backfire if the

station is not set up to service.

6. Campaigns Need Better Local Measurement Tools, Metrics, Transparency: There is significant

confusion and the lack of measurement services has made it difficult to determine best solution

for clients and stations. If the marketplace pushes for KPIs that require measurement

guarantees across a wide number of providers, it could be less beneficial for stations to pursue.

7. Seek the Opportunities that Exist with National Brands Spending More to Target Local

Audiences in Digital: BIA/Kelsey forecasts that spending by national advertisers targeting local

audiences will grow nearly $11 billion from $61.5 billion in 2016 to $72.4 billion by 2020.

Programmatic exchanges and data management platforms are adding efficiencies to the buyer

challenge of reaching target audience segments and clearing inventory with geographic criteria.

Programmatic and data-driven audience targeting is rapidly becoming the norm in the digital

advertising world and soon the clear majority of digital trading will flow through programmatic

platforms and ad exchanges.

Local TV Stations and Digital Advertising

Confidential 4 BIA/Kelsey

Part 1: Setting the Stage: BIA/Kelsey's Local Ad Market Insights BIA/Kelsey analyzes media advertising platforms delivering local audiences and provides advertising

forecasts, market share and other analytics and insight for 16 media including local TV and digital.

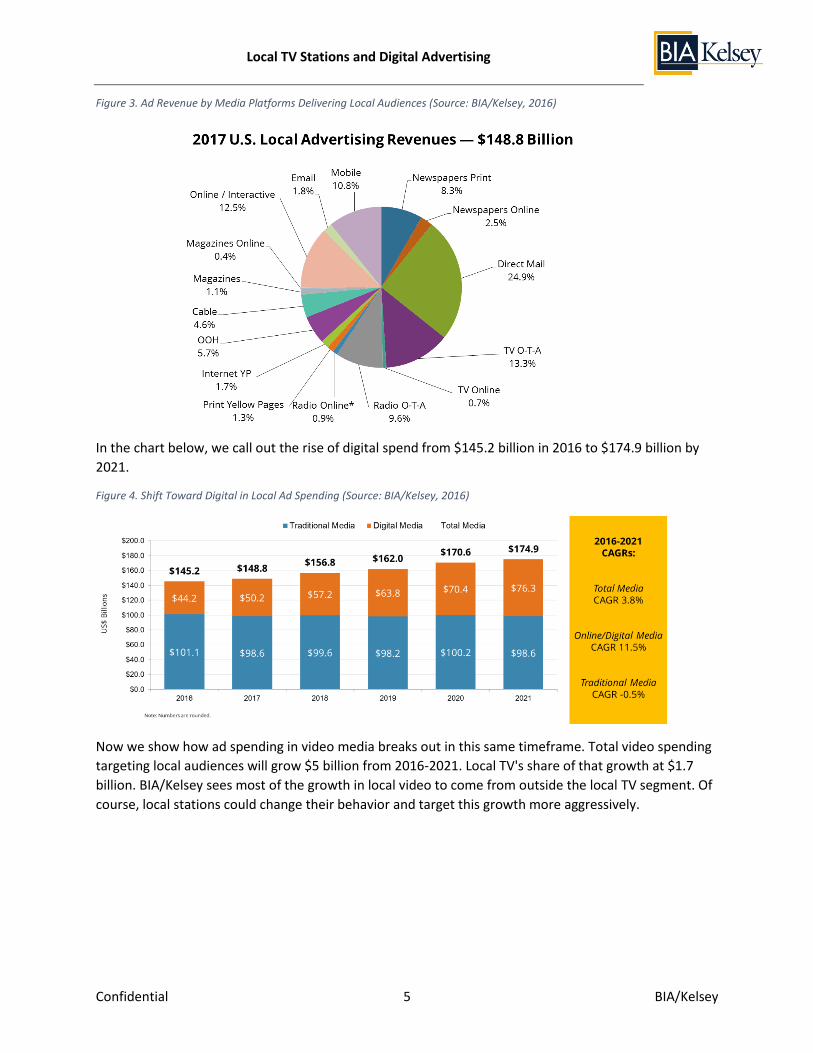

Looking at the total U.S. advertising market, BIA/Kelsey estimates that in 2017 $148.8 billion will be

spent targeting local audiences. Local TV at $20.9 billion in ad revenues ranks second behind Direct Mail.

Figure 1. Top 5 Local Ad Media in 2017 (Source: BIA/Kelsey, 2016)

Overall, about 30% of this total spending goes to digital media, the rest to traditional media like

broadcast TV. BIA/Kelsey forecasts that digital spending will grow to 43.6% of the ad spend targeting

local audiences by 2021, or $76.3 billion. Thus, the local market for digital advertising, already

significant, is growing fast and at the expense of traditional media. Digital will grow at 11.5% CAGR

versus a projected flat (-0.50%) growth for traditional media. For local TV, we forecast a 1.5% CAGR for

the 2016-2021 period as a point of comparison.

Figure 2. Digital to Account for 43.6% of Total Local Ad Spend by 2021 (Source: BIA/Kelsey, 2016)

Local TV stations will capture 13.3% of the 2017 total ad spend with their ("OTA" or over-the-air)

broadcast platform and another 0.7% of the total spend with their digital products. Digital revenues

typically come to about 5% of total local TV station revenue, though there are keen exceptions where

we've seen double digit revenue share coming from the digital side of local TV sales efforts.

Local TV Stations and Digital Advertising

Confidential 5 BIA/Kelsey

Figure 3. Ad Revenue by Media Platforms Delivering Local Audiences (Source: BIA/Kelsey, 2016)

In the chart below, we call out the rise of digital spend from $145.2 billion in 2016 to $174.9 billion by

2021.

Figure 4. Shift Toward Digital in Local Ad Spending (Source: BIA/Kelsey, 2016)

Now we show how ad spending in video media breaks out in this same timeframe. Total video spending

targeting local audiences will grow $5 billion from 2016-2021. Local TV's share of that growth at $1.7

billion. BIA/Kelsey sees most of the growth in local video to come from outside the local TV segment. Of

course, local stations could change their behavior and target this growth more aggressively.

Local TV Stations and Digital Advertising

Confidential 6 BIA/Kelsey

Figure 5. Local Video Ad Growth 2016-2012 by Segment (Source: BIA/Kelsey, 2016)

To give a market-specific view of the advertising landscape, we present in the table below the Top Ten

ad billers in the New York television market. Google is the #1 biller by far. Again, for these estimates we

are counting only ad spend that has some type of local signal designated in the audience targeting.

Table 1. Top Ten Ad Billers in New York Television Market (Source: BIA/Kelsey, 2016)

Our expectation is that there is significant potential upside for local television groups and stations to

target revenue growth from digital media platforms including their owned and operated websites,

mobile apps and other bundled solutions such as SEO/SEM, listings, reputation management, audience

extension and other services that are often provided by white label vendors. However, digital selling

requires different partnerships, expertise, fulfillment and service and market approaches than

traditional TV selling.

Rank Company Media Type 2015 (000s)Share of Total

Market

1 Google Online/Digital $771,492 7.64%

2 New York Times Company Local Newspaper $448,908 4.44%

3 News Corporation (New) Local Newspaper $353,002 3.49%

4 Comcast/NBC Local Television $312,897 3.10%

5 Fox Television Local Television $286,944 2.84%

6 ABC/Disney Local Television $284,006 2.81%

7 CBS Radio Local Radio $215,292 2.13%

8 CBS TV Local Television $211,046 2.09%

9 iHeartMedia Local Radio $207,137 2.05%

10 Cablevision Systems Corp Local Newspaper $182,350 1.80%

Note: Some of the other nationwide digital companies generated roughly the following amounts in this market (000s):

Facebook $157,595 Bing $69,693 Yahoo $57,514 AOL $44,129 Yelp $43,034 Pandora $29,589 Twitter $27,527

Top Ten Billers of AdvertisingNew York, NY

Local TV Stations and Digital Advertising

Confidential 7 BIA/Kelsey

Two secular trends that clearly benefit local TV are increasing demand for video ad inventory generally,

and an increase in spending by national advertisers targeting local audiences. Indeed, BIA/Kelsey

forecasts that spending by national advertisers targeting local audiences will grow nearly $11 billion

from $61.5 billion in 2016 to $72.4 billion by 2020. One thing we heard from agencies serving national

marketers is that they just don't understand local and how local targeting drives higher ROI. Still, given

the spending levels we are forecasting, we're confident the industry is beginning to factor the value of

local in at a higher level.

We wanted to include this overall to demonstrate the opportunity of local digital advertising as it exists

now and how it will grow by 2021 to frame the context of this study. In this study we collect insights and

assessments from local TV buyers and sellers to document insights, experiences and recommendations

for how local TV digital selling efforts are faring in the marketplace and what changes may be

recommended to enhance local TV's digital advertising future.

Local TV Stations and Digital Advertising

Confidential 8 BIA/Kelsey

Part 2: BIA/Kelsey Study of Local TV Sellers and Buyers BIA/Kelsey study for TVB examined what differentiates local television stations' digital offerings from

their competition from both sellers' and buyers' points of view. In particular, our goal was to understand

which of these differences resonate most with advertisers and agencies.

TVB's overall goals of the study were to identify:

Key strengths of broadcast stations’ digital offerings including stations own website, mobile, and

digital ad networks our stations sell.

Significant and appreciable differences between local broadcast assets and competitors’ assets

in order to inform sales.

Perceived barriers/challenges to using broadcast TV stations digital assets in order to find

solutions.

From the buying community, TVB wanted to, "determine which of the points identified from

above interviews, resonates most with advertisers/agencies to motivate future

consideration/sales of TV stations’ digital assets; see if there are any points not identified by TVB

members that they feel is a distinct advantage and identify the barriers/challenges in doing

digital business with local stations."

Methodology

The study's methodology was to conduct in-depth interviews with TVB members, agencies, and clients.

We completed 18 interviews overall with 10 buyers (agencies and clients) and 8 local TV sellers (groups

and stations). See Appendix A for a list of the interviewees participating in this study. The overall value

of this cross section of sales and buy side decision makers demonstrated a significant variety of views

that are fueling local digital advertising perceptions today.

We had two parts to our interviews process. First, we interviewed TV sellers to understand their value

propositions, perceived strengths, appreciable differences, and challenges for their digital assets. From

those interviews, we distilled several topical themes related to the value propositions local TV stations

offer marketers and agencies. We then queried the buy-side about these value propositions.

Local TV Stations and Digital Advertising

Confidential 9 BIA/Kelsey

Part 3: Perception versus Reality Local TV Sellers' Value Propositions

From our interviews with station executives, we developed a deep understanding of their perceived

value propositions for digital offers. We'll go into these in a moment and how buyers further assessed

these value points.

The value propositions converged on these main themes and we'll organize our analysis around these

themes about what local TV stations offer buyers with their digital initiatives:

Premium Content

Trusted relationships

Integrated Solutions

Unique Inventory

Audience Targeting

Validating Local Audiences

Sellers and Buyers: Perception versus Reality

Now let's turn to a detailed comparison of the perceptions of sellers' value propositions versus the

realities of how marketers and agencies view these offerings.

We summarize these perceptions versus reality findings in the table below.

Table 2. Sellers and Buyers: Perception versus Reality (Source: BIA/Kelsey, 2016)

Perception Seller POV Buyer POV

Local TV Digital Premium Content Value proposition: Stations are well known and respected versus digital competition (brand equity) and offer audiences attracted to premium content.

Local TV stations have well known and trusted brands in the market.

Local station brands are particularly strong for news stations.

Stations attract valuable audiences with premium network programming, local news and special event programming.

Agency and client side interviewees acknowledged the value of localized content and relevance to the market.

For some buyers, it is important to be associated with community leadership and supporting the local TV station can accomplish some of this.

Even so, buyers want more qualitative data to better understand the relationship between the audiences delivered by local stations.

Bottom line is that even with high value station brands, buyers are driven to data.

Unless stations can quantify the value of their brand and

Local TV Stations and Digital Advertising

Confidential 10 BIA/Kelsey

Perception Seller POV Buyer POV

premium content, buyers may go to pure play digital platforms delivering impressions from audiences that over-index against their targets.

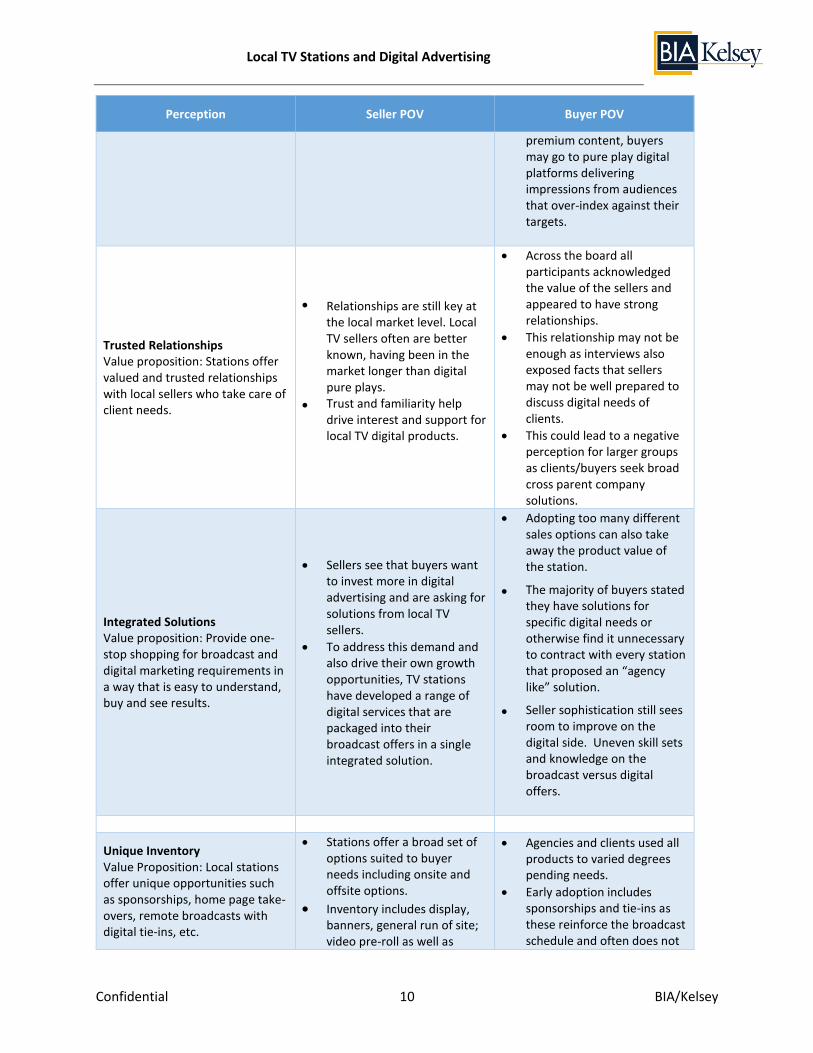

Trusted Relationships Value proposition: Stations offer valued and trusted relationships with local sellers who take care of client needs.

Relationships are still key at the local market level. Local TV sellers often are better known, having been in the market longer than digital pure plays.

Trust and familiarity help drive interest and support for local TV digital products.

Across the board all participants acknowledged the value of the sellers and appeared to have strong relationships.

This relationship may not be enough as interviews also exposed facts that sellers may not be well prepared to discuss digital needs of clients.

This could lead to a negative perception for larger groups as clients/buyers seek broad cross parent company solutions.

Integrated Solutions Value proposition: Provide one-stop shopping for broadcast and digital marketing requirements in a way that is easy to understand, buy and see results.

Sellers see that buyers want to invest more in digital advertising and are asking for solutions from local TV sellers.

To address this demand and also drive their own growth opportunities, TV stations have developed a range of digital services that are packaged into their broadcast offers in a single integrated solution.

Adopting too many different sales options can also take away the product value of the station.

The majority of buyers stated they have solutions for specific digital needs or otherwise find it unnecessary to contract with every station that proposed an “agency like” solution.

Seller sophistication still sees room to improve on the digital side. Uneven skill sets and knowledge on the broadcast versus digital offers.

Unique Inventory Value Proposition: Local stations offer unique opportunities such as sponsorships, home page take-overs, remote broadcasts with digital tie-ins, etc.

Stations offer a broad set of options suited to buyer needs including onsite and offsite options.

Inventory includes display, banners, general run of site; video pre-roll as well as

Agencies and clients used all products to varied degrees pending needs.

Early adoption includes sponsorships and tie-ins as these reinforce the broadcast schedule and often does not

Local TV Stations and Digital Advertising

Confidential 11 BIA/Kelsey

Perception Seller POV Buyer POV

sponsorship and page takeovers.

require any measurement KPI.

Sponsorships largely are used by local clients within the market who already utilize the stations and feel comfortable using the digital extension.

Cost efficiency seems to prevail and the wider use of individual local digital options is limited within the national agencies.

Individual clients have limited budgets and appear to utilize a smaller number of stations for digital efforts which may follow the same share percentage they extend to broadcast.

Validating Local Audiences Value Proposition: Station owned and operated websites focus on an individual market so station can demonstrate the audience sourcing and reach versus a larger aggregator who may not be able to track back to the individual local audience.

Google analytics generally used for target delivery.

Client needs for data verification are inconsistent.

Buyers had varied sophistication or understanding of what the proper KPIs should be for video only product or non-video online digital.

Buyer/client experienced sellers' knowledge as inconsistent and this increased frustration or confusion.

One thing that surfaced loud and clear in the study is that while Sellers would like to consider as a Value Proposition their ability to deliver local audiences, this is actually more of a challenge at the moment than an Accepted Value Proposition.

Local TV Stations and Digital Advertising

Confidential 12 BIA/Kelsey

Part 4: A Deeper Dive into Our Interviews In the previous section, we highlighted sellers' value propositions versus the realities of how marketers

and agencies view these offerings. In this section, we want to take a deeper dive into our interviews on

the thinking behind those highlights and the business aspects of selling/buying digital.

TV Sellers

From our interviews with local TV sellers, we developed six high level take-aways:

1. There is broad sentiment shared among sellers about the current state of digital in local TV.

2. Sales processes and structures vary by stations and markets.

3. Product sets are evolving.

4. Client results are tied to platforms and goals.

5. Revenue from digital is strategic but small relative to overall station revenue.

6. Audience extension brings in more data-driven audience targeting

Broad Sentiments Shared Among Sellers

The market for local digital advertising, where certainly facing disruption, innovation and both new

entrants and firms leaving the market – it is becoming a mature part of the advertising mix. TV sellers

are seeing a more entrenched market that is looking not just for the next solution that comes out but for

integrated, trusted solutions.

One thing we saw on the buy side is that the way they are organized varies a bit. At the agencies, some

are still organized into national and local teams, broadcast and digital teams. As the current market

starts to blur these distinctions, we are in a period of disruption as both sellers and buyers reassess how

to best organize their business processes and workflow. Inertia, confusion and an array of tools and

techniques in the buying/selling dialogue can frustrate even the most committed buyer who might be

interested in local TV's broadcast and digital inventory. From local TV's perspective, it is important to the

selling outcome whether their offers get viewed through buyers' broadcast budget and campaign plan

only or if they can also get access to the increasing larger digital budgets.

Here's a representative sampling of the insights from our sales side interviews.

As media device and content choices expand, it has enabled broader advertising sales channel

opportunities but also greater competition for both local and national advertising dollars.

Digital buyers at all levels are gaining more experience and practice with different channels

making it more challenging to bring on board if they are satisfied with alternative channels that

provide similar options (i.e., Google or Facebook may offer options that advertisers feel to be

sufficient for their results and don’t need to add in more options).

Digital buyers are also overwhelmed with choices and sales pitches making it hard to cut

through the noise.

Relationships are still key at the local market level.

Trust and familiarity help drive interest and support for local TV digital products- Brand still

means something- news stations more specifically.

Local TV Stations and Digital Advertising

Confidential 13 BIA/Kelsey

TV station brand has value for competitive differentiation.

Local SMB community is still developing digital practices and offer promising potential business

growth for local stations.

Sales Processes and Structures Vary

TV sellers adopt different approaches to selling digital offers in their markets. There has been an

industry discussion about how to most effectively sell digital – with digital-only sales teams, or cross-

functional sellers who offer both traditional broadcast TV with digital solutions. A number of

broadcasters have tried the digital-only sales force approach but been disappointed over time with the

performance of this sales strategy. Much more so these days, TV sellers represent the full range of

station offers to the marketplace. However, we still see some broadcasters with separate sales forces

where they feel it makes sense. In larger markets, the economies of scale can support separate sales

forces given the level of opportunity in those markets. In other cases, there will be a core digital team

trained as experts less in the sales side as much as in the technology, execution, analytics and reporting

of digital advertising. These teams often are housed at the group level or actually this function can be

outsourced to digital agencies as another option.

There are probably three main drivers to fielding sales teams that service both broadcast and digital

solutions. First, the expense and complexity of running two different sales teams has become

increasingly impractical. Second, what the marketplace wants is an integrated marketing solution that

addresses their needs in a cost-effective and efficient solution. Having two sales teams from every

station calling on them has proven less effective over time. Clients who are interested in giving a station

their business want to speak to the station's full range of capabilities with one sales team. And finally,

the third reason is that stations that effectively combine their range of broadcast and digital offers into

effectively sold and serviced packages are driving higher revenue growth.

From our interview series with TV sellers on the topics of sales process and structures, here are some

highlights:

There remains a varied approach across groups with digital-only sellers or integrative sellers

who represent both TV and Digital.

Market size and digital sales opportunity does offer rationale for a digital only sales force as

reported by some groups.

Having a Digital Sales Manager who see and operates against the big picture is critical at all

stations even if sales people are integrated traditional-digital sellers.

One drawback with hiring digital experts is that they may not have TV knowledge which can

hinder cross platform educational selling. Broadcasters report it is often easier to train TV sellers

on digital than to integrate digital sellers.

Sales models are evolving as general market buyers integrate more digital into their jobs.

True digital buying, including impression goals and delivery is not always the only entry point

into digital. Some TV buyers are using web page contests or small promotions to incorporate a

digital buy. This may or may not be cannibalizing TV budgets.

Local TV Stations and Digital Advertising

Confidential 14 BIA/Kelsey

Seller sophistication still sees room to improve. Changing landscape and market needs or client

needs may hinder learning curve.

Groups who have adapted a corporate oversight of digital sales opportunities and products for

integration with the sales teams have seen value in extending education.

Expanding small business and local business coverage is seen as an untapped opportunity but

will also likely mean they have to put more labor against the sales to cover the accounts.

Even as programmatic selling has dramatically impacted the digital advertising community, it is

still early days in broadcast television. Local TV is not selling broadcast programmatically,

thought there is some programmatic selling on the digital side.

Product Sets Evolving

Exactly what local TV stations go to market with in their digital offerings is in flux. Too many options get

confusing even when just one station brings these to the market, let alone a variety of stations bringing

a confusing mix to clients trying to understand the differences and complexities.

Some digital products, such as stations' owned-and-operated websites and mobile apps are core

components to the digital product sets brought to the market. But in a marketplace increasingly looking

for digital video impressions, audience targeting at scale, analytics and accountability these products are

facing some challenges. Websites and apps tend to be sold on a sponsorship basis. That works fine for

some clients and campaigns but data-driven audience planning and buying certainly is on the rise.

The types of viewpoints we heard in our interviews are represented here:

Broadcast content is rendered cross-platform to create inventory and attract audiences – news,

weather, sports, traffic.

Very different response across groups/stations. Some see a profit in shifting their own inventory

toward third-party sellers while others feel they can sell it more effectively and at a premium

locally. Some stations have a noticeable amount of digital only sales while others have only a

few.

Display, banners and general run of site; video pre-roll as well as sponsorship and page

takeovers. Seek to promote sponsorships with local clients to insure long term contracts.

Native and video inventory drive higher CPMs.

Groups see measurement and the value of their own product that has developed in market to

be of premium value - early adopter stations have longer history with success metrics but see

market continuously evolving sports, news, weather apps are seen as valuable to seller

community.

Larger groups who have more markets/inventory are seeing benefits in managing these

inventory exchanges but it requires dedicated yield manager at the group level.

Sellers see that the impression aggregators may be reselling their own inventory along with

other third party inventory that could be blocked by them if they choose

Local TV Stations and Digital Advertising

Confidential 15 BIA/Kelsey

There is some indication that certain sellers are acting as a digital agency and helping clients

purchase their audience extension impressions as no single station can fulfill the audience

impressions on their own

Labor allocation and margins are a big question surrounding most digital sales plans. How deep

do you go, and what cut off should you limit for the long tail of digital buys. Some groups apply

these minimums but it varies by opportunity and market size.

Client Results Tied to Platforms and Goals

Sellers report that clients have various goals for their ad campaigns that are tied to their media plan and

allocations to different channels they see as effective in the marketing funnel.

As you'd expect, TV is more top of the funnel whereas digital drives more to engagement and activation

goals and so do different goals and metrics apply to TV versus digital.

Sellers report that their buyers do want to see more cross-platform attribution from them. In other

words, when buying broadcast and digital from a local TV station, clients want to see the combined

effect of the package not siloed results. This reflects growing sophistication in the market around

marketing mixes, optimization, and attribution at a time when budgets under scrutiny require more

efficiency and effectiveness.

Cross-checking and validation of local digital buys can be difficult for sellers and agencies and there is a

need to educate ecosystem. Difficulty arises with third party aggregators that promise low cost

impressions that may or may not be in market- lack of forensic measurement or validation. Most digital

sellers still use Google analytics to defend digital metric. ComScore and Nielsen are used for the video

measurement in some cases.

Revenue Growth is Small but Strategic

As we noted at the beginning of this report, digital revenues for local TV stations in 2016 will amount to

only about 5% of their total industry revenue line. In addition to be much smaller than the broadcast

revenue line, digital sales are lower margin, more complex, require different management and training

and can be hard to package into broadcast selling initiatives. So why the focus on digital? Because it

represents both paths to strategic growth and competitive opportunity.

Here's how local TV sellers view digital sales revenue opportunities:

Over overall goal points to the desire to control the sale and insure capture of highest budget,

not just the TV budget.

Revenue from digital is growing in low single to high teens across most groups on an annual

basis but typically represents well under 10% of their total revenue.

Large groups or stations that have captured large market share for several years see the lower

single digit increases, as they’re seeing they’ve already tapped the revenue opportunity (also at

a higher base for percentage comparisons).

Local TV Stations and Digital Advertising

Confidential 16 BIA/Kelsey

Stations with higher digital growth rates are newer to the digital game and are benefiting from

“catch-up” growth (e.g., earlier sales are the easier sales and lower base for percentage

purposes).

SMBs and other local businesses are listed as the best untapped opportunity to tap additional

digital sales dollars in the near term.

Audience Extension Brings Data-Driven Audience Targeting

Broadcasters sell based on gender/age ratings demos for their over-the-air product. However, they

cannot bring that metric to the audiences gathered on their websites and mobile apps. In fact, these

digital platforms will attract some of the broadcast audience but also audience segments that

broadcasters might not otherwise attract to their broadcast platforms. Of course, the Holy Grail is to

attract digital audiences and then convert them to the broadcast platform where they can more easily

be monetized. However, there is limited ability to do this. And advertisers want the kind of extended

audience reach they can add to their broadcast audiences over digital platforms.

One issue for broadcasters is that while over-the-air they may well attract the biggest audiences in the

market, they cannot be targeted well beyond gender/age. When broadcasters develop digital audiences,

while still significant, the overall size of these in-market audiences for single stations is insufficient to

deliver sizeable enough specific audience targets that digital buyers want.

Here's few observations from broadcasters:

TV's ability to extend audiences from broadcast to digital is a key selling point for digital

products to reach segments underserved by broadcast and/or to serve broadcast audiences in

multiple touchpoints across platforms.

Broadcasters add value we can show that we are not limited to our TV audience only. TV

stations have products that appeal to new audiences who otherwise may not view the stations

regularly.

Groups that have built out their own content channels and additional product offerings across

holding company may have an advantage to attract dollars beyond their direct market as it

enables them to compete outside their core geography, their television market. Some have

actually garnered national buys as a result of the wider geography offered.

In some cases, TV stations do reap a premium CPM but it is not consistent across markets or

sellers.

Additional Insights from TV Sellers

Beyond what we've already shared from sellers, we did hear loud and clear that there is a commitment

to building audiences and business opportunities across platforms. The path may not be clear but the

need and opportunity are forefront.

Here are some additional insights from our local TV seller interviews:

There are long term needs for consistency and driving local value of the TV/digital content is key

to success in the eyes of many.

Local TV Stations and Digital Advertising

Confidential 17 BIA/Kelsey

No one wants to lose business on one side in order to gain in another and the value of using

digital as an extension to the TV buy is gaining traction

Measurement cross channel is still difficult even for groups that are using impression buying for

TV. Different methodologies and audiences are used to buy TV versus digital

Stations continue to question the complexity of the sales process and continuous shifts of needs

in the market.

Majority dependent on a third party for data management systems- could be an opportunity to

gain more control but is beyond the resource and capital budgeting for many

As digital offerings expand and new standards of terms change it becomes incumbent on the TV

groups to stay current but also stay true to what they do best.

Determination of where resources and focus should apply are important considerations as the

groups move forward.

Interviews with Marketers and Agencies

On the buyer side of the equation, both at agencies and with clients, the whole marketing business has

been changing for them. Businesses that have long favored local TV advertising are now motivated to

allocate more spend to digital video because of its audience targeting, analytics and attribution

capabilities.

Of course, long-time buyers have established relationships with local TV sellers they view as trusted

professionals representing quality brands and premium content. This means a lot in the marketplace.

But as newer buyers come in to the mix, budgets are challenged, and the press for demonstrable ROI

grows more urgent, in many ways digital is doing a better job of answering the call.

We saw these key themes emerge in our buyer interviews:

Station brand equity and premium content is a positive factor.

Agencies and markets acknowledge and respect their trusted relationships with local TV sellers.

Buyers are open to local TV sellers' offers of providing integrated solutions.

Accountability matters to buyers, with tighter budgets and more ad platform choices, they need

more metrics and data to drive buying decisions.

Unique and valuable content offered by local TV stations is attractive but still needs to be tied to

outcomes in audience targeting and content that helps audience engagement with ads.

Audience targeting varies by buyer goals. Stations will be more effective with buyers when they

relate the audiences they deliver to specific buyer goals beyond gender and age.

Validating local audiences is a continuing challenge in local. This gets to audience measurement

and reporting and the kinds of analytics that help buyers understand what they are getting.

More work is needed throughout the industry to improve local audience measurement.

Audience extension is a useful add-on product but be mixing apples and oranges, potentially

diluting local TV's unique selling prospects by adding in impressions from other sources to meet

audience target and impression goals. Buyers do want to see audience extension particularly

across screens.

Local TV Stations and Digital Advertising

Confidential 18 BIA/Kelsey

Value of uniform content is important to buyers and is one of local TV's strong points. This ties

into the previous point about some pros and cons of audience extension as it inherently brings

in audiences from different content environments.

In the next section, we'll share more of the insights from buyers on these themes.

Station Brand Equity and Premium Content

Given the prominent position in the local media mix and our growth forecast for local television ad

revenues, we can safely conclude broadcaster investments in station brand and premium content earn a

nice ROI. However, what explains digital's rapid double digit rise in the market without a commensurate

investment in brand and content? In fact, digital pure plays present themselves as trusted brands

providing premium content environments and as platforms that can meet exacting audience targeting

requirements.

Data drives digital buyers to find their audiences. The long-term proxy of finding the "right" audiences in

the "right" programs survives over time largely to the extent broadcasters can complement quantitative

gender/age ratings with qualitative data matched to buyers' target segments. Beyond that, broadcasters

must demonstrate the buyers' audience targets over-index in their programs more so than the

competitions'.

Having the #1 news program in town is certainly a plus and yields an observable revenue dividend. But

the clear market trend on the buy side falls along the lines of, "yes, you've got the #1 newscast, but how

many women 25-34 who are married, have kids and are looking to buy a Lexus in the next 30 days do

you have?"

Digging a bit into the kinds of viewpoints we heard from buyers on these topics, here's some of the

insights we gleaned:

When digital pure plays deliver the target audiences more cost-effectively, buyers will shift their

spending. Audience targets trump content to significant extent.

Given that this is the political season; some broadcast inventory pricing is pushing out some

typical advertisers. In one case a buyer cited having developed expensive creative for a client

but then couldn't run it on local TV due to current pricing. So the buyer had to look at digital

audience to run the video. At the time of our interview, not all the analytics were back but early

indications pointed to a successful digital campaign.

Stations’ high value content on owned and operated sites are more attractive to buyers in

sponsorship plans than audience targeting buys.

Data needed for cross-platform audience delivery when selling broadcast and digital content-

oriented packages.

Buyers want audience delivery guarantees based on Nielsen or comScore reports. Not all

stations subscribe and that’s an issue. But it also was not clear that one service or the other will

be the long term preferred metric of choice.

Local TV Stations and Digital Advertising

Confidential 19 BIA/Kelsey

Local markets and stations do not offer enough digital video impressions to fulfill buyer

requirements. This may be an overhang from old media planning techniques that rely on broad

reach but still demonstrate the current use of audience extensions.

For local TV, digital money may not be new money but keeps them close to advertisers looking

for digital inventory and retains that money at the TV station.

Accountability and lack of resources across the buy side was a shared concern. Among other

things, given smaller agency margins, the purchase of multiple individual stations' digital assets

does not support the incremental labor cost.

Valued and Trusted Relationships

Across the board, we heard sellers speak to the value of selling relationships and professionalism. TV

sellers often have been in the market long enough to have established a number of trusted relationships

with clients and agencies that parlay into business success. Indeed, one local market client told us that in

their family business, TV has long been the major component of their media mix because of the trust

factor. But this inertia accruing to local TV's credit is being challenged even in family owned businesses

that are undergoing generational leadership and ownership changes. The digital challenge is on and

testing even long term TV relationships.

Relationships are valuable but in a market where everyone's margins are getting squeezed, it's starting

to test not the validity of these relationships but the scrutiny of what results these relationships can

deliver. Certainly, the local TV seller has a longer history in the market than the relatively newer digital

pure plays. But results speak and buyers are starting to see digital results.

Here's a snapshot of buyer views on their relationships with sellers:

Local TV buyers value relationships but need to see seller diligence in understanding their goals

and how what the sellers are offering specifically advance these goals.

Stations will serve themselves well by building capabilities to distinguish some key products that

make sense for each client.

Key positive is that sellers have preferred access to local clients based on their long-term

relationships. This is a clear differentiator from digital pure plays, but less so when compare to

other local traditional media also selling digital inventory.

Relationships only go so far with buyers. They need to see solutions embracing audience

targeting, cross-platform campaign integration and awareness of their business goals and

attribution.

Providing a shopping list of local stations’ digital ad inventory without showing how these

options address client needs is a negative for buyers. It can strain otherwise good relationships

by revealing a lack of concern and preparation for understanding client needs.

Local TV Stations and Digital Advertising

Confidential 20 BIA/Kelsey

Providing Integrated Solutions

BIA/Kelsey once estimated that dozens of media account executives might call on a client or agency

each month, selling their preferred platform solution. These days, each account executive will be selling

not only their own advertising platform but also a range of other services.

In recent years, to grow overall share of budget media companies have expanded their product set to

include digital agency, search agency, SEO, website hosting, mobile app development and a range of

other advertising products and services. To some buyers, it's become a bit bewildering how to deal with

the plethora of sellers and types of solutions pitched to them.

Again, as we show in our forecasts and even today in markets like New York, digital advertising is not

only accepted and mainstream, in the case of Google, a single digital brand can be the #1 biller in the

market.

What this adds up to is that digital advertising is an important part of the ad mix. Local TV sellers exclude

digital offers at their peril. However, it's not just digital offers that will win in the market, it's the level of

service, analytics, insights and recommendations that top performing sellers bring to their clients that

makes a difference.

Buyers understand there are many and complex choices that may do a better or worse job in achieving

their goals. They simply do not have the resources to figure out what might be the best outcome. They

need to look for scale efficiencies. While they might do a better overall job of making individual

advertising decisions, if they can make smart enough buys to deliver the results they need, that gets the

job done well enough.

Here's the kind of sentiments we obtained from buyers:

Buyers prefer the scale and efficiency of integrated campaign activations. However, in a market

where many local media sellers are offering “agency like” integrated solutions, it just is hard for

every station in a market to stand out. They all seem to be offering similar, if not always

comparable, solutions.

Many buyers looking for digital solutions need to include Google, Facebook and other pure plays

in their plans. As the local selling efforts of these platforms become stronger, buyers could easily

convert to direct buying.

When local TV stations adopt too many different sales options, this can detract from the

product value. The value proposition gets lost, or indeed may not exist.

Buyers tend to be committed to a current set of solution providers. Would go with a different

source, but it needs to be cheaper, better.

Accountability Matters

The issues surrounding audience measurement, appropriate metrics, data methodologies, transparency

of the research and data analytics processes, and cross-platform intelligence are all urgent concerns

among the buying community. They need to see what they're getting to do better jobs with strategy,

planning, buying, optimization and showing ROI. And they need to do this with a view across media

platform silos to understand the complementary effectiveness of their total media campaigns.

Local TV Stations and Digital Advertising

Confidential 21 BIA/Kelsey

Accountability is urgent. The challenge is how to measure and report accountability in a clear, sound

manner that ports across markets in comparable metrics.

Buyers like it best when they can directly measure or at least see trusted third-party results. Getting

results from publisher side ad and content servers is interesting. But these metrics can be gamed and

also be rather idiosyncratic. This can make it hard for clients to roll up metrics for an overall campaign

level view.

When it comes to attribution, metrics, and local markets, here's what's on the minds of buyers:

Majority of interviews relayed usage of the station-provided metrics to assess KPIs.

Those with access to their own digital reporting (e.g., 1st party, internal target verification,

Google Analytics, etc.) also included some of these data into their own independent valuation.

Weaknesses around local metrics and the difficulty with adopting sound practices for the use of

Nielsen or comScore for digital video creates some confusion in the market.

Agencies and clients referenced their own lack of knowledge about how to work best with local

markets to support digital metrics.

Cost of measurement services and varied options adopted across stations create some

confusion regarding broader adoption or usage of digital products from stations.

There appears to be an opportunity to assess pro and cons of current measurement services

across markets to support discussion and development recommendations for better options.

Unique Inventory Offered by Local TV Stations

Local TV stations can provide a range of products and services to advertisers when it comes to digital

offers. This includes sponsorships, home page takeovers, participation in remote or special broadcast

programming and event coverage. We probed buyers to see how these types of unique inventory

appealed to them.

Agencies and clients used all products to varied degrees pending needs.

Early adoption includes sponsorships and tie-in strategies as this supports the broadcast

schedule and often does not require measurement KPIs.

Sponsorships are largely used by local clients within the market who already utilize the stations

and feel comfortable using the digital extension.

We see some evidence that stations’ digital sales are not net new revenue but reallocation

within the local station budget.

In fact, some buyers report that they accept the digital inventory as value added to integrated

packages. Clients sometimes attribute minimal value to station digital inventory in these

packages.

Larger buyers are interested in clearing the market at scale and would prefer to do so with

fewer rather than more transactions. They'd like to see even one media owner offer the

Local TV Stations and Digital Advertising

Confidential 22 BIA/Kelsey

aggregated inventory across their properties in a market rather than in a siloed set of offers.

Even better, some buyers argue, if local TV stations could come together and offer access to

their combined market footprint.

Cost efficiency seems to prevail more so than unique inventory.

Individual clients have limited budgets and appear to utilize a smaller number of stations for

their digital efforts that may follow the same share percentage as their broadcast buys.

Audience Targeting Needs Vary by Client Goals

One of local TV's strengths is that is provides market-wide audience coverage with its broadcast product.

And on the digital side, this can be complemented by offering inventory that can target audiences in

smaller than full market geographies for advertisers needing to reach less than the full market. For

example, tire dealers may serve mainly the close-in western suburbs of a market and don't need to pay

to reach audience outside their primary service area. The pricing for audiences in smaller geographies

could be attractive enough to bring in new advertiser who couldn't afford the broadcast product. Or

perhaps additional spending might come from advertisers seeking to complement their broadcast

advertisers with more specific messaging to hyperlocal geographic targets.

In speaking to buyers, we learned that:

The ability to target at both the market level but also have addressability for smaller

geotargeted areas is a main draw for clients who use the digital properties.

This was highlighted by clients active in the top 10 markets that carry a high price for broadcast

video. With budget limitations but an appetite for video, online video offers a way to participate

in the market and stretch dollars.

A challenge stations do face with their online video products is that they deliver audience sizes

often too small to achieve goals for impressions in target segments (e.g., weekly reach &

frequency goals, rating point goals).

Buyers require qualitative data to plan and evaluate buys for specific audience segments.

Marketplace unclear on how to evaluate local metrics.

Stations live in hybrid world with traditional broadcast buyers, some of whom are moving into

digital.

Stations in local markets provide different audience figures from different sources and this

confuses buyers trying to understand what’s going on in the market.

Buyers would like to see stations come together and utilize more consistent audience metrics,

demonstrate transparency of data sources and show how each data source may have market

specific nuances.

Validating Local Audiences

Measurement, analytics, and reporting became a recurring theme in our interviews with buyers. They

are data-driven on the digital side and trying to get more unified view of what local audiences they are

Local TV Stations and Digital Advertising

Confidential 23 BIA/Kelsey

reaching. To validate audience delivery, buyers used a variety of different data services. Additionally,

they had different audience delivery requirements depending on the client and campaign goals.

The need to validate local audiences is a bit of a hot spot among buyers. In part, this is because without

a clear and consistent way to measure local audiences, developing meaningful KPIs becomes a bit

challenged.

Some insights from buyers include:

Measurement systems and the ability for buyers to optimize their campaigns provide a

challenge to the market.

Beyond measurement, reporting is also seen to be a huge challenge. One example cited is that a

buyer looking to get impressions in a particular market may get a report showing that target was

hit, but in fact all those impressions may have come from just one or two counties even though

based on the report, the buyer could conclude the market had been covered.

Buyer perceptions of sellers’ knowledge of digital audience data and analytics was a bit

inconsistent and led to increased frustration and confusion.

Some local TV sellers were praised for their digital knowledge, in other cases both the lack of

digital sales knowledge and quality of the inventory were rated far below digital pure play

competitors.

Buyers themselves had varied sophistication on understanding what the proper KPIs should be

for online video and other digital inventory.

An opportunity exists to highlight some of the inconsistencies that currently exist across local

markets regarding access to data and delivery confirmation.

Audience Extension Across Local Platforms

Buyers seeking to identify and reach their target audience segments incorporate several media

platforms into their campaigns to better achieve reach and frequency goals than they can achieve by

using just one or two media channels. For local TV, their broadcast and digital platforms may share a

common audience but also deliver unique audience segments. For example, advertisers can reach some

consumers on local TV digital platforms that aren't in the broadcast audience. Buyers see this

particularly to be the case with mobile video services.

The ability to reach an extended audience using broadcast and digital platforms provided by local TV

stations is helpful to buyers but not without issues. One factor in the local marketplace is that local TV

sellers both sell their own digital inventory but also put some of the inventory into ad networks or

exchanges. Some stations keep prime inventory for their own sales teams and put remnant or otherwise

unsold inventory into exchanges.

Buyers may see station inventory as relatively more expensive for direct buying versus buying through

exchanges. Or they may assume they're already getting digital inventory from the stations by buying

from exchanges but without getting the transparency of where the audience is coming from.

Some of the thoughts buyers shared with us include:

Local TV Stations and Digital Advertising

Confidential 24 BIA/Kelsey

More qualitative data needed regarding audiences reached on both platforms; duplication vs

extension.

Ad networks were often cited as the key avenue that buyers pursued for audience extension

needs.

National agencies and regional clients that segregate digital buying from traditional broadcast

were more inclined to need scaled solutions that ad networks offer, i.e., accessing audience

targeted inventory across publisher sites with one demand-side platform.

Majority of buyers do not realize that a station may have the ability to override an ad network

spot nor are they aware of which stations may participate in and sell inventory to the ad

networks.

Clients may use stations’ capabilities to help them purchase audiences beyond the individual

station, but this seems like a limited opportunity for all stations to pursue.

Low margins and competition for these services from local agencies or in-house teams

(particularly at larger clients) may limit this option for stations in the longer term.

There is stronger opportunity and interest for a media owner with multiple in-market

properties, if they can be combined in an integrated buy versus buying at the individual property

level.

There is an unmet buyer need that stations could address. Stations could come together and

provide buyers with a transparent overview of the audience extension within a market.

Buyers want to have transparency of where these audiences are sourced locally and where the

traffic and final sale resides (i.e., the ad network or the station).

Value of Uniform Content

Unlike some digital properties, local TV content is curated and audiences have an expectation of what

they will get. The value of this type of uniform content is in drawing a consistent audience with

characteristics that are predictable and attractive to a large set of advertisers. Indeed, the quality and

reputation of broadcasters and their program may lend a sort of brand halo effect that could be

attractive to advertisers.

So again we focused our discussions with buyers on the relative value of the particular properties of the

content local TV broadcasters provide and how this fits into their value equation. And again, while the

content has value, buyers seem more concerned with data and how audience segments index against

their target segment.

The appeal of localized content is important to all buyers but digital buyers are trained and

conditioned to deliver efficient CPMs against target audiences that require scale and buying

efficiency.

There is a lack of understanding as to how local audiences perceive this content that makes it

difficult for buyers to distinguish differences among sellers. For example, while the early evening

Local TV Stations and Digital Advertising

Confidential 25 BIA/Kelsey

news is seen to be premium content offered by all the stations, which station’s audience over-

indexes buyer’s specific target segment?

Buyers want to see more evidence of how premium content enhances the audience perception

of or engagement with their ads.

The word premium also conjures different meanings across the buy side community. Market

specific local sports or investigative news may not be valued the same by all clients. Audience

metrics that confirm this are important considerations for defending the demand and price of

inventory.

It feels a bit early to make an informed call on the value of different local station content to

advertisers on their digital platforms. Buyers have not spent enough, long enough across

stations to warrant a strong feeling one way or another.

Local TV Stations and Digital Advertising

Confidential 26 BIA/Kelsey

Part 5: Recommendations Marketers and agencies are still evolving their media planning and buying to incorporate digital

platforms and more data-driven audience buying. Of course, they show preference for traditional or

pure play options that offer cost efficiency. However, the marketplace is not clear on how local

measurement metrics translate or how to properly evaluate them.

Stations live a hybrid existence with their largest and most profitable clients utilizing TV broadcast who

may just reallocate part of their broadcast budget to local TV digital offers rather than bringing in new

digital dollars. Sellers should unify communication as it relates to local digital opportunities and promote

the benefits of utilizing these sites overall even if it means promoting in market competition. The

objective is to garner a favorable view of TV digital offerings and their associated assets versus other

choices. Individual stations will benefit from building universal appeal and helping to drive awareness.

A key positive position is that sellers do have access to local clients based on long term selling

relationships. Other traditional media (radio and newspaper) also have this selling capability within

many markets and could be competing for online budgets. Based on our key learnings from this study,

we offer these major recommendations for local TV sellers:

1. Increase Digital Knowledge, Skills, Experience: Continuing to educate local TV sales team and

clients on digital but also work on building capabilities to distinguish some key products that

make sense for the client in question. In some instances, the clients feel that too many sellers

want their time and as media options increase, stations may be shut out due to lack of time on

client part. Broader educational option exists to help clients better understand what is available

to them in the market and how this relates to objectives they may have for various campaigns.

Keep it simple and do homework before pitching a client. It should not be presented as a

shopping list.

2. Clearly Differentiate Benefits of Local TV Premium Content. Buyers concur that local stations

offer unique and valuable content. What they'd like to see more of is what quantifiable value

this can offer to them in terms of delivering audiences over-indexing in their target segments or

how this high value content delivers more engaged audiences that can benefit marketers.

3. Develop Digital Packages that Are Measurable and Sustainable: Selling integrated broadcast

and a wide variety of digital offers may not be a profitable option for TV sellers in the long term.

Those who may have established the capability in the market and also have a strong station

seem to fair better than those who are trying to be digital agencies offering broad services. It is

important to select a package of digital services that both address buyers' needs and that make

good business sense for the stations. Margins should be examined to determine if low ticket

sales are worth the effort.

4. Audience Extension Can be a Double-Edged Sword: Often digital buyers require a larger volume

of digital video impressions than the Local Station can deliver, and Local TV stations may extend

their own digital audiences by going to ad networks and programmatic exchanges. While

servicing buyer’s immediate needs, long term this may impact station’s digital profits and make

them more vulnerable to defection. In any event, we encourage stations to be transparent

Local TV Stations and Digital Advertising

Confidential 27 BIA/Kelsey

about use of audience extension and the content and audiences added to the overall mix of

impressions. Small markets and clients who may not have many resources seem to be the main

constituents who turn to the digital agency run by a station. It is presently filling a void in the

market but may not be sustainable long term given the labor put forth by these stations.

Smaller media budgets across a wide number of clients could suppress margin growth over time

as budgets flatten due to market maturity. Or these current clients may take the tasks in house

or award to another agency that they feel is more objective. There is a perception that the

stations that run these services may be garnering a higher share of revenue or perhaps reaping a

commission that won’t need to be paid if they go direct.

5. Digital Packages Should Be Based on and Fulfill Client Needs: Local TV can become more

systematic in offering a set of digital offers that are both more curated and focuses on clients'

needs and their ability to fulfill and service these products. Indeed, local TV's approach in this

regard could be shared across the market to encourage broader use of TV digital products and

services. There is a perception that some sellers are simply trying to be all things to clients to

make a sale. This could backfire if the station is not set up to service.

6. Campaigns Need Better Local Measurement Tools, Metrics, Transparency: There is significant

confusion and the lack of measurement services has made it difficult to determine best solution

for clients and stations. Agency and client sophistication varies considerably making it hard for

stations to consider a few key delivery services. If the marketplace pushes for KPIs that require

measurement guarantees across a wide number of providers, it could be less beneficial for

stations to pursue. There are two avenues for station websites to pursue. One is the traditional

digital play that competes with pure plays but the smaller cap of audience impressions makes it

difficult to sustain in a meaningful way. Bundling with other stations to encourage an in market

mini ad network could be attractive to buyers as it encourages more measurement transparency

around the participants. The other avenue is a video extension play where traditional OTA

buyers use digital sites to extend the TV schedule. This too needs to align with measurement

guarantees that vary by agency shop or advertiser and require more scale for the buyer who

finds it cumbersome to deal with each individual station.

7. Seek the Opportunities that Exist with National Brands Spending More to Target Local

Audiences in Digital: BIA/Kelsey forecasts that spending by national advertisers targeting local

audiences will grow nearly $11 billion from $61.5 billion in 2016 to $72.4 billion by 2020.

Programmatic exchanges and data management platforms are adding efficiencies to the buyer

challenge of reaching target audience segments and clearing inventory with geographic criteria.

To date, programmatic trading has not been a factor in local TV. Programmatic and data-driven

audience targeting is rapidly becoming the norm in the digital advertising world and soon the

vast majority of digital trading will flow through programmatic platforms and ad exchanges. We

see the television networks moving with increasing commitment to the programmatic trading

world. Of course, the national TV market is different in many ways from the local TV market.

But, if local TV operators can develop measurement, reporting and trading solutions that allow

buyers to evaluate and clear video impressions across local TV broadcast and digital properties,

this could be a significant win for broadcasters. This could bring in more spending by national

Local TV Stations and Digital Advertising

Confidential 28 BIA/Kelsey

advertisers as well as local and regional advertisers. Local TV controls prime video inventory and

the market demand for video is increasing, and particularly as we noted earlier, mobile video

inventory.

In summary, we see that local TV sellers have made commitments to be stronger players in the digital

market. These commitments range from providing digital as a value add to broadcast in what buyers

sometime perceive as half-hearted selling efforts to full-out and aggressive build-out of digital

capabilities and a desire to be competitive and achieve significant revenue growth. Local TV buyers are

committed to broadcast and tend to pull dollars for their increased spend in digital from print media

rather than local TV. In some cases, increased spend on local TV's digital offerings comes not as

incremental new dollars to TV but rather a reallocation of the TV budget across linear and digital

offerings. This is an artifact of the way local TV sellers approach the market (i.e., digital is a value-add)

and buyer perceptions of local TV. With more market education on the buyer and seller sides, better

measurement and reporting, and a commitment to developing and servicing quality digital solutions, we

see significant upside for local TV and their digital offerings.

Local TV Stations and Digital Advertising

Confidential 29 BIA/Kelsey

Appendix A: Interviewees

Agencies and Marketers

Debbie Basham, SVP/Director of Audio and Video Investment, Media Hub (division of Mullen

Lowe U.S.)

Adam Blanck, Chief of Staff, Wallside Windows

Michael Bologna, President, MODI Media (division of Group M)

Margie Carrasquillo, Group Media Director, The Gate Worldwide

Summer Craig, Senior Manager, Integrated Media, Gulf States Toyota

Kathy Doyle, EVP/Managing Partner, UM WW

Katie Fourney, Director of Media and Research, Right Idea Media & Creative

Pattie Glod, Managing Director, Mediopolis Media

Sue Joehnning, Managing Director, Local Investment, Initiative

Scott Stansfield, President, Centriply

Local TV Sellers

Mike Cukyne, VP/GM, KCTV/KSMO-TV

Brian Hellman, Senior Director, Digital Sales, E.W. Scripps

Tom O'Brien, EVP, Digital Media and Chief Revenue Officer, Nexstar

Steve Chase, VP, Director of Sales, Cordillera Communications

Steve Scadden, General Sales Manager, WISC-TV

Gary Macko, P Sales/ Graham Media Group & General Sales Manager at WDIV-TV

Tim Warner, Director of Sales, WTHR-TV

Eddie Melendez, EVP, Integrated Marketing Solutions, Entravision

Local TV Stations and Digital Advertising

Confidential 30 BIA/Kelsey

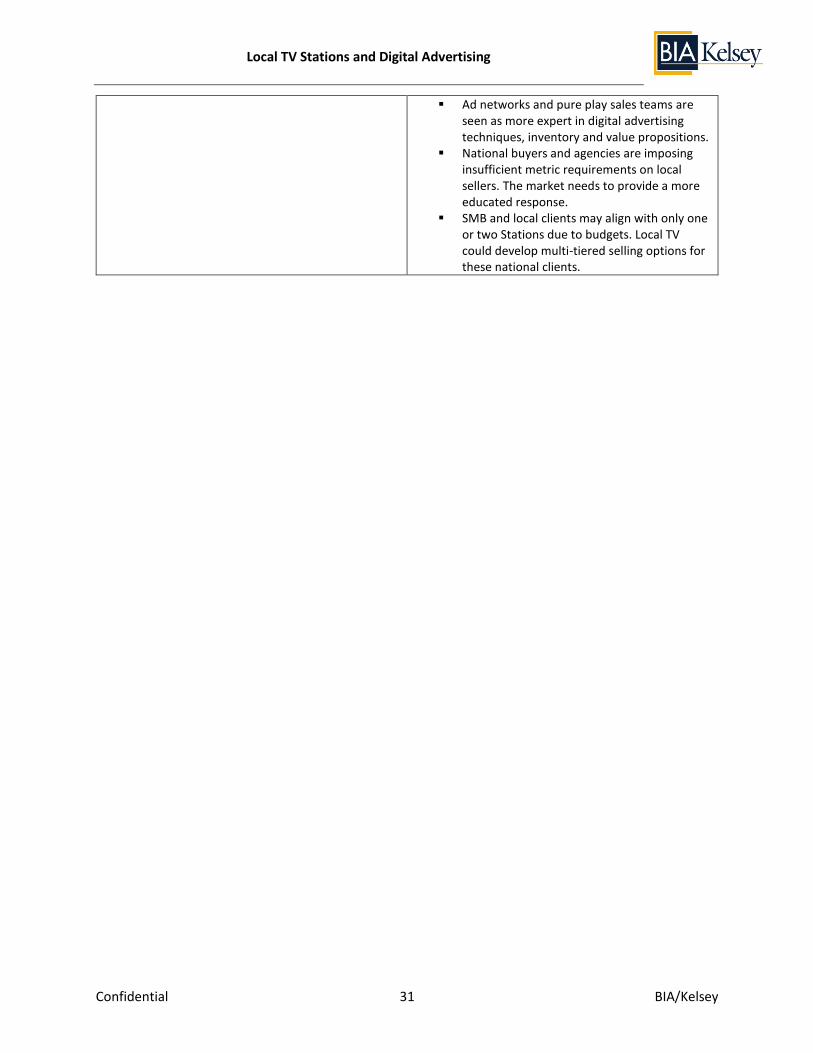

Appendix B: BIA/Kelsey’s Local TV and Digital Offerings SWOT Analysis With this "Perception versus Reality" comparison of local station seller versus agency and client

viewpoints, we wanted to pull out a summary of local station Strengths, Weaknesses, Threats and

Opportunities (SWOTs). This table summarizes some of the bonds and gaps that exist between sellers.

Table 3. SWOT Analysis of Local TV Station Digital Sales (Source: BIA/Kelsey, 2016)

Strengths Identifiable brand content Local market partner Trusted relationships with local sales staffs Service minded attitude Association with larger parent company/content Market knowledge Video extension beyond linear TV station Sponsorship opportunities Broader service capabilities (creative, traffic, etc.) Adaptable

Weaknesses Inconsistent product sales Limited digital sales knowledge Often think TV first, digital second Introduces/offers too many solutions in broadest

terms Perception from digital only buyers that TV sites

already available on ad networks at cost efficient price

Client/buyers digital fluency level may inhibit TV digital sales due to agency dictates or multi market needs

No consistent qualitative or quantitative data to compare across digital sites or within digital to linear TV audiences

No scalable solution to purchase digital within the same parent company

Buyers/agencies/clients using multiple measurement techniques.

Opportunities Focus on priority products with simple sales

premise Educate market by aligning TV sellers with similar

market metrics to enable comparison versus pureplay digital products

Build seller digital fluency across various measurement options (GRP/TV impressions versus digital metrics)

Understand margins across all selling channels to determine core product focus

Focus on differentiating TV sites from broader digital options and provide key measurable attributes that apply to all markets

Work collaboratively within markets to offer saleable client solutions through a mini network or dashboard (too many sellers confuse clients)

Address local measurement shortcomings and develop vision/roadmap to transition

Threats Third party representation (for FB, Google)

could negatively impact long term margins as clients convert directly to primary seller versus local TV resellers.

Ad network alliances have diminished value of local TV digital product

Lack of consistent measurement techniques or ability to compare audience data will inhibit local sales revenue potential

Digital video may cannibalize linear sales. Digital requires identifiable benefit of audience extension versus other digital competition.

Agency and client buyers have varied understanding of digital marketplace. This confuses how the overall needs of the market gets expressed. This opens up a seller opportunity to collectively align.

TV owned and operated websites are variously perceived as old school design populated with click bait to cleaner more modern sites that provide a better user and advertiser experience.

Local TV Stations and Digital Advertising

Confidential 31 BIA/Kelsey

Ad networks and pure play sales teams are seen as more expert in digital advertising techniques, inventory and value propositions.

National buyers and agencies are imposing insufficient metric requirements on local sellers. The market needs to provide a more educated response.

SMB and local clients may align with only one or two Stations due to budgets. Local TV could develop multi-tiered selling options for these national clients.