Embed Size (px)

Citation preview

Secretaria de Política Econômica

Developing Local Corporate Bond Markets in Brazil: Recent Developments and Policies

Istanbul, May 2013

Pablo Fonseca P. dos SantosDeputy‐Secretary of Economic Affairs

Ministry of FinanceEconomic Policy Secretariat

Secretaria de Política Econômica

Outline

Brazilian Capital Markets Its short‐term natureRecent developments

Long‐term bank lendingThe role of BNDES

Policies to reduce short‐termism Why do we care?1st generation of policies2nd generation of policies

BNDES “crowding‐in”, private sector initiatives and challenges ahead

2

Secretaria de Política Econômica

Federal Public DebtPrivate Debt

Financial and Non‐financial Debentures

3

Private and Federal Public Debt (% of total debt ‐ January 2013)

Source: STN, ANBIMA and CETIP Elaboration: Ministry of Finance

Secretaria de Política Econômica

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%Jan‐90

Jan‐91

Jan‐92

Jan‐93

Jan‐94

Jan‐95

Jan‐96

Jan‐97

Jan‐98

Jan‐99

Jan‐00

Jan‐01

Jan‐02

Jan‐03

Jan‐04

Jan‐05

Jan‐06

Jan‐07

Jan‐08

Jan‐09

Jan‐10

Jan‐11

Jan‐12

Jan‐13

Fixed Rate

Exchange Rate

Floating Rate**Inflation Linked

4.3

23.0

35.5

37.1

4

* Including domestic and external debts managed by the National Treasury.** Including SELIC, TR and others.

Source: Brazilian National Treasury Secretariat Elaboration: Ministry of Finance

Federal Public Debt Profile * ( % of total debt)

Secretaria de Política Econômica

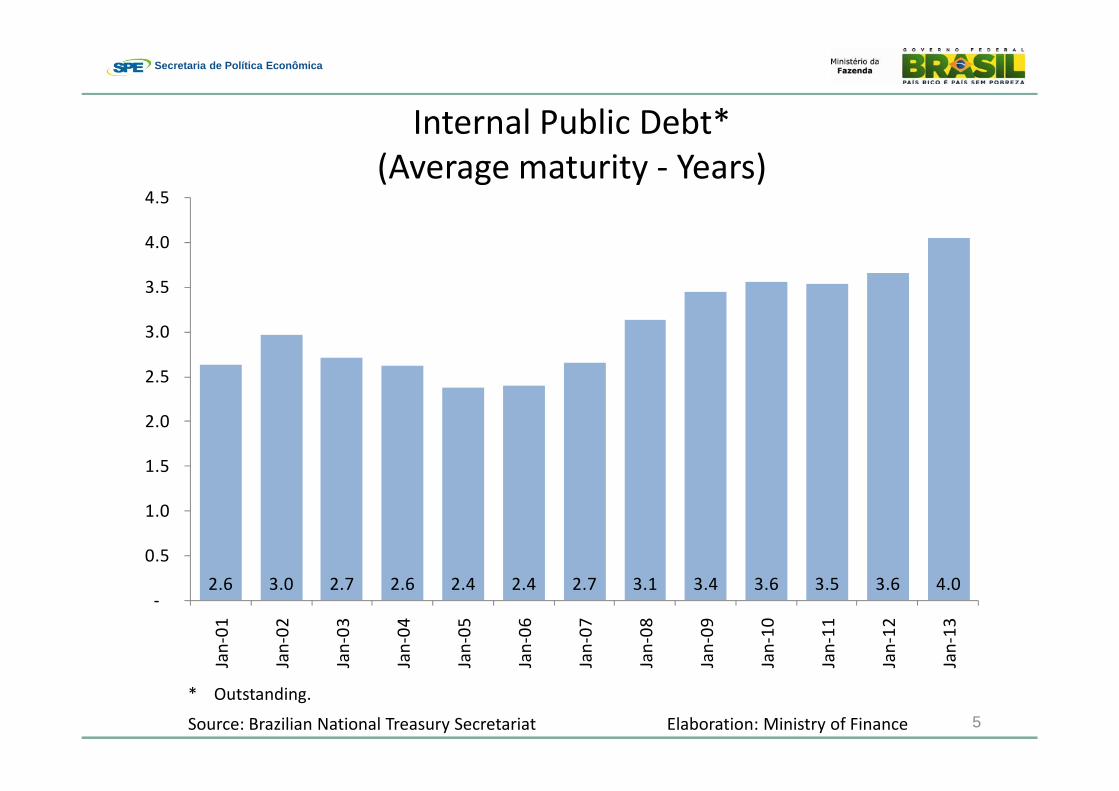

5Source: Brazilian National Treasury Secretariat Elaboration: Ministry of Finance

Internal Public Debt*(Average maturity ‐ Years)

2.6 3.0 2.7 2.6 2.4 2.4 2.7 3.1 3.4 3.6 3.5 3.6 4.0‐

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5 Jan‐01

Jan‐02

Jan‐03

Jan‐04

Jan‐05

Jan‐06

Jan‐07

Jan‐08

Jan‐09

Jan‐10

Jan‐11

Jan‐12

Jan‐13

* Outstanding.

Secretaria de Política Econômica

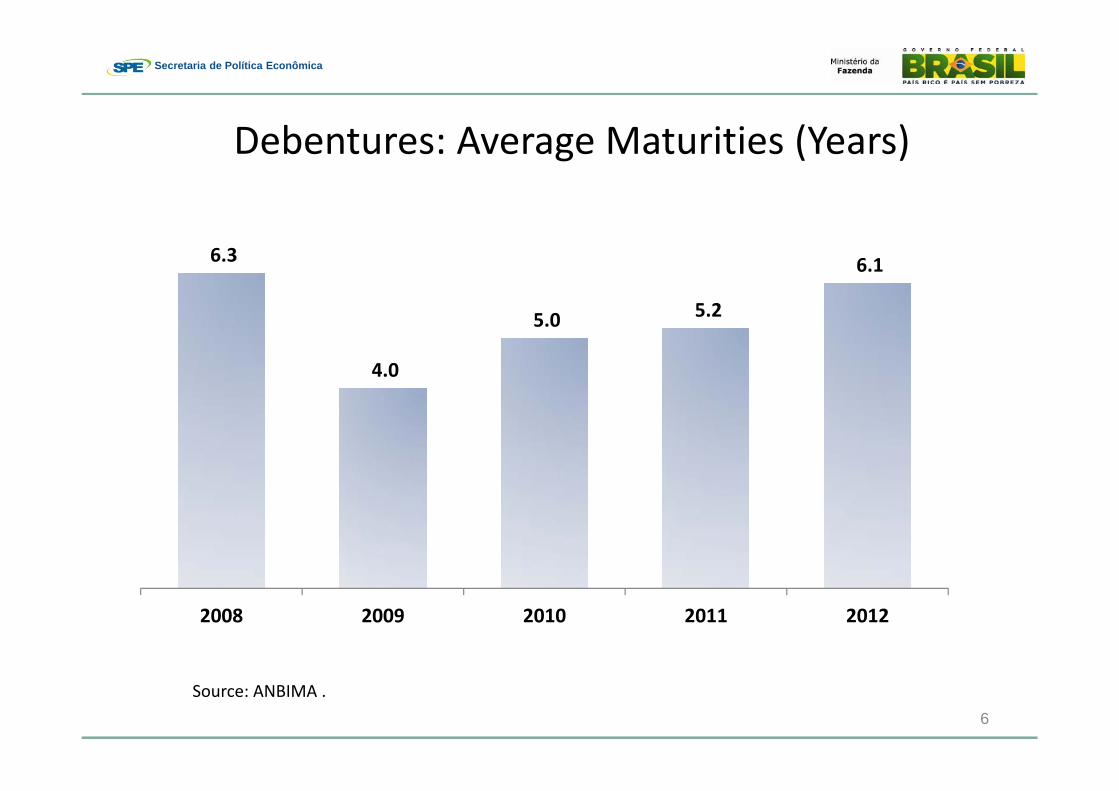

Debentures: Average Maturities (Years)

Source: ANBIMA .

6.3

4.0

5.0 5.2

6.1

2008 2009 2010 2011 2012

6

Secretaria de Política Econômica

Capital Market – Public Offers (R$ billion)

7

0

50

100

150

200

250

3001995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Debêntures Ações+CDA FIP Notas Promissórias FIDC CRI FII Demais

Source: CVM and ANBIMA. Elaboration: MF/SPE.

Secretaria de Política Econômica

Debentures, Promissory Notes, FIDC and CRI Issuances (Current Value – BRL Million)

22,643

18,737

18,899

22,637

27,614

52,947

50,687

86,616

10,272

13,920

17,068

5,593

3,196

7,767

13,382

9,947

2009

2010

2011

2012

Promissory Notes FIDC Debenture CRI

Debentures growth in 2012: 70.9%

Source: CVM and ANBIMA. Elaboration: MF/SPE. 8

Secretaria de Política Econômica

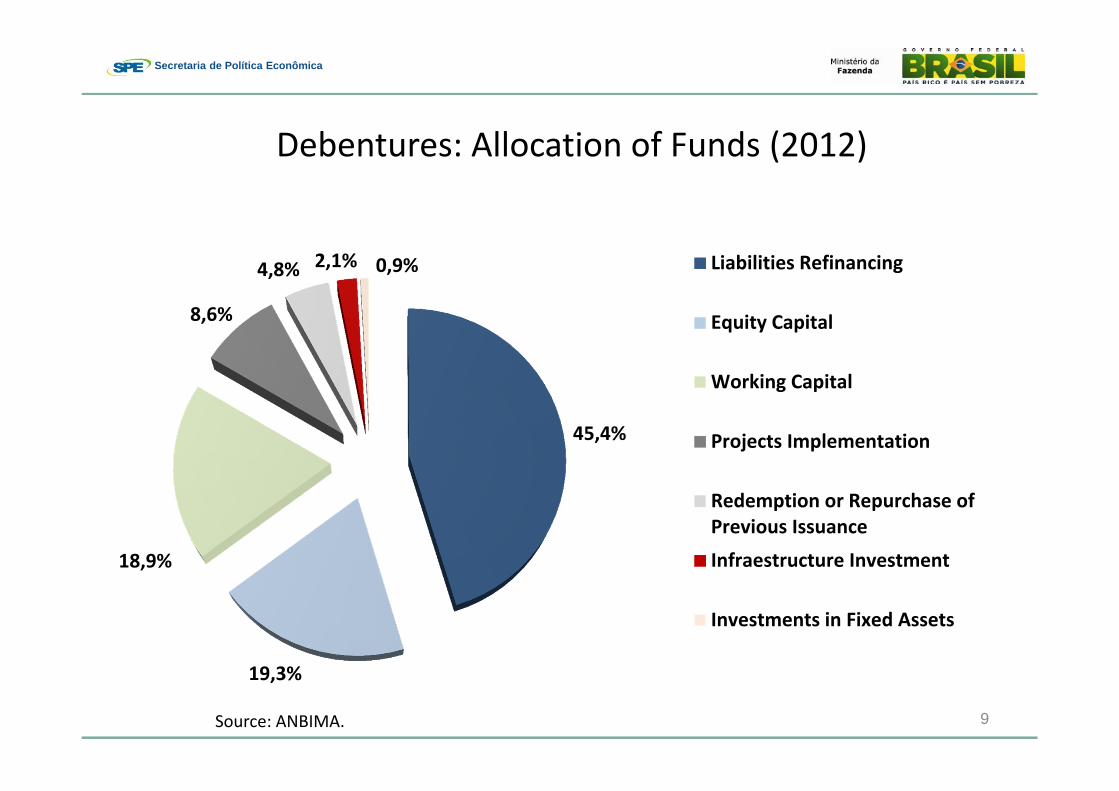

Debentures: Allocation of Funds (2012)

Source: ANBIMA.

45,4%

19,3%

18,9%

8,6%

4,8% 2,1% 0,9% Liabilities Refinancing

Equity Capital

Working Capital

Projects Implementation

Redemption or Repurchase ofPrevious Issuance

Infraestructure Investment

Investments in Fixed Assets

9

Secretaria de Política Econômica

Outline

Brazilian Capital Markets Its short‐term natureRecent developments

Long‐term bank lendingThe role of BNDES

Policies to reduce short‐termism Why do we care?1st generation of policies2nd generation of policies

BNDES “crowding‐in”, private sector initiatives and challenges ahead

10

Secretaria de Política Econômica

11

Long‐Term Credit( % of credit portfolio – September 2012)

49.8

21.2

9.6 5.4

8.2 5.9

0

10

20

30

40

50

60

CE

F

BB

Bra

desc

o

Itaú

San

tand

er

BN

DE

S

89.1

3.5 3.3 2.0 1.1 1.00

20

40

60

80

100

BN

DE

S

BB

CE

F

Itaú

Bra

desc

o

San

tand

er

Maturity ‐ 5 to 15 years Maturity – over 15 years

Source: Central Bank of Brazil Elaboration: Ministry of Finance

Secretaria de Política Econômica

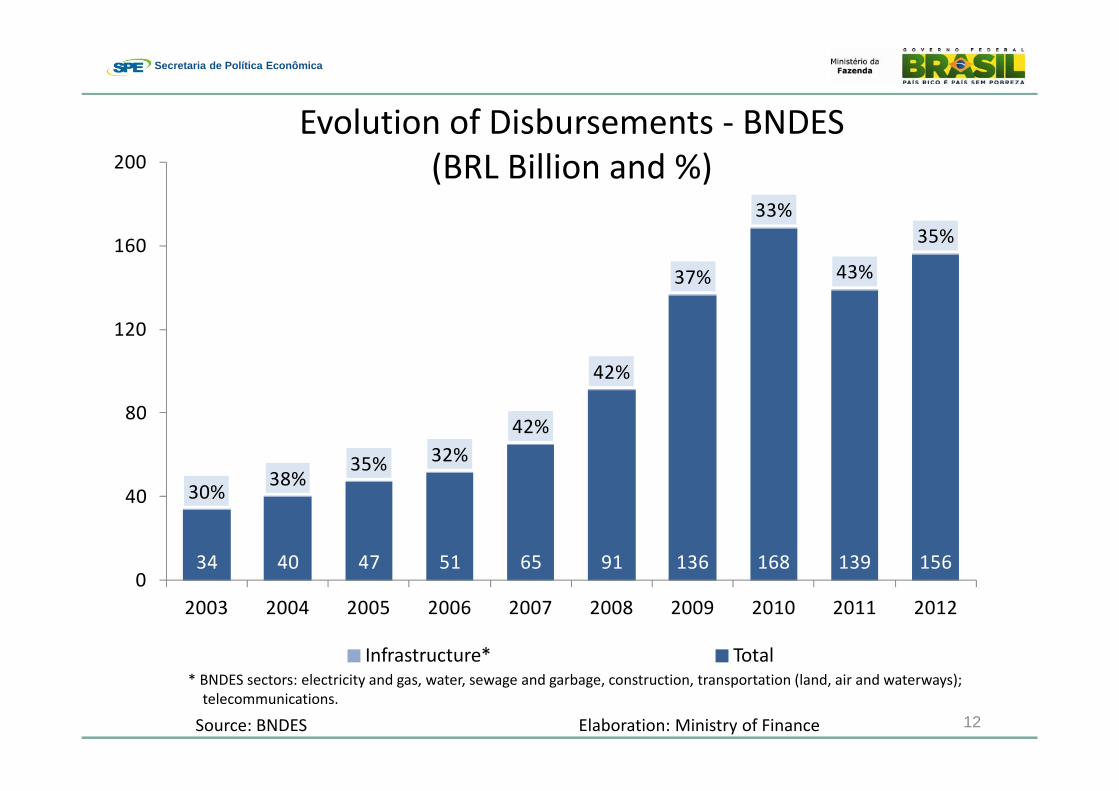

34 40 47 51 65 91 136 168 139 156

30%38%

35% 32%42%

42%

37%

33%

43%

35%

0

40

80

120

160

200

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Infrastructure* Total

12

* BNDES sectors: electricity and gas, water, sewage and garbage, construction, transportation (land, air and waterways); telecommunications.

Evolution of Disbursements ‐ BNDES(BRL Billion and %)

Source: BNDES Elaboration: Ministry of Finance

Secretaria de Política Econômica

Outline

Brazilian Capital Markets Its short‐term natureRecent developments

Long‐term bank lendingThe role of BNDES

Policies to reduce short‐termism Why do we care?1st generation of policies2nd generation of policies

Pr BNDES “crowding‐in”, private sector initiatives and challenges ahead

13

Secretaria de Política Econômica

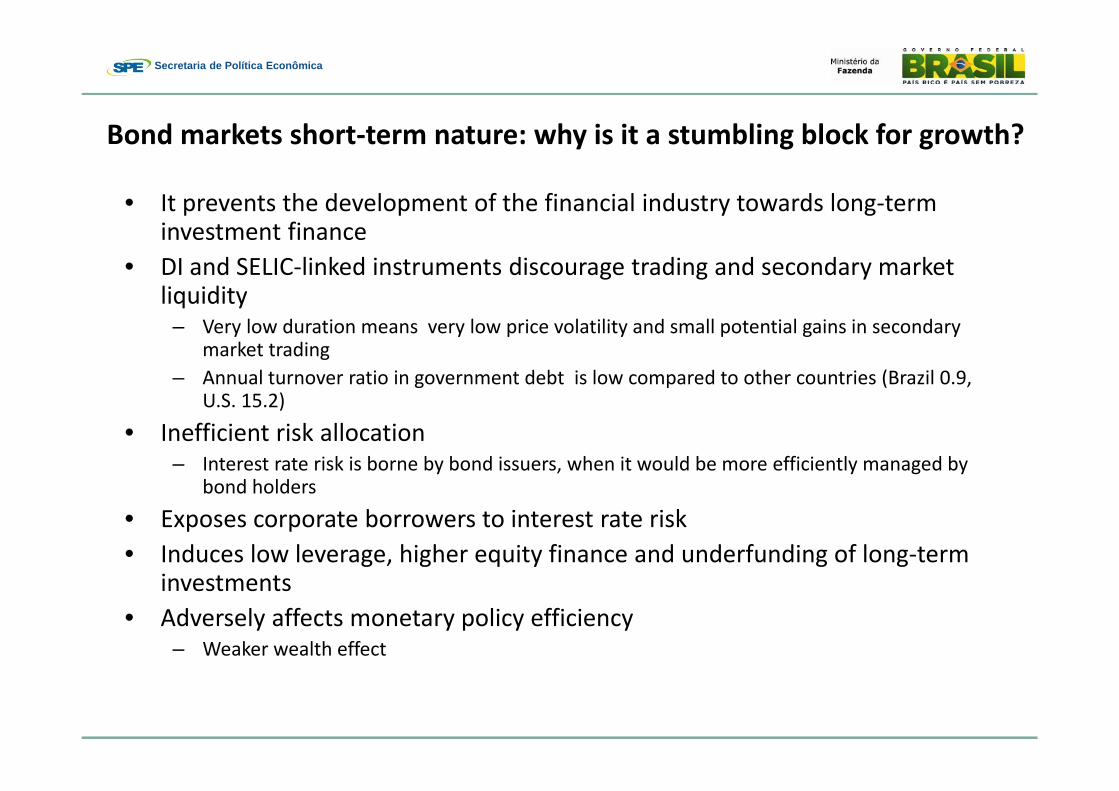

• It prevents the development of the financial industry towards long‐term investment finance

• DI and SELIC‐linked instruments discourage trading and secondary market liquidity

– Very low duration means very low price volatility and small potential gains in secondary market trading

– Annual turnover ratio in government debt is low compared to other countries (Brazil 0.9, U.S. 15.2)

• Inefficient risk allocation– Interest rate risk is borne by bond issuers, when it would be more efficiently managed by

bond holders

• Exposes corporate borrowers to interest rate risk • Induces low leverage, higher equity finance and underfunding of long‐term

investments • Adversely affects monetary policy efficiency

– Weaker wealth effect

Bond markets short‐term nature: why is it a stumbling block for growth?

Secretaria de Política Econômica

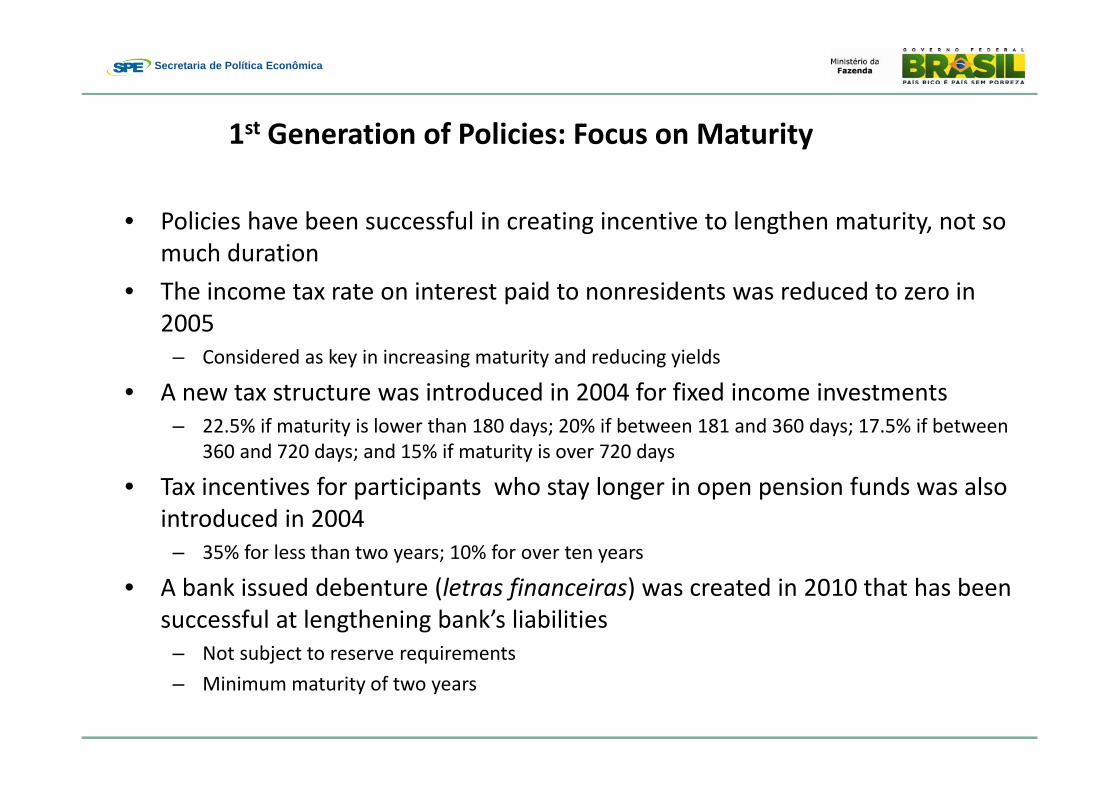

• Policies have been successful in creating incentive to lengthen maturity, not so much duration

• The income tax rate on interest paid to nonresidents was reduced to zero in 2005

– Considered as key in increasing maturity and reducing yields

• A new tax structure was introduced in 2004 for fixed income investments– 22.5% if maturity is lower than 180 days; 20% if between 181 and 360 days; 17.5% if between

360 and 720 days; and 15% if maturity is over 720 days

• Tax incentives for participants who stay longer in open pension funds was also introduced in 2004

– 35% for less than two years; 10% for over ten years

• A bank issued debenture (letras financeiras) was created in 2010 that has been successful at lengthening bank’s liabilities

– Not subject to reserve requirements – Minimum maturity of two years

1st Generation of Policies: Focus on Maturity

Secretaria de Política Econômica

• Institutional Investors – BRL 2.7 trillion (65% of GDP)“Open” Pension Plans/Funds ‐ very short duration“Closed” Pension Plans/Funds – search for yield Mutual Funds – short duration and daily liquidity

• Creation of Project Bonds and Funds to provide funding for long‐term investments, particularly in infrastructure

• BNDES “crowding‐in” – helping to develop alternative sources of long‐term funding

• Fixed‐income ETFs – to incrrease liquidity at the higher end of the yield curve

2nd Generation of Policies: Focus on Duration

Secretaria de Política Econômica

• Industry was irrelevant in 2005, now holds close do BRL 300 billion in assets (7% of GDP, expected to increase to 15% of GDP in 10 years)

• Over 90% are variable contribution plans

• In 2011 it invested only 3.5% of its assets in equity and 90% in fixed income

• 58% of fixed income investments were linked to overnight rate (1‐day duration) ‐ 28% were Repos!

• In January 2013 a minimum duration benchmark was introduced by a National Monetary Council (CMN) resolution

• Discussion under way to reform the industry regulation in order to provide for greater flexibility in investments

Open Pension Plans

Secretaria de Política Econômica

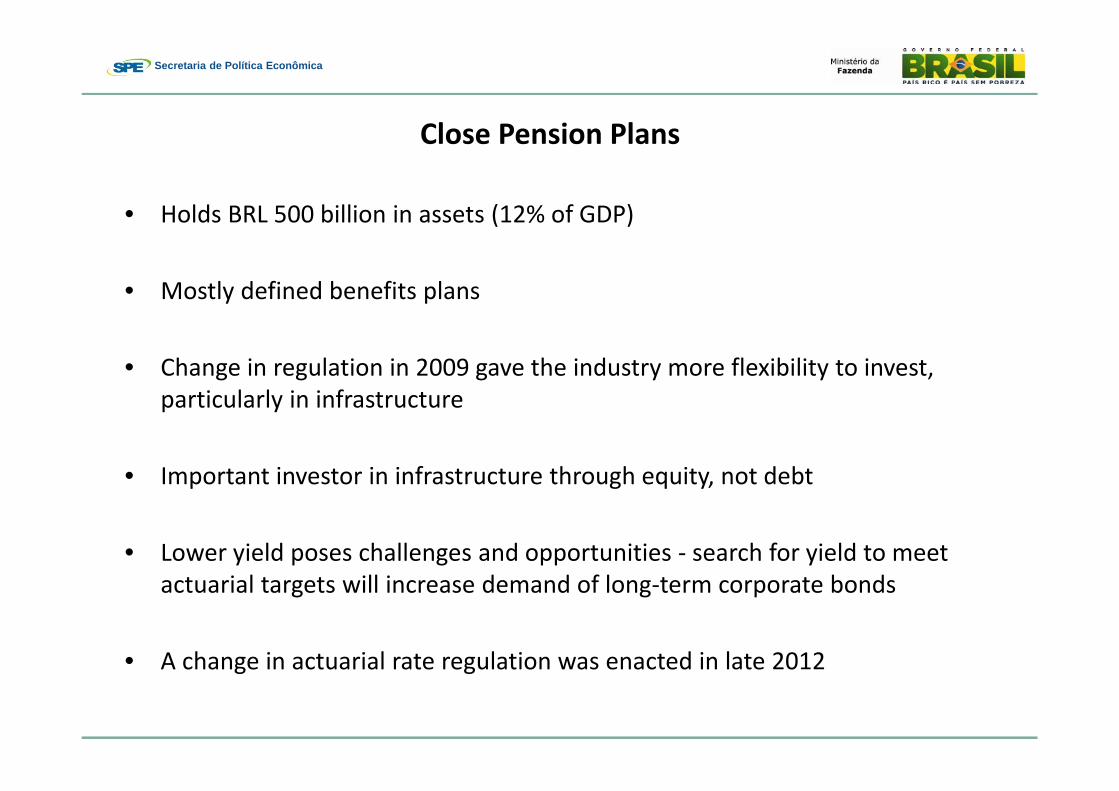

• Holds BRL 500 billion in assets (12% of GDP)

• Mostly defined benefits plans

• Change in regulation in 2009 gave the industry more flexibility to invest, particularly in infrastructure

• Important investor in infrastructure through equity, not debt

• Lower yield poses challenges and opportunities ‐ search for yield to meet actuarial targets will increase demand of long‐term corporate bonds

• A change in actuarial rate regulation was enacted in late 2012

Close Pension Plans

Secretaria de Política Econômica

• BRL 1.8 trillion industry (43% of GDP)

• Most is invested in short duration instruments

• Investors daily liquidity culture poses challenges to asset managers, as higher yields are in long term, higher duration and less liquid instruments

• Recent success in Real State Funds presents a promising way out:– It has tax breaks for (Income and IOF) to non‐residents and residents– It addressed the following dilemma in fixed income market: investors seek for liquidity and fund

managers need lock up periods– They are close‐end funds with quotas trade in the market– Quotas trading has been remarkably active providing liquidity

• 10 major local banks are working on the design of an infrastructure fund with similar traits

Mutual Funds

Secretaria de Política Econômica

Objectives:

‐ Level the playing filed with Treasury Bonds‐ To promote private long‐term financing of investments, by giving taxbreaks (Income TAX and IOF) for capital market instruments, creatingalternative sources of long‐term funding, other than BNDES.

Financial instruments:‐ Capex Bonds: tax break applies only to non‐residents;

‐ Infrastructure Bond: tax break applies to both residents and non‐residents.

Qualified investment vehicles:‐ Investment funds that hold at least 85% of its net worth in project bonds(67% during the first two years)‐ Receivables investments Funds (FIDC) ‐ .

Development of Corporate Bond MarketProject Bonds ‐ Law 12,431/11

20

Secretaria de Política Econômica

Development of Corporate Bond MarketProject Bonds ‐ Law 12,431/11

Main features:

Funds must be used in Capital Expenditures (Investments or Infrastructure)

Minimum duration: 4 years (6 years in the case of FIDC);

Fixed rate or inflation‐linked;

No repurchase by issuer during the first 2 years after the issuance date;

No investor resale commitment;

Periodic interest payments (if applicable) of no less than 180 days;

Registration of the instrument in a regulated securities market authorizedby the Central Bank of Brazil or the Brazilian Securities Commission;

* The Government is not involved in the trading or issuance process21

Secretaria de Política Econômica

22

LAW 12,431/11(Results and Forecasts)

6 infrastructure bonds and 4 capex bonds have already been since August 2012.

Pipeline: 32 infrastructure projects in energy and transportation with anestimated amount of BRL 61.6

billion in investment projects.

Forecast: 10% to 20% of the funding should be provided by Capex and/orInfrastructure Bonds.

The first BRL 1 billion (USD 500 million) infrastructure bond deal is expected tofor next month

Secretaria de Política Econômica

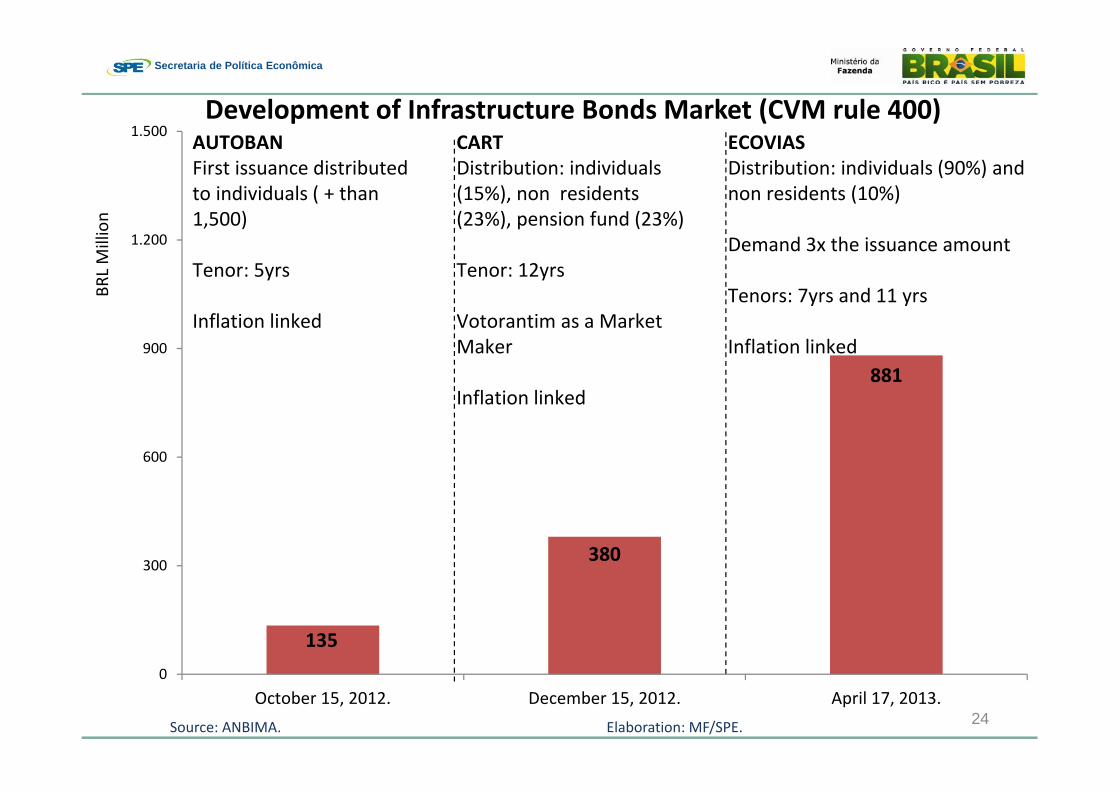

LAW 12,431 PROJECT BONDS(CAPEX and Infrastructure Bonds, Selected Issuances)

23

1.CAPEX Bond (also referred to as Law 12,431 article 1 debenture) ‐ local currency IOF and income tax exempt bond for non‐residents. Funds raised must be used in capitalexpenditures.

2. Infrastrucuture Bond (also referred to as Law 12.431 article 2 debenture) ‐ local currency IOF and income tax exempt bond for non‐residents and resident retail investors. A ten‐percentage point income tax rate reduction applies for local companies. Funds raised must be used in infrastrucuture expenditures.

3. Consumer price index.4.CVM rule #476 ‐ public offer in which up to 20 qualified investors can participate.5.CVM rule #400 ‐ public offer.

Source: Anbima, CETIP, BNDES and line ministries.

Issuer Ticker Bond Type Issue Value Maturity Yield Rating Sector Offer TypeDate (R$ million) (years) (local)

Linhas de Transmissão de Montes Claros S.A. LTMC12 Infrastructure² 8/15/2012 25 17 8.75% + IPCA³ Electric Power Transmission Line CVM 4764

Rio Canoas Energia S.A. RCNE22 CAPEX¹ 8/15/2012 75 12 7.89 + IPCA³ Hydroelectric Power Plants CVM 4764

ALL – América Latina Logística Malha Norte S.A. FERR18 Infrastructure² 9/25/2012 160 8 10.10% Railway CVM 4764

Concessionária do Sistema Anhanguera-Bandeirantes S.A. (Autoban) ANHB24 Infrastructure² 10/15/2012 135 5 2.71% + IPCA³ brAAA (S&P) Toll Road CVM 4005

BR Malls Participações S.A. BRML13 CAPEX¹ 12/15/2012 420 11 13.49% Shopping Malls CVM 4764

Concessionária Auto Raposo Tavares S.A. (CART) CART12 Infrastructure² 12/15/2012 380 12 5.80% + IPCA³ A1.br (Moody's) Toll Road CVM 4005

Santo Antônio Energia S.A. SAES12 Infrastructure² 12/27/2012 420 10 6.20% + IPCA³ Energy CVM 4764

Interligação Elétrica do Madeira IEMD12 Infrastructure² 3/18/2013 350 12 5.50% + IPCA³ Energy CVM 4764

7 3.80% + IPCA³

11 4.28% + IPCA³Concessionária Ecovias dos Imigrantes S.A. Infrastructure² 881 Toll Road CVM 4005AAA (S&P)4/17/2013

Secretaria de Política Econômica

24

Development of Infrastructure Bonds Market (CVM rule 400)BR

L Million

Source: ANBIMA. Elaboration: MF/SPE.

135

380

881

0

300

600

900

1.200

1.500

October 15, 2012. December 15, 2012. April 17, 2013.

AUTOBANFirst issuance distributed to individuals ( + than 1,500)

Tenor: 5yrs

Inflation linked

CARTDistribution: individuals (15%), non residents (23%), pension fund (23%)

Tenor: 12yrs

Votorantim as a Market Maker

Inflation linked

ECOVIASDistribution: individuals (90%) and non residents (10%)

Demand 3x the issuance amount

Tenors: 7yrs and 11 yrs

Inflation linked

Secretaria de Política Econômica

Outline

Brazilian Capital Markets Its short‐term natureRecent developments

Long‐term bank lendingThe role of BNDES

Policies to reduce short‐termism Why do we care?1st generation of policies2nd generation of policies

BNDES “crowding‐in”, private sector initiatives and challenges ahead

25

Secretaria de Política Econômica

BNDES

Collateral may be shared pari passu with investors;

Contracts may include cross‐default provisions;

BNDESPAR may buy and sell Capex and Infrastructure bonds to stimulate liquidityin the secondary market.

Anbima’s New Fixed Income Market

Rules applied to public issuances, by voluntary decision, in order to guaranteehigher security, transparency and liquidity.

Some features are aligned with Law 12,431/11, especially regarding the termextension (duration of 4 years) and not linked to floating rates.

26

Development of Corporate Bond MarketProject Bonds ‐ Law 12,431/11

Secretaria de Política Econômica

Development of Corporate Bond MarketProject Bonds ‐ Law 12,431/11

NEXT STEPS

Consolidation of avaible vehicles: Mutual Investment Fund (IF) and ReceivablesSecuritization Fund (FIDC).

To improve diversification of domestic investor base: combination of lowinvestment amount and no need of credit analysis by investors.

Extension in the rules of eligible infrastructure projects:

Health, Education and Prisions

Develop a project finance market, especially for high yield credits

Expertise for assessing risk in projects as well as knowledge of structures tomitigate these risks other than traditional banking guarantees needs do bedeveloped.

So far successful deals were related to brownfield projects, with investmentgrade sponsors and BNDES collateral sharing clauses.

27

Secretaria de Política Econômica

Development of Corporate Bond MarketInvestor Base

DISCUSSIONS UNDER WAY

Changes in the investment rules of open pension funds – will increase demandfor long‐term bonds.

Corporate and Government Bond ETF (Exchange‐Traded Funds) – simplicity, lowcost and transparency provide an adequate environment for investments fromthe retail investment base.

One of the alternatives for a ETF index is to consider Capex and Infrastructurebonds (or any other long‐term corporate bond) in its composition.

BNDES as an important partner to develop this new vehicle.

28

Secretaria de Política Econômica

Development of Corporate Bond MarketSecondary Market

LIQUIDITY

BNDES has an important role in the development of corporate bond market. Its main actions are:

(i) Program for acquisition of debentures –primary and public issuances in order to guarantee between 5% and 20% of total issuance;

(ii) Presence in secondary market trough electronic platform to increase liquidity;

(iii) Issuances of debenture to promote a market standardization, incentivizing longer maturities bonds and with fixed rates or inflation linked bonds.

29

Secretaria de Política Econômica

LIQUIDITY

Market Maker Fund – ongoing discussion.

May increase demand by institutional investors and non residents for corporate bonds.

Eligible bonds would be corporate bonds under Law 12,431 and Anbima’s New Market Fixed Income – best practices and standardization

Banks as Market Maker of Issuances

“Concessionária Auto Raposo Tavares” hired Votorantim (an investment bank) as market maker of “CART12” (infrastructure bond).

Liquidity highlights ‐ CART12 Jan. 13 – top 10 most traded debentureFeb. 13 – the most actively traded corporate bondMar. 13 – among the most traded debentures, eleventh most traded.

Development of Corporate Bond MarketSecondary Market

30

Secretaria de Política Econômica

31

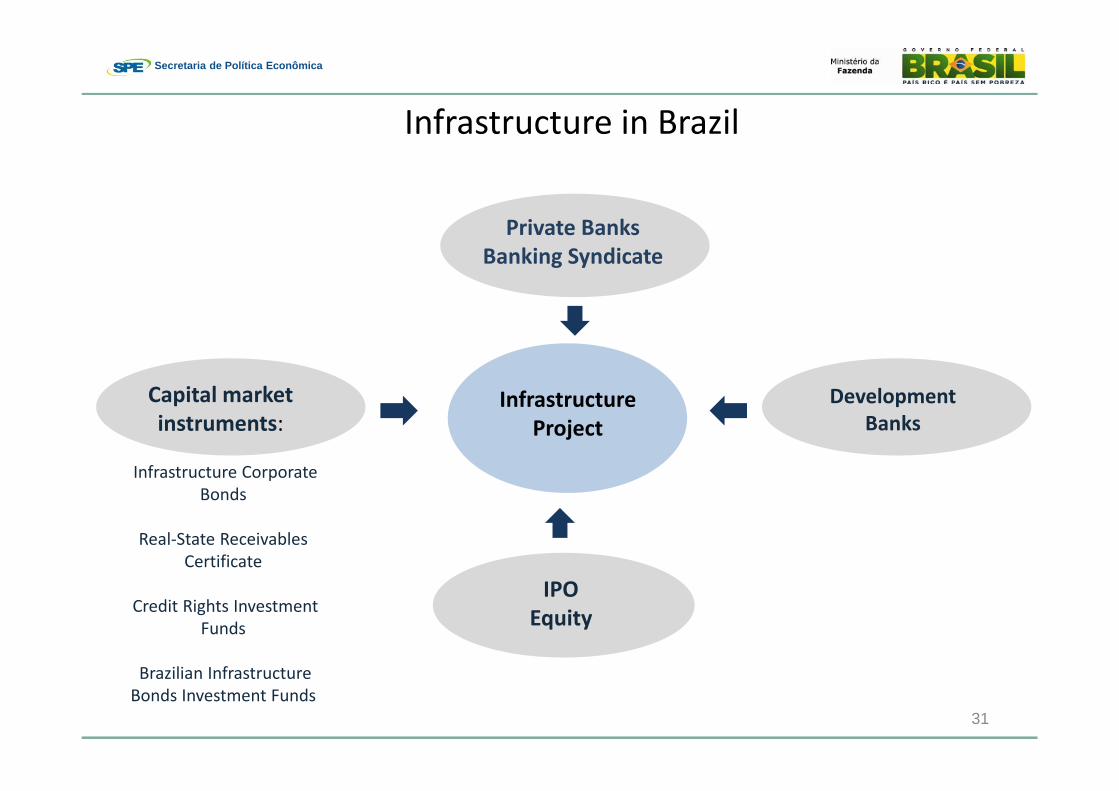

Infrastructure in Brazil

Infrastructure Project

Private BanksBanking Syndicate

Development Banks

Capital marketinstruments:

IPOEquity

Infrastructure Corporate Bonds

Real‐State Receivables Certificate

Credit Rights Investment Funds

Brazilian Infrastructure Bonds Investment Funds

Secretaria de Política Econômica

Source: ANBIMA. Elaboration: MF/STN.Note: Credit Bonds represent securitized credit, such as mortgages and agricultural notes.

Fixed Income Market Distribution (BRL bn) – Mar/13 Private Fixed Income Distribution (BRL bn) – Mar/13

Private Fixed Income Distribution by Instrument – Mar/13

DI‐linked 88.7%

Inflation‐linked 6.2%

Selic 0.7% TR 1.5% Other 1.3%

Fixed rate 1.6%

Other 11.7%

33

(86% of GDP)

Secretaria de Política Econômica

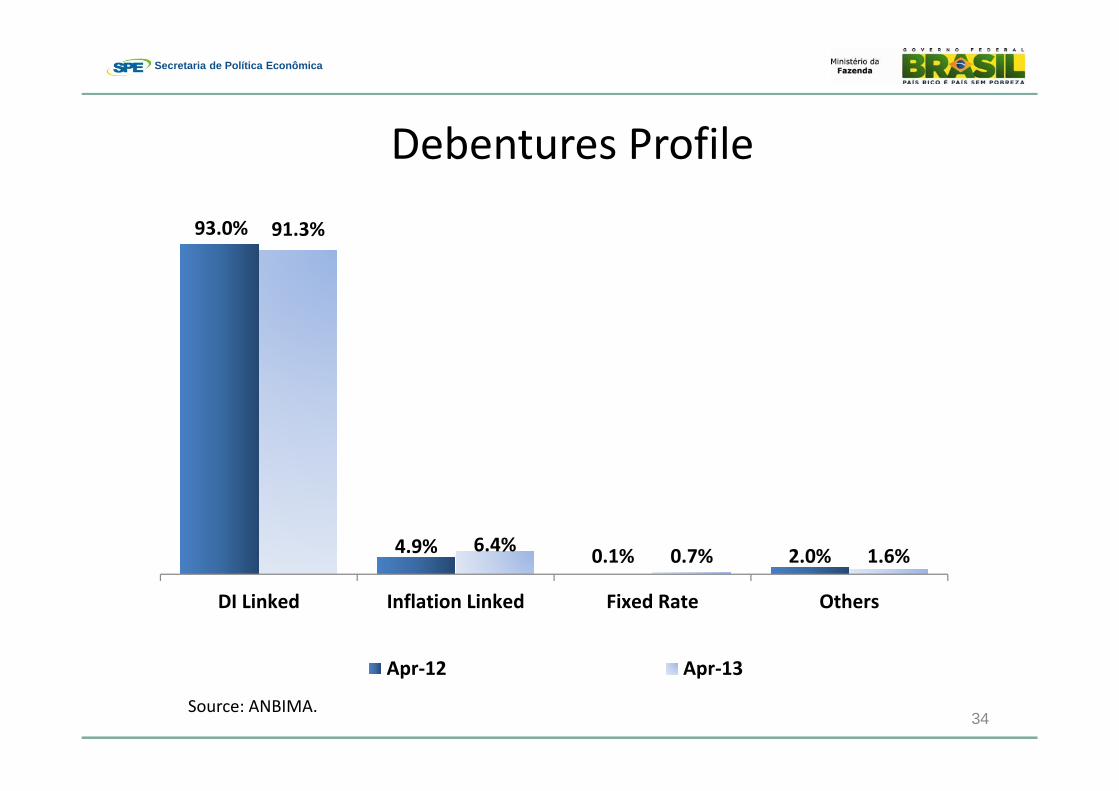

Debentures Profile

Source: ANBIMA.

93.0%

4.9% 0.1% 2.0%

91.3%

6.4% 0.7% 1.6%

DI Linked Inflation Linked Fixed Rate Others

Apr‐12 Apr‐13

34

Secretaria de Política Econômica

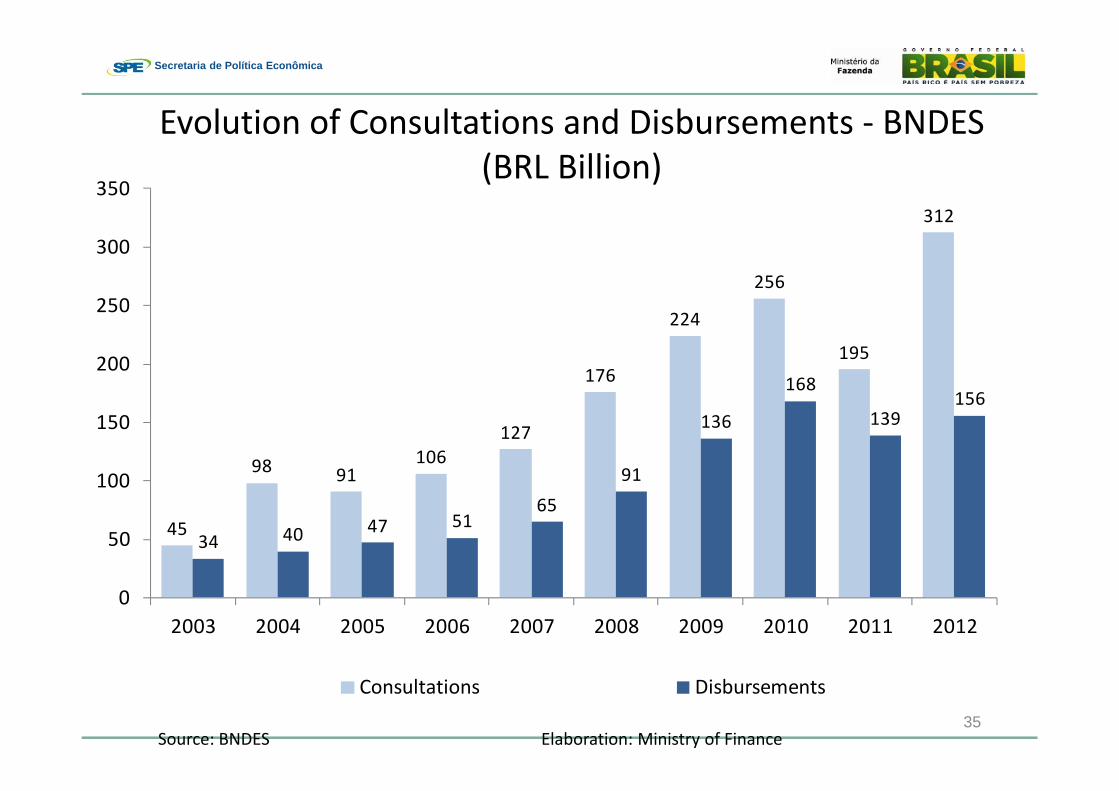

35

Evolution of Consultations and Disbursements ‐ BNDES(BRL Billion)

Source: BNDES Elaboration: Ministry of Finance

45

98 91106

127

176

224

256

195

312

34 40 47 5165

91

136

168

139156

0

50

100

150

200

250

300

350

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Consultations Disbursements

Secretaria de Política Econômica

36

Infrastructure Concession Program – Next Thirty Years

Source: Ministry of Transport Elaboration: Ministry of Finance

Concessions BRL Billion

Logistics 242.0

Highways 42.0

Railways 91.1

Ports 54.6

High‐Speed Train 35.6

Airports 18.7

Electricity 148.1

Oil & Gas 80.0

Total 470.1

Secretaria de Política Econômica

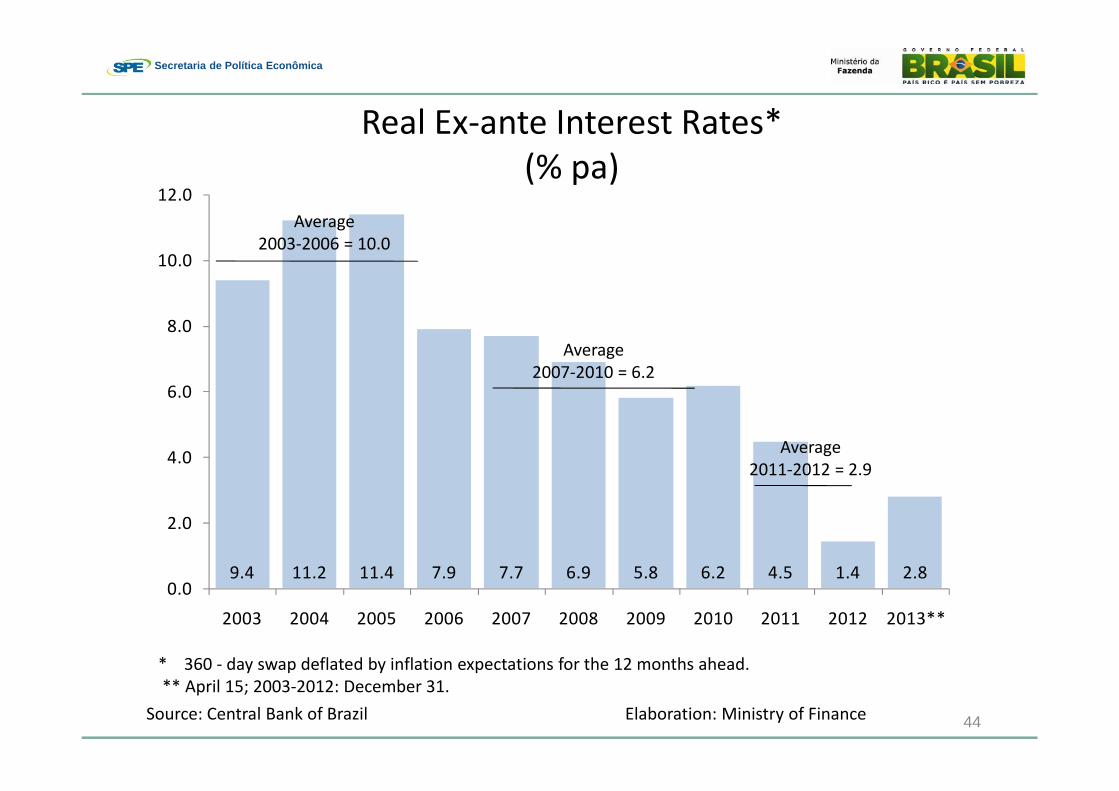

9.4 11.2 11.4 7.9 7.7 6.9 5.8 6.2 4.5 1.4 2.80.0

2.0

4.0

6.0

8.0

10.0

12.0

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013**

* 360 ‐ day swap deflated by inflation expectations for the 12 months ahead.** April 15; 2003‐2012: December 31.

37

Real Ex‐ante Interest Rates*(% pa)

Average 2003‐2006 = 10.0

Average 2007‐2010 = 6.2

Average 2011‐2012 = 2.9

Source: Central Bank of Brazil Elaboration: Ministry of Finance

Secretaria de Política Econômica

2.7

0.8 0.5 0.4 0.1 0.1 0.1

‐0.5 ‐0.7 ‐1.0 ‐1.2 ‐1.3 ‐1.5 ‐1.9‐2.8

‐3.8 ‐4.1‐4.3

‐6.5‐8.0

‐6.0

‐4.0

‐2.0

0.0

2.0

4.0

38* Data: November 2012

Real Interest Rate(Cross‐country comparisons ‐ % pa ‐ 2012)

Source: International Monetary Fund Elaboration: Ministry of Finance

Secretaria de Política Econômica

Primary Market Secondary Market

Turnover Ratio *Issuance ‐ BR$ Millions Trading Volume ‐ BR$ Millions

Source: ANBIMA Elaboration: Economic Policy Secretariat

380,0 114,6 168,5 99,0

December 15, 2012 Jan 2013 Feb 2013 Mar 2013

29,48 %

43,34 %

25,46%

9th Position

1th Position

11th Position

Ranking of the most traded debentures:

CART ‐ Infrastructure Debenture

* It is a measure of bond market liquidity that shows the extent of trading in the secondary market relative to the amount of bonds outstanding.

Secretaria de Política Econômica

40

GDP Growth(% YoY)

1.1 5.7 3.2 4.0 6.1 5.2 ‐0.3 7.5 2.7 0.9

‐1

0

1

2

3

4

5

6

7

8

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Source: IBGE Elaboration: Ministry of Finance

Secretaria de Política Econômica

41

Quarterly GDP Growth and Expectations(% QoQ)

0.8 0.5 0.9 1.4 2.5 3.0 3.3 3.40

1

2

3

4

Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013* Q2 2013* Q3 2013* Q4 2013*

GDP Actual GDP Expectations

Source: IBGE and Central Bank of Brazil Elaboration: Ministry of Finance

Secretaria de Política Econômica

Unemployment Rate(% share of economically active population)

12.3 11.5 9.8 10.0 9.3 7.9 8.1 6.7 6.0 5.50

2

4

6

8

10

12

14

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Source: IBGE Elaboration: Ministry of Finance

Secretaria de Política Econômica

43

Consumer Price Index – IPCA Index(% YoY)

Source: IBGE and Central Bank of Brazil Elaboration: Ministry of Finance

8.9 6.0 7.7 12.5 9.3 7.6 5.7 3.1 4.5 5.9 4.3 5.9 6.5 5.8 5.60

2

4

6

8

10

12

14

1999 2000 2001 2002 2003 2004+ 2005 2006 2007 2008 2009 2010 2011 2012 2013*

IPCA Lower Bound Center of the Target Upper Bound

Secretaria de Política Econômica

9.4 11.2 11.4 7.9 7.7 6.9 5.8 6.2 4.5 1.4 2.80.0

2.0

4.0

6.0

8.0

10.0

12.0

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013**

* 360 ‐ day swap deflated by inflation expectations for the 12 months ahead.** April 15; 2003‐2012: December 31.

44

Real Ex‐ante Interest Rates*(% pa)

Average 2003‐2006 = 10.0

Average 2007‐2010 = 6.2

Average 2011‐2012 = 2.9

Source: Central Bank of Brazil Elaboration: Ministry of Finance

Secretaria de Política Econômica

45

Banking Spread to Individuals and Corporations *(pp)

21.8 10.218.0 7.80.0

5.0

10.0

15.0

20.0

25.0

Individuals Corporations

Jan 2012 Jan 2013

Source: Central Bank of Brazil Elaboration: Ministry of Finance

* Spread = Lending Rate – Funding Rate.

Secretaria de Política Econômica

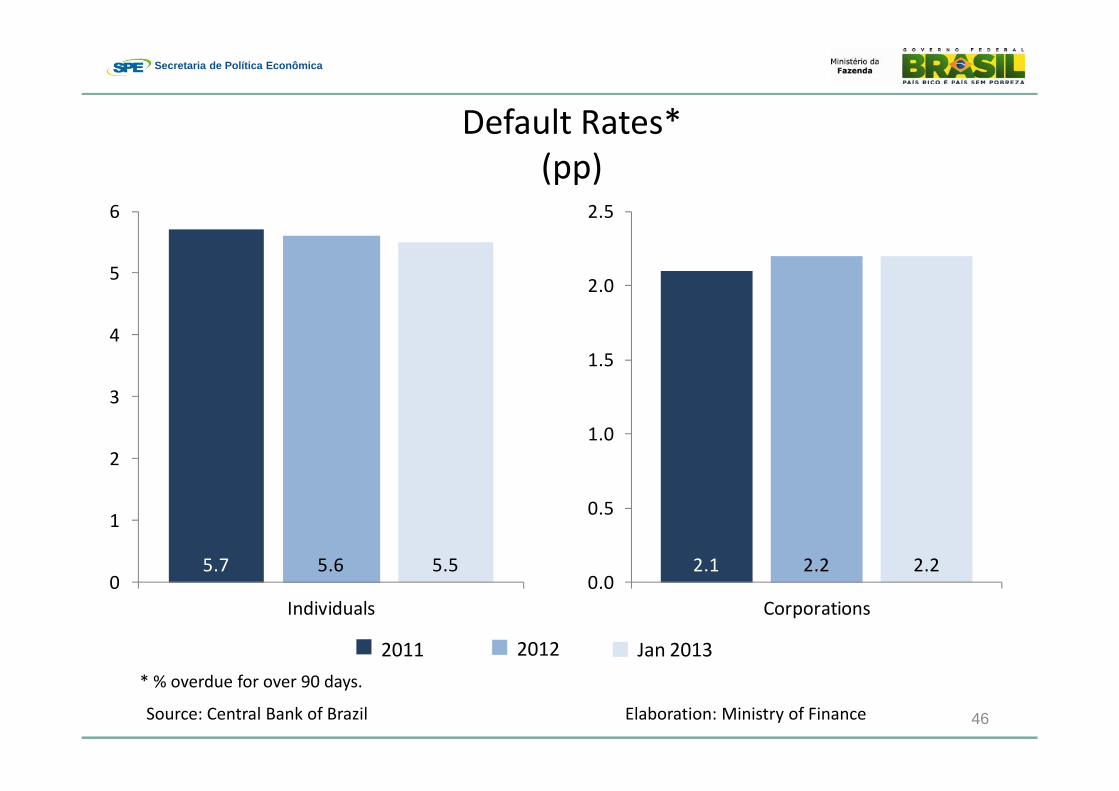

46

Default Rates*(pp)

2011 2012 Jan 2013

Source: Central Bank of Brazil Elaboration: Ministry of Finance

* % overdue for over 90 days.

5.7 5.6 5.50

1

2

3

4

5

6

Individuals

2.1 2.2 2.20.0

0.5

1.0

1.5

2.0

2.5

Corporations

Secretaria de Política Econômica

47

Foreign Direct Investment, Portfolio Foreign Investment and Current Account Balance ‐ (% do GDP)

Source: Central Bank of Brazil Elaboration: Ministry of Finance

2.8

0.7

‐2.6‐3

‐2

‐1

0

1

2

3

4

Sep‐08 Jan‐09 May‐09 Sep‐09 Jan‐10 May‐10 Sep‐10 Jan‐11 May‐11 Sep‐11 Jan‐12 May‐12 Sep‐12 Jan‐13

Foreign Direct Investment Foreign Portfolio Investment Current Account Balance