Embed Size (px)

Citation preview

1

We are a financial organization, which provides excellent service in meeting the

financial, social and educational needs of our members while maintaining long

term financial stability and member’s confidence.

LOAN POLICY

SAVE MONTHLY

INVEST WISELY

BORROW PRUDENTLY

REPAY PROMPTLY

AND

GROW WITH US

“See Fire First!”

TRINIDAD AND TOBAGO FIRE SERVICE CREDIT UNION CO-OPERATIVE SOCIETY LIMITED

2

TABLE OF CONTENTS

Contents

INTRODUCTION ............................................................................................................................................. 4

DEFINITIONS .................................................................................................................................................. 4

GENERAL PROVISIONS .................................................................................................................................. 5

CREDIT COMMITTEE...................................................................................................................................... 5

ROLE OF THE MANAGER/ LOAN OFFICER ..................................................................................................... 6

CREDIT APPROVAL LIMITS ............................................................................................................................. 6

LOANS TO CREDIT UNION OFFICERS ............................................................................................................. 7

LOANS TO STAFF ........................................................................................................................................... 7

LOAN TABLE .................................................................................................................................................. 7

LOAN APPLICATION ....................................................................................................................................... 7

INTERVIEWS .................................................................................................................................................. 8

ELIGIBILITY FOR LOAN ................................................................................................................................... 8

REPAYMENT PERIOD ..................................................................................................................................... 8

LIMIT OF LOAN .............................................................................................................................................. 8

RATE OF INTEREST ........................................................................................................................................ 9

RE-FINANCING ............................................................................................................................................... 9

RE-SCHEDULING ............................................................................................................................................ 9

ADDITIONAL LOANS TO MEMBERS ............................................................................................................... 9

WAIVER ......................................................................................................................................................... 9

BRIDGING ...................................................................................................................................................... 9

SURCHARGES FOR LATE PAYMENT ............................................................................................................... 9

FEES ............................................................................................................................................................. 10

INSTANT DEPOSITS ...................................................................................................................................... 10

PRODUCTIVE / INVESTMENT LOANS ........................................................................................................... 10

DEMAND LOANS ......................................................................................................................................... 10

SECURITIES .................................................................................................................................................. 11

PAYMENTS .................................................................................................................................................. 11

LOAN TERMS ............................................................................................................................................... 11

3

NOTICE OF DENIAL OR CHANGE ................................................................................................................. 12

REPAYMENT DIFFICULTIES .......................................................................................................................... 12

EXISTING PROPERTY .................................................................................................................................... 12

REPAIRS, RENOVATIONS, EXTENSIONS ....................................................................................................... 12

RENTAL LANDS – CHATTEL PROPERTY ........................................................................................................ 12

APPLYING FOR A LOAN ............................................................................................................................... 12

CONFIDENTIALITY ETHICS ........................................................................................................................... 13

POLICY AMENDMENTS ................................................................................................................................ 13

4

LOAN POLICY OF THE FIRE SERVICE CREDIT UNION CO-OPERATIVE

SOCIETY LIMITED

INTRODUCTION This credit policy provides the necessary rules and guidelines to ensure that the granting of loans

and the administration of the loan portfolio are managed in order to achieve the set objectives

of the Credit Union in addition to the following:

1. To provide a reliable source of funds to members.

2. To protect member savings and deposits and promote their interest.

3. To ensure that loans are adequately secured.

4. To ensure that investment in loans are of high quality.

5. To ensure equity of treatment in the processing and granting of loans.

DEFINITIONS For the purpose of this document the terms listed hereunder shall, unless indicated otherwise,

be interpreted as follows:

Net Income Income after all deductions as evidenced by salary slip or statement of

the member.

Stocks And Shares Equity in approved companies, and public companies listed on the

Trinidad and Tobago Stock Exchange.

Units Securities held with the Trinidad and Tobago Unit Trust Corporation.

Mortgage Loans Loans granted for the purpose of purchase of land, land and buildings,

construction of houses, or down payments required in respect of

mortgage offered by recognized financial institutions.

Character Loan That portion of a loan which is in excess of a member’s shareholding

and not otherwise secured.

Waiver The suspension of installment/s on a loan.

Provident Loan A loan granted for the purpose of enhancing a member’s standard of

living including housing, household items, education, health, motor

vehicles, vacation, debt consolidation etc.

Productive Loans A loan granted for agriculture, livestock, industry, commerce, service

industry, small and micro enterprise etc.

Demand Loans A loan of which repayment terms and duration are fixed at the

beginning of the agreement.

Secured Loans These are loans that are fully secured by collateral.

5

GENERAL PROVISIONS It shall be the policy of the Fire Service Credit Union to grant loans for provident and productive

purposes to eligible members of the Credit Union, based primarily on the character and integrity

of the individual and secured by whatever security is deemed necessary under the co-operative

Legislation Regulations, the Society’s bye-laws, as well as the Credit Union’s Credit Policy.

1. All loans shall be granted within the limits and restrictions of the Co-operative Societies

Act and accompanying Regulations.

2. The Board of Directors will be responsible for formulating, reviewing and adjusting the

Credit Policy, which is subject to change in whole or in part from time to time by said

Board, in the interest of the membership. Any actions taken by management, officers

and/or committees resulting from such policy shall only take place with the expressed

delegation of the Board of Directors.

3. The Credit Committee is charged with the responsibility of granting loans to members

within the loan policies established by the Board of Directors.

CREDIT COMMITTEE The Credit Committee will comprise five (5) members who will be elected at the Annual General

Meeting. They will meet at least once per week to process loan applications and perform other

related duties.

The Committee will be responsible for:

1. Setting the loan repayment terms, loan amounts, and distribution terms of each loan.

2. Approving and disapproving loan applications.

3. Conducting loan interviews and site visits.

4. Acting on all members request for loans.

5. Ensuring that all loan decisions are within the boundaries of the laws and the policies

established by the Board of Directors.

6. Monitoring and assisting in the collection of loans.

7. Promoting thrift.

8. Encouraging the wise use of credit.

9. Promoting and providing financial counselling as needed.

10. Using the consideration of character, capital, condition (economic or otherwise)

collateral capability and capacity to repay.

11. Granting sound loans.

12. Ensuring that no member or category of member is discriminated against.

13. Delegating authority to the Manager and/or Loan Officer.

14. Serving as a forum of appeal for applicants denied by the delegated authority.

6

The Credit Committee shall report to the Board of Directors each month on the performance of

the Loan Portfolio. The Committee shall also prepare an annual report that will be submitted to

the Annual General Meeting.

ROLE OF THE MANAGER/ LOAN OFFICER The Credit Committee may delegate The Manager or Loan Officer the authority to approve

loans. The Manager or Loans Officer will be responsible for the performance of the following

duties:

1. Acceptance of loan application.

2. Verify loan application information.

3. Access and check credit bureau reports.

4. Conduct loan interviews.

5. Analyze loan application and credit information using the six C’s of credit appraisal –

Character, Capital, Conditions (economic and otherwise), Collateral, Capability, and

Capacity to Replay (cash flow).

6. Make loan decisions.

7. Approve loans up to limits approved by the Board of Directors, on advice of the Credit

Committee.

8. Inform members of loan decisions.

9. Calculate loan payments and set loan terms.

10. Determine collateral values.

11. Perfect liens on collateral.

12. Prepare loan documents.

13. Obtain member’s signature on all documents.

14. Disburse loan cheques.

15. Monitor all loans and collect problem loans.

16. Approve emergency loans outside the normal jurisdiction subject to sanction by the

Credit Committee.

CREDIT APPROVAL LIMITS The Credit Committee shall be authorized to approve loans to a maximum of fifty thousand

dollars ($50 000.00). Request for loans in excess of the above shall be directed to the Board of

Directors for waiver of policy and directive as necessary.

The Manager shall be authorized to approve refinance loans up to seven thousand five hundred

dollars ($7500.00) in situations which warrant his/her action. Apart from the above, the Manager

may approve loans within the borrower’s share capital providing that all other policy

requirements are met.

7

The Loans Officer shall be authorized to approve loans as determined from time to time by the

Board of Directors on the advice of the Credit Committee.

LOANS TO CREDIT UNION OFFICERS Loans to Credit Union Officials in excess of their holdings must be approved by 2/3 of the Board

of Directors, Supervisory Committee and Credit Committee sitting together, without the

applicant, or by referendum (round robin). In which case every officer (except the applicant) must

sign the approval.

LOANS TO STAFF All loans to staff who are members shall conform to the same regulations, which obtain for the

general membership.

LOAN TABLE Loans may be granted based on holdings as follows:

Up to $25 000.00 Two to One

From $25 000.00 - $28 000.00. $25 000.00. In excess to shares

Above $28 000.00 - $30 000.00. $26 000.00. “ “

$30 000.00 - $35 000.00. $28 000.00. “ “

$35 000.00 - $40 000.00. $30 000.00. “ “

$40 000.00 - $45 000.00. $32 000.00. “ “

$45 000.00 - $50 000.00. $34 000.00. “ “

$50 000.00 - $55 000.00. $36 000.00. “ “

$55 000.00 - $60 000.00. $38 000.00. “ “

$60 000.00 - $65 000.00. $40 000.00. “ “

$65 000.00 - $70 000.00. $42 000.00. “ “

Over $70 000.00 - $44 000.00. “ “

Notwithstanding the above a member may obtain a loan in excess of the quoted figures if his

situation warrants it, the society can afford it and he provides security for the additional amount.

The Credit Union’s credit portfolio shall in its entirety be demandable, so that its recovery should

be either in cash or in its cash equivalent. This means that credit shall be based on the member’s

ability to repay and not solely on the quality of the guarantee offered by the borrower.

LOAN APPLICATION All credit granted by the Credit Union shall be based on a loan application submitted by the

member. This application should have the corresponding documents and certificates required by

the Credit Union. Staff will ensure that all applications are complete and accurate and also that

8

the application form is completed legibly and includes the member’s signature and personal

identification data as required, including:

Amount of the loan.

Purpose of the loan.

Security offered, if any.

Address and duration at present address.

Telephone number.

Employment.

Sources of income.

Total monthly obligations.

Credit history, including records.

INTERVIEWS Members may be required to attend an interview with the Manager, Loans Officer or Credit

Committee if there is need to:

Provide additional information on the application.

Verify the purpose of the loan.

Confirm the financial status of the applicant.

Give advice to the member about the convenience of credit.

Determine the reliability of the applicant according to his/her personality/character.

Establish a personal relationship.

Consider alternative arrangements.

ELIGIBILITY FOR LOAN Notwithstanding normal eligibility requirements any loan exceeding a new member’s holding

may be granted only after (6) months of regular saving.

REPAYMENT PERIOD Maximum loan repayment will be six (6) years (72 months). Every loan will have a specific

repayment schedule, which should be clearly related to the borrower’s income and ability to

repay. The Board of Directors may extend the repayment period.

LIMIT OF LOAN In no case will the amount loaned to a single member exceed ten percent (10%) of the society’s

unimpaired capital surplus re: the last audited annual account.

9

RATE OF INTEREST Rates of interest charged on loans shall be determined from time to time by the Board of

Directors.

RE-FINANCING 1. For a loan to be refinanced the borrower must have made regular payments over the

proceeding six (6) months and be otherwise eligible for the new loan.

2. Except in extreme cases, no loan other than a share loan shall be refinanced outside the

term of six (6) months.

RE-SCHEDULING Where a delinquent account is to be considered for re-negotiation, interest accrued to that

period must be paid.

All requests for extensions, re-negotiations or reductions are to be submitted to the Credit

Committee. The Credit Committee would undertake a full assessment and ensure as far as

possible that the final decision improves the member’s position while the Credit Union’s interest

is secured.

ADDITIONAL LOANS TO MEMBERS Members may have more than one loan at a time provided that he/she has the capacity to service

both loans.

WAIVER 1. Waiver of payment will only be considered in emergencies.

2. Waivers will not be granted to members in arrears.

3. No more than one (1) waiver may be granted per member per year at the discretion of

the Credit Committee.

BRIDGING Bridging of finance loans would be granted in accordance with the Bridging of Finance Policy.

SURCHARGES FOR LATE PAYMENT There will be a late payment surcharge for default in repayment at the due date. The surcharge

will be 0.25% per month on the outstanding balance until such time as the situation is rectified.

There shall be a grace period of four (4) days to allow for principal payment without incurring the

surcharge. After this period, the surcharge may be calculated from the day on which the payment

was due.

10

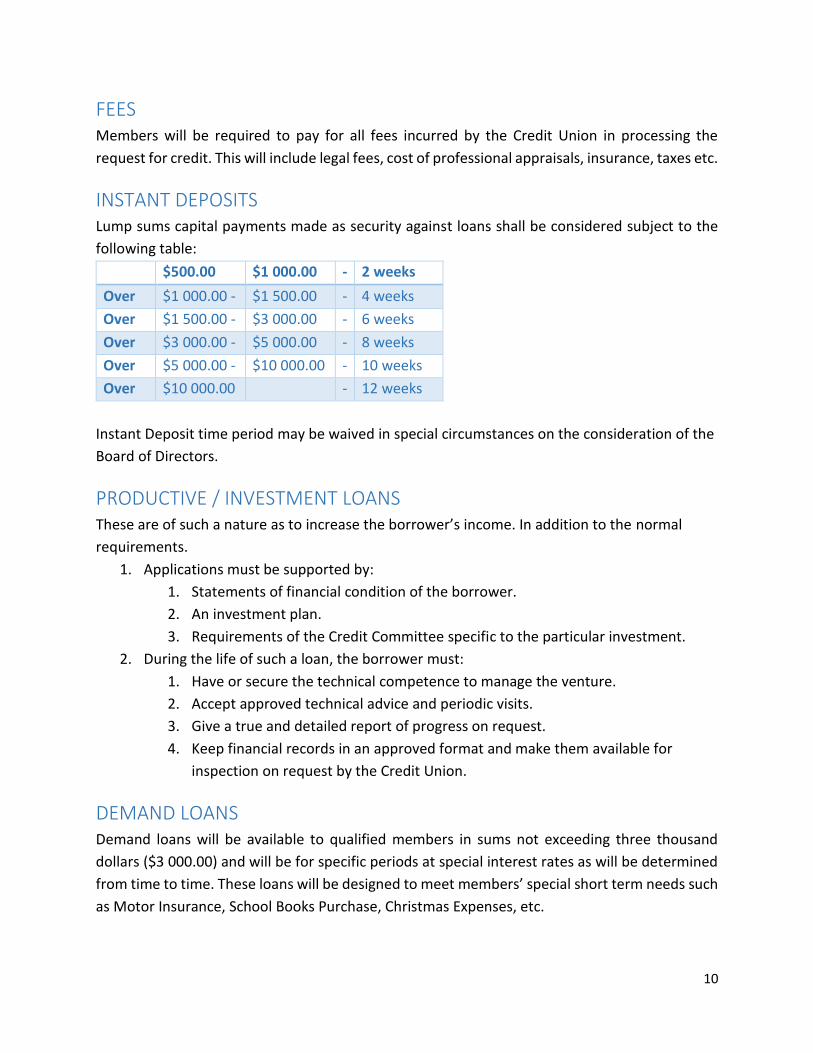

FEES Members will be required to pay for all fees incurred by the Credit Union in processing the

request for credit. This will include legal fees, cost of professional appraisals, insurance, taxes etc.

INSTANT DEPOSITS Lump sums capital payments made as security against loans shall be considered subject to the

following table:

$500.00 $1 000.00 - 2 weeks

Over $1 000.00 - $1 500.00 - 4 weeks

Over $1 500.00 - $3 000.00 - 6 weeks

Over $3 000.00 - $5 000.00 - 8 weeks

Over $5 000.00 - $10 000.00 - 10 weeks

Over $10 000.00 - 12 weeks

Instant Deposit time period may be waived in special circumstances on the consideration of the

Board of Directors.

PRODUCTIVE / INVESTMENT LOANS These are of such a nature as to increase the borrower’s income. In addition to the normal

requirements.

1. Applications must be supported by:

1. Statements of financial condition of the borrower.

2. An investment plan.

3. Requirements of the Credit Committee specific to the particular investment.

2. During the life of such a loan, the borrower must:

1. Have or secure the technical competence to manage the venture.

2. Accept approved technical advice and periodic visits.

3. Give a true and detailed report of progress on request.

4. Keep financial records in an approved format and make them available for

inspection on request by the Credit Union.

DEMAND LOANS Demand loans will be available to qualified members in sums not exceeding three thousand

dollars ($3 000.00) and will be for specific periods at special interest rates as will be determined

from time to time. These loans will be designed to meet members’ special short term needs such

as Motor Insurance, School Books Purchase, Christmas Expenses, etc.

11

SECURITIES Loans must be secured by one or more of the following:

1. Borrower’s character;

2. Applicant/Borrower’s Share Capital;

3. Co-makers (who must also complete a separate form);

4. Share/Stock Certificates (at a percentage to be determined by the Board of Directors from

time to time);

5. Unencumbered Property (preferable in the name of the applicant);

6. Insurance Policy(ies) – (ninety percent of cash surrender value) NB: The applicant is

responsible for maintaining the value of the policy;

7. Any other securities which may be deemed necessary (from time to time) by the Board of

Directors.

PAYMENTS Repayment is to be made by means of one of the following methods:

Salary assignment.

Salary deduction.

Standing order from the member’s bank.

Standing order for deductions from the member’s savings account at the Credit Union.

Other modes of repayment must be specially authorized.

Payments additional to those scheduled may be made at any time.

LOAN TERMS The normal period of a loan with the Credit Union will be a maximum of six (6) years with the

following table as a general guide.

Amount Months

Up to $1 000.00 12 months

$1 001.00 - $5 000.00 20 months

$5 001.00 - $7 000.00 26 months

$7 001.00 - $10 000.00 32 months

$10 001.00 - $15 000.00 38 months

$15 001.00 - $20 000.00 44 months

$20 001.00 - $25 000.00 50 months

$25 001.00 - $30 000.00 56 months

$30 001.00 - $40 000.00 60 months

Over $40 000.00 72 months

12

NOTICE OF DENIAL OR CHANGE All applicants whose request for credit has been denied will be notified in writing. This notice will

also state the reasons for the denial.

Loan applicants will be notified in writing of any change in the conditions of their requests.

REPAYMENT DIFFICULTIES Members experiencing difficulty in meeting loan payments should advise the Credit Union

immediately in writing.

Financial Counseling will be made available to members having difficulty in repaying loans.

EXISTING PROPERTY A request to purchase an existing property must be accompanied by:

A copy of the deed.

Proper and Authentic proof of ownership.

Evidence encumbered status of the property.

Evidence of market value.

REPAIRS, RENOVATIONS, EXTENSIONS A request for credit to erect to a new building must be accompanied by the following:

An estimate of the cost of the project – including labour and materials.

A statement of the expected length of the project, including the expected date of

completion signed by the contractor.

Drawings of the proposed renovations or extensions where applicable.

RENTAL LANDS – CHATTEL PROPERTY Where there is no lease for rented lands, proof of tenancy must be firmly established and the

landlord must supply a letter of consent.

APPLYING FOR A LOAN Members applying for loans are required to submit the following documents where applicable

in order to facilitate processing:

1. Most recent payslip.

2. Original invoices or quotation for furniture, appliances, machinery equipment, airline

ticket, school books, insurance policy etc.

3. Proper statement of estimates for labour, construction service etc.

4. Certified copy of ownership of vehicle.

13

CONFIDENTIALITY ETHICS All transactions with members of the Fire Service Credit Union shall be kept confidential. Staff

members who reveal confidential information under unauthorized conditions can be dismissed.

Credit Committee members guilty of a breach of confidentiality shall be suspended. Staff and

officials shall not be involved in consideration of loan applicants of immediate family members.

Credit Committee member must disclose conflicts of interest.

POLICY AMENDMENTS The Board of Directors may amend this policy, but must minute the amendments and post the

change for the information of all members as soon as possible after the change is made.