Embed Size (px)

Citation preview

Welcome the Logistics Officer Association Professional Development Module 3, Show Me the Money. This module was developed by the Robins Air Force Base Middle Georgia Chapter. The purpose of this module is to educate Air Force logisticians from all career fields on how the military and DoD allocates, approves and spends money with particular focus on the Air Force.

1

Today we will be discussing the flow of money into the various acquisition programs in the Air Force. We will go over the budget resolution, where the money comes from and the framework for the federal budget. Additionally, we’ll cover the authorizations and appropriation acts, who authorizes and approves the money. Furthermore, we’ll touch on the different colors of money and the different pots of money for specific parts of a program. Finally we’ll discuss monetary concepts and continuing resolution and how we execute that money.

We will start off with the Budget resolution which will set the pace for this module and also describes high-level money planning from Congress where they decide what the various budget totals are and divide money into the different functional categories.

2

To start the enactment process, Congress produces a concurrent resolution on the budget. The budget resolution provides guidance for each year's revenue and spending legislation. Congress uses this guidance as it coordinates various budget-related actions, such as the consideration of appropriations and revenue measures.

It is legislation in the form of a concurrent resolution setting forth the congressional budget. The budget resolution establishes various budget totals, divides spending totals into functional categories like national defense, transportation, education, healthcare and international security assistance. There are 20 major functional categories of the federal budget and may include reconciliation instructions to designated House or Senate committees.

Once Congress decides who will get what amount of money, it goes through a g g y g gprocess before it reaches the lowest levels, such as the system program offices where it will be actually spent. The starting point for all of this is authorization.

3

The Authorization Act defines the scope and content of programs and policies.

Authorization committees are the House Armed Services Committee (HASC) and Senate ArmedAuthorization committees are the House Armed Services Committee (HASC) and Senate Armed Services Committee (SASC). The HASC is a committee within the U.S. House of Representatives dealing with military spending and oversight. Committee members organize into subcommittees for hearings on military training, housing, research, and other matters of national defense. These subcommittees are responsible for recommending legislation that maintains and improves the efficiency of the U.S. Armed Forces. They are the starting point for legislation dealing with personnel, operations, and resources of the Armed Forces.

Legislation approved by a majority of the HASC are sent to the full House for a vote. This vote determines whether pending legislation is rejected or sent to the Senate Armed Services Committee for approval. The SASC must approve the legislation as passed by the House before the full Senate votes on the bill. Members of the House and Senate Armed Services Committees may be asked to develop compromise legislation if both bodies disagree on details of a particular bill.

The SASC is the primary vehicle through which the Senate exercises its constitutional and statutory duties to oversee national defense. The committee’s responsibilities encompass “comprehensive study and review of matters relating to the common defense policy of the United States.” The committee crafts the annual National Defense Authorization Act, which authorizes spending on weapon systems as well as pay and benefits for troops and sets policy on a multitude of issues relevant to defense. The issues range from research and development of new weapons to personnel policies. It is also responsible f l i h f h D f D f i l di h D f h A hfor general oversight of the Department of Defense, including the Department of the Army, the Department of the and the Department of the Air Force.

The authorization act provides authorization for each DoD appropriation account. Before money is to be approved for any spending, the committees involved in this act ensure that the appropriation account is authorized, that it is legal and that it is an item that the DOD needs.

Through this act, the committees are able to program approval, procurement quantities, personnel end strength and funding ceilings.

Next, we will talk about the appropriations act, what it is and how it fits into the flow of money schedule.

4

The Appropriations Act contains the budget for the entire nation. Everything that is being bought with taxpayer money falls into a category or account and that account is an appropriation. For example, in the defense budget for the AF, we would have an appropriation account for acquiring weapon systems, which we will see later in this module.

Like the Authorization Committees, the Appropriations Committees are the House pp pAppropriations Committee (HAC) and the Senate Appropriations Committee (SAC). The HAC is the committee that is in charge of setting the specific expenditures of money by the government. They hold the power of the purse. The SAC is a standing committee, which is a committee established by an official and providing for its scope and powers, and the largest committee in the U.S. senate. Its role is defined by the U.S. Constitution and requires "appropriations made by law" prior to the expenditure of any money from the Treasury and is therefore one of theprior to the expenditure of any money from the Treasury, and is therefore one of the most powerful committees in the Senate. It writes the legislation that allocates federal funds to the numerous government agencies, departments, and organizations on an annual basis. Appropriations are limited to the levels set by a Budget Resolution, drafted by the Senate Budget Committee.

Through this act the committees are able to give the structure to designate specificThrough this act, the committees are able to give the structure to designate specific amounts of money for specific programs. They provide the funds to operate.

Some key things to note here are that the Appropriation is not money, but rather, the obligation authority. There are 12 Appropriations Acts each year, and Defense is usually funded by 3 Acts, which are Defense, Military Construction and Energy and WaterWater.

Now that we’ve discussed the authorizations and appropriations acts, you may be wondering what the real difference between the two are since they both have high powered committees involved in similar actions.

5

Many people get confused with the terms appropriations and authorizations, so what y p p g pp p ,do they really mean and what’s the difference? In layman’s terms, one puts money in the checkbook and one opens the checkbook, or allows it to be used. The appropriations puts money and the authorization opens the checkbook.

Simply put, the Appropriation bills actually provide the money for the project, and the Authorization bills create projects and establish how much money can be spent p j y pon them.

The appropriations takes care of the legal part of things and gives specific rules on what and how we are to spend the money, and then puts that money in the account. Think of it like when you apply for a credit card, or like our government travel card. The credit card company will decide how much money they will give you, or how p y y y g y ,much line of credit, and they will also give you rules on the interest rate and how you can use the card and even give you details on how to use the card for rewards. As you all know, the GTC card is meant to be used for military travel during TDY and there are special rules as to what you will and will not use it for. They then authorize it by sending you the card, or give you the card to spend the money.

Now that you know what authorizations and appropriations are, lets take a look at a chart which shows the different steps and levels of how the money flows.

6

This diagram illustrates the flow of money all the way from when it is decided that money is needed to fund a project or program down to the program office that will execute it. After Congress passes the DoD Appropriations Bill and the President signs it, then the Office of Management and Budget (OMB) distributes the Budget Authority to the DoD. This distribution is called Apportionment. The Apportionment process can take several weeks. A signed document accompanies and carries out the actual movement of funds. The program office cannot obligate funds until the authority the paperwork reaches the comptroller for the programfunds until the authority, the paperwork, reaches the comptroller for the program office. The Office of Management and Budget (OMB) apportions funds to the DoDComptroller on a quarterly, annual, or other periodic basis, depending on the appropriation.

The funds can then be obligated for the programs and needs defined in the budget development process At the bottom you will see that the money reaches thedevelopment process. At the bottom, you will see that the money reaches the program office, but how is the money is executed?

Sources:

https://learn.dau.mil/CourseWare/1_9/rem/summary_L10.html

7

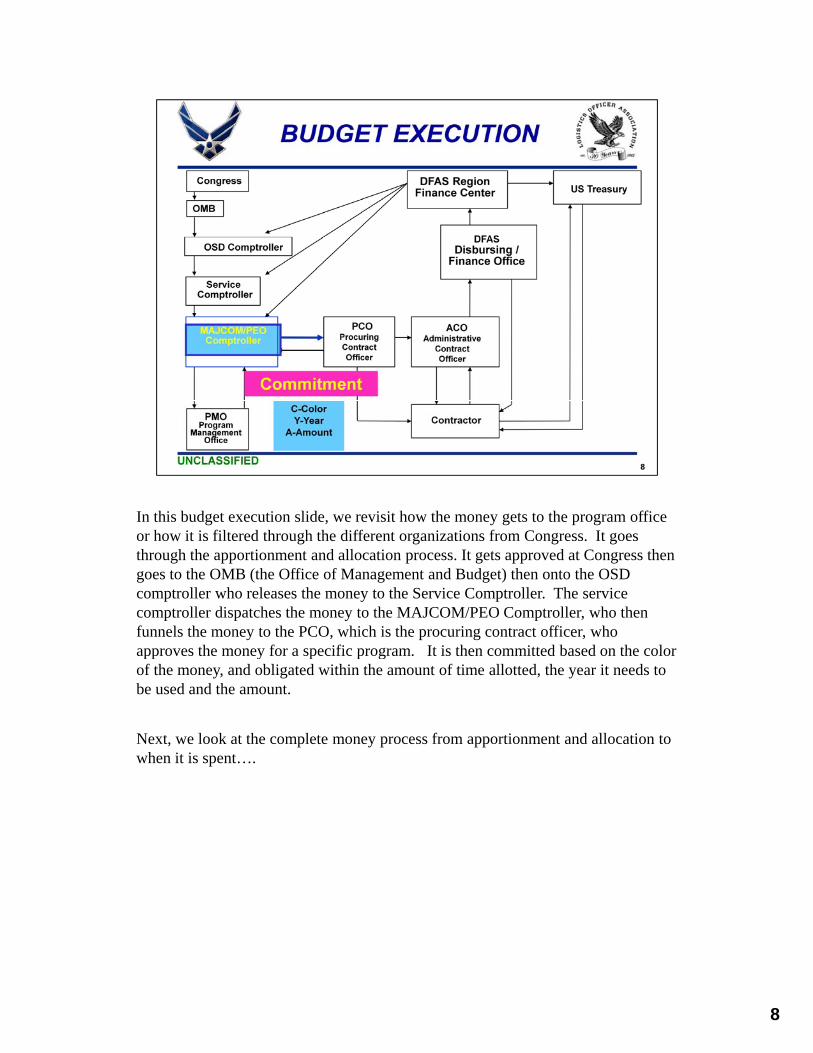

In this budget execution slide, we revisit how the money gets to the program office or how it is filtered through the different organizations from Congress. It goes through the apportionment and allocation process. It gets approved at Congress then goes to the OMB (the Office of Management and Budget) then onto the OSD comptroller who releases the money to the Service Comptroller. The service comptroller dispatches the money to the MAJCOM/PEO Comptroller, who then funnels the money to the PCO, which is the procuring contract officer, who approves the money for a specific program It is then committed based on the colorapproves the money for a specific program. It is then committed based on the color of the money, and obligated within the amount of time allotted, the year it needs to be used and the amount.

Next, we look at the complete money process from apportionment and allocation to when it is spent….

8

1115

The left side of the diagram is the Apportionment Process we just went over. So now let’s look at how the PMO t ll t f dPMO actually executes funds.

So we start off with the Funding Document (number 1). The money commitment is in response to a formal request from the PMO or program management office. This could be because of a procurement request, a project order, a MIPR (military interdepartmental purchase request) or an engineering change proposal that will modify an existing contract.

Then we move on to the actual commitment, numbers 2, 3 and 4. Here, you have the comptroller above the PMO level (could be a MAJCOM or product center) who certifies that funds are available by checking three things: Correct Appropriation (color), work is identified for the right fiscal year, and that there are enough funds (amount) to cover the anticipated obligation. Then they commit the funds (ADMIN res of funds) and issues a certification to the PCO that funds are available.

Then we move on to the Obligation portion of the chart where in number 5, the PCO signs the contract mod, and obligates the funds. Then the PCO passes the information on to

DFAS and to the ACO, who exercises surveillance over the contractor (often at the plant). The PCO also provides a record of the obligation back to the Comptroller.

We then move on to the invoice portions which are numbers 9 and 10. At number 9, the contractor does the work and incurs the cost, then submits the invoice or payment request to the ACO

The ACO then certifies that the work was done and passes the invoice to DFAS.

In numbers 11, DFAS then sends a check to the contractor and number 12 is when the expenditure is reported to the DFAS Regional. Finance center.

We then move on to reporting the expenditure. Number 13 deals with the expenditure reporting system where DFAS Regional passes the expenditure info on to Treasury (in number 14) and back to the Comptrollers

Next we move on to Cash In number 15 after the Treasury receives confirmation of the expenditure and

9

Next we move on to Cash. In number 15, after the Treasury receives confirmation of the expenditure and the Contractor cashes the check which is called the Outlay (number 16) -- the first time real money changes hands. Up until here it’s all been only promises, no cash.

Because of the complexity of the process, mistakes are inevitable. Next we’ll talk about some laws which address some of thepossible mistakes.

When it comes to spending money there are certain rules that we have to follow orWhen it comes to spending money, there are certain rules that we have to follow, or else laws can be broken. So, how can we get in trouble? Three questions we should always ask ourselves when we’re about to spend money are

1. Do we have the right “color of money” to make this purchase?

2. Is the appropriation we’ll be using still available for obligations and does thispass the bonafide need test?

3. Do we currently have the amount of funding needed for this purchase?

It is a violation if we spend money on something we are not authorized to. For example, we were given money for operation and maintenance of a weapons system. It would be a violation if we decided to take the allotted O&M money to spend on research and development, which is supposed to come from a different pot of money.

Next we have the bonafide need rule, which provides for a certain amount of time to obligate money to spend. You’ll recall that we just learned that the different appropriations have different appropriation life before they expire. For example, the obligation period for MILPERS is one year, which means that if we get the go ahead to obligate funds in FY15, then it can only be used for FY15, not FY16 or 17 or whenever we feel is the best time for the money to be used. It has to be obligated to be used in the FY15 timeframe. If we don’t follow that rule, it will result in a bona fide need violation.

The third legal restriction deals with spending money you don’t have. You are given a certain amount of money to spend and if you need more, than you ask for more, but it is not a good idea to go ahead and promise and spend money for the future with funds that you don’t even have. DO NOT obligate or expense in excess of amount authorized and DO NOT obligate or expense in advance of an appropriation. This is called an anti-deficiency act.

10

These are important rules to remember. However, there are some exceptions, or rather, differences to be aware of.

Various categories of funding or appropriations made available to the Government are commonly referred to as "Colors“ of money to distinguish their unique purpose and usage. The main appropriations that we will deal with in the Air Force are the five here. They are procurement, MILCON, MILPERS, O&M and R&D. The chart also shows the appropriate life in years. For example, if we look at the O & M category, you will have one year to obligate the money once it’s appropriated, in order to get it on contract to startyou will have one year to obligate the money once it s appropriated, in order to get it on contract to start using it. The obligation period is the amount of time you have to use the money before it expires.

The procurement appropriation category consists of a number of procurement titles such as Shipbuilding and Conversion Navy, Aircraft Procurement Air Force, Missile Procurement Army, Procurement Marine Corps, etc. Procurement appropriations are used to finance investment items, and should cover all costs necessary to deliver a useful end item intended for operational use or inventory. Items classified asnecessary to deliver a useful end item intended for operational use or inventory. Items classified as investments and financed with Procurement appropriations include those whose system unit cost exceeds $250K. For example, 3010 is aircraft procurement, 3020 is missiles procurement and 3080 is classified as “other”.

Military Construction appropriation accounts receive considerable attention from Congress, and are enacted separately from the Defense Appropriations Act These appropriations fund the costs of majorenacted separately from the Defense Appropriations Act. These appropriations fund the costs of major construction projects such as bases, facilities, military schools, etc. Project costs include architecture and engineering services, construction design, real property acquisition costs, and land acquisition costs necessary to complete the construction project. MILCON is considered an investment account. Examples of projects properly financed in the MILCON appropriations include missile storage facilities, intermediate maintenance facilities, medical and dental clinics, technical libraries, and physical fitness training centers.

Military Personnel appropriation accounts are similar in nature to those of O&M in that both are considered expense accounts. MILPERS appropriations are used to fund the costs of salaries and compensation for active military and National Guard personnel as well as personnel-related expenses such as costs associated with permanent change of duty station (PCS), training in conjunction with PCS moves, subsistence, temporary lodging, bonuses, and retired pay accrual.

Operations and Maintenance appropriations traditionally finance those things whose benefits are derived for a limited period of time rather than investments. Examples of costs financed by O&M funds are headquarters operations, civilian salaries and awards, travel, fuel, minor construction projects of $750K or less, expenses of operational military forces, training and education, recruiting, depot maintenance, purchases from Defense Working Capital Funds, think spare parts, base operations support, and assets with a system unit cost less than the current procurement threshold of $250K O&M appropriations are

11

with a system unit cost less than the current procurement threshold of $250K. O&M appropriations are normally available for obligation for one fiscal year. O&M appropriations are budgeted using the annual funding policy.

Research, Development, Test and Evaluation appropriation accounts finance RDT&E efforts performed by contractors and government installations to develop equipment, material, or computer application software

The other colors of money include those that are not appropriated directly to a program. That may use existing funds to reimburse Working Capitol Funds. That tap industry to fund upfront on redesign. And lastly, that receive Congressional plus-ups for Special Interest Items.

In the acquisition community, especially in logistics, we may not deal directly with this, or deal with it as frequently as the other clearly defined colors of money, but it is good to know that there are colors of money not strictly defined.

Now that you have an idea of the different colors of money, let’s talk about how and when money is allotted based on its purpose.

12

DoD funding policies are the ground rules, derived from Congressional direction, concerning the amount and timing of budget requests for various appropriations; in other words how much budget authority may be requested to support a particularother words, how much budget authority may be requested to support a particular effort during a fiscal year. Essentially, these funding policies serve to ration scarce budget authority among DoD's many activities and programs.

Appropriations fall into three basic groups, to which the DoD has corresponding policies for budgeting.

First, we have the annual funding policy which applies to appropriations that are only available for obligation for one year, O&M and MILPERS appropriations. Simply stated, the policy requires that you request budget only for the estimated cost of the goods and services needed in a given fiscal year. Costs budgeted in Operations and Maintenance (O&M) and Military Personnel (MILPERS) appropriations are considered expenses and are therefore subject to the annualappropriations are considered expenses and are, therefore, subject to the annual funding policy.

Next, we have the full funding. Costs budgeted in the Procurement and Military Construction (MILCON) appropriations are considered investments and are, therefore, subject to the full funding policy.

Lastly, we have the incremental funding policy which applies to Research, Development, Test, and Evaluation (RDT&E) appropriations. Although RDT&E efforts often span several years, the incremental funding policy requires that the effort generally be budgeted in annual increments based on when costs are expected to be incurred. Costs budgeted in the Research, Development, Test and Evaluation (RDT&E) appropriations include both expenses and investments and are therefore(RDT&E) appropriations include both expenses and investments and are, therefore, subject to the incremental funding policy.

As you can see, there a lot of rules concerning how the AF and other services within the DoD spend, handle and manage money. We covered the colors of money, legal restrictions, and funding policies, now we will review the status of funds.

13Sources:

h //l d il/C W /10 7/ di / d2/ 2 h l

There are three main status of funds and they are active, expired and cancelled funds. Active or Current Funds are when funds can be obligated and ready to spend on new items. That is monies whose availability for new obligations has not yet expired under the terms of the governing appropriations act.

Next is expired funding. This is money that can no longer be obligated or put on contract for new requirements, but is still available to pay the bills. That is monies whose availability has expired for new obligations, but which are available to adjust and liquidate previous obligations.

Third, we have cancelled funds, which are funds that are no longer available for anything, including to pay the bills.

Continuing resolution has been a hot topic in the news lately, but what does it really mean?

14

If Congress is unable to pass one or more appropriations acts by 1 October, the beginning of the fiscal year, it must provide Continuing Resolution Authority (CRA) to prevent agencies whose appropriations have not been passed from shutting down. This must happen because money is needed to keep programs running. A Continuing Resolution (CR) provides "stopgap" funding to keep affected agencies operating for a specified period of time. This period, spelled out in the resolution, may range from a few days to a few weeks or months, depending on when Congress believes it can pass the final appropriations bills or actswhen Congress believes it can pass the final appropriations bills or acts.

This happens through a joint resolution that is passed by Congress and then signed by the President. This then allows the government to continue to operate for a limited period of time with a limited amount of money, until they resolve the issues that are preventing appropriation and get back on schedule.

Late enactment of appropriations presents several problems to DoD and its programs. First, Continuing Resolutions usually contain language which prohibits "new starts," or activities which were not funded and did not take place in preceding years. Secondly, rates of obligation permitted under a Continuing Resolution are usually limited and may impede the timely execution of program efforts.

15

In this professional development module, we discussed the importance of money in the DOD and how it is approved, allocated and spent, with particular emphasis on the Air Force, and how money is distributed to different programs. We also discussed the budget resolution and the importance of the budget being resolved. It is equally important for us to understand the authorization and appropriations act and the difference between the two. We then talked about the flow of funds and how they are executed, the different colors of money, what they mean and how they are represented as well as their obligated time periods and important rules such asare represented, as well as their obligated time periods and important rules such as the various violations that can occur if the money is not used in the way it is intended. We touched on monetary concepts as far as funding polices and the status of funds, and the purpose of continuing resolution.

So far this process has worked in the DoD despite the recent challenges the military has experienced with the current drawdown and drastic budget cuts as well ashas experienced with the current drawdown and drastic budget cuts as well as budget resolution and the continuing resolution that we currently have in place. However, it is a process that can function in the way its intended to, and it is important for everyone to understand or at least have an idea of how the flow of money works all the way from the apportionment to the cashed check, no matter your AFSC. Money will always be the important issue and an extremely strong factor in our military mission in the US and worldwide.

16

17