Embed Size (px)

Citation preview

This presentation has been provided to you for use in a private and confidential meeting to discuss potential or existing investment advisory relationship. This presentation is not an advertisement and is not intended for public use or distribution beyond our private meeting.

Mitch Stapley, CFAChief Fixed Income Officer

Fifth Third Asset Management

Living In The U.S. Of AA+

2

Source: Bloomberg PIIG 2 Year Yields 1/13/06 – 1/11/12

Greece – Going, Going…

3

Mr. Market not believing the 50% haircut

Remember the “Voluntary” 50% Haircut?

4

Total Gross Federal Debt And GSE Debt To GNP/GDP

1916, 7.3%

1929, 16.3%

1975, 28.9%

1946, 115.7%

1919

34.7%1867, 30.7%

2011est.

101.0%

2010, 146.03%

0%

20%

40%

60%

80%

100%

120%

140%

160%

17

91

18

01

18

11

18

21

18

31

18

41

18

51

18

61

18

71

18

81

18

91

19

01

19

11

19

21

19

31

19

41

19

51

19

61

19

71

19

81

19

91

20

01

20

11

20

21

0%

20%

40%

60%

80%

100%

120%

140%

160%

Civil War

WW1

WW2

1791 to 1928 = GNP

1929 to 2010 = GDP

If GSEs Are

Counted

This Is AAA? U.S. Debt To GDP

Source: Bianco Research

5

Federal Gov't Spending and Revenue

(Pct. GDP, OMB Proj. '10-'20)

10

12

14

16

18

20

22

24

26

'46 '56 '66 '76 '86 '96 '06

Spending

Revenue

Spending At

Highest Level Since

WWII

Again, This Is A AAA Credit?

Spending = 24.5% GDPRevenues = 15.6% GDPDeficit = (8.9)% of GDP

% of GDP

Source: Strategas

6

Growth In Mandatory Entitlement SpendingSocial Security, Medicare, Medicaid

7

Source: Bloomberg C15

Imagine If They Had Cut Us To BAA?!Treasury Yields Post – Downgrade to AA+

8

$14,582

$5,878$5,497

$3,309$2,560 $2,246 $2,087 $2,051

$1,729 $1,574 $1,479 $1,407$1,039 $1,014

0

2000

4000

6000

8000

10000

12000

14000

16000

Global GDP = $63.0 trillion

Biggest Is Best

Source: Bloomberg

9

Holdings of Treasury SecuritiesThe Federal Reserve, Japan and China

0

100

200

300

400

500

600

700

800

900

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,700A

pr-

00

De

c-0

0

Au

g-0

1

Ap

r-0

2

De

c-0

2

Au

g-0

3

Ap

r-0

4

De

c-0

4

Au

g-0

5

Ap

r-0

6

De

c-0

6

Au

g-0

7

Ap

r-0

8

De

c-0

8

Au

g-0

9

Ap

r-1

0

De

c-1

0

Au

g-1

1

Ap

r-1

2

Bill

ion

s o

f D

olla

rs

0

100

200

300

400

500

600

700

800

900

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,700

Bill

ion

s o

f D

olla

rs

Japan

China

Federal Reserve

Source: Arbor

Don’t Fight the Fed

10

Source: www.crgraphs.com

Operation Twist –How Much Bang For The Buck?

QE I

QE II

Twist

11

Presidential Re-Election &

Change In The Unemployment Rate

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

-3 -2 -1 0 1 2

'04

'96

'80

'92

'84

'54

'7 2Margin of

Reelection

Victory

Change In Election Y ear

Unemployment Rate

No post-WWII presidenthas won re-election with arising unemployment ratein a presidential electionyear & vice versa.

The Ultimate Presidential Election Indicator

12

'82 '84 '86 '88 '90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '102,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

80,000

90,000

100,000

110,000

120,000

130,000

140,000

150,000

Employment

GDP (left)

Gross Domestic Product, Bil. $, Saar - United States (Left)All Employees, Total Nonfarm Payroll, Thousands Of Persons, Sa - United States (Right)Recession Periods - United States

Source: FactSet

GDP Back To New Highs – With 7 MillionFewer Jobs

13

'07 '08 '09 '10 '110

500

1,000

1,500

2,000

2,500

5,500

6,000

6,500

7,000

7,500

8,000

8,500

9,000

Bank

Deposits

w ith Fed

(R)

Corporate

Cash (R)

Bank

Deposits (L)

Cash piles continue to build on the sidelines...

H.8, Liabilities Of Commercial Banks, Deposits, Bil. Usd, Sa - United States (Right)H.4.1- Liabilities of All Federal Reserve Banks, Deposits, Depository Institutions (Mil $) - United States / 1000 (Left)Nonfarm Nonfinancial Corporate Business - Total Liquid Assets, L.102 - Levels - United States (Left)Recession Periods - United States

Vote With Your Cash

Source: FactSet

14

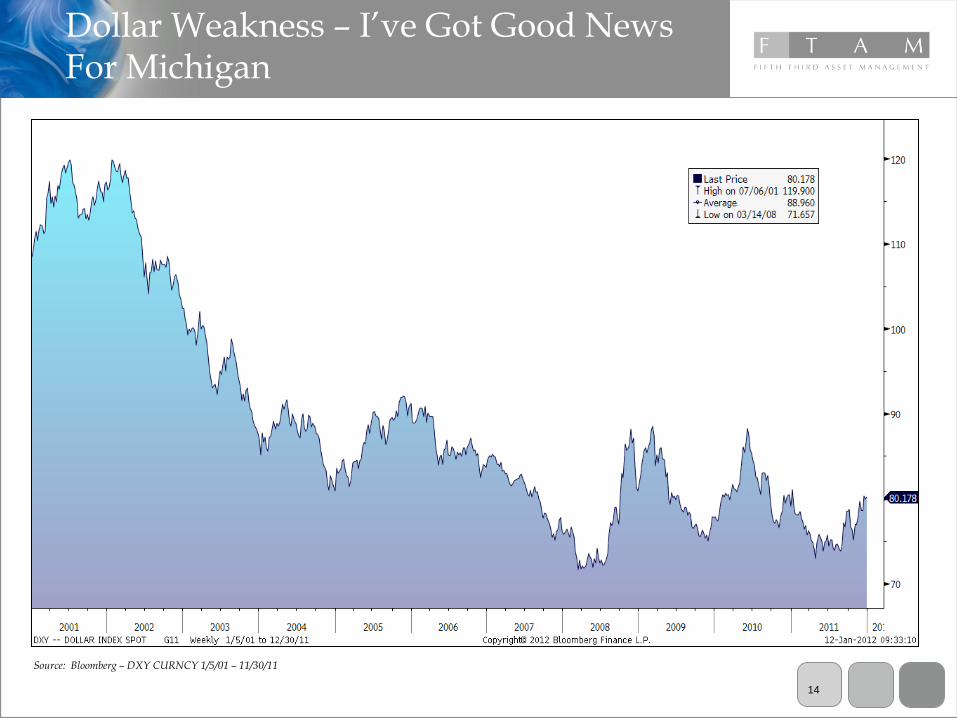

Dollar Weakness – I’ve Got Good NewsFor Michigan

Source: Bloomberg – DXY CURNCY 1/5/01 – 11/30/11

Flight to Quality

Back to Reality?

Flight to Quality

Back to Reality?Flight to

Quality

15

'82 '84 '86 '88 '90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '108

10

12

14

16

18

20

22

24

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Housing

Starts

Vehicle

Sales (L)

Construction

($bil l ions)

Exports

($bil l ions)

Economic Trends

Motor Vehicles Total vehicle sales, Number of, Annual Rate, SA - United States (Left)Housing Starts 1 unit, Number of, Annual Rate, SA - United States (Right)Total Construction Put in Place, Mil. USD, SA - United States / 1000 (Right)Net Exports Of Goods & Services, Exports, Bil. Chained 2005 $, Saar - United States (Right)Recession Periods - United States

Source: FactSet

Exports Driving The Economy

16

Source: Bloomberg Michigan Employment 12/31/1980 – 11/30/2011

Michigan On The Mend

Michigan Unemployment

Rate

Total Michigan Manufacturing Jobs

National – UR 8.5%

GR Wyoming – UR 7.1%

17Source: Ward’s Autodata (unadj.), Updated YTD 12/31/11

Detroit TurnaroundU.S. Market Share of Major Automakers:

GM FORD TOYOTA CHRYSLER HONDA NISSAN

19.6% 16.8% 12.9% 10.6% 9.0% 8.2%

35.5%

19.6%

7.6%

12.9%

23.9%

16.8%

12.2%

10.6%

6.2%

9.0%

4.5%

8.2%

0%

5%

10%

15%

20%

25%

30%

35%

40%

18

Source: Bloomberg GM UN Equity 11/18/2010 – 12/31/2011

Remember that $33 IPO Price?GM Looking Better

19

2.6%

-3.7%

-12.9%

-18.4%

7.7%

13.5%

4.9%

8.9%

-8.5%

8.4%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

S&P 500 Russell 2000

MSCI EAFE

MSCI EM BC Agg Bond

BC TIPS BC HY Bond

S&P REIT

CRB Index

Gold

YTD Asset Class Total Returns

Source: Bloomberg/FactSet; As of 12/31/2011

20

Source: Bloomberg SPX Index 12/31/10 – 12/31/2011

All This to End Up Unchanged?

21

Source: FactSet

PE And EPS Have Traded Places Since 1999

'92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '1120

30

40

50

60

70

80

90

100

110

120

8

10

12

14

16

18

20

22

24

26

28

PE Multiple

Trendline

Trendline

EPS

S&P 500 - Earnings per Share vs. PE Multiple

S&P 500 - Earnings per Share (Left)S&P 500 - Price to Earnings Ratio (Right)

Recession Periods - United StatesTrendline: Linear

Trendline: Linear

22

21.113.6

9.915.5

23.1

51.1

0x

10x

20x

30x

40x

50x

60x

60's 70's 80's 90's 00's Current

Average Bond “P/E” by Decade(100/10-Year Treasury Yield)

18.1

12.5 11.7

19.5 20.1

12.1

0x

5x

10x

15x

20x

25x

60's 70's 80's 90's 00's Current

Average S&P 500 Trailing “P/E”By Decade

29.716.0 10.6

20.0

49.6

100.0

0x

20x

40x

60x

80x

100x

'60's '70's '80's '90's '00's Current

Average Cash “P/E” by Decade(100/Fed Funds Rate)

What’s Cheap? Stocks, Bonds or Cash….

Source: Strategas

23

Source: Bianco Research

Treasury Constant Maturity 10 Year Yields

9/22/2011, 1.72%

12/18/2008, 2.08%

4/5/1946, 1.54%

9/30/1981, 15.84%

0%

2%

4%

6%

8%

10%

12%

14%

16%6

/2/1

94

1

5/2

9/1

94

3

6/1

/19

45

7/3

0/1

94

7

12

/22

/19

49

5/2

0/1

95

2

10

/13

/19

54

3/1

2/1

95

7

8/4

/19

59

1/2

/19

62

5/2

8/1

96

4

10

/21

/19

66

3/2

0/1

96

9

8/1

7/1

97

1

1/1

5/1

97

4

6/1

1/1

97

6

11

/8/1

97

8

4/8

/19

81

8/3

1/1

98

3

2/3

/19

86

6/2

7/1

98

8

11

/19

/19

90

4/1

5/1

99

3

9/7

/19

95

1/3

0/1

99

8

6/1

9/2

00

0

11

/8/2

00

2

2/2

5/2

00

5

6/1

5/2

00

7

10

/2/2

00

9

1/2

0/2

01

2

5/9

/20

14

0%

2%

4%

6%

8%

10%

12%

14%

16%

Last: Oct-11, 2011: 2.18%

How Low Can They Go?

24

'02 '03 '04 '05 '06 '07 '08 '09 '10 '11-6-6

-4-4

-2-2

00

22

44

66

88

2-year

5-year

10-year

30-year

©FactSet Research Systems

Real Treasury Yields

US Benchmark Bond - 2 Year - Yield - CPI-U All Items U.s. City Average SA 1982-84=100 - United States

US Benchmark Bond - 5 Year - Yield - CPI-U All Items U.s. City Average SA 1982-84=100 - United States

US Benchmark Bond - 10 Year - Yield - CPI-U All Items U.s. City Average SA 1982-84=100 - United States

US Benchmark Bond - 30 Year - Yield - CPI-U All Items U.s. City Average SA 1982-84=100 - United States

Recession Periods - United States

Financial Repression –How Long Can It Last?

25

4/10 7/10 10/10 1/11 4/11 7/11 10/11 1/12-2-2

00

22

44

66

88

1010

Money

Markets

10yr

Treasury

S&P 500

DJIA

LQD

HYG

Comparative Current Yields

US Benchmark Bond - 3 Month - Yield

DJ Industrial Average - Dividend Yield

iShares iBoxx $ InvesTop Investment Grade Bond Fund - Dividend Yield

iShares iBoxx $ High Yield Corporate Bond Fund - Dividend Yield

US Benchmark Bond - 10 Year - Yield

S&P 500 - Dividend Yield

Where Do I Go For Yield?

26

Source: Bloomberg MUB US Equity 12/31/2008 – 12/31/2011

Muni’s Bouncing Back - +12.98% in 2011

*Only 10 municipal defaults in 2011

Meredith Moment

27

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

PIT

Sales Tax

Total

Year –Over-Year Nominal Change in State Tax Collections

State Tax Collections Continue To Rebound

Source: Rockefeller Institute

28

Source: Bloomberg – CPI YOY Index 12/31/71 – 12/31/2011

Flight to Quality

Back to Reality?

Flight to Quality

Back to Reality?Flight to

Quality

CPI – Inflation Creeping Back

29

TIPS A Better Hedge Than Hedge Funds?

30

Putting the Federal Budget in Perspective

U.S. Federal Government Example Using Median U.S. Household Income

Example Using Hypothetical Household Income of $100,000

Annual Income $2,228,000,000,000¹ $49,777³ $100,000

Annual Spending $3,708,000,000,000¹ $82,8434 $166,4274

Annual Deficit $1,480,000,000,000¹ $33,066 $66,427

Total Debt $14,993,709,044,141² $334,9834 $672,9674

¹Estimates for 2011 from the Congressional Budget Office’s ‘Budget and Economic Outlook: Fiscal Years 2011 to 2021,’ Table 1-1.

²Total public debt outstanding as of 10/31/2011 as reported by Treasurydirect.gov, ‘The Debt to the Penny and Who Holds It.’

³Median household income in the U.S. as of 2009 as reported by the U.S. Census Bureau, ‘The 2012 Statistical Abstract,’ Table 690.

4Calculations based on percentage of ‘Annual Income’ in proportion to that of ‘U.S. Federal Government’ figures.

What personal finances of typical U.S. households would look like if they mirrored the finances of the U.S. Federal Government

31

Fifth Third Asset Management, Inc. is an investment adviser registered under the Investment Advisers Act of 1940. Theinformation presented in the material is general in nature and is not designed to address your investment objectives, financialsituation or particular needs. Prior to making any investment decision, you should assess, or seek advice from a professionalregarding whether any particular transaction is relevant or appropriate to your individual circumstances. Although taken fromreliable sources, FTAM cannot guarantee the accuracy of the information received from third parties. Graphs and charts, bythemselves, cannot be used to make investment decisions.

The opinions expressed herein are those of FTAM and may not actually come to pass. This information is current as of the date ofthis newsletter and is subject to change at any time, based on market and other conditions.

Disclosures

FTAM January, 2011