Embed Size (px)

Citation preview

Report of Programme Committee D

TRIENNIUM 2003 – 2006

Chairperson Chawki Mohamed Rahal

Algeria

LIQUEFIED NATURAL GAS

June 2006

ABSTRACT This report details the work undertaken by Programme Committee D during the triennium 2003–2006. This report of Programme Committee D consists of three parts. The first describes the results achieved by the Committee Management with respect to the objectives assigned as part of the Triennial Work Program adopted in 2003. The second part consists of the detailed report prepared by the Vice Chairman of the Committee which gives the situation of the LNG industry worldwide in 2004. The third part describes the results achieved by the three Study Groups which have constituted the core of the activities of the Committee. The subjects relating to LNG are as follows: • LNG Quality • Safety and Technology Developments in LNG Terminals and Vessels • The future of the LNG spot market. These reports have been the result of intense activities of PGC D members which were joined by a number of invited experts who accepted to participate in these studies. These themes which show that the LNG industry as a whole is experiencing unprecedented vitality and growth will be presented during the World Gas Conference at the PGC D Committee Sessions and Expert forums together with the contribution of a large number of authors. The approved Triennial Work Program, the membership of Programme Committee D and the meeting schedule of its members are listed in Annex 1, Annex 2 and Annex 3 respectively.

RESUME Ce rapport contient le détail des travaux entrepris par le Comité Programme D durant le triennat 2003-2006. Ce rapport du Comité Programme D comprend trois parties. La première partie décrit les résultats accomplis par le Comité Management en ce qui concerne les objectifs qui lui ont été assignés dans le cadre du Programme Triennal de Travail adopté en 2003. La deuxième partie comporte le rapport détaillé préparé par le Vice Président du Comité donnant la situation de l’industrie mondiale du GNL en 2004. La troisième partie décrit les résultats accomplis par les trois Groupes d’Etude au centre des activités du Comité. Les sujets ayant trait au GNL sont comme suit : Qualité du GNL Sécurité et Développements Technologiques dans les Terminaux et Navires

Méthaniers Le futur du marché Spot du GNL

Ces rapports sont le résultat des activités intenses des membres du PGC D auxquels se sont joints sur invitation un certain nombre d’experts qui ont accepté de participer à ces études. Ces thèmes, qui montrent que l’industrie du GNL dans son ensemble fait preuve d’une vitalité et d’une croissance sans précédents, seront présentés, en même temps que les contributions de nombreux auteurs, durant le World Gas Conférence aux Sessions du Comité PGC D et aux Forums d’Experts. Le Programme Triennal de Travail, la liste des Membres du Comité PGC D et le calendrier de réunion de ses Membres se trouvent respectivement en Annexe1, Annexe 2 et Annexe 3.

TABLE OF CONTENTS

Abstract

1. THE ACTIVITIES OF PROGRAMME COMMITTEE D DURING THE TRIENNIUM 2003-2006

2. THE WORLDWIDE LNG INDUSTRY AT THE END OF 2004

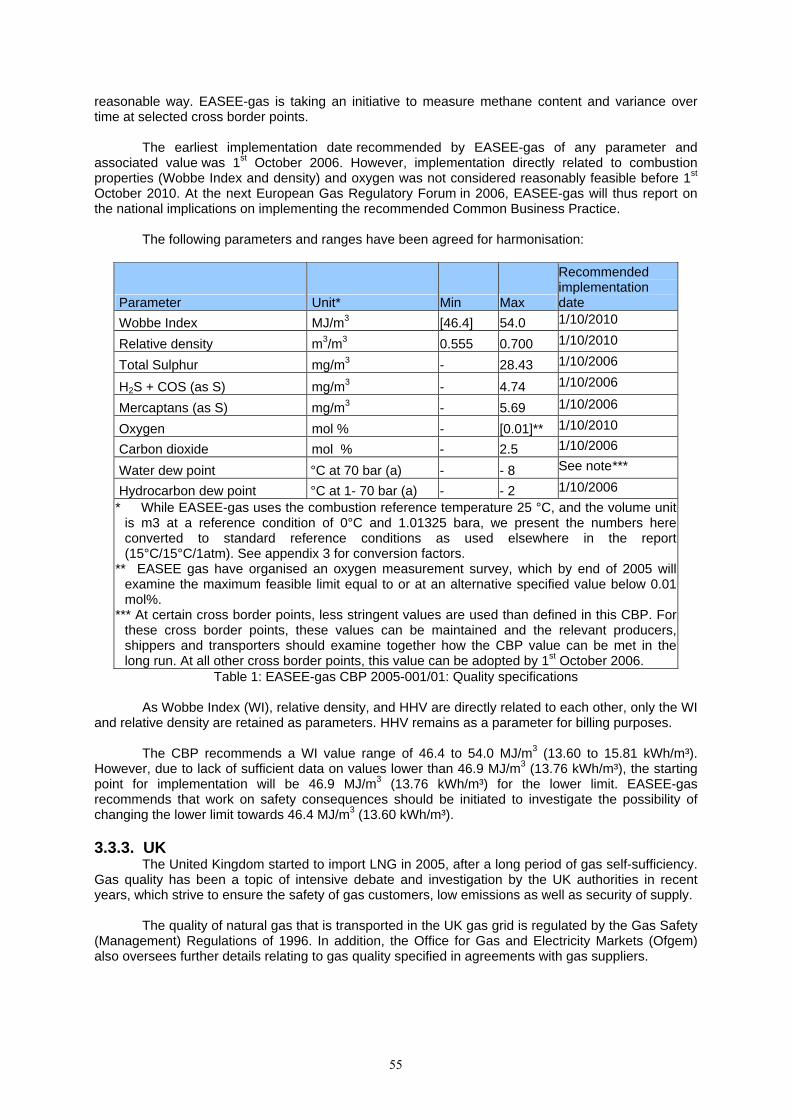

3. REPORT OF STUDY GROUP D1: “LNG QUALITY”

4. REPORT OF STUDY GROUP D2: “SAFETY AND TECHNOLOGY

DEVELOPMENTS IN LNG TERMINALS AND VESSELS”

5. REPORT OF STUDY GROUP D3: “THE FUTURE OF THE LNG SPOT MARKET”

6. ACKNOWLEDGEMENTS

Appendix A: Triennial Work Program of PGCD Appendix B: Membership of the PGCD and Study Groups Appendix C: Committee Meetings.

5

1. THE ACTIVITIES OF PROGRAMME COMMITTEE D DURING THE

TRIENNIUM 2003-2006

Programme Committee D has had a very dynamic and active triennium at a time where LNG is experiencing much renewed interest in the world and this will be an ongoing trend for the coming years as natural gas is more and more appreciated for its environment friendly quality. PGC D will, as part of its activities in this triennium has set itself the following objectives:

- Monitor the LNG industry, - Attract old and new actors to participate or take an active role in the IGU activities, - Rationalise the LNG activities of IGU in cooperation with the other international LNG

organisations, - Monitor and support when necessary the activities of the Working Committees 1-5 as well as

those of the other Programme Committees by providing the necessary expertise in the field of LNG,

- Organise workshops and/or participate at conferences, - PGC D will also perform, during this triennium, studies on LNG topics of interest to IGU

Members. Experts should be invited to participate to PGC D activities particularly for the Study Groups.

1.1. MONITOR THE LNG INDUSTRY Traditionally, the Committee in charge of LNG in the IGU produces a report that reports the trend experienced by the LNG industry during the triennium. This document is a very rich and complete database for the LNG industry worldwide. It is a task generally assigned to the Vice Chairman of the Committee and this document is a compilation of data from various sources validated by the members of the Committee which represent a large part of the Industry. This complete report, the LNG Industry worldwide in 2004 follows this chapter and will be presented at the World gas Conference where a update of the data till the end of 2005 will be provided. 1.2. ATTRACT OLD AND NEW ACTORS OF THE LNG INDUSTRY It has been felt by Committee members that an attempt should be made to attract the maximum number of representatives of countries and associated members affiliated to the IGU which are involved in one way or another with the LNG industry.

In order to achieve this objective, the Committee Management has been in contact with the national associations of countries which are already involved in LNG activities. As such the following countries have been approached: Brunei, Egypt, India, Indonesia, Libya, Malaysia, Nigeria, Oman, Portugal, People’s Republic of China, Qatar, Republic of China Taiwan, Trinidad and Tobago, Turkey, and United Arab Emirates. This contact has resulted over the triennium in the nomination of Members from Indonesia, Malaysia, People’s Republic of China, Qatar, Republic of China Taiwan and United Arab Emirates.

It is suggested that the Management of the IGU as well as the management of PGC D continues this effort of attempting to attract members from these countries as they already play a role in LNG.

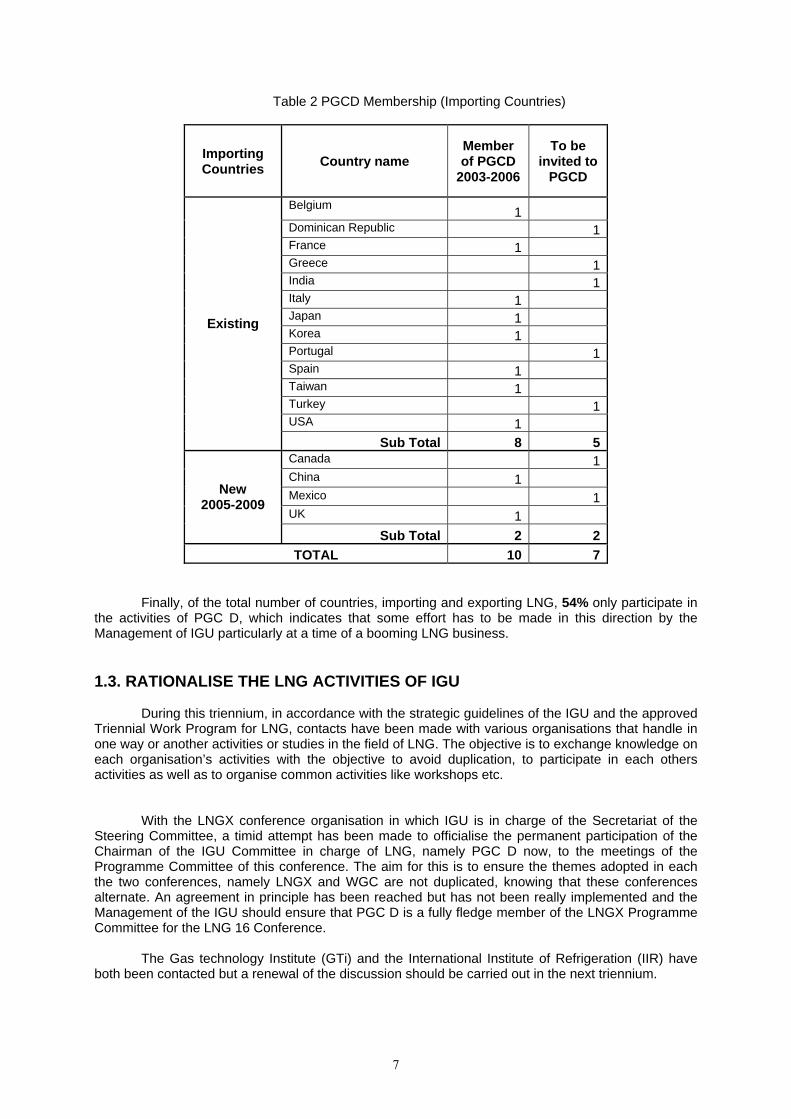

Overall, it can be said that during the triennium 2003-2006, seven (7) LNG existing Exporting out of a total of twelve (12) and three (3) future Exporting countries during the next triennium out of eight (8) indicating a representing 50% of the potential of Exporters. Table 1 below give the detailed status of the LNG Exporting countries at the end of triennium 2003-2006 as well as the perspectives for triennium 2006-2009.

6

Table 1 PGCD Membership (Exporting Countries)

Exporting Countries Country name

Member of PGCD

2003-2006

To be invited to

PGCD Algeria 1 Australia 1 Brunei 1 Indonesia 1 Libya 1 Malaysia 1 Nigeria 1 Oman 1 Qatar 1 Trinidad and Tobago 1 United Arab Emirates 1 USA 1

Existing

Sub Total 7 5 Angola 1 Egypt 1 Equatorial Guinea 1 Iran 1 Norway 1 Peru 1 Russia 1 Yemen 1

New 2005-2009

Sub Total 3 5 TOTAL 10 10

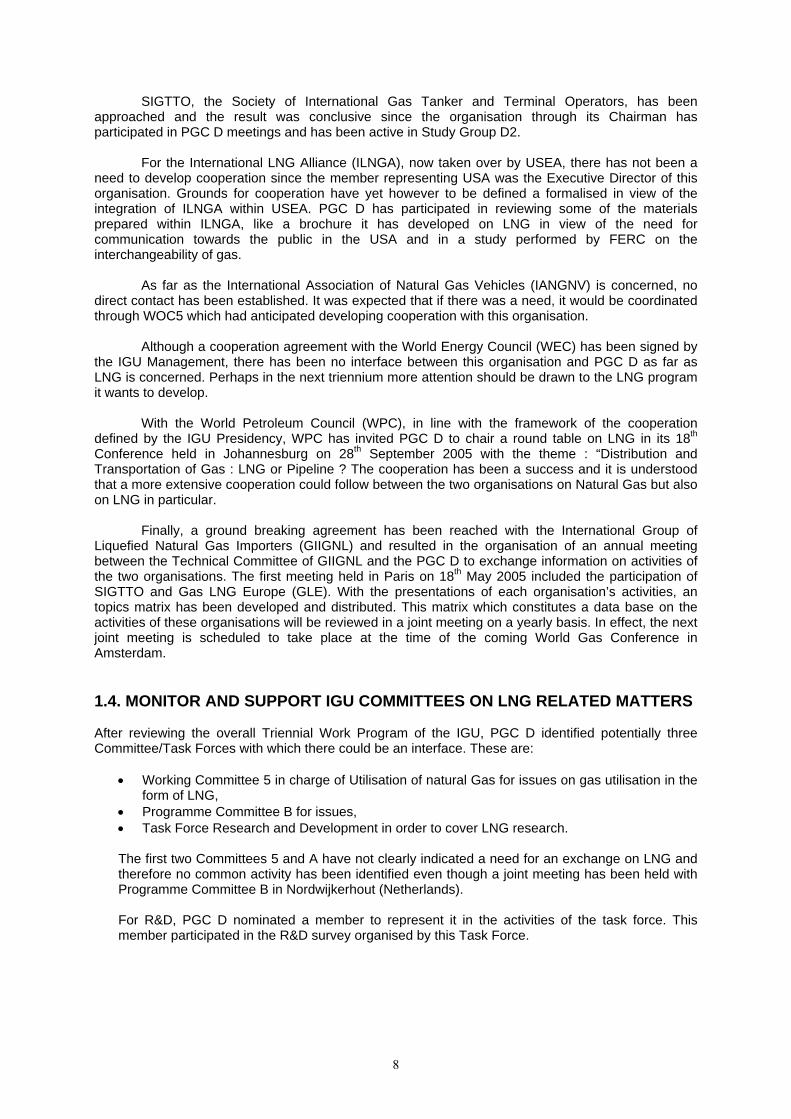

Eight (8) out of thirteen (13) existing LNG importing countries and two (2) out of (4) future

importers during the coming triennium participate in the PGC D activities representing 59 %of the potential of importers. Table 2 below give the detailed status of the LNG Importing countries at the end of triennium 2003-2006 as well as the perspectives for triennium 2006-2009.

7

Table 2 PGCD Membership (Importing Countries)

Importing Countries Country name

Member of PGCD

2003-2006

To be invited to

PGCD

Belgium 1 Dominican Republic 1 France 1 Greece 1 India 1 Italy 1 Japan 1 Korea 1 Portugal 1 Spain 1 Taiwan 1 Turkey 1 USA 1

Existing

Sub Total 8 5 Canada 1 China 1 Mexico 1 UK 1

New 2005-2009

Sub Total 2 2 TOTAL 10 7

Finally, of the total number of countries, importing and exporting LNG, 54% only participate in

the activities of PGC D, which indicates that some effort has to be made in this direction by the Management of IGU particularly at a time of a booming LNG business.

1.3. RATIONALISE THE LNG ACTIVITIES OF IGU

During this triennium, in accordance with the strategic guidelines of the IGU and the approved Triennial Work Program for LNG, contacts have been made with various organisations that handle in one way or another activities or studies in the field of LNG. The objective is to exchange knowledge on each organisation’s activities with the objective to avoid duplication, to participate in each others activities as well as to organise common activities like workshops etc.

With the LNGX conference organisation in which IGU is in charge of the Secretariat of the Steering Committee, a timid attempt has been made to officialise the permanent participation of the Chairman of the IGU Committee in charge of LNG, namely PGC D now, to the meetings of the Programme Committee of this conference. The aim for this is to ensure the themes adopted in each the two conferences, namely LNGX and WGC are not duplicated, knowing that these conferences alternate. An agreement in principle has been reached but has not been really implemented and the Management of the IGU should ensure that PGC D is a fully fledge member of the LNGX Programme Committee for the LNG 16 Conference.

The Gas technology Institute (GTi) and the International Institute of Refrigeration (IIR) have both been contacted but a renewal of the discussion should be carried out in the next triennium.

8

SIGTTO, the Society of International Gas Tanker and Terminal Operators, has been approached and the result was conclusive since the organisation through its Chairman has participated in PGC D meetings and has been active in Study Group D2.

For the International LNG Alliance (ILNGA), now taken over by USEA, there has not been a need to develop cooperation since the member representing USA was the Executive Director of this organisation. Grounds for cooperation have yet however to be defined a formalised in view of the integration of ILNGA within USEA. PGC D has participated in reviewing some of the materials prepared within ILNGA, like a brochure it has developed on LNG in view of the need for communication towards the public in the USA and in a study performed by FERC on the interchangeability of gas.

As far as the International Association of Natural Gas Vehicles (IANGNV) is concerned, no direct contact has been established. It was expected that if there was a need, it would be coordinated through WOC5 which had anticipated developing cooperation with this organisation.

Although a cooperation agreement with the World Energy Council (WEC) has been signed by the IGU Management, there has been no interface between this organisation and PGC D as far as LNG is concerned. Perhaps in the next triennium more attention should be drawn to the LNG program it wants to develop.

With the World Petroleum Council (WPC), in line with the framework of the cooperation defined by the IGU Presidency, WPC has invited PGC D to chair a round table on LNG in its 18th Conference held in Johannesburg on 28th September 2005 with the theme : “Distribution and Transportation of Gas : LNG or Pipeline ? The cooperation has been a success and it is understood that a more extensive cooperation could follow between the two organisations on Natural Gas but also on LNG in particular.

Finally, a ground breaking agreement has been reached with the International Group of Liquefied Natural Gas Importers (GIIGNL) and resulted in the organisation of an annual meeting between the Technical Committee of GIIGNL and the PGC D to exchange information on activities of the two organisations. The first meeting held in Paris on 18th May 2005 included the participation of SIGTTO and Gas LNG Europe (GLE). With the presentations of each organisation’s activities, an topics matrix has been developed and distributed. This matrix which constitutes a data base on the activities of these organisations will be reviewed in a joint meeting on a yearly basis. In effect, the next joint meeting is scheduled to take place at the time of the coming World Gas Conference in Amsterdam. 1.4. MONITOR AND SUPPORT IGU COMMITTEES ON LNG RELATED MATTERS After reviewing the overall Triennial Work Program of the IGU, PGC D identified potentially three Committee/Task Forces with which there could be an interface. These are:

• Working Committee 5 in charge of Utilisation of natural Gas for issues on gas utilisation in the form of LNG,

• Programme Committee B for issues, • Task Force Research and Development in order to cover LNG research.

The first two Committees 5 and A have not clearly indicated a need for an exchange on LNG and therefore no common activity has been identified even though a joint meeting has been held with Programme Committee B in Nordwijkerhout (Netherlands). For R&D, PGC D nominated a member to represent it in the activities of the task force. This member participated in the R&D survey organised by this Task Force.

9

1.5. ORGANISE WORKSHOPS AND/OR PARTICIPATE AT CONFERENCES During this triennium, various communications have been done by Members of PGC D in various Conferences. The following papers have been presented:

• Panel 8 - 4th LAGCEC – Rio de Janeiro 28th April 2004 : “The new rise of LNG” , Dr. C.M. RAHAL

• LNG & GTL: World-wide and Russian prospects - Moscow 26 May 2004: “vvvv”, Dr M. Taleb

• IGRC 2004 - Vancouver - 1-4 November 2004: "Gas technology in realising a sustainable energy future", Mr. Rob NAGELVOORT.

• FLAME 2005 – Amsterdam – xx February 2005: "Assessing the Impact of Gas Quality on the

LNG market ", Rob KLEIN NAGELVOORT.

10

6. THE LNG INDUSTRY WORLD WIDE AT THE END OF 2004

PGC D LNG SURVEY

“The world-wide LNG industry at the end of 2004”

Vice Chairman/Vice Président

Seiichi UCHINO

Japan

11

ABSTRACT

As is customary for the Committee in charge of LNG within the International Gas Union, presently named Program Committee D, a report has been prepared during each triennium to show the evolution of the LNG industry as a whole during the triennium 2003-2006.

The Vice Chairman of the Committee, held by Japan for triennium 2003 - 2006, customarily has been engaged in the preparation of this report.

This report, based on various related data from different sources, referenced in the report, provides information and trends of the world LNG industry. It covers all segments of the LNG chain namely LNG plants, LNG carriers and LNG receiving terminals in terms of capacity and number of units, type of processes or technology as well the import export trade statistics for the period 2001-2004.

The presentation of this report at the 23rd World Gas Conference in Amsterdam will include an update of the data contained in this report for the year 2005.

Résumé

Comme il est de coutume pour le Comité ayant la charge du GNL au sein de l’Union Internationale de l’Industrie du Gaz, dénommé « Program Committee D », un rapport est préparé pendant chaque triennat pour montrer l’évolution de l’industrie du GNL d’une façon générale pendant le triennat 2003-2006.

Il revient comme de coutume, au Vice Président du Comité, position tenue par le Japon pour 2003-2006, de préparer ce rapport.

Ce rapport, basé sur une variété de données provenant de différentes sources référencées dans le rapport, procure des informations pertinentes et des tendances de l’‘industrie mondiale du GNL. Ce rapport couvre tous les segments de la chaine GNL, en particulier les unités de liquéfaction, les navires de transport ainsi que les terminaux de réception, ceci en termes de capacité, et nombre d’unités, de type de procédés ou de technologie utilisés. Il comporte aussi les statistiques du commerce import/export pour la période 2001-2004.

La présentation de ce rapport au 23ème Congrès Mondial du Gaz à Amsterdam comprendra une mise à jour des données contenues dans ce rapport pour l’année 2005.

12

TABLE OF CONTENTS

2.1. Foreword 2.2. Key Facts 2.3. Amount of LNG Import and Export

Overview LNG trade volume Amount of export by country Amount of import by country Interregional import and export volume by region Spot market

2.4. LNG Liquefaction plants Overview Liquefaction capacity Liquefaction capacity by region Liquefaction capacity by country Liquefaction train capacity Liquefaction process Newly initiated plants and trains Terminals and trains under construction or in planning

2.5. LNG Receiving Terminals Overview Number of receiving terminals by country Number of receiving terminals by region Number of receiving terminals by year of start-up LNG storage capacity Maximum capacity of LNG carriers able to berth Gas sendout capacity Newly initiated terminals Terminals under construction or in planning

2.6. LNG Carriers Overview Capacity Number of commissions Tank type

2.7. Conclusion 2.8. References

13

2.1. FOREWORD More than 40 years have passed since the first commercial export of LNG in the world. Utilization

of LNG has been rapidly spreading in recent years owing to the growing energy needs of the world. The growth of the LNG traded volumes is the highest of all fuels thanks to the environment-friendly characteristics of natural gas and the transportability of LNG.

Compiled from various data, this report presents in one document the status of the LNG industry in 2004 in all its segments, LNG liquefaction plants, receiving terminals, LNG and LNG carriers as well as provides import and export statistics to attest of the growing importance of this form of energy.

The LNG committee of the IGU has traditionally prepared this report, and the one for the preceding term (2000 - 2003) profiled the LNG industry as of 2001. This latest edition, in addition to the status of the industry in 2004, includes comparisons with 2001. Finally, the report would not be complete without some comments on the outlook for LNG liquefaction and receiving terminals and LNG carriers.

2.2. KEY FACTS

The key facts for the LNG industry over the years 2001 - 2004 were as follows. 1) The volume of LNG trade reached 142.4 million tons and increased 35 million tons, or 33%,

from 2001. 2) The share of spot trade in LNG has been increasing substantially in recent years to reach

19% of total LNG trade volumes in 2004. 3) The world LNG liquefaction capacity totaled 139.5 million tons per year in 2004 and

increased 18.1 million tons since 2001. 4) The number of liquefaction trains in operation numbered 73 in 12 countries. 5) The number of LNG receiving terminals in operation around the world reached 47. These

terminals were located in 13 countries on three continents. 6) 174 LNG carriers were in operation. The combined capacity of these ships is 20.72 million

cubic meters, which has increased by 6.45 million cubic meters, or 45%, from 2001, for an average of 119,000 cubic meters per carrier.

2.3. AMOUNT OF LNG IMPORT AND EXPORT Overview

In 2004, the volume of LNG trade reached 142.4 million tons. Countries exporting LNG numbered 12, the same as in 2001 (i.e., Algeria, Libya, Nigeria, United

States, Trinidad and Tobago, Australia, Brunei, Indonesia, Malaysia, United Arab Emirates, Oman, and Qatar). Over the same period, the number of countries importing LNG increased by three (Portugal, India, and Dominican Republic) to 13 (the other ten being Japan, South Korea, Taiwan, United States, Italy, Spain, Belgium, France, Turkey, and Greece).

LNG trade volume Figure 1 shows the trend of the LNG trade volume over the years 1984 - 2004. Over the years

2001 - 2004, liquefaction capacity increased substantially due to the construction of new, and expansion of existing, plants and trains. As a result, the 2004 LNG trade volume represented a hefty increase of 35 million tons, or 33%, from 2001. The LNG trade volume is expected to continue to increase rapidly, in light of the many plans for addition and expansion of liquefaction plants, trains, and receiving terminals.

14

020406080

100120140160

1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Year

Trad

e Q

uant

ityMTPY

Fig.1 LNG Trade Quantity from 1984 to 2004

Source: "BP Statistical Review of World Energy June 2005"

Amount of export by country The amount of LNG export by each country is shown below.

Table 1 LNG Export per Country in 2004 Country Amount MTPY

Indonesia 26.8 Malaysia 22.1 Algeria 20.6 Qatar 19.3

Trinidad and Tobago 11.2 Nigeria 10.1

Australia 9.7 Brunei 7.6 Oman 7.2

United Arab Emirates 5.9 USA 1.3 Libya 0.5

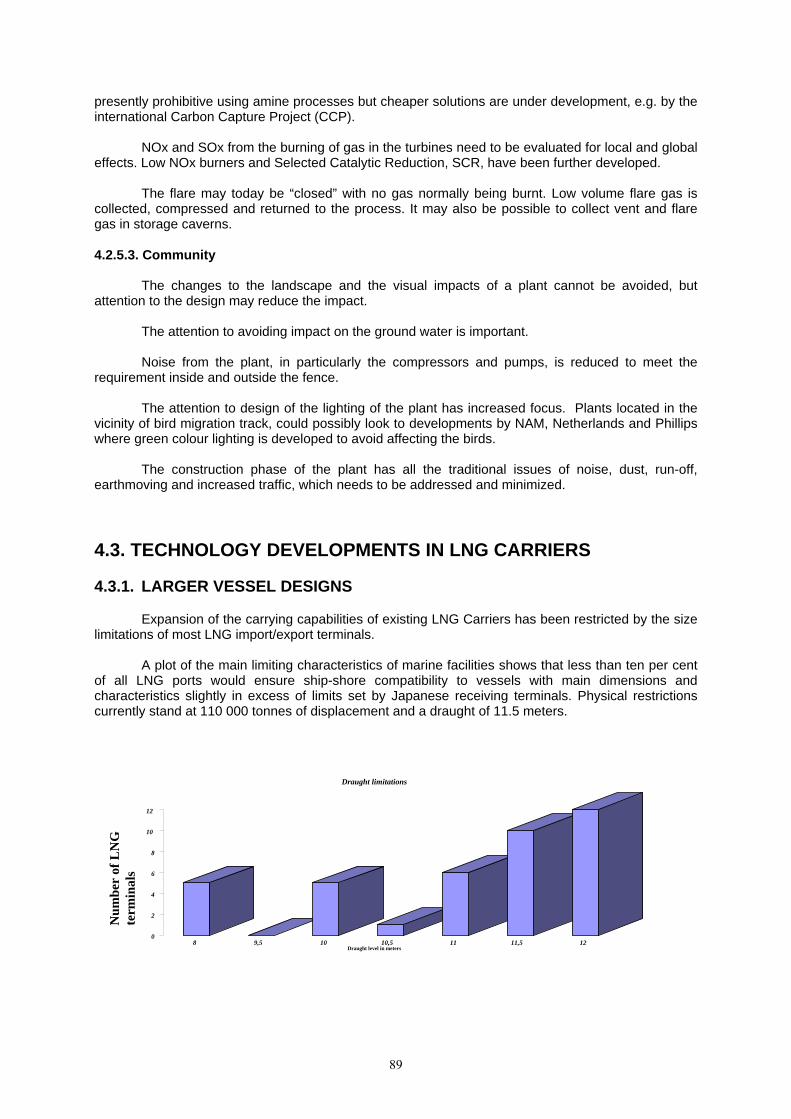

Source: "BP Statistical Review of World Energy June 2005" Figure 2 indicates the share breakdown of the 2004 LNG export amount by country, and Figure 3,

4 comparisons with 2001. Indonesia is still the largest exporter, accounting for some 27 million tons or 19% of the total in 2004. The share breakdown of the total LNG export by country remains the same relative to the total liquefaction capacity, however slight variations are observed due to respective operation rate of the liquefaction plants.

15

Nigeria7.1%

Libya0.4%

USA0.9%

TrinidadTobago7.9%

Australia6.8%

Brunei5.3%

Oman5.1%

UAE4.1%

Algeria14.5%

Indonesia18.8%

Malaysia15.6%

Qatar13.5%

Fig.2 LNG Exports per Country in 2004

Source: "BP Statistical Review of World Energy June 2005"

As compared to 2001, the amount of export exhibited increases in the case of Malaysia, Qatar,

Nigeria, and Trinidad and Tobago, where trains have been expanded. Partly because of the increase in the overall export volume, there is a decline in the shares of Indonesia and Algeria, the two largest exporters.

0

5

10

15

20

25

30MTPY

Algeria Nigeria Libye USA TrinidadTobago

Australia Brunei Malaisia Indonesia Oman UAE Qatar

2001

2004

Fig.3 LNG Exports per Country in 2001 and 2004

Source: "BP Statistical Review of World Energy June 2005"

0

5

10

15

20

25

30(%)

Algeria Nigeria Libye USA TrinidadTobago

Australia Brunei Malaisia Indonesia Oman UAE Qatar

2001

2004

Fig.4 LNG Exports per Country in 2001 and 2004 Source: "BP Statistical Review of World Energy June 2005"

16

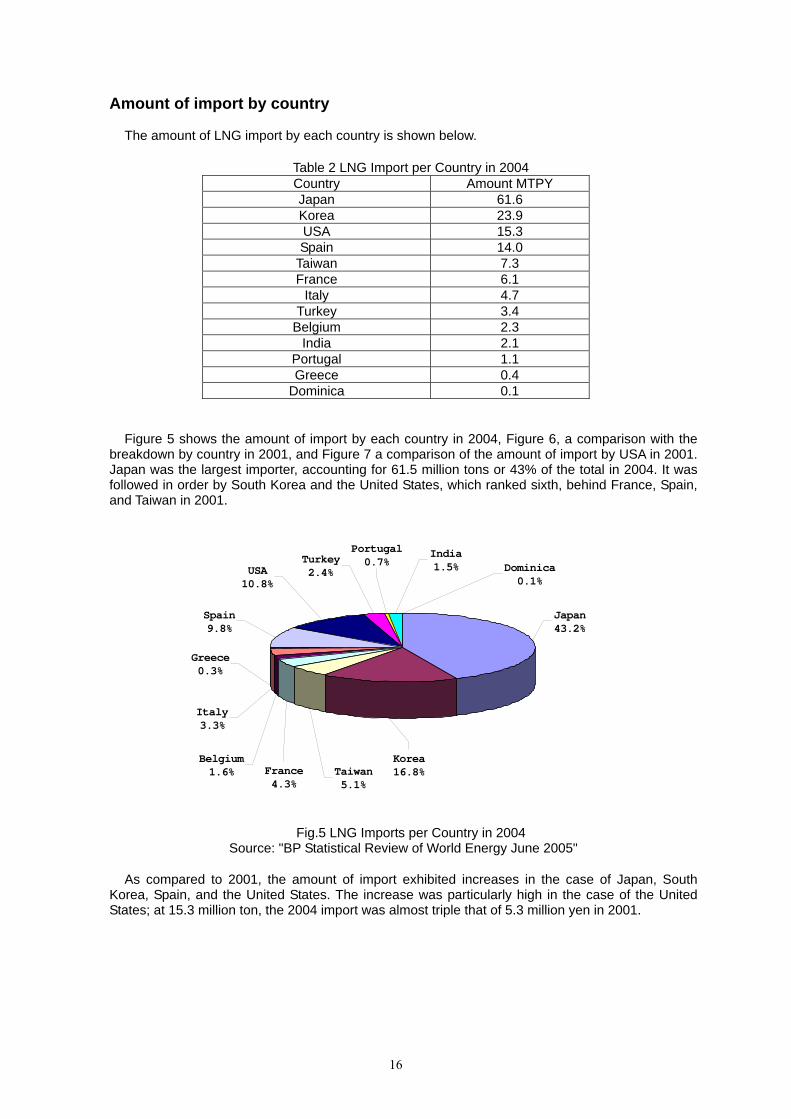

Amount of import by country The amount of LNG import by each country is shown below.

Table 2 LNG Import per Country in 2004 Country Amount MTPY Japan 61.6 Korea 23.9 USA 15.3 Spain 14.0

Taiwan 7.3 France 6.1

Italy 4.7 Turkey 3.4

Belgium 2.3 India 2.1

Portugal 1.1 Greece 0.4

Dominica 0.1

Figure 5 shows the amount of import by each country in 2004, Figure 6, a comparison with the

breakdown by country in 2001, and Figure 7 a comparison of the amount of import by USA in 2001. Japan was the largest importer, accounting for 61.5 million tons or 43% of the total in 2004. It was followed in order by South Korea and the United States, which ranked sixth, behind France, Spain, and Taiwan in 2001.

Japan43.2%

USA10.8%

Spain9.8%

India1.5%

Korea16.8%

Dominica0.1%

Taiwan5.1%

Italy3.3%

France4.3%

Belgium1.6%

Greece0.3%

Portugal0.7%Turkey

2.4%

Fig.5 LNG Imports per Country in 2004 Source: "BP Statistical Review of World Energy June 2005"

As compared to 2001, the amount of import exhibited increases in the case of Japan, South

Korea, Spain, and the United States. The increase was particularly high in the case of the United States; at 15.3 million ton, the 2004 import was almost triple that of 5.3 million yen in 2001.

17

0

10

20

30

40

50

60

70MTPY

Japan Korea Taiwan France Belgium Italy Greece Spain USA Turkey Portugal India Dominica

2001

2004

Fig. 6 LNG Imports per Country in 2001 and 2004 Source: "BP Statistical Review of World Energy June 2005"

0

5

10

15

20MTPY

USA

2001

2004

Fig. 7 LNG Imports to USA Source: "BP Statistical Review of World Energy June 2005"

As for the share breakdown by country, there were declines in the share occupied by Japan, the

biggest importer, and France. Whereas the import by France declined in absolute terms, the decline in Japan's share came in spite of an increase in its import, partly because of a significant expansion in the total import.

18

0

10

20

30

40

50

60

(%)

Japan Korea Taiwan France Belgium Italy Greece Spain USA Turkey Portugal India Dominica

2001

2004

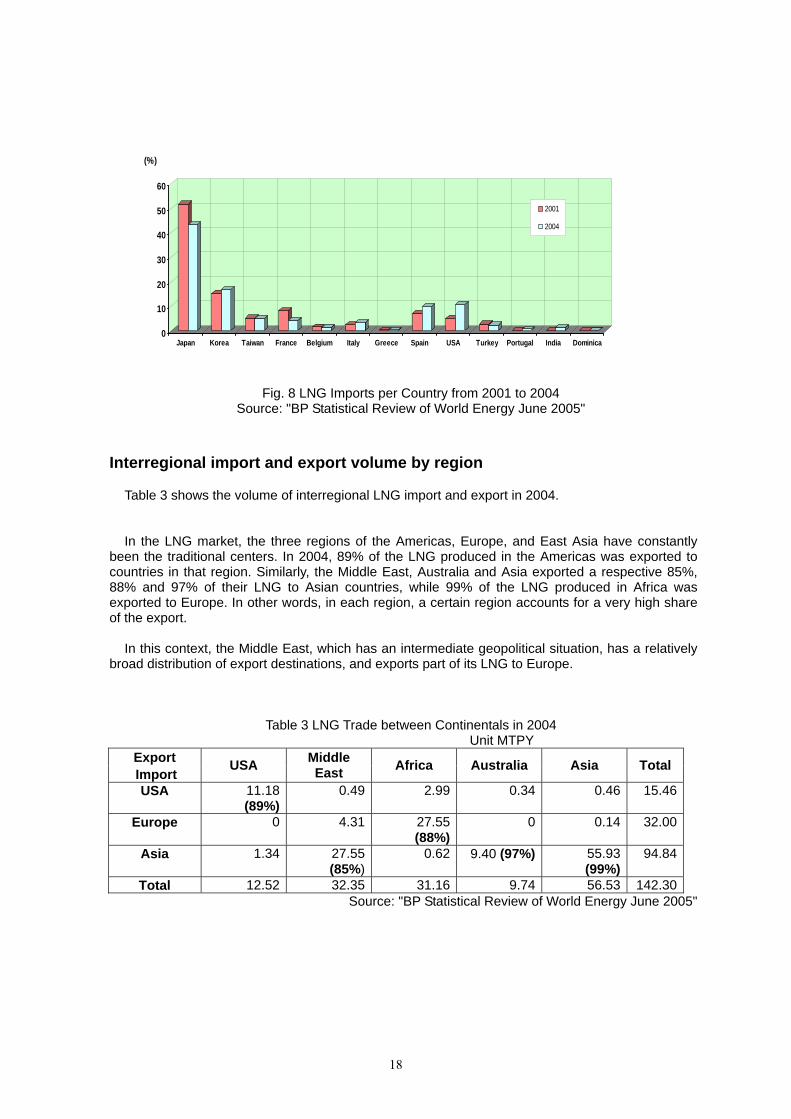

Fig. 8 LNG Imports per Country from 2001 to 2004 Source: "BP Statistical Review of World Energy June 2005"

Interregional import and export volume by region Table 3 shows the volume of interregional LNG import and export in 2004. In the LNG market, the three regions of the Americas, Europe, and East Asia have constantly

been the traditional centers. In 2004, 89% of the LNG produced in the Americas was exported to countries in that region. Similarly, the Middle East, Australia and Asia exported a respective 85%, 88% and 97% of their LNG to Asian countries, while 99% of the LNG produced in Africa was exported to Europe. In other words, in each region, a certain region accounts for a very high share of the export.

In this context, the Middle East, which has an intermediate geopolitical situation, has a relatively

broad distribution of export destinations, and exports part of its LNG to Europe.

Table 3 LNG Trade between Continentals in 2004 Unit MTPY

Export Import

USA Middle East Africa Australia Asia Total

USA 11.18 (89%)

0.49 2.99 0.34 0.46 15.46

Europe 0 4.31 27.55 (88%)

0 0.14 32.00

Asia 1.34 27.55 (85%)

0.62 9.40 (97%) 55.93 (99%)

94.84

Total 12.52 32.35 31.16 9.74 56.53 142.30Source: "BP Statistical Review of World Energy June 2005"

19

Tables 4, 5, and 6 present detailed figures for LNG trade volume in 2002, 2003, and 2004.

Table 4 LNG Trade Quantity in 2002 Unit MTPY

Export

Import USA Trinida

d Oman Qatar UAE Algeria Libya Nigeri

a Australia

Brunei

Indonesia

Malaysia Total

USA 3.42 0.07 0.79 0.60 0.18 0.06 0.06 5.18Puerto Rico 0.46 0.04 0.50

Dominica 0.00Belgium 0.08 2.56 2.64France 0.43 8.16 0.64 9.23Greece 0.40 0.40

Italia 1.76 2.80 4.56Portugal 0.34 0.34

Spain 0.37 0.61 1.76 0.40 4.76 0.50 1.29 0.06 0.06 9.81Turkey 3.26 1.02 4.28India

Japan 1.36 0.87 6.72 4.74 7.78 6.36 18.72

11.60

58.15

Korea 4.38 5.56 0.26 0.19 0.83 5.42 2.48 19.13

Taiwan 3.32 2.28 5.60Total 1.36 4.26 6.37 14.8

7 5.48 21.50 0.50 6.27 8.02 7.31 27.4

6 16.4

2119.

83Source: "BP Statistical Review of World Energy June 2005"

Table 5 LNG Trade Quantity in 2003

Unit MTPY Export

Import USA Trinid

ad Oma

n Qatar UAE Algeria Libya Nigeri

a Australia

Brunei

Indonesia

Malaysia Total

USA 8.57 0.19 0.31 1.21 1.14 0.06 11.48Puerto Rico 0.24 0.24

Dominica 0.59 0.59Belgium 2.52 2.52France 7.36 0.54 7.90Greece 0.44 0.44

Italia 1.62 2.80 4.42Portugal 0.68 0.68

Spain 0.06 0.26 1.50 0.19 5.98 0.60 3.38 0.06 12.03Turkey 3.09 0.90 3.99India 0

Japan 1.31 0.06 1.73 7.24 5.50 8.22 7.14 19.24 13.38 63.82Korea 5.19 6.30 0.18 0.14 0.59 5.54 3.03 20.98Taiwan 3.74 2.24 5.98Total 1.31 9.53 7.37 15.35 5.69 22.40 0.60 9.43 8.42 7.74 28.53 18.71 135.07

Source: "BP Statistical Review of World Energy June 2005"

20

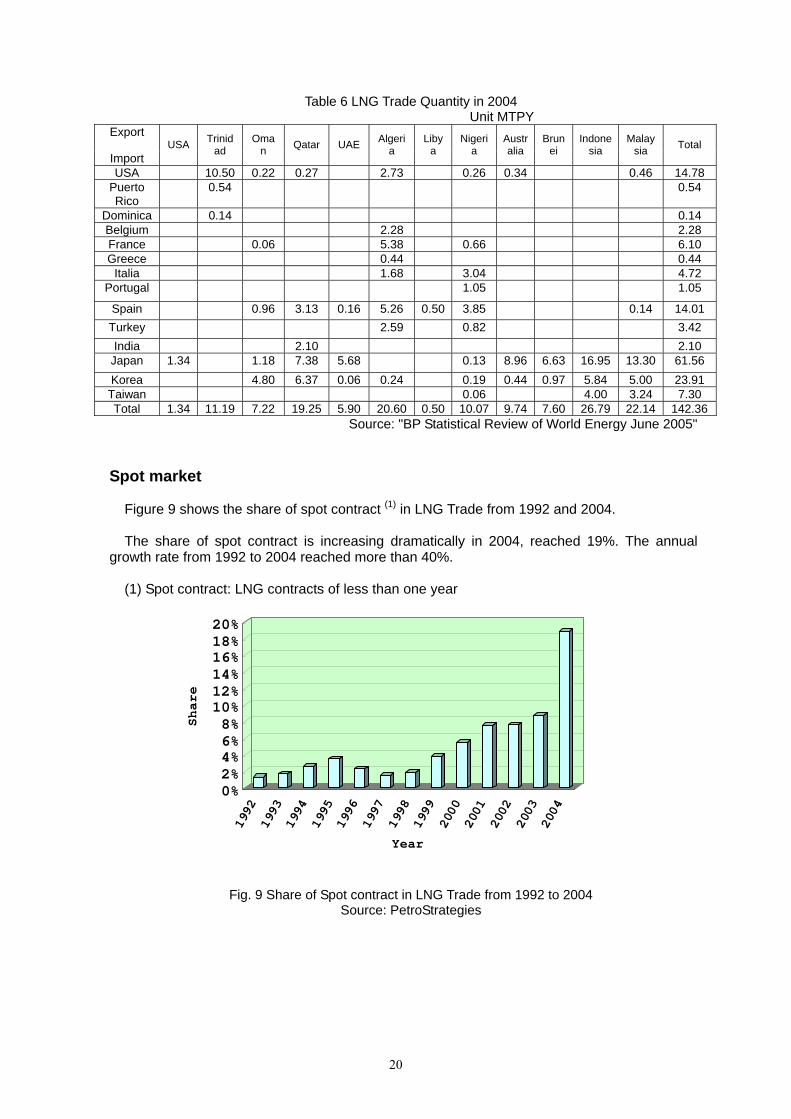

Table 6 LNG Trade Quantity in 2004 Unit MTPY

Export

Import USA Trinid

ad Oma

n Qatar UAE Algeria

Libya

Nigeria

Australia

Brunei

Indonesia

Malaysia Total

USA 10.50 0.22 0.27 2.73 0.26 0.34 0.46 14.78 Puerto Rico

0.54 0.54

Dominica 0.14 0.14 Belgium 2.28 2.28 France 0.06 5.38 0.66 6.10 Greece 0.44 0.44

Italia 1.68 3.04 4.72 Portugal 1.05 1.05

Spain 0.96 3.13 0.16 5.26 0.50 3.85 0.14 14.01 Turkey 2.59 0.82 3.42 India 2.10 2.10

Japan 1.34 1.18 7.38 5.68 0.13 8.96 6.63 16.95 13.30 61.56 Korea 4.80 6.37 0.06 0.24 0.19 0.44 0.97 5.84 5.00 23.91 Taiwan 0.06 4.00 3.24 7.30 Total 1.34 11.19 7.22 19.25 5.90 20.60 0.50 10.07 9.74 7.60 26.79 22.14 142.36

Source: "BP Statistical Review of World Energy June 2005"

Spot market

Figure 9 shows the share of spot contract (1) in LNG Trade from 1992 and 2004. The share of spot contract is increasing dramatically in 2004, reached 19%. The annual

growth rate from 1992 to 2004 reached more than 40%. (1) Spot contract: LNG contracts of less than one year

0%2%4%6%8%10%12%14%16%18%20%

Share

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

Year

Fig. 9 Share of Spot contract in LNG Trade from 1992 to 2004 Source: PetroStrategies

21

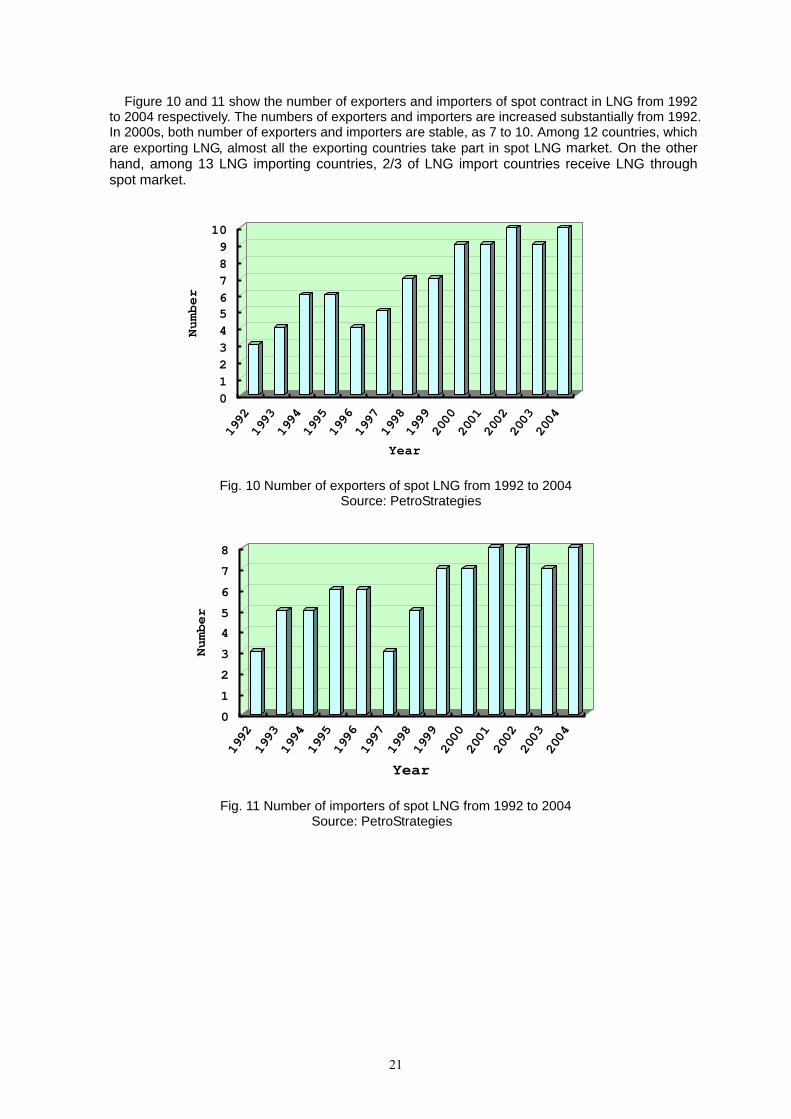

Figure 10 and 11 show the number of exporters and importers of spot contract in LNG from 1992 to 2004 respectively. The numbers of exporters and importers are increased substantially from 1992. In 2000s, both number of exporters and importers are stable, as 7 to 10. Among 12 countries, which are exporting LNG, almost all the exporting countries take part in spot LNG market. On the other hand, among 13 LNG importing countries, 2/3 of LNG import countries receive LNG through spot market.

0123456789

10

Number

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

Year

Fig. 10 Number of exporters of spot LNG from 1992 to 2004

Source: PetroStrategies

0

1

2

3

4

5

6

7

8

Number

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

Year

Fig. 11 Number of importers of spot LNG from 1992 to 2004

Source: PetroStrategies

22

Figure 12 shows the number of LNG cargos for spot contract LNG from 1992 to 2003 and the number reached 250 cargos in 2003. The number of cargos began to increase from 1999, when spot trading LNG volume started to explode.

0

50

100

150

200

250

300Number

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

Year

Fig. 12 Number of LNG cargos for spot LNG from 1992 to 2003

Source: PetroStrategies

2.4. LNG LIQUEFACTION PLANTS Overview

In 2004, 19 LNG liquefaction plants were in operation on four different continents. The oldest has

been in operation for 40 years. Since 2001, a new LNG liquefaction plant Tiga has been placed into operation in Bintulu,

Malaysia. Plans envisioned the commencement of operations by two plants (Damietta and Idku) in 2005, one (Darwin) in 2006, and four (Bioko Island, Donggi, Sakhalin, and Snohvit) in 2007. These additions when in operation will make a significant increase in the total number of trains, from 19 at present to 26.

In 2004, LNG was being produced by 12 countries, the same number as in 2001 (i.e., Algeria,

Libya, Nigeria, United States, Trinidad and Tobago, Australia, Brunei, Indonesia, Malaysia, United Arab Emirates, Oman, and Qatar). These are expected to be joined by Egypt, Equatorial Guinea, Nigeria, Russia, and Norway over the years 2005 - 2007. As such, the number of producer countries is projected to jump from 12 to 17.

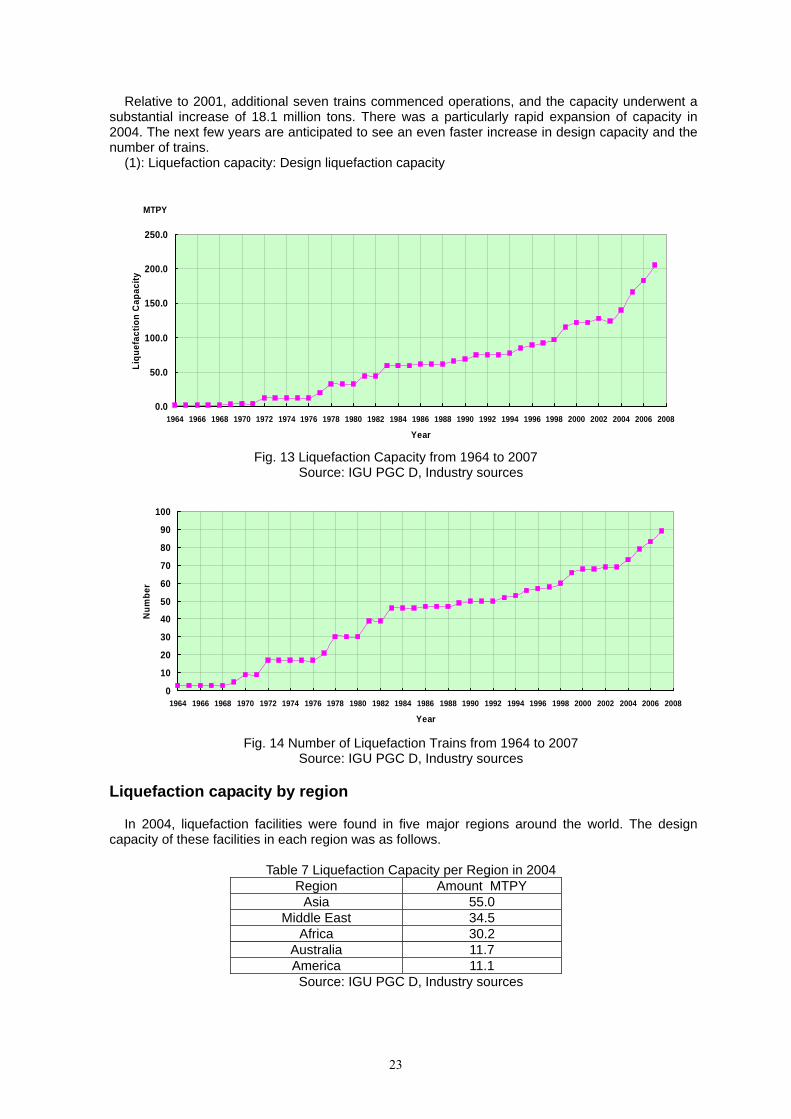

Liquefaction capacity (1) Figure 13 shows the trend of world liquefaction capacity from 1964 to 2004 and the forecast for

this capacity change up to and including 2007, and Figure 14, the corresponding trend of the number of liquefaction trains. As of 2004, the world capacity totaled 139.5 million tons per year, and liquefaction trains numbered 73. It can be seen that the capacity has increased greatly; the 2004 figure was 35 times as large as that in 1970, four times as large as that in 1980, and twice as large as that in 1990.

23

Relative to 2001, additional seven trains commenced operations, and the capacity underwent a substantial increase of 18.1 million tons. There was a particularly rapid expansion of capacity in 2004. The next few years are anticipated to see an even faster increase in design capacity and the number of trains.

(1): Liquefaction capacity: Design liquefaction capacity

0.0

50.0

100.0

150.0

200.0

250.0

1964 1966 1968 1970 1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

Year

Liqu

efac

tion

Cap

acity

MTPY

Fig. 13 Liquefaction Capacity from 1964 to 2007

Source: IGU PGC D, Industry sources

0

10

20

30

40

50

60

70

80

90

100

1964 1966 1968 1970 1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

Year

Num

ber

Fig. 14 Number of Liquefaction Trains from 1964 to 2007

Source: IGU PGC D, Industry sources

Liquefaction capacity by region In 2004, liquefaction facilities were found in five major regions around the world. The design

capacity of these facilities in each region was as follows.

Table 7 Liquefaction Capacity per Region in 2004 Region Amount MTPY

Asia 55.0 Middle East 34.5

Africa 30.2 Australia 11.7 America 11.1 Source: IGU PGC D, Industry sources

24

Figure 15 shows the regional shares of the world liquefaction capacity in 2004, and Figure 16, a comparison of these shares with those in 2001. It should be noted that in 2004, Asia continued to have the largest share of this capacity at 55.0 million tons per year (39%). Comparison with 2001 reveals a decline in the share occupied by Africa and rise in those occupied by Middle East, Australia and the Americas.

Over the years 2005 - 2007, a series of projects for construction of liquefaction plants and additional trains in Africa is forecast to bring a big expansion in Africa's share and relative decline in Asia's share, and make Africa the largest region of production.

Australia8%

Middle East24%

Africa21%

Asia39%

America8%

Fig. 15 Liquefaction Capacity per Region in 2004

Source: IGU PGC D, Industry sources

0

5

1015

20

2530

3540

45

Shar

e of

Liq

uefa

ctio

nC

apac

ity

AsiaAfric

a

Middle Eas

t

Australi

a

America

2001

2004

%

Fig. 16 Liquefaction Capacity per Region in 2001 and 2004

Source: IGU PGC D, Industry sources

25

Liquefaction capacity by country

Figures for liquefaction capacity in each country are shown below.

Table 8 Liquefaction Capacity per Country in 2004 Country Amount MTPY

Indonesia 26.1 Malaysia 23.9

Qatar 23.2 Algeria 20.0

Australia 11.7 Trinidad and Tobago 9.6

Nigeria 8.9 Oman 6.6 Brunei 5.0

United Arab Emirates 4.7 USA 1.5 Libya 1.3 Source: IGU PGC D, Industry sources

Figure 17 shows country shares of the world liquefaction capacity in 2004, and Figure 18, a

comparison of these shares with those in 2001. Indonesia had the largest share of this capacity at 26.1 million tons per year (18%). As compared to 2001, there was a sizable increase in the capacities of countries where new trains were added, i.e., Malaysia, Qatar, Australia, Nigeria, and Trinidad and Tobago.

Australia8% Qatar

16%

Indonesia18%

Oman5%

UAE3%

Nigeria6%

Brunei4%

USA1%

Libya1%

Trinidad & Tobago7%

Malaysia17%

Algeria14%

Fig.17 Liquefaction Capacity per Country in 2004 Source: IGU PGC D, Industry sources

26

0

5

10

15

20

25

30

35

Liqu

efac

tion

Cap

acity

Indonesia

Algeria

Malaysia

Qatar

Australi

a

Trinidad

& Tobag

o

Nigeria

BruneiOman UAE

USALibya

2001

2004

MTPY

Fig.18.Liquefaction Capacity per Country in 2001 and 2004

Source: IGU PGC D, Industry sources By the end of 2007, many new liquefaction plants should be operating in Egypt, Equatorial

Guinea, Nigeria, and Norway. These additions will presumably result in a relative decline in the shares of the total occupied by the existing LNG producer countries (with the exception of those constructing more trains) even if they maintain their production volumes on the same level. For this reason, the global production should be distributed among more countries around the world.

Liquefaction train capacity Figure 19 shows the trend of (average) liquefaction capacity per train over the years 2001 - 2004

and the corresponding forecast trend over the years 2005 - 2007. Four generations of liquefaction capacity per train per year can be distinguished, as follows.

First generation: about 1 million tons (1964 - 1972) Second generation: expansion to about 2.5 million tons (1972 - 1989) Third generation: expansion to about 3.5 million tons (1989 - 2003) Fourth generation: expansion to about 4 million tons (beginning in 2004)

The liquefaction capacity per train has been steadily increasing. The first train to have one of

more than 4 million tons went into operation in 2004. Capacity is anticipated to reach 5 million tons per year in 2005. Nevertheless, not all new trains are going to have such a large capacity; in recent years, trains with various capacities have been constructed, chiefly through expansions at existing plants.

27

0.0

1.0

2.0

3.0

4.0

5.0

6.0

1964 1966 1968 1970 1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

Year

Des

ign

Liqu

efac

tion

Trai

n C

apac

ity

MTPY

Fig.19 Liquefaction Train Capacity from 1964 to 2007

Source: IGU PGC D, Industry sources

Liquefaction processes There were eight types of liquefaction process in use at liquefaction plants as of 2004. Figure 20 shows the shares of the entire liquefaction capacity occupied by each type of process.

The most extensively used process was APCI C3/MCR, which accounted for liquefaction of 134 million tons per year, or the vast majority (87%) of the world total.

0102030405060708090

Shar

e

APCI- MCR PRICO MCR TEAL MCR APCI-C3/MCR

PhillipsCascade

TechnipCascade

Conoco-Phillips

OptimizedCascadeProcess

(%)

Fig. 20 Liquefaction Processes in 2004 Source: IGU PGC D, Industry sources

Figure 21 presents a comparison of the capacity share breakdowns by process in 2001, 2004,

and 2007 (forecast). Although there has been, and is anticipated to be, no change in the clear dominance of the APCI C3/MCR, use of other processes (such as optimal cascades, APCI C3/Shell MCR and Shell DMR) has been gradually increasing, and this trend is expected to continue.

28

0

20

40

60

80

100

Shar

e

APCI- MCR PRICO MCR TEAL MCR APCI- C3/MCR Phillips Cascade TechnipCascade

Conoco-PhillipsOptimizedCascade

LINDE MFC Shell DMR

Process

(%)

Fig. 21 Liquefaction Processes in 2001, 2004 and 2007

Source: IGU PGC D, Industry sources

Newly initiated plants and trains Table 9 shows the plants and trains that were first placed into operation from 2002 to 2004. An additional plant and six trains went into operation from 2002. In 2004, the Rasgas 2 train, with

a capacity of 4.7 million tons per year, the largest in the world, went into operation in Qatar.

Table 9 Newly Commenced LNG Liquefaction Plants and Trains from 2002 to 2004 Country Plant

Name Start UP

Owners Design Capacity

MTPY

Number of trains

Design Capacit

y per Train MTPY

Process Method

Nigeria Nigeria LNG 3

2002 Nigeria LNG (NNPC, Shell, Total,

ENI)

3.2 1 3.2 APCI-C3/MCR

Trinidad &

Tobago

A LNG 2 2002 Atlantic LNG (NGC/BP/Repsol/BG)

3.2 1 3.2 Optimized

Cascade Malaysi

a Tiga 2003 Malaysia LNG 6.8 2 3.4 APCI-C3/

Trinidad &

Tobago

A LNG 3 2003 Atlantic LNG (NGC/BP/Repsol/BG)

3.2 1 3.2 Optimized

Cascade Qatar Ras

Laffan 3 (Ras

Gas2)

2004 QP/ ExxsonMobil 4.7 1 4.7 APCI-C3/MCR

Australia

NWS 4 2004 NWS J/V �Woodside/Shell/

BHP/BP/ ChevronTexaco/MIMI

�

4.2 1 4.2 APCI-C3/MCR

Source: IGU PGC D, LNG Journal, GIIGNL “The LNG Industry in 2004”, Industry sources

29

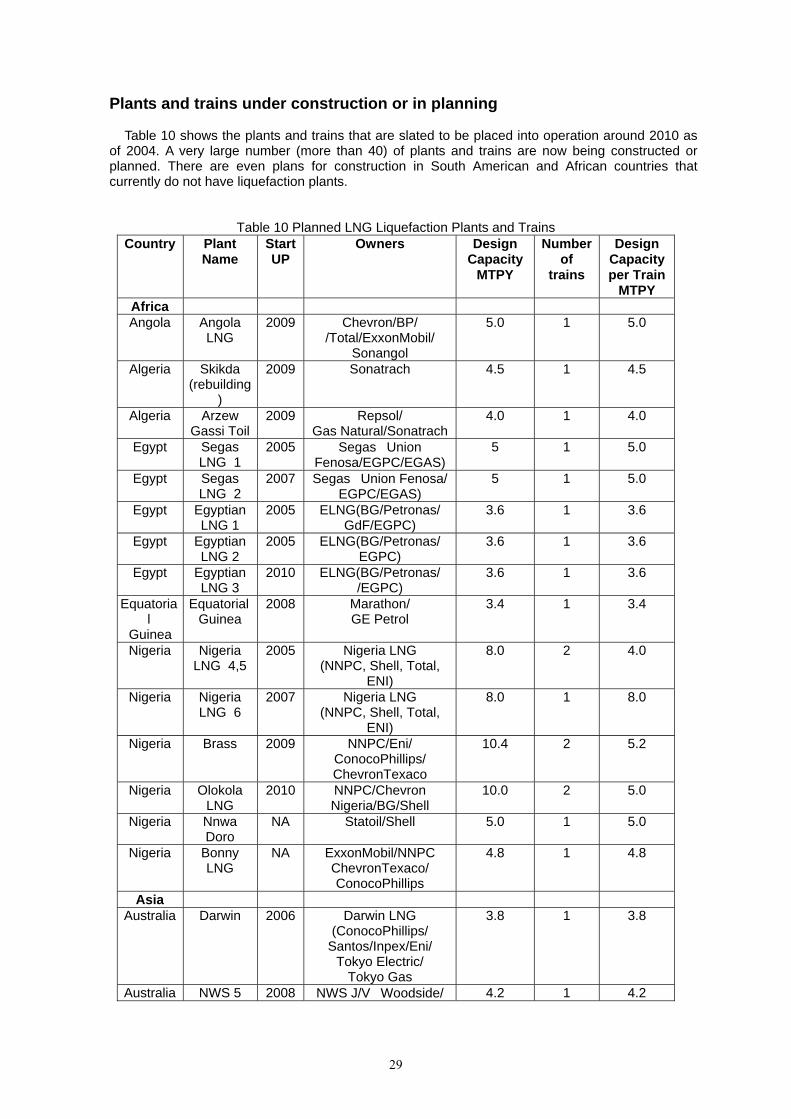

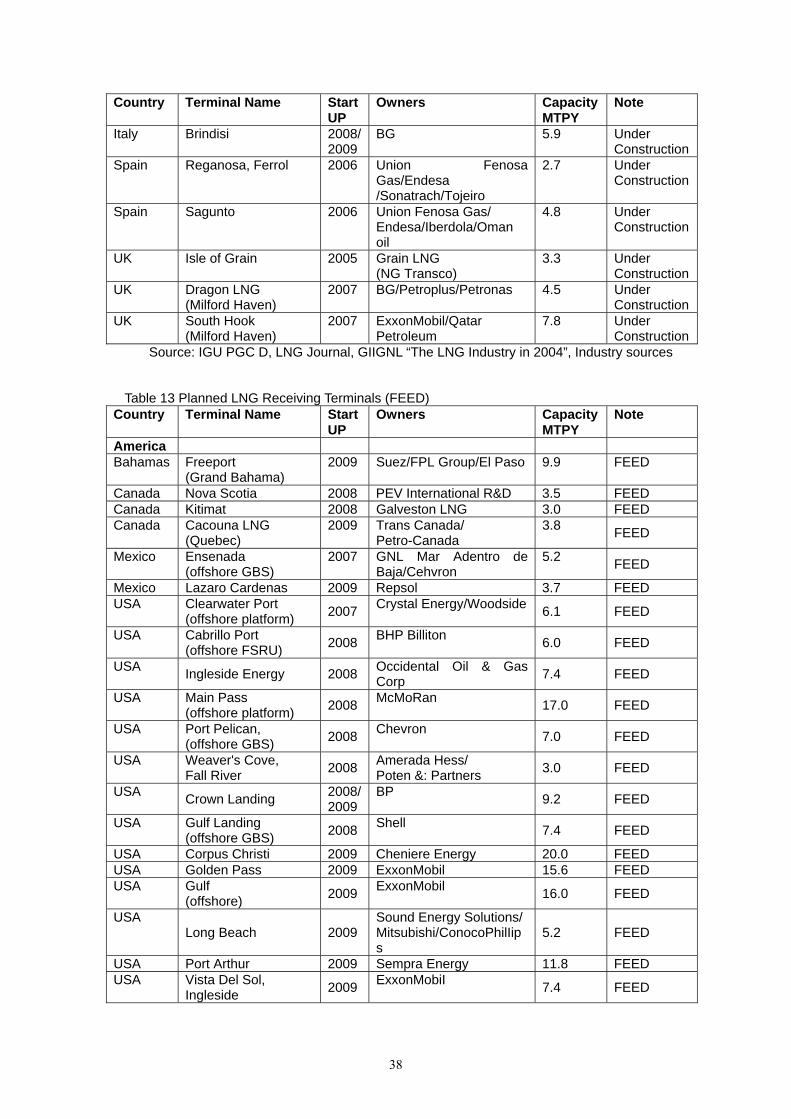

Plants and trains under construction or in planning Table 10 shows the plants and trains that are slated to be placed into operation around 2010 as

of 2004. A very large number (more than 40) of plants and trains are now being constructed or planned. There are even plans for construction in South American and African countries that currently do not have liquefaction plants.

Table 10 Planned LNG Liquefaction Plants and Trains Country Plant

Name Start UP

Owners Design Capacity

MTPY

Number of

trains

Design Capacity per Train

MTPY Africa Angola Angola

LNG 2009 Chevron/BP/

/Total/ExxonMobil/ Sonangol

5.0 1 5.0

Algeria Skikda (rebuilding

)

2009 Sonatrach 4.5 1 4.5

Algeria Arzew Gassi Toil

2009 Repsol/ Gas Natural/Sonatrach

4.0 1 4.0

Egypt Segas LNG 1

2005 Segas�Union Fenosa/EGPC/EGAS)

5 1 5.0

Egypt Segas LNG 2

2007 Segas�Union Fenosa/ EGPC/EGAS)

5 1 5.0

Egypt Egyptian LNG 1

2005 ELNG(BG/Petronas/ GdF/EGPC)

3.6 1 3.6

Egypt Egyptian LNG 2

2005 ELNG(BG/Petronas/ EGPC)

3.6 1 3.6

Egypt Egyptian LNG 3

2010 ELNG(BG/Petronas/ /EGPC)

3.6 1 3.6

Equatorial

Guinea

Equatorial Guinea

2008 Marathon/ GE Petrol

3.4 1 3.4

Nigeria Nigeria LNG 4,5

2005

Nigeria LNG (NNPC, Shell, Total,

ENI)

8.0 2 4.0

Nigeria Nigeria LNG 6

2007 Nigeria LNG (NNPC, Shell, Total,

ENI)

8.0 1 8.0

Nigeria Brass 2009 NNPC/Eni/ ConocoPhillips/ ChevronTexaco

10.4 2 5.2

Nigeria Olokola LNG

2010 NNPC/Chevron Nigeria/BG/Shell

10.0 2 5.0

Nigeria Nnwa Doro

NA Statoil/Shell 5.0 1 5.0

Nigeria Bonny LNG

NA ExxonMobil/NNPC ChevronTexaco/ ConocoPhillips

4.8 1 4.8

Asia Australia Darwin 2006 Darwin LNG

(ConocoPhillips/ Santos/Inpex/Eni/

Tokyo Electric/ Tokyo Gas

3.8 1 3.8

Australia NWS 5 2008 NWS J/V�Woodside/ 4.2 1 4.2

30

Country Plant Name

Start UP

Owners Design Capacity

MTPY

Number of

trains

Design Capacity per Train

MTPY Shell/BHP/BP/

ChevronTexaco/MIMI) Australia Gorgon 2009 Chevron/

ExxonMobil/ Shell

10.0 2 5.0

Australia Greater Sunrise

NA Woodside/ Osaka Gas/

ConocoPhillips/Shell

5.3 1 5.3

Brunei Lumut 6 2011 Brunei LNG (Brunei

Government/Shell/ Mitsubishi)

4.2 1 4.2

Indonesia Tangguh 2008 Pertamina BP/CNOOC/

Mitsubishi/Inpex/ Nippon Oil/ Kanematsu/ LNG Japan

8.4 2 4.2

Indonesia Dongi 2010 Pertamina/Medeco 7.0 2 3.5 Indonesia Bontang I NA Pertamina/Total/Unocal/

VICO 3.5 1 3.5

Russia Sakhalin 2 2007 Sakhalin LNG (Shell/Mitsui/Mitsubishi)

9.6 2 4.8

America Bolivia Pacific LNG NA Repsol/BG 7.0 2 3.5 Brazil Solimoes NA Statoil /Petrobras 2.5 1 2.5 Peru Peru LNG 2008 Hunt Oil/

SK/Sonatrach/Repsol 4.4 1 4.4

Trinidad & Tobago

A LNG 4 2005 Atlantic LNG (NGC/BP/Repsol/BG)

5.2 1 5.2

Venezuela Mariscal Surce

NA PdV/Shell/ Mitsubishi

4.7 1 4.7

M. East Iran Persian

LNG 2009 NIOC/Shell/

Repsol 10 2 5.0

Iran NICO LNG 2009 NIOC/BG 9.6 2 4.8 Iran Pars LNG 2009 NIOC/Total/Petronas 10 2 5.0 Iran Iran North

Pars NA NIOC/Indian Oil/

Petropars 8 2 4.0

Oman Qalhat LNG 2006 Oman Government/ Oman LNG/ Union

Fenosa Gas

3.7 1 3.7

Qatar Qatar Gas 2 2008 QP/ ExxsonMobil QP/ExxsonMobil/Total

15.6 2 7.8

Qatar Qatar Gas 3 2009 QP/ ConocoPhillips 7.8 1 7.8 Qatar Qatar Gas 4 2012 QP/Shell 7.8 1 7.8 Qatar Ras Laffan

4 2005 QP/ ExxsonMobil 4.7 1 4.7

Qatar Ras Laffan 5

2007 QP/ ExxsonMobil 4.7 1 4.7

Qatar Ras Laffan 6,7

2009 QP/ ExxsonMobil 15.6 2 7.8

Yemen Yemen LNG 2008 Yemen LNG (Total/Kogas/Yemen

Gas/Hunt Oil/SK/Hyundai)

6.9 2 3.45

Europe Norway Snohvit 2007 Statoil/Petoro/Total/

GdF/Amerada 4.2 1 4.2

31

Country Plant Name

Start UP

Owners Design Capacity

MTPY

Number of

trains

Design Capacity per Train

MTPY Hess/RWE-DEA)

Source: IGU PGC D, LNG Journal, GIIGNL “The LNG Industry in 2004”, Industry sources

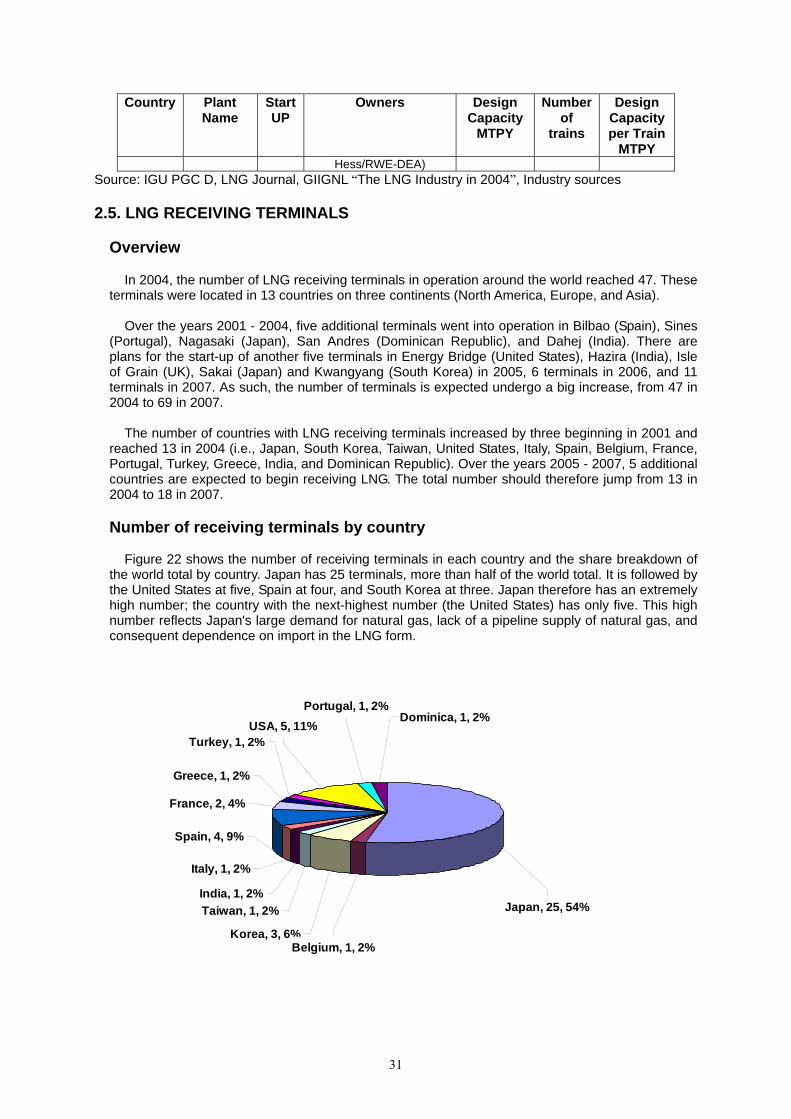

2.5. LNG RECEIVING TERMINALS Overview

In 2004, the number of LNG receiving terminals in operation around the world reached 47. These

terminals were located in 13 countries on three continents (North America, Europe, and Asia). Over the years 2001 - 2004, five additional terminals went into operation in Bilbao (Spain), Sines

(Portugal), Nagasaki (Japan), San Andres (Dominican Republic), and Dahej (India). There are plans for the start-up of another five terminals in Energy Bridge (United States), Hazira (India), Isle of Grain (UK), Sakai (Japan) and Kwangyang (South Korea) in 2005, 6 terminals in 2006, and 11 terminals in 2007. As such, the number of terminals is expected undergo a big increase, from 47 in 2004 to 69 in 2007.

The number of countries with LNG receiving terminals increased by three beginning in 2001 and

reached 13 in 2004 (i.e., Japan, South Korea, Taiwan, United States, Italy, Spain, Belgium, France, Portugal, Turkey, Greece, India, and Dominican Republic). Over the years 2005 - 2007, 5 additional countries are expected to begin receiving LNG. The total number should therefore jump from 13 in 2004 to 18 in 2007.

Number of receiving terminals by country

Figure 22 shows the number of receiving terminals in each country and the share breakdown of

the world total by country. Japan has 25 terminals, more than half of the world total. It is followed by the United States at five, Spain at four, and South Korea at three. Japan therefore has an extremely high number; the country with the next-highest number (the United States) has only five. This high number reflects Japan's large demand for natural gas, lack of a pipeline supply of natural gas, and consequent dependence on import in the LNG form.

Dominica, 1, 2%

Italy, 1, 2%

India, 1, 2%Taiwan, 1, 2%

Korea, 3, 6%Belgium, 1, 2%

Spain, 4, 9%

France, 2, 4%

Greece, 1, 2%

Turkey, 1, 2%USA, 5, 11%

Portugal, 1, 2%

Japan, 25, 54%

32

Fig.22 LNG Receiving Terminals per Country In 2004 Source: IGU PGC D, LNG Journal, GIIGNL "The LNG Industry in 2004", Industry sources

33

Number of receiving terminals by region Figure 23 shows the number of receiving terminals in each region. The share of the total

occupied by Asia is substantial, mainly because of the many terminals in Japan. Asia accounts for about 65% of the total.

Asia, 30, 64%

Europe, 11, 23%USA, 6, 13%

Fig.23 LNG Receiving Terminals per Region In 2004

Source: IGU PGC D, LNG Journal, GIIGNL "The LNG Industry in 2004", Industry sources

Number of receiving terminals in each year of start-up

Figure 24 shows the number of receiving terminals in each year (period) of start-up. The number

of terminals placed into operation increased over the years 1970 - 1990, leveled off in the first half of the 1990s, and began to increase again in the second half of the 1990s. Numerous terminals are under construction or in planning, and the number is anticipated to increase at an explosive rate beginning around 2005.

0

1

2

3

4

5

6

7

8

Number

-1970 1971-1975

1976-1980

1981-1985

1986-1990

1991-1995

1996-2000

2001-2004

Year

Fig. 24 Start Year of LNG Receiving Terminals from 1969 to 2004 Source: IGU PGC D, LNG Journal, GIIGNL "The LNG Industry in 2004", Industry sources

34

LNG storage capacity Figure 25 shows the LNG storage capacity (the combined capacity of LNG tanks) in each country

in 2004. Japan, which also had the most LNG receiving terminals, had the largest capacity, accounting for about 60% of the world total, and was followed by South Korea at about 17%. This huge storage capacity derives from the country's dependence on import of LNG due to the lack of natural gas supply by pipeline, and the need to absorb the great degree of seasonal demand fluctuation due to the high demand in the civil sector.

South Korea has many large-scale terminals, and its storage capacity is consequently high for its

number of terminals. LNG storage tanks in receiving terminals range in capacity from 35,000 to 200,000 cubic meters.

The largest ones are underground tanks built in Japan.

Dominica1%

India4%

Italy1%

Portugal1%

USA5%

Turkey1%

Greece1%France

3%

Belgium1%

Korea17%

Taiwan2%

Spain3%

Japan60%

Fig.25 LNG storage capacity per country

Source: IGU PGC D, LNG Journal, GIIGNL "The LNG Industry in 2004", Industry sources

Maximum capacity of LNG carriers able to berth Figure 26 shows the maximum capacity of LNG carriers able to berth at LNG receiving terminals. Large carriers are able to berth at almost all terminals; terminals able to accept shipments from

carriers with a capacity of 100,000 cubic meters or more account for 84% of the total number. Eleven percent can accommodate carriers with a capacity of more than 140,000 cubic meters as

well, and some are already taking steps to handle larger carriers. Terminals of this type are likely to increase in number over the coming years.

35

70,000-100,000m35%

140,000 or morem3

11%10,000-70,000 m3

14%

100,000-140,000m3

70%

Fig.26 Maximum Capacity of LNG Carriers for LNG Receiving Terminals in 2004 Source: IGU PGC D, Gas LNG Europe, Industry sources

Gas send out capacity

Figure 27 shows the total send out capacity of LNG terminals. Terminals with sendout capacity

between five and ten billion cubic meters per year are the most frequent.

0

2

4

6

8

10

12

14

16

18

Num

ber

<1 1.0-<5.0 5.0-<10 10-<20 20-<30 30-<40

Capacity Bm3PY

Fig.27 Total Gas Send out Capacity of LNG Terminals in 2004

Source: IGU PGC D, Gas LNG Europe, LNG in Japan, GIIGNL "The LNG Industry in 2004", Industry sources

36

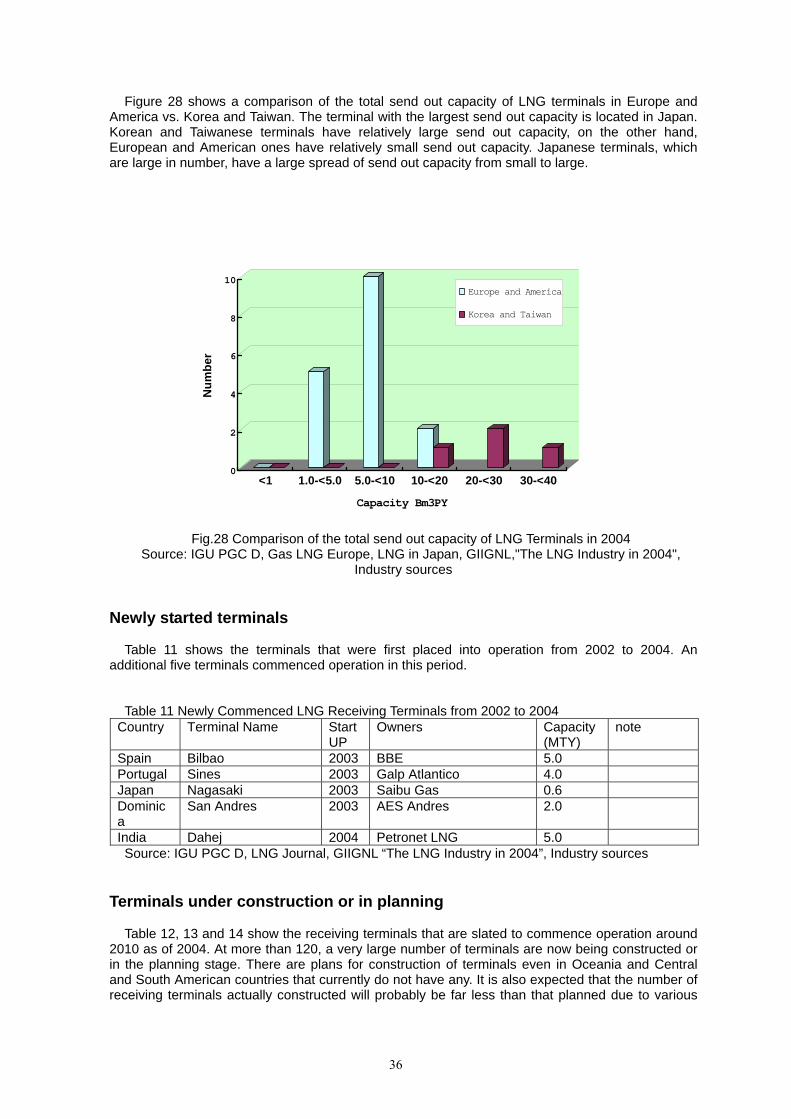

Figure 28 shows a comparison of the total send out capacity of LNG terminals in Europe and America vs. Korea and Taiwan. The terminal with the largest send out capacity is located in Japan. Korean and Taiwanese terminals have relatively large send out capacity, on the other hand, European and American ones have relatively small send out capacity. Japanese terminals, which are large in number, have a large spread of send out capacity from small to large.

0

2

4

6

8

10

Num

ber

<1 1.0-<5.0 5.0-<10 10-<20 20-<30 30-<40

Capacity Bm3PY

Europe and America

Korea and Taiwan

Fig.28 Comparison of the total send out capacity of LNG Terminals in 2004 Source: IGU PGC D, Gas LNG Europe, LNG in Japan, GIIGNL,"The LNG Industry in 2004",

Industry sources

Newly started terminals

Table 11 shows the terminals that were first placed into operation from 2002 to 2004. An

additional five terminals commenced operation in this period. Table 11 Newly Commenced LNG Receiving Terminals from 2002 to 2004

Country Terminal Name Start UP

Owners Capacity (MTY)

note

Spain Bilbao 2003 BBE 5.0 Portugal Sines 2003 Galp Atlantico 4.0 Japan Nagasaki 2003 Saibu Gas 0.6 Dominica

San Andres 2003 AES Andres 2.0

India Dahej 2004 Petronet LNG 5.0 Source: IGU PGC D, LNG Journal, GIIGNL “The LNG Industry in 2004”, Industry sources

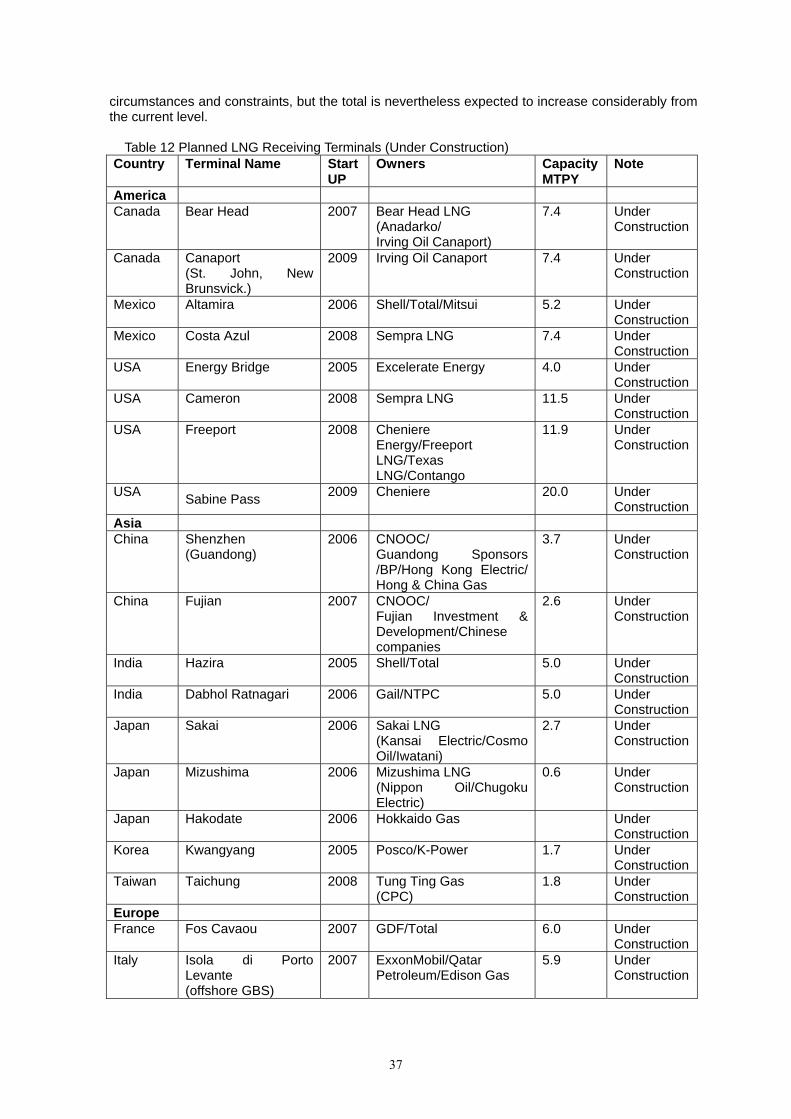

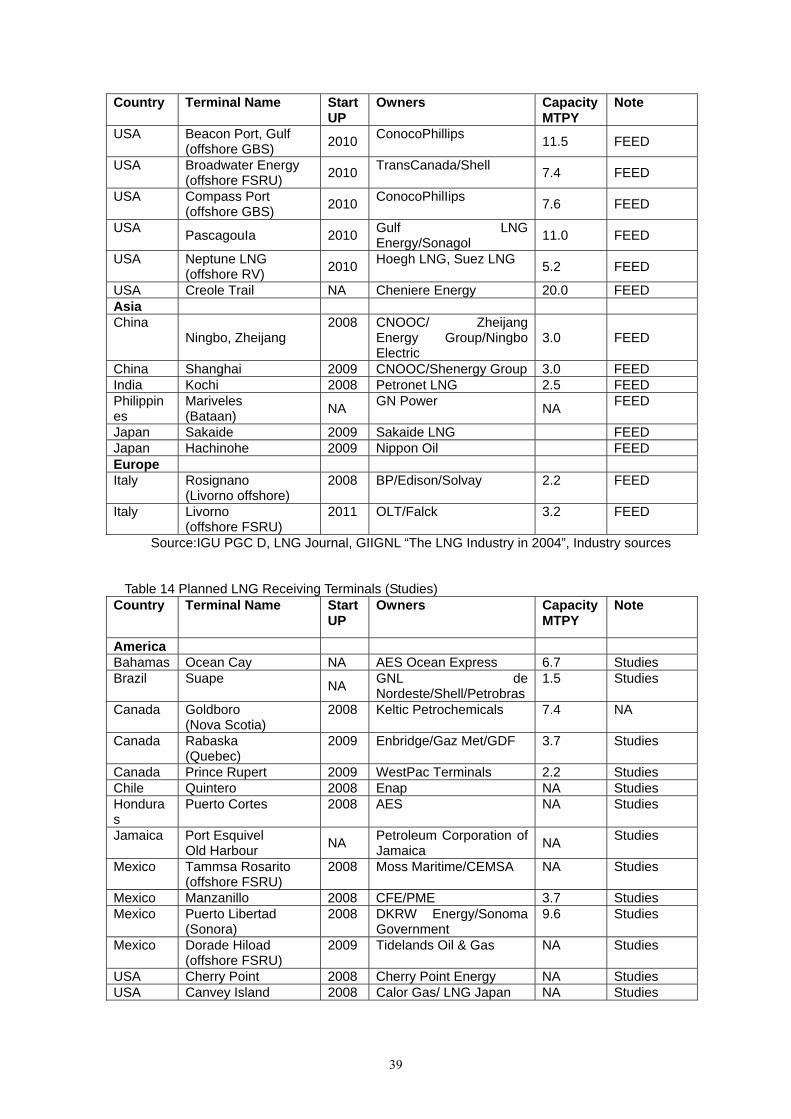

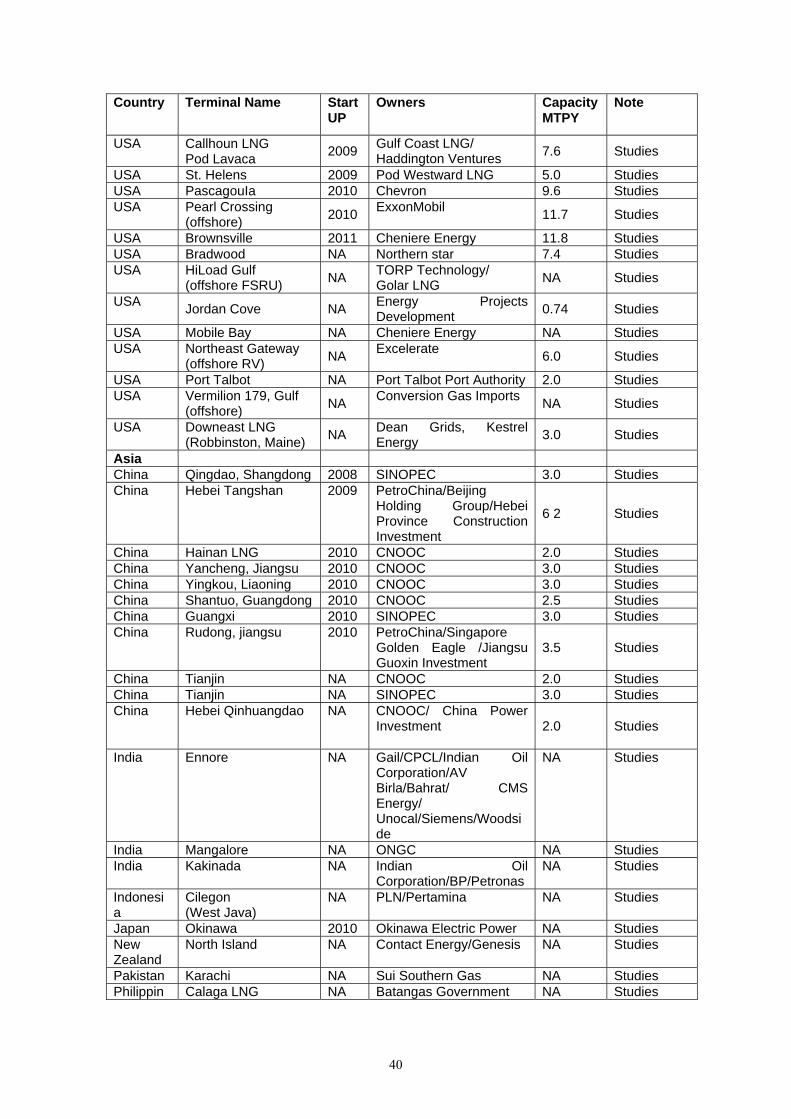

Terminals under construction or in planning

Table 12, 13 and 14 show the receiving terminals that are slated to commence operation around 2010 as of 2004. At more than 120, a very large number of terminals are now being constructed or in the planning stage. There are plans for construction of terminals even in Oceania and Central and South American countries that currently do not have any. It is also expected that the number of receiving terminals actually constructed will probably be far less than that planned due to various

37

circumstances and constraints, but the total is nevertheless expected to increase considerably from the current level.

Table 12 Planned LNG Receiving Terminals (Under Construction)

Country Terminal Name Start UP

Owners Capacity MTPY

Note

America Canada Bear Head 2007 Bear Head LNG

(Anadarko/ Irving Oil Canaport)

7.4 Under Construction

Canada Canaport (St. John, New Brunsvick.)

2009 Irving Oil Canaport 7.4 Under Construction

Mexico Altamira 2006 Shell/Total/Mitsui 5.2 Under Construction

Mexico Costa Azul 2008 Sempra LNG 7.4 Under Construction

USA Energy Bridge 2005 Excelerate Energy 4.0 Under Construction

USA Cameron 2008 Sempra LNG 11.5 Under Construction

USA Freeport 2008 Cheniere Energy/Freeport LNG/Texas LNG/Contango

11.9 Under Construction

USA Sabine Pass 2009 Cheniere 20.0 Under Construction

Asia China Shenzhen

(Guandong) 2006 CNOOC/

Guandong Sponsors /BP/Hong Kong Electric/ Hong & China Gas

3.7

Under Construction

China Fujian 2007 CNOOC/ Fujian Investment & Development/Chinese companies

2.6 Under Construction

India Hazira 2005 Shell/Total 5.0 Under Construction

India Dabhol Ratnagari 2006 Gail/NTPC 5.0 Under Construction

Japan Sakai 2006 Sakai LNG (Kansai Electric/Cosmo Oil/Iwatani)

2.7 Under Construction

Japan Mizushima 2006 Mizushima LNG (Nippon Oil/Chugoku Electric)

0.6 Under Construction

Japan Hakodate 2006 Hokkaido Gas Under Construction

Korea Kwangyang 2005 Posco/K-Power 1.7 Under Construction

Taiwan Taichung 2008 Tung Ting Gas (CPC)

1.8 Under Construction

Europe France Fos Cavaou 2007 GDF/Total 6.0 Under

Construction Italy Isola di Porto

Levante (offshore GBS)

2007 ExxonMobil/Qatar Petroleum/Edison Gas

5.9 Under Construction

38

Country Terminal Name Start UP

Owners Capacity MTPY

Note

Italy Brindisi 2008/2009

BG 5.9 Under Construction

Spain Reganosa, Ferrol 2006 Union Fenosa Gas/Endesa /Sonatrach/Tojeiro

2.7 Under Construction

Spain Sagunto 2006 Union Fenosa Gas/ Endesa/Iberdola/Oman oil

4.8 Under Construction

UK Isle of Grain 2005 Grain LNG (NG Transco)

3.3 Under Construction

UK Dragon LNG (Milford Haven)

2007 BG/Petroplus/Petronas 4.5 Under Construction

UK South Hook (Milford Haven)

2007 ExxonMobil/Qatar Petroleum

7.8 Under Construction

Source: IGU PGC D, LNG Journal, GIIGNL “The LNG Industry in 2004”, Industry sources

Table 13 Planned LNG Receiving Terminals (FEED) Country Terminal Name Start

UP Owners Capacity

MTPY Note

America Bahamas Freeport

(Grand Bahama) 2009 Suez/FPL Group/El Paso 9.9 FEED

Canada Nova Scotia 2008 PEV International R&D 3.5 FEED Canada Kitimat 2008 Galveston LNG 3.0 FEED Canada Cacouna LNG

(Quebec) 2009 Trans Canada/

Petro-Canada 3.8 FEED

Mexico Ensenada (offshore GBS)

2007 GNL Mar Adentro de Baja/Cehvron

5.2 FEED

Mexico Lazaro Cardenas 2009 Repsol 3.7 FEED USA Clearwater Port

(offshore platform) 2007 Crystal Energy/Woodside 6.1 FEED

USA Cabrillo Port (offshore FSRU) 2008 BHP Billiton 6.0 FEED

USA Ingleside Energy 2008 Occidental Oil & Gas Corp 7.4 FEED

USA Main Pass (offshore platform) 2008 McMoRan 17.0 FEED

USA Port Pelican, (offshore GBS) 2008 Chevron 7.0 FEED

USA Weaver's Cove, Fall River 2008 Amerada Hess/

Poten &: Partners 3.0 FEED

USA Crown Landing 2008/2009

BP 9.2 FEED

USA Gulf Landing (offshore GBS) 2008 Shell 7.4 FEED

USA Corpus Christi 2009 Cheniere Energy 20.0 FEED USA Golden Pass 2009 ExxonMobil 15.6 FEED USA Gulf

(offshore) 2009 ExxonMobil 16.0 FEED

USA Long Beach 2009

Sound Energy Solutions/ Mitsubishi/ConocoPhilIips

5.2 FEED

USA Port Arthur 2009 Sempra Energy 11.8 FEED USA Vista Del Sol,

Ingleside 2009 ExxonMobiI 7.4 FEED

39

Country Terminal Name Start UP

Owners Capacity MTPY

Note

USA Beacon Port, Gulf (offshore GBS) 2010 ConocoPhillips 11.5 FEED

USA Broadwater Energy (offshore FSRU) 2010 TransCanada/Shell 7.4 FEED

USA Compass Port (offshore GBS) 2010 ConocoPhilIips 7.6 FEED

USA PascagouIa 2010 Gulf LNG Energy/Sonagol 11.0 FEED

USA Neptune LNG (offshore RV) 2010 Hoegh LNG, Suez LNG 5.2 FEED

USA Creole Trail NA Cheniere Energy 20.0 FEED Asia China

Ningbo, Zheijang 2008 CNOOC/ Zheijang

Energy Group/Ningbo Electric

3.0 FEED

China Shanghai 2009 CNOOC/Shenergy Group 3.0 FEED India Kochi 2008 Petronet LNG 2.5 FEED Philippines

Mariveles (Bataan) NA GN Power NA FEED

Japan Sakaide 2009 Sakaide LNG FEED Japan Hachinohe 2009 Nippon Oil FEED Europe Italy Rosignano

(Livorno offshore) 2008 BP/Edison/Solvay 2.2 FEED

Italy Livorno (offshore FSRU)

2011 OLT/Falck 3.2 FEED

Source:IGU PGC D, LNG Journal, GIIGNL “The LNG Industry in 2004”, Industry sources

Table 14 Planned LNG Receiving Terminals (Studies)

Country Terminal Name Start UP

Owners Capacity MTPY

Note

America Bahamas Ocean Cay NA AES Ocean Express 6.7 Studies Brazil Suape NA GNL de

Nordeste/Shell/Petrobras 1.5 Studies

Canada Goldboro (Nova Scotia)

2008 Keltic Petrochemicals 7.4 NA

Canada Rabaska (Quebec)

2009 Enbridge/Gaz Met/GDF 3.7 Studies

Canada Prince Rupert 2009 WestPac Terminals 2.2 Studies Chile Quintero 2008 Enap NA Studies Honduras

Puerto Cortes 2008 AES NA Studies

Jamaica Port Esquivel Old Harbour NA Petroleum Corporation of

Jamaica NA Studies

Mexico Tammsa Rosarito (offshore FSRU)

2008 Moss Maritime/CEMSA NA Studies

Mexico Manzanillo 2008 CFE/PME 3.7 Studies Mexico Puerto Libertad

(Sonora) 2008 DKRW Energy/Sonoma

Government 9.6 Studies

Mexico Dorade Hiload (offshore FSRU)

2009 Tidelands Oil & Gas NA Studies

USA Cherry Point 2008 Cherry Point Energy NA Studies USA Canvey Island 2008 Calor Gas/ LNG Japan NA Studies

40

Country Terminal Name Start UP

Owners Capacity MTPY

Note

USA Callhoun LNG� Pod Lavaca 2009 Gulf Coast LNG/

Haddington Ventures 7.6 Studies

USA St. Helens 2009 Pod Westward LNG 5.0 Studies USA PascagouIa 2010 Chevron 9.6 Studies USA Pearl Crossing

(offshore) 2010 ExxonMobil 11.7 Studies

USA Brownsville 2011 Cheniere Energy 11.8 Studies USA Bradwood NA Northern star 7.4 Studies USA HiLoad Gulf

(offshore FSRU) NA TORP Technology/ Golar LNG NA Studies

USA Jordan Cove NA Energy Projects Development 0.74 Studies

USA Mobile Bay NA Cheniere Energy NA Studies USA Northeast Gateway

(offshore RV) NA Excelerate 6.0 Studies

USA Port Talbot NA Port Talbot Port Authority 2.0 Studies USA Vermilion 179, Gulf

(offshore) NA Conversion Gas Imports NA Studies

USA Downeast LNG (Robbinston, Maine) NA Dean Grids, Kestrel

Energy 3.0 Studies

Asia China Qingdao, Shangdong 2008 SINOPEC 3.0 Studies China Hebei Tangshan 2009 PetroChina/Beijing

Holding Group/Hebei Province Construction Investment

6 2 Studies

China Hainan LNG 2010 CNOOC 2.0 Studies China Yancheng, Jiangsu 2010 CNOOC 3.0 Studies China Yingkou, Liaoning 2010 CNOOC 3.0 Studies China Shantuo, Guangdong 2010 CNOOC 2.5 Studies China Guangxi 2010 SINOPEC 3.0 Studies China Rudong, jiangsu 2010 PetroChina/Singapore

Golden Eagle /Jiangsu Guoxin Investment

3.5 Studies

China Tianjin NA CNOOC 2.0 Studies China Tianjin NA SINOPEC 3.0 Studies China Hebei Qinhuangdao NA CNOOC/ China Power

Investment

2.0 Studies

India Ennore NA Gail/CPCL/Indian Oil Corporation/AV Birla/Bahrat/ CMS Energy/ Unocal/Siemens/Woodside

NA Studies

India Mangalore NA ONGC NA Studies India Kakinada NA Indian Oil

Corporation/BP/Petronas NA Studies

Indonesia

Cilegon (West Java)

NA PLN/Pertamina NA Studies

Japan Okinawa 2010 Okinawa Electric Power NA Studies New Zealand

North Island NA Contact Energy/Genesis NA Studies

Pakistan Karachi NA Sui Southern Gas NA Studies Philippin Calaga LNG NA Batangas Government NA Studies

41

Country Terminal Name Start UP

Owners Capacity MTPY

Note

es (Manila) Singapore

NA 2012 Singapore Energy Authority

NA Studies

Thailand Map Ta Phud NA PTT NA Studies Europe Cyprus Vassiliko 2009 Cyprus Government 0.7 Studies Germany Wilhemshaven NA E. ON NA Studies Italy Taranto 2009 Gas Natural 5.9 Studies Italy Priolo/Augusta/Melilli 2010 Shell Energy

Europe/ERG Power & Gas

5.9 Studies

Italy Monfalcone (offshore)

2010 Endesa 6.0 Studies

Italy Sicily 2010 EPG power & Gas 5.8 Studies Netherlands

Maasvlakte Port of Rotterdam

2010 Gasunie/Royal Vopak 6.4 Studies

Netherlands

Port of Rotterdam

2010 Petroplus NA Studies

Poland Baltic NA PGNiG NA Studies Spain Arinaga

(Gran Canary Island) 2008 Gascan/Unelco Endesa 1.5 Studies

Spain Granadilla 2008 Gascan/Unelco Endesa 1.5 Studies Sweden Oxelusund NA Sydkraft Gas

(Eon) NA Studies

UK Canvey Island 2010 Calor Gas/LNG Japan/Centrica/Osaka Gas

4.0 Studies

UK Amlwch (Anglesey)

NA Canatxx NA Studies

Source: IGU PGC D, LNG Journal, GIIGNL “The LNG Industry in 2004”, Industry sources 2.6. LNG CARRIERS

Overview

In 2004, a total of 174 LNG carriers were in operation. Taken together, they had a combined

capacity of 20.72 million cubic meters, for an average of 119,000 cubic meters per carrier. Over the years 2001 - 2004, an additional 47 carriers were placed into service, and the combined

capacity jumped by 6.45 million cubic meters or 45%. Due to the commissioning of large carriers, the average capacity was 3,000 cubic meters larger than in 2001.

Capacity

Figure 29 shows the distribution of the number of LNG carriers by capacity class in 2004. The share occupied by large carriers has become large; carriers with a capacity of at least 135,000 cubic meters accounted for 78% of the total. A carrier in the Oman project had the highest capacity at 147,000 cubic meters.

42

135,000m3�46%

� 40,000m35%

� 100,000m311%

� 135,000m332%

Fig. 29 Capacity of LNG Carriers

Source: GIIGNL “The LNG Industry in 2004”, Tokyo Gas, Industry sources

Figure 30 shows the trend of LNG carrier age (number of years of service) and capacity for carriers that were commissioned over the years 1969 – 2004 and the corresponding forecast trend over the years 2005-2008. Carrier size began to increase around 1975, when carriers in the 125,000-cubic-meter class made their appearance. Almost all carriers commissioned since 1998 have a capacity of at least 135,000 cubic meters.

020,00040,00060,00080,000

100,000120,000140,000160,000180,000200,000220,000240,000

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

Year of Delivery

Cap

acity

m3

Fig. 30 Capacity of LNG Carriers from 1969 to 2004

Source: GIIGNL “The LNG Industry in 2004”, Tokyo Gas, Industry sources

The needs for cost reduction are expected to lead to an increase in commissions of carriers in the class of 150,000 cubic meters. Furthermore, carriers with a capacity in excess of 200,000 cubic meters are scheduled to be placed into service beginning in 2007. Carrier capacities are therefore projected to become much larger.

Figure 31 shows the trend of the combined LNG carrier capacity over the years 1969 to 2004

and the corresponding forecast trend over the years 2005-2008. The placement of many large carriers into service since 2002 greatly increased the total capacity, which reached 20.72 cubic meters in 2004. The total capacity will keep increasing rapidly from 2004 to 2008.

43

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

19691971197319751977197919811983198519871989199119931995199719992001200320052007

Year

Capacity

km3

Fig. 31 Total Capacity of LNG Carriers Source: GIIGNL "The LNG Industry in 2004", Tokyo Gas, Industry sources

Number of commissions

Figure 32 shows the trend of the number of LNG carriers commissioned over the years 1969-

2004 and the corresponding forecast trend over the years 2005-2008. Newly commissioned carriers numbered nine in 2002, 15 in 2003, and 23 in 2004.

The number of vessels commissioned was in average about eight at the most up until 1999, but

has been steadily increasing since 2000. This increase is linked to that in the LNG import and export volume accompanying the construction of additional liquefaction and receiving terminals. An additional 21 carriers were scheduled to be commissioned in 2005, and the number of additions will amount to 47 in 2008.

05101520253035404550

Number

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Year

Fig. 32 Number of Delivery of LNG Carriers from 1969 to 2004 Source: GIIGNL "The LNG Industry in 2004", Tokyo Gas, Industry sources

Figure 33 shows the trend of the total number of commissions over the years 1969 – 2004 and

the corresponding forecast trend over the years 2005-2008. The number rapidly raised beginning in 2002, reached 174 in 2004 and will reach 302 in 2008.

44

0

50

100

150

200

250

300

350

1969 1971 1973 1975 1977 1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007

Year

Number

Fig. 33 Total Number of Delivery of LNG Carriers from 1969 to 2004 Source: GIIGNL "The LNG Industry in 2004", Tokyo Gas, Industry sources

Tank type

Figure 34 shows the number of carriers in each category of tank type. There are four basic types:

Moss, Esso, SPB, and membrane. The Moss and membrane types are two major types, and the membrane type accounts for 61%.

020406080100120140160180

Number

Esso Moss SPB Membrane

Tank Type

Fig. 34 Tank Type of LNG Carriers from 1969 to 2004

Source: GIIGNL "The LNG Industry in 2004", Tokyo Gas, Industry sources

45

2.7. CONCLUSION

1) The volume of LNG trade reached 142.4 million tons and increased 35 million tons, or 33%, from 2001.

2) The share of spot trade in LNG has been increasing substantially in recent years to reach 19% of total LNG trade volumes in 2004.

3) The world LNG liquefaction capacity totaled 139.5 million tons per year in 2004 and increased 18.1 million tons since 2001.

4) The number of liquefaction trains in operation numbered 73 in 12 countries. 5) The number of LNG receiving terminals in operation around the world reached 47. These

terminals were located in 13 countries on three continents. 6) 174 LNG carriers were in operation. The combined capacity of these ships is 20.72 million

cubic meters, which has increased by 6.45 million cubic meters, or 45%, from 2001, for an average of 119,000 cubic meters per carrier.

7) LNG industry has been keeping rapid growth in recent years due to the environment-friendly characteristics and the transportability of LNG. This trend will continue for the years to come.

2.8. REFERENCES

1. Inter Group of Liquefied National Gas Importers (GIIGNL). (2005). The LNG industry 2004

2. BP (2005) Statistical Review of World Energy June 2005

3. International Gas Union (IGU) (2003) The World-wide LNG Industry until 2001 and

forecasts of its development for 2004 and 2014 4. Japan Gas Association (JGA). (2004). LNG in Japan 2004

5. LNG journal (2005) Tables of Liquefaction Terminals 6. LNG journal (2005) Tables of Reception Terminals

7. PetroStrategies

46

3. LNG QUALITY

REPORT OF STUDY GROUP D1

“LNG quality”

RAPPORT DU GROUPE DE TRAVAIL D1

“Qualité du GNL”

Study Group Chairman/Président du Groupe de Travail

Rob Klein Nagelvoort

THE NETHERLANDS

47

ABSTRACT

LNG quality is of growing interest to producers and buyers alike as the LNG market becomes more liquid. Historical reasons have lead to a situation today in which the large traditional LNG markets in the Far East, which are used to rich LNG, struggle to accept lean LNG with a High Heating Value (HHV) of less than about 411 MJ/m3, or better a Wobbe Index (WI) of about 52 MJ/m3. On the other hand, some fast-growing new LNG markets that are used to lean pipeline gas cannot accept LNG with a WI above about 52 MJ/m3 without (expensive) quality adjustment at their import terminals. This paper describes the situation in detail and explores possible processing options in LNG export plants and import terminals, to ensure that available LNG meets market demands. We review the quality of LNGs currently produced, and highlight the reasons why suppliers have historically tended to design their plants for richer product. After a review of the quality debate in the major traditional, growing and emerging LNG markets, we predict that the LNG market will move towards trading two distinct LNG grades: “High Wobbe LNG”, with a WI above about 52 MJ/m3 and “Low Wobbe LNG”, with a WI below this value. Certain markets, e.g. Europe, are striving for broad LNG specifications that allow them to accept both grades.

RESUME

La qualité du GNL a un intérêt croissant pour les fournisseurs et les acheteurs alors que le marché devient de plus en plus ouvert. Des raisons historiques ont conduit à une situation dans laquelle les importants marchés traditionnels de l’extrême orient qui utilisent un GNL plus riche ont des difficultés à accepter un GNL plus pauvre avec un pouvoir calorifique supérieur (PCS) inférieur à 41 MJ/m3 ou un indice de Wobbe d’environ 52 MJ/m3. D’un autre côté, quelques-uns uns des nouveaux marchés dynamiques du GNL, qui utilisent habituellement du gaz pauvre, ne peuvent accepter un GNL avec un indice de Wobbe au-dessus de 52 MJ/m3 sans un ajustement de qualité coûteux aux terminaux importateurs. Cet article décrit précisément la situation actuelle et montre, dans les usines de GNL et les terminaux d’importations, les options possibles qui assurent l’adéquation entre la demande des marchés et le GNL disponible. Nous faisons l’inventaire des qualités du GNL actuellement produit et nous montrons les raisons historiques qui poussent les fournisseurs à avoir une tendance à concevoir leurs usines pour un produit plus riche. Apres une analyse de la qualité dans les principaux marchés : traditionnels, émergeants et en croissance ; nous montrons que les marchés du GNL vont évoluer vers deux commerces de qualités distinctes : l’un avec un GNL possédant un indice de Wobbe supérieur à 52 MJ/m3 et l’autre avec un indice de Wobbe plus faible. Certains marchés, comme l’Europe, s’efforcent d’accepter ces deux qualités de GNL, avec des spécifications du GNL très large.

1 This report used throughout standard reference conditions as described in ISO norm 13443:1996, i.e. a combustion reference temperature of 15°C, and reference conditions for volume measurements of 15°C and 1 atm pressure (1.01325 bara). For conversion factors to other units and reference conditions, see appendix 3.

48

TABLE OF CONTENT

3.1. Introduction

3.2. Essential LNG quality specifications • General • Combustion properties • Impurities

3.3. The current LNG quality debate in key importing countries • Japan • EU (EASEE-gas) • UK • USA • China • India

3.4. Technical possibilities for LNG quality adjustment • At the export plant • At the import terminal

3.5. Conclusions and Recommendations • General conclusions • Available LNG and market requirements • View to the future • Recommendations

Appendices • Biliography • Conversion factors for High Heating Value and Wobbe Index • Further details on China

49

3.1. INTRODUCTION

Until the late 1990’s, LNG trade was predominantly based on long-term contracts between a single supplier and a single customer. That meant in most cases the supplier could adjust the product to suit an established pipeline gas market, or an emerging LNG market’s specifications became aligned to the dominant supplier’s product.

More recently, utilisation of spare plant capacity beyond contracted volumes has made additional cargoes available for sale into an increasingly diverse and expanding market. At the same time, gas demand has risen while local gas supplies by pipeline have diminished, increasing the movement of gas over long distances. In extreme cases, cargoes have crossed traditional regional boundaries and become the first global trades. In the 21st century, entry of a number of new large and smaller players, and renewal of some of the old contracts, has either forced or enabled suppliers to set up multiple contracts with customers in different locations and even different regions.

The LNG produced around the world varies in composition depending on the nature of reservoir fluids, whether or not they are associated with an oil production, and how much LPG is extracted during liquefaction. And to further complicate matters, for historical reasons charted in more detail in Section 3.3 of this report, individual nations have developed different gas specifications. So a 21st century supplier is faced with matching his product to different market requirements, and a terminal operator has to consider flexibility to receive LNG of different quality from different sources.

This report addresses the dilemma of how to reconcile varying compositions and specifications - but only at one level, and that is the issue of international specifications. It does not remove the final problem of quality adjustment, whether at the liquefaction end of the chain or at the regasification terminal, from economic decisions in a free market by both suppliers and customers. Instead, it seeks to foster co-operation and balancing of costs and benefits along the gas value chain by suggesting a way of harmonising the specifications. It aims to make economic decisions more transparent. And finally it offers a tool for briefing legislators and other stakeholders about a specialist topic. The specifications themselves vary in ways that are discussed in more detail in Section 2. Broadly speaking, they refer to:

• Combustion properties, which specify the energy content and also affect gas flame characteristics (Wobbe index, High Heating Value and Relative Density)

• Compositional limits such as maximum sulphur and oxygen, acceptable nitrogen content and sometimes limits on some individual hydrocarbon components

Supply of gas outside these limits could have major commercial, safety and environmental

implications for some individual customers. Finally, specifications are sometimes written in different units with different reference conditions.

Methods currently available for quality adjustment are discussed briefly in Section 3.4. There is plenty of material on this subject in the public domain and within other industry groups. We explain advantages and disadvantages of the various available options, and draw some general conclusions.

In Section 3.5 we offer our conclusions and some perceptions of our members on where current trends are leading the LNG trade over the next 10-15 years, as a guide to where the next wave of investment will be needed. This is to begin to answer the questions: “What type of LNG will be sellable?” and “What type of quality adjustment equipment will needed?”

50

3.2. ESSENTIAL LNG QUALITY SPECIFICATIONS 3.2.1. GENERAL

When talking about the “quality” of LNG, people mostly refer to the High Heating Value (HHV) or Gross Calorific Value (GCV), a measure of its energy content per volume. The HHV or GCV is the number of heat units generated when a unit volume of product in the vapour phase at standard temperature and pressure is burnt completely in dry air. The gaseous products of combustion are brought to the same standard conditions of temperature and pressure, but the water produced is condensed to liquid in equilibrium with water vapour.