Embed Size (px)

Citation preview

September 2016 Update

Link’n Learn: Property Funds, Private Equity and Real Estate

Speakers

Francesco PiantoniDirector– Strategy, Regulatory and Corporate FinanceDeloitte LuxembourgE: [email protected]: +352 451 453 371

David McCaffreySenior Manager– AuditDeloitte IrelandE: [email protected]: +353 1 417 2983

Rory Brown Manager– AuditDeloitte IrelandE: [email protected]: +353 1 417 5745

Agenda

1

2 RE Strategies

3

Financial Cash Flows & Operations4

Balance Sheet and Profit & Loss examples5

RE from an Investor Perspective6

Fund Structures

Numbers and Trends

Numbers and Trends

© 2016 Link’n Learn Webinars 5

Constant growth of AuM and strong concentration

The Global Real Estate Funds market as a whole

Concentration

• Strong concentration of assets held by largest players

• €627 million is the average size of private RE funds

• 2015 was record high: investment volumes reached highest level since 2008

At global level, RE funds are by far the preferred structure to invest in RE, with 60.86% of AuM held

33% of AuM are managed by top 10

53% by top 20

Sources: Institutional Real Estate, Global Investment Managers 2016, Preqin Global Real Estate Report 2016

0.00 €

0.50 €

1.00 €

1.50 €

2.00 €

2.50 €

3.00 €

2010 2011 2012 2013 2014 2015+120%

Agg

rega

te A

uM(€

trill

ion)

1.09€1.29€

1.41€1.55€

2.40€

2.05€ CAGR17.1%

+18%+9%

+10%

+32%

+17%

Top 100 firms in aggregate (AuM, € trillion)

Real Estate funds

Discretionary separate accounts

Advisory separate accounts

Not disclosed

Global AUM by investment structure

14%

61%

11%

14%

Numbers and Trends

© 2016 Link’n Learn Webinars 6

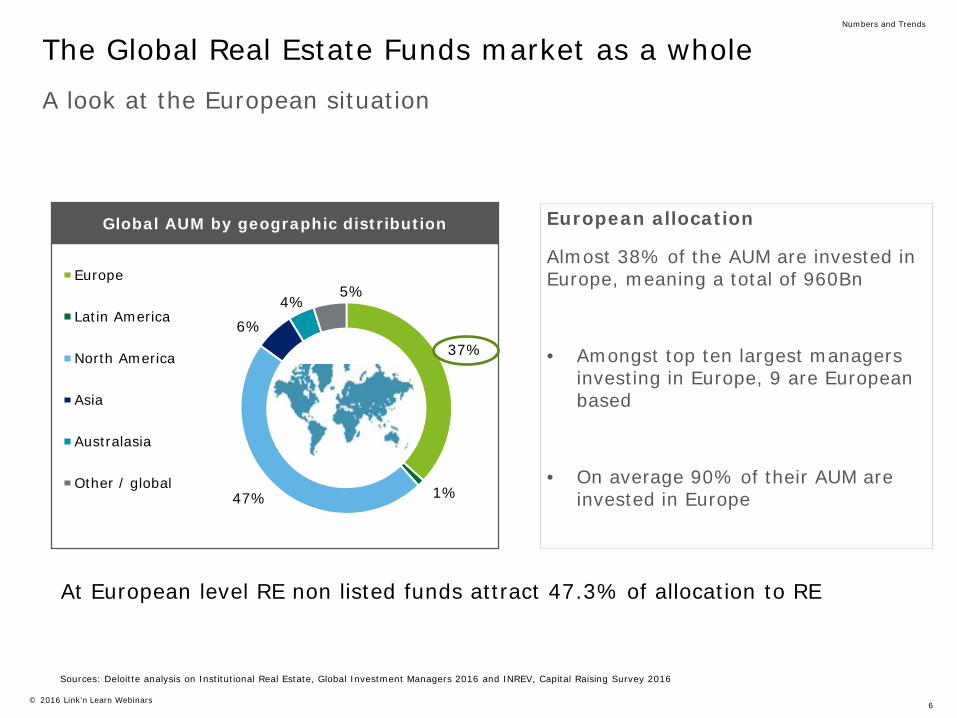

The Global Real Estate Funds market as a wholeA look at the European situation

37%

1%47%

6%4%

5%Europe

Latin America

North America

Asia

Australasia

Other / global

Global AUM by geographic distribution European allocation

Almost 38% of the AUM are invested in Europe, meaning a total of 960Bn

• Amongst top ten largest managers investing in Europe, 9 are European based

• On average 90% of their AUM are invested in Europe

Sources: Deloitte analysis on Institutional Real Estate, Global Investment Managers 2016 and INREV, Capital Raising Survey 2016

At European level RE non listed funds attract 47.3% of allocation to RE

Numbers and Trends

© 2016 Link’n Learn Webinars 7

Real Estate in NumbersLargest Investment managers based on AuM

Source: Institutional Real Estate, Inc – Global Investment Mangers 2016

Global

Rank Investment Manager Europe AuM in €M

Total AuM in €M

1 Swiss Life Asset Managers 62,200.00 62,200.00

2 AXA Investment Managers – Real Assets 59,152.00 62,904.00

3 Aviva Investors 44,120.87 45,719.95

4 Credit Suisse Real Estate Investment Management 42,070.49 45,775.44

5 CBRE Global Investors 41,779.69 82,639.11

6 Deka ImmobilienInvestment/WestInvest 30,961.00 33,173.20

7 The Blackstone Group 29,036.88 135,795.02

8 M&G Real Estate 28,734.61 33,905.48

9 Aberdeen Asset Management 26,143.74 26,289.11

10 TH Real Estate 25,448.80 84,400.49

Rank Investment Manager Total AuM in €M

1 Brookfield Asset Management 137,054.00

2 The Blackstone Group 135,795.02

3 TH Real Estate 84,400.49

4 CBRE Global Investors 82,639.11

5 Hines 82,031.74

6 MetLife Investment Management 75,993.93

7 UBS Asset Management, Global Real Estate 67,259.28

8 AXA Investment Managers – Real Assets 62,904.00

9 Swiss Life Asset Managers 62,200.00

10 J.P. Morgan Asset Management – Global Real Assets 60,071.64

Europe

Numbers and Trends

© 2016 Link’n Learn Webinars 8

Global fundraising and capital allocation to RE

• In Europe constant growth of capital raising for the past three years (+16,5% from 2014 to 2015)

• Capital raised in 2015 is more than double than in 2012

• Non listed RE funds dominate the allocation with 47.3%

• Despite the global macro economy outlook, investment into global RE has been strong

• RE is the asset class for pension funds and insurance companies, which contribute for 60% of the total allocation

• Top 20 firms control 53% of the industry asset

Sources: INREV, Investment Intention Survey 2016; Institutional Real Estate, Global Investment Managers 2016

Numbers and Trends

EUROPE€60.1Bn

ASIA PAC€19Bn

NORTH AMERICA€44.4Bn

OTHER€13Bn

EUROPE€63.1Bn

ASIA PAC€16.9Bn

NORTH AMERICA

€34.5Bn

AFRICA

0%OTHER

€9.1Bn

fundraising for RE globally

investment allocation in RE globally

© 2016 Link’n Learn Webinars 9

Source: INREV, Capital Raising Survey 2016 (it includes non-listed RE funds, JV, club deals, separate accounts and non-listed debt products)

Fundraising – latest trends from INREV surveyAn extraordinary momentum for the RE industry

In 2015, 51.1% or €63.1 billion committedto vehicles with a preference for Europe

0

50

100

2013 2014 2015

€ 96.2 BILLION

€ 122.7 BILLION

€ 123.6 BILLION

New capital raised Main sources of capital

Product typesTotal capital raised

-6,4%

-1,7%

+6,5%

-2,9%

+2,5%

N/A

+1,4%

+0,9%

+0,2%

-2,5%

Numbers and Trends

© 2016 Link’n Learn Webinars 10

Source: INREV, Investment Intention Survey 2016; INREV fund termination study

RE fund lifecycle – recycling of capital

holding sellingfundraising investing

AU

M

Time

Recycling of capital

Snapshot of the next three years

holding sellingfundraising investing

Funds launched in 2005, 2006 and 2007 are reaching the end of their life and are currently divesting, or about to divest, their assets:

• From 2016 to 2018, 72 funds will be liquidated, representing a current NAV of €11,1Bn

• In the period 2016 to 2018 approximately one third of all closed end funds with termination dates between 2009 and 2019 will be wounded up

Boosted by the extraordinary capital allocation to RE, a lot of new funds have been set up and are currently deploying their capital

• Looking at investment intention for 2016, €19,99bn is targeting Europe

• This means a capital inflow for RE managers of about €39,2bn over the last couple of years (€19,2bn for 2015)

Numbers and Trends

RE Strategies

© 2016 Link’n Learn Webinars 12

Core• Fund assets provide stable income returns and

investments are made in diversified metropolitan areas

• Low level of leverage

Value Added• May require a higher level of active management • Medium to high level of leverage • Returns are driven by a combination of income

and capital return

Opportunistic• A high level of active management is required:

tactical investments• High level of leverage• Returns are driven primarily through capital

return

Core Plus• Generally involves core properties requiring

further investments (refurbishments, extensions, etc.)

Distressed• Investments are made in distressed properties

(foreclosure order, sale by mortgagee…)• High level of risk and complexity• Active management is required

RE Fund Strategies

Core

Core PlusValue Added

Opportunistic

Real Estate fund strategiesType of fund strategies

RE Strategies

© 2016 Link’n Learn Webinars 13

Real Estate fundsFund strategies - Comparison

Core Core plus Value added Opportunistic Distressed

Fund assets / properties

Stabilized, income producing

Core properties requiring further investments

Assets often require some refurbishment, active asset

management or development

Acquisition of distressed assets, large portfolio acquisitions and re-

packaging in smaller lot sizes, tactical investments

Distressed properties ( foreclosure order, sale by

mortgagee, etc.)

Return driver Stable income return with small capital return Income & capital return Capital return

Timeframe of investments

Management activity

Overall target return .

LTV

Risk

20% and more p.a.5-6% p.a.

HigherLower

Short termLong term

Very activePassive

Fund duration by investment style

0%

20%

40%

60%

80%

100%

Core Opportunity Value Added

% o

f to

tal n

umbe

r of

Lu

x RE

fund

s

11-15 y 8 - 10 y Infinite Up to 7 years

Management fees range for direct RE funds in basis points Overall target return & risk

In general, high return = high risk

Risk & performance feesIn general, high risk = high fees

Risk & fund durationIn general, long term = lower risk

Source: ALFI survey November 2015

Lower Higher

26%

33%

17%

17%

6%

0 to 50 51 to 100 101 to 150 > 150 No Data

RE Strategies

Fund Structures

© 2016 Link’n Learn Webinars 15

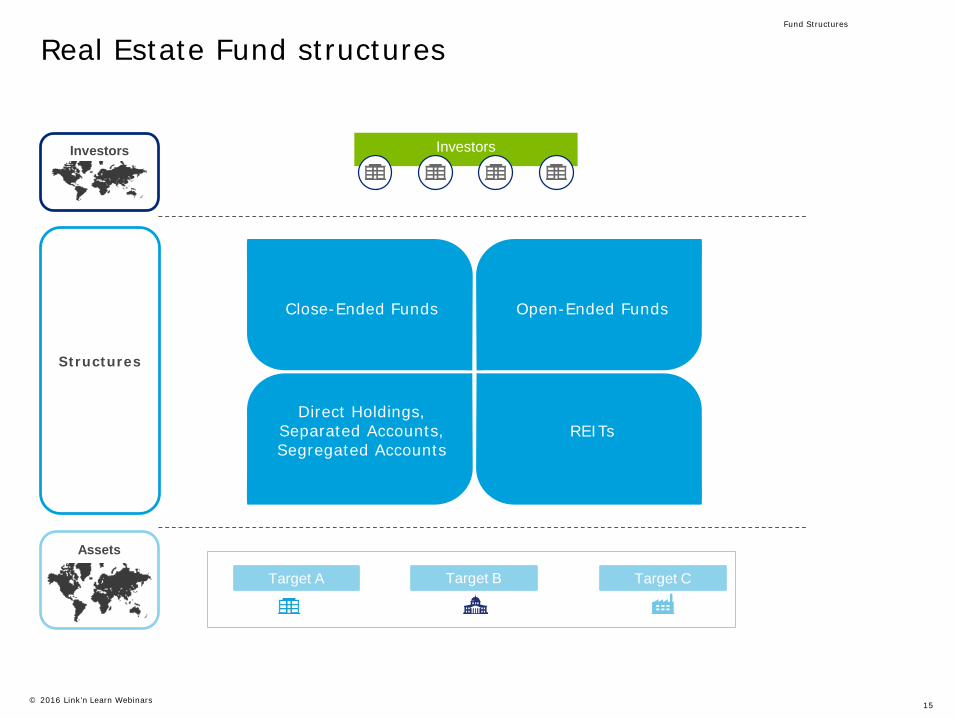

Real Estate Fund structures

Investors

Target BTarget A Target C

Investors

Assets

Structures

Close-Ended Funds Open-Ended Funds

Direct Holdings, Separated Accounts, Segregated Accounts

REITs

Fund Structures

© 2016 Link’n Learn Webinars 16

Close-ended FundFunds set up for a limited period of time: Definite Life

holding sellingfundraising investing

In a Nutshell

• Fund with a fixed life and well defined timeframe to buy and sell assets

• Subscriptions are made for capital commitment which are subsequently drawn up over time

• Redemptions are generally not permitted

Au

M

Fund Manager looks for investors to join the fund through

roadshows and fund marketing

Fund Manager finds investors and starts

to buy assets

Management of the assets according to the strategy of the

fund

Disposal of the assets and

distribution of proceeds

Fund Structures

Time

© 2016 Link’n Learn Webinars 17

Open-ended FundShares issued and redeemed at any time during the life of the fund

holding, buying & sellingfundraising investing

In a Nutshell

• Fund set up for unlimited period of time, after the initial period assets can be bought and sold anytime

• Investors can redeem and subscribe at anytime during the life of the fund, usually subscriptions are made through capital commitment

• Given redemption rights cash management is of paramount importance

AuM

Set up: similar to Close-ended The number of acquisitions and disposals is linked with the ability of the manager to attract future investors in the fund

Acquisitions to invest capital raised during the life of the fund. Disposal to pay

investors redemptions

Tactical acquisition and disposal to

deploy the strategy of the fund

Fund Structures

Time

© 2016 Link’n Learn Webinars 18

REIT structures

REIT Structures

Transparency of financial reporting

Tax neutral structures

Obligation to distribute the bulk of its rental income

Generally listed and traded on stock

exchanges

REIT legislation prohibits

over-gearing and over-exposure

EPRA Best Practices

Recommendations

Diversified investors

Regulated environment

Fund Structures

Financial Cash Flows & Operations

© 2016 Link’n Learn Webinars 20

Cash Flows & Operations

Financial Cash Flows & Operations

Real Estate Funds

Investors

Property BProperty A Property C

Investors

Assets Portfolios

Structure

Management and performance fees

Fund Management

servicesDebt repayment + interests

Fund expenses

Capital / equity injectionServices

Banks (Debt Provider)

Investment manager

TrusteeProperty manager

Lending

Property management services

Property manager fees

Trustee fees

Acts on behalf of investors

Ownership of properties

Rental income and

sales proceeds

Distributions (Mainly

Dividends)

Balance Sheet and Profit & Loss examples

© 2016 Link’n Learn Webinars 22

Balance Sheet and Profit & Loss examples

Balance Sheet and Profit & Loss examples

Assets

As at31/12/2015

CU’000

As at31/12/2014

CU’000Current assetsCash and cash equivalents 270 139Interest receivable 387 677Investment property 198,245 127,448

Financial assets at fair value through profit or loss 36,579 15,957

Total assets 235,481 144,221

LiabilitiesCurrent liabilitiesAccrued expenses 659 416Borrowings 25,227 10,005Financial liabilities at fair value through profit or loss 1,411 2,064Total liabilities (excluding net assets attributable to holders of redeemable shares) 27,297 12,485

Net assets attributable to holders of redeemable shares 208,184 131,736

© 2016 Link’n Learn Webinars 23

Balance Sheet and Profit & Loss examples

Balance Sheet and Profit & Loss examples

Year ended31/12/2015

CU’000

Year ended31/12/2014

CU’000Revenue

Rental income 29,521 10,909Net change in unrealized gains/(losses) on financial assets and liabilities

held at fair value through profit or loss 15,741 (4,301)

Fair value movement on investment property 32,993 3,551Total operating income 78,255 10,159Expenses

Management fees (1,998) (2,851)Performance fees (88) (174)Custodian fees (216) (443)Administration fees (138) (76)Transaction costs (107) (321)Professional fees (7) (10)Director’s fees (15) (15)Other expenses (7) (1)Total operating expenses (2,579) (3,893)Operating profit/(loss) 75,679 6,268

Finance costsInterest expense (386) (1,419)

Profit/(loss) after distributions and before tax 75,293 4,849Withholding taxes (87) (60)

Profit/(loss) after distributions and tax 76,058 4,789

Increase/(decrease) in net assets attributable to holders of redeemable shares

75,206 4,789

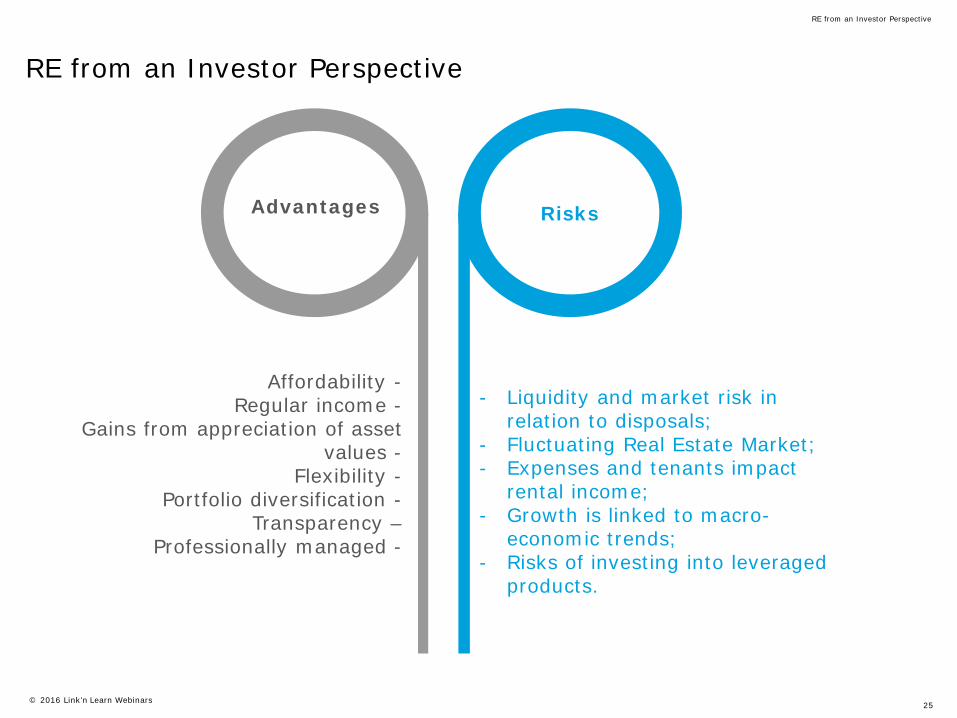

RE from an Investor Perspective

© 2016 Link’n Learn Webinars 25

RE from an Investor Perspective

RE from an Investor Perspective

RisksAdvantages

Affordability -Regular income -

Gains from appreciation of asset values -

Flexibility -Portfolio diversification -

Transparency –Professionally managed -

- Liquidity and market risk in relation to disposals;

- Fluctuating Real Estate Market;- Expenses and tenants impact

rental income;- Growth is linked to macro-

economic trends;- Risks of investing into leveraged

products.

© 2016 Link’n Learn Webinars 26

Questions?

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a private company limited byguarantee, and its network of member firms, each of which is a legally separate and independententity. Please see www.deloitte.com/ie/about for a detailed description of the legal structure of DeloitteTouche Tohmatsu Limited and its member firms.

With nearly 2,000 people in Ireland, Deloitte provide audit, tax, consulting, and corporate finance topublic and private clients spanning multiple industries. With a globally connected network of memberfirms in more than 150 countries, Deloitte brings world-class capabilities and high-quality service toclients, delivering the insights they need to address their most complex business challenges. With over210,000 professionals globally, Deloitte is committed to becoming the standard of excellence.

This publication contains general information only, and none of Deloitte Touche Tohmatsu Limited,Deloitte Global Services Limited, Deloitte Global Services Holdings Limited, the Deloitte ToucheTohmatsu Verein, any of their member firms, or any of the foregoing’s affiliates (collectively the“Deloitte Network”) are, by means of this publication, rendering accounting, business, financial,investment, legal, tax, or other professional advice or services. This publication is not a substitute forsuch professional advice or services, nor should it be used as a basis for any decision or action thatmay affect your finances or your business. Before making any decision or taking any action that mayaffect your finances or your business, you should consult a qualified professional adviser. No entity inthe Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relieson this publication.

© 2016 Deloitte. All rights reserved