Embed Size (px)

Citation preview

1

Limited Liability Partnership

Presentation by Lakhani & Co.

CHARTERED ACCOUNTANTS

2

Index

Features

Notified Dates

International Presence

Activities

Comparison

Partners

First Schedule

Formation of LLP

Taxation of LLP

Conversion of Partnership Firm into LLP

Conversion of Company into LLP

Tax issues relating to conversion of Company into LLP

Conversion of LLP into Company

Lakhani & Co.

3

Index

Chartered Accountant in Practice - LLP

Statutory Compliances

Audit of Accounts

Compromise & Arrangements

Merger & Demerger

Dissolution of LLP

Winding up of LLP

FEMA Provisions - Inbound and Outbound Investments

Stamp duty implications

Lakhani & Co.

4

Features

An alternative corporate business form which combines the benefits of Limited Liability and flexibility of partnership.

Granted the status of corporate body and hence, its existence is perpetual.

Can hold movable and immovable properties in its own name.

A separate legal entity having its own assets and liabilities. The assets of the LLP can be appropriated fully towards its liabilities. The liability of the partners is limited to the extent of their contribution in the LLP.

Liability of the partner is limited to the extent of his contribution and the partners are not liable on account of any independent or unauthorized action of the other partners.

Lakhani & Co.

5

Notified Dates

Rajya Sabha - 24th October, 2008

Lok Sabha - 13th December, 2008

President of India - 7th January, 2009

Official Gazette - 9th January, 2009

LLP Act – Effective date 1st April, 2009

LLP Rules – Effective date 1st April, 2009

Various amendments made from time to time

Lakhani & Co.

6

International Presence

Australia

France

Gulf Countries

Italy

Singapore

United Kingdom

United State of America

In some countries, with minor modification, the structure is known as LLC

Indian LLP structure is broadly based on UK LLP and Singapore LLP structure

Lakhani & Co.

7

Activities

Can carry on any business or profession

Cannot carry out any non-profit activities.

Cannot carry out business of lending, financing and investments (NBFC activities). No specific restriction in LLP Act, 2008, but ROC and RBI does not permit these activities.

Lakhani & Co.

8

Comparison – LLP vs Partnership

LLP Minimum partners – 2

Maximum partners – unlimited

A legal entity

Registration is compulsory

May have its own common seal

Name has to be approved by the registrar and must have LLP as suffix

Agreement available for inspection

Can hold property in its own name

Foreign nationals can be partners

Liability is limited. Partner is liable only to the extent of agreed contribution and not for any independent/ unauthorized act of other partners

Partnership Minimum partners – 2

Maximum partners – 20

Not a legal entity

Registration is optional

No concept of common seal

Any name of its choice

Deed not available for inspection

Cannot hold property in its own name

Foreign nationals cannot be partners

Liability is unlimited. Partner is jointly and severally liable for all the acts of the firm and its other partners

Lakhani & Co.

9

Comparison – LLP vs Partnership

LLP Relationship of Partner and LLP

and partner inter-se depends upon terms of LLP agreement

Provisions of Indian Partnership Act, 1932 not applicable

Is a legal entity which can be sued as well as it can sue the third party

Minor cannot become partner

Partnership Partner can act as an agent of the

firm as well as agent of the other partners

Provisions of Indian Partnership Act, 1932 applicable

Legal proceedings can be taken against a partnership firm irrespective whether it is registered or not. Only registered partnership firm can take legal recourse or defend legal proceedings

Minor can be admitted to the benefits of partnership

Lakhani & Co.

10

Comparison – LLP vs Company

LLP LLP Act, 2008

Ownership and management can be with same person or can be divorced

Operational structure has more flexibility Eg. change in terms of partnership, change in profit sharing ratio, remunerating the partners, introduction and withdrawal of capital, dissolution of LLP etc.

Company Companies Act, 1956

Ownership and management is divorced

Operational structure has less flexibility

Lakhani & Co.

11

Comparison – LLP vs Company

LLP Statutory compliance easy

approval by Partners only

Accounts can be maintained either on cash or mercantile system

Company Statutory compliance complex

approval by BOD’s/ Shareholders

Accounts have to maintained on mercantile system

Lakhani & Co.

12

Partners

Minimum two individuals as partners who will be identified as Designated Partners.

There is no upper limit for number of partners.

Individuals, Foreign nationals, Indian Companies, Foreign Companies, Foreign LLP and Foreign LLC can become partner.

In a case where corporate bodies are only partners at least two corporate bodies will have to nominate two individuals as partners who will be identified as Designated Partners.

Government will issue guidelines for Foreign LLP and Foreign LLC to become partner in LLP. They will be governed by FEMA regulations.

Minors cannot become partners of LLP.

Lakhani & Co.

13

Obligations of Designated Partner

Lakhani & Co.

Every LLP shall have atleast two individuals as Designated Partners.

One of Designated Partner should be resident in India meaning he should be residing in India for more than 182 days in any financial year.

The Designated Partners are responsible for compliance of the statutory compliance of Limited Liability Partnership Act, 2008 and Limited Liability Partnership Rules, 2009.

Every Designated Partner will have to obtain “Designated Partner’s Identification Number” (DPIN).

Designated Partner can retire from LLP.

14

Admission and Retirement

Lakhani & Co.

Any eligible entity can become partner of LLP at the time when the said LLP is incorporated or at any time after its incorporation.

Any partner can retire from LLP at any time subject to the terms and condition of LLP agreement.

LLP has to inform the Registrar about change in the composition of the partners.

15

Transfer of Economic Interest

Lakhani & Co.

Any partner of a LLP can transfer and assign his full or part share to any third person subject to LLP agreement. Such a transfer shall not by itself cause the partner’s disassociation or dissolution and winding up of LLP.

The transferee or assignee shall not be eligible to participate in the management or conduct of the LLP’s activities. He will not be deemed to be a partner of the LLP.

16

Partner by Holding Out

Lakhani & Co.

Any person, not being the partner of any LLP, who by words spoken or written or by conduct represents himself or knowingly permits himself to be represented to be a partner of LLP then he will be treated as “ partner by holding out”. He will be liable to any person who has on the faith of any such representation given credit to the LLP, whether the person representing himself or represented to be a partner does or does not know that the representation has reached the person so giving credit.

If LLP receives any credit then it shall be liable to the extent of credit received by it or any financial benefit derived by it.

17

First Schedule The provisions of First Schedule are subject to the terms and conditions

stipulated in the LLP agreement.

All the partners are entitled to share equally in the capital, profits and losses of LLP.

LLP shall indemnify each partner in respect of payments made and personal liability incurred by him in the ordinary course of business of LLP.

Every partner can take part in the management of LLP.

No partner shall be entitled to remuneration for managing and conducting business of LLP.

No person may be introduced as a partner without the consent of the existing partners.

All matters shall be decided by a resolution passed by a majority in number of the partners and for this purpose each partner shall have one vote.

Lakhani & Co.

18

First Schedule Every decision taken by LLP shall be recorded in minutes within 30 days of

taking such decision.

If any partner carries on any business of the same nature and compets with LLP he must account for an pay over to LLP all profits made by him in this business.

If any partner derives any benefit without the consent of LLP from any transaction concerning the LLP or any use by him of the property, name or other business connection of LLP then he shall account for the same to LLP.

Majority of the partners cannot expel any partner.

All disputes inter-se of partners shall be resolved as per the provisions of Arbitration and Conciliation Act, 1996.

Lakhani & Co.

Formation of LLP

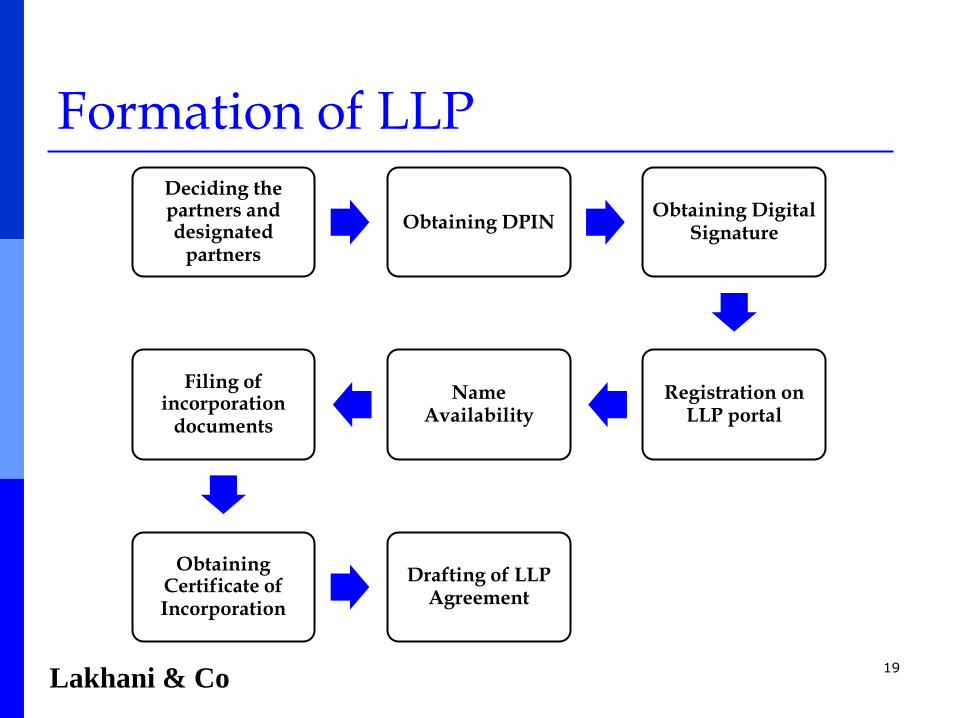

Lakhani & Co 19

Deciding the partners and designated

partners

Obtaining DPIN Obtaining Digital

Signature

Registration on LLP portal

Name Availability

Filing of incorporation

documents

Obtaining Certificate of Incorporation

Drafting of LLP Agreement

20

Agreement

Partners can execute LLP agreement which will set out terms upon which the LLP conducts its activities.

This agreement can set out the mutual rights and duties of the partners and the relationship of LLP and its partners and partners inter-se.

If the partners decide not to execute LLP agreement then the mutual rights and obligations of the partners shall be as provided under First Schedule to the Limited Liability Partnership Act, 2008.

Lakhani & Co.

21

Taxation of LLP The Finance Bill (No.2), 2009 has amended the definition of firm to include

LLP. The status of LLP is equal to the firm.

The status of a partner of LLP is equal to the partner of a firm.

The taxable income of LLP will be subjected to tax at the maximum marginal rate being 30%.

No surcharge is payable by LLP. Cess as applicable is payable.

Interest and Remuneration payable to partners, subject to provisions of Section 40(b) will be allowed as deduction while computing the taxable income of LLP.

The distribution of income by LLP is not subjected to dividend distribution tax. LLP is not subjected to double taxation.

In the hands of the partner the amount received from LLP as share of profit is exempt u/s 10(2A) of Income Tax Act, 1961.

Interest and remuneration received by the partners of LLP will be subjected to tax under the head “Income from Business or Profession”.

Contd….

Lakhani & Co.

22

Taxation of LLP

Any company which is a partner in a LLP is not liable to pay MAT on the share of profit receivable from LLP.

LLP is generally not liable to pay MAT. Certain LLPs are liable to pay MAT on its adjusted total income u/s 115 JC which is introduced from A.Y. 2012-13. Adjusted total income include total income as increased by the deduction claimed u/s VIA and Section 10AA.

MAT is payable @ 18.5% on adjusted total income.

LLP will be entitled to MAT credit u/s 115JD which can be carried forward upto to 10th Assessment year.

In case of retirement or dissolution of LLP, provisions of S.45(4) of the Income Tax Act, 1961 may be applicable.

One of the Designated Partner has to sign the return of income. If due to unavoidable circumstances, Designated Partner can not sign the return of income then any of the other partners may sign the return.

Contd….

Lakhani & Co.

23

Taxation of LLP

Each partner of LLP is jointly and severally liable for tax due of LLP.

Under Section 188A of Income-tax Act,1961, in case of a partnership firm, the partners are jointly and severally liable for tax payable by the firm. Section 167C of Income-tax Act,1961 will apply to the partners of LLP and if the partner of LLP proves that non recovery cannot be attributed to any gross neglect, misfeasance or breach of duty on his part in relation to the affairs of the LLP then he will not be personally liable.

Lakhani & Co.

24

Partnership LLP

Existing Partnership Firm can be converted into LLP and all the assets, liabilities and business of existing partnership firm will vest in to LLP.

The conversion of partnership into LLP will not attract any tax liability. The Explanatory Memorandum explaining the clauses of The Finance Bill (No.2), 2009 has clarified that conversion of firm into LLP will not attract any tax.

All the existing partners must be the partners of LLP.

Relevant Provisions:

Chapter X – Section 55 of LLP Act, 2008

Second Schedule of the LLP Act, 2008

Rule 38 of LLP Rules, 2009

Lakhani & Co.

25

Company LLP

Existing Private and Public Limited Company (except Listed Company) can be converted into LLP and all the assets, liabilities and business of existing Company will vest in to LLP.

If the security interest subsists on the assets of the eligible company then it cannot be converted into LLP. Company which has taken secured loan of any nature which is outstanding as on the date of conversion cannot be converted into LLP.

Lakhani & Co.

26

Company LLP

All the existing shareholders must be the partners of LLP as per LLP Act, 2008.

Company which has repaid loans must ensure that the necessary formality of the Companies Act,1956 is complete and the charge is removed.

Relevant Provisions:

Chapter X – Section 56 and 57 of LLP Act, 2008

Third and Fourth Schedule of the LLP Act, 2008

Rule 39 and 40 of LLP Rules, 2009

Lakhani & Co.

Tax issues on conversion of a Company into LLP Reference to Section 47(xiiib): If conditions of Section 47(xiiib) are satisfied then there will not be any

liability for payment of capital gains.

If the conditions stipulated under proviso to Section 47 (xiiib) are not satisfied then as per provisions of Section 47 A (4) will apply and there will be a tax liability for payment of capital gains.

Section 47(xiiib)(e) refers to total sales, turnover or gross receipts in the business of the company in any of the three previous years preceding the previous year in which the conversion takes place and the limit prescribed is Rs.60 lakhs.

If the company receives rent of Rs.100 lakhs in the course of business of letting, which is taxable u/s 22, whether the benefit of Section 47(xiiib) will be applicable?

If the company does not carry on any business but whose gross receipt is more than Rs.60 lakhs, whether the benefit of Section 47(xiiib) will be applicable?

27 Lakhani & Co.

Tax issues on conversion of a Company into LLP

Without reference to Section 47(xiiib): Issue for consideration is whether on conversion of company into LLP -

without taking into consideration the provisions of Section 47(xiiib), there will be any liability for payment of capital gains?

Section 58(4)(b) of LLP Act,2008 provides that on conversion of a company into LLP, “all tangible (movable or immovable) and intangible property vested in the partnership firm or the company, as the case may be, all assets, interests, rights, privileges, liabilities, obligations relating to the partnership firm or the company, as the case may be, and the whole of the undertaking of the firm or the company, as the case may be, shall be transferred to and shall vest in the limited liability partnership without further assurance, act or deed.”

Part IX of the Companies Act,1956 deals with the scenario where certain legal entities can be registered as company under the provisions of the Companies Act, 1956. Sections 565 to 579 deals with this issue.

28 Lakhani & Co.

Tax issues on conversion of a Company into LLP

Without reference to Section 47(xiiib):

Under Section 565 the Government under Press Release dated 5/8/1999 has clarified that the Registrar of Companies will register partnership firms under Part IX of the Companies Act as Joint Stock Companies subject to fulfillment of certain terms & conditions.

Section 575 of the Companies Act, 1956 provides that all property, movable and immovable (including actionable claim), belonging to a firm, shall on such registration pass to and vest in the company.

29 Lakhani & Co.

Tax issues on conversion of a Company into LLP

Without reference to Section 47(xiiib): The Bombay High Court in the case of CIT vs Texspin Engg. & Mfg. Works

reported in 263 ITR pg.345 had occasion to deal with the issue of applicability of provisions of Section 45 of Income Tax Act on conversion of partnership firm into a company. The Hon’ble Bombay High Court has held that the conversion of partnership firm into company under Part IX of the Companies Act,1956 did not attract provisions of Section 45(4) as there is no distribution of capital asset on dissolution and provisions of Section 45(1) also does not apply as the vesting of the properties of the firm in the company was not consequent or incidental to a transfer as contemplated u/s 45(1).

Ratio of Bombay High Court decision will directly apply and there may not be any liability for payment of capital gains de hors the provisions of Section 47(xiiib).

30 Lakhani & Co.

Tax issues on conversion of a Company into LLP

Without reference to Section 47(xiiib):

Umicore Finance Luxembourg, In re – Advance ruling – 189 Taxman 250

Unity care & Health Services – Banglore ITAT 103 ITD – 53

Will Pack Packaging – Ahmedabad ITAT – 78 TTJ (Ahd) – 448

Vali Pattabhirama Rao vs. Shri Ramanuja Ginning & Rice Factory (P) Ltd. (1986) 60 Company Cases 568 (AP) had held that there is no transfer under General Law. No separate conveyance necessary. Section 5 of Transfer of Property Act not applicable.

31 Lakhani & Co.

Tax issues on conversion of a Company into LLP

Carry forward of business loss / unabsorbed depreciation: Carried forward of business losses or unabsorbed depreciation of a

company which is converted into LLP can be carried forward in the hands of LLP and set off against the profit of LLP.

Section 72(6A) – the reference is to satisfaction of conditions u/s 47(xiiib) – benefit of carry forward will only be available if condition of Section 72(6A) are satisfied.

The spirit is that when company is converted to LLP there is no transfer and hence the benefit to the company be permitted in the hands of LLP. Whether a view can be taken that de hors the provisions of Section 47(xiiib), there is no transfer and hence the benefit of carry forward be allowed even if the conditions of Section 47(xiiib) are not satisfied.

32

Lakhani & Co.

Tax issues on conversion of a Company into LLP - Relevant provisions of Income Tax Act No.

Section

Subject

Effective Date

1. Section 32(1) 5th Proviso

Depreciation in the year of conversion prorate allocation between the company and LLP

A.Y. 2011-2012

2. Section 35 DDA (4A)

Amortisation of expenditure incurred on Voluntary Retirement Scheme – LLP eligible to claim deduction for balance period A.Y. 2011-2012

3. Section 43(1) Explanation

13(b)(iii)

Actual cost – where deduction is allowed u/s 35AD – cost will be Nil A.Y. 2011-2012

4. Section 43(6) Explanation 2C

Written down value – w.d.v in the hands of company will be w.d.v. in the hands of LLP A.Y. 2011-2012

5. Section 49(1)(iii)(e) Cost to previous owner – cost in the hands of LLP will be cost in the hands of company. A.Y 1999-2000

6. Section 49 (2AAA) Rights of partner in LLP – Cost of acquisition A.Y. 2011-2012

7. Section 72A (6A) Carry forward of business loss and unabsorbed depreciation A.Y. 2011-2012

8. Section 115JAAA(7) Carry forward of MAT credit of Company not available to LLP A.Y. 2011-2012

33

In all the Sections there is reference to provisions of Section 47(xiiib). If the exemption is not available u/s 47(xiiib) or assessee opts not to avail exemption u/s 47(xiiib), whether the benefit of above provisions will be applicable ?

Lakhani & Co.

34

LLP Company

LLP can be converted into a company, however there is no provision under LLP Act, 2008, for such conversion.

FAQ on LLP clarifies that enabling provisions would be required to be made in the Companies Act, 1956 for such conversion.

Issue for consideration is whether LLP can be converted into a Company under Part-IX of the Companies Act,1956 ?

Lakhani & Co.

Chartered Accountant in Practice - LLP

Practicing C.A. can from a new LLP or convert existing Partnership Firm

into LLP.

Section 2(2) of the Chartered Accountants Act, 1949 defines a member in practice.

A member can practice in partnership with other Chartered Accountants in practice.

The word ‘partnership’ is not defined under the Chartered Accountants Act, 1949.

35

Lakhani & Co.

Chartered Accountant in Practice - LLP

GOI – Ministry of Corporate Affairs have issued Circular No.10/2011 dated 4/4/2011 clarifying that word partnership is Section 2(2) will include LLP where other partners of LLP are individuals.

GOI – Ministry of Corporate Affairs have issued Notification No. S.O.190(E) dated 30/1/2012 notifying the effective date for amendments made by the Chartered Accountants (Amendment) Act, 2011. The effective date is 1/2/2012.

36 Lakhani & Co.

Chartered Accountant in Practice - LLP

Section 226(3)(a) of the Companies Act, 1956, provides that a body

corporate will not qualify for appointment as Auditor of a company. LLP being a body corporate would not have qualified to become the Auditor of a Company. The Ministry of Corporate Affairs have issued clarification vide General Circular No. 30A/2011 on 26/05/2011 that LLP of Chartered Accountants will not be treated as body corporate for the limited purpose of Section 226(3)(a) of the Companies Act,1956.

For converting existing C.A. firm into LLP the relevant provisions are :

■ Chapter X – Section 55 of LLP Act, 2008

■ Second Schedule of LLP Act, 2008

■ Rule 38 of LLP Rules, 2009

37 Lakhani & Co.

Chartered Accountant in Practice - LLP

The provisions of Chartered Accountants Act, 1949, Chartered Accountant

Regulations 1988, and code of Ethics issued by ICAI, shall be applicable to all the partners of LLP jointly and severally.

Issue not yet resolved is with ref. to Section 224 of Companies Act, 1956. Eg. At AGM C.A. firm is appointed as Statutory Auditors. This C.A. firm is converted in to LLP during the year. Whether the appointment will be valid for LLP or there will be casual vacancy and the new appointment will have to be made.

38 Lakhani & Co.

39

Statutory Compliances

Under LLP Act, 2008 every LLP has to file annual return giving the complete details of the name and address of the partners, designated partners, business activities, contribution received and other information as may be specified from time to time.

Under LLP Act, 2008 LLP has to file once in a year a statement of account and solvency declaration. The statement of accounts are to be prepared as per Schedule VI of the Companies Act, 1956. The solvency declaration gives the details of the particulars of the charges created, modified or satisfied during the financial year.

Lakhani & Co.

40

Audit of Accounts Accounts of LLP have to be audited annually as per the provisions of LLP

Act, 2008.

LLP carrying on business or profession and whose turnover does not exceed Rs.40 lakhs is not required to get its accounts audited under LLP Act, 2008 or LLP where partners contribution does not exceed Rs.25 lakhs is not required to get its accounts audited under LLP Act, 2008. If either of the conditions are satisfied the audit of accounts is compulsory.

LLP carrying on business and having gross turnover, receipts or sales exceeding Rs.100 lakhs or more and LLP carrying on profession and having gross receipts of Rs.25 lakhs or more is required to get accounts audited u/s 44AB of Income-tax Act,1961.

Lakhani & Co.

41

Compromise and Arrangement

Under the LLP Act, 2008 there are procedures and formalities for compromise and arrangement :-

between LLP and creditors.

between LLP and its partners.

Lakhani & Co.

42

Merger & Demerger Amalgamation/Reconstruction of LLP is possible and an application has to

be made to the Competent Court.

Under Amalgamation/Merger the assets and liabilities of one LLP can be transferred to another LLP.

Under Demerger part assets and liabilities of one LLP can be transferred to another LLP.

Whether LLP can be merged with the corporate body under the scheme of merger u/s 391 / 394 of the Companies Act,1956 ?

Lakhani & Co.

43

Dissolution of LLP As per the terms of LLP agreement, LLP can be dissolved by executing

dissolution deed.

The net assets of the LLP can be distributed amongst the partners in a manner specified under LLP agreement.

The return of capital in the hands of partners till the date of dissolution will not attract any tax liability.

The distribution of share of profit upto date of dissolution by LLP to partners will not attract any tax liability.

If LLP distributes any other amount over & above the original capital and share of profit for the year till dissolution then the tax issues may arise depending upon the nature of the distribution and the character of amount being received by each partner. Provisions of Section 45(4) and the ratio of decision in the case of A.L.A. Firm 189 ITR pg.285 (SC) is to be considered.

Lakhani & Co.

44

Winding up of LLP LLP can be wound up when a resolution is passed at the General Meeting

of the partners and 3/4th majority of the partners approve the winding up of LLP.

The competent Court has power to pass the necessary orders based on the application made by LLP for winding up.

The consent of the lenders and creditors will be necessary before the Court passes an order for winding up of the LLP.

The creditors also have power to make an application for winding up of LLP if 2/3rd in value of the creditors establish that LLP is not in a position to pay the debts to the creditors.

Lakhani & Co.

LLP – FEMA Provisions

Inbound Investments:

Foreign Direct Investments (FDI) in India is subject to FEMA Regulations.

Government has liberalized the policy and has permitted Foreign Direct Investment ranging from 26% to 100% under automatic route, subject to certain terms and conditions, provided the investee entity is an Indian company.

Status of LLP is that of corporate body, but FDI in LLP under automatic route is not permitted.

In April 2012, the GOI has announced FDI policy and Guidelines for FDI in LLP.

FDI will be allowed, through Government approval route only in LLP. FDI is permitted in sectors/activities where 100% FDI is allowed through the automatic route and there are no FDI linked performance conditions. (Such as for NBFC or for Development of Township activity).

45 Lakhani & Co.

LLP – FEMA Provisions

Inbound Investments:

LLP with FDI will not be allowed to operate in agricultural, plantation,

print media or real estate business.

An Indian company, having FDI will be permitted to make down stream investments in an LLP only if both the company and LLP are operating in sectors where 100% FDI is allowed through the automatic route and there are no FDI linked performance conditions.

LLP with FDI will not be eligible to make any downstream investments.

Foreign capital participation in LLPs will be allowed only by way of cash consideration received by inward remittance, through normal banking channels or by debit to NRE / FCNR account of the persons concerned, maintained with an authorized dealer / authorized bank.

46 Lakhani & Co.

LLP – FEMA Provisions

Inbound Investments:

Foreign Institutional Investors (FIIs) and Foreign Venture Capital Investors

(FVCIs) can not make investments in LLP.

LLPs are not permitted to avail External Commercial Borrowing (ECB).

Only company registered in India under the provisions of the Companies Act, 1956 can nominate a designated partner in LLPs having FDI. No other entity such as Foreign LLP or Trust can nominate designated partner.

LLPs with FDI, can appoint the designated partner who should be:

(i) Person resident in India as per defined in Explanation to Section 7(1) of LLP Act, 2008.

and

(ii) Person residing in India as per provisions of Section 2(v)(1) of the Foreign Exchange Management Act, 1999.

47 Lakhani & Co.

LLP – FEMA Provisions

Inbound Investments:

The designated partner of LLP with FDI will be responsible for compliance

with all the conditions and also shall be responsible for all the penalties imposed on the LLP for their contravention, if any.

Conversion of company with FDI into LLP, will be allowed only if the above stipulations are met and with prior approval of FIBP/Government.

48 Lakhani & Co.

LLP – FEMA Provisions

Outbound Investments:

Indian Company can make Overseas Direct Investments in Joint Venture

(JV)/wholly owned subsidy (WOS) abroad upto 4 times its net worth subject to certain conditions of carrying on business activities, under automatic route.

Partnership firms, are allowed to invest outside India under automatic route.

The status of LLP is equal to partnership, however LLP is not permitted to make investments under automatic route.

LLP can make investments with prior approval of RBI. No guidelines are framed so far.

49 Lakhani & Co.

LLP – FEMA Provisions

Issues:

Whether LLP having exports of goods/services will only be permitted to

make outbound investments?

Existing Companies which have made outbound investments under automatic route whether can be converted into LLP? If yes with the RBI permission or without RBI permission?

LLP is not permitted to carry out NBFC activities. Whether only investments in JV/WOS will be permitted when :

(i) JV/WOS is carrying on the business activity outside India

(ii) JV/WOS is only investment company, which has made down stream investments in other business entities outside India.

50

Lakhani & Co.

Stamp Duty Implications Company having immovable property when converted into LLP, whether

there is liability for payment of stamp duty ?

As per Section 58 of LLP Act, 2008, all the assets and liabilities vest into LLP. There is no transfer of assets and liabilities.

As per decision of Bombay High Court in the case of Taxpin Engg.& Mfg. Works and A.P. High Court in the case of Vali Pattabhirama Rao vs. Shri Ramanuja Ginning & Rice Factory (P) Ltd. when the firm is converted into company under Part IX of Companies Act, 1956, the assets of the firm vest into the company and there is no transfer. Whether the ratio of these decisions can be applied on the issue of payment of stamp duty ?

If LLP does not pay stamp duty and continues to enjoy the property being registered in the name of company, can the title of the property be considered as defective ? Whether at the time of sale of such property any issue can arise ?

51

Lakhani & Co.

52

Thank You

Lakhani & Co.