Embed Size (px)

Citation preview

LHN Limited

Initiating coverage 18 February 2016

Overweight

Current Price S$0.128 Fair Value S$0.225 Up / (downside) 75.8%

Stock Statistics

Market cap S$46.3m

52-low S$0.125 52-high S$0.260

Avg daily vol 918,760

No of share 361.52m

Free float 23.93%

Key Indicators

ROE 16F 10.5%

ROA 16F 5.7%

P/BV 0.81

Net gearing Net cash

Major Shareholders

Hean Nerng Group 76.1%

Kelvin Lim 76.1% Jess Lim 76.1%

Historical Chart

Source: Bloomberg

In the Business of Creating Value

Improving occupancy at new leases to drive grow. LHN Limited is a property services company specializing in revitalizing industrial and commercial properties by maximizing net lettable area and optimizing tenant and usage mix. We initiate coverage on LHN as we expect LHN’s performance to improve in 2016, in the absence of one-off costs incurred in 2015, and as a result of higher occupancy at new leases secured over the past year. At new master lease 18 Tampines Industrial Crescent, occupancy has increased from over 75% to near 90% over the last two to three months.

Space Optimisation to potentially double earnings. Assuming that LHN grows its portfolio by 0.5m sq. ft. or 11%, we forecast that net profit attributable to shareholders may grow by 44% to S$6.09m in FY16. However, this does not include any fair value gains from investment properties. LHN is in the midst of re-designing 100 Eunos Ave 7 (acquired in August 2015 at S$12.85m) to increase its gross floor area by 50%, which justifies S$3m to S$5m of upside from this asset alone. Currently, LHN is acquiring 38 Ang Mo Kio Industrial Park 2, which will likely provide similar or more upside when revalued at the end of the financial year.

Opportunity to grow exponentially over the next two years. We are mindful that industrial rentals fell by 2.1% in 2015. However, LHN leases most of its properties from owners. The situation is actually an opportunity for LHN to secure new (and renew existing) master leases at lower rental rates and rapidly grow its portfolio over the next two years. More recently, LHN has been taking advantage of its post-IPO balance sheet to acquire selected properties with Space Optimisation upside potential. We expect these investments to help save on leasing costs and maintain margins.

New businesses bring fresh twist to Space Optimisation. In recent years, LHN has started providing serviced office/SOHO (GreenHub) and warehousing/self-storage (Work+Store) services. GreenHub’s revenue has exceeded S$1.0m/year and it is now available in six locations in Singapore, Indonesia and Myanmar. GreenHub and Work+Store further improves space efficiency via sharing arrangements. As they are more cost effective than renting a full office unit and traditional rent-a-unit self-storage solutions, these businesses have the potential to raise LHN’s growth profile in the long term. Over time, there is the potential for them to be spin-off, given their separate branding and service profiles.

Undemanding valuation. LHN currently trades at 0.81x P/BV and has net cash of 1.6 cents per share, equivalent to about 13% of its share price. We value the company at S$0.225 per share, translating to FY16 P/E of 13.3x and FY16 P/B of 1.34x, supported by high projected earnings growth of 44% in FY16 and 21% over the forecast horizon of up FY20.

Liu Jinshu

(+65) 6236-6887 [email protected] www.nracapital.com

Key Financial Data

(S$ m, FYE Sep) 2014 2015 2016F 2017F 2018F

Sales 90.7 96.4 106.0 116.6 122.4

Gross Profit 25.0 23.4 26.5 29.2 30.6

Net Profit 12.8 4.2 6.1 7.9 8.8

EPS (cents) 3.5 1.3 1.7 2.2 2.4

EPS grow th (%) 54.8 (62.0) 25.6 30.6 10.9

PER (x ) 3.6 9.6 7.6 5.8 5.3

NAV/share (cents) 9.1 15.3 16.7 18.4 20.4

DPS (cents) NA 0.3 0.3 0.4 0.5

Div Yield (%) NA 2.3 2.6 3.4 3.5

Source: NRA Capital forecasts

0.08

0.14

0.20

0.26

0

10

20

04/15 06/15 08/15 10/15 12/15

page 2

LHN Limited

Company Background

Key Competency in Space Management. LHN Limited (LHN) is a professional real estate management services group with a portfolio of 38 leased and owned commercial, industrial and residential properties in Singapore, Indonesia and Myanmar. These properties cover a total net lettable area of over 4.5m sq. ft. with average occupancy rate of over 90%, as of February 2016.

For the financial year ended September 2015, the group generated total revenue of about S$96.4m. The key Space Optimisation segment (the company’s real estate management and leasing business) contributed 75% or S$71.95m of revenue. The Facilities Management business provides general maintenance, car park management and other services for properties owned and leased by the group and external properties. This business contributed 10% or S$9.75m of revenue in FY15.

The Logistics Services business provides transportation services, and management services for container depots. Transportation services pertain to the transport of chemicals, bitumen and related products between refineries, storage and retail locations of clients. This segment generated about 15% or S$14.67m of revenue last financial year.

Figure 1: Revenue Mix – Delivering Annual Growth

Source: Company, NRA Capital

Figure 2: Revenue Mix of Space Optimisation Business

Source: Company, NRA Capital

64.06 66.76 70.56 71.95

8.66 10.92 11.70 14.672.406.06 8.48 9.75

0.00

40.00

80.00

120.00

2012 2013 2014 2015

S$m

Space Optimisation Logisitics Facilities Support

29.7839.14 40.48 45.86

15.70

18.82 21.2023.4518.58

8.818.88

2.64

0.00

40.00

80.00

2012 2013 2014 2015

S$m

Industrial Commercial Residential

page 3

LHN Limited

Cross synergies between business segments. The Space Optimisation and Facilities Management businesses are integrated and highly complementary. Intuitively, the insourcing of facilities management activities allows for margin capture and better understanding and management of the group’s properties. The Logistics Services and Space Optimisation businesses are related as they share common customers who lease industrial space from the group and uses its transportation services. To this extent, both the logistics and space optimisation businesses allows the group to provide a one-stop solution for customers.

Supported by decades of experience. LHN’s scale and capabilities today is partially due to its long operating history, which facilitated the accumulation of network and experience. LHN was founded in 1991 by Mr. Lim Hean Nerng who has since retired. His children Mr. Kelvin Lim (Executive Chairman and Group Managing Director) and Ms. Jess Lim (Executive Director and Group Deputy Managing Director) joined the firm in 1997 and 2002 respectively.

Figure 3: History

1991 Started leasing out part of space in family-owned factory to tenants 1998 - 2006 Acquired new master leases. Diversified by leasing out space to other industrial tenants

2003 Started logistics business – prov iding base oil and bitumen transportation serv ices for oil majors 2005 Ex panded logistics services to include container trucking

2005 Started facilities management business, beginning w ith security services

2006 Started to renovate and refurbish properties before leasing them out 2007 Secured master lease of first commercial property 2007 Facilities management ex panded into v ehicle car park management

2009 Ex panded logistics services to include ISO tank trucking 2012 Launched GreenHub brand of suited offices 2013 Started container depot management

2013 Acquires 68,000 sq ft industrial property

2013 Ex panded GreenHub to Jakarta, Indonesia

Apr-15 Listing on SGX Catalist May -15 Added one more container depot in Laem Chabang, Thailand May -15 Ex panded GreenHub to Yangon, Myanmar w ith first GreenHub branded SOHO serv iced residence Nov -15 Opened second GreenHub serv iced office in Indonesia

Source: Company, NRA Capital

Figure 4: Shareholding Structure

HN Capital Ltd.’s ultimate parent is a trust w hose beneficiaries are Mr. Lim Hean Nerng, his spouse Foo Siau Foon, Kelv in Lim and Kelv in Lim’s direct lineal issues.

Source: Company, NRA Capital

Acquires new

capabilities and expands into adjacent businesses

Commences regional

expansion

page 4

LHN Limited

Space Optimisation – A Key Value Creator

We highlight LHN’s Space Optimisation expertise as a key value creator. While the model of leasing and subletting properties is common, LHN’s ability to expand and grow the net lettable area of its properties deserves further thought. Essentially, a higher net lettable area reduces the average lease cost of a property and allows LHN to raise its margin.

Revitalising under-utilised properties. The company is able to increase the net lettable area (NLA) of its properties by focusing on old and under -utilised properties whose net lettable area can be maximized via re-design and addition & alteration (A&A) work. In fact, LHN’s willingness to invest in its leased properties also increases the company’s attractiveness when tendering for master leases, as owners will want to work with partners that can add value.

Enhance own property value. More importantly, LHN has recently started to selectively acquire its own investment properties. By expanding the net lettable area of its own properties, the company would be able to raise the value of its investment properties and generate positive fair value gains to enhance recurring income. For instance, LHN acquired 72 Eunos Ave 7 in FY13, and subsequently increased its net lettable area from 45,000 sq. ft. to 51,000 sq. ft . (+13.3%). In FY14, the property was revalued from S$13.4m to S$20.0m (including additional PPE costs) and the company recognized a fair value gain of S$5.8m in FY14 on its portfolio of investment properties.

Figure 5: Change in NLA for Selected Properties after Space Optimisation

10-40 Tuas South Street 1 is not show n. *72 Eunos Ave 7 and 100 Eunos Av e 7 are ow ned by the group. For 100 Eunos Av e 7, only gross floor area is av ailable and the change of 50% is an estimate only – A&A w ork is in progress.

Before After Change % 10 Raeburn Park 115,000 130,000 15,000 13.0%

43 Keppel Road 75,000 111,000 36,000 48.0% 2 Soon Wing Road 76,000 85,000 9,000 11.8%

27 West Coast Highw ay 49,000 54,000 5,000 10.2% 10-40 Tuas South Street 1 850,000 896,000 46,000 5.4%

72 Eunos Av e 7 45,000 51,000 6,000 13.3% 100 Eunos Av e 7 – gross floor area 45,500 68,250 (est.) 22,750 (est.) 50.0%

aa

Source: Company, NRA Capital

13.0%

48.0%

11.8%

10.2% 13.3%50.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

10 RaeburnPark

43 KeppelRoad

2 Soon WingRoad

27 WestCoast

Highway

72 EunosAve 7*

100 EunosAve 7*

sq. ft.

Before After

page 5

LHN Limited

Changing Landscape Creates Demand for Third Party Managers

Steadily more multiple-user factories. The proportion of multi-user factories in Singapore grew from 22.5% of total industrial gross floor area in 2011 to 23.3% in 2015. In terms of floor area, multiple-user factories expanded by 1.7m square metres (sqm) during the same period, growing at a rate of 4.6% CAGR over a four-year period. In land scarce Singapore, we can expect more high-rise multiple-user industrial space to be built, as opposed to single-use factories, in order to conserve land. We highlight this point, as these multi-tenanted buildings demonstrate the relevance of professional management services companies such as LHN to plan and provide services for the betterment of the tenants and the property owner.

More financial investors are developing industrial properties. In 2015, public sector industrial projects accounted for only 3.2% or 54,400 sqm of completed industrial space built by 52 developers. We scanned through the list of completed properties and reckon that less than half of them were for own use. The large number of developers with financial rather than utility interests is interesting, as not all developers will have their own property and facilities management companies, especially for financial investors who are vested for opportunistic reasons. Even among industrial properties developed for own use, we have noticed that some companies will allocate a portion of their properties for rent to external users – the space they need may be less than the maximum achievable gross floor area.

How LHN helps property owners. The prevalence of small-scale property investors presents a market space for professional real estate management companies. LHN has the advantage of its wide network of 700+ tenants, readily available facilities management capabilities, and economies of scale – accumulated via its portfolio of 38 properties and 25 years of experience. Property owners are less likely to set up their own real estate and facilities management teams if companies like LHN are able to present more cost effective and efficient solutions. Secondly, the overall value of the property can be enhanced if LHN is able to secure the master lease, optimise the space and sublet to tenants at higher rates.

Figure 5: Value Proposition of LHN’s Space Optimisation Business

Source: Company FY15 results presentation slide 8

page 6

LHN Limited

Figure 6: Stock of Multiple-User Factories (m sqm)

Source: JTC, NRA Capital

Figure 7: Multiple-User Factories (% of Total Industrial Stock in GFA)

Source: JTC, NRA Capital

Figure 8: Industrial GFA Completed in 2015

Public sector projects refers to GFA completed by for instance JTC.

Source: JTC, NRA Capital

8.659.02

9.36

9.89

10.34

7.00

8.00

9.00

10.00

11.00

2011 2012 2013 2014 2015

million sqm

22.5%

22.9% 22.9%

23.1%

23.3%

22.0%

22.5%

23.0%

23.5%

2011 2012 2013 2014 2015

Public; 54,400 sqm;

3%

Priv ate; 1,671,500 sqm;

97%

page 7

LHN Limited

In Sweet Spot to Capitalize on Current Market Conditions

Industrial rental rates have been falling…We are mindful that industrial rent has been falling. The quarterly rental index for all industrial spaces, compiled by the JTC, fell from 102.8 in 4Q14 to 100.6 in 4Q15. Vacancy rate has in turn increased from 9.1% to 9.4% during the same period with 4.19m sqm of vacant space across all categories as of end 2015. Based on the list of major industrial projects in the pipeline as at end 4Q 2015 compiled by JTC, at least 1.3m sqm and up to 2.9m sqm of industrial property will be completed in 2016.

Figure 9: Rental Index of Industrial Properties

Source: JTC, NRA Capital

Figure 10: Major Industrial Projects in the Pipeline (as at End 4Q15)

Source: JTC, NRA Capital

Asset light strategy: Key for LHN is the spread between rental costs and income, NOT topline rental rates! However, we emphasize that LHN employs an asset light strategy with very few selected property acquisitions that provide high Space Optimisation potential. Of its 38 properties, the group only owns four of them, representing about 3% of gross floor area, and leases the remaining 34 of them. The bulk of LHN’s income is still earned from properties under master leases with the owner! This is a key point, as rental rates are important to property owners who require a return in excess of their cost of capital. For management services companies such as LHN, the key lies with how it can widen the spread between the rental costs that it pays to the owner and the rental income it receives from individual tenants.

100.4 100.3

104.7 105 105.3 105.3

103.4102.8 103.2

102.5101.7

100.6

96

99

102

105

108

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15

1.05

0.19 0.18 0.04

0.81

0.16

0.250.11

0.33

0.00

0.50

1.00

1.50

2016 2017 2018 2020 No TimelineProvided

Mill

ions

Sqm

Private Public

page 8

LHN Limited

Expertise driven business in the long run…In the long run, the width of LHN’s spread is driven by its ability to optimize its properties’ efficiency (in terms of maximization of net lettable area), use (mix of space allocated to retail, storage and factory purposes) and tenant mix. In the long term, changes in rental rates due to structural reasons such as imbalances in demand and supply are passed on to the owners via the master lease agreements.

Portfolio approach to buffer against short-term fluctuations in rental rates. Moreover, LHN maintains a portfolio of leases of various durations. Its industrial properties typically have leases of two to 15 years, while its commercial properties are on leases of two to six years. Between LHN and its tenants, the rental agreement terms are typically for up to three years. Hence, LHN will face lower margins at properties with lower rental rates amidst fixed lease costs, but will also benefit from lower costs from head leases due for renewal. Therefore, careful duration matching by having the same amount of floor area of leases and rental contracts maturing in the same period can help the company to reduce margin risk.

However, current market conditions offer tactical opportunity to widen medium term spreads. On the other hand, we argue that LHN is in a position to take advantage of the current downturn to enhance its medium term growth potential. This is because rising vacancies and falling rental rates have raised the bargaining power of LHN to acquire new leases at low rates or new properties at attractive valuations. By locking in a portfolio of low cost leases and properties, LHN will be able to widen its spread when rental rates recover.

In fact, we argue that the recent acquisition of its own properties should help the company to maintain its margins, with the company already showing an improvement in gross margin in its 1Q16 results.

Figure 11: LHN’s Asset Light Strategy Reduces Risk to Rental Rates

Source: NRA Capital

page 9

LHN Limited

Growing Portfolio of Leases to Provide Larger Revenue Base

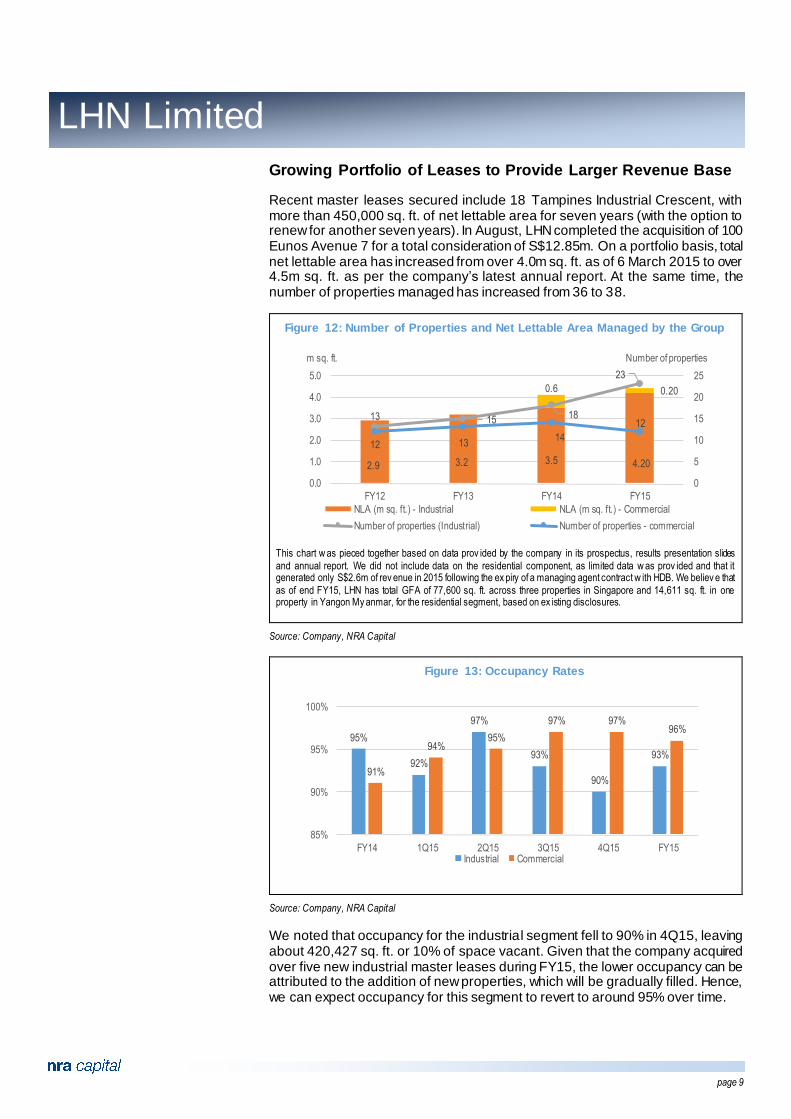

Recent master leases secured include 18 Tampines Industrial Crescent, with more than 450,000 sq. ft. of net lettable area for seven years (with the option to renew for another seven years). In August, LHN completed the acquisition of 100 Eunos Avenue 7 for a total consideration of S$12.85m. On a portfolio basis, total net lettable area has increased from over 4.0m sq. ft. as of 6 March 2015 to over 4.5m sq. ft. as per the company’s latest annual report. At the same time, the number of properties managed has increased from 36 to 38.

Figure 12: Number of Properties and Net Lettable Area Managed by the Group

This chart w as pieced together based on data prov ided by the company in its prospectus, results presentation slides

and annual report. We did not include data on the residential component, as limited data w as prov ided and that it generated only S$2.6m of rev enue in 2015 following the ex piry of a managing agent contract w ith HDB. We believ e that

as of end FY15, LHN has total GFA of 77,600 sq. ft. across three properties in Singapore and 14,611 sq. ft. in one property in Yangon My anmar, for the residential segment, based on ex isting disclosures.

Source: Company, NRA Capital

Figure 13: Occupancy Rates

Source: Company, NRA Capital

We noted that occupancy for the industrial segment fell to 90% in 4Q15, leaving about 420,427 sq. ft. or 10% of space vacant. Given that the company acquired over five new industrial master leases during FY15, the lower occupancy can be attributed to the addition of new properties, which will be gradually filled. Hence, we can expect occupancy for this segment to revert to around 95% over time.

2.9 3.2 3.5 4.20

0.6 0.20

13 15 18

23

12 1314

12

0

5

10

15

20

25

0.0

1.0

2.0

3.0

4.0

5.0

FY12 FY13 FY14 FY15

Number of propertiesm sq. ft.

NLA (m sq. ft.) - Industrial NLA (m sq. ft.) - Commercial

Number of properties (Industrial) Number of properties - commercial

95%

92%

97%

93%

90%

93%

91%

94%95%

97% 97%96%

85%

90%

95%

100%

FY14 1Q15 2Q15 3Q15 4Q15 FY15Industrial Commercial

page 10

LHN Limited

Portfolio GFA to grow by 341,000 sq. ft. or 7.5% with new acquisition. The number of properties managed should increase when the acquisition of 38 Ang Mo Kio Industrial Park 2 is completed in the next few months. As announced in December 2015, LHN has entered into a 50/50 joint venture to acquire the property for a total consideration of S$30m. As of February, the joint venture has received in-principle no objection from HDB to purchase the property.

The property, comprising of three buildings and one annexe, has an approximate gross floor area of 341,000 sq. ft., of which up to 30% may be sublet to tenants based on our understanding of current regulations. The remaining space of about 240,000 sq. ft. will be used for self-storage and last mile logistics, including space for the Work+Store business. Although LHN will only own 50% of the property, it will continue to fully manage and run the property in accordance to the joint venture agreement, and earn both rental and service income from 38 Ang Mo Kio Industrial Park 2. Based on the company’s behaviour in the past, some A&A work will likely be done on the property over the next two to six months. Overall, we are likely to see this property commence contribution towards the company in FY16.

Getting good value from 38 Ang Mo Kio Industrial Park 2. 38 Ang Mo Kio Industrial Park 2 is located next to Techplace II along Ang Mo Kio Ave 5. As Techplace II is owned by Ascendas REIT, we are able to derive that Techplace II was valued at S$154.7 per sq. ft. (psf) of gross floor area as of 31 March 2015. In comparison, LHN is acquiring 38 Ang Mo Kio Industrial Park 2 for S$87.8 psf.

The difference in price is partially due to their remaining lease tenure. Techplace II has a remaining tenure of 36 years, compared to 25 years for 38 Ang Mo Kio Industrial Park 2. Adjusting for the shorter lease life, we would still expect 38 Ang Mo Kio to generate some fair value gains for LHN. We understand that the existing owner Renesas Semiconductor Singapore Pte Ltd has previously put the property up for sale in May 2015. LHN and its joint venture partner are likely able to extract good value from this property due to Renesas probably having to exit its operation at this site within a set schedule.

Figure 14: 38 Ang Mo Kio Industrial Park 2 (red outline)

GFA (sq ft) S$m S$psf Remaining

Lease

Techplace II 1,239,592 191.8* 154.7 36 y ears 38 Ang Mo Kio Industrial Park 2 341,539 30** 87.8 25 years

*Valuation as of 31 March 2015 **Purchase consideration

Source: URA, Ascendas REIT website, NRA Capital

page 11

LHN Limited

Expansion into Downstream Businesses

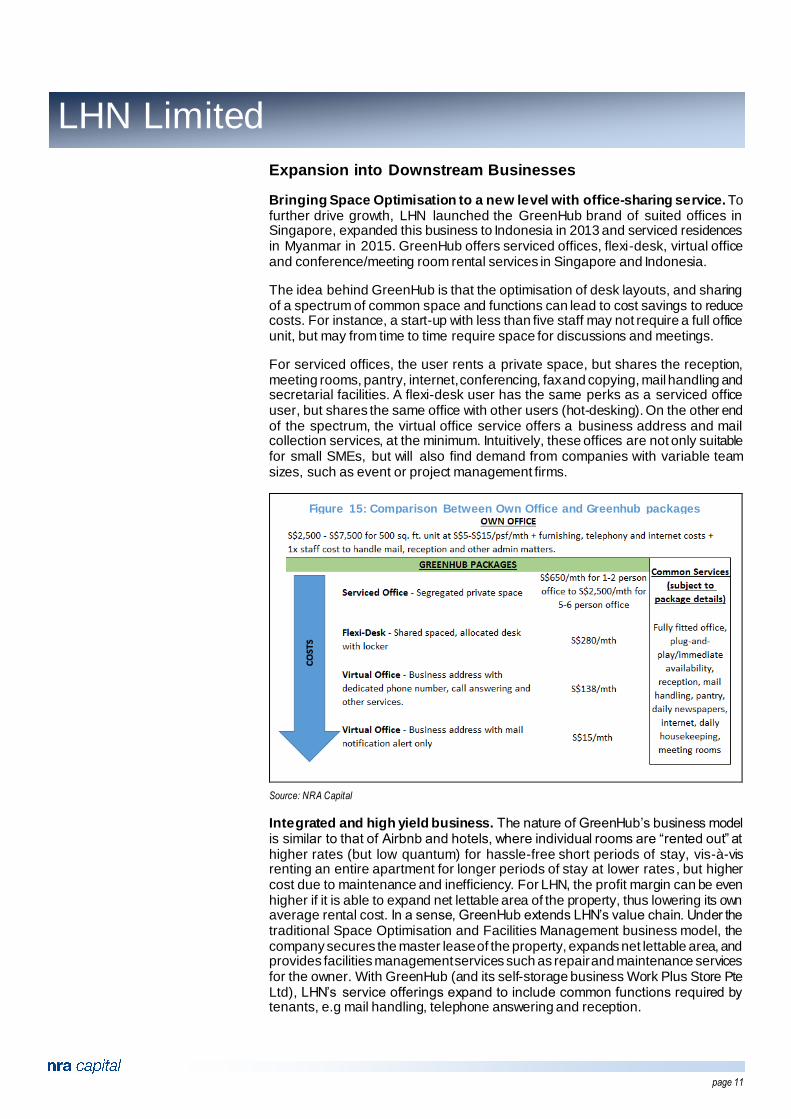

Bringing Space Optimisation to a new level with office-sharing service. To further drive growth, LHN launched the GreenHub brand of suited offices in Singapore, expanded this business to Indonesia in 2013 and serviced residences in Myanmar in 2015. GreenHub offers serviced offices, flexi-desk, virtual office and conference/meeting room rental services in Singapore and Indonesia.

The idea behind GreenHub is that the optimisation of desk layouts, and sharing of a spectrum of common space and functions can lead to cost savings to reduce costs. For instance, a start-up with less than five staff may not require a full office unit, but may from time to time require space for discussions and meetings.

For serviced offices, the user rents a private space, but shares the reception, meeting rooms, pantry, internet, conferencing, fax and copying, mail handling and secretarial facilities. A flexi-desk user has the same perks as a serviced office user, but shares the same office with other users (hot-desking). On the other end of the spectrum, the virtual office service offers a business address and mail collection services, at the minimum. Intuitively, these offices are not only suitable for small SMEs, but will also find demand from companies with variable team sizes, such as event or project management firms.

Figure 15: Comparison Between Own Office and Greenhub packages

Source: NRA Capital

Integrated and high yield business. The nature of GreenHub’s business model is similar to that of Airbnb and hotels, where individual rooms are “rented out” at higher rates (but low quantum) for hassle-free short periods of stay, vis-à-vis renting an entire apartment for longer periods of stay at lower rates, but higher cost due to maintenance and inefficiency. For LHN, the profit margin can be even higher if it is able to expand net lettable area of the property, thus lowering its own average rental cost. In a sense, GreenHub extends LHN’s value chain. Under the traditional Space Optimisation and Facilities Management business model, the company secures the master lease of the property, expands net lettable area, and provides facilities management services such as repair and maintenance services for the owner. With GreenHub (and its self-storage business Work Plus Store Pte Ltd), LHN’s service offerings expand to include common functions required by tenants, e.g mail handling, telephone answering and reception.

page 12

LHN Limited

Office rental rates range from around S$3.50-S$4.00 per sq. ft. for a 500 sq. ft. to 600 sq. ft. unit in Paya Lebar to up to S$15.00 per sq. ft. in the city centre area. Hence, renting a full office unit will incur at least S$1,750 to S$9,000 in rental cost on a monthly basis, not to mention furnishing costs. On the other hand, SMEs can rent fully furnished serviced office space for five to six persons at just S$2,000 per month from GreenHub.

Figure 16: GreenHub Increases Business Integration

Source: NRA Capital

Growth has been impressive. LHN only started GreenHub in FY12, which generated S$0.4m of revenue in FY13 and S$1.4m of revenue in FY14. The company did not disclose its revenue from GreenHub in FY15, but added two new locations during FY15. Workstations in Jakarta, Indonesia were nearly doubled with a second location of 13,200 sq. ft. and the company entered the Myanmar market with the SOHO concept, comprising of 20 one-and three bedroom units, and 28 capsule concept units.

Figure 17: GreenHub Locations

Location Net Lettable Area (sq ft) No of workstations Remarks

Singapore

10 Raeburn Park 3,980 406

27 West Coast Highw ay 16,087

Phoenix Park 4,668

Indonesia

88 Kota Kasablanka 18,500 246 Added in 2013 Plaza Marein, Jalan

Jenderal Sudirman 13,200 198

Added in 2015

Myanmar

85 SOHO, 85 Boy ar Ny unt Street

14,600

20 one-bedroom and

three-bedroom units and 28 capsule

concept units.

Added in May 2015

Source: Company, NRA Capital

Occupancy seems to be quite decent. We estimate that 27 West Coast Highway most likely has about 240 workstations, of which about 8% is available for rent, based on GreenHub’s website as of end January. The remaining workstations are occupied.

page 13

LHN Limited

Work+Store - the next lap solution for industrial Space Optimisation. Work +Store is a new business by LHN that provides inventory/warehousing solutions for small businesses and start-ups and valet self-storage services for consumers, thus complementing GreenHub’s suited office/SOHO services. Whereas the conventional self-storage unit is designed such that it is neutral to business and consumer users, Work+Store’s concept units are highly targeted towards the needs of small business users, especially e-commerce setups.

Other than servicing small businesses, Work+Store also provides valet self-storage services for consumers to put away their belongings, without having to even lease any storage unit, for a low monthly fee of at least S$12/box/month. This form of self-storage is very space efficient as items are stored in standard sized storage boxes that can be stacked away. Hence, Work+Store offers two well differentiated services designed for different users.

Currently, Work+Store is available at three locations 680 Upper Thomson Road, 18 New Industrial Road and 18 Tampines Industrial Crescent (at least 10,000 sq. ft. each). Given that 100 Eunos Ave 7 and 38 Ang Mo Kio Industrial Park 2 are acquired under Work Plus Store Pte Ltd a wholly owned subsidiary of LHN, Work+Store seems to be showing some business momentum and will likely expand to these two locations as well.

Figure 18: The Work Plus Store Business Model

Source: Company

Business users

Consumers

page 14

LHN Limited

Car Park Management and Logistics Services to Provide Opportunistic Growth

Has scale and established systems in the car park management business. Other than managing the parking lots in its properties, LHN also manages car parks of government bodies and private enterprises, as part of its Facilities Management business. The interesting part of this business is that LHN has a management system in place to monitor its car parks remotely using technology – thus offering a low cost solution to clients. As of March 2015, LHN managed some 4,958 car parking lots over 26 car parks, of which 17 of them are located in the central area. Within six months (end September 2015), the company has expanded its portfolio to manage over 5,400 parking lots. Hence, the company has demonstrated some growth in this business within a short period of time.

New container depot in Thailand to provide additional revenue for logistics business. LHN’s Logistics Services Business is supported by over 35 prime movers, over 10 road tankers and over 110 trailers to provide transportation services for clients. The company started providing container depot management services at 27 Benoi Sector in 2013, pursuant to a service agreement with Keppel Logistics Pte Ltd. Essentially, LHN runs the depot and provides container surveying and maintenance services. Such maintenance services include repair, cleaning and storage of general purpose and refrigerated containers.

Key business merits include fast turnaround time for repairs. The fastest was two days for shipping operators. Container survey/inspection services are performed by an inspection team certified by the Institute of International Container Lessors (IICL). There are less than 20 IICL certified inspectors in Singapore – presenting a barrier of entry for competitors.

The 230,000 sq ft depot in Singapore is able to handle 6,200 TEUs. In May 2015, LHN added a second container depot to its portfolio, in Laem Chabang, Thailand. This second TEU is able to handle 7,000 TEUs. Given that it only became fully operational in May 2015, the depot in Laem Chabang will contribute revenue for the whole of FY16. We noted that the Logistics has been steadily improving in profitability, from a loss of S$0.16m in FY13 to an operating profit of S$0.79m in FY14. In FY15, this business experienced a further improvement in net margin from 6.7% a year ago to 8.6%.

Figure 19: Logistics Services Business – Revenue and Operating Profit

Source: Company, NRA Capital

-0.48 -0.16

0.791.26

8.66

10.9211.70

14.67

-1.0

-0.5

0.0

0.5

1.0

1.5

0.0

5.0

10.0

15.0

FY12 FY13 FY14 FY15

Operating profit, S$mRev enue,S$m

Operating profit Revenue

page 15

LHN Limited

Financial Review – 1Q16 Results Show Company Back on Growth Track

FYE Sep (S$ m) 1Q16 1Q15 yoy % 4Q15 QoQ %

chg chg Comments

Rev enue 25.9 22.6 15 25.7 1 Driv en by 6.4% increase in industrial revenue

Operating costs (22.6) (20.0) 13 (24.4) -7 Due to increase in costs and new sites secured

EBITDA 3.3 2.6 28 1.2 167

EBITDA margin (%) 12.8 11.5 12 4.9 165 1.3%-point improv ement in EBITDA margin, as rev enue outgrew costs

Depn & amort. (1.7) (1.3) 30 (1.6) 7

EBIT 1.7 1.3 27 (0.3) 643 27% grow th y ear-on-year, reversal from 4Q loss

Interest ex pense (0.2) (0.1) 59 (0.1) 22

Interest & inv t inc 0.3 0.1 298 0.5 -36

Associates' contrib 0.0 0.0 0 0.0 50

Ex ceptionals 0.0 (0.2) -100 0.0 0 No IPO ex penses

Pretax profit 1.9 1.1 75 0.1 1,858 75% grow th y ear-on-year

Tax (0.3) (0.3) 2 0.6 -160

Tax rate (%) 18.0 30.7 -41 (589.5) 103

Minority interests 0.0 (0.0) 175 0.1 -93

Net profit 1.5 0.7 111 0.8 95

EPS (cts) 0.42 0.26 62 0.22 91

Source: Company, NRA Capital

1Q16 results were generally positive. LHN’s financial year ends in September. For the financial quarter ended December 2015, the company reported an improvement in revenue with revenue growing by 15% year-on-year. Compared to 4Q15, revenue grew by about S$0.2m. However, effective cost management led net income attributable to shareholders to grow by 95% or S$0.7m quarter-on-quarter. Compared to 1Q15, net profit attributable to shareholders rose by 111% or S$0.8m, partly due to the absence of S$0.25m of IPO expenses in 1Q16.

Revenue growth was mainly driven by growth from the industrial properties and Facilities Management businesses on a quarter-to-quarter basis, while gross margin improved from 19.3% to 24.7%. The improvement in margins explained for much of the increase in net profit. There were no fair value gains in 1Q16.

1Q16 results imply reversion to growth in FY16. During FY15, the group’s net profit attributable to shareholders fell from S$12.76m to S$4.2m, due to S$5.78m of fair value gain from investment properties in FY14 and S$1.56m of IPO expenses in FY15. Even then, operating profit fell by 36% or S$2.97m as gross profit margin shrank from 27.6% to 24.3%, resulting in gross profit falling by S$1.6m in spite of revenue growth of S$5.6m.

The 1Q16 results show improvement in terms of both gross margin and net profit attributable to shareholders. Annualizing the 1Q16 results, net profit would have been around S$6.1m, or about 45% higher than that of FY15. The improvement in 1Q16 results support our earlier argument that changes in rental spreads are usually temporary as LHN takes advantage of lower rental rates to reduce its own leasing costs.

Strong track record of positive cash flows. We also highlight that LHN has demonstrated strong cash generating ability in the past. For instance, it generated net operating cash flow of S$7.65m on S$4.05m of net profit in FY15. Tracking the company’s results since 2Q14, it has generated total net operating cash flow of S$20.1m on profit after tax of S$17.2m, of which S$6.36m were fair value gains from investment properties. Over the past eight quarters, the company only suffered negative cash flow in 2Q15. The strong cash flow implies positively of the company’s quality of earnings and low financing risk.

page 16

LHN Limited

Valuation

Expect high double digit growth in FY16. Based on portfolio net lettable area of 4.0m sq. ft. to 4.5m sq. ft., we estimate that LHN’s space optimization revenue of S$71.95m in FY15 works out to an impressive yield of about S$16 to S$18 psf. We expect LHN’s group revenue to grow by about 10% in FY16 from S$96.37m to S$106.01m. Growth will likely continue to be driven by increase in occupancy net lettable area with additional master leases secured and properties acquired, such as at 100 Eunos Ave 7, 18 Tampines Industrial Crescent and 38 Ang Mo Kio Industrial Park 2.

Given that 38 Ang Mo Kio Industrial Park 2 will contribute 341,000 sq. ft. of gross floor area and that 100 Eunos Ave 7 will be expanded by about 50% or around 20,000 sq. ft., we can reasonably expect NLA to grow by about 500,000 sq. ft. to about 5.0m sq. ft. in FY16, with a few new leases or acquisitions. Based on an average rental rate of S$16psf, revenue from the Space Optimization segment should likely grow to around S$80m in FY16. Assuming stable gross margin at around 25% and 2% increase in selling & distribution and administrative costs, profit after tax attributable to shareholders is projected to increase to S$6.09m for FY16, translating to high double digit growth of around 44%.

100 Eunos Ave 7 and 38 Ang Mo Kio Industrial Park 2 to provide potential fair value upside. Our forecasts do not assume any revaluation or fair value gains from LHN’s investment properties. However, we highlight that 100 Eunos Avenue 7 may provide fair value gains of about S$3m to S$5m, based on a fair value of S$10.2m for the portion of the asset held as investment properties and S$13.2m for the entire asset, including S$3.0m held as PPE. The upside shall be driven by the company’s plan to increase NLA at 100 Eunos Avenue 7 by 50%. 38 Ang Mo Kio Industrial Park 2 also has the potential to deliver some revaluation gains given the difference in valuation between itself and Techplace II. To be conservative, we do not factor in any fair value gain from property in our forecasts.

Figure 20: Summary of Assumptions and Forecasts

Forecasting Assumptions FY13 FY14 FY15 FY16F FY17F FY18F FY19F FY20F Rev enue grow th rate 11.5% 8.3% 6.2% 10.0% 10.0% 5.0% 5.0% 5.0%

Gross margin 26.7% 27.6% 24.3% 25.0% 25.0% 25.0% 25.0% 25.0% Selling and admin ex penses (% change) 9.9% -3.2% 10.4% 2.0% 2.0% 2.0% 2.0% 2.0%

Effectiv e tax rate 11% 9% 5% 17% 17% 17% 17% 17% Net inv esting cash flow -10.71 -5.35 -20.56 -20.00 -20.00 -20.00 -17.50 -15.00

Return on av erage assets 10.4% 18.1% 4.5% 5.7% 6.8% 6.9% 7.2% 7.3% Net cash/(net debt) 10.55 5.44 22.38 -0.56 5.13 10.30 10.43 7.88

Debt to common equity 82.1% 43.6% 42.0% 33.6% 37.9% 34.3% 31.0% 28.0% Summary Forecasts (S$m)

Rev enue 83.75 90.74 96.37 106.01 116.61 122.44 128.57 134.99 Gross profit 22.35 25.03 23.45 26.50 29.15 30.61 32.14 33.75

Fair v alue gain on inv estment properties 0.83 5.78 0.57 0.00 0.00 0.00 0.00 0.00 Net Income to shareholders 8.24 12.76 4.22 6.09 7.95 8.81 9.72 10.70

Source: NRA Capital

Valuation. To value LHN using the free cash flow approach, we adopted a five-year forecast horizon, of which the capex is assumed at S$20m/year from FY16 to FY18, S$17.5m in FY19 and S$15m/year in FY20. The reduced capex is offset by slower revenue growth assumptions of 5% per annum from FY18 to FY20. Under this set of assumptions, we are able to derive positive free cash flow to equity in FY19 and FY20, and maintain stable return on average assets of 7.2% and 7.3% respectively. Projected return on equity is also stable at around 12.5% from FY17 to FY20.

page 17

LHN Limited

Applying a cost of equity of 13.4% (assume beta of 1.5x) and terminal growth rate of 2%, we obtained a valuation of S$0.224 (round to S$0.225) per share for LHN. This valuation works out to 13.3x FY16 EPS and 1.34x FY16 NAV per share. Given that we expect FY16 ROE to be 10.5% and 12.5% thereafter, a valuation of 1.34x P/B can be deemed to be reasonable, against a peer average P/B of 1.6x and ROE of 15.7%. We repeat that our forecasts do not include any fair value gains which are actually a measure of the company’s Space Optimisation ability.

Likewise, the valuation P/E multiple of 13.3x is supported by estimated average annual EPS growth of 25.6% in FY16F and 17.5% over our forecast horizon. Currently, LHN trades at 9.2x P/E and 0.81x P/BV based on a share price of S$0.128 per share.

The alternative valuation approach would have been a sum-of-parts methodology whereby we value LHN based on its separate businesses and the RNAV of its investment properties. However, this approach is not feasible without separating cash flows and earnings from leased and owned properties.

Figure 21: Free Cash Flow to Equity Valuation

FY16 FY17 FY18 FY19 FY20 Net profit after tax 6.09 7.95 8.81 9.72 10.70

Depreciation & Amortization 7.415 6.743 7.650 8.304 8.776 Capex -20.00 -20.00 -20.00 -17.50 -15.00

Change in non-cash w orking capital -1.32 -1.24 -0.17 -1.31 -0.24 Non cash w orking capital -11.41 -12.65 -12.82 -14.12 -14.37

Change in borrow ings -3.05 5.00 0.00 0.00 0.00 Free cash flow to equity -10.87 -1.55 -3.71 -0.78 4.23

Terminal v alue 37.86 Discount rate 0.88 0.78 0.69 0.60 0.53

PV of free cash flow to equity -9.59 -1.21 -2.54 -0.47 2.26 Ex plicit v alue -11.55

PV of terminal v alue 85.42 Net cash as of end FY15 6.98

Value of equity 80.85 No. of shares (m) 361.52 Cost of equity 13.4%

Value per share (S$) 0.224 Terminal grow th rate 2%

Source: NRA Capital

Figure 22: Sensitivity Analysis

Terminal Growth Rate 1% 2% 3%

Cost of equity

11.4% 0.267 0.300 0.341

12.4% 0.232 0.258 0.290 13.4% 0.202 0.224 0.249

14.4% 0.178 0.196 0.216 15.4% 0.158 0.172 0.189

Source: NRA Capital

Figure 23: Peer Comparison

Company Name Mkt Cap (S$m) P/E P/B Ret. On Com.

Equity Debt/Com.

Equity

CWT Limited 1,080.5 11.28 1.31 12.5% 184.6% Cogent Holdings 208.1 7.18 2.17 33.0% 120.3%

Poh Tiong Choon Logistics 143.7 12.17 1.86 15.8% 60.1% ISOTeam Limited 87.9 10.57 1.80 21.4% 10.9%

GKE 54.2 NA 0.69 -4.1% 89.4% Average 314.9 10.3 1.6 15.7% 93.0%

LHN Limited 46.3 9.2 0.81 8.8% 39.8%

Source: Bloomberg, NRA Capital

page 18

LHN Limited

Figure 24: List of LHN’s Leased and Owned Properties

Property GFA (sq. ft.)

Industrial 3,244,000

566 Woodlands Road Singapore 728697 50,000 23 Woodlands Industrial Park E1 Singapore 757741 2,000

253 Kranji Road Singapore 739500 5,000 18 New Industrial Road Singapore 536205 75,000

Former Canteen Block and Annex Building at Depot Lane 122,000 43, Keppel Road, Singapore 099418 84,000

34 Boon Leat Terrace Singapore 119866 273,000 72 Eunos Av e 7, Singapore Handicrafts Centre, 68,000

State Land Lot 3145 MK 24 at 2 Soon Wing Road 105,000 4 Penjuru Road Singapore 609122 333,000

245 Jalan Ahmad Ibrahim Singapore 629144 36,000 51 Jalan Buroh Singapore 619495 12,000

No. 10 Tuas South Street 1, Singapore 637466

819,000 No. 20 Tuas South Street 1, Singapore 637465

No. 30 Tuas South Street 1, Singapore 637464 No. 40 Tuas South Street 1, Singapore 637463

No. 16 Tuas South Street 2, Singapore 637786 54,000 Lot 449 at Jalan Papan Singapore 610000 413,000

18 Penjuru Road (Lot 2339C Pt Mukim 5) 216,000 15 Jalan Terusan (Lot 505 Mukim 6) Singapore 619294 79,000

2 Tuas South Av enue 2, Singapore 637601 221,000 798/800 Upper Bukit Timah Road, Singapore 678138 67,000

7A Jalan Papan Singapore 619408 60,000 30 Jalan Terusan Singapore 619305 150,000

Commercial 656,400

Lot 228,342 & 346 Mukim XIV Woodlands Singapore 59,000

45 Burghley Driv e Singapore 559022 21,000 10 Raeburn Park Singapore 088702 163,000

300-320 Tanglin Road (Phoenix Park) Singapore 247970/247980 145,000 27 West Coast Highw ay Singapore 117867 68,000

1557 Keppel Road Singapore 089066 94,000 23A/B Turnhouse Road Singapore 507760/507764 8,000

34 Pulau Ubin Singapore 502487 1,600 42 Pulau Ubin Singapore 502487 1,300

200 Pandan Gardens Singapore 609336 14,000 260 Upper Bukit Timah Singapore 588190 33,000

215 Upper Bukit Timah Singapore 588184 30,000 88 Kota Kasablanka (Jakarta, Indonesia) 18,500

Residential 92,211

15 Robin Road, Singapore 258196 52,000

5 Peck Hay Road Singapore 228307 1,600 Keramat Road 24,000

No. 85 Boy ar Ny unt Street, Dagon Tow nship, Yangon Region (Myanmar) 14,611

New Sites 849,700

100 Eunos Av enue 7 45,500

18 Tampines Industrial Crescent 450,000 Plaza Marein, Jalan Jenderal Sudirman (Jakarta Indonesia) 13,200

38 Ang Mo Kio Industrial Park 2 (pending formal completion) 341,000 Total (Gross Floor Area) 4,842,311

Source: IPO Prospectus, FY15 annual report and respective announcements

page 19

LHN Limited

Key Risks

Soft rental market may lead to further margin squeeze in the short term. While LHN’s gross margin has improved in 1Q16, we are also mindful that gross margin may fluctuate along with tenant expiries at existing properties. Should the rental market continue to deteriorate, LHN’s margin maybe squeezed further. Based on data compiled by JTC, about 2.9m sqm of industrial properties may come online in 2016, which is equivalent to about 6% of existing stock across all categories.

Ability to renew leases. LHN’s business model is reliant on its ability to secure master leases for its properties. Should the company fail to secure the master lease for any property, income from that property will be affected. In turn, the company’s results maybe affected as it looks for new leases.

GreenHub and Work+Store are still in early stages of growth. While the concept of GreenHub and Work+Store is interesting, these businesses may take some time to contribute significantly towards bottom-line. In the interim, the company may be required to invest further resources in growing these businesses.

Recommendation

We reiterate that LHN is in a sweet spot to capitalize on current conditions in the industrial property market to reduce its rental costs and acquire new master leases and properties at low costs. The company faces low property price risk exposure as its own investment properties make up for less than 10% of its portfolio of managed properties, in terms of floor area. Moreover, it has thus far been acquiring properties with high Space Optimisation potential; suggesting that revaluation upside is more likely than any loss from lower property prices.

In the near term, it may face some margin pressure from tenants that ask for lower rents before the company can renew the lease at lower rental costs. However, rental cost savings from its own properties and new leases secured at lower rates mitigate this risk.

Longer term, LHN is growing its direct-to-user businesses with promising new concepts GreenHub and Work+Store, with regional expansion as a key theme. Should these businesses prove to be successful, the company may even be in a position to spin them off a few years down the road. In terms of valuation, LHN is not trading at rich levels and further upside can be derived with future earnings growth. In view of these factors, we rate LHN Overweight.

page 20

LHN Limited

Profit & Loss (S$ m, FYE Sep) 2014 2015 2016F 2017F 2018F 2019F 2020F

Rev enue 90.7 96.4 106.0 116.6 122.4 128.6 135.0

Operating ex penses (78.7) (87.5) (92.6) (101.6) (105.5) (109.9) (114.7)

EBITDA 12.0 8.9 13.4 15.0 16.9 18.7 20.3

Depreciation & amortisation (5.2) (5.5) (7.4) (6.7) (7.6) (8.3) (8.8)

EBIT 6.8 3.3 6.0 8.2 9.3 10.4 11.6

Net interest & inv t income 7.2 2.5 1.3 1.3 1.3 1.3 1.3

Associates' contribution 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Ex ceptional items 0.0 (1.6) 0.0 0.0 0.0 0.0 0.0

Pretax profit 14.0 4.3 7.3 9.6 10.6 11.7 12.9

Tax (1.3) (0.2) (1.2) (1.6) (1.8) (2.0) (2.2)

Minority interests 0.1 0.2 0.0 0.0 0.0 0.0 0.0

Net profit 12.8 4.2 6.1 7.9 8.8 9.7 10.7

Shares at y ear-end (m) NA 361.5 361.5 361.5 361.5 361.5 361.5

Balance Sheet (S$ m, as at Sep) 2014 2015 2016F 2017F 2018F 2019F 2020F

PPE 19.9 26.6 24.2 27.5 29.8 31.5 32.7

Inv estment properties 20.6 31.3 46.3 56.3 66.3 73.8 78.8

Other long-term assets 0.4 0.7 0.7 0.8 0.8 0.8 0.8

Total non-current assets 40.9 58.6 71.3 84.5 96.9 106.1 112.4

Cash and equiv alents 20.0 30.3 20.8 20.1 15.0 14.8 17.4

Stocks 0.3 0.2 0.2 0.2 0.2 0.2 0.2

Trade debtors 10.2 14.3 12.4 17.0 13.8 18.6 15.5

Other current assets 1.0 3.2 3.2 3.2 3.2 3.2 3.2

Total current assets 31.5 48.0 36.6 40.5 32.2 36.8 36.2

Trade creditors 23.6 26.5 25.8 31.7 28.7 34.7 31.9

Short-term borrow ings 2.2 3.0 3.0 3.0 3.0 3.0 3.0

Other current liabilities 1.6 1.3 1.3 1.3 1.3 1.3 1.3

Total current liabilities 27.3 30.8 30.1 36.0 33.0 39.0 36.2

Long-term borrow ings 12.1 20.3 17.3 22.3 22.3 22.3 22.3

Other long-term liabilities 0.4 0.2 0.2 0.2 0.2 0.2 0.2

Total long-term liabilities 12.5 20.6 17.5 22.5 22.5 22.5 22.5

Shareholders' funds 32.7 55.4 60.3 66.7 73.7 81.5 90.0

Minority interests (0.1) (0.1) (0.1) (0.1) (0.1) (0.1) (0.1)

NAV/share (S$) 0.09 0.15 0.17 0.18 0.20 0.23 0.25

Total Assets 72.4 106.7 107.8 125.1 129.1 142.9 148.6

Total Liabilities + S’holders' funds 72.4 106.7 107.8 125.1 129.1 142.9 148.6

Cash Flow (S$ m, FYE Sep) 2014 2015 2016F 2017F 2018F 2019F 2020F

Pretax profit 14.0 4.3 7.3 9.6 10.6 11.7 12.9

Depreciation & non-cash adjustments 0.1 5.5 7.4 6.7 7.6 8.3 8.7

Working capital changes (2.1) (1.2) 1.3 1.2 0.2 1.3 0.2

Cash tax paid (0.8) (0.8) (1.2) (1.6) (1.8) (2.0) (2.2)

Cash flow from operations 11.2 7.7 14.8 15.9 16.6 19.3 19.7

Capex (4.8) (10.7) (5.0) (10.0) (10.0) (10.0) (10.0)

Net inv estments & sale of FA (0.6) (10.0) (15.0) (10.0) (10.0) (7.5) (5.0)

Others 0.1 0.1 0.0 0.0 0.0 0.0 0.0

Cash flow from investing (5.4) (20.6) (20.0) (20.0) (20.0) (17.5) (15.0)

Debt raised/(repaid) (4.8) 8.8 (3.1) 5.0 0.0 0.0 0.0

Equity raised/(repaid) 0.0 16.2 0.0 0.0 0.0 0.0 0.0

Div idends paid 0.0 (2.0) (1.2) (1.6) (1.8) (1.9) (2.1)

Others (0.0) 0.1 0.0 0.0 0.0 0.0 0.0

Cash flow from financing (4.8) 23.1 (4.3) 3.4 (1.8) (1.9) (2.1)

Change in cash 1.1 10.2 (9.5) (0.7) (5.2) (0.1) 2.5

Change in net cash/(debt) 3.9 1.3 (6.4) (5.7) (5.2) (0.1) 2.5

Ending net cash/(debt) 5.7 7.0 0.6 (5.1) (10.3) (10.4) (7.9)

KEY RATIOS (FYE Sep) 2014 2015 2016F 2017F 2018F 2019F 2020F

Rev enue grow th (%) 8.3 6.2 10.0 10.0 5.0 5.0 5.0

EBITDA grow th (%) 25.7 (26.1) 51.1 11.7 13.0 10.4 8.8

Pretax margins (%) 15.4 4.4 6.9 8.2 8.7 9.1 9.5

Net profit margins (%) 14.1 4.4 5.7 6.8 7.2 7.6 7.9

Effectiv e tax rates (%) 9.3 5.0 17.0 17.0 17.0 17.0 17.0

Net div idend pay out (%) NA 22.4 20.0 20.0 20.0 20.0 20.0

ROE (%) 48.1 9.6 10.5 12.5 12.5 12.5 12.5

Free cash flow y ield (%) 2.4 (13.2) (23.5) (3.3) (8.0) (1.7) 9.1

Source: NRA Capital forecasts

page 21

LHN Limited

NRA Capital Pte. Ltd (“NRA Capital”) has received compensation for this valuation report. This publication is confidential a nd general in nature. It was prepared from data which NRA Capital believes to be reliable , and does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. No representatio n, express

or implied, is made with respect to the accuracy, completeness or reliability of the information or opinions in this publication. Accordingly, neither we nor any of our affiliates nor persons related to us accept any liability whatsoever for any direct, i ndirect, special or consequential damages or economic loss that may arise from the use of information or opinions in this publication. Opinions expressed are subject to change without notice. NRA Capital and its related companies, their associates, directors, connected parties and/or employees may own or have positions in any securities mentioned herein or any securities related thereto and may from time to time add or dispose of or may be materially interested in any such securities. NRA Capital and its related companies may from time to time perform advisory, investment or other services for, or solicit such advisory, investment or other services from any entity mentioned in this report. The research p rofessionals who were involved in the preparing of this material may participate in the solicitation of such business. In reviewing these materials, you should be aware that any or all of the foregoing, among other things, may give rise to real or potential conflicts of int erest. Additional information is, subject to the duties of confidentiality, available on request. You acknowledge that the price of securities

traded on the Singapore Exchange Securities Trading Limited ("SGX-ST") are subject to investment risks, can and does fluctuate, and any individual security may experience upwards or downwards movements, and may even become valueless. There is an inherent risk that losses may be incurred rather than profit made as a result of buying and selling securities traded on the SGX-ST. You are aware of the risk of exchange rate fluctuations which can cause a loss of the princip al invested. You also acknowledge that these are risks that you are prepared to accept. You understand that you should make the decision to invest only after due and careful consideration. You agree that you will not make any orders in reliance on any representation/advice, view, opinion or other statement made by NRA Capital, and you will not hold NRA Capital either directly or indirectly liable for any loss suffered by you in the event you do so rely on them. You understand that you should seek independent professional advice if you are uncertain of or have not understood any aspect of this risk disclosure statement or the nature and risks involved in trading of securities on the SGX-ST.

![(LQGH[DPHQKDYRPX ]LHN - Havovwo.nlhavovwo.nl/havo/hmu/bestanden/hmu13iopg.pdf · (LQGH[DPHQKDYRPX ]LHN , havovwo.nl havovwo.nl examen-cd.nl cd 1 track 5 Je hoort een langer fragment](https://img.dokumen.tips/doc/110x75/5e236c223f2dde5df66014d2/lqghdphqkdyrpx-lhn-lqghdphqkdyrpx-lhn-havovwonl-havovwonl-examen-cdnl.jpg)

![PX]LHN KDYR 201 - Havovwo.nl](https://img.dokumen.tips/doc/110x75/6236f197e50d6a06ee263c2c/pxlhn-kdyr-201-.jpg)