Embed Size (px)

Citation preview

A7031-01 Issue 4 5010276X April15

LEVEL 1 AWARD IN

BOOK-KEEPING

QUALIFICATION GUIDANCE

[5010276X]

About ABC Awards

ABC Awards is a leading national awarding organisation which has a long-

established reputation for developing and awarding high quality vocational

qualifications. We are committed to developing qualifications, which help learners

and organisations, by cultivating the relevant skills for learning, skills for employment

and skills for life.

We work with hundreds of centres nationally and thousands of learners achieve an

ABC Awards qualification each year.

Established in 1998, ABC Awards combines more than 180 years of examination and

assessment expertise but at the same time integrates a responsive, flexible approach

to the needs of our customers.

ABC has an on-line registration system to help customers register learners on ABC’s

qualifications, units and exams. In addition it provides features to view exam results,

invoices, mark sheets and other information about learners already registered.

The system is accessed via a web browser by connecting to our secure website

using a username and password.

https://secure.abcawards.co.uk/ors/secure_login.asp

Sources of Additional Information

The ABC website www.abcawards.co.uk provides access to a wide variety of

information.

Copyright

All rights reserved. No part of this publication may be reproduced, stored in a

retrieval system, or transmitted in any form or by any means, electronic, mechanical,

photocopying, recording or otherwise, without the prior permission of the publishers.

This document may be copied by approved centres for the purpose of assessing

learners. It may also be copied by learners for their own use.

Contents Qualification Summary 1 Introduction 3 Aims 3 Target Group 3 Progression Opportunities 3 Unit Details 4 Recognition of Prior Learning (RPL), Exemption and Credit Transfer 30 Certification 30

1

Qualification Summary ABC Awards Level 1 Award in Book-Keeping

Qualifications

Level 1 Award in Book-Keeping

Assessment Internal assessment, internal and external moderation

Grading Pass

Operational Start Date 01/07/2010

Operational End Date 31/12/15

ABC Sector Business and Enterprise

Ofqual SSA Sector 15.1 Accounting and Finance

Stakeholder Support

This qualification is supported by FSSC, the Financial Services Skills Council

Contact

See ABC website for the Centre Support Officer responsible for this qualification

2

Level 1 Award in Book-Keeping Learners must complete all eight mandatory units to

Unit Level Credit Value

GLH Page No.

Introduction to book-keeping [M/600/8737] 1 1 4 4

Working within book-keeping [T/600/8738] 1 2 8 8

Banking procedures [A/600/8739] 1 1 3 12

Preparing and processing book-keeping documents [M/600/8740]

1 1 3 15

Recording credit transactions [A/600/8742] 1 1 4 18

Making and receiving payments [J/600/8744] 1 1 6 21

Recording receipts and payments [L/600/8745] 1 1 5 24

Maintaining petty cash records [R/600/8746] 1 1 5 27

Numbers in box brackets indicate QCF unit Number If learners achieve credits from units of the same title (or linked titles) at more than one level, they cannot count credits achieved from both units towards the credit target of a qualification

Entry Requirements There are no specific entry requirements

Age Range Pre 16 16 – 18 19 +

LARS Reference 5010276X

Recommended GLH 38

Foundation Learning This qualification sits within Foundation Learning

Type of Funding Available

See LARS (Learning Aim Rates Service)

Minimum Qualification Fee

See ABC web site for current fees and charges

Unit Fee Unit fees are based upon a unit’s individual credit value. Please see the ABC web site for the current fee charged per credit.

Additional Information See ABC website for resources available for this qualification

3

Introduction Book-Keeping qualifications have a long history stretching back over many years within ABC Awards - deriving from a Union of Lancashire and Cheshire Institutes (ULCI) general commerce qualification in 1964, a result of the need identified for a specific book-keeping qualification. The Level 1 Award in Book-Keeping has been developed in collaboration with FSSC and other Awarding Organisations. It provides practical experience and knowledge of Book-Keeping to support engagement, participation, achievement and progression for learners at Level 1. The qualification could help learners to decide whether to undertake further training or employment within the financial services occupational area. This qualification sits within Foundation Learning.

Aims The ABC Level 1 Award in Book-Keeping aims to enable learners to

gain work-related skills

develop generic employability skills

prepare for further training within this occupational area

gain an insight into core activities within this occupational area in order to allow them to make informed career decisions

Target Group This qualification is designed for young people aged 14+ and adults who have an interest in the financial sector as an area of employment and want to develop practical skills in this area. ABC expects approved centres to recruit with integrity on the basis of a learner’s ability to contribute to and successfully complete all the requirements of a unit/s or the full qualification.

Progression Opportunities Progression could be to appropriate Level 2 qualifications or into full or part-time employment Centres should be aware that reasonable Adjustments which may be permitted for assessment may in some instances limit a learner’s progression into the sector. Centres must, therefore, inform learners of any limits their learning difficulty may impose on future progression

4

Unit Details

Unit Title

M/600/8737 Introduction to book-keeping

Level

1

Credit Value

1

Guided Learning Hours

4

Unit Summary For the learner to have a clear understanding of the job role of a book-keeper and to appreciate the career path a book-keeper may take

Learning Outcomes (1 to 3) The learner will

Assessment Criteria (1.1 to 3.3) The learner can

1. Understand the job role and career path for a book-keeper

1.1 Outline the job role of a book-keeper 1.2 Outline how the role of the book-keeper fits within the business organisation 1.3 Outline how bookkeeping can become a career pathway

2. Understand different types of business organisations

2.1 Give examples of different types of business organisation 2.2 Define the organisations known as

sole trader

partnership

3. Know the terminology used in book-keeping

3.1 Identify the difference between a book-keeper and an accountant 3.2 Explain the correct use of two of the following (minimum) bookkeeping terms

petty cash imprest system

sales

purchase

customer

supplier

receipt

payment

income

expenditure

5

3.3 State how two (minimum) of the following bookkeeping documents are used

petty cash voucher

purchase order

invoice

credit note

statement of account

remittance advice

Mapping to National Occupational Standards Direct relationship based on NOS for Accountancy and Finance PS-1, FA-1 and FA-2

6

SUPPORTING UNIT INFORMATION

M/600/8737 Introduction to book-keeping - Level 1

INDICATIVE CONTENT To successfully achieve this unit, learners need to provide evidence that they have met the learning outcomes and assessment criteria for the unit. Indicative content is offered as guidance to aid delivery of the unit and to set the learning outcomes and assessment criteria in context.

Learning Outcome 1. Understand the job role and career path for a book-keeper

Principle role of a book keeper

Legal requirement to keep proper books of account

Employment / self- employment

Public / private sector employment

Learning Outcome 2. Understand different types of business organisations

Different types of business ownership

Limited company, partnership, sole trader, public limited company, co-operative company

Nature and differences of sole trader / partnership Learning Outcome 3. Know the terminology used in book-keeping

Role of book keeper – records day to day financial transactions

Role of accountant – collates financial and other information to analyse and evaluate business potential

Nature and purpose of each term / document and relation to book keeping system TEACHING STRATEGIES AND LEARNING ACTIVITIES Centres should adopt a delivery approach which supports the practical skills and knowledge development of their particular learners. The aims and aspirations of all learners, including those with identified special needs including learning difficulties/disabilities, should be considered, and appropriate support mechanisms put in place. Centres should adopt a delivery approach which supports the development of their particular learners. The aims and aspirations of all learners, including those with identified special needs, including learning difficulties/disabilities, should be considered and appropriate support mechanisms put in place. METHODS OF ASSESSMENT

This unit will be internally assessed, internally and externally moderated via a learner’s portfolio and other related evidence, against the unit outcomes and assessment criteria. All learners must complete a portfolio of evidence that shows achievement of all the relevant learning outcomes and assessment criteria

7

Minimum requirements when assessing this unit ABC expects that staff will be appropriately qualified to assess learners against the outcomes and criteria within the units. Generally teaching staff should be qualified and/or vocationally experienced to at least a level above that which they are teaching. EVIDENCE OF ACHIEVEMENT

Evidence presented to support achievement is not prescribed for each learning outcome. It could typically include some of the following

Product evidence

Observation reports

Oral/written questions and answers

Reports/notes

Witness statements

Taped evidence (video or audio)

Photographic evidence

Case studies/assignments/projects

Interview/professional discussion

Pictorial identifications

Letters / emails seeking clarification / confirmation of understanding

Internet research / copies of items with relevant knowledge highlighted

This is not an exhaustive list and learners should be encouraged to develop the most appropriate evidence to demonstrate their achievement of the learning outcomes and assessment criteria. ADDITIONAL INFORMATION

See ABC web site for further information

8

Unit Title

T/600/8738 Working within book-keeping

Level

1

Credit Value

2

Guided Learning Hours

8

Unit Summary For the learner to have a clear understanding of the principles and procedures related to the processing of business transactions

Learning Outcomes (1 to 6) The learner will

Assessment Criteria (1.1 to 6.2) The learner can

1. Understand single-entry bookkeeping

1.1 Explain single entry bookkeeping 1.2 Outline the books used in single entry book-keeping

2. Know the general principles of VAT

2.1 State when a business must register for VAT

2.2 State the various rates of VAT in general use

3. Understand what is meant by both cash and credit transactions

3.1 Explain what is meant by cash sales 3.2 Explain what is meant by cash purchase 3.3 Explain what is meant by trading on credit 3.4 Identify the various documents needed to record a credit sale or purchase

4. Understand the principles of coding and batch control

4.1 Explain why a coding system is used for financial transactions 4.2 Outline the use of batch control

5. Understand how to process information in the books of prime entry (excluding the Journal)

5.1 State where to find financial information for entry into the bookkeeping system 5.2 State where to enter relevant information in the books of prime entry (excluding the Journal) 5.3 Outline the need to cross check totals for accuracy

9

6. Understand responsibilities when working in a bookkeeping environment

6.1 Outline the responsibilities relating to security of data when dealing with customers, suppliers and other external agencies 6.2 Identify where to gain authorisation for expenditure and when dealing with queries related to various financial transactions

Mapping to National Occupational Standards Direct relationship based on NOS for Accountancy and Finance PS-1, FA-1 and FA-2

10

SUPPORTING UNIT INFORMATION T/600/8738 Working within Book-keeping - Level 1

INDICATIVE CONTENT To successfully achieve this unit, learners need to provide evidence that they have met the learning outcomes and assessment criteria for the unit. Indicative content is offered as guidance to aid delivery of the unit and to set the learning outcomes and assessment criteria in context. Learning Outcome 1. Understand single-entry book-keeping

Principles of single entry book keeping

Differences between single & double entry book keeping

Advantages / disadvantages of single entry book keeping

Purchase / returns day book

Sales / returns day book

Bank / cash book

Petty cash book Learning Outcome 2. Know the general principles of VAT

HMRC role in collecting VAT

Requirements of registration – voluntary / mandatory

Rates of VAT, exempt, non-exempt, standard rate, zero rate, reduced rate Learning Outcome 3. Understand what is meant by both cash and credit transactions

Nature and difference between cash / credit transaction

Book keeping terms - debtor / creditor Learning Outcome 4. Understand the principles of coding and batch control

Advantages of coding and batch control

Efficiency of data capture, entry and analysis Learning Outcome 5. Understand how to process information in the books of prime entry (excluding the Journal)

Nature and purposes of books of prime / original entry

Advantages of cross checking Learning Outcome 6. Understand responsibilities when working in a bookkeeping environment

Code of professional ethics

Data Protection Act 1998

Hierarchy and lines of authority within an organisation TEACHING STRATEGIES AND LEARNING ACTIVITIES Centres should adopt a delivery approach which supports the practical skills and knowledge development of their particular learners.

11

The aims and aspirations of all learners, including those with identified special needs including learning difficulties/disabilities, should be considered, and appropriate support mechanisms put in place. Centres should adopt a delivery approach which supports the development of their particular learners. The aims and aspirations of all learners, including those with identified special needs, including learning difficulties/disabilities, should be considered and appropriate support mechanisms put in place. METHODS OF ASSESSMENT This unit will be internally assessed, internally and externally moderated via a learner’s portfolio and other related evidence, against the unit outcomes and assessment criteria. All learners must complete a portfolio of evidence that shows achievement of all the relevant learning outcomes and assessment criteria Minimum requirements when assessing this unit ABC expects that staff will be appropriately qualified to assess learners against the outcomes and criteria within the units. Generally teaching staff should be qualified and/or vocationally experienced to at least a level above that which they are teaching. EVIDENCE OF ACHIEVEMENT Evidence presented to support achievement is not prescribed for each learning outcome. It could typically include some of the following

Product evidence

Observation reports

Oral/written questions and answers

Reports/notes

Witness statements

Taped evidence (video or audio)

Photographic evidence

Case studies/assignments/projects

Interview/professional discussion

Pictorial identifications

Letters / emails seeking clarification / confirmation of understanding

Internet research / copies of items with relevant knowledge highlighted

This is not an exhaustive list and learners should be encouraged to develop the most appropriate evidence to demonstrate their achievement of the learning outcomes and assessment criteria. ADDITIONAL INFORMATION

See ABC web site for further information

12

Unit Title

A/600/8739 Banking procedures

Level

1

Credit Value

1

Guided Learning Hours

3

Unit Summary The purpose of this unit is to develop the learners’ knowledge and understanding of the UK banking system and organisational activities and procedures related to banking

Learning Outcomes (1 to 2) The learner will

Assessment Criteria (1.1 to 2.2) The learner can

1. Understand the banking process

1.1 Identify the main services offered by banks and building societies 1.2 Describe how the banking clearing system works 1.3 Identify different forms of payment which include

cash

cheques

credit cards

debit cards

direct payments 1.4 Identify the information required to ensure the following payments are valid

cash

cheque

credit card

debit card 1.5 Describe the processing and security procedures relating to the different forms of payments

2. Understand document retention and storage requirements

2.1 Explain why it is important for an organisation to have a formal document retention policy 2.2 Identify the different types of documents that may be stored

Mapping to National Occupational Standards Direct relationship based on the NOS for Accountancy and Finance FA-3

13

SUPPORTING UNIT INFORMATION A/600/8739 Banking procedures - Level 1

INDICATIVE CONTENT

To successfully achieve this unit, learners need to provide evidence that they have met the learning outcomes and assessment criteria for the unit. Indicative content is offered as guidance to aid delivery of the unit and to set the learning outcomes and assessment criteria in context.

Learning Outcome 1. Understand the banking process

Bank accounts

Personal / secured loans

Mortgages

Investments

CHAPS and BACS payments

Different types of financial transactions

Components of valid financial transactions

Learning Outcome 2. Understand document retention and storage requirements

Importance of complying with legislation

Data Protection Act 1998

Current and historic records

Retention periods TEACHING STRATEGIES AND LEARNING ACTIVITIES Centres should adopt a delivery approach which supports the practical skills and knowledge development of their particular learners. The aims and aspirations of all learners, including those with identified special needs including learning difficulties/disabilities, should be considered, and appropriate support mechanisms put in place. Centres should adopt a delivery approach which supports the development of their particular learners. The aims and aspirations of all learners, including those with identified special needs, including learning difficulties/disabilities, should be considered and appropriate support mechanisms put in place. METHODS OF ASSESSMENT This unit will be internally assessed, internally and externally moderated via a learner’s portfolio and other related evidence, against the unit outcomes and assessment criteria. All learners must complete a portfolio of evidence that shows achievement of all the relevant learning outcomes and assessment criteria

14

Minimum requirements when assessing this unit ABC expects that staff will be appropriately qualified to assess learners against the outcomes and criteria within the units. Generally teaching staff should be qualified and/or vocationally experienced to at least a level above that which they are teaching. EVIDENCE OF ACHIEVEMENT

Evidence presented to support achievement is not prescribed for each learning outcome. It could typically include some of the following

Product evidence

Observation reports

Oral/written questions and answers

Reports/notes

Witness statements

Taped evidence (video or audio)

Photographic evidence

Case studies/assignments/projects

Interview/professional discussion

Pictorial identifications

Letters / emails seeking clarification / confirmation of understanding

Internet research / copies of items with relevant knowledge highlighted

This is not an exhaustive list and learners should be encouraged to develop the most appropriate evidence to demonstrate their achievement of the learning outcomes and assessment criteria. ADDITIONAL INFORMATION

See ABC web site for further information

15

Unit Title

M/600/8740 Preparing and processing book-keeping documents

Level

1

Credit Value

1

Guided Learning Hours

3

Unit Summary The purpose of this unit is to develop the learners’ skills in processing credit sales and purchase documents

Learning Outcomes (1 to 2) The learner will

Assessment Criteria (1.1 to 2.3) The learner can

1. Process sales invoices and credit notes

1.1 Prepare sales invoices and sales credit notes from source documents 1.2 Calculate relevant sales tax (eg VAT) and check it has been applied accurately 1.3 Code sales invoices and credit notes

2. Process supplier invoices and credit notes

2.1 Check the accuracy of supplier invoices and credit notes against purchase orders, goods received and delivery notes 2.2 Check that agreed trade and bulk discounts have been applied accurately. 2.3 Code supplier invoices and credit notes

Mapping to National Occupational Standards Direct relationship based on the NOS for Accountancy and Finance FA-1 and FA-2

16

SUPPORTING UNIT INFORMATION M/600/8740 Preparing and processing bookkeeping documents - Level 1

INDICATIVE CONTENT To successfully achieve this unit, learners need to provide evidence that they have met the learning outcomes and assessment criteria for the unit. Indicative content is offered as guidance to aid delivery of the unit and to set the learning outcomes and assessment criteria in context. Learning Outcome 1. Process sales invoices and credit notes

Importance and relevance of coding documents

Importance of accounting separately for VAT Learning Outcome 2. Process supplier invoices and credit notes

Importance of verifying supplier invoices against goods received/ purchase orders/ delivery notes

Principles of discounts allowed TEACHING STRATEGIES AND LEARNING ACTIVITIES Centres should adopt a delivery approach which supports the practical skills and knowledge development of their particular learners. The aims and aspirations of all learners, including those with identified special needs including learning difficulties/disabilities, should be considered, and appropriate support mechanisms put in place. Centres should adopt a delivery approach which supports the development of their particular learners. The aims and aspirations of all learners, including those with identified special needs, including learning difficulties/disabilities, should be considered and appropriate support mechanisms put in place. METHODS OF ASSESSMENT This unit will be internally assessed, internally and externally moderated via a learner’s portfolio and other related evidence, against the unit outcomes and assessment criteria. All learners must complete a portfolio of evidence that shows achievement of all the relevant learning outcomes and assessment criteria Minimum requirements when assessing this unit ABC expects that staff will be appropriately qualified to assess learners against the outcomes and criteria within the units. Generally teaching staff should be qualified and/or vocationally experienced to at least a level above that which they are teaching.

17

EVIDENCE OF ACHIEVEMENT Evidence presented to support achievement is not prescribed for each learning outcome. It could typically include some of the following

Product evidence

Observation reports

Oral/written questions and answers

Reports/notes

Witness statements

Taped evidence (video or audio)

Photographic evidence

Case studies/assignments/projects

Interview/professional discussion

Pictorial identifications

Letters / emails seeking clarification / confirmation of understanding

Internet research / copies of items with relevant knowledge highlighted

This is not an exhaustive list and learners should be encouraged to develop the most appropriate evidence to demonstrate their achievement of the learning outcomes and assessment criteria. ADDITIONAL INFORMATION

See ABC web site for further information

18

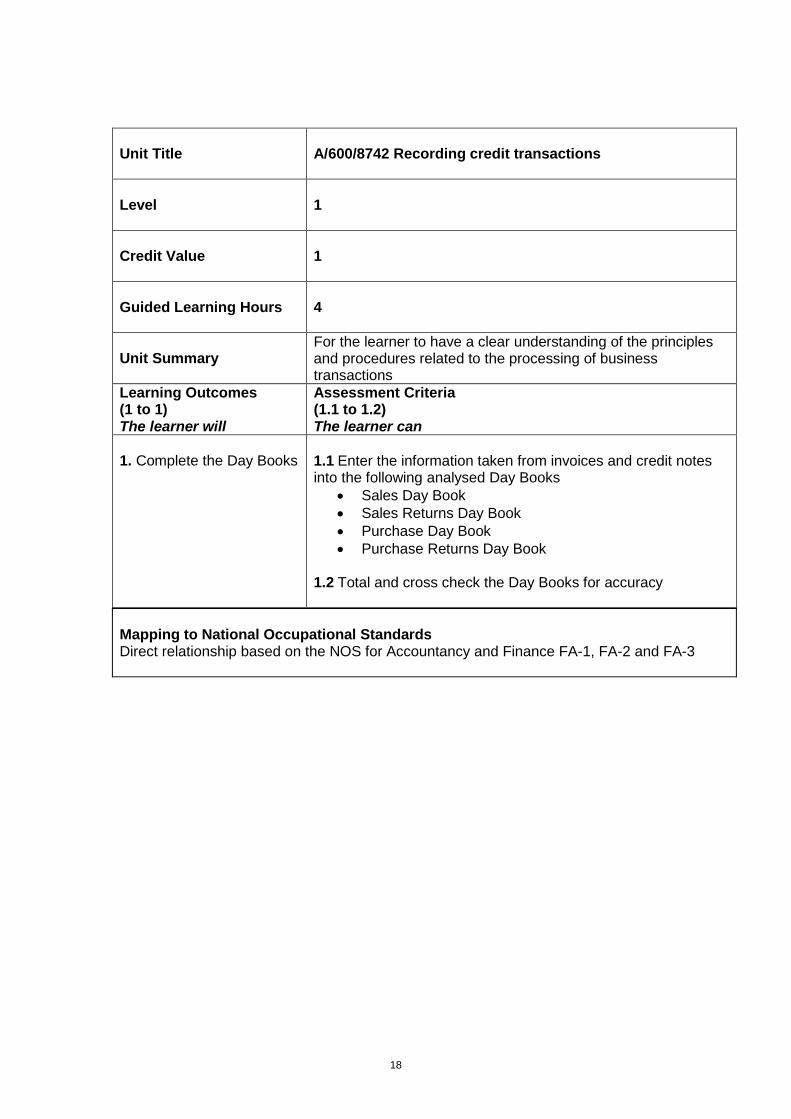

Unit Title

A/600/8742 Recording credit transactions

Level

1

Credit Value

1

Guided Learning Hours

4

Unit Summary For the learner to have a clear understanding of the principles and procedures related to the processing of business transactions

Learning Outcomes (1 to 1) The learner will

Assessment Criteria (1.1 to 1.2) The learner can

1. Complete the Day Books

1.1 Enter the information taken from invoices and credit notes into the following analysed Day Books

Sales Day Book

Sales Returns Day Book

Purchase Day Book

Purchase Returns Day Book 1.2 Total and cross check the Day Books for accuracy

Mapping to National Occupational Standards Direct relationship based on the NOS for Accountancy and Finance FA-1, FA-2 and FA-3

19

SUPPORTING UNIT INFORMATION A/600/8742 Recording credit transactions - Level 1

INDICATIVE CONTENT To successfully achieve this unit, learners need to provide evidence that they have met the learning outcomes and assessment criteria for the unit. Indicative content is offered as guidance to aid delivery of the unit and to set the learning outcomes and assessment criteria in context.

Learning Outcome 1. Complete the Day Books

nature and purpose of Day Books

importance of source documents

importance of analysis and cross checking TEACHING STRATEGIES AND LEARNING ACTIVITIES Centres should adopt a delivery approach which supports the practical skills and knowledge development of their particular learners. The aims and aspirations of all learners, including those with identified special needs including learning difficulties/disabilities, should be considered, and appropriate support mechanisms put in place. Centres should adopt a delivery approach which supports the development of their particular learners. The aims and aspirations of all learners, including those with identified special needs, including learning difficulties/disabilities, should be considered and appropriate support mechanisms put in place. METHODS OF ASSESSMENT This unit will be internally assessed, internally and externally moderated via a learner’s portfolio and other related evidence, against the unit outcomes and assessment criteria. All learners must complete a portfolio of evidence that shows achievement of all the relevant learning outcomes and assessment criteria Minimum requirements when assessing this unit ABC expects that staff will be appropriately qualified to assess learners against the outcomes and criteria within the units. Generally teaching staff should be qualified and/or vocationally experienced to at least a level above that which they are teaching. EVIDENCE OF ACHIEVEMENT Evidence presented to support achievement is not prescribed for each learning outcome. It could typically include some of the following

Product evidence

20

Observation reports

Oral/written questions and answers

Reports/notes

Witness statements

Taped evidence (video or audio)

Photographic evidence

Case studies/assignments/projects

Interview/professional discussion

Pictorial identifications

Letters / emails seeking clarification / confirmation of understanding

Internet research / copies of items with relevant knowledge highlighted

This is not an exhaustive list and learners should be encouraged to develop the most appropriate evidence to demonstrate their achievement of the learning outcomes and assessment criteria. ADDITIONAL INFORMATION

See ABC web site for further information

21

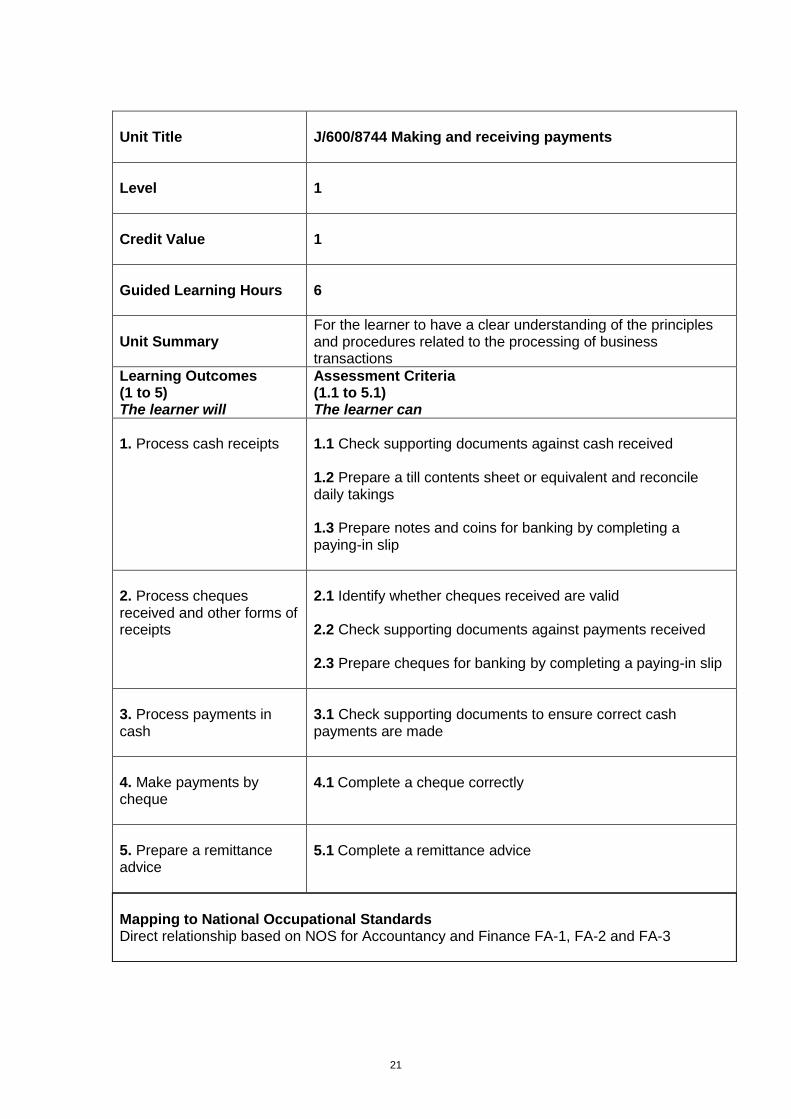

Unit Title

J/600/8744 Making and receiving payments

Level

1

Credit Value

1

Guided Learning Hours

6

Unit Summary For the learner to have a clear understanding of the principles and procedures related to the processing of business transactions

Learning Outcomes (1 to 5) The learner will

Assessment Criteria (1.1 to 5.1) The learner can

1. Process cash receipts

1.1 Check supporting documents against cash received 1.2 Prepare a till contents sheet or equivalent and reconcile daily takings 1.3 Prepare notes and coins for banking by completing a paying-in slip

2. Process cheques received and other forms of receipts

2.1 Identify whether cheques received are valid 2.2 Check supporting documents against payments received 2.3 Prepare cheques for banking by completing a paying-in slip

3. Process payments in cash

3.1 Check supporting documents to ensure correct cash payments are made

4. Make payments by cheque

4.1 Complete a cheque correctly

5. Prepare a remittance advice

5.1 Complete a remittance advice

Mapping to National Occupational Standards Direct relationship based on NOS for Accountancy and Finance FA-1, FA-2 and FA-3

22

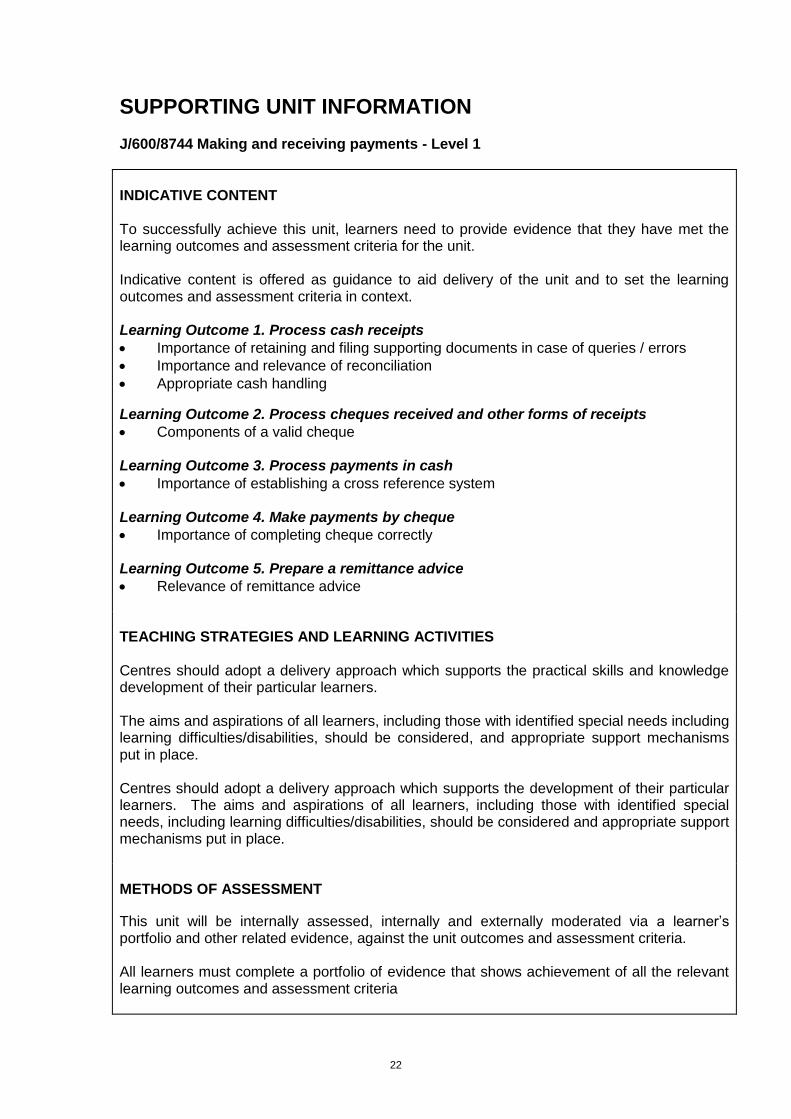

SUPPORTING UNIT INFORMATION J/600/8744 Making and receiving payments - Level 1

INDICATIVE CONTENT To successfully achieve this unit, learners need to provide evidence that they have met the learning outcomes and assessment criteria for the unit. Indicative content is offered as guidance to aid delivery of the unit and to set the learning outcomes and assessment criteria in context. Learning Outcome 1. Process cash receipts

Importance of retaining and filing supporting documents in case of queries / errors

Importance and relevance of reconciliation

Appropriate cash handling

Learning Outcome 2. Process cheques received and other forms of receipts

Components of a valid cheque Learning Outcome 3. Process payments in cash

Importance of establishing a cross reference system Learning Outcome 4. Make payments by cheque

Importance of completing cheque correctly Learning Outcome 5. Prepare a remittance advice

Relevance of remittance advice TEACHING STRATEGIES AND LEARNING ACTIVITIES Centres should adopt a delivery approach which supports the practical skills and knowledge development of their particular learners. The aims and aspirations of all learners, including those with identified special needs including learning difficulties/disabilities, should be considered, and appropriate support mechanisms put in place. Centres should adopt a delivery approach which supports the development of their particular learners. The aims and aspirations of all learners, including those with identified special needs, including learning difficulties/disabilities, should be considered and appropriate support mechanisms put in place. METHODS OF ASSESSMENT

This unit will be internally assessed, internally and externally moderated via a learner’s portfolio and other related evidence, against the unit outcomes and assessment criteria. All learners must complete a portfolio of evidence that shows achievement of all the relevant learning outcomes and assessment criteria

23

Minimum requirements when assessing this unit ABC expects that staff will be appropriately qualified to assess learners against the outcomes and criteria within the units. Generally teaching staff should be qualified and/or vocationally experienced to at least a level above that which they are teaching. EVIDENCE OF ACHIEVEMENT Evidence presented to support achievement is not prescribed for each learning outcome. It could typically include some of the following

Product evidence

Observation reports

Oral/written questions and answers

Reports/notes

Witness statements

Taped evidence (video or audio)

Photographic evidence

Case studies/assignments/projects

Interview/professional discussion

Pictorial identifications

Letters / emails seeking clarification / confirmation of understanding

Internet research / copies of items with relevant knowledge highlighted

This is not an exhaustive list and learners should be encouraged to develop the most appropriate evidence to demonstrate their achievement of the learning outcomes and assessment criteria. ADDITIONAL INFORMATION

See ABC web site for further information

24

Unit Title

L/600/8745 Recording receipts and payments

Level

1

Credit Value

1

Guided Learning Hours

5

Unit Summary The purpose of this unit is to develop the learners’ skills in maintaining a two column analysed cash book and reconciling it to the bank statement

Learning Outcomes (1 to 2) The learner will

Assessment Criteria (1.1 to 2.3) The learner can

1. Maintain a two column analysed cash book

1.2 Enter receipts and payment details from relevant primary records into the two column analysed cash book 1.3 Enter sales tax (eg VAT) 1.4 Total, balance and cross check the cash book

2. Reconcile the bank statement with the cash book

2.1 Check individual items on the bank statement against the cash book 2.2 Update the cash book from the bank statement 2.3 Prepare a bank reconciliation statement

Mapping to National Occupational Standards Direct relationship to the NOS for Accounting. Learning Outcomes and Assessment Criteria devised and mapped from NOS Units FA-1, FA-2 and FA-3

25

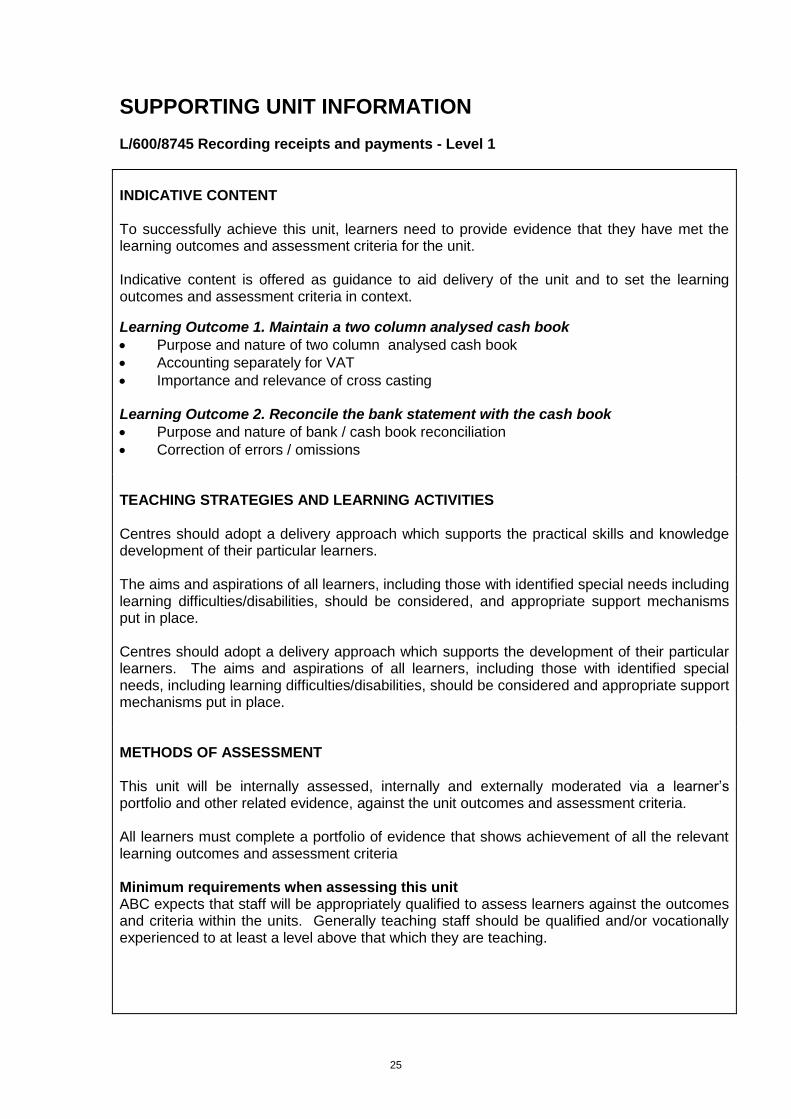

SUPPORTING UNIT INFORMATION L/600/8745 Recording receipts and payments - Level 1

INDICATIVE CONTENT To successfully achieve this unit, learners need to provide evidence that they have met the learning outcomes and assessment criteria for the unit. Indicative content is offered as guidance to aid delivery of the unit and to set the learning outcomes and assessment criteria in context.

Learning Outcome 1. Maintain a two column analysed cash book

Purpose and nature of two column analysed cash book

Accounting separately for VAT

Importance and relevance of cross casting Learning Outcome 2. Reconcile the bank statement with the cash book

Purpose and nature of bank / cash book reconciliation

Correction of errors / omissions TEACHING STRATEGIES AND LEARNING ACTIVITIES Centres should adopt a delivery approach which supports the practical skills and knowledge development of their particular learners. The aims and aspirations of all learners, including those with identified special needs including learning difficulties/disabilities, should be considered, and appropriate support mechanisms put in place. Centres should adopt a delivery approach which supports the development of their particular learners. The aims and aspirations of all learners, including those with identified special needs, including learning difficulties/disabilities, should be considered and appropriate support mechanisms put in place. METHODS OF ASSESSMENT This unit will be internally assessed, internally and externally moderated via a learner’s portfolio and other related evidence, against the unit outcomes and assessment criteria. All learners must complete a portfolio of evidence that shows achievement of all the relevant learning outcomes and assessment criteria Minimum requirements when assessing this unit ABC expects that staff will be appropriately qualified to assess learners against the outcomes and criteria within the units. Generally teaching staff should be qualified and/or vocationally experienced to at least a level above that which they are teaching.

26

EVIDENCE OF ACHIEVEMENT Evidence presented to support achievement is not prescribed for each learning outcome. It could typically include some of the following

Product evidence

Observation reports

Oral/written questions and answers

Reports/notes

Witness statements

Taped evidence (video or audio)

Photographic evidence

Case studies/assignments/projects

Interview/professional discussion

Pictorial identifications

Letters / emails seeking clarification / confirmation of understanding

Internet research / copies of items with relevant knowledge highlighted

This is not an exhaustive list and learners should be encouraged to develop the most appropriate evidence to demonstrate their achievement of the learning outcomes and assessment criteria. ADDITIONAL INFORMATION

See ABC web site for further information

27

Unit Title

R/600/8746 Maintaining petty cash records

Level

1

Credit Value

1

Guided Learning Hours

5

Unit Summary

For the learner to have a clear understanding of the principles and procedures related to the processing of petty cash transactions and the maintenance of the petty cash float known as the imprest

Learning Outcomes (1 to 3) The learner will

Assessment Criteria (1.1 to 3.4) The learner can

1. Complete a petty cash voucher

1.1 Prepare petty cash vouchers 1.2 Calculate the purchase tax (eg VAT) where the expense includes it

2. Maintain an analysed petty cash book

2.1 List the petty cash vouchers into an analysed petty cash book ensuring that the expenses are entered and analysed 2.2 Account for any tax paid eg VAT 2.3 Total and cross cast the petty cash book

3. Maintain the petty cash balance

3.1 Balance off the petty cash book using the imprest system 3.2 Reconcile the petty cash book with cash in hand 3.3 Prepare a petty cash reimbursement request or equivalent 3.4 Show the reimbursement of the petty cash expenditure in the petty cash book

Mapping to National Occupational Standards Direct relationship based on NOS for Accountancy and Finance FA-2 and FA-3

28

SUPPORTING UNIT INFORMATION R/600/8746 Maintaining petty cash records - Level 1

INDICATIVE CONTENT To successfully achieve this unit, learners need to provide evidence that they have met the learning outcomes and assessment criteria for the unit. Indicative content is offered as guidance to aid delivery of the unit and to set the learning outcomes and assessment criteria in context. Learning Outcome 1. Complete a petty cash voucher

Nature and purpose of petty cash vouchers

VAT fraction and decimal fraction

Importance of obtaining authorised petty cash voucher Learning Outcome 2. Maintain an analysed petty cash book

Nature and purpose of analysed cash booked

Accounting separately for sales tax Learning Outcome 3. Maintain the petty cash balance

Principles of the imprest system

Effective method of control

Principles of reconciliation TEACHING STRATEGIES AND LEARNING ACTIVITIES Centres should adopt a delivery approach which supports the practical skills and knowledge development of their particular learners. The aims and aspirations of all learners, including those with identified special needs including learning difficulties/disabilities, should be considered, and appropriate support mechanisms put in place. Centres should adopt a delivery approach which supports the development of their particular learners. The aims and aspirations of all learners, including those with identified special needs, including learning difficulties/disabilities, should be considered and appropriate support mechanisms put in place. METHODS OF ASSESSMENT

This unit will be internally assessed, internally and externally moderated via a learner’s portfolio and other related evidence, against the unit outcomes and assessment criteria. All learners must complete a portfolio of evidence that shows achievement of all the relevant learning outcomes and assessment criteria

29

Minimum requirements when assessing this unit ABC expects that staff will be appropriately qualified to assess learners against the outcomes and criteria within the units. Generally teaching staff should be qualified and/or vocationally experienced to at least a level above that which they are teaching. EVIDENCE OF ACHIEVEMENT Evidence presented to support achievement is not prescribed for each learning outcome. It could typically include some of the following

Product evidence

Observation reports

Oral/written questions and answers

Reports/notes

Witness statements

Taped evidence (video or audio)

Photographic evidence

Case studies/assignments/projects

Interview/professional discussion

Pictorial identifications

Letters / emails seeking clarification / confirmation of understanding

Internet research / copies of items with relevant knowledge highlighted

This is not an exhaustive list and learners should be encouraged to develop the most appropriate evidence to demonstrate their achievement of the learning outcomes and assessment criteria. ADDITIONAL INFORMATION

See ABC web site for further information

30

Recognition of Prior Learning (RPL), Exemptions, Credit Transfers and Equivalencies

The QCF enables learners to avoid duplication of learning and assessment in a

number of ways:

Recognition of Prior Learning (RPL) – a method of assessment that considers

whether a learner can demonstrate that they can meet the assessment

requirements for a unit through knowledge, understanding or skills they

already possess and do not need to develop through a course of learning.

Exemption - individuals with certificated achievements outside the QCF can

claim exemption from some of the achievement requirements of a QCF

qualification, using evidence of certificated, non-QCF achievement deemed to

be of equivalent value’.

Credit Transfer - for achievements within the QCF it is possible to transfer

credits awarded in the context of one QCF qualification or awarded by a

different awarding organisation towards the achievement requirements of

another QCF qualification. This would apply when a unit in one level is also

listed within another level/qualification and the unit has the same QCF

number.

Equivalencies – opportunities to count credits from the unit(s) from other

qualifications or from unit(s) submitted by other recognised organisations

towards the place of mandatory or optional unit(s) specified in the rule of

combination. The unit must have the same credit value or greater than the

unit(s) in question and be at the same level of higher.

ABC encourages its centres to recognise the previous achievements of learners

through Recognition of Prior Learning (RPL), Exemption, Credit Transfer and

Equivalencies. Prior achievements may have resulted from past or present

employment, previous study or voluntary activities. Centres should provide advice

and guidance to the learner on what is appropriate evidence and present that evidence

to the external moderator in the usual way.

Further guidance can be found in ‘Delivering and Assessing ABC Awards

Qualifications’ which can be downloaded from http://www.abcawards.co.uk/centres-

grid-page-move/policies-procedures/

Certification

Learners will be certificated for all units and qualifications that are achieved and claimed. ABC’s policies and procedures are available on the ABC website.

![Level 1 Award, Certificate and Diploma in Creative ... · Level 1 Award, Certificate and Diploma in Creative Techniques [7111] 1 Level 1 Award, Certificate and Diploma in Creative](https://img.dokumen.tips/doc/110x75/5ae4eff37f8b9a7b218f0872/level-1-award-certificate-and-diploma-in-creative-1-award-certificate-and.jpg)