Embed Size (px)

Citation preview

Lender Relations Division

ACCESS TO CAPITAL FOR

SMALL BUSINESSES Annie Hudspeth

Aixa [email protected]

210.403.5920

Lionel [email protected]

210.403.5917

Lender Relations Specialists

Lender Relations Division

U.S. Small Business Administration (SBA)

Mission Established on July 30, 1953 to aid, counsel, assist

and protect the interests of small business concerns; to preserve free competitive enterprise and to maintain and strengthen the overall economy of our nation.

SBA helps Americans start, build and grow their businesses.

SBA has the 3 Cs – Capital, Certification & Counseling

Lender Relations Division

Getting Started — Is Entrepreneurship for You?

Are you a self-starter?

How well do you get along with different personalities?

How good are you at making decisions?

Do you have the physical and emotional stamina to run a business?

How well do you plan and organize?

Is your drive strong enough?

How will the business affect your family?

Financing Your Business

Lender Relations Division

Financing Your Business

Teen Business Link

Young Entrepreneurs:http://www.sba.gov/content/youth-entrepreneurship-0

mindyourownbiz.org

Lender Relations Division

SBA Today

Experience the New SBA.gov!

The Answers You Need Starts Here:♦ SBA Direct

♦ Answers, Support and Resources for Your Small Business. Fast and Easy!

♦ Give you information and services based on your unique business needs

♦ Find Exporting Opportunities and much more…

Lender Relations Division

Financing Options for Small Businesses

Personal Savings Friend & Relatives Credit Cards Business Earnings Partners

Trade CreditInvestorsBanks/Credit UnionsSBAFactoring CompaniesMicro Loans

Lender Relations Division

Biggest Question Small Businesses ask… Does SBA have grants?

www.grants.govNon-profit agenciesEnvironment InventionsResearch & DevelopmentScience & Technology

Lender Relations Division

SBA Today Financial Assistance - SBA is a government guarantee

loan program offered through SBA participating lenders (banks and credit unions). SBA does not loan money directly.

SBA is the largest single financial backer of the federal government for the nation’s small businesses.

Used when a small business (start-up or existing) cannot obtain financing on bank terms but is still viable.

SBA participating Lenders play the Central Role between you and the SBA.

Lender Relations Division

Access to Capital

Grants NOT available from SBA

SBA offers loan guarantees to lenders Partial refund for defaulted loan Lender obtains guarantee

Lenders handle all loan transactions Application Approval Disbursement Servicing Collection

Lender Relations Division

Access to Capital

So Why Go With an SBA Guarantee??

Lender Relations Division

Access to Capital Not everyone needs an SBA Guarantee

SBA guaranteed loan programs provide an alternative

Used when a viable business cannot obtain financing through normal lending channels on reasonable terms.

If risk is too high –lender comes to SBA--guarantee reduces lender risk

SBA participating lenders play a Central Role between you and the SBA.

Lender Relations Division

7(a) Loan Program

Benefits for small business: Provides funding when financing is not otherwise

available on reasonable terms. Longer Terms Interest Rate not-to-exceed SBA maximums &

driven by prime-rate. SBA supports start-up position.

Lender Relations Division

SBA Comes to mind when…

Start-up Business Insufficient of Collateral Lower Than Normal Down

payment (Equity) Longer Term/Lower

Payments to Meet Debt Coverage

Riskier Industries (Entertainment, High-Tech, Service, Retail)

Uneven Historical Cash Flow

Tighter Debt Coverage Change of Ownership/

Management Lending Limits Reliance on Projections

Lender Relations Division

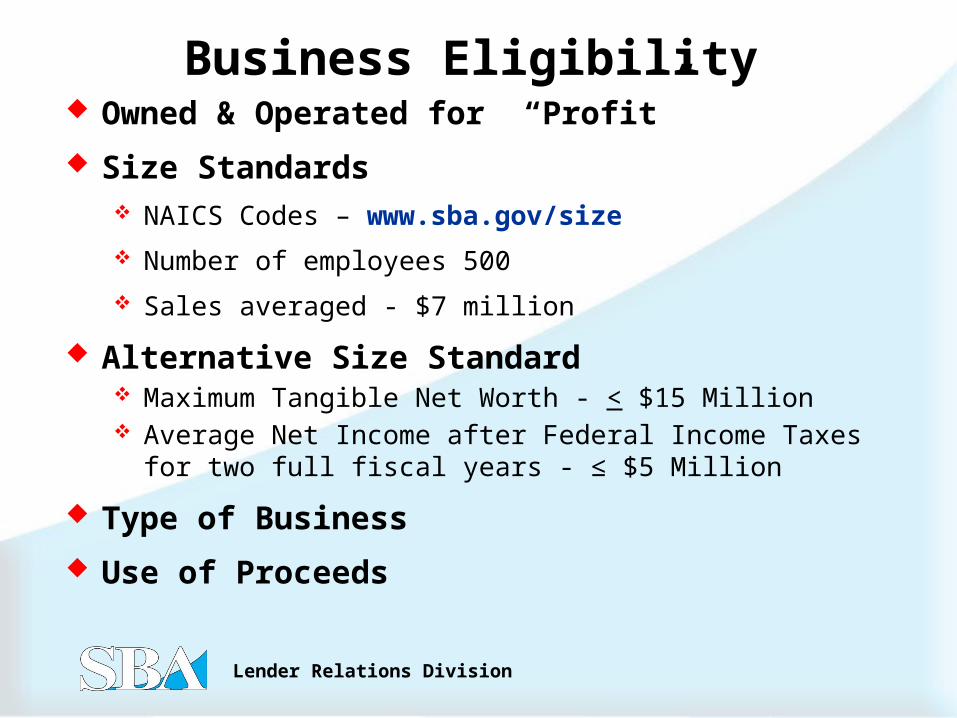

Business Eligibility Owned & Operated for “Profit”

Size Standards NAICS Codes – www.sba.gov/size

Number of employees 500

Sales averaged - $7 million

Alternative Size Standard Maximum Tangible Net Worth - < $15 Million Average Net Income after Federal Income Taxes for two full

fiscal years - ≤ $5 Million

Type of Business

Use of Proceeds

Lender Relations Division

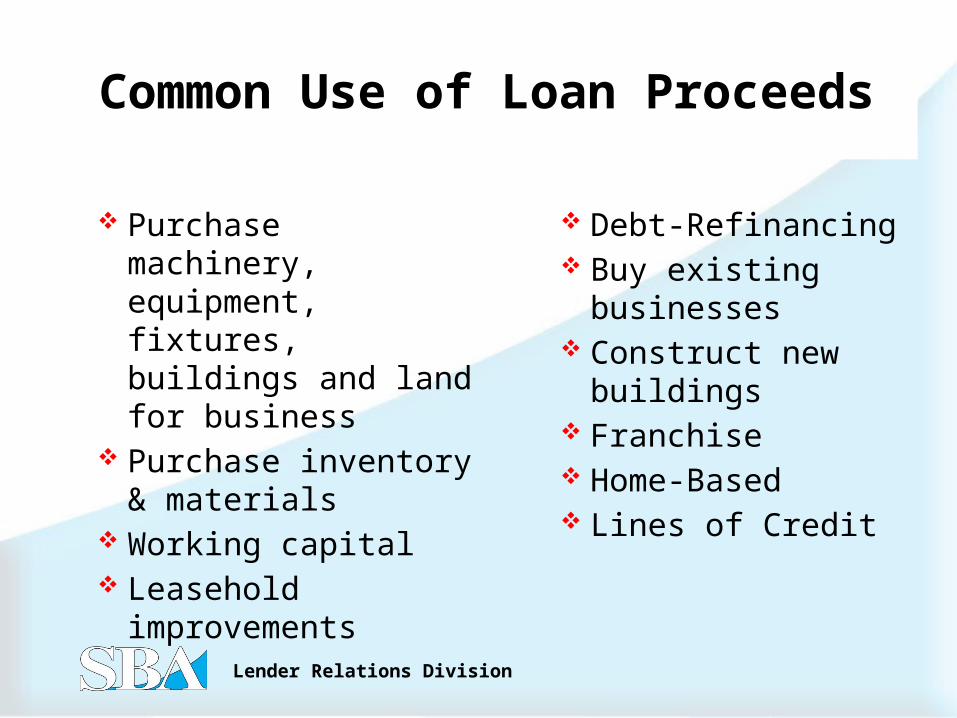

Common Use of Loan Proceeds

Purchase machinery, equipment, fixtures, buildings and land for business

Purchase inventory & materials

Working capital Leasehold

improvements

Debt-Refinancing Buy existing

businesses Construct new

buildings Franchise Home-Based Lines of Credit

Lender Relations Division

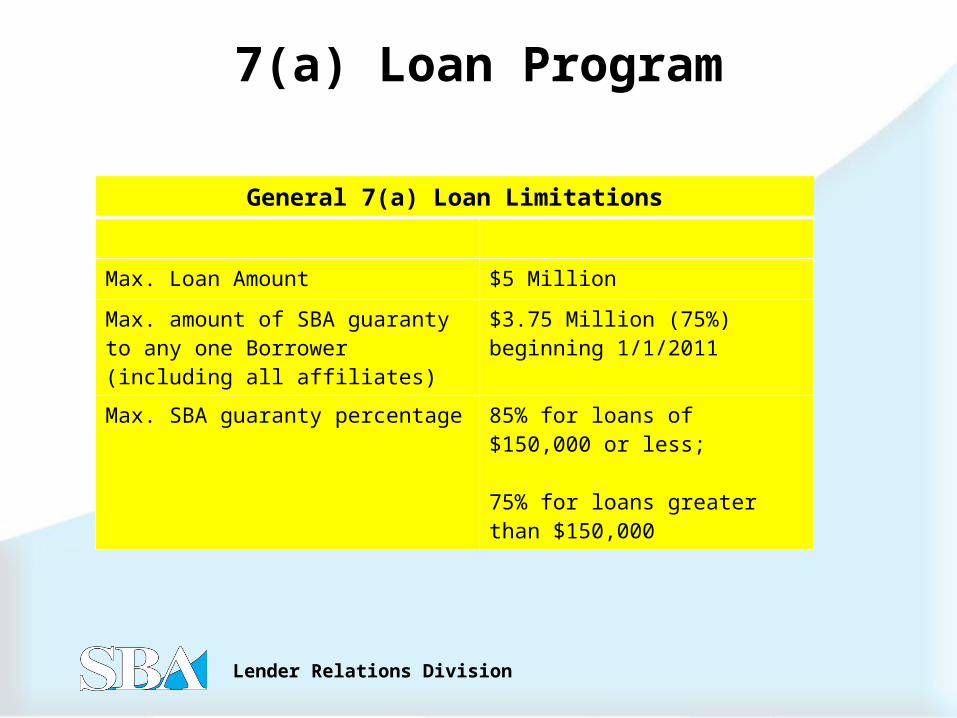

7(a) Loan Program

General 7(a) Loan Limitations

Max. Loan Amount $5 Million

Max. amount of SBA guaranty to any one Borrower (including all affiliates)

$3.75 Million (75%) beginning 1/1/2011

Max. SBA guaranty percentage 85% for loans of $150,000 or less;

75% for loans greater than $150,000

Lender Relations Division

7(a) Loan Program SBA Guaranty Fees Quick Reference Chart

Gross Loan Size Fees Notes

Loans of $150,000 or less Currently No Fee Maturities that exceed 12 months

$150,0001 to $700,000 3% of guaranteed portion

$700,001 to $5,000,000 3.5% of guaranteed portion up to $1,000,000 PLUS 3.75% of the guaranteed portion over $1,000,000

Short Term Loans – Up to $5,000,000

0.25% of the guaranteed portion Maturities of 12 months or less

Lender Relations Division

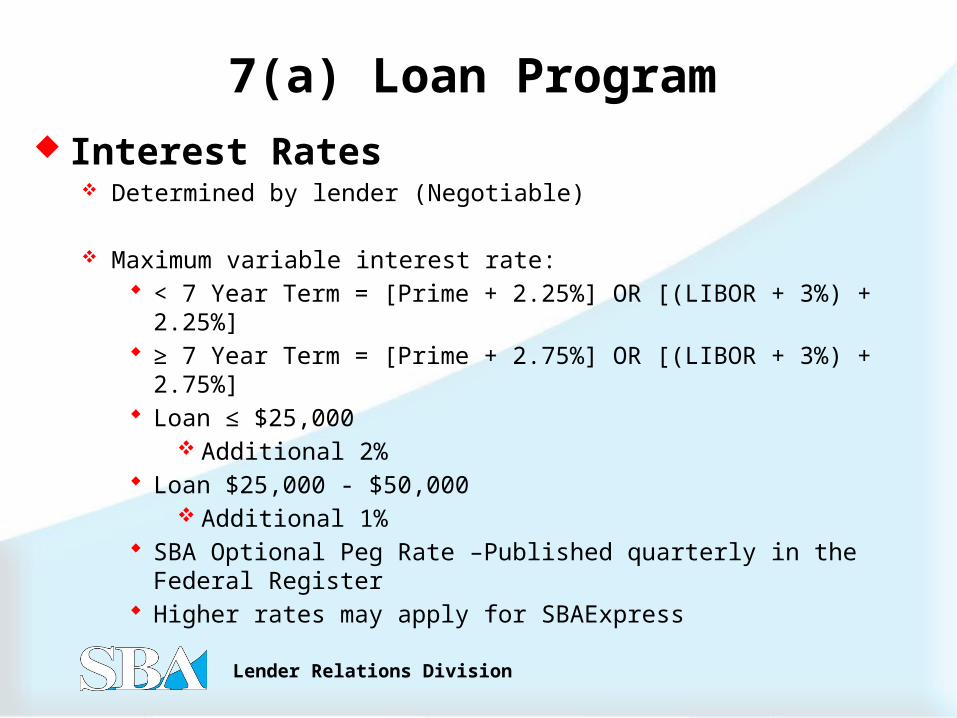

7(a) Loan Program Interest Rates

Determined by lender (Negotiable)

Maximum variable interest rate: < 7 Year Term = [Prime + 2.25%] OR [(LIBOR + 3%) + 2.25%] ≥ 7 Year Term = [Prime + 2.75%] OR [(LIBOR + 3%) + 2.75%] Loan ≤ $25,000

Additional 2% Loan $25,000 - $50,000

Additional 1% SBA Optional Peg Rate –Published quarterly in the Federal Register Higher rates may apply for SBAExpress

Lender Relations Division

Working Capital – will not typically exceed 7 years. In some cases may go up to 10 years.

Fixed Assets – other than real estate will be limited to the economic life of those assets.

Real Estate – will not typically exceed 20 years. In some cases may go up to 25 years.

Maturity

Lender Relations Division

7(a) Specialized Loan Programs

SBAExpress Loan Program – $350,000

Veteran’s Advantage Loan Program - $350,000 (No Fees up to $350,000)

Export Express Loan Program - $500,000

Small Loan Advantage - $350,000

Community Advantage 7(a) Loan - $250,000

Non-7(a) Loans:

CDC/504 Loan Program $5,000,000 up to $5.5 million

Microloans - $50,000

Lender Relations Division

Community Advantage Community Advantage - is a pilot initiative aimed at

increasing the number of SBA 7(a) lenders who reach underserved communities, targeting mission-focused financial institutions which were previously not able to offer SBA loans. Maximum Loan Size: $250,000 Guaranty: 85 percent for loans up to $150,000 and 75 percent

for those greater than $150,000.

Underserved Communities are small businesses in or that have more than 50 percent of their workforce residing in low-to-moderate income (LMI) communities; in Empowerment Zones and Enterprise Communities; in HUBZones; start-ups (firms in business less than 2 years); and veteran-owned businesses and those that would be eligible for Patriot Express.

Lender Relations Division

504 Loan Program

504 Loan Limitations

Maximum Loan Amount (generic 504) $5 Million

Maximum Loan Amount if a public policy goal $5 Million

Maximum Loan Amount if a small manufacturer $5.5 Million

Maximum Loan Amount if at least 10% reduction in borrower’s energy consumption

$5.5 Million

Maximum Loan Amount if project generates renewable energy or renewable fuels, such as biodiesel or ethanol production

$5.5 Million

Lender Relations Division

CDC/504 Program

Long-term financing program Land and Existing Buildings Renovate or Expand Existing Facility New Building Construction Acquire/Install Machinery and Equipment Debt refinancing opportunity for expansion projects Soft Costs may be rolled into the project financing (i.e.

appraisal, environmental assessments, interest on interim loan, etc.)

Access through Certified Development Company (CDC)

Lender Relations Division

CDC/504 Program

Business Eligibility For Profit ≤ 500 Employees Job creation and retention Net Worth ≤ $8.5 Million Net Income After Taxes ≤ $3.0 Million

Max Debenture CDC/504 Loan Amount $5.0M for regular 504 loans $5.0M - businesses that meet specific public policy goals $5.5M - for manufacturers, business reducing energy

consumption by @ least 10% and for plant, equipment and process upgrades of renewable energy resources.

Lender Relations Division

CDC/504 Program Typical Structure

Lender 50% 504 Program 40% Owners’ Equity 10% Special circumstances

Single purpose building +5% Owners’ Equity Start-up business +5% Owners’ Equity

Interest Rates 504 portion typically close to Prime Rate 504 portion fixed interest rate

Longer Repayment Term Heavy Machinery/Equipment 10 Years Real Estate 20 Years

Refinance Option Eligible up to 50% of the new project costs

Lender Relations Division

Special Purpose Building Examples

Special use or special purpose properties include: theaters, sports arenas, schools, dormitories, cold storage

plants, tennis clubs, golf courses, marinas, gasoline service stations, automatic car wash properties, hospitals, medical centers, nursing homes, funeral homes, cemeteries, historic properties, sanitary landfills, museums, clubhouses, and some recreational properties.

Generally, SBA considers hotels or motels to be included as a special-use or special-purpose property.

Lender Relations Division

Community Development and/or Public Policy Goals

Aiding Rural Development Promoting Women, Minority, or Veteran-Owned Businesses Expanding Exports Revitalizing Economic Development Districts Restructuring due to Federally Mandated Standards and/or Policies Modernizing Manufacturing Facilities – may go up to $5.5 million Job creation is not waived on manufacturing Changes Necessitated by Federal Budget Cutbacks Retrofitting to Save on Energy Consumption – may go up to $5.5 million Production of Alternative Energy Sources

Opportunity to fund up to $5.0 Million and requirement to Create one job for each $65,000 is waived

Opportunity to fund up to $5.0 Million and requirement to Create one job for each $65,000 is waived

Lender Relations Division

Recent Addition: Energy Efficiency (GO GREEN)

Max Debenture CDC/504 Loan Amount $5.5M Project reduces borrower’s energy consumption by at least 10%

Project generating renewable energy fuels

Biodiesel or ethanol production

Projects that meet above criteria can qualify without job creation

and retention requirement, so long as the CDC portfolio average is

at least $50,000

CDC/504 Program

Lender Relations Division

Microloan Program

Accessed through SBA Microloan Intermediaries

Intermediaries Borrow Dollars from SBA and Lend Directly to Borrowers

Use of Proceeds Working Capital Machinery and Equipment/Inventory Leasehold Improvements

Cannot be used for down payment of or to purchase real estate

Lender Relations Division

Microloan Program Maximum loan amount

Up to $50,000

Eligibility Same as 7(a) Criteria

Maturity Short-term, Not to Exceed 6 Years

Fixed Interest Rates Negotiable

Lender Relations Division

Disaster Assistance

Loans for Federal Declared Disaster Zones Business Homeowners Renters *Not for secondary homes or vacation properties

Physical Damage Max $200,000 – Home Loans Max $40,000 - Personal Property Loans

Business Max $2.0M – Business Loans

Economic Injury Disaster Loans Terms

Interest rates - typically 2 - 4% Up to 30 years

Lender Relations Division

Common Ineligible Businesses or Situations

Non-Profit Financial Institutions Investment Companies Limited Membership Clubs Over 1/3 of Revenues from

Legal Gambling Default on Federal Loans Delinquent Withholding

Federal Taxes

Probation, Parole, or Pending criminal charges

Pyramid Sales Plans Race Tracks Gambling & Illegal

Activities Religious Teaching Sexual Nature Delinquent in Child

Support (60-90 days)

Lender Relations Division

What Lenders Look For… 5 Cs of Credit

Character - Background, Education, Experience, Credit

Capacity - Source of RepaymentCollateral - Assets you own Capital - Money you have investedConditions - Your Industry

Also…Debt Position (both Business & Personal)Sound Business Plan

Lender Relations Division

Business Plan classes are offered by SBA resource partners i.e. SCORE, UTSA-SBDC And Women’s Business Centers or you may go to www.sba.gov for sample module and on-line class.

The BUSINESS PLAN will be your FINANCIAL PROPOSAL as a startup business and potential borrower especially for those larger loan amounts.

Adds creditability!

Presentation-Presentation-Presentation!

Lender Relations Division

SBA Today Federal Procurement Assistance - Committed to increase business

participation to women, veterans, and minorities

Central Contractor Registration – http://www.sams.gov

8(a) Business Development Program - Offers a broad scope of assistance to socially and economically disadvantaged firms, helping these entrepreneurs to compete in the Federal contracting arena. http://www.sba.gov/aboutsba/sbaprograms/8abd/index.html

SBA HUBZone Empowerment Program ("Historically Underutilized Business Zone”) - Designed to promote economic development and employment growth in economically distressed areas - Are you in a HUBZone? http://www.sba.gov/hubzone

Mentor Protégé Program - Allows start-up companies to learn the ropes from experienced businesses. http://www.sba.gov/aboutsba/sbaprograms/8abd/mentorprogram/index.html

New! Women-Owned Small Business Program – authorizes contracting officers to specifically limit, or set aside, certain requirements for competition solely amongst women-owned small businesses (WOSBs) or economically disadvantaged women-owned small businesses (EWOSBs). www.sba.gov/wosb

Lender Relations Division

SBA Today Surety Bond Guarantee Program - A surety bond is a type of insurance

that guarantees performance of a contract. If one party does not fulfill its end of the bargain, then the surety bond provides financial compensation to the other party. Bid Bond – guarantees the bidder will enter into a contract and

provide the required performance and payment bond Performance Bond: guarantees the contract will be completed in

accordance with terms, conditions and specifications. Payment Bond: guarantees the contractor will pay all contract

suppliers and vendors. Any Federal Construction contract valued at $100,000+ requires a surety

bond as a condition of contract award. Most State & municipal governments have similar requirements, as well as private entities. Many service contracts, and occasionally, supply contracts, also require surety bonds.

A list of surety companies and agents who participate in the SBA Surety Bond Guarantee Program are provided at http://www.sba.gov/content/surety-bonds-explained

Lender Relations Division

SBA Today

Management & Technical Assistance –SBA Resource Partners Nationwide

(Free confidential One-on-One Counseling Services, Education and Training)

SCORE counselors Small Business Development Centers Women’s Business Centers International Trade Centers – Specialized in Export/Import

SBA together with our resource partners are able to reach, teach and educate potential business owners in our 55 counties territory.

Lender Relations Division

SBA Today

Start-Up Businesses Business PlanFinancial ProjectionsFinancing Assistance

Existing Businesses Managing & Growing a New

BusinessDeveloping New MarketsFinancing AssistanceAccounting IssuesHuman ResourcesInternational TradeAnd much more…

What SBA Resource Partners Can Do For You…

Lender Relations Division

Summary STEP 1

Research the feasibility of starting up or expanding a business. Do your homework!

STEP 2 Prepare Business Plan/Financial Proposal

STEP 3 Approach Lender for Loan Request

STEP 4 Ask Lender regarding an SBA guaranty loan.

If yes, Lender will help you with the application process.

Lender Relations Division

Questions