Embed Size (px)

Citation preview

mergermarket M&A Round-up for Q1-Q3 2012 8 October 2012 for immediate release

press releasePRESS CONTACTS

EMEA: Flora Wilke

fl [email protected]: +44 207 059 6348

Americas: Dara Silverstein

[email protected]: +1 646 3783118

Asia-Pacifi c: Jessica Chan

[email protected]: +852 21589706 www.mergermarket.com

Global M&A in Q1-Q3 2012 down 17.4% compared to same period last year • Q3 2012 total of US$ 461bn, down 16.1% from Q2 2012 • Q3 2012 resumed freefall from Q4 2010 after brief spike in Q2 • Energy, Mining & Utilities saw 26.1% of total global deal value this year

Clifford Chance tops global and Europe advisory league tables for Q1-Q3 2012 • Clifford Chance jumped 15 places from its Q1-Q3 2011 fi nish to claim top spot in the global legal adviser league table • Skadden Arps Slate Meagher & Flom moved up three places to fi nish top of the Americas legal adviser league table • Freshfi elds Bruckhaus Deringer Citigroup jumped six places to achieve top rank in Asia Pacifi c (excl. Japan)

mergermarket Heat Charts reveal TMT as the most popular “Companies for sale” sector globally • Industrials & Chemicals and the Consumer sector dominate both the CEE and Germanic region • TMT maintained top post in the US Heat Chart • Industrials & Chemicals led in the Asia-Pacifi c, mainly in Greater China

European M&A in the fi rst nine months of 2012 down 22.6% on Q1-Q3 2011 • Europe posted lowest quarter since Q3 2009 • Germanic region remained the most active in Europe with 27.5% market share • Construction saw 48.7% pickup in activity compared to Q1-Q3 2011

US takes brunt of slide with year-to-date total 18.6% lower than this time last year • Q3 2012 US M&A totalled US$ 206.7bn, up 4.8% on Q3 2011 • Q1-Q3 2012 down 18.6% from Q1-Q3 2011 • Industrials & Chemicals saw sharp decline of 51.9% from Q1-Q3 2011

Asia-Pacifi c fi rst nine months M&A down 13.2% on Q1-Q3 2011 • Third quarter total of US$ 89.5bn, up 16.6% on Q2 2012 • Indonesia Q1-Q3 2012 deals recorded biggest rise, up 185.3% on Q1-Q3 2011 • South Korea and Australia down 47% and 43.9% respectively in 2012 so far

Private Equity buyouts in Q1-Q3 2012 down 22.8% year to date • Value of buyouts for Q3 2012 down 27.8% on Q3 2011 • European buyouts at third lowest Q3 level on mergermarket record • US buyouts in Q3 up 18.9% compared to same period last year

Emerging Markets deals down by 22.9% since last year • BRICs witness lowest quarterly total since Q1 2009 • 33.2% drop in inbound investment from Europe in Q1-Q3 2012 • European bidders are most active investors

Energy, Mining & Utilities increased dominant market share in Q1-Q3 2012 • However activity fell by 7.6% on Q1-Q3 2011 • Inbound European deals boosted Construction and Transport in the region • Emerging Markets saw growth in Technology by 94.3%

CONTENTS:

2 mergermarket M&A Round-Up

3 Global M&A Overview

7 - Mid-Market 8 - Private Equity Buyouts9 - Private Equity Exits 10 - Emerging Markets 11 - Premia / Multiples Analysis12 - Consideration Structure

Insolvency13 - Deal Value Breakdown14 - Global League Table of Legal

Advisers16 - European M&A Overview

29 - US M&A Overview

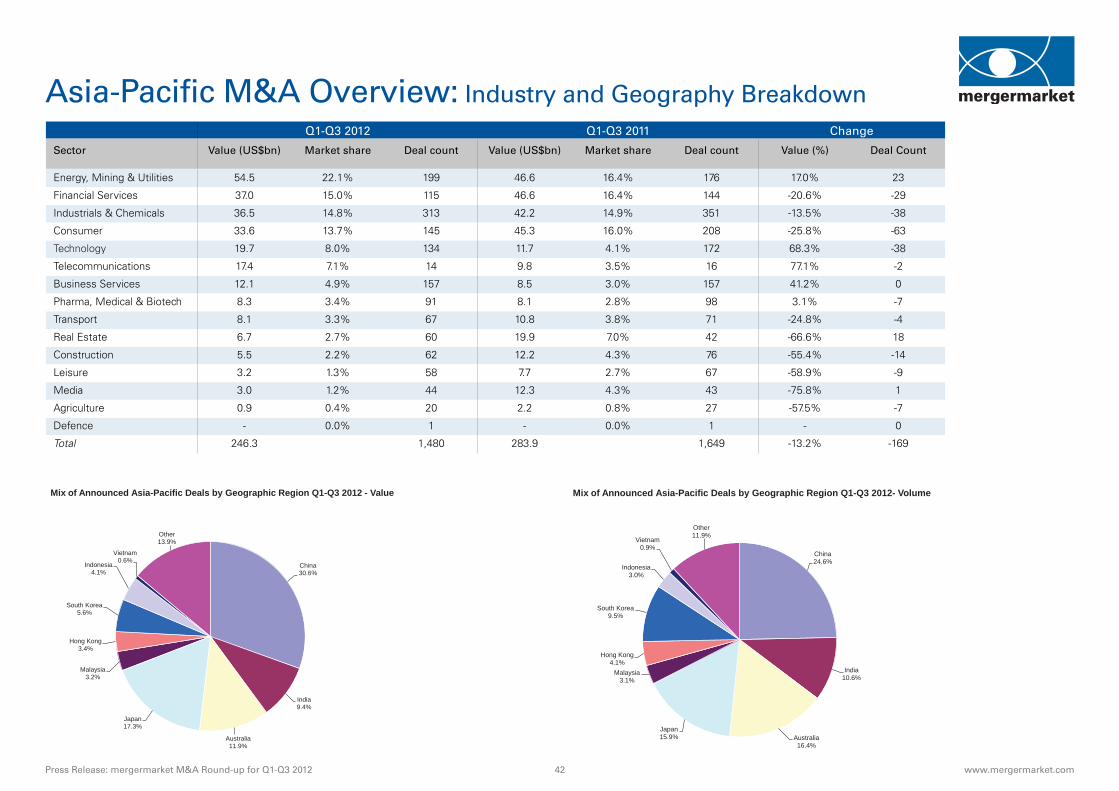

39 - Asia-Pacifi c M&A Overview (ex. Japan)

49 - Africa & MIddle East M&A Overview

53 - Criteria/ About mergermarket

MEDIA CONTACTS:EMEA: Flora Wilke

+44 207 059 6348

Americas: Dara Silverstein

+1 646 378 3118

Asia-Pacifi c: Jessica Chan

+852 2158 9706

mergermarket M&A Round-up for Q1-Q3 2012

Press Release: mergermarket M&A Round-up for Q1-Q3 2012 2 www.mergermarket.com

• Q3 2012 global M&A at US$ 461bn, down 16.1% from Q2 2012 • Q1-Q3 2012 total of US$ 1,461.1bn, down 17.4% on the same period in 2011 • Drastic decline in Europe of 46.1% from the previous quarter • Asia-Pacifi c and US regions see quarter-on-quarter increase by 16.6% and

11.7% respectively

Global M&A in the fi rst three quarters of 2012 added up to US$ 1,461.1bn, down by 17.4% on the same period in 2011 (US$ 1,769bn), and representing the second lowest total since Q1-Q3 2009 (US$ 1,142bn). Q3 2012 totaled US$ 461bn, down 16.1% from Q2 2012 (US$ 549.7bn), resuming the freefall briefl y paused by a rally in Q2. The third quarter was also the second lowest Q3 since 2004 (US$ 343.4bn)

The fi nancial crisis is evident within the European M&A market as it has seen its slowest quarter in three years. Q3 2012 M&A in Europe totaled US$100.3bn, down 46.1% on Q2 2012 (US$ 186.3bn) and a 39.3% decrease on Q3 2011 (US$ 165.2bn). The fi rst nine months added up to US$ 457.5bn, a decrease of 22.6% compared to the same period last year, and the lowest since Q1-Q3 2010 (US$ 399.9bn).

The US, with US$ 512.1bn worth of M&A deals announced in Q1-Q3 2012 saw a decrease of 18.6% on the same period in 2011 (US$ 628.8bn), but registered a quarter-on-quarter in-crease of 11.7%, with Q3 2012 M&A coming in at US$ 206.7bn. The quarter was boosted by Kraft Food’s US$ 26.3bn spin-off of its North American business accounting for a sizeable chunk of this. This also ensured that US made up the largest share of global M&A of any region; it accounted for 35% of total deal value in the fi rst nine months of 2012.

The Asia-Pacifi c region has seen M&A deals in 2012 adding up to US$ 246.3bn, down 13.2% on Q1-Q3 2011. For Q3 2012, Asia-Pacifi c showed an increase in activity by 16.6% from the previous quarter (US$ 76.8bn).

Q3 2012 saw US$ 191.5bn-worth of cross-border deals, down 23.2% from the previous quarter (US$ 249.5bn) and 15% from the same period last year (US$ 225.3bn). Cross-border deals accounted for 41.5% of all global M&A (US$ 461bn) last quarter. Deals between re-gions added up to US$ 138.7bn in Q3 2012 and accounted for 30.1% of all global M&A. They were down 21.4% from Q2 2012 (US$ 176.4bn), and 10.7% from the same period last year.

Energy, Mining & Utilities saw a drop in deal value in Q1-Q3 2012 compared to the same period last year, but remained the most active sector in global M&A and increased its mar-ket share. The sector registered US$ 380.9bn-worth of deals, down 7.7% from the fi rst three quarters of 2011 (US$ 412.5bn), but market share increased from 23.3% to 26.1%.

Clifford Chance claimed the Q1-Q3 2012 global legal advisers mantle, by deal value, after climbing 15 places from its Q1-Q3 2011 fi nish. DLA Piper won the day by claiming top spot for the deal volume crown.

Global M&A Overview

0

100

200

300

400

500

600

700

800

900

1,000

1,100

1,200

1,300

1,400

1,500

Valu

e of

Dea

ls (U

S$bn

)

Global Cross Border M&A Analysis - Value

Global Cross Border (regions) Global M&A Global Cross Border (individual countries)

Press Release: mergermarket M&A Round-up for Q1-Q3 2012 3 www.mergermarket.com

©2012 Google - Map data © 2012 Google

Global M&A Heat ChartSector Americas Asia Europe Africa Middle

EastTotal

TMT 1,278 680 621 17 71 2,667

Industrials & Chemicals 473 1,031 705 22 20 2,251

Energy, Mining & Utilities 947 666 445 102 27 2,187

Consumer 572 575 637 22 16 1,822

Pharma, Medical & Biotech 682 310 308 3 29 1,332

Business Services 528 280 293 13 15 1,129

Financial Services 409 328 317 54 23 1,131

Leisure 246 204 232 6 13 701

Transportation 167 176 193 8 14 558

Construction 71 176 173 20 6 446

Defence 71 5 22 2 2 102

Real Estate 67 205 95 14 12 393

Agriculture 50 135 43 6 2 236

Government 16 2 9 27

Other 6 31 10 2 49

Total 5,583 4,804 4,103 291 250 15,031

Hot Warm Cold

1,000 300 50

650 200 20

500 100 0

Note: The Intelligence Heat Chart are based on “companies for sale” tracked by mergermarket in the respective regions between 12 March 2012 and 11 September 2012. Opportunities are captured according to the dominant geography and sector of the potential target company. mergermarket’s Heat Chart of predicted deal flow is based on the intelligence collected in our database relating to companies rumoured to be for sale, or officially up for sale in the respective regions. It is therefore indicative of areas that are likely to be active in the months to come. The intelligence comes from a range of sources, including press reports, company statements and our own team of journalists gathering proprietary intelligence from M&A across the regions. The data does not differentiate between small and large transactions, nor between deals that could happen in the short or long-term.

The derailment of the economic recovery has led to signifi cant declines in the M&A market. Two major factors are still affecting M&A right now: the wide bid-ask spread and the likelihood of completion. With all of the uncertainty on the macro level, corporates are taking a wait-and-see attitude. For the M&A fl oodgates to open some large corporate trans-action announcements will be required.

Expectations based on “Companies for sale” analysis are:

• North America to dominate, followed by Europe. • Americas to see TMT focus, possibly indicating a move towards an anticipated consolidation within the sector. • Industrials & Chemicals sector to maintain its top position in Asia and Europe. • Energy, Mining & Utilities sector to lead in the African region (whilst second in the Americas, third in Asia and fourth in Europe).

Press Release: mergermarket M&A Round-up for Q1-Q3 2012 4 www.mergermarket.com

Global M&A Overview: Industry and Geography Breakdown

North America 32.7%

Central & South America 5.0%

Western Europe 24.8%

Southern Europe 5.5%

Northern Europe 5.7%

Central & Eastern Europe 4.2%

North Asia 7.8%

Japan 3.2%

Australasia 3.8%

South & Central Asia 2.3%

South East Asia 2.8%

Africa & Middle East 2.5%

Mix of Announced Deals by Geographic Region Q1-Q3 2012 - Volume

North America 40.8%

Central & South America 5.6%

Western Europe 20.8%

Southern Europe 5.4%

Northern Europe 2.5%

Central & Eastern Europe 2.6%

North Asia 8.5%

Japan 3.5%

Australasia 2.6%

South & Central Asia 2.1%

South East Asia 3.6%

Africa & Middle East 2.0%

Mix of Announced Deals by Geographic Region Q1-Q3 2012 - Value

Q1-Q3 2012 Q1-Q3 2011 Change

Sector Value (US$bn) Market share Deal count Value (US$bn) Market share Deal count Value (%) Deal Count

Energy, Mining & Utilities 380.9 26.1% 863 412.5 23.3% 912 -7.6% -49

Consumer 196.6 13.5% 1,163 148.2 8.4% 1,308 32.6% -145

Industrials & Chemicals 187.1 12.8% 1,814 308.4 17.4% 1,954 -39.3% -140

Financial Services 148.6 10.2% 752 207.6 11.7% 878 -28.4% -126

Pharma, Medical & Biotech 108.3 7.4% 652 164.4 9.3% 785 -34.1% -133

Technology 97.8 6.7% 966 113.0 6.4% 1,063 -13.4% -97

Business Services 80.1 5.5% 1,025 83.0 4.7% 1,270 -3.6% -245

Telecommunications 59.1 4.0% 91 94.9 5.4% 118 -37.8% -27

Real Estate 51.3 3.5% 186 90.2 5.1% 169 -43.1% 17

Transport 42.2 2.89% 291 40.2 2.3% 318 5.1% -27

Media 33.7 2.3% 296 34.9 2.0% 306 -3.4% -10

Leisure 30.3 2.1% 319 34.6 2.0% 355 -12.3% -36

Construction 26.9 1.8% 314 25.4 1.4% 380 6.1% -66

Agriculture 10.9 0.7% 91 6.1 0.3% 114 78.3% -23

Defence 5.3 0.4% 29 5.9 0.3% 29 -10.2% 0

Total 1,459.1 8,852 1,769.3 9,959 -17.5% -1,107

Press Release: mergermarket M&A Round-up for Q1-Q3 2012 5 www.mergermarket.com

Global Top Deals for Q1-Q3 2012Top 10 Announced Deals for Q1-Q3 2012

Announced Date

Bidder Company Bidder Legal Adviser Target Company Target/Seller Legal Adviser Seller Company Deal Value (US$m)

07-Feb-12 Glencore International plc Clifford Chance (Advising Citigroup; Credit Suisse; Morgan Stanley); Linklaters

Xstrata Plc (65.92% Stake) Freshfields Bruckhaus Deringer; King & Wood Mallesons

50,563

14-Aug-12 Kraft Foods Inc (shareholders) Kraft Foods Group Inc Clifford Chance; Cravath Swaine & Moore

Mondelez International Inc 26,294

04-Apr-12 Conocophillips Company (shareholders)

Phillips 66 Bracewell & Giuliani ConocoPhillips Company 20,790

29-Jun-12 Anheuser-Busch InBev NV Alston & Bird (Advising Barclays); Clifford Chance; Freshfields Bruckhaus Deringer; Mijares, Angoitia, Cortes y Fuentes; Skadden Arps Slate Meagher & Flom; Sullivan & Cromwell

Grupo Modelo SAB de CV (49.7% Stake)

Cravath Swaine & Moore; Creel, Garcia-Cuellar, Aiza y Enriquez; Greenberg Traurig (Advising Morgan Stanley)

20,100

23-Jul-12 China National Offshore Oil Corporation Ltd

Cleary Gottlieb Steen & Hamilton (Advising Citigroup); Davis Polk & Wardwell; Herbert Smith; Morrison & Foerster; Stikeman Elliott

Nexen Inc Blake, Cassels & Graydon; Osler, Hoskin & Harcourt (Advising Goldman Sachs; RBC Capital Markets); Paul Weiss Rifkind Wharton & Garrison

17,654

04-Jul-12 Volkswagen AG Clifford Chance; Hogan Lovells; White & Case

Dr Ing hc F Porsche AG (50.1% Stake)

Freshfields Bruckhaus Deringer; Hengeler Mueller

Porsche Automobil Holding SE 14,238

22-Aug-12 China Telecom Corporation Limited

Freshfields Bruckhaus Deringer; Sullivan & Cromwell

China Telecommunication Corporation (certain CDMA Network assets)

China Telecommunications Corporation

13,307

21-May-12 Nuclear Damage Compensation Facilitation Corporation

Anderson Mori & Tomotsune (Advising Nomura Holdings); Mori Hamada & Matsumoto (Advising JPMorgan); Nishimura & Asahi

Tokyo Electric Power Co Inc (75.7% Stake)

Nagashima Ohno & Tsunematsu 12,600

21-May-12 Eaton Corporation A&L Goodbody; Davis Polk & Wardwell (Advising Citigroup; Morgan Stanley); Kinstellar; Matheson Ormsby Prentice; McCann FitzGerald (Advising Citigroup; Morgan Stanley); Simpson Thacher & Bartlett

Cooper Industries Plc Arthur Cox; Blake, Cassels & Graydon; Cleary Gottlieb Steen & Hamilton (Advising Goldman Sachs); Slaughter and May; Wachtell, Lipton, Rosen & Katz

11,940

23-Apr-12 Nestle SA A&L Goodbody; King & Wood Mallesons; Mayer Brown; White & Case

Pfizer Nutrition Baker & McKenzie; Clifford Chance; DLA Cliffe Dekker Hofmeyr; DLA Piper; Kirkland & Ellis (Advising Centerview Partners); Lee and Li Attorneys at Law; McCann FitzGerald; Skadden Arps Slate Meagher & Flom

Pfizer Inc 11,850

Press Release: mergermarket M&A Round-up for Q1-Q3 2012 6 www.mergermarket.com

Global M&A Overview: Mid-market M&A Activity • Global mid-market M&A in 2012 declined to US$ 558.2bn, the third lowest

level since 2005 • Energy, Mining & Utilities sector with top market share of 23.3%, a 11.9%

decrease on Q1-Q3 2011 • Latham & Watkins topped legal advisers ranking with US$ 38.9bn in deals

Global mid-market M&A transactions for the fi rst three quarters of 2012 added up to US$ 558.2bn, 11.9% less than Q1-Q3 2012 (US$ 633.8bn), making it the third lowest Q1-Q3 period since 2005 (US$ 536bn). The third quarter saw mid-market deals valuing US$ 175.5bn, down by 17.9% from the previous quarter (US$ 213.9bn). The proportion of total global M&A accounted for by the mid-market, however, was roughly level: 38.1% (of US$ 461bn) in Q3, slightly down from 38.9% (of US$ 549.7bn) in Q2.

Most major regions saw a signifi cant downturn in mid-market deals. The drop-off was most pronounced in Africa and the Middle East (38.6% decrease on Q1-Q3 2011), but Asia-Pacifi c (ex Japan) and Europe also experienced decreases of 29.3% and 24.8% respectively. The US was the only major economy seeing an increase – of 12.1% – on Q1-Q3 2011. The Energy, Mining & Utilities sector accounted for 23.3% of total mid-market activity so far this year, with deal values totalling US$ 130.3bn, down by 11.9% on the same period in 2011 (US$ 147.9bn).

The acquisition of Vivint Inc by Blackstone Group, a deal valued at US$ 2bn, was the largest mid-market M&A transaction announced in Q3, followed by the acquisition of Veolia ES Solid Waste by Highstar Capital for US$ 1.9bn.

Latham & Watkins was involved in more mid-sized deals than any other legal advisors and topped the mid-market legal adviser league table with US$ 38.9bn-worth of deals.

Energy, Mining & Utilities 23.3%

Industrials & Chemicals 12.7%

Consumer 12.0%

Financial Services 10.2%

Technology 8.2%

Pharma, Medical & Biotech 7.2%

Business Services 6.2%

Real Estate 5.0%

Leisure 3.6%

Transport 3.4%

Media 2.5%

Construction 1.8%

Telecom 3.0%

Agriculture 0.2%

Mid-Market M&A Industry Breakdown Q1-Q3 2012 - Value

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

0

50

100

150

200

250

300

350

Valu

e of

Dea

ls (U

S$bn

)

Global Mid-Market M&A Activity - Quarterly

RoW M&A Asia-Pacific ex Jp Mid-Market M&A US Mid-Market M&A European Mid-Market M&A % of Global M&A

% o

f Glo

bal M

&A

Global mid-market Legal Adviser League Tables Q1-Q3 2012Ranking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2012

Q1-Q3 2011 Company Name

Value (US$bn)

Deal Count

Value (US$bn)

% Val. Change

1 3 Latham & Watkins 38.9 55 44.3 -12.2%2 9 Sullivan & Cromwell 36.2 40 32.7 10.8%3 2 Skadden Arps Slate Meagher &

Flom36.1 50 46.3 -22.1%

4 6 Simpson Thacher & Bartlett 35.2 44 37.6 -6.3%5 5 Freshfields Bruckhaus Deringer 35.1 47 41.7 -15.8%6 1 Linklaters 33.3 50 49.0 -32.1%7 4 Clifford Chance 33.0 50 43.6 -24.3%8 10 Kirkland & Ellis 30.8 44 32.4 -5.2%9 12 Cleary Gottlieb Steen & Hamilton 30.7 36 31.1 -1.5%10 7 Allen & Overy 29.0 40 37.2 -22.0%

Press Release: mergermarket M&A Round-up for Q1-Q3 2012 7 www.mergermarket.com

• Global buyouts for Q3 2012 down 27.8% on Q3 2011 and down 22.8% year-to-date

• Europe suffered third lowest Q3 on mergermarket record but US Q3 was up 18.9% on 2011

• Latham & Watkins was leading advisor with US$ 25.3bn in deal value

Global buyouts in Q1-Q3 2012 totalled US$ 176.1bn, down 22.8% compared to the same period in 2011 (US$ 228.0bn). Activity in Europe fell to US$ 62.5bn, a 29.5% drop from the US$ 88.6bn announced in 2011. Asia-Pacifi c (excluding Japan) fared worse with a 41.2% decline to US$ 18.1bn year-to-date.

12.7% of total global M&A in Q3 this year was attributable to private equity buyouts, standing at US$ 58.6bn. This was the lowest value for global Q3 buyouts since 2009 (US$ 24.4bn). Eurozone unsettlement contributed to a 39.9% drop from Q2 in European buyouts (from US$ 23.3bn to US$ 14bn), the largest drop between these quarters since 2007.

The availability of cheap debt in the US made room for more buyouts, borne out by a 18.6% increase in the total value of US buyouts in Q3 2012 (US$ 31.9bn) as compared with Q3 2011 (US$ 26.9bn). Total US buyouts (US$ 82.2bn) in 2012 have accounted for 46.7% of global buyouts, a modest 4.8% decline from the same time in 2011 (US$ 86.3) when com-pared with other regions.

The Carlyle Group made the largest deal in Q3 when acquiring DuPont Performance Coat-ings from E. I. du Pont de Nemours and Company in a deal valued at US$ 4.9bn.

Latham & Watkins tops the legal advisers ranking by value, advising on 36 deals valued at US$ 25.3bn in 2012 to date.

Global M&A Overview: Private Equity Buyouts

0%

10%

20%

30%

40%

50%

60%

70%

80%

0

1

2

3

4

5

6

7

2004 2005 2006 2007 2008 2009 2010 2011 Q1-Q3 2012

Deb

t/Tot

al F

undi

ng (%

)

Deb

t/EB

ITD

A (x

)

Global Debt Financing Ratios Trend (US$200m+ buyouts, excluding buy-ins)

Debt/EBITDA Multiple (x) Debt/Total Funding (%)

0%

5%

10%

15%

20%

25%

30%

35%

0

50

100

150

200

250

300

350

400

Perc

enta

ge o

f Glo

bal M

&A

Valu

e of

Dea

ls (U

S$bn

)

Global Private Equity Buyout Activity - Quarterly

Rest of the World (Value)

Asia-Pacific ex Japan (Value)

US (Value)

Europe (Value)

Buyouts (% of Total M&A)

Top 10 Global private equity fi rms Q1-Q3 2012 - buyoutsRank Company Name Value (US$m) Deal Count

1 The Carlyle Group 15,495 202 Blackstone Group 8,741 143 AXA Private Equity 1,816 124 Kohlberg Kravis Roberts & Co 2,858 115 The Riverside Company - 106 Lloyds TSB Development Capital 396 97 H.I.G. Capital 47 88 EQT Partners 3,419 79 Vista Equity Partners 2,501 710 Warburg Pincus 1,638 7

Press Release: mergermarket M&A Round-up for Q1-Q3 2012 8 www.mergermarket.com

• Global exits (US$ 203.3bn) down 16.4% on same period last year • SBOs steady; drop in exits driven by 21.9% drop in trade sales • 2012 European exit premiums down to 15%

Private Equity fi rms were sitting tight on their investments as they waited for safer condi-tions. Total exits in Q1-Q3 2012 totalled US$ 203.3bn, down 16.4% on the same period in 2011 (US$ 243.2bn). Trade sales made up 69.2% of total PE backed exits, secondary buy-outs (SBOs) the other 30.8%.

SBOs remained steady compared to last year, matching the last year’s Q1-Q3 total value of USD$62.8bn with the current up to date 2012’s value of US$62.6bn. The third quarter alone saw US$ 28.2bn-worth of activity, up 21.6% on Q3 2011 (US$ 23.2bn).

It was trade sales that were down - by 21.9% for 2012 (US$ 140.8bn) compared to the same period in 2011 (US$ 180.4bn). The third quarter’s activity of US$ 41.2bn was down 34.9% on Q2’s US$ 63.3bn: companies appeared to be avoiding risk and remained prudent in their divestments.

Global exit premiums were up from 32.4% in 2011 to 34.9%. US premiums at 48.8% (37.9% in 2011) supported the reported slow recovery while, not surprisingly, European premiums have decreased to 15% in 2012 so far (31.1% in 2011). Global EBITDA exit multiple, at 9.9x, was behind 2011 (12.6x) and the lowest since 2003. Europe’s 10.9x was only just higher than the US’ 9.8x.

The Industrials & Chemicals sector saw the top deal of the quarter, in which Japanese Dai-kin Industries acquired Goodman Global from US Hellman & Friedman for US$ 3.7bn.

Kirkland & Ellis advised on most deals: 46 deals with a total value of US$ 16.5bn.

Global M&A Overview: Private Equity Exits

6

8

10

12

14

16

18

20

22

24

2004 2005 2006 2007 2008 2009 2010 2011 Q1-Q3 2012

EBIT

DA

Mul

tiple

(x) -

Ave

rage

Exit EBITDA Multiple Analysis - Average

Global Europe US

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

10

20

30

40

50

60

70

80

90

100

110

120

130

140

150

Perc

enta

ge o

f Tot

al E

xits

(exc

l. IP

Os)

Valu

e of

Dea

ls (U

S$bn

)

Trade Sales vs SBO Exit Activity - Quarterly

Trade Sales (Value) SBOs (Value) Trade Sales (% of total exits) SBOs (% of total exits)

Top 10 Global private equity fi rms Q1-Q3 2012 - exitsRank Company Name Value (US$m) Deal Count

1 Intel Capital 1,531 122 Draper Fisher Jurvetson 1,948 113 3i Group 1,122 114 Battery Ventures 830 95 The Riverside Company 70 96 Macquarie Group 6,971 87 The Carlyle Group 6,653 88 Sun Capital Partners 98 89 Benchmark Capital 1,619 610 Atlas Venture 1,571 6

Press Release: mergermarket M&A Round-up for Q1-Q3 2012 9 www.mergermarket.com

• Emerging Markets deals down by 22.9% since last year • BRICs witnessed lowest quarterly total since Q1 2009 • 33.2% drop in inbound investment from Europe in Q1-Q3 2012 • Skadden Arps Slate Meagher & Flom top legal adviser with a total value of

US$ 60.6bn for the year to date

The third quarter saw Emerging Markets M&A deals adding up to US$ 69.3bn, still 49% less than Q3 2011 (US$ 135.8bn), the lowest Q3 since Q3 2008 (US$ 49.3bn) and the second low-est since Q3 2006 (US$ 67bn). The total for fi rst three quarters of the year was US$ 293.5bn, 24.1% less than Q1-Q3 2011 (US$ 386.8bn). Emerging Markets accounted for 15% of global M&A activity in Q3 2012, down from the 23.5% they accounted for in the same period in 2011. Year-to-date activity accounted for 20.4% of global M&A, compared to 21.9% in 2011.

BRIC M&A activity also decreased for the second quarter in a row to US$ 47.1bn (from US$ 75.6 in Q1 2012), the lowest quarterly BRIC total since Q1 2009 (US$ 38.6bn). Inbound cross-border activity into Emerging Markets in Q3 2012 totalled US$ 24.3bn, down 61.8% from Q2 2012 (US$ 63.7bn) and a 52% drop from Q3 2011 (US$ 50.6bn). In Q1-Q3 2012, European bidders remained the most active investors into Emerging Markets with US$ 47.2bn-worth of deals, although this was a decrease of 33.2% compared to the same period last year (US$ 70.6bn).

Gains have been seen in the Emerging Markets with Technology deals totalling US$ 21bn for Q1-Q3 2012, almost double from the same period last year (US$ 10.8bn), aided by the Yahoo-Alibaba deal valued at US$ 7.1bn.

Global M&A Overview: Emerging Markets

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

0

10

20

30

40

50

60

2004 2005 2006 2007 2008 2009 2010 2011 Q1-Q3 2012

Perc

enta

ge (%

)

Valu

e (U

S$bn

)

Emerging Markets Buyout Activity Trend

Value (US$bn)

% of Global BO (Value)

% of EM M&A (Value)

0%

5%

10%

15%

20%

25%

30%

0

20

40

60

80

100

120

140

160

180

200

% o

f Glo

bal M

&A

Valu

e of

Dea

ls (U

S$bn

)

Emerging Markets M&A Activity Trend

Other EM (Value) BRIC (Value) EM M&A as % of Global M&A

Press Release: mergermarket M&A Round-up for Q1-Q3 2012 10 www.mergermarket.com

• Average global premiums for Q1-Q3 2012 at 28%, up from 26.6% in 2011 • North America premiums highest of any region at 41.1% • European average EBITDA multiples continue to be lowest with Asia-Pacifi c

not far behind • Decrease in overall global Q1-Q3 2012 EBITDA to 11.4x, lowest since 2003

The average premium (one day before) of global M&A deals in Q1-Q3 2012 was 28%, a slight increase from 2011 (26.6%).

North American premiums continued to trump all other regions in Q1-Q3 2012 at 41.1%, up from 37.6% in 2011. Meanwhile, European premiums took a dip in Q1-Q3 2012 at 19.3%, down from 21.9% in 2011. Targets in Asia-Pacifi c (ex Japan) had Q1-Q3 2012 average premi-ums of 24.4%, an increase from 2011 (19%) and the highest on mergermarket record (since 2001).

The average EBITDA multiple across global M&A was 11.4x in Q1-Q3 2012, down from 13.3x in 2011 and the lowest level since 2003 (10.6x). In Europe, the average EBITDA multiple was 9.8x, down from 13.7x in 2011 and the lowest on mergermarket record (since 2001).

North America’s EBITDA multiple for Q1-Q3 2012 was 12.6x, down from 2011 when it reached 13.6x.

In Japan, the Q1-Q3 2012 multiple stood at 9.8x, which, while a decrease from 2011 (14.4x), was an increase from H1 2012, when multiples were at 8.9x.

Global M&A Overview: Premia and Multiples Analysis

0

5

10

15

20

25

30

2004 2005 2006 2007 2008 2009 2010 2011 Q1-Q3 2012

EBIT

DA

Mul

tiple

(x) -

Ave

rage

EBITDA Multiple Analysis - Average

Global

Europe

North America

Asia-Pacific (excl. Japan)

Japan

0%

10%

20%

30%

40%

50%

60%

2004 2005 2006 2007 2008 2009 2010 2011 Q1-Q3 2012

Prem

ium

s %

Premium Analysis - Average

Global Europe North America Asia-Pacific (excl. Japan) Japan

Press Release: mergermarket M&A Round-up for Q1-Q3 2012 11 www.mergermarket.com

Consideration Structure

• Proportion of global M&A funded with cash-only up for third year running to hit highest ratio on record while equity contributions hit record low

• Cross-border deals have seen second highest proportion of cash-only deals in 11 years

Cash-only transactions accounted for 73.8% of the total value of M&A transactions in 2012, the highest proportion on mergermarket record (since 2001). This proportion increased for the third year running. The proportion of cross-border deals which were cash-only was also up (for the third year running) to 86.7%, with US$ 300.4bn-worth of cash-only cross-border deals announced this year.

Equity-only M&A deals, down globally, were particularly absent in Europe which saw only nine deals worth a total of US$ 1.2bn this quarter, compared with 20 deals worth US$ 11.9bn in Q3 last year. Of all global M&A deals this year, only 15.5% was paid in bidder’s shares, the lowest proportion on mergermarket record (since 2001).

The largest transaction in Q3 2012 was Kraft Foods Inc’s spin-off of its North American gro-cery business, valued at US$ 26.3bn.

Insolvency

• Q3 2012 global insolvency deals totaled US$ 4.0bn, up 18.9% from Q2 2012 • Japan’s Elpida Memory insolvency deal accounted for 62.5% of global insol-

vency value in Q3 2012 • European insolvencies in 2012 hit highest total since 2007

The third quarter of 2012 saw 65 global insolvency deals with a total value of US$ 4.0bn, a 18.9% increase from Q2 2012 (US$ 3.4bn). Global insolvency deals in Q1-Q3 2012 showed only 1.7% decrease to a total of US$ 14.0bn, compared to the US$ 14.2bn for the same period in 2011.

Asia-Pacifi c saw the highest value of insolvency deals in Q3 2012, mainly due to the acquisi-tion by Micro Technology, the US semiconductor producer, of Elpida Memory, its Japanese counterpart, for US$ 2.5bn.

Europe saw a 71.7% decrease in Q3 in the total value of insolvency deals, which fell from US$ 2.8bn in Q2 2012 to US$ 0.8bn in Q3 2012. However, the year overall hit US$ 7bn, the highest European Q1-Q3 value since 2007.

US insolvencies for the year to date fell 40.4% from US$ 5.4bn in Q1-Q3 2011, to US$ 3.2bn in Q1-Q3 2012.

Global M&A Overview: Consideration Structure/ Insolvency

0

25

50

75

100

125

150

175

200

0

10

20

30

40

50

60

Num

ber o

f dea

ls

Valu

e of

Dea

ls (U

S$bn

)

Quarterly Insolvency Deals - Global

Value (US$bn) Volume

59.1% 59.1% 59.9% 67.4% 71.0%

58.8% 67.9% 69.7%

73.8%

18.3% 18.8% 26.0%

17.9%

22.9%

22.2%

20.5% 18.6% 15.5%

22.6% 22.1% 14.1% 14.7%

6.1%

18.9% 11.5% 11.7% 10.7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2004 2005 2006 2007 2008 2009 2010 2011 Q1-Q3 2012

% o

f Glo

bal M

&A

Global Consideration Breakdown - Value % cash only deals % equity only deals % cash & equity deals

Press Release: mergermarket M&A Round-up for Q1-Q3 2012 12 www.mergermarket.com

• Mega-deals accounted for 16.6% of Q1-Q3 2012 global M&A with total of US$ 242.5bn

• US Q3 2012 average deal size hit second highest since Q1 2011

Mega-deals – those worth more than US$ 10bn – accounted for 16.6% of the value of global M&A transactions announced in Q1-Q3 2012, the highest proportion since 2010 but sub-stantially below the 20-plus% each year between 2004 and 2009. In the third quarter mega-deals amounted to US$ 81.6bn, 7.4% below the total for Q2 2012 (US$ 88.1bn).

US deals valued at US$ 2bn to US$ 10bn during 2012 added up to US$ 182bn, representing 35.55% of all US M&A deals announced in this period. This fi gure was marginally under the 35.85% registered in 2011 and marked the second highest level since 2007.

In the US, the average Q3 2012 deal size of US$ 516m was the highest since Q1 2011 (US$ 526m) and represented a second successive quarterly increase. This has pushed up the global average deal size, which has climbed for the third consecutive quarter to US$ 335m, the highest average deal size since Q1 2011 (US$ 361m).

Global M&A Overview: Deal Value Breakdown

28.0% 23.5% 20.1% 20.4% 23.4% 22.4% 24.6% 24.7% 24.1%

24.5%

22.0% 20.8% 22.9% 19.3% 20.5%

27.5% 26.3% 27.9%

25.5% 30.1%

27.0% 29.9% 27.9% 27.5%

32.6% 34.0% 31.4%

21.9% 24.5% 32.0%

26.7% 29.4% 29.6%

15.4% 15.0% 16.6%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2004 2005 2006 2007 2008 2009 2010 2011 Q1-Q3 2012

Global M&A Deal Size Breakdown - % by Deal Value

$0m - $500m $501m - $2,000m $2,001 - $10,000m mega deals (over $10,001m)

Press Release: mergermarket M&A Round-up for Q1-Q3 2012 13 www.mergermarket.com

Global: League Tables of Legal AdvisersLeague Table of Legal Advisers to Global M&A: Volume

Ranking Q1-Q3 2012 Q1-Q3 2011Q1-Q3 2011

Q1-Q3 2012 Company Name

Value (US$m)

Deal Count

Deal Count

Count Change

1 1 DLA Piper 34,041 206 259 -533 2 Jones Day 87,333 204 229 -252 3 Latham & Watkins 126,483 192 232 -408 4 Kirkland & Ellis 90,859 186 196 -104 5 Linklaters 151,048 166 205 -397 6 Clifford Chance 219,543 152 196 -445 7 Baker & McKenzie 53,283 149 198 -4910 8 Skadden Arps Slate Meagher & Flom 190,993 143 169 -269 9 Allen & Overy 76,250 137 189 -526 10 Freshfields Bruckhaus Deringer 205,564 131 196 -6515 11 White & Case 95,043 122 115 713 12 Weil Gotshal & Manges 98,470 118 133 -1511 13 CMS 9,174 110 161 -5112 14 Hogan Lovells 46,225 101 152 -5118 15 Sullivan & Cromwell 126,419 87 106 -1917 16 Ashurst 31,911 86 107 -2114 17 Simpson Thacher & Bartlett 103,593 83 116 -3326 18 Paul Hastings 13,932 78 87 -921 19 Cleary Gottlieb Steen & Hamilton 120,576 77 97 -2032 20 Stikeman Elliott 51,063 77 75 2

League Table of Legal Advisers to Global M&A: ValueRanking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2011

Q1-Q3 2012 Company Name

Value (US$m)

Deal Count

Value (US$m)

% Val. Change

16 1 Clifford Chance 219,543 152 96,240 128.1%7 2 Freshfields Bruckhaus Deringer 205,564 131 204,391 0.6%3 3 Skadden Arps Slate Meagher & Flom 190,993 143 233,530 -18.2%5 4 Linklaters 151,048 166 213,931 -29.4%9 5 Latham & Watkins 126,483 192 195,603 -35.3%1 6 Sullivan & Cromwell 126,419 87 318,424 -60.3%11 7 Cleary Gottlieb Steen & Hamilton 120,576 77 166,396 -27.5%14 8 Davis Polk & Wardwell 104,111 75 116,746 -10.8%2 9 Simpson Thacher & Bartlett 103,593 83 295,246 -64.9%13 10 Weil Gotshal & Manges 98,470 118 116,904 -15.8%23 11 White & Case 95,043 122 67,604 40.6%66 12 King & Wood Mallesons 91,176 61 24,487 272.3%20 13 Kirkland & Ellis 90,859 186 74,507 21.9%4 14 Wachtell, Lipton, Rosen & Katz 87,526 43 225,418 -61.2%17 15 Jones Day 87,333 204 93,855 -6.9%12 16 Allen & Overy 76,250 137 161,672 -52.8%10 17 Cravath Swaine & Moore 74,670 34 167,170 -55.3%19 18 Blake, Cassels & Graydon 72,479 76 79,845 -9.2%8 19 Shearman & Sterling 66,622 74 199,800 -66.7%21 20 Baker & McKenzie 53,283 149 72,206 -26.2%

Press Release: mergermarket M&A Round-up for Q1-Q3 2012 14 www.mergermarket.com

Global: League Tables of Legal AdvisersLeague Table of Legal Advisers to Global Buyouts*: Volume

Ranking Q1-Q3 2012 Q1-Q3 2011Q1-Q3 2011

Q1-Q3 2012 Company Name

Value (US$m)

Deal Count

Deal Count

Count Change

1 1 Kirkland & Ellis 11,429 69 84 -153 2 Latham & Watkins 25,261 36 38 -22 3 Weil Gotshal & Manges 16,232 33 42 -95 4 Clifford Chance 7,826 25 32 -74 5 Jones Day 3,930 24 34 -106 6 Simpson Thacher & Bartlett 15,997 23 30 -713 7 SJ Berwin 2,647 23 21 27 8 Linklaters 13,199 22 30 -89 9 Freshfields Bruckhaus Deringer 13,310 19 24 -520 10 Paul Weiss Rifkind Wharton &

Garrison 9,624 17 15 2

10 11 DLA Piper 493 16 24 -819 12 Skadden Arps Slate Meagher & Flom 2,836 15 15 018 13 Paul Hastings 1,319 14 16 -261 14 Vinson & Elkins 10,549 13 7 627 15 White & Case 2,573 13 13 026 16 Mayer Brown 2,177 13 13 042 17 McDermott Will & Emery 288 13 9 432 18 Debevoise & Plimpton 18,347 12 10 228 19 Willkie Farr & Gallagher 10,755 12 12 011 20 Allen & Overy 6,735 12 21 -9

League Table of Legal Advisers to Global Buyouts*: ValueRanking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2011

Q1-Q3 2012 Company Name

Value (US$m)

Deal Count

Value (US$m)

% Val. Change

5 1 Latham & Watkins 25,261 36 12,538 101.5%6 2 Debevoise & Plimpton 18,347 12 11,576 58.5%3 3 Weil Gotshal & Manges 16,232 33 19,465 -16.6%1 4 Simpson Thacher & Bartlett 15,997 23 33,870 -52.8%12 5 Freshfields Bruckhaus Deringer 13,310 19 9,978 33.4%13 6 Linklaters 13,199 22 9,593 37.6%2 7 Kirkland & Ellis 11,429 69 21,315 -46.4%27 8 Willkie Farr & Gallagher 10,755 12 3,795 183.4%125 9 Vinson & Elkins 10,549 13 468 2,154%25 10 Paul Weiss Rifkind Wharton & Garrison 9,624 17 3,953 143.5%4 11 Clifford Chance 7,826 25 15,220 -48.6%9 12 Torys 7,797 5 10,814 -27.9%32 13 Wachtell, Lipton, Rosen & Katz 7,745 3 3,191 142.7%34 14 Sullivan & Cromwell 7,236 8 3,037 138.3%30 15 Allen & Overy 6,735 12 3347 101.2%- 16= Campos Ferreira, Sa Carneiro e Asociados 5,633 1 - -- 16= Morais Leitao Galvao Teles Soares Da

Silva & Associados5,633 1 - -

- 16= Vieira de Almeida & Associados 5,633 1 - -394 19 Veirano Advogados 4,900 1 - -10 20 Ropes & Gray 4,730 12 10,438 -54.7%

* Based on the target geography only and the adviser advising the buy-side only

Press Release: mergermarket M&A Round-up for Q1-Q3 2012 15 www.mergermarket.com

• Europe posted its lowest quarter since Q3 2009 • Q1-Q3 totalled US$ 457.5bn, down 22.6% on Q1-Q3 2011 • Germanic region led continent in activity

The fi nancial crisis appears to have taken a fi rm grip on the European M&A market as it has seen its slowest quarter for three years. European deals in Q3 totalled US$ 100.3bn, down 46.1% from Q2 (US$ 186.3bn) and 39.3% from Q3 2011 (US$ 165.2bn). This steep drop-off comes after two consecutive quarters of growth, and was the lowest quarter since Q3 2009, and the fourth lowest quarter on mergermarket record (since 2001).

European deals for the year to date amounted to US$ 457.5bn, a 22.6% drop on the same period in 2011 (US$ 591bn). This leaves the region needing to post its highest quarter since Q3 2008 in Q4 if it is to reach 2011’s year-end total of US$ 725.2bn-worth of deals.

The Germanic region remained the most active in the European M&A market in terms of deal value from Q1-Q3 2012 with a 27.5% market share. Energy, Mining & Utilities ac-counted for 26.3% of European deals in Q1-Q3 2012, boosted by the US$ 50.1bn Glen-core/Xstrata megadeal. Construction enjoyed a 48.7% pickup in activity for the same pe-riod compared to Q1-Q3 2011, making up US$ 12.3bn-worth of all European transactions with Camargo Correa’s US$ 5.4bn offer for Cimpor the top deal. Defence, whilst typically a quiet sector, could see a big fi llip if the rumoured EADS takeover of BAE goes through.

European inbound investment in Q3 2012 added up to US$ 38.8bn, down 50.1% from the previous quarter (US$77.7bn) and down 32.2% from the same period last year (US$57.2bn).

Europe continued to be the most attractive region for investors from outside the target country, with 42.2% of total cross-border investment by country going into Europe. Asian interest in European investments continues, particularly amongst Chinese and Japanese companies, with the latter accounting for 13% (US$ 21.6bn) of investment into Europe so far this year. The Eurozone crisis has led to a decline in inbound investment from non-zone countries. Q3 2012 saw inbound M&A into the Eurozone (US$ 26.5bn) at its second lowest level since Q2 2010 (US$ 17bn).

Clifford Chance topped the legal adviser league tables for the year to date with US$ 181.2bn-worth of deals. Freshfi elds Bruckhaus Deringer came in second with US$ 174.6bn.

European M&A Overview

0

25

50

75

100

125

150

175

200

225

250

275

300

0

10

20

30

40

50

60

70

80

90

100

110

120

130

140

150

Volu

me

of D

eals

Valu

e of

Dea

ls (U

S$bn

)

European Inbound/Outbound M&A

Inbound Value (US$bn) Outbound Value (US$bn) Inbound Volume Outbound Volume

Press Release: mergermarket M&A Round-up for Q1-Q3 2012 16 www.mergermarket.com

European M&A Overview: Industry and Geography Breakdown

UK & Ireland 23.3%

Germanic 18.0%

France 11.6%

Italy 5.7%

Iberia 5.1%

Benelux 8.9%

Nordic 14.1%

Central & Eastern Europe 9.8%

South Eastern Europe 3.2%

Other 0.2%

Mix of Announced European Deals by Geographic Region Q1-Q3 2012 - Volume

UK & Ireland 25.1%

Germanic 27.5%

France 5.6%

Italy 7.1%

Iberia 7.8%

Benelux 8.2%

Nordic 8.1%

Central & Eastern Europe 8.0%

South Eastern Europe 2.4%

Other 0.05%

Mix of Announced European Deals by Geographic Region Q1-Q3 2012 - Value

Q1-Q3 2012 Q1-Q3 2011 Change

Sector Value (US$bn) Market share Deal count Value (US$bn) Market share Deal count Value (%) Deal Count

Energy, Mining & Utilities 120.2 26.3% 240 131.3 22.2% 320 -8.5% -80

Industrials & Chemicals 69.1 15.1% 817 98.2 16.6% 884 -29.6% -67

Financial Services 60.0 13.1% 273 94.6 16.0% 313 -36.5% -40

Consumer 48.4 10.6% 568 62.1 10.5% 638 -22.0% -70

Pharma, Medical & Biotech 24.8 5.4% 191 56.2 9.5% 259 -55.8% -68

Technology 23.6 5.2% 340 31.2 5.3% 340 -24.3% 0

Transport 23.1 5.1% 139 10.8 1.8% 156 114.2% -17

Business Services 22.5 4.9% 419 24.6 4.2% 586 -8.7% -167

Telecommunications 20.4 4.5% 44 33.3 5.6% 53 -38.8% -9

Real Estate 14.4 3.1% 63 15.5 2.6% 69 -7.5% -6

Construction 12.3 2.7% 150 8.3 1.4% 183 48.7% -33

Media 9.6 2.1% 121 8.9 1.5% 148 7.3% -27

Leisure 7.8 1.7% 128 13.8 2.3% 168 -43.6% -40

Agriculture 1.0 0.2% 37 1.4 0.2% 41 -26.8% -4

Defence 0.3 0.1% 9 0.6 0.1% 7 -40.9% 2

Total 457.5 3,539 590.7 4,165 -22.5% -626

Press Release: mergermarket M&A Round-up for Q1-Q3 2012 17 www.mergermarket.com

European M&A Overview: Top DealsTop 10 Announced Deals for Q1-Q3 2012

Announced Date

Bidder Company Bidder Legal Adviser Target Company Target/Seller Legal Adviser Seller Company Deal Value (US$m)

07-Feb-12 Glencore International plc Clifford Chance (Advising Citigroup; Credit Suisse; Morgan Stanley); Linklaters

Xstrata Plc (65.92% Stake) Freshfields Bruckhaus Deringer; King & Wood Mallesons

50,563

04-Jul-12 Volkswagen AG Clifford Chance; Hogan Lovells; White & Case

Dr Ing hc F Porsche AG (50.1% Stake)

Freshfields Bruckhaus Deringer; Hengeler Mueller

Porsche Automobil Holding SE 14,238

21-May-12 Eaton Corporation A&L Goodbody; Davis Polk & Wardwell (Advising Citigroup; Morgan Stanley); Kinstellar; Matheson Ormsby Prentice; McCann FitzGerald (Advising Citigroup; Morgan Stanley); Simpson Thacher & Bartlett

Cooper Industries Plc Arthur Cox; Blake, Cassels & Graydon; Cleary Gottlieb Steen & Hamilton (Advising Goldman Sachs); Slaughter and May; Wachtell, Lipton, Rosen & Katz

11,940

16-Apr-12 GDF Suez SA Cleary Gottlieb Steen & Hamilton (Advising Lazard); Linklaters; Weil Gotshal & Manges

International Power Plc (30.23% Stake)

Clifford Chance 10,867

17-Jan-12 Sumitomo Mitsui Financial Group Inc

A&L Goodbody; Milbank Tweed Hadley & McCloy; Nagashima Ohno & Tsunematsu

RBS Aviation Capital Limited Clifford Chance; McCann FitzGerald

Royal Bank of Scotland Group Plc 7,300

19-Mar-12 United Parcel Service Inc Freshfields Bruckhaus Deringer TNT Express NV Allen & Overy; Clifford Chance (Advising Lazard); Stibbe; Sullivan & Cromwell (Advising Goldman Sachs)

6,843

19-Jun-12 Walgreen Company Allen & Overy; Cleary Gottlieb Steen & Hamilton (Advising Goldman Sachs); Davis Polk & Wardwell (Advising Bank of America Merrill Lynch); Gibson Dunn & Crutcher (Advising Lazard); Wachtell, Lipton, Rosen & Katz; Weil Gotshal & Manges

Alliance Boots GmbH (45% Stake) Clifford Chance; Darrois Villey Maillot Brochier; Simpson Thacher & Bartlett; Niederer Kraft & Frey

AB Acquisitions Holdings Limited 6,690

06-May-12 Electricite de France SA Clifford Chance; Freshfields Bruckhaus Deringer (Advising BNP Paribas); Jones Day; Paul Weiss Rifkind Wharton & Garrison

Edison International SpA (19.36% Stake)

6,438

31-May-12 Sara Lee Corporation (shareholders)

D.E MASTER BLENDERS 1753 BV De Brauw Blackstone Westbroek; Skadden Arps Slate Meagher & Flom; Allens

Hillshire Brands Co 5,876

25-Apr-12 Watson Pharmaceuticals Inc Latham & Watkins; Loyens & Loeff; Skadden Arps Slate Meagher & Flom

Actavis Group hf Clifford Chance (Advising Deutsche Bank); Kinstellar; Linklaters; Shearman & Sterling

5,806

Press Release: mergermarket M&A Round-up for Q1-Q3 2012 18 www.mergermarket.com

Europe M&A Heat Chart

Sector Ger -manic

CEE (excl.

Russia)

UK & Ireland

Italy France Nordics Ben -elux

Russia Greece &

Turkey

Iberia Total

Industrials & Chemicals 170 130 72 81 63 51 28 41 49 19 636

Consumer 130 134 68 71 55 47 30 37 35 29 704

TMT 82 105 109 32 67 64 59 43 21 37 619

Energy, Mining & Utilities 47 120 90 31 14 47 17 41 21 16 444

Pharma, Medical & Biotech 77 40 64 19 24 35 15 5 13 16 308

Business Services 43 34 77 20 23 26 25 20 12 13 293

Financial Services 38 60 58 42 13 13 19 30 27 14 314

Leisure 33 44 51 17 17 7 8 16 19 20 232

Transportation 19 43 12 15 14 19 13 23 22 13 193

Construction 20 42 14 11 22 11 6 14 13 20 173

Real Estate 24 19 14 7 3 2 6 14 5 1 95

Agriculture 7 11 1 3 3 1 14 1 1 42

Defence 4 11 1 3 3 22

Other 1 0 2 1 6 10

Government 3 1 2 3 9

Total 691 789 640 347 321 325 228 304 250 199 4,094

Hot Warm Cold

150 80 20

120 60 10

100 40 0

Note: The Intelligence Heat Chart are based on “companies for sale” tracked by mergermarket in the respective regions between 12 March 2012 and 11 September 2012. Opportunities are captured according to the dominant geography and sector of the potential target company. mergermarket’s Heat Chart of predicted deal flow is based on the intelligence collected in our database relating to companies rumoured to be for sale, or officially up for sale in the respective regions. It is therefore indicative of areas that are likely to be active in the months to come. The intelligence comes from a range of sources, including press reports, company statements and our own team of journalists gathering proprietary intelligence from M&A across the regions. The data does not differentiate between small and large transactions, nor between deals that could happen in the short or long-term.

The CEE region is set to be the most active region in Europe according to the amount of intelligence on upcoming M&A, with the Consumer sector leading amid a slew of large and high profi le deals in the sector and consolidation of Russia’s supermarket industry.

Russia’s new WTO membership has seen massive investment into the country, leading to the Industrial & Chemicals sector being the second most active industry.

The Consumer sector and the Industrial and Chemicals sector – but in reverse order - also dominate in the Germanic region, EMEA’s second most active and among the least affected by Europe’s sovereign debt crisis. The TMT sector dominates “Companies for sale” in all other European regions except Italy and Greece & Turkey.

©2012 Google - Map data © 2012 Google

Press Release: mergermarket M&A Round-up for Q1-Q3 2012 19 www.mergermarket.com

Europe: League Tables of Legal AdvisersLeague Tables of Legal Advisers to European M&A: Volume

Ranking Q1-Q3 2012 Q1-Q3 2011Q1-Q3 2011

Q1-Q3 2012 Company Name

Value (US$m)

Deal Count

Deal Count

Count Change

2 1 Linklaters 138,428 148 176 -284 2 Clifford Chance 181,148 121 158 -375 3 DLA Piper 27,468 116 152 -361 4 Freshfields Bruckhaus Deringer 174,562 115 178 -633 5 CMS 8,624 109 159 -506 6 Allen & Overy 65,718 105 145 -407 7 Baker & McKenzie 32,630 84 124 -4011 8 Jones Day 23,078 74 90 -1610 9 White & Case 52,235 72 90 -188 10 Hogan Lovells 37,989 66 98 -329 11 Latham & Watkins 50,031 64 93 -2913 12 Eversheds 13,219 64 78 -1420 13 Skadden Arps Slate Meagher & Flom 89,375 56 54 215 14 Ashurst 16,903 56 65 -919 15 Pinsent Masons 3,401 54 55 -117 16 SJ Berwin 4,481 49 62 -1383 17 Bech-Bruun 7,452 48 20 2816 18 Loyens & Loeff 18,776 46 65 -1922 19 Mannheimer Swartling 2,557 44 52 -834 20 Hengeler Mueller 40,381 43 39 4

League Tables of Legal Advisers to European M&A: ValueRanking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2011

Q1-Q3 2012 Company Name

Value (US$m)

Deal Count

Value (US$m)

% Val. Change

6 1 Clifford Chance 181,148 121 80,799 124.2%1 2 Freshfields Bruckhaus Deringer 174,562 115 193,824 -9.9%2 3 Linklaters 138,428 148 172,911 -19.9%13 4 Skadden Arps Slate Meagher & Flom 89,375 56 50,118 78.3%7 5 Cleary Gottlieb Steen & Hamilton 78,241 42 79,893 -2.1%

127 6 King & Wood Mallesons 71,580 9 3,697 1,836%4 7 Allen & Overy 65,718 105 112,204 -41.4%3 8 Sullivan & Cromwell 57,510 25 129,914 -55.7%10 9 White & Case 52,235 72 59,961 -12.9%14 10 Weil Gotshal & Manges 50,459 40 49,971 1.0%11 11 Latham & Watkins 50,031 64 54,347 -7.9%8 12 Simpson Thacher & Bartlett 44,422 20 79,781 -44.3%9 13 Wachtell, Lipton, Rosen & Katz 41,763 11 76,256 -45.2%22 14 Hengeler Mueller 40,381 43 40,641 -0.6%23 15 Hogan Lovells 37,989 66 40,612 -6.5%35 16 Davis Polk & Wardwell 36,489 17 24,043 51.8%45 17 Kirkland & Ellis 34,043 31 19,361 75.8%67 18 A&L Goodbody 32,745 15 11,433 186.4%26 19 Baker & McKenzie 32,630 84 37,197 -12.3%21 20 Slaughter and May 32,314 29 42,315 -23.6%

Press Release: mergermarket M&A Round-up for Q1-Q3 2012 20 www.mergermarket.com

Europe: League Tables of Legal AdvisersLeague Tables of Legal Advisers to European Buyouts* Volume

Ranking Q1-Q3 2012 Q1-Q3 2011Q1-Q3 2011

Q1-Q3 2012 Company Name

Value (US$m)

Deal Count

Deal Count

Count Change

5 1 SJ Berwin 2,647 23 21 21 2 Linklaters 11,757 19 28 -93 3 Clifford Chance 5,009 17 23 -64 4 Freshfields Bruckhaus Deringer 12,192 15 23 -88 5 Latham & Watkins 1,586 13 15 -26 6 Weil Gotshal & Manges 6,898 11 19 -82 7 CMS 950 11 25 -1413 8 Kirkland & Ellis 4,210 10 12 -215 9 Mayer Brown 953 9 11 -218 10 Eversheds 339 9 10 -17 11 Allen & Overy 6,140 8 17 -916 12 Vinge 2,255 8 10 -219 13 White & Case 1,282 8 10 -226 14 Olswang 698 8 9 -112 15 Ashurst 687 8 12 -432 16 Macfarlanes 31 8 7 150 17 Hannes Snellman 788 7 5 211 18 DLA Piper 379 7 14 -720 19 Pinsent Masons 50 7 10 -331 20 De Pardieu Brocas Maffei - 7 7 0

League Tables of Legal Advisers to European Buyouts* ValueRanking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2011

Q1-Q3 2012 Company Name

Value (US$m)

Deal Count

Value (US$m)

% Val. Change

2 1 Freshfields Bruckhaus Deringer 12,192 15 9,978 22.2%3 2 Linklaters 11,757 19 8,788 33.8%13 3 Weil Gotshal & Manges 6,898 11 4,144 66.5%21 4 Allen & Overy 6,140 8 2,737 124.3%- 5= Campos Ferreira, Sa Carneiro e Asociados 5,633 1 - -- 5= Morais Leitao Galvao Teles Soares Da Silva

& Associados5,633 1 - -

- 5= Vieira de Almeida & Associados 5,633 1 - -1 8 Clifford Chance 5,009 17 10,089 -50.4%57 9 Sullivan & Cromwell 4,524 2 649 597.1%11 10 Kirkland & Ellis 4,210 10 4,262 -1.2%

175 11 Advokatfirmaet BA-HR DA 2,834 3 - -33 12 SJ Berwin 2,647 23 1,621 63.3%54 13 Slaughter and May 2,640 2 654 303.7%25 14 Bech-Bruun 2,628 6 2,091 25.7%18 15 Simpson Thacher & Bartlett 2,576 2 3,067 -16.0%93 16 Roschier 2,518 4 171 1,373%39 17 Baker & McKenzie 2,408 4 1,360 77.1%100 18 P+P Poellath + Partners 2,313 6 139 1,564%10 19 Ropes & Gray 2,308 2 4,304 -46.4%7 20 Vinge 2,255 8 5,620 -59.9%

* Based on the target geography only and the adviser advising the buy-side only

Press Release: mergermarket M&A Round-up for Q1-Q3 2012 21 www.mergermarket.com

Europe: League Tables of Legal Advisers

Legal Advisers to French M&A: VolumeRanking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2011

Q1-Q3 2012 Company Name

Value (US$m)

Deal Count

Deal Count

Count Change

1 1 Linklaters 15,370 23 35 -1210 2 De Pardieu Brocas Maffei 1,280 22 22 04 3 SJ Berwin 2,476 21 27 -69 4 CMS 285 21 22 -120 5 Baker & McKenzie 5,365 18 15 32 6 Clifford Chance 17,989 17 31 -147 7 Latham & Watkins 4,360 17 24 -76 8 Gide Loyrette Nouel 2,326 17 25 -817 9 Jones Day 3,463 16 16 012 10 Cleary Gottlieb Steen & Hamilton 23,101 14 19 -513 11 White & Case 2,061 14 19 -53 12 Mayer Brown 1,063 14 29 -1518 13 Weil Gotshal & Manges 12,902 13 16 -315 14 Hogan Lovells 3,200 13 18 -519 15 Paul Hastings 107 13 16 -3

Legal Advisers to French M&A: ValueRanking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2011

Q1-Q3 2012 Company Name

Value (US$m)

Deal Count

Value (US$m)

% Val. Change

7 1 Cleary Gottlieb Steen & Hamilton 23,101 14 11,359 103.4%6 2 Clifford Chance 17,989 17 14,533 23.8%1 3 Linklaters 15,370 23 46,827 -67.2%39 4 Weil Gotshal & Manges 12,902 13 2,851 352.5%2 5 Freshfields Bruckhaus Deringer 8,863 11 32,305 -72.6%24 6 Darrois Villey Maillot Brochier 7,060 8 5,203 35.7%11 7 Baker & McKenzie 5,365 18 9,174 -41.5%5 8 Latham & Watkins 4,360 17 18,336 -76.2%3 9 Bredin Prat 3,880 11 26,405 -85.3%30 10 Jones Day 3,463 16 3,948 -12.3%71 11 Paul Weiss Rifkind Wharton & Garrison 3,449 3 921 274.5%80 12 Dechert 3,281 8 748 338.6%35 13 Hogan Lovells 3,200 13 3,142 1.8%16 14 Sullivan & Cromwell 3,189 2 8,095 -60.6%15 15 Loyens & Loeff 2,915 7 8,724 -66.6%

Legal Advisers to UK M&A: VolumeRanking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2011

Q1-Q3 2012 Company Name

Value (US$m)

Deal Count

Deal Count

Count Change

2 1 Linklaters 42,050 64 68 -41 2 DLA Piper 12,048 63 79 -166 3 Pinsent Masons 3,401 54 55 -13 4 Freshfields Bruckhaus Deringer 39,204 49 60 -114 5 Eversheds 9,221 49 59 -107 6 Clifford Chance 48,003 47 53 -65 7 Allen & Overy 28,850 40 56 -168 8 CMS 6,089 32 49 -1710 9 Hogan Lovells 11,646 30 38 -814 10 Ashurst 5,931 30 34 -425 11 Macfarlanes 2,604 30 24 619 12 Travers Smith 10,297 28 30 -220 13 Olswang 1,421 28 30 -29 14 Slaughter and May 19,296 26 44 -1823 15 Squire Sanders 1,133 26 26 0

Legal Advisers to UK M&A: ValueRanking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2011

Q1-Q3 2012 Company Name

Value (US$m)

Deal Count

Value (US$m)

% Val. Change

11 1 Clifford Chance 48,003 47 16,131 197.6%2 2 Linklaters 42,050 64 68,418 -38.5%14 3 Weil Gotshal & Manges 39,531 21 14,573 171.3%1 4 Freshfields Bruckhaus Deringer 39,204 49 68,798 -43.0%33 5 Cleary Gottlieb Steen & Hamilton 37,033 8 7,933 366.8%3 6 Allen & Overy 28,850 40 65,166 -55.7%22 7 Simpson Thacher & Bartlett 28,152 11 13,246 112.5%25 8 Latham & Watkins 22,006 23 11,920 84.6%21 9 Wachtell, Lipton, Rosen & Katz 20,918 6 13,330 56.9%13 10 Sullivan & Cromwell 20,662 14 14,666 40.9%4 11 Slaughter and May 19,296 26 36,950 -47.8%15 12 Skadden Arps Slate Meagher & Flom 17,935 21 14,476 23.9%16 13 Kirkland & Ellis 16,440 18 14,407 14.1%119 14 Kaye Scholer 15,193 4 901 1,586%30 15 Fried Frank Harris Shriver & Jacobson 12,323 4 10,401 18.5%

Press Release: mergermarket M&A Round-up for Q1-Q3 2012 22 www.mergermarket.com

Europe: League Tables of Legal Advisers

Legal Advisers to Germanic M&A: VolumeRanking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2011

Q1-Q3 2012 Company Name

Value (US$m)

Deal Count

Deal Count

Count Change

1 1 Freshfields Bruckhaus Deringer 94,719 53 75 -222 2 CMS 2,766 49 69 -203 3 Clifford Chance 94,033 39 44 -56 4 Hengeler Mueller 39,608 39 33 65 5 Baker & McKenzie 19,968 35 36 -111 6 Noerr 7,563 27 27 04 7 Linklaters 69,205 26 38 -127 8 Allen & Overy 26,694 25 30 -517 9 Jones Day 8,847 23 18 514 10 Hogan Lovells 23,694 22 21 18 11 P+P Poellath + Partners 4,491 22 29 -710 12 Latham & Watkins 7,855 20 27 -712 13 White & Case 32,081 19 25 -69 14 DLA Piper 12,331 19 28 -919 15 Skadden Arps Slate Meagher & Flom 27,806 18 14 4

Legal Advisers to Germanic M&A: ValueRanking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2011

Q1-Q3 2012 Company Name

Value (US$m)

Deal Count

Value (US$m)

% Val. Change

3 1 Freshfields Bruckhaus Deringer 94,719 53 59,863 58.2%21 2 Clifford Chance 94,033 39 20,988 348.0%55 3 King & Wood Mallesons 70,840 6 2,483 2,753%4 4 Linklaters 69,205 26 56,106 23.3%11 5 Hengeler Mueller 39,608 39 38,722 2.3%13 6 White & Case 32,081 19 32,355 -0.8%36 7 Skadden Arps Slate Meagher & Flom 27,806 18 8,738 218.2%26 8 Allen & Overy 26,694 25 15,024 77.7%44 9 Hogan Lovells 23,694 22 4,216 462.0%34 10 Baker & McKenzie 19,968 35 9949 100.7%47 11 Gibson Dunn & Crutcher 17,847 5 3,192 459.1%31 12 Davis Polk & Wardwell 16,708 7 12,267 36.2%53 13 Kirkland & Ellis 16,586 7 2,560 547.9%16 14 Weil Gotshal & Manges 15,886 7 22,349 -28.9%24 15 Mayer Brown 13,883 10 16,567 -16.2%

Legal Advisers to German M&A: VolumeRanking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2011

Q1-Q3 2012 Company Name

Value (US$m)

Deal Count

Deal Count

Count Change

2 1 CMS 2,285 44 61 -171 2 Freshfields Bruckhaus Deringer 41,408 40 61 -214 3 Hengeler Mueller 39,608 38 33 53 4 Clifford Chance 22,757 32 42 -107 5 Noerr 7,563 27 26 16 6 P+P Poellath + Partners 4,491 22 28 -615 7 Hogan Lovells 23,694 20 14 610 8 Latham & Watkins 7,855 20 22 -216 9 Jones Day 4,999 19 14 513 10 Baker & McKenzie 5,703 18 18 08 11 Allen & Overy 18,403 17 24 -75 12 Linklaters 8,388 17 29 -1211 13 White & Case 20,231 16 22 -69 14 Luther 1,333 16 23 -712 15 DLA Piper 456 14 20 -6

Legal Advisers to German M&A: ValueRanking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2011

Q1-Q3 2012 Company Name

Value (US$m)

Deal Count

Value (US$m)

% Val. Change

12 1 Freshfields Bruckhaus Deringer 41,408 40 20,607 100.9%8 2 Hengeler Mueller 39,608 38 38,722 2.3%32 3 Hogan Lovells 23,694 20 3234 632.7%11 4 Clifford Chance 22,757 32 20,652 10.2%14 5 White & Case 20,231 16 16,870 19.9%17 6 Allen & Overy 18,403 17 14,768 24.6%9 7 Linklaters 8,388 17 28920 -71.0%52 8 Weil Gotshal & Manges 7,941 4 1,158 585.8%13 9 Latham & Watkins 7,855 20 17,088 -54.0%31 10 Noerr 7,563 27 3,830 97.5%27 11 Skadden Arps Slate Meagher & Flom 6,300 11 5,184 21.5%29 12 Baker & McKenzie 5,703 18 4,388 30.0%20 13 Davis Polk & Wardwell 5,688 3 12,267 -53.6%- 14 Gleiss Lutz 5,136 13 - -

15 15 Cravath Swaine & Moore 5,044 3 16,762 -69.9%

Press Release: mergermarket M&A Round-up for Q1-Q3 2012 23 www.mergermarket.com

Europe: League Tables of Legal Advisers

Legal Advisers to Italian M&A: VolumeRanking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2011

Q1-Q3 2012 Company Name

Value (US$m)

Deal Count

Deal Count

Count Change

1 1 Chiomenti Studio Legale 6,613 26 32 -62 2 Gianni, Origoni, Grippo, Cappelli & Partners 12,866 18 23 -53 3 d'Urso Gatti e Bianchi - Studio

Legale Associato10,263 18 18 0

7 4 NCTM Studio Legale Associato 5,050 16 13 34 5 Bonelli Erede Pappalardo 6,833 13 15 -214 6 Linklaters 2,371 10 8 26 7 Studio Pedersoli e Associati 441 10 13 -35 8 Clifford Chance 5,450 8 13 -520 9 Grimaldi e Associati 1,017 6 6 021 10 BLF Studio Legale 729 6 6 08 11 Latham & Watkins 700 6 11 -522 12 CMS 302 6 6 09 13 Freshfields Bruckhaus Deringer 9,404 5 10 -524 14 Jones Day 3,729 5 5 031 15 Pirola Pennuto Zei & Associati 1,248 5 4 1

Legal Advisers to Italian M&A: ValueRanking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2011

Q1-Q3 2012 Company Name

Value (US$m)

Deal Count

Value (US$m)

% Val. Change

5 1 Gianni, Origoni, Grippo, Cappelli & Partners 12,866 18 7,053 82.4%3 2 d'Urso Gatti e Bianchi - Studio

Legale Associato10,263 18 7,584 35.3%

4 3 Freshfields Bruckhaus Deringer 9,404 5 7,234 30.0%2 4 Bonelli Erede Pappalardo 6,833 13 10,580 -35.4%1 5 Chiomenti Studio Legale 6,613 26 12,569 -47.4%10 6 Clifford Chance 5,450 8 5,690 -4.2%75 7 Paul Weiss Rifkind Wharton & Garrison 5,277 4 125 4,122%36 8 NCTM Studio Legale Associato 5,050 16 575 778.3%11 9 Cleary Gottlieb Steen & Hamilton 4,298 3 5,656 -24.0%99 10 Jones Day 3,729 5 40 9,223%19 11 Linklaters 2,371 10 2,071 14.5%- 12= Epstein Rosenblum Maoz 1,989 2 - -- 12= Rosenram 1,989 2 - -- 12= Yigal Arnon & Co 1,989 2 - -

50 15 White & Case 1,663 2 319 421.3%

Legal Advisers to Benelux M&A: VolumeRanking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2011

Q1-Q3 2012 Company Name

Value (US$m)

Deal Count

Deal Count

Count Change

2 1 Loyens & Loeff 7,725 36 56 -201 2 Allen & Overy 21,330 35 59 -249 3 De Brauw Blackstone Westbroek 14,585 31 29 23 4 NautaDutilh 4,406 22 42 -2012 5 Houthoff Buruma 1,435 22 26 -48 6 Freshfields Bruckhaus Deringer 36,081 21 29 -84 7 Linklaters 7,369 21 40 -19- 8 Stibbe 3,998 21 - -6 9 DLA Piper 967 20 31 -117 10 CMS 716 18 30 -1211 11 Baker & McKenzie 1,284 13 26 -1337 12 AKD lawyers & civil law notaries 29 13 5 825 13 Lexence - 13 8 55 14 Clifford Chance 32,341 12 33 -2118 15 Eubelius 255 11 10 1

Legal Advisers to Benelux M&A: ValueRanking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2011

Q1-Q3 2012 Company Name

Value (US$m)

Deal Count

Value (US$m)

% Val. Change

2 1 Freshfields Bruckhaus Deringer 36,081 21 21,271 69.6%1 2 Sullivan & Cromwell 32,909 4 22,976 43.2%24 3 Skadden Arps Slate Meagher & Flom 32,599 10 4,376 644.9%10 4 Clifford Chance 32,341 12 9,933 225.6%7 5 Allen & Overy 21,330 35 11,909 79.1%31 6 Greenberg Traurig 20,422 3 3,343 510.9%202 7 Alston & Bird 20,115 2 - -139 8 Cravath Swaine & Moore 20,100 2 100 20,000%

- 9= Creel, Garcia-Cuellar, Aiza y Enriquez 20,100 1 - -65 9= Mijares, Angoitia, Cortes y Fuentes 20,100 1 756 2,559%28 11 De Brauw Blackstone Westbroek 14,585 31 3,728 291.2%15 12 Wachtell, Lipton, Rosen & Katz 8,649 3 9,000 -3.9%16 13 Cleary Gottlieb Steen & Hamilton 8,078 8 7,013 15.2%4 14 Loyens & Loeff 7,725 36 19514 -60.4%3 15 Linklaters 7,369 21 19,908 -63.0%

Press Release: mergermarket M&A Round-up for Q1-Q3 2012 24 www.mergermarket.com

Europe: League Tables of Legal Advisers

Legal Advisers to Spanish M&A: VolumeRanking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2011

Q1-Q3 2012 Company Name

Value (US$m)

Deal Count

Deal Count

Count Change

1 1 Garrigues 10,110 31 37 -62 2 Cuatrecasas, Goncalves Pereira 1,767 21 31 -103 3 Uria Menendez 9,816 17 30 -137 4 Linklaters 4,627 17 16 111 5 Baker & McKenzie 2,078 11 11 013 6 DLA Piper 289 11 10 19 7 Deloitte Legal 468 10 13 -320 8 Ashurst 1,386 9 4 54 9 Freshfields Bruckhaus Deringer 11,200 8 22 -145 10 Clifford Chance 4,256 7 18 -1116 11 Jones Day 1,575 6 7 -118 12 Hogan Lovells 3,092 5 5 0- 13 Bird & Bird 530 4 - -8 14 KPMG Abogados 470 4 15 -11- 15 Lefosse Advogados 3,931 3 - -

Legal Advisers to Spanish M&A: ValueRanking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2011

Q1-Q3 2012 Company Name

Value (US$m)

Deal Count

Value (US$m)

% Val. Change

2 1 Freshfields Bruckhaus Deringer 11,200 8 36,957 -69.7%7 2 Garrigues 10,110 31 10,791 -6.3%1 3 Uria Menendez 9,816 17 42,781 -77.1%5 4 Linklaters 4,627 17 17,454 -73.5%3 5 Clifford Chance 4,256 7 26,556 -84.0%- 6 Lefosse Advogados 3,931 3 - -

19 7= Machado Meyer Sendacz e Opice 3,255 2 3,161 3.0%18 7= Souza, Cescon, Barrieu & Flesch Advogados 3,255 2 3,509 -7.2%73 9 Hogan Lovells 3,092 5 111 2,686%16 10 Baker & McKenzie 2,078 11 4,212 -50.7%4 11 Cuatrecasas, Goncalves Pereira 1,767 21 20,931 -91.6%53 12 Jones Day 1,575 6 245 542.9%21 13 Sullivan & Cromwell 1,413 1 2,925 -51.7%37 14 Ashurst 1,386 9 720 92.5%46 15 Ramon & Cajal 1,311 2 354 270.3%

Legal Advisers to Iberian M&A: VolumeRanking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2011

Q1-Q3 2012 Company Name

Value (US$m)

Deal Count

Deal Count

Count Change

1 1 Garrigues 10,110 31 39 -82 2 Cuatrecasas, Goncalves Pereira 2,371 24 35 -116 3 Linklaters 12,296 23 18 53 4 Uria Menendez 15,303 19 31 -1211 5 Baker & McKenzie 2,078 11 11 013 6 DLA Piper 289 11 10 19 7 Deloitte Legal 468 10 13 -322 8 Ashurst 1,386 9 4 54 9 Freshfields Bruckhaus Deringer 11,200 8 22 -145 10 Clifford Chance 4,520 8 18 -1016 11 Jones Day 1,575 6 7 -126 12 Morais Leitao Galvao Teles Soares Da

Silva & Associados6,468 5 4 1

18 13 Hogan Lovells 3,092 5 5 0103 14 PLMJ - Sociedade de Advogados 5,810 4 1 315 15 Allen & Overy 3,942 4 7 -3

Legal Advisers to Iberian M&A: ValueRanking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2011

Q1-Q3 2012 Company Name

Value (US$m)

Deal Count

Value (US$m)

% Val. Change

1 1 Uria Menendez 15,303 19 42,781 -64.2%5 2 Linklaters 12,296 23 17,454 -29.6%2 3 Freshfields Bruckhaus Deringer 11,200 8 36,957 -69.7%- 4 Campos Ferreira, Sa Carneiro e Asociados 11,060 2 - -6 5 Garrigues 10,110 31 15,762 -35.9%

107 6 Morais Leitao Galvao Teles Soares Da Silva & Associados

6,468 5 8 80,750%

96 7 PLMJ - Sociedade de Advogados 5,810 4 29 19,934%- 8 Servulo Correia & Associados 5,696 2 - -

109 9 Vieira de Almeida & Associados 5,633 1 6 93,783%11 10= Bredin Prat 5,427 1 6,031 -10.0%28 10= Mattos Filho, Veiga Filho, Marrey Jr. e

Quiroga Advogados5,427 1 2,005 170.7%

3 12 Clifford Chance 4,520 8 26,556 -83.0%18 13 Allen & Overy 3,942 4 4,407 -10.6%- 14 Lefosse Advogados 3,931 3 - -

21 15= Machado Meyer Sendacz e Opice 3,255 2 3,161 3.0%8 15= Souza, Cescon, Barrieu & Flesch Advogados 3,255 2 8,472 -61.6%

Press Release: mergermarket M&A Round-up for Q1-Q3 2012 25 www.mergermarket.com

Europe: League Tables of Legal AdvisersLegal Advisers to Nordic M&A: Volume

Ranking Q1-Q3 2012 Q1-Q3 2011Q1-Q3 2011

Q1-Q3 2012 Company Name

Value (US$m)

Deal Count

Deal Count

Count Change

19 1 Bech-Bruun 7,452 48 19 292 2 Mannheimer Swartling 2,540 42 51 -98 3 Kromann Reumert 6,498 37 31 69 4 Wiersholm 6,631 36 29 71 5 Vinge 3,821 35 51 -163 6 Schjodt 2,957 35 39 -44 7 Hannes Snellman 5,435 30 38 -85 8 Roschier 4,446 28 35 -76 9 Plesner 3,024 28 34 -610 10 Thommessen 7,063 27 29 -211 11 Wikborg Rein & Co 2,097 27 29 -218 12 Gorrissen Federspiel 3,564 26 20 614 13 Advokatfirman Lindahl 257 26 24 27 14 Accura 3,411 22 32 -1033 15 Delphi 165 18 10 8

Legal Advisers to Nordic M&A: ValueRanking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2011

Q1-Q3 2012 Company Name

Value (US$m)

Deal Count

Value (US$m)

% Val. Change

12 1 Clifford Chance 15,449 12 9,724 58.9%40 2 Shearman & Sterling 11,612 1 2,678 333.6%1 3 Freshfields Bruckhaus Deringer 10,813 10 24,142 -55.2%14 4 Linklaters 9,967 13 8,506 17.2%8 5 Skadden Arps Slate Meagher & Flom 8,925 3 11,581 -22.9%4 6 Bech-Bruun 7,452 48 14,820 -49.7%3 7 White & Case 7,367 16 20,682 -64.4%16 8 Thommessen 7,063 27 8,016 -11.9%15 9 Wiersholm 6,631 36 8154 -18.7%11 10 Kromann Reumert 6,498 37 10,242 -36.6%36 11 Latham & Watkins 6,275 4 3,016 108.1%153 12 Loyens & Loeff 5,875 4 54 10,780%18 13 Eversheds 5,814 10 6,834 -14.9%- 14 Kinstellar 5,806 3 - -

19 15 Hannes Snellman 5,435 30 6,633 -18.1%

Legal Advisers to Swedish M&A: ValueRanking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2011

Q1-Q3 2012 Company Name

Value (US$m)

Deal Count

Value (US$m)

% Val. Change

1 1 Freshfields Bruckhaus Deringer 7,234 5 22,384 -67.7%11 2 Clifford Chance 6,249 9 7,625 -18.0%4 3 Bech-Bruun 3,837 6 13,740 -72.1%9 4 Vinge 3,821 34 7,965 -52.0%2 5 White & Case 3,532 12 20,072 -82.4%48 6 Kromann Reumert 3,380 7 895 277.7%16 7 Kirkland & Ellis 3,257 2 3,707 -12.1%23 8 Roschier 3,009 13 3204 -6.1%65 9 Advokatfirmaet BA-HR DA 2,834 4 444 538.3%49 10 Accura 2,816 6 878 220.7%38 11 Gernandt & Danielsson 2,622 12 1,474 77.9%12 12 Mannheimer Swartling 2,414 40 6,475 -62.7%46 13 Allen & Overy 2,302 3 990 132.5%75 14 Baker & McKenzie 2,301 6 289 696.2%13 15 P+P Poellath + Partners 2,289 3 4,634 -50.6%

Legal Advisers to Swedish M&A: VolumeRanking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2011

Q1-Q3 2012 Company Name

Value (US$m)

Deal Count

Deal Count

Count Change

2 1 Mannheimer Swartling 2,414 40 50 -101 2 Vinge 3,821 34 50 -163 3 Advokatfirman Lindahl 248 24 24 06 4 Hannes Snellman 1,723 19 19 09 5 Wistrand 470 17 16 114 6 Delphi 165 17 10 711 7 Roschier 3,009 13 15 -28 8 White & Case 3,532 12 18 -67 9 Gernandt & Danielsson 2,622 12 19 -74 10 Cederquist 1,919 11 21 -1025 11 Clifford Chance 6,249 9 4 55 12 Setterwalls 1,609 9 19 -1010 13 Linklaters 1,353 8 15 -718 14 Kromann Reumert 3,380 7 7 021 15 Eversheds 2,039 7 6 1

Press Release: mergermarket M&A Round-up for Q1-Q3 2012 26 www.mergermarket.com

Europe: League Tables of Legal Advisers

Legal Advisers to Russian M&A: VolumeRanking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2011

Q1-Q3 2012 Company Name

Value (US$m)

Deal Count

Deal Count

Count Change

2 1 White & Case 7,642 8 12 -418 2 Skadden Arps Slate Meagher & Flom 7,101 8 3 54 3 Akin Gump Strauss Hauer & Feld 4,351 5 9 -413 4 Cleary Gottlieb Steen & Hamilton 4,151 5 4 16 5 DLA Piper 2,620 5 6 -117 6 Clifford Chance 590 5 4 13 7 Linklaters 3,736 4 9 -526 8 SALANS 500 4 2 219 9 Squire Sanders 208 4 3 15 10 Hogan Lovells 2,261 3 8 -510 11 Debevoise & Plimpton 902 3 4 -11 12 Freshfields Bruckhaus Deringer 620 3 15 -1211 13 Allen & Overy 463 3 4 -124 14 Hannes Snellman 33 3 2 18 15 Baker & McKenzie - 3 5 -2

Legal Advisers to Russian M&A: ValueRanking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2011

Q1-Q3 2012 Company Name

Value (US$m)

Deal Count

Value (US$m)

% Val. Change

11 1 White & Case 7,642 8 2,741 178.8%10 2 Skadden Arps Slate Meagher & Flom 7,101 8 2,881 146.5%7 3 Akin Gump Strauss Hauer & Feld 4,351 5 4,639 -6.2%13 4 Cleary Gottlieb Steen & Hamilton 4,151 5 1,873 121.6%1 5 Linklaters 3,736 4 16,416 -77.2%- 6= Kinstellar 3,525 1 - -- 6= Taboglu & Demirhan 3,525 1 - -8 8 DLA Piper 2,620 5 3,801 -31.1%15 9 Hogan Lovells 2,261 3 1,397 61.8%- 10 YukselKarkinKucuk Law Firm 1,900 2 - -- 11 Herguner Bilgen Ozeke 1,900 1 - -- 12 Liniya Prava 1,774 2 - -3 13 Debevoise & Plimpton 902 3 12,137 -92.6%- 14= Herbert Smith 714 2 - -

63 14= LAWIN 714 2 - -

Legal Advisers to CEE M&A: VolumeRanking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2011

Q1-Q3 2012 Company Name

Value (US$m)

Deal Count

Deal Count

Count Change

12 1 Allen & Overy 4,817 16 11 53 2 Clifford Chance 1,426 14 21 -72 3 CMS 658 14 23 -91 4 White & Case 7,915 13 24 -115 5 Linklaters 4,386 12 20 -88 6 DLA Piper 4,471 11 15 -410 7 LAWIN 714 11 14 -36 8 Baker & McKenzie 513 10 19 -914 9 SORAINEN 216 10 10 013 10 Wolf Theiss 53 9 11 -230 11 Skadden Arps Slate Meagher & Flom 7,101 8 4 424 12 SALANS 760 8 6 27 13 Raidla Lejins & Norcous 217 8 18 -104 14 Freshfields Bruckhaus Deringer 4,595 7 20 -1316 15 Havel, Holasek & Partners 3,602 6 9 -3

Legal Advisers to CEE M&A: ValueRanking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2011

Q1-Q3 2012 Company Name

Value (US$m)

Deal Count

Value (US$m)

% Val. Change

12 1 White & Case 7,915 13 5,534 43.0%17 2 Skadden Arps Slate Meagher & Flom 7,101 8 3,390 109.5%8 3 Weil Gotshal & Manges 5,439 5 8,476 -35.8%3 4 Allen & Overy 4,817 16 13,583 -64.5%1 5 Freshfields Bruckhaus Deringer 4,595 7 24,414 -81.2%5 6 DLA Piper 4,471 11 10,790 -58.6%2 7 Linklaters 4,386 12 22,884 -80.8%13 8 Akin Gump Strauss Hauer & Feld 4,351 5 4,639 -6.2%23 9 Cleary Gottlieb Steen & Hamilton 4,151 5 1,873 121.6%50 10 Havel, Holasek & Partners 3,602 6 219 1,545%70 11 Kinstellar 3,558 6 98 3,531%- 12 Taboglu & Demirhan 3,525 1 - -

81 13 Kirkland & Ellis 3,498 2 46 7,504%- 14 McCarthy Tetrault 3,498 1 - -

26 15 Hogan Lovells 2,261 4 1,397 61.8%

Press Release: mergermarket M&A Round-up for Q1-Q3 2012 27 www.mergermarket.com

Europe: League Tables of Legal AdvisersLegal Advisers to Irish M&A: Volume

Ranking Q1-Q3 2012 Q1-Q3 2011Q1-Q3 2011

Q1-Q3 2012 Company Name

Value (US$m)

Deal Count

Deal Count

Count Change

2 1 A&L Goodbody 20,895 14 22 -81 2 Arthur Cox 13,489 11 26 -155 3 McCann FitzGerald 8,156 9 13 -43 4 William Fry 941 9 16 -74 5 Matheson Ormsby Prentice 13,254 8 15 -76 6 Mason Hayes & Curran 62 7 10 -311 7 Linklaters 1,328 6 3 3- 8 Maples & Calder 7 6 - -

10 9 DLA Piper 589 4 3 129 10 Pinsent Masons 143 4 2 217 11 Clifford Chance 7,387 3 3 08 12 Allen & Overy 750 3 5 -262 13 CMS 151 3 1 2- 14 SALANS 16 3 - -7 15 Eversheds 7 3 8 -5

Legal Advisers to Irish M&A: ValueRanking Q1-Q3 2012 Q1-Q3 2011

Q1-Q3 2011

Q1-Q3 2012 Company Name

Value (US$m)

Deal Count

Value (US$m)

% Val. Change

3 1 A&L Goodbody 20,895 14 10,333 102.2%1 2 Arthur Cox 13,489 11 23,462 -42.5%9 3 Matheson Ormsby Prentice 13,254 8 3,913 238.7%23 4 Cleary Gottlieb Steen & Hamilton 12,635 2 960 1,216%44 5 Latham & Watkins 11,940 2 161 7,316%76 6= Blake, Cassels & Graydon 11,940 1 - -- 6= Davis Polk & Wardwell 11,940 1 - -- 6= Kinstellar 11,940 1 - -

31 6= Simpson Thacher & Bartlett 11,940 1 370 3,127%12 6= Slaughter and May 11,940 1 2,583 362.3%- 6= Wachtell, Lipton, Rosen & Katz 11,940 1 - -

20 12 McCann FitzGerald 8,156 9 1,499 444.1%37 13 Clifford Chance 7,387 3 222 3,227%- 14= Milbank Tweed Hadley & McCloy 7,300 1 - -- 14= Nagashima Ohno & Tsunematsu 7,300 1 - -

Press Release: mergermarket M&A Round-up for Q1-Q3 2012 28 www.mergermarket.com

• Q3 2012 US M&A totaled US$ 206.7bn, up 4.8% on Q3 2011 • Q1-Q3 2012 down 18.6% from Q1-Q3 2011 • Industrials & Chemicals saw sharp decline

The US saw M&A in Q3 2012 with a total value of US$ 206.7bn, up 11.7% from Q2 2012 (US$ 185.1bn). Combined, Q1-Q3 2012’s total of US$ 512.1bn was however down by 18.6% on Q1-Q3 2011 (US$ 628.8bn), making it the lowest Q1-Q3 period since Q1-Q3 2010 (US$ 476.4bn). Q3 2012 saw a year-on-year increase of 4.8% from Q3 2011 (US$ 197.2bn). It was the highest quarterly total since Q1 2011 (US$ 247.2bn) and third highest since Q3 2008 (US$ 263bn). The US accounted for 35% of aggregate global deal activity in 2012 to date, down slightly from its 35.5% share in 2011.

Energy, Mining & Utilities was the most active sector in Q1-Q3 2012 with US$ 117bn-worth of deals, accounting for 22.9% of US M&A in Q1-Q3 2012. Industrials & Chemicals was down 51.9% from the comparable period in 2011 with US$ 60.3bn in deals in 2012 compared to US$ 125.5bn in Q1-Q3 2011.

Four of the top ten deals in the fi rst three quarters of 2012 were in the Energy, Mining & Utili-ties sector, which continued to dominate. They included the US’s second largest 2012 deal so far, ConocoPhillips spinning off its downstream operations valued at US$ 20.8bn. The remain-ing Energy, Mining & Utilities transactions were all valued above US$ 5bn.

US inbound cross-border deals amounted to US$ 44.4bn in Q3, the second highest quarterly total since Q4 2010 (US$ 63bn). US outbound cross-border deals totalled US$ 29.7bn, down 51.5% from the previous quarter (US$ 61.3bn), and down 43.3% from the same period last year (US$ 52.4bn).

Skadden Arps Slate Meagher & Flom topped the legal advisory ranking by total deal value, up four spots from last year. Latham & Watkins came in at second, also up four spots from last year. Both fi rms had signifi cant declines in deal value from the comparable period last year. Simpson Thacher & Bartlett dropped from the top spot in 2011 to third for 2012.

US M&A Overview

0

25

50

75

100

125

150

175

200

225

250

275

300

325

0

10

20

30

40

50

60

70

80

90

100

110

120

130

140

Volu

me

of D

eals

Valu

e of

Dea

ls (U

S$bn

)

US Inbound/Outbound M&A

Inbound Value (US$bn) Outbound Value (US$bn) Inbound Volume Outbound Volume

Press Release: mergermarket M&A Round-up for Q1-Q3 2012 29 www.mergermarket.com

Americas M&A Heat Chart

Hot Warm Cold

600 100 20

400 60 10

300 30 0

Note: The Intelligence Heat Chart are based on “companies for sale” tracked by mergermarket in the respective regions between 12 March 2012 and 11 September 2012. Opportunities are captured according to the dominant geography and sector of the potential target company. mergermarket’s Heat Chart of predicted deal flow is based on the intelligence collected in our database relating to companies rumoured to be for sale, or officially up for sale in the respective regions. It is therefore indicative of areas that are likely to be active in the months to come. The intelligence comes from a range of sources, including press reports, company statements and our own team of journalists gathering proprietary intelligence from M&A across the regions. The data does not differentiate between small and large transactions, nor between deals that could happen in the short or long-term.

In the US, it is hoped that the Federal Reserve’s QE3 launch will give the currently sluggish economic recovery a much needed boost.

• TMT is seen as the hottest sector based on the “Companies for sale” activity. Social collaboration, mobile and data analytics continue to pave the way for more activity in technology; print media has been revived in light of an increased interest in regional papers; and telecom deals will remain on the rise in light of heightened Internet traffi c driving activity in fi ber to wireless towers.

• The Pharma, Medical & Biotech sector comes second with the healthcare sector expected to continue its consolidation as the Affordable Care Act (ACA) was upheld by the US Supreme Court in June 2012.