Embed Size (px)

DESCRIPTION

reference

Citation preview

7/15/2019 Legal Acctng Cases

http://slidepdf.com/reader/full/legal-acctng-cases 1/108

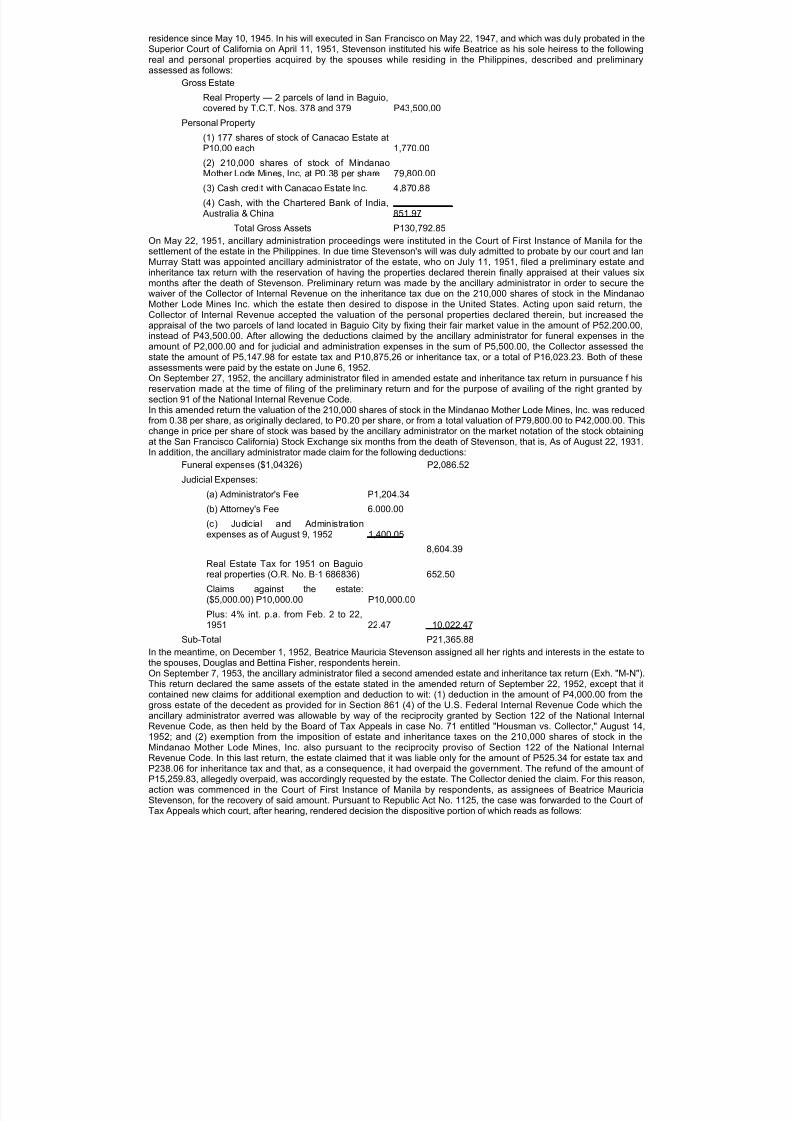

1. WILLIAM LI YAO vs. COLLECTOR OF INTERNAL REVENUE, G.R. No. L-11875, Dec. 28, 19632. DR. LUCAS G. ADAMSON and ADAMSON MANAGEMENT CORP. vs. CA and APAC HOLDINGS LIMITED,

G.R. No. 106879, May 27, 19943. PRESIDENTIAL ANTI-GRAFT COMMISSION (PAGC) and THE OFFICE OF THE PRESIDENT vs. SALVADOR

A. PLEYTO, G.R. No. L-17715, July 31, 19634. JOSE AVELINO vs. COLLECTOR OF INTERNAL REVENUE, G.R. No. 176058, March 23, 20115. CHIEF JUSTICE RENATO C. CORONA vs. SENATE OF THE PHILIPPINES sitting as an IMPEACHMENT

COURT, BANK OF THE PHILIPPINE ISLANDS, PHILIPPINE SAVINGS BANK, ARLENE "KAKA" BAG-AO,GIORGIDI AGGABAO, MARILYN PRIMICIAS-AGABAS, NIEL TUPAS, RODOLFO FARINAS, SHERWIN

TUGNA, RAUL DAZA, ELPIDIO BARZAGA, REYNALDO UMALI, NERI COLMENARES (ALSO KNOWN AS THEPROSECUTORS FROM THE HOUSE OF REPRESENTATIVES), G.R. No. 200242, July 17, 20126. PCIB vs. VENICIO ESCOLIN, Presiding Judge of the CFI Iloilo, Branch II, and AVELINA A. MAGNO, G.R. Nos. L-

27860 and L-27896 March 29, 1974 / TESTATE ESTATE OF THE LATE LINNIE JANE HODGES vs. LORENZOCARLES, et. al., G.R. Nos. L-27936 & L-27937 March 29, 1974

7. OCA vs. JUDGE UYAG P. USMAN, Judge, Shari'a Circuit Court, Pagadian City, A.M. No. SCC-08-12, October 19, 2011 (Formerly OCA I.P.I. No. 08-29-SCC)

8. BRIGIDO B. QUIAO vs. RITA C. QUIAO, KITCHIE C. QUIAO, LOTIS C. QUIAO, PETCHIE C. QUIAO, rep bytheir mother RITA QUIAO, G.R. No 176556, July 4, 2012

9. WONDER BOOK CORP. vs. PHIL. BANK OF COMMUNICATIONS, G.R. No. 187316, July 16, 201210. FERDINAND R. MARCOS, JR. vs. REPUBLIC rep. by the PCGG, G.R. No. 189434, April 25, 2012 IMELDA

ROMUALDEZ-MARCOS vs. REPUBLIC, G.R. No. 18950511. COLLECTOR OF INTERNAL REVENUE vs. DOUGLAS FISHER AND BETTINA FISHER, CA, G.R. No. L-11622,

January 28, 1961 / DOUGLAS FISHER AND BETTINA FISHER vs.COLLECTOR OF INTERNAL REVENUE, and the CA, G.R. No. L-11668, January 28, 196112. SAMHWA COMPANY LTD., and LOTUS EXPORTS SPECIALISTS, INC. vs. IAC, LOUIS SHEFF and

HERSCHELL SWIRYN, G.R. No. 74305, January 31, 199213. COMMISSIONER OF INTERNAL REVENUE vs. CA, R.O.H. AUTO PRODUCTS PHILIPPINES, INC. and CTA,

G.R. No. 108358, January 20, 199514. TOMAS CALASANZ, ET AL. vs. COMM. INTERNAL REVENUE & CTA, G.R. No. L-26284, 10-8-86 15. HEIRS OF TAN ENG KEE vs. CA and BENGUET LUMBER COMPANY, G.R. No. 126881, Oct 3, 2000

WILLIAM LI YAO vs. COLLECTOR OF INTERNAL REVENUE, G.R. No. L-11875, December 28, 1963

LABRADOR, J.:This is a petition filed by William Li Yao for the review of a decision of the Court of Tax Appeals in C.T.A. Case No. 30,

entitled "William Li Yao, petitioner, vs. Collector of Internal Revenue, respondent." The record discloses that petitioner is anaturalized Filipino of Chinese parents, the eldest son of a prosperous local businessman by the name of Li Chay Too,who died sometime in 1948. In 1945 petitioner organized the Li Yao and Company and made himself managing partner;from 1948 to February 1955 he was president of, and owned shares in, the Li Chay Too and Sons, Inc.; and in 1950 heorganized a corporation known as the Far East Realty and Investment Co. (known as FERIN for short) of which he wasalso stockholder and president. Petitioner filed his income tax returns for the years 1945 to 1951, paying the followingtaxes:

YEAR AMOUNT OF TAX

1945 P 918.31

1946 1,393.42

1947 5,923.57

1948 700.34

1949 538.07

1950 3,837.00

1951 2,971.00

In 1948 a verification of his income tax returns for the years 1945 to 1947 was made and a deficiency income tax in theamount of P5,470.98 was assessed against him, which he paid.In 1952 the Collector of Internal Revenue, believing that petitioner had not reported his true incomes for the previousyears, appointed a team to examine his books, on July 30, 1952 an additional assessment of P898,794.02 was madeagainst him for the years 1945 to 1951, inclusive. A second team of investigators was appointed on June 30, 1953 thisteam recommended a deficiency income tax assessment of P2,722,030.33. This team employed what is known as the net

worth or inventory method. A third team was appointed, headed by BIR Examiner Quesada. This team recommended anassessment of P1,505,768.54 against petitioner; the inventory method was also used in making this assessment. Demandwas made for the collection of said assessment on August 10, 1954, so petitioner herein presented a petition with theCourt of Tax Appeal for the review of the said assessment.

After hearing the Court of Tax Appeals, after revising the various items contained in the assessment of BIR Examiner Quesada, made various findings of fact on the issues presented by the parties and thereafter rendered a decision in whichit found that the amount of the income tax deficiency due from petitioner P424,536.77. The resume of the assessmentmade in the decision of the Court of Tax Appeals is as follows:

1945

Assets admitted by parties Add assets established at trial:

P 41,538.50143,910.89

7/15/2019 Legal Acctng Cases

http://slidepdf.com/reader/full/legal-acctng-cases 2/108

Funds held in trust by father, Li Chay TooNet Worth as of December 31, 1945Less Net Worth as of January 1, 1945:

P 185,449.39

Assets admitted by Parties Add assets proven at trialFunds held in trust by father, Li Chay Too

P 500.00159,910.89160,410.89

Increase in net worth in 1945 Add non-deductible expenditures:

Personal living and family expenses

P 25,038.503,500.00

28,538.50

Less personal exemptions 3,500.00

Amount subject to tax 25,038.50

Tax due thereon 1,082.31

Less tax already paid 1,111.74

No deficiency tax due(29.43)

=================

1946

Assets admitted by both parties Add assets established at trial:cash funds from loansTotal assets

P 148,326.7790,032.43

P 238,359.20

Liabilities established at trial 100,000.00

Net worth as of December 31, 1946Less net worth as of Jan. 1, 1946 185,449.39

Decrease in net worth in 1946 (P 47,090.19)

Add non-deductible expenditures:Personal living and family expenses 3,500.00

Income tax paid in previous year 918.91

Net loss(P 42,671.88)=================

1947

Assets admitted by parties P 184,453.45

Add assets established at trial:Cash funds from loans P 78,036.52

Total assets P 262,489.97

Liabilities established at trial 100,000.00

Net worth as of December 31, 1947 P 162,489.97

Less net worth as of Jan. 1, 1947 138,359.20

Increase in net worth in 1947 P 24,130.77

Add: non-deductible expenditures:

Personal, living and familyexpenses 3,500.00

Income tax paid in previous year 1,393.42

Net Income P 29,024.19

Less personal exemptions 3,500.00

Amount subject to tax 25,524.19

Tax due thereon 3,795.32

7/15/2019 Legal Acctng Cases

http://slidepdf.com/reader/full/legal-acctng-cases 3/108

Less tax already paid 10,055.78

No deficiency tax due(P 6,260.46)=============

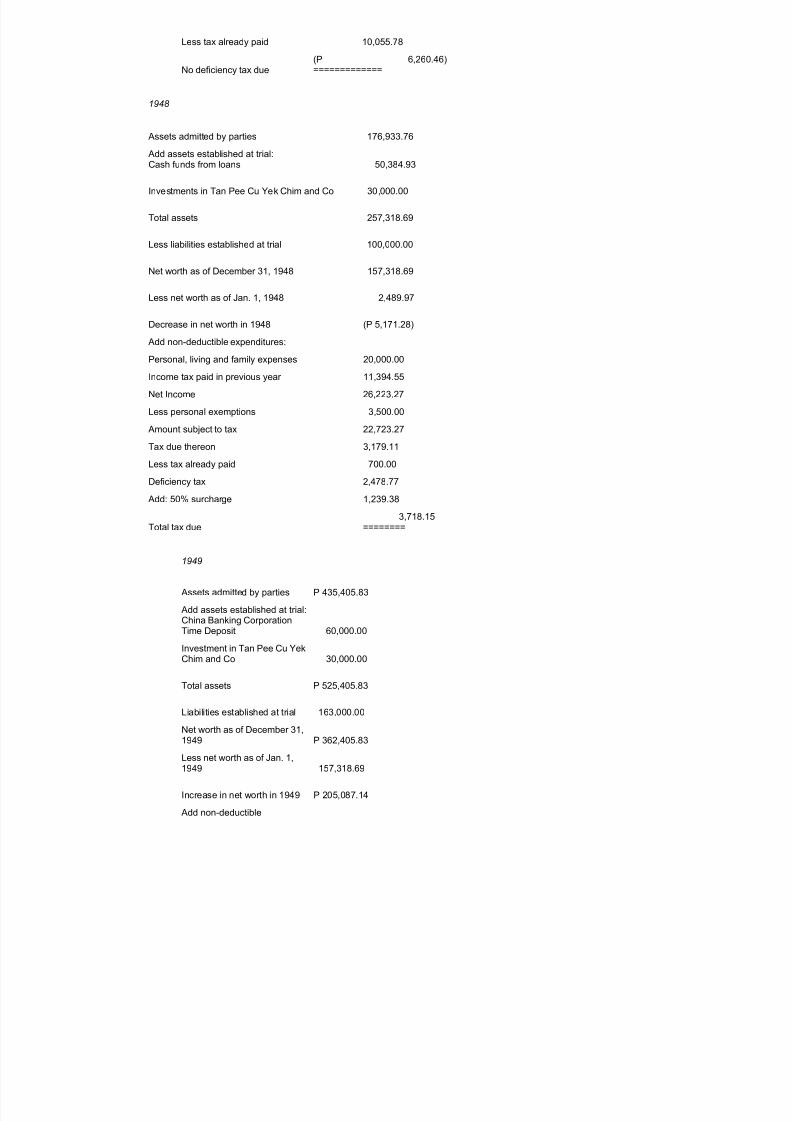

1948

Assets admitted by parties

176,933.76 Add assets established at trial:Cash funds from loans 50,384.93

Investments in Tan Pee Cu Yek Chim and Co 30,000.00

Total assets 257,318.69

Less liabilities established at trial 100,000.00

Net worth as of December 31, 1948 157,318.69

Less net worth as of Jan. 1, 1948 2,489.97

Decrease in net worth in 1948 (P 5,171.28)

Add non-deductible expenditures:

Personal, living and family expenses 20,000.00

Income tax paid in previous year 11,394.55

Net Income 26,223.27

Less personal exemptions 3,500.00

Amount subject to tax 22,723.27

Tax due thereon 3,179.11

Less tax already paid 700.00

Deficiency tax 2,478.77

Add: 50% surcharge 1,239.38

Total tax due3,718.15

========

1949

Assets admitted by parties P 435,405.83

Add assets established at trial:China Banking CorporationTime Deposit 60,000.00

Investment in Tan Pee Cu YekChim and Co 30,000.00

Total assets P 525,405.83

Liabilities established at trial 163,000.00

Net worth as of December 31,1949 P 362,405.83

Less net worth as of Jan. 1,1949 157,318.69

Increase in net worth in 1949 P 205,087.14

Add non-deductible

7/15/2019 Legal Acctng Cases

http://slidepdf.com/reader/full/legal-acctng-cases 4/108

expenditures:

Personal, living and familyexpenses 20,000.00

Income tax paid in previousyear 700.34

Net Income P 225,787.48

Less personal exemptions 3,500.00

Net income before deductionof inheritance P 222,287.48

Less inheritance 72,392.91

Amount subject to tax 149,894.57

Tax due thereon 47,137.82

Less tax already paid 538.07

Deficiency tax P 46,599.75

Add: 50% surcharge 23,299.87

Total tax dueP 69,899.62=============

1950

Assets admitted by parties P 842,273.50

Add assets established at trial:Investments in Tan Pee CuYek Chim and Co 30,000.00

Investments in FERIN throughothers 170,000.00

Race Horses 11,500.00

Total Assets P1,053,773.50

Liabilities established at trial 445,500.00

Net worth as of Dec. 31, 1950 608,273.50

Less net worth as of Jan. 1,

1950 362,405.83

Increase in net worth in 1950 P 245,867.67

Add: non-deductibleexpenditures:

Personal, living and familyexpenses 20,000.00

Income tax paid in previousyear 538.07

Net Income 266,405.74

Less personal exemptions 4,200.00

Amount subject to tax P 262,205.74

Tax due thereon 125,977.00

Less tax already paid 3,837.00

Deficiency tax P 122,140.00

Add: 50% surcharge 61,070.00

Total tax due P 183,210.00

7/15/2019 Legal Acctng Cases

http://slidepdf.com/reader/full/legal-acctng-cases 5/108

=============

1951

Assets admitted by partiesP1,630,658.94

Add assets established at trial:Investments in Tan Pee Cu Yek Chim

and Co 30,000.00Investments in FERIN through others 200,000.00

Race Horses 11,500.00

Total Assets 1,872,158.94

Liabilities established at trial 1,040,500.00

Net worth as of Dec. 31, 1951 831,658.94

Less net worth as of Jan. 1, 1951 608,273.50

Increase in net worth 223,385.44

Add: non-deductiblePersonal, living and family expenses 20,000.00

Income tax paid in previous year 3,839.00

Net Income P 247,222.44

Less personal exemptions 4,800.00

Amount subject to tax 242,422.44

Tax due thereon P 114,777.00

Less tax already paid 2,971.00

Deficiency tax 111,806.00

Add: 50 % surcharge 55,903.00

Total tax dueP 167,709.00===========

Summary of Tax Due

1945 None

1946 None

1947 None

1948 P 3,718.15

1949 69,899.62

1950 183,210.00

1951 167,709.00

Total tax due P 424,536.77===========

Petitioner Li Yao sought to reconsider the decision and the assessment, alleging that the sum of P5,470.98 paid by him asadditional tax for the years 1945 to 1947 should be credited against his deficiency income taxes, so that instead of P424,536.77 this sum due should be only P411,294.12, following the decision in the case of University of Santo Tomas

vs. Collector of Internal Revenue, C.T.A. Case No. 10, dated June 4, 1956, in which the doctrine of equitable recoupmentwas applied provided the two requirements for its applicability are met. The court approved this petition for recoupmentand reduced the assessment to P411,293.80.Both petitioner and respondent appealed from the decision of the Court of Tax Appeals — petitioner's appeal is within thecase G.R. No. L-11875 and the respondent's appeal is case G.R. No. L-11861. This decision deals with Li Yao's appeal.Two principal questions are raised by petitioner Li Yao before Us, the first of which questions the validity of the net worthmethod of inventory used against him, and the second assails the Court of Tax Appeals, refusal to grant petitioner'srequest that the deficiency income assessed be distributed evenly over the taxable years. We will leave these questionsfor the present until after We have decided the appeal raised against various items of the assessment.The first issue relates to the disapproval of various items, claimed by petitioner to be his obligations, which are as follows:

J. Crisostomo Chavez P100,000.00

7/15/2019 Legal Acctng Cases

http://slidepdf.com/reader/full/legal-acctng-cases 6/108

Li Chick Eng 50,000.00

Ong Tiao Seng 20,000.00

Li Chiu Ka 20,000.00

Li Tong Na 20,000.00

Ko Chiu Seng 10,000.00

Carlos M. Go 10,000.00

Dee Mong @ Lim Sing 25,000.00

Arturo Mercado 10,000.00

Go Hoc 20,000.00

Ong Chin P 30,000.00

T O T A L P 315,000.00===========

The procedure adopted by the Court of Tax Appeal in passing upon the first of these alleged obligations is as follows:

. . . that when a taxpayer claims he owes money to another for the purpose of reducing his tax liability, particularly the NetWorth Expenditure (Inventory) Method of investigation is employed against him, his admission (claim) must corroboratedby other evidence independent of the admission itself. For example, the promissory note, if there be any, should beproduced for the inspection of the Court and government counsel. The alleged creditor must be produced in Court toconfirm the taxpayer's admission and to give government's counsel an opportunity to cross-examine him, unless he isdead, outside of the Philippines, or unable to testify for one reason or another. If the taxpayer is in business, his books asrequired of him by the National Internal Revenue Code should be produced showing the corresponding entry or entries of his alleged liabilities. If for one reason or another the alleged creditor is not available as a witness, his financial capacity toextend the loan should at least be established.

Attacking the above procedure counsel for petitioner argues that in the inventory method the burden of proof lies with theGovernment; that the taxpayer completes his obligation if he furnishes the lead by presenting the evidence of theobligation, and it is thereafter incumbent the Government to follow the lead to determine if the alleged liabilities actually or really existed.

We find no merit or sense in the above contention. The taxpayer has no means of proving the existence of the obligationand it is he that must produce such proof. The obligation and it is he that must produce such proof. The procedurefollowed by the Court of Tax Appeals is that laid down by the rules on evidence; that is, that the taxpayer who allegesthereof by preponderance of evidence. This rule is not only a legal one. In the nature of things, the obligor or taxpayer hasthe means of proving that the obligation does not exist or has been paid; the Government collecting the tax cannot beexpected to find the evidence itself, because it is natural that the taxpayer would try to suppress such evidence as mayprove that the obligation still exists. The court below ruled, in relation to the obligation or the supposed loan given byCrisostomo Chavez, as follows:

Although this loan is evidenced by a duplicate promissory note, Exhibit JJJJ, we find the explanation of petitioner regarding the reproduction of the original note marked Exhibit 55-A from which Exhibit JJJJ was taken, to be highlyfantastic. This alleged creditor was seen by the Court on several occasions loitering in the Court promises during the earlystages of the trial of this case. However, when his turn came to testify as witness for the respondent, he could not beserved with a summons. He was cited by respondent's counsel precisely to confirm or repudiate the contents of an

affidavit which he executed dated July 6, 1955 denying having made such a loan. Considering the past criminal record of this alleged creditor, his failure to testify before this Court upon being cited to do so and the explanation of petitioner regarding the two controversial promissory notes Exhibits 55 and JJJJ, which we believe to be much too strained andfantastic, we cannot give credit to this alleged liability of petitioner.We agree with the court below; the supposed duplicate of the promissory note could well have been fabricated.Furthermore, the supposed creditor had denied the existence of the loan in an affidavit and the taxpayer failed to producehim in evidence. Lastly the taxpayer suppressed the evidence to show that the obligation still exists and if he did so it isbecause the same would be unfavorable to his claim.In connection with the loans of Ong Tiao Seng for P20,000.00, Li Chiu Ka for P20,000.00, Li Tong Na for P20,000.00, KoChiu Seng for P10,000.00, Carlos M. Go for P10,000.00 and Lim Siong for P25,000.00, We, also agree with the courtbelow that as petitioner had not presented the supposed creditors to confirm the existence of the loans, and noexplanation had been given for such failure to present them, the existence of these loans cannot be considered asproven. The petitioner suppressed evidence which should favor him, and his suppression of such evidence proves thatsaid evidence would be unfavorable to him if produced. As to the other loans that had been disapproved for the same

reason, we find the ruling of the court below correct.One of the items subject of the appeal is the P30,000.00 investment in the Tan Pee, Cu Yek Chim and Co., Inc. The saidamount represent shares of stocks issued in the name of Li Yao, petitioner, now contending that Tan Pee transferred theshares to Li Yao in 1948, as he felt ill and was in danger of death, and that when he recovered in the year 1952 hedecided to recall the shares and so requested Li Yao to endorse the certificates of stock back to him, which Li Yao did.Thereafter the shares were again placed in the name of Tan Pee. After analyzing the evidence submitted to support theclaim of petitioner that Tan Pee did not intend ultimately to transfer his stocks to his son-in-law Li Yao, the court belowdeclared that the explanation was not sufficient to refute the presumption that the transfer of said stocks was made for avalid consideration, in the ordinary course of business, so that it considered the item an unreported asset of petitioner for the years 1948 to 1951. After reading the arguments presented by petitioner and considering that the witnesses for petitioner herein are his father-in-law and his wife and their testimonies failed to convince the judges of the court below,this Court finds no potent reason why the findings of the court below that heard the evidence should be disturbed.

7/15/2019 Legal Acctng Cases

http://slidepdf.com/reader/full/legal-acctng-cases 7/108

Another item subject of the appeal is the amount of P60,000.00 deposited with the China Banking Corporation in thename of petitioner as of the end of the year 1949. Petitioner claims that one by the name of James Li, a friend of his,came to the Philippines from Hongkong 1949 bringing with him $30,000.00 in cash which he intended to invest in the localtextile business, so petitioner alleges he deposited this sum with the China Banking Corporation in his name; that the sumwas withdrawn 1949 upon instruction of James Li and delivered to an emissary of the latter by the name of Chen Heng.

As the supposed owner of the fund, James Li was not presented to corroborate petitioner's claim that he owned themoney, nor any other circumstances proved to corroborate petitioner's explanation, the court below held that the evidencewas insufficient and declared the sum as an asset of the petitioner. We also find no reason for disturbing the conclusion of fact and of law made by the court below. It is strange that no evidence of any kind was ever presented to corroborate thestory that the sum belonged to petitioner's friend James Li; no written or testimonial evidence was also presented to provethat the amount, after it was withdrawn from the bank, was actually sent to the supposed owner. Counsel for petitioner contends that there is no prima faciepresumption in favor of the correctness of the assessment made by the respondent.This is true, but the question now involved is not the correctness of the assessment but whether or not the amount of P60,000.00 deposited with the China Banking Corporation belong to Li Yao, petitioner herein. There being no credibleevidence presented that the said amount belongs to James Li and not to Li Yao, then the only reasonable inference is thatthe money must belong to petitioner. The Court of Tax Appeals therefore correctly included it among the assets of thepetitioner. The next items also disallowed by the Court of Tax Appeals are the amounts of P100,000.00 each, belonging totaxpayers Vicente Duazo and Delfin Fulay. The findings of the Court of Tax Appeals on these items are as follows:Of the five, Gloria Pineda and Delfin Fulay are the two persons upon whom suspicion could rest because of their closeassociation with petitioner. As we have said, Gloria Pineda is the private secretary and accountant of petitioner and DelfinFulay is his driver and bodyguard. However, with respect to Gloria Pineda, who is single, her income tax returns Exhibits58, 59, 60, 61 and 62 for 1946 to 1951, inclusive, show that she had a total net income of P25,299.50 during those years.From these returns, it is quite apparent that the investment of P25,000.00 attributed to her in 1950 which was increased to

P40,000.00 in 1951 is not far beyond her reach. The relations of employer and employee between petitioner and GloriaPineda cannot be considered, therefore, as a decisive factor in determining whether she could well afford to investP40,000.00 in the corporation headed by her employer.The case of Delfin Fulay, who is admittedly a bodyguard and driver of petitioner, is quite different. The books of FERINshow that Delfin Fulay invested P85,000.00 in said corporation in 1950, which he increased to P100,000.00 in 1951. Hisincome tax return for the years 1949, Exhibit 66, and his return for 1951, Exhibit 67, show that he had a total net incomeof only P8,500.00 during those years. Could it be possible for a mere hireling like Delfin Fulay, with such a moderateincome to have invested such an enormous amount as P100,000.00 in FERIN? The investment of Fulay in FERIN is sohighly disproportionate to his income, that we find it impossible to believe the investment to be his own. And if theinvestment did not come from his own personal funds with his meager salary as driver and bodyguard, from who elsecould it have come but petitioner, considering the latter's admission that he purposely saw to it that the incorporators of FERIN were his close friends and persons whom he could trust. From all appearance, the petitioner could not havechosen a person more trustworthy than Delfin Fulay the "Man Friday" entrusted with the protection of his life and

limb.lawphil.net The case of Vicente Duazo who is admittedly a bodyguard and driver of petitioner's mother would seem at first blush to beentirely different from that of Delfin Fulay as far as relationship with petitioner is concerned. It appears from the evidencefor the respondent that Vicente Duazo declared a net come in his return for 1948, Exhibit 63, the amount of P2,345.00; for 1949, Exhibit 64, the amount of P1,640.00 and for 1950, Exhibit 65, the amount of P3,480.00 or a total of P7,465.00. Hisinvestment in FERIN in 1950 was P85,000.00 and in 1951, it was increased to P100,000.00. It will be noted that the netincome of Vicente Duazo for three years (1948, 1949, 1950) much less than that of Delfin Fulay for two years (1949,1951). Yet, far from being just a mere coincidence, they invested P25,000.00 each in FERIN in August 25, 1950.... Thisstriking similarity in the amounts invested at the same time, let alone the disparity in the amounts of their respectiveincomes, has led us to the conclusion that the investments of these two persons in said corporation came from only onesource. And the evidence on record indubitably point to petitioner as the source considering his admission that after thedeath of his father, he was entrusted with the business affairs of his family he being the eldest son and favorite of thedeceased.We find no flaw in the facts and in the conclusion arrived at that the two supposed stockholders in FERIN, Duazo andFulay, are mere dummies and said facts an conclusion are hereby affirmed.The last item questioned by petitioner is the sum of P30,000.00 alleged to be his obligation to one Ong Chiu. To supportpetitioner's claim is a copy of a complaint in court against petitioner for the amount. Respondent found one Benjamin OngChiu, who was presented by respondent to show that he had no claim or had filed no such action at the trial that hiscreditor is not the one that respondent presented at the trial, but petitioner did not present the one whom he claims to bethe real creditor. Assuming for the sake of argument that the one presented by respondent is not the real creditor, why didnot petitioner present the supposed real creditor? If there are nine Ong Chiu's well may he have conceived of presenting afictitious action in court in the name of one of them. The case is the same as the other cases above explained - one wherepetitioner has failed to present corroborative evidence, or the real creditor, to prove the existence of the debt in dispute.Failure to adduce the proof required, the petitioner' own testimony may not be held sufficient in law to prove his claim of the existence of the obligation.We next come to the question of the use of the inventory method in assessing the income taxes due from petitioner. Theuse of the inventory method is authorized under Section 15 of the National Internal Revenue Code (Com. Act No. 466), as

amended, which authorizes the Collector of Internal Revenue to assess taxes due a taxpayer from any other availablefact or evidence. If a taxpayer commits a violation of the law, hiding his income to evade payment of taxes, theGovernment must be permitted to resort to all evidence or sources available to determine his said income, so that the taxmay be collected for public purposes. There is and there should be a presumption of regularity accorded this action of theCollector of Internal Revenue in assessing the tax on the best evidence obtainable, otherwise it would be impossible toassess taxes due from a dishonest taxpayer.This form of assessment has also been adopted by the Collector of Internal Revenue with the approval of this Court inthree cases, Perez vs. Collector , G.R. No. L-10507, May 30, 1958; Collector vs. Reyes, G.R. Nos. L-115534 and L-11558,Nov. 25, 1958; and Avelino vs. Collector , No. L-17715, July 31, 1963. In the case at bar the existence of assets or properties appearing in the name of the taxpayer or in the name of his dummies or friends, without the taxpayer beingable to give a definite reasonable explanation for their existence, justifies the Court of Tax Appeals and this Court to resortto the inventory method of assessment, such being necessary and at the same time just and equitable.

7/15/2019 Legal Acctng Cases

http://slidepdf.com/reader/full/legal-acctng-cases 8/108

The last important legal question raised is petitioner's claim that the unreported incomes which appeared during the lastyears of the period of assessment should not be considered as having been earned during the years in which saidincomes appeared but should be spread throughout the whole period covered by the assessment, that is, from 1945 to1951. As authority for this claim the case of U.S. v. Ridley, 120 Fed. Supp. 530 is cited. In the said case Claude Ridleywas assessed for the years through 1951, including taxes, penalties and interests amounting to $106,674.37. Thespouses Claude Ridley were a frugal couple, living in a small farm in which they resided and kept a small store. Norecords were kept of the amount of income earned and of the business transactions entered into from time to time, and itwas possible to determine accurately not only the amount of income received by Claude Ridley, but also to determineaccurately the years in which such income was received. The purchases and expenditures made by the spousesappeared through the years 1937 to 1951, without any specific amount for any particular year. The District Court held thatinasmuch as the oral testimony as well as the oral circumstances indicate that the investment purchases were made fromaccumulated savings rather than from current income and there being no evidence to indicate greater income in one year than in another, the income should be distributed evenly through the years 1937 to 1951, inclusive.The above decision does not sustain the argument adduced by counsel for petitioner. The facts found in the case at bar do not justify the petitioner's claim. Petitioner does not claim that the amounts appearing in the last period of theassessment were acquired through savings or accumulated savings or accumulated savings or any slow and continuousprocess, such that the incomes cannot be distributed to any particular year of the period of assessment.On the other hand, Section 39 of the National Internal Revenue Code requires the taxpayer to report yearly to theCollector of Internal Revenue the income that he gets during the year from whatever source and include the same in thetaxable year in which the income was received by him. It is to be presumed that the income was earned at the time that itappeared in the possession or control of the taxpayer, in accordance with the rule that the law has been followed. [Rule123, Section 69 (q), Rules of Court] Were we to sanction the use of the spreading method claimed, We would betolerating a violation of the law or rule that the taxpayer must report his income in the year it was earned. Under the

practice advocated, a taxpayer would be encouraged to hide his income because in any case, if his unreported incomewould be discovered afterwards the said income, although appearing in one year, would be distributed over a period of years. In other words, we will have a rule, as advocated by petitioner's counsel, that would be discourage the hiding of taxable income because any discovery of any unreported income could always be allowed to be distributed over a periodof years. In the case at bar, the distribution over a period of years demanded by petitioner would bring about a reductionof the tax assessed by the Court of Tax Appeals from P424,536.77 to P232,416.59 (see computation attached to Motionfor Reconsideration, Annex K of Petition for Review), or about one-half of the assessment made by the Court of Appeals.We are not prepared to permit such unauthorized reduction in public taxes favorable to a dishonest taxpayer andprejudicial to the interests of the State.WHEREFORE, finding no merit in the various supposed errors attributed to the Court of Tax Appeals in its decision, Wehereby find that the decision is justified by law and the evidence. Wherefore, the decision appealed from is herebyaffirmed, with costs against the petitioner. So ordered.Bengzon, C.J., Padilla, Bautista Angelo, Concepcion, Reyes, J.B.L., Barrera, Paredes, Dizon, Regala and Makalintal,

JJ., concur. DR. LUCAS G. ADAMSON and ADAMSON MANAGEMENT CORPORATION vs. HON. COURT OF APPEALS andAPAC HOLDINGS LIMITED, G.R. No. 106879 May 27, 1994

ROMERO, J.:Before us is a petition for review on certiorari

of a decision of the Court of Appeals, the dispositive portion of which isquoted hereunder:WHEREFORE, judgment is hereby rendered setting aside respondent judge's questioned order dated 23 August 1991and confirming the subject arbitration award. Costs against private respondents.SO ORDERED.The antecedents of this case are as follows:On June 15, 1990, the parties, Adamson Management Corporation and Lucas Adamson on the one hand, and APAC

Holdings Limited on the other, entered into a contract whereby the former sold 99.97% of outstanding common shares of stocks of Adamson and Adamson, Inc. to the latter for P24,384,600.00 plus the Net Asset Value (NAV) of Adamson and Adamson, Inc. as of June 19, 1990. But the parties failed to agree on a reasonable Net Asset Value. This prompted themto submit the case for arbitration in accordance with Republic Act No. 876, otherwise known as the Arbitration Law.On May 15, 1991, the Arbitration Committee rendered a decision finding the Net Asset Value of the Company to beP167,118.00 which was computed on the basis of a pro-forma balance sheet submitted by SGV and which was thedifference between the total assets of the Company amounting to P65,554,258.00 (the sum of the balance sheet assetamounting to P65,413,978.00 and the increase in Cuevo appraisal amounting to P140,280.00) and total liabilitiesamounting to P65,387,140.00 (the difference between current liabilities and long term debt amounting to P68,356,132.00and Tax Savings for 1987 amounting to P2,968,992).In so holding that NAV equals P167,118.00, the Arbitration Committee disregarded petitioners' argument that there was afixed NAV amounting to P5,146,000.00 as of February 28, 1990 to which should be added the value of intangible assets(P19,116,000.00), the increment of tangible assets excluding land (P17,003,976.00), the 1987 tax savings(P2,968,992.00), and estimated net income from February 28, 1990 to June 19, 1990 (P1,500,000.00, later increased toP3,949,772.00). According to the Committee, however, the amount of P5,146,000.00 which was claimed as initial NAV bypetitioners, was merely an estimate of the Company's NAV as of February 28, 1990 which was still subject to financialdevelopments until June 19, 1990, the cut-off date. The basis for this ruling was Clause 3(B) of the Agreement which fixedthe said amount; Clause 1(A) which defined NAV and provided that it should be computed in accordance with Clause7(A); Clause 7(A) which directed the auditors to prepare in accordance with good accounting principles a balance sheetas of cut-off date which would include the goodwill and intangible assets (P19,116,000.00), the value of tangible assetsexcluding the land as per Cuervo appraisal, the adjustment agreed upon by the parties, and the cost of redeemingpreferred shares; and Clause 5(E). Furthermore, the Committee held that the parties used the figures in the pro-formabalance sheet to arrive at the said amount of P5,146,000.00; that the same had already included the value of theintangible assets and of the Cuervo appraisal of the tangible assets so that the latter items could not be added again towhat Vendor claimed to be the initial NAV; and that apart from being an estimate, the amount of P5,146,000.00 was

7/15/2019 Legal Acctng Cases

http://slidepdf.com/reader/full/legal-acctng-cases 9/108

tentative as it was still subject to the adjustments to be made thereto to reflect subsequent financial events up to the cut-off date.In the computation of the NAV, the Committee deemed it proper to appreciate in favor of petitioners the 1987 tax savingsbecause as of the date of the proceedings, no assessment was ever made by the BIR and the three-year prescriptiveperiod had already expired. However, it did not consider the estimated net income for the period beginning February 28,1990 to June 19, 1990 as part of the NAV because it found that as of June 1990, the books of the company carried a netloss of P4,678,627.00 which increased to P8,547,868.00 after the proposed adjustments were included in the computationof the NAV. The Committee pointed out that although petitioners herein contested the adjustments, they were, however,not able to prove that these were not valid, except with respect to the tax savings.

Aside from deciding the amount of NAV, the Committee also held that any ambiguity in the contract should not necessarilybe interpreted against herein private respondents because the parties themselves had stipulated that the draft of theagreement was submitted to petitioners for approval and that the latter even proposed changes which were eventuallyincorporated in the final form of the Agreement.Thereafter, APAC Holdings Ltd. filed a petition for confirmation of the arbitration award before the Regional Trial Court of Makati. Herein petitioners opposed the petition and prayed for the nullification, modification and/or correction of the same,alleging that the arbitrators committed evident partiality and grave abuse of discretion as shown by the following errors:a. In creating an entirely new contract for the parties that contradicts the essence of their agreement and results in theabsurd situation where a seller incurs enormous expense to sell his property;b. In treating the provisions in the Agreement independently of one another and thereby nullifying the simple, clear andexpress stipulations therein;c. In interpreting the Agreement although it is couched in plain, simple and clear language, contrary to the well establishedprinciple that if the terms of a contract are clear, the literal meaning of its stipulations shall control;d. In accepting SGV's proposed adjustments, contrary to the parties' stipulation that the final adjustment items shall

pertain to a specific period and subject to their agreement; and in giving full reliance on SGV report despiteSGV's disclosure of its lack of independence because it acted solely to assist petitioner and its report was intended solelyfor petitioner's information;e. In not applying the "suppressed evidence" rule against petitioner inspite of its refusal to present the Company's incomestatement or any other similar report for the adjustment period; and in disregarding respondent's estimate of the netincome for the period as "Adjustment" using SGV's figures and ratios;f. In not awarding damages and attorney's fee to respondents despite petitioner's bad faith in violating the contract. 1

The Regional Trial Court rendered a decision vacating the arbitration award. The dispositive portion of the decision readsas follows:WHEREFORE, the Decision/Arbitration Award in question is hereby VACATED, and APAC (herein petitioner) is herebyordered to pay ADAMSON (herein respondents) the final NAV of Forty-seven Million One Hundred Twenty-One ThousandFour Hundred Sixty-Eight Pesos (P47,121,468.00), Philippine Currency, in accordance with the pertinent stipulationsexpressed in the Agreement as discussed above, plus twelve (12) percent interest on the above amount

which ADAMSON should have earned had the balance of the final NAV been paid to the Escrow Agent after offset on August 2, 1990. ADAMSON's claim for moral and exemplary damages and attorney's fees are (sic) dismissed for lack of sufficient merit.SO ORDERED. 2

On appeal, the above decision was reversed and a petition for review was filed in this Court. Petitioners allege that theCourt of Appeals erred and acted in excess of jurisdiction or with grave abuse of discretion in holding that: (a) the trial

judge reversed the arbitration award solely on the basis of the pleadings submitted by the parties; (b) petitioners failed tosubstantiate with proofs their imputation of partiality to the members of the arbitration committee; (c) the nullification by thetrial court of the award was not based on any of the grounds provided by law; (d) to allow the trial judge to substitute hisown findings in lieu of the arbitrators' would defeat the object of arbitration which is to avoid litigation; and (e) if there reallywas a ground for vacating the award, it was improper for trial judge to reverse the decision because it contravenedSection 25 of R.A. No. 876.Did the Court of Appeals err in affirming the arbitration award and in reversing the decision of the trial court?The Court of Appeals, in reversing the trial court's decision held that the nullification of the decision of the ArbitrationCommittee was not based on the grounds provided by the Arbitration Law and that ". . . private respondents [petitionersherein] have failed to substantiate with any evidence their claim of partiality. Significantly, even as respondent judge ruledagainst the arbitrators' award, he could not find fault with their impartiality and integrity. Evidently, the nullification of theaward rendered at the case at bar was made not on the basis of any of the grounds provided by law." 3

Assailing the above conclusion, petitioners argue that ". . . evident partiality is a state of mind that need not be proved bydirect evidence but may be inferred from the circumstances of the case (citations omitted). It is related to intention whichis a mental process, an internal state of mind that must be judged by the person's conduct and acts which are the bestindex of his intention (citations omitted)." 4 They pointed out that from the following circumstances may be inferred thearbitrators' evident partiality:1. the material difference between the results of the arbitrators' computation of the NAV and that of petitioners;2. the alleged piecemeal interpretation by the arbitrators of the Agreement which went beyond the clear provisions of thecontract and negated the obvious intention of the parties;3. reliance by the arbitrators on the financial statements and reports submitted by SGV which, according to petitioners,

acted solely for the interests of private respondents; and4. the finding of the trial court that "the arbitration committee has advanced no valid justification to warrant a departurefrom the well-settled rule in contract interpretation that if the terms of the contract are clear and leave no doubt upon theintention of the contracting parties the literal meaning of its interpretation shall control." 5

We find no reason to depart from the Court of Appeal's conclusion.Section 24 of the Arbitration Law provides as follows:Sec. 24. Grounds for vacating award . — In any one of the following cases, the court must make an order vacating theaward upon the petition of any party to the controversy when such party proves affirmatively that in thearbitration proceedings:(a) The award was procured by corruption, fraud or other undue means; or (b) That there was evident partiality or corruption in the arbitrators or any of them; or

7/15/2019 Legal Acctng Cases

http://slidepdf.com/reader/full/legal-acctng-cases 10/108

(c) That the arbitrators were guilty of misconduct in refusing to postpone the hearing upon sufficient cause shown, or in refusing to hear evidence pertinent and material to the controversy; that one or more of the arbitrators was disqualifiedto act as such under section nine hereof, and willfully refrained from disclosing such disqualifications or any other misbehavior by which the rights of any party have been materially prejudiced; or (d) That the arbitrators exceeded their powers, or so imperfectly executed them, that a mutual, final and definite awardupon the subject matter submitted to them was not made. . . .Petitioners herein failed to prove their allegation of partiality on the part of the arbitrators. Proofs other than mereinferences are needed to establish evident partiality. That they were disadvantaged by the decision of the ArbitrationCommittee does not prove evident partiality.Too much reliance has been accorded by petitioners on the decision of the trial court. However, we find that the same isbut an adaptation of the arguments of petitioners to defeat the petition for confirmation of the arbitral award in the trialcourt by herein private respondent. The trial court itself stated as follows:In resolving the issues in favor of respondents, the Court has no alternative but to agree with the contention of said party,as supported by their exhaustive and very convincing arguments contained in more than twenty-one (21) pages, doubled-spaced, which are adopted and reproduced herein by reference. Said arguments may be CAPSULIZED as follows:The penultimate paragraph of its decision reads, thus:To allay any fear of petitioner that its reply and opposition, dated 11 June 1991, has not been taken into account inresolving this case, it will be well to state that the court has carefully read the same and, what is more, it has also readrespondents' comment, dated 19 June 1991, wherein they made convincing arguments which are likewise adopted andincorporated herein by reference. 6

The justifications advanced by the trial court for vacating the arbitration award are the following: (a) ". . . that the arbitrationcommittee had advanced no valid justification to warrant a departure from the well-settled rule in contract interpretationthat if the terms of the contract are clear and leave no doubt upon the intention of the contracting parties the literal

meaning of its interpretation shall control; (b) that the final NAV of P47,121,468.00 as computed by herein petitioners waswell within APAC's normal investment level which was at least US$1 million and to say that the NAV was merelyP167,118.00 would negate Clause 6 of the Agreement which provided that the purchaser would deposit in escrowP5,146,000.00 to be held for two (2) years and to be used to satisfy any actual or contingent liability of the vendor under the Agreement; (c) that the provision for an escrow account negated any idea of the NAV being less than P5,146,000.00;and (d) that herein private respondent, being the drafter of the Agreement could not avoid performance of its obligationsby raising ambiguity of the contract, or its failure to express the intention of the parties, or the difficulty of performing thesame.It is clear therefore, that the award was vacated not because of evident partiality of the arbitrators but because the latter interpreted the contract in a way which was not favorable to herein petitioners and because it considered that hereinprivate respondents, by submitting the controversy to arbitration, was seeking to renege on its obligations under thecontract.That the award was unfavorable to petitioners herein did not prove evident partiality. That the arbitrators resorted to

contract interpretation neither constituted a ground for vacating the award because under the circumstances, the samewas necessary to settle the controversy between the parties regarding the amount of the NAV. In any case, this Courtfinds that the interpretation made by the arbitrators did not create a new contract, as alleged by herein petitioners but wasa faithful application of the provisions of the Agreement. Neither was the award arbitrary for it was based on thestatements prepared by the SGV which was chosen by both parties to be the "auditors."The trial court held that herein private respondent could not shirk from performing its obligations on account of thedifficulty of complying with the terms of the contract. It said further that the contract may be harsh but private respondentcould not excuse itself from performing its obligations on account of the ambiguity of the contract because as its drafter,private respondent was well aware of the implications of the Agreement. We note herein that during the arbitrationproceedings, the parties agreed that the contract as prepared by private respondent, was submitted to petitioners for approval. Petitioners, therefore, are presumed to have studied the provisions of the Agreement and agreed to its importwhen they approved and signed the same. When it was submitted to arbitration to settle the issue regarding thecomputation of the NAV, petitioners agreed to be bound by the judgment of the arbitration committee, except in caseswhere the grounds for vacating the award existed. Petitioners cannot now refuse to perform its obligation after realizingthat it had erred in its understanding of the Agreement.Petitioners also assailed the arbitrator's reliance upon the financial statements submitted by SGV as they allegedly servedthe interests of private respondents and did not reflect the true intention of the parties. We agree with the observationmade by the arbitrators that SGV, being a reputable firm, it should be presumed to have prepared the statements inaccordance with sound accounting principles. Petitioners have presented no proof to establish that SGV's computationwas erroneous and biased.Petitioners likewise pointed out that the computation of the arbitrators leads to the absurd result of petitioners incurringgreat expense just to sell its properties. In arguing that the NAV could not be less than P5,146,000, petitioners quoteClause (B) of the Agreement as follows:CLAUSE 3(B)The consideration for the purchase of the Sale Shares by the Purchaser shall be equivalent to the Net Asset Value of theCompany, . . . which the parties HAVE FIXED at P5,146,000.00 prior to Adjustments . . .However, such quotation is incomplete and, therefore, misleading. The full text of the above provision as quoted by the

arbitration committee reads as follows:(B) The consideration for the purchase of the Sale Shares by the purchaser shall be equivalent to the Net Asset Value of the Company, without the Property, which the parties have fixed at P5,146,000 prior to Adjustments plus P24,384,600.The consideration for the sale of the Sale Shares by the Vendor, is the acquisition of the property by the Vendor, through

Aloha, from the Company at historical cost plus all Taxes due on said transfer of Property, and the release of allcollaterals of the Vendor securing the RSBS Credit Facility. However, in the implementation of this Agreement, the partiesshall designate the amounts specified in Clause 5 as the purchaser prices in the pro-forma deeds of sale andother documents required to effect the transfers contemplated in this Agreement.Thus, petitioner cannot claim that the consideration for private respondent's acquisition of the outstanding common sharesof stock was grossly inadequate. If the NAV as computed was small, the result was not due to error in the computationsmade by the arbitrators but due to the extent of the liabilities being borne by petitioners. During the arbitrationproceedings, the committee found that petitioner has been suffering losses since 1983, a fact which was not denied by

7/15/2019 Legal Acctng Cases

http://slidepdf.com/reader/full/legal-acctng-cases 11/108

petitioner. We cannot sustain the argument of petitioners that the amount of P5,146,000.00 was an initial NAV as of February 28, 1990 to which should still be added the value of tangible assets (excluding the land) and of intangible assets.If indeed the P5,146,000.00 was the initial NAV as of February 28, 1990, then as of said date, the total assets andliabilities of the company have already been set off against each other. NET ASSET VALUE is arrived at only after deducting TOTAL LIABILITIES from TOTAL ASSETS. "TOTAL ASSETS" includes those that are tangible and intangible.If the amount of the tangible and intangible assets would still be added to the "initial NAV," this would constitute doublecounting. Unless the company acquired new assets from February 28, 1990 up to June 19, 1990, no value correspondingto tangible and intangible assets may be added to the NAV.We also note that the computation by petitioners of the NAV did not reflect the liabilities of the company. The term "netasset value" indicates the amount of assets exceeding the liabilities as differentiated from total assets which include theliabilities. If petitioners were not satisfied, they could have presented their own financial statements to rebut SGV's reportbut this, they did not do.Lastly, in assailing the decision of the Court of Appeals, petitioners would have this Court believe that the respondentcourt held that the decision of the arbitrators was not subject to review by the courts. This was not the position taken bythe respondent court.The Court of Appeals, in its decision stated, thus:It is settled that arbitration awards are subject to judicial review. In the recent case of Chung Fu Industries (Philippines),Inc., et. al. v. Court of Appeals, Hon Francisco X. Velez, et. al ., G. R. No. 96283, February 25, 1992, the Supreme Courtcategorically ruled that:It is stated expressly under Art. 2044 of the Civil Code that the finality of the arbitrators' award is not absolute andwithout exceptions. Where the conditions described in Articles 2038, 2039 and 2040 applicable to both compromises andarbitrations are obtaining, the arbitrators' award may be annulled or rescinded. Additionally, under Sections 24 and 25 of the Arbitration Law, there are grounds for vacating, modifying or rescinding anarbitrators' award. Thus, if and when the

factual circumstances referred to in the above-cited provisions are present, judicial review of the award is properlywarranted.Clearly, though recourse to the courts may be availed of by parties aggrieved by decisions or awards rendered byarbitrator/s, the extent of such is neither absolute nor all encompassing. . . . 7

It is clear then that the Court of Appeals reversed the trial court not because the latter reviewed the arbitration awardinvolved herein, but because the respondent appellate court found that the trial court had no legal basis for vacating theaward.WHEREFORE, in view of the foregoing, this petition is hereby DISMISSED and the decision of the Court of Appeals

AFFIRMED.SO ORDERED.Feliciano, Bidin, Melo and Vitug, JJ., concur.

PRESIDENTIAL ANTI-GRAFT COMMISSION (PAGC) and THE OFFICE OF THE PRESIDENT vs. SALVADOR A.

PLEYTO, G.R. No. 176058, March 23, 2011

D E C I S I O NABAD, J.:This case is about the dismissal of a department undersecretary for failure to declare in his Sworn Statement of Assets,Liabilities, and Net Worth (SALN) his wife’s business interests and financial connections.The Facts and the CaseOn December 19, 2002 the Presidential Anti-Graft Commission (PAGC) received an anonymous letter-complaint 1fromalleged employees of the Department of Public Works and Highways (DPWH). The letter accused DPWH UndersecretarySalvador A. Pleyto of extortion, illicit affairs, and manipulation of DPWH projects.In the course of the PAGC’s investigation, Pleyto submitted his 1999, 2 2000,3 and 20014 SALNs. PAGC examined theseand observed that, while Pleyto said therein that his wife was a businesswoman, he did not disclose her businessinterests and financial connections. Thus, on April 29, 2003 PAGC charged Pleyto before the Office of the President (OP)

for violation of Section 8 of Republic Act (R.A.) 6713,5

also known as the Code of Conduct and Ethical Standards for Public Officials and Employees" and Section 7 of R.A. 30196 or "The Anti-Graft and Corrupt Practices Act."7

Pleyto claimed that he and his wife had no business interests of any kind and for this reason, he wrote "NONE" under thecolumn "Business Interests and Financial Connections" on his 1999 SALN and left the column blank in his 2000 and 2001SALNs.8 Further, he attributed the mistake to the fact that his SALNs were merely prepared by his wife’s bookkeeper.9

On July 10, 2003 PAGC found Pleyto guilty as charged and recommended to the OP his dismissal with forfeiture of allgovernment financial benefits and disqualification to re-enter government service.10

On January 29, 2004 the OP approved the recommendation.11 From this, Pleyto filed an Urgent Motion for Reconsideration12 claiming that: 1) he should first be allowed to avail of the review and compliance procedure in Section10 of R.A. 671313 before he is administratively charged; 2) he indicated "NONE" in the column for financial and businessinterests because he and his wife had no business interests related to DPWH; and 3) his failure to indicate his wife’sbusiness interests is not punishable under R.A. 3019.On March 2, 2004 PAGC filed its comment,14 contending that Pleyto’s reliance on the Review and Complicance Procedurewas unavailing because the mechanism had not yet been established and, in any case, his SALN was a sworn statement,the contents of which were beyond the corrective guidance of the DPWH Secretary. Furthermore, his failure to declare hiswife's business interests and financial connections was highly irregular and was a form of dishonesty.On March 11, 2005 Executive Secretary Eduardo R. Ermita ordered PAGC to conduct a reinvestigation of Pleyto’scase.15 In compliance, PAGC queried the Department of Trade and Industry of Region III–Bulacan regarding thebusinesses registered in the name of Miguela Pleyto, his wife. PAGC found that she operated the following businesses: 1)R.S. Pawnshop, registered since May 19, 1993; 2) M. Pleyto Piggery and Poultry Farm, registered since December 29,1998; 3) R.S. Pawnshop–Pulong Buhangin Branch, registered since July 24, 2000; and 4) RSP Laundry and DryCleaning, registered since July 24, 2001.16

The PAGC also inquired with the DPWH regarding their Review and Compliance procedure. The DPWH said that, theymerely reminded their officials of the need for them to comply with R.A. 6713 by filing their SALNs on time and that they

7/15/2019 Legal Acctng Cases

http://slidepdf.com/reader/full/legal-acctng-cases 12/108

had no mechanism for reviewing or validating the entries in the SALNs of their more than 19,000 permanent, casual andcontractual employees.17

On February 21, 2006 the PAGC maintained its finding and recommendation respecting Pleyto.18 On August 29, 2006 theOP denied Pleyto’s Motion for Reconsideration.19 Pleyto raised the matter to the Court of Appeals (CA), 20 which onDecember 29, 2006 granted Pleyto’s petition and permanently enjoined the PAGC and the OP from implementing their decisions.21 This prompted the latter offices to come to this Court on a petition for review.22

Issues PresentedThis case presents the following issues:1. Whether or not the CA erred in not finding Pleyto’s failure to indicate his spouse’s business interests in his SALNs aviolation of Section 8 of R.A. 6713.2. Whether or not the CA erred in finding that under the Review and Compliance Procedure, Pleyto should have first beenallowed to correct the error in his SALNs before being charged for violation of R.A. 6713.The Court’s RulingsThis is the second time Pleyto’s SALNs are before this Court. The first time was in G.R. 169982, Pleyto v. PhilippineNational Police Criminal Investigation and Detection Group (PNP-CIDG).23 In that case, the PNP-CIDG filed on July 28,2003 administrative charges against Pleyto with the Office of the Ombudsman for violating, among others, Section 8 of R.A. 6713 in that he failed to disclose in his 2001 and 2002 SALNs his wife’s business interests and financial connections.On June 28, 2004 the Office of the Ombudsman ordered Pleyto dismissed from the service. He appealed the order to theCA but the latter dismissed his petition and the motion for reconsideration that he subsequently filed. Pleyto then assailedthe CA’s ruling before this Court raising, among others, the following issues: 1) whether or not Pleyto violated Section 8(a)of R.A. 6713; and 2) whether or not Pleyto’s reliance on the Review and Compliance Procedure in the law wasunwarranted.

After threshing out the other issues, this Court found that Pleyto’s failure to disclose his wife’s business interests and

financial connections constituted simple negligence, not gross misconduct or dishonesty. Thus:Neither can petitioner’s failure to answer the question, "Do you have any business interest and other financialconnections including those of your spouse and unmarried children living in your household?" be tantamount togross misconduct or dishonesty. On the front page of petitioner’s 2002 SALN, it is already clearly stated that hiswife is a businesswoman, and it can be logically deduced that she had business interests. Such a statement of his wife’s occupation would be inconsistent with the intention to conceal his and his wife’s business interests.That petitioner and/or his wife had business interests is thus readily apparent on the face of the SALN; it is justthat the missing particulars may be subject of an inquiry or investigation.An act done in good faith, which constitutes only an error of judgment and for no ulterior motives and/or purposes, does not qualify as gross misconduct, and is merely simple negligence. Thus, at most, petitioner isguilty of negligence for having failed to ascertain that his SALN was accomplished properly, accurately, and inmore detail.Negligence is the omission of the diligence which is required by the nature of the obligation and corresponds

with the circumstances of the persons, of the time and of the place. In the case of public officials, there isnegligence when there is a breach of duty or failure to perform the obligation, and there is gross negligencewhen a breach of duty is flagrant and palpable. Both Section 7 of the Anti-Graft and Corrupt Practices Act andSection 8 of the Code of Conduct and Ethical Standards for Public Officials and Employees require theaccomplishment and submission of a true, detailed and sworn statement of assets and liabilities. Petitioner wasnegligent for failing to comply with his duty to provide a detailed list of his assets and business interests in hisSALN. He was also negligent in relying on the family bookkeeper/accountant to fill out his SALN and in signingthe same without checking or verifying the entries therein. Petitioner’s negligence, though, is only simple and notgross, in the absence of bad faith or the intent to mislead or deceive on his part, and in consideration of the factthat his SALNs actually disclose the full extent of his assets and the fact that he and his wife had other businessinterests.Gross misconduct and dishonesty are serious charges which warrant the removal or dismissal from service of the erring public officer or employee, together with the accessory penalties, such as cancellation of eligibility,forfeiture of retirement benefits, and perpetual disqualification from reemployment in government service. Hence,a finding that a public officer or employee is administratively liable for such charges must be supported bysubstantial evidence.24

The above concerns Pleyto’s 2001 and 2002 SALN; the present case, on the other hand, is about his 1999, 2000 and2001 SALNs but his omissions are identical. While he said that his wife was a businesswoman, he also did not discloseher business interests and financial connections in his 1999, 2000 and 2001 SALNs. Since the facts and the issues in thetwo cases are identical, the judgment in G.R. 169982, the first case, is conclusive upon this case.There is "conclusiveness of judgment" when any right, fact, or matter in issue, directly adjudicated on the merits in aprevious action by a competent court or necessarily involved in its determination, is conclusively settled by the judgmentin such court and cannot again be litigated between the parties and their privies whether or not the claim, demand,purpose, or subject matter of the two actions is the same.25

Thus, as in G.R. 169982, Pleyto’s failure to declare his wife’s business interest and financial connections does notconstitute dishonesty and grave misconduct but only simple negligence, warranting a penalty of forfeiture of the equivalentof six months of his salary from his retirement benefits.26

With regard to the issue concerning compliance with the Review and Compliance Procedure provided in R.A. 6713, thisCourt already held in G.R. 169982 that such procedure cannot limit the authority of the Ombudsman to conductadministrative investigations. R.A. 6770, otherwise known as "The Ombudsman Act of 1989," intended to vest in theOffice of the Ombudsman full administrative disciplinary authority.27 Here, however, it was the PAGC and the OP,respectively, that conducted the investigation and meted out the penalty of dismissal against Pleyto. Consequently, theruling in G.R. 169982 in this respect cannot apply.

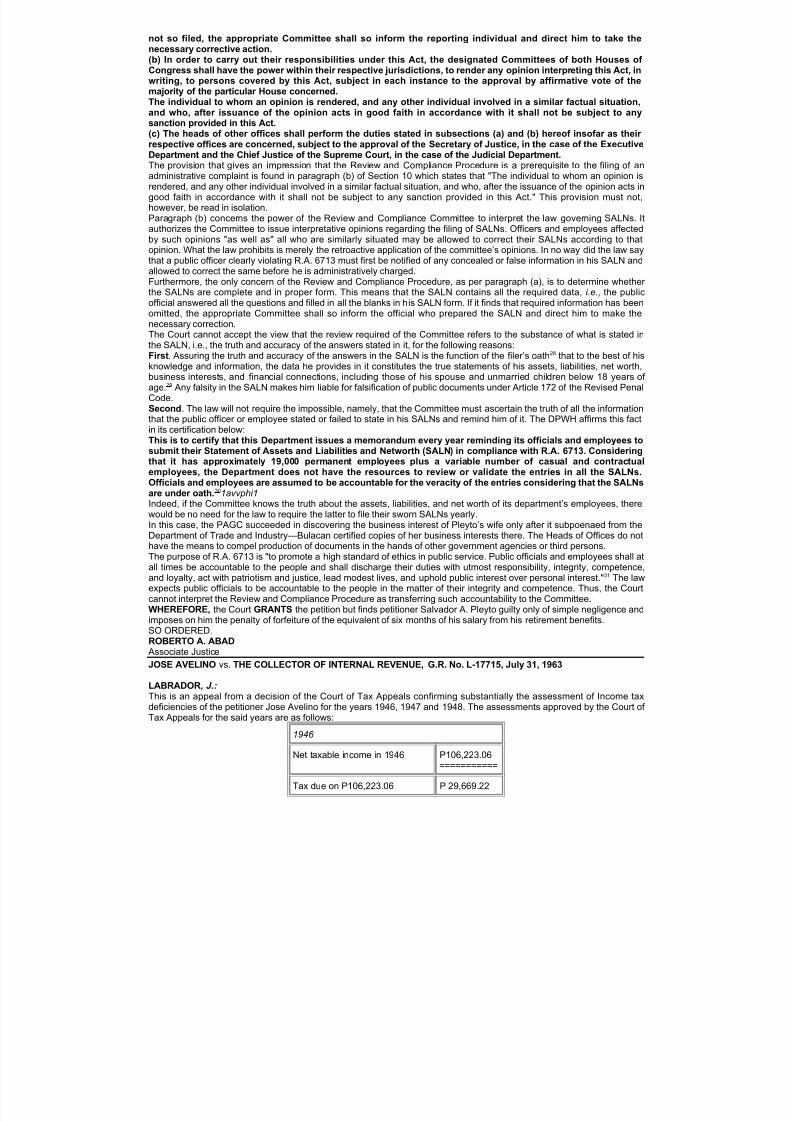

Actually, nowhere in R.A. 6713 does it say that the Review and Compliance Procedure is a prerequisite to the filing of administrative charges for false declarations or concealments in one’s SALN. Thus:Section 10. Review and Compliance Procedure. - (a) The designated Committees of both Houses of the Congressshall establish procedures for the review of statements to determine whether said statements which have beensubmitted on time, are complete, and are in proper form. In the event a determination is made that a statement is

7/15/2019 Legal Acctng Cases

http://slidepdf.com/reader/full/legal-acctng-cases 13/108

not so filed, the appropriate Committee shall so inform the reporting individual and direct him to take thenecessary corrective action.(b) In order to carry out their responsibilities under this Act, the designated Committees of both Houses of Congress shall have the power within their respective jurisdictions, to render any opinion interpreting this Act, inwriting, to persons covered by this Act, subject in each instance to the approval by affirmative vote of themajority of the particular House concerned.The individual to whom an opinion is rendered, and any other individual involved in a similar factual situation,and who, after issuance of the opinion acts in good faith in accordance with it shall not be subject to anysanction provided in this Act.(c) The heads of other offices shall perform the duties stated in subsections (a) and (b) hereof insofar as their respective offices are concerned, subject to the approval of the Secretary of Justice, in the case of the ExecutiveDepartment and the Chief Justice of the Supreme Court, in the case of the Judicial Department.The provision that gives an impression that the Review and Compliance Procedure is a prerequisite to the filing of anadministrative complaint is found in paragraph (b) of Section 10 which states that "The individual to whom an opinion isrendered, and any other individual involved in a similar factual situation, and who, after the issuance of the opinion acts ingood faith in accordance with it shall not be subject to any sanction provided in this Act." This provision must not,however, be read in isolation.Paragraph (b) concerns the power of the Review and Compliance Committee to interpret the law governing SALNs. Itauthorizes the Committee to issue interpretative opinions regarding the filing of SALNs. Officers and employees affectedby such opinions "as well as" all who are similarly situated may be allowed to correct their SALNs according to thatopinion. What the law prohibits is merely the retroactive application of the committee’s opinions. In no way did the law saythat a public officer clearly violating R.A. 6713 must first be notified of any concealed or false information in his SALN andallowed to correct the same before he is administratively charged.

Furthermore, the only concern of the Review and Compliance Procedure, as per paragraph (a), is to determine whether the SALNs are complete and in proper form. This means that the SALN contains all the required data, i.e., the publicofficial answered all the questions and filled in all the blanks in his SALN form. If it finds that required information has beenomitted, the appropriate Committee shall so inform the official who prepared the SALN and direct him to make thenecessary correction.The Court cannot accept the view that the review required of the Committee refers to the substance of what is stated inthe SALN, i.e., the truth and accuracy of the answers stated in it, for the following reasons:First. Assuring the truth and accuracy of the answers in the SALN is the function of the filer’s oath28 that to the best of hisknowledge and information, the data he provides in it constitutes the true statements of his assets, liabilities, net worth,business interests, and financial connections, including those of his spouse and unmarried children below 18 years of age.29 Any falsity in the SALN makes him liable for falsification of public documents under Article 172 of the Revised PenalCode.Second. The law will not require the impossible, namely, that the Committee must ascertain the truth of all the information

that the public officer or employee stated or failed to state in his SALNs and remind him of it. The DPWH affirms this factin its certification below:This is to certify that this Department issues a memorandum every year reminding its officials and employees tosubmit their Statement of Assets and Liabilities and Networth (SALN) in compliance with R.A. 6713. Consideringthat it has approximately 19,000 permanent employees plus a variable number of casual and contractualemployees, the Department does not have the resources to review or validate the entries in all the SALNs.Officials and employees are assumed to be accountable for the veracity of the entries considering that the SALNsare under oath.301avvphi1Indeed, if the Committee knows the truth about the assets, liabilities, and net worth of its department’s employees, therewould be no need for the law to require the latter to file their sworn SALNs yearly.In this case, the PAGC succeeded in discovering the business interest of Pleyto’s wife only after it subpoenaed from theDepartment of Trade and Industry—Bulacan certified copies of her business interests there. The Heads of Offices do nothave the means to compel production of documents in the hands of other government agencies or third persons.The purpose of R.A. 6713 is "to promote a high standard of ethics in public service. Public officials and employees shall atall times be accountable to the people and shall discharge their duties with utmost responsibility, integrity, competence,and loyalty, act with patriotism and justice, lead modest lives, and uphold public interest over personal interest."31 The lawexpects public officials to be accountable to the people in the matter of their integrity and competence. Thus, the Courtcannot interpret the Review and Compliance Procedure as transferring such accountability to the Committee.WHEREFORE, the Court GRANTS the petition but finds petitioner Salvador A. Pleyto guilty only of simple negligence andimposes on him the penalty of forfeiture of the equivalent of six months of his salary from his retirement benefits.SO ORDERED.ROBERTO A. ABAD

Associate Justice

JOSE AVELINO vs. THE COLLECTOR OF INTERNAL REVENUE, G.R. No. L-17715, July 31, 1963

LABRADOR, J.:This is an appeal from a decision of the Court of Tax Appeals confirming substantially the assessment of Income taxdeficiencies of the petitioner Jose Avelino for the years 1946, 1947 and 1948. The assessments approved by the Court of Tax Appeals for the said years are as follows:

1946

Net taxable income in 1946 P106,223.06===========

Tax due on P106,223.06 P 29,669.22

7/15/2019 Legal Acctng Cases

http://slidepdf.com/reader/full/legal-acctng-cases 14/108

Less tax previously assessed &paid

1,472.08

Deficiency tax P 28,197.14

50% surcharge 14,098.57

Total deficiency tax & surchargeP 42,295.71===========

1947

Net taxable income in 1947 P 43,504.34===========

Tax due on P43,504.34 P 8,361.22

Less tax previously assessed &paid

4,375.72.

Deficiency tax P 3,985.50

50% surcharge 1,992.75

Total deficiency tax & surchargeP 5,978.25===========

1948

Net taxable income in 1948 P 38,885.81===========

Tax due on P38,885.81 P 7,090.31

Less tax previously assessed &paid

747.51

Deficiency tax P 6,342.80

50% surcharge 3,171.40

Total deficiency tax & surchargeP 9,514.20===========

SUMMARY

Deficiency tax & surcharge for 1946

P 42,295.71

Deficiency tax & surcharge for

1947 5,978.25

Deficiency tax & surcharge for 1948

9,414.20

GRAND TOTALP 57,788.16===========

In the brief of the petitioner various assignments of errors are made, each error raising specific questions of law and of fact. The errors will now be considered one by one, each independently of the others.ITHE COURT OF TAX APPEALS ERRED IN NOT HOLDING THAT THE NET WORTH METHOD USED BYRESPONDENT IN DETERMINING PETITIONER'S TAXABLE INCOME IS WITHOUT JUSTIFIABLE BASISIt is contended under this assignment of error that there is no reasonable certainty of the amount taken as an opening networth, there being no sufficient basis for establishing such opening net worth. Included in the opening net worth as of January 1, 1946, both according to the petitioner as well as to the Commissioner of Internal Revenue, are P700.00 andP5,500.00, representing cash in bank, PNB savings account and PNB current account, respectively. But petitioner claimsthat the cash on hand in the opening net worth should be, on December 31, 1945 (or January 1, 1946), not P100.00 asestimated by respondent but P47,300.00, for the reason that in an income tax return submitted by the wife of thepetitioner, Mrs. Enriqueta Avelino, she made it appear that the netted a profit of P55,000.00 from her business of importation of shoes, operation of a bar, and of a restaurant, shortly after liberation. The income tax return submitted byher for the year 1946 was submitted in the year 1949 and was presented at the hearing as Exhibit "A". Petitioner assertsthat his wife made a gain of P55,000.00 during the year 1946, but the supposed copy of the income tax return that shehas submitted as evidence does not show how that amount had been earned. If she did actually earn that amount Exhibit"A" would have contained the details indicating the transactions in which the big sum was earned. Why none of that

7/15/2019 Legal Acctng Cases

http://slidepdf.com/reader/full/legal-acctng-cases 15/108

amount or the greater part thereof appears to have been deposited in a bank has not been explained. Apparently thecourt below considered the return as a self-serving statement, and We agree that on the basis of that income tax return,without any other explanation how the gains were used or invested or deposited, there is no reason to disturb the action of the court below in giving no credence to the said alleged existence of the cash net worth existing at the beginning of theyear 1946. We therefore declare that the alleged error has not been committed.IITHE COURT OF TAX APPEALS, IN COMPUTING THE DEFICIENCY INCOME TAX ALLEGEDLY DUE FROM THEPETITIONER, ERRED IN NOT DEDUCTING FROM THE INCREASE IN NET WORTH OF THE PETITIONER FOR THEYEAR 1948, THE SUM OF P6,508.00 REPRESENTING ONE-HALF (½) OF THE CAPITAL GAIN REALIZED FROM THESALE OF TWO PARCELS OF LAND (CAPITAL ASSETS) MADE IN 1948.The respondent denies that this error have been committed. In Annex 1, the yellow working sheet prepared by Examiner Lasquety, it is shown that the sum of P6,508.00 was deducted in the year 1948 is the taxable capital gain. This deductionwas sustained by the Court below. The alleged error, therefore, is disproved by Annex I.IIITHE COURT OF TAX APPEALS ERRED IN DISALLOWING THE AMOUNT OF P9,816.78 AS DEPRECIATION ONRENTAL PROPERTIES IN DETERMINING THE PETITIONER'S NET WORTH FOR THE YEAR 1948.This supposed error was not committed as evidenced by an examination of Annex I, which shows that P9,816.78 wasallowed as deduction for 1948 under the heading "Reserve for Depreciation, Building".IVTHE COURT OF TAX APPEALS ERRED IN FAILING TO REFLECT OR TAKE UP IN 1947 THE IMPROVEMENTSVALUED AT P35,000.00. ERECTED IN 1947 IN THE QUEZON CITY LOT OF PETITIONER.This error again is disproved by Annex I, the yellow working sheet prepared by Bureau of Internal Revenue Examiner Lasquety. This working sheet was adopted by the Court of Tax Appeals and it shows that P35,000.00 alleged to have

been omitted was actually taken into account in the computation of the 1947 accounts of the petitioner, as improvementson four buildings.VTHE COURT OF TAX APPEALS ERRED IN HOLDING THAT THE PETITIONER AND HIS WIFE HAD INVESTMENT INTHE TALISAY LUMBER COMPANY IN THE SUM OF P20,000.00 WITHOUT CONSIDERING AN OFFSETTINGLIABILITY IN THE SAME AMOUNT.Neither do we find any merit in this assignment of error. According to the evidence, the articles, of incorporation of theTalisay Lumber Company, which is under oath, petitioner and his wife invested the sums of P28,000.00 and P1,000.00 inthe company. If these sums were not furnished by the petitioner but by the organizer of the company, still the total amountof P29,000.00 should be considered as a gift, or an income received by the petitioner and his wife from the said organizer of the Talisay Lumber Company, which income is liable to tax.VITHE COURT OF TAX APPEALS ERRED IN HOLDING THAT THE PETITIONER HAD INVESTMENT IN AVELINO,

BAGTAS, ALZATE AND COMPANY IN THE SUM OF P5,000.00 FOR EACH OF THE YEARS 1946 TO 1950.Under this assignment of error, petitioner argues that the appearance of the said amount as having been contributed tothe partnership by petitioner is no proof that that amount was petitioner's actual investment in the company. The samereasons obtaining in the case of the investment of P29,000.00 of the spouses in the Talisay Lumber Company obtain inthe case of the petitioner's investment in the partnership of Avelino, Bagtas, Alzate and Company.VIITHE COURT OF TAX APPEALS ERRED IN HOLDING THAT THE LOAN OF P10,000.00 FROM ROSARIO GRAY DEHAYS AND ANOTHER LOAN OF P30,000.00 FROM ANGELA M. VDA. DE BUTTE NEVER EXISTED.In support of this assignment of error, petitioner contends that he owed the sum of P10,000.00 to Rosario Gray de Hays,which amount represents one-half of the price of P20,000.00 which was the consideration for the sale of certain propertydescribed in Exhibit "C". But the original of the document shows that the amount of the consideration was P22,000.00 andthe vendor was Severina de Casal, and nothing is said in the original of the document that any part of the amount under consideration has not been paid.It is also alleged in support of this error that the petitioner is indebted to Angela M. Vda. de Butte in 1948 in the sum of P30,000.00. Mrs. Butte testified that petitioner owed her the amount of P30,000.00; that the debt was in the form of acheck and that in 1949 Mr. Avelino, the petitioner, paid P15,000.00, and that he paid the balance in 1951, no interest onthe loan having been demanded and paid. Evidence of this character has, as a rule, been declared insufficient for purposes of the income tax law. (Eugenio Perez vs. Court of Tax Appeals, et al., G.R. No. L-10507, May 30, 1958; AurelioP. Reyes vs. Collector of Internal Revenue, G.R. Nos. L-11534 & L-11558, Nov. 25, 1958.) We declare that inconsonance with the rule which appears to be reasonable, the alleged loan cannot be declared as, actually existing.VIIITHE COURT OF TAX APPEALS ERRED IN HOLDING THAT THE PETITIONER COMMITTED FRAUD IN FILING HISINCOME TAX RETURNS FOR THE YEARS UNDER REVIEW.Under this alleged error it is contended that there was no evidence of fraud committed by the petitioner. We find that theacts of the petitioner in declaring an income of only P5,258.99 in the year 1946 when he had an actual income of P105,223.06; his act in submitting an income tax return for 1947 only for the amount of P12,219.96 when he actually hada net taxable income of P43,504.34; and lastly his act in reporting an income for the year 1948 which is only ten percent