Embed Size (px)

Citation preview

Investment decisions•Dividend decisions•Financing decisions•

Financial Decisions

Objective is to maximise shareholder wealth through optimal choices in the three major financial decisions•

Present value of expected future returns to owners of the firm○Represented by market price of firm's common stock (assuming that marks are in equilibrium)○

Shareholder Wealth:•

Financial Management

Amount○Timing ○Risk○

Cash Flow•

Can only compare cash flows valued at the same point in time○Need to use an appropriate opportunity cost of capital○

Money has a time value•

Determinants of Value

NPV = PV (benefits) - PV (costs)○Extension of present value concept, taking into account the cost of investment•

Optimal rule○NPV represents change in shareholder wealth○

Objective of wealth maximisation is simply to maximise NPV of firm's investment projects•

Net Present Value

Explicitly considers timing and risk of expected benefits○Can determine whether a decision is consistent with objectives○Provides an impersonal objective○

Advantages of Shareholder Wealth Maximisation Objective•

Does not consider timing of expected benefits (ie. Static evaluation)○Multiple definitions of profit permissible (uncertain which measure of profit should be maximised)○Does not consider risk associated with alternative decisions○

Limitations of Profit Maximisation Objective•

Wealth does not equal Profit

Considering the interests of all shareholders - customers, employees, suppliers, communities, as well as the shareholders

○

Ethical business practices○

Corporate Social Responsibility1)

Arise as a result of divergent objectives between different stakeholders within organisation○Agency relationship - exists when one party (principal P) engages another party (agent A) to act on their behalf

○

Agency costs are mechanisms employed to reduce agency problems and align the interests of A with the interests of P

○

Agency Problems2)

Constraints

Investment decisions are entirely at your discretion○Liability is unlimited so risky investments may have a higher actual risk○Harder to obtain funding○Major source of funding would be banks○

Sole Proprietorship•

Shared (therefore less) liability (but still unlimited)○Can choose to be a limited liability partner for less potential return/stake○However, investment decisions are a joint decision - not entirely at your discretion○Harder to obtain funding○Major source of funding would be banks○

Partnership•

Separate legal entity○Not personally responsible for company debts○Value of shares is a risk however personal assets not at risk○Represent less than 20% of businesses however they make 90% of the revenue○

Corporation•

Forms of Business Organisation

Accounting○Macroeconomics○Microeconomics ○

Primary Disciplines•

Marketing○Production○HR Management○Quantitative Methods○

Other related Disciplines•

Multi-Disciplinary Approach

○

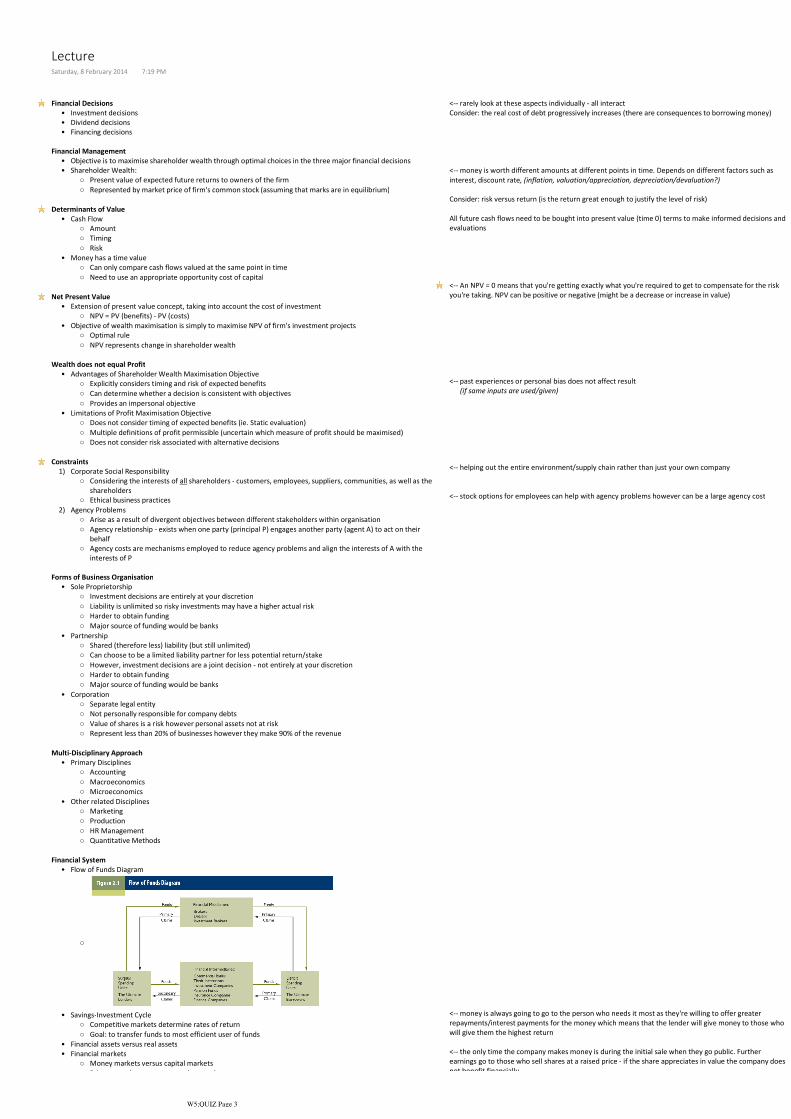

Flow of Funds Diagram•

Competitive markets determine rates of return○Goal: to transfer funds to most efficient user of funds○

Savings-Investment Cycle•

Financial assets versus real assets•

Money markets versus capital markets○Primary markets versus secondary markets○

Financial markets•

Financial System

<-- rarely look at these aspects individually - all interactConsider: the real cost of debt progressively increases (there are consequences to borrowing money)

<-- money is worth different amounts at different points in time. Depends on different factors such as interest, discount rate, (inflation, valuation/appreciation, depreciation/devaluation?)

Consider: risk versus return (is the return great enough to justify the level of risk)

All future cash flows need to be bought into present value (time 0) terms to make informed decisions and evaluations

<-- An NPV = 0 means that you're getting exactly what you're required to get to compensate for the risk you're taking. NPV can be positive or negative (might be a decrease or increase in value)

<-- past experiences or personal bias does not affect result (if same inputs are used/given)

<-- helping out the entire environment/supply chain rather than just your own company

<-- stock options for employees can help with agency problems however can be a large agency cost

<-- money is always going to go to the person who needs it most as they're willing to offer greater repayments/interest payments for the money which means that the lender will give money to those who will give them the highest return

<-- the only time the company makes money is during the initial sale when they go public. Further earnings go to those who sell shares at a raised price - if the share appreciates in value the company does not benefit financially

LectureSaturday, 8 February 2014 7:19 PM

W5;QUIZ Page 3

Chapter 1

Shareholder wealth is defined as the present value of the expected future returns to the owners of the firm. It is measured by the market value of the shareholders' common stock holdings

•

The primary normative goal of the firm is to maximise shareholder wealth•Achievement of the shareholder wealth maximisation goal is often constrained by CSR concerns and problems arising out of agency relationships

•

The market value of a firm's stock is determined by the magnitude, timing and risk of the cash flows the firm is expected to generate.

•

Managers can take a variety of actions to influence the magnitude, timing and risk of the firm's cash flows. These actions are often classified as investment, financing and dividend decisions

•

Ethical standards of performance are an increasingly important dimension of the decision-making process of managers

•

The most important forms of business organisation are sole proprietorships, partnerships (general and limited), and corporations. Corporations have the advantages of limited liability, perpetual life and the ability to raise large amounts of capital. They account for only 20% of US firms however they account for over 90% of US business revenues.

•

Financial management responsibilities are often divided between the controller and treasurer

○

The controller normally has responsibility for all activities related to accounting○The treasurer is normally concerned with acquisition, custody and expenditure of funds○

The finance function is usually headed by a vice president or chief financial officer (CFO)•

Key Concepts

Agency relationships give rise to certain agency problems and costs that can have an important impact on firm performance

•

A corporation is defined as a 'legal person' composed of one or more actual individuals or legal entities. The owners of a corporation are called stockholders (or shareholders). The stockholders elect a board of directors that usually deals with broad policy matters, whereas the day-to-day operations are supervised by the corporate officers.

•

Corporations issue debt securities to investors who lend money to the corporation•Corporations issue equity securities to investors who become owners of the corporation•

Summary

Shareholder Wealth = Number of Shares Outstanding x Market Price Per Share•Important Equation

Chapter 2

Include securities brokers and investment bankers!financial middlemen○

Include commercial banks, thrift institutions, investment companies and finance companies

!financial intermediaries○

In the US financial system, funds flow from net savers (ie households) to net investors (ie businesses) through…

•

Financial markets are classified as money or capital markets and primary or secondary markets•

Key Concepts

TextbookSaturday, 8 February 2014 7:19 PM

W5;QUIZ Page 5

Holding Period Return (ex post) - actual realised returns

P1 = end price○P0 = initial price○D1 = share dividend○

!"#$%&"' )*!(%) =*/ − *1 + 3/

*1

44444444444× 100%

!"#$%&"' )*!(%)

=

(89'%9: *;%<") − (=":%99%9: *;%<") + (3%&>;%?@>%A9& !"<"%B"')

(=":%99%9: *;%<")44444444444444444444444444444444444444444444444444444444× 100%

Expected Holding Period Return (ex ante) - estimated values

P1 = end price○P0 = initial price○D1 = share dividend○

8CD"<>"' )*!(%) =*/ − *1 + 3/

*1

44444444444× 100%

8CD"<>"' )*!(%)

=

(89'%9: *;%<") − (=":%99%9: *;%<") + (3%&>;%?@>%A9& !"<"%B"')

(=":%99%9: *;%<")44444444444444444444444444444444444444444444444444444444× 100%

Can be calculated for any period however if making comparisons, you must use the same length periods

○----------------------

FormulasSaturday, 8 February 2014 7:25 PM

W5;QUIZ Page 7

Define variables as a first step•State formula•Substitute values•

Process

Compensation for the fact that you aren't spending money now (compensation for forgoing consumption or alternative investment opportunities)

•

Difference between nominal and real interest rate is inflation!Real interest rate is ex-inflation!

(1 + nominal) = (1 + real) (1 + inflation)□In practice, interest rates are quoted on nominal basis□

Fisher's Equation!

Real IR = Nominal IR - Inflation (pi)□Nominal IR = Real IR + Inflation (pi)□

Basic Equation!

A quoted rate or undefined rate is always the nominal rate!

Nominal versus real interest rates○

Interest calculated on principal amount only□HPR decreases as your investment increases but your return interest doesn't change

□

Suggests that interest earned is just deadweight. People would take it out of an investment and put it elsewhere where it's useful… the market realises that and doesn't use simple interest

□

Simple interest!

The standard in the market□Interest calculated on current balance at time of interest calculation□Interest-on-interest□

Compound interest!

LMN = *M1(1 + %)N•

Subscripts are optional notation, so…•LM = *M(1 + %)

N•If the interest rates change half way through an investment period you can do…

•

LM = *M(1 + %1)N/

(1 + !2)$%•

Future Value - Single Sum!

&'( = * +'$(1 + !)$///////0•

Present Value - Single Sum!

Valuing alternatives need to be bought back to time 0 to work out their present value

•Valuing Alternatives!

Simple versus Compound Interest○

In practice, interest rates quoted as nominal per annum rates!Cannot use nominal rates in time value money (TVM) calculations!

Use effective annual rates instead•Cannot compare nominal rates with different compounding frequencies!

Inom = nominal p.a. rate•M = number of compounding periods per year•

Calculating Effective Interest Rates!

Nominal versus Effective Interest○

Classifications•

Interest Rates

LectureSaturday, 8 February 2014 7:19 PM

W5;QUIZ Page 10

Real vs Nominal Interest Rates (Fisher's Equation)Nominal IR = Inflation inclusiveReal IR = Ex-inflation

(1 + %NOP) = (1 + %VRWX

)(1 + Y)

%NOP = (1 + %VRWX)(1 + Y) − 1

%VRWX =

(1 + %NOP)

(1 + Y)444444444 − 1

Where:Y = %9Z$#>%A9 ;#>"

Rate of ReturnSimple InterestHPR proves that each year less interest is received as only the interest on the initial investment is paid. For example…

P1 = end price○P0 = initial price○

)*!(%) =*/ − *1

*1

4444444× 100%

Compound Interest

P1 = end price○P0 = initial price○

)*!(%) =*/ − *1

*1

4444444× 100%

FormulasSaturday, 8 February 2014 7:45 PM

W5;QUIZ Page 12