Embed Size (px)

DESCRIPTION

acc--3 & 4

Citation preview

ACCOUNTING FOR MERCHANDISING OPERATIONS

Dr. Md. Hamid U Bhuiyan

Merchandising Operations Merchandising companies buy and sell merchandise rather than

performing services as their prime source of revenue. For example: Wal-Mart, Kmart, and Target

Merchandising companies that purchase and sell directly to consumers are called RETAILERS

Merchandising companies that sell to retailers are known as WHOLESALERS

the primary source of revenues for merchandising companies is the sale of merchandise, often referred to simply as SALES REVENUE OR SALES

COST OF GOODS SOLD (COGS) is the total cost of merchandise sold during the period

Income Measurement Process for a Merchandising Company

Operating Cycle of a Merchandising Company

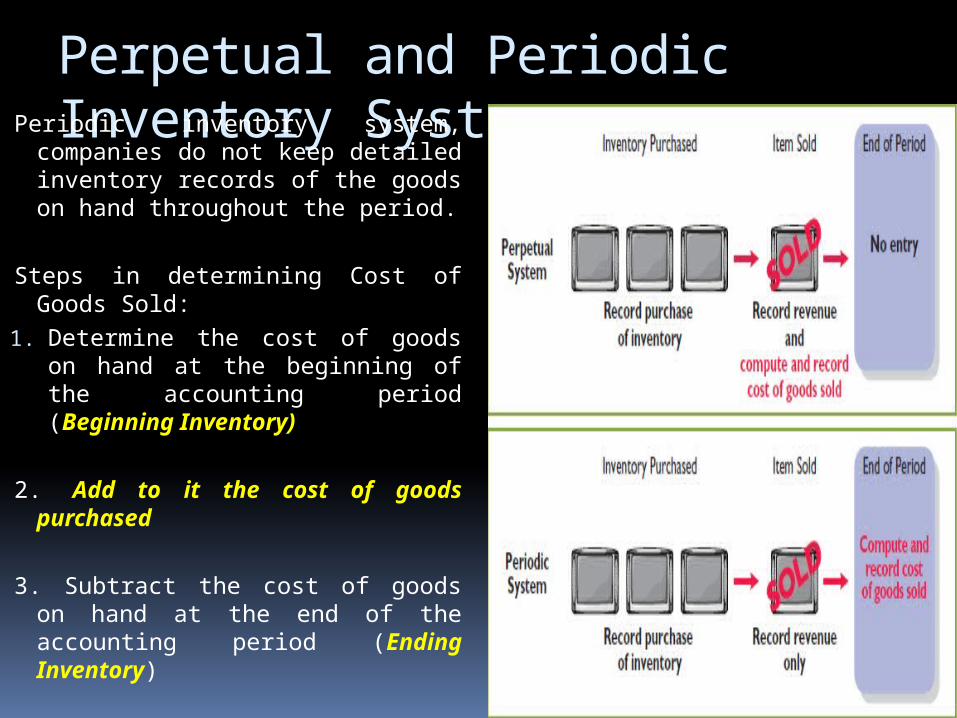

Perpetual and Periodic Inventory SystemPerpetual inventory system:

companies keep detailed records of the cost of each inventory purchase and sale

These records continuously show the inventory that should be on hand for every item

Under a perpetual inventory system, a company determines the cost of goods sold each time a sale occurs

Perpetual and Periodic Inventory SystemPeriodic inventory system, companies

do not keep detailed inventory records of the goods on hand throughout the period.

Steps in determining Cost of Goods Sold:

1. Determine the cost of goods on hand at the beginning of the accounting period (Beginning Inventory)

2. Add to it the cost of goods purchased

3. Subtract the cost of goods on hand at the end of the accounting period (Ending Inventory)

Freight Cost – Who Will Pay

The sales agreement should indicate who - the seller or the buyer is

to pay for transporting the goods to the buyer’s warehouse

Freight terms are expressed as either FOB shipping point or FOB

destination. The letters FOB mean free on board

FOB shipping point means that the seller places the goods free on

board the carrier, and the buyer pays the freight costs

FOB destination means that the seller places the goods free on

board to the buyer’s place of business, and the seller pays the

freight

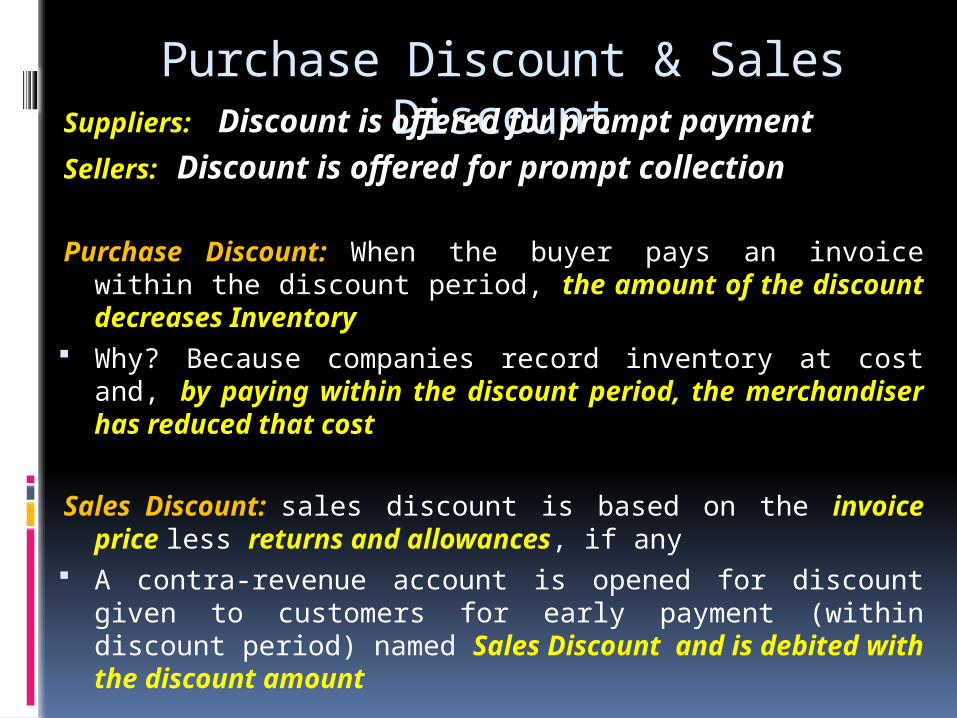

Purchase Discount & Sales DiscountSuppliers: Discount is offered for prompt payment

Sellers: Discount is offered for prompt collection

Purchase Discount: When the buyer pays an invoice within the discount period, the amount of the discount decreases Inventory

Why? Because companies record inventory at cost and, by paying within the discount period, the merchandiser has reduced that cost

Sales Discount: sales discount is based on the invoice price less returns and allowances, if any

A contra-revenue account is opened for discount given to customers for early payment (within discount period) named Sales Discount and is debited with the discount amount

Purchase Returns & Sales ReturnsPurchase Returns: A purchaser may be dissatisfied with the

merchandise received because the goods are damaged or defective, of inferior quality, or do not meet the purchaser’s specifications

In such cases, the purchaser may return the goods to the seller for credit (for credit purchase) or cash (for cash purchase)

Purchase return will be treated as a reduction in liability or cash & the returned goods will decrease the value of inventory

Sales Returns: A contra-revenue account is to be opened to record goods returned from customers named ‘Sales Returns & Allowances’ & there will a decrease in accounts receivable or cash. In addition, sales returns will also increase the inventory and decrease the cost of goods sold at the fair value of the returned goods

Perpetual Inventory System Problem

Pace Distributing Company completed the following

merchandising transactions in the month of April. At the

beginning of April, the ledger of Pace showed Cash of

$9,000 and Owner’s Capital of $9,000.

April. 2: Purchased merchandise on account from Monaghan Supply Co. $6,900, terms 1/10, n/30

April 2: Inventory $6900

Accounts Payable $6900

[To record goods purchased on account]

Perpetual Inventory System Problem

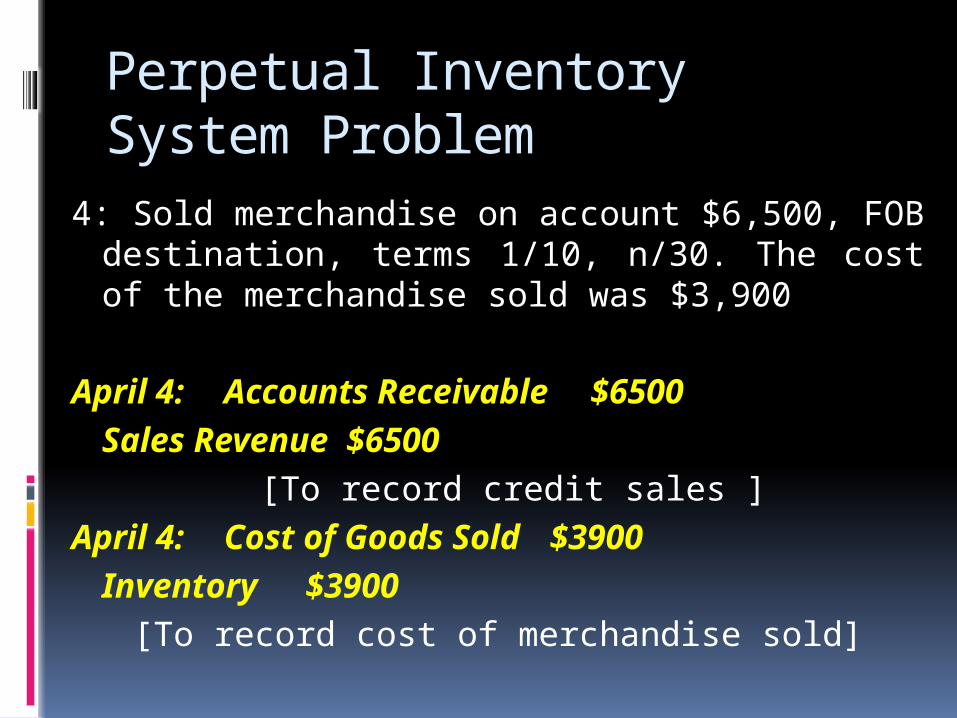

4: Sold merchandise on account $6,500, FOB destination, terms 1/10, n/30. The cost of the merchandise sold was $3,900

April 4: Accounts Receivable $6500

Sales Revenue $6500

[To record credit sales ]

April 4: Cost of Goods Sold $3900

Inventory $3900

[To record cost of merchandise sold]

Perpetual Inventory System Problem

5: Paid $240 freight on April 4 sale

April 5: Freight – Out $240Cash 240

[To record payment of freight on goods sold]

6: Received credit from Monaghan Supply Co. for merchandise returned $500

April 6: Accounts Payable $500Inventory $500

[To record return on goods purchased from Morgan Supply Co.]

Perpetual Inventory System Problem

11 Paid Monaghan Supply Co. in full, less discount

April 11: Accounts Payable $6400

Cash $6336

Inventory $64

[To record payment within discount period]

13 Received collections in full, less discounts, from customers billed on April 4.

April 13: Cash $6435

Sales Discount $65

Accounts Receivable $6500

[To record collection within 1/10, n/30 discount period]

Perpetual Inventory System Problem14 Purchased merchandise for cash $3,800

April 14: Inventory $3800

Cash $3800

[To record goods purchased for cash]

16 Received refund from supplier for returned goods on cash purchase of April 14, $500

April 16: Cash $500

Inventory $500

[To record return on goods purchased]

Perpetual Inventory System Problem

18 Purchased merchandise from Dominic Distributors $4,500, FOB shipping point, terms 2/10, n/30

April 18: Inventory $4500

Accounts Payable $4500

[To record merchandise purchase on account from Dominic Distributors]

20 Paid freight on April 18 purchase $100.

April 20: Inventory $100

Cash $100

[To record payment of freight on goods purchased]

Perpetual Inventory System Problem

23 Sold merchandise for cash $7,400. The merchandise sold had a cost of $4,120.

April 23: Accounts Receivable $7400

Sales Revenue $7400

[To record cash sales ]

April 23: Cost of Goods Sold $4120

Inventory $4120

[To record cost of merchandise sold]

Perpetual Inventory System Problem

26 Purchased merchandise for cash $2,300

April 26: Inventory $2300

Cash $2300

[To record goods purchased for cash]

27 Paid Dominic Distributors in full, less discountApril 27: Accounts Payable $4500

Cash $4410

Inventory $90

[To record payment within discount period]

Perpetual Inventory System Problem

29 Made refunds to cash customers for defective merchandise $90. The returned merchandise had a fair value of $30

April 29:

Sales Returns & Allowances 90

Cash 90

[To record refund granted to cash customers]

April 29:

Inventory $30

Cost of goods sold $30

Perpetual Inventory System Problem 30 Sold merchandise on account $3,700, terms n/30. The cost of

the merchandise sold was $2,800.

April 30: Accounts Receivable $3700

Sales Revenue $3700

[To record credit sales ]

April 30: Cost of Goods Sold $2800

Inventory $2800

[To record cost of merchandise sold]

Instructions (a) Journalize the transactions using a perpetual inventory

system.

Worksheet Worksheet: facilitates the end-of-period (monthly,

quarterly, or annually) accounting and reporting process.

Use of a worksheet helps a company prepare the financial statements on a more timely basis

A company prepares a worksheet either on columnar paper or within a computer spreadsheet. In either form, a company uses the worksheet to adjust account balances and to prepare financial statements

Worksheet

The worksheet does not replace the financial statements. Instead, it is an informal device for accumulating and sorting information needed for the financial statements

Completing the worksheet provides considerable assurance that a company properly handled all of the details related to the end-of-period accounting and statement preparation

The 10-column worksheet provides columns for the first trial balance, adjustments, adjusted trial balance, income statement, and balance sheet.

Steps in Preparing a Worksheet

Adjusting Entries

Adjustments ensure that a company follows the revenue recognition and

expense recognition principles

In order for revenues to be recorded in the period in which services are

performed and for expenses to be recognized in the period in which

they are incurred, companies make adjusting entries

Adjusting entries ensures that balance sheet reports the appropriate

assets, liabilities, and owners’ equity at the statement date.

Adjusting entries also ensure that income statement reports the proper

revenues and expenses for the period

Adjusting Entries

The trial balance—the first pulling together of the transaction data—may

not contain up-to-date and complete data.

This occurs for the following reasons:

Some events are not recorded daily because it is not efficient to do so

Examples are the use of supplies and the earning of wages by employees

Some costs are not recorded during the accounting period because these costs expire with the passage of time rather than as a result of recurring daily transactions

Examples of such costs are building and equipment depreciation and rent and insurance

Some items may be unrecorded

An example is a utility service bill that will not be received until the next accounting period

Adjusting EntriesAdjusting entries are classified as either deferrals

or accruals

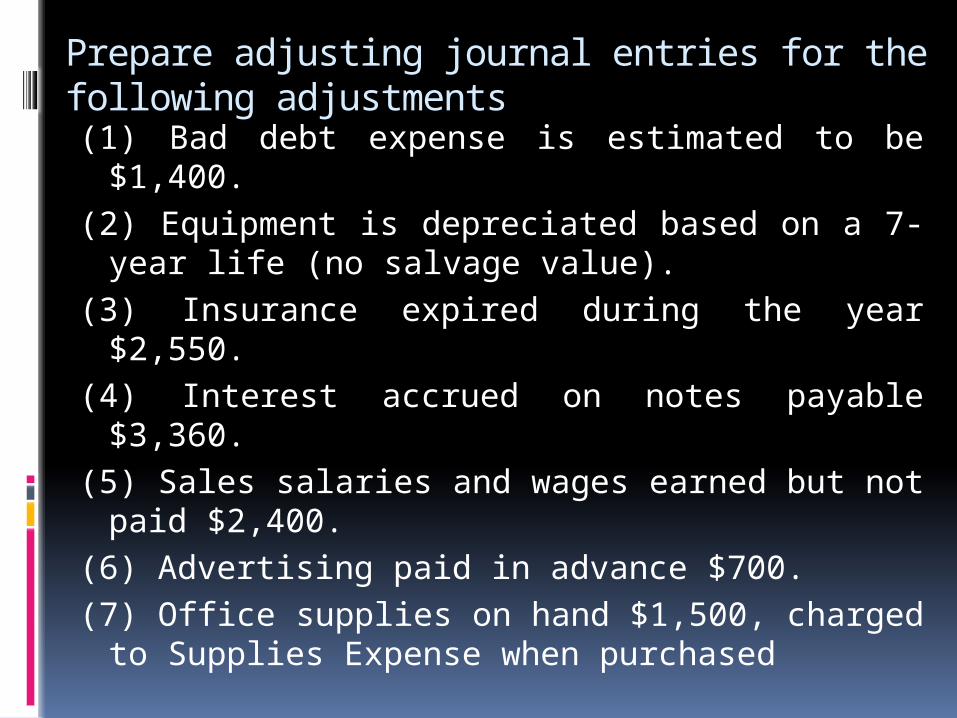

Presented below is the December 31 trial balance of New York Boutique (P3-10)

Prepare adjusting journal entries for the following adjustments

(1) Bad debt expense is estimated to be $1,400.

(2) Equipment is depreciated based on a 7-year life (no salvage value).

(3) Insurance expired during the year $2,550.

(4) Interest accrued on notes payable $3,360.

(5) Sales salaries and wages earned but not paid $2,400.

(6) Advertising paid in advance $700.

(7) Office supplies on hand $1,500, charged to Supplies Expense when purchased

General Journal - Adjusting EntriesDate Name of Accounts Ref. Debit Credit

Dec. 31 Bad Debt Expense 1 $1400

Allowance for Doubtful Accounts $1400

Dec. 31 Depreciation Expenses 2 12000

Accumulated Depreciation - Equipment 12000

Dec. 31 Insurance Expenses 3 2550

Prepaid Insurance 2550

Dec. 31 Interest Expenses 4 3360

Interest Payable 3360

Dec. 31 Salaries and Wages Expenses (Sales) 5 2400

Salaries and Wages Payable 2400

Dec. 31 Prepaid Advertising 6 700

Advertising Expenses 700

Dec. 31 Supplies 7 1500

Supplies Expense 1500

Worksheet

Dr. Cr Dr. Cr Dr. Cr Dr. Cr Dr. Cr

Cash $18,500 $18,500 $18,500

Accounts Receivable 32000 32000 32000

Allowance for Doubtful Accounts 700 1400 2100 2100

Inventory, December 31 80000 80000 80000

Prepaid Insurance 5100 2550 2550 2550

Equipment 84000 84000 84000

Accumulated Depreciation - Equipment 35000 12000 47000 47000

Notes Payable 28000 28000 28000

Common Stock 80600 80600 80600

Retained Earnings 10000 10000 10000

Sales Revenue 600000 600000 600000

Cost of Goods Sold 408000 408000 408000

Salaries and Wages Expense (Sales) 50000 2400 52400 52400

Advertising Expenses 6700 700 6000 6000

Salaries and Wages Expense (Administrative) 65000 65000 65000

Supplies Expenses 5000 1500 3500 3500

Total 754300 754300

Bad Debt Expense 1400 1400 1400

Depreciation Expense 12000 12000 12000

Insurnace Expense 2550 2550 2550

Interest Expense 3360 3360 3360

Interest Payable 3360 3360 3360

Salaries and Wages Payable 2400 2400 2400

Prepaid Advertising 700 700 700

Supplies 1500 1500 1500

Total 23910 23910 $773,460 $773,460

Net Income 45790 45790

600000 600000 $219,250 $219,250

Trial Balance Adjustments Adjusted Trial Balance Income Statement Balance SheetName of Accounts

Preparation of Financial Statement

Income Statement: The purpose of the income statement , sometimes called the statement of operations or statement of earnings , is to summarize the profit-generating activities that occurred during a particular reporting period.

Many investors and creditors perceive it as the statement most useful for predicting future profitability (future cash-generating ability).

Income Statement Income from Continuing Operations

Income from continuing operations: includes the revenues,

expenses, gains and losses that will probably continue in future

periods .

Revenues are inflows of resources resulting from providing

goods or services to customers.

Expenses are outflows of resources incurred while generating

revenue. They represent the costs of providing goods and

services. The matching principle is a key player in the way we

measure expenses.

Income Statement Income from Continuing Operations

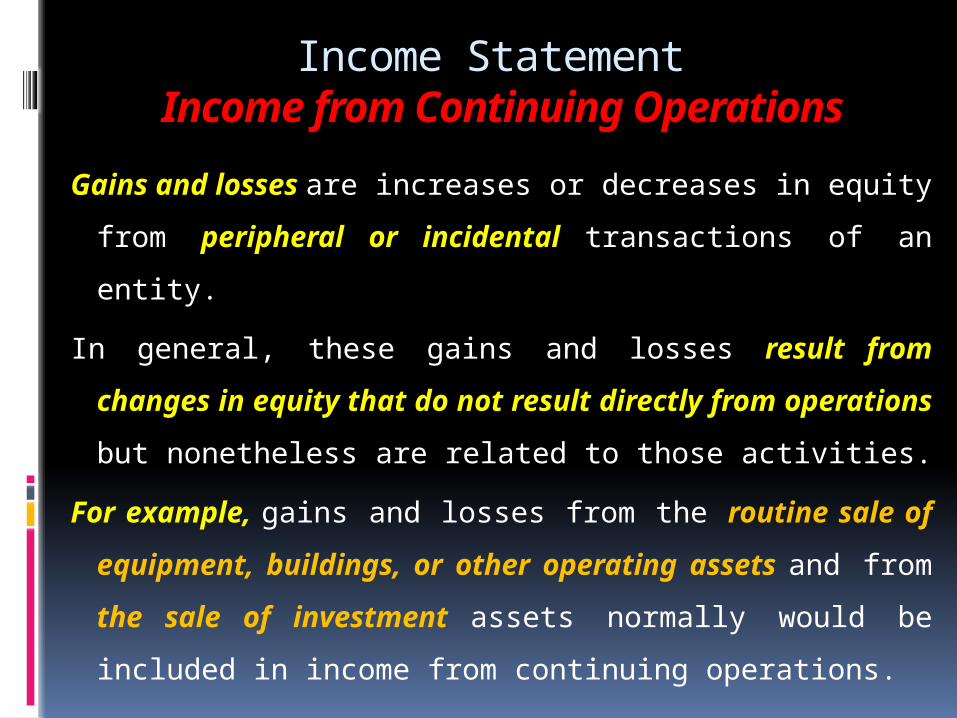

Gains and losses are increases or decreases in equity from

peripheral or incidental transactions of an entity.

In general, these gains and losses result from changes in equity

that do not result directly from operations but nonetheless are

related to those activities.

For example, gains and losses from the routine sale of

equipment, buildings, or other operating assets and from the

sale of investment assets normally would be included in

income from continuing operations.

Income Statement Operating Vs. Non-Operating Income & Expenses

Many corporate income statements distinguish between operating

income and non operating income.

Operating income includes revenues and expenses directly

related to the primary revenue-generating activities of the

company

For example, operating income for a manufacturing company

includes sales revenues from selling the products it manufactures

as well as all expenses related to this activity

Income Statement Operating Vs. Non-Operating Income & Expenses

Non-operating income relates to peripheral or

incidental activities of the company.

For example, a manufacturer would include interest

and dividend revenue, gains and losses from selling

investments, and interest expense in non-operating

income

Income Statement – Income Tax Expenses

Income taxes represent a major expense to a corporation, and

accordingly, income tax expense is given special treatment in the

income statement.

Like individuals, corporations are income-tax-paying entities.

Because of the importance and size of income tax expense

(sometimes called provision for income taxes ), it always is

reported as a separate expense in corporate income statements.

Income Statement Format – Single -Step Single-step format: lists all the revenues and gains included in

income from continuing operations. Then, expenses and losses

are grouped, subtotaled, and subtracted—in a single step—from

revenues and gains to derive income from continuing operations.

In a departure from that, though, companies usually report income

tax expense as a separate last item in the statement.

Operating and non-operating items are not separately classified.

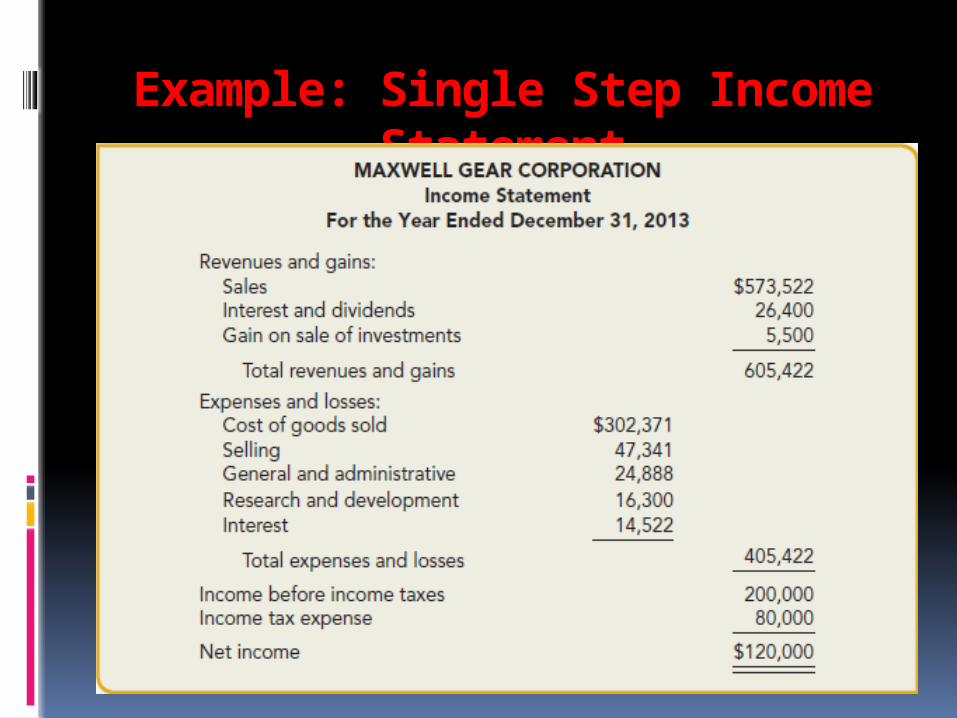

Example: Single Step Income Statement

Income Statement Format – Multiple -Step

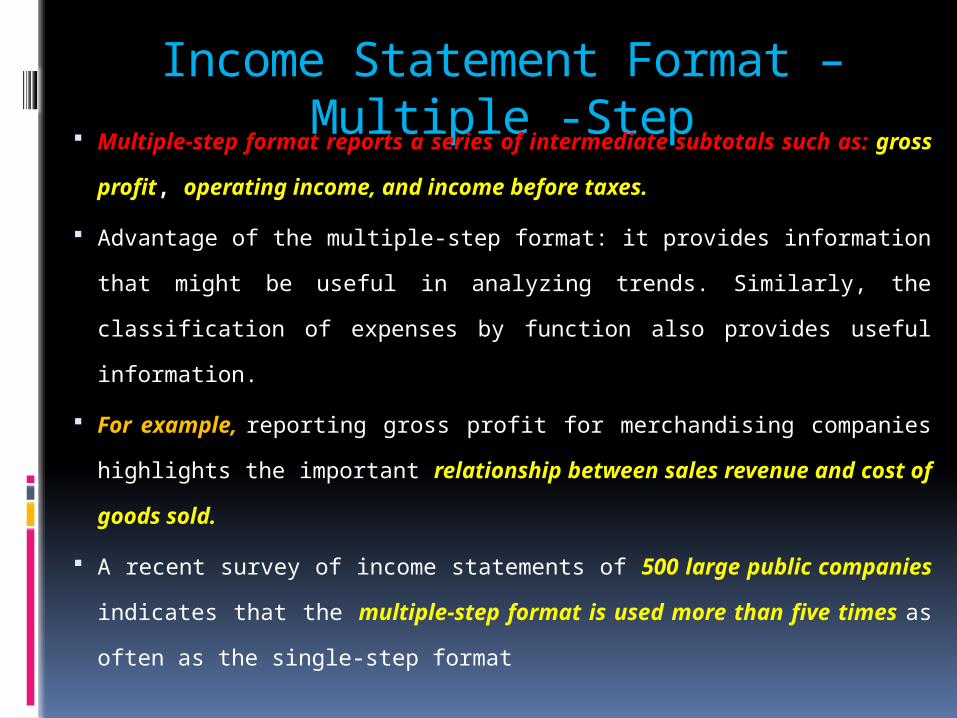

Multiple-step format reports a series of intermediate subtotals such as:

gross profit, operating income, and income before taxes.

Advantage of the multiple-step format: it provides information that might be

useful in analyzing trends. Similarly, the classification of expenses by

function also provides useful information.

For example, reporting gross profit for merchandising companies highlights

the important relationship between sales revenue and cost of goods sold.

A recent survey of income statements of 500 large public companies

indicates that the multiple-step format is used more than five times as often

as the single-step format

Example: Multiple – Step Income Statement

Balance Sheet

The purpose of the balance sheet , sometimes referred to as the

statement of financial position , is to report a company’s

financial position on a particular date.

The balance sheet, along with accompanying disclosures,

provides a wealth of information to external decision makers.

The information provided is useful not only in the prediction of

future cash flows but also in the related assessments of

liquidity and long-term solvency.

Classification of Elements in the Balance Sheet

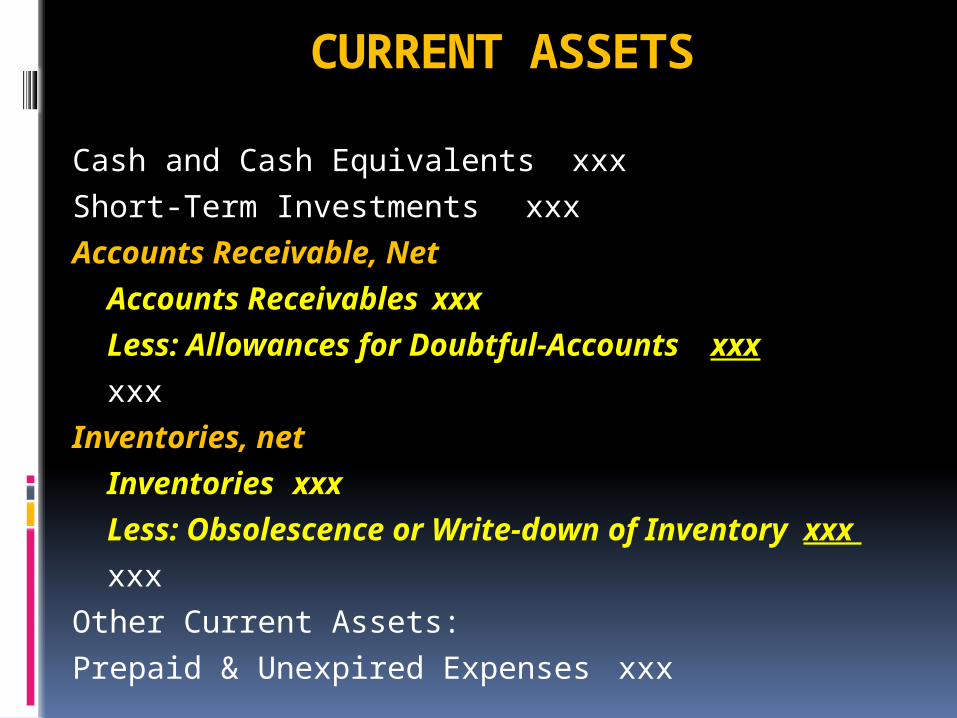

CURRENT ASSETS

Cash and Cash Equivalents xxx

Short-Term Investments xxx

Accounts Receivable, Net

Accounts Receivables xxx

Less: Allowances for Doubtful-Accounts xxx

xxx

Inventories, net

Inventories xxx

Less: Obsolescence or Write-down of Inventory xxx

xxx

Other Current Assets:

Prepaid & Unexpired Expenses xxx

NON – CURRENT ASSETS

Property, Plant, & Equipment xxx

Less: Accumulated Depreciation xxx xxx

Investments xxx

Long-Term Financing Receivables xxx

Goodwill xxx

Less: Amortization xxx xxx

Purchased Intangible Assets xxx

(Patents, Copyrights, Franchise)

Less: Amortization xxx xxx

Other Non-Current Assets xxx

(Deferred Charges, Long-Term

Financing Receivables)

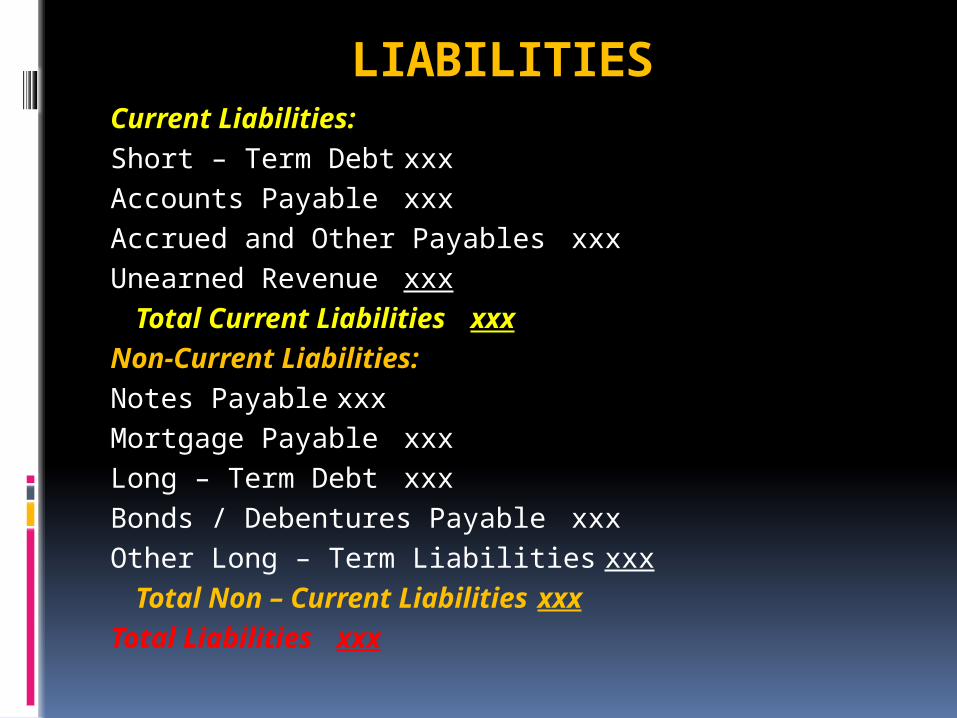

LIABILITIESCurrent Liabilities:

Short – Term Debt xxx

Accounts Payable xxx

Accrued and Other Payables xxx

Unearned Revenue xxx

Total Current Liabilities xxx

Non-Current Liabilities:

Notes Payable xxx

Mortgage Payable xxx

Long – Term Debt xxx

Bonds / Debentures Payable xxx

Other Long – Term Liabilities xxx

Total Non – Current Liabilities xxx

Total Liabilities xxx

SHAREHOLDERS’ EQUITY

Common Stock xxx

Less: Treasury Stock xxx xxx

Paid – In – Capital in Excess of Par xxx

Other Comprehensive Surplus / Losses xxx

Retained Earnings xxx

Total Shareholder’s Equity xxx

York Boutique Income Statement

For the year ended December 31

Name of Accounts $ $Revenue:Sales 600000Less: Cost of Goods Sold 408000Gross Margin 192000Less: Operating Expense:Selling & Distribution Expenses:Salaries and Wages Expense 52400Advertising Expenses 6000Total Selling & Distribution Expenses 58400Administrative Expenses:Salaries and Wages Expense 65000Supplies Expenses 3500Bad Debt Expense 1400Depreciation Expense 12000Insurnace Expense 2550Total Administrative Expenses: 84450Total Operating Expense: 142850Income from Operations 49150Finacial Income:Financial Expenses:Interest Expense 3360Net Income before Taxes 45790Less: Income Tax ExpenseNet Income after Taxes 45790

York Boutique Balance Sheet

As at December 31 Name of Accounts $ $

Assets:Current Assets:Cash $18,500Accounts Receivable 32000Less: Allowance for Doubtful Accounts 2100

29900Inventory, December 31 80000Prepaid Insurance 2550Prepaid Advertising 700Supplies 1500Total Current Assets $133,150Non-Current Assets:Equipment 84000Less: Accumulated Depreciation - Equipment 47000

37000Total Non-Current Assets 37000

Total Assets $170,150

Liabilities and Owners Equity:Liabilities:Current Liabilities:Interest Payable 3360Salaries and Wages Payable 2400Total Current Liabilities 5760Non-Current Liabilities:Notes Payable 28000Total Non-Current Liabilities 28000Total Liabilities 33760Owners Equity:Common Stock 80600Retained Earnings 55790Total Owners Equity 136390Total Liabilities and Equity 170150

Completing the Accounting Cycle