-

8/12/2019 Lecture 17 the Financial Crisis

1/25

International Political Economy #17

The Global Financial Crisis

William Kindred Winecoff

Indiana University Bloomington

October 29, 2013

W. K. Winecoff | IPE #17: The Global Crisis 1/25

http://find/

-

8/12/2019 Lecture 17 the Financial Crisis

2/25

Why Is This Worth Talking About?

Alan Greenspan: Likely to be judged the most virulent global

financial

crisis ever.

Huh? What about the Great Depression? How could this be more

virulent than that?

The U.S. lost $14 trillion in wealth, or 100% of GDP, via

the

stock market collapse in 2008-2009.

The U.S. lost $8-13 trillion in production as well.

Fine, but it was just a U.S. crisis, right?

Nope. Global equity wealth destroyed was nearly $35

trillion,

or the combined GDP of US, EU, and Japan... worlds three

largest economies at the time.

W. K. Winecoff | IPE #17: The Global Crisis 2/25

http://find/

-

8/12/2019 Lecture 17 the Financial Crisis

3/25

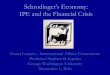

Why Is This Worth Talking About?

0.5

0.0

0

.5

1.0

Period

PercentChange

2004 2005 2006 2007 2008 2009

Global Equity Markets, 20042009

S&P 500FTSEHang SengNikkei

W. K. Winecoff | IPE #17: The Global Crisis 3/25

http://find/

-

8/12/2019 Lecture 17 the Financial Crisis

4/25

What Is This Worth Talking About?

Okay, but thats just stock markets. Rich people can afford

it.

W. K. Winecoff | IPE #17: The Global Crisis 4/25

http://goforward/http://find/http://goback/

-

8/12/2019 Lecture 17 the Financial Crisis

5/25

Why Is This Worth Talking About?

Ouch. That five percentage point drop represents about 17

million

Americans that lost their jobs, and theyve mostlystayedlost.

W. K. Winecoff | IPE #17: The Global Crisis 5/25

http://find/

-

8/12/2019 Lecture 17 the Financial Crisis

6/25

Why Is This Worth Talking About?

5

0

5

10

15

Year

GDP

Growth

2001 2002 2003 2004 2005 2006 2007 2008 2009

GDP Growth, 20012009

United StatesUnited Kingdom

JapanChina

World

W. K. Winecoff | IPE #17: The Global Crisis 6/25

http://find/

-

8/12/2019 Lecture 17 the Financial Crisis

7/25

Who Can We Blame For This?

Scape-goating is the national pastime. So who should we put in

the

stocks? Some popular explanations:

Bankers are greedy bastards. Then again, bankers are always

greedy bastards; cant explain change with a static variable.

Government: policies that rewarded risky mortgage

lending?Regulators: hobbled by free market economic ideology?

Issues:

Need to explain the global nature of the crisis.

Need to explain why the crisis occurred in many different

jurisdictions, with different banking sectors, regulatory

policies, and government types.

Crisis not limited to places where US government set

housing/monetary policy.

W. K. Winecoff | IPE #17: The Global Crisis 7/25

http://find/

-

8/12/2019 Lecture 17 the Financial Crisis

8/25

Who Can We Blame For This?

So the popular explanations contain some truth, but they cant

explaineverything. They dont explain why we got the financial

crisis we got,

when we got it.

W. K. Winecoff | IPE #17: The Global Crisis 8/25

http://find/

-

8/12/2019 Lecture 17 the Financial Crisis

9/25

Why We Got What We Got When We Got It

The financial collapse began with complicated financial

instruments

linked to the subprime mortgage real estate sector.

Explaining those in detail is too wonky for this class, but for

those

interested see two This American Lifepodcasts:

The Giant Pool of Money (episode 355, 5.9.2008)

Another Frightening Show About the Economy (episode

365, 10.3.2008)

These partially reinforce the greedy bankers and bad

regulatorsexplanations. But there is a difference between proximate

causes and

fundamental causes.

W. K. Winecoff | IPE #17: The Global Crisis 9/25

http://find/

-

8/12/2019 Lecture 17 the Financial Crisis

10/25

Why We Got What We Got When We Got It

The Story of Chimerica: the linkages between the U.S. and

Chinese

economies during the Naughties. (Subset of the Global Savings

Glut.)

The U.S. had low unemployment, and wanted to consume.

China had high unemployment, and wanted to produce.

U.S. policy: tax cuts + plus cheap loans for students and

home-buyers =

Ownership society + Go shopping or the terrorists win.

China policy: Under-valued currency + savings rates from 40-50%

of

GDP = boost employment via exporting goods and capital to

U.S.The result:

W. K. Winecoff | IPE #17: The Global Crisis 10/25

http://find/

-

8/12/2019 Lecture 17 the Financial Crisis

11/25

Why We Got What We Got When We Got It

W. K. Winecoff | IPE #17: The Global Crisis 11/25

http://find/

-

8/12/2019 Lecture 17 the Financial Crisis

12/25

Why We Got What We Got When We Got It

Remember your national accounting: S - I = X - M.

China: S > I implies X > M.

U.S.: S < I implies X < M.

A U.S. current account deficit implies an equal capital account

surplus.

I.e., China (a poor country) was sending the U.S. (a rich

country)

consumption goodsand investment finance. In exchange we gave

them

IOUs and boosted their employment. Crazy?

No. Political. We want our houses and consumption goods. They

want

jobs. Leaders in both countries enacted policy to meet the

demands oftheir polities.

Hundreds of billions of dollars flowing into the U.S. economy

every year

has to go somewhere.

W. K. Winecoff | IPE #17: The Global Crisis 12/25

http://find/

-

8/12/2019 Lecture 17 the Financial Crisis

13/25

Why We Got What We Got When We Got It

Okay. But why housing? Macroeconomic story:

1 Foreign purchases of $ >

2 $ appreciation >

3 Increase in imports (CA deficit) + increase in

non-tradable

goods prices relative to tradable goods prices >

4 Shift in investment from manufacturing to housing.

At first, this just meant low mortgage rates for qualified

borrowers. But

then there were no more qualified borrowers, and still all this

foreignsavings coming into the U.S.

W. K. Winecoff | IPE #17: The Global Crisis 13/25

http://find/

-

8/12/2019 Lecture 17 the Financial Crisis

14/25

Why We Got What We Got When We Got It

Macropolitical story:

1 GSG increases supply in (non-US) S >

2 Fannie Mae/Freddie Mac guarantee + tax/regulatory code

increases demand for (US) I

>

3 Creation and global dissemination of mortgage-backed

securities make risky mortgages safer.

Not mutually exclusive of course. The result: a huge housing

bubble,

backed up by mountains of opaque, illiquid financial

instruments. These

later become known as toxic assets, or, the sort of thing you

dont

want to be holding when the music stops. This is what TARP

bought.

W. K. Winecoff | IPE #17: The Global Crisis 14/25

http://find/

-

8/12/2019 Lecture 17 the Financial Crisis

15/25

Why We Got What We Got When We Got It

In other words, theres plenty of blame to go around: the

citizens, the

bankers, the regulators, the government, the Chinese. We in the

U.S.

wanted the things big houses, cheap consumer goods that the

financial sector, incentivized by the government, provided.

But this only explains why the U.S. had a financial crisis. How

did a

local housing crisis turn into a global meltdown?

W. K. Winecoff | IPE #17: The Global Crisis 15/25

http://find/

-

8/12/2019 Lecture 17 the Financial Crisis

16/25

How They Got What They Got When They Got It

W. K. Winecoff | IPE #17: The Global Crisis 16/25

http://find/

-

8/12/2019 Lecture 17 the Financial Crisis

17/25

How They Got What They Got When They Got It

W. K. Winecoff | IPE #17: The Global Crisis 17/25

http://find/

-

8/12/2019 Lecture 17 the Financial Crisis

18/25

How They Got What They Got When They Got It

W. K. Winecoff | IPE #17: The Global Crisis 18/25

http://find/

-

8/12/2019 Lecture 17 the Financial Crisis

19/25

-

8/12/2019 Lecture 17 the Financial Crisis

20/25

What They Got

So there are dozens of banking crises around the world, almost

all of

which happened in developed countries strongly connected to the

U.S.

(according to IMF researchers).

So there is a debt crisis that threatens to destroy the

Europeanmonetary union. (More on Thurs)

So there is a fixed investment bubble in China that threatens to

pop and

drag down the worlds fastest-growing major economy.

So there is a drop in Japanese growth and increase in debt, even

before

the earthquake and nuclear meltdown in Fukushima.

The collapse in global demand hurts poor workers in exporting

countries.

W. K. Winecoff | IPE #17: The Global Crisis 20/25

http://find/

-

8/12/2019 Lecture 17 the Financial Crisis

21/25

What They Got

Many governments respond with expansionary monetary policy (i.e.

low

interest rates) to try to stabilize the banks and generate

economic

activity by stimulating consumption and investment demand. The

U.S.

Federal Reserve is the most important, globally.

But there is an unintended consequence: extreme commodity

price

volatility, which (remember Malthusian conflict?) can lead to

civil

unrest, particularly in places with youth bulges in large urban

areas.

Which places are those? Refer to past lectures.

W. K. Winecoff | IPE #17: The Global Crisis 21/25

http://find/

-

8/12/2019 Lecture 17 the Financial Crisis

22/25

What They Got

W. K. Winecoff | IPE #17: The Global Crisis 22/25

http://find/

-

8/12/2019 Lecture 17 the Financial Crisis

23/25

What We All Did

Developed Countries:

Governments bailed out banks (U.S., E.U., Japan).

E.U. bailing out highly-indebted countries (kind of).Voted out

our governments (U.S., U.K., Ireland, Iceland,

Greece, Japan, etc.).

Stimulus vs. austerity: Leads to protest movements, e.g. Tea

Party and Occupy Wall Street. Spanish Indignados. General

strikes in a number of European countries (e.g. Greece,

Italy).

W. K. Winecoff | IPE #17: The Global Crisis 23/25

http://find/

-

8/12/2019 Lecture 17 the Financial Crisis

24/25

What We All Did

Developing Countries:

Some governments e.g. Saudi Arabia increase transfers

to citizens and/or institute price controls to keep food and

fuel prices from spiraling too far out of control.

Some pass a number of reforms related to civil rights.

Others do not. Let them eat cake". Protests begin.

Citizens of Tunisia, Egypt, Libya, Yemen overthrow their

governments.

Citizens of Bahrain, Syria, Iran still trying.

W. K. Winecoff | IPE #17: The Global Crisis 24/25

http://find/

-

8/12/2019 Lecture 17 the Financial Crisis

25/25

The Lesson

Maybe Greenspan was right: maybe this was most virulent

financial

crisis ever.

Outcomes not as bad as Great Depression because governments

intervened earlier, plus institutions exist to foster

cooperation (IMF, UN,

EU). Thankfully, we learned some lessons.End up with Arab Spring

rather than another World War?

But interventions are political... should we be bailing out the

banks?

How do we narrow deficits: raise taxes or cut spending? How do

we

manage civil unrest in the Gap?

Central point: the causes of the crisis, and the reactions to

it, were

largely political and largely global. Just blaming the bankers

isnt good

enough.

W. K. Winecoff | IPE #17: The Global Crisis 25/25

http://goforward/http://find/http://goback/