Embed Size (px)

Citation preview

1

LBS and leisure market overviewLBS and leisure market overview

Boris KennesR&D and Market Monitoring Officer

European GNSS Supervisory Authority

3

Mobile LBS are finally starting to take off as Mobile LBS are finally starting to take off as remaining obstacles are largely addressedremaining obstacles are largely addressed

More and more devices with GNSS inside (EU-27)

Application stores provide a viable business model for all stakeholders

Consumer and developer awareness is high

38

29

148

0

10

20

30

40

0

5

10

15

20

25

2010200920082007

GNSS shipments (mln)

GNSS penetration

• 140,000 apps• 3 bn dowloads• $1 bn gross revenues• Driving iPhone sales• 70% of gross

revenues to developers

• Increasing mobile traffic

• Similar concepts by Google, Nokia, RIM

Apple example

80

60

40

20

100

0

5

25

20

15

10

02009

21

100

2008

12

10

2007

10

iPhones sold (mln)

Apps available (000’s)

• In UK, FR, DE, 5 out of 10 best selling i-phone apps in 2009 are related to navigation or LBS – and not the cheapest (!)

• 30% of Android developer’s contest winners used location in the application

• Nokia recorded 1.4 mln map downloads in 4 days when the company launched a new version that includes free navigation

• 5-6000 location based applications on App store

Navigation performance increasing (but still long way to go)

Leading smart-phones display a host of technologies to improve position performance

• Assisted – GPS to reduce Time To First Fix

• Magnetic Compass• Highly sensitive receiver• WiFi and cellular positioning as back-up• Motion sensors and gyroscopes for tilt• Map matching • Reduced power consumption

4

LBS is at the start of an impressive growth curve, LBS is at the start of an impressive growth curve, possibly resulting in a >100bn marketpossibly resulting in a >100bn market

GNSS Devices and penetration

• GNSS becoming a standard feature on medium-high end mobile phones

• Mobile penetration continues to grow in emerging markets

• Replacement sales driving most of the sales

GNSS revenues

• Increasing device sales somewhat offset by declining prices and GNSS adoption on cheaper phones

• Increasing use of value added services driven by success of app stores.

0

200

400

600

800

1000

1200

1400

1600

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2030

Mill

ion

units

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

GNSS enabled handsets (Smarphones, PDA's, Mobiles) sales GNSS penetration

0

500

1000

1500

2000

2500

3000

3500

4000

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2030

Mill

ions

0

5

10

15

20

25

30

35

40

€/ye

ar

Worldwide subscribers Average annual ARPU

5

LBS services, such as emergency call, can save lives LBS services, such as emergency call, can save lives and result in fewer severe injuries and result in fewer severe injuries

VAT

All All Emergency applications

Mobility applications

Mobility applications

Mobility applications

1 mln lives

improved

270.000 Violent crimes avoided

LBS non-monetized benefits (cumulated 2010-2030)

~ 130.000 lives saved**

Benefit for public institutions Benefit for users

Social benefits

GNSS - LBS monetized benefits (Billions of Euros, cumulated 2010-2030)

Applications involved

~2 bln litres ~8 mln tons~640 000 injuries

Equivalent to

~ 25.000new jobs

*Estimates are performed considering Workplace and Home & Leisure accidents**Lives saved include a share of causes of deaths where speed of intervention is critical (ischaemic heart diseases, cerebrovascular diseases and asthma)

159

123

29

Corporate TaxVAT Reduced injuries

Reduced fuel consumption

4

2 1 0

Reduced air pollution

Reduced CO2 emission

total

6

Deve- lopers

Vertical integration has resulted in a more mature Vertical integration has resulted in a more mature value chain and business modelsvalue chain and business models

Chipset manu-

facturersMap data providers App stores

Device Vendors

Top 5 companies (81% market share)

• Nokia• RIM (Blackberry)• Apple• HTC• Samsung

Trends• Fast growing

market (15% in 09), resulting in higher share of mobile market (15% in 09)

• Highly competitive market

• Increasing emphasis on luring software developers

• Relentless innovation

Top 5 companies• Broadcom (Motorola,

Apple, Samsung)• SiRF / CSR (HTC)• Texas Instrument• Qualcomm• ST Microelectronics

Trends• Increasing

integration of technologies (GPS + Cellular + Wifi,…)

• Vertical integration and disappearance of independent chipset manufacturers

• Low cost and power consumption

• Diversification of markets (cameras, PNDs, watches)

Global map data providers:

• Navteq (Nokia)• TeleAtlas (TomTom)

Regional map data providers:

• Google (US), Navinfo(CN), Autonavi (CN), Mapmyindia (IN)

Trends• Maps offered for free

(Nokia and Google)• Innovation (3D,

detailed maps)

Major stores• Apple: App store

(140,000 aps)• Google: Android market

(20,000 aps)• Nokia: Ovi Store• Blackberry: app world

rends• Increasing importance of

app stores: working business model (revenue sharing)

• Developer contests• Explosive growth of

applications (140,000 in app store)

• Navigation free, basic service

Main categories:• Navigation• Games• Information

Services• News• Social Networking

Developers• Huge population

(iPhone developer SDK downloaded 100,000 times in 6 days)

Trends• Larger companies

entering the arena

• Global market with local accents

Increasing integration

Mobile opera-

tors

Major types• 3-5 mobile

networks per country

• Several alternatives based on WiFi and FWA

Trends• Increasing

network speeds 3G, 3.5G, WiFi etc.

• Decreasing data pricing, roaming charges still high

• Major operators have own services and applications

7

GSA is planning specific actions for stimulating GSA is planning specific actions for stimulating driversdrivers

• Positioning performance (Indoor positioning, TTFF, Position accuracy, energy consumption)

• Lower Cost• Content availability and developer

ecosystem

• Visibility on market opportunities

• Funding• Availability of talented

developers• Content availability

• Visibility on market opportunities

• R&D funding• Pricing information• Stable specifications

Applications R&D funding

47 projects in 2 calls total €40mln

3rd call expected later this year (€38 mln)

Horizontal actions

EGNOS market stimulating actions

Co-marketing with stakeholders

Awareness and EGNOS portal

Adapting EGNOS for different circumstances

Market monitoring

Market forecasts

Indirect benefits and public utility of satellite navigation

Galileo and EGNOS added value

Deve- lopers

Chipset manu-

facturersMap data providers App stores

Device Vendors

Increasing consolidation

Mobile opera-

tors

Dri

vers

fo

r LB

S

ad

op

tio

nG

SA

mark

et

stim

ula

tio

n a

ctio

ns

• Safety• Environm

ent• Economic

Growth

8

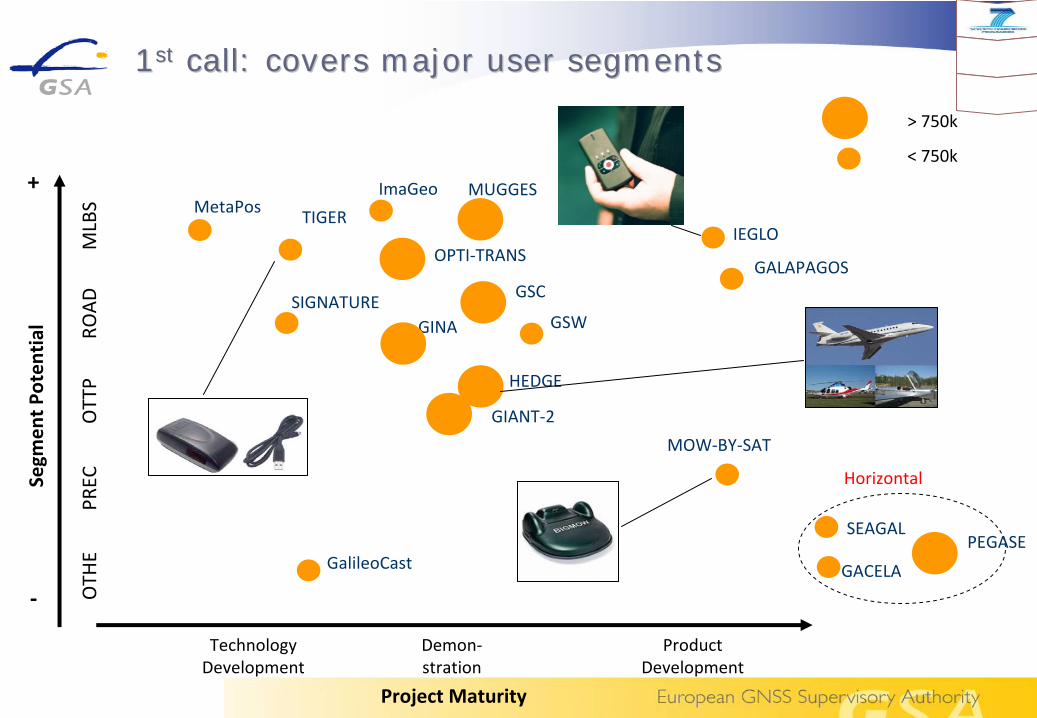

11stst call: covers major user segmentscall: covers major user segments

Project Maturity

Technology

Development

Demon‐

stration

Product

Development

OPTI‐TRANS

MUGGES

MOW‐BY‐SAT

> 750k

< 750k

Segm

ent P

oten

tial

+

‐

MLBS

ROAD

OTTP

OTH

EPR

EC

IEGLO

GALAPAGOS

TIGER

SIGNATUREGSW

GSC

GINA

GalileoCast

MetaPos

SEAGAL

GACELA

Horizontal

PEGASE

HEDGE

GIANT‐2

ImaGeo

9

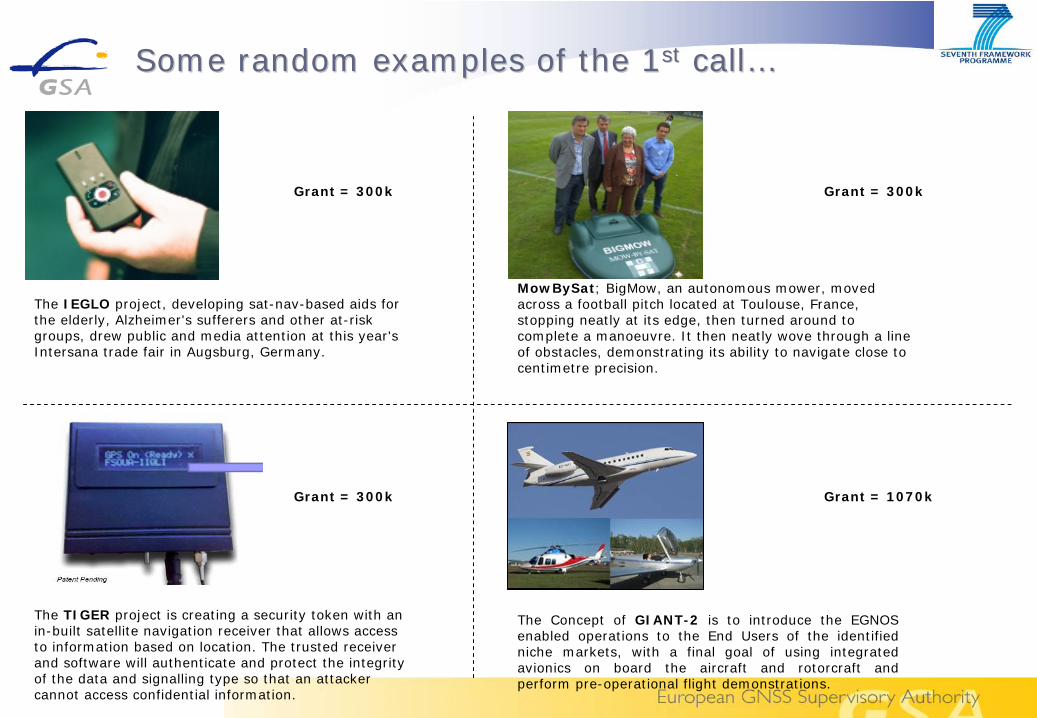

Some random examples of the 1Some random examples of the 1stst callcall……

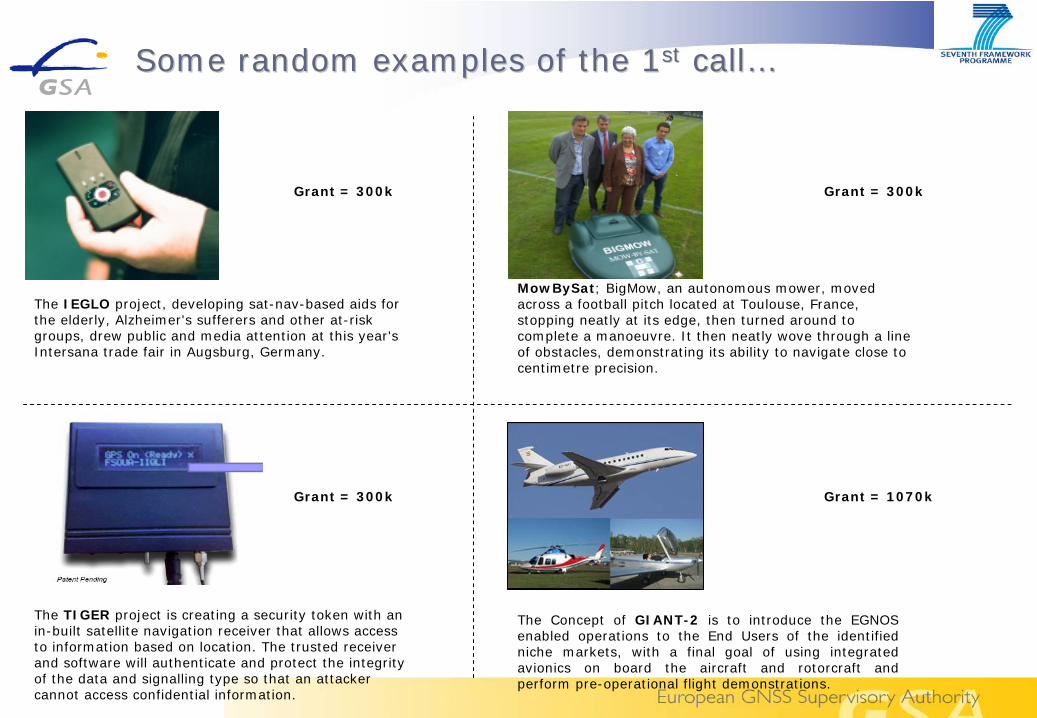

The IEGLO project, developing sat-nav-based aids for the elderly, Alzheimer's sufferers and other at-risk groups, drew public and media attention at this year's Intersana trade fair in Augsburg, Germany.

MowBySat; BigMow, an autonomous mower, moved across a football pitch located at Toulouse, France, stopping neatly at its edge, then turned around to complete a manoeuvre. It then neatly wove through a line of obstacles, demonstrating its ability to navigate close to centimetre precision.

The TIGER project is creating a security token with an in-built satellite navigation receiver that allows access to information based on location. The trusted receiver and software will authenticate and protect the integrity of the data and signalling type so that an attacker cannot access confidential information.

The Concept of GIANT-2 is to introduce the EGNOS enabled operations to the End Users of the identified niche markets, with a final goal of using integrated avionics on board the aircraft and rotorcraft and perform pre-operational flight demonstrations.

Grant = 300k Grant = 300k

Grant = 300k Grant = 1070k

10

What more can we expect in the 2What more can we expect in the 2ndnd call?call? Some examples Some examples ……

LS4P - LiveSailing for Professionals, a High precision and reliable positioning system for sailing professionals.

Grant = 484k

CLOSE-SEARCH - Accurate and safe EGNOS-SoL Navigation for UAV- based low-cost SAR operations. Prototype a small unmanned helicopter with integrated thermal sensor and a multisensor GPS- EGNOS-based navigation system with an Autonomous Integrity Monitoring capability, to support search in SAR operations in remote, difficult-to-access areas and/or in time critical situations.

SCUTUM - SeCUring the EU GNSS adopTion in the dangeroUs Material transportImplementation of an EGNOS/EDAS based system for the monitoring of dangerous goods transport

ATLAS - Authenticating Time and Location within Liability- critical Applications and ServicesDevelop a GNSS Evidential Support Service and Authenticated GNSS Service to provide authenticated position and time information for multimedia captures.

Grant = 1,407kGrant = 271k

Grant = 308k

11

In the 2nd call, we are also supporting horizontal In the 2nd call, we are also supporting horizontal activitiesactivities

G-TRAIN – Supporting Education and Training in GNSS

Framework for higher education in GNSS at European level, addressing: MSc, a Specializing Master, support to PhD training and networking, creation of a Satellite University Network (SUN).

GAINS - Galileo Advanced INnovation Services

Implementation of ‘innovation valleys’ in the GNSS downstream market by validating and supporting GNSS ideas from Galileo Masters in Living Labs

12

2 Support Facilities

6 Navigation Land Earth Stations

GPS & GLONASS

Users & Service Providers

34 Ranging & Integrity Monitoring Stations (RIMS)

3 GEO Satellites

4 Mission Control Centres

EGNOS is there EGNOS is there –– use it!use it!

EGNOS awareness campaign

EGNOS system architecture

13

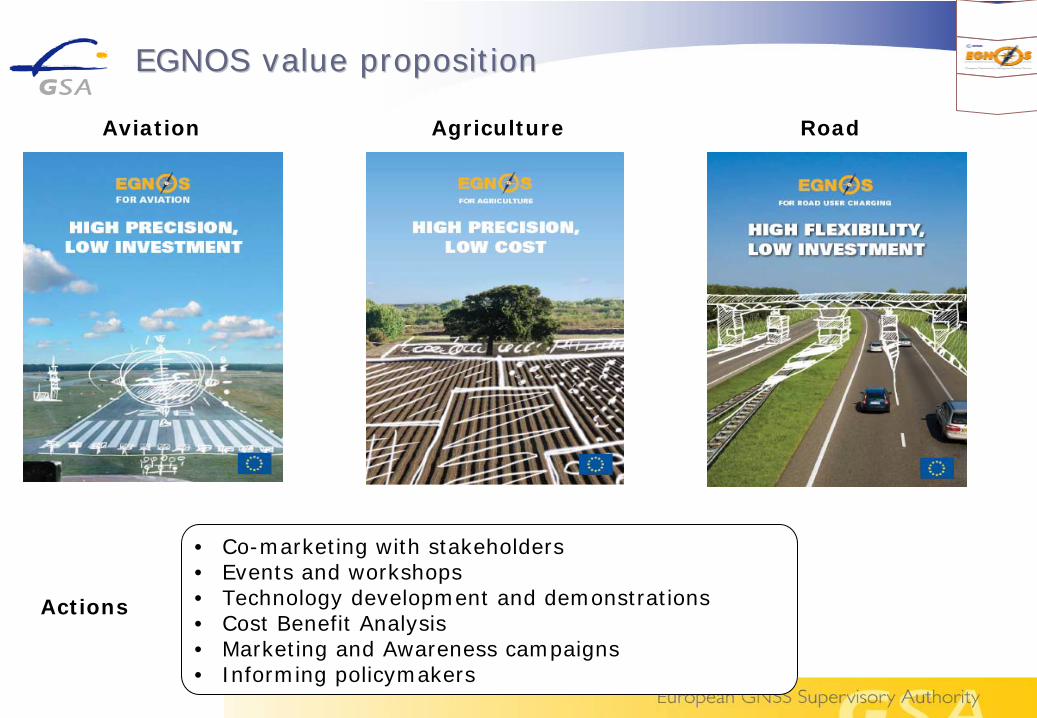

EGNOS value propositionEGNOS value proposition

• Co-marketing with stakeholders• Events and workshops• Technology development and demonstrations• Cost Benefit Analysis• Marketing and Awareness campaigns• Informing policymakers

Aviation Agriculture Road

Actions

14

EGNOS Data Access Service EGNOS Data Access Service (EDAS)(EDAS)

Phased approach:

Phase 1: prototyping since March 2008

Free-of-charge

Helpdesk

No guarantee of service

Phase 2: commercial exploitation

Feature enhancement

Enhancement of service level

Pricing (cost recovery)

Value-addedservice provider

End users

User-specificinformation

EGNOS data (real-time):

RIMS raw observations

SBAS messages

Online content: new website http://egnos-edas.gsa.europa.e

15

EGNOS portal EGNOS portal -- http://www.egnoshttp://www.egnos--portal.euportal.eu//

16

Market monitoring in support of GNSS programme Market monitoring in support of GNSS programme and GNSS industryand GNSS industry

0

20

40

60

80

100

120

140

160

180

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2030

Bill

ion

€

0%

10%

20%

30%

40%50%

60%

70%

80%

90%

100%

European Union North AmericaRest of the World GNSS Penetration European UnionGNSS Penetration North America

Road45.81%

LBS51.46%

PA1.62%

Aviation1.12%

European GNSS revenues by civil applicationGlobal GNSS revenues

Mark

et

Mo

nit

ori

ng

Pro

cess

Exam

ple

ou

tpu

ts

17

Afternoon programmeAfternoon programme

Market and industry overview

ESNC success stories

New applica- tion ideas - Elevator pitches

FP7 project presen- tations

Business speed dating*

Reception and concert

Break Break

* only for registered participants

Keynote presentations on the LBS market and trends

Presentations of past winners of Galileo masters

Short presentations other ESNC idea with live feedback

Presentations of ongoing EU funded projects on satnav applications

Short one-to- one meetings

Networking cocktail and piano concert in the village

18

Keynote speakers Keynote speakers -- changedchanged

14:20: Dominique Bonte – ABI Research - Practice Director, Telematics & Navigation - The future of Location in Consumer Markets

14:40: Laurent De Hauwere – Managing Partner – PTOLEMUS – Do you really mean business in LBS?

15:00: Rainer Horn – Managing Partner – SpaceTecCapital Partners - Market Challenges for LBS Developers

Thank you !Thank you !

Boris KennesR&D and Market Monitoring Officer

European GNSS Supervisory Authority

How GSA can help youHow GSA can help you

Boris KennesR&D and Market Monitoring Officer

European GNSS Supervisory Authority

21

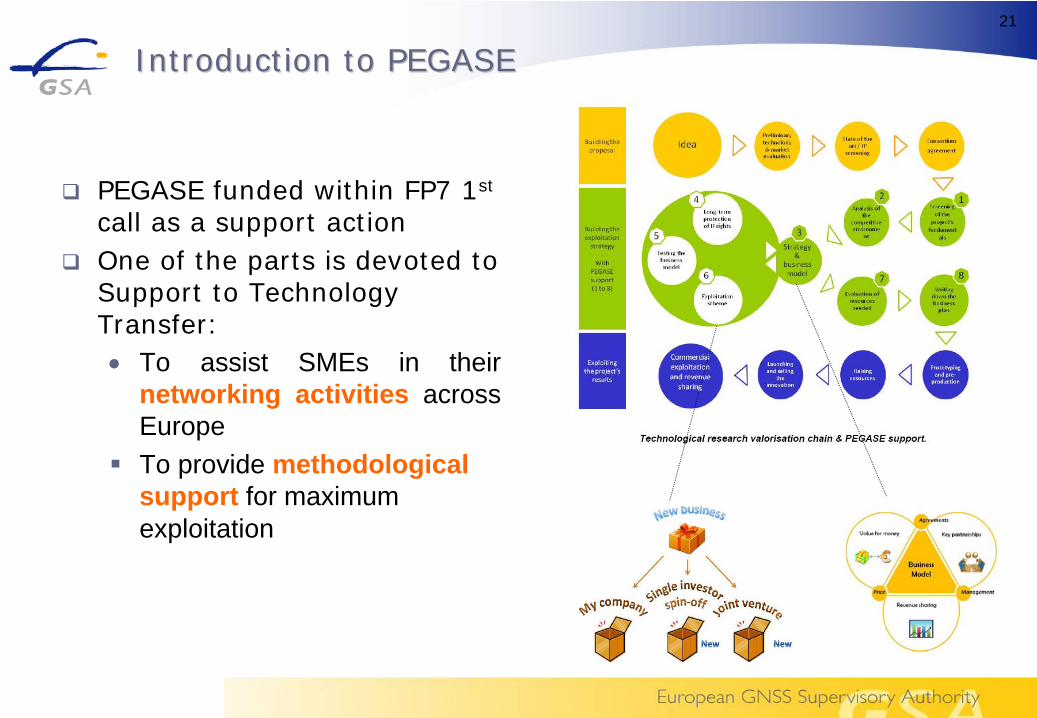

Introduction to PEGASEIntroduction to PEGASE

PEGASE funded within FP7 1st

call as a support action

One of the parts is devoted to Support to Technology Transfer:

To assist SMEs in their networking activities across Europe

To provide methodological support for maximum exploitation

22

Council andEuropean Parliament

European GNSSProgramme Committee

European Commission

Independantadvisors

European Space Agency

IOV contracts

FOC contracts

GNSS SupervisoryAuthority

MarketpreparationResearchAssistance tasks to EC

Tasks delegated by EC

Political oversight

Programme oversight and Programme Management

Execution

Others

dele

gatio

n

assi

stan

ce a

ndde

lega

tion

Accreditation

GSA supports European Commission on market development GSA supports European Commission on market development and security accreditationand security accreditation

Role of GSA being revised

23

GSA Market Development GSA Market Development visionvision

We believe that …

The GNSS market is developing very fast

GNSS is benefiting citizens, businesses and governments alike

Galileo and EGNOS are essential to capture full GNSS potential in Europe

GNSS enabled market (€

bn)

Public benefits of Galileo estimated at over

€50 bn

(cumulative)

0

20

40

60

80

100

120

140

160

180

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

Bill

ion

€

0%

10%

20%

30%

40%50%

60%

70%

80%

90%

100%

European Union North AmericaRest of the World GNSS Penetration European UnionGNSS Penetration North America

24

GSA Market Development GSA Market Development initiativesinitiatives

Applications R&D funding

47 projects in 2 calls total €40mln

3rd call expected later this year (€38 mln)

Horizontal actions

EGNOS market stimulating actions

R&D projects

Co-marketing with stakeholders

Awareness and EGNOS portal

Market monitoring

Market forecasts

Indirect benefits and public utility of satellite navigation

Galileo and EGNOS added value

25

Galileo R&D in FP7Galileo R&D in FP7

Cooperation

Ideas

Capacities

People

4 main blocks of activities

10 themes in cooperation

1. Health

10. Security

7. Transport (including

Aernautics)

4 sub themes in transport

Different calls for Galileo

Aeronautics and transport

Sust. surface transport

Galileo

Horizontal activities

2007, 1st call: €25m*

2008, 2nd

call: €40m**

€50.5bn €32.4bn €4.2bn

FP7 covers period 2007-2013* 19 mln for CP and CSA** 28 mln for CP and CSA

2011, 3rd call€38m

€103m+

26

FP7 1FP7 1stst and 2and 2ndnd call funding*call funding*

* Collaborative Projects and Coordination and Supporting Actions

(excludes tenders)

4%

6%16%

20%

Other

BE13%

AT 3%

NL3%

CH

UK

IT

10%

FR12%

DE

14%

ES

Funding per countryFunding per topic

4%

4%

9% 17%

20%

Scientific applications

2%

Rail

3%

Education and innovation

3%Precision and professional

3%Support3%SAR

International

Maritime

Aviation

LBS

9%

SME11%

Road

13%

Receivers

27

11stst call: covers major user segmentscall: covers major user segments

Project Maturity

Technology

Development

Demon‐

stration

Product

Development

OPTI‐TRANS

MUGGES

MOW‐BY‐SAT

> 750k

< 750k

Segm

ent P

oten

tial

+

‐

MLBS

ROAD

OTTP

OTH

EPR

EC

IEGLO

GALAPAGOS

TIGER

SIGNATUREGSW

GSC

GINA

GalileoCast

MetaPos

SEAGAL

GACELA

Horizontal

PEGASE

HEDGE

GIANT‐2

ImaGeo

28

22ndnd call: diversified portfolio of projectscall: diversified portfolio of projects

ACCEPTA

INCLUSION

SMART-WAY

SafePort

GRAIL-2

PERNASVIP

LS4P

PUMA

CLOSE SEARCH

CoSuDEC

GOLDEN-ICE

ERSEC

GNSSmeter

ATLAS

LIVELINE

I2GPS

ASPHALT

SX5

SIRAJ

ENCORE

CIGALA

ESESA

EEGS

GSARSED

SCUTUM

COVEL

GENEVA

G-TRAIN

GAINS

29

Some random examples of the 1Some random examples of the 1stst callcall……

The IEGLO project, developing sat-nav-based aids for the elderly, Alzheimer's sufferers and other at-risk groups, drew public and media attention at this year's Intersana trade fair in Augsburg, Germany.

MowBySat; BigMow, an autonomous mower, moved across a football pitch located at Toulouse, France, stopping neatly at its edge, then turned around to complete a manoeuvre. It then neatly wove through a line of obstacles, demonstrating its ability to navigate close to centimetre precision.

The TIGER project is creating a security token with an in-built satellite navigation receiver that allows access to information based on location. The trusted receiver and software will authenticate and protect the integrity of the data and signalling type so that an attacker cannot access confidential information.

The Concept of GIANT-2 is to introduce the EGNOS enabled operations to the End Users of the identified niche markets, with a final goal of using integrated avionics on board the aircraft and rotorcraft and perform pre-operational flight demonstrations.

Grant = 300k Grant = 300k

Grant = 300k Grant = 1070k

30

What more can we expect in the 2What more can we expect in the 2ndnd call?call? Some examples Some examples ……

LS4P - LiveSailing for Professionals, a High precision and reliable positioning system for sailing professionals.

Grant = 484k

CLOSE-SEARCH - Accurate and safe EGNOS-SoL Navigation for UAV- based low-cost SAR operations. Prototype a small unmanned helicopter with integrated thermal sensor and a multisensor GPS- EGNOS-based navigation system with an Autonomous Integrity Monitoring capability, to support search in SAR operations in remote, difficult-to-access areas and/or in time critical situations.

SCUTUM - SeCUring the EU GNSS adopTion in the dangeroUs Material transportImplementation of an EGNOS/EDAS based system for the monitoring of dangerous goods transport

ATLAS - Authenticating Time and Location within Liability- critical Applications and ServicesDevelop a GNSS Evidential Support Service and Authenticated GNSS Service to provide authenticated position and time information for multimedia captures.

Grant = 1,407kGrant = 271k

Grant = 308k

31

In the 2nd call, we are also supporting horizontal In the 2nd call, we are also supporting horizontal activitiesactivities

G-TRAIN – Supporting Education and Training in GNSS

Framework for higher education in GNSS at European level, addressing: MSc, a Specializing Master, support to PhD training and networking, creation of a Satellite University Network (SUN).

GAINS - Galileo Advanced INnovation Services

Implementation of ‘innovation valleys’ in the GNSS downstream market by validating and supporting GNSS ideas from Galileo Masters in Living Labs

32

The 2The 2ndnd call in numberscall in numbers

104 proposals were received

From 486 different companies and institutions

Originating from 40 countries

In total, €108m in grants were requested

About 4 times the €28.5m budget that was announced

Almost 70% of proposals were above threshold with an average score of 10.9

29 projects selected for funding

SMEs were present in 90% of the winning proposals and received 36% of the funds

Average consortium consisted of 6 partners and requested 1 mln EUR

33

33rdrd call: it is not too early to startcall: it is not too early to start

To be announced later this year

Total amount of funding €38mln covering all areas in the Galileo Work Programme

Applications

Receivers

Tools

Programme support

International and horizontal activities

34

2 Support Facilities

6 Navigation Land Earth Stations

GPS & GLONASS

Users & Service Providers

34 Ranging & Integrity Monitoring Stations (RIMS)

3 GEO Satellites

4 Mission Control Centres

EGNOS is there EGNOS is there –– use it!use it!

EGNOS awareness campaign

EGNOS system architecture

35

EGNOS value propositionEGNOS value proposition

36

EGNOS portal EGNOS portal -- http://www.egnoshttp://www.egnos--portal.euportal.eu//

37

EGNOSEGNOS Data Access Service Data Access Service (EDAS)(EDAS)

Phased approach:

Phase 1: prototyping since March 2008

Free-of-charge

Helpdesk

No guarantee of service

Phase 2: commercial exploitation

Feature enhancement

Enhancement of service level

Pricing (cost recovery)

Value-addedservice provider

End users

User-specificinformation

EGNOS data (real-time):

RIMS raw observations

SBAS messages

Online content: new website http://egnos-edas.gsa.europa.e

38

Market monitoring in support of GNSS programme and GNSS Market monitoring in support of GNSS programme and GNSS industryindustry

0

20

40

60

80

100

120

140

160

180

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2030

Bill

ion

€

0%

10%

20%

30%

40%50%

60%

70%

80%

90%

100%

European Union North AmericaRest of the World GNSS Penetration European UnionGNSS Penetration North America

Road45.81%

LBS51.46%

PA1.62%

Aviation1.12%

European GNSS revenues by civil applicationGlobal GNSS revenues

Mark

et

Mo

nit

ori

ng

Pro

cess

Exam

ple

ou

tpu

ts

39

Enjoy the event!

40

All major CA/GA device manufacturers acknowledge EGNOS value proposition

CBA outcomes proved to be positive for the key players

Cooperation being defined with device manufacturers

Marketing campaign– Participate to key events (e.g. EBACE, Le Bourget)– Communication (e.g. video, print ads with EC, …)

Co-finance of landing procedures to create airports cluster (e.g., FP7 projects)

Flight and ground handling demos for business aviation, helicopters, private planes and regional airlines

Garmin committed to promote EGNOS receivers

Procedures are being developed in Spain, France, UK, Poland, Italy

“High precision landing, low investment” value proposition

CBA to support adoption decision (in cooperation with Eurocontrol)

Assess market situation and opportunities for adoption

Follow-up on progress of pre-conditions for adoption with EC, EASA, ESSP and RNAV task force

Market adoption info to key players; also ready to be included in upcoming EGNOS portal

Actions Results

Mark

et

kn

ow

led

ge

Pu

shin

g f

or

ad

op

tio

nM

ark

et

en

try

Aviation: fostering accelerated adoption from 2010Aviation: fostering accelerated adoption from 2010

41

Major Electronic Tolling service providers now acknowledge the EGNOS potential

Results of business case with road operator expected by March 2010

Field trials to demonstrate EGNOS benefits

Marketing campaign with decision makers:- increase knowledge of the GNSS potential- promote EGNOS value added

ENI: early EGNOS adopter (FP6 Mentore)

EGNOS trials in progress:– 2 Service Providers evaluating EGNOS

(results by 2010)– 1 nationwide trial in the Netherlands in

March 10 (FP7 GINA)

Road Operators (e.g., ASECAP members) and relevant National Authorities (e.g., ABvM) being reached

Creation of the EGNOS value proposition: “high flexibility, low investment “

GNSS/ EGNOS CBA in RUC: a tool to show competitive advantage to the different actors

Assess EU market situation andopportunities for adoption

Analyze GNSS/ EGNOS value

Identification of: – Potential next adopters of GNSS

RUC schemes– Potential adopters of EGNOS

Actions Results

Mark

et

kn

ow

led

ge

Pu

shin

g f

or

ad

op

tio

nM

ark

et

en

try

Road: positioning EGNOS as Road: positioning EGNOS as ““the solutionthe solution””

42M

ark

et

kn

ow

led

ge

Pu

shin

g f

or

ad

op

tio

n

Build active cooperation with device and tractor manufacturers

Marketing campaign– Participation at key European events (e.g.,

JIAC, Agritechnica)– Communication (e.g., brochures, video,

flyers)

4 leading brands decided to introduce new EGNOS products to their portfolio

Other major brands declared interest in a partnership

Actions Results

Create the “affordable precision” value proposition

Build CBA to support adoption decision

Assess current market situation and opportunities for adoption

Analyse existing technologies

Analysis on market size and EGNOS market share

Demonstrated EGNOS ability to fulfill user needs in a wide range of applications

Mark

et

en

try

09E 10F

25

50

75

100

0

EGNOS

DGPS

RTK

12F11F

EGNOS penetration

136k 165k 200k 240k

Major device and tractor manufacturers acknowledge EGNOS value proposition

…

Precision Agriculture Market share (%)

Precision Agriculture: Harvesting EGNOS benefitsPrecision Agriculture: Harvesting EGNOS benefits