Embed Size (px)

Citation preview

Launching the European Semester Country Report for Romania

Thematic session on Competitiveness, Business Environment and Investment

- Key findings from the Country Report -

• Bucharest

• 15 March 2017

Outline

1. Annual Growth Survey and European Semester 2017

2. Economic performance and main challenges

3. Implementation of country-specific recommendations

4. Key messages from the 2017 Country Report

1. Cost competitiveness 2. Education, skills, research

3. Digital skills and ICT 4. Business environment

5. Taxation 6. Public investment and infrastructure

7. Corporate governance 8. Judicial system

9. Public administration 10. Public procurement

5. Conclusions

Annual Growth Survey 2017

• political guidelines: “strengthen competitiveness and stimulate

investment for the purpose of job creation” incl. “investment in infrastructure”, “the right regulatory environment” and “a climate of entrepreneurship and job creation”

• AGS priorities 2016/17: redouble the efforts on the three key priotities and put the focus on social fairness to deliver more inclusive growth:

(1) boost investment; (2) pursue structural reform;

(3) ensure responsible fiscal policy.

• Key developments: The tailwinds that have supported the economy are fading and there are increasing risks to the outlook. Structural reforms remain incomplete in many Member States. High levels of inequality reduce the output of the economy and the potential for sustainable growth.

European Semester 2017

• further streamlining and new features:

• longer-term view of the progress made and the challenges ahead, given that reform priorities are often decided at the start of a new government’s term and that implementing comprehensive structural reforms may take years;

• focus on sequencing of reforms and due attention to distributional impacts (population groups, firms, regions, ...);

• for the first time, a multi-annual assessment of the implementation of country-specific recommendations in the CR;

• further increase the ownership of the reform agenda, including through strengthened dialogue with the MS at technical and political level, consultation on draft reports and stronger policy coordination at MS level, involving the social partners in the design and implementation of reforms.

Outline

1. Background: Annual Growth Survey and 2015 CSRs

2. Economic performance and main challenges

3. Implementation of country-specific recommendations

4. Key messages

1. Cost competitiveness 2. Education, skills, research

3. Digital skills and ICT 4. Business environment

5. Taxation 6. Public investment and infrastructure

7. Corporate governance 8. Judicial system

9. Public administration 10. Public procurement

5. Conclusions

6

Ec. performance and main challenges

• Recovery from the economic crisis is steady, based on strong consumption and moderate investment growth. The European economy has proven resilient against increasing risks. Yet, sustainability of the recovery depends on effective implementation of reforms.

Source: European Commission (2016), report on Competitiveness and Single Market Integration in the EU

Source: European Commission (2017), Winter Forecast • Fiscal policy needs to be

oriented towards policies that improve medium-term growth.

• Structural reforms to provide enabling conditions for investment, boost labour force participation, promote a better business environment, foster innovation, increase dynamic in product and services markets and address inequalities.

7

Investment trends and challenges

• Investment has returned to pre-crisis growth rates. Despite these recent improvements, persistent weaknesses in investment.

• Low demand growth and expectations of weak potential growth hold back a more sustained investment recovery.

• While having one of the highest investment ratios in the EU, the quality of public investment remains an issue in Romania.

Gross fixed capital formation, 2005-2018

• FDI inflows and trade integration remain low. Only 13% of European SMEs participate in international trade, despite support measures.

• Investment in intangibles is improving at low levels. Structural issues account for increasing heterogeneity and subdued performance of total factor productivity which in turn hold back investment.

• Need to increase investment in knowledge-based capital, in line with circular economy principles and strengthen public-private cooperation.

• Investment barriers remaining.

Source: 2017 CR

Outline

1. Background: Annual Growth Survey and 2015 CSRs

2. Economic performance and main challenges

3. Implementation of country-specific recommendations

4. Key messages

1. Cost competitiveness 2. Education, skills, research

3. Digital skills and ICT 4. Business environment

5. Taxation 6. Public investment and infrastructure

7. Corporate governance 8. Judicial system

9. Public administration 10. Public procurement

5. Conclusions

CSR implementation: overall

• strong variation in pace and depth of implementation of reforms in MS

• particularly encouraging progress in the area of financial sector and labour market policy

• more varied progress in improving the business environment and boosting investment

• least progress in opening product and services markets and addressing social exclusion

• available EU funds under MFF are used by MS to prepare and implement structural reforms; closer link between funds and structural reform through targeted investment and ex-ante conditionalities that help improve the overall investment environment; additional support available from new Structural Reform Support Service

CSR implementation: overall (cont.)

• importance of clear commitment and appropriate sequencing of reforms and close involvement of social partners and local/regional stakeholders in their evidence-based design and implementation;

• distributional effects have to be taken into account in the planning and sequencing of structural reforms;

• reforms that help more evenly spread productivity growth across firms, sectors and regions can help increase wages and incomes, foster convergence and reduce inequalities and thereby complement redistributive policies;

• wide array of reforms needed to tackle investment barriers (business environment, public administration, regulatory predictability, skill shortages, access to finance, rule of law)

• good practices (incl. RO: competitiveness strategy, tax exemptions)

CSR implementation: Romania

• CSR 1: (fiscal and financial stability)

• CSR 2: (employment agencies, minimum wages, early- school leaving, pension age)

• CSR 3: (healthcare; public administration reform; simplification; corporate governance)

Simplify administrative procedures for business and the public.

• CSR 4: (integrated public services, infrastructure and economic diversification in particular in rural areas; Transport Master Plan; public investment)

Strengthen public investment project prioritisation and preparation.

• multi-annual assessment of CSR implementation

Outline

1. Background: Annual Growth Survey and 2015 CSRs

2. Economic performance and main challenges

3. Implementation of country-specific recommendations

4. Key messages

1. Cost competitiveness 2. Education, skills, research

3. Digital skills and ICT 4. Business environment

5. Taxation 6. Public investm. and infrastructure

7. Corporate governance 8. Judicial system

9. Public administration 10. Public procurement

5. Conclusions

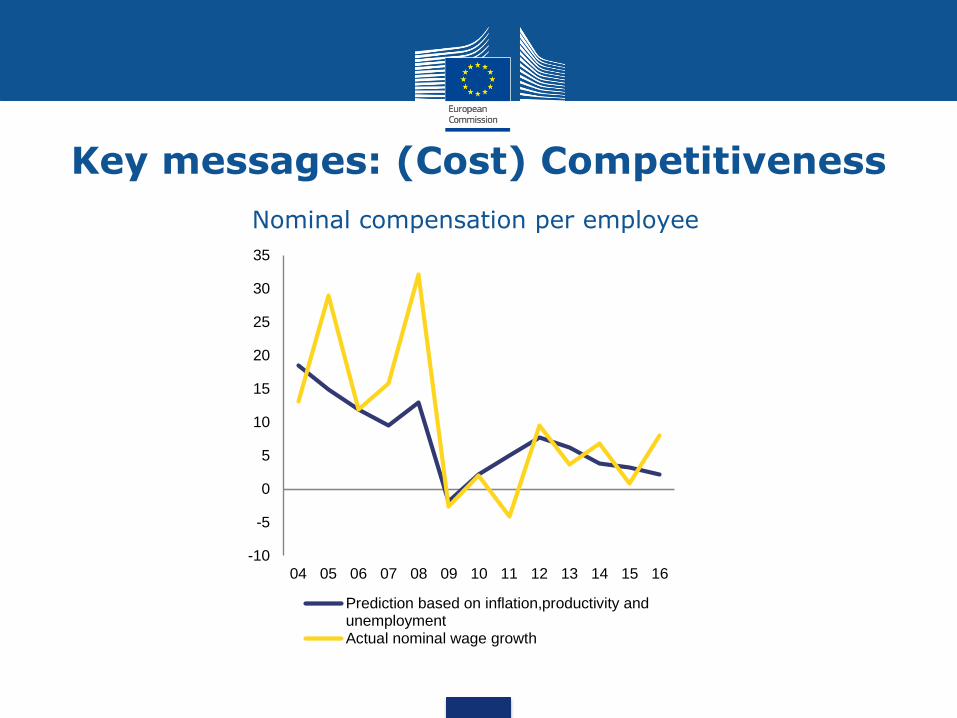

Key messages: (Cost) Competitiveness

• risks with regard to cost competitiveness

• cost competitiveness has been the main contributor to strong export performance, albeit at declining pace;

• traditional export sectors are losing market shares;

• public-sector wage adjustments are leading changes in wages in the tradable sector; these spillovers from the non-tradable to the tradable sector may weaken external competitiveness;

• a predictable wage-setting process for public and minimum wages would help avoid adverse effects on competitiveness.

Key messages: (Cost) Competitiveness

Nominal compensation per employee

-10

-5

0

5

10

15

20

25

30

35

04 05 06 07 08 09 10 11 12 13 14 15 16

Prediction based on inflation,productivity andunemploymentActual nominal wage growth

Key messages: Education, skills, research

• skill-biased sectoral shift, typical of a transition economy;

• skill shortages and difficulties with retaining higher-skilled employees in fast-growing sectors are a challenge to growth;

• low public expenditure on and unequal provision of quality education, underachievement in basic skills, low digital skills in the population, high early school leaving, under-developed vocational education and training systems, low tertiary attainment and very low participation in lifelong learning;

• despite some progress, the quality and labour market relevance of tertiary education remains a challenge, and progress in vocational education and training is insufficient to meet labour market needs.

• very high inactivity rates, high share of young NEETs

Key messages: Digital skills and ICT

• Companies' low level of digitisation is constraining productivity improvements;

• workforce's digital skills are one of the lowest in the EU: despite the existence of many skilled ICT specialists, the general workforce lacks digital skills;

• Broadband networks are underdeveloped in rural areas, with risk of digital exclusion while Romania is one of the world's leading countries in terms of internet speed.

Key messages: Digital skills and ICT

Digital intensity score for enterprises

Key messages: Digital skills and ICT

Digital intensity score for enterprises

Key messages: Digital skills and ICT

Digital intensity score for enterprises

Key messages: Inequality

• persisting high income inequality: Romania has one of the highest, and rising, levels of income inequality in the EU and rising; market income inequality has been stable; decreasing redistributive effects of the tax and transfer system

• unequal access to education and services

Key messages: Inequality

GDP per capita in PPS in 2015 vs income quintile ratio (S80/S20)

Key messages: Business environment

• improving business environment yet weaknesses remain: infrastructure, administrative burden, labour market, health, education, corruption and governance issues in the public sector;

• ongoing simplification of administrative procedures for business and the public are being simplified;

• modern e-government solutions remain largely untapped; e-commerce remains under-developed;

• access to finance is expected to improve with a set of new financial instruments: ongoing work to set up a national promotional bank

Key messages: Business environment

SBA profile 2016

Key messages: Business environment

Global Competitiveness Index, 2010 and 2016

Key messages: Taxation

• overall structure of the tax system is favourable to economic growth; tax revenues depend to a larger extent on consumption taxes and to a lesser extent on taxes on corporate income and on labour;

• relatively low impact of the tax and benefit system on reducing income inequality, and low difference between market income inequality and disposable income inequality; reduced VAT rates are not the most efficient instrument for decreasing income inequalities

• high incidence of undeclared work, representing 15-20 % of GDP; unfocused, insufficient preventive measures;

• low tax compliance and largest, increasing VAT gap despite a good economic environment and the introduction of anti-fraud measures;

Public investment and infrastructure

• high but inefficient public investment spending; despite overall improvements in performance, RO ranks last in the EU in the perceived quality of infrastructure; high administrative burdens and low provision of e-government services weigh on growth and productivity;

• poor infrastructure is a key factor constraining growth and competitiveness, and it exacerbates regional disparities and inclusion problems;

• measures to improve investments in the transport sector;

• stronger absorption of EU funds could improve infrastructure spending, based on improved governance, removing public procurement delays and bureaucratic obstacles, and improving beneficiaries' capacity to prepare and deliver high-quality projects.

Key messages: Infrastructure

Global Competitiveness Index, 2010 and 2016

Key messages: Infrastructure

Public investment spending and quality of infrastructure

Key messages: Corporate governance

• SOEs are not on as firm a financial footing as their private-sector counterparts as they have higher debt ratios and lower profitability than their private sector counterparts;

• despite negative operational results in 2015 and 2016, the restructuring of loss-making SOEs has not advanced; the privatization agenda has not yet started moving forward;

• legislation on improving corporate governance was adopted and the law and its implementing legislation follow good international practices in ensuring transparency in the appointment of board members and the management of SOEs; the Ministry of Finance has greater powers to monitor how legislation is being implemented and companies' performance.

Key messages: Judicial system • substantial progress on the reform of the judicial system and

investigation of high-level corruption; efforts are still required as regards judicial independence in public life, finalising reforms of the criminal and civil codes and ensuring efficiency in the implementation of court decisions and of preventive policies; irreversibility of progress made is key;

• higher efficiency of courts yet no action to address the problem of non-enforcement of final court decisions;

• limited progress on improving insolvency procedures; time to conclude procedures is among the longest in the EU;

• e-commerce solutions remain under-developed due to a lack of enforcement of consumer protection;

• further measures to fight against corruption, in particular at local government, yet corruption persists at all levels.

Key messages: Public administration

• public administration reform accelerated in 2016, but is not yet complete; measures to strengthen transparency and take proper account of consultations with the relevant authorities and stakeholders in decision-making and legislative activities; civil service and staff training strategies were adopted but implementation hinges on legislative amendments and a proper institutional set-up;

• slow progress in public administration reform hinders the delivery of structural reforms; incomplete human resources reforms limit public institutions' capacity to develop and implement policies in a strategic and coordinated manner;

• strategic planning and regulatory impact assessment instruments are not systematically used; parliamentary legislative initiatives are not subject to budgetary impact analysis.

Key messages: Public procurement

• progress in public procurement reform: implementation of the public procurement strategy and action plan progressed in 2016; adoption of law for the PREVENT system for systematic ex-ante checks of conflicts of interests and set-up of the National Agency for Public Procurement (ANAP) for robust and efficient corruption control and preventive institutional mechanisms; set-up of an inter-ministerial committee for public procurement to ensure the overall coherence of the public procurement system;

• several measures are still outstanding: web-based guidelines to help contracting authorities during the procurement process are still under development;

• little strategic use of procurement.

Outline

1. Background: Annual Growth Survey and 2015 CSRs

2. Economic performance and main challenges

3. Implementation of country-specific recommendations

4. Key messages

1. Cost competitiveness 2. Education, skills, research

3. Digital skills and ICT 4. Business environment

5. Taxation 6. Public investment and infrastructure

7. Corporate governance 8. Judicial system

9. Public administration 10. Public procurement

5. Conclusions

Conclusions

Ease-of-doing busines indicators and structural reforms, 2010-2016

Thank you for your attention.

Vă multumesc

pentru atenție.

Merci de votre attention.

Vielen Dank für Ihre Aufmerksamkeit.

http://ec.europa.eu/about/juncker-commission

http://ec.europa.eu/growth/about-us/index_en.htm

36

ULC EX (change) TFP (change) TRADE INT. DB 2016 GCI 2015/16 REER (HICP) WGI (gov. eff.) GTCI

Romania Lithuania Latvia Slovakia Denmark Germany United Kingdom Finland Luxembourg

Ireland Romania Ireland Czech Republic United Kingdom Netherlands Ireland Netherlands Denmark

Greece Luxembourg Romania Hungary Sweden Finland Hungary Denmark Sweden

Croatia Bulgaria Slovakia Belgium Finland Sweden Portugal Sweden United Kingdom

Portugal Latvia Lithuania Estonia Germany United Kingdom Germany Germany Finland

Cyprus Estonia Slovenia Slovenia Estonia Denmark France Luxembourg Netherlands

Luxembourg Slovakia Malta Netherlands Ireland Belgium Sweden United Kingdom Germany

Spain Poland United Kingdom Lithuania Lithuania Luxembourg Netherlands Ireland Austria

Hungary Portugal Germany Latvia Austria France Denmark Austria Ireland

Slovenia Ireland Spain Bulgaria Latvia Austria Greece Belgium Belgium

United Kingdom Czech Republic Estonia Austria Portugal Ireland Cyprus France Czech Republic

Poland Slovenia Czech Republic Poland Poland Estonia Poland Spain Estonia

Czech Republic Malta Hungary Luxembourg France Czech Republic Italy Cyprus France

Denmark Spain Netherlands Malta Netherlands Spain Austria Estonia Slovenia

Italy United Kingdom Sweden Romania Slovak Republic Lithuania Croatia Malta Slovakia

Finland Germany Poland Ireland Slovenia Portugal Belgium Czech Republic Malta

Malta Netherlands Denmark Croatia Spain Poland Spain Portugal Latvia

Slovakia France France Portugal Czech Republic Italy Malta Slovenia Hungary

Belgium Belgium Belgium Germany Romania Latvia Finland Lithuania Cyprus

France Greece Bulgaria Denmark Bulgaria Malta Slovenia Latvia Portugal

Germany Italy Portugal Sweden Croatia Romania Luxembourg Slovakia Lithuania

Austria Austria Luxembourg Finland Hungary Bulgaria Romania Poland Spain

Netherlands Hungary Austria Spain Belgium Slovenia Czech Republic Croatia Poland

Latvia Denmark Croatia France Italy Hungary Lithuania Hungary Italy

Lithuania Croatia Italy Italy Cyprus Cyprus Estonia Greece Croatia

Sweden Sweden Finland Cyprus Greece Slovakia Bulgaria Italy Bulgaria

Estonia Finland Cyprus United Kingdom Luxembourg Croatia Latvia Bulgaria Greece

Bulgaria Cyprus Greece Greece Malta Greece Slovakia Romania Romania