Embed Size (px)

DESCRIPTION

Citation preview

Later Life 2011

National and International Trends

Prepared by Age UK Research Department

Overview

Demographics and population trends

Health and wellbeing

Money matters

Home and care

Public policy challenges

Opportunities for enterprise

Demographics and Population Trends

Ageing in the UK

TODAY

– 10 million aged over 65

– 1.3 million aged over 85

– 11,000 aged over 100

THE FUTURE

– 12.5 million over-65s by 2020, 16 million by 2030

– Fastest growth post-85

– 250,000 aged over 100 by 2050

UK population pyramid (mid-2009 estimate)

Source: ONS 2010

Ageing of the UK population

Source: ONS 2010

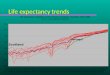

“At current rates, life expectancy in the UK is increasing at the rate of about two years for each decade that passes”

Source: House of Lords Science and Technology Committee 2005

Ageing: Scientific Aspects

Life Expectancy at birth (UK)

Life expectancy at birth (UK)

1980 2000 2010

Males 70.8 75.3 77.9

Females 76.9 80.182.0

(Source: World Bank Development Indicators 20 Nov 09 and ONS Oct 2010)

Life Expectancy at Birth 1980-82 to 2006-08

(Source: ONS 2010)

Ageing - Internationally

Across EU population growth over next 25 years:

– 81% over-60s

– 7% 18-59 year olds

Across the world, by 2050 people over 60 will make up

– 1/3 of rich world

– 1/5 of developing world

Global Population – Aged 80+ years

1950 – 14 million

Today – 300 million

Longevity Revolution - Global

Source: WHO 2010

12.4

16.0

16.0

16.4

16.4

16.5

16.7

16.9

17.0

17.1

17.2

17.3

17.8

18.6

19.5

19.5

United States

Finland

United Kingdom

France

Croatia

Latvia

Estonia

Spain

Portugal

Belgium

Bulgaria

Sweden

Greece

Germany

Italy

Japan

Source: Haub C, 2006; World Population Data Sheet

The World’s 15 ‘Oldest’ Countries (%65+)

“The number of centenarians in Japan increased almost one-hundredfold from 154

in 1963 to more than 13,000 at the beginning of this century and is projected to increase to

almost 1,000,000 by 2050”

Ageing Horizons, 3,1 (2005)

Longevity Revolution - Japan

Italy – population pyramids

15 10 5 0 5 10 1515 10 5 0 5 10 1515 10 5 0 5 10 15

1950 2000

Male Female Male Female

Age

Source: World Population Prospects: The 2004 Revision (2005).

China – population pyramids(millions, by age and sex)

80+ 75-79 70-74 65-69 60-64 55-59 50-54 45-49 40-44 35-39 30-34 25-29 20-24 15-19 10-14

5-90-4

Age

2050

Female

80+ 75-79 70-74 65-69 60-64 55-59 50-54 45-49 40-44 35-39 30-34 25-29 20-24 15-19 10-14

5-90-4

Male

Life Expectancy and Development

0 10,000 20,000 30,000 40,000

40

50

60

70

80

life

expe

ctan

cy, 2

000

gdp per capita, 2000, current PPP $

USA

Japan

Germany

FranceItaly

UK

Spain

Korea

Argentina

South Africa

Equatorial Guinea

Mexico

Russia

Brazil

Botswana

Namibia

Gabon

China

India

Indonesia

Pakistan

Bangladesh

Nigeria

Later life in the UK- an overview

Over 1.3 million people are aged 85 or over. One in four children born today will live to 100

People aged 65 now have an average life expectancy of 82-85 years, the last 7-9 years with a disability

Nearly 2.5 million people aged 65+ in England have care needs

3.7 million people aged 65+ currently live alone

821,000 people aged 65+ currently have dementia. is This is projected to double in less than 40 years

Later Life – internationally: an overview Of the current total world population of over 6.8 billion, there are over 790 million people aged 60 and over

Life expectancy at birth ranges from 82.6 years in Japan to 39.6 years in Swaziland

70% of the world’s older people (60+) live in less developed countries

60% of people with dementia live in developing countries, and this is expected to rise to 71% by 2040

70% of mortality in low income countries is due to communicable disease and 30% to chronic long term illness; this will be reversed by 2030

Health and wellbeing

While health is clearly an outcome in itself, it is also a key driver of outcomes in other domains, including employment and ability to contribute

ELSA (Wave 2, 2006) indicates the two-way relationship between health and wealth: greater financial resources reduce the chances of poor health, and good health has a positive relationship to financial wellbeing

• Services are hospital focused, prioritising cure rather than prevention or complex case management, commissioning is in early stages of development, question marks over value for money, realisation that some target-driven achievements occurred at the expense of quality.

• National priorities remain but emphasis on local decision making• Choice as a patient right and a tool to drive up quality along with

contestability between providers for contracts framed by ambition to provide care closer to home

In eight years’ time, demographic change alone would mean that there would be:

• Nearly 2.7 million people aged 75+ with at least one limiting long term illness and over 4.3 million people aged 65+ with LLTI

• People living an average of 7-9 years at the end of their lives with a disability

• Nearly seven million older people who cannot walk up one flight of stairs without resting

• One-and-a-half million older people who cannot see well enough to recognise a friend across a road

• Over 4 million with major hearing problems • Up to a third of a million people aged 75+ with dual sensory loss• A third of a million who have difficulty bathing• Nearly a million with dementia• Between 4-7 million with urinary incontinence • One-and-a-half million suffering from depression

Why is this important? Policy

TrendsWhat do older people think?• Mental health – older people’s preference for services include peer

support; a range of activities and opportunities of things to do; 24-hour help in a crisis that helps you maintain everyday life; supported housing options, technologies and skills and learning opportunities that enable independent living. More broadly older people suggest the following to improve mental health and wellbeing: improve public attitudes; provision of activities for older people; befriending schemes (esp. those aged 90+); improved access to quality public services, and improving standard of living (mostly younger respondents).

• Community Services –priority areas for action include: improving the range of support for carers; making services personalised and holistic; joining up health and social care so there is one point of call; considering the transport implications of any changes to services

• Intermediate care – help with keeping out of long term care is important e.g. mentoring and advocacy to help them through the health and social care system; more time from care assistants; more availability and affordability of high quality home and telecare; help with practical matters such as laundry, adequate refreshments and warmth.

Prevention package

Mental health – new horizons

Quality accounts

New regulatory system

Personal health budgets

Dementia strategy

Stroke strategy

End of life care strategy

Primary care strategy

Transforming community servicesLINks and local accountability Physical activity strategyPOPPSWorld class commissioning

HEALTH

Long Term Health Conditions: The Strategic Challenge

There are over 15 million people in England with long-term health needs.

Long term conditions are those that cannot, at present, be cured, but can be controlled by medication and other therapies.

The impact on the NHS and social care for supporting people with long term conditions is significant.

Currently 69% of the total health and social care spend in England is spent on the treatment and care of people with long term conditions (DoH 2008).

By 2025 the number of people will at least one long term condition will rise by 3 million to 18 million (DoH 2008).

This will be due to a rise in the ageing population and the increased survival of pre-term babies.

Coronary Heart Disease – 2.6 million people are living with CHD in the UK (89% of 190,000 deaths per year were in people 65 years or older)

Stroke – 80% of 150,000 cases per year are over 65. Stroke is the leading cause of severe adult disability

Diabetes – 2 million people in the UK are diagnosed. Prevalence rises with age from one in 20 people over age of 65 to one in five in people over 85 years

Chronic Lung Disease – 766,000 people in the UK diagnosed. In 2004 there were 10,740 deaths – 92% occurred in people 65 years and older

Prevalence of Long Term Conditions (1)

Cancer – incidence increases with age – of the 135,000 deaths in 2004, three quarters occurred in people aged 65 and over.

Arthritis – Osteoarthritis affects about 60% of men and 70% of women aged over 65.

Osteoporosis – Up to 14,000 people die following osteoporotic hip fractures each year in the UK.

Parkinson’s Disease – The second most common neuro-degenerative disorder (120,000 have clinical diagnosis). The incidence increases with age.

Sensory impairments - 2 million people in the UK have a sight problem. Of these, 1 in 10 people over 75 years and 1 in 3 over 90 years has a significant visual impairment. Over 6 million people over 60 years are deaf or hard of hearing.

Prevalence of Long Term Conditions (2)

Prevalence of Long Term Conditions (3)

Depression – The commonest mental health condition in the older population. A quarter of older people living in the community have symptoms which warrant intervention. Around half of these meet the clinical criteria for a diagnosis of depression.

Dementia – Over 820,000 people are estimated to be suffering from late onset dementia in the UK. This overall figure is forecast to increase to 1,735,087 by 2051. Dementia affects 1 person in 6 over 80 and 1 in 3 over 95.

%Dependent

Disability, age and ADL

Older people and functional limitations

37% of men and 40% of women aged 65 and over have at least one functional limitation (seeing, hearing, communication, walking, or using stairs).

This increases to 57% and 65% respectively in those aged 85 and over.

More than half of men and women reporting any functional disability were unable to walk 200 yards or more unaided without stopping or discomfort. Both prevalence and severity increased with age.

The number of functional limitations also increased with age with 17% of men and 19% of women aged 85 and over with three or more functional limitations.

Functional limitations can result in depression and social isolation.

Severe Cognitive Limitation by Age and Gender (US)

0%

5%

10%

15%

20%

25%

51-54 55-59 60-64 65-69 70-74 75-79 80-84 85+

Age

Pe

rce

nt

Males

Females

Total

Healthy Life Expectancy

Life expectancy is increasing and until recently, healthy life expectancy has been increasing at a slower rate

This has meant that many older people are living longer in poor health

There is evidence of some success in compressing morbidity and evidence that disability rates are declining

Work and Learning

05

1015202530354045

Pe

rce

nta

ge

45-54

55-64

65-74

75+

2005

2005

2005

2005

2005

2006

2006

2006

2006

2006

0%

10%

20%

30%

40%

50%

60%

70%

80%

16-49 50-64 65-79 80+ 50+

2005 2006

All those who want to work, need to be in work – however older workers are particularly disadvantaged by lack of educational qualifications - employment rates are significantly lower for those with no qualifications whatsoeverMental activity like learning can also slow cognitive decline reduce morbidity and facilitate healthier lives

• Lack of interest and feeling too old are the man barriers to learning as people get older.

The number of people undertaking learning decreases significantly with age

Why is this important? Policy

TrendsWhat do older people think?

• Poor information about availability of learning opportunities and inappropriate courses may explain lack of interest.

• One survey found 43% of older people agree that there is not enough information on what education courses are available and 30% believe courses on offer are not appropriate for older learners

Access to learning centres becomes more difficult with age – with FE colleges, adult education centres and the home being main locations of learning

WORK AND LEARNING

Economic activity by highest qualification, 50-69 y/o

0%

20%

40%

60%

80%

100%

Degree/ equiv

Higher edu

A-Level /equiv

GCSE A*-C/equiv

Other No Qual

Those 50+ with no qualifications experience employment rates over 20% lower than those with qualifications – much of the difference explained by illness or disability

Employed

Unemployed

Inactive: sick or disabled

Inactive: Other

Inactive: looking after family/home

Inactive: Retired

•Flexible New Deal; •Train to Gain programmes;•Pathways to work;•Extending Working Life proposals; •Age Positive initiative on employer attitudes•Digital inclusion strategy•Informal adult learning white paper though funding largely focused • on skilling “adults of working age” up for joining/re-joining the • workforce

• Employment supports an individual’s ability to contribute in addition to their material wellbeing (ELSA Wave 3 presentation, Banks and Tetlow 2008).

• All those who want to work need to be in work – and work needs to be promoted as a mechanism for achieving wellbeing and independence in later life

• In line with other OECD countries, Britain has adopted Active Labour Market Policies (ALMPs) to combat unemployment and economic inactivity.Government initiatives have generally been designed to combat :

• Youth unemployment, particularly longer-term unemployment (e.g. Future Jobs Fund announced in 2009 Budget) and

• the high cost of unemployment benefits (Welfare Reform)• Incentives to stay at work likely to increase (ELSA Wave 3)

Why is this important? Policy

TrendsWhat do older people think?

More people enjoy work:

• The majority of those aged 55 and over would prefer to be working full time than not working at all, and it is common for older people to view working as the ‘ideal’ situation for them

… and want to keep working

A 2003 survey found over two-thirds of respondents aged between 50-70 who were in, or looking for, a job planned to work in some capacity during retirement or never retire

• The average age at which workers over 50 retired reached its highest level for men (64.6 years) since 1984. For women comparable figures showed an increase from 60.7 in 1984 to 61.9 in 2008.

• The employment rate of those over SPA remains relatively small at 8.8% (Nov 2010), although those between 50-State Pension Age have closed the employment rate gap on the 16-SPA group by 5.3% since 1993.

• ELSA respondents report increasing expectation of working longer• Increasing the female SPA may also lead to higher employment rates• According to the latest LMO survey (Summer 2009), employers say

they are more likely to recruit 19–24-year-olds (63%) and older workers (60%).

• Employment rates of people aged above SPA vary considerably between regions (range of 8.8% up to 14.3%)

• Poor health, absence of qualifications, and caring responsibilities are key barriers to employment, and these barriers can interact with each other

• Redundancy rates during the recession have increased more slowly in the 50+ age group than any other.

• The impact of projected pension shortfalls on the timing of retirement is not yet clear, but concern about financial security is likely to bring about a further rise in working post SPA.

EMPLOYMENT

Money Matters

• An individual’s income clearly supports their material wellbeing. • It also enables independent living and appropriate housing• ELSA (2006 and 2008) provides strong evidence of a positive

correlation between higher income/ wealth and reduced risk of developing most of the age-related chronic conditions, including type 2 diabetes, high blood pressure, raised cholesterol, disability (reduced strength and mobility)

• Currently developments led by market not by Government policy• Pension reform, including introduction of auto enrolment from • 2012 (DWP developing 10 yr pension communication strategy)• Money guidance service being developed following Throresen

review • Range of govt info services including ageing strategy, one-stop-

shop and increased collaboration with Third Sector, but unclear how these link up

• Financial services sector doesn’t understand what opportunities are available for them in care funding/equity release/advice

• Need for Govt. to oversee private financial industry solutions

Why is this important? Policy

TrendsWhat do older people think?• Confusion regarding choices of pensions, savings and care• Lack of interest in accessing products online• Concern about pensions (55-65 year-olds currently finding out that

their pensions will not be adequate):

• Increasing reliance on private sector, complexity in products on offer

• Individual exposure to risk – more individuals are directly exposed: a significant percentage of 50-65 year olds are in danger of having replacement rates below benchmarks of adequacy

• Increase in need for info. and advice to access entitlements and make appropriate decisions about finances

• Increasing use of websites as main channel rather than (more expensive) face to face (although Pension Service home visits)

• Digital exclusion now leading to increase in financial exclusion, not just in banking, but increasingly public services and private care funding (poor risks?)

• Greater exposure to financial abuse• Gaps in support for frail vulnerable older people especially

around money management.

INCOME

0%

10%

20%

30%

40%

50%

Pensionparticipation

Pensionincome

+ All non-pensionfinancialwealth

liquidated

+ Half ofhousingwealth

liquidated

+ Allanticipated

inheritancesliquidated

Final report

1st report

(Turner Final Report 2006)

Health and financial status

1.8 million pensioners live in poverty. Nearly two-thirds of these are women.

Older people on higher incomes are more likely to report their health as ‘good’ or ‘very good’.

People on lower incomes are more likely to report asthma, chronic lung disease and diabetes. High blood pressure is more common among poorer older people.

Wealth and health

Net Worth by Health of Husband and Wife

Excel

lent

V Goo

d

GoodFai

r

Poor

Poor

Fair

Good

V GoodExcellent

050

100150200250300350400450

Ne

t W

ort

h(i

n T

ho

us

an

ds

)

Wife's Health

Husband's Health

Pension coverage in UK

0

20

40

60

80

100

Earnings

Per

cent

age

Occupational pension Both Personal pension No private pension

11.2

6.6

6.2

4.8

4.7

4.4

4.0

3.8

3.7

3.7

3.5

2.4

1.9

1.9

-0.5

3.2

-5 0 5 10 15

GreeceSpain

NetherlandsGermany

FinlandIreland

PortugalAustriaFrance

BelgiumDenmarkSweden

LuxembourgItalyUK

EU

Forecast change in public pension spending 2000–2040 (%)

0

0.25

0.5

0.75

1

50 55 60 65 70

Age

Su

rviv

al p

rob

abil

ity

UK men

No Occupational Pension

With Occupational Pension

Do Pension Incentives Matter?Survival probabilities, by pension status

UK women

No Occupational Pension

With Occupational Pension

Survival probabilities, by pension status

0

0.25

0.5

0.75

1

50 55 60 65 70

Age

Su

rviv

al

pro

ba

bil

ity

Home and Care

• Decent and appropriate housing is a key element in quality of life and good health in older age

• Demographic changes, combined with changes in policy on care provision and home ownership have meant - and will continue to mean - an increasing number of the oldest old living longer, and often alone, in their own homes

• Older people (especially single people aged 75+) are more likely to live in older, non-decent homes (English House Condition Survey, 2009)

Why is this important? Policy

TrendsWhat do older people think?• 92% of adults say they envisage living in a home they have for life,

but 23% said their current home was unsuitable to live in in old age (B&Q survey, 2008)

• More older people refusing to purchase preventative services to save money as the result of increased 'choice' and rising charges

• Opinions sharply divided between those who benefit from Assistive Technology and those who see reduced contact with 'human' support

• Concern about inheritance tax is not necessarily exclusive to the very rich. ELSA (Wave 3, Emmerson Muriel 2008) found that 1 in 8 of their representative 50+ sample have assets above the IHT threshold

• Whatever the merits of residential in comparison with living in the community, over 70% of adults surveyed view it negatively: 48% of homeowners 18+ say they can’t think of anything worse than moving into a care home.

• A further 14% say they would be nervous and 9% frightened (B&Q survey 2008)

• 5% of people aged 65+ in the UK need but do not receive help with everyday jobs such as hoovering or changing a light bulb

• Continued push on homeownership - experience of Right to Buy generation unable to maintain housing should provide lessons

• Growth in need for local housing advice and advocacy – opportunities for one-stop shop services

• Growing inequality of retirement provision between private and public sectors• Growing regional and local inequality in regard to poor housing

Expansion in private rented sector - more older people living in insecure tenancies

• Increasingly difficult to obtain additional resources from PCTs • Housing support and service charges - growing divide between

those receiving benefits and those paying for themselves - likely to increase friction within retirement housing

• Likely increase in numbers of older homeless people resettled in poor temporary accommodation

• Public sector will focus on the most vulnerable • Possible further decline in specialist housing. Growing debate

around mobility (moving to be nearer friends and relatives offering support) and flexibility within social rented sector

HOUSING

• Government encouraging institutional investment more in private rented sector to make up the shortfall in social housing.

• Growing debate around reconciling housing related support, social care and health services to deliver independence at home (role of common assessment framework)• Cuts in preventative services - housing related support - more

funding diverted to social care Further decline in retirement housing in the social sector - increased focus on the most vulnerable

• Reforms to security of tenure (see Hills report) possibly less security for both private and social residents – issue around offering settled

accommodation to older people • Calls for improved coordination - partnership with LAs and PCTs

increasing focus on the role of retirement communities - some growth

• Increasing push towards assistive technology to replace or reduce housing support workers - increased pressure to cut labour costs

through assistive technology but likely to remain marginal for next 5-10 years (except top end of market)

Health and Home The majority of older people live within the

community.

26% of households with someone aged over 75 live in social housing and 68% are home owners.

5% of older households live in sheltered housing

5% of older people live in a care home.

Poor housing has a detrimental impact on both physical and mental health.

2.7 million households with at least one person aged over 60 are living in a non-decent home.

Older people are more likely to be living in non-decent homes in the private sector if they are over 75, aged 60 or more and living alone.

60% of women aged 75 and over live alone compared to 36% of men of the same age.

Care and support at home There are 6 million carers in the UK.

2.8 million people aged 50 and over provide unpaid care; nearly 1 million of these are aged 65+ and nearly 50,000 are aged 85+.

There are 8,000 carers aged 90+ (4000 providing 50+ hours of care per week.

Unpaid carers currently provide 65% of care compared to 25% paid for by the state (10% is privately purchased).

73% of English local authorities have plans to limit care to people with substantial and critical needs only.

The growing number of older people means that the need for support from unpaid carers could rise by 30% over the next 35 years (9.1 million).

Empowering older people with supported self-care

Older people and their carers want services that will:

– improve their quality of life, health and well-being and enable them to be more independent.

– Be supported and enable them to self care and have active involvement in decisions about their care and support.

– To have choice and control – services built around the needs of individuals and carers.

The 2006 White Paper Our health, our care, our say, promoted telecare and assistive technology in helping people retain their independence and improve their quality of life.

The use of the internet by older people, particularly over 75s has increased (from 14% to 27%), many older people continue to be excluded from the benefits of new technologies (Age Agenda 2008, Age Concern).

As people age, the risk of being lonely increases

For details of trends in volunteering and digital inclusion, see Appendix

0

10

20

30

40

50

No social exclusion Temporary socialexclusion

Persistent socialexclusion

Mean

Qu

ality

of

Lif

e S

co

re

Pleasure

Self-realisation

Autonomy

Control

Social isolation prevents ability to contribute. It also is a risk factor for health.

Inactivity and isolation accelerate physical and psychological declines, creating a negative spiral towards premature, preventable ill health and dependency. A recent ELSA study revealed that social detachment reduces quality of life.

Depression is associated with lack of social support (36% of men and 54% of women with severe lack of social support have high depressive symptoms)

Social isolation is a cross-cutting issue and the responsibility for alleviating it lies with several Government departments. Policies which may directly impact on social isolation are fragmented but include:

•Linkage Plus aimed to improve outcomes for older people through better joining-up between services and linking older people to services.•Developments in transport policy including making the freedom pass available, amending community transport regulations and •Investment of £5.5 mil into intergenerational volunteering•Individual budgets for those that access social care•Positive duty as applied to culture and leisure opportunities •Lifetime neighbourhoods•Neighbourhood warden schemes•Informal learning white paper

• 29% of respondents to an Age Concern survey saw friends and 36% saw family a few times and month or less

• However many people at mid- to later life may not consider they need to expand their social networks

• 44% state they do not need lots of friends

• 45% disagreed that they feel lonely from time to time

• Analysis of ELSA wave 3 has found that life satisfaction significantly decreases after certain life events, with many underlying factors clustering around themes of social isolation and lack of support.

One person households are projected to overtake married couple households by 2030

226,000

797,000

923,000

834,000

947,000

1,061,000

1,659,000

254,000

1,048,000

1,460,000

1,415,000

1,792,000

1,559,000

2,359,000

0 500,000 1,000,000 1,500,000 2,000,000 2,500,000

Under 25

25 - 34

35 - 44

45 - 54

55 - 64

65 - 74

75 and over

2026

2003

Why is this important? Policy

What do older people think?

Satisfaction with current levels of social interaction could be a barrier to individuals building up social networks

TrendsSOCIAL INCLUSION

Public Policy Challenges

Long term challenges

A decade of spending cuts – doing more with less?

Demographic change – a manageable transition (working longer; pensions reform) but we must now prepare our public services

Income – pensioner poverty stuck around 20% for the next decade despite pension reform

Healthy life expectancy - remains an elusive goal, avoid longer periods of disability

Social and technological change – changes in family life, communities and the digital divide – what next?

2011: Uncertainty and Opportunity

UNCERTAINTY Older people not immune from

the recession

– Job losses hitting older workers

– Rising costs of living

– Impact on savings and annuities

Now - a focus on employment and skills; an end to forced retirement

The aftermath – public service cuts must not disproportionately harm older people

OPPORTUNITY A new ageing strategy

Social care reform - 2011 is ‘make or break’ for the long term

The Equality Bill – new rights outside work; end forced retirement?

Pensioner poverty – Child poverty Bill focuses minds on ending pensioner poverty

Coalition pressing older people’s priorities

Equal citizens, equal rights

PROPOSALS

1. Use Equality Bill to outlaw age

discrimination in goods and

services, rapidly and with minimal

exemptions

2. Support EU directive on

discrimination beyond the workplace

3. Robust enforcement and promotion

of existing age discrimination law

4. Extend Human Rights Act to private

providers of public services

INDICATORS

68% say politicians see older

people as a low priority

60% say age discrimination exists

in older people’s lives

60% say age discrimination exists

in the workplace

53% say people in very old age

are treated like children

52% say those planning services

don’t pay enough attention to

older people

PRIORITY: Outlaw mandatory retirement ages (2010 priority)

Enough Money

PROPOSALS

1. Government commitment to end pensioner poverty

2. Public services work together to push take-up of benefits

3. Index State Pension to earnings now and improve pensions for women who retired before 2010

4. Urgent review of Fuel Poverty Strategy

INDICATORS

16% (AHC) of pensioners in poverty

59-67% of those eligible receive Pension Credit

56% of employees covered by a non-state pension

36% of over-60s avoid heating rooms to save money

7% of 85+ households don’t have a bank account

PRIORITY: Roll out automatic payment of benefits

My life, my care

PROPOSALS

1. Increase investment in preventative support and information, advice and advocacy

2. A fair national system for assessing need and allocating resources

3. A radical new long-term settlement for care and support, which increases access and quality, and is fair and affordable for all

INDICATORS

410,000 people over 65 with unmet need for help around the home

67,000 households receiving low-level home care

347,000 people receiving home care

£60 gap between average weekly fees for a care home and the standard council payment

27,000 people over 65 receiving Direct Payments

PRIORITY: Spend an extra £1-2bn on older people’s care

Staying well and feeling good

PROPOSALS

1. All public services to work to promote lifetime good health

2. NHS reform to reflect older people’s needs and preferences

3. Improve access to primary care for carers and care home residents

4. All health providers to adopt person-centred measures of dignity

5. Age-aware workforce development strategies

INDICATORS

24% of over-65s say quality of life has worsened in the last year

7.3 years for men and 9.4 years for women of future disability at age of 65

19% of 65-74s and 7% of over-75s do recommended levels of exercise

149,000 75+ emergency readmissions within 1 month of discharge

64% say health and care staff don’t always treat older people with dignity

PRIORITY: Re-direct the NHS to prevent and manage common

conditions of ageing

Places to age in

PROPOSALS

1. Local public agencies to commit to ‘lifetime neighbourhoods’ principles

2. Rapid adoption of Lifetime Homes planning standard

3. Review policy and funding for supported housing

4. During recession, anti-crime initiatives for and with older people

INDICATORS

11% of over -65s say they are lonely

35% of 60+ households live in poor housing conditions

26,000 65+ excess winter deaths

9-10% of over 75s find it very difficult to access doctor, post office, supermarket

6% of over-65s leave home once a week or less

PRIORITY: a national ‘offer’ and brand for local older people’s services

Opportunities and contributions

PROPOSALS

1. Employers to adopt flexible working and ‘age management’ policies, with a right to request flexible work.

2. All local public services to facilitate lifelong learning

3. IT industry to embrace accessibility and inclusive design

4. Public bodies to involve diverse groups of older people in decisions affecting them

INDICATORS

76% say the country fails to make good use of older people’s skills and talents

312,000 over-50s unemployed

168,000 over-60s participating in state-funded learning

60% of over-65s have never used the internet

39% of 65-74s and 24% of over 75s participate in formal volunteering at least once a month

PRIORITY: ‘age proof’ employment and skills support during recession

Public Policy at Age UKNATIONAL

COMMUNITY AND SOCIETY

– Income and inequality

– Housing

– Communities and transport

PUBLIC SERVICES

– Health and healthcare

– Independence and support

– Equality and human rights

PRIVATE SECTOR

– Employment and

opportunities

– Consumer markets

– Financial services

LOCAL

Supporting Age Concerns and other

partners influence effectively

National programmes where the key

decisions are local

REGIONAL

Regional teams working with

partners

INTERNATIONAL

EU and international institutions

Partnership with HelpAge

International

Opportunities for enterprise

0

10000

20000

30000

40000

50000

60000

70000

2002 2006 2026 2036

0-15

16-29

30-49

50-59

60-74

75+

'000s

Source: National Statistics 2004

The opportunity…..a large and growing older population

Spending, income and wealth

SPENDING

About £102 billion spent by 65+ households every year

Rich people spend same amount, whatever their age. Poor people in

later life spend less than younger groups with the same income

INCOME

Lower incomes on average, but similar poverty rate

WEALTH

2.2 million with no savings; 3 million with over £20,000

Huge inequalities in wealth, but richer than younger age groups on

average (housing)

Distribution of wealth within and between cohorts

0 200,000 400,000 600,000 800,000 1,000,000 1,200,000 1,400,000

16-24

25-34

35-44

45-54

55-64

65-74

75-84

85+

Tota

l Wea

lth

Real spending power

Over 50’s account for 80% of UK financial wealth

On average, higher disposable income than under 50’s

But huge variation in terms of who accounts for it……..

Wealth concentrated among current 50 - 64’s:

– 80% home ownership

– spend more per week than any other age group

65 – 75’s already have similar spending power to under 50’s versus…

40% of retired who rely on state pension: 60% home ownership over 75’s

Assumptions about older consumers

Often misrepresented, neglected, ignored

55% of over 55s agree ‘business and retailers have little interest in the consumer needs of older consumers’

Ageism – stereotyping of a whole age group as

– Homogenous ‘others’

– Warm, friendly

– Incompetent and incapable

Neglected even for products mainly for older age groups… reinforcing and responding to internalised ageism

Facts about older consumers (1)

People get more diverse as they get older…

Full-time, part-time, retired, caring, grand-parenting, volunteering etc

8% of people over 65 are from BME backgrounds 5-7% over over-60s are LGB A third of over-65s are disabled, rising to 2/3 of over-85s A quarter have symptoms of depression

Facts about older consumers (2)

Driving – half of over-70s don’t have a driving licence

Valuing home – over-65s spend more time at home (80% of the week) and like them more. But some feel trapped at home.

Living alone – half of 75+ households live alone. 7% over over-65s are often or always lonely

Not exercising enough – 7% of over-75s meet guidelines

Having cognitive difficulties – especially over 80s

Facts about older consumers (3)

Late adopters, but get there…

– 77% of 65-74 year olds use a mobile

– 40% aged over 65 have used the internet, including a million almost every day

– 1 in 10 60-69 year olds own an MP3 player

Spend higher share on essentials (food, energy, housing etc)

A little less susceptible to switching products, advertising etc

Hate stigmatising products… eg ugly adaptations

But mainstream products don’t always serve their needs

Impact of ageing on activities of daily living

Impacts on hearing, sight, touch, dexterity, muscular strength, mobility etc

28% of over-65s have significant sight loss

55% of over 60s have hearing problems

One third of over-65s have a fall each year

9 million people have arthritis

Small print harder to read

Call centres more difficult to navigate

Bending and stretching to reach shelves

Fiddly buttons on clothes

Sending text messages on mobile phones

Shopping harder to carry

Packaging harder to open

Facts about older consumers (4)

So, what is the problem?

As a society, we have failed to come to terms with the dramatic increase in the number of older people, both in absolute terms and proportionate to the population

Denial; the difficulty we all have in coming to terms with getting older, our own ageing process

Older people feel they are marginalised, ignored, stereotyped

Products, marketing and communications still addressed to the younger generation

Society does not place a high value on old age

Sheer numbers mean there is no status or achievement in having defied the odds

As a revered minority, older people used to carry the wisdom of their tribe and family. But now:

– no longer natural leaders

– diminishing role in extended family

In a secular / Western society, there is no sense of the development of spiritual wisdom that comes with age

Experience used to be a basis for respect. But with the impact of technological change the experience of age is increasingly replaced by the expertise of youth

Longer life seen as a burden, not a benefit

Society is dominated by youth culture

Huge pressure to remain looking and feeling young:

– role models are young and beautiful

– men worry about loss of potency, power and success

– women about a decline in their attractiveness

Business still tends to innovate and grow by focusing on the young

The majority of people working in marketing, communication and design are under 40 (including Age UK)

Society is bound by cultural conditioning and stereotyping of what old age means and looks like

Deterioration and decay, no sex, no fun

Traditional and conservative, not innovative, lacking in discernment, not interested in style, fashion, technology

Stereotyped prejudice written into the language: ‘grumpy old’, ‘silly old’, ‘boring old’, ‘dirty old man’

Indeed, society tends to shut old age away, rather than living with it

The idea and fact of ageing can be traumatic

Coping with ‘retirement’

Coming to terms with loss of youth

Fear of physical and mental decay

Fear of being alone, isolated, abandoned, helpless

Of being poor

Many live in denial: suppressing and denying our own fears we do not put ourselves into the shoes of being an older person…….

Summary: the business case

Recognise that business opportunities come with change

Recognise the complexity of the market

Think beyond age

The ‘Third Age’ should present rich opportunities

The changing lifestyle of ‘retirement’

Different priorities and needs

More time, and different uses

New interests and opportunities

More disposable income

Potentially a different life and opportunitiesFamily woman

Focus on the family

Spending on them

Family food and toiletry products:

– value packs to suit all

– chips and pizza

No time for me

Family holiday

Swim with the kids

DIY face pack

Family wagon

Take away

Old TV and video

Empty Nester

Focus on me (us)

Spending on me

My food and beauty preferences;

– premium toiletry products

– salad bags and fish

More time for me

Tour of China, cruise

Swim and Yoga

Weekly professional manicure

Sporty car

Meals at nice restaurants

New DVD system

Thinking beyond age

Not helpful to think of age per se.

Ageing is an individual experience; people age in different ways

The accumulation of ‘damage’ is dramatically different from one person to another

People’s response to and ability to cope with the ageing process, differs dramatically

Basic differences in attitudes towards life become magnified

Attitudes are much more defining Potentially a more complex segmentation than for younger

markets:

– less vulnerable to peer group pressure

– less need to conform, more individualistic

Most helpful segmentation based on understanding a range of feelings about ageing

Overlaid by attitude towards life per se

Whilst spending power is clearly a critical marketing variable

Conclusions Immense business opportunities if we are up to the challenge:

– to harness spending power

– provide products which are relevant to a different lifestage and lifestyle

– which help to cope with the process and consequences of ageing (practically, emotionally)

– but, are not limited by age

To make the most of those opportunities:

– develop ideas about targeting

– more insights and greater understanding

– consider the special needs of this market

– appropriate communication and design

– relevant imagery, not stereotyped and patronising

The way forward... Question the notion of ageing; in society, in ourselves

Ignore the calendar; chronological age is progressively less relevant

Develop products which are appropriate to this lifestage, to the ‘third age’

Think about the role of these products:

– enabling life and living

– enhancing the quality of life

– simplifying life