Embed Size (px)

Citation preview

www.elsevier.com/locate/eswa

Expert Systems with Applications 32 (2007) 814–821

Expert Systemswith Applications

Knowledge assets value creation mapAssessing knowledge assets value drivers using AHP

Daniela Carlucci a, Giovanni Schiuma a,b,*

a Center for Value Management (LIEG-DAPIT), Universita della Basilicata, Via dell’Ateneo lucano, 10, 85100 Potenza, Italyb Center for Business Performance, Cranfield School of Management, Cranfield, Bedfordshire MK43 0AL, UK

Abstract

The paper presents an application of the analytic hierarchy process (AHP) methodology to support the complex decision making pro-cess concerning with the development of causal models showing how organisational knowledge assets contribute to create company’svalue. The research is grounded in the resource-based view of the firm, which argues that organisational resources are bundled together.This involves difficulties in understanding which are the most important knowledge assets and how they contribute to company’s per-formance improvements. The application of the AHP allows to assess the weights for setting the priorities among knowledge assetsagainst the company’s performance targets. Adopting the AHP, the knowledge assets value creation map (KAVCM) is proposed asan approach to visualise and analyse the cause-and-effect relationships linking knowledge assets with company’s performance. Thisallows to understand how to lever and drive knowledge assets in order to sustain company’s value creation dynamics. The applicationof the KAVCM is, finally, tested by its application to the identification of the knowledge assets value drivers at the basis of NPD per-formance improvements within an Italian leader company operating in sofa industry.� 2006 Elsevier Ltd. All rights reserved.

Keywords: Resource based view; Knowledge assets; Value drivers; Analytic hierarchy process; Knowledge assets value creation map

1. Introduction

A company’s capability to create value depends on itsability to implement strategies that respond to marketopportunities by exploiting their internal resources andcapabilities (Penrose, 1959). Therefore, managers need tounderstand what are the key internal resources and driversof performance in their organisations. Traditionally, thoseresources were physical, such as machines and equipments,and financial capital. In today’s economy traditional tangi-ble resources seem to become increasingly transient andrarely provide a long-term competitive advantage. In fact,more and more successful companies tend to be those ones

0957-4174/$ - see front matter � 2006 Elsevier Ltd. All rights reserved.

doi:10.1016/j.eswa.2006.01.046

* Corresponding author. Address: Center for Value Management(LIEG-DAPIT), Universita della Basilicata, Via dell’Ateneo Lucano, 10,85100 Potenza, Italy. Tel.: +39 0971 205178; fax: +39 0971 205185.

E-mail addresses: [email protected] (D. Carlucci), [email protected], [email protected] (G. Schiuma).

that continuously are able to develop and lever intangibleassets, such as the skills and know-how of their employees,the organisational culture and company’s image. Thisreflects the belief that knowledge resources are fundamen-tal source of corporate growth and organisations need toput in place structured approaches for managing theirknowledge resources.

In the last years, with the attempt to make operative thenotion of organisation knowledge the concept of intellectualcapital (IC) has emerged as a key one to analyse and evalu-ate the intangible and knowledge dimensions of organisa-tions. It has been popularised by practitioners looking fora conceptualisation to handle the difficult and the evasivenotion of organisational knowledge resources. In particu-lar, the pioneristic approach of Skandia to the assessmentof its intellectual capital has promoted the diffusion of theconcept in the management literature. In Skandia the intel-lectual capital was initially defined as ‘‘the possession ofknowledge, applied experience, organisational technology,

Table 1Assessing the indirect relationships among knowledge assets

Performance objective A Knowledgeasset a

Knowledgeasset b

Knowledgeasset c

Knowledge asset a – – –Knowledge asset b h – h

Knowledge asset c – j –

j Strong importance.h Moderate importance.

D. Carlucci, G. Schiuma / Expert Systems with Applications 32 (2007) 814–821 815

customer relationships, and professions skills that providesSkandia AFS with a competitive edge in the market’’ (Edv-insson, 1997, p. 368). As stressed by Roos (1998) the mana-gerial appeal of the concept of IC is related to its easyapplication in the business and also to the relevance whichattributes to the strategy as the starting point for any effort.Today IC can be considered as the deeper and not visibledriver of future earnings (Roos, 1998). It is a performancedriver and is at basis of the improvement of the company’svalue creation capabilities (Carlucci, Marr, & Schiuma,2004; Chase, 1997; Edvinsson, 1997; Edvinsson & Sullivan,1996; Itami, 1987; Nahapiet & Ghoshal, 1998; Stewart,1994, 1997; Teece, 2000).

The concept of performance driver suggests causal rela-tionships between knowledge resources and company’svalue creation. In order to understand how organisationalresources translate into value, Kaplan and Norton (2000)suggest visually mapping the causal relationships into astrategy map. Based on the perspectives of the BalancedScorecard (Kaplan & Norton, 1996) a strategy map con-tains outcome measures and performance drivers, linkedtogether in a cause-and-effect diagram. Mapping organisa-tional resources, performance drivers and outcomes has agreat relevance when we take into account the resource-based view of the firm to investigate and understand thefoundations of company’s growth and wealth creation(Barney, 1991; Wernerfelt, 1984). However a clear identifi-cation of these causal relationships is not an easy task. Infact, organisational resources, and in particular knowledgeresources, work and exist as a bundle within a firm. More-over, these resource bundles impact performances withcausal ambiguity (Lippman & Rumelt, 1982) and it is dif-ficult to identify how individual resources contribute tosuccess without taking into account the interdependencieswith other assets.

It is of great importance to understand how knowledgeresources interact to create value. This can show the mech-anisms by which organisation knowledge resources sustaincompany’s value creation dynamics. Moreover, a betterunderstanding of the company’s value creation dynamicsgrounded in knowledge resources can be used as a manage-rial tool for decision-making (Ittner & Larcker, 1998). Insuch a prospect, we propose a model, the knowledge assetsvalue creation map (KAVCM), aimed to aid managers inunderstanding how knowledge assets drive company’sbusiness performance improvements and sustain value cre-ation dynamics. This model complements the strategy mapapproach (Kaplan & Norton, 2000), by deepening the roleof knowledge assets in achieving business performance.

The building process of the KAVCM is based on theadoption of the analytic hierarchy process (AHP) method-ology (Saaty, 1980, 1994). It allows to break down theproblem concerning a better understanding of the relationsbetween resources, the way resources are clustered and howthey interplay in value creation.

This paper is organised as follows. Section 2 analysesICs components and introduces the concept of knowledge

assets as well as discusses the notion of strategy mappingin further detail with specific attention to its appropriate-ness to map how IC contributes to organisation perfor-mance improvements. Section 3 presents the model of theknowledge assets value creation map (KAVCM) as anapproach to assess how knowledge assets impact on com-pany’s performance. Section 4 describes the applicationof the KAVCM within an Italian leader company in sofaindustry. Finally, some managerial implications andinsights for future research are provided.

2. Research background

2.1. Intellectual capital and knowledge assets

Knowledge has always been a fundamental productionfactor to perform organisational activities, as highlightedby Marshall (1890) who, over a century ago, acknowledgedknowledge as an important resource and a powerful engineof production. However only in last decades knowledge hasbeen recognised as a key success factor in acquiring andmaintaining company’s competitive advantages. This isresulted from an evolution of the competitive scenariowhich has stressed that heterogeneity and the immobilityare the two fundamental criteria for discerning thoseorganisational resources that are strategically valuablebecause of they are source of sustainable competitiveadvantage and are hard to transfer and accumulate, inimi-table, not substitutable, hydiosincratic in nature, synergis-tic and not consumable because of their use. This haslead to the understanding that at the basis of company’scompetitiveness resides the possession of strategic intangi-ble and hydiosincratic resources as well as core competen-cies, distinctive capabilities and absorptive capacity. Theseare in today’s economic scenario the main source of com-petitive advantage (Drucker, 1959; Hall, 1992, 1993; Itami,1987; Liebowitz, 1999; Quinn, 1992; Stewart, 1994).

In the last years with the aim to identify, classify andmanage organisational knowledge resources, different clas-sifications have been proposed in the literature and the con-cept of IC has emerged as a key one. Despite there has beena large recognition that the notion of IC denotes the intan-gible and knowledge resources of an organisation system,today there is still considerable lack of consensus on a pre-cise definition of IC. In Table 1 some of the most relevantdefinitions of IC are summarised.

816 D. Carlucci, G. Schiuma / Expert Systems with Applications 32 (2007) 814–821

The analysis of the different IC definitions together withthe main insights of the knowledge management literaturesuggests two important interpretative dimensions of IC: itis a group of knowledge assets that are attributed to anorganisation and its most important role and feature is thatmost significantly drives organisation’s value creationmechanisms.

In order to make possible the identification and evalua-tion of the different components of the IC, can be adoptedthe Knowledge Assets classification, proposed by Marr andSchiuma (2001), which interprets the IC as the sum of twocategories of knowledge assets: Stakeholder Assets andStructural Assets. This classification reflects the two keycomponents of any company: its actors and its constituentparts, i.e. the infrastructure items. Each category is furtherdivided in sub-categories in order to provide managers witha structured approach for the identification of ICs dimen-sions within organisations. Stakeholder Assets are dividedinto Stakeholder Relationship Assets and Human Assets.Structural assets are split into Physical and Virtual Assets,which refers to their tangible and intangible nature.Finally, the Virtual Assets are further divided into CultureAssets, Routines and Practices Assets, and IntellectualProperty Assets. More in detail the Stakeholder Relation-ship Assets represent the relationships between an organi-sation and its stakeholders as well as any knowledge linkbetween them. The Human Assets represent the knowledgerelated to organisations human resources. The PhysicalAssets comprise all tangible infrastructure assets incorpo-rating specific codified knowledge, such as structural layoutand information and communication technology. The Cul-ture Assets embrace categories such as corporate culture,organisational values and management philosophies. TheRoutines and Practices Assets include internal practicesand routines; these can be formal or informal proceduresand tacit rules. The Intellectual Property Assets is thesum of assets such as patents, copyrights, trademarks,brands, registered design, trade secrets and processes whoseownership is granted to the company by law. They repre-sent the tools and enablers that allow a company to gaina protected competitive advantage.

2.2. Mapping and visualising value creation

Organisations need approaches to map and visualisetheir value creation mechanisms. Any strategy can be inter-preted as a map driving organisations towards their valuecreation targets. In order to provide managers withapproaches and tools to analyse the causal links betweenorganisation resources, management actions and com-pany’s business performance, new models have been intro-duced in the management literature. In particular, Kaplanand Norton (2000) have introduced strategy maps as toolsto chart how organisational strategic objectives are trans-lated into company’s performance outcomes. Based onthe four perspectives of the Balanced Scorecard (BSC),the strategy maps show the causal relationships between

organisational resources and company’s business results.Despite, the strategy map is a relevant approach to showhow organisational resources can be translated into corpo-rate goals, it seems to present some shortcomings indescribing and evaluating how knowledge assets sustainvalue creation dynamics. It appears mainly an approachto underline the role of intangible assets in the strategicplanning in accordance with the four perspectives of theBSC. In fact, a strategy map provides an interpretativevisual framework of the cause-and-effect relationshipsamong the components of an organisation’s strategy, butdoes not evaluate how IC contributes to company’s perfor-mance improvements. Moreover the strategy map seemsmainly focus on the analysis of direct relationships betweenintangible assets and outcome objectives (Kaplan & Nor-ton, 2004). However, many scholars have emphasized theinterconnectivity of assets, especially between the knowl-edge assets. The company’s performances are the resultof a bundle of organisational resources in which the differ-ent assets depend on each other to create value (Grant,1991; Roos & Roos, 1997; Wernerfelt, 1984). Carmeliand Tishler (2004, p. 1261) argue that ‘‘the interactionamongst elements is complementary in that the value ofone element is increased by the presence of other ele-ments’’. Therefore, the role and contribution of one assetcan rarely be expressed independently from other assets.

An efficient management of organisational knowledgeassets requires an understanding of the role and the inter-dependencies of such assets in value creation.

In order to understand, evaluate and manage the corpo-rate mechanisms at the basis of value creation, it is neces-sary to map direct dependencies as well as indirectdependencies between knowledge assets.

3. The value dynamics of knowledge assets

3.1. Applying AHP to map value creation dynamics

In order to address the management’s attention on therole of knowledge assets in causal dynamics in value deliv-ering and, more specifically, how these assets, separatelyand interactively, enhance company’s performance, theknowledge assets value creation map (KAVCM) is pro-posed. It is a visual framework providing a representationand an evaluation of the links between organisational per-formance and knowledge assets. The KAVCM shares somefundamental hypotheses of other similar approaches pro-posed in the management literature to visualise the causallinks between intangible value drivers and organisationalperformance outcomes, such as, in particular, the strategymap (Kaplan & Norton, 2000, 2004) and the success map(Neely, Adams, & Kennerley, 2002). However, theKAVCM not only illustrates the links between knowledgeassets and business performance, but provides an evalua-tion for them in terms of importance in value creation.Moreover it represents how knowledge assets interact witheach other in achieving performance.

Fig. 1. Linking knowledge assets to performance objectives.

D. Carlucci, G. Schiuma / Expert Systems with Applications 32 (2007) 814–821 817

The KAVCM provides an uniform and consistent wayto describe the knowledge assets at the basis of company’svalue creation for business success, so that the knowledgeassets value drivers can be identified, assessed against thecompany’ business objectives and managed.

The building process of the map involves the applicationof the analytic hierarchy process (AHP) methodology andis based on several steps.

The first step in designing a KAVCM follows the sameprinciples as that of designing a strategy map. The designstarts from the definition of the organisational objectives,mission and vision. Differing slightly from the BalancedScorecard approach, it is suggested to adopt a wider stake-holder approach when defining the organisation strategyand business objectives (Neely et al., 2002). Once the orga-nisation strategy has been defined, managers can translateit into performance objectives to be carried out. In partic-ular, performance objectives can be expressed in terms of ageneral objective and specific performance objectives cas-caded from the previous ones. For each performance objec-tive a set of performance indicators should be defined inorder to measure the performance achievement.

According with several authors (Barney, 2001; Sullivan,2000; Zack, 1999), who have argued the importance ofidentifying the key intangible resources, involved in valuecreation, the second step concerns with the identificationof the most important knowledge assets required to achievethe performance objectives, i.e. the key knowledge assetsvalue drivers. Specifically, starting from the performanceobjectives, the managers have to select the key knowledgeassets that underpin the achievement of those objectives.

The identification of the important company’s knowl-edge assets against performance company’s objectives canbe performed by building a Matrix of Direct Dependencies.In this matrix, the company’s knowledge assets are listed inrows and the targeted performance objectives are listed incolumns. Using the matrix, managers can judge, adoptinga binomial approach, the relevance of company’s knowl-edge assets for the achievement of the performance objec-tives. In order to disclose company’s knowledge assets,managers can adopt the knowledge assets taxonomy aboveintroduced. However, also others similar taxonomies, pro-vided by the IC literature, could be adopted.

Once the knowledge assets have been selected by theMatrix of Direct Dependencies they have to be assessedin terms of importance against the performance objectives.The AHP methodology (Saaty, 1980, 1994) represents asuitable approach to provide a possible answer to thisissue. It allows to extract weights for setting the prioritiesamong knowledge assets against the targeted company’sperformance objectives. The AHP is a powerful and flexiblemulti-criteria decision making process for helping manag-ers to set priorities and make the best decision when bothqualitative and quantitative aspects of a decision need tobe considered. The methodology has been applied to a widerange of managerial practical problems including planning,prioritizing, optimization, benefit/cost analysis, decision

making in many areas such as transportation, energy pol-icy, international conflict and so on.

Due to its characteristics the AHP is a suitable means toassess the links and importance of the knowledge assetsagainst the targeted performance objectives. Especially itcan be applied to the hierarchy structure shown in Fig. 1.The first level of the hierarchical structure contains the gen-eral performance objective; while the second level containsthe performance objectives cascaded from the general one.The breaking down process can be further extended tillreaching the interested detail level of analysis. At the bot-tom level, the knowledge assets underpinning the achieve-ment of performance objectives are located.

Applying the AHP to the hierarchical structure it is pos-sible to evaluate the order of priorities or, in other words,the level of importance of each knowledge assets againstthe targeted performance objectives. In particular, theimplementation of the AHP allows to determine thestrength by which the elements in one level of the hierarchi-cal structure are related to the elements in the next higherlevel, and the relative importance of the knowledge assetsat the bottom level to achieve the general performanceobjective.

Although, the AHP is a powerful tool to weight theimportance of a knowledge asset against a performanceobjective, it does not take into account the interactionsbetween elements at the same level of the hierarchical struc-ture. In order to overcome this shortcoming, the Matrix ofthe Indirect Dependencies can be used. The cells of thismatrix contain a judgment concerning the relevance(strong or moderate) of the interaction between knowledgeassets (or performance objectives) for achieving the perfor-mance objective to which they are linked (see Table 2). Theassessment of the indirect relationships among knowledgeassets can be further extended by using likert scale or oth-ers algorithms.

Combing the results of the AHP application with thoseof the Matrix of Indirect Dependencies, it is possible todraw the KAVCM (see Fig. 2). It provides a representationand an evaluation of the links between performance objec-tives and knowledge assets. Moreover it shows how knowl-edge assets are linked to performance objectives and howdifferent knowledge assets (and objectives) interact witheach other to create corporate value. The map has nodesand arrows. Knowledge assets and performance objectivesare on the nodes. The width of each node represents theimportance of the element in the node (i.e. knowledge asset

Table 2Main definitions of intellectual capital

References Intellectual capital

Hall (1992) It is set up by intangible property and intangible resourcesEdvinsson and Sullivan (1996) It is knowledge that can be converted into valueBrooking (1996) It is the result of four main components, which are the market assets, human-centred assets, intellectual property

assets and infrastructure assetsSveiby (1997) It is related to three categories of intangible assets: internal structure, external structure and human competenceRoos, Roos, Dragonetti and

Edvinsson (1997)It is composed of (and generated by) a thinking part, i.e. the human capital, and a non-thinking part,i.e. the structural capital

Stewart (1997) It is an intellectual material that has been formalised, captured, and leveraged to produce a higher-valued assetEdvinsson and Malone (1997) It is the sum of human and structural capital. In more detail it involves applied experience, organisational

technology, customer relationships and professional skills that provide an organisation with a competitive advantagein the market

Bontis, Dragonetti,Jacobsen and Roos (1999)

It is a concept under which are classified all organisation intangible resources as well as their interconnections

Fig. 2. The knowledge asset value creation map.

818 D. Carlucci, G. Schiuma / Expert Systems with Applications 32 (2007) 814–821

or performance objective) against the general performanceobjective. The hatched arrows identify the interdependen-cies among assets as well as performance objectives. While,the continuous arrows visualise the links among elementsof different levels. The width of continuous arrow standsfor the importance (in terms of global priority) of an asset(or performance objective) in order to achieve the objectivein which the arrow ends. The KAVCM provides an under-standing of how knowledge assets contribute to companyperformance, and therefore helps managers to identifyand focus their attention on the most important knowledgeassets which represent the key knowledge assets value driv-ers, since they are those organisational resources whichsupport strategy execution.

4. Empirical evidences from a case study

In the following it is presented a case study showing theapplication of the KAVCM within in an Italian leadercompany in sofa industry. It illustrates how the KAVCMhas been adopted to identify the key knowledge assetsvalue drivers at basis of the performance improvementsof company’s new product development (NPD). From anoperative point of view the KAVCM has been drawnadopting the Expert Choice as a tool to implement theAHP methodology. In the following, first we provide abrief description of the context of research and then illus-trate the steps of the decision making process entailingthe definition of the KAVCM.

4.1. Company’s description

The company is a large furniture manufacturer whichdesigns, produces, and sells residential upholstered furniturelocated in south of Italy. It has leading market shares in theNorth America and Europe. It produces nearly 300 differentmodels each year, with a turnover of about 100 million USDollars in the year 2004. About 90% of its production isdesigned for exports. The application of KAVCM has beenencouraged by the relevance played by knowledge assets forthe company’s NPD process performance improvement.This relevance is related to two main reasons. First, in thegrowing competition in sofa industry, the NPD is a key pro-cess for the acquisition of competitive advantages. In sofaindustry, the company’s competitiveness is strongly affectedby the ability to create a wide range of products with a highnumber of stylistic and functional characteristics, to fre-quently renovate the portfolio’s products and to controlthe production costs by developing new operational solu-tions, standardising the products’ components as well asadopting new materials. In other terms, companies operatingin sofa industry are pushed to innovate continuously theirproducts. In such a competitive context, the improvementof NPD process performance is a strategic lever for control-ling the growing competition and sustaining company’svalue creation. The second reason is related to some featuresof the NPD. It can be considered as a knowledge intensiveprocess. In fact, a new sofa model is the output of a knowl-edge intensive process based on the know-how of some keyindividuals, such as designers and prototypists which, onthe base of their craftsman skills and tacit know-how, respec-tively design and prototype the different parts of the newsofa, providing to the product specific stylistic and functionalcharacteristics. Consequently, the systematic management oforganisation’s knowledge assets, at the basis of NPD pro-cess, is critical to support NPD performance improvement.

4.2. Identifying knowledge assets value drivers

The first step in the application of AHP to develop aKAVCM has been the building of a hierarchical structure

Fig. 3. Evaluation of the local priorities of knowledge assets.

D. Carlucci, G. Schiuma / Expert Systems with Applications 32 (2007) 814–821 819

breaking down the problem of the identification of keyknowledge assets value drivers against specific performanceobjectives.

For this reason some focus groups involving the com-pany’s top management have been managed. The aim hasbeen to understand the most important NPD performanceareas to be improved. In this phase, the links between gen-eral company’s strategy and NPD performance improve-ment have been analysed. Two main performancedimensions affecting the NPD process performance havebeen identified: the reduction of the product design activi-ties as well as prototyping time, and the improvement ofthe conformity of the prototype to the standards of thedesigned product. These performances were adopted astwo fundamental dimensions of the improvement of prod-uct design and prototyping efficiency. Starting from thedefinition of these performance objectives, company’s man-agers have selected the knowledge assets underpinning theachievement of those objectives. Through the implementa-tion of the Matrix of Direct Dependencies the followingknowledge assets have been identified: (i) technical exper-tise of the designers; (ii) problem solving capability of thedesigners; (iii) ICT infrastructure and particularly designsoftware as knowledge platform; (iv) working practices interms of team-working; (v) codified knowledge related toroutines and practices.

4.3. Comparative judgments to establish priorities

Once the hierarchical structure has been defined, the pri-orities have been calculated. This can be performed byadopting pairwise comparison matrixes. In the case of theidentification of the knowledge assets value drivers at thebasis of NPD performance improvement the evaluationhas been carried out from managers working in the NPDprocess. They, first, have defined the level of priorities ofthe performance objectives against the general performanceand subsequently the relevance of the knowledge assets hasbeen evaluated.

In order to determine the relative importance of the twoperformance objectives against the general objective a 2 · 2matrix has been defined. The comparisons have been car-ried out using the AHPs scale through nine points. Then,by a process of pairwise comparison the level of impor-tance of each knowledge asset against each performanceobjectives has been evaluated. This had lead to the defini-

Fig. 4. Synthesis of the know

tion of the level of priority of each knowledge asset forthe achievement of the performance objective (see Fig. 3).

The overall priority of each knowledge asset has beencalculated by multiplying its local priority with its corre-sponding weight along the hierarchy. Fig. 4 summarisesthe results of the analysis carried out by the AHP method-ology application.

The results have showed that the technical expertise ofdesigners, the working practices and the software fordesign represent very important knowledge assets todevelop for the achievement of performance objectives.Moreover, it is important to stress that the overall consis-tency at all levels has been within the acceptable ratio of0.1.

4.4. Defining the KAVCM

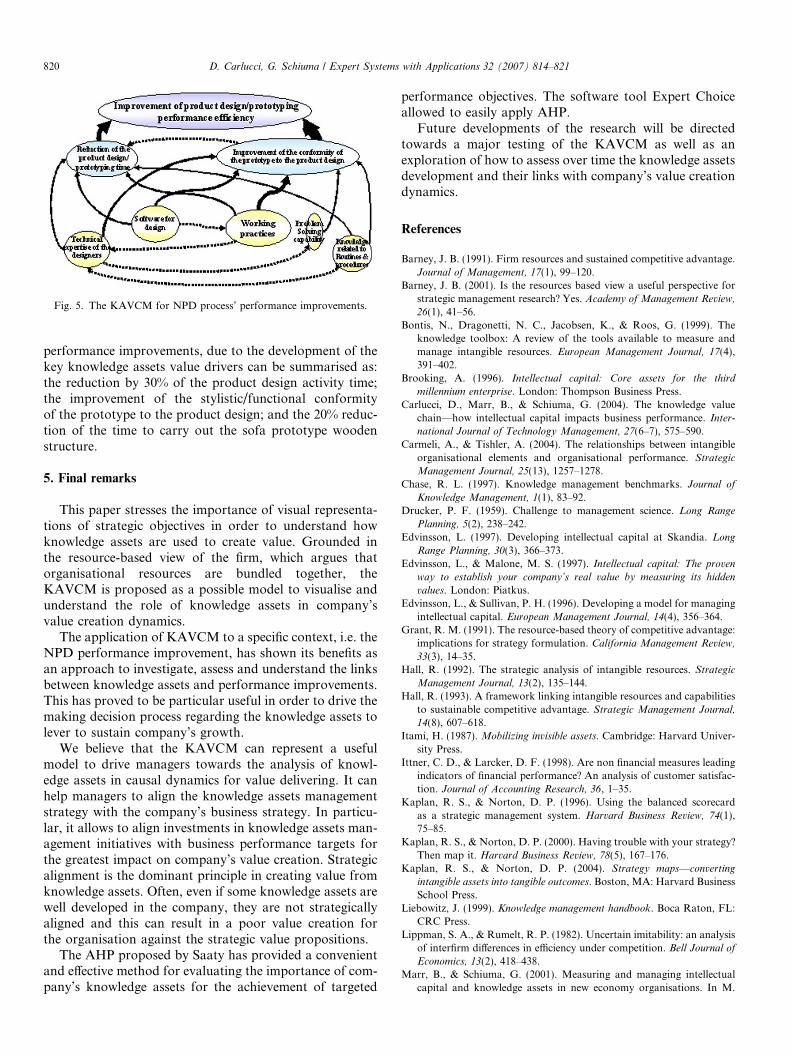

Afterwards the application of the AHP, the Matrix ofthe Indirect Dependencies has been defined. Then, combin-ing the results of the AHP methodology with those of theMatrix of the Indirect Dependencies, the KAVCM hasbeen drawn (see Fig. 5). The map has been particularly use-ful for understanding and discussing the most importantknowledge assets, i.e. the key knowledge assets value driv-ers, to be developed and managed to support NPD perfor-mance improvements. In particular, the working practices,a knowledge platform in the form of a solution for gather-ing and using codified knowledge to support the designprocess and the knowledge related to routines and proce-dures have been identified as key value resources. Theyhave been developed by the implementation of knowl-edge assets management initiatives. So far, the main

ledge assets prioritisation.

Fig. 5. The KAVCM for NPD process’ performance improvements.

820 D. Carlucci, G. Schiuma / Expert Systems with Applications 32 (2007) 814–821

performance improvements, due to the development of thekey knowledge assets value drivers can be summarised as:the reduction by 30% of the product design activity time;the improvement of the stylistic/functional conformityof the prototype to the product design; and the 20% reduc-tion of the time to carry out the sofa prototype woodenstructure.

5. Final remarks

This paper stresses the importance of visual representa-tions of strategic objectives in order to understand howknowledge assets are used to create value. Grounded inthe resource-based view of the firm, which argues thatorganisational resources are bundled together, theKAVCM is proposed as a possible model to visualise andunderstand the role of knowledge assets in company’svalue creation dynamics.

The application of KAVCM to a specific context, i.e. theNPD performance improvement, has shown its benefits asan approach to investigate, assess and understand the linksbetween knowledge assets and performance improvements.This has proved to be particular useful in order to drive themaking decision process regarding the knowledge assets tolever to sustain company’s growth.

We believe that the KAVCM can represent a usefulmodel to drive managers towards the analysis of knowl-edge assets in causal dynamics for value delivering. It canhelp managers to align the knowledge assets managementstrategy with the company’s business strategy. In particu-lar, it allows to align investments in knowledge assets man-agement initiatives with business performance targets forthe greatest impact on company’s value creation. Strategicalignment is the dominant principle in creating value fromknowledge assets. Often, even if some knowledge assets arewell developed in the company, they are not strategicallyaligned and this can result in a poor value creation forthe organisation against the strategic value propositions.

The AHP proposed by Saaty has provided a convenientand effective method for evaluating the importance of com-pany’s knowledge assets for the achievement of targeted

performance objectives. The software tool Expert Choiceallowed to easily apply AHP.

Future developments of the research will be directedtowards a major testing of the KAVCM as well as anexploration of how to assess over time the knowledge assetsdevelopment and their links with company’s value creationdynamics.

References

Barney, J. B. (1991). Firm resources and sustained competitive advantage.Journal of Management, 17(1), 99–120.

Barney, J. B. (2001). Is the resources based view a useful perspective forstrategic management research? Yes. Academy of Management Review,

26(1), 41–56.Bontis, N., Dragonetti, N. C., Jacobsen, K., & Roos, G. (1999). The

knowledge toolbox: A review of the tools available to measure andmanage intangible resources. European Management Journal, 17(4),391–402.

Brooking, A. (1996). Intellectual capital: Core assets for the third

millennium enterprise. London: Thompson Business Press.Carlucci, D., Marr, B., & Schiuma, G. (2004). The knowledge value

chain—how intellectual capital impacts business performance. Inter-

national Journal of Technology Management, 27(6–7), 575–590.Carmeli, A., & Tishler, A. (2004). The relationships between intangible

organisational elements and organisational performance. Strategic

Management Journal, 25(13), 1257–1278.Chase, R. L. (1997). Knowledge management benchmarks. Journal of

Knowledge Management, 1(1), 83–92.Drucker, P. F. (1959). Challenge to management science. Long Range

Planning, 5(2), 238–242.Edvinsson, L. (1997). Developing intellectual capital at Skandia. Long

Range Planning, 30(3), 366–373.Edvinsson, L., & Malone, M. S. (1997). Intellectual capital: The proven

way to establish your company’s real value by measuring its hidden

values. London: Piatkus.Edvinsson, L., & Sullivan, P. H. (1996). Developing a model for managing

intellectual capital. European Management Journal, 14(4), 356–364.Grant, R. M. (1991). The resource-based theory of competitive advantage:

implications for strategy formulation. California Management Review,

33(3), 14–35.Hall, R. (1992). The strategic analysis of intangible resources. Strategic

Management Journal, 13(2), 135–144.Hall, R. (1993). A framework linking intangible resources and capabilities

to sustainable competitive advantage. Strategic Management Journal,

14(8), 607–618.Itami, H. (1987). Mobilizing invisible assets. Cambridge: Harvard Univer-

sity Press.Ittner, C. D., & Larcker, D. F. (1998). Are non financial measures leading

indicators of financial performance? An analysis of customer satisfac-tion. Journal of Accounting Research, 36, 1–35.

Kaplan, R. S., & Norton, D. P. (1996). Using the balanced scorecardas a strategic management system. Harvard Business Review, 74(1),75–85.

Kaplan, R. S., & Norton, D. P. (2000). Having trouble with your strategy?Then map it. Harvard Business Review, 78(5), 167–176.

Kaplan, R. S., & Norton, D. P. (2004). Strategy maps—converting

intangible assets into tangible outcomes. Boston, MA: Harvard BusinessSchool Press.

Liebowitz, J. (1999). Knowledge management handbook. Boca Raton, FL:CRC Press.

Lippman, S. A., & Rumelt, R. P. (1982). Uncertain imitability: an analysisof interfirm differences in efficiency under competition. Bell Journal of

Economics, 13(2), 418–438.Marr, B., & Schiuma, G. (2001). Measuring and managing intellectual

capital and knowledge assets in new economy organisations. In M.

D. Carlucci, G. Schiuma / Expert Systems with Applications 32 (2007) 814–821 821

Bourne (Ed.), Handbook of performance measurement (chapter c4b, pp.

1–30). London: Gee.Marshall, A. (1890). Principles of economics. London: Macmillan.Nahapiet, J., & Ghoshal, S. (1998). Social capital, intellectual capital, and

the organizational advantage. Academy of Management Review, 23(2),242–266.

Neely, A., Adams, C., & Kennerley, M. (2002). The performance prism:

The scorecard for measuring and managing business success. London:Financial Times Prentice Hall.

Penrose, E. T. (1959). The theory of the growth of the firm. New York:John Wiley.

Quinn, J. B. (1992). Intelligent enterprise: A knowledge and service based

paradigm for industry. New York: Free Press.Roos, J. (1998). Exploring the concept of intellectual capital (IC). Long

Range Planning, 31(1), 150–153.Roos, G., & Roos, J. (1997). Measuring your company’s intellectual

performance. Long Range Planning, 30(3), 413–426.Roos, J., Roos, G., Dragonetti, N. C., & Edvinsson, L. (1997). Intel-

lectual capital: Navigating the new business landscape. London:Macmillan.

Saaty, T. L. (1980). The analytic hierarchy process. New York: McGraw-Hill.

Saaty, T. L. (1994). Fundamentals of decision making and priority theory

with the AHP. Pittsburgh: RWS Publications.Stewart, T. A. (1994). Your company’s most valuable asset: intellectual

capital. Fortune, 130(7), 68–74.Stewart, T. A. (1997). Intellectual capital: The new wealth of organizations.

New York: Doubleday/Currency.Sullivan, P. H. (2000). Value driven intellectual capital: How to convert

intangible corporate assets into market value. Hardcover: John Wiley &Sons.

Sveiby, K. E. (1997). The new organizational wealth: Managing and

measuring knowledge-based assets. San Francisco: Barrett-KohlerPublishers.

Teece, D. J. (2000). Managing intellectual capital: Organizational, strate-

gic, and policy dimensions. Oxford: Oxford University Press.Wernerfelt, B. (1984). A resource based view of the firm. Strategic

Management Journal, 5(3), 171–180.Zack, M. (1999). Developing a knowledge strategys. California Manage-

ment Review, 41(3), 125–145.