Embed Size (px)

Citation preview

© 2010 Treasury Strategies, Inc. All rights reserved.

Key Trends in Online Banking

PRESENTED BY:Dan Miner, Principal

May 19, 2010

w w w . T r e a s u r y S t r a t e g i e s . c o m 2

Market Trends - Overview

• Heightened sensitivity

• Counterparty risk

• Payments fraud

• The Internet removesboundaries.

• Global needs enhancevalue.

• Companies are looking forsolutions, not products.

• Companies seek deeperintegration opportunities.

RiskGlobalizationTreasury 3.0

The Web is becoming the primary channel and face of the bank.

w w w . T r e a s u r y S t r a t e g i e s . c o m 3

Time

Rev

enue

Treasury Management Timeline

1947 - 1970 1970 - 2005 Now - Future

BusinessServices

ClientAccommodations

Cash Management /Treasury

Management

$0

$100B

$1T+

Comprehensive payment& liquidity solutions

Supply chain solutions

Increased segmentationand refined competitive

identities

Web solutions /innovations

Rapid volume andservice scope

growth, butrevenues remained

at $0 as industryfailed to

commercialize

Approaching zero-sumgame

dominated byseveral “global”players & selectregional players

TS 1.0 TS 2.0 TS 3.0

Market Trends - Treasury 3.0

w w w . T r e a s u r y S t r a t e g i e s . c o m 4

Market Trends - Treasury 3.0

Receivables ReconciliationDisbursementA/PCashConcentrationCollectionsBilling

• Establish and manage credit risk

• Create invoice

• Receive / acquire payment

• Remittance processing

• Exception processing

• Payment clearing

• Cash application

• Disputes / collections

• Customer service

Receipts PaymentsLiquidity• Investigate vendors to work with• Analyze supplier risks• Negotiate contract with vendor• Receive and sort invoice• Enter invoice data into ERP• Manually correct data entry errors• Route invoice for approval• Manage vendor file• Resolve matching errors• Authorize payment• Clear and settle payment• Reconcile payment• Customer service / inquiries• Make sales tax payment• Issue 1099• Manage escheated payments• Research and communicate with

vendors

• Concentrate funds

• Cash position

• Cash forecast

• Investment selection

• Investment policy management

• Reconcile investments

• Benchmark and portfoliomanagement

• Secure credit facilities

• Borrow and repay debt

• Manage interest rate, foreigncurrency, and commodity risk

$1 Trillion

w w w . T r e a s u r y S t r a t e g i e s . c o m 5

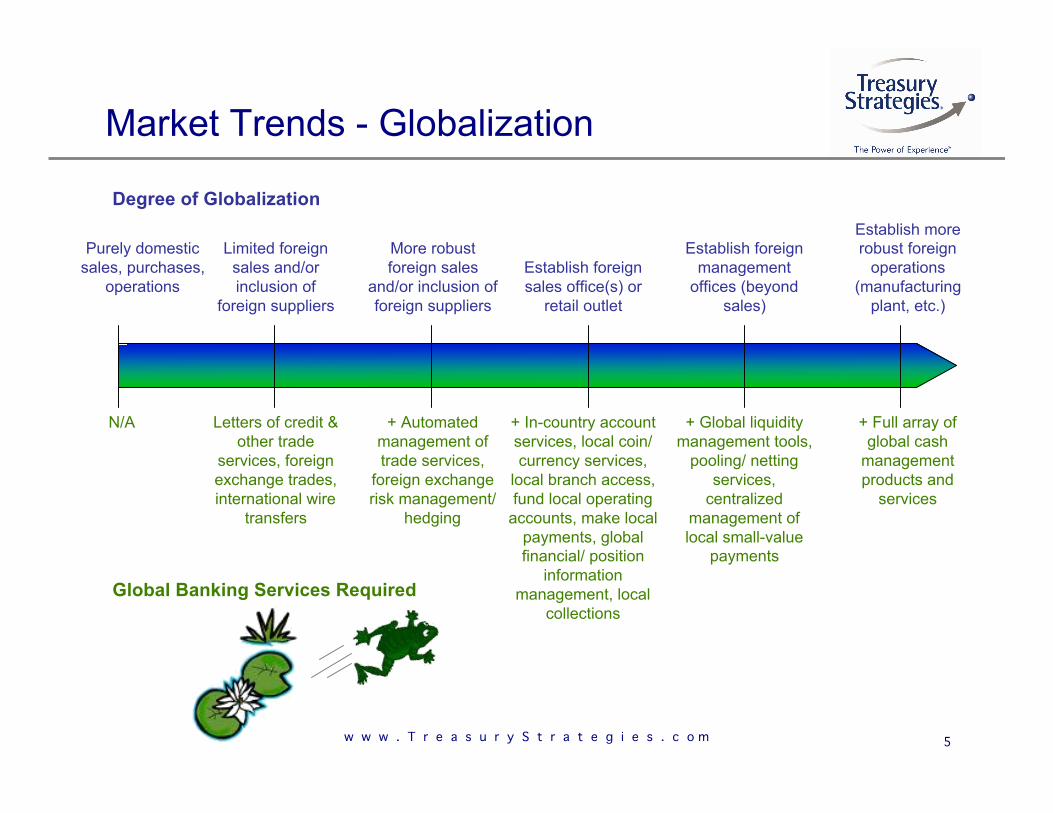

Market Trends - Globalization

Degree of Globalization

Global Banking Services Required

Purely domesticsales, purchases,

operations

N/A

Limited foreignsales and/orinclusion of

foreign suppliers

Letters of credit &other trade

services, foreignexchange trades,international wire

transfers

More robustforeign sales

and/or inclusion offoreign suppliers

+ Automatedmanagement oftrade services,

foreign exchangerisk management/

hedging

Establish foreignsales office(s) or

retail outlet

+ In-country accountservices, local coin/currency services,

local branch access,fund local operating

accounts, make localpayments, globalfinancial/ position

informationmanagement, local

collections

Establish foreignmanagement

offices (beyondsales)

+ Global liquiditymanagement tools,

pooling/ nettingservices,

centralizedmanagement oflocal small-value

payments

Establish morerobust foreign

operations(manufacturing

plant, etc.)

+ Full array ofglobal cash

managementproducts and

services

w w w . T r e a s u r y S t r a t e g i e s . c o m 6

Market Trends - Globalization

More businesses are globalizing and the extent of their globalization isbecoming more profound.

Source: Treasury Strategies Corporate Treasury Research Program - 970 Corporate Treasurers interviewed

w w w . T r e a s u r y S t r a t e g i e s . c o m 7

• 2009 AFP Payments Fraud Survey found that 71% of all firmsexperienced at least an attempted fraud in 2008.

• Estimates have put the total cost of payments fraud at $50 billion ayear.

• Online fraud is increasing

• Banks have failed!

Market Trends - Risk

w w w . T r e a s u r y S t r a t e g i e s . c o m 8

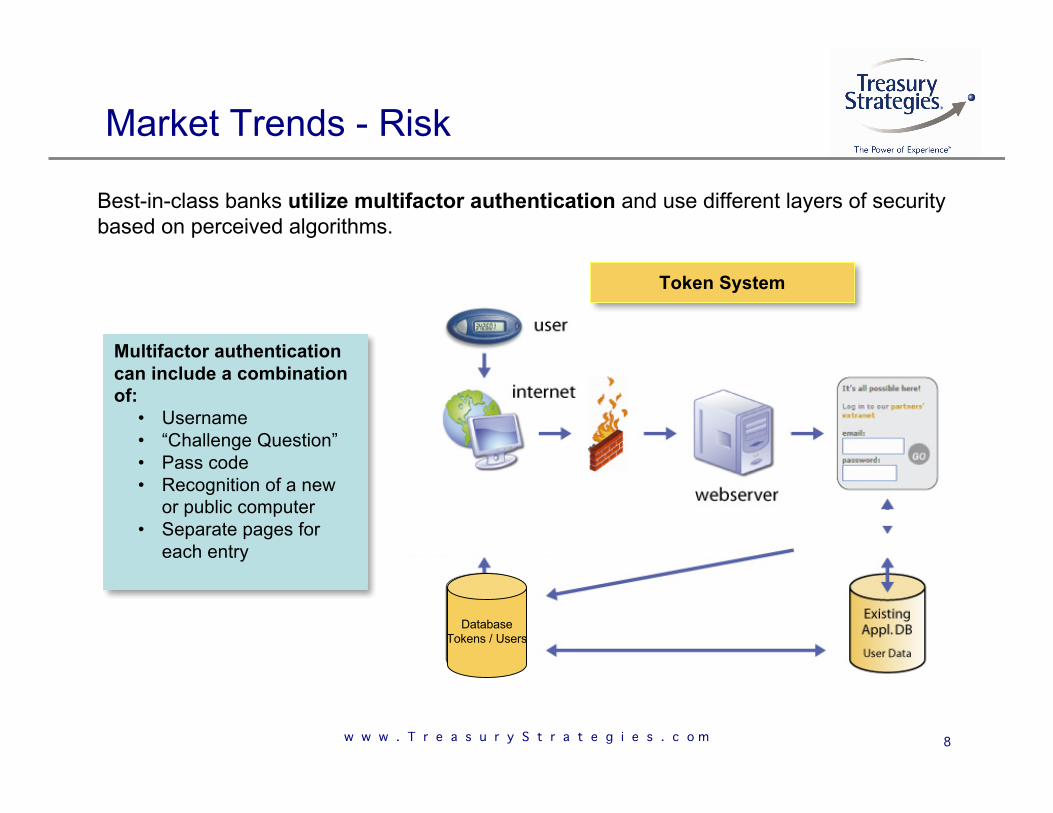

Best-in-class banks utilize multifactor authentication and use different layers of securitybased on perceived algorithms.

Multifactor authenticationcan include a combinationof:

• Username• “Challenge Question”• Pass code• Recognition of a new

or public computer• Separate pages for

each entry

Token System

DatabaseTokens / Users

Market Trends - Risk

w w w . T r e a s u r y S t r a t e g i e s . c o m 9

Bank back-office systems could monitor individualtransactions for anomalies:• Unusual transaction type, amount, and payors

can be flagged for review by the bank’s risk /fraud group.

• Parameters should be set which determine theresolution of suspicious activities (e.g., confirmvalidity with RM or client call, text message toclient).

Banks can help corporates decrease risk / fraud.• Requiring clients to purchase positive pay along

with a business checking account.• Advanced user administration features specifying

parameters by payment type, amount, and payor.• Future bank solutions that monitor other products

in the same manner.• Training and education

Market Trends - Risk

w w w . T r e a s u r y S t r a t e g i e s . c o m 10

Security depends on more than technology.Policies, procedures, and controls on the front- and back-ends of webportals are necessary to accommodate the increasing security needs ofbanks and their clients.

Future security measures could include technology that has alreadybeen developed but has not yet moved into the banking industry:

• Fingerprint Recognition• Face Recognition• Voice Recognition• Keystroke Recognition

• Finger and Hand Geometry• Retina Scan• Iris Scan• Handwriting Recognition

Market Trends - Risk

w w w . T r e a s u r y S t r a t e g i e s . c o m 11

Market Trends - Implications

• Deploy a portfolio of security measures• Educate customers - the weak link in the risk chain - of

their responsibilities and best practices in managing risk

Payments fraud

• Provide near-real time views of cash balances• Deliver tools and information to help clients understand

and forecast their cash position

Real-time information

• Deliver seamless information, payment and collectioncapabilities via the web

• Provide education and training to clients on global issues

Globalization

• Deliver accessible, easy to use tools to help firms bill,collect, pay and manage cash

• Ensure web channel is extensible, permitting scopeexpansion

Deeper integration

• Deliver entire bank through a web channel with singlesign-on and integrated data and workflow (e.g., FXintegration with international wire)

Solutions not products

ImplicationTrend

w w w . T r e a s u r y S t r a t e g i e s . c o m 12

Power of the Web Channel

• Migrate customerservice and setupto the web

• Promote lowercost channels

• Validatetransactions toincrease STP

• Automateprocesses

• Provide intuitivenavigation soclients don’t haveto have a “PhD inbanking”

• Increase clientloyalty

• Increaseintegration and“stickiness”

• Act as anaggregator forclients usingmultiple banks

• Increase clientsatisfaction

• Deepen processand dataintegration

• Personalize thecustomer / userexperience

• Deliver integratedsolutions

• Motivate referrals

• Brand the bank

• Differentiatecompetitively

• Provide afoundation forgrowth

• Align with thebank’s identityand valueproposition

Improve BankEfficiency

Improve ClientProductivity

Increase ClientRetention

Deepen ClientRelationships

Attract NewClients

w w w . T r e a s u r y S t r a t e g i e s . c o m 13

Power of the Web Channel

Product & UsageEducation

Integrated ProductAccess

Customer Service

Indirect Sales

Supports Clients

IntegratedProduct Delivery

Risk Management

Customer ServiceRisk Management

Web Channel

Direct Sales Branding

Operations

Client DataMining & Analytics

On-boarding &Implementation

InformationMgmt & Integration

Best Practices &Efficiency Education

Peer Networking& Education

Market & IndustryEducation

Bank-Driven Education

Self ServiceIntegratedFinancial Mgmt

The web channel has a far-reaching impact on business banking activities.

w w w . T r e a s u r y S t r a t e g i e s . c o m 14

At MarketBelow Market Above Market

Pricing of Information Services

Information Services Pricing

Pricing of TransactionsCom

posi

tion

ofTo

tal P

ricin

g

100%

50%

0%

Inform-ation-

Centric

AverageBank

Trans-action-Centric

Price Information at PremiumPrice Transaction at Premium

Some banks price their onlinebanking platforms below themarket average with hopes ofencouraging the transaction-driven revenue needed to offsetbelow-market pricing.

Transaction-CentricSome banks price their onlinebanking platforms above themarket average and dependless on transaction-drivenrevenue.

Most banks price their onlinebanking platform at the marketaverage and rely ontransaction-driven revenuepriced at market average toensure client-level profitability.

Information-CentricAverage Bank

Power of the Web - Pricing & Adoption

Banks are pricing their online services to leverage the value provided.

w w w . T r e a s u r y S t r a t e g i e s . c o m 15

MONTHLY BASE MAINTENANCE FEEUsually includes prior day reporting for at least 1 account.

•The reporting is usually at the summary level.•Some banks include unlimited accounts.

MONTHLY ENHANCED MAINTENANCE FEEThis charge usually offers current day reporting.

•A few banks offer detailed reporting as well at this level.

SET

UP

FEES

DATAEXCHANGE

• These can be peritem or monthlycharges.

• E.g. BAI Detail forData Exchange.

• File Transmission.

CUSTOMREPORTS

• Any special reportsare charged amonthly fee or a perreport fee.

TRANSACTIONACTIVITYREPORTING

• At some banks, thisis offered at a per-item price, notcommon outside US.

• Could be bundledinto monthlymaintenance.

Additional Fees FEES

PER USER MAINTENANCE FEES

SUPPO

RT FEESPER ACCOUNT MAINTENANCE FEES

OTHER FEES• e.g.Penalty

Pricing• Manual entry of

positive pay.• Paper Image

Statements.

Access and Maintenance Fees

MONTHLY MODULE MAINTENANCE FEESThese are fees for access to specific modules such as ACH, wire transfer and internal transfer.

•Some banks do not charge module charges at all.

$ $$ $

Pricing Components

Power of the Web - Pricing & Adoption

w w w . T r e a s u r y S t r a t e g i e s . c o m 16

Competitive Trends

The largest cash management banks spend anywhere from 100 to 200X thelevel of small regional banks on discretionary IT investments.• The average bank invests 12% of total cash management revenues (fees

+ spread) in IT and of this spend, roughly 45% is discretionary investment.• As a rule of thumb, banks generate roughly 2.5% of C&I loan balances as

cash management revenues.• The largest banks essentially run “in-house” software companies.

$0.6 MM$1.5 MM$12.5 MM$500 MM

$240.0 MM$600.0 MM$5.0 B$200 B

$120.0 MM$300.0 MM$2.5 B$100 B

$12.0 MM$1.2 MM

TypicalDiscretionary Spend

$250.0 MM$25.0 MM

Typical CMRevenues

$30.0 MM$10 B$3.0 MM$1 B

Typical ITSpend

C&I LoanPortfolio

w w w . T r e a s u r y S t r a t e g i e s . c o m 17

Competitive Trends

Consolidation and technology innovation are rewriting industry scaledynamics. Small and mid-sized players continue to grow, however, byleveraging the scale of partners like FIS.

Nimble regional and community banks are leveraging the power ofthird-party partners to win and retain business.• Faster to market• Meet current needs and consider future needs

Even regional and community banks are beginning to develop specificidentities beyond just a “local relationship bank.”

w w w . T r e a s u r y S t r a t e g i e s . c o m 18

Open Discussion

?