Embed Size (px)

Citation preview

Kellogg School of Management, Northwestern University

22nd Annual Corporate Governance Conference

The Corporate Governance Landscape

April 23, 2013

Martin Lipton

Topics

• Key Issues Requiring Directors’ Focus

• Purpose of Corporate Governance

• Corporate Governance Trends

• Director Duties and Risk Management

• Executive Compensation

• Board Structure

• Director Elections

• Takeover Defenses

• Shareholder Activism

1

Key Issues Requiring Directors’ Focus • Working with management to encourage entrepreneurship, appropriate risk-taking, and

investment to promote long-term success, despite pressures for short-term performance, and navigating changes in economic, social and political conditions

• Working with management and advisors to review business and strategy, with a view toward minimizing vulnerability to attacks by activist hedge funds

• Resisting the escalating demands of corporate governance activists

• Organizing the business, and maintaining the collegiality, of the board and its committees so that matters requiring board and committee oversight receive appropriate attention

• Developing an understanding of shareholder perspectives and fostering long-term relationships with shareholders, as well as coping with the escalating requests from activist shareholders for meetings to discuss governance and business proposals

• Developing an understanding of how the company and board will function in a crisis

• Retaining and recruiting directors who meet the requirements for experience, expertise, diversity, independence, leadership ability and character, and compensating directors in a manner that fairly reflects significantly increased demands

• Working with management to cope with the proliferation of new regulations and changes in the general perception of business since the financial crisis

• Dealing with populist demands, such as criticism of executive compensation and risk management

2

Purpose of Corporate Governance

• The core purpose of corporate governance is to enable a corporation to “build long-term

sustainable growth in shareholder value” (NYSE Commission on Corporate Governance)

The purpose of corporate governance is “to curb harmful short-termism and excessive risk-taking,” and

shareholders should “be encouraged to take an interest in sustainable returns and longer-term performance”

(European Commission green paper)

“[W]hy should we expect corporations to chart a sound long-term course of economic growth, if the so-

called investors who determine the fate of their managers do not themselves act or think with the long term

in mind?” (Chancellor Strine)

“Improving corporate governance will require separating out patient shareholders from short-term traders

and determining how others can step in to perform tasks that shareholders can’t” (Justin Fox and Jay

Lorsch)

• Sound corporate governance encourages directors and managers to develop policies and

procedures that:

Enable them to best perform their duties

Facilitate risk management, but do not unduly dampen risk-taking

Encourage long-term value creation

Are conducive to good corporate citizenship and social responsibility

3

Corporate Governance Trends

• Corporate governance norms have changed radically during the last 10 years, and

fallout from the financial crisis and ensuing economic recession continues to fuel

campaigns for reform. Principal areas of governance pressure and change include:

• Evolving governance regime is derived from federal legislation, SEC rulemaking,

state corporate legislation, SRO rules, shareholder proposals, best-practice standards

and judicial decisions, principally those of the Delaware Court of Chancery

4

Risk Management Executive

Compensation Board Structure Director Elections Takeover Defenses

• Enhanced Risk

Management

Disclosure

• Board Responsibility

for Risk Management

and Risk Failures

• Mandatory Board-

level Risk

Committees

• CEO Succession

Planning Disclosure

• Say on Pay

• Say on Golden

Parachutes

• Cut Backs on Golden

Parachutes/ Eliminate

Gross-Ups

• Clawbacks

• Enhanced

Compensation

Disclosure

• Independent

Compensation

Committees and

Consultants

• Separate

Chair/CEO

• Director

Independence

• Elimination of

Classified Boards

• Enhanced Board

Structure Disclosure

• Board Diversity

Policy Disclosure

• Direct Shareholder

Communication with

Independent

Directors

• Majority Voting

• Shareholder Proxy

Access

• Eliminate Broker

Discretionary Voting

• Enhanced Candidate

Qualifications

Disclosure

• Eliminate Shareholder

Rights Plans

• Elimination of

Classified Boards

• Lower Threshold for

Shareholder-Initiated

Special Meetings

• Permit Shareholders

to Act by Written

Consent

• Eliminate

Supermajority Voting

Provisions

Director Duties and Risk Management

Business Judgment Rules and Directors’ Basic Duties

• The basic responsibilities of directors are to exercise business judgment and act in a manner

they reasonably believe to be in the best interests of the company and its shareholders

• Key responsibilities of the board include:

Establishing the appropriate “Tone at the Top”

Choosing and monitoring performance of CEO and establishing succession plans

Planning for and dealing with crises

Determining executive compensation

Interviewing and nominating director candidates and monitoring the board’s performance

Approving the company’s annual operating plan and long-term strategy; monitoring performance and

providing advice to management as a strategic partner

Determining risk appetite; setting standards for managing risk; monitoring risk management

Setting standards for and monitoring compliance; responding appropriately to “red flags”

Taking center stage in any proposed transaction that creates a seeming conflict between the best

interests of stockholders and those of management

Setting high standards for corporate social responsibility and monitoring compliance

Overseeing relations with government, community and other constituents

Reviewing corporate governance guidelines and committee charters

5

Director Duties and Risk Management (cont’d)

Recent Developments in Risk Management

• The financial crisis and continued economic instability have sharpened scrutiny of

board oversight of risk management, and this trend has expanded beyond the financial

sector

• Bank regulators are intensely focusing on risk management and have criticized risk

oversight at companies that experienced difficulty during the financial crisis

• Nonfinancial companies are also focusing on risk management; financial as well as

operational risks are being considered (e.g., BP oil spill)

SEC rules require enhanced disclosure of the board’s role in risk oversight

To the extent that risks arising from a company’s compensation policies are reasonably likely

to have a “material adverse effect” on the company, SEC proxy rules also require a company

to discuss how its compensation policies and practices relate to risk management and risk-

taking incentives

The Committee of Sponsoring Organizations of the Treadway Commission (COSO)

recommends that companies develop “key risk indicators” – metrics to provide an early

warning signal of increasing risk exposures and strengthen enterprise risk management

6

Director Duties and Risk Management (cont’d)

Recent Developments in Risk Management (cont’d)

• In 2012, ISS added material failures of risk oversight to the list of factors it considers in recommending “against” or “withhold” votes in uncontested director elections

Per ISS, this addition was not intended to “penalize boards for taking prudent business risks or for exhibiting reasonable risk appetite.” (However, ISS did not elaborate how it would distinguish in hindsight such conduct from more fundamental, systemic shortcomings)

Per ISS, examples of failure of risk oversight include: bribery; large or serial fines or sanctions from regulatory bodies; significant adverse legal judgments or settlements; hedging of company stock; significant pledging of company stock

CEO Succession Planning

• Recent high CEO turnover rates and visible succession crises have thrust CEO succession planning into the spotlight and promoted related shareholder activism

In 2012, at least five proposals regarding disclosure of succession planning policies were withdrawn after companies implemented them; another four made it to the ballot (receiving at most 36% support)

• Succession planning is a key duty of boards, which should be involved in identifying talented leaders and developing a pipeline of internal and external CEO candidates

7

Director Duties and Risk Management (cont’d)

Observations

• Director liability under current Delaware law:

Directors are only liable for failure of board oversight if “sustained or systemic failure of the board to exercise oversight – such as an utter failure to attempt to assure a reasonable information and reporting system exists” (Caremark – 1996)

“[E]xtremely high burden” in claims for personal director liability for failure to monitor business risk (Citigroup – 2009)

“Oversight duties under Delaware law are not designed to subject directors…to personal liability for failure to predict the future and to properly evaluate business risk” (Goldman Sachs – 2011, citing Citigroup)

• Board should reassess the adequacy of company’s risk management processes and procedures, including by considering:

Risk appetite and risk tolerance, measurement and hedging of risk

How risks are identified and reported up through the organization, how management responsibilities are allocated and how management is incentivized

Sufficiency of response-preparedness, including the plans in place, how frequently they are reviewed and how they are communicated, whether risk managers have direct access to the CEO and board, how incidents are investigated and how findings are acted upon

Procedures to monitor evolving regulations, industry standards and best practices

• CEO succession planning should be a top priority of the board and be addressed on a regular basis

8

Executive Compensation

Say on Pay

• Dodd-Frank (and SEC adopting rules) requires a nonbinding shareholder vote at least every three years to approve the compensation of a company’s named executive officers (NEOs) and a nonbinding shareholder vote at least once every six years to determine the frequency of “say-on-pay” votes

JOBS Act exempts newly public “emerging growth companies” from say-on-pay and various other requirements for earliest of five years or the meeting of any of specified size thresholds

• At a large majority of companies, shareholders have opted for annual say-on-pay vote

• In 2012, the second season of mandatory say on pay, approximately 52 companies’ proposals (under 3%) failed (relative to 2011’s ~41 companies)

Say-on-pay proposals averaged 91% shareholder support, median 96% support

• ISS recommendations continued to meaningfully influence voting results in 2012

ISS recommended against 13% of management say-on-pay proposals with reported results

– Of these proposals, 19% failed, a notably higher rate than for the full sample

During the first two seasons of say on pay, only two companies that received a positive ISS recommendation failed to receive majority shareholder support

One study found support levels for companies with negative say-on-pay recommendations to have been an average 30 percentage points lower than those with positive recommendations

ISS negative recommendations are mostly based on perceived pay-for-performance disconnect

9

Executive Compensation (cont’d)

Say on Pay (cont’d)

• Per its revised 2013 policy, ISS generally analyzes pay-for-performance alignment by

considering:

(1) Peer group alignment: (a) alignment between total shareholder return (TSR) rank and

CEO total pay rank within a peer group, measured over one-year and three-year periods

(weighted 40/60); and (b) multiple of CEO’s total pay relative to peer group median

– ISS selects peer group of 14-24 companies, using as guidelines market capitalization, revenues (or assets

for certain financial firms), company’s Global Industry Classification Standard (GICS) industry group

and company’s selected peers’ GICS industry group with size constraints, “via a process designed to

select peers that are closest to the subject company in terms of revenue/assets and industry and also

within a market cap bucket that is reflective of the company’s”

– “Super-mega” non financial group for companies with more than $50 billion in revenue and at least

$30 billion in market capitalization

10

Executive Compensation (cont’d)

Say on Pay (cont’d)

(2) Absolute alignment: absolute alignment between trend in CEO pay and TSR over prior

five fiscal years (difference between trend in annual pay changes and trend in annualized

TSR)

Qualitative factors: if the above analysis demonstrates a pay-for-performance disconnect, ISS

may consider factors including: (a) ratio of performance- to time-based equity awards;

(b) overall ratio of performance-based compensation; (c) completeness of disclosure and rigor

of performance goals; (d) company’s peer-group benchmark practices; (e) actual results of

financial/operational metrics (absolute and relative to peers); (f) special circumstances;

(g) realizable pay compared to grant pay; and (h) other relevant factors

• ISS’s 2013 updates include changes to peer group selection methodology and

consideration of realizable pay, where relevant, to analysis for large-cap companies

11

Executive Compensation (cont’d)

Say on Pay (cont’d)

• ISS policy also entails case-by-case recommendations on say-on-pay proposals and

compensation committee member elections where company’s prior-year say-on-pay

proposal received support of less than 70% of votes cast

Cases where support was less than 50% will “warrant the highest degree of responsiveness”

ISS also added a policy for evaluating board responsiveness to votes regarding say-on-pay

vote frequency and generally will recommend voting “against” or “withhold” as to the entire

board if the board implements a say-on-pay vote less frequently than the option chosen by a

majority of shareholders (case-by-case if option chosen by only a plurality of shareholders)

• In 2012, the UK Business Secretary announced proposals that would give shareholders

a binding vote on the executive pay policy of listed companies

Enactment anticipated by October 2013

• In early 2013, binding shareholder approval of executive compensation was approved

by voters in Switzerland

Regulations expected by March, 2014

12

Executive Compensation (cont’d)

Say on Golden Parachutes

• Dodd-Frank requires:

Mandatory disclosure in any proxy statement relating to approval of an M&A transaction of

any compensation arrangement with an NEO that is based on or related to the M&A

transaction, including the total amount of potential payments

A nonbinding shareholder vote (via the same proxy statement) with respect to any such

arrangement (unless previously subject to a separate say-on-golden-parachute vote)

• SEC rules also require golden-parachute disclosure in connection with third-party

tender offers, but do not require a shareholder vote in this context

• Revised ISS policy for 2013 entails consideration of existing change-in-control

arrangements, as well as new or materially amended ones, and an additional focus on

“multiple legacy problematic features”

• The vote results of Say on Golden Parachutes do not appear to indicate any correlation

between levels of support on the Say on Golden Parachute vote and the vote on the

underlying transaction

13

Executive Compensation (cont’d)

Proxy Disclosure Litigation

• New wave of litigation alleging proxy disclosure is inadequate with respect to

executive compensation or equity compensation plans

• Plaintiffs in these cases allege breach of fiduciary duty by directors and seek to enjoin

a company’s annual meeting until the company makes additional disclosures

• Plaintiffs have recently obtained a preliminary injunction of an annual meeting in at

least three cases (Apple; Brocade; ChinaCast) (albeit not on disclosure or

compensation related grounds in Apple’s case)

Other cases have settled based on additional proxy statement disclosures and the payment of

legal fees for plaintiffs’ counsel

Plaintiffs making expansive discovery demands

• Earlier wave of lawsuits that targeted companies with failed say-on-pay votes has

subsided (Raul v. Rynd); same fate is likely to befall the current wave, but only if

companies are willing to fight

• Courts have recently rejected challenge to sufficiency of disclosures concerning

executive compensation / say-on-pay (Apple; Symantec)

14

Executive Compensation (cont’d)

Independence of Compensation Committee and Advisors

• In mid-2012, the SEC promulgated final rules implementing Dodd-Frank

independence requirements for public-company compensation committee members

and advisors

All compensation committee members must satisfy independence standards to be established

by each stock exchange

Compensation committees must have access to independent advisors and consider

independence factors in selecting advisors

– Rules do not require that compensation committee only hire independent advisors; they mandate only

that the independence factors be considered in the selection

Rules also implement disclosure obligations regarding compensation-consultant conflicts

• In September 2012, the NYSE and Nasdaq filed proposed changes to their listing

standards designed to comply with Dodd-Frank independence requirements

Proposed NYSE changes generally are limited to implementation of the SEC codifying rule

Nasdaq proposal includes additional requirements that more closely align Nasdaq’s rules with

the existing NYSE standards (e.g., requirement of a compensation committee and a charter)

Proposed rules remain subject to revision, SEC final approval and implementation timelines

15

Executive Compensation (cont’d)

Enhanced Clawback Requirements

• Dodd-Frank mandates adoption of an executive compensation clawback policy

applicable in the event of an accounting restatement due to material noncompliance

with financial reporting requirements

Other Compensation-Related Requirements of Dodd-Frank

• Mandatory annual proxy disclosure regarding the relationship between executive

compensation and the company’s financial performance, and the company’s policies

regarding employees and directors engaging in hedging transactions on stock

• Mandatory disclosure of the ratio of the median annual total compensation of the

company’s employees (excluding the CEO) to that of the CEO

• These clawback and certain other Dodd-Frank requirements have not yet been

implemented and are subject to future rulemaking by the SEC and national securities

exchanges

16

Executive Compensation (cont’d)

Observations

• In the current environment, boards and compensation committees need to:

Balance pay-for-performance principles with avoidance of policies encouraging excessive risk-taking

Be sensitive to compensation packages that could be deemed “excessive” by proxy advisors or shareholders given the post-crisis emphasis on financial restraint

Closely consider elements of compensation package that could lead to failed say-on-pay vote

• But boards and compensation committees must not lose sight of the underlying goal of executive compensation – to attract, retain and incentivize highly qualified individuals

Despite the new say-on-pay regime, there is no reason to change the longstanding law and practice recognizing that boards are best qualified to decide what corporate policies are needed to achieve this goal

• Goldman Sachs (2011): “The decision as to how much compensation is appropriate to retain and incentivize employees, both individually and in the aggregate, is a core function of a [board] exercising its business judgment.”

A compensation committee that follows normal procedures and has the advice of legal counsel and an independent consultant should not fear being second-guessed by the courts

17

Executive Compensation (cont’d)

Observations (cont’d)

• Companies should carefully review their compensation disclosures to ensure that they

fulfill securities law requirements, paying particular attention to areas on which

plaintiffs have focused to date

• The compensation committee and full board should be advised of the potential

litigation risk during the proxy preparation process and should consult with outside

counsel in order to be prepared to respond to a lawsuit if one is filed

Review terms of D&O insurance on an annual basis

• The say-on-pay vote in the U.S. should remain nonbinding, regardless of rules that

may in the future apply in the U.K., Switzerland or elsewhere

18

Board Structure

Elimination of Classified Boards

• Generally, in a classified board, 1/3 of directors are elected each year for three-year terms

• Percentage of domestic S&P 500 companies with classified boards is in decline

Approximately 16% in 2012 (down from 47% as recently as 2005)

• Activists continue to push declassification proposals for all directors to be elected annually, especially in the wake of 2011 Airgas reaffirmation of validity of poison pill

Lucian Bebchuk’s Harvard Law School Shareholder Rights Project (SRP) advised institutional shareholders in connection with declassification proposals at 89 S&P 500 companies in 2012

– Negotiated settlements with 48 companies (over 1/3 of S&P 500 companies that had classified boards at the beginning of the season) where management committed to propose declassification

– At companies that did not reach agreements with the SRP, precatory proposals were approved at 38 companies (averaged 82% support); two others failed with support just below 50%

SRP announced the submission of 74 declassification proposals for the 2013 proxy season

• In 2012, shareholders at 51 companies voted on declassification proposals – proposals averaged 81% support (vs. 39 proposals with 73% support in full-year 2011)

Management at 66 companies initiated declassification proposals in 2012 – these proposals averaged 99% support (vs. 49 proposals with 98% support in full-year 2011)

19

Board Structure (cont’d)

Separation of Chairman and CEO

• Disclosure in annual meeting proxy statement

• ISS generally recommends a vote for shareholder proposals requiring an independent

chairman unless the company maintains a “counterbalancing governance structure,”

including a lead director who:

Presides at all board meetings at which chairman is not present

Serves as liaison between chairman and independent directors

Approves information sent to board, meeting agendas and schedules

Has authority to call meetings of independent directors

If requested by major shareholders, is available for consultation and direct communication

• In 2012, shareholders at 54 companies voted on proposals to require an independent

chairman – proposals averaged 35% shareholder support

Significant increase over the 28 proposals voted on in full-year 2011 (average 33% support)

• The CEO is also Chairman at approximately 57% of S&P 500 companies

Approximately 92% of S&P 500 boards have a lead or presiding director

20

Board Structure (cont’d)

Other Disclosure Requirements

• Disclosure for each director nominee of the experience, qualifications, attributes or

skills that qualified that person to serve as a director

• Disclosure regarding how the nominating committee considers diversity

Director Independence

• SOX, Dodd-Frank, NYSE and NASDAQ rules all focus on director independence

Boards of listed companies must have a majority of independent directors

All audit, compensation and nominating committee members must be independent; national

securities exchanges and SEC are developing enhanced independence criteria for

compensation committee members, as required by Dodd-Frank

ISS Policy

• Policies of proxy advisory firms such as ISS impose additional constraints on director

profiles (e.g., ISS “overboarding” policy, as tightened for 2013 to count subsidiary

boards with public shareholders as separate boards)

21

Board Structure (cont’d)

Observations

• Board structure should be conducive to effective stewardship

• There is no persuasive evidence that declassifying boards enhances shareholder value over the long term

• A classified board can help assure continuity and stability of strategy, management and policies

• Majority of directors have company-specific experience at any given time

Facilitates developing and carrying out long-term plans

Does not affect accountability of the board

Reduces vulnerability to abusive takeover tactics (but has rarely stopped a well-priced, all-cash takeover bid)

• Nonetheless, if facing declassification, must consider immediate or phased transition

• A combined Chairman/CEO role can be highly effective, despite increased activist focus on this issue in 2012

AFSCME independent chairmanship proposals at 21 prominent companies

Chairmen’s Forum model statement urging boards to adopt separation policies

• Overemphasis on director independence and compliance with proxy advisor policies can deprive boards of valuable experience, qualifications and skills

22

Director Elections

Majority Voting

• In uncontested elections directors historically were elected by plurality vote

Delaware law provides for plurality voting as the default, but was amended to accommodate

implementation of majority voting in bylaws

• “Majority voting” in director elections has become the norm among larger

companies – adopted by approximately 82% of domestic S&P 500 companies (another

10% have a plurality vote standard with a resignation policy)

Majority voting provisions require that in uncontested elections directors be elected by a

majority of votes cast

Incumbent directors who are not reelected by a majority vote must tender resignations

– Delaware courts generally will apply the “business judgment rule” in assessing a board’s rejection of the

resignation of a director who did not receive a majority of votes cast for reelection (Axcelis – 2010)

Significantly less penetration to date amongst mid- and small-cap companies

• Majority voting gives “teeth” to recommendations by proxy advisory firms to

“withhold the vote” for directors

23

Director Elections (cont’d)

Elimination of Broker Discretionary Voting

• Historically, NYSE rules permitted brokers to vote on behalf of clients who failed to

provide voting instructions in uncontested director elections

• NYSE Rule 452 now prohibits such broker discretionary voting

• Additionally, Dodd-Frank eliminates broker discretionary voting for certain matters

(election of a director, executive compensation or “any other significant matter” as

determined by the SEC)

Makes it more difficult to achieve majority votes in uncontested director elections

Increases the voice of activist shareholders

Enhances the power of proxy advisory firms such as ISS

• In 2012 the NYSE eliminated broker discretionary voting on selected corporate

governance proposals, including proposals to de-stagger the board, adopt majority

voting, eliminate supermajority voting, provide for the right to use written consents,

provide for the right to call a special meeting and provide for certain anti-takeover

provision overrides

24

Director Elections (cont’d)

Shareholder Proxy Access

• In 2011 the D.C. Circuit Court of Appeals struck down Rule 14a-11, which would have provided a mechanism for including shareholder nominees in company proxy statements

Court found that the regime represented an “arbitrary and capricious” exercise of SEC’s authority

Opinion criticized SEC for failing “adequately to assess the economic effects of” the rule and for relying on “insufficient empirical data” to support a conclusion that proxy access would improve board performance and increase shareholder value

– This standard, if applied in other circumstances, could invalidate other SEC rules

• SEC’s amendments to Rule 14a-8 became effective in 2011

Permit shareholders to submit proposals for proxy access

• ISS will maintain a case-by-case approach to its recommendations on proxy access shareholder proposals (which will also apply to management proposals)

In formulating recommendations, ISS will consider company-specific and proposal-specific factors (e.g., minimum share ownership, proportion of directors shareholders can nominate, procedures to resolve conflicts among multiple shareholders seeking to make nominations)

Proponent’s rationale no longer cited as enumerated core factor, but still may be considered

25

Director Elections (cont’d)

Shareholder Proxy Access (cont’d)

• 2012 was the inaugural season for 14a-8 shareholder proxy access proposals

24 shareholder proxy access proposals were submitted (9 binding; 15 precatory)

Shareholders voted on 12 such proposals, with 10 failing and two passing (both of the latter alongside failed say-on-pay votes)

– Two proposals were withdrawn after management implemented accommodating corporate governance changes or promised to submit a management proposal in 2013

SEC responded to multiple proxy access no-action requests, providing guidance on potential bases for exclusion of proposals (or portions thereof)

– Allowed eight such exclusions based on vague and indefinite nature or multiple proposals

– Denied seven, rejecting arguments based on various grounds, including false/misleading or vague/indefinite nature, substantial implementation, violation of law and others

Proxy Plumbing/Alignment of Voting and Economic Interest

• SEC is considering modernizing “proxy plumbing,” including with respect to:

Accuracy, transparency and efficiency of the voting process

Shareholder communications; retail participation in voting process

Misalignment of voting power and economic interests (CSX case)

Role of proxy advisory firms (ISS, Glass Lewis)

26

Director Elections (cont’d)

Beneficial Ownership Reporting

• Wachtell Lipton filed a rulemaking petition with the SEC in 2011 proposing to shorten the Section 13(d) reporting deadline and expand the definition of beneficial ownership under the reporting rules

Academics filed counter-petition

• SEC proposal in 2011 to readopt without change portions of the beneficial ownership reporting rules under Sections 13 and 16 of the Securities Exchange Act of 1934 as they relate to transactions in security-based swaps

Intended to prevent Dodd-Frank from unintentionally excluding such transactions from the scope of the existing rules

• SEC has indicated that it plans to commence “a broad review of our beneficial ownership reporting rules” covering:

Whether to shorten the 10-day filing deadline for Schedule 13D filings

Whether beneficial ownership reporting should be changed with respect to cash-settled equity swaps and other derivatives

How the presentation of information on Schedules 13D and 13G can be improved

• Turnover in SEC leadership introduces potential uncertainty to agenda

27

Director Elections (cont’d)

Beneficial Ownership Reporting (cont’d)

• In February 2013, the NYSE, the Society of Corporate Secretaries and Governance

Professionals and the NIRI filed a joint rulemaking petition with the SEC seeking

prompt updating of the reporting rules under Section 13(f) of the 1934 Act, as well as

supporting a more comprehensive study of the beneficial ownership reporting rules

under Section 13

Petitioners urge the SEC to shorten the reporting deadline under Rule 13f-1 from 45 days to

two business days after the relevant calendar quarter and to amend Section 13(f) to provide for

reporting on at least a monthly basis (rather than quarterly)

28

Director Elections (cont’d)

Observations

• Majority voting (and elimination of broker discretionary voting in director elections)

magnifies the influence of proxy advisory firms such as ISS

Voting power is increasingly in the hands of large institutional investors, many of which follow

proxy advisory firms’ recommendations

Lack of accountability and transparency in how proxy advisory firms formulate voting

recommendations; potential conflicts of interest; insufficiently tailored recommendations

Analogy to lax supervision over, and overreliance on recommendations of, credit rating agencies

(issues being rectified)

• Proposals for regulation of proxy advisory firms by the SEC

Also, private-sector efforts to disintermediate proxy advisory firms (e.g., BlackRock)

• Shortening of Section 13(d) reporting deadline and expansion of beneficial ownership

definition would serve Section 13(d)’s underlying purpose – “to alert the marketplace to

every large, rapid aggregation or accumulation of securities”

• FTC Chairman recently indicated that HSR’s “passive investment exemption is a narrow

one, and we will not hesitate to seek civil penalties against companies that try to abuse it”

• Recent Canadian case (Telus v. CDS) highlights the need for action on empty voting issue

29

Director Elections (cont’d)

Observations (cont’d)

• Since it is now clear that the SEC will not pursue a mandatory proxy access regime in

the near term, focus on private ordering through shareholder proposals will continue

and likely intensify

• With each iteration of SEC no-action guidance, activists are better able to craft

resolutions that can withstand companies’ exclusion efforts and garner shareholder

support

• It is advisable for companies to take preparatory actions, including:

Monitoring and engaging proactively with significant shareholders

Reviewing director qualification bylaws, advance notice bylaws, corporate governance

policies and board committee charters

Considering proactive adoption of proxy access, where appropriate

30

Takeover Defenses

Takeover Preparedness

• Notwithstanding the constant criticism from academics, activists and other so-called

governance experts, takeover preparedness has never been more important

• Failure to prepare for a takeover or pressure from an activist exposes a potential target

to pressure tactics and reduces the target’s ability to control its own destiny

• Whatever the state of the law may be and however it may change, in order to achieve

the best result in a takeover situation, a company must have effective defenses and

keep them up to date

• A board of directors’ “fire drill,” with participation of the company’s investment

banker, legal counsel, proxy soliciting firm and public relations consultant, on an

annual basis is critical to success in dealing with an attack, if one comes

The Shareholder Rights Plan (“Poison Pill”) and Structural Defenses

• A rights plan is the primary structural defense that empowers a board to “Just Say No”

(Time Warner; Paramount; Unitrin; Airgas)

• Board-implemented mechanism; no shareholder approval required

31

Takeover Defenses (cont’d)

The Shareholder Rights Plan and Structural Defenses (cont’d)

• Strongest in combination with a classified board

• Only the board can remove the barrier created by a rights plan

But a rights plan will not interfere with a board-approved transaction

• A rights plan does not immunize a company from takeover, but enables the board to

control the process and is conducive to a higher acquisition price

• ISS policy is to generally recommend “withhold” for all directors following adoption

of a rights plan with a term of more than 12 months, or renewal of any existing rights

plan, that is not subject to shareholder ratification

• Other key structural defenses include:

Classified board

Limited ability for shareholders to call a special meeting

Advance notice provisions in company bylaws

Limited ability for shareholders to act by written consent

Delaware General Corporation Law Section 203 and other state antitakeover statutes

32

Takeover Defenses (cont’d)

Observations

• Takeover defenses have been significantly scaled back as a result of persistent

activism led by ISS and other proxy advisors, unions and public pension funds,

academics, activist shareholders and corporate raiders

Only 7% of S&P 500 companies currently have a rights plan in effect (vs. 45% as recently as

2005 and 60% in 2000)

In 2012, shareholders at 18 companies voted on proposals seeking the right of shareholders to

call special meetings – proposals averaged 45% shareholder support

Also in 2012, shareholders at 21 companies voted on proposals seeking the right to act by

written consent – proposals averaged 46% shareholder support

33

Takeover Defenses (cont’d)

Observations (cont’d)

• Although fewer companies currently have rights plans in effect than in the recent past,

the defense remains vigorous because of a board’s ability to rapidly adopt

• Delaware courts have continued to uphold the vitality of rights plans:

A board is not required to redeem a rights plan in the face of a tender offer that the board

determines to be inadequate. If directors act “in good faith and in accordance with their

fiduciary duties,” the courts will continue to respect a board’s “reasonably exercised

managerial discretion” (Airgas – 2011)

Rights plan with a 4.99% trigger designed to protect the company’s net operating loss

carryforwards (NOLs) (Selectica – 2010)

Rights plan featuring a 20% trigger that included an exemption for an ~30% ownership

position held by a company insider (Yucaipa – 2010)

• Companies should, as part of regular “fire drills,” consult with counsel about the

utility of keeping a rights plan “on the shelf,” and where applicable should consider

adopting a rights plan to protect NOLs

• Companies should not scuttle takeover defenses without careful consideration

34

Shareholder Activism

Ascendant Concepts of Corporate Governance

• Shareholder-managed governance

Activist investors and hedge funds; ISS; academics

• Compliance criteria and standardized “best practices”

Sarbanes-Oxley; Dodd-Frank; SEC; ISS

• Corporate social responsibility

United Nations; unions; pension funds; charities; academics

35

Shareholder Activism: Shareholder-Managed Governance

Director-Managed or Shareholder-Managed Governance

• “The business and affairs of every corporation … shall be managed by or under the

direction of a board of directors …” (Delaware General Corporation Law § 141(a))

• “Shareholder power to adopt governance arrangements should include the power to

adopt provisions that would allow shareholders … to initiate and vote on proposals

regarding specific corporate decisions. Increasing shareholder power to intervene …

would improve corporate governance and enhance shareholder value” (Bebchuk)

• ISS policy to vote “against” or “withhold” from selected directors or board if board

fails to act on shareholder proposal that received majority vote in specified

circumstances

36

Shareholder Activism: Shareholder-Managed Governance (cont’d)

Shareholder Activist Objectives, Tools and Impact

• Key shareholder activist governance objectives:

Institute majority voting in director elections

Declassify board of directors

Require independent board chairman

Allow shareholders the right to call special meetings and act by written consent

Reduce/rescind supermajority vote provisions in charter and bylaws

Provide for shareholder proxy access

• Activist tools: 14a-8 proposals, proxy fights, withhold campaigns, PX14A6G filings

• Governance activism erodes takeover defenses and board functionality

37

Shareholder Activism: Shareholder-Managed Governance (cont’d)

ISS Policy on Board Responsiveness to Majority-Supported Shareholder Proposals

• In its 2013 updates, ISS tightened its policy regarding board responsiveness to majority-supported shareholder proposals such that it will vote “against” or “withhold” from individual directors, committee members, or the entire board of directors if:

For 2013, the board failed to act on a shareholder proposal that received the support of a majority of the shares outstanding in the previous year or that received the support of a majority of shares cast in the last year and one of the two previous years

For 2014, the board failed to act on a shareholder proposal that received the support of a majority of the shares cast in the previous year

Responding to the shareholder proposal will generally mean either full implementation or, if the matter requires a shareholder vote, a management proposal on the next annual ballot to implement the proposal. Responses involving less than full implementation will be considered on a case-by-case basis

For shareholder proposals that won a majority of votes cast during the 2012 proxy season, board responsiveness will be assessed under the existing standard, which requires approval by a majority of outstanding shares the previous year or the support of a majority of votes cast in both the last year and one of the two previous years

• Continues the trend of narrowing director discretion in matters traditionally considered to be within directors’ authority

38

Shareholder Activism: Shareholder-Managed Governance (cont’d)

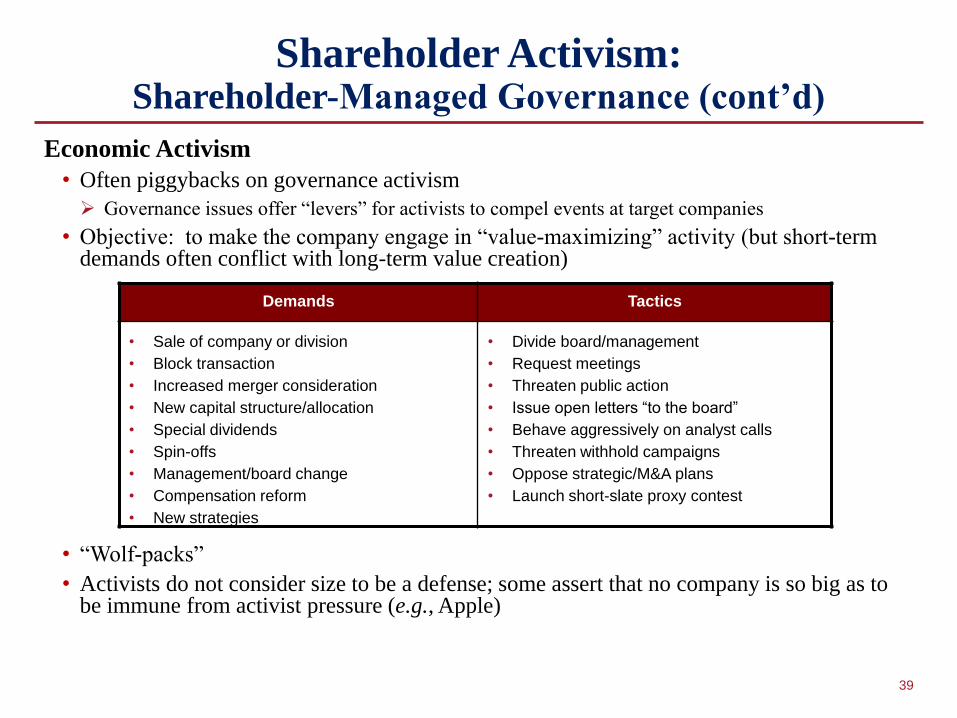

Economic Activism

• Often piggybacks on governance activism

Governance issues offer “levers” for activists to compel events at target companies

• Objective: to make the company engage in “value-maximizing” activity (but short-term demands often conflict with long-term value creation)

• “Wolf-packs”

• Activists do not consider size to be a defense; some assert that no company is so big as to be immune from activist pressure (e.g., Apple)

39

Demands Tactics

• Sale of company or division

• Block transaction

• Increased merger consideration

• New capital structure/allocation

• Special dividends

• Spin-offs

• Management/board change

• Compensation reform

• New strategies

• Divide board/management

• Request meetings

• Threaten public action

• Issue open letters “to the board”

• Behave aggressively on analyst calls

• Threaten withhold campaigns

• Oppose strategic/M&A plans

• Launch short-slate proxy contest

Shareholder Activism: Compliance Criteria

• Impact of Sarbanes-Oxley, Dodd-Frank and related rules

• Advent of the monitoring/compliance board

Increasing emphasis on director independence and monitoring of the board itself

• The corporate governance industry:

Proxy advisory firms (e.g., ISS, Glass Lewis)

Labor organizations/pension funds (e.g., AFL-CIO, AFSCME, CalPERS)

Other key players: (e.g., CII, The Corporate Library, CtW Investment Group)

• ISS replaced its “GRId” methodology with “Governance QuickScore” in 2013

Quantitatively driven; ranks companies in deciles within each of ISS’s existing four “pillars” (Audit, Board Structure, Compensation and Shareholder Rights) and provides overall governance rating

New methodology provides no more complete or accurate assessment of corporate governance practices than the previous one

• Limits on executive compensation

• Efforts to create new forums for shareholders to communicate directly with directors (e.g., “fifth analyst call”)

40

Shareholder Activism: Corporate Social Responsibility

• Corporate social responsibility is a major concern for companies and boards

• Over 358 “environmental and social” Rule 14a-8 shareholder resolutions proposed during the 2012 proxy season (only one received majority support), including:

Political contributions and activity (118)

Environmental issues (including climate change, energy, other) (90) and sustainability (35)

Sexual orientation non discrimination/EEO reporting (31)

Animal welfare (19)

Human rights (18) and labor issues (12)

• Enhanced focus on political spending in light of the Supreme Court’s 2010 Citizens United decision (and affirmation in June 2012) and election year

Petition for rule-making by academic group (including Bebchuk) on political spending disclosure under consideration by SEC

• For the 2013 proxy season, ISS updated its voting policy on social and environmental proposals with a case-by-case recommendation considering whether implementation is likely to enhance and protect shareholder value and a number of enumerated factors

• Revised ISS policies for 2013 also include a shift from a general recommendation “against” to a “case-by-case” analysis for shareholder proposals related to linking executive pay to environmental and social criteria and clarifications of its lobbying policy

• United Nations blueprint to promote human rights in the conduct of global business

41

Shareholder Activism: Activist Red Flags

• Companies that consistently fall short of expectations but have no logical, clearly

articulated business plan to achieve consistent performance

• A board that does not hold management accountable for poor performance

• Overtenured or figurehead directors

• Directors who “rubber stamp” management decisions without performing their own

thorough review

• Lack of succession planning for CEO and key management positions, including CEO

• Management compensation structures that are not linked to the business model, strategic

goals or other objectives or are not in line with industry standards – “Pay for Performance”

• Failure to engage in meaningful competitive and industry analysis on a regular basis –

“Peer Review”

• Advisors that are captured by management

• Weak or defective internal audit controls and procedures

• Persistent criticism of company strategy and management by research analysts

• Institutional investors who believe that they cannot communicate effectively with the board

42

![KELLOGG SCHOOL OF MANAGEMENT, NORTHWESTERN …faculty.haas.berkeley.edu/vissing/vissing_nberma_article.pdftherein]), (2) the small firm effect (small stocks have outperformed large](https://img.dokumen.tips/doc/110x75/5e7477a72bf99b0a2431a76e/kellogg-school-of-management-northwestern-therein-2-the-small-irm-effect.jpg)