Embed Size (px)

Citation preview

KDFED

Financial Markets and

Institutions

Unit No. I to V

KDFED – Financial Markets & Institutions

TM

UNIT I – SYLLABUS Meaning, role, functions and constituents of financial

markets

Financial instruments

Indian Money and Capital Markets

Money Market: Meaning,characteristics, objectives,

importance, general functions and segments of money market

Characteristics of a developed money market

Money market Vs Capitalmarket

Global money markets

2

Financial System

• Financial system of a country consists of a network of inter

connected system of markets, institutions and services

• It connects the savings-surplus and savings-deficit institutions and

establishes a regular flow of funds in the capital market of a country.

KDFED – Financial Markets & Institutions 3

https://www.slideshare.net/divyaactive/indian-financial-system-ppt

Structure of the Financial

System

Financial markets

Financial institutions

Financial assets

Financial services

KDFED – Financial Markets & Institutions 4

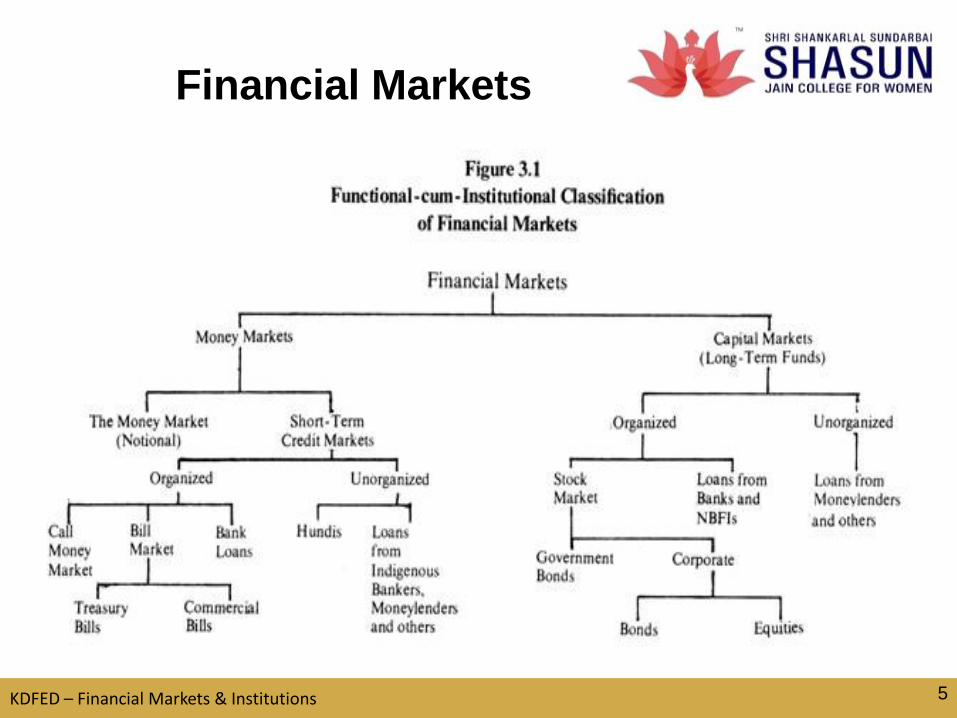

Financial Markets

KDFED – Financial Markets & Institutions 5

FINANCIAL INSTRUMENTS

KDFED – Financial Markets & Institutions6

7KDFED – Financial Markets & Institutions 7

FINANCIAL INSTRUMENTS

Money Market

KDFED – Financial Markets & Institutions 8

Money market

• Money market is a collective name given to all the institutions that

are dealing in short term funds

• Instruments dealt in the money market includes cheques, bills,

promissory notes, commercial paper, treasury bills and government

bonds

KDFED – Financial Markets & Institutions

https://www.slideshare.net/kashish1109/ppt-onmoneymarket1?next_slideshow=1

9

Functions of Money

market

• To maintain monetary equilibrium.

• To promote economic growth.

• To provide help to Trade and Industry.

• To help in implementing Monetary Policy

• To help in Capital Formation

• Money market provides non-inflationary sources of finance to

government

• Money market is a collective name given to all the institutions that

are dealing in short term funds

• Instruments dealt in the money market includes cheques, bills,

promissory notes, commercial paper, treasury bills and government

bonds

KDFED – Financial Markets & Institutions 10

KDFED – Financial Markets & Institutions11

IMPORTANCE OF MONEY MARKET

Characteristics of a well

developed money market

• Presence of a strong central bank

• Well organised banking industry

• Availability of credit instrument and resources

• Free movement of funds

• Integrated monetary and fiscal policies

KDFED – Financial Markets & Institutions 12

Capital Market vs Money MarketBASIS FOR

COMPARISONMONEY MARKET CAPITAL MARKET

Meaning

lending and borrowing of

short term securities are

done.

long term securities are

issued and traded.

Financial instruments

Treasury Bills, Commercial

Papers, Certificate of

Deposit, Trade Credit etc.

Shares, Debentures,

Bonds, Retained Earnings,

Asset Securitization, Euro

Issues etc.

Institutions

Central bank, Commercial

bank, non-financial

institutions, bill brokers,

acceptance houses, and so

on.

Commercial banks, Stock

exchange, non-banking

institutions like insurance

companies etc.

Time Horizon Within a year More than a year

MeritIncreases liquidity of funds

in the economy.

Mobilization of Savings in

the economy.

Return on Investment Less Comparatively High

14

Profile of Indian money market

Call money rates

Commercial Paper Market

Commercial Bill Market

Indian Bill Market

Bill Market Schemes

RBI directives

KDFED – Financial Markets & Institutions 14

UNIT II – SYLLABUS

Indian Money Market• The India money market is a monetary system that involves the

lending and borrowing of short-term funds.

• Financial institutions employ money market instruments for financing

short-term monetary requirements of various sectors such as

agriculture, finance and manufacturing.

• Central bank of the country - the Reserve Bank of India (RBI) has

always been playing the major role in regulating and controlling the

India money market.

• The intervention of RBI is varied - curbing crisis situations by

reducing the cash reserve ratio (CRR) or infusing more money in the

economy.

KDFED – Financial Markets & Institutions15

Participants

• Central Government

• State Government

• Public Sector Undertakings

• Scheduled Commercial Banks

• Private Sector Companies

• General Insurance Companies

• Life Insurance Companies

• Mutual Funds

• Non-banking Finance Companies

• Primary Dealers (PDs)

KDFED – Financial Markets & Institutions16

Call Money Market

• Call money market is that part of the national money market where

the day-to-day surplus funds, mostly of banks, are traded in.

• The instruments dealt in this markets are short term in nature

• They are repayable on demand

• They are highly liquid, their liquidity being exceeded only by cash.

KDFED – Financial Markets & Institutions17

CALL MONEY MARKET IN INDIA

• In India there are no separate short-term money markets but call

loans in India are given as follows:

• To the bill market

• For the purpose of dealing in the bullion markets and stock

exchanges

• Between banks and

• Frequently to individuals of high financial status

KDFED – Financial Markets & Institutions18

PARTICIPANTS

• SCHEDULED COMMERCIAL BANKS

• NON-SCHEDULED COMMERCIAL BANKS

• FOREIGN BANKS

• STATE, DISTRICT AND URBAN, COOPERATIVE BANKS

• DISCOUNT AND FINANCE HOUSE OF INDIA (DFHI)

• SECURITIES TRADING CORPORATION OF INDIA (STCI)

KDFED – Financial Markets & Institutions19

LOCATION

• Call money markets are mainly located in big industrial and

commercial centers like Mumbai, Kolkata, Chennai, Delhi and

Ahmedabad.

• Among these centers Mumbai and Kolkata are more significant

places.

KDFED – Financial Markets & Institutions 20

COMMERCIAL PAPER MARKET

https://www.slideshare.net/tatamut

ualfund/commercial-papers

KDFED – Financial Markets & Institutions 21

TYPES OF BILL OF EXCHANGE

• DEMAND BILLS – Payable immediately to the drawee

• DOCUMENTARY BILLS - The drafts are accompanied by

documents of title to goods, such as railway receipts or bill of lading.

• INLAND BILLS – Must be drawn or made in India, and must be

payable in India or drawn upon any person resident in India.

• FOREIGN BILLS – They are drawn outside India or may be payable

in and by a party outside India andd made payable outside India.

KDFED – Financial Markets & Institutions 22

Commercial bills in India

• Commercial bills may be used for financing the movement and

storage o goods between cuntries before exports and also within the

country.

• In India the use of bill of exchange appears to be in vogue for

financing agricultural operations, cottage and small scale industries,

and other commercial and trade transactions

KDFED – Financial Markets & Institutions 23

PROCESS OF BILL FINANCE

• STEP I

A bill is passed through many hands before its maturity which means

one discounting agency may discount it further with another.

• STEP II

The service of acceptance are provided by a bank or a specialised

institution on behalf of the debtors.

Maturity of Bills

• It is defined as the date on which its payment fall due.

• The normal maturity period of usance is 30 or 60 or 90 or 120 days.

KDFED – Financial Markets & Institutions 24

RBI INITIATIVES

• With effect from June 1974, the RBI has taken innovative step of

permitting scheduled commercial banks to rediscount genuine trade

bills with other commercial banks, LIC, GIC and ICICI.

• This has increased the number and type of institutions participating

in the bill market in India.

• The RBI used to prescribe a ceiling on the rate of discount at which

a bill could be discounted by banks with other commercial banks

and with approved institutions. With effect from May 1989, this

ceiling has been withdrawn by the bank.

KDFED – Financial Markets & Institutions 25

Certificate of Deposit Market

Time deposit Vs certificate of deposit

Role of DFHI and banks

Treasury Bills Market

Gilt-edged securities market

REPOS – Repo Accounting

Government bonds

KDFED – Financial Markets & Institutions 26

UNIT III – SYLLABUS

Treasury Bill Market

https://www.slideshare.net/PallaviSYadav/treasury-bills-28438392

Treasury bills, or T-bills, are short-term debt instruments issued by

the U.S Treasury. T-bills are issued for a term of one year of less. T-

bills are considered the world’s safest debt as they are backed by

the full faith and credit of the United States government.

KDFED – Financial Markets & Institutions 27

KDFED – Financial Markets & Institutions 28

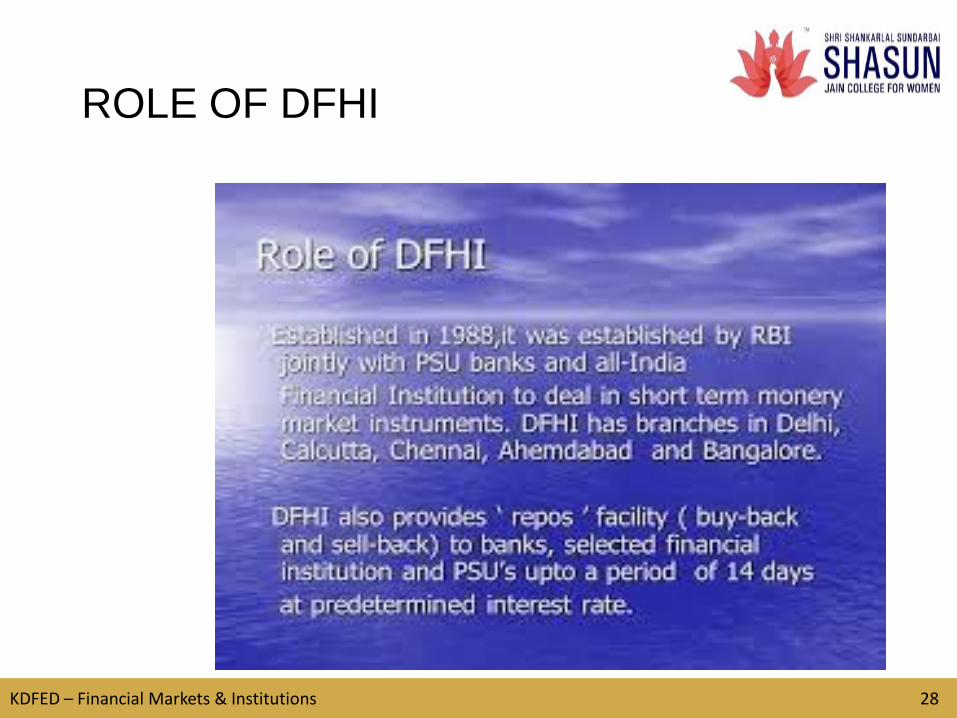

ROLE OF DFHI

Certificate of Deposits

A certificate of deposit (CD) is a savings certificate with a

fixed maturity date, specified fixed interest rate and can be

issued in any denomination aside from minimum investment

requirements. A CD restricts access to the funds until the

maturity date of the investment. CDs are generally issued by

commercial banks

KDFED – Financial Markets & Institutions 29

KDFED – Financial Markets & Institutions 30

KDFED – Financial Markets & Institutions 31

ROLES OF DFHI

Gilt-Edged Securities

• Government securities are instruments issued by the government to borrow

money from the market. They are also known as gilts or gilt edged securities

• It is created and issued by the Government for the purpose of raising a

public loan or for any other purpose as may be notified by the Government in

the Official Gazette and having one of the forms mentioned in the

Government Securities Act, 2006.

• Depending upon the expiry date, government securities are divided into

short term and long term securities.

• Short term government securities are Treasury bills. They have a maturity of

less than one year. There are three main treasury bills in India – 91 day, 182

day and 364 day.

• Long term government securities are known as government bonds or dated

securities. They have a maturity period of five years, ten years, fifteen years

etc.

KDFED – Financial Markets & Institutions 32

Features of Gilt – Edged

SecuritiesSafety

Government rarely fails financially and there is no risk for losing our money or

there is zero income default.

High Rate of Interest

In India, the G secs are allocated among the buyers through auction method.

This auction ensures competitive interest rate for government securities.

Given their zero risk default nature, the interest rate is very good for Gsecs.

Liquidity

Third feature of G secs is that they are very liquid. This is because the Gsecs

are tradable in the stock m market. High marketability and tradability gives

high liquidity for Gsecs.’

KDFED – Financial Markets & Institutions 33

Repos

https://www.icmagroup.org/Regulatory-Policy-and-Market-

Practice/repo-and-collateral-markets/icma-ercc-

publications/frequently-asked-questions-on-repo/1-what-is-a-repo/

KDFED – Financial Markets & Institutions34

Capital market

Indian money market

Indian capital market

New financial instruments

Major issues of Indian capital market

Capital market instruments

New Issues Market

NIM Vs secondary market

Intermediaries in NIM

KDFED – Financial Markets & Institutions 35

UNIT IV – SYLLABUS

KDFED – Financial Markets & Institutions36

Indian Capital Market

37KDFED – Financial Markets & Institutions 37

Indian Capital Market

Recent Initiative in Indian capital

Market

KDFED – Financial Markets & Institutions 38

Major issues in Indian Capital

Markets

http://www.greenworldinvestor.com/2013/03/07/8-major-

challenges-in-the-growth-of-the-indian-capital-market/

KDFED – Financial Markets & Institutions 39

New Issue Markets

https://www.slideshare.net/ragarwal76/new-issue-market

New Issue Market. New issues are offered in the

primary market and sold to the public for the first time as initial

public offerings, or IPOs. New issues are usually handled for a

corporation by an underwriting syndicate comprised of

investment banks and selling groups.

KDFED – Financial Markets & Institutions 40

KDFED – Financial Markets & Institutions 41

Primary Market And Secondary

Market

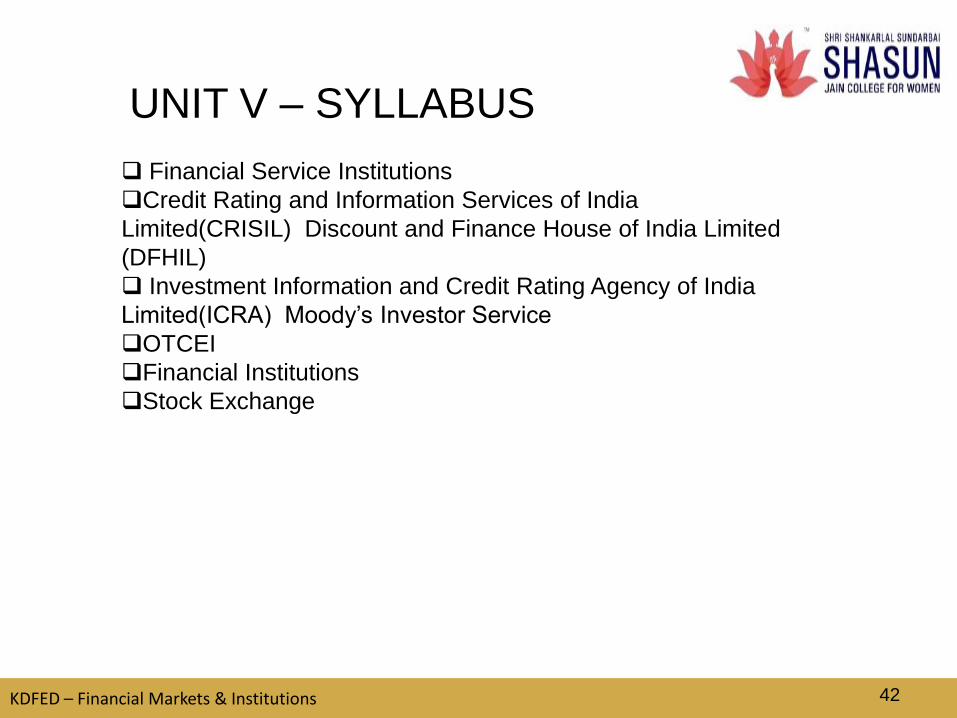

Financial Service Institutions

Credit Rating and Information Services of India

Limited(CRISIL) Discount and Finance House of India Limited

(DFHIL)

Investment Information and Credit Rating Agency of India

Limited(ICRA) Moody’s Investor Service

OTCEI

Financial Institutions

Stock Exchange

KDFED – Financial Markets & Institutions 42

UNIT V – SYLLABUS

•The Clearing Corporation of India Ltd. (CCIL) was set up in April, 2001 to

provide guaranteed clearing and settlement functions for transactions in

Money, G-Secs, Foreign Exchange and Derivative markets.

• The introduction of guaranteed clearing and settlement led to significant

improvement in the market efficiency, transparency, liquidity and risk

management/measurement practices in these market along with added

benefits like reduced settlement and operational risk, savings on settlement

costs, etc.

CCIL

KDFED – Financial Markets & Institutions 43

• CCIL also provides non-guaranteed settlement for Rupee interest rate

derivatives and cross currency transactions through the CLS Bank

• CCIL’s adherence to the stringent principles governing its operations

as a Financial Market Infrastructure has resulted in its recognition as a

Qualified Central Counterparty (QCCP) by the Reserve Bank of India in

2014.

•It has also set up a Trade Repository to enable financial institutions to

report their transactions in OTC derivatives.

KDFED – Financial Markets & Institutions 44

CCIL

Credit Rating Information

Services of India Limited•CRISIL Ratings is India's leading rating agency. They pioneered the concept

of credit rating in India in 1987.

• They rate the entire range of debt instruments: bank loans, certificates of

deposit, commercial paper, non-convertible debentures, bank hybrid capital

instruments, asset-backed securities, mortgage-backed securities, perpetual

bonds, and partial guarantees.

CRISIL they have instituted several innovations in India including rating

municipal bonds, partially guaranteed instruments and microfinance

institutions.

They pioneered a globally unique and affordable rating service for Small and

Medium Enterprises (SMEs).This has significantly expanded the market for

ratings and is improving SMEs' access to affordable finance.

KDFED – Financial Markets & Institutions45

Clients of CRISIL

• CRISIL Ratings serves lenders, investors, issuers, market

intermediaries and regulators by improving information availability

and providing benchmarks.

• They rate most of India's largest companies and several of the

smallest.

• Their ratings cover manufacturing companies, banks, non-banking

finance companies, public sector undertakings, financial institutions,

state governments, urban local bodies, mutual funds across 190

industry sectors

KDFED – Financial Markets & Institutions46

Services of CRISIL

• CRISIL's ratings assist issuers and borrowers in enhancing their access to

funding, widening the range of funding alternatives, and optimising the

cost of funds.

• Investors and lenders use the ratings to supplement their internal

evaluation process and to benchmark credit quality across investment

options.

• CRISIL ratings act as a market benchmark for pricing and trading of debt

instruments.

• They help regulators in measurement and management of credit risks at a

systemic level.

• CRISIL's ratings are used in the computation of capital adequacy in the

banking sector.

• The ratings are also used to determine the eligible investment pool for

insurance companies, pension funds, and provident funds.

KDFED – Financial Markets & Institutions 47

The Discount and Finance House

of India (DFHI)

• The RBI set up the Discount and Finance House of India (DFHI) in

Pursuance the Vaghul Working Group recommendation to provide

enhanced liquidity to the money market instruments, jointly with

public sector banks and the all-India financial institutions.

• DFHI was incorporated in March 1988 and it commenced operation

in April 1988.

KDFED – Financial Markets & Institutions 48

Objectives

• The main objective of this money market institution is to facilitate

smoothening of the short-term liquidity imbalances by developing an

active secondary market for the money market instruments. Its

authorized capital is Rs. 250 crores.

• DFHI fills this gap by buying and selling these bills in the secondary

market. The presence of DFHI in the secondary market has

facilitated corporate entities and other bodies to invest their short-

term surpluses and to en cash them when necessary.

KDFED – Financial Markets & Institutions 49

Indian Credit Rating Agency

• ICRA Limited (ICRA) is an Indian independent and professional

investment information and credit rating ageny. It was established in

1991, and was originally named Investment Information and Credit

Rating Agency of India Limited (IICRA India).

• It was a joint-venture between Moody’s and various Indian

commercial banks and financial services companies.

• The company changed its name to ICRA Limited, and went public

on 13 April 2007, with a listing on the Bombay Stock exchange and

the National Stock Exchange

KDFED – Financial Markets & Institutions 50

Indian Credit Rating

Agency

• ICRA’s credit ratings are symbolic representations of its current opinion

on the relative credit risks associated with the rated debt

obligations/issues.

• These ratings are assigned on an Indian (that is, national or local)

credit rating scale for Indian Rupee denominated debt obligations.

• Credit ratings aside, ICRA also assigns Corporate Governance

Ratings, besides Performance Ratings, Gradings and Rankings to

mutual funds, construction companies and hospitals.

KDFED – Financial Markets & Institutions 51

KDFED – Financial Markets & Institutions 52

KDFED – Financial Markets & Institutions

• Moody's Investors Service is a leading provider of credit ratings, research, and

risk analysisThe ratings and analysis track debt covers more than:130 countries

11,000 corporate issuers,21,000 public finance issuers,76,000 structured

finance obligations

•Credit ratings and research help investors analyze the credit risks associated

with fixed-income securities

•It contribute to efficiencies in fixed-income markets and other obligations, such

as insurance policies and derivative transactions, by providing credible and

independent assessments of credit risk.

Moody’s default studies validate our predictive ratings. The published research

and investor briefings draw thousands of attendees each year and keep

investors current with the rationale underlying our credit opinions.

Moody’s Investor Services

53

Standard & Poor's Financial

Services LLC (S&P)

• Standard & Poor's Financial Services LLC (S&P) is an American

financial services company.

• It is a division of S&P Global that publishes financial research and

analysis on stocks, bonds and commodities.

• S&P is known for its stock market indices such as the U.S.-based

S&P 500, the Canadian S&P/TSX, and the Australian S&P/TSX

200.

• S&P is considered one of the Big three credit-rating agencies, which

also include Moody’s Investors Services

KDFED – Financial Markets & Institutions 54

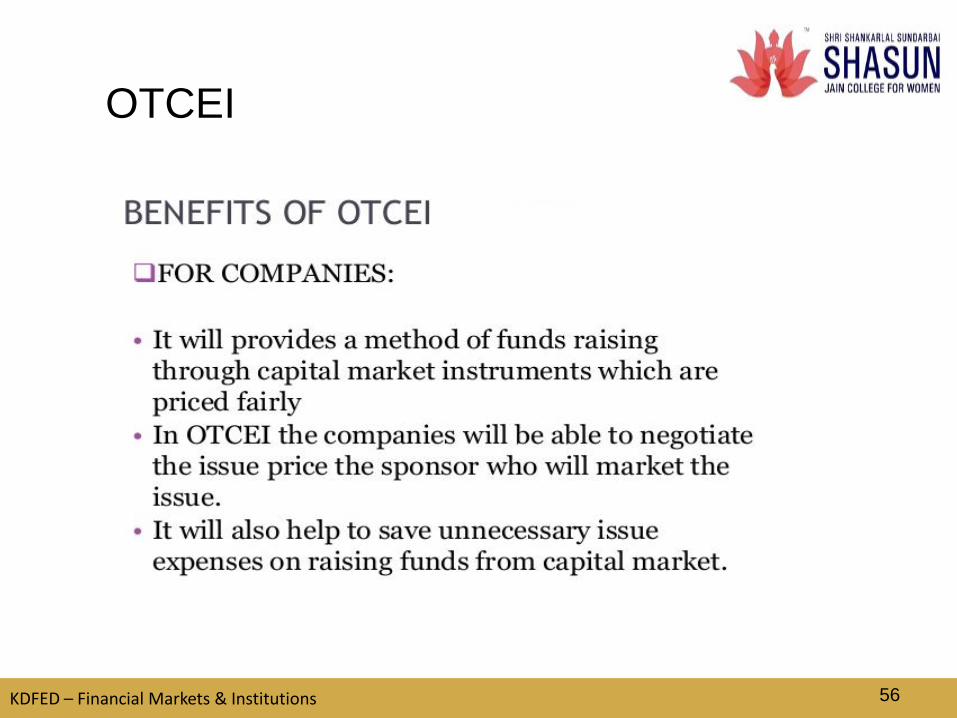

OTCEI

• The over-the-counter exchange of India (OTCEI) is an electronic

stock exchange based in India that is comprised of small- and

medium-sized firms looking to gain access to the capital

markets Like electronic exchanges in the U.S. such as the Nasdaq

there is no central place of exchange and all trading is done through

electronic networks.

KDFED – Financial Markets & Institutions 55

KDFED – Financial Markets & Institutions 56

OTCEI

KDFED – Financial Markets & Institutions 57

OTCEI

KDFED – Financial Markets & Institutions 58

OTCEI

National Securities Depository Limited (NSDL) is an Indian central

securities depository based in Mumbai It was established on 8 November

1996 as the first electronic securities depository in India with national

coverage based on a suggestion by a national institution responsible for the

economic development of India .

The enactment of Depositories Act in August 1996 paved the way for

establishment of National Securities Depository Limited (NSDL), the first

depository in India.

It went on to establish infrastructure based on international standards that

handles most of the securities held and settled in de-materialised form in the

Indian capital markets.

KDFED – Financial Markets & Institutions 59

National Securities Depository

Limited (NSDL)

In the depository system, securities are held in depository accounts, which

are similar to holding funds in bank accounts.

Transfer of ownership of securities is done through simple account transfers.

This method does away with all the risks and hassles normally associated

with paperwork.

NSDL is promoted by Industrial Development Bank Of India

Limited (IDBI), Unit Trust of India and National Stock Exchange of India

Limited (NSE)

KDFED – Financial Markets & Institutions 60

Securities Trading

Corporation of India

Limited • STCI Finance Ltd. (formerly known as Securities Trading

Corporation of India Limited), non-deposit taking NBFC registered

with Reserve Bank of India. Presently STCI Finance Ltd is classified

as a loan NBFC.

STCI Finance Limited was promoted by Reserve Bank of India in

May 1994 with the objective of fostering an active secondary market

in Government of India Securities and Public Sector bonds.

• The Company had a subscribed and paid up capital of Rs 500

crores with RBI owning the majority stake of 50.18%. In 1996, STCI

was authorized by RBI as one of the first Primary Dealers in India.

KDFED – Financial Markets & Institutions 61

Securities Trading

Corporation of India

Limited

• As the leading Primary Dealer in the country, the Company was a

market maker in government securities, corporate bonds and money

market instruments apart from carrying out proprietary trading in

equity both in the cash & derivatives (F&O) segment.

• The Company’s other lines of activities included trading in interest

rate swaps - both for hedging and market making.

• It had the distinction of achieving secondary market turnover of more

than Rs.2.00 lakh crore in sovereign paper.

KDFED – Financial Markets & Institutions 62

National Bank for Agriculture and

Rural Development (NABARD)

• National Bank for Agriculture and Rural

Development (NABARD) is an apex development financial

institution in India, headquartered at Mumbai with branches all over

India. The Bank has been entrusted with "matters concerning policy,

planning and operations in the field of credit for agriculture and other

economic activities in rural areas in India". NABARD is active in

developing financial Inclusion policy and is a member of the Allience

for Financial Inclusion.

KDFED – Financial Markets & Institutions 63

Role of NABARD• Serves as an apex financing agency for the institutions providing

investment and production credit for promoting the various

developmental activities in rural areas

• Takes measures towards institution building for improving absorptive

capacity of the credit delivery system, including monitoring, formulation

of rehabilitation schemes, restructuring of credit institutions, training of

personnel, etc.

• Co-ordinates the rural financing activities of all institutions engaged in

developmental work at the field level and maintains liaison with

Government of India, state governments, Reserve Bank of India (RBI)

and other national level institutions concerned with policy formulation

• Undertakes monitoring and evaluation of projects refinanced by it.

KDFED – Financial Markets & Institutions 64

Functions of NABARD

• NABARD refinances the financial institutions which finances the

rural sector.

• NABARD partakes in development of institutions which help the

rural economy.

• NABARD also keeps a check on its client institutes.

• It regulates the institutions which provide financial help to the rural

economy.

• It provides training facilities to the institutions working in the field of

rural upliftment.

• It regulates the cooperative banks and the RRB’s.

KDFED – Financial Markets & Institutions 65

https://www.slideshare.net/avinashvarun2/stock-exchange-simple-

ppt

Functions of Stock Exchange

KDFED – Financial Markets & Institutions 66