Embed Size (px)

Citation preview

KBC Bank & Insurance Group

General Investor PresentationJune 2002

2

KBC Bank & Insurance Group

ProfileStrategyFuture Profit DriversInvestor Considerations

3

KBC Bank & Insurance GroupKey features

Ranking Belgium 3rd fin.

group Bank 3rd Insurance (overall) 3rd

Europe : Bank (Tier-1 capital) 27 th : Group (market cap) 30 th

Staff 42 700 Belgium 20 700 Abroad 22 000

Customers in first home market (Belgium) +/- 3.5

million in second home market (Central Europe) +/- 5.7

million

Domestic network bank branches (KBC +CBC) 1 200 independent insurance agencies: 684

Worldwide presence 30 countries

4

Almanij NV

KBC Bank & Insurance

Holding NV

KBC Bank KBC Insurance

67.9%

100%100%

32% FreeFloat

KBC Asset Man45%

55%

KBC Bank & Insurance Group Group structure

Cera Holding Almancora Flemish Families MRBB9.3% 16.6%15.8%28.3%

FreeFloat

26%

5

KBC Bank & Insurance GroupOverall business characteristics

Good track record in profitability

Solid solvency ratio’s

Diversified but balanced business income

Good asset quality

Strong market shares

Success in bancassurance

Successful expansion in Central Europe

6

KBC Bank & Insurance GroupGroup profit and profitability

798

970

355 316

10221166

1998 1999 2000 2001 1Q01 1Q02

Net profit ROE

+12.8%

+21.6%

16.1%

20.5%23.3%In

mill

ions

of

EU

R

+20.2%

-12.3%

17.3% -11.1%

15.9%

7

KBC Bank & Insurance GroupSustained solid solvency ratios

2000

Bank Tier-1 ratio CAD ratio

Insurance (*) Solvency ratio

7.2%

11.5%

311%

9.5%

16.0%

307%

(*) excluding unrealized capital gains

1998

7.4%

12.8%

298%

1999 2001

8.8%

14.7%

318%

1Q 02

9%

14.9%

323%

8

KBC Bank & Insurance GroupStrong homebase for expansion abroad

Profit contributionby group entity

Insurance35% Holding - 3%

Normalized profit contribution by region

Banking 70%

USA 2.5%

Belgium 66%

West. Eur 17%

Cent. Eur 12%

Asia 2.5%

9

KBC Bank & Insurance GroupDiversified but balanced business income

Gross operat. income banking4 977 m EUR (FY 2001)

Net interest income 53%

Commission income

21%

Other incomebanking 8%

Gross premium earned insurance2 570 m EUR (FY 2001)

Trad. life 18%

Profit Fin.Transact. 18%

Non-life 34%

Unit-linked 48%

10

Good asset quality in banking

2000

Loan loss ratio Non performing ratio

0.38%

2.1%

0.40%

2.1%

1999 2001

0.36%

2.8%

1Q 02

0.34%

2.9%

11

KBC Bank & Insurance Group

ProfileStrategyFuture Profit DriversInvestor Considerations

12

KBC’s strategic intent

… creating sustainable value for shareholders

A bancassureur and financial service provider in Europe

… in a standalone position

Activity portfolio

Ambitious financial targets

Corporate scaleCapital generation

13

A focused but diversified activity portfolio

Focus on 4 activities- Retail bancassurance- Corporate services- Asset Management- Market activities

Focus on Europe- Belgium : home market- Central Europe : second home market- Western Europe : smaller countries/regions

Focus on local clients- Retail- SME- Selected corporates

Profit contribution (avg 2000-2001)

12% Central Europe

36% Retail

16% CorporateServices

9% Asset Management

12% Market Activities

15% Group

14

Strategic objectives per activity

Retail bancassurance Increase cross-selling in Belgium Creation of a second home market in Central Europe and implement bancassurance concept

Asset Management Increase AUM Expand distribution network

Market activities Create European corporate finance / brokerage platform for SME’s

Corporate Services Strategic reduction of risk weighted assets Scale down exposure on large multinationals Refocus on SME’s and a selection of larger corporates

15

Target Realized Q1 2002

ROE at group level

EPS growth

Cost/income ratio bank

Combined ratio insurer

min. Tier-1 ratio bank

min. CAD ratio bank

min. Solvency ratio insurer

20%

15% (1)

55% (2)

103% (2)

7%

11%

200%

15.9%

-11.8%

65.4%

102%

9%

14.9%

323%

Overall financial targets

(1) average over the period 2000-2004

(2) by 2004

16

Cost of capital

Focus on shareholder value

Retailbancassurance

Corporate services

Asset management

Market activities

Central Europe

TOTAL at operational level

TOTAL at group level

8.5%

10.5%

8%

11.5%

13%

10 %

-

ROE targetROE Targets per activity

20.0%

12.5%

13.0%

21.0%

15.0%

17%

20%

ROE target per activity based on 2 x cost of capital Reallocation of capital from activities with low or volatile ROE to

activities with high or stable ROE

(*)

(*)

(*) Interim target

17

Considerations on the level of corporate scale

Partnership, outsourcing Focus on retailing (less susceptible for scale effects) Focus on SME Risk avoidance, rational capital management Strongly tied up with local market / culture Low 'complexity' costs, cost efficient group structure

Non-evident scale effects on financial performance

Opportunities for a mid-scale player in Europe

Market cap. Tier-1 Cost/Income

EUR 5 – 10 bn10 – 15 bn15 – 20 bn20 – 30 bn30 – 50 bn

> 50 bn

6.7%7.2%6.5%8.1%7.7%7.4%

68%74%65%73%74%71%

(Source: Bloomberg, 65 – European banks / insurers)

18

External growth capacity

Group Capital Planning ( bn. EUR)

1Q02 2004 Hypothesis

Target Ratio Excess Dividend payout 40%

2002: 34% stake NLB

Potential increase participation Warta

Bank Tier 1 7.0% 9.0% 1.9 bn EUR

Insurance Solv. 200% 323% 0.5 bn EUR

Excess capital (strictu senso) 2.4 bn EUR 3.5 bn EUR

Unrealized capital gains (shares) Capital increase (dilution of Almanij to 51%) Additional leveraging holding

potential excess capital of 12 bn. EUR

(broad sense)

19

KBC Bank & Insurance Group

ProfileStrategyFuture Profit DriversInvestor Considerations

20

KBC Bank & Insurance Group Key future profit drivers

Full realization of merger in Belgium

Upside potential of bancassurance in Belgium

Development of second home market in Central Europe

Continue growth in Asset Management

21

Important merger effects on cost efficiency

57

122

205225

0

50

100

150

200

250

2002 2003 2004 2005

KBC Bank N.V. (Belgium) Target Start End Realised to date

Closure of bank branches 650 1999 2004 62%

Account migration (ICT-platform) All 2000 2003 81%

Headcount reduction 1 650 2001 2004 32%

Expected cost savings (m EUR)

22

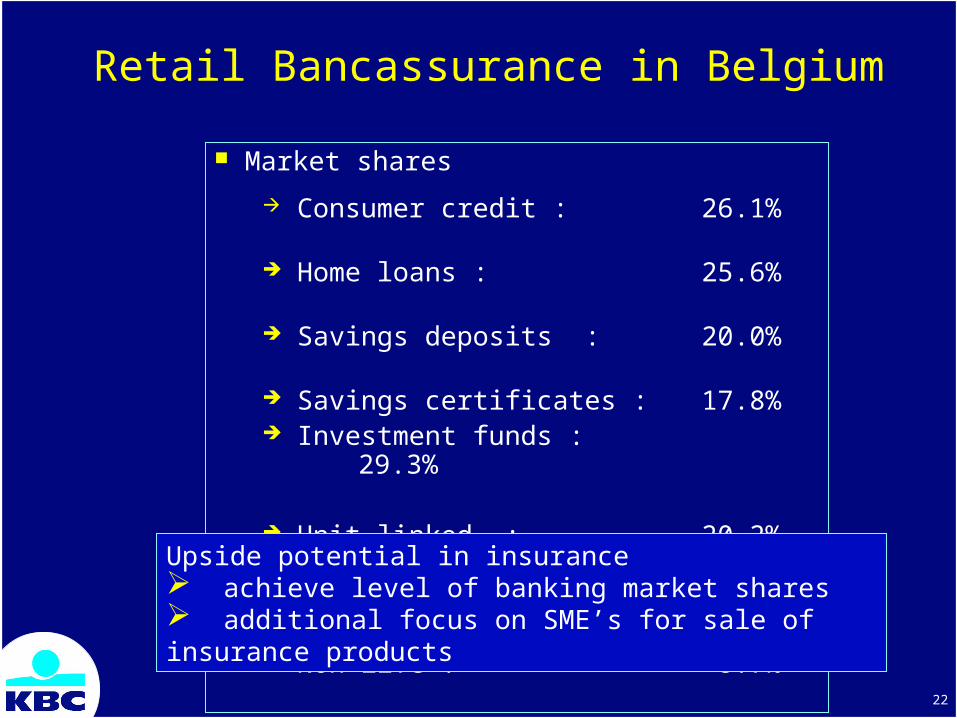

Retail Bancassurance in Belgium

Market shares

Consumer credit : 26.1%

Home loans : 25.6%

Savings deposits : 20.0%

Savings certificates : 17.8% Investment funds : 29.3% Unit-linked : 20.2%

Traditional life : 5.5%

Non-life : 8.7%

Upside potential in insurance achieve level of banking market shares additional focus on SME’s for sale of insurance products

23

Retail bancassurance Belgium

171 000

555 000

762 000

1 527 000

Retail customers

Stable banking customers

Bancassurancecustomers

Market sharebanking20 à 25%insuranceca. 11%

Stable bancassurancecustomers

40%

15%11%

36%

50%

100%

Min. 3 banking products (*)

Min. 1 banking and 1 insurance

product (*)

Min. 3 banking and 3 insurance

products (*)

Immediatetargets

(*) out of a range of 6 banking products (current account, savings account, mortgage loan, credit card, …)

and 6 insurance products (car, home, health, life, …)

24

Strategy for Central Europe

Strategy Create a second homemarket in future EU member

countries

Focus on Countries with highest transition indices Banks with a significant market share and acceptable

asset quality Acquisitions of non-life insurance companies but

mainly greenfield operations for life insurance

Introduction of KBC’s bancassurance concept Acquired banks are to be universal banks with an

important retail activity Life insurance to be sold through banknetwork Non-life insurance mainly to be sold through agents

25

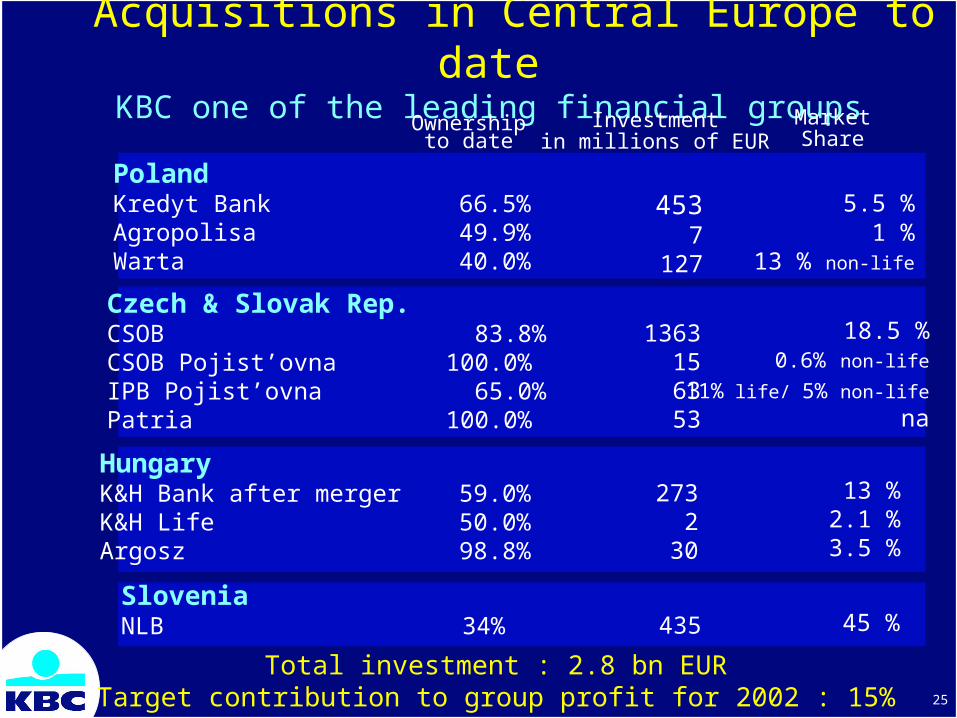

Acquisitions in Central Europe to dateKBC one of the leading financial groups

PolandKredyt BankAgropolisaWarta

Czech & Slovak Rep.CSOBCSOB Pojist’ovnaIPB Pojist’ovnaPatria

HungaryK&H Bank after mergerK&H LifeArgosz

66.5% 49.9% 40.0%

83.8%100.0% 65.0% 100.0%

59.0%50.0% 98.8%

Ownership to date

4537

127

1363156353

2732

30

Investmentin millions of EUR

Total investment : 2.8 bn EURTarget contribution to group profit for 2002 : 15%

5.5 %1 %

13 % non-life

18.5 %0.6% non-life

11% life/ 5% non-life

na

13 %2.1 %3.5 %

MarketShare

SloveniaNLB 34% 435 45 %

26

Growth potential Central Europe

Belgium1st home market

Central Europe2nd home market

- Hungary- Czech Rep.- Slovakia- Poland

- Slovenia

Gross operating income:expected annual growth to 2004 of ca. 20%

Planning assumptions: Increasing penetration

banking/insurance(currently 40-45% of EU-average)

Faster GDP-growth than EU (2002e: 2 times real EU-average)

Increase in market share via bancassurance concept

27

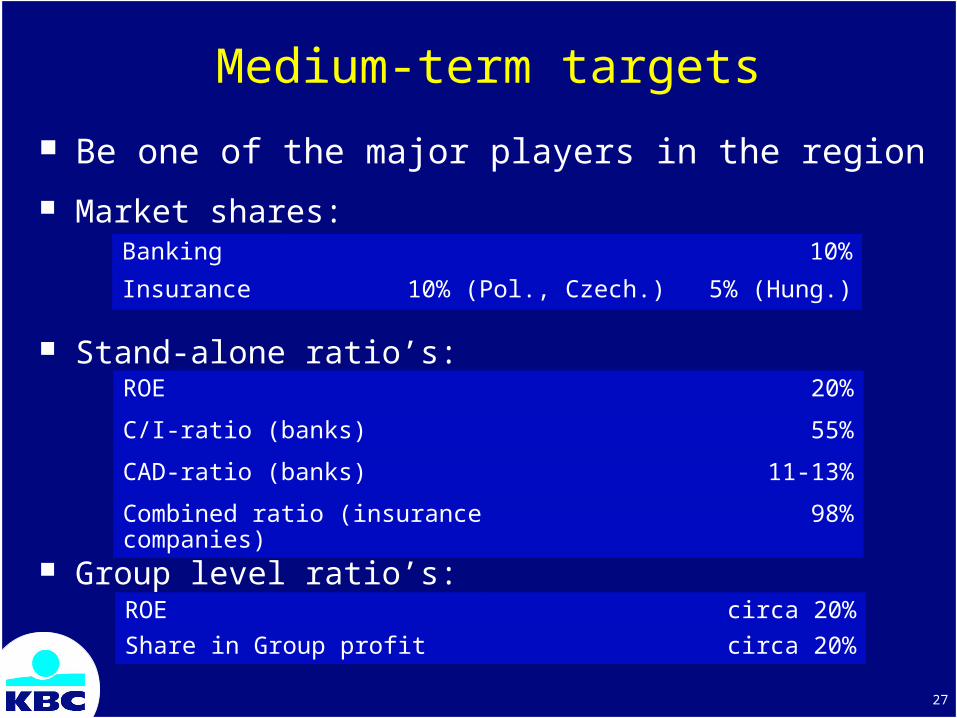

Medium-term targets

Be one of the major players in the region

Market shares:

Stand-alone ratio’s:

Group level ratio’s:

Banking 10%

Insurance 10% (Pol., Czech.) 5% (Hung.)

ROE 20%

C/I-ratio (banks) 55%

CAD-ratio (banks) 11-13%

Combined ratio (insurance companies) 98%

ROE circa 20%

Share in Group profit circa 20%

28

Asset ManagementFurther growth in assets under management

27.4

4.64.8

34.5

12.2

5.3

40.2

24.3

5.1

42.2

24.3

4.7

43

24.8

5.1

1998 1999 2000 2001 1Q02

36.8 (+18.3%)

51.9 (+41%)

In b

n.

EU

R

69.6 (+34.1%)

Private Banking Institutional funds

Mutual funds

% of total AUM 2000 2001 1Q02

71.1 (+2.2%)

7%34%59%

7%35%58%

72.9 (+2.5%)

7%34%59%

29

KBC Bank & Insurance Group

ProfileStrategyFuture Profit DriversInvestor Considerations

30

KBC Bank & Insurance GroupInvestor considerations

Strenghts Strong domestic market shares Diversified income Unique bancassurance concept Sound solvency ratios Good profitability track record

Opportunities Merger effects to materialize Strategy in Central Europe and

future return Investment of excess capital Low valuation

Weaknesses Still high cost/income ratio Low profitability of i.a.

corporate services Volatility of niche market

earnings

Threats Low free float High cost of capital Consolidation in Europe

31

19991998

Net profit

P/E

Gross dividend

Pay-out ratio

Net asset value

Price / NAV

2.69

25.0

1.09

40.6%

32.3

2.1

3.26

16.4

1.23

37.7%

33.8

1.6

2000

3.90

11.8

1.42

36.4%

35.2

1.3

KBC Bank & Insurance GroupKey figures per share

2001

3.39

11.1

1.48

43.6%

33.8

1.1

32

KBC Bank & Insurance Holding NVStock market info

Market cap : 12.5 bn. EUR

Number of outstanding shares : 302 000 000 Free float : 32 %

Listed on Euronext Brussels Included in following indices : Euronext 100,

Bel-20,Eurostoxx Financials, MSCI World Index, FTSE300 Financials

Sell-side analyst coverage : +/- 25 analysts

33

KBC Bank & Insurance GroupShareholder composition

Total number of shares : 302 000 000

Belg. instit. Invest. 8 %

Almanij 68 %

Unidentified 9 %

Other group cies. 3 %

Personnel 2 %

Belgian retail invest. 5 %

UK 3 %

USA 2 %

KBCBank & Insurance Group

June 2002