Embed Size (px)

Citation preview

Estate Planning for Farm Families Katie E. Watson, J.D., LL.M.

Friday, Eldredge & Clark, LLP

Topics

Incapacity

Terminally Ill

Asset Disposition

Advanced Planning Techniques

Farm Specific Planning Techniques

Incapacity

Overview - Incapacity

Durable General Power of Attorney

Durable Power of Attorney for Health Care

Durable General

Power of Attorney

Incapacity - DGPOA

Durable

Power of Attorney (“POA”) is not affected by

subsequent disability or incapacity.

Current POA or Springing POA

Should be acknowledged.

Incapacity - DGPOA

Specific Powers

Safe deposit box

Create, revoke and/or amend revocable trust.

Alter beneficiary designations.

Make gifts to family or charity.

Must specifically reference these powers in the

instrument.

Incapacity - DGPOA

Conservator or Guardian

POA may nominate conservator or guardian.

Attorney-in-fact is held accountable to

conservator or guardian.

Conservator or guardian can revoke or amend

POA.

In sum, conservator or guardian trumps POA.

Incapacity - DGPOA

Multiple Attorneys-in-Fact

Default rule: majority vote

Instrument can provide otherwise.

Unanimously, majority or individually?

Incapacity - DGPOA

Revocation

By agent, principal or death

Newer POA does not revoke prior POA unless

specifically stated.

Notify anyone holding prior POA that you have

revoked such POA.

Incapacity - DGPOA

Substitutes

Trust

Joint ownership

Business agreements

Some retirement plans

Durable Power of

Attorney for

Health Care

Incapacity – Health Care

“Health Care”

All care, treatment and procedures

Does not include decisions regarding life-

sustaining treatment, but it may contain a

declaration as to such treatment.

Incapacity – Health Care

Formalities

Written

Signed

2 witnesses

Should be acknowledged.

Incapacity – Health Care

Appointed agent takes precedent over others.

HIPAA authorization (federal)

Unanimously, majority or individually?

Incapacity – Health Care

Revocation

By agent or principal

Newer HCPOA does not revoke prior HCPOA

unless so stated.

Notify anyone holding prior HCPOA that such

HCPOA has been revoked.

Terminally Ill

Overview – Terminally Ill

Declaration to Physicians (“Living Will”)

Proxy

Do Not Resuscitate

Declaration to

Physicians

“Living Will”

Terminally Ill - Declaration

Declaration to Withhold or Withdraw Life-

Sustaining Treatment

Written, signed and 2 witnesses (should be

acknowledged)

Effective when in a terminal condition or

permanently unconscious as determined by

attending physician and another physician.

Terminally Ill - Declaration

Declaration to Withhold or Withdraw Life-

Sustaining Treatment (continued)

If given to care provider, part of medical record

and care provider must promptly notify if

unwilling to comply and patient must be

promptly transferred.

Other clear and convincing evidence of wishes

allowed in addition to written declaration.

Terminally Ill - Declaration

Revocation of Declaration

At any time and in any manner, without regard

to physical or mental condition

Notify anyone holding prior declaration.

Terminally Ill - Declaration

Comfort and Care

Always provide treatment for nutrition and

hydration (can be waived or is waived if

insertion of apparatus is required unless use of

artificial means is specified) and the comfort,

care or alleviation of pain.

Proxy

Terminally Ill - Proxy

Proxy

Gives authority to another to make decisions.

Unanimously, majority or individually?

Surrogate can be appointed by health care

provider.

Terminally Ill - Proxy

No Proxy

Legal guardian

If unmarried minor – parents

Spouse

Majority of adult children participating

If adult – parents

Majority of adult siblings participating

Loco parentis

Majority of adult heirs participating

Do Not

Resuscitate

Terminally Ill - DNR

Approved Identification

Standardized card, form, necklace or bracelet

Identifies existing declaration addressing CPR; or

Issued by attending physician.

Questions?

Asset Disposition

Overview - Disposition

Title

Designation

Trust

Will

Default

Title

Asset Disposition - Title

Title (not subject to will or probate)

Joint property with survivorship passes to

survivor, regardless of what your estate

planning documents say.

Name on account, then can withdraw

everything (best not to add names to accounts

as this can defeat your testamentary plan)

Designation

Asset Disposition - Designation

Designation (not subject to will or probate)

Life insurance

Retirement account

Payable on death or transfer on death

accounts

Beneficiary deed for real estate

Trust

Asset Disposition - Trust

Trust (not subject to will, probate, POA or

guardian)

Must transfer assets to the trust.

Name trust as designated beneficiary of life

insurance, retirement accounts, other accounts

and real estate.

Asset Disposition - Trust

Revocable trust benefits

Avoid probate (to the extent assets are

transferred to the trust)

Privacy (does not have to be filed with the

court)

Avoid guardianship

Tax savings (basis and estate)

Joint planning (“freeze” the overall plan)

Asset Disposition - Trust

Irrevocable Trust Benefits

Asset protection

Removes assets and future appreciation from

estate and possibly future estates.

Your terms (control)

Spendthrift trust (creditors and in-laws)

Charitable trusts

Will

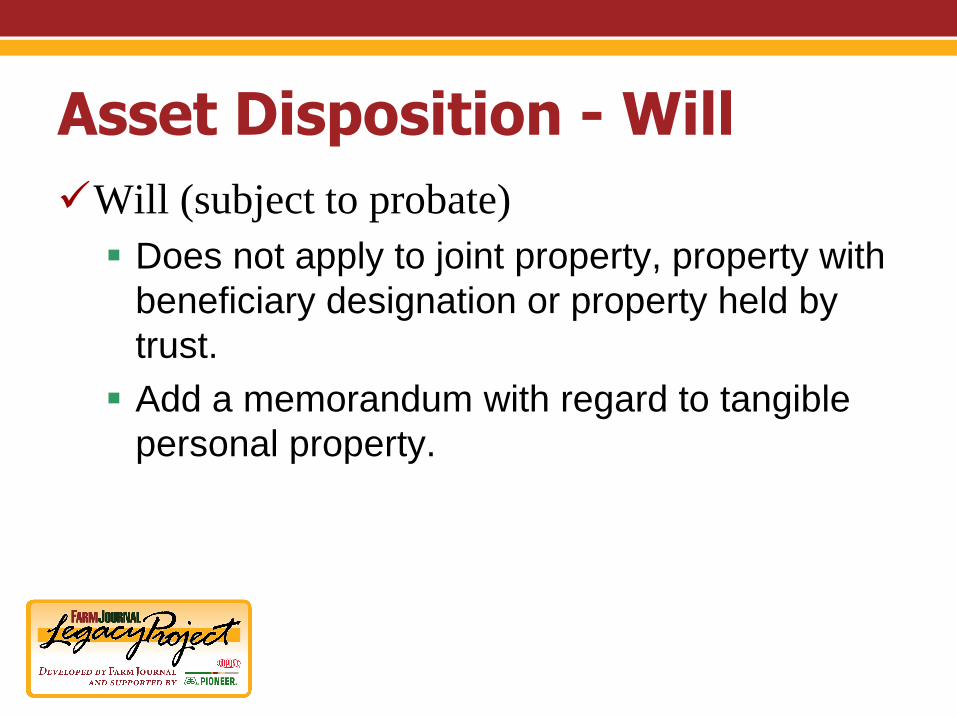

Asset Disposition - Will

Will (subject to probate)

Does not apply to joint property, property with

beneficiary designation or property held by

trust.

Add a memorandum with regard to tangible

personal property.

Default

Asset Disposition - Default

No will, trust, joint ownership or designation

Home and 1/3 of all other property to spouse

(real property for life only)

Remainder (or if no spouse) to:

Descendants, or, if none,

All to spouse, or, if none,

All to parents, or, if none,

All to descendants of parents.

Asset Disposition - Default

Reasons to have a Will or Trust

Name your executor, trustee and guardian.

Alter the disposition on previous slide.

Provide for trusts instead of outright

inheritance.

Questions?

Advanced

Planning

Techniques

Overview

Current Tax Exemptions

Discounts and Freezes

Maximizing Tax Basis

Life Insurance Trust

Asset Protection Trust

Current Tax

Exemptions

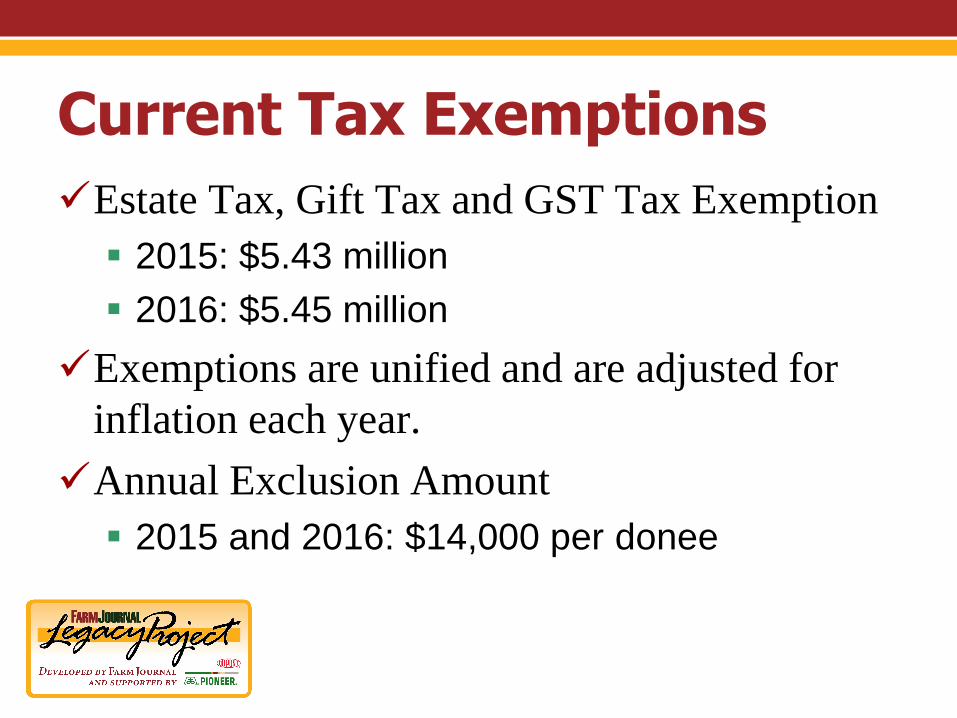

Current Tax Exemptions

Estate Tax, Gift Tax and GST Tax Exemption

2015: $5.43 million

2016: $5.45 million

Exemptions are unified and are adjusted for

inflation each year.

Annual Exclusion Amount

2015 and 2016: $14,000 per donee

Discounts and

Freezes

Discounts and Freezes

Discount Valuation on Transfer

Separate control from value transferred (i.e., limited

partnership, voting/non-voting stock)

Transfer non-controlling interest

Transfer non-marketable interest

Retaining control, if desired (can create problems if not

done correctly)

Avoid discounts if no estate tax (higher basis)

Congress could limit

Discounts and Freezes

Freeze Estate Value

If no gift tax exemption or desire future cash

flow, then transfer by sale (outright or to trust).

Gifts avoid all future appreciation.

Sales avoid future appreciation that is greater

than the imputed interest on promissory note

(currently the AFR is very low).

Can gift note as exemption increases.

Maximizing

Income Tax Basis

Income Tax Basis

Include Maximum Amount in Estate of First

Spouse to Die

Joint revocable trust for married persons to

include all assets in estate of first-to-die.

General power of appointment held by first-to-

die over other spouse’s revocable trust.

Transfers to dying spouse

Income Tax Basis

Assets held in irrevocable trust may not qualify

for FMV basis on death of beneficiary.

Make distributions of appreciated assets

outright to beneficiary prior to death.

Include contingent general power of

appointment to cause inclusion in beneficiary’s

estate.

Life Insurance

Trust

Life Insurance Trust

Death Benefit Included

For estate tax, incident of ownership includes death

benefit.

Three-year rule on gift of policy

If policy is gifted, must survive 3 years to avoid

inclusion of death benefit.

Alternative is to sell policy to avoid 3-year rule (grantor

trust can be used to avoid income tax issues).

Life Insurance Trust

Irrevocable Trust

Trust is the owner and beneficiary of the policy (trust is

the initial purchaser or purchases policy from grantor).

Insured cannot be a beneficiary (spouse of insured can

be a beneficiary).

Insured cannot be a trustee with regard to the policy

and must be limited with regard to replacing such

trustee.

Life Insurance Trust

Premium Payment

Premium payments are paid by (or on behalf of) the

trust.

Contributions to the trust are gifts.

Grantor and spouse can use annual exclusion gifts to

fund the trust (need Crummey powers).

Life Insurance Trust

Proceeds Death benefit is paid to trust and is excluded from the

insured’s estate.

Asset protection applies as long as proceeds are held in

trust.

If lifetime trusts for children, then GST exemption is

allocated to all contributions even if all contributions were

annual exclusion gifts.

Can use proceeds to buy assets out of insured’s estate.

Asset Protection

Trust

Asset Protection Trust

Beneficiary’s Creditors

If no spendthrift, then a court may authorize reaching a

beneficiary’s interest in the trust.

Spendthrift Provision

Must restrain voluntary and involuntary transfers.

Saying “spendthrift” in the trust works.

If spendthrift, then beneficiary’s interest may not be

reached unless distribution is made.

Asset Protection Trust

Discretionary Trusts

Creditors cannot compel discretionary

distribution even if it is subject to a standard or

the trustee has abused its discretion.

Interest of a beneficiary who is also a trustee

may not be reached if the trustee’s discretion is

limited by an ascertainable standard.

May vs. shall

Asset Protection Trust

Claims Against Settlor

Revocable Trust (with or without spendthrift)

During settlor’s lifetime, subject to creditors

Irrevocable Trust (with or without spendthrift)

Maximum amount that can be distributed to settlor

If more than one settlor, only settlor’s contributions can be

reached.

Power of Withdrawal (same as revocable trust)

Asset Protection Trust

Overdue Distribution

With or without spendthrift, creditors may reach

undistributed mandatory distributions.

Asset Protection Trust

Portability Election

Allows surviving spouse to use most recent

deceased spouse’s unused gift/estate tax

exemption (both spouses must die after

12/31/10).

Estate of deceased spouse must file a

complete and timely estate tax return (election

is default position if return is filed).

Asset Protection Trust

Better to not rely on portability

No asset protection

No control over future dispositions

Future appreciation is included in survivor’s estate

Portability may not last

Must file complete and timely estate tax return to make

election

Remarriage/divorce could reduce amount available

Questions?

Farm Specific

Planning

Farm Specific Planning

Formation of an entity (or multiple entities)

Create operations entity and land entity

Liability protection (injuries on the farm,

lawsuits)

Valuation discounts

Transfer restrictions

754 election

Farm Specific Planning

Farming heirs vs. non-farming heirs

Allocate farm to farming heir(s) to the extent

possible; non-farming heir(s) receive other

assets and/or a non-controlling/non-voting

interest in the farm.

Give farming heir(s) the option to purchase any

portion of the farm not allocated to their share.

Buy-sell agreement; restrictive transfers

Farm Specific Planning

Special Code provisions

Special use valuation under I.R.C. § 2032A

Must meet certain requirements.

Maximum value adjustment for 2015: $1.1 million

Extended time to pay estate tax under I.R.C. §

6166

Must meet certain requirements.

IRS serves as lender.

Questions?