Embed Size (px)

Citation preview

Founded in 1852 by Sidney Davy Miller

MICHIGAN: Ann Arbor Detroit Grand Rapids

Howell Kalamazoo Lansing Monroe

Saginaw Troy

New York, NY Pensacola, FL

Washington, DC

CANADA: Windsor, ONSHERRI A. WELLMAN TEL: (517) 483-4954 FAX: (517) 374-6304 E-MAIL: [email protected]

One Michigan Avenue, Suite 900 Lansing, Michigan 48933

TEL: (517) 487-2070 FAX: (517) 374-6304

www.millercanfield.com

POLAND: GdyniaWarsaw Wrocław

June 7, 2013

Ms. Mary Jo Kunkle Executive Secretary Michigan Public Service Commission 6545 Mercantile Way, Suite 7 Lansing, MI 48911 Re: Michigan Gas Utilities Corporation 2014 Rate Case

MPSC Case No. U-17273 Dear Ms. Kunkle: Attached for filing are an Application, draft Notice of Hearing, and supporting Direct Testimony, Exhibits, and Workpapers of Katherine A. De Cramer, Matthew M. Dirksen, Christine M. Phillips, Noreen E. Cleary, Chuck F. Hauska, Brian E. Kage, Michael E. Gerth, Tracy L. Kupsh, Lisa J. Gast, Paul R. Moul, Joylyn C. Hoffman Malueg, David J. Tyler, and John R. Wilde. Also attached is documentation which complies with the Rate Case Filing Requirements established by the Commission’s Orders dated December 23, 2008 and February 20, 2009 issued in Case No. U-15895. Very truly yours, SAW/djk Sherri A. Wellman Enclosures cc with enc: David J. Kyto, PE, CMA

STATE OF MICHIGAN

BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION

* * * * * In the matter of the application of ) MICHIGAN GAS UTILITIES CORPORATION ) for authority to increase retail natural gas rates. ) Case No. U-17273 )

APPLICATION

MICHIGAN GAS UTILITIES CORPORATION (“MGUC”), requests authority from the

Michigan Public Service Commission (“Commission”) to increase its rates for the sale and

transportation of natural gas, and other relief, and in support thereof respectfully represents

as follows:

INTRODUCTION

1. MGUC is a public utility engaged in the purchase, storage, transportation,

distribution and sale of natural gas to approximately 166,000 customers in 147 communities

in the Southern and Western portions of Michigan’s Lower Peninsula.

2. MGUC is a corporation organized under the laws of the state of Delaware,

with its principal office located at 899 S. Telegraph Road, Monroe, Michigan 48161, and is

authorized to transact business in the state of Michigan. MGUC is a subsidiary of Integrys

Energy Group, Inc. (“Integrys”), which prior to February 21, 2007, was known as WPS

Resources Corporation (“WPSR”). MGUC is a sister utility company to Upper Peninsula

Power Company and Wisconsin Public Service Corporation, both of which are also

regulated by this Commission. MGUC is also a sister utility company to, among others,

Minnesota Energy Resources Corporation, The Peoples Gas Light and Coke Company, and

North Shore Gas Company, none of which is regulated by this Commission. MGUC was

acquired by WPSR from Aquila, Inc. on April 1, 2006 as authorized by the Commission’s

- 2 -

order in Case No. U-14657. Prior to its acquisition by WPSR, MGUC conducted business

as “Aquila Networks – MGU”.

3. MGUC’s retail natural gas sales and transportation business is subject to the

jurisdiction of the Commission pursuant to 1909 PA 300, as amended, MCL 462.2 et seq.;

1919 PA 419, as amended, MCL 460.51 et seq.; 1939 PA 3, as amended, MCL 460.1 et

seq.; 1982 PA 304, as amended, MCL 460.6h et seq.; 1969 PA 306, as amended, MCL

24.201 et seq.; and the Commission’s Rules of Practice and Procedure, as amended, 1999

AC, R 460.17101 et seq.

4. In its last general rate case for retail natural gas service, Case No. U-15990,

MGUC used a 2010 test year. A settlement was reached and approved by the Commission

in its Order Approving Partial Settlement Agreement dated December 16, 2009. This order

granted rate relief of $3.5 million annually, based on a 10.75% return on common equity,

effective January 1, 2010.

5. MGUC’s rates established in Case No. U-15990 do not reflect the current

costs of providing retail gas service, and MGUC requires further rate relief.

REQUESTED RELIEF

6. For purposes of this case, MGUC has undertaken a complete examination of

its investments, expenses and revenues based on a 2014 test year. Using a 2014 test year,

and a return on common equity of 10.75%, MGUC calculates a rate revenue deficiency of

$8,036,820, or 6.01%. The key factors contributing to the revenue deficiency results

include:

a. The 2012 historic test year indicates that MGUC suffered a revenue deficiency of $6,301,860, which corresponds to a 6.14% return on common equity. This value is well below MGUC’s authorized return on common equity of 10.75% authorized in MGUC’s most recent general rate case proceeding in Case No. U-15990.

b. The cost of upgrades to the MGUC gas transmission and distribution systems,

c. A decrease in margin revenues,

- 3 -

d. A higher cost of capital;

e. Increased costs associated with filling employee vacancies,

f. Increased costs associated with building maintenance,

g. The cost of engineering analysis on vintage natural gas transmission and

distribution mains,

h. Increased costs of customer service functions, and

i. General inflation.

7. MGUC represents that in order to establish rates for natural gas service

which are just and reasonable, it is essential that the Commission order an increase in

natural gas base rates that will produce additional revenues on an annual basis of

approximately $8,036,820, or 6.01%.

8. MGUC represents that its present return on investment is and will be below

that required by sound regulation; that MGUC’s present natural gas rates and charges, if not

increased, will produce increasingly inadequate natural gas revenues to MGUC and, thus,

are unjust and unreasonable; that rate relief is required to permit MGUC to continue to

achieve its goal of rendering adequate natural gas service to the public; and that rate relief,

effective in the near future, is necessary to protect the rights of MGUC and to prevent it from

being deprived of its property contrary to the Fourteenth Amendment of the Constitution of

the United States of America and contrary to the provisions of the Constitution of 1963 of the

State of Michigan.

RATE DESIGN, TARIFF AND OTHER PROPOSALS

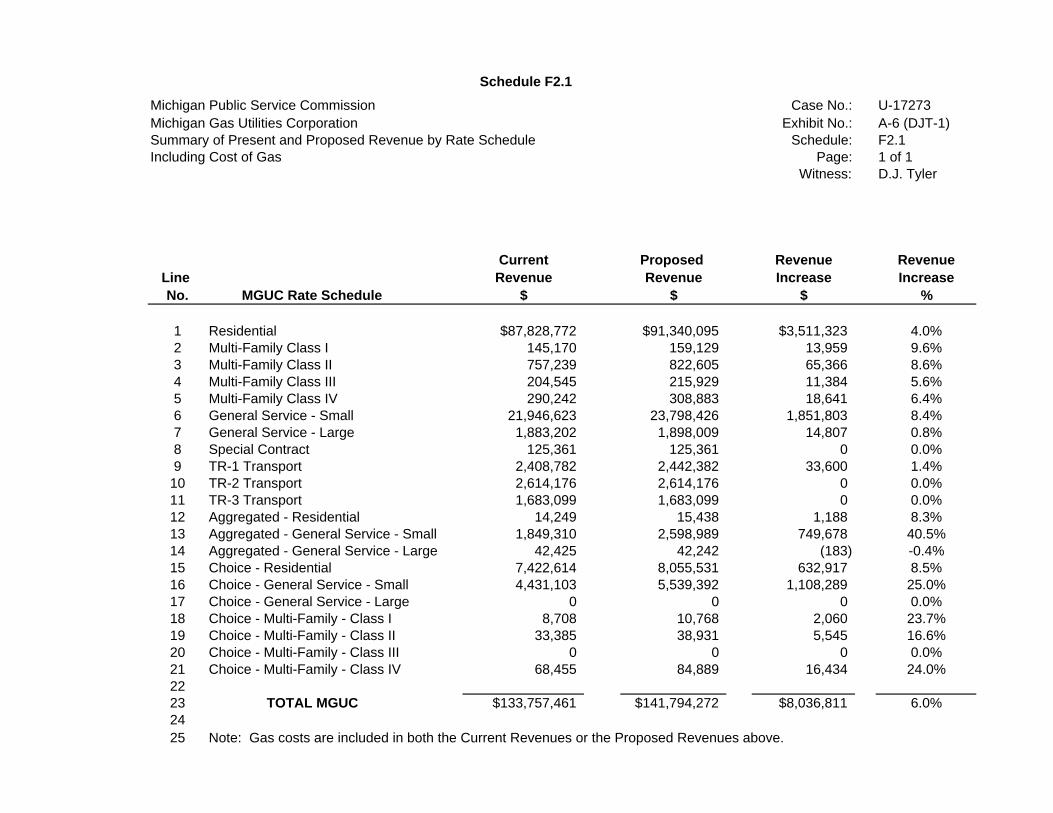

9. MGUC’s proposed rate increases by rate schedule are shown on Schedules

F3.1 and F3.2 of Exhibit A-6 (DJT-1). These rates are designed to recover the revenue

deficiency. Furthermore, MGUC also requests authority from the Commission to continue its

currently authorized revenue decoupling mechanism, as initially authorized in Case No. U-

- 4 -

15990. This plan helps stabilize MGUC’s revenues from the impacts of the economy,

energy efficiency, and other factors.

10. MGUC also requests the authority from the Commission to continue its

Uncollectible Expense True-Up Mechanism (“UETM”), as ordered in Case No. U-15990.

The UETM helps to stabilize MGUC’s uncollectibles expense. Given the state of the

Michigan economy and the MPSC rules regarding shut-off, continuation of the UETM is

reasonable and necessary.

11. In addition, MGUC proposes revisions to its tariffs to reflect the change in

rates.

IMPLEMENTATION OF RATES

12. In accordance with MCL 460.6a(1), if the Commission has not acted on the

Company’s application within 180 days of the filing, MGUC intends to implement interim

rates for service rendered on and after January 1, 2014, up to the amount of the proposed

annual rate request, through equal percentage increases applied to all rates.

TESTIMONY AND EXHIBITS

13. MGUC is filing herewith written testimonies, exhibits and work papers in

support of the requested rate increase and related approvals requested herein.

14. MGUC represents that the proposals contained in this Application,

testimonies, exhibits and work papers are just, reasonable and in the public interest.

WHEREFORE, Michigan Gas Utilities Corporation requests that this Commission:

A. Set an early hearing date on this Application for rate relief;

B. Find and determine that MGUC’s existing rates and charges are

unreasonably low, inadequate and should be increased;

- 5 -

C. Authorize MGUC to file and make effective, at the earliest possible date, its

proposed final rates and charges for the sale and transportation of natural gas;

D. Authorize MGUC to continue its revenue decoupling mechanism;

E. Authorize MGUC to continue its Uncollectible Expense True-Up Mechanism;

and

F. Grant MGUC such other and further relief and authorizations as may be

lawful and proper.

Respectfully submitted,

MICHIGAN GAS UTILITIES CORPORATION

Dated: June 7, 2013 By: _______________________________

One of Its Attorneys Sherri A. Wellman (P38989) Paul M. Collins (P69719) MILLER, CANFIELD, PADDOCK and STONE, PLC One Michigan Avenue, Suite 900 Lansing, MI 48933 (517) 487-2070 Attorneys for Michigan Gas Utilities Corporation

- 6 -

MICHIGAN PUBLIC SERVICE COMMISSION

CASE NO. U-17273 Date: June 7, 2013

GENERAL APPLICATION FOR CHANGE IN GAS UTILITY RATES BEFORE MICHIGAN PUBLIC SERVICE COMMISSION CLASS A & B UTILITIES COMPANY NAME: Michigan Gas Utilities Corporation ADDRESS: 899 S. Telegraph Road, Monroe, Michigan 48161 TELEPHONE: AREA CODE (920) NUMBER 433-1502 COMPANY OFFICIAL TO BE CONTACTED PERTAINING TO RATE CASE MATTERS: David J. Kyto, PE, CMA FILING DATE: June 7, 2013 TITLE OF AUTHORIZED OFFICER: Director - Rate Case Process

* * * COMMISSION ONLY * * *

DATE RECEIVED BY COMMISSION: DOCKET NUMBER ASSIGNED: RECEIVED BY: DATE ACCEPTED: ACCEPTED BY: NOTIFICATION DATE(S): SCHEDULED PRE-HEARING DATE:

- 7 -

STATE OF MICHIGAN

BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION

* * * * * In the matter of the application of ) MICHIGAN GAS UTILITIES CORPORATION ) for authority to increase retail natural gas rates. ) Case No. U-17273 )

CERTIFICATION OF DAVID J. KYTO, PE, CMA

David J. Kyto, PE, CMA, Director - Rate Case Process of Integrys Business Support, LLC, states that he has provided the data required pursuant to Rate Case Filing Requirements established by the Commission’s Orders dated December 23, 2008 and February 20, 2009 issued in Case No. U-15895, and pursuant to these requirements, certifies the data so provided.

Dated: June 7, 2013 David J. Kyto, PE, CMA

STATE OF MICHIGAN BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION

* * * * *

NOTICE OF HEARING

FOR THE CUSTOMERS OF MICHIGAN GAS UTILITIES CORPORATION

CASE NO. U-17273

• Michigan Gas Utilities Corporation may increase its retail natural gas rates by $8,036,820 annually, or 6.01%, if the Michigan Public Service Commission approves its request.

• A TYPICAL RESIDENTIAL CUSTOMER WHO USES 88 MCF (THOUSAND CUBIC

FEET) OF NATURAL GAS PER YEAR MAY SEE AN ANNUAL INCREASE OF $28.09, OR ABOUT 4.0%, IF THE REQUESTED RATE RELIEF IS GRANTED.

• The information below describes how a person may participate in this case.

• You may call or write Michigan Gas Utilities Corporation, 899 S. Telegraph Road,

Monroe, Michigan 48161, (734) 457-6133 for a free copy of its application. Any person may review the application on Michigan Gas Utilities Corporation’s website at michigangasutilities.com, or at its offices in Monroe, Coldwater, Benton Harbor and Grand Haven.

• The first public hearing in this matter will be held:

DATE: July XX, 2013

This hearing will be a prehearing conference to set future hearing dates and decide other procedural matters.

TIME: 9:00 a.m.

PRESIDING OFFICER: Administrative Law Judge XXXXXXX

LOCATION: Constitution Hall

525 West Allegan Lansing, Michigan

PARTICIPATION: Any interested person may attend and participate. The hearing site is accessible, including handicapped parking. Persons needing any accommodation to participate should contact the Commission’s Executive Secretary at (517) 241-6160 a week in advance to request mobility, visual,

hearing or other assistance. The Michigan Public Service Commission (Commission) will hold a public hearing to consider the June 7, 2013 application of Michigan Gas Utilities Corporation (MGUC), which seeks the Commission’s approval to increase revenues for the sale, transportation and distribution of natural gas. MGUC states that it has a jurisdictional revenue deficiency of $8,036,820, or 6.01%.

Page 2 U-17273

All documents filed in this case shall be submitted electronically through the Commission’s E-Dockets Website at: michigan.gov/mpscedockets. Requirements and instructions for filing can be found in the User Manual on the E-Dockets help page. Documents may also be submitted, in Word or PDF format, as an attachment to an email sent to [email protected]. If you require assistance prior to e-filing, contact Commission staff at (517) 241-6180 or by e-mail at [email protected]. Any person wishing to intervene and become a party to the case shall file a Petition to Intervene with this Commission by July XX, 2013. (Residential customers may file petitions to intervene using the traditional paper format.) The proof of service shall indicate service upon Michigan Gas Utilities Corporation’s attorney, Sherri A. Wellman, Miller, Canfield, Paddock, and Stone, P.L.C., One Michigan Avenue, Suite 900, Lansing, Michigan 48933. Any person wishing to make a statement of position without becoming a party to the case may participate by filing an appearance. To file an appearance, the individual must attend the hearing and advise the presiding administrative law judge of his or her wish to make a statement of position. All information submitted to the Commission in this matter will become public information, available on the Michigan Public Service Commission's Web site, and subject to disclosure.

Requests for adjournment must be made pursuant to the Commission’s Rules of Practice and Procedure R 460.17315 and R 460.17335. Requests for further information on adjournment should be directed to (517) 241-6060.

A copy of Michigan Gas Utilities Corporation’s request may be reviewed on the

Commission’s Web site at michigan.gov/mpscedockets, or at the office of the Commission’s Executive Secretary, 6545 Mercantile Way, Suite 7, Lansing, MI, and at the office of Michigan Gas Utilities Corporation, 899 S. Telegraph Road, Monroe, Michigan 48161. For more information on how to participate in a case, you may contact the Commission at the above address or by telephone at (517) 241-6180.

Jurisdiction is pursuant to 1909 PA 300, as amended, MCL 462.2 et seq.; 1919 PA 419, as amended, MCL 460.51 et seq.; 1939 PA 3, as amended, MCL 460.1 et seq.; 1982 PA 304, as amended, MCL 460.6h et seq.; 1969 PA 306, as amended, MCL 24.201 et seq.; and the Commission’s Rules of Practice and Procedure, as amended, 1999 AC, R 460.17101 et seq. July XX, 2013 Lansing, Michigan

Exhibit Schedule Title Witness

A-1 (KAD-1) A1 Revenue Deficiency (Excess) Katherine A. De Cramer, CPAA-1 (KAD-1) A2 Bridge Between 2012 Historical Test Year and 2014 Projected Test Year Katherine A. De Cramer, CPA

A-2 (KAD-2) B1 Proposed Rate Base Katherine A. De Cramer, CPAA-2 (KAD-2) B2 Proposed Utility Plant Katherine A. De Cramer, CPAA-2 (KAD-2) B3 Proposed Accumulated Provision for Depreciation Katherine A. De Cramer, CPAA-2 (KAD-2) B4 Proposed Working Capital Katherine A. De Cramer, CPAA-2 (CFH-1) B5 Capital Expenditures of Projects > $500,000 Charles F. HauskaA-2 (KAD-2) B6 Rate Base Trending Katherine A. De Cramer, CPA

A-3 (KAD-3) C1 Proposed Net Operating Income Katherine A. De Cramer, CPAA-3 (KAD-3) C2 Revenue Conversion Factor Katherine A. De Cramer, CPAA-3 (KAD-3) C3 Proposed Sales Revenue Katherine A. De Cramer, CPAA-3 (KAD-3) C4 Proposed Cost of Gas Sold Katherine A. De Cramer, CPAA-3 (KAD-3) C5 Proposed Operation and Maintenance Expense Katherine A. De Cramer, CPAA-3 (KAD-3) C6 Proposed Depreciation and Amortization Expense Katherine A. De Cramer, CPAA-3 (KAD-3) C7 Proposed General Taxes Katherine A. De Cramer, CPAA-3 (KAD-3) C8 Proposed Federal Income Taxes Katherine A. De Cramer, CPAA-3 (KAD-3) C9 Proposed State Income Taxes Katherine A. De Cramer, CPAA-3 (KAD-3) C10 Proposed Local Taxes Katherine A. De Cramer, CPAA-3 (KAD-3) C11 Proposed Allowance for Funds Used During Construction Katherine A. De Cramer, CPAA-3 (KAD-3) C12 Income Tax Effect of Interest Calculation Katherine A. De Cramer, CPAA-3 (KAD-3) C13 Operation and Maintenance Expenses including Cost of Gas Katherine A. De Cramer, CPAA-3 (KAD-3) C14 Calculation of K&M Adjustment for Increase in MGP Amortization Katherine A. De Cramer, CPAA-3 (KAD-3) C15 Calculation of K&M Adjustment for Increase in Pay-at-Risk at Target Katherine A. De Cramer, CPAA-3 (CFH-2) C16 Calculation of K&M Adjustment for Increase in Storage Field Costs Charles F. HauskaA-3 (CFH-2) C17 Calculation of K&M Adjustment for Increase in Well Logs Costs Charles F. HauskaA-3 (CFH-2) C18 Calculation of K&M Adjustment for Increase in Building Expenses Charles F. HauskaA-3 (CFH-2) C19 Calculation of K&M Adjustment for Increase due to filling Non-Union Staff Vacancies Charles F. HauskaA-3 (CFH-2) C20 Calculation of K&M Adjustment for Increase for High Risk Mains Charles F. HauskaA-3 (CFH-2) C21 Calculation of K&M Adjustment for Increase due to filling Union Staff Vacancies Charles F. HauskaA-3 (KAD-3) C22 Calculation of K&M Adjustment for Increase of Customer Relations and ICE O&M Costs Katherine A. De Cramer, CPAA-3 (KAD-3) C23 Calculation of K&M Adjustment for Uncollectible Accounts Katherine A. De Cramer, CPAA-3 (KAD-3) C24 Bad Debt Expense Calculation Katherine A. De Cramer, CPAA-3 (KAD-3) C25 Calculation of K&M Adjustment for Increase due to filling IBS Vacancies Katherine A. De Cramer, CPAA-3 (KAD-3) C26 Calculation of K&M Adjustment for Increase due to IBS Regulatory Affairs Labor Katherine A. De Cramer, CPAA-3 (KAD-3) C27 Calculation of K&M Adjustment for Increase due to A&G Loader Adjustments Katherine A. De Cramer, CPAA-3 (KAD-3) C28 Calculation of K&M Adjustment for Increase due to IBS Regulatory Affairs Non-Labor Katherine A. De Cramer, CPAA-3 (KAD-3) C29 Calculation of K&M Adjustment for Injuries and Damages Katherine A. De Cramer, CPAA-3 (KAD-3) C30 Calculation of K&M Adjustment for Benefit Costs Katherine A. De Cramer, CPAA-3 (KAD-3) C31 Calculation of K&M Adjustment for Increase in IBS Depreciation Gas Management System & ICE Hardware Katherine A. De Cramer, CPAA-3 (TLK-1) C32 Master Regulated Affiliated Interest Agreement Tracy L. KupshA-3 (TLK-1) C33 Asset Ownership by Integrys Business Support Tracy L. KupshA-3 (CMP-1) C34 Summary of Benefit Costs for MGUC Employees Christine M. Phillips, CPAA-3 (CMP-1) C35 Summary of Benefit Costs for IBS Employees Christine M. Phillips, CPAA-3 (BEK-1) C36 Inputs into Summary of Calculations of Net Present Value of Revenue Requirement Brian E. KageA-3 (MEG-1) C37 Summary of Calculations of Net Present Value of Revenue Requirement ("NPVRR") Michael E. Gerth

A-4 (LJG-1) D1 Rate of Return Summary Lisa J. Gast, CPAA-4 (LJG-1) D2 Cost of Long Term Debt Lisa J. Gast, CPAA-4 (LJG-1) D3 Cost of Short Term Debt Lisa J. Gast, CPAA-4 (LJG-1) D4 Cost of Preferred Stock Lisa J. Gast, CPAA-4 (LJG-1) D5 Cost of Common Equity Lisa J. Gast, CPAA-4 (PRM-1) D6 Summary Cost of Equity Paul R. MoulA-4 (PRM-1) D7 MGUC Historical Capitalization and Financial Statistics Paul R. MoulA-4 (PRM-1) D8 Delivery Group Historical Capitalization and Financial Statistics Paul R. MoulA-4 (PRM-1) D9 Standard & Poor's Public Utilities Historical Capitalization and Financial Statistics Paul R. MoulA-4 (PRM-1) D10 Dividend Yields Paul R. MoulA-4 (PRM-1) D11 Historical Growth Rates Paul R. MoulA-4 (PRM-1) D12 Projected Growth Rates Paul R. MoulA-4 (PRM-1) D13 Financial Risk Adjustment Paul R. MoulA-4 (PRM-1) D14 Interest Rates for Investment Grade Public Utility Bonds Paul R. MoulA-4 (PRM-1) D15 Common Equity Risk Premiums Paul R. MoulA-4 (PRM-1) D16 Component Inputs for the Capital Asset Pricing Model Paul R. MoulA-4 (PRM-1) D17 Comparable Earnings Approach Paul R. Moul

Projected Test Year Ending December 31, 2014

MICHIGAN PUBLIC SERVICE COMMISSION

Michigan Gas Utilities CorporationCase No. U-17273

Index to Standard Schedules and Associated Workpapers Filed with Application for General Rate Relief

- Gas Investor Owned -

Exhibit Schedule Title Witness

Projected Test Year Ending December 31, 2014

MICHIGAN PUBLIC SERVICE COMMISSION

Michigan Gas Utilities CorporationCase No. U-17273

Index to Standard Schedules and Associated Workpapers Filed with Application for General Rate Relief

- Gas Investor Owned -

A-5 (MMD-1) E1 Proposed Sales Data 2013-2017 Matthew M. DirksenA-5 (MMD-1) E1.1 Proposed Sales Data Rate Class Matthew M. DirksenA-5 (MMD-1) E2 Proposed Fixed Charge Count Data Matthew M. DirksenA-5 (MMD-1) E3 MGUC's Virtual Weather Station HDDs as Moving Averages Matthew M. DirksenA-5 (MMD-1) E4 Change in Sales Volumes from 30 to 15 Year Forecast Matthew M. DirksenA-5 (MMD-1) E5 Change in Revenues from 30 to 15 Year Forecast Matthew M. Dirksen

A-6 (JCHM-1) F1.1 MGUC 2014 Projected COSS - General Summary per MPSC Filing Requirements Joylyn C. Hoffman Malueg, CMAA-6 (JCHM-1) F1.2 MGUC 2014 Projected COSS - Detailed Summary Joylyn C. Hoffman Malueg, CMA

A-6 (JCHM-1) F1.3MGUC 2014 Projected COSS - Individual Rate Schedule Gas Revenue Requirements and Rate Base Components Joylyn C. Hoffman Malueg, CMA

A-6 (JCHM-1) F1.4 MGUC 2014 Projected COSS - Consumption Costs by Billing Unit Joylyn C. Hoffman Malueg, CMAA-6 (JCHM-1) F1.5 MGUC 2014 Projected COSS - Allocation Methodologies Joylyn C. Hoffman Malueg, CMAA-6 (JCHM-1) F1.6 MGUC Account 380 - Cost per Service Analysis Joylyn C. Hoffman Malueg, CMAA-6 (JCHM-1) F1.7 MGUC Account 381 - Cost per Service Analysis Joylyn C. Hoffman Malueg, CMAA-6 (JCHM-1) F1.8 MGUC 2014 Projected COSS - Classification and Functionalization of Costs/Investment Joylyn C. Hoffman Malueg, CMAA-6 (JCHM-1) F1.9 MGUC 2014 Projected COSS - Distribution O&M Account Translation for FERC Plant Account Joylyn C. Hoffman Malueg, CMAA-6 (JCHM-1) F1.10 MGUC Transmission System Zero-Intercept Regression Analysis Joylyn C. Hoffman Malueg, CMAA-6 (JCHM-1) F1.11 MGUC Distribution System Zero-Intercept Regression Analysis Joylyn C. Hoffman Malueg, CMAA-6 (DJT-1) F2.1 Summary of Proposed Revenues Including Cost of Gas David J. TylerA-6 (DJT-1) F2.2 Summary of Proposed Revenues Excluding Cost of Gas David J. TylerA-6 (DJT-1) F3.1 Detail of Proposed Revenues Including Cost of Gas David J. TylerA-6 (DJT-1) F3.2 Detail of Proposed Revenues Excluding Cost of Gas David J. TylerA-6 (DJT-1) F4 Comparison of Proposed Monthly Bills David J. TylerA-6 (DJT-1) F5 Proposed Tariff Sheets David J. TylerA-6 (DJT-1) F6 Calculation of Interim Rates David J. Tyler

A-7 (KAD-4) Calculation of Inflation Factors Katherine A. De Cramer, CPA

A-8 (KAD-5) Uncollectible Expense True-Up Mechanism Allocators Katherine A. De Cramer, CPA

A-9 (KAD-6) Integrys Energy Group, Inc. Awards & Recognition: 2006-2012 Katherine A. De Cramer, CPA

A-10 (NEC-1) Pay-at-Risk Plan Noreen E. Cleary

STATE OF MICHIGAN

BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION

* * * * * In the matter of the application of ) MICHIGAN GAS UTILITIES CORPORATION ) for authority to increase retail natural gas rates. ) Case No. U-17273 )

DIRECT TESTIMONY AND EXHIBITS OF

KATHERINE A. DE CRAMER, CPA

FOR

MICHIGAN GAS UTILITIES CORPORATION

June 7, 2013

- 1 -

STATE OF MICHIGAN

BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION

* * * * *

In the matter of the application of ) MICHIGAN GAS UTILITIES CORPORATION ) for authority to increase retail natural gas rates. ) Case No. U-17273 )

QUALIFICATIONS OF

KATHERINE A. DE CRAMER, CPA PART I

Q. Please state your name, business address and position. 1

A. My name is Katherine A. De Cramer, CPA. My business address is Integrys 2

Business Support, LLC (“IBS”), 700 North Adams Street, P.O. Box 19001, Green 3

Bay, WI 54307-9001. I am a Rate Case Consultant in the Regulatory Affairs 4

Department of Integrys Energy Group, Inc (“Integrys”). Both IBS and Michigan Gas 5

Utilities Corporation (“MGUC”) are wholly-owned subsidiaries of Integrys. Integrys 6

resulted from the February 21, 2007 merger between WPS Resources Corporation 7

(“WPSR”) and Peoples Energy Corporation. 8

9

Q. For whom are you providing testimony? 10

A. I am providing testimony on behalf of MGUC. 11

12

Q. Please describe briefly your educational, professional, and utility background. 13

A. I have a Bachelors Degree from Lakeland College, Sheboygan, Wisconsin in 14

Accounting. I have a Masters Degree in Business Administration from the University 15

of Wisconsin-Oshkosh, and a Master of Science Degree in Information Systems from 16

the University of Wisconsin-Oshkosh. I am licensed in the State of Wisconsin to 17

practice as a Certified Public Accountant. 18

- 2 -

1

In June of 2003, I was hired by Wisconsin Public Service Corporation (“WPS Corp”) 2

as a Revenue Requirements Forecaster in the Regulatory Affairs Department. While 3

working as a Revenue Requirements Forecaster, my primary responsibility was the 4

revenue requirements analysis for WPS Corp’s wholesale electric jurisdiction. Since 5

the acquisition of MGUC in 2006, my job responsibilities have expanded to include 6

the revenue requirements, decoupling, and Uncollectibles Expense Tracking 7

Mechanism analyses for MGUC, as well. In January of 2013, I became a Rate Case 8

Consultant within the Regulatory Affairs Department. 9

10

Q. Have you previously testified before any regulatory agency? 11

A. Yes, I have. I have submitted testimony before the Michigan Public Service 12

Commission (“Commission”) on behalf of MGUC in Case Nos. U-15990, U-16976, U-13

16977, U-17221 and U-17222. In addition, I have prepared various accounting and 14

filing exhibits for WPS Corp for presentation to the Public Service Commission of 15

Wisconsin (“PSCW”) and for MGUC for presentation to the Commission.16

- 3 -

KATHERINE A. DE CRAMER DIRECT TESTIMONY

PART II

Q. What is the purpose of your pre-filed direct testimony? 1

A. The purpose of my pre-filed direct testimony is to provide an explanation of the 2

methodology used to develop MGUC’s revenue deficiency for the 2014 projected test 3

year. 4

5

Q. Are you sponsoring any exhibits in this proceeding? 6

A. Yes, I am. I am sponsoring: 7 8

1. Exhibit A-1 (KAD-1), Schedules A1 and A2, 9 10

2. Exhibit A-2 (KAD-2), Schedules B1-B4, B6, 11 12

3. Exhibit A-3 (KAD-3), Schedules C1-C15, C22-C31, 13 14 4. Exhibit A-7 (KAD-4), 15 16 5. Exhibit A-8 (KAD-5), 17

18 6. Exhibit A-9 (KAD-6), 19

20 7. Exhibit A-11 (KAD-7), Schedule A1, 21

22 8. Exhibit A-12 (KAD-8), Schedules B1-B4, and 23

24 9. Exhibit A-13 (KAD-9), Schedules C1-C11. 25

26

Q. Were these exhibits prepared by you or under your direction and supervision? 27

A. Yes, they were. 28

29

Q. Please describe Schedule A1 of Exhibit A-1 (KAD-1). 30

A. Schedule A1 of Exhibit A-1 (KAD-1) calculates MGUC’s 2014 projected test year 31

revenue deficiency based on its rate base, adjusted net operating income, rate of 32

return, and revenue conversion factor. 33

34

- 4 -

Q. Please describe Schedule A2 of Exhibit A-1 (KAD-1). 1

A. Schedule A2 of Exhibit A-1 (KAD-1) provides the bridge between the 2012 historical 2

test year revenue deficiency and 2014 projected test year. 3

4

Q. Please describe Schedule B1 of Exhibit A-2 (KAD-2). 5

A. Schedule B1 of Exhibit A-2 (KAD-2) calculates MGUC’s 2014 projected test year rate 6

base. 7

8

Q. Please describe Schedule B2 of Exhibit A-2 (KAD-2). 9

A. Schedule B2 of Exhibit A-2 (KAD-2) calculates MGUC’s 2014 projected test year 10

utility plant. 11

12

Q. Please describe Schedule B3 of Exhibit A-2 (KAD-2). 13

A. Schedule B3 of Exhibit A-2 (KAD-2) depicts MGUC’s 2014 projected test year 14

accumulated provision for depreciation. 15

16

Q. Please describe Schedule B4 of Exhibit A-2 (KAD-2). 17

A. Schedule B4 of Exhibit A-2 (KAD-2) calculates MGUC’s 2014 projected test year 18

working capital. 19

20

Q. Please describe Schedule B5 of Exhibit A-2 (CFH-1). 21

A. Schedule B5 of Exhibit A-2 (CFH-1) will be discussed in the pre-filed direct testimony 22

of Mr. Charles F. Hauska. 23

24

Q. Please describe Schedule B6 of Exhibit A-2 (KAD-2). 25

A. Schedule B6 of Exhibit A-2 (KAD-2) is a trending analysis of MGUC’s rate base from 26

2007 through the 2014 projected test year. 27

- 5 -

1

Q. Please describe Schedule C1 of Exhibit A-3 (KAD-3). 2

A. Schedule C1 of Exhibit A-3 (KAD-3) calculates MGUC’s 2014 projected test year 3

adjusted net operating income. 4

5

Q. Please describe Schedule C2 of Exhibit A-3 (KAD-3). 6

A. Schedule C2 of Exhibit A-3 (KAD-3) calculates MGUC’s 2014 projected test year 7

gross revenue conversion factor. 8

9

Q. Please describe Schedule C3 of Exhibit A-3 (KAD-3). 10

A. Schedule C3 of Exhibit A-3 (KAD-3) depicts MGUC’s 2014 projected test year total 11

revenue. 12

13

Q. Please describe Schedule C4 of Exhibit A-3 (KAD-3). 14

A. Schedule C4 of Exhibit A-3 (KAD-3) depicts MGUC’s 2014 projected test year cost of 15

gas. 16

17

Q. Please describe Schedule C5 of Exhibit A-3 (KAD-3). 18

A. Schedule C5 of Exhibit A-3 (KAD-3) calculates MGUC’s 2014 projected test year 19

total operation and maintenance (“O&M”) expense, exclusive of the cost of gas. 20

21

Q. Please describe Schedule C6 of Exhibit A-3 (KAD-3). 22

A. Schedule C6 of Exhibit A-3 (KAD-3) depicts MGUC’s 2014 projected test year total 23

depreciation and amortization expense. 24

25

Q. Please describe Schedule C7 of Exhibit A-3 (KAD-3). 26

A. Schedule C7 of Exhibit A-3 (KAD-3) calculates MGUC’s 2014 projected test year 27

- 6 -

total for taxes other than income taxes. 1

2

Q. Please describe Schedule C8 of Exhibit A-3 (KAD-3). 3

A. Schedule C8 of Exhibit A-3 (KAD-3) depicts MGUC’s 2014 projected test year 4

federal income taxes. 5

6

Q. Please describe Schedule C9 of Exhibit A-3 (KAD-3). 7

A. Schedule C9 of Exhibit A-3 (KAD-3) depicts MGUC’s 2014 projected test year state 8

income taxes. 9

10

Q. Please describe Schedule C10 of Exhibit A-3 (KAD-3). 11

A. Schedule C10 of Exhibit A-3 (KAD-3) depicts MGUC’s 2014 projected test year local 12

taxes. 13

14

Q. Please describe Schedule C11 of Exhibit A-3 (KAD-3). 15

A. Schedule C11 of Exhibit A-3 (KAD-3) depicts MGUC’s 2014 projected test year 16

AFUDC. 17

18

Q. Please describe Schedule C12 of Exhibit A-3 (KAD-3). 19

A. Schedule C12 of Exhibit A-3 (KAD-3) calculates the Income Tax Effect of Interest for 20

MGUC’s 2014 projected test year. 21

22

Q. Please describe Schedule C13 of Exhibit A-3 (KAD-3). 23

A. Schedule C13 of Exhibit A-3 (KAD-3) develops the O&M costs for MGUC’s 2014 24

projected test year. 25

26

Q. Please describe Schedule C14 of Exhibit A-3 (KAD-3). 27

- 7 -

A. Schedule C14 of Exhibit A-3 (KAD-3) calculates the Known & Measurable (“K&M”) 1

adjustment associated with the amortization of Manufactured Gas Plant remediation 2

costs. 3

4

Q. Please describe Schedule C15 of Exhibit A-3 (KAD-3). 5

A. Schedule C15 of Exhibit A-3 (KAD-3) calculates the K&M adjustment for paying Pay-6

at-Risk at the “Target” level, rather than at the level paid in the 2012 historical period. 7

8

Q. Please describe Schedules C22 of Exhibit A-3 (KAD-3). 9

A. Schedule C22 of Exhibit A-3 (KAD-3) calculates the K&M adjustment related to the 10

customer relations and Integrys Customer Experience (“ICE”) 2016 project O&M 11

costs. 12

13

Q. Please describe Schedule C23 of Exhibit A-3 (KAD-3). 14

A. Schedule C23 of Exhibit A-3 (KAD-3) calculates the K&M adjustment associated with 15

uncollectibles expense. 16

17

Q. Please describe Schedule C24 of Exhibit A-3 (KAD-3). 18

A. Schedule C24 of Exhibit A-3 (KAD-3) calculates the 2014 uncollectibles expense of 19

$1,917,930, and supports Schedule C23 of Exhibit A-3 (KAD-3). 20

21

Q. Please describe Schedule C25 of Exhibit A-3 (KAD-3). 22

A. Schedule C25 of Exhibit A-3 (KAD-3) calculates the K&M adjustment associated with 23

filling IBS vacancies. 24

25

Q. Please describe Schedule C26 of Exhibit A-3 (KAD-3). 26

A. Schedule C26 of Exhibit A-3 (KAD-3) calculates the K&M adjustment associated with 27

- 8 -

an increase in IBS Regulatory Affairs labor. 1

2

Q. Please describe Schedule C27 of Exhibit A-3 (KAD-3). 3

A. Schedule C27 of Exhibit A-3 (KAD-3) calculates the K&M adjustment due to A&G 4

loader adjustments. 5

6

Q. Please describe Schedule C28 of Exhibit A-3 (KAD-3). 7

A. Schedule C28 of Exhibit A-3 (KAD-3) calculates the K&M adjustment associated with 8

an increase in IBS Regulatory Affairs non-labor. 9

10

Q. Please describe Schedule C29 of Exhibit A-3 (KAD-3). 11

A. Schedule C29 of Exhibit A-3 (KAD-3) calculates the K&M adjustment associated with 12

Injuries and Damages. 13

14

Q. Please describe Schedule C30 of Exhibit A-3 (KAD-3). 15

A. Schedule C30 of Exhibit A-3 (KAD-3) calculates the K&M adjustment associated with 16

MGUC benefit costs. 17

18

Q. Please describe Schedule C31 of Exhibit A-3 (KAD-3). 19

A. Schedule C31 of Exhibit A-3 (KAD-3) calculates the K&M adjustment for increases to 20

IBS Depreciation for the Gas Management System and ICE 2016 Hardware. 21

22

Q. Please describe Exhibit A-7 (KAD-4). 23

A. Exhibit A-7 (KAD-4) calculates the inflation factors for 2013 and 2014 that were 24

applied to the 2012 historic test year O&M expenses to determine 2014 projected 25

test year O&M expenses, exclusive of K&M items. 26

27

- 9 -

Q. Please describe Exhibit A-8 (KAD-5). 1

A. Exhibit A-8 (KAD-5) depicts the Uncollectibles Expense True-Up Mechanism 2

Allocators. 3

4

Q. Please describe Exhibit A-9 (KAD-6). 5

A. Exhibit A-9 (KAD-6) is a summary of Awards & Recognition earned by Integrys and 6

Integrys subsidiaries during 2006-2012. 7

8

Q. Please describe Schedule A1 of Exhibit A-11 (KAD-7). 9

A. Schedule A1 of Exhibit A-11 (KAD-7) calculates MGUC’s 2012 historic test year 10

revenue deficiency based on its rate base, adjusted net operating income, rate of 11

return, and revenue conversion factor. 12

13

Q. Please describe Schedule B1 of Exhibit A-12 (KAD-8). 14

A. Schedule B1 of Exhibit A-12 (KAD-8) calculates MGUC’s 2012 historic test year rate 15

base. 16

17

Q. Please describe Schedule B2 of Exhibit A-12 (KAD-8). 18

A. Schedule B2 of Exhibit A-12 (KAD-8) calculates MGUC’s 2012 historic test year 19

utility plant. 20

21

Q. Please describe Schedule B3 of Exhibit A-12 (KAD-8). 22

A. Schedule B3 of Exhibit A-12 (KAD-8) depicts MGUC’s 2012 historic test year 23

accumulated provision for depreciation. 24

25

Q. Please describe Schedule B4 of Exhibit A-12 (KAD-8). 26

A. Schedule B4 of Exhibit A-12 (KAD-8) calculates MGUC’s 2012 historic test year 27

- 10 -

working capital. 1

2

Q. Please describe Schedule C1 of Exhibit A-13 (KAD-9). 3

A. Schedule C1 of Exhibit A-13 (KAD-9) calculates MGUC’s 2012 historic test year 4

adjusted net operating income. 5

6

Q. Please describe Schedule C2 of Exhibit A-13 (KAD-9). 7

A. Schedule C2 of Exhibit A-13 (KAD-9) calculates MGUC’s 2012 historic test year 8

gross revenue conversion factor. 9

10

Q. Please describe Schedule C3 of Exhibit A-13 (KAD-9). 11

A. Schedule C3 of Exhibit A-13 (KAD-9) calculates MGUC’s 2012 historic test year total 12

revenue. 13

14

Q. Please describe Schedule C4 of Exhibit A-13 (KAD-9). 15

A. Schedule C4 of Exhibit A-13 (KAD-9) calculates MGUC’s 2012 historic test year total 16

cost of gas. 17

18

Q. Please describe Schedule C5 of Exhibit A-13 (KAD-9). 19

A. Schedule C5 of Exhibit A-13 (KAD-9) calculates MGUC’s 2012 historic test year total 20

O&M expense, exclusive of the cost of gas. 21

22

Q. Please describe Schedule C6 of Exhibit A-13 (KAD-9). 23

A. Schedule C6 of Exhibit A-13 (KAD-9) depicts MGUC’s 2012 historic test year total 24

depreciation and amortization expense. 25

26

27

- 11 -

Q. Please describe Schedule C7 of Exhibit A-13 (KAD-9). 1

A. Schedule C7 of Exhibit A-13 (KAD-9) calculates MGUC’s 2012 historic test year total 2

for taxes other than income taxes. 3

4

Q. Please describe Schedule C8 of Exhibit A-13 (KAD-9). 5

A. Schedule C8 of Exhibit A-13 (KAD-9) depicts MGUC’s 2012 historic test year federal 6

income taxes. 7

8

Q. Please describe Schedule C9 of Exhibit A-13 (KAD-9). 9

A. Schedule C9 of Exhibit A-13 (KAD-9) depicts MGUC’s 2012 historic test year state 10

income taxes. 11

12

Q. Please describe Schedule C10 of Exhibit A-13 (KAD-9). 13

A. Schedule C10 of Exhibit A-13 (KAD-9) depicts MGUC’s 2012 historic test year local 14

taxes. 15

16

Q. Please describe Schedule C11 of Exhibit A-13 (KAD-9). 17

A. Schedule C11 of Exhibit A-13 (KAD-9) depicts MGUC’s 2012 historic test year 18

Allowance of Funds Used During Construction (“AFUDC”). 19

20

Q. Please describe Schedule C12 of Exhibit A-13 (KAD-9). 21

A. Schedule C12 of Exhibit A-13 (KAD-9) depicts MGUC’s 2012 historic test year 22

Income Tax Effect of Interest. 23

24

Background 25 Q. Are you familiar with the application of MGUC for authority to increase retail 26

gas rates? 27

A. Yes, I am. 28

- 12 -

1

Q. Please provide a brief description of MGUC and the area it serves. 2

A. MGUC is a corporation organized under the laws of the state of Delaware, with its 3

principal office located at 899 S. Telegraph Road, Monroe, Michigan 48161, and is 4

authorized to transact business in the state of Michigan. MGUC is a subsidiary of 5

Integrys, which prior to February 21, 2007, was known as WPSR. MGUC is a sister 6

utility company to UPPCO and WPS Corp, both of which are also regulated by this 7

Commission. MGUC is also a sister utility company to, among others, Minnesota 8

Energy Resources Corporation, The Peoples Gas Light and Coke Company, and 9

North Shore Gas Company, none of which is regulated by this Commission. MGUC 10

was acquired by WPSR from Aquila, Inc. on April 1, 2006 as authorized by the 11

Commission’s order in Case No. U-14657. Prior to its acquisition by WPSR, MGUC 12

conducted business as “Aquila Networks – MGU”. 13

14

MGUC is a public utility engaged in the purchase, storage, transportation, distribution 15

and sale of natural gas to approximately 166,000 customers in 147 communities in 16

the Southern and Western portions of Michigan’s lower peninsula. 17

18

Integrys and its subsidiaries have been recognized as superior performers in the 19

utility industry, as summarized on Exhibit A-9 (KAD-6). 20

21

Q. Please describe the most recent rate relief obtained by MGUC. 22

A. In the most recent rate case, Case No. U-15990, MGUC used a 2010 test year. A 23

settlement was reached and approved by the Commission granting rate relief of $3.5 24

million, based on an overall rate of return of 7.16%, and a return on common equity 25

of 10.75%, effective January 1, 2010. 26

27

- 13 -

MGUC was also authorized to implement an Uncollectibles Expense Tracking 1

Mechanism (“UETM”) under which MGUC annually defers, and subsequently 2

surcharges or credits, 80% of the difference between MGUC’s future annual Net 3

Uncollectibles Expense and the $2,009,903 of Net Uncollectibles Expense included 4

in the revenue requirement in Case No. U-15990. 5

6

In addition, MGUC was authorized to implement a revenue decoupling mechanism 7

(“RDM”). The MGUC RDM is symmetrical, and reconciles volumetric distribution 8

margin revenue (exclusive of Gas Cost Recovery revenue) per customer for the 9

Residential, Multi-Family, and Small Commercial and Industrial rate schedules. 10

MGUC compares weather adjusted actual sales per customer during each 12-month 11

period, with the base sales per customer established in Case No. U-15990 for the 12

decoupled rate schedules. MGUC annually defers an amount for the difference, 13

which is subsequently reconciled with the Commission, and surcharged or credited 14

to customers. 15

16

MGUC’s rates for retail gas service established in Case No. U-15990 do not reflect 17

the current costs of providing retail gas service, and MGUC requires further rate 18

relief. 19

20

Q. Please explain, generally, why rate relief is sought at this time. 21

A. First, the 2012 historic test year indicates that MGUC suffered a revenue deficiency 22

of $6,301,860. This corresponds to a 6.14% return on common equity. This value is 23

well below MGUC’s authorized return on common equity of 10.75% authorized in 24

MGUC’s most recent general rate case proceeding in Case No. U-15990. MGUC 25

expects to suffer a significant revenue deficiency in 2013 and 2014 as well due to: 26

27

- 14 -

First, the cost of upgrades to the MGUC gas transmission and distribution systems, 1

2

Second, margin revenues have decreased since MGUC’s most recent general rate 3

case proceeding in Case No. U-15990 from $63.5 million to $62.3 million. 4

5

Third, MGUC is projecting a higher Cost of Capital in the 2014 projected test year. 6

7

Fourth, MGUC had a number of positions that were vacant during the 2012 Historical 8

Test period. MGUC expects to fill these positions throughout 2013 and 2014, as 9

discussed in the pre-filed direct testimony of Mr. Charles F. Hauska. 10

11

Fifth, MGUC’s building expenses will increase due to needed repairs and 12

maintenance during the 2014 projected test year. 13

14

Sixth, the cost of engineering analysis on vintage natural gas transmission and 15

distribution mains. 16

17

Seventh, customer relations costs and O&M costs will increase due to a project to 18

consolidate customer service functions such as billing, payments, and web access 19

for customers to more efficiently manage their accounts. 20

21

Lastly, general inflation is expected to increase costs at a rate of about 3.74% over 22

the 2012-2014 timeframe. MGUC’s estimate for inflation for 2013 and 2014 was 23

calculated using a methodology similar to that used by MPSC Staff witness, Kirk K. 24

Megginson, in Case No. U-14893, SEMCO Energy Gas Company’s 2007 general 25

rate case. 26

27

- 15 -

As shown above, the growth in revenues has not kept up with the growth in costs. 1

2

MGUC Witnesses 3 Q. Please identify the MGUC witnesses, and indicate the subjects they will 4

address in their testimony. 5

A. I provide testimony and evidence regarding: 6

1. The revenue deficiency, including 7 a. O&M Expenses, 8 b. K&M Items, 9 c. Common equity adjustments, 10 d. Capital structure adjustments, 11 e. Rate base, and 12 f. Operating Income 13

14 2. Depreciation rates, 15

16 3. Bonus Depreciation, 17

18 4. Continuation of an uncollectible expense true-up mechanism, 19

20 5. Continuation of a revenue decoupling mechanism, 21

22 6. Interim rates, and 23

24 7. Gas Costs and Revenues. 25

26

Mr. Matthew M. Dirksen provides testimony on the sales forecast and a 27

recommendation for a change in the period for weather normalization. 28

29

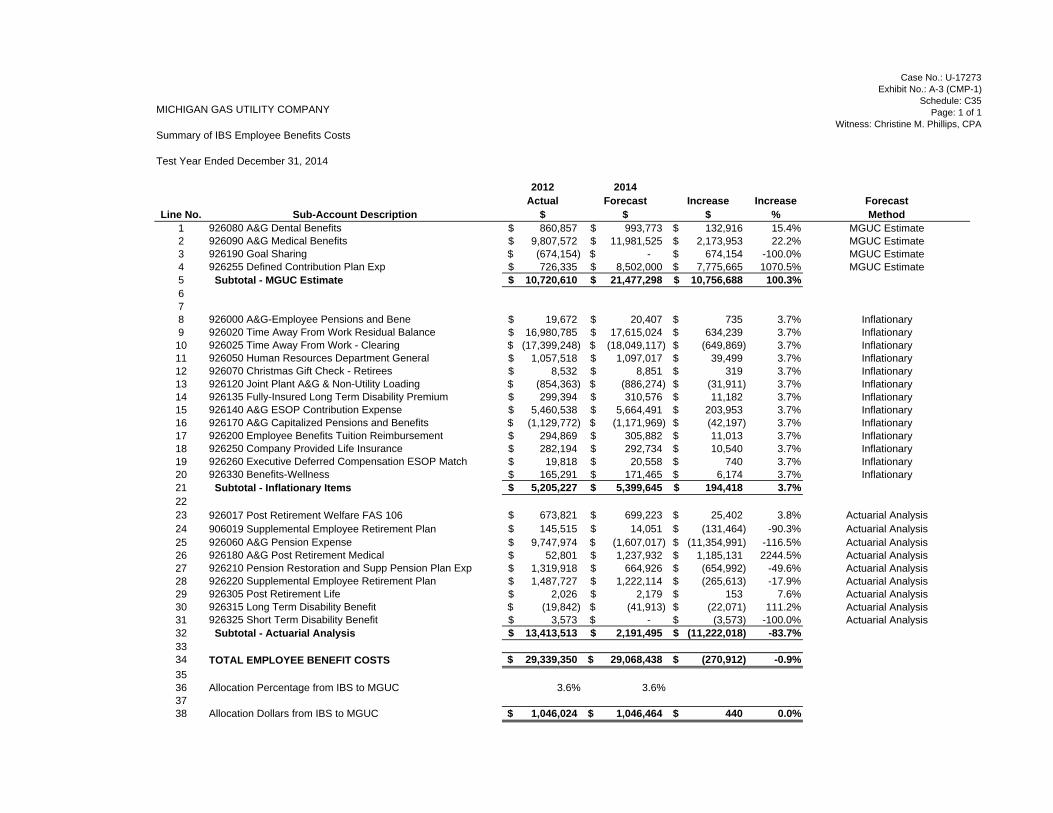

Ms. Christine M. Phillips, CPA, provides testimony regarding employee benefits. 30

31

Ms. Noreen E. Cleary provides testimony about the MGUC and Integrys Pay-at-Risk 32

plan. 33

34

Mr. Charles F. Hauska provides testimony regarding capital expenditures greater 35

than $500,000, as well as K&M adjustments relating to staff vacancies, high risk 36

mains, building expenses, storage field costs and well logs costs. 37

- 16 -

1

Mr. Brian E. Kage provides testimony to describe the ICE 2016 project, as well as 2

the Intangible Benefits of ICE 2016. 3

4

Mr. Michael E. Gerth provides testimony about the Net Present Values of the ICE 5

2016 project. 6

7

Ms. Tracy L. Kupsh provides testimony on IBS charges. 8

9

Ms. Lisa J. Gast, CPA, provides testimony on MGUC’s capital structure and 10

requested return on common equity. 11

12

Mr. Paul R. Moul provides testimony on the required return on common equity. 13

14

Ms. Joylyn C. Hoffman Malueg, CMA, provides testimony on the class cost of service 15

studies. 16

17

Mr. David J. Tyler provides testimony on rate design, including the proposed rate 18

design for interim rate relief. In addition, Mr. Tyler sponsors the proposed tariff 19

changes. 20

21

Mr. John R. Wilde provides testimony on certain tax issues. 22

23

The Revenue Deficiency 24 Q. What is the amount of rate relief MGUC is seeking in this proceeding? 25

A. MGUC’s analysis of the test year ending December 31, 2014 indicates a need for an 26

annual rate increase of $8,036,820, or 6.01%, for retail gas operations. This 27

increase is based on the rates authorized in the Commission’s December 16, 2009 28

- 17 -

Order Approving Partial Settlement Agreement in Case No. U-15990 and a proposed 1

return on common equity of 10.75%, which is supported by the pre-filed direct 2

testimony of Mr. Paul R. Moul. 3

4

The rates sponsored by Mr. David J. Tyler are designed to produce the requested 5

revenue requirement, and to move toward the MGUC goal of a rate design where 6

each rate schedule will return the overall allowed rate of return, consistent with 7

MGUC’s cost of service study, MGUC’s rate design general principles, and existing 8

law. 9

10

Q. What test period is MGUC’s proposed rate increase based on? 11

A. MGUC has used a projected test year ending December 31, 2014. 12

13

O&M Expenses 14 Q. Please describe how MGUC developed 2014 O&M expenses. 15

A. MGUC started with 2012 actual O&M expenses, and inflated them to 2014 using 16

inflation factors developed by a methodology similar to that used by MPSC Staff 17

witness, Kirk D. Megginson, in Case No. U-14893, SEMCO Energy Gas Company’s 18

2007 general rate case. The inflation factors used were 1.708% for 2013, and 19

1.993% for 2014, as developed on Exhibit A-7 (KAD-4). MGUC then adjusted this 20

2014 O&M expense value for the K&M items, as described later in this testimony, 21

and in the testimony of Charles F. Hauska and Christine M. Phillips. 22

23

K&M Items 24 Q. Please describe the K&M adjustments included in the 2014 projected test year 25

O&M expenses, as detailed on Schedules C14 – C15 and C22 – C31 of Exhibit 26

A-3 (KAD-3), Schedules C16 – C21 of Exhibit (CFH-2), and Schedule C34 of 27

Exhibit A-3 (CMP-1) compared to actual O&M expenses from the 2012 historic 28

- 18 -

test year. 1

A. There are eighteen K&M adjustments. Fifteen are K&M increases, and three are 2

K&M decreases. 3

4

MGUC has defined K&M items to be any O&M cost item that was increased (or 5

decreased) at a rate other than the rates of inflation calculated on Exhibit A-7 (KAD-6

4). 7

8

The fifteen K&M increases are associated with: 9

1. Manufactured Gas Plant Remediation costs, 10 11

2. The increased costs of the Integrys Pay-at-Risk plan, 12 13

3. Storage Field Costs, 14 15

4. Well Logs Costs, 16 17

5. Building Expenses, 18 19

6. Non-Union Staff costs, 20 21

7. High Risk Mains costs, 22 23

8. Union Staff costs, 24 25

9. Customer Relations and ICE 2016 O&M costs, 26 27

10. Uncollectible Accounts, 28 29

11. IBS Staff costs, 30 31

12. IBS Regulatory Affairs Labor costs, 32 33

13. A&G Loader Adjustment, 34 35

14. IBS Regulatory Affairs Non-Labor costs, and 36 37

15. IBS Depreciation Gas Management System & ICE Hardware costs. 38 39 40

The three K&M decreases are associated with: 41

1. Injuries and Damages, 42 43

- 19 -

2. Benefits Amortizations Expense, and 1 2 3. Benefits Expense (less transitions costs and amortizations). 3

4

Each of these K&M adjustments is discussed in further detail later in this testimony, 5

or in the pre-filed direct testimony of Mr. Charles F. Hauska or Ms. Christine M. 6

Phillips. 7

8

Q. Please explain Schedule A1 of Exhibit A-1 (KAD-1). 9

A. Schedule A1 of Exhibit A-1 (KAD-1) calculates MGUC’s 2014 projected test year 10

revenue deficiency based on its rate base, adjusted net operating income, rate of 11

return, and revenue conversion factor. This schedule indicates that the 2014 Total 12

Company revenue deficiency is $8,036,820, or 6.01%, based on the rates authorized 13

in the Commission’s December 19, 2009 Order Approving Partial Settlement 14

Agreement in Case No. U-15990, and a proposed 10.75% return on equity. The 15

component parts of this schedule are taken from the various sources indexed to the 16

left of each value. 17

18

Common Equity Adjustments 19 Q. What adjustments were made to the equity portion of MGUC’s capital 20

structure? 21

A. MGUC has removed certain accounts both from the 2012 historic test year and the 22

2014 projected test year. For both the 2012 historic test year and the 2014 projected 23

test year, Goodwill, Trade Name, and the associated deferred income taxes, were 24

removed from MGUC’s Equity balance. In addition, two Deferred Compensation 25

accounts were removed. This resulted in a reduction of equity of $62,231,636 in 26

2012, and $57,013,414 in 2014, which tends to reduce the revenue requirement. 27

28

29

- 20 -

Capital Adjustments 1 Q. What adjustments were made to MGUC’s overall capital structure? 2

A. For both the 2012 historic test year and the 2014 projected test year, interest bearing 3

accounts in working capital were removed from the capital structure to prevent 4

MGUC from earning a return on these items. This adjustment included items related 5

to: 6

1. GCR Over/Under Collections, 7

2. Customer Advances and Deposits, 8

3. UETM accounts, 9

4. RDM accounts, and 10

5. MI Energy Optimization. 11

This resulted in a reduction in the capital structure of $4,391,294 in 2012, and 12

$5,003,188 in 2014, which tends to reduce the revenue requirement. 13

14

Q. Please explain Schedule A2 of Exhibit A-1 (KAD-1). 15

A. Schedule A2 of Exhibit A-1 (KAD-1) provides the bridge between the 2012 historical 16

test year revenue deficiency and 2014 projected test year revenue deficiency. 17

18

Rate Base 19 Q. Please explain Schedule B1 of Exhibit A-2 (KAD-2). 20

A. Schedule B1 of Exhibit A-2 (KAD-2) calculates MGUC’s 2014 projected test year rate 21

base. The 2014 Total Company rate base is $210,493,148, as shown on Line 21. 22

The component parts of this schedule are taken from the various sources indexed to 23

the left of these amounts. Also, all values shown are 13-month averages. 24

25

Q. Please explain Schedule B2 of Exhibit A-2 (KAD-2). 26

A. Schedule B2 of Exhibit A-2 (KAD-2) depicts MGUC’s 2014 projected test year utility 27

plant. To arrive at the 2014 projected test year utility plant, the June 30, 2012 actual 28

- 21 -

balance of utility plant was projected forward using MGUC’s 2012, 2013, and 2014 1

construction budgets. The 2014 Total Company utility plant is $353,437,557, as 2

shown on Line 13. Also, all values shown are 13-month averages. 3

4

Q. Please explain Schedule B3 of Exhibit A-2 (KAD-2). 5

A. Schedule B3 of Exhibit A-2 (KAD-2) depicts MGUC’s 2014 projected test year 6

accumulated provision for depreciation. To arrive at the 2014 projected test year 7

accumulated provision for depreciation, the June 30, 2012 actual balance of 8

accumulated provision for depreciation was projected forward using MGUC’s 2012, 9

2013, and 2014 construction budgets. The 2014 Total Company accumulated 10

provision for depreciation is $189,078,201, as shown on Line 2. Also, all values 11

shown are 13-month averages. 12

13

Q. Please explain Schedule B4 of Exhibit A-2 (KAD-2). 14

A. Schedule B4 of Exhibit A-2 (KAD-2) calculates MGUC’s 2014 projected test year 15

working capital. The 2014 Total Company working capital is $46,133,792, as shown 16

on Line 41. Also, all values shown are 13-month averages. 17

18

Q. Please explain Schedule B6 of Exhibit A-2 (KAD-2). 19

A. Schedule B6 of Exhibit A-2 (KAD-2) presents a projected 2014 rate base developed 20

by trending analysis. The results from this trending show that MGUC’s 2014 trended 21

rate base based upon actual historical data from January 1, 2007 through December 22

31, 2012 is $11 million lower than MGUC’s 2014 projected test year rate base in the 23

instant general rate case proceeding, as shown on Line 35. 24

25

The major reasons for the difference between the 2014 trended rate base and the 26

2014 forecasted rate base include an increase in Net Plant of $25M due to 27

- 22 -

forecasted capital spending being higher than the trended amount of capital 1

spending. MGUC has recently committed to an increased capital expenditures plan 2

to improve its transmission and distribution systems. In the past few years, MGUC 3

had spent between $7.0 and $11.7 million on capital per year. In the 2012 Historical 4

Test Year, capital expenditures were $16.3 million. In the next few years, MGUC 5

plans to spend between $16.2 and $19.7 million per year on capital projects. 6

7

In addition to the Net Plant increase, other rate base variances include a decrease in 8

CWIP of $4M having closed all projects to Plant as of December 31, 2014; a 9

decrease in Working Capital, including a decrease in Temporary Cash of $4M, a 10

decrease in customer Accounts Receivable of $4M, and an increase in Accrued 11

Utility Revenue of $1.7M; and a decrease in Storage Gas of $1.6M due to a lower 12

cost of gas commodity. 13

14

Operating Income 15 Q. Please explain Schedule C1 of Exhibit A-3 (KAD-3). 16

A. Schedule C1 of Exhibit A-3 (KAD-3) calculates MGUC’s 2014 projected test year 17

adjusted net operating income. The 2014 Total Company adjusted net operating 18

income is $8,565,375, as shown on Line 22. 19

20

Q. Please explain Schedule C2 of Exhibit A-3 (KAD-3). 21

A. Schedule C2 of Exhibit A-3 (KAD-3) calculates MGUC’s 2014 projected test year 22

gross revenue conversion factor. The 2014 gross revenue conversion factor is 23

1.637, as shown on Line 14. 24

25

26

Q. Please explain Schedule C3 of Exhibit A-3 (KAD-3). 27

A. Schedule C3 of Exhibit A-3 (KAD-3) calculates MGUC’s 2014 projected test year 28

- 23 -

total revenue. The 2014 Total Company total revenue is $134,862,467, as shown on 1

Line 6. 2

3

Q. Please explain Schedule C4 of Exhibit A-3 (KAD-3). 4

A. Schedule C4 of Exhibit A-3 (KAD-3) calculates MGUC’s 2014 projected test year 5

cost of gas. The 2014 Total Company cost of gas is $71,684,716, as shown on Line 6

7. 7

8

Q. Please explain Schedule C5 of Exhibit A-3 (KAD-3). 9

A. Schedule C5 of Exhibit A-3 (KAD-3) calculates MGUC’s 2014 projected test year 10

total O&M expense, exclusive of the cost of gas. The 2014 Total Company total 11

O&M expense, exclusive of the cost of gas, is $37,518,049, as shown on Line 19. 12

13

Q. Please explain Schedule C6 of Exhibit A-3 (KAD-3). 14

A. Schedule C6 of Exhibit A-3 (KAD-3) depicts MGUC’s 2014 projected test year total 15

depreciation and amortization expense. The 2014 Total Company total depreciation 16

and amortization expense is $9,779,652, as shown on Line 6. 17

18

Q. Please explain Schedule C7 of Exhibit A-3 (KAD-3). 19

A. Schedule C7 of Exhibit A-3 (KAD-3) calculates MGUC’s 2014 projected test year 20

total for taxes other than income taxes. The 2014 Total Company total for taxes 21

other than income taxes is $4,504,777, as shown on Line 32. 22

23

Q. Please explain Schedule C8 of Exhibit A-3 (KAD-3). 24

A. Schedule C8 of Exhibit A-3 (KAD-3) depicts MGUC’s 2014 projected test year 25

federal income taxes. The 2014 Total Company federal income taxes are 26

$2,509,208, as shown on Line 2. 27

- 24 -

1

Q. Please explain Schedule C9 of Exhibit A-3 (KAD-3). 2

A. Schedule C9 of Exhibit A-3 (KAD-3) depicts MGUC’s 2014 projected test year state 3

income taxes. The 2014 Total Company state income taxes are $295,743, as shown 4

on Line 2. 5

6

Q. Please explain Schedule C10 of Exhibit A-3 (KAD-3). 7

A. Schedule C10 of Exhibit A-3 (KAD-3) depicts MGUC’s 2014 projected test year local 8

taxes. The 2014 Total Company local taxes are $0, as shown on Line 2. 9

10

Q. Please explain Schedule C11 of Exhibit A-3 (KAD-3). 11

A. Schedule C11 of Exhibit A-3 (KAD-3) depicts MGUC’s 2014 projected test year 12

AFUDC. The 2014 Total Company AFUDC is $0, as shown on Line 5. 13

14

Q. Please explain Schedule C12 of Exhibit A-3 (KAD-3). 15

A. Schedule C12 of Exhibit A-3 (KAD-3) calculates the Income Tax Effect of Additional 16

Interest Allowed for MGUC’s 2014 projected test year. The tax effect of additional 17

interest allowed multiplied by the current income tax rate of 41% is $4,947, as shown 18

on line 20. 19

20

Q. Please explain Schedule C13 of Exhibit A-3 (KAD-3). 21

A. Schedule C13 of Exhibit A-3 (KAD-3) develops the O&M costs for MGUC’s 2014 22

projected test year. This series of workpapers starts with 2012 actual O&M 23

amounts. The 2012 expenses were first inflated at the estimated inflation factors of 24

1.708% for 2013 and 1.993% for 2014, as calculated on Exhibit A-7 (KAD-4). Next, 25

the Cost of Gas accounts were trued up to the 2014 forecasted costs. Lastly, O&M 26

was adjusted for K&M items. 27

- 25 -

1

Q. Please explain Schedule C14 of Exhibit A-3 (KAD-3). 2

A. Schedule C14 of Exhibit A-3 (KAD-3) calculates the K&M increase regarding costs to 3

remediate former manufactured gas plant sites. In its March 30, 1994 order in Case 4

No. U-10503, and its November 10, 2005 order in Case No. U-14657, the 5

Commission authorized MGUC to employ deferred accounting treatment for costs 6

associated with the remediation of former manufactured gas plant sites. Since 2002, 7

MGUC has conducted remediation activities at former manufactured gas plant sites 8

located in: 9

1. Benton Harbor (Remedial investigations, source removal, groundwater 10 monitoring, and property acquisition) 11

12 2. Cadillac (Remedial investigations, groundwater monitoring, source 13

removal, and property acquisition) 14 15

3. Coldwater Race Street (Remedial investigations, source removal, 16 groundwater monitoring, and closure documentation) 17

18 4. Grand Haven (Remedial investigations, source removal, and groundwater 19

monitoring) 20 21

5. Hillsdale (Remedial investigations, source removal, and groundwater 22 monitoring) 23

24 6. Otsego (Remedial investigations, source removal, groundwater 25

monitoring, and property acquisition) 26 27

7. South Haven (Remedial investigations, source removal, and property 28 acquisition) 29

30 8. Sturgis (Groundwater monitoring and closure documentation) 31

32 9. Traverse City (Groundwater monitoring) 33

34 10. Coldwater Chicago Street (Remedial investigations). 35

36

MGUC calculated the 2014 projected test year amortization expense in accordance 37

with the Commission’s current practice of amortizing deferred manufactured gas 38

plant remediation costs on a vintage basis over ten years. Therefore, for the 2014 39

projected test year, MGUC has calculated a K&M increase of $127,247 in Account 40

- 26 -

735, as shown on Line 8. 1

2

Q. Are environmental response activities performed and costs incurred under the 3

direction of the Michigan Department of Environmental Quality (MDEQ), as 4

required under Part 201, Environmental Remediation of the Natural Resources 5

and Environmental Protection Act (NREPA), 1994 PA 451, as amended (Act 6

451)? 7

A. Yes, they are. 8

9

Q. For what time period has Commission Staff already audited MGUC’s 10

Manufactured Gas Plant expenses? 11

A. As documented in Case No. U-15990, Data Request 01-JEL-10, provided on 12

September 24, 2009, Commission Staff has audited Manufactured Gas Plant 13

expenses through August 21, 2009 business. 14

15

Q. Please explain Schedule C15 of Exhibit A-3 (KAD-3). 16

A. Schedule C15 of Exhibit A-3 (KAD-3) calculates the $68,127 K&M adjustment 17

associated with Pay-at-Risk. Page 1 of 3 of Schedule C30, Exhibit A-3 (KAD-3) 18

calculates the K&M increase; page 2 of 3 identifies the removal of the 2012 inflated 19

Pay-at-Risk expenses; and page 3 of 3 calculates the inclusion of the forecasted 20

2014 Pay-at-Risk expenses. This adjustment was made so that all Pay-at-Risk 21

expenses that are included in the 2014 forecasted test year were included at the 22

“target” level. 23

24

Q. Please explain Schedule C22 of Exhibit A-3 (KAD-3). 25

A. Schedule C22 of Exhibit A-3 (KAD-3) calculates the K&M adjustment related to the 26

customer relations and ICE 2016 O&M costs related to the ICE 2016 project. The 27

- 27 -

ICE 2016 project is further explained in the pre-filed direct testimony of Mr. Brian E. 1

Kage and Mr. Michael E. Gerth. 2

3

The O&M costs related to customer relations and the ICE 2016 project are recorded 4

in FERC Accounts 901, 903, 905, 907, and 908. These costs can be summarized 5

into three categories: Customers Relations Labor, Customer Relations Non-Labor, 6

and ICE 2016 O&M. 7

8

The Customer Relations Labor and Customer Relations Non-Labor costs include the 9

impact of the ICE Project on IBS Customer Relations operational O&M costs 10

allocated to MGUC. These summaries exclude ICE 2016 Project Implementation 11

Costs except for the portion of IBS Customer Relations operating labor resources 12

that are forecasted to be capitalized during 2014 and 2015; these are recognized as 13

a partial return of that labor to O&M in 2015 and full return in 2016. 14

15

The ICE 2016 O&M costs that are depicted are the costs incurred during the 16

implementation phases of the ICE 2016 Project. These costs include project O&M 17

expense contingency for internal Integrys labor, contracted labor, Accenture partner 18

labor and expenses, software O&M, and miscellaneous O&M. The project O&M 19

expense for internal labor has been subtracted out of the project total O&M to avoid 20

double counting the O&M expense for internal labor between the Project O&M, IBS 21

Customer Relations O&M, and ITS operational O&M. 22

23

Schedule C22 of Exhibit A-3 (KAD-3), Page 2 of 2, presents the expenses in FERC 24

accounts 901, 903, 905, 907, and 908 for the 2012 Historical Test Year, summarized 25

by the three categories discussed above. Line 1 contains Customer Relations Labor 26

costs of $577,313; Line 2 contains Customer Relations Non-Labor costs of 27

- 28 -

$4,905,754; Line 3 contains ICE 2016 O&M costs of $79,074; and Line 4 displays 1

the balance contained in the five accounts of $1,104,356; for a total in these 2

accounts of $6,666,497. The 2012 costs are inflated based on the inflation factors 3

presented in Exhibit A-7 (KAD-4). The inflated 2014 forecasted costs in accounts 4

901, 903, 905, 907, and 908 are further adjusted for K&M costs of $372,785 related 5

to the customer relations and ICE 2016 project O&M costs for 2014, resulting in a 6

total 2014 forecasted amount of $7,288,282, as shown on page 1 of 2 of Schedule 7

C22, Exhibit A-3 (KAD-3). 8

9

Q. Please explain Schedule C23 of Exhibit A-3 (KAD-3). 10

A. Schedule C23 of Exhibit A-3 (KAD-3) calculates the K&M adjustment associated with 11

uncollectibles expense. MGUC has forecasted its 2014 projected test year 12

uncollectibles expense to equal a 3-year historical average of 2010 - 2012, which is 13

$1,917,930. This results in a total K&M increase of $422,307 in Account 904, as 14

shown on Line 8. 15

16

Q. Please explain Schedule C24 of Exhibit A-3 (KAD-3). 17

A. Schedule C24 of Exhibit A-3 (KAD-3) calculates the 2014 projected test year 18

uncollectibles expense of $1,917,930 referenced in Schedule C23 of Exhibit A-3 19

(KAD-3). As shown on this exhibit, for the 3-year period 2010-2012, MGUC’s 20

average net uncollectibles have equaled 1.43389% of MGUC’s tariff revenues. This 21

value was multiplied by MGUC’s 2014 projected test year retail revenues of 22

$133,757,462 to arrive at a 2014 projected test year uncollectibles expense of 23

$1,917,930, as shown on Line 11. MGUC proposes that its UETM be updated with 24

this new value for uncollectibles expense. 25

26

27

- 29 -

Q. Please explain Schedule C25 of Exhibit A-3 (KAD-3). 1

A. Schedule C25 of Exhibit A-3 (KAD-3) calculates the $213,581 K&M adjustment for 2

vacant positions IBS experienced in 2012. As shown on Schedule C25, Page 2 of 2, 3

this adjustment was calculated by dividing the average base and overtime of IBS 4

internal O&M by the average FTE’s in 2012. This average O&M per FTE was then 5

multiplied by the 72 vacant FTE’s IBS experienced in 2012. MGUC is allocated 3.6% 6

of these IBS costs; the remaining costs are allocated to the other Integrys 7

subsidiaries. The result was then multiplied by the inflation factor from Exhibit A-7 8

(KAD-4) to calculate the K&M adjustment. 9

10

Q. Please explain Schedule C26 of Exhibit A-3 (KAD-3). 11

A. Schedule C26 of Exhibit A-3 (KAD-3) calculates the $78,433 K&M adjustment related 12

to an increase in regulatory labor expenses associated with a rate case. There was 13

no rate case in 2012; therefore, there were no costs associated with a rate case in 14

the 2012 Historical Test Year O&M expenses. 15

16

Q. Please explain Schedule C27 of Exhibit A-3 (KAD-3). 17

A. Schedule C27 of Exhibit A-3 (KAD-3) calculates the $146,069 K&M adjustment 18

related to the elimination of the A&G Loader that was previously added to all MGUC 19

capital projects. This practice is not followed at the other Integrys utilities and in the 20

interest of standardizing accounting practices, the A&G Loader is being eliminated. 21

The value was calculated as the five-year historical average of the A&G loader, as 22

shown on line 15. 23

24

Q. Please explain Schedule C28 of Exhibit A-3 (KAD-3). 25

A. Schedule C28 of Exhibit A-3 (KAD-3) calculates the $6,395 K&M adjustment related 26

to an increase in regulatory non-labor expenses associated with a rate case. There 27

- 30 -

was no rate case in 2012; therefore, there were no costs associated with a rate case 1

in the 2012 Historical Test Year O&M expenses. 2

3

Q. Please explain Schedule C29 of Exhibit A-3 (KAD-3). 4

A. Schedule C29 of Exhibit A-3 (KAD-3) calculates the decrease of $22,007 K&M 5

adjustment associated with injuries and damages. MGUC has forecasted its 2014 6

projected test year injuries and damages expense to be equal to its 3-year historical 7

average, which is $446,851 as shown on line 12. 8

9

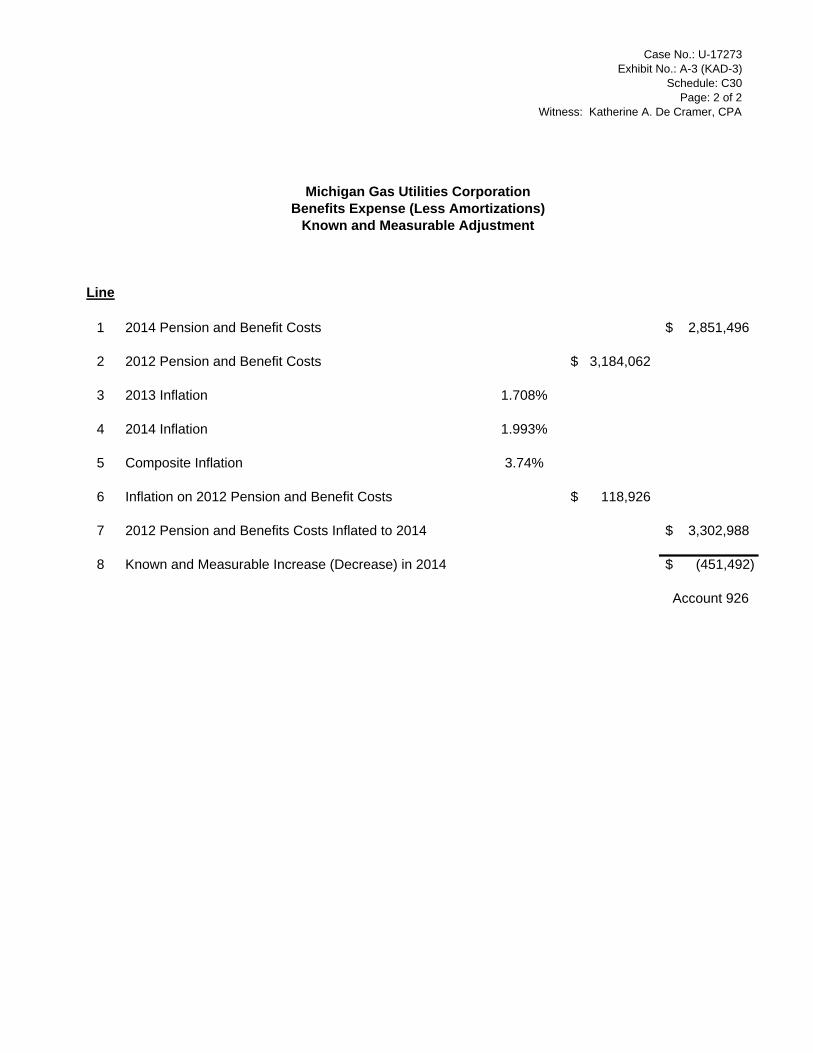

Q. Please explain Schedule C30 of Exhibit A-3 (KAD-3). 10

A. Schedule C30 of Exhibit A-3 (KAD-3) calculates the Benefits K&M decrease for 11

MGUC. 12

13

First, in the Commission’s January 9, 2007 Order in Case No. U-15138, the 14

Commission authorized the deferral and amortization of MGUC’s pension and OPEB 15

obligations recorded on its opening balance sheet as a result of the purchase of 16

MGUC from Aquila. As a result of this order, MGUC annually amortized $1,594,678 17

of expense, which was decreased to $1,594,610 for 2012, due to an amortization 18

that ended. Due to the combination of the lower amortization amount, and because 19

this amortization is not impacted by inflation, a K&M decrease of $90,559 in Account 20

926 was calculated, as shown on Line 8 of page 1. 21

22

Second, excluding the Account 926 impact of the K&M adjustment in Schedule C15 23

of Exhibit A-3 (KAD-3), and the amortization discussed above, MGUC is forecasting 24

a K&M decrease for MGUC employees of $451,492 in Account 926, as shown on 25

Line 8 of page 2. Further information regarding this calculation can be found on 26

page 2 of Schedule C30 of Exhibit A-3 (KAD-3), and in the pre-filed direct testimony 27

- 31 -

of Christine M. Phillips. 1

2

Taken together, these two adjustments result in a net K&M decrease of $542,051 in 3

Account 926. 4

5

Q. Please explain Schedule C31 of Exhibit A-3 (KAD-3). 6

A. Schedule C31 of Exhibit A-3 (KAD-3) calculates the $119,810 K&M adjustment 7

related to IBS depreciation of a Gas Management System (“GMS”) and ICE 2016 8

hardware. The annual IBS depreciation is allocated to each business unit based on 9

gas throughput; therefore, MGUC will be allocated $98,863. The annual IBS 10

depreciation for MGUC for the ICE 2016 hardware is $20,947. Taken together, 11

these values sum to $119,810. 12

13

Q. Please explain Exhibit A-7 (KAD-4). 14

A. Exhibit A-7 (KAD-4) calculates the inflation factors for 2013 and 2014 that were 15

subsequently applied to 2012 historic year O&M expenses to calculate 2014 16

projected test year O&M expenses. The schedule calculates the simple average of 17

five independent inflation forecasts, and results in an inflation factor if 1.708% for 18

2013, and 1.993% for 2014. 19

20

This methodology is similar to that used by MPSC Staff witness, Kirk K. Megginson, 21

in Case No. U-14893, SEMCO Energy Gas Company’s 2007 general rate case. 22

23

Q. Please explain Exhibit A-8 (KAD-5). 24

A. Exhibit A-8 (KAD-5) is a schedule of the Uncollectibles Expense Tracking 25

Mechanism (“UETM”) allocation factors for MGUC. As previously stated, MGUC 26

requests to extend its currently authorized UETM until its next general rate case. 27

- 32 -

Therefore, MGUC here provides updated allocators for the UETM, which are based 1

on actual Uncollectibles Expense from 2013. 2

3

Q. Please describe Exhibit A-9 (KAD-6). 4

A. Exhibit A-9 (KAD-6) is a summary of Awards & Recognition earned by Integrys and 5

Integrys subsidiaries during 2006-2012. 6

7

Q. Please explain Schedule A1 of Exhibit A-11 (KAD-7). 8

A. Schedule A1 of Exhibit A-11 (KAD-7) calculates MGUC’s 2012 historic test year 9

revenue deficiency based on its rate base, adjusted net operating income, rate of 10

return, and revenue conversion factor. This schedule develops the 2012 Total 11

Company revenue deficiency of $6,301,860, as shown on Line 16, using a 10.75% 12

return on equity. The component parts of this schedule are taken from the various 13

sources indexed to the left of these amounts. 14

15

Q. Please explain Schedule B1 of Exhibit A-12 (KAD-8). 16

A. Schedule B1 of Exhibit A-12 (KAD-8) calculates MGUC’s 2012 historic test year rate 17

base. The 2012 Total Company rate base is $194,076,269, as shown on Line 21. 18

The component parts of this schedule are taken from the various sources indexed to 19

the left of these amounts. 20

21

Q. Please explain Schedule B2 of Exhibit A-12 (KAD-8). 22

A. Schedule B2 of Exhibit A-12 (KAD-8) calculates MGUC’s 2012 historic test year 23

utility plant. The 2012 Total Company utility plant is $314,401,740, as shown on Line 24

13. 25

26

27

- 33 -

Q. Please explain Schedule B3 of Exhibit A-12 (KAD-8). 1

A. Schedule B3 of Exhibit A-12 (KAD-8) depicts MGUC’s 2012 historic test year 2

accumulated provision for depreciation. The 2012 Total Company accumulated 3

provision for depreciation is $171,640,370, as shown on Line 2. 4

5

Q. Please explain Schedule B4 of Exhibit A-12 (KAD-8). 6

A. Schedule B4 of Exhibit A-12 (KAD-8) calculates MGUC’s 2012 historic test year 7

working capital. The 2012 Total Company working capital is $51,314,899, as shown 8

on Line 41. 9

10

Q. Please explain Schedule C1 of Exhibit A-13 (KAD-9). 11

A. Schedule C1 of Exhibit A-13 (KAD-9) calculates MGUC’s 2012 historic test year 12

adjusted net operating income. The 2012 Total Company adjusted net operating 13

income is $9,943,804, as shown on Line 22. 14

15

Q. Please explain Schedule C2 of Exhibit A-13 (KAD-9). 16

A. Schedule C2 of Exhibit A-13 (KAD-9) calculates MGUC’s 2012 historic test year 17

gross revenue conversion factor. The 2012 gross revenue conversion factor is 18

1.637, as shown on Line 14. 19

20

Q. Please explain Schedule C3 of Exhibit A-13 (KAD-9). 21

A. Schedule C3 of Exhibit A-13 (KAD-9) calculates MGUC’s 2012 historic test year total 22

revenue. The 2012 Total Company total revenue is $122,621,203, as shown on Line 23

6. 24

25

Q. Please explain Schedule C4 of Exhibit A-13 (KAD-9). 26

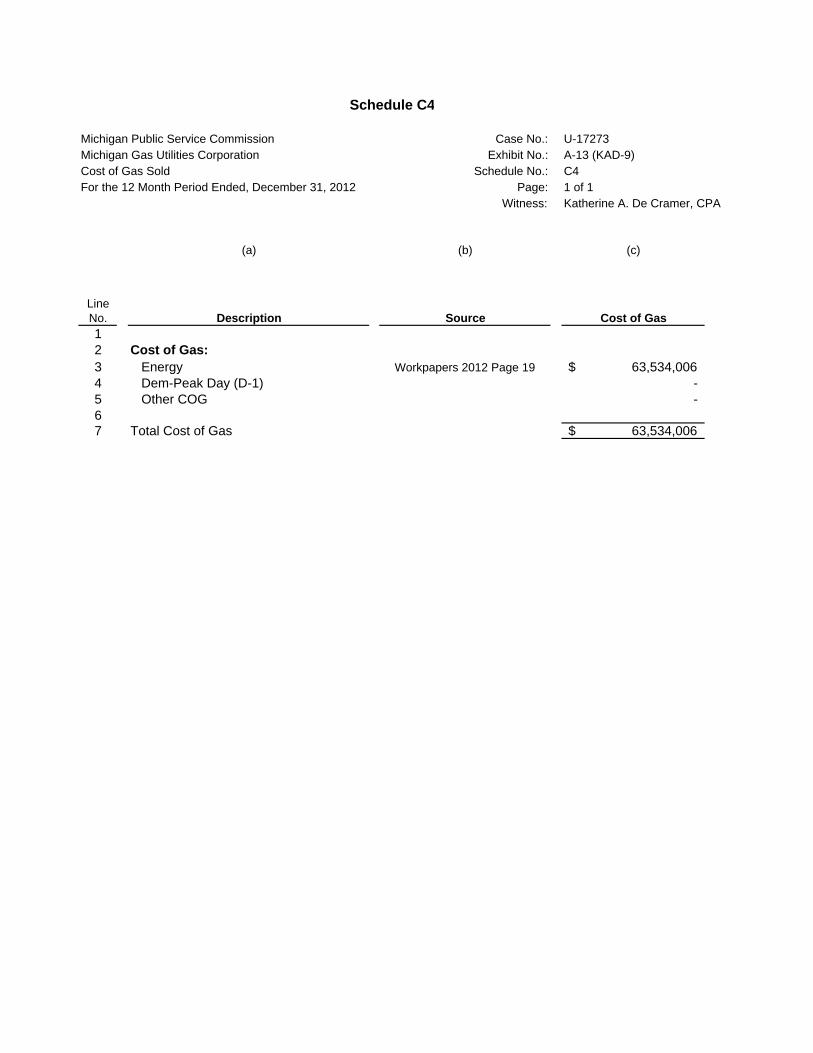

A. Schedule C4 of Exhibit A-13 (KAD-9) calculates MGUC’s 2012 historic test year cost 27

- 34 -

of gas. The 2012 Total Company cost of gas is $63,534,006, as shown on Line 7. 1

2

Q. Please explain Schedule C5 of Exhibit A-13 (KAD-9). 3

A. Schedule C5 of Exhibit A-13 (KAD-9) calculates MGUC’s 2012 historic test year total 4

O&M expense, exclusive of the cost of gas. The 2012 Total Company total O&M 5

expense, exclusive of the cost of gas, was $33,647,791, as shown on Line 19. 6

7

Q. Please explain Schedule C6 of Exhibit A-13 (KAD-9). 8

A. Schedule C6 of Exhibit A-13 (KAD-9) depicts MGUC’s 2012 historic test year total 9

depreciation and amortization expense. The 2012 Total Company total depreciation 10

and amortization expense is $8,115,375, as shown on Line 6. 11

12

Q. Please explain Schedule C7 of Exhibit A-13 (KAD-9). 13

A. Schedule C7 of Exhibit A-13 (KAD-9) calculates MGUC’s 2012 historic test year total 14

for taxes other than income taxes. The 2012 Total Company total for taxes other 15

than income taxes is $4,264,075, as shown on Line 31. 16

17

Q. Please explain Schedule C8 of Exhibit A-13 (KAD-9). 18

A. Schedule C8 of Exhibit A-13 (KAD-9) depicts MGUC’s 2012 historic test year federal 19

income taxes. The 2012 Total Company federal income taxes are $2,868,188, as 20

shown on Line 2. 21

22

Q. Please explain Schedule C9 of Exhibit A-13 (KAD-9). 23

A. Schedule C9 of Exhibit A-13 (KAD-9) depicts MGUC’s 2012 historic test year state 24

income taxes. The 2012 Total Company state income taxes are $200,010, as shown 25

on Line 2. 26

27

- 35 -

Q. Please explain Schedule C10 of Exhibit A-13 (KAD-9). 1

A. Schedule C10 of Exhibit A-13 (KAD-9) depicts MGUC’s 2012 historic test year local 2

taxes. The 2012 Total Company local taxes are $0, as shown on Line 2. 3

4

Q. Please explain Schedule C11 of Exhibit A-13 (KAD-9). 5

A. Schedule C11 of Exhibit A-13 (KAD-9) depicts MGUC’s 2012 historic test year 6

AFUDC. The 2012 Total Company AFUDC is $0, as shown on Line 5. 7

8

Q. Please explain Schedule C12 of Exhibit A-13 (KAD-9). 9

A. Schedule C12 of Exhibit A-13 (KAD-9) calculates the Income Tax Effect of Additional 10

Interest Allowed for MGUC’s 2012 historical test year. The tax effect of additional 11

interest allowed multiplied by the current income tax rate of 41% is $47,954, as 12

shown on line 20. 13

14

Depreciation Rates 15 Q. What depreciation rates were used in this rate case? 16