Embed Size (px)

Citation preview

INVESTMENT SOLUTIONS & PRODUCTS Economic Research

Company succession in practice

June 2016

The challenge of generation change

Succession rate Type of succession Distribution principles Every fifth SME is ap-proaching company suc-cession

Page 8

More than half of SMEs handed over to non-family members

Page 18

Ownership and management: Who receives what?

Page 22

2Swiss Issues Industries I June 2016

Publishing information

Publisher: Investment Solutions & Products Loris Centola Global Head of PB Research Tel. +41 (0)44 333 57 89 Email: [email protected] Dr. Oliver Adler Head of Economic Research Tel. +41 (0)44 333 09 61 Email: [email protected] Contact Credit Suisse Economic Research Email: [email protected] Tel. +41 (0)44 333 77 35 Center for Family Business (CFB), University of St. Gallen Email: [email protected] Tel. +41 (0)71 224 71 00 Editorial deadline May 20, 2016 Publication series Swiss Issues Branchen Orders Electronic copies via www.credit-suisse.com/research. Copyright The publication may be quoted with reference to the source. Copyright © 2016 Credit Suisse AG and/or its affiliates. All rights reserved.

Authors

Mateja Andric, CFB, University of St. Gallen Dr. Miriam Bird, CFB, University of St. Gallen Andreas Christen, Credit Suisse Economic Research Emilie Gachet, Credit Suisse Economic Research Dr. Frank A. Halter, CFB, University of St. Gallen Sonja Kissling, CFB, University of St. Gallen Roman Schenk, Credit Suisse Economic Research Prof. Dr. Thomas Markus Zellweger, CFB, University of St. Gallen Contribution Thomas Schatzmann, Credit Suisse Economic Research

3Swiss Issues Industries I June 2016

Contents

Editorial 4

Management summary 5

Information on the survey 7

Company succession – Stock-taking 8

Entrepreneur demographics 12

Family firms – Overview 14

Family firms – Governance structures at SMEs 16

Type of succession – Overview 18

Type of succession – Family influence 20

Distribution principles 22

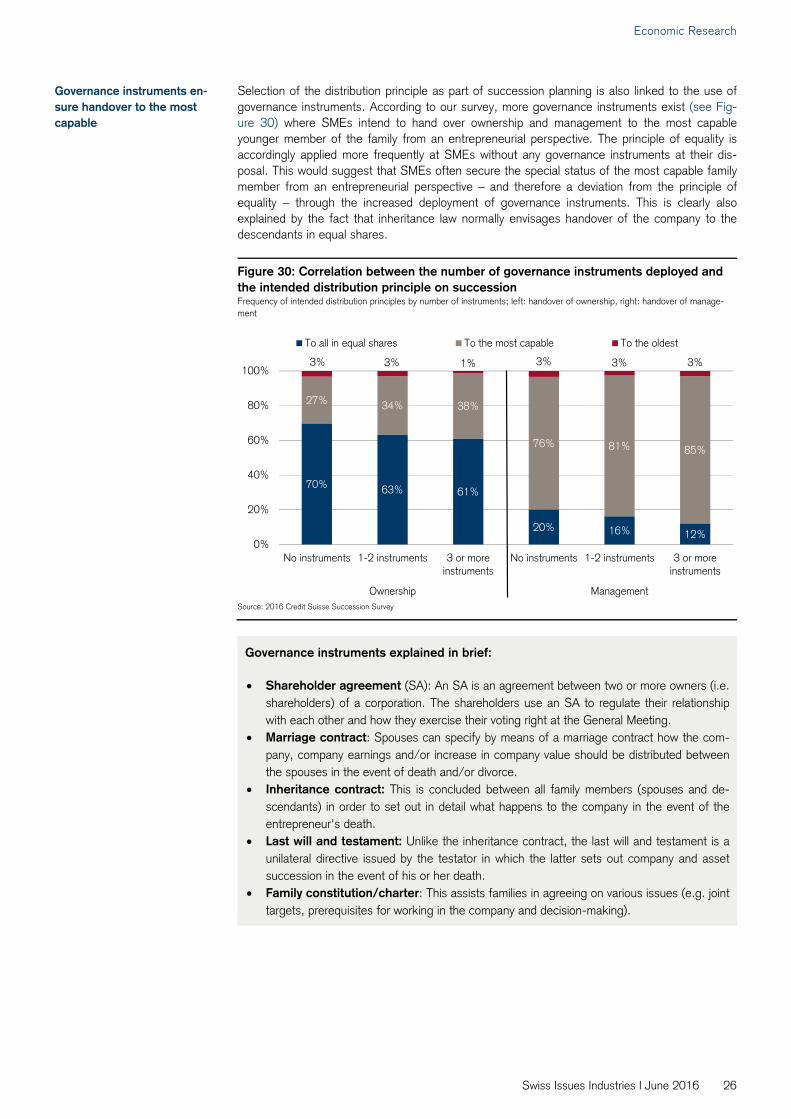

Governance instruments 25

Asset governance 28

4Swiss Issues Industries I June 2016

Economic Research

Editorial Just like the founding or expansion period, company succession is one of the decisive stages in the life cycle of every company. A generation change at the top of the company is a complex process that poses a wide range of challenges to both the entrepreneurs affected and their environment, as not only material and financial aspects are involved in succession planning but emotional aspects almost always also play a role. This is naturally all the more so in the case of family firms for which the business and private spheres are strongly interwoven. In our 2016 succession survey, over 1,300 small and medium-sized enterprises provided an insight into their ownership and management structures and reported on their experiences and plans with regard to company succession. Our study accordingly contributes to a better under-standing of the challenges confronting Swiss SMEs in the field of succession. We would like to take this opportunity once again to express our warm thanks to all participants in the survey. The high relevance and topicality of the issue are underlined by the survey results: Over three quar-ters of those surveyed have already begun to think about their own succession arrangements, and one in five even plans to hand over the company within the next five years. Based on this information we estimate that over 70,000 SMEs are currently approaching a generation change in Switzerland. This study is a joint project by our Economic Research and the Center for Family Business (CFB) of the University of St. Gallen, the leading Swiss institution in the research and teaching of com-pany succession. Credit Suisse and the CFB of the University of St. Gallen can look back on a sound track record of successful cooperation: Detailed examinations of key questions concern-ing the issue of company succession were already carried out in the preceding studies in 2009 and 2013. This year's study contains an update of the most important key figures as well as new and in-depth findings about the causal relationships of succession processes. Among other things we examine the question of how the demographic change is set to influence the number of company successions in Switzerland in the years to come. We also investigate the effect of family dynamics and government instruments on company handovers. Each section is supple-mented with practical recommendations. As the bank for entrepreneurs, Credit Suisse supports its clients in all phases of entrepreneur-ship as a professional contact partner. For example, we support more than 350 company suc-cessions each year. We hope that you as an entrepreneur are able to gain some helpful input for planning your own succession from our study and would be delighted to assist you with this task. We wish you an interesting and informative read!

Andreas Gerber Andreas Arni Dr. Oliver Adler Head of SME Business Switzerland Head of Entrepreneurs & Executives Head of Economic Research

Corporate & Institutional Clients Private & Wealth Management Clients International Wealth Management

5Swiss Issues Industries I June 2016

Economic Research

Management summary Company succession represents one of the most core strategic tasks facing all entrepreneurs. Almost every entrepreneur has to address it sooner or later. And it is not just a question of finan-cial but almost always also of intangible assets, as one's own business is generally more than a mere source of income. Our survey among over 1,300 SMEs illustrates clearly just how im-portant the topic is in the eyes of entrepreneurs. More than three quarters of the chief execu-tives questioned have at least partially addressed their own succession planning. One in five SMEs is actually planning a company succession within the next five years. Extrapo-lated for the overall economy, this means that by 2021 around 70,000 to 80,000 SMEs will be facing a generation change. These companies are responsible for over 400,000 jobs, which is equivalent to around 10% of all employees in Switzerland. The high macroeconomic importance of successful succession processes is therefore undeniable. A failed or unsatisfactory company succession exerts a negative impact not only on the company affected and its workforce, but also on its business partners. According to our survey, around a quarter of all SMEs often had negative experiences with company successions of business partners such as clients and suppli-ers. The share of SMEs seeking to hand over to the next generation within the coming five years has fallen slightly compared with 2013 from 22% to 20%. We think that this decrease is very likely only to be a temporary phenomenon. More than half of SME chief executives are today aged between 50 and 65 and thus belong to the babyboomer generation. Today around 560,000 people throughout Switzerland are between 60 and 65 years of age and therefore immediately approaching retirement. At 750,000, this figure will be almost 50% higher in 2030. The retirement of this babyboomer generation is therefore very likely to result in significantly more company successions in the next 15 years. As at the same time the age group of the successor generation is growing much more slowly, an increasing shortage of potential successors could arise in the next 15 years. One possible strat-egy for filling this gap is to appoint more woman chief executives, since although the share of women holding management positions has risen in recent decades, women are today still only in charge of just under 10% of all SMEs. The share of women on boards of directors and executive boards amounts to around 20%. An increasing share of woman chief executives could potential-ly cushion the upcoming demographically-related imbalance between (male) sellers and (male) acquirers. While company succession does not just affect family firms, the latter are more strongly affected by the issue as the entrepreneur's financial and personal bonds with the company are particularly strong here. According to the survey, 75% of all SMEs are currently family firms. Extrapolated for Switzerland, this corresponds to 375,000 family firms with 1.6 million employees. Compared with surveys carried out in 2004 and 2013, the share of family firms has fallen somewhat. Rea-sons for this decrease could be of both an economic and sociological nature. On the one hand, industries have predominantly grown in Switzerland in recent years that are characterized less by family firms, such as healthcare and IT and corporate service providers. At the same time, social changes over the past few decades have led to more and more successors from entrepreneurial families pursuing a career outside the family business. Or to put it another way: Children today are less frequently willing to take over the business of their parents than used to be the case. It comes as little surprise in this context that family and non-family succession plans are now balancing each other. Although a relative majority of 41% of SMEs still wish to hand over the company within the family, around a fifth of these are also considering non-family solutions. Altogether, marginally more SMEs are today seeking a purely non-family succession solution (34%) than a purely family solution (33%). In our 2013 survey, the opposite ratio held. Among the non-family succession plans, selling to former (senior) employees is most frequently cited (management buyout, 25%), followed by selling to another company or a private equity company (21%) and selling to an individual outside the company (management buy-in, 17%). In reality,

Over three quarters of SME entrepreneurs have ad-dressed their own succes-sion (p. 8-11)

Every fifth SME is approach-ing company succession (p. 8-11)

Demographics will lead to more succession cases in the next few years (p. 12-13)

Lower but rising share of women on the management of SMEs (p. 12-13, 17)

Share of family firms falling (p. 14-15)

More than half of compa-nies handed over to non-family members (p. 18-19)

6Swiss Issues Industries I June 2016

Economic Research

above all management buy-ins take place more frequently than many SMEs plan. Forty-six per-cent of today's chief executives took over their company from a family member, 25% as part of a management buyout and 30% by means of a management buy-in. The influence of the family within the company has a decisive impact on the choice of type of succession, with the family relationships among the owners also playing an important role. SMEs in which there are no family members among the owners plan one day above all to hand over the company to (senior) employees. The more family members there are among the owners and on the executive board, the more likely the family buyout option is likely to gain significance at the cost of the management buyout. However, the readiness to sell to buyers outside the family and company only depends little on the strength of the family influence within the company. The intention to keep the company within the family is at its greatest at family firms if the owners include parents with their child and/or sibling relationships. If only spouses are included in the ownership, almost half of family firms plan a non-family handover. The question arises in the case of family successions as to which younger members of the fami-ly management and ownership should be handed over to. A range of distribution principles can be crucial for this decision: Should the company go to the most competent younger family mem-bers from an entrepreneurial perspective or be divided equally between all of them? According to our survey, the majority of SMEs would prefer to hand over ownership to all younger members in equal shares (65%). However, when handing over management SMEs would focus on the most capable family members from an entrepreneurial perspective. Only 3% of SMEs favor the princi-ple of primogeniture, that is, handover to the oldest son or daughter. The selection of distribution principles among other things also exerts an influence on company performance. If the previous generation focused on the performance principle when handing over management, today's man-agers will assess the development of company performance to be better than if the principle of equality or even the principle of primogeniture was applied to the change of management. A succession brings about changes to the structures and decision makers within the company. It is therefore very important that instruments are at hand for guaranteeing a smooth handover. According to our survey, frequent use of such governance instruments is made among owners of SMEs. Forty-two percent of SMEs make recourse to shareholder agreements, 36% to con-tracts under inheritance law and 35% to contracts under matrimonial law. Governance instru-ments can among other things serve to pave the way for future succession planning. Those SMEs that make use of a larger number of governance instruments accordingly display a greater tendency toward family succession plans. Family firms therefore appear to fall back on govern-ance instruments in order to preserve future family control within the company and in doing so prevent a sale of the company to non-family members. All succession planning involves setting a price for the company to be handed over. This price depends strongly on the personal relationship between the seller and the successor. Our survey shows that family members and friends are able to acquire the company at particularly favorable terms. Both groups receive an average discount of 41% of the market price. Eighteen percent of family successors even receive the business 'free of charge'. Only around a third of all ac-quirers pay the full market price or more. At 22%, business partners receive the smallest dis-count. The discount in the case of purchase by previously unknown persons or handover within the business is 27%.

Family influence determines type of succession (p. 20-21)

The principle of equality prevails for handover of ownership and that of per-formance for handover of management (p. 22-24)

SMEs make greater re-course to governance in-struments for family suc-cessions (p. 25-27)

Family members and friends acquire companies at the best price (p. 28)

7Swiss Issues Industries I June 2016

Economic Research

Information on the survey For the third time after 2009 and 20131, the Center for Family Business of the University of St. Gallen and Credit Suisse are jointly investigating the topic of company succession among Swiss small and medium-sized enterprises (SMEs) in 2016. As with the previous editions, the present study is based on a large-scale survey among company chief executives. The Credit Suisse 2016 succession survey is based on two questionnaires. The first question-naire was completed by 1,343 SME entrepreneurs from all parts of the country. They answered questions about the structure and history of their company, corporate management and the general handling of the topic of company succession. Five hundred and thirty-four entrepreneurs who took over their business in the last 20 years completed an additional questionnaire with further questions about the process of company succession. The sample size can therefore vary depending on the question and evaluation. The survey was conducted by an independent polling organization on an anonymous basis in January and February 2016. The anonymous data was collated and analyzed by the Center for Family Business of the University of St. Gallen and Credit Suisse Economic Research. The distribution of the survey participants deviates somewhat from the sector and size structure of the overall Swiss SME landscape2 reflected in the most recent statistics on corporate struc-ture (STATENT) of the Swiss Federal Statistical Office (SFSO) dating from 2013. Construction and industrial firms in particular are overrepresented in the survey, while SMEs from various service sectors are underrepresented (see Figure 1). In addition, micro firms with fewer than ten full-time equivalents (FTEs) are underrepresented in the survey compared to their actual fre-quency in Switzerland – in contrast to small and medium-sized enterprises (see Figure 2). How-ever, these discrepancies barely limit the survey's validity.

1 Credit Suisse (2009): Effective Succession Management – A Study of Emotional and Financial Aspects in SMEs; Credit Suisse (2013): Success Factors for Swiss SMEs – Company Succession in Practice. 2 The following sectors are excluded from the analysis: agriculture/forestry, energy/water supply, finance/insurance, public administration.

Figure 1: Sector distribution of survey participants Figure 2: Company size of survey participants Share of companies Share of companies

Source: 2016 Credit Suisse Succession Survey, Swiss Federal Statistical Office Source: 2016 Credit Suisse Succession Survey, Swiss Federal Statistical Office

0% 5% 10% 15% 20% 25% 30%

Construction

Trade and sales

Corporate services

Traditional industry

Healthcare, education and social services

High-tech industry

Information, communication, IT

Tourism and personal service providers

Traffic and transport

2016 Credit Suisse Succession Survey2013 economic structure according to SFSO

0% 20% 40% 60% 80% 100%

Micro firms(0–9 FTEs)

Small enterprises(10–49 FTEs)

Medium-sized enterprises

(50–249 FTEs)

2016 Credit Suisse Succession Survey2013 economic structure according to SFSO

8Swiss Issues Industries I June 2016

Economic Research

Company succession – Stock-taking

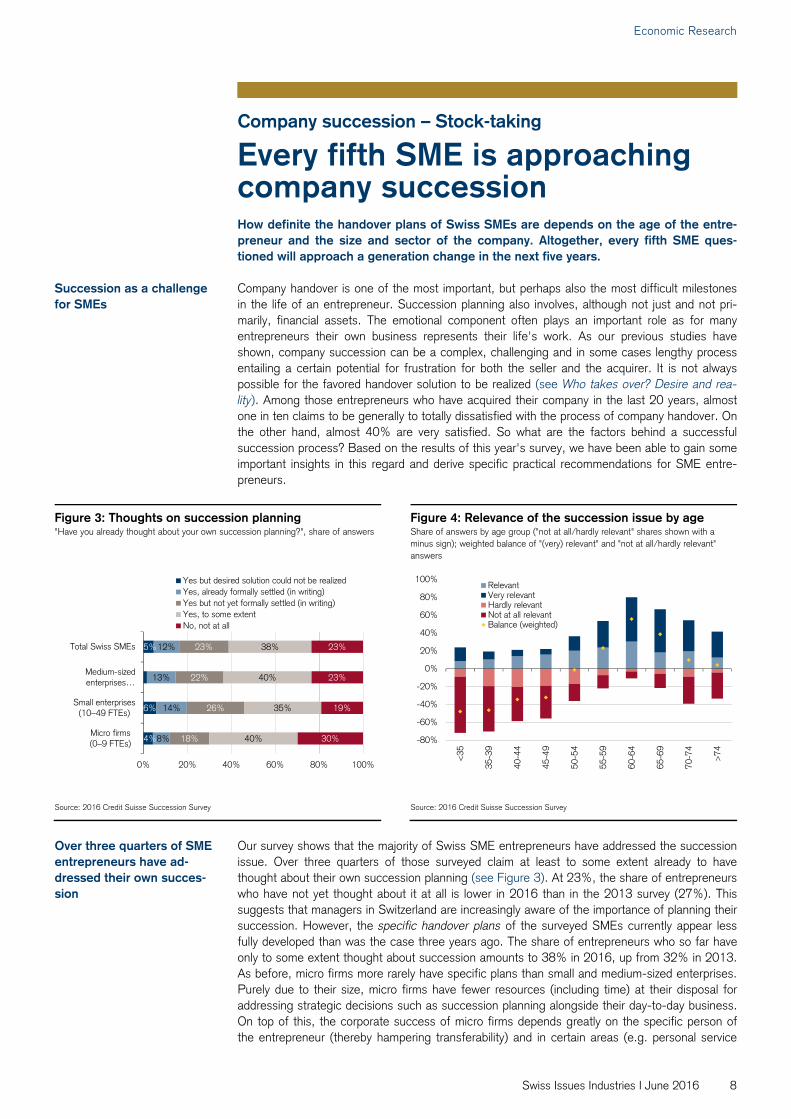

Every fifth SME is approaching company succession How definite the handover plans of Swiss SMEs are depends on the age of the entre-preneur and the size and sector of the company. Altogether, every fifth SME ques-tioned will approach a generation change in the next five years. Company handover is one of the most important, but perhaps also the most difficult milestones in the life of an entrepreneur. Succession planning also involves, although not just and not pri-marily, financial assets. The emotional component often plays an important role as for many entrepreneurs their own business represents their life's work. As our previous studies have shown, company succession can be a complex, challenging and in some cases lengthy process entailing a certain potential for frustration for both the seller and the acquirer. It is not always possible for the favored handover solution to be realized (see Who takes over? Desire and rea-lity). Among those entrepreneurs who have acquired their company in the last 20 years, almost one in ten claims to be generally to totally dissatisfied with the process of company handover. On the other hand, almost 40% are very satisfied. So what are the factors behind a successful succession process? Based on the results of this year's survey, we have been able to gain some important insights in this regard and derive specific practical recommendations for SME entre-preneurs.

Our survey shows that the majority of Swiss SME entrepreneurs have addressed the succession issue. Over three quarters of those surveyed claim at least to some extent already to have thought about their own succession planning (see Figure 3). At 23%, the share of entrepreneurs who have not yet thought about it at all is lower in 2016 than in the 2013 survey (27%). This suggests that managers in Switzerland are increasingly aware of the importance of planning their succession. However, the specific handover plans of the surveyed SMEs currently appear less fully developed than was the case three years ago. The share of entrepreneurs who so far have only to some extent thought about succession amounts to 38% in 2016, up from 32% in 2013. As before, micro firms more rarely have specific plans than small and medium-sized enterprises. Purely due to their size, micro firms have fewer resources (including time) at their disposal for addressing strategic decisions such as succession planning alongside their day-to-day business. On top of this, the corporate success of micro firms depends greatly on the specific person of the entrepreneur (thereby hampering transferability) and in certain areas (e.g. personal service

Succession as a challenge for SMEs

Figure 3: Thoughts on succession planning Figure 4: Relevance of the succession issue by age "Have you already thought about your own succession planning?", share of answers Share of answers by age group ("not at all/hardly relevant" shares shown with a

minus sign); weighted balance of "(very) relevant" and "not at all/hardly relevant" answers

Source: 2016 Credit Suisse Succession Survey Source: 2016 Credit Suisse Succession Survey

Over three quarters of SME entrepreneurs have ad-dressed their own succes-sion

4%

6%

5%

8%

14%

13%

12%

18%

26%

22%

23%

40%

35%

40%

38%

30%

19%

23%

23%

0% 20% 40% 60% 80% 100%

Micro firms (0–9 FTEs)

Small enterprises (10–49 FTEs)

Medium-sized enterprises …

Total Swiss SMEs

Yes but desired solution could not be realizedYes, already formally settled (in writing)Yes but not yet formally settled (in writing)Yes, to some extentNo, not at all

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

<35

35-3

9

40-4

4

45-4

9

50-5

4

55-5

9

60-6

4

65-6

9

70-7

4

>74

RelevantVery relevantHardly relevantNot at all relevantBalance (weighted)

9Swiss Issues Industries I June 2016

Economic Research

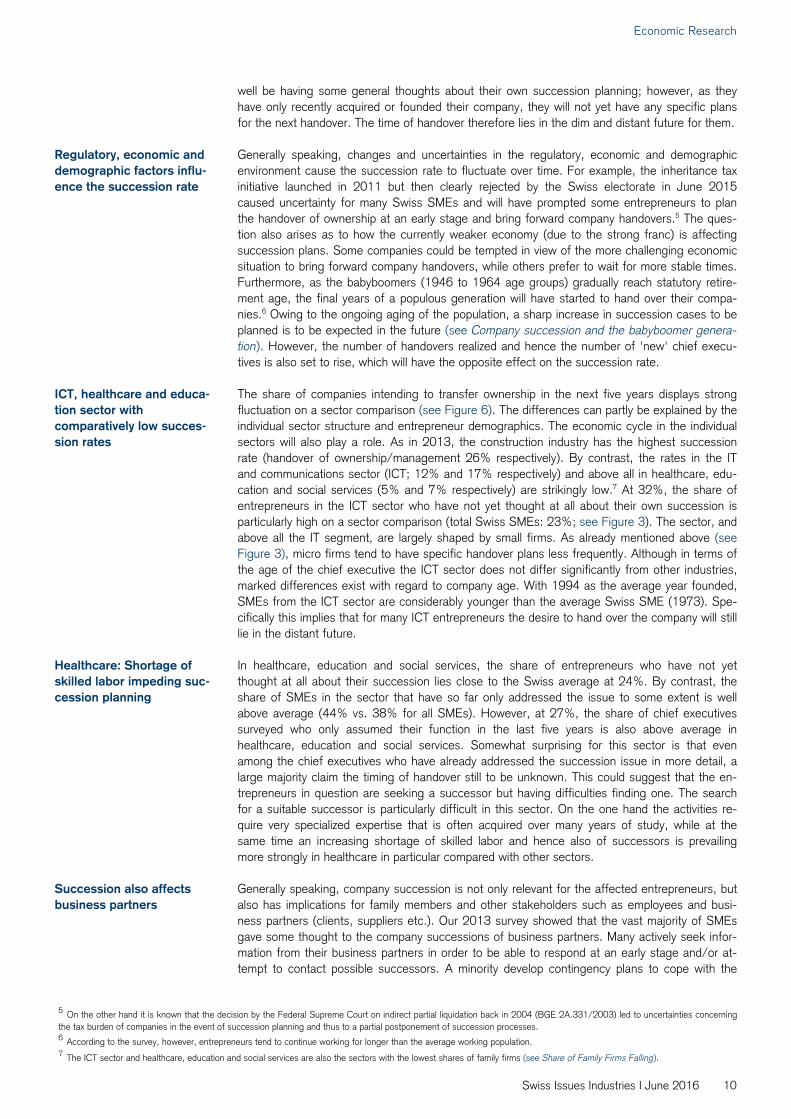

providers) new companies of the same type can be founded relatively easily so that transfer to the next generation of entrepreneurs may seem less attractive. How relevant the topic of succession is for each individual entrepreneur depends on a range of factors. The 2013 survey suggested that age combined with health was by far the most im-portant reason for withdrawing from the company, before the desire for more free time and financial aspects. As chief executives get older, the relevance of the succession issue accord-ingly increases for them (see Figure 4). Although there are isolated cases of young entrepre-neurs addressing the issue of their succession, the topic significantly gains importance from the age of 50. The relevance peaks between the ages of 60 and 65, i.e. shortly before statutory retirement age. In future the demographic changes that Switzerland is set to undergo over the coming years and decades could therefore exert a decisive influence on the number of planned company handovers. We address this issue in more detail in the section entitled Company suc-cession and the babyboomer generation. According to the survey, just under 30% of Swiss SMEs currently have a specific timetable regarding succession (see Figure 5). Twenty percent intend to transfer ownership of the compa-ny in the next five years; almost 14% already plan to do this in the next two years. Similar figures emerge for the transfer of management (21% and 14% respectively for a planned trans-fer in the next five or two years). However, for more than 70% of those surveyed the precise timing of their own succession is still not known – around a third of these comprise entrepre-neurs who have not yet thought at all about succession planning. At 20%, the current succession rate3 of Swiss SMEs is lower than in our previous surveys. In 2013, 22% of those surveyed intended to transfer ownership of the company within five years; in 2009 this share came to 29%. At the same time, the share of companies unable to state any specific timing for succession has risen in 2016 compared with the previous surveys (2009: 20%; 2013: 68%, 2016: 72%). However, for methodological reasons (among other things a different wording of the questions and sampling structure), the temporal comparison should be treated with a certain degree of caution.4

A more detailed analysis of the survey results brings to light some interesting findings that could help to explain why the succession rate in 2016 is lower than in 2013 despite SMEs devoting more attention to the issue. It thus appears that around a fifth of the chief executives taking part in this year's survey only assumed their present function within the last five years (i.e. in 2011 or later). In the 2013 survey this figure was just under 14%. These 'newly-fledged' managers may

3 We define the succession rate as the share of companies planning company succession in the next five years. 4 For example, the survey participants in 2009 also included companies with over 250 employees. In order to facilitate a representative comparison over time, we weight the succession rates calculated in the individual surveys for micro, small and medium-sized enterprises (see Figure 7 for the 2016 figures) with the number of companies by size category in accordance with the 2013 STATENT (see Information on the Survey). This results in a weighted SME succession rate (ownership handover) of 26% for the year 2009, 19% for 2013 and 15% for 2016, thus confirming the picture of a declining succession rate.

Succession issue becomes increasingly relevant with age

One fifth of SMEs plan a transfer by 2021

Succession rate lower in 2016 than in 2013

Figure 5: Time horizon of handover plans Figure 6: Succession rate by sector "When do you intend to hand over ownership/management of the company?", share of answers

Share of companies with handover plans for the next five years

Source: 2016 Credit Suisse Succession Survey Source: 2016 Credit Suisse Succession Survey

20% of those surveyed only became chief executive of their SME in the last five years

14%

14%

7%

6%

6%

5%

2%

3%

71%

72%

0% 20% 40% 60% 80% 100%

Managementhandover

Ownership handover

0–2 years 3–5 years 6–10 years > 10 years not yet known

0% 5% 10% 15% 20% 25% 30% 35%

Construction

High-tech industry

Corporate services

Total Swiss SMEs

Trade and sales

Tourism and personal service providers

Traffic and transport

Traditional industry

Information, communication, IT

Healthcare, education and social services

OwnershiphandoverManagementhandover

10Swiss Issues Industries I June 2016

Economic Research

well be having some general thoughts about their own succession planning; however, as they have only recently acquired or founded their company, they will not yet have any specific plans for the next handover. The time of handover therefore lies in the dim and distant future for them. Generally speaking, changes and uncertainties in the regulatory, economic and demographic environment cause the succession rate to fluctuate over time. For example, the inheritance tax initiative launched in 2011 but then clearly rejected by the Swiss electorate in June 2015 caused uncertainty for many Swiss SMEs and will have prompted some entrepreneurs to plan the handover of ownership at an early stage and bring forward company handovers.5 The ques-tion also arises as to how the currently weaker economy (due to the strong franc) is affecting succession plans. Some companies could be tempted in view of the more challenging economic situation to bring forward company handovers, while others prefer to wait for more stable times. Furthermore, as the babyboomers (1946 to 1964 age groups) gradually reach statutory retire-ment age, the final years of a populous generation will have started to hand over their compa-nies.6 Owing to the ongoing aging of the population, a sharp increase in succession cases to be planned is to be expected in the future (see Company succession and the babyboomer genera-tion). However, the number of handovers realized and hence the number of 'new' chief execu-tives is also set to rise, which will have the opposite effect on the succession rate. The share of companies intending to transfer ownership in the next five years displays strong fluctuation on a sector comparison (see Figure 6). The differences can partly be explained by the individual sector structure and entrepreneur demographics. The economic cycle in the individual sectors will also play a role. As in 2013, the construction industry has the highest succession rate (handover of ownership/management 26% respectively). By contrast, the rates in the IT and communications sector (ICT; 12% and 17% respectively) and above all in healthcare, edu-cation and social services (5% and 7% respectively) are strikingly low.7 At 32%, the share of entrepreneurs in the ICT sector who have not yet thought at all about their own succession is particularly high on a sector comparison (total Swiss SMEs: 23%; see Figure 3). The sector, and above all the IT segment, are largely shaped by small firms. As already mentioned above (see Figure 3), micro firms tend to have specific handover plans less frequently. Although in terms of the age of the chief executive the ICT sector does not differ significantly from other industries, marked differences exist with regard to company age. With 1994 as the average year founded, SMEs from the ICT sector are considerably younger than the average Swiss SME (1973). Spe-cifically this implies that for many ICT entrepreneurs the desire to hand over the company will still lie in the distant future. In healthcare, education and social services, the share of entrepreneurs who have not yet thought at all about their succession lies close to the Swiss average at 24%. By contrast, the share of SMEs in the sector that have so far only addressed the issue to some extent is well above average (44% vs. 38% for all SMEs). However, at 27%, the share of chief executives surveyed who only assumed their function in the last five years is also above average in healthcare, education and social services. Somewhat surprising for this sector is that even among the chief executives who have already addressed the succession issue in more detail, a large majority claim the timing of handover still to be unknown. This could suggest that the en-trepreneurs in question are seeking a successor but having difficulties finding one. The search for a suitable successor is particularly difficult in this sector. On the one hand the activities re-quire very specialized expertise that is often acquired over many years of study, while at the same time an increasing shortage of skilled labor and hence also of successors is prevailing more strongly in healthcare in particular compared with other sectors. Generally speaking, company succession is not only relevant for the affected entrepreneurs, but also has implications for family members and other stakeholders such as employees and busi-ness partners (clients, suppliers etc.). Our 2013 survey showed that the vast majority of SMEs gave some thought to the company successions of business partners. Many actively seek infor-mation from their business partners in order to be able to respond at an early stage and/or at-tempt to contact possible successors. A minority develop contingency plans to cope with the

5 On the other hand it is known that the decision by the Federal Supreme Court on indirect partial liquidation back in 2004 (BGE 2A.331/2003) led to uncertainties concerning the tax burden of companies in the event of succession planning and thus to a partial postponement of succession processes. 6 According to the survey, however, entrepreneurs tend to continue working for longer than the average working population. 7 The ICT sector and healthcare, education and social services are also the sectors with the lowest shares of family firms (see Share of Family Firms Falling).

Regulatory, economic and demographic factors influ-ence the succession rate

ICT, healthcare and educa-tion sector with comparatively low succes-sion rates

Healthcare: Shortage of skilled labor impeding suc-cession planning

Succession also affects business partners

11Swiss Issues Industries I June 2016

Economic Research

potential succession failure at their business partners. Our survey this year shows how important such measures are: Twenty-three percent of the SMEs surveyed claim to have had negative experiences with company successions of business partners frequently to very frequently. If profitable businesses fail as a result of succession planning and are thus forced to close their doors, economic value is lost in the form of jobs, value creation and tax receipts. As in the previ-ous editions, the information obtained in the context of this year's survey allows us to quantify the current and future significance of company succession for the Swiss economy. By extrapo-lating the size category-specific succession rates derived from the survey to the entire Swiss SME landscape, we arrive at the following results: In the next five years – i.e. by 2021 – over 74,000 companies with a total workforce of 406,000 full-time equivalents will be affected by an ownership handover (see Figure 7). This is equivalent to around 10% of all employees in Swit-zerland. According to these extrapolations, around 80,000 small and medium-sized enterprises with a total of 464,000 employees will be subjected to management handover in the next five years. These figures demonstrate vividly how important it is for the Swiss economy as a whole that the forthcoming succession processes actually succeed. We therefore aim with the analyses in the following sections to foster a better understanding of the mechanisms behind successful successions.

Stock-taking: findings and recommendations for practice Around 20% of all companies are invariably confronted with company succession – you

could talk about a mass phenomenon. At the same time, all succession planning must be viewed very individually.

Underlying conditions such as the economic environment, changes in legislation or the economy have an impact on the liquidity of the succession market. The significance of these trends which it is not possible for owners to influence varies for their own succes-sion depending on the sector.

The willingness of potential succession candidates to take on the business is receding in our part of the world. You should not therefore shut the door too quickly if you have a po-tential successor. There is no guarantee that you will find another one quickly in the fore-seeable future.

Your succession also affects your business partners (clients, suppliers etc.). Succession planning carried out early and then communicated clearly offers them security.

8 This figure corresponds to the succession rate calculated in Footnote 4 and weighted by size category.

70,000 to 80,000 Swiss SMEs affected by a succes-sion in the next five years

Figure 7: Significance of company successions up to 2021 Extrapolation

Economy* Ownership transfer Management transfer

Company size SMEs Employees

(FTE) Succession <5 years

SMEs Employees

(FTE) Succession <5 years

SMEs Employees

(FTE)

Micro firms 459,636 823,260 14% 64,349 115,256 15% 68,945 123,489

Small enterprises 35,031 710,854 25% 8,758 177,713 26% 9,108 184,822

Medium-sized enter-prises

7,115 707,151 16% 1,138 113,144 22% 1,565 155,573

Total 501,782 2,241,265 15%8 74,245 406,114 16% 79,619 463,884

Source: Swiss Federal Statistical Office, 2016 Credit Suisse Succession Survey *2013, excluding agriculture/forestry, energy/water supply, finance/insurance and public administration

12Swiss Issues Industries I June 2016

Economic Research

Entrepreneur demographics

Company succession and the babyboomer generation Many SME entrepreneurs belong to the babyboomer generation that will reach statuto-ry retirement age in the next ten years. The number of entrepreneurs wishing to hand over their business is therefore set to rise. The issue of company succession is closely connected with the age of the entrepreneur. As we have seen in the preceding section, it particularly gains significance between the ages of 50 and 65. It is therefore essential when examining the topic of company succession to be familiar with the demographic structure of the entrepreneurs. As in our study back in 2013, we accordingly take a close look at entrepreneur demographics. According to this year's survey, the average age of Swiss SME chief executives is 54 (2013: 55). They are therefore older than the entire working population that has an average age of 41 (see Figure 8). Entrepreneurs also continue working beyond regular retirement age considerably more frequently than the working population as a whole. Nevertheless, only 12% of SME chief executives are aged over 65. The majority (around 55%) are between 50 and 65 years of age and thus belong to the 1951 to 1966 birth cohorts – those generally referred to as the babyboomers. The babyboomer generation is among other things characterized by the fact that – as the name implies – it had a very high birth rate that was never again reached by the succeeding genera-tions. This is directly reflected in the population size of the individual age cohorts, as Figure 8 shows. The populous babyboomer generation is now gradually reaching regular retirement age. Switzerland therefore will see an unprecedented wave of retirements in the next 15 years or so. While in 2006 there were around 510,000 people aged between 60 and 65 and thus approach-ing retirement, there are now over 560,000 and in ten years there will be 750,000. This effect should level off again from around 2030 (see Figure 9). Although the demographic profile of Swiss SME entrepreneurs is not congruent with that of the working population as a whole (see Figure 8), it can be assumed that this 'babyboomer effect' also plays a role for company succession. The correlation between the planned time of handover of the company and proximity to regular retirement age is accordingly very strong, as we have illustrated in the preceding section. Furthermore, according to the 2013 survey, age and health factors were the main motive for around 61% of entrepreneurs to hand over their company. It is

More than half of Swiss SME entrepreneurs are aged between 50 and 65

Babyboomer generation reaching retirement age

Demographics will lead to more company successions in the next few years

Figure 8: Demographics of entrepreneurs and population Figure 9: Swiss population by age group Percentage by age (in years): SME entrepreneurs, working population (FTEs) in 2014, usual resident population in 2014

Number of persons; forecast from 2015

Source: 2016 Credit Suisse Succession Survey, Swiss Federal Statistical Office Source: Credit Suisse, Swiss Federal Statistical Office

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

2 12 22 32 42 52 62 72 82 92 102

Age of SME chief executives

Age of working population

Age of population

1,900,000

2,000,000

2,100,000

2,200,000

2,300,000

2,400,000

2,500,000

2,600,000

2,700,000

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

1980 1990 2000 2010 2020 2030 2040

No. of 60 to 65-year-olds in pastForecast no. of 60 to 65-year-oldsNo. of 25 to 45-year-olds in past (rt.-hand axis)Forecast no. of 25 to 45-year-olds (rt.-hand axis)

13Swiss Issues Industries I June 2016

Economic Research

therefore to be anticipated that the number of aspired company successions is set to rise for purely demographic reasons in the next ten years unless, for instance, the retirement age of SME chief executives rises as part of a general increase in retirement age. This development entails both an increasing need for advice about succession solutions among SME entrepreneurs as well as greater demand for potential successors. The average SME entrepreneur became chief executive at the age of 38 (admission to the ex-ecutive board at 36). Three quarters of the entrepreneurs surveyed were aged between 25 and 45 when they took over the management (see Figure 10). In absolute figures this cohort will only grow half as fast within the overall population as that of the 60 to 65-year-olds in the next ten years (see Figure 9).9 If we assume that there will be no change to the average accession age of SME chief executives in the future, the pool of potential succession candidates in relation to the number of potential sellers will accordingly contract significantly: Today there are 4.3 25 to 45-year-olds for every 65-year-old but in 2030 there will be only 3.4. To put it another way, the demographic trend is likely to impede the search for potential successors in the next decade. Two developments could mitigate this demographically-induced disparity between sellers and potential successors. Firstly, it is conceivable that owing to the general aging of the population the average age of takeover could also rise. It is already the case today that 12% of chief ex-ecutives currently in office were aged 50 or above when they assumed their position. Should this share rise as part of the demographic change of society or a general increase in the retirement age, the aforementioned disparity between sellers and potential successors will diminish some-what. A rising share of woman chief executives could also ease the situation. While only 4% of the predecessors of today's chief executives were women, at 10% this share is significantly higher for the current generation but still very low. Although woman chief executives are still clearly in a minority, the share of women who have taken over this position in the past ten years has nevertheless reached 12% (see Figure 11).10 This still very low share suggests considerable potential for growth. Further information about the participation of women in the management of Swiss SMEs can be found in Family Firms – Governance Structures at SMEs.

9 The growth of the successor group (25 to 45-year-olds) in relation to the strength of the individual age cohorts only amounts to one eighth of the seller group (60 to 65-year-olds). 10 As construction and industrial firms are overweighted and healthcare SMEs and personal service providers underweighted in the sample (see Figure 1 in Information on the survey), the share of woman chief executives of SMEs will in practice be slightly higher. Around a third of corporate management in healthcare, education and social services comprises women, compared with just 3% in construction. If we take these sector distortions into account, the share of woman chief executives increases slightly.

Is the demographic trend impeding the search for successors?

Older and more woman chief executives could ease the problem

Figure 10: Age on takeover of management Figure 11: Share of woman chief executives over time Percentage of respective age cohorts Share of woman chief executives; takeover of management in applicable period

Source: 2016 Credit Suisse Succession Survey Source: 2016 Credit Suisse Succession Survey

0%

5%

10%

15%

20%

25%

15-19 25-29 35-39 45-49 55-59 65-69 75-790%

2%

4%

6%

8%

10%

12%

before 1986 1986 to 1995 1996 to 2005 2006 to present

14Swiss Issues Industries I June 2016

Economic Research

Family firms – Overview

Share of family firms falling Seventy-five percent of all Swiss SMEs are family firms. This share has shrunk since 2013 and could fall further in the years to come. Nevertheless, the SME landscape will remain shaped by family firms in the future. Family firms are affected in a particular manner by the issue of company succession as the worlds of work and family are especially closely linked here. When the entrepreneur retires, the company and family therefore have to redefine themselves independently from each other in the absence of internal family succession. Moreover, the financial connection between the family and the business is often particularly strong in the case of family firms. The theme of fairness also takes on a special significance: For example, should the company be transferred to the most competent younger family members from an entrepreneurial perspective or should all family members be considered equally? What impact will this have on the future success of the busi-ness? To find out more about the importance of company succession for family firms, please see the following sections from page 20. The global share of family firms is estimated to be around 60 to 90%. The estimates for Switzer-land range from 88% in 200411 to 81% in 201312 and – based on our survey – 75% in 201613. If SMEs are questioned directly, only 60% describe themselves as family firms (2013: 66%). Family firms represent a majority of companies in all size categories and sectors, although they are found more frequently in certain economic branches than in others (see Figure 12). Extrapo-lated for Switzerland as a whole, a share of family firms of 75% corresponds to around 375,000 family SMEs in which some 1.6 million people are employed – around 41% of all employees in Switzerland. Family firms accordingly pose a central pillar of the Swiss economy.

11 Frey, Halter, Zellweger (2004): Bedeutung und Struktur von Familienunternehmen in der Schweiz. 12 Credit Suisse (2013): Success Factors for Swiss SMEs – Company Succession in Practice (newly weighted). 13 We describe family firms as companies in which there is a "substantial family influence". We consider there to be a substantial family influence if the sum of the family's percentage of total equity, seats on the management board and seats on the supervisory body is greater than 100% (see Halter/Schröder 2010). In the case of companies that cannot be clearly identified as family or non-family firms owing to a lack of data, we use the subjective assessment of companies that was also requested in the survey. The answers of the survey participants have been weighted by sector and size category in order to obtain a representative result that can be compared over time.

Family firms particularly affected by succession

Seventy-five percent of Swiss SMEs are family firms

Figure 12: Proportion of family companies by sector* Figure 13: Proportion of family firms and entrepreneur -generations* by period of foundation

Share of family firms; growth in number of companies 2011–2013 Vertical axis: share of companies; horizontal axis: period of foundation

Source: 2016 Credit Suisse Succession Survey, Swiss Federal Statistical Office; *according to substantial family influence, see Footnote 13

Source: 2016 Credit Suisse Succession Survey; *generation of entrepreneurs: answer to question of which generation is primarily active on the executive board

56%

59%

62%

75%

78%

79%

83%

83%

88%

0% 20% 40% 60% 80% 100%

Healthcare, education, social services

Information, communication, IT

Corporate services

High-tech industry

Construction

Tourism and personal service providers

Trade and sales

Traffic and transport

Traditional industry 0%

2%

-1%

4%

3%

-4%

8%

5%

8%

2011-2013 growth in no. of com

panies

0%

20%

40%

60%

80%

100%

2007

-201

6

1997

-200

6

1987

-199

6

1977

-198

6

1967

-197

6

1957

-196

6

1947

-195

6

1937

-194

6

1927

-193

6

befo

re 1

927

Share of founding generation Share of 2nd generationShare of 3rd generation Share of 4th generationShare of 5th generation and older Share of family firms

15Swiss Issues Industries I June 2016

Economic Research

A comparison of the survey results from the years 2004, 2013 and 2016 seems to suggest a constant decline in the share of family firms. However, these figures must be interpreted with a certain degree of caution. For example, the downturn between 2013 and 2016 lies within the range of uncertainty of the survey method. It is therefore not possible to conclude with certainty from these figures that the share of family firms really has decreased in the last few years. In order to answer this question, we need to consider other indicators. Figure 13 shows that the share of family firms is linked to the age of the company. Of those companies that were founded in the past ten years, only 58% are family firms. However, the share for periods of foundation preceding the end of the 1970s largely lies above 80%. This difference does not necessarily mean that the share of family firms has declined over time. First of all, the low rate among young companies could also partially be due to the fact that many initially do not consider themselves to be family firms at all but that a transformation takes place in this regard over time, for instance when the children complete their education and join the company. Secondly, founders of non-family firms will less frequently (wish to) hand over their businesses as independent companies than founders of family firms. Thirty-five percent of the founders of non-family firms but only 29% of first generation family firms ultimately intend to liquidate their company or sell it to another company. In other words, the share of family firms automatically increases with the gradual retirement of the founding generation and the leap to the second generation (see Figure 13). On the other hand, we also find indications that the share of family firms is indeed decreasing, although on a very long-term basis. Switzerland's economic structure is changing, with the im-portance of industry and trade decreasing while healthcare, corporate service providers and IT are growing continuously.14 Precisely these three growth sectors feature a significantly lower share of family firms than the other sectors (see Figure 12). The reasons for the relatively small number of family firms in these sectors will be both a relatively high degree of specialization and a strong dependence of the company on the specific person of the chief executive. By contrast, the highest share of family firms is to be found in industry and trade. If the number of companies from healthcare, IT and corporate services increases in proportion to the other sectors, the share of family firms from the perspective of the overall economy will shrink as a result. As well as the changing economic structure, sociological changes will also be responsible for the decline in the share of family firms.15 Since the end of the 1960s, the traditional family image has changed and the role of the individual has gained importance. Economic and social changes (due to the multi-option society) have increasingly opened up opportunities for potential succes-sors within the family also to found a company or pursue a career outside the family. This is another factor accounting for the gradual increase over time of the share of non-family company handovers (see Who takes over? Desire and reality). A frequent reason for non-family takeovers that comes as little surprise in the context of the aforementioned multi-option society is the lack of interest in a takeover among the children.16 Although these changes in the economy and society could lead to a further (slow) decline in the share of family firms in the years to come, family firms will continue to shape the image of the Swiss SME landscape. Fundamentally, the family firm business model – the focus on the long term, strong emphasis on quality, employee-friendly corporate culture and the importance of sustainable business management – has not lost any of its appeal since the last survey. Fur-thermore, family members still remain the most popular business partners when founding a com-pany. There is a high level of trust between family members as they have known each other for a long time.

14 See Credit Suisse (2016): Sector Handbook 2016 – Reverberations of the Swiss Franc Shock. 15 For a more detailed discussion, see Frey, Halter, Zellweger (2004): Bedeutung und Struktur von Familienunternehmen in der Schweiz. 16 See Credit Suisse (2013): Success Factors for Swiss SMEs – Company Succession in Practice; also Zellweger, Sieger & Englisch (2015): Coming Home or Breaking Free? A Closer Look at the Succession Intentions of Next Generation Family Business Members. Ernst & Young.

Is the share of family firms really falling?

Likelihood that a company is a family firm increases with its age

Future growth sectors more strongly shaped by non-family firms

More opportunities today of founding a company outside the family than previously

Family firms will continue to account for the majority of Swiss SMEs for a long time to come

16Swiss Issues Industries I June 2016

Economic Research

Family firms – Governance structures at SMEs

Families are omnipresent at SMEs Figure 14: Influence of the family at SMEs Distribution of family share; 100% = completely family owned and/or all members

come from the family; 0% = no family ownership/members

As illustrated in the previous section, most SMEs are familyfirms. The family influence at SMEs is therefore very strong.This is particularly noticeable with regard to the companyshares that at around three quarters of all SMEs are complete-ly family owned. However, the executive board is only com-prised exclusively of family members in 55% of cases. Theshare of family members on the board of directors is somewhatlower. This is completely made up of family members in 48%of cases. Families thus primarily control the company via own-ership participation, while the share of non-family members ofthe executive board and board of directors is comparativelyhigh.

Source: 2016 Credit Suisse Succession Survey

Ownership, management and board of directors are intertwined

Figure 15: Intertwining between ownership, executive board and board of directors

Average shares

The boundaries between ownership, executive board and boardof directors at SMEs are fluid. On average, 80% of all ownerssimultaneously also sit on the executive board, while membersof the executive board hold an average of 77% of the compa-ny's shares. The board of directors is also not just limited to itsfunction as a supervisory body. An average 65% of the mem-bers of the board of directors are also operationally activewithin the company. Altogether there is therefore no clearseparation between ownership, management and board ofdirectors. Instead, the same persons often execute multiplefunctions.

Source: 2016 Credit Suisse Succession Survey

Spouses and parent-child relationships dominate Figure 16: Family relationships among owners and on the executive board

Share of responses; multiple responses possible

Similar family relationships prevail overall on the executiveboard and among owners, although comparatively more familyrelationships are found among owners. However, spouses andparent-child relationships dominate in both functions. Thegroup of owners comprises parents and their children in 43%and spouses in 42% of cases. By contrast, spouses are en-countered more frequently than parent-child relationships onthe executive board. Siblings are represented in 30% of casesamong the owners and on the executive board at 23% of allSMEs. Members of the extended family such as uncles, auntsand cousins are involved comparatively rarely.

Source: 2016 Credit Suisse Succession Survey

48%

55%

75%

22%

16%

14%

13%

15%

17%

13%

0% 20% 40% 60% 80% 100%

Share of family members on board ofdirectors

Share of family members on executiveboard

Share of family in ownership

100% 50%-99% 1%-49% 0%

5% 6%

65%

77%

80%

0% 20% 40% 60% 80% 100%

Share of operationally active board ofdirector members

Company shares held by executive board

Share of owners active on the executiveboard

36%42%

32%

43%

23%

30%

8% 10%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Executive board Owners

Spouses Parent(s) with child Siblings Extended family

17Swiss Issues Industries I June 2016

Economic Research

Family firms – Governance structures at SMEs

Chief executives mainly come from the owner family Figure 17: Chief executives at SMEs Share of yes/no responses

Families are not only proportionately well represented on theexecutive board at SMEs. The position of chief executive isalso occupied by a member of the owner family at most SMEs.Sixty-five percent of SMEs claim to have a chief executive fromthe owner family. It is also striking to observe that chief execu-tives of SMEs simultaneously occupy the position of chair of the board of directors in 64% of cases. This result likewisemakes clear that it is comparatively rare for the functions of theboard of directors and operational management to be clearlyseparated at SMEs despite the fact that such separation is tobe recommended for good corporate management in order toguarantee that the functions are exercised independently.

Source: 2016 Credit Suisse Succession Survey

Minor differences in the share of women between the different functions

Figure 18: Share of women in different functions at SMEs

Average share of women in the respective functions

Women on average make up a share of 23% each among theowners and on the executive board. They are slightly less wellrepresented on the board of directors with a share of 22%.Altogether the three functions therefore barely differ from eachother in terms of the share of women. By contrast, the shareof women among the chief executives of the companies sur-veyed is comparatively low, with only 10% of all chief execu-tives at SMEs women. However, as we illustrate in the sectionentitled Company succession and the babyboomer generation, this share is slowly but steadily rising.

Source: 2016 Credit Suisse Succession Survey

Better management prospects for women from the family Figure 19: Share of women on SME executive boards Shares in percent; multiple responses possible

The executive board on average comprises 77% men and23% women. A glance at the composition of this 23% showsthat the vast majority of women active on the executive boardcome from the owner family. Only 20% of the female mem-bers of the executive board are non-family persons. Womenfrom the owner family thus appear to have significantly betterprospects for management positions than those from outsidethe family. This result simultaneously suggests that womenfrom outside the family face greater obstacles in terms ofgaining a foothold in the management.

Source: 2016 Credit Suisse Succession Survey

64%

65%

36%

35%

0% 20% 40% 60% 80% 100%

Is chief executive also chair of board ofdirectors?

Is chief executivea family member?

Yes No

10%

22%

23%

23%

0% 5% 10% 15% 20% 25%

Chief executive

Board of directors

Executive board

Owner

77% 80% 20%23%

Share of men on executive boardShare of women on executive boardFrom familyOutside family

18Swiss Issues Industries I June 2016

Economic Research

Type of succession – Overview

Who takes over? Desire and reality Internal family succession is just one of several possibilities. More than half of compa-nies are handed over to non-family members and a third to persons who belong to neither the family nor the company. All succession planning starts with the question of who should one day take over the company. We generally distinguish between internal family succession (family buyout or FBO for short), handover to (senior) employees (management buyout, MBO), handover to external persons (management buy-in, MBI) and sale to another company or to a private equity company. As in 2013, our survey this year illustrates how often these types of succession occur in practice. We examine both the handover intentions and plans of today's chief executives and the actual fre-quency of the individual types of succession. The focus is placed on both management and ownership transfer. A relative majority of 41% of SME entrepreneurs plans or wishes to handover ownership of the company to family members. Twenty-five percent are planning a management buyout, 17% a management buy-in and 21% a sale to another company (see Figure 20, left). These figures add up to more than 100% as various survey participants are pursuing a mixture of these types of handover or considering multiple options. For example, around 8% wish to transfer ownership both within and outside the family. Altogether, 33% are pursuing an exclusively internal family and 34% an exclusively non-family solution. All types of succession were cited more frequently compared with our 2013 survey (see Fig-ure 20, left). This is primarily attributable to an increase in the number of multiple answers. Alto-gether, non-family succession plans have tended to gain significance slightly. There was a mar-ginal decrease in exclusively family handover plans (-0.4 percentage points). By contrast, exclu-sively non-family plans rose slightly (+1.1 percentage points). Mixed handover plans (both family and non-family) increased by 1.7 percentage points. Forty-two percent of all SMEs surveyed are accordingly considering non-family succession solutions – compared with 39% in 2013. This (slight) increase in the share of non-family transfers is likely to be closely linked to the decline in the share of family firms and its causes (see Share of family firms falling).

Who do entrepreneurs hand over their SMEs to?

Internal family and external handover plans more or less balance each other

Non-family succession solu-tions have gained signifi-cance somewhat

Figure 20: Ownership and management handover plans Figure 21: Planned vs. realized succession Share of responses; sum of all types of transfer can add up to more than 100% due to multiple answers

Share of responses; sum of all types of transfer can add up to more than 100% due to multiple answers

Source: 2013 and 2016 Credit Suisse Succession Surveys Source: 2016 Credit Suisse Succession Survey

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Ownership 2013 Ownership 2016 Management 2013 Management 2016

FBO MBO MBI Sale

n.a.

n.a.

41%

25%

17% 21

%

23%

46%

25% 30

%

0%

10%

20%

30%

40%

50%

FBO MBO MBI Sale Not known

Handover plans Reality

n.a.

n.a.

19Swiss Issues Industries I June 2016

Economic Research

A similar trend can also be observed with regard to the transfer of management of the compa-ny (see Figure 20, right). Exclusively family succession solutions marginally lose importance (from 30% to 29%), while exclusively non-family solutions (i.e. MBO, MBI and sale) are being pursued somewhat more frequently than in 2013 (38% vs. 35%).17 However, what has not changed since 2013 is the fact that SMEs wish to keep ownership within the family somewhat more frequently than management. Conversely, (senior) employees are envisaged more fre-quently for taking over management than ownership (see Figure 20, comparison of left with right). Despite these differences, ownership and management are often intended for transfer to the same person or persons at least in the case of an FBO or MBO. If a family handover of owner-ship is planned, management – if already known – is also intended for transfer to family mem-bers in 89% of cases. If in the event of a family handover of ownership no family members are envisaged for management, SMEs in many cases prefer existing employees to any external successors. If ownership is to be handed over to employees, the latter are also envisaged for management in 93% of cases. However, if the company is to be sold to persons outside the company or to other companies, there are plans in more than half of cases for existing employ-ees or family members also to be included in the management. These results do not reflect the succession solutions actually realized but the desires and plans of the current chief executives. However, the actual implementation of succession plan-ning often differs from these. Of the takeovers actually carried out in the last 20 years or so, 46% took place within the family (FBO). Employees took over the company in 25% of cases (MBO) and persons outside both family and company in 30% of cases (MBI). It was almost always the children who took over in the case of family handovers. In 50% of cases resulting in an MBI, the selling generation had previously had a friendly or business relationship with the buyer of the company. This did not apply to the other half of such cases. These are the so-called 'classical' MBI cases where buyer and seller come into contact via an advertisement or broker. In Figure 21 we compare the current handover plans with the successions actually realized. The comparison is only approximate as the options "not known" and "sale" (to other company) are also possible in the planning phase but not available for the succession cases actually realized.18 Nevertheless, Figure 21 clearly suggests that above all MBIs take place more frequently than planned in reality – a fact that we also observed back in 2013. A disproportionately large number of entrepreneurs who for a long time have no specific idea about who to hand over their busi-ness to will ultimately transfer it to an external person for lack of alternatives.

Desire and reality: findings and recommendations for practice

Always think and act in scenarios. There is no guarantee that the envisaged succession candidate will then actually take over the company.

The different types of succession FBO, MBO, MBI and sale to company entail different succession processes (in terms of duration, parties involved and purchase price). Take account of these aspects in your succession planning.

Openness and honesty in the evaluation of succession candidates (particularly in the case of FBO/MBO) are necessary for the sake of the company. It is essential to scruti-nize the ability and motivation of the candidates – even if you would prefer to put this off within the family due to family relationships.

Discuss with the parties involved whether ownership and management succession should be linked.

17 The differences between the 2013 and 2016 surveys are marginal for transfer of both management and ownership. It is therefore not possible to rule out that the changes are partially attributable to differences in the sample. 18 For a direct comparison of the percentages to be meaningful, the shares of the "not known" and "sale" options must be subtracted out so that the responses to the options FBO, MBO and MBI also add up to 100% for the question concerning the handover plans. Calculated in this way, the FBO share comes to 49%, the MBO share 30% and the MBI share 21%. This would mean that the FBO and MBO shares are lower in reality than in the succession plans, while the MBI share remains higher.

Handover of ownership more frequently within the family than transfer of man-agement

Ownership and manage-ment often intended for the same recipient(s)

More than half of compa-nies taken over outside the family

MBIs occur more frequently than planned in reality

20Swiss Issues Industries I June 2016

Economic Research

Type of succession – Family influence

Family influence determines type of succession The influence of the family has a decisive impact on the choice of type of succession, with the family relationships among the owners also playing a significant role. In keeping with the important role played by families at SMEs, succession planning for the ma-jority of companies is also a significant aspect and an important step as part of the generation change within the family. In the preceding section we show which of the four types of succes-sion (FBO, MBO, MBI and sale to another company) SMEs desire as a whole and put into prac-tice in reality. We now examine the hypothesis that SMEs make different decisions about the type of succession depending on the influence of the family. The question in particular also arises as to whether and to what extent different family relationships among the owners exert an impact on the planned choice of succession type. According to our survey, different family rela-tionships do indeed play an important role for succession planning. For instance, the intention to keep the company within the family is at its greatest if the owners include parents with their child (see Figure 22). Sibling relationships among the owners also strengthen the resolve to secure the family's future control.

Interestingly, the intention of keeping the company within the family is significantly lower among spouses in the group of owners than among siblings and where parents with their child are in-volved in the company, i.e. the younger and older generations are involved. The existence of descendants who are already involved in the ownership thus appears to be an important factor for company succession. It also suggests a certain readiness among the younger generation to keep the company within the family. By contrast, the involvement in the company of the extend-ed family is reflected by a comparatively weak intention to keep ownership of the company within the family in the long term. A similar picture emerges from an examination of the preferred types of succession (see Fig-ure 23). For those companies only including spouses but no other family relationships among their owners, an FBO, that is, handover to another family member, is only considered in 51% of cases. This share is significantly higher at 68% and 65% respectively in the case of sibling and parent-child relationships. Regardless of the nature of the family relationships, the family firms

Family relationships influence the desire to keep the com-pany within the family

Figure 22: Effect of family relationships on the intention to keep the company within the family

Figure 23: Effect of family relationships among owners on the planned choice of succession type

Average of responses depending on the family relationships at hand (among the owners) on a scale from 1 to 7; 1 = very weak intention, 7 = very strong intention; sample only comprises family firms

Frequency of planned types of succession (for ownership) depending on the family relationships at hand; sample only comprises family firms

Source: 2016 Credit Suisse Succession Survey Source: 2016 Credit Suisse Succession Survey

Intention of preserving family ownership comparatively low among spouses

Spouses sell company to third parties comparatively fre-quently

4.5

5.3

5.1

4.5

1.00 2.00 3.00 4.00 5.00 6.00

Extended family

Parent(s) with child

Siblings

Spouses

61%

65%

68%

51%

12%

12%

14%

17%

12%

8%

6%

13%

15%

15%

12%

19%

0% 20% 40% 60% 80% 100%

Extended family

Parent(s) with child

Siblings

Spouses

FBO MBO MBI Sale

21Swiss Issues Industries I June 2016

Economic Research

surveyed in most cases favor an FBO as their planned succession solution. However, alongside FBOs many owners also consider selling to another company, with the share of this alternative highest in the case of spouses under the owners at 19%. The importance of the family influence on the transfer of ownership becomes particularly clear when we expand our field of vision to include non-family firms. SMEs without family members among the owners envisage an MBO for the future transfer of ownership in 53% of cases (see Figure 24, left). This share amounts to just 31% if the group of owners partially comprises family members and a mere 16% if all owners are members of the family. Conversely, in the event of full family ownership the owners prefer an FBO in 52% of cases. The owners thus tend to opt more for an FBO rather than an MBO as the family influence within the group of owners in-creases. Remarkably, the share of those SMEs planning a sale to another company or an MBI only changes little as the family influence rises. With a share of 12% to 16%, the MBI option assumes the least significance throughout. A similar situation holds for the family influence on the executive board. If the executive board is comprised exclusively of family members, the owners largely prefer an FBO as the planned succession solution (see Figure 24, right). However, an MBO is the most frequently considered option for SMEs managed by an entirely non-family executive board.

Figure 24: Effect of family influence on the planned choice of succession type Type of succession (for ownership) depending on the share of family members among the owners/on the executive board

Source: 2016 Credit Suisse Succession Survey

8%17%

53%48%

16% 13%

23% 22%

38%45%

31% 21%

12% 12%

19% 22%

52% 52%

16% 16%

14% 14%

19% 17%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

No familymembers

Family membersand externals

Family membersonly

No familymembers

Family membersand externals

Family membersonly

Owners Executive board

FBO MBO MBI Sale

MBOs particularly popular at non-family firms

Family influence on the ex-ecutive board also exerts an impact on succession plan-ning

Type of succession and family influence: findings and recommendations for practice For company succession the acquirers need to be prepared for their tasks and the

handover of the tasks and responsibility needs to be carefully planned. You should therefore plan enough time for the handover.

Make sure that you include all parties involved in the process. This is particularly im-portant if you are planning an FBO. Bear in mind that the various family members have different roles and interests and that you should take these into account.

Many family firms wish to hand over the company to the next generation. However, it must be ensured that younger members of the family wishing to take over the company also possess the necessary skills to manage the company successfully.

Keep a "plan B" to hand. There is no guarantee that the preferred option will actually work.

22Swiss Issues Industries I June 2016

Economic Research

Distribution principles

Ownership and management: who receives what? The majority of SMEs intend to hand over ownership to all younger members in equal shares. However, when handing over management, SMEs would focus on the most capable family members from an entrepreneurial perspective. The question regularly arises in the case of family successions as to which younger members of the family management and ownership should be handed over to. A range of distribution princi-ples can be crucial for this decision (see example in box). If the focus is on equal treatment, a handover of the company in equal shares and thus equal distribution among all descendants makes sense. However, as well as this principle of equality, owners can also focus on the per-formance principle and place the company in the hands of the most capable candidate from an entrepreneurial perspective. Finally, another possible handover principle is that to the oldest son or daughter (principle of primogeniture, see box on page 23). According to our survey, different distribution principles are decisive for ownership on the one hand and transfer of management on the other. While 81% of all SMEs surveyed would hand over management to the most capa-ble younger member of the family from an entrepreneurial perspective, the principle of equality clearly dominates at 65% with regard to the handover of ownership (see Figure 25).19 Owners of SMEs thus consider it particularly important to place operational management in the hands of the most capable family member from an entrepreneurial perspective in accordance with the perfor-mance principle. By contrast, the descendants' entrepreneurial capabilities play a considerably more minor role in the handover of ownership.

Example: The Gasser family has a chemicals company. All three children work in the busi-ness. Nadine is chief executive, Martin works in research and Lisa is in the marketing de-partment. The Gassers' mother wishes to transfer the majority of the family firm's ownership to Nadine. But how do Martin and Lisa respond to this financial disadvantage? Do conflicts arise within the family or in the company? What is a fair form of succession, distribution of ownership by equality or performance?

19 It should be noted that the question posed here to the chief executives of the SMEs was of an entirely fictitious nature for which FBO was predefined as the type of succession. The precise wording of the question was as follows: "Assuming you handover your company to your descendants, how would you hand over management and ownership?"

Different principles for the handover of ownership and management

Figure 25: How would SMEs distribute ownership and management among the descendants?

Figure 26: Correlation between family participation in ownership and preferred distribution principle

Distribution of responses Distribution of responses by share of family in ownership of the company; sample comprises family firms only

Source: 2016 Credit Suisse Succession Survey Source: 2016 Credit Suisse Succession Survey

17%

65%

81%

33%

0% 20% 40% 60% 80% 100%

Management

Ownership

To all in equal shares To the most capable To the oldest

3%

15%

61%

82%

36%

3%

3%

14%

63%

83%

34%

3%

3%

32%

67%

68%

33%

0% 20% 40% 60% 80% 100%

100%

50%-99%

1%-49%

100%

50%-99%

1%-49%

Man

agem

ent h

ando

ver

Ow

ners

hip

hand

over

To all in equal shares To the most capable To the oldest

23Swiss Issues Industries I June 2016

Economic Research