Embed Size (px)

Citation preview

July – September 2017

2 © Experian Public

OverviewSnapshot of Experian

• Total Revenue: US$4.3bn• Benchmark EBIT: US$1.2bn • Market Cap*: c.£16bn• In top 50 of FTSE-100• Employees: c.16,000• Offices in 37 countries• Largest markets: US, Brazil, UK• Corporate headquarters: Dublin

For the year ending 31 March 2017* At 14 July 2017

Experian is the world’s leading global information services company. Our roots lie in assessing credit risk; today we do much more.

3 © Experian Public

Market leading global information company• Unique proprietary data, coupled with

analytics and software• Scalable business model

Strong market positions• No. 1 or 2 position across our largest markets• High barriers to entry

Significant growth potential• By bringing our assets together to access new

market opportunities

Strong financial track record• High quality, recurring revenues• Highly cash generative with low capital intensity

OverviewThe Experian investment case

4 © Experian Public

OverviewExperian business activities

Decision Analytics

• Helping clients to:• Lend effectively• Minimise the risk

of fraud• Using advanced

software and analytics, and expert consulting

CreditServices

• Large databases of information, used to manage risk

• 17 consumer credit bureaux

• 11 business credit bureaux

• Automotive information

• Health

Marketing Services

• Data quality and management

• Targeting relevant offers to individuals

Consumer Services

• Direct to consumer credit monitoring

• Credit matching services / lead generation

• Identity theft protection services

• Affinity (white label) credit and identity monitoring services

55% 13% 10% 22%% split of revenue shown for the year ending 31 March 2017.

By customer segment

OverviewGlobal revenue FY17

Diverse portfolio by region, business activity and customer segment

Credit Services

Decision Analytics

Marketing Services

55%

13%

10%By business activity

22%

EMEA/Asia Pacific

UK and Ireland

North America

Latin America

8%

19%

56%

17%

Consumer Services

By region

33%

Financial services

Direct to consumer

Healthcare

Retail

Automotive

Telco and utilities

Insurance

Media technology

Public sector/education

Other

19%17%

7%

5%

5%

5%4%

3%2%

33%

56% 77%

88%* 83%

92%64%*

44%

23%

12% 17%

8%36%

4,3351

3,1452

1,7662 1,7042

88018813

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Experian Equifax TransUnion D&B FICO Acxiom

North America Other regions

OverviewMarket leader with unparalleled global reach and range

1 Year ended 31 March 20172 Year ended 31 December 2016This analysis covers traditional competitors that are publicly listed. It does not include companies where a single division competes against Experian.

*US only. Source: Latest full year revenue, company SEC filings

3 Year ended 30 September 2016

Glo

bal r

even

ue U

S$m

7 © Experian Public

Strategic overview

8 © Experian Public

Strategic overviewIn 2014, we set a clear plan of action

8

• Simplified our portfolio• Growth has returned to our target range• Considerably improved performance in Brazil and Marketing Services• Executing on a strategic repositioning of our relationship with consumers• Driven substantial efficiencies from our business, and used the funds to invest• Innovation is accelerating• Rigorous approach to capital allocation

FocusGrowth

Improve performance Efficiency

Capital optimisation

9 © Experian Public

Strategic overviewWe have enhanced our foundations to drive better performance at lower cost

9

Superior technology

Operating excellence across core functions

Open systemsCloud computing

API HubAgile development

Transformed call centres

Introduced new standards for customer service

Investment in our people

Greater speed, accuracy and flexibility

Improved time to market with new products

Enhancing client access to our data

Enhanced consumer experience

Higher client and employee retention

Unmatched global footprint

and offering

Scaling our technology platforms across markets

10 © Experian Public

Strategic overviewDefining the path ahead: our growth objectives

Broaden and deepen our data assets

Extend our lead in analytics and software solutions

Transform engagement with consumers

Accelerate pace of innovation

Exploit the breadth of our capabilities

Scale in targeted verticals and geographies

11 © Experian Public

Strategic overview Building engagement with consumers in North America

11

LendingWorks

• 9m free members, growing 0.5m per month; accelerate through free FICO offer

• Shifting further to new revenue models during FY18

• LendingWorks: • Over 200 card and personal loan

products and growing• Serves up the best offer for

consumers• Prescreens using lenders’ exact

credit criteria

www.experian.com

12 © Experian Public

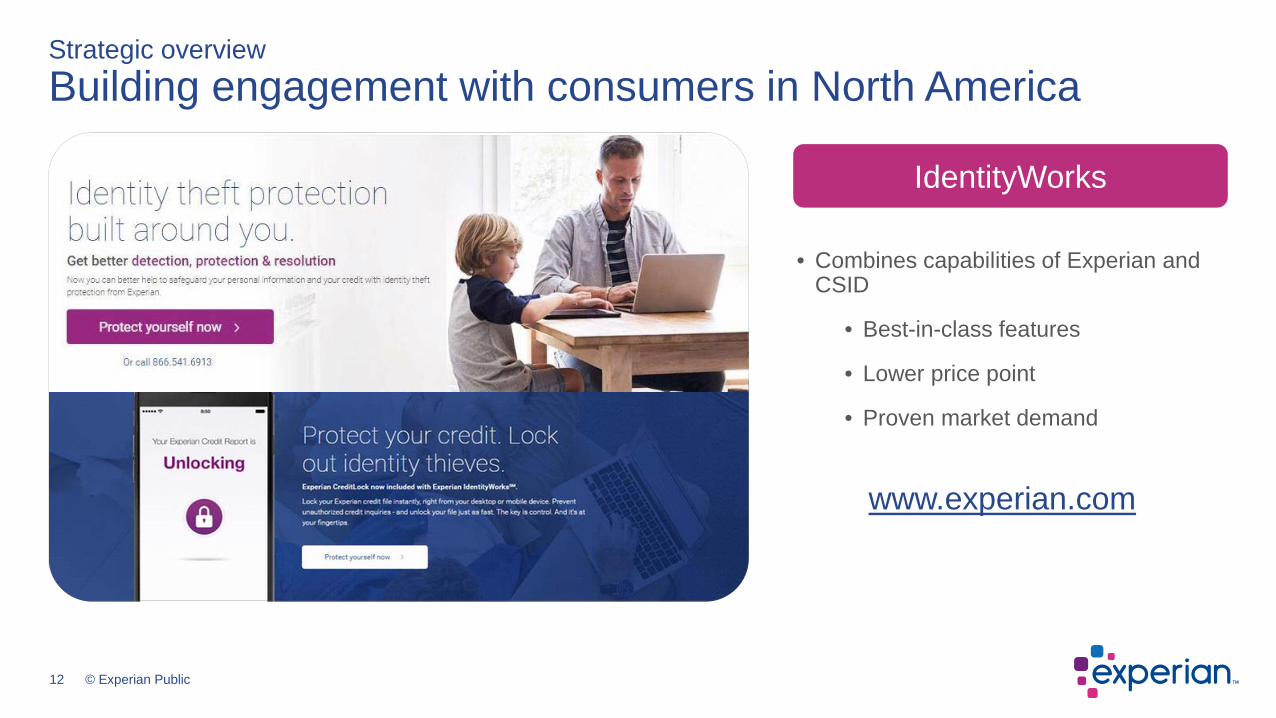

Strategic overviewBuilding engagement with consumers in North America

12

IdentityWorks

• Combines capabilities of Experian and CSID

• Best-in-class features

• Lower price point

• Proven market demand

www.experian.com

13 © Experian Public

Strategic overviewDelivering innovation to meet growing new customer needs

Data• Data ingestion engine• Alternative sources of data, including positive data• Targeted digital advertising• Pandora

Platforms• CrossCore• PowerCurve Collections

Analytics• North America Credit Services DaaS• Decision Analytics SaaS

Services • SerasaConnecta• Digital Credit Marketing• Universal Master Patient Index (UMPI)• Text To Credit

• Deliver fast, efficient services in the digital ecosphere

• Undertake checks in real time to ensure a smooth customer experience while managing risks

• Counter risks from fraud while authenticating people quickly

• Make sense of data across their whole organisation, to get a single view of their customer

• Know why a customer has missed a loan payment or is late paying a bill and deliver a better collections experience

Experian innovationB2B customer needs

14 © Experian Public

Strategic overviewCase study: digital credit marketing update

14

15 © Experian Public

Current process Text for credit option

Strategic overviewCase study: Text for Credit

16 © Experian Public

Strategy management

Originations

Customer management

CollectionsPowerCurve®

Over 200 installed clients

Strategic overviewPowerCurve: better decisions, faster

17 © Experian Public

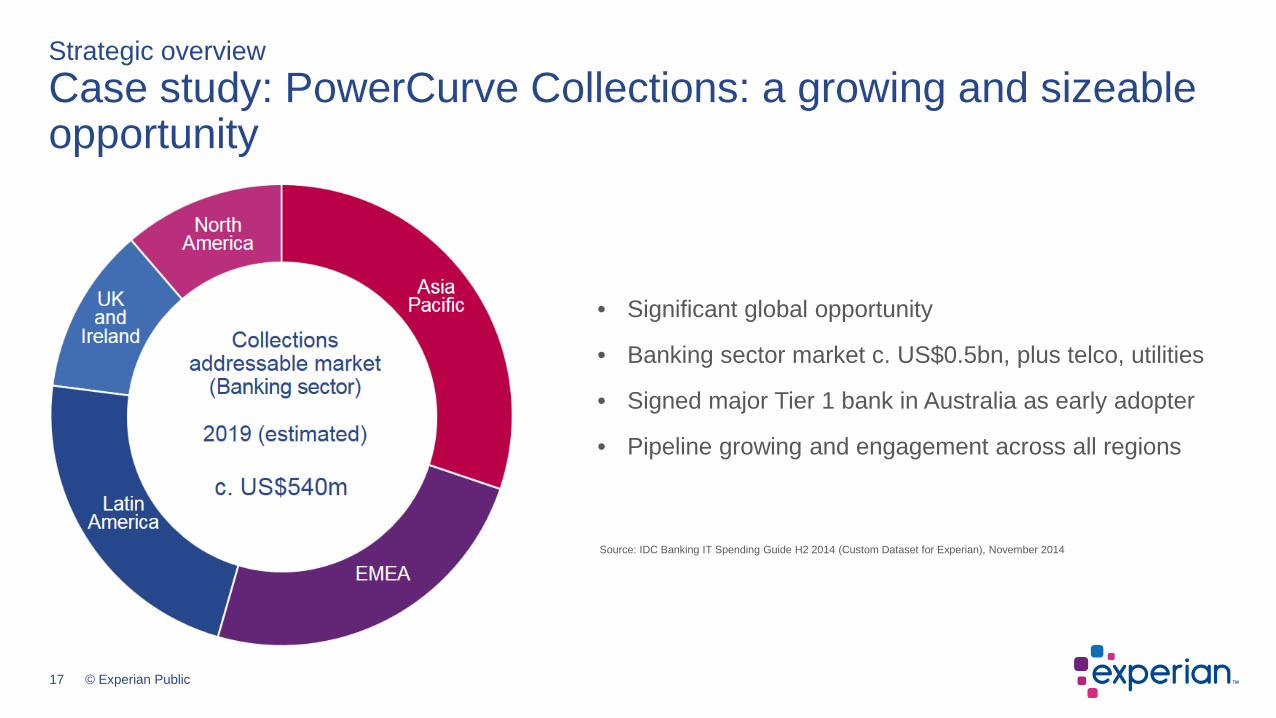

Strategic overviewCase study: PowerCurve Collections: a growing and sizeable opportunity

17

Source: IDC Banking IT Spending Guide H2 2014 (Custom Dataset for Experian), November 2014

• Significant global opportunity

• Banking sector market c. US$0.5bn, plus telco, utilities

• Signed major Tier 1 bank in Australia as early adopter

• Pipeline growing and engagement across all regions

18 © Experian Public

Strategic overviewLatin America

Small Moderate LargeCore

Positioned to capture the structural potential

BusinessInformation

D&B

DecisionAnalytics

EXPN

MarketingServices

EXPN

ConsumerDirect

Healthcare

EXPN

Automotive

Fraud & ID

EXPN

Others

Insurance

EXPN

LexisNexis

Affinity

EXPN

Core Consumer Information

EXPN

EXPN

EXPN

CoreBusiness

InformationEXPN

DecisionAnalytics

EXPN

MarketingServices

EXPN

ConsumerDirect

EXPN

Insurance

EXPN

Fraud & ID

EXPN

Affinity

EXPN

BusinessInformation

Core Consumer Information

EXPN

EXPN

United StatesBrazil

19 © Experian Public

Capital strategyOur medium-term financial framework

Organic business

Mid single-digit organic growth

Operating cash flow application

Strong growth in Benchmark earnings per share

• Structural growth

• Strong cash generation

• Strong core and portfolio optionality

Organic investment Portfolio Shareholder

returns

Optimised capital allocation

20 © Experian Public

Recent performance

21 © Experian Public

Recent performanceSummary of portfolio performance

Horizontal axis indicates share of revenue excluding CSIdentity and vertical axis indicates organic revenue growth.

UK&I Consumer Services

(9)%

EMEA/APACCredit Services

(3%)

North America Consumer Services

(2%) UK&ICredit

Services

3%

Latin America Credit Services

6%

Global Marketing Services

8%

North AmericaCredit Services

8%

Global Decision Analytics

9%

Two thirds of the portfolio growing in mid-high single digit for FY17 FY17: 5% organic growth

Q1 FY18Total revenue growthOrganic revenue growth 4%

6%

22 © Experian Public

Recent performanceRevenue walkthrough

FY16 revenue

including CCM

FY17 reported revenue

North America

ForeignExchange

4,477

UK and Ireland

EMEA/APAC

CCM

FY17 revenue before

FX

FY16 restated revenue

Latin America

(313)

+5% +9% +1% +9%

4,164

4,335

Acquisitions

+5% Group organic revenue growth+6% total revenue growth

+4%1 total revenue growth

1 At actual FX rates

23 © Experian Public

Recent performanceCapital framework

1 Share repurchases as at 31 March 2017.2 Funds from Operations is defined as Benchmark free cash flow plus organic capital investment (capital expenditure).

0

200

400

600

800

1,000

1,200

1,400

1,600

Cashgenerated

Uses ofcash

Capital summary

Organic capital investment

Share repurchaseprogramme

Dividends

Acquisitions and minority investments

Funds from Operations2

Increase in net debt

Other

Capital allocation

• Organic innovation investment

• Signed agreement for the sale of CCM

• FY17 shareholder returns:• Dividend growth of 4%• US$353m1 net share repurchases completed

during the year

• Expect to make US$600m of share repurchases in FY18.

24 © Experian Public

SummaryInvesting in the growth of the future

24

Investing for a better and stronger business, well positioned for future growth

25 © Experian Public

Appendix

26 © Experian Public

AppendixModelling considerations for FY18

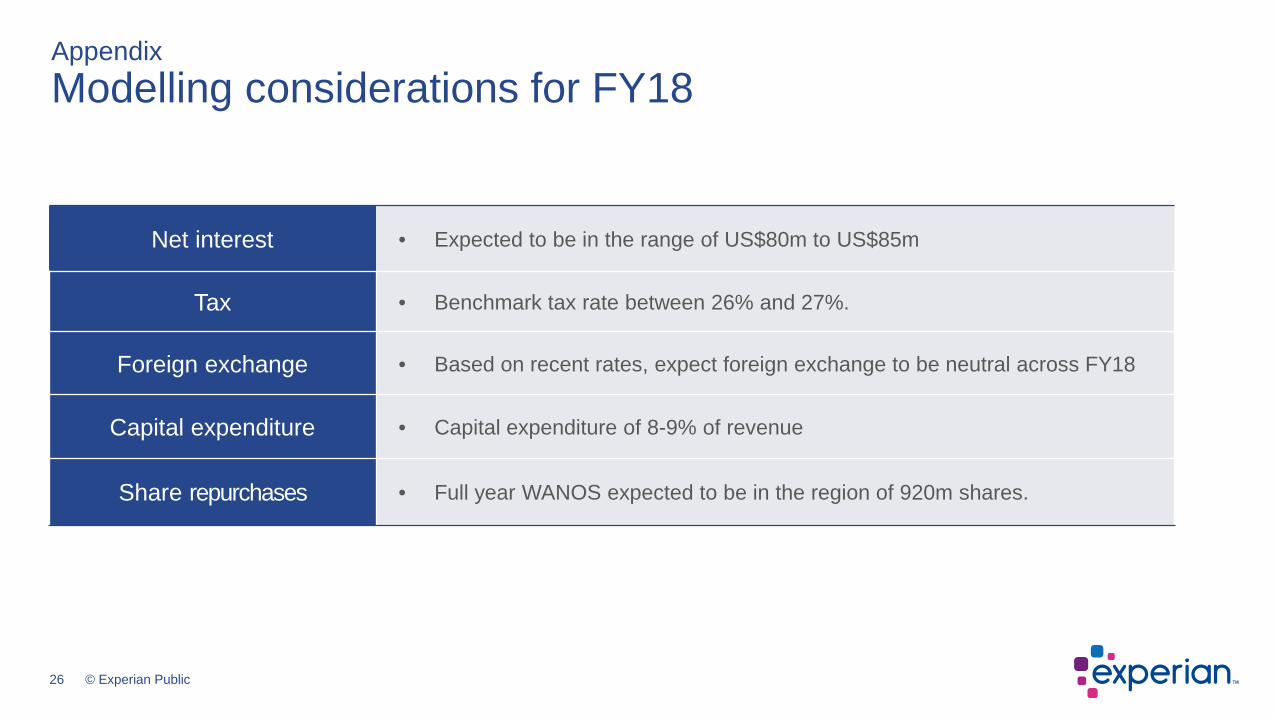

Net interest • Expected to be in the range of US$80m to US$85m

Tax • Benchmark tax rate between 26% and 27%.

Foreign exchange • Based on recent rates, expect foreign exchange to be neutral across FY18

Capital expenditure • Capital expenditure of 8-9% of revenue

Share repurchases • Full year WANOS expected to be in the region of 920m shares.

27 © Experian Public

AppendixRecent trends

Organic revenue growths for all prior periods are as reported and have not been restated for subsequent divestmentsB2B defined as Credit Services, Decision Analytics and Marketing Services

Organic revenue growth continues to be in our target mid-single digit organic revenue growth range…

7%

6%

5%

4%

3%

2%

1%

0%

8%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

FY15 FY16 FY17 FY18Q1

7%

6%

5%

4%

3%

2%

1%

0%

8%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

FY15 FY16 FY17Q4

FY18Q1

…with high single-digit B2B growth

28 © Experian Public

AppendixImpact of discontinued operations

Revenue (US$m)

Total revenue growth1 (%)

Organic revenue growth1 (%)

EBIT margin (%)

Continuing EBIT (US$m)

Year ended 31 March

Benchmark EPS (US cents)

308

54

CCM

4.0

Margin change vs FY161

4,335

6

5

27.7

1,199

2017 as reported

88.4

+30 bps

4,643

6

4

27.0

1,253

2017 includingCCM

92.4

1 Shown at constant currency

29 © Experian Public

AppendixBenchmark EBIT margin walkthrough

EBIT margins calculated on an ongoing activities basis.

FY16 Benchmark EBIT margin

including CCM

FY17 reported Benchmark EBIT margin

FY16 CCM restatement

ForeignExchange

26.7%

27.7%

0.2%

0.4%

FY17 Benchmark EBIT margin

before FX

27.1%

0.7%Latin

AmericaUK and Ireland

EMEA/APAC

(0.3)%

27.4%

FY16 restated Benchmark EBIT margin

North America

0.3%(0.3)%

30 © Experian Public

Revenue 2017 2016 Total growth

Organic growth

BenchmarkEBIT

margin

Q1 FY18 Organic growth

Credit Services 2,389 2,240 6% 6% 34.2% 5%

Decision Analytics 584 566 9% 9% 20.5% 13%

Marketing Services 421 407 8% 8% 22.6% 12%

Consumer Services 941 951 2% (4)% 25.8% (8)%

Total revenue – ongoing activities 4,335 4,164 6% 5% 4%

Benchmark EBIT – ongoing activities 1,199 1,130 7%

Benchmark EBIT margin 27.7% 27.1%

Twelve months ended 31 MarchUS$million

All results are Benchmark figures and are on an ongoing activities basis. Growth at constant exchange rates. The 2016 results have been restated to reflect the email/cross-channel marketing business ('CCM') reclassification as a discontinued operation.

AppendixRevenue and Benchmark EBIT by business activity

31 © Experian Public

Revenue 2017 2016Total

growth %

Organic growth

%

Benchmark EBIT

margin

Q1 FY18Organic

growth %

North America 2,457 2,294 7 5 31.8% 4%

Latin America 730 631 9 9 34.4% 8%

UK and Ireland 807 924 1 1 30.5% (3)%

EMEA/Asia Pacific 341 315 9 9 (0.9)% 7%

Total revenue – ongoing activities 4,335 4,164 6 5 4%

Benchmark EBIT – ongoing activities 1,199 1,130 7

Benchmark EBIT margin 27.7% 27.1%

Twelve months ended 31 MarchUS$million

AppendixRevenue and Benchmark EBIT by region

All results are Benchmark figures and are on an ongoing activities basis. Growth at constant exchange rates. The 2016 results have been restated to reflect the email/cross-channel marketing business ('CCM') reclassification as a discontinued operation.

32 © Experian Public

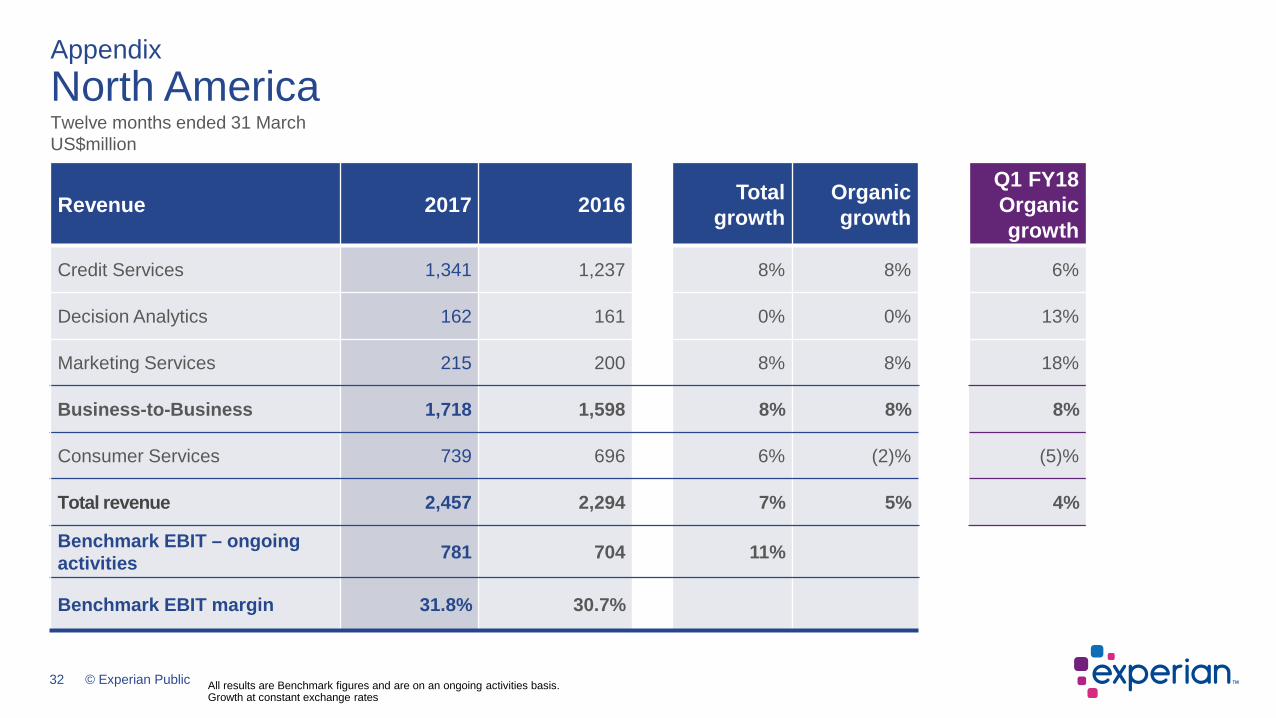

Revenue 2017 2016 Total growth

Organic growth

Q1 FY18Organic growth

Credit Services 1,341 1,237 8% 8% 6%

Decision Analytics 162 161 0% 0% 13%

Marketing Services 215 200 8% 8% 18%

Business-to-Business 1,718 1,598 8% 8% 8%

Consumer Services 739 696 6% (2)% (5)%

Total revenue 2,457 2,294 7% 5% 4%

Benchmark EBIT – ongoing activities 781 704 11%

Benchmark EBIT margin 31.8% 30.7%

Twelve months ended 31 MarchUS$million

AppendixNorth America

All results are Benchmark figures and are on an ongoing activities basis.Growth at constant exchange rates

33 © Experian Public

Revenue 2017 2016 Total growth

Organic growth

Q1 FY18Organic growth

Credit Services 658 579 6% 6% 5%

Decision Analytics 48 36 34% 34% 44%

Marketing Services 24 16 39% 39% 44%

Total revenue 730 631 9% 9% 8%

Benchmark EBIT – ongoing activities 251 226 3%

Benchmark EBIT margin 34.4% 35.8%

AppendixLatin AmericaTwelve months ended 31 MarchUS$million

All results are Benchmark figures and are on an ongoing activities basis.Growth at constant exchange rates

34 © Experian Public

Revenue 2017 2016 Total growth

Organic growth

Q1 FY18Organic growth

Credit Services 246 275 3% 3% 3%

Decision Analytics 214 234 5% 5% 7%

Marketing Services 145 160 5% 5% 0%

Business-to-Business 605 669 4% 4% 4%

Consumer Services 202 255 (9)% (9)% (19)%

Total revenue 807 924 1% 1% (3)%

Benchmark EBIT – ongoing activities 246 297 (4)%

Benchmark EBIT margin 30.5% 32.1%

AppendixUK and IrelandTwelve months ended 31 MarchUS$million

All results are Benchmark figures and are on an ongoing activities basis.Growth at constant exchange rates

35 © Experian Public

Revenue 2017 2016 Total growth

Organic growth

Q1 FY18Organic growth

Credit Services 144 149 (3)% (3)% 0%

Decision Analytics 160 135 21% 21% 13%

Marketing Services 37 31 16% 16% 13%

Total revenue 341 315 9% 9% 7%

Benchmark EBIT – ongoing activities (3) (15) 47%

Benchmark EBIT margin (0.9)% (4.8)%

AppendixEMEA/Asia PacificTwelve months ended 31 MarchUS$million

All results are Benchmark figures and are on an ongoing activities basis.Growth at constant exchange rates

36 © Experian Public

Appendix

Credit Services

Revenue 2017 2016Total

GrowthOrganic growth

Q1 FY18Organic growth

North America 1,341 1,237 8% 8% 6%

Latin America 658 579 6% 6% 5%

UK and Ireland 246 275 3% 3% 3%

EMEA/Asia Pacific 144 149 (3)% (3)% 0%

Total revenue 2,389 2,240 6% 6% 5%

Benchmark EBIT 817 791 2%

Benchmark EBIT margin 34.2% 35.3%

All figures above on a ongoing activities basisGrowth at constant exchange rates

Twelve months ended 31 MarchUS$million

37 © Experian Public

Appendix

Decision Analytics

Revenue 2017 2016Total

GrowthOrganic growth

Q1 FY18Organic growth

North America 162 161 0% 0% 13%

Latin America 48 36 34% 34% 44%

UK and Ireland 214 234 5% 5% 7%

EMEA/Asia Pacific 160 135 21% 21% 13%

Total revenue 584 566 9% 9% 13%

Benchmark EBIT 120 104 27%

Benchmark EBIT margin 20.5% 18.4%

All figures above on a ongoing activities basisGrowth at constant exchange rates

Twelve months ended 31 MarchUS$million

38 © Experian Public

AppendixMarketing Services

Revenue 2017 2016Total

GrowthOrganic growth

Q1 FY18Organic growth

North America 215 200 8% 8% 18%

Latin America 24 16 39% 39% 44%

UK and Ireland 145 160 5% 5% 0%

EMEA/Asia Pacific 37 31 16% 16% 13%

Total revenue 421 407 8% 8% 12%

Benchmark EBIT 95 76 32%

Benchmark EBIT margin 22.6% 18.7%

All figures above on a ongoing activities basisGrowth at constant exchange ratesThe 2016 results have been restated to reflect the email/cross-channel marketing business ('CCM') reclassification as a discontinued operation.

Twelve months ended 31 MarchUS$million

39 © Experian Public

Appendix

Consumer Services

Revenue 2017 2016Total

growthOrganic growth

Q1 FY18Organic growth

North America 739 696 6% (2%) (5)%

UK and Ireland 202 255 (9)% (9)% (19)%

Total revenue 941 951 2% (4)% (8)%

Benchmark EBIT 243 241 4%

Benchmark EBIT margin 25.8% 25.3%

All figures above on a ongoing activities basisGrowth at constant exchange rates

Twelve months ended 31 MarchUS$million

40 © Experian Public

AppendixBenchmark cash flow performance

Benchmark EBIT

Benchmark operating cash

flow

Working capital and

other

Net capital expenditure

Amortisation and

depreciation

Benchmark free cash flow

Net interest paid

Tax paid on operating activities

1,199 (393)322

21

1,149 (70)(144)

(2)

933

96%conversion of EBIT into

operating cash flow

112%conversion of Benchmark

earnings into free cash flow

Dividends to minorities

41 © Experian Public

AppendixNet debt reconciliation

Net debt at 1 April 2016Net debt /

Benchmark EBITDA 1.9x

Net share purchases

Equity dividends paid

Benchmark free cash flow

Acquisitions and minority investments

Net debt at31 March 2017

Net debt / Benchmark EBITDA

2.1x

FX and other

3,023

392

(933)

432

353

381

(83)

3,173

42 © Experian Public

AppendixExperian American Depositary Receipt (ADR) program

For ADR shareholder enquiries, please contact:Shareholder RelationsBNY Mellon Depositary ReceiptsPO Box 30170College StationTX 77842-3170United States

T: + 1 201 680 6825 (From the US: 1-888-BNY-ADRS, toll free)

E: [email protected]: www.mybnymdr.com

Experian ADR shares trade on the OTCQX under the following information:Symbol EXPGYCUSIP 30215C101Ratio 1 ADR : 1 ORDCountry United KingdomEffective Date October 11, 2006Underlying SEDOL B19NLV4Underlying ISIN GB00B19NLV48U.S. ISIN US30215C1018Depositary BNY Mellon

43 © Experian Public

AppendixContacts

ExperianCardinal Place80 Victoria StreetLondon Tel: +44 (0)203 042 4200SW1E 5JL Website: www.experianplc.com

Nadia Ridout-Jamieson Peg SmithChief Communications Officer Executive Vice-PresidentEmail: [email protected] Email: [email protected]

Sarah SchibliInvestor Relations and Communications ManagerEmail: [email protected]

AppendixContacts

44 © Experian Public

20 July 2017 Annual General Meeting

15 November 2017 Half year financial report

AppendixEvent calendar

45 © Experian Public

• This presentation is being made only to, and is only directed at, persons to whom this presentation may lawfully be communicated(“relevant persons”). Any person who is not a relevant person should not act or rely on this presentation or any of its contents.

• Information in this presentation relating to the price at which relevant investments have been bought or sold in the past or the yield on such investments cannot be relied upon as a guide to the future performance of such investments.

• This presentation does not constitute or form part of, and should not be construed as, an offering of securities or otherwise constitute an invitation, inducement or recommendation to any person to underwrite, subscribe for or otherwise acquire securities in anycompany within the Experian group (the “Group”).

• Certain statements made in this presentation are forward looking statements. Such statements are based on current expectations and are subject to a number of risks and uncertainties that could cause actual events or results to differ materially from any expected future events or results expressed or implied in these forward-looking statements. Forward-looking statements speak only as of the date of this presentation.

• This presentation contains certain non-GAAP financial information. The Group’s management believes that these measures provide valuable additional information in understanding the performance of the Group or the Group’s businesses because they provide measures used by the Group to assess performance. Although these measures are important in the management of the business, they should not be viewed as replacements for, but rather as complementary to, the GAAP measures.

AppendixDisclaimer