Embed Size (px)

Citation preview

MATT BRIGHTSenior Advisor, Advocacy & Communications

JULY 2021

101 QUESTIONS AND 101 ANSWERS FROM THE CCS 101 WEBINAR SERIES

101 QUESTIONS AND 101 ANSWERS FROM THE CCS 101 WEBINAR SERIES2

1.0 THE CCS 101 WEBINAR SERIES: AN OVERVIEW 32.0 CRITERIA AND ORGANIZATION OF THE CCS 101 WEBINARS’ 101 QUESTIONS AND ANSWERS 43.0 101 QUESTIONS AND ANSWERS FROM THE CCS 101 WEBINAR SERIES 5

3.1 QUESTIONS ABOUT AND FOR THE GLOBAL CCS INSTITUTE 53.2 CCS TECHNOLOGY 63.3 CCS ECONOMICS – COSTS AND FINANCING 103.4 CCS TRANSPORT 123.5 CCS STORAGE 143.6 CCS GEOGRAPHY 183.7 CCS POLICY 203.8 CARBON UTILISATION 24

4.0 REFERENCES 25

CONTENTS

101 QUESTIONS AND 101 ANSWERS FROM THE CCS 101 WEBINAR SERIES3

Between 23 April and 21 May, 2021, the Global CCS Institute hosted a series of three webinars every other Friday from 10-11 am Eastern Time, titled The Carbon Capture and Storage 101 Webinars. The purpose was to give U.S. Congressional staffers and other interested stakeholders an introduction to the key facets of the global CCS industry. With only one hour allocated to each webinar, the theme for each one was chosen carefully not only to answer as many questions as possible about the current state of the CCS enterprise but also to focus on the requisites for accelerating the deployment of more facilities across the world. Accordingly, the first webinar focused on “Introducing a CCS Project1,” the second was on “CCS Infrastructure for a Net-Zero Future2,” and the third was titled “CCS Policy for a Net-Zero Future3.”

Based on attendance statistics alone, the series demonstrated a high level of interest in CCS. The webinars averaged 605 attendees with a maximum of 792 and a minimum of 465 from 55 countries on 6 continents. More importantly, these webinars generated an extraordinary number of questions – 101 in total. Their breadth and depth emphasised the many technological, financial, geographical, social, and political aspects of CCS that must be met to achieve the scale-up required to manage climate change4. These questions also clearly indicate the need for more educational materials on CCS.

This brief seeks to fill that void by answering the 101 questions from the CCS 101 webinars. It should be an especially effective educational tool because it deals

with specific themes in the CCS universe that are either misunderstood, mischaracterized, or missing information to a very diverse audience composed of experts and non-experts alike. Indeed, questions came from industry representatives, academics, Capitol Hill staffers, members of the press, and the general public. Some were extremely technical and some quite general. Accordingly, some required detailed, nuanced answers and some no more than a few words. Regardless, with nearly 1000 people attending at least one webinar in the CCS 101 Series, it is likely that these questions represent the queries of a broad swath of the public interested in developing or investing in a CCS project. The answers provide a rich tableau of insights into the current status and future potential of CCS.

1.0 THE CCS 101 WEBINAR SERIES: AN OVERVIEW

Table 1. General overview and attendance statistics from the CCS 101 Webinar Series.

STATISTICS INTRODUCING A CCS PROJECT

CCS INFRASTRUCTURE FOR A NET-ZERO FUTURE

CCS POLICY FOR A NET-ZERO FUTURE

Date 23 April, 2021 7 May, 2021 21 May, 2021

Speakers

• Peter Sherk• Syrie Crouch• Ryan Edwards• Jannicke Bjerkas

• Matt Vining• Susan Hovorka• Jean-Philippe Hiegel• Ian Hunter

• Shuchi Talati• Lee Beck• Jena Lococo• Shannon Heyck-Williams

Speaker Affiliations

• Wabash Valley Resources• Shell• Oxy Low Carbon Ventures• Fortum Oslo Varme

• Navigator Energy Services• University of Texas, Austin• Northern Lights CCS Project• Net Zero Teesside & Northern

Endurance Partnership

• Office of Fossil Energy, DOE

• Clean Air Task Force• ClearPath• National Wildlife Federation

Attendees 792 557 465

Questions included in this Brief

51 29 21

101 QUESTIONS AND 101 ANSWERS FROM THE CCS 101 WEBINAR SERIES4

Selecting questions to include in this brief was no trivial undertaking. At the end of each webinar, Zoom, (the Institute’s webinar platform) generated a Q&A report in Microsoft Excel. Each row in the report represented a discreet question or comment posted in Zoom’s Q&A function during the webinar. Commentary was not included in this brief, and not all rows in the Q&A report generated questions that were selected for this brief. For example, the first webinar’s Q&A report had 160 rows of questions or comments to sort through of which 51 were included in this brief.

A criteria was developed to select suitable questions. First, the questions had to be germane to CCS. Second, the author of this brief had to understand the question. Third, questions of a speculative nature (e.g., “Do you think a certain bill dealing with CCS in the U.S. Congress will pass this year?”) were generally discarded unless the item of speculation allowed the author to expound on an important point. Fourth, only questions with broad interest to a general audience were answered, and those that focused on specific projects (e.g., “How is the Wabash Valley Resources project financed?”) or those that were directed at specific people were typically omitted unless the project served as a model for the larger industry.

Some questions were asked multiple times by different individuals (e.g., about the safety and longevity of underground storage), in which case the question was counted only once but flagged in parentheses to include the number of times it was asked. All questions were kept anonymous. In addition, some were paraphrased for clarity, but as much as possible the author has tried to maintain the original intent and phrasing of the question.

This brief arranges questions in eight categories according to certain broad themes rather than in chronological order by webinar. Some questions could be placed in several categories in which case the author made a judgment call about the most appropriate category. All questions are numbered to make it easier to navigate this brief. Question categories and numbers can be found in Table 2.

As much as possible, this brief seeks to answer questions using Global CCS Institute publications and its multimedia library presentations. In this way, the brief underscores the wealth of Institute educational materials freely available to the general public.

Table 2. The 8 categories used to group webinar questions.

2.0 CRITERIA AND COLLATION OF THE CCS 101 WEBINARS’ 101 QUESTIONS AND ANSWERS

QUESTION CATEGORIES

QUESTION NUMBERS

Questions about and for the Institute 1-6

CCS Technology 7-14

CCS Economics – Costs & Financing 15-20

CCS Transport 21-33

CCS Storage 34-63

CCS Geography 64-74

CCS Policy 75-99

Carbon Utilisation 100-101

101 QUESTIONS AND 101 ANSWERS FROM THE CCS 101 WEBINAR SERIES5

3.1 Questions about and for the Global CCS Institute

1. How often does the Global CCS Institute update its CO2RE projects database?

A. The Global CCS Institute updates its CO2RE (projects) database5 twice per year.

2. How does the Institute characterize its projects in its CO2RE database in terms of stages of development? Are all of the projects “in development” stages post-Final Investment Decision (FID)?

A. The Institute characterizes its projects in the CO2RE database in six different ways: “early development” and “advanced development” (which are both pre-Final Investment Decision stages), “in construction” and “operating” (which are both post-Final Investment Decision stages), and “suspended” or “completed” (which means the CCS facility did capture CO2 at one point but is currently not capturing or did capture CO2 and is in the process of decommissioning). This chart (below) will help clarify our project status characterization.

• Examine short listed options and sub-options

• Establish if any fatal flaws

• Select one best option for taking forward

• “What should it be?”

• Feasibility studies

• Estimate overall project capital cost (20-25%) and operating costs (10-15%)

• Site assessment studies

• Examine selected option and provide further definition to allow investment decision to be made

• Demonstrate a technical and economic viability of the project

• “What will it be?”

• FEED

• Estimate overall project capital cost (10-15%) and operating costs (5%)

• Site selection studies

• Undertake remianing detailed design

• Build organisation to comission and operate asset

• Undertake construction activites

• Undertake comissioning

• Operate the asset within regulatory compliance requreiments, for the operating life of the asset

• Prepare for decommissioning

• Asset decomissioning

• Post-injection monitoring program bring implemented

3.0 101 QUESTIONS AND ANSWERS FROM THE CCS 101 WEBINAR SERIES

EARLY DEVELOPMENT IN CONSTRUCTIONADVANCED

DEVELOPMENT

DECOMMISSIONED

OPERATING COMPLETION

FINAL INVESTMENT DECISION

101 QUESTIONS AND 101 ANSWERS FROM THE CCS 101 WEBINAR SERIES6

3. Did you say the first CCS project was started in 1972? Are you referencing the first Exxon project with CO2 being used for enhanced oil recovery (EOR)?

A. That is correct. The first CCS project started capturing CO2 in 19726 (though construction started in 1971) on a natural gas processing plant in Terrell, Texas. The captured CO2 was then transported by pipeline to an EOR field.

4. What would be the earliest carbon capture, use and storage (CCUS) can become commercialized to be able to work towards net-zero?

A. CCUS is already commercialized. The technology works and there are currently 26 commercial, operating CCS facilities around the globe that are engaged in active capture and storage of almost 40 million tonnes per annum (Mtpa)7. To date, 300 million tonnes of CO2 have already been captured around the globe and permanently stored. These emissions reductions are helping to mitigate climate change. Strong policies and investment in CCS will further help commercialize the technology to accelerate its deployment on the much larger scale needed to defeat climate change.

5. If your company is developing a new CCUS technology what are your recommendations for connecting with the appropriate agencies or individuals?

A. Reach out to the Institute ([email protected]), and we will help you facilitate those connections. The Institute is well connected to the Department of Energy (one of our members), businesses and governments and can direct you to the appropriate place.

6. Do any of the panelists have any recommendations for students or early-career professionals who are very interested in CCS? (X2)

A. The Institute is thrilled to see such enthusiasm about CCS. A good place to start is continuing to attend webinars like this. Study policy, finance, engineering, economics, or law and focus your studies on aspects of CCS that relate to these knowledge fields. Work for a company that employs CCS, and in your job interview specify that you want to work on the technology. Demonstrate that you already know a significant amount about CCS. Employers will see your passion, and somebody will give you an opportunity to shine.

3.2 Questions about and for the Global CCS Institute

7. What is the difference between pre-combustion and post-combustion carbon capture technologies, and how can they be used more in the future?

A. (See the Institute’s diagrams and webpage for more information.) Pre-combustion and post-combustion carbon capture refer to the two predominant types of CO2 capture8. Pre-combustion technologies separate a carbon-based fuel into CO2 and H2 before the H2 portion of the fuel is converted into energy. The CO2 can then be compressed and stored. Post-combustion refers to capturing CO2 from the exhaust gases that are released after a carbon-based fuel. Pre-combustion technology is currently being used in industrial processes such as chemicals production. Post-combustion technology is more widely used at present and is being employed for power generation facilities as well as capture from ethanol, etc. The technology for post-combustion technology is very advanced and will likely continue to be widely used while pre-combustion will only be employed on new power generation facilities not existing plants.

8. Are there new carbon capture chemical processes being discovered?

A. New carbon capture chemical processes are being developed all the time because innovative research and development (R&D) continues at the U.S. Department of Energy9 and many other public and private research organizations and companies around the globe. Read our report, Technology Readiness and Costs of CCS10, to get a detailed view of new carbon capture processes. And subscribe to the Global CCS Institute’s Newsletter11 to stay current on all of the latest CCS news. (For example, our May, 2021 Newsletter highlights that Net Power just recently announced its plans to build the world’s first zero emissions natural gas power plants12 – an enormous leap in carbon capture innovation.)

9. Does CCS decrease the efficiency of power plants, thus increasing their generation costs.

A. Just like other emission/pollution removal technologies, CCS requires energy input and extra equipment to function, thus reduces the efficiency of power plants. Please refer to NETL’s report: “Cost and Performance Baseline for Fossil Energy Plants13”: • CCS capturing 90% CO2 reduces the Plant

Efficiency (HHV) of the supercritical coal fired power (SCPC) plant from 40.3% to 31.5%, but the CO2 emission is reduced from 777 Kg/ MWh to 99 Kg/MWh.

101 QUESTIONS AND 101 ANSWERS FROM THE CCS 101 WEBINAR SERIES7

• CCS capturing 90% CO2 reduces the Plant Efficiency (HHV) of the natural gas combined cycle power (NGCC) plant from 53.6% to 47.7%, but the CO2 emission is reduced from 342 Kg/ MWh to 38 Kg/MWh.

There are emerging CCS technologies, which require considerably lower energy consumption (for example, carbon capture regeneration duty reduces from 3.5 GJ/tonne CO2 of 1st generation capture technology to 2.4 GJ/tonne CO2 of 2nd generation capture technology in coal fired power generation). This will further minimize the impact on the energy efficiency of power plants.

10. Can CCS power generation projects economically compete with the renewable power generation?

A. When talking about the economic competence in electricity generation technologies, we used to refer to the levelized cost of electricity (LCOE). See

the following Figure ES2, from IEA’s “Projected Costs of Generating Electricity 202014,” (See below.) the economic competence of renewable is dependent on different countries/regions. Even in the same country/region, the availability of renewables is diverse in different areas. Thus renewables may be considered economical in one place, but less so in others.

Plus, renewable technologies are variable power generation technologies (meaning not always available), in which the LCOE is incomplete to reflect, or compare with dispatchable technologies. IEA is introducing Value Adjusted Levelised Cost of Electricity (VALCOE) and US EIA is introducing the Levelised Avoided Cost of Electricity (LACE). Both VALCOE and LACE are similar to consider:

• Energy value• Flexibility value • Capacity value

INDIA UNITED STATES CHINA EUROPE JAPAN

Med

ian

LCO

E (U

SD/M

Wh)

Note: Values at 7% discount rate

CO

AL

50

100

150

200

250

NU

CLE

AR

NU

CLE

AR

ON

SH

OR

E W

IND

(>=1

MW

)

ON

SH

OR

E W

IND

(>=1

MW

)

ON

SH

OR

E W

IND

(>=1

MW

)

ON

SH

OR

E W

IND

(>=1

MW

)

ON

SH

OR

E W

IND

(>=1

MW

)

SO

LAR

PV

(UTI

LITY

SC

ALE

)

SO

LAR

PV

(UTI

LITY

SC

ALE

)

SO

LAR

PV

(UTI

LITY

SC

ALE

)

SO

LAR

PV

(UTI

LITY

SC

ALE

)

SO

LAR

PV

(UTI

LITY

SC

ALE

)

CO

AL

OFF

SH

OR

E W

IND

OFF

SH

OR

E W

IND

OFF

SH

OR

E W

IND

OFF

SH

OR

E W

IND

GA

S (C

CG

T)

NU

CLE

AR

CO

AL

GA

S (C

CG

T)

NU

CLE

AR

NU

CLE

AR

CO

AL

GA

S (C

CG

T)

GA

S (C

CG

T)

101 QUESTIONS AND 101 ANSWERS FROM THE CCS 101 WEBINAR SERIES8

See Figure 4.5 for the competitiveness comparison after the adjustment. However, IEA/EIA are still working on the new matrix with the inclusion of CCS. As mentioned, please read IEA’s Projected Costs of Generating Electricity 2020 and U.S. EIA’s Levelized Costs of New Generation Resources in the Annual Energy15 for more information.

USD

/MW

hU

SD/M

Wh

20

-20

-40

-60

-80

-100

0

20

-20

-40

-60

-80

-100

0

ON

SH

OR

E W

IND

SO

LAR

PV

WIT

H S

TOR

AG

E

OFF

SH

OR

E W

IND

NU

CLE

AR

CO

AL

GA

S (C

CG

T)

GA

S (G

T)

ENERGY CORRECTION

ON

SH

OR

E W

IND

SO

LAR

PV

WIT

H S

TOR

AG

E

OFF

SH

OR

E W

IND

NU

CLE

AR

CO

AL

GA

S (C

CG

T)

GA

S (G

T)

CAPACITY CORRECTION FLEXIBILITY CORRECTION

By 2025, value adjustments are already important in evaluating the competitiveness of solar PV without storage, and remain important to peaking plants like open-cycle gas turbines.

SO

LAR

PV

(UTI

LITY

SC

ALE

)

SO

LAR

PV

(UTI

LITY

SC

ALE

)

101 QUESTIONS AND 101 ANSWERS FROM THE CCS 101 WEBINAR SERIES9

11. What are the emissions created to capture (scrub the amine) and compress the CO2, and do you think that these emissions can be reduced or eliminated long term?

A. This depends on the capture process used. Adsorption-based capture processes tend to rely on the compression energy used to drive the separation – in this case, the emissions are those associated with the electricity supply to the gas compressor or vacuum pump. Solvent-based capture requires the solvent to be regenerated with heat. If the heat is available from the host plant (e.g. if it’s a combined heat and power unit) then no additional emissions would be produced. If the heat source (usually steam) is required to be generated separately, then there would be combustion emissions from the steam generation plant. CO2 compression is typically done with electrically driven compressors. Hence the emissions are those associated with the electricity source used (scope 2 emissions).

12. Are any chemicals consumed or wasted in the CO2 capture process and thus must be replaced?

A. Amine based capture plants usually experience solvent degradation over time. Eventually the solvent needs to be replaced. This is an ongoing area of research to understand and minimise degradation. Non-amine processes (e.g. those using potassium carbonate solvents, or membrane-based capture plants) do not have significant chemical consumption or waste production.

13. What are the additional costs of liquefying with regard to compression?

A. The costs of both liquefaction and compression are very dependent on the scale of operation, and so need to be assessed on a case-by-case basis. However, generally liquefaction is more expensive than gas compression, but is typically done when ships are required for CO2 transport.

101 QUESTIONS AND 101 ANSWERS FROM THE CCS 101 WEBINAR SERIES10

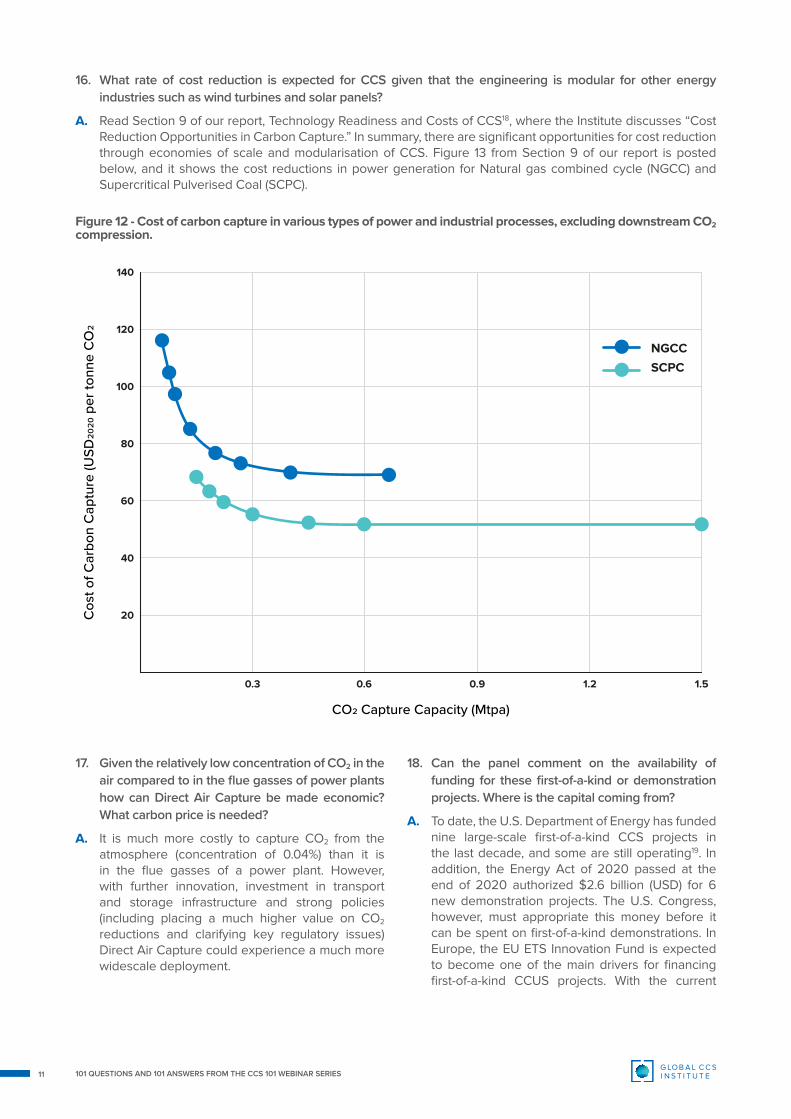

Figure 12 - Cost of carbon capture in various types of power and industrial processes, excluding downstream CO2 compression.

0

50

100

200

300

150

250

POWER GENERATION INDUSTRY SECTORS

REFINERY CEMENT IRON & STEEL

14. How can you produce net negative fuels using CCS?

A. CCS can be used to produce net negative fuels through a process known as bioenergy with carbon capture and storage (BECCS). When plants or other photosynthetic organisms capture CO2 and convert it into sugars using photosynthesis, that reaction represents a net negative capture process because photosynthesis removes CO2 from the atmosphere and converts it into a solid. If the energy in the sugars of the plants is then converted into a fuel at a bioenergy refinery and all of the CO2 is captured in the process of fuel conversion, the resulting fuel will be a net negative fuel because more CO2 is captured in the process of photosynthesis than is omitted in burning the fuel. Watch a video recap of an Institute webinar where we explain the process16.

3.3 CCS Economics – Costs and Financing

15. What are the per tonne capture costs of CCS on different applications (e.g., ethanol) including direct air capture (DAC)? (X3)

A. Take a look at Figure 12 from our report, Technology Readiness and Costs of CCS17, posted below. The capture costs for ethanol are below $20 (USD)/tonne. For DAC, it is far more difficult to determine the cost because currently there are no facilities operating on a large scale. The capture cost estimates range from $200-$600/tonne.

101 QUESTIONS AND 101 ANSWERS FROM THE CCS 101 WEBINAR SERIES11

16. What rate of cost reduction is expected for CCS given that the engineering is modular for other energy industries such as wind turbines and solar panels?

A. Read Section 9 of our report, Technology Readiness and Costs of CCS18, where the Institute discusses “Cost Reduction Opportunities in Carbon Capture.” In summary, there are significant opportunities for cost reduction through economies of scale and modularisation of CCS. Figure 13 from Section 9 of our report is posted below, and it shows the cost reductions in power generation for Natural gas combined cycle (NGCC) and Supercritical Pulverised Coal (SCPC).

17. Given the relatively low concentration of CO2 in the air compared to in the flue gasses of power plants how can Direct Air Capture be made economic? What carbon price is needed?

A. It is much more costly to capture CO2 from the atmosphere (concentration of 0.04%) than it is in the flue gasses of a power plant. However, with further innovation, investment in transport and storage infrastructure and strong policies (including placing a much higher value on CO2 reductions and clarifying key regulatory issues) Direct Air Capture could experience a much more widescale deployment.

18. Can the panel comment on the availability of funding for these first-of-a-kind or demonstration projects. Where is the capital coming from?

A. To date, the U.S. Department of Energy has funded nine large-scale first-of-a-kind CCS projects in the last decade, and some are still operating19. In addition, the Energy Act of 2020 passed at the end of 2020 authorized $2.6 billion (USD) for 6 new demonstration projects. The U.S. Congress, however, must appropriate this money before it can be spent on first-of-a-kind demonstrations. In Europe, the EU ETS Innovation Fund is expected to become one of the main drivers for financing first-of-a-kind CCUS projects. With the current

Figure 12 - Cost of carbon capture in various types of power and industrial processes, excluding downstream CO2 compression.

20

0.3 0.6 0.9

NGCC

SCPC

1.2 1.5

40

60

80

100

120

140

CO2 Capture Capacity (Mtpa)

Cos

t of C

arbo

n C

aptu

re (U

SD20

20 p

er to

nne

CO

2

101 QUESTIONS AND 101 ANSWERS FROM THE CCS 101 WEBINAR SERIES12

EU ETS carbon price fluctuating around 50 EUR, the size of the fund would be 22.5 billion EUR for the ten-year period of 2021-2030. The first large-scale call saw over 60 CCUS project applications. The Innovation fund is expected to be a major source of funding for both the planning, and the construction and operation of CCS across the EU, and this expectation is further strengthened by the recent European Commission proposal to double the size of the Innovation Fund during the next EU ETS review.

19. On the topic of costs, are any of you also calculating (or thinking about) the cost of CO2 avoided (most relevant to climate change) as opposed to the lower cost of capture?

A. Yes. This is why it is important to consider the emissions associated with the energy supply in any capture process. External emissions would reduce CO2 avoided. But if the energy source comes from the host plant (e.g. a CHP unit) then the emissions are already being captured and accounted for.

20. How much can we expect energy costs to rise to fund CCS? Are there any reliable projections?

A. While operating a CCS facility does require energy, there is no reason to believe that a company’s voluntary decision to fund a CCS project will result in high energy costs to the company’s client base. Tax credits like 45Q and the ability to sell CO2 for use in EOR, the food and beverage industry, etc. typically provide a direct financial incentive to a company that installs CCS equipment in the U.S. In general, however, there are too many unknowns in the world of energy supply and demand to forecast energy costs in the future (and especially on a global scale).

3.4 CCS Transport

21. Won’t the energy consumed in offshore transport of CO2 be greater than the climate value of storing the CO2?

A. No, the CO2 emissions incurred for offshore storage will be a tiny fraction of the emissions reduced through the transport and storage of CO2 offshore.

22. What are the limitations to transporting the CO2 and H2 gas with current technologies?

A. The primary limitation to transporting CO2 and H2 gas with current technologies is the lack of CO2 transport infrastructure. In the onshore U.S., there are approximately 50 CO2 pipelines that cover a distance of roughly 5,000 miles, yet there

are hundreds of thousands of miles of natural gas and oil pipelines. The same is true in Europe. For offshore shipping of CO2 there aren’t enough ships yet available for a large-scale CO2 transport industry. There will need to be a roughly 100-fold scale up of CO2 transport infrastructure around the globe to help the world achieve 2050 climate goals.20

23. Will the lack of CO2 transport infrastructure to areas where sequestration is geologically feasible be a limiting factor in truly scaling up CCS?

A. The lack of CO2 transport infrastructure is definitely a limiting factor. See the answer to the question above. However, transport and storage need to be developed hand-in-hand in sync with carbon capture technology to help accelerate the deployment of CCS.

24. What are the risks to CO2 leaking from CO2 pipelines and is there research on it?

A. We have answered this question on the Global CCS Institute’s website: “CO2 pipelines and ships pose no higher risk than is already safely managed for transporting hydrocarbons such as natural gas and oil. International standards are being developed to further promote safe and efficient operation of CO2infrastructure21.”

25. Assuming that in the long-term, demand for natural gas will decrease, can existing oil and gas pipelines be converted to CO2 transport pipelines and how simple is the process? (X5)

A. Existing oil and gas pipelines can be converted to CO2 transport pipelines for short-distance, low-volume transport but in general new ones would need to be constructed for large-volume, long-distance transport. This is because the steel typically must be significantly thicker in a CO2 pipeline than in one that transports hydrocarbons. For long-distance transport, the pressures needed to move CO2 through a CO2 pipeline are much higher than what is required for hydrocarbon transport. However, existing hydrocarbon pipeline corridors can be used to build CO2 pipelines that run parallel to other pipelines. In this way, the environmental impacts of constructing a new CO2 pipeline can be minimised.

26. Could you elaborate more on what kind of pipe (metallurgy requirements) is needed for CO2 transportation?

A. Carbon steel is suitable, so long as the flanges and pipe schedules are suitable for the high pressures required (well in excess of 74 bar). It is essential that CO2 be dehydrated to very low dew points to

101 QUESTIONS AND 101 ANSWERS FROM THE CCS 101 WEBINAR SERIES13

ensure no liquid water can condense in the CO2 stream (this would be highly corrosive to steel in presence of high CO2 partial pressures).

27. What price multiplier should be considered with a CO2 pipeline compared with oil or gas pipelines $/mile?

A. It isn’t easy to generalise about this. For starters, pipeline costs tend to vary with length and pipeline diameter, so a $/mile figure ignores one of the two main cost drivers. CO2 pipelines for bulk transport typically operate well above the critical pressure of CO2 (74 bar). So the pressure rating of the pipeline needs to be higher than it may be in non-CO2 applications, though this won’t always be the case. Pipelines are typically carbon steel and not dissimilar to those used in oil and gas transport, apart from the sometimes higher pressure ratings required. Dense phase CO2 has a higher density than natural gas at similar pressures, which means you can generally make a smaller diameter pipeline for a given mass flowrate.

28. What type of ships do you need to transport CO2?

A. Dedicated CO2 ship designs are being developed. It is fair to say that no clear consensus on the best kind of design has yet to emerge, as bulk transport of CO2 at the scale required for CCS is a relatively new area. CO2 is loaded as a liquid at moderate pressure. It is anticipated that most will hold CO2 in multiple pressure vessels on board, to enable distribution of the CO2 load across the vessel. Storage tanks will need to be designed to safely accommodate the cold (-50 to -30 C) liquid CO2.

29. How does the cost of CO2 transport by truck, rail, and ship compare to transport by pipeline? How is that comparison affected by the cost of constructing new pipeline infrastructure as opposed to using existing road, rail, and port infrastructure? (X2)

A. Shipping tends to be lower cost per tonne for very long transport distances (well above 500km). Pipelines tend to be more cost effective for shorter distances. Trucks are expected to be be more expensive than ships or pipelines due to the smaller annual tonnages involved with trucks.

30. What is cost per mile of CO2 pipeline? (X2) In what phase is CO2 piped? (X2)

A. Matt Vining, the CEO of Navigator Energy Services who is currently planning a 1200-mile CO2 pipeline in the Midwestern U.S., answered this question with a figure of $1-2 Million USD/mile. However, the cost is also dependent on the capacity of the pipeline.

31. In what phase is CO2 piped? (X2)?

A. For shorter distances it may be transported in the gas phase. Longer-distance transport will almost always be piped as a dense phase fluid (well above the 73.9 bar critical pressure of CO2). Sometimes this is termed “supercritical”, though strictly speaking this only applies if the temperature is also above CO2’s critical temperature of 31 degrees C.

32. Does there need to be a CO2 specification in terms of purity that must be met by emitters in order to transport CO2 in a pipeline system? How would this specification be defined and monitored?

A. The CO2 needs to be dry, i.e., have no water in it otherwise it will become carbonic acid which corrodes steel pipelines. The ISO has developed a standard for CO2 specification for pipeline transport – ISO 27913:2016. Among other things, this sets specifications for CO2 purity (>95 mol%), water dew point limits to prevent corrosion and hydrate formation, and concentrations of other trace impurities.

33. What determines the purity/specifications of the CO2 from a capture perspective: the transport by pipeline or the geological storage / EOR requirements?

A. Project economics and safety ultimately dictate thresholds for impurities in CO2 gas streams. Impurities impact project economics in at least three ways compared to a pure CO2 stream: 1) Removing impurities increases CO2 capture cost; 2) Impurities may impact storage capacity and injectivity due to changes in phase behavior and buoyancy; and 3) Impurities can corrode pipelines and well components. In terms of specific impurities - Inerts such as nitrogen can remain in small quantities – essentially these will not cause a problem with transport, but they will displace pore space in the storage resource. Ultimately, the purity selected is a balance between capture cost and storage resource utilisation. Some capture technologies inherently produce high purity CO2 (e.g. amines) whereas for others, purity is a design decision. Water is an essential component to remove. High purity CO2 in the presence of water can, if it is allowed to condense, form carbonic acid which can corrode downstream equipment. This is why CO2 dehydration is an essential part of any CO2 compression system that is discharging to pipeline. If the CO2 is being liquefied for transport by ship, water removal is also essential to prevent ice formation in cold CO2.22

101 QUESTIONS AND 101 ANSWERS FROM THE CCS 101 WEBINAR SERIES14

3.5 CCS Storage

34. What are the long-term impacts and risks (such as leakage) to injecting carbon deep underground? (X6)

A. The long-term impact of injecting CO2 deep underground is that it will help mitigate climate change. The risks to injecting CO2 underground are minimal. CO2 is not flammable or explosive like natural gas. It is not toxic like refrigerants used in refrigerators and air conditioners. Natural analogues, research tests, and CO2 operations confirm that it is virtually impossible for CO2 to pose a catastrophic leak to the atmosphere after being injected one to two kilometers under the Earth’s surface into suitable, permeable storage basins which are capped by non-permeable rock.23 Millions of tonnes of CO2 have already been captured and stored safely.24 CO2 storage reservoirs are operated below the fracture pressure of the rock formation with a margin of safety – there is no “fracing”. Any seismicity resulting from CO2 injection is very minor, requiring instrumentation to detect it.25 In addition, EOR projects, where CO2 storage occurs incidentally, have been operating safely for decades. This has been validated by the work of intergovernmental and industry partnerships, research programs, and stakeholder networks. No significant safety, health or environmental impacts have been documented from existing CCS projects.26

35. What is the potential for CO2 leakage from a geological storage site especially in earthquake areas? (X5)

A. There is limited potential for CO2 to leak from a geological storage site. For example, earthquakes, such as those regularly experienced in Japan, have not caused any leakages from their CO2 storage basins.27 The Tomakomai Project in Northern Japan was actively injecting and storing CO2 when a large earthquake occurred in the region. A world-class monitoring and verification programme confirmed there was no impact to the stored CO2.

36. As you said, the use of CO2 for EOR application has been in place for many decades, but the total volume injected seems small in comparison to the CO2 volumes expected in the next 20-30 years... Do you think all the risks still make this application safe when volumes increase so substantially?

A. See the answer to the question above. EOR projects, where CO2 storage occurs incidentally, have been operating safely for decades. This has been validated by the work of intergovernmental

and industry partnerships, research programs, and stakeholder networks. The total volume injected is not the critical part; the injection rates are what matters. We know there is more than enough storage resource available (volume) to meet targets. We know from historical injection rates of CO2-EOR operations that high rates can be achieved and sustained. The three largest operational projects are injecting between 4 and 7 million tonnes of CO2 per annum, the largest being operational for over 30 years. No significant safety, health or environmental impacts have been documented from existing CCS projects, while the EOR industry has an excellent safety record over four decades of operation.28 In summary, there are not a lot of “risks” to using CO2 for EOR followed by storage.

37. Is there enough geological storage space for the future of all the CO2 that can be captured, or is there an upper limit? How many billions of tonnes is this, and how many years of capture does this represent? (X3)

A. Read the Institute’s fact sheet titled, “Geological Storage of CO2: Safe, Permanent, and Abundant29.” There is more underground storage resources (billions of tonnes) than is actually needed to meet climate targets. The world’s key CO2 storage locations have now been assessed and almost every high-emitting nation has demonstrated substantial underground storage resources. As an example, there is between 2,000 and 20,000 billion tonnes of storage resources in North America alone. (Only 300 million tonnes of anthropogenic CO2 has been captured to date by comparison30.) Countries including China, Canada, Norway, Australia, US and the UK all boast significant storage availability, and other countries such as Japan, India, Brazil and South Africa have also proven their storage capability.

38. What are the different types of storage sites and the ideal geological formations beneficial for carbon storage? (X2)

A. There are two different types of storage site options: saline formations, and depleted oil and gas reservoirs31. Mineral carbonation, storing in rocks such as basalts are now emerging as viable options for storage, but more work is required. The ideal geological formation has the pore space (porosity) to accept all the CO2 required from operation at the rate required (permeability), permanently.

101 QUESTIONS AND 101 ANSWERS FROM THE CCS 101 WEBINAR SERIES15

39. Do you store liquid or gaseous CO2?

A. Once CO2 is captured, it is compressed into a fluid almost as dense as water (known as dense-phase CO2, which is neither liquid nor gas) and pumped down through a well into a porous geological formation32.

40. How do you monitor CO2 plumes underground?

A. (Answered by Jean-Philippe Hiegel) Monitoring will be done through 4D seismic technology. (From the Institute) The main monitoring tools for CO2 injection operations are those standard in the oil and gas industry: geophysical logging tools, pressure and temperature sensors, as well as seimic surveys. There are a growing number of tools being refined for CO2 storage including, include tracers, satellite measurements, soil and groundwater sensors.

41. Where does the displaced brine go when CO2 is injected underground?

A. Once CO2 is captured, it is compressed into a fluid almost as dense as water and pumped down through a well into a porous geological formation that often contains salty water or brine. Initially, the CO2 will displace the brine in the storage formation. But because injected CO2 is slightly more buoyant than the brine that co-exists within the storage reservoir, a portion of the CO2 will migrate to the top of the formation and become structurally trapped beneath the impermeable cap rock that acts as a seal. In most natural systems, there are numerous barriers between the reservoir and the surface. Some of the trapped CO2 will slowly start to dissolve into the saline water and become trapped indefinitely (called solution trapping); another portion may become trapped in tiny pore spaces (referred to as residual trapping). The ultimate trapping process involves dissolved CO2 reacting with the reservoir rocks to form a new

101 QUESTIONS AND 101 ANSWERS FROM THE CCS 101 WEBINAR SERIES16

mineral. This process, called mineral trapping, may be relatively quick or very slow, but it effectively locks the CO2 into a solid mineral permanently33.

42. What purity of CO2 is needed for it to be sequestered?

A. See our answer to question 33. There is no “need” for CO2 to be pure in terms of safety. CO2 has been injected and stored at various levels of concentration. However, a higher purity results in a more efficient utilisation of pore space and removing impurities from the CO2 generally makes the transportation process cheaper and more efficient over the long-term.

43. Do the ones who inject CO2 own the pore space, or who owns it?

A. This changes from country to country and state to state. In some states in the U.S., the person who owns the land above the pore space will own the pore space, but this is not true in every state, e.g., Texas. On the other hand, in Canada, the Crown owns all of the underground mineral space. This is an active area for policy consideration right now around the globe.

44. Impurities in the CO2 stream can have a flow assurance impact on fluid behaviour in the wellbore and subsurface. When taking CO2 from multiple sources how are impurities and variability of the gas content managed? When you say the system is agnostic to source how do you cope with impurities, particularly considering flow assurance concerns downhole (Joules-Thompson) if impurities are present? (X3)

A. (Answered by Matt Vining) “From a pipeline perspective, the CO2 product in transit will all meet the same specification. For the emitter, that translates into a nuanced engineered capture solution to extract or condition the impurities that would impact the overall operations of the system and sequestration. (i.e. The CAPEX answer is very different for an ammonia plant vs. cement vs. fossil power.)”

45. Why is it so critical to have a good storage seal on a CO2 injection well? If the CO2 can be held very securely by the capillary, microscopic spaces, why would we need to seal the well with concrete? (X2)

A. (Answered by Susan Hovorka) “Initially, the CO2 brought back to the surface, it is at a high saturation and high pressure. Sealing the well removes the pathway (for escape). Over time (years) the saturation will drop and the driving force on wells will reduce. Proper maintenance

of wells is expensive and to avoid well isolation failure, the best practice is plug them properly.

46. When CO2 is used in EOR what percent of the CO2 returns to the surface with the oil, gas, water? Is the CO2 processed and then injected again into the reservoir and how much is permanently stored?

A. Amounts of injected CO2 returning to the surface can vary depending on reservoir temperature, pressure, and oil properties, but at the surface, any CO2 is separated from the produced fluids, recompressed, and reinjected – essentially forming a closed loop. The most critical aspect is the timing of the operation. As the operation proceeds, the amount of CO2 recovered increases. As long as wells are properly plugged and abandoned, all injected CO2 stays in the subsurface permanently34.

47. After CO2 used for EOR is permanently stored, how is the storage verified and monitored and for how long?

A. The regulatory requirements for monitoring an EOR sites varies between jurisdictions. The main monitoring tools for CO2 injection operations are those standard to the oil and gas industry: geophysical logging tools, pressure and temperature sensors, as well as seismic surveys. There are a growing number of tools being refined for CO2 storage including, include tracers, satellite measurements, soil and groundwater sensors.

48. When you say sequestration sites in North America will be developed in parallel, does that refer to creating smaller more frequent sequestration sites, or is that specifically larger sequestration sites that will require a large/long pipeline infrastructure?

A. (Answered by Matt Vining) “Ultimately, we think this represents an interconnected network of larger scale sequestration sites.”

49. Given the number of different sources you list on slide 4 how do you accommodate and account for (in the pipeline design) for the different contaminants from all these different sources (say water, hydrogen, ammonia, amines, TEG etc.)?

A. Impurities need to be removed at the source facility prior to the stream entering the CO2 pipeline. The pipeline will be designed to handle impurities as per an agreed operating standard. It is essential that all upsteam facilities manage their operations to ensure this standard. Of specific importance is controlling water dew point for all CO2 sources.

101 QUESTIONS AND 101 ANSWERS FROM THE CCS 101 WEBINAR SERIES17

50. Is there a federal depth regulation for sequestration? or is it state by state?

A. There is no specific depth requirement in number of meters required for underground storage. Rather the permit needed for an underground storage well will require the injectors to show that their CO2 will not leak. There must be the right type of rocks in place – porous ones to receive the CO2 capped by very hard, non-porous rock above it to prevent the CO2 from escaping. These rocks need to be of a sufficient thickness and depth to safely store CO2 – generally at least 1 km underneath the earth’s surface.

51. Could you elaborate on what happens to CO2 once it’s already stored? Are there chemical reactions on CO2? In a long period of time, let’s say 20 years after the storage site is full, what would we found if we were to study the geology and chemistry of the site?

A. (Answered by Susan Hovorka) “The major chemical reaction is CO2 dissolution in water. CO2 can react with minerals. If the rock is reactive e.g. basalt, reaction may be the dominant mechanism. Most rocks are less reactive, capillary trapping remains the dominant (and sufficient) storage process.” (From the Institute’s website) “Some of the trapped CO2 will slowly start to dissolve into the saline water and become trapped indefinitely (called solution trapping); another portion may become trapped in tiny pore spaces (referred to as residual trapping). The ultimate trapping process involves dissolved CO2 reacting with the reservoir rocks to form a new mineral. This process, called mineral trapping, may be relatively quick or very slow, but it effectively locks the CO2 into a solid mineral permanently35.”

52. Are all the storage spaces are based on microscopic capillary dimension?

A. (Answered by Susan Hovorka) “In most cases the compression needed to make the CO2 dense for transportation is sufficient for injection.” (From Peletiri et al.36) – “Typically, CO2 pipeline operating pressures range from 10 to 15 MPa and temperatures from 15 to 30°C or 8.5 to 15 MPa and 13 to 44°C. Stipulating minimum pipeline pressure above 7.38 MPa, the critical pressure of CO2, ensures that the CO2 fluid remains in the supercritical state.”

53. How much pressure is needed to put the CO2 into the ground? How much energy is needed? would it be one of those situations where the energy needed to access this solution might make it more

prohibitively expensive?

A. (Answered by Susan Hovorka) “In most cases the compression needed to make the CO2 dense for transportation is sufficient for injection.” (From Peletiri et al.37) – “Typically, CO2 pipeline operating pressures range from 10 to 15 MPa and temperatures from 15 to 30°C or 8.5 to 15 MPa and 13 to 44°C. Stipulating minimum pipeline pressure above 7.38 MPa, the critical pressure of CO2, ensures that the CO2 fluid remains in the supercritical state.”

54. Are there special considerations for Closed Loop EOR from subservice, materials, connections, cementing, etc.?

A. (Answered by Susan Hovorka) “EOR is a closed loop system as operated commercially today. It requires a fluid processing plant to separate oil, water, and CO2, and then to clean and recompress CO2 for reinjection.”

55. Where is the insurance market for storage facilities?

A. There currently is no insurance market for CO2 storage facilities.

56. Has it been observed Joule-T related low-temperature integrity events in EOR applications?

A. (Answered by Susan Hovorka) “Expansion and cooling is a CO2 property. To inject CO2 requires a pressure drop. Engineering to manage cooling and avoid unwanted icing is needed.”

57. What are the limitations / best opportunities for CO2 EOR versus the other types of EOR (N2, water, etc). Is it essentially a question of field maturity?

A. EOR is a reservoir engineering problem unique to each oil field. The best fluid(s) to use for primary, secondary, or tertiary oil recovery depends on multiple factors including reservoir pressures, temperatures, and oil properties. The majority of studies around the world have found that a lack of CO2 supply is the limiting factor to deploying CO2-EOR.

58. What are the differences technically and economically to comply with CA LCFS (California Low Carbon Fuel Standard) vs. 45Q for geologic storage?

A. (Answered by Susan Hovorka) “The technical requirements are similar. The LCSF is more specified in detail and requires longer monitoring

101 QUESTIONS AND 101 ANSWERS FROM THE CCS 101 WEBINAR SERIES18

post injection. Economically, the LCFS credits trade for a much higher value (over $180/tCO2 in early July) whereas the value of the 45Q tax credit is currently $50/tCO2.” Read the Institute’s brief that discusses the LCFS38 and our Insight that discusses 45Q39.”

59. Are there key differences in technical/engineering aspects if we were to look at basalt or offshore storage instead?

A. Each storage operation will be different, no matter the geological or geographical terrane. One difference for basalt storage is CO2 can be injected at shallower depths. Instead of injecting at depths >800m, the CarbFix Project in Iceland is able to inject at shallow depths because the CO2 is dissolved in water before injection, rather than the conventional method which compresses pure CO2 to a higher-pressure supercritical phase (which requires deeper, higher pressure reservoirs for storage). A second difference is the primary storage mechanism is different than in conventional (typically sandstone) reservoirs. In basalt reservoirs, the primary storage mechanism is mineral carbonation, which occurs by a rapid chemical reaction of the dissolved CO2 with the unique, highly reactive basalt mineralogy to form stable, permanently stored carbonate minerals.

60. Does the use of old gas reservoirs carries a significant well integrity risk from old producing wells?

A. Old wells present the only real risk of CO2 storage to the atmosphere in a well-regulated environment. A paper published in Nature Communications by Alcade et al. 2018 (https://www.nature.com/articles/s41467-018-04423-1), addressed the chances of leakage. In a well-regulated industry, there is a 50% probability that more than 98% of the injected CO2 will remain trapped in the subsurface over 10,000 years. When you break down those numbers, it is 0.01% per year. Basically, minimal risk of leakage. In the paper, under modelled scenarios, the main pathway was through unknown abandoned wells.

61. How do you manage intermittent CO2 flow through the process of offshore sequestration, especially in stopping CO2 phase changes in the subsea segment?

A. Intermittent flow of CO2 has been shown to be both beneficial for CO2 storage, enabling the CO2 to “fill” more of the pore space. However, other studies have found that intermittent injection can cause issues in flow rates. As with any operation, each situation will be unique. There are tools and

techniques to monitor and verify flow rates and plume movement. Also, the prediction of the CO2 plume under different scenarios is not novel to science and engineering worlds.

62. Are saline aquifers more “porous” than other geological structures?

A. Every geological structure is different, some saline formations may be more porous than others; but the alternative is just as true. Importantly, the CO2 industry has tools and techniques to characterise the porosity of a geological structure.

63. Saline wells have also been proposed to store hydrogen. Saline domes close to high demand sites might therefore become very demanded. Would this compete with CO2 storage as this would also increase demand for salines domes near industrial sites?

A. The demand for pore space is one factor that will emerge for the CO2 storage industry in the coming decades. Generally, hydrogen would be stored in much shallower depths than CO2 and, more often than not, in depleted gas fields. These two factors enable hydrogen to be pumped and extracted more effectively in terms of cost and efficiency.

3.6 CCS Geography

64. What is the situation with CCS in Iceland regarding the use of salinated water in the CCS process?

A. Please visit the CarbFix website (https://www.carbfix.com/) for a nice summary of storage via mineral carbonation in basalts. Their process has some advantages over conventional CCS projects including shallower storage depths and lower cost materials in some cases. Their process is water-intensive, but recent research shows sea water could be effective alternative to fresh water for mineral carbonation in basalt reservoirs.

65. Are there plans for CCS facilities in Russia?

A. Recently, Rosneft and Gazprom Neft, two giant Russian oil producers signed agreements with Baker Hughes and Shell respectively to explore the possibility of either deploying a CCS at their joint oil ventures in Russia (in the case of the latter) or of constructing blue hydrogen facilities (H2 produced from steam methane reforming that captures the CO2 in the process)40. Note that articles like this are featured in our monthly newsletter which is free to all subscribers41.

101 QUESTIONS AND 101 ANSWERS FROM THE CCS 101 WEBINAR SERIES19

66. Are there underground storage basins along the coastline of India?

A. Yes. Several suitable storage basins exist on the both the west and east coast of India. The majority of the basins exist offshore, but some have onshore extensions. The Institute encourages you to look at our CO2RE database’s section on storage. The Institute has given India has a score of 48 (on a scale of 1-100) on a combination of its storage potential and how it has developed its resources.

67. What is the feasibility of Storage in China as they have quite a number of coal power plants likely to continue for a while?

A. China contains significant CO2 storage availability. There is great potential there for deploying more CCS facilities.

68. Which countries in Latin America are leading efforts to develop CCUS?

A. Brazil is the leading country for operational CCS in Latin America. Since 2011, the company Petrobas has been engaged in carbon capture and EOR storage off the coast of southern Brazil in the Santos Basin Pre-Salt. As of December, 2019, Petrobas had injected 14.4 million tonnes of CO2

42.

69. What factors are most important in deciding on a location for a CCS project? For direct air capture projects, are there benefits to some locations over others?

A. There are important factors to consider on the capture, storage and transportation side of the CCS equation. On the capture side, the costs must be favorable for installing point source capture equipment on either a power generation or an industrial facility. For example, running capture equipment on an ethanol biorefinery is cheaper than running capture equipment on a natural gas-fired power plant because the stream of captured CO2 is much purer and consequently easier to capture from the former. Then a developer must take into account whether their facility can take advantage of tax credits and other financial incentives to make their project feasible. For example, facilities have to be a certain size (capturing a certain volume of CO2) to be eligible to receive the 45Q tax credit. If the economics of a capture site are favorable, then a developer must take into account the accessibility of an underground storage site either for enhanced oil recovery (EOR) or secure geologic storage. Some underground storage locations are directly under the capture site (e.g., the Archer Daniels

Midland facility in Decatur, Illinois) and some are located not far away. If the capture site requires transport to a storage site, then the availability and cost of CO2 transport infrastructure is very important. A developer must ask: Are there CO2 pipelines readily available or shipping? How much will it cost to build a new pipeline if needed? Will there be other suppliers that can use the transport infrastructure? As you can see, there are a lot of factors that go into locating a CCS facility and please read our report about the costs of CCS43.

70. Are CCS projects happening in Italy?

A. At the moment, there are no projects happening in Italy. Between 2010-2012, there was a pilot-scale plant at the Brindisi power plant in southeastern Italy which tested a number of solvent technologies. Our CO2RE database keeps track of all CCS projects around the globe44.

71. What is total storage capacity of Mt Simon complex in MT CO2?

A. The Mt. Simon Sandstone storage complex has a potential sequestration capacity of 27 to 109 billion tonnes of CO2

45.

72. I hear a lot about Mt. Simon and Illinois, but what about south central Indiana just a little east? Same promising outlook as Illinois? Or other options as this is still in the Illinois Basin?

A. The Mt. Simon Sandstone storage complex underlies most of Illinois, Michigan, Iowa, Indiana, and Ohio46. Western Indiana is very well suited for underground storage in the Mt. Simon Sandstone47.

73. Is California a “no prospect” storage state because of seismicity?

A. No, California has more than 60 billion tonnes of CO2 storage capacity (enough to store at a rate of 60 Mtpa for the next 1000 years) mostly in the Central Valley, and there are currently 76 existing electricity and industrial facilities that are suitable candidates for CCS retrofit according to a report by Stanford University48. See our answer to question #35 in regards to the safety of underground storage zones around earthquakes.

74. Much of the CCUS focus seems to be oriented towards larger-scale infrastructure - important, to be sure, for the major impacts required. What is being done to encourage complementary, distributed CCUS solutions - that accelerate adoption and contribute to local economies?

101 QUESTIONS AND 101 ANSWERS FROM THE CCS 101 WEBINAR SERIES20

A. Our report, Technology Readiness and Costs of CCS49, discusses aspects of how to overcome this difficult challenge. Encouraging complementary, distributed CCUS solutions will largely be a function of strong policy often at the state and local (rather than federal) level. Several U.S. states such as North Dakota and Wyoming have passed legislation to encourage distributed CCUS solutions in their areas. At the federal level, strong policy priorities can also still encourage complementary, distributed CCUS that creates conditions for investment, including placing a value of CO2 emissions reductions.

3.7 CCS Policy

75. Are there gaps in government funding for CCS?

A. Our latest Thought Leadership Report, Unlocking Private Finance to Support CCS Investments, deals heavily with this subject50. In summary, many governments are actively supporting CCS but the overall capital requirement for widescale deployment far outstrips what they have been or are willing to provide. We are still in the early stages of CCS deployment, so the cost of CCS is relatively high. But if governments allocated more money for large-scale demonstrations, CO2 transport and storage infrastructure, and further innovation measures, it would help bring down the costs for CCS and further spur the growth of CCS projects. Further, governments have the important role of supporting commercial CCS projects so that they can raise debt financing. This is important because for CCS to meet deployment targets (such as those outlined in the IEA-SDS), most of the funding will have to come from the private sector.

76. Besides 45Q what supports governmental incentives exist for CCS around the world?

A. Forty-five countries around the world have a carbon price which covers 20% of global emissions. Those prices are incentives for CCS, especially in a country like Canada where prices are due to rise significantly . Canada also has a Low Carbon Fuel Standard (LCFS) which includes CCS as does the state of California. In the European Union (EU) and China51, there is an Emissions Trading System (ETS) that is an incentive for CCS and also an EU Innovation Fund which will provide millions to billions in funding for CCS projects. (See answers to questions 18 and 83.). Other incentives include an implicit value placed on the capture of CO2, for example, in Canada and emissions performance standard is what led to the development of the Boundary Dam project.

In Australia, CCS was a mandatory condition of the Gorgon project. In addition, the Australian government has a CCUS Development fund to spur projects52. Finally, many countries such as the U.S. are investing millions of dollars in R&D and demonstration programs to spur the deployment and growth of the technology.

77. Beside costs, what else is the key bottleneck in implementing CCUS? capture units? transportation/pipeline? or storage/utilization?

A. There are a number of key barriers to accelerating more CCS facilities. Lack of CO2 transportation and storage infrastructure is certainly a bottleneck; lack of stronger policies around a value on carbon and other financial incentives for spurring CCS is also a critical one; a lack of a legal and regulatory framework, especially in relation to long-term storage liability is a major barrier to investment in CCS; in the absence of a shared transport and storage network, industries/businesses not familiar with CCS may not be able to manage the cross-chain risk associated with the coordination of the CCS value chain; the lack of public awareness around how CCS can benefit climate, create jobs, sustain communities and provide a just transition for many communities is an equally critical barrier. Our Thought Leadership report, Policy Incentives To Enable Private Investment In CCS53, answers this question in greater depth.

78. Has there been any public opposition to onshore storage sites in the U.S. as in e.g. Germany?

A. So far, there has not been a lot of public opposition to onshore storage sites in the U.S. But there is a lot of uncertainty about who owns the pore space in the U.S. and the differences between surface v. mineral v. pore space ownership which complicates the matter. This is a current topic for policy development. The U.S. is also a lot less densely populated than most of Europe, and a significant amount of land is owned by the federal government. Underground storage also does not preclude surface use of the land. It is most important to keep in mind that onshore storage is safe and permanent. (See the Q&A for “CCS Storage” in Section 3.5) Education through the work of the Institute will be crucial to assuaging unfounded fears.

79. How are permitting and regulatory requirements a factor in the development and operation of these projects, and how do they compare between Europe and the U.S.?

A. The main permitting and regulatory requirements in the U.S. are centered on the storage portion of the CCS equation. In order to do non-EOR

101 QUESTIONS AND 101 ANSWERS FROM THE CCS 101 WEBINAR SERIES21

secure underground geologic storage in the U.S. a developer is required to get a Underground Injection Control (UIC) Class VI permit from the Environmental Protection Agency (EPA). Currently, this process will take at least 2 years if not more, though the EPA is trying to reduce this timeline to 18 months and some states (Wyoming and North Dakota) now have primacy to be able to issue the Class VI permits following EPA regulations. Using CO2 in EOR fields followed by storage requires a Class II UIC permit which takes half a year or less to obtain. There are also regulations required for building a pipeline to transport CO2 through to a storage site, but often pipelines can or will use existing pipeline corridors to transport which makes the permitting process easier. In the U.S. there is a lot more land than in Europe for onshore storage, whereas Europe must rely more on offshore storage. In addition, the U.S. is less densely populated and there is more federally owned land which makes it easier to do onshore projects.

80. How does the LCFS (Low Carbon Fuel Standard) help DAC (Direct Air Capture) economics?

A. Read our report, which dives into the intricacies of the LCFS54, but in summary if CO2 captured from a DAC facility can be converted into a fuel that is then sold on the California market, the net zero fuel will generate credits currently worth nearly $200/tonne of CO2. In order to take advantage of the LCFS, however, this DAC to fuels pathway must be used.

81. Is CCS just a diversion? Should we be focusing on other climate technologies with more promise?

A. CCS is most certainly not a diversion. It is a powerful climate change technology that is vital to use to help the world reach mid-century climate goals. The scientific consensus among researchers and modelers is that it will be almost impossible to reach net-zero emissions by midcentury without a significant scale up of CCS55.

101 QUESTIONS AND 101 ANSWERS FROM THE CCS 101 WEBINAR SERIES22

82. At some point, if climate change is severe enough, will we have to do CCS at whatever the cost?

A. A significant amount of CCS is already being used around the world56. It is one of the best tools we have available to prevent climate change from becoming too severe. We cannot speculate on future scenarios, but we advocate for strong proactive not reactive policies for CCS.

83. With the Emissions Trading System (ETS) prices bound to increase, is there any further need for state support in Europe?

A. The EU ETS covers 40% of emissions in the EU. Most CCS applications are under the EU ETS and can benefit from its carbon price, with the notable exception of BECCS (incl waste-to-energy) and DACCS. The expected rise of the carbon price will increase the likelihood of creating a business case for the more expensive CCS applications in industry. The European Commission has proposed Carbon Contracts for Difference in their EU ETS revision which is another tool that could help bridge the gap between the carbon price and necessary investments in the coming years. Further, the European Commission is currently working towards developing a carbon removal certificate, which will incentivise nature based solutions as well as negative emissions technologies such as DAC and BECCS. Given the long lead times in developing CCS projects, and the need to get started as soon as possible, the state support will remain a much needed element until the business cases emerge.

84. Are project economics in part dependent on carbon reduction credits becoming more developed and widespread - i.e. a price on carbon?

A. (Answered by Matt Vining) “Specifically no (for the Navigator Energy Project). The project is not directly participating in the end-market benefits (45Q or LCFS), however, those are highly impactful for our customers and appreciation in the value and the accessibility of those markets directly correlates to the addressable market for CCS projects.” (From the Institute) Stronger policies including a strong price on carbon will accelerate the deployment of more CCS facilities.

85. If I am correct, there is no legal basis (regulation) today, allowing for export of CO2 from other countries to Norway (London Protocol). When is it to be expected that export from one to another country is allowed for?

A. A 2019 decision by the Parties to the London Protocol, an international agreement governing the dumping of wastes in the marine environment, finally removed a significant barrier to the transboundary movement of CO2. Project proponents will now be able to avail themselves of the provisions of an earlier 2009 amendment to the Protocol, which provided a mechanism for enabling transboundary shipments of CO2 for the purposes of geological storage. It is important to note, however, that the ability to use these new provisions will depend upon national governments putting in place the necessary international agreements.

86. When will the Energy Act of 2020 authorized a lot of new money for CCS. When will that be appropriated?

A. Congress must pass yearly appropriations to keep the government funded, and that process usually occurs in the North American fall of each year (at the end of the U.S. fiscal year – 30 September). Among the parts of the government receiving these yearly appropriations are the CCS RD&D program in the Department of Energy. For the past few years, yearly appropriations for CCS have been ~$250million (USD). The Energy Act significantly increased the amount of dollars that Congress could spend on CCS, and some of this money can be spent in other ways than just yearly appropriations, e.g., in a large infrastructure bill. It is up to the U.S. Congress and the President to determine how much of the Energy Act’s $6.72 billion authorization on CCS.

87. How is the DOE promoting CCS markets?

A. The DOE has financed more CCS RD&D (including large-scale commercial demonstration projects still operating today) than any other government in the world. They spend over $200 million USD/year in addition to billions more on special appropriations. The money that the DOE spends is aimed at developing tools that will be used by multiple stakeholders to develop a CCS industry. For example, the DOE’s Carbon SAFE program looks to develop large storage sites that can form as hubs and clusters for multiple projects. The same is true for R&D focused on CCS technologies that can benefit multiple stakeholders in industrial and power generation. In addition, they also facilitate permitting and regulation to facilitate the CCS market. In this way, the DOE does a lot to promote CCS markets.

101 QUESTIONS AND 101 ANSWERS FROM THE CCS 101 WEBINAR SERIES23

88. What is the general policy with regard to presently operating coal-fired power plants in terms of DOE participation in adding CCS technology?

A. The DOE has funded a considerable amount of CCS RD&D on coal-fired power plants. We encourage you to examine the DOE’s website to see more about their research agenda57.

89. The MD Energy Administration is look at the Warrior Run coal-fired power plant in Western MD. Currently, the facility captures about 5% of the CO2 and they sell it to the food and beverage industry. Could you provide us with you contact information in order to walk us through the protocols for funding at DOE?

A. Please visit our website’s Multimedia Library to view our 26 March webinar and a PDF of the presentation: “Opportunities in CCS: Finding Government Funding and Business Partners58.” There are lots of resources that will help you navigate funding at DOE.

90. I might have missed this, but about how much $$$ will the DOE/government put this year towards CCS? By how much will this increase in the coming years, if any?

A. Congress appropriated about $250 million this year (FY2021) for CCS activities59. We cannot speculate how much Congress will increase funding in coming years.

91. What is the Scale Act?

A. The SCALE Act stands for the Storing CO2 and Lowering Emissions Act and was introduced by a bipartisan group of U.S. Senators and Representatives in March, 2021. It incentivises the build-out of CO2 transport and storage infrastructure60.

92. This question is regarding the “organisation” of CO2 Transport and Storage. As the UK favors a regulated asset base (potentially operated by a new group of National Grid) with regulated tariffs, offering service on a non-discriment basis, other countries seem to follow more a fully privately managed route (except the initial funding). What route do you think provides more advantages?

A. The regulated asset base (RAB) model enables shared transportation and storage networks. These are essential for managing the cross-chain risk, which is highest in a single source, single sink model. The RAB achieves this by regulating the cost of transport and storage so

that it is affordable and relatively predictable. At the same time, it also makes it possible for a transport and storage operator to service multiple capture facilities without having to face the high capital cost of oversizing pipelines without a corresponding revenue stream during the early stages of operation. The fully privatised model may work for some regions and industries, but without a regulation on tariffs, this can lead to natural monopolies that may disadvantage capture plant operators (by increasing their costs).

93. What are the names of the current bills in Congress that deal with carbon capture?

A. There are seven bipartisan bills that deal with carbon capture currently introduced in the U.S. Congress: Accelerating Carbon Capture and Extending Secure Storage (ACCESS) 45Q Act, CCUS Tax Credits Amendments Act, Carbon Capture Modernization Act, Storing CO2 and Lowering Emissions (SCALE) Act, Financing Our Energy Future Act, Coordinated Action to Capture Harmful Emissions (CATCH) Act, Carbon Capture Improvement Act61.

94. Would you share more information on how Environmental Justice should be incorporated into CCS projects. Is the goal to locate more projects in these communities?

A. Environmental justice or a “just transition” is a very important component of accelerating the deployment of CCS. Every time a CCS facility is constructed it reduces not only CO2, but also NOx and other harmful gases that destroy the environment and burden communities. A just transition is one of the Institute’s key messages: “CCS facilitates a just transition by allowing existing industries to transform to low carbon opportunities and make sustained contributions to local economies while moving toward net-zero62.”

95. When the 45Q tax credit ramps down and no longer provides this revenue stream, what do the panelists see as the most promising way forward to ensure that CCS plants do not shut down due to market forces, such as what happened with Petra Nova this summer?

A. Without supportive policies that address the CO2 emissions externality, CCS facilities will not be deployed at scale. What we have seen in the past is that commercial arrangements (sale of CO2 for EOR) can provide enough incentive for investments in some CCS projects, but not at the scale required to meet emissions reduction targets. If the 45Q tax credit ramps down, other mechanisms will have to

101 QUESTIONS AND 101 ANSWERS FROM THE CCS 101 WEBINAR SERIES24

be introduced. For example, the broadening of the LCFS across multiple states could help to support deployment in refineries and DAC. But there are other policies and mechanisms that could be effective across other sectors e.g. EPS, carbon tax, ETS.

96. Just curious about the main differences between the additional state policies? I am familiar with CA, but not sure about the other.

A. The main difference between state policies for CCS is their generation and implementation of rules and regulations for transport and storage of CO2. The ability of states to implement their own EPA-sanctioned Class VI well primacy (as is the case in North Dakota and Wyoming) will enable these states to permit CCS projects more quickly. Other states are looking to achieve this primacy. In addition, CCS is present in some state’s allowable decarbonisation strategies, e.g., Virginia allows CCS to qualify in its Clean Energy Standards.

97. What can this community do to help build local stakeholder support for deployment in communities where projects will be located. This could be a significant challenge for larger projects?

A. Reach out to your Member of Congress and/or other local elected officials to tell them that you support carbon capture and why. Tell them that it is important for your community to have a CCS facility. Do the same with community planning organisations. A significant barrier to the acceleration of CCS is an overall lack of awareness by the general public about CCS. Any way that you can help to educate more people to the climate and economic benefits of CCS, the higher the likelihood that the technology will be deployed in your community.

98. One of the presentations had a news snippet which described CCUS as an “unpopular technology” in Germany. Can the panelists comment on public opinion/skepticism about CCUS around the world, and what potential roadblock this presents?

A. The main challenge is that the vast majority of the general public is unaware that the underground storage of CO2 is permanent and safe and that CCS is one of the best tools to reach mid-century emissions reductions targets. Scientists are clear that we have almost no chance of decarbonising fully without CCS. Education is crucial, and the work of the Institute can help dispel common misconceptions about CCS.

99. Is S.986 same as Energy Act 2020?

A. No, S. 986 stands for the Carbon Capture, Utilization, and Storage Tax Credits Amendments Act introduced by Sen. Tina Smith on 25 March, 202163. Read more about this bill in the Institute’s brief64.

3.8 Carbon Utilisation

100. Can the captured CO2 be utilised to make chemicals or polymers?