Embed Size (px)

Citation preview

Jul-00 Bank of IsraelForeign Currency

Dept.

Active Risk Management Framework

Zvi Wiener Bank of Israel slide 2

Major risksmanaged by the department

Measurable

• currency risk

• interest rate risk

• some credit risk

Hardly Measurable

• operational risk

• liquidity risk

• some credit risk

Zvi Wiener Bank of Israel slide 3

Currently used methods

• benchmark as a starting point

• limits on position

• limits on counterparty

• other limits

Zvi Wiener Bank of Israel slide 4

Proposed Scheme

Three layers:

1. Global (yearly) stop loss

2. Dynamic VaR bounds

3. Limits to non-measurable risk components

(credit, liquidity, etc.)

Zvi Wiener Bank of Israel slide 5

Global (yearly) stop loss

In order to avoid a big loss we should introduce a global

stop loss (like 30-40bp).

As soon as the portfolio approaches the stop loss, we

should decrease VaR limits for each desk, so that they

become zero as soon as the stop loss is reached.

Zvi Wiener Bank of Israel slide 6

Dynamic VaR bounds

Each desk will receive its weekly VaR that can be used for risk taking (like 3-5 bp initially).

This VaR can be used by each desk (or temporarily borrowed from another desk).

If at some time moment VaR limit is exceeded, the manager must return to the permitted VaR during one day (or get a special permission).

See example below.

Zvi Wiener Bank of Israel slide 7

Reporting and responsibility

• investment committee

• desk managers

• risk manager

Zvi Wiener Bank of Israel slide 8

Investment committee is responsible for

• setting the yearly stop loss limit

• setting VaR limits for each desk weekly

• supervising the desk managers

(but not interfering their decisions too much)

• supervising stress test results (?)

Zvi Wiener Bank of Israel slide 9

Desk manager is responsible for

• keeping the risk under his VaR limit

• returning to the limit if exceeded

• reporting to the investment committee on

• his current VaR and its components

• cases of overexposure and how it was handled

• reasons for the current exposure (?)

Zvi Wiener Bank of Israel slide 10

Risk manager is responsible for

• supporting and developing the VaR program

• measuring and reporting VaR of the whole

portfolio

• communicating to desk managers and investment

committee on diversification among desks

• backtesting, stress test

Zvi Wiener Bank of Israel slide 11

VaR and stop-loss take-profitsVaR can NOT replace the technique of setting stop loss and take profit limits.

However VaR can answer the following questions: what is the current probability that the stop loss (take profit) order will be met during some time interval, or to give the probability distribution over a specified time horizon.

Setting stop loss orders can reduce VaR.

Zvi Wiener Bank of Israel slide 12

VaR and stop-loss take-profits

P&L

1 day

1 week

Zvi Wiener Bank of Israel slide 13

Advantages

• This language of risk is used worldwide

• Uniformity of different risks

• More freedom to desk managers in risk allocation

• More transparency on current risks and potential

losses

• Cross time and cross asset comparison

Zvi Wiener Bank of Israel slide 14

Example (Tal, Zvi)

Assume that the short dollar benchmark has neutral duration of T=6 months.

Manager has VaR limit of 3 bp. and he has to make two decisions:

a – % of assets kept in spread products

q – duration mismatch

we assume that all instruments (both treasuries and spread) have the same duration T+q months.

Zvi Wiener Bank of Israel slide 15

q - durationmismatch

Contour Levels of VaR (static)

0 0.2 0.4 0.6 0.8 1

-6

-4

-2

0

2

4

6

a (% of spread)

Zvi Wiener Bank of Israel slide 16

0 0.2 0.4 0.6 0.8 1

-6

-4

-2

0

2

4

6

q - durationmismatch

a (% of spread)

position

VaR=2 bp

VaR=3 bp

Zvi Wiener Bank of Israel slide 17

0 0.2 0.4 0.6 0.8 1

-6

-4

-2

0

2

4

6

q - durationmismatch

a (% of spread)

In order to reducerisk one can increase duration(in this case).

Zvi Wiener Bank of Israel slide 18

0 0.2 0.4 0.6 0.8 1

-6

-4

-2

0

2

4

6

What we can do using limits

VaR = 6 bp

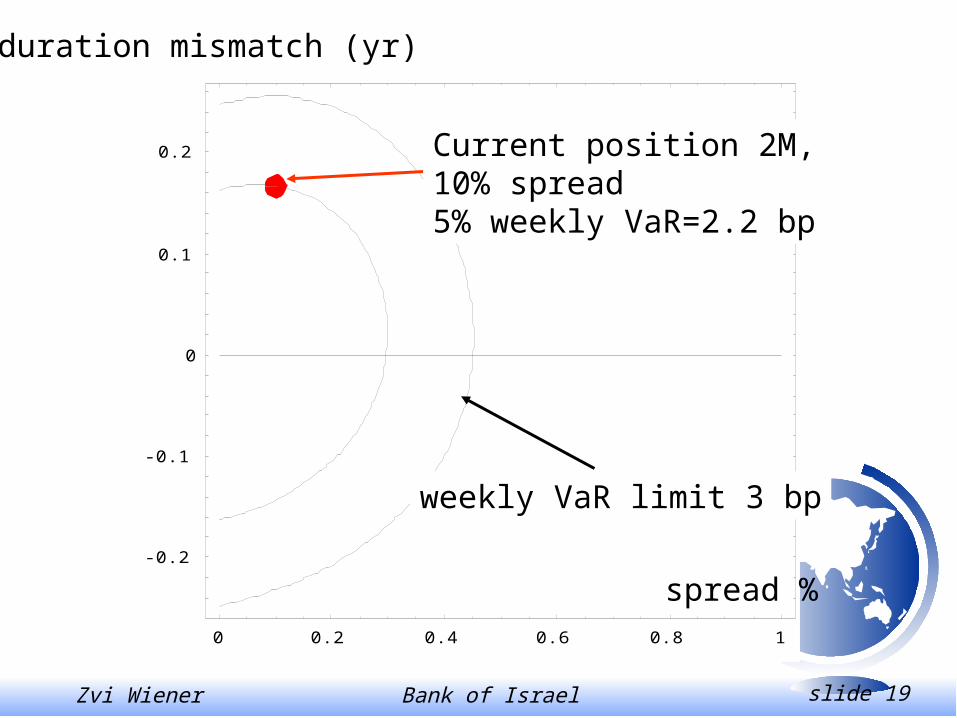

Zvi Wiener Bank of Israel slide 19

0 0.2 0.4 0.6 0.8 1

-0.2

-0.1

0

0.1

0.2

spread %

duration mismatch (yr)

Current position 2M,10% spread5% weekly VaR=2.2 bp

weekly VaR limit 3 bp

Zvi Wiener Bank of Israel slide 20

What should be done

• a simple VaR measuring tool at trading desks

professional software (RMG or other)

• reporting in terms of VaR

• to get used to this new language

• to build a historical data set

• backtest

• stress test library

Zvi Wiener Bank of Israel slide 21

Proposed Scheme

Three layers:

1. Global (yearly) stop loss (30-40 bp.)

2. Dynamic VaR bounds (initially 3-5 bp.)

3. Old limits to non-measurable components

(credit, liquidity, etc.)