Embed Size (px)

Citation preview

Indian

Journal of Commerce and

Management

Volume 2 Issue 3 December 2014

Indexed in

Copyright © Indian Journal of Commerce and Management

No portion of the material published in the Indian Journal of Commerce and Management should be reproduced in any way form without the written permission of the editor.

Disclaimer

The views expressed by the authors do not necessarily represent those of the editor or publisher, or the management of IJOCAM. Though every care has been taken to avoid errors,

this journal is being published on the condition and understanding that all the information provided herein is merely for reference and must not take as having authority of or binding

in any way on the authors, editor and publishers who do not owe any responsibility for any damage or loss to any person, for the result of any action taken on the basis of this work.

The publisher shall be obliged if mistakes are brought to their notice.

Editor In Chief

Rama Bhadra Rao Maddu

Managing Editor

Dr.Jetti Pandu Ranga Rao

Executive Editor

R. Srinivasa Rao

Honorary Associate Editor

Dr. D. Thiruvengala Chary

Editorial Advisory Board

Prof. G. Kameswara rao,

Ph.d, (iit mad)

Rtd., professor of cbit, hyderabad

Dr. P. Veehraiah,

Professor, pss central institute of

ocational education, ncert, 131,

sone-ii, madya pradesh, bhopal-

462011

Dr. A. Narasimharao,

professor in commerce and

business management

Andhra university, ap

Prof. G.v.chalam

M.com., ll.m., m.b.a., ph.d.

dean, college development council

Department of commerce &

business administration

Acharya nagarjuna university

nagarjuna nagar - 522 510, andhra

pradesh, india.

Dr.k c biswal,

North estren hill university ,

Tura campus ,

Department of management ,

Tura - 794002,

Chandmari post ,

Megalaya

Mobile: +91 08414077901

Gouher ahmed,

ph.d; pmp

International management

consultant, north america, middle

east & south asia

Associate professor

Al ghurair university |

po box 37374 dubai | uae.

Tel: (+971 4) 4200223 ext: 323 |

fax: (+971 4) 4200224

Mobile: (+971 50) 836 7165

Dr. K. Kanaka raju,

andhra university pg centre,

tadepallygudem

e-mail:

mobile: 0091 8125387145

Dr. Janaki rao rajana assistant professor,

department of social work

adikavi nannaya university,

rajahmundry – ap.

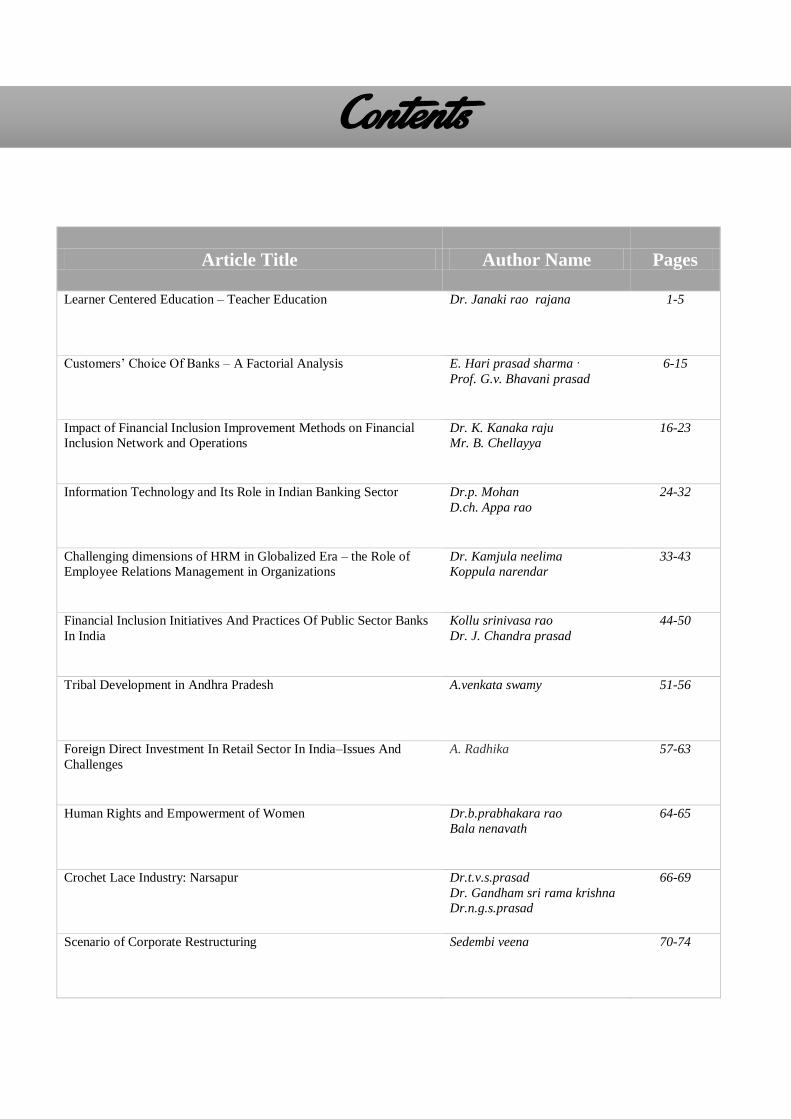

Contents

Article Title Author Name Pages

Learner Centered Education – Teacher Education Dr. Janaki rao rajana

1-5

Customers’ Choice Of Banks – A Factorial Analysis E. Hari prasad sharma ,

Prof. G.v. Bhavani prasad

6-15

Impact of Financial Inclusion Improvement Methods on Financial

Inclusion Network and Operations

Dr. K. Kanaka raju

Mr. B. Chellayya

16-23

Information Technology and Its Role in Indian Banking Sector Dr.p. Mohan

D.ch. Appa rao

24-32

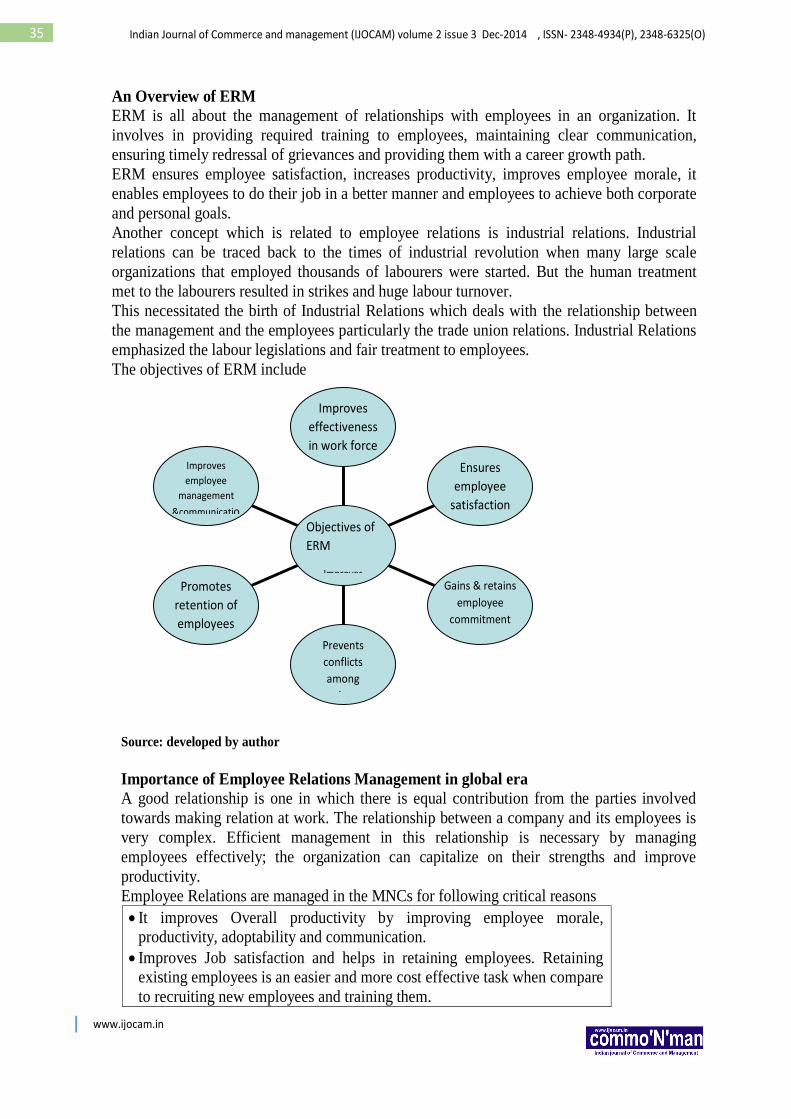

Challenging dimensions of HRM in Globalized Era – the Role of

Employee Relations Management in Organizations

Dr. Kamjula neelima

Koppula narendar

33-43

Financial Inclusion Initiatives And Practices Of Public Sector Banks

In India

Kollu srinivasa rao

Dr. J. Chandra prasad

44-50

Tribal Development in Andhra Pradesh A.venkata swamy

51-56

Foreign Direct Investment In Retail Sector In India–Issues And

Challenges

A. Radhika

57-63

Human Rights and Empowerment of Women Dr.b.prabhakara rao

Bala nenavath

64-65

Crochet Lace Industry: Narsapur Dr.t.v.s.prasad

Dr. Gandham sri rama krishna

Dr.n.g.s.prasad

66-69

Scenario of Corporate Restructuring Sedembi veena

70-74

www.ijocam.in

1 Indian Journal of Commerce and management (IJOCAM) volume 2 issue 3 Dec-2014 , ISSN- 2348-4934(P), 2348-6325(O)

Learner Centered Education – Teacher Education

Dr. Janaki Rao Rajana

Assistant Professor, Department of Social Work

Adikavi Nannaya University, Rajahmundry – AP. 'Educated youth are the important a s s e t s of any nation. The whole

Process of

education is centered on them from elementary stage to higher stage of Education. A child is

influenced by many factors which surround him. One of the major socializing agents which

contribute a potent source of contact on him is his immediate family which one's personality is

shaped and character enlivened. The training provided at home is more practical than

theoretical. Children who are monitored more carefully by their parents tend to do better than

their peers. Learning environment is one in which resources and supports abound for learners

for the active creation of knowledge and construction of their own meaning. Authentic

assessments, when properly implernented are critical strategies for enabling people to

properly demonstrate learning. In this scenario the constructivist theory of learning and

knowledge will support teachers in creating a community of learners.

Every civilized society aims to educate every one of its children. This sworn commitment however should not be about just enacting well meaning legislations and

amendments to the constitution. Good intentions are a starting point but ultimately it is the

result that matters. We must look for creative and innovative ways of fulfilling our promise of

quality education to the next generation

The role of a teacher as an interventionist in imparting, reviving, re-designing and remodeling values by means of crystallization of facts and realities in terms of

life and reality is yet to be undertaken. The teachers alone can pave and prepare

avenues of learning by means of self-enquiry, self-appreciation and self-evaluation.

Education should pave the way for enhanced awareness, greater openness, ability and

courage to question, and toughness to search for solutions

What is learner centered education?

Learner cen te redness is a construct a n d philosophy b a s e d on the learner-

centered psychological principles. The perspective that couples a focus on individual

learners their heredity, experiences, perspectives, backgrounds, talents, interests,

capacities, and needs along with another focus on learning. The best available

knowledge about learning and how it occurs and about teaching practices, that are most

effective in promoting the highest levels of motivation, learning, and achievement for

all learners. This dual focus then informs and drives educational decision-making.

"Learner centered education can be viewed as a fundamental change in orientation from the traditional "content-centric' teaching and learning format in most

K-20 classrooms. The transition can be characterized along five dimensions" -

Weimer,[2002].

www.ijocam.in

2 Indian Journal of Commerce and management (IJOCAM) volume 2 issue 3 Dec-2014 , ISSN- 2348-4934(P), 2348-6325(O)

"Learner Centered Education-Teacher Education"

Teacher-learner autonomy, by analogy with previous definitions of learner

autonomy, might be defined as the ability to develop appropriate skills, knowledge and attitudes

for oneself as a teacher, in cooperation with others

The learner is the beginning a n d the end point of the learning process. The learner

needs the focus of the course and he is in control of the learning experience. They are the

active partners i n the learning process. Learner centeredness is grounded i n

constructivist learning theory. Can t h i s h a p p e n in the case of teacher education

too. Of course is appears to be difficult i f not impossible.

But the educational administrator's now-a-days think, believe, and plan the whole process of teacher education in a centralized manner believing the way they

themselves did gain that area of knowledge holds good for this day too. But can we

say that is the reality? It does not seem to be. There are plans and plans, activities and

activities added. Record work, project work, community services and so on are added, edited,

cut and pasted. However, the general quality of teacher education does not seem to be going in

any way a forward and positive manner. How then the future teacher can influence children in

their endeavor to learn and develop and then apply them for sustainable development of

the nation they belong to. The answer to us seems to the ‘CONSTUCTIVISTIC’ approach.

What is constructivism?

Constructivism is a theory of how knowledge is created and how learning occurs. This

theory suggests that knowledge can in no way be treated as a liquid that can be poured

from the heads teacher to a student's head. As teachers or parents the best one can

do is to create environment that encourages children to construct their own knowledge and

understanding.

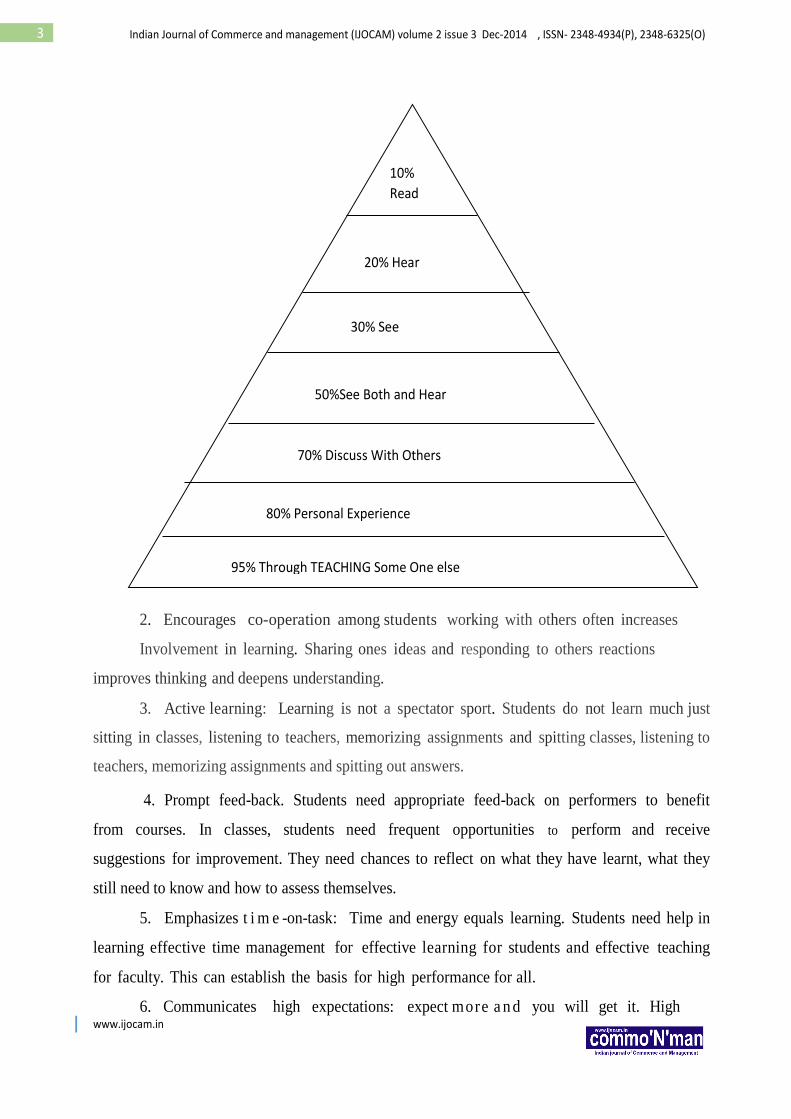

The original cone is attributed to Edgar Dale, 1949 and it indicates that we learn

best when we are involved in "Direct, Purposeful experiences"

Seven principles of good practice in undergraduate education have been

prepared by the Center for Learner Centered Education in the Arizona University,U.S.

Will these following good practices b e useful for us too in India? And for Teacher

Education? Why n o t we think, deliberate, prepare modules of it and experiment these

for the benefit of quality teacher education?

1. Student-faculty contact; frequent contact with faculty in and out of classes is the

most important factor in student motivation in involvement. Intellectual commitment encourages

them to think about their own values and future plans.

www.ijocam.in

3 Indian Journal of Commerce and management (IJOCAM) volume 2 issue 3 Dec-2014 , ISSN- 2348-4934(P), 2348-6325(O)

2. Encourages co-operation among students working with others often increases

Involvement in learning. Sharing ones ideas and responding to others reactions

improves thinking and deepens understanding.

3. Active learning: Learning is not a spectator sport. Students do not learn much just

sitting in classes, listening to teachers, memorizing assignments and spitting classes, listening to

teachers, memorizing assignments and spitting out answers.

4. Prompt feed-back. Students need appropriate feed-back on performers to benefit

from courses. In classes, students need frequent opportunities to perform and receive

suggestions for improvement. They need chances to reflect on what they have learnt, what they

still need to know and how to assess themselves.

5. Emphasizes t i m e -on-task: Time and energy equals learning. Students need help in

learning effective time management for effective learning for students and effective teaching

for faculty. This can establish the basis for high performance for all.

6. Communicates high expectations: expect more a n d you will get it. High

10%

Read

20% Hear

30% See

50%See Both and Hear

70% Discuss With Others

80% Personal Experience

95% Through TEACHING Some One else

www.ijocam.in

4 Indian Journal of Commerce and management (IJOCAM) volume 2 issue 3 Dec-2014 , ISSN- 2348-4934(P), 2348-6325(O)

Expectations are important for everyone. For poorly prepared, for those who are unwilling to

exert themselves and for the bright and well motivated. Teachers and institutions hold high

expectations for them and make extra efforts.

7. Respects diverse talents and ways of learning: students need the opportunity to

show their talents and learn in ways that work for them. Then they can be pushed to learn in new

ways that do not come so easily.

Recall, Comprehension, Application, Analysis, Synthesis and evaluation in one sense,

Bloom’s T a x o n o m y is upside-down. We remember information because we have worked

to use it in a meaningful way. Challenge a student to evaluate, and he will learn to synthesize,

analyze, apply, comprehend and utilize information. Much of the information he utilizes, he will

remember because of the context in which it was used. Challenge students to evaluate why an

apple falls from a tree and they will function in all classifications of Bloom's Taxonomy. Ifa

lesson is constructivist, it challenges students to apply each of these components of the

Taxonomy.

Teacher effectiveness is greatly dependant on teacher clientele. We often find

student-teacher to be more interested in practice than in theories in teaching. This

substantiates the point that the effectiveness of teaching and therefore the teachers

engaged in teaching are more concerned with practice than with

principles with teachers making through teacher education, a thriving proposition ..-.:- , .

both scientifically as-well-as psychologically.

Teacher education should therefore consider the following as essential features of teacher

effectiveness:

a) Proneness to development

b) Reciprocality c) Practicality

d) Contemporaneity e) Creativity

f) Aesthetic awareness

Teacher education, therefore, necessitates a re-orientation of the present poor environment

so that teachers become inspired in effective teaching. Admittedly, teacher education should pay

greater attention to cultivate creativity among teachers and teacher educators..

Suggestions: ,1-'\-.

1. The teachers as lifelong learners

www.ijocam.in

5 Indian Journal of Commerce and management (IJOCAM) volume 2 issue 3 Dec-2014 , ISSN- 2348-4934(P), 2348-6325(O)

4. Diversified teacher education courses- regional need based -~ .... _. f • '. ", ..::-

3. Frequent supervisory activities m o r e as a feedback exercises

4. The heads of the institution invite new trends, and innovative practices

5. Student teachers carrying out action research projects

6. Freedom to student teachers to prepare teaching strategies on their

own.

References:

1. http://www.abor.asu.ed.ul4_special_programs/lce/ugprinciples_lce.htm

(Arizona University _

USA)

2. http://ll}ettleweb.unimelb.edu.aulguide/principles.html

3. Melbourne University - Australia http.Zwww.learnercentereded.org/

4. Methods for Quality Education-Prof.K.K. Vijayan Nambiar.

www.ijocam.in

6 Indian Journal of Commerce and management (IJOCAM) volume 2 issue 3 Dec-2014 , ISSN- 2348-4934(P), 2348-6325(O)

Customers’ Choice Of Banks – A Factorial Analysis (A Study of Rural Bank Customers in Karimnagar District of Andhra Pradesh State in India)

E. HARI PRASAD SHARMA , Prof. G.V. BHAVANI PRASAD

Abstract:

Commercial Banking sector in India, after liberalization, had grown substantially in spite of its

social, political and economic problems. However, no study was made to find out the most

important factors that affect the customer a lot in selecting the bank. This study aims to determine

the most significant factors that rural customer thinks as important in his/her choice of bank.

Key Words: Commercial Banks, Public Sector Banks, Private Sector Banks, Rural Areas,

Influencing Factors.

Introduction:

Liberalization of Indian economy and introduction of financial sector reforms had changed the

financial system in general and banking system in particular. Many private and foreign banks are

entering into the Indian financial market and offering various innovative services to attract new

customers and to retain existing customers. This competition has a great challenge to all banking

institutions of all sizes. Customers are exposed to wider opportunities and in term lead to their focus

on value for their money. In this situation, (Sharma, 2010) the issue of how customers select their

banks has been given considerable attention by researchers. Exploring such information will help

banks to identify the appropriate marketing strategies needed to attract new customers and retain

existing ones.

Review of Literature

It is relevant to refer briefly to the previous studies and research in the related areas of the subject to

find out and to fill up the research gaps. The following are the some studies conducted by the

eminent authors and practitioners on the area of determinants of bank selection of a customer.

In Pakistan, (Saima, 2008), Another study in Pakistan, (AHMED*, 2008), In Tunisian (AZOUZI,

2009), (Kumar M, 2010), (Olawale Fatoki, 2011) In India, (VIRPARIA, 2013) a study made on

various selected factors and also analyzed as to which of these factors exercise the greatest,

moderate, and relatively lower influence as choice criteria in selection of a bank. 15 factors

identified, approximately in the order of their importance. General Group Impression as per the

Mean score technique was applied to elicit the results. According to the findings, based on the

empirical study, the three factors i.e. (1) Safety of Deposits (2) Security of Environment (3)

Cordiality of Staff exert the greatest influence, next six factors such as (1) Accuracy (2) Product

Packing (3) General Service Quality (4) Size and Strength (5) Advertisement and Publicity (6)

Friendship with Staff had the moderate importance and the rest six factors (1) Price and Service

Charges (2) Speed of Delivery (3) Peer Group Impression, (4) Face Lift, (5) Face lift (6) Proximity

had relatively lower influence in selection of a bank in India.

Need of the Study

Several studies have been made to investigate factors that affect customers’ choices in selecting a

bank. Among these studies include (Mokhlis S., 2010) who studied the determinants of bank

www.ijocam.in

7 Indian Journal of Commerce and management (IJOCAM) volume 2 issue 3 Dec-2014 , ISSN- 2348-4934(P), 2348-6325(O)

selection criterion in Malaysia considering undergraduate students; while (Mokhlis S. S. H., 2009)

made an attempt to analyze gender-based choice decisions for selection of banks. Correspondingly,

in Bahrain (Almossawi, 2001), a case of college students and in Greek (Mylonakis, 2007), a

research task of customer preferences in the home loans market were done. Other studies are also

undertaken in Europe (Bosnia & Herzegovina) by (Cicic M., 2004) on the issue of bank selection

criteria in line with customers’ preference: what, why and how customers choose a particular bank

to be served. Although such studies have contributed substantially to the literature on bank

selection, their findings may not be applicable to other countries like India due to differences in

social, cultural, economic, political and legal environments.

Objectives of the Study

The research paper aims at identifying factors influencing customers’ choice of a bank. The

following are the main objectives of the present study:

To identify the influencing factors that affect customers’ choice of banking services.

To rank the factors affecting the choice of bank.

Methodology

In this paper an attempt has been undertaken to carry out a descriptive study regarding influence of

various factors in selection of a bank.

Data Collection

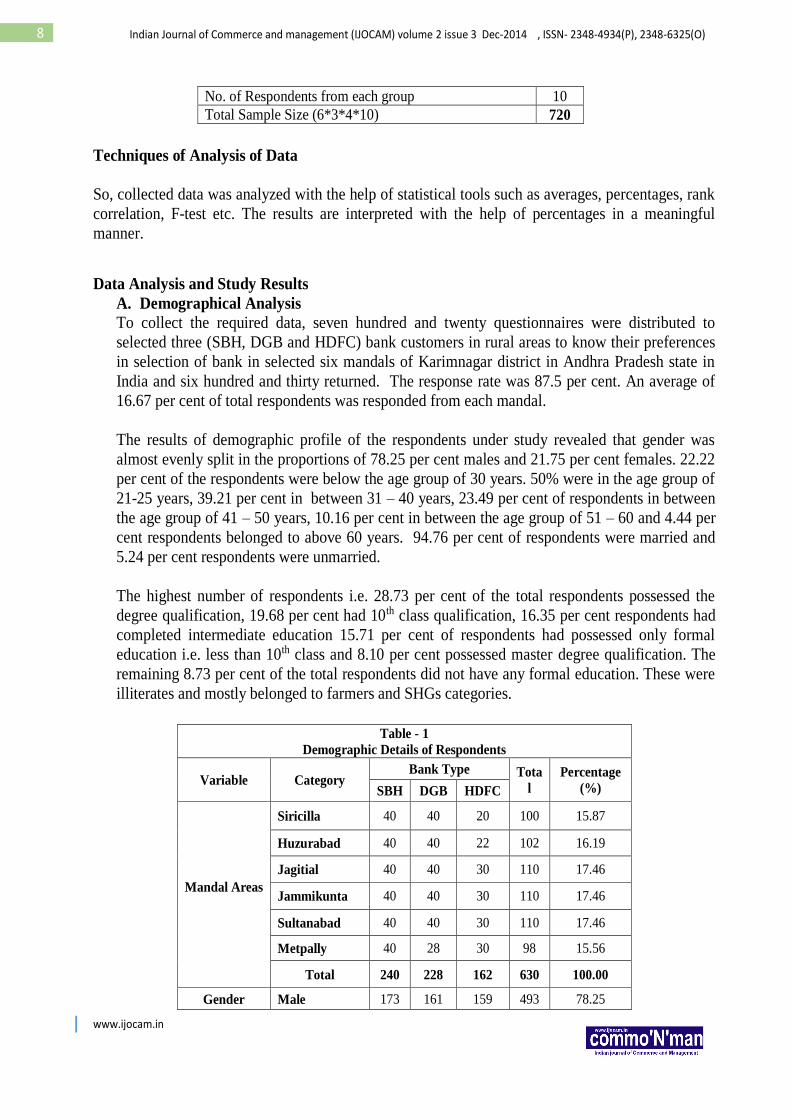

The study was conducted by taking three commercial banks, one from public sector (SBH), one

from private sector (HDFC) and one from Regional Rural Banks (RRBs).

The required data was collected from two sources namely Primary Data and Secondary Data.

Primary data was collected through structured questionnaire from the existing bank customers.

Secondary data was collected from the previous publications.

Sampling Unit

The sample unit consists of customers of the public sector, the private sector banks and RRBs of

rural areas in Karimnagar district of Andhra Pradesh in India. The respondents are farmers,

Employees, Business Persons and SHGs.

Size of the Sample

SAMPLE SIZE

Particulars No.

No. of Mandals Selected for the study (10% of the Total

57 Mandals in the District) 6

No. of Banks Selected (SBH, DGB & HDFC) 3

Target Groups (Farmers, Employees, Business People

and SHGs) 4

www.ijocam.in

8 Indian Journal of Commerce and management (IJOCAM) volume 2 issue 3 Dec-2014 , ISSN- 2348-4934(P), 2348-6325(O)

No. of Respondents from each group 10

Total Sample Size (6*3*4*10) 720

Techniques of Analysis of Data

So, collected data was analyzed with the help of statistical tools such as averages, percentages, rank

correlation, F-test etc. The results are interpreted with the help of percentages in a meaningful

manner.

Data Analysis and Study Results

A. Demographical Analysis

To collect the required data, seven hundred and twenty questionnaires were distributed to

selected three (SBH, DGB and HDFC) bank customers in rural areas to know their preferences

in selection of bank in selected six mandals of Karimnagar district in Andhra Pradesh state in

India and six hundred and thirty returned. The response rate was 87.5 per cent. An average of

16.67 per cent of total respondents was responded from each mandal.

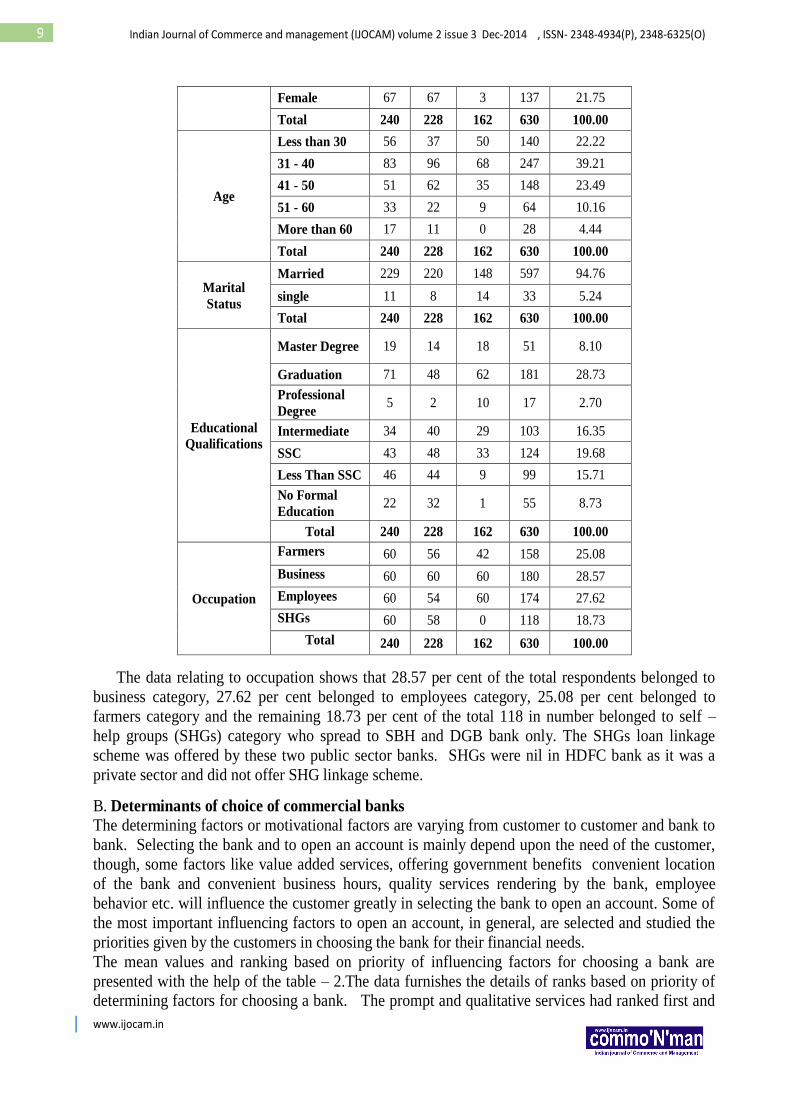

The results of demographic profile of the respondents under study revealed that gender was

almost evenly split in the proportions of 78.25 per cent males and 21.75 per cent females. 22.22

per cent of the respondents were below the age group of 30 years. 50% were in the age group of

21-25 years, 39.21 per cent in between 31 – 40 years, 23.49 per cent of respondents in between

the age group of 41 – 50 years, 10.16 per cent in between the age group of 51 – 60 and 4.44 per

cent respondents belonged to above 60 years. 94.76 per cent of respondents were married and

5.24 per cent respondents were unmarried.

The highest number of respondents i.e. 28.73 per cent of the total respondents possessed the

degree qualification, 19.68 per cent had 10th class qualification, 16.35 per cent respondents had

completed intermediate education 15.71 per cent of respondents had possessed only formal

education i.e. less than 10th class and 8.10 per cent possessed master degree qualification. The

remaining 8.73 per cent of the total respondents did not have any formal education. These were

illiterates and mostly belonged to farmers and SHGs categories.

Table - 1

Demographic Details of Respondents

Variable Category Bank Type Tota

l

Percentage

(%) SBH DGB HDFC

Mandal Areas

Siricilla 40 40 20 100 15.87

Huzurabad 40 40 22 102 16.19

Jagitial 40 40 30 110 17.46

Jammikunta 40 40 30 110 17.46

Sultanabad 40 40 30 110 17.46

Metpally 40 28 30 98 15.56

Total 240 228 162 630 100.00

Gender Male 173 161 159 493 78.25

www.ijocam.in

9 Indian Journal of Commerce and management (IJOCAM) volume 2 issue 3 Dec-2014 , ISSN- 2348-4934(P), 2348-6325(O)

The data relating to occupation shows that 28.57 per cent of the total respondents belonged to

business category, 27.62 per cent belonged to employees category, 25.08 per cent belonged to

farmers category and the remaining 18.73 per cent of the total 118 in number belonged to self –

help groups (SHGs) category who spread to SBH and DGB bank only. The SHGs loan linkage

scheme was offered by these two public sector banks. SHGs were nil in HDFC bank as it was a

private sector and did not offer SHG linkage scheme.

B. Determinants of choice of commercial banks The determining factors or motivational factors are varying from customer to customer and bank to

bank. Selecting the bank and to open an account is mainly depend upon the need of the customer,

though, some factors like value added services, offering government benefits convenient location

of the bank and convenient business hours, quality services rendering by the bank, employee

behavior etc. will influence the customer greatly in selecting the bank to open an account. Some of

the most important influencing factors to open an account, in general, are selected and studied the

priorities given by the customers in choosing the bank for their financial needs.

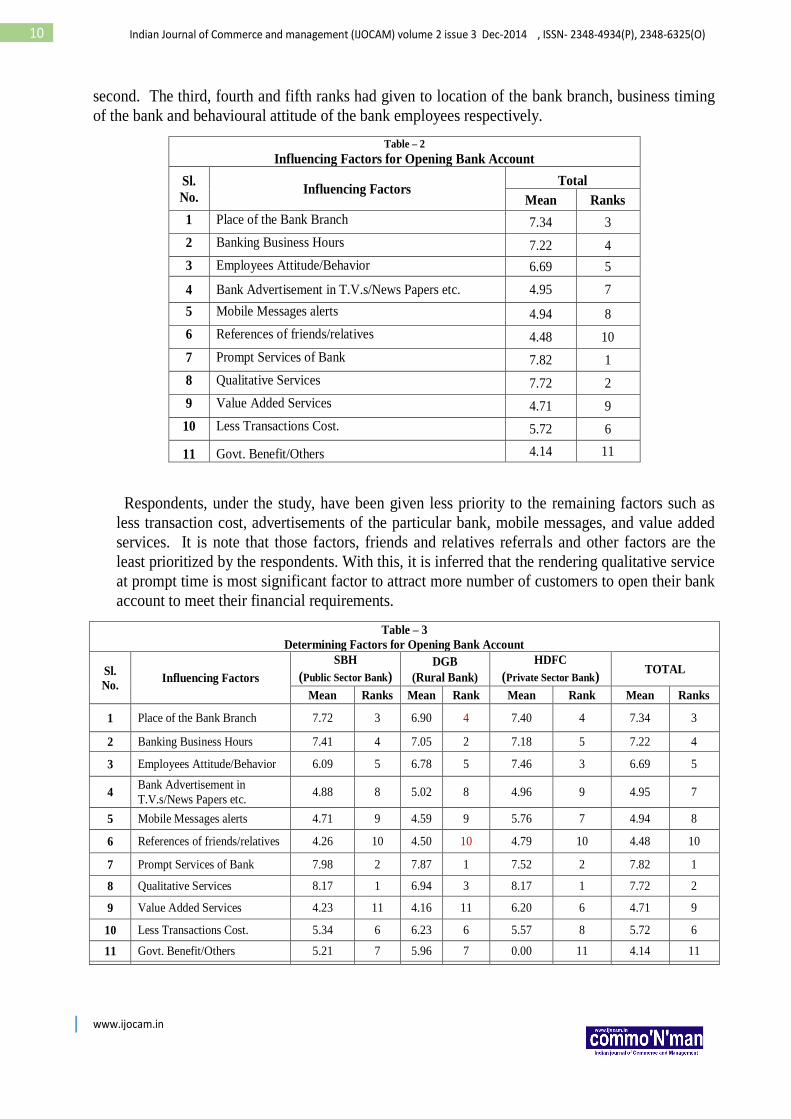

The mean values and ranking based on priority of influencing factors for choosing a bank are

presented with the help of the table – 2.The data furnishes the details of ranks based on priority of determining factors for choosing a bank. The prompt and qualitative services had ranked first and

Female 67 67 3 137 21.75

Total 240 228 162 630 100.00

Age

Less than 30 56 37 50 140 22.22

31 - 40 83 96 68 247 39.21

41 - 50 51 62 35 148 23.49

51 - 60 33 22 9 64 10.16

More than 60 17 11 0 28 4.44

Total 240 228 162 630 100.00

Marital

Status

Married 229 220 148 597 94.76

single 11 8 14 33 5.24

Total 240 228 162 630 100.00

Educational

Qualifications

Master Degree 19 14 18 51 8.10

Graduation 71 48 62 181 28.73

Professional

Degree 5 2 10 17 2.70

Intermediate 34 40 29 103 16.35

SSC 43 48 33 124 19.68

Less Than SSC 46 44 9 99 15.71

No Formal

Education 22 32 1 55 8.73

Total 240 228 162 630 100.00

Occupation

Farmers 60 56 42 158 25.08

Business 60 60 60 180 28.57

Employees 60 54 60 174 27.62

SHGs 60 58 0 118 18.73

Total 240 228 162 630 100.00

www.ijocam.in

10 Indian Journal of Commerce and management (IJOCAM) volume 2 issue 3 Dec-2014 , ISSN- 2348-4934(P), 2348-6325(O)

second. The third, fourth and fifth ranks had given to location of the bank branch, business timing

of the bank and behavioural attitude of the bank employees respectively.

Table – 2

Influencing Factors for Opening Bank Account

Sl.

No. Influencing Factors

Total

Mean Ranks

1 Place of the Bank Branch 7.34 3

2 Banking Business Hours 7.22 4

3 Employees Attitude/Behavior 6.69 5

4 Bank Advertisement in T.V.s/News Papers etc. 4.95 7

5 Mobile Messages alerts 4.94 8

6 References of friends/relatives 4.48 10

7 Prompt Services of Bank 7.82 1

8 Qualitative Services 7.72 2

9 Value Added Services 4.71 9

10 Less Transactions Cost. 5.72 6

11 Govt. Benefit/Others 4.14 11

Respondents, under the study, have been given less priority to the remaining factors such as

less transaction cost, advertisements of the particular bank, mobile messages, and value added

services. It is note that those factors, friends and relatives referrals and other factors are the

least prioritized by the respondents. With this, it is inferred that the rendering qualitative service

at prompt time is most significant factor to attract more number of customers to open their bank

account to meet their financial requirements.

Table – 3

Determining Factors for Opening Bank Account

Sl.

No. Influencing Factors

SBH

(Public Sector Bank) DGB

(Rural Bank)

HDFC

(Private Sector Bank) TOTAL

Mean Ranks Mean Rank Mean Rank Mean Ranks

1 Place of the Bank Branch 7.72 3 6.90 4 7.40 4 7.34 3

2 Banking Business Hours 7.41 4 7.05 2 7.18 5 7.22 4

3 Employees Attitude/Behavior 6.09 5 6.78 5 7.46 3 6.69 5

4 Bank Advertisement in

T.V.s/News Papers etc. 4.88 8 5.02 8 4.96 9 4.95 7

5 Mobile Messages alerts 4.71 9 4.59 9 5.76 7 4.94 8

6 References of friends/relatives 4.26 10 4.50 10 4.79 10 4.48 10

7 Prompt Services of Bank 7.98 2 7.87 1 7.52 2 7.82 1

8 Qualitative Services 8.17 1 6.94 3 8.17 1 7.72 2

9 Value Added Services 4.23 11 4.16 11 6.20 6 4.71 9

10 Less Transactions Cost. 5.34 6 6.23 6 5.57 8 5.72 6

11 Govt. Benefit/Others 5.21 7 5.96 7 0.00 11 4.14 11

www.ijocam.in

11 Indian Journal of Commerce and management (IJOCAM) volume 2 issue 3 Dec-2014 , ISSN- 2348-4934(P), 2348-6325(O)

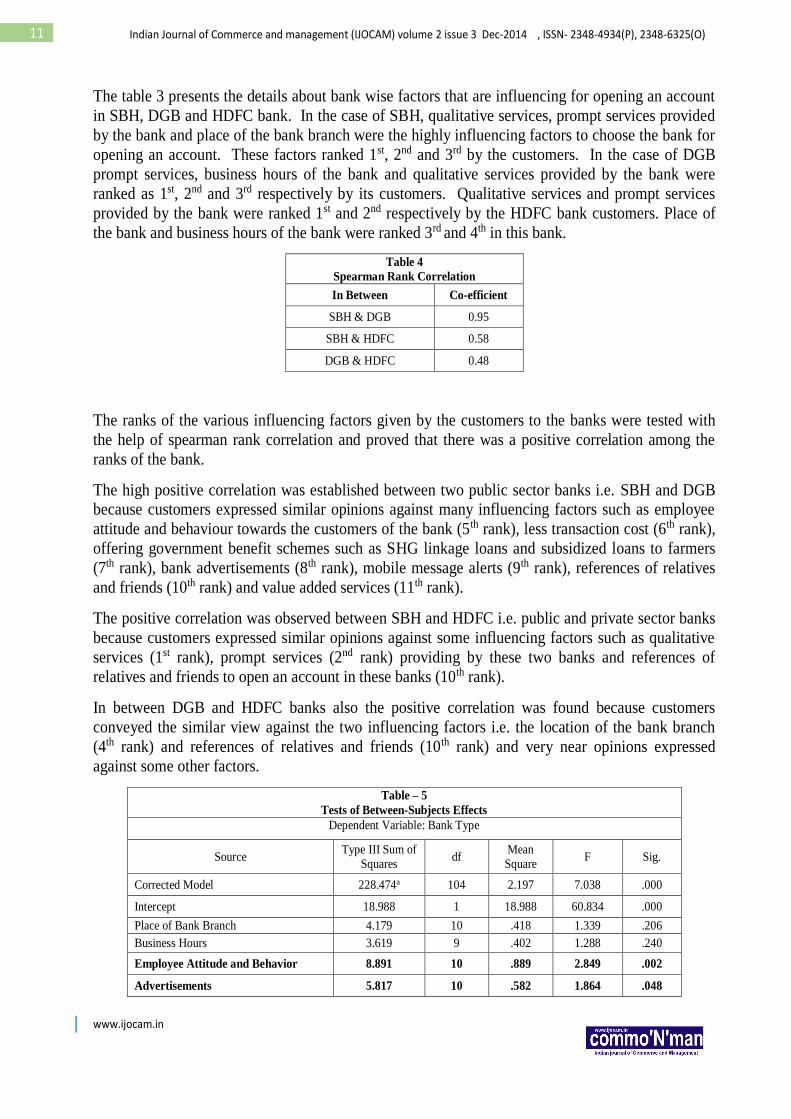

The table 3 presents the details about bank wise factors that are influencing for opening an account

in SBH, DGB and HDFC bank. In the case of SBH, qualitative services, prompt services provided

by the bank and place of the bank branch were the highly influencing factors to choose the bank for

opening an account. These factors ranked 1st, 2nd and 3rd by the customers. In the case of DGB

prompt services, business hours of the bank and qualitative services provided by the bank were

ranked as 1st, 2nd and 3rd respectively by its customers. Qualitative services and prompt services

provided by the bank were ranked 1st and 2nd respectively by the HDFC bank customers. Place of

the bank and business hours of the bank were ranked 3rd and 4th in this bank.

Table 4

Spearman Rank Correlation

In Between Co-efficient

SBH & DGB 0.95

SBH & HDFC 0.58

DGB & HDFC 0.48

The ranks of the various influencing factors given by the customers to the banks were tested with

the help of spearman rank correlation and proved that there was a positive correlation among the

ranks of the bank.

The high positive correlation was established between two public sector banks i.e. SBH and DGB because customers expressed similar opinions against many influencing factors such as employee

attitude and behaviour towards the customers of the bank (5th rank), less transaction cost (6th rank),

offering government benefit schemes such as SHG linkage loans and subsidized loans to farmers

(7th rank), bank advertisements (8th rank), mobile message alerts (9th rank), references of relatives

and friends (10th rank) and value added services (11th rank).

The positive correlation was observed between SBH and HDFC i.e. public and private sector banks

because customers expressed similar opinions against some influencing factors such as qualitative

services (1st rank), prompt services (2nd rank) providing by these two banks and references of

relatives and friends to open an account in these banks (10th rank).

In between DGB and HDFC banks also the positive correlation was found because customers

conveyed the similar view against the two influencing factors i.e. the location of the bank branch

(4th rank) and references of relatives and friends (10th rank) and very near opinions expressed

against some other factors.

Table – 5

Tests of Between-Subjects Effects

Dependent Variable: Bank Type

Source Type III Sum of

Squares df

Mean Square

F Sig.

Corrected Model 228.474a 104 2.197 7.038 .000

Intercept 18.988 1 18.988 60.834 .000

Place of Bank Branch 4.179 10 .418 1.339 .206

Business Hours 3.619 9 .402 1.288 .240

Employee Attitude and Behavior 8.891 10 .889 2.849 .002

Advertisements 5.817 10 .582 1.864 .048

www.ijocam.in

12 Indian Journal of Commerce and management (IJOCAM) volume 2 issue 3 Dec-2014 , ISSN- 2348-4934(P), 2348-6325(O)

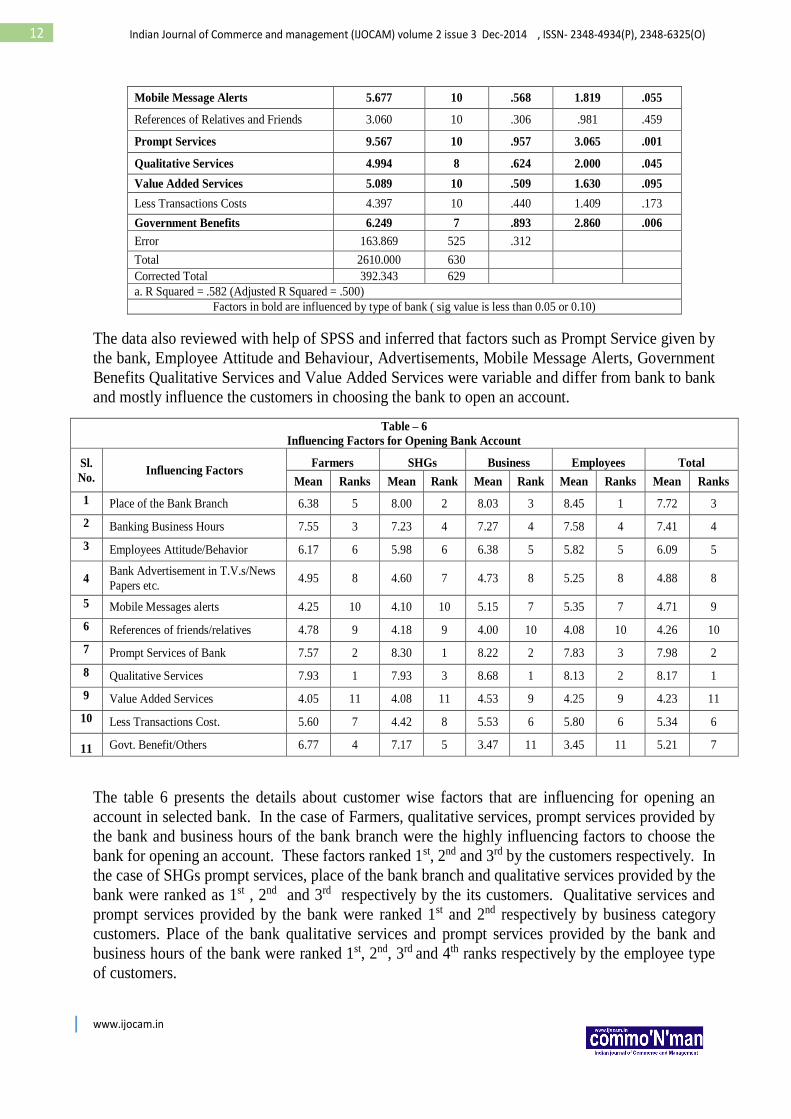

Mobile Message Alerts 5.677 10 .568 1.819 .055

References of Relatives and Friends 3.060 10 .306 .981 .459

Prompt Services 9.567 10 .957 3.065 .001

Qualitative Services 4.994 8 .624 2.000 .045

Value Added Services 5.089 10 .509 1.630 .095

Less Transactions Costs 4.397 10 .440 1.409 .173

Government Benefits 6.249 7 .893 2.860 .006

Error 163.869 525 .312

Total 2610.000 630

Corrected Total 392.343 629

a. R Squared = .582 (Adjusted R Squared = .500)

Factors in bold are influenced by type of bank ( sig value is less than 0.05 or 0.10)

The data also reviewed with help of SPSS and inferred that factors such as Prompt Service given by

the bank, Employee Attitude and Behaviour, Advertisements, Mobile Message Alerts, Government

Benefits Qualitative Services and Value Added Services were variable and differ from bank to bank

and mostly influence the customers in choosing the bank to open an account.

Table – 6

Influencing Factors for Opening Bank Account

Sl.

No. Influencing Factors

Farmers SHGs Business Employees Total

Mean Ranks Mean Rank Mean Rank Mean Ranks Mean Ranks

1 Place of the Bank Branch 6.38 5 8.00 2 8.03 3 8.45 1 7.72 3

2 Banking Business Hours 7.55 3 7.23 4 7.27 4 7.58 4 7.41 4

3 Employees Attitude/Behavior 6.17 6 5.98 6 6.38 5 5.82 5 6.09 5

4 Bank Advertisement in T.V.s/News

Papers etc. 4.95 8 4.60 7 4.73 8 5.25 8 4.88 8

5 Mobile Messages alerts 4.25 10 4.10 10 5.15 7 5.35 7 4.71 9

6 References of friends/relatives 4.78 9 4.18 9 4.00 10 4.08 10 4.26 10

7 Prompt Services of Bank 7.57 2 8.30 1 8.22 2 7.83 3 7.98 2

8 Qualitative Services 7.93 1 7.93 3 8.68 1 8.13 2 8.17 1

9 Value Added Services 4.05 11 4.08 11 4.53 9 4.25 9 4.23 11

10 Less Transactions Cost. 5.60 7 4.42 8 5.53 6 5.80 6 5.34 6

11 Govt. Benefit/Others 6.77 4 7.17 5 3.47 11 3.45 11 5.21 7

The table 6 presents the details about customer wise factors that are influencing for opening an

account in selected bank. In the case of Farmers, qualitative services, prompt services provided by

the bank and business hours of the bank branch were the highly influencing factors to choose the

bank for opening an account. These factors ranked 1st, 2nd and 3rd by the customers respectively. In

the case of SHGs prompt services, place of the bank branch and qualitative services provided by the

bank were ranked as 1st , 2nd and 3rd respectively by the its customers. Qualitative services and

prompt services provided by the bank were ranked 1st and 2nd respectively by business category

customers. Place of the bank qualitative services and prompt services provided by the bank and

business hours of the bank were ranked 1st, 2nd, 3rd and 4th ranks respectively by the employee type

of customers.

www.ijocam.in

13 Indian Journal of Commerce and management (IJOCAM) volume 2 issue 3 Dec-2014 , ISSN- 2348-4934(P), 2348-6325(O)

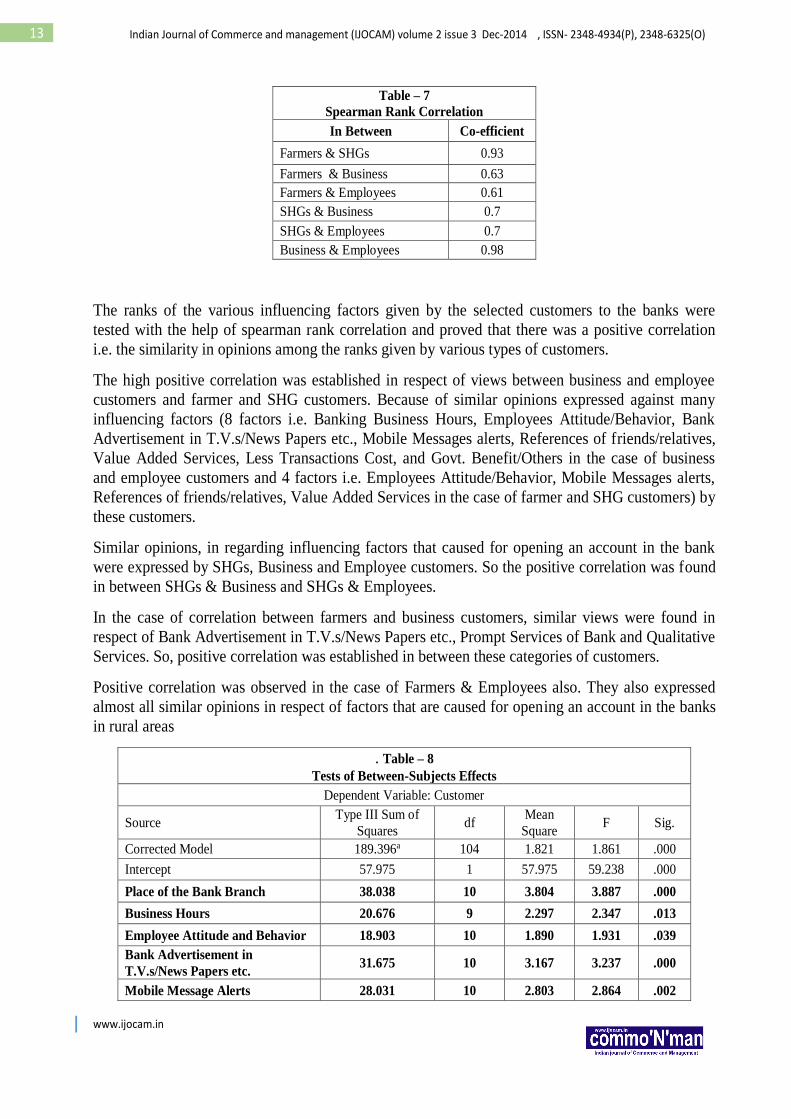

Table – 7

Spearman Rank Correlation

In Between Co-efficient

Farmers & SHGs 0.93

Farmers & Business 0.63

Farmers & Employees 0.61

SHGs & Business 0.7

SHGs & Employees 0.7

Business & Employees 0.98

The ranks of the various influencing factors given by the selected customers to the banks were

tested with the help of spearman rank correlation and proved that there was a positive correlation

i.e. the similarity in opinions among the ranks given by various types of customers.

The high positive correlation was established in respect of views between business and employee

customers and farmer and SHG customers. Because of similar opinions expressed against many

influencing factors (8 factors i.e. Banking Business Hours, Employees Attitude/Behavior, Bank

Advertisement in T.V.s/News Papers etc., Mobile Messages alerts, References of friends/relatives,

Value Added Services, Less Transactions Cost, and Govt. Benefit/Others in the case of business

and employee customers and 4 factors i.e. Employees Attitude/Behavior, Mobile Messages alerts,

References of friends/relatives, Value Added Services in the case of farmer and SHG customers) by

these customers.

Similar opinions, in regarding influencing factors that caused for opening an account in the bank

were expressed by SHGs, Business and Employee customers. So the positive correlation was found

in between SHGs & Business and SHGs & Employees.

In the case of correlation between farmers and business customers, similar views were found in

respect of Bank Advertisement in T.V.s/News Papers etc., Prompt Services of Bank and Qualitative

Services. So, positive correlation was established in between these categories of customers.

Positive correlation was observed in the case of Farmers & Employees also. They also expressed

almost all similar opinions in respect of factors that are caused for opening an account in the banks

in rural areas

. Table – 8

Tests of Between-Subjects Effects

Dependent Variable: Customer

Source Type III Sum of

Squares df

Mean

Square F Sig.

Corrected Model 189.396a 104 1.821 1.861 .000

Intercept 57.975 1 57.975 59.238 .000

Place of the Bank Branch 38.038 10 3.804 3.887 .000

Business Hours 20.676 9 2.297 2.347 .013

Employee Attitude and Behavior 18.903 10 1.890 1.931 .039

Bank Advertisement in

T.V.s/News Papers etc. 31.675 10 3.167 3.237 .000

Mobile Message Alerts 28.031 10 2.803 2.864 .002

www.ijocam.in

14 Indian Journal of Commerce and management (IJOCAM) volume 2 issue 3 Dec-2014 , ISSN- 2348-4934(P), 2348-6325(O)

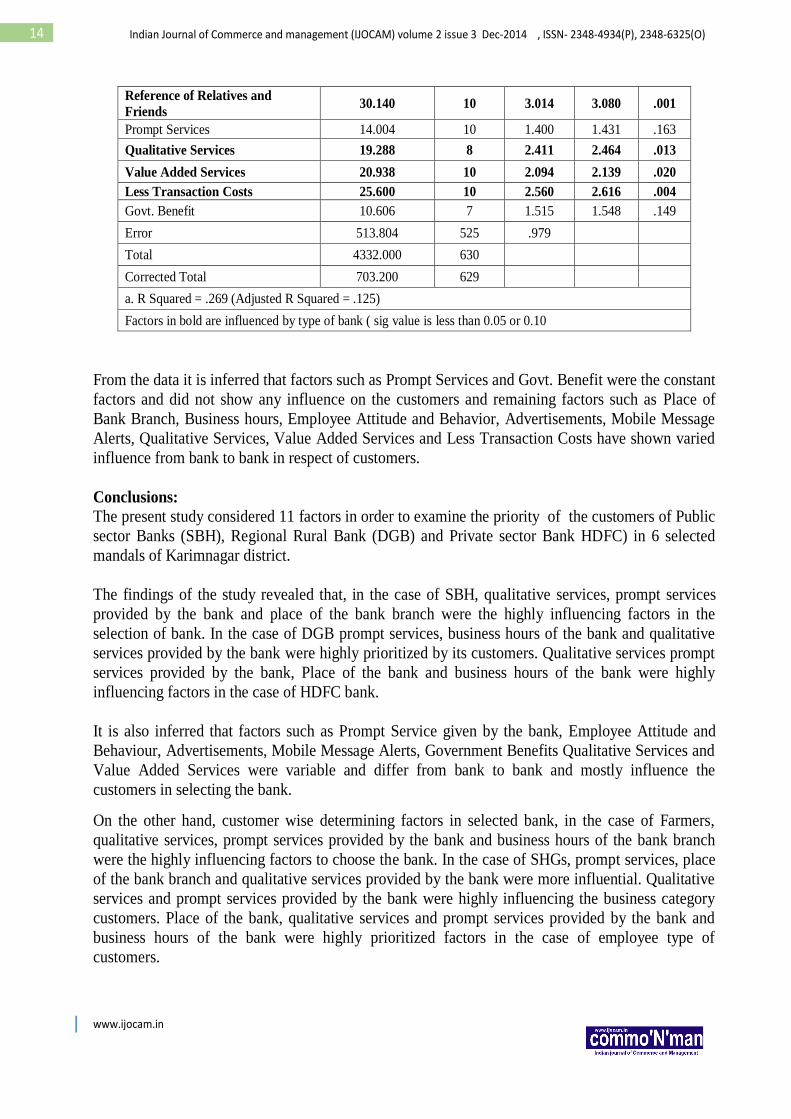

Reference of Relatives and

Friends 30.140 10 3.014 3.080 .001

Prompt Services 14.004 10 1.400 1.431 .163

Qualitative Services 19.288 8 2.411 2.464 .013

Value Added Services 20.938 10 2.094 2.139 .020

Less Transaction Costs 25.600 10 2.560 2.616 .004

Govt. Benefit 10.606 7 1.515 1.548 .149

Error 513.804 525 .979

Total 4332.000 630

Corrected Total 703.200 629

a. R Squared = .269 (Adjusted R Squared = .125)

Factors in bold are influenced by type of bank ( sig value is less than 0.05 or 0.10

From the data it is inferred that factors such as Prompt Services and Govt. Benefit were the constant

factors and did not show any influence on the customers and remaining factors such as Place of

Bank Branch, Business hours, Employee Attitude and Behavior, Advertisements, Mobile Message

Alerts, Qualitative Services, Value Added Services and Less Transaction Costs have shown varied

influence from bank to bank in respect of customers.

Conclusions:

The present study considered 11 factors in order to examine the priority of the customers of Public

sector Banks (SBH), Regional Rural Bank (DGB) and Private sector Bank HDFC) in 6 selected

mandals of Karimnagar district.

The findings of the study revealed that, in the case of SBH, qualitative services, prompt services

provided by the bank and place of the bank branch were the highly influencing factors in the

selection of bank. In the case of DGB prompt services, business hours of the bank and qualitative

services provided by the bank were highly prioritized by its customers. Qualitative services prompt

services provided by the bank, Place of the bank and business hours of the bank were highly

influencing factors in the case of HDFC bank.

It is also inferred that factors such as Prompt Service given by the bank, Employee Attitude and

Behaviour, Advertisements, Mobile Message Alerts, Government Benefits Qualitative Services and

Value Added Services were variable and differ from bank to bank and mostly influence the

customers in selecting the bank.

On the other hand, customer wise determining factors in selected bank, in the case of Farmers,

qualitative services, prompt services provided by the bank and business hours of the bank branch

were the highly influencing factors to choose the bank. In the case of SHGs, prompt services, place

of the bank branch and qualitative services provided by the bank were more influential. Qualitative

services and prompt services provided by the bank were highly influencing the business category

customers. Place of the bank, qualitative services and prompt services provided by the bank and

business hours of the bank were highly prioritized factors in the case of employee type of

customers.

www.ijocam.in

15 Indian Journal of Commerce and management (IJOCAM) volume 2 issue 3 Dec-2014 , ISSN- 2348-4934(P), 2348-6325(O)

The study also reviewed that factors such as Prompt Services and Govt. Benefit were the constant

factors and did not show any influence on the customers and remaining factors such as Place of

Bank Branch, Business hours, Employee Attitude and Behavior, Advertisements, Mobile Message

Alerts, Qualitative Services, Value Added Services and Less Transaction Costs were differed from

customer to customer and mostly influence the customers in choosing the bank.

Bibliography

AHMED*, H. U. (2008). AN EMPIRICAL ANALYSIS OF THE DETERMINANTS. Pakistan

Economic and Social Review , 46 (2), 147-160.

Almossawi, M. (2001). Bank Selection Criteria Employed by College Students in. International

Journal of Bank , 3 (19), 115-25,.

AZOUZI, D. (2009). The Adoption of Electronic Banking in Tunisia: An Exploratory Study.

Journal of Internet Banking and Commerce , 14 (3), 1-11.

Cicic M., B. N. (2004). Bank Selection Criteria Employed by.

Commercial Bank Selection:. (2009). European Journal of Economics, Finance and Administrative

Sciences , 1 (16), 263-73.

Dr.Mohmod Jasim Alsamydia, D. O. (2012). The factors Influencing consumers' satisfaction and

continuity to deal With E-Banking Services in Jordan. Global Journal of Managment and Business

research , 12 (14), 129-141.

Fatoki, C. C. (2011). Factors Influencing the Choice of Commercial Banks by. International Journal

of Business and Management , 6 (6), 66-76.

www.ijocam.in

16 Indian Journal of Commerce and management (IJOCAM) volume 2 issue 3 Dec-2014 , ISSN- 2348-4934(P), 2348-6325(O)

Impact of Financial Inclusion Improvement Methods on Financial Inclusion

Network and Operations

Dr. K. Kanaka Raju,

Assistant Professor,

E-Mail: [email protected]

Mobile: 0091 8125387145

Mr. B. Chellayya,

Research Scholar,

E- Mail: [email protected]

Mobile: 0091 9491789332

Abstract

The data has been collected through the structured questionnaire from the 750 respondents. The

secondary data obtained from the existing literature and review. The study found that 23.5 per cent

of variation in Financial Inclusion Network and Operations (FINO) was explained by the

independent variables and state that there was a significant difference between each other. The

study also found that joint liability group was more favourable towards the Financial Inclusion

Network and Operations (FINO), founded by the Zero Balance accounts, Self-Help Groups (SHGs),

micro finance, business facilitators and business correspondents. Finally it is advised that improve

the degree of literacy level of our people to familiarize the financial literacy for well being of the

human kind.

Introduction:

Financial access provides an environment where the common people have access to the

formal financial institutional system and thereby are able to access various financial products such

as deposits, credit, micro-insurance/pensions; financial counselling and safe funds transfer at

affordable prices and with ease of access. The access could be to all or any of the formal financial

institutions, markets and payment systems with all or any financial instrument. Thus, financial

inclusion is the process of facilitating the access of those sectors/segments of the population which

are denied these facilities to become a part of the formal financial system, either as individuals or as

groups. The easiest way to ensure better financial inclusion is to open more branches of banks and

financial inclusions, removing various obstacles in accessing financial services from banks by very

poor people. Technological advances can only reduce transaction costs, of the clients and the

banks/financial institutions. Thus, financial inclusion should not add to the operational costs of

financial institutions so that these continue to render affordable services to the common customers.

Review of literature:

S.Mahendra Dev (2006) opined that required new regulatory procedures and devpoliticisation of

the financial system

S.Ramesh and Preeti Sahai (2007) OPinioned that notwithstanding the regulatory, operational and

other aspects in focus, financial inclusion is a complex issue which cannot be solved alone by any

actors in the system. Formal financial institutions such as, banks, insurance companies, mutual

funds, pension companies will have to join hands with small NGO-MFIs, larger NBFC- MFIs, and

technology providers to enable inclusion. The strengths of these institutions will have to be put

together through sound collaborations for financial inclusion. Local and national presence

organizations have to ensure that these partnerships look at both commercial and social aspects to

help achieve scale, sustainability, and impact.

Dr. J. Sadakkadulla (2009) concludes that, “Financial inclusion is not an option but a compulsion.

www.ijocam.in

17 Indian Journal of Commerce and management (IJOCAM) volume 2 issue 3 Dec-2014 , ISSN- 2348-4934(P), 2348-6325(O)

Elaben Bhatt (2009) estimated that globally over two billion people are excluded from access to

financial services, of which one third is in India. The committee on financial inclusion (Rangarajan

Committee 2006) observed that in India 51.4 per cent of former households are financially excluded

from both formal and informal sources and 73 per cent of the farmer households do not access

formal sources of credit. To be specific, those excluded are marginal farmers who happen to be

women who are further excluded right from the first stage of perception.

M. Ramachandran (2009) explained that the government as a part of its initiative has setup a

Pooled Finance Development Fund (PFDF) to provide credit enhancement to the local bodies to

access funds from the capital market, based on their credit worthiness for funding bankable urban

infrastructure projects. This could enable the ULBs to achieve sustainability and eventually attain

financial inclusiveness.

C.B. Bhave (2009) proposed that the various ways in which people in remote areas can be brought

into the system. In this process of inclusion, the first inclusion that needs to be made, if we really

want them to be included into things, is including them in the power structure. Do we really want to

take choices to a person who is not a part of the power system is the issue that we need to answer. It

should not be our effort to say that this man who is outside the banking system must come into the

banking system because. We don’t know whether the banking system is good for him or not. So the

issue of inclusion becomes one of getting him into the banking system. The real issue is whether he

has the choice to decide whether he wants to get into the banking system or not, and are we offering

him a real choice or not.

CMA C. R. Shiv Kumaran (2010) stated that one of the most important challenges being faced

today with regard to Financial Inclusion is about establishing the identity and delivering efficiently

the financial products.

Nandan Nilekani (2010) emphasized that building services and products to cater to the poor -

accessible consumer goods, decentralized governance infrastructure, low-cost solutions in lighting,

water supply, transportation, and so on.

Ambreena Manji (2010) opined that, it was difficult to reconcile the promotion of financial

inclusion with the aim of international development to end poverty.

N. D. S. V. Nageswara Rao (2010) suggested that Banks / RBI should conduct awareness camps

about Financial Inclusion to the Bank staff.

D. Devandhiran and Sreehari R.(2011) attempts to explore now technological services which

are relevant to various strategies followed by banks to deliver banking technological services in

rural banking.

Sachin Joseph (2011) stated that Micro-credit and Micro-savings have great potential to alleviate

poverty in India. The success of small packaged products and one Rupee Sachets in FMCG sector

has shown how selling in small amounts and utilizing the principle of economies of scale can lead

to better profit margins. Through regulatory reforms in the field of Financial Inclusion small and

large financial institutions are free to expand their range of products and delivery channels in

partnership with other stakeholders, to reach the poorest of the poor and still make a profit. Thus

through the use of technology, innovation and marketing strategies, financial inclusion will prove

that “Small is Beautiful

Srinivas Vissapragada(2013) concludes that It is becoming increasingly apparent that addressing

financial exclusion will require a holistic approach on the part of the banks in creating awareness

about financial products, education, and advice on money management, debt counseling, savings

www.ijocam.in

18 Indian Journal of Commerce and management (IJOCAM) volume 2 issue 3 Dec-2014 , ISSN- 2348-4934(P), 2348-6325(O)

and affordable credit. The various financial services include credit, savings, insurance and payments

and remittance facilities.

Manjunath(2013) strongly believe that financial inclusion plays a crucial role in development and

sustainable prosperity as is being increasingly recognized and acknowledged globally. Large

segments of populations need to be part of formal payment system and financial savings and lead to

higher economic development. It is clear from the study that, inclusive growth is very necessary for

sustainable development and equitable generation of wealth and prosperity. Thus, “financial

inclusion is no longer a policy choice today but a policy compulsion”.

Objectives of the study: after verifying the existing literature, the following objectives were found.

1. To examine the perceptions of respondents regarding various issues of financial inclusion.

2. To know the relationship between the FINO and the independent variables.

3. To offer a suitable suggestions to strengthen the financial inclusion.

Methodology of the study: The data obtained from the structured questionnaire through the 750

respondents, the secondary data obtained from the existing literature and review.

Analysis and interpretations of the study

Table 1. Gender of the respondents

Gender Frequency Percent

Male 480 64.0

Female 270 36.0

Total 750 100.0

In table.1: describes about the distribution of the respondents based on gender. The majority

of the respondents (64 per cent) belonged to the male category and rest of them confined to the 36

per cent. Hence, it can be concluded that majority of the respondents belonged to the male category.

Table .2 Ages of the respondents

Age(in years) Frequency Percent

18-25 108 14.4

25-35 222 29.6

35-45 244 32.5

45and above 176 23.5

Total 750 100.0

Table 2: This table reflects that the distribution of respondents based on the age. The 32.5 percent

of the respondents belong to the age group of the 35-45, followed by the 25-35 years, 45 and above,

and 18-25. Hence, it can be concluded that the more number of respondents belonged to the age

group of 35-45.

Table 3.Marital status of the respondents

Marital status Frequency Per cent

un married 24 3.2

married 596 79.5

widow/widower 108 14.4

divorced 22 2.9

Total 750 100.0

In table 3 explains the marital status of the respondents. The majority of the respondents (79.5 per

cent) belonged to the married group, followed by the widow/widower, unmarried and divorced.

Table.4 Religion of the respondents

Religion Frequency Percent

www.ijocam.in

19 Indian Journal of Commerce and management (IJOCAM) volume 2 issue 3 Dec-2014 , ISSN- 2348-4934(P), 2348-6325(O)

Hindu 694 92.5

Muslim 26 3.5

Christian 30 4.0

Total 750 100.0

Table. 4 tells us that the distribution of respondents based on the religion. The majority of the

respondents (92.5 percent) belonged to the religion of the Hindu, followed by the Christian and

Muslim.

Table.5 Language of the respondents

Language Frequency Percent

Telugu 750 100.0

Table 5 indicates that 100 per cent of respondents belonged to the Telugu. Hence, it can be

concluded that all the respondents belonged to the Telugu.

Table.6 Literacy Level of the respondents

Literacy Level Frequency Percent

Illiterate 180 24.0

Signature capacity 84 11.2

Not completed SSC 140 18.7

SSC 82 10.9

Intermediate 76 10.1

Polytechnic 64 8.5

Bachelor degree 94 12.5

Master degree 30 4.0

Total 750 100.0

Table 6 reflects that the distribution of respondents based on the literacy level. The 24 per cent of

the respondents belonged to the illiterate, followed by the Non completion of SSC, Bachelor

degree, signature capacity, SSC, Intermediate, Polytechnic and MasterDegree.

Table .7Professions of respondents

Profession Frequency Percent

Farmer 132 17.6

agriculture labour 262 34.9

construction labour 48 6.4

industrial labour 42 5.6

rearing livestock 36 4.8

household industry 30 4.0

Business 38 5.1

government employee 68 9.1

private employee 94 12.5

Total 750 100.0

In table 7 narrates about the distribution of respondents based on their profession. The 34.9 per cent

of respondents belonged to the agriculture labour, followed by the farmer, private employee,

government employee, construction labour, business rearing livestock and household industry.

Table.8Income of the respondents

Income of the respondents Frequency Percent

Below 5000 106 14.1

5001 - 10000 424 56.5

www.ijocam.in

20 Indian Journal of Commerce and management (IJOCAM) volume 2 issue 3 Dec-2014 , ISSN- 2348-4934(P), 2348-6325(O)

10001 - 15000 114 15.2

15001 -20000 42 5.6

20001 -25000 38 5.1

Above - 250001 26 3.5

Total 750 100.0

Table 8 furnishes the information regarding the distribution of respondents based on their level of

Income. The majority of the respondents (56.5 per cent) earn the income level between 5001-10000,

followed by the 10001-15000. Hence, it can be concluded that the majority of respondents belonged

to the income group of 5,001-10,000.

Table.9 Variables Entered/ Removed

Model Variables Entered Variables Removed Method

Zero Balance Accounts?

No Frills Account

business correspondents

Micro insurance

Self Help Groups (SHGs)

business Facilitators

Joint liability Groups

Micro Financea

a. All requested variables entered.

b. Dependent Variable: Financial inclusion improveMethods-Financial Inclusion Network and

Operations (FINO)

Analysis: Table 9 narrates about the entered as independent variations, Financial Inclusion

Network and Operation (FINO) considered as a dependent variables.

Table.10 Model summary

Model R R Square Adjusted R Square Std. Error of the

Estimate

1 .485a .235 .228 .967

a. Predictors: (Constant), Financial inclusion improves methods- Zero Balance Accounts? No

Frills Account, business correspondents, Micro insurance, Self Help Groups (SHGs),

business Facilitators, liability Groups, Micro Finance.

Analysis: The above regression table explains about 23.5 percent of variation in the Financial

Inclusion Network and Operation (FINO) was explained by the variables of independent

variables. The standard error of the estimate of this table is error of the estimate of this table is

0.976, it indicates that it is a fit for the regression model.

Table 11: ANOVAb

Model Sum of Squares Df Mean Square F Sig.

Regression 213.064 7 30.438 32.571 .000a

Residual 693.410 742 .935

Total 906.475 749

a. Predictors: (Constant), Financial inclusion improves methods- Zero Balance Accounts?

No Frills Account, Financial inclusion improve methods-business correspondents, Financial

inclusion improve methods- Micro insurance, Financial inclusion improve methods-Self Help

Groups (SHGs), Financial inclusion improve methods-business Facilitators, Financial inclusion

improve methods-Joint liability Groups, Financial inclusion improve methods- Micro Finance.

www.ijocam.in

21 Indian Journal of Commerce and management (IJOCAM) volume 2 issue 3 Dec-2014 , ISSN- 2348-4934(P), 2348-6325(O)

b. Dependent Variable: Financial inclusion improve methods- Financial Inclusion Network

and Operation (FINO)

Hypothesis -1

Null Hypothesis (H0): There is no significant difference between the dependent variable of FINO

to the predictors of above.

Alternative Hypothesis (H1): There is a significant difference between the dependent variable of

FINO to the predictors of above.

Analysis: The sum of squares of the residual value was much more than the sum of square of the

regression, where df=749, F=32.571, P=0.000. Hence, it is observed that proposed null hypothesis

was rejected and inferred that there was a significant difference between the FINO to the predictors.

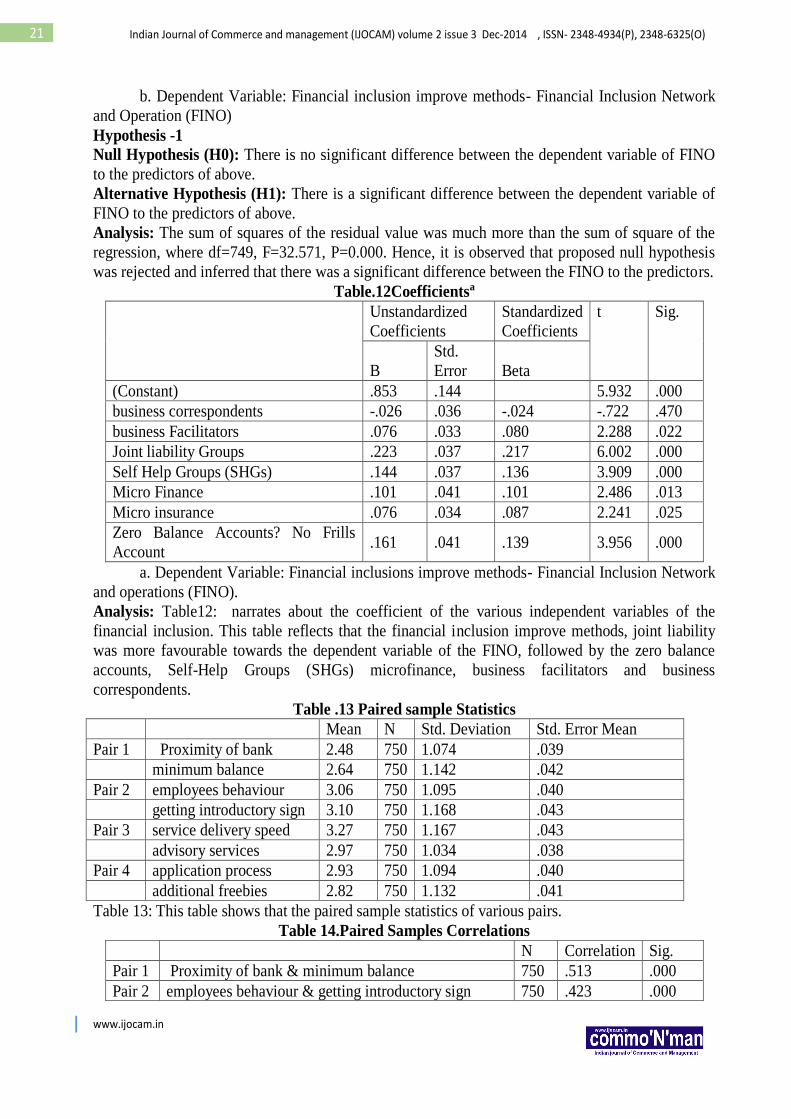

Table.12Coefficientsa

Unstandardized

Coefficients

Standardized

Coefficients

t Sig.

B

Std.

Error Beta

(Constant) .853 .144 5.932 .000

business correspondents -.026 .036 -.024 -.722 .470

business Facilitators .076 .033 .080 2.288 .022

Joint liability Groups .223 .037 .217 6.002 .000

Self Help Groups (SHGs) .144 .037 .136 3.909 .000

Micro Finance .101 .041 .101 2.486 .013

Micro insurance .076 .034 .087 2.241 .025

Zero Balance Accounts? No Frills

Account .161 .041 .139 3.956 .000

a. Dependent Variable: Financial inclusions improve methods- Financial Inclusion Network

and operations (FINO).

Analysis: Table12: narrates about the coefficient of the various independent variables of the

financial inclusion. This table reflects that the financial inclusion improve methods, joint liability

was more favourable towards the dependent variable of the FINO, followed by the zero balance

accounts, Self-Help Groups (SHGs) microfinance, business facilitators and business

correspondents.

Table .13 Paired sample Statistics

Mean N Std. Deviation Std. Error Mean

Pair 1 Proximity of bank 2.48 750 1.074 .039

minimum balance 2.64 750 1.142 .042

Pair 2 employees behaviour 3.06 750 1.095 .040

getting introductory sign 3.10 750 1.168 .043

Pair 3 service delivery speed 3.27 750 1.167 .043

advisory services 2.97 750 1.034 .038

Pair 4 application process 2.93 750 1.094 .040

additional freebies 2.82 750 1.132 .041

Table 13: This table shows that the paired sample statistics of various pairs.

Table 14.Paired Samples Correlations

N Correlation Sig.

Pair 1 Proximity of bank & minimum balance 750 .513 .000

Pair 2 employees behaviour & getting introductory sign 750 .423 .000

www.ijocam.in

22 Indian Journal of Commerce and management (IJOCAM) volume 2 issue 3 Dec-2014 , ISSN- 2348-4934(P), 2348-6325(O)

Pair 3 service delivery speed & advisory services 750 .444 .000

Pair 4 additional freebies 750 .267 .000

Analysis: Table 14: reflects that the information o the two variables, in pair, having of moderate

relationship between the variables of the balance and minimum balance in pair 2 as well as pair 3

also consist of a moderate relationship, but there was a weak relationship from the application

process to the additional freebies.

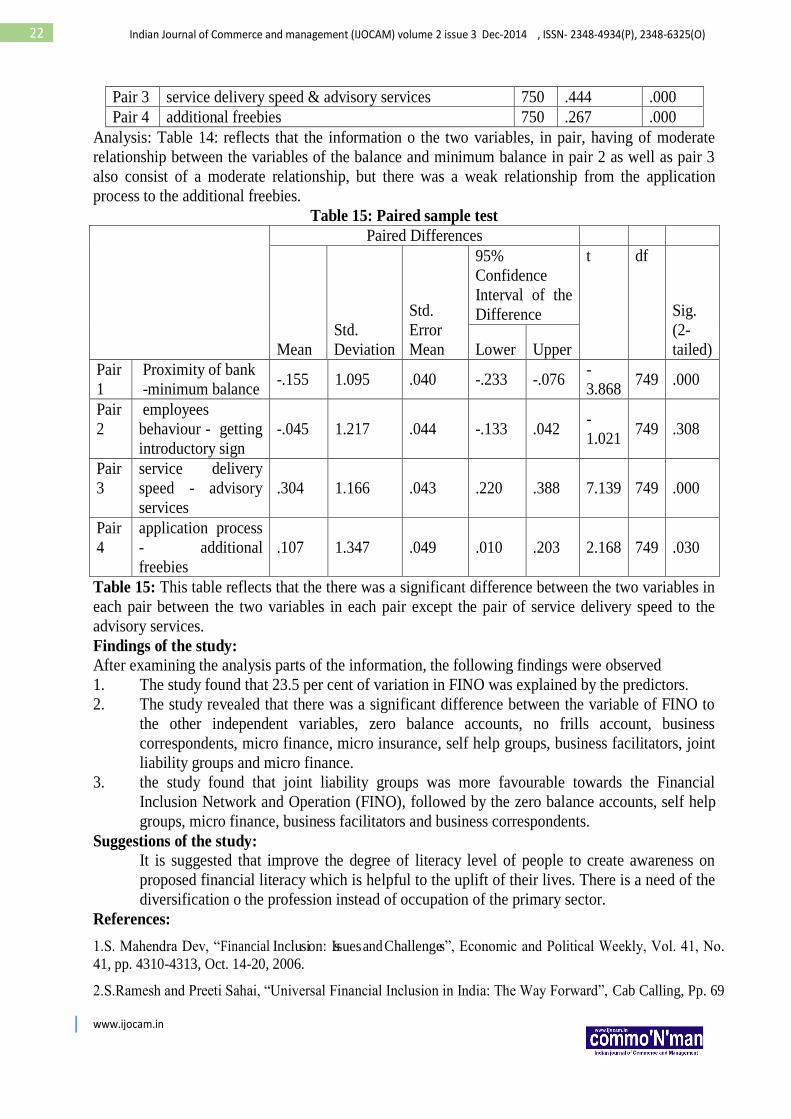

Table 15: Paired sample test

Paired Differences

Mean

Std.

Deviation

Std.

Error

Mean

95%

Confidence

Interval of the

Difference

t df

Sig.

(2-

tailed) Lower Upper

Pair

1

Proximity of bank

-minimum balance -.155 1.095 .040 -.233 -.076

-

3.868 749 .000

Pair

2

employees

behaviour - getting

introductory sign

-.045 1.217 .044 -.133 .042 -

1.021 749 .308

Pair

3

service delivery

speed - advisory

services

.304 1.166 .043 .220 .388 7.139 749 .000

Pair

4

application process

- additional

freebies

.107 1.347 .049 .010 .203 2.168 749 .030

Table 15: This table reflects that the there was a significant difference between the two variables in

each pair between the two variables in each pair except the pair of service delivery speed to the

advisory services.

Findings of the study:

After examining the analysis parts of the information, the following findings were observed

1. The study found that 23.5 per cent of variation in FINO was explained by the predictors.

2. The study revealed that there was a significant difference between the variable of FINO to

the other independent variables, zero balance accounts, no frills account, business

correspondents, micro finance, micro insurance, self help groups, business facilitators, joint

liability groups and micro finance.

3. the study found that joint liability groups was more favourable towards the Financial

Inclusion Network and Operation (FINO), followed by the zero balance accounts, self help

groups, micro finance, business facilitators and business correspondents.

Suggestions of the study:

It is suggested that improve the degree of literacy level of people to create awareness on

proposed financial literacy which is helpful to the uplift of their lives. There is a need of the

diversification o the profession instead of occupation of the primary sector.

References:

1.S. Mahendra Dev, “Financial Inclusion: Issues and Challenges”, Economic and Political Weekly, Vol. 41, No.

41, pp. 4310-4313, Oct. 14-20, 2006.

2.S.Ramesh and Preeti Sahai, “Universal Financial Inclusion in India: The Way Forward”, Cab Calling, Pp. 69

www.ijocam.in

23 Indian Journal of Commerce and management (IJOCAM) volume 2 issue 3 Dec-2014 , ISSN- 2348-4934(P), 2348-6325(O)

– 73, July – September 2007.

3.Dr. J. Sadakkadulla, “Financial inclusion: the road ahead”, The Journal of Indian Institute of Banking &

Finance, Vol. 80, No. 1, pp. 70 – 72, January - March 2009.

4.Elaben Bhatt, “Financial Inclusion”, The Journal of Indian Institute of Banking & Finance, Vol. 80, No. 1,

pp. 73 – 75, January - March 2009.

5.M. Ramachandran, “Urban local bodies and Financial Inclusion”, Financial Inclusion, Edited by Sameer

Kochhar, R. ChandraShekhar, K.C. Chakrabarty and Deepak B. Phatak, pp. 33 – 38, 2009.

6.C.B. Bhave, “Is Technology Inclusive?”, Financial Inclusion, Edited by Sameer Kochhar, R.

ChandraShekhar, K.C. Chakrabarty and Deepak B. Phatak, pp. 39 – 42, 2009.

7.CMA C. R. Shiv Kumaran, “The Role of Telecom in Financial Inclusion - A Sunrise Opportunity for the

CMA in India”, The Management Accountant, Vol. 45, No. 12, December 2010 pp. 971 - 973, December

2010.

8.Nandan Nilekani, “Financial inclusion - have we reached the tipping point?”, The Journal of Indian

Institute of Banking & Finance, Vol. 81, No. 4, pp. 5 – 9, October - December 2010.

9.Ambreena Manji, “Eliminating Poverty? ‘Financial Inclusion’, Access to Land, and Gender Equality

in International Development”, The Modern Law Review Vol. 73, Issue 6, pp. 985 – 1004, November

2010.

10.N. D. S. V. Nageswara Rao, “Financial Inclusion - Banker's Perspective”, The Journal of Indian Institute

of Banking & Finance, Vol. 81, No. 4, pp. 20 – 26, October - December 2010.

11.D. Devandhiran and Sreehari .R, “Technological Services in Rural Banking: A study with reference to

bank branches in Tirunelveli district”, International journal

12. Sachin Joseph, “Financial Inclusion : Involving the Uninvolved through Product, Channel and Marketing

Innovations”, The Journal of Indian Institute of Banking & Finance, Vol. 82, No. 2, pp. 34 – 40, April – June

2011.

13.Srinivas Vissapragada, “Financial inclusion in India – Taking financial services to the rural masses”,

Financial inclusion in India – Challenges and strategies, edited by Dr. M. S. V. Prasad and Dr. G. V.

SatyaSekhar, Excel Books, pp. 281-289, 2013.

14. Manjunath, “Financial inclusion and rural cooperative banks in Hyderabad – Karnataka region: A

theoretical overview”, Financial inclusion in India – Challenges and strategies, edited by Dr. M. S. V. Prasad

and Dr. G. V. SatyaSekhar, Excel Books, pp. 209-218, 2013.

15.K.G. Karmakar,G.D.Benerjee, N.P.Mohapatra(2011) “Towards Financial Inclusion in India”, Sage

Publications, New Delhi, India. www.sagepub.in. Page no:3-18

www.ijocam.in

24 Indian Journal of Commerce and management (IJOCAM) volume 2 issue 3 Dec-2014 , ISSN- 2348-4934(P), 2348-6325(O)

Information Technology and Its Role in Indian Banking Sector

Dr.P. Mohan 1Principal,

Manair College of Management,

Khammam.

D.CH. APPA RAO, Ph.D Scholer

Acharya Nagarjuna University & Lecturer in

Commerce

GDC, Buttaigudem-534447 (W.G.Dist)

Abstract

With the globalization trends world over it is difficult for any nation big or small, developed

or developing, to remain isolated from what is happening around. For a country like India, which is

one of the most promising emerging markets, such isolation is nearly impossible. More particularly

in the area of Information Technology, where India has definitely an edge over its competitors,

remaining away or uniformity of the world trends is untenable. Financial sector in general and

banking industry in particular is the largest spender and beneficiary from information technology.

This endeavours to relate the international trends in it with the Indian banking industry. An attempt

has been made in this paper to examine various innovative instruments that have been introduced

by Banks in recent times.

Keywords

Banking Sector, Information Technology, Automated Systems and Processes, Mobile

Banking and Knowledge Management.

Introduction:

Information technology refers to the acquisition, processing, storage and

dissemination of all types of information using computer technology and telecommunication

systems. Technology includes all maters concerned with the furtherance of computer science

and technology and with the design, development, installation and implementation of

information system and applications. Information technology architecture is an integrated

framework for acquiring and evolving IT to achieve strategic goals. It has both logical and

technical components. Computer hardware and software, voice, data, network, satellite, other

telecommunications technologies, multimedia are application development tools.

These technologies are used for the input, storage, processing and communication of information.

Information technology includes ancillary equipment, software, firmware and similar

procedures, services etc. Modern high throughput technologies are providing vast amounts of the

sequences, expressions and functional data for genes and protein. One of the most difficult

challenges is turning this enormous pool of information into useful scientific insight and novel therapeutic products.

Technology has brought a complete paradigm shift in the functioning of banks and

delivery of banking services. Gone are the days when every banking transaction required a visit

to the bank branch. Today, most of the transactions can be done from the home and customers need

www.ijocam.in

25 Indian Journal of Commerce and management (IJOCAM) volume 2 issue 3 Dec-2014 , ISSN- 2348-4934(P), 2348-6325(O)

not visit the bank branch for anything. Technology is no longer an enabler, but a business driver.

The growth of the internet, mobiles and communication technology has added a different

dimension to banking. The information technology (IT) available today is being leveraged in

customer acquisitions, driving automation and process efficiency, delivering ease and efficiency to

customers.

The increased penetration and impact on the scale of business can be judged from metrics

such as deposit and credit per account, which according to the RBI data was INR 6,412 and INR

20, 757 in 1992 and INR 19, 898 and INR84, 618 in 2000—these metrics increased to INR59, 217

and INR258, 751 in 2009, respectively, approximately thrice the levels in 2000 and 10 times the

levels in 1992.

Many of the IT initiatives of banks started in the late 1990s or early 2000 with an

emphasis on the adoption of core banking solutions (CBS), automation of branches and

centralization of operations in the CBS. Over the last decade, most of the banks completed the

transformation to technology-driven organizations. Moving from a manual, scale-constrained

environment to a global presence with automated systems and processes, it is difficult to envisage

the adverse scenario, the sector was in the era before the reforms, when a simple deposit or

withdrawal of cash would require a day. ATMs, mobile banking and online bill payments faclities

to vendors and utility service providers have almost obviated the need for customers to visit a

branch. Branches are also transforming from operating as transaction processing points into

relationship management hubs. The change has been very productive for banks bringing in an

increase in productivity and operational efficiency to be more competitive. Better risk

management due to centralization of information and real time availability of critical data for

decision making.

With most of the banks being technology-enabled, the focus is shifting to computerizing

regional rural banks (RRBs). In addition, banks are moving toward decision making and business

intelligence software and trying to optimize the IT infrastructure created.

Growth and Expansion

Over the last Decade, the size of the banking industry has grown by 7.5 times. The

business per employee has increased from INR 27.6 million in 2007-08 to INR 62.7million

in 2011-12, while the profit per employee increased from INR 0.12 million in 2007-08 to

INR 0.39 million in 2011-12. Indian banks are also no longer constrained by geography as they

have worldwide operations. IT has been instrumental in the global expansion of banks. It is a

huge challenge for banks to maintain and keep the vast network operational. IT has helped banks

put in place alternate delivery channels such as internet and phone. Mobile banking and ATMs are

rapidly becoming the prime delivery channels. The consolidation and centralization of information

is also providing banks with accelerated decision making and risk management capabilities.

Electronic payments through credit and debit cards are also emerging as a fast-growing segment

providing ease of use and convenience to customers. The banking sector is projected to grow at a

strong pace over the next decade and will need to strongly leverage the IT infrastructure to acquire

and service the customer base and risk management.

Computerization in Banks

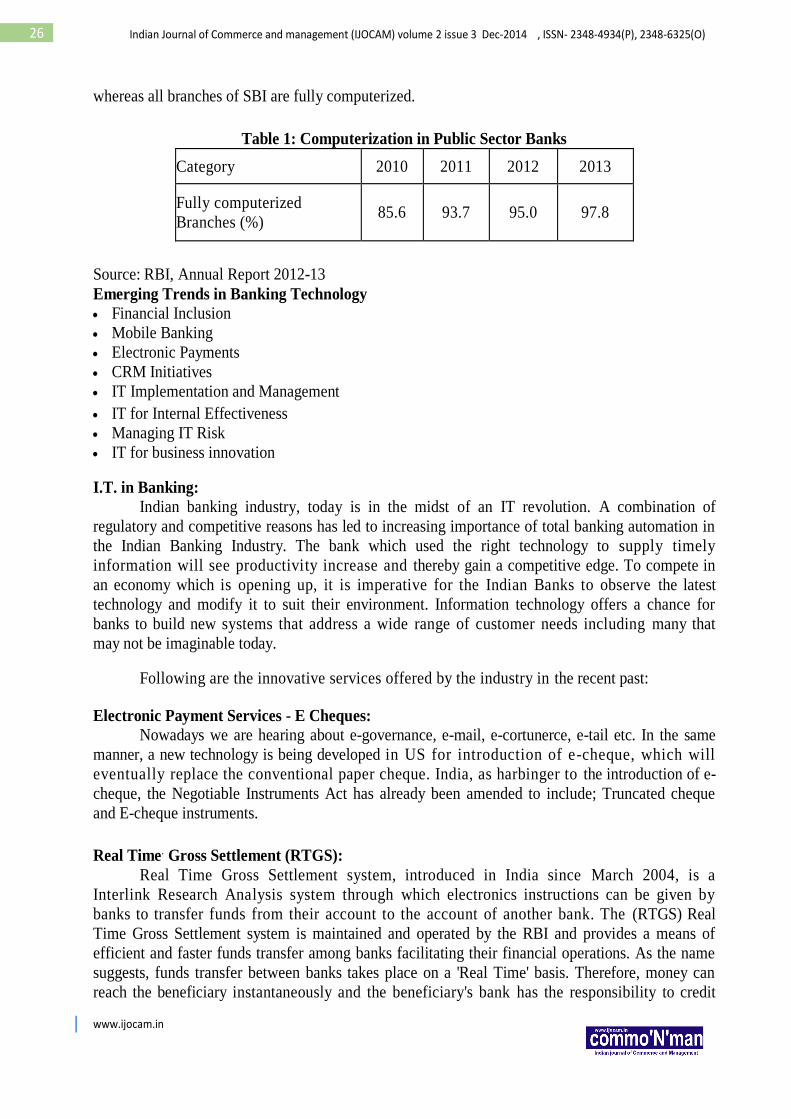

Technology has charged the face of the Indian banking sector through computation,

while new private sector banks and foreign banks have an edge in this regard. Among the total

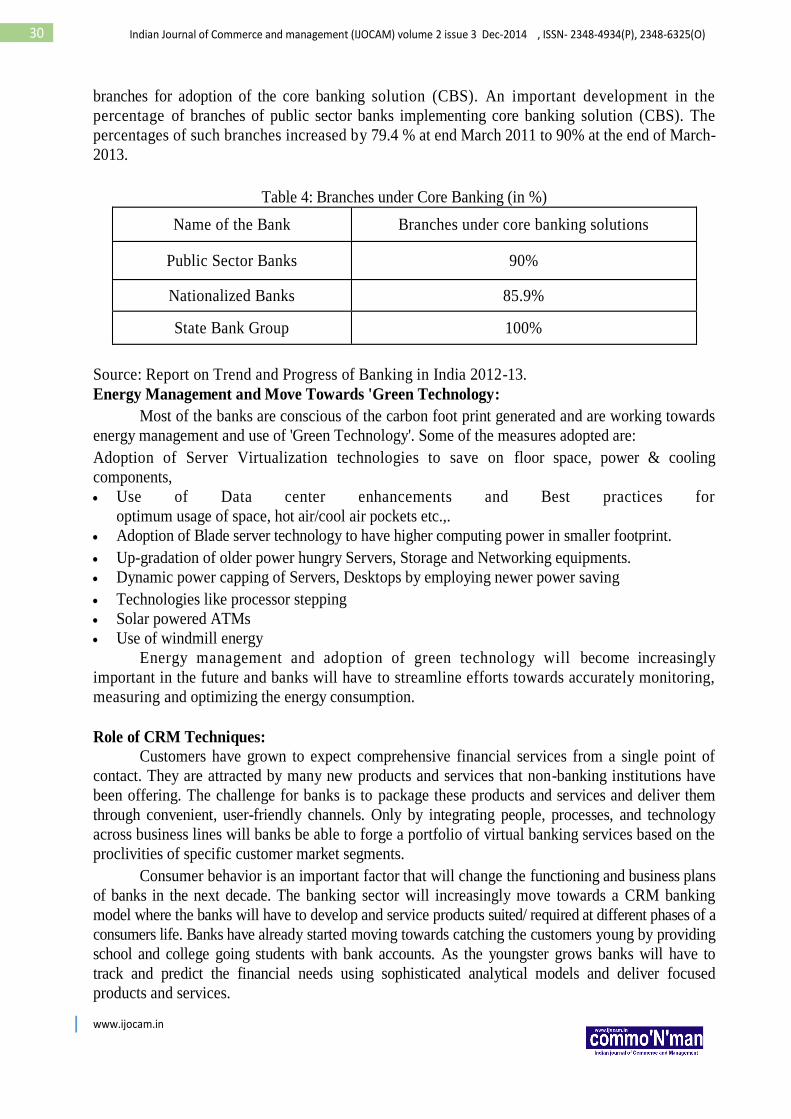

number of public sector bank branches, 97.8 percent are fully computerized at end – March 2013

www.ijocam.in

26 Indian Journal of Commerce and management (IJOCAM) volume 2 issue 3 Dec-2014 , ISSN- 2348-4934(P), 2348-6325(O)

whereas all branches of SBI are fully computerized.

Table 1: Computerization in Public Sector Banks

Category 2010 2011 2012 2013

Fully computerized

Branches (%) 85.6 93.7 95.0 97.8

Source: RBI, Annual Report 2012-13

Emerging Trends in Banking Technology Financial Inclusion

Mobile Banking

Electronic Payments

CRM Initiatives

IT Implementation and Management

IT for Internal Effectiveness

Managing IT Risk

IT for business innovation

I.T. in Banking:

Indian banking industry, today is in the midst of an IT revolution. A combination of

regulatory and competitive reasons has led to increasing importance of total banking automation in

the Indian Banking Industry. The bank which used the right technology to supply timely

information will see productivity increase and thereby gain a competitive edge. To compete in

an economy which is opening up, it is imperative for the Indian Banks to observe the latest

technology and modify it to suit their environment. Information technology offers a chance for

banks to build new systems that address a wide range of customer needs including many that

may not be imaginable today.

Following are the innovative services offered by the industry in the recent past:

Electronic Payment Services - E Cheques:

Nowadays we are hearing about e-governance, e-mail, e-cortunerce, e-tail etc. In the same

manner, a new technology is being developed in US for introduction of e-cheque, which will

eventually replace the conventional paper cheque. India, as harbinger to the introduction of e-

cheque, the Negotiable Instruments Act has already been amended to include; Truncated cheque

and E-cheque instruments.

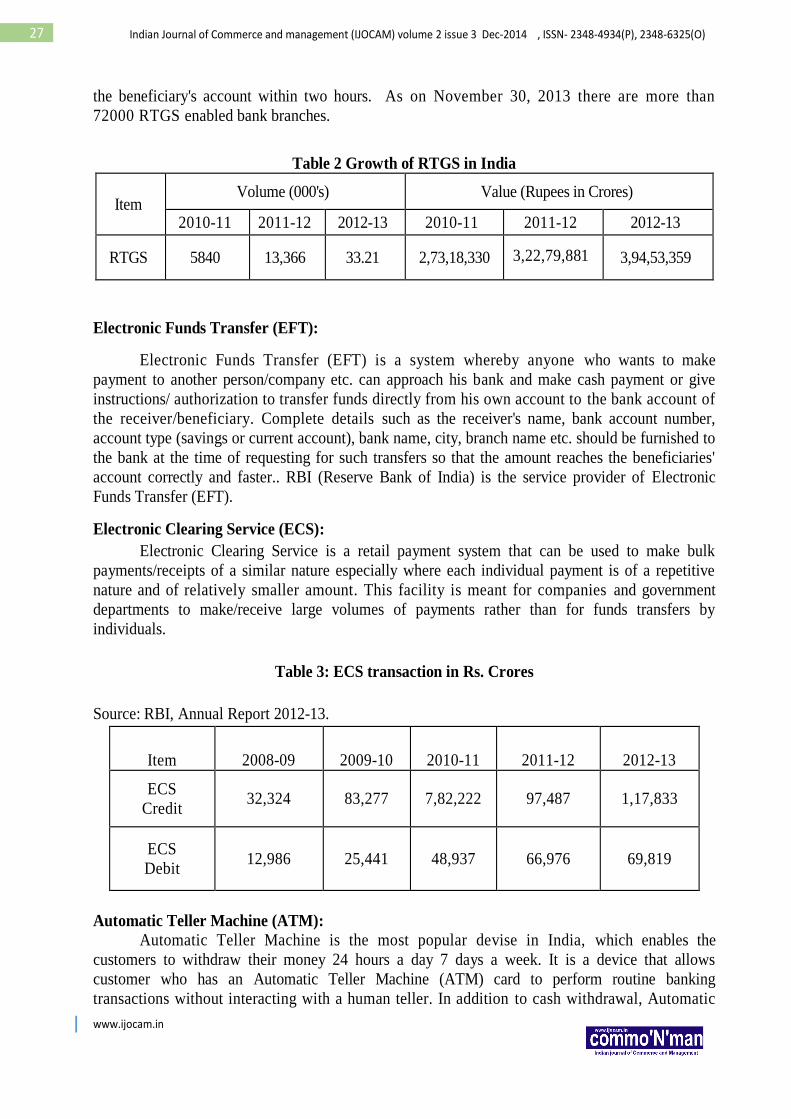

Real Time. Gross Settlement (RTGS):

Real Time Gross Settlement system, introduced in India since March 2004, is a

Interlink Research Analysis system through which electronics instructions can be given by

banks to transfer funds from their account to the account of another bank. The (RTGS) Real

Time Gross Settlement system is maintained and operated by the RBI and provides a means of

efficient and faster funds transfer among banks facilitating their financial operations. As the name

suggests, funds transfer between banks takes place on a 'Real Time' basis. Therefore, money can

reach the beneficiary instantaneously and the beneficiary's bank has the responsibility to credit

www.ijocam.in

27 Indian Journal of Commerce and management (IJOCAM) volume 2 issue 3 Dec-2014 , ISSN- 2348-4934(P), 2348-6325(O)

the beneficiary's account within two hours. As on November 30, 2013 there are more than

72000 RTGS enabled bank branches.

Table 2 Growth of RTGS in India

Item Volume (000's) Value (Rupees in Crores)

2010-11 2011-12 2012-13 2010-11 2011-12 2012-13

RTGS 5840 13,366 33.21 2,73,18,330 3,22,79,881 3,94,53,359

Electronic Funds Transfer (EFT):

Electronic Funds Transfer (EFT) is a system whereby anyone who wants to make

payment to another person/company etc. can approach his bank and make cash payment or give

instructions/ authorization to transfer funds directly from his own account to the bank account of

the receiver/beneficiary. Complete details such as the receiver's name, bank account number,

account type (savings or current account), bank name, city, branch name etc. should be furnished to

the bank at the time of requesting for such transfers so that the amount reaches the beneficiaries'

account correctly and faster.. RBI (Reserve Bank of India) is the service provider of Electronic

Funds Transfer (EFT).

Electronic Clearing Service (ECS):

Electronic Clearing Service is a retail payment system that can be used to make bulk

payments/receipts of a similar nature especially where each individual payment is of a repetitive

nature and of relatively smaller amount. This facility is meant for companies and government

departments to make/receive large volumes of payments rather than for funds transfers by

individuals.

Table 3: ECS transaction in Rs. Crores

Source: RBI, Annual Report 2012-13.

Item 2008-09 2009-10 2010-11 2011-12 2012-13

ECS

Credit 32,324 83,277 7,82,222 97,487 1,17,833

ECS

Debit 12,986 25,441 48,937 66,976 69,819

Automatic Teller Machine (ATM):

Automatic Teller Machine is the most popular devise in India, which enables the

customers to withdraw their money 24 hours a day 7 days a week. It is a device that allows

customer who has an Automatic Teller Machine (ATM) card to perform routine banking

transactions without interacting with a human teller. In addition to cash withdrawal, Automatic

www.ijocam.in

28 Indian Journal of Commerce and management (IJOCAM) volume 2 issue 3 Dec-2014 , ISSN- 2348-4934(P), 2348-6325(O)

Teller Machines (ATMs) can be used for payment of utility bills, funds transfer between accounts,

deposit of cheques and cash into accounts, balance enquiry etc.

Point of Sale Terminal:

Point of Sale Terminal is a computer terminal that is linked online to the computerized

customer information files in a bank and magnetically encoded plastic transaction card that

identifies the customer to the computer. During a transaction, the customer's account is debited and

the retailer's account is credited by the computer for the amount of purchase.

Tele Banking:

Tele Banking facilitates the customer to do entire non-cash related banking on telephone.