Embed Size (px)

Citation preview

Report No. 7984-JO

JordanEnergy Sector Study(In Two Volumes) Volume II: Background PapersFebruary 7, 1990

Country Department IlIlIndustry & Energy Operations DivisionEurope, Middle East and North Africa Regional Office

FOR OFFICIAL USE ONLY

Document of the World Bank

This document has a restricted distribution and may be used by recipientsonly in the performance of their official duties. Its contents may not otherwisebe disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTSCurrency Unit Jordan Dinars (JD)JD 1.00 = 1,000 filsJD 0.500 US$1.00 (March, 1989)JD 1.00 = US$2.00

WEIGHTS AND MEASURES1 meter (m) = 3.281 (feet)1 kilometer (km) = 0.621 mile1 kilogram (kg) 2.205 pounds1 ton (1,000 kg) - 1.102 short ton

- 0.984 long ton1 barrel (bbl; o.159 m3) - 42 US gallons1 kilowatt (kW) = 1,000 watts1 megawatt (MW) 1,000 kW1 kilowatt hour (kWh) 1,000 watthours1 gigawatt hour (GWh) = 1,000,000 kWh - 1,000 MWh (10 6kWh)1 kilovolt (kV) 1,000 volts1 kilovolt ampere (kVA) = 1,000 volts amperes1 megavolt ampere (MVA) 1,000 kVA1 kilo liter (103 liters) - 6.28981 American barrels1 cubic meter - 6.29 barrels1 bbl oil = 0.1349 tons oil1 cubic meter 6.28976 US bbl1 tonnes = 8.17 US1 metric ton - 0.77 cubic meters

GLOSSARY OF ABBREVIATIONSATPS - Aqaba Thermal Power StationEMENA - Europe, Middle East and North AfricaESS - Energy Sector StudyFBC - Fluidized Bed CombustionHTPS - Hussein Thermal Power StationICB - International Competitive BiddingIDECO - Irbid District Electricity CompanyIAEA - International Atomic Energy AgencyIOC - International Oil CompanyJEA - Jordan Electricity AuthorityJEPCO - Jordanian Electric Power CompanyJPRC - Jordan Petroleum Refining CompanyLPG - Liquefied Petroleum GasMAED - Model for Analysis of Energy DemandMEMR - Ministry of Energy and Mineral ResourcesMOP - Ministry of PlanningPCIAC - PetroCanada International CooperationNRA - Natural Resources AuthoritySOE - Statement of Expendituretoe - tons of oil equivalentWASP III - Wien's Automatic System Program Package III

Financial Year - Calendar Year

FOR OFFICIAL USi ONLY

JORDAN

ENERGY SECTOR STUDY

Abstract

The oblective of this report is to assist GOJ develop a refined energysector development strategy. It reviews changes in Jordan's energy sector inlight of macro-economic situation; institutional changes, current energypricing policies, demand management and conservation needs; energy supplydiversification; and the prospects for developing primary energy resourceswithin Jordan. The report analyzes issues of energy demand projections,exploration and development of domestic energy resources, institutional andoperational efficiency and energy sector investment and financing. It focuseson ke factors: human resources development, debt reduction and the expansionof the private sector role in energy investment and environmental protection.The preferred strategy is a continuation of GOJ's policies: energyconservation; the development of indigenous resources to substitute forimports; economic pricing; efficient investment and operations; and theremoval of institutional rigidities. The report recommends continuingpetroleum products and electricity pricing reforms, restructuring of sectorinstitutions to improve efficiency and expanding the role of the privatesector in energy sector development projects.

The study was undertaken as a collaborative effort of the World Bank and theGovernment of Jordan. The World Bank core group for this report was R.Vedavalli (Task Manager), J. Maweni, A. Adamantiades and P. Cordukes (PowerSubsector); U. Kirmani (Oil and Gas, and Oil Shale); and R. Berney (PetroleumRefining). The core Jordanian counterpart team: R. Aburas (Team Coordinatorand Energy Conservation), A. El-Saadi (Joint Team Coordinator), M. Zaharan, M.Dabbas and M. Talal (Macroeconomic Prospects); Ali Anani (Renewable Energy),M. Faisal and M. Abu-Aqola (Energy Demand, Energy-Economy Model, and PetroleumRefining); F. El-Karmi, F. Kharbhat, N. Idris, Z. Khamis (Power Subsector andWASP model), M.A. Nabulsi and K.H. Khal4di (Oil and Gas); M. Abu Ajamieh, F.El-Faiz, W. Jaouni, and M. Bseaso (Ot' Shale).

r This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

JORDAN'

Energy Sector Study

Background Papers - Volume II

Table of Contents

Background Paper 1: Oil and Natural Gas Exploration and Development ... 1

Backgrouid Paper 2: Oil Shale Development ............................. 33

Background Paper 3: Petroleum Refining, Storage and Transportation .... 44

Background Paper 4: Power Subsector .68

Background Paper 5: Renewable Energy .136

Background Paper 6: Energy Conservation ........ ............... . ... 145

Maps: IBRD 21350IBRD 21349IBRD 21351

aQ'

Background Paper 1

Oil and Natural Gas Exploration and Development

Table of Contents

Page No.

Introduction ...... I............................................. 1Role of Oil and Gas in Jordan's Energy Sector ..... .............. 1Regional Geology and Exploration Areas .......................... 2Summa'y Overview of Exploration Plays ........................... 5Review of Exploration Activities in Jordan ...................... 6Production Sharing Agreements ................................ 9Government's Strategy for Oil and Gas Exploration .... ........... 10Review of Current Status ........................................ 11Future Strategy to Accelerate Exploration, Exploitation andDevelopmeint Activities ........................................ 13

Natural Gas .............. ....................................... 15Geology and Risha Field Evaluation .............................. 15Future Program ............ ...................................... 15Reserve Estimates and F4ztor Determining Production Profile .15Estimation of Potential Demand for Gas .......................... 16Institutional Aspects ............................................ 17Current Status of Natural Resources Authority ..... .............. 17Proposals to Improve Oil and Gas Sector Activities .... .......... 17Revised Role of N.R.A. .......................................... 18Petroleum Law ........... 18Proposed Organizational Structure of an Oil Company .... ......... 19Natural Gas Pricing ............................................. 20Recommen'ed Pricing Approach .................................... 20Investment Strategy ............................................. 20Investment in Oil and Gas Exploration and Production Between1986-1990 . .................................................... 20

Investment for Exploration and Development (1990-2000) .... ...... 20

AnnexesAnnex 1.1 Oil and Gas DevelopmentAnnex 1.2 Oil and Gas Exploration and DevelopmentAnnex 1.3 Seismic Surveys in Different Exploration AreasAnnex 1.4 Distribution of Regions and Areas

Tablk of Contants (cont'd)

Annex 1.5 NRA Oil and Gas Exploration ExpendituresAnnex 1.6 Petroleum LawAnnex 1.7 Terms-of-Refererce for a diagnostic study of Risha Gas Reservoir

Organization Chart: Natural Resources Authority (Present Status)Organization Chart: Natural Resources Authority (Proposed Status)

JORDAN

Energy Sector Study

Background Paner I

Oil and Natural Gas Exploration and DeveloRment

Introduction

1.01 The Role of Oil and Gas in Jordan's Energy Sector. Jordan is totallydependent on imported crude oil to meet the bulk of its energy requirements.Petroleum consumption is expected to grow at an average rate of 31 per annumin the next ten years. Crude oil imports are projected at about 3.4 milliontoe in 1990. as compared with about 3.1 million toe in 1988. Oil importsaccount for 501 of projected exports in 1990 and will have a significantimpact on the balance of payments. It is, therefore, clear that Jordan willincreasingly depend on imported petroleum in the foreseeable future unlesssignificant reserves of recently discovered oil and gas resources are provenand addditinal discoverias arc mrnde thrcugh the ongoinr. e.pl^rat4^n cempvign.

1.02 Jordan's presently known indigenous energy resources consist of largeoil shale deposits and tar sands, modest hydro potential (87 Gwh per year),and low geothermal sources. To date no commercially exploitable coal, orlignite reserves have been discovered. Only small deposits of oil werediscovered in Azraq in 1984, and some oil shows were tested in Sirhan area in1988. In 1987 gas was discovered in the Risha area, however, commercialreserves have yet to be proven. It is therefore clear that to date, with theexception of wind and solar energy, Jordan's resources of proven commercialand renewal energy are modest.

1.03 With the addition of recent knowledge in the subsurface geology of thepotential hydrocarbon bearing areas in Jordan's sedimentary basin, and thepresence of oil and gas in some areas (e.g. Sirhan and Risha), the prospectsfor petroleum resources have enhanced significantly. The interest by a numberof foreign oil companies, and recently signed exploration and productionsharing agreements with the international oil companies (IOC's), demonstratestheir optimism in proving Jordan's oil potential.

-2-

1.04 Regional Geology. Jordan covers an area of 96,500 sq km in thenorthwestern part of the Arabian peninsula, of which about 75,000 sq km iscovered by sedimentary rocks ranging in age from Lower Cambrian toQuarternary. These sediments attain a thickness of more than 12 km in theJordan Rift area, and betwean 6 and 8 km in other areas.

1.05 While most of the Arabian peninsula is characterized by uniformmorphology, the northwestern part, where Jordan is located, shows considerablevariations with distinct physiographic properties. On this basis, Jordan canbe broadly divided into the following geological regions:

(i) The Central Plateau

It is bordered in the west by ridges that follow the Dead Sea graben,grading into flat lands in the east. This region covers an area of10,527 sq km south of Amman. The south and southw.est is mainlyunderlain by sedimentary rocks of Mesozoic age with thickness rangingfrom 3,000 to 4,000 meters. These rocks contain an abundance ofclastics and only minor shale deposits. In the eastern part, oldersedimentary formations are overlain by very thick Cretaceous andTertiary rocks that can attain a thickness of several thousand meters.Harls, limestones and dolomites predominate, but there are some thicksandstones which are potential reservoir rocks- Source and cap rocksare well estnblished. Surface geolegic'l -Aork and scs:mic studiesindicate that traps for oil accumulation could be present. To date theonly major occurrence of petroleum are the huge oil shale deposits ofEl Lajun and Sultani. Other than that, there has so far not been muchevidence of large oil bearing reservoirs in this area. Further studiesare needed to identify the subsurface hydrocarbon accumulations.

(ii) Northeastern Plateau (Risha)

It is a monotonous flat area which extends into Syria in the north,Iraq in the east and Saudi Arabia in the south. The area within Jordancomprises some 15,250 sq km between the Basalt plateau and theinternational border. Zxtensive seismic surveys indicate that asedimentary column extending in thickness to 7,000 meters exists with awidespread angular unconformity separating Mesozoic and Paleozoicrocks. Exploratory wells on Mesozoic anomalies in the western part ofthe Risha region revealed the presence of thick Silurian (Paleozoic)hydrocarbon source rocks beneath the Mesozoic unconformity. Detailedanalysis has indicated that source rock sections thicken towards theeast and cover most of the Risha area. The geochemical analysis of thewell data indicate the possibility of a petroliferous Paleozoic basinin the Risha area. In 198f, NRA discovered natural gas in Risha andproved the existence of gaseous hydrocarbons in Ordovician sandstonesin this area at about 2,700m. Other areas within the Risha regionappear to offer good prospects for finding hydrocarbon accumulations.

Recent improvemerts in processing the seismic data have shown thac thedeep Paleozoic structures can be mapped. This opens up a series of newdeep prospects which could prove to be oil bearing. NRA is condiuctingextensive seismic data evaluation in cooperation with PetroCana5aInternational Cooperation (PCIAC) to assess the hydrocarbon potentialof this area.

(iii) The Mountain _id-t along the Dead Sea Graben and Northern Highlands

This area forms part of a regional geological trend which extends fromEgypt and plunges northward into the I!mascus Basin in Syria. Thethick sediments are of Mesozoic age, mostly of marine origin and thusfavorable for oil generation. Reservoir rocks and seal rocks areevidenced in Triassic and Jurassic sequences. Recent seismic data andlandset interpretation by NRA suggest that Jurassic and Triassicformation may offer good hydrocarbon prospects. Further detaileds:ismic surveys followed by exploratory drilling is required toinvestigate the hydrocarbon potential of this area.

(iv) The Aaaba-jordan Rift Valley

This is a narrow depression extending from Aqaba, 360 km to the north(Lake Tiberies). It is a highly disturbed zone, over 300 km long and14-30 km wide, and contains a sedimentary sequence over 10,000 metersin thiclties. Xost likely, Paleozoic and Mesozoic sediments could bepresent at the base, but the late Tertiary sedimentary sections attairgreat thickness. Included in this area are isolated deposits of saltand other evaporates with a thickness of some 5,000 meters.

Flanking the valley are some oil and gas seepages which may be linkedgeochemically with rich upper Cretaceous source rocks on both flanks.Strong subsidence, particularly during the late Tertiary age, togetherwith intensive salt flow structures suggest that some structural trapsfor hydrocarbons may have been formed. The seismic data obtained todate is not sufficient to map deeper horizons because thick salt layersoverlap these formations. So far oil exploration work in this area hasbeen inconclusive.

(v) Southern Mountain Desert

This area is characterized by crystalline basement outcrops with littleoil potential. t'o the north, sedimentary sequences of Paleozoic andMesozoic ages could be favorable to oil occurrences. Detailed seismicand other studies are required to study the prospects for hydrocarbonexploration in this area.

- 4_

(vi) &rth Pla-teau-Basalt Province

The large basalt plateau covering over 11,000 sq km in northeasternJordan is a Mesozoic basinal area. On the eastern flank of the Basaltplateau, gentle regional dips prevail toward the west in a Mesozoicsection which thickens westwards. It is bqlieved that the Basaltplateau overlies a graben area similar to the Azraq region. Basaltlavas occur at the surface over a stretch of 700 km from Syria throughJordan into Saudi Arabia, with a maximum thickness of basalt of about1,00) meters. However, most of the area is covered by about 100 metersof basalt.

The hydrocarbon prospects in this area are considered similar to thatof the Azraq area; and similar plays are anticipated with theCretaceous source rocks feeding into the Cretaceous and Jurassicsandstones and carbonates. Due to deeply weathered basalt flows,accessibility has hampered exploration in the past. However,Petrofina, a Belgian company, has recently acquired concessions overthis area and, by utilizing the latest techniques, has overcomelogistics problems and run extensive seismic surveys in the concessionarea.

(vii) !' -an.Area

The Paleozoic prospects appear most interesting for hydrocarbonexploration in this basin since the Mesozoic and Tertiary sections arethin and presumably immature. Silurian shales, which are up to 500meters thick in exploratory wells drilled so far, are considered to bethe source rock for this large Paleozoic basin. Recently NRA has foundoil in Wadi Sirhan test wells. Detailed seismic surveys are needed todefine the potential hydrocarbon traps. The Japanese have recentlysigned a cooperation agreement with NRA to further explore the northernpart of the Sirhan area.

(viii)Azrag Area

The Azraq basin lies between the high central plateau on the west andthe basalt plateau on the east. The first oil discovery at Hamza wasmade by NRA in this basin. Some 20 wells have been drilled on thefield which produces about 500 bbl/day oil from cretaceous limestonesand dolomites.

The Fuluk growth fault is the main structural feature responsible forthe development of a NW-SE trending graben. Because of the extensivefaulting, the traps are structural closures in many fault blocks.

-5-

In additional to the proven oil accumulations in the Hamza area,located on down side of the Fuluk fault, there are shallower prospectson the ward block which need additional detailed seismic andexploratory drilling to prove oil reservoirs.

1.06 Exploration Artas. As discussed in pf.ra 1.05 above, Jordan canbe divided into a series of broad plateau-like ar.hes and gentle desertcovered by basins. For exploration purposes NRA has divided the abovegeological regions into ten areas (see Annex 1.1).

A) Precambrian OutcropB) Basalt PlateauCl) Azraq DepressionC2) Risha AreaC3) Sirhan AreaC4) Jordan ValleyCS) North HighlandsC6) Aljafr DepressionC7) Central PlateauC8) Southern Desert Area

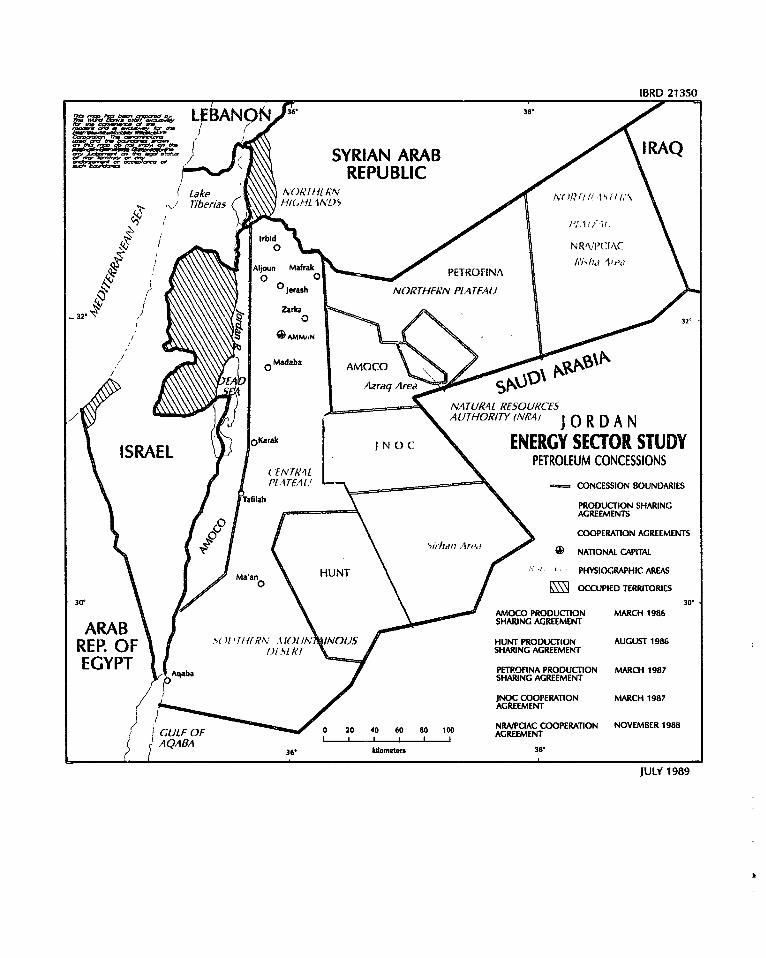

1.07 NRA has signed production sharing agreements w;hn several IOCs(para 1.23) in some of the areas (e.g. B, Cl, C4 and C6) and is continuingexploration promotion in the remaining open areas (Annex 1.4 and IBRD Map:21350).

1.08 Jordan is favorably located between the Precambrian outcrop beltand the rich oil-producing area of the Gulf Coast. This is a prime area forfinding oil and gas in Mesozoic and Paleozoic sediments, as evidenced by thefollowing features: (a) a favorable environment for oil hydrocarbongeneration, oil seepages, and accumulation is seen in the numerous oil and gasshown in the wells drilled, asphalt impregnations and extensive oil shaledeposits; (b) the presence of source rocks at different stratigraphic levelsranging from the Tertiary to the Paleozoic is well established. The abilityof some of these potential source rocks to generate hydrocarbons in differentbasins is demonstrated by the discovery of oil in tne Cretaceous of the Azraqbasin, the Ordovician in the Sirhan area and the natural gas in the Ordoviciansands in the Risha area, as well as in the live oil and asphalt seepages inthe Dead Sea area. (para 1.05); (c) potential reservoir rocks are alsoabundant. There are substantial thicknesses of clean Paleozoic and LowerCretaceous sands, as well as reservoir potential in Triassic and Cretaceouscarbonates; (d) seals are present at different levels ranging from LowerCambrian to the Cretaceous, and a very thick Silurian shale covers the rest ofthe Paleozoics in the Risha and Sirhan area; (e) traps can be found instructural anomalies in the different sedimentary areas. These can beanticlinal features, tilted fault blocks and saltdomes, as may be found in theAzraa. Risha and the Jordan rift areas; and (f) stratigraphic plays include

-6-

the possibilities of sand pinchouts, thinning over highs and lensing in thePaleozoic in Risha and Sirhan areas, as well as the possible development ofporous facies (reefs, dolomitized zones) in the Mesozoic of the northhighlands area.

1.09 Review of Exoloration Activities in Jordan. The explorationactivities in Jordani can be divided into the following phases.

(a) Phase I: Exploration by International Oil Companies (IOCs)1946-1978)

(b) Phase II: by NRA only (1976-current)

(c) Phase III: NRA and International Oil Companies (IOCs)(1986-current)

Phase I: Exploration by International Oil Comganies (1946-1978)

1.10 Between 1946 and 1978 seven foreign oil companies acquiredconcessions in Jordan. Geological and geophysical surveys were undertaken,and 14 exploratory wells were drilled. In several wells, oil and gas showswere observed. However no commercial oil and gas discoveries were made. As aresult, by the mid-7Qs all internationa. oil companties abandoned explorationwork in Jordan.

1.11 The inability of various concessionaires to locate commercialhydrocarbon deposits could be attributed to several reasons, namely: (i) theinsufficient and poor quality of the seismic data gathered; (ii) the faultylocation of exploration wells, based on limited geological and geophysicaldata; (iii) insufficient capital expenditure allocations to meet contractualobligations; and (iv) the disappointment in not striking "mid-east" type oilreserves in exploration efforts.

Phase II: Exploration by Natural Resources Authority (NRA)(1976-current)

1.12 In 1965, the Government established the Natural ResoarcesAuthority (NRA) to undertake investigations of mineral resources anid conductgeological surveys. NRA started direct participation in the exploration forhydrocarbons in 1976, only after the Government was convinced that foreign oilcompanies were not interested in further exploration and that in order tofully evaluate the oil and gas p:tential, a national exploration effort fundedby the Government was necessary.

1.13 NRA started by a revision and reassessment of all previousgeological and geophysical data, with the assistance of foreign consultants.Later NRA hived foreign companies under service contracts to condu%.c extensive

geophysical surveys using the latest techniques and reprocessing all previousdata. In 1980 NRA made another effort to attract foreign companies in oilexploration by compiling and offering a complete geological and geophysicaldata package. The response by foreign oil companies was very disappointing.As a result, NRA embarked upon an exploration plan utilizing funds allocatedby the Government from its own resources.

1.14 Since 1980 NRA has embarked on its own seismic work andexploration drilling program. It shot over 14,700 km seismic surveysutilizing international geophysical service comipanies.

1.15 Other oil exploration work was carried out by Yugoslavia's Naftagas under an agreement signed in 1981 for the supply of ar oil drilling rigand for exploration drilling in Azraq area. The first well discovered oil insmall quantities at 2,650 feet near Azraq. NRA stepped up its drillingactivities by hiring two more drilling rigs from Rompetrol (Romania). Modestreserves of oil were found in Cretaceous limestones in the Hamza field in1984. However, because of the geological complexities of the Azraq area,further exploration efforts by NRA were suspended until a comprehensive andintegrated study covering geological, geophysical and well data was completed.In the Sirhan area, NRA tested 43 deg. API oil at 1,398 meters from Ordoviciansandstones in Wadi Sirhan Well No. 4. The data obtained is being studied, andfurther appraisal drilling is planned.

1.16 In 1987, NRA made a gas discovery at Risha when well No. 3 test idry sweet gas at 15 million cu. ft/day. To date NRA has drilled fourteenwells in Risha. Some of the wells have shown the presence of gas. However,only two wells have been tested to provide commercial quantities of gas.Additional studies are required to evaluate the subsurface data gathered todate in order to delineate the limits of the Risha field and to determine gasreserves. Currently, NRA is continuing its exploratory drilling with two rigsin the Sirhan and Hamza area. It is continuing seismic surveys and dataanalyses with the collaboration of the PCIAC in the Risha and Sirhan area.Other exploration is being undertaken by IOCs under production sharingagreements (para 1.23).

1.17 GCJ has spent over US$220 million for oil/gas exploration fromits own resources. The annual expenditures are given in Table 1. So far,except for small oil and gas finds in Hamza and Risha, respectively, and someencouraging oil shows in the Wadi Sirhan area, no commercial production hasbeen achieved.

- 8 -

Table 1&RDloration Expenditures

Year USS Million

1977 0.21978 2.61979 0.8.980 0.91981 15.11982 14.11983 13.01984 13.91985 35.81986 43.51987 35.61988 44.4 1/

1/ Budget Allocation.

- 9 -

Phase III: Extloration by NRA/IOCs (1986-current)

1.18 In order to share the exploration risks and to benefit from the moderntechnology available to IOCs, the Government has directed its explorationstrategy towards: (a) inviting IOCs to participate in exploration in theidentified sedimentary areas isee Annex 1.3) by preparing explorationpromotion packages and offering attractive financial terms (under productionsharing agreements); (b) collaborating with PCIAC for seismic dataacquisition, processing and the interpretation of geological complexities; and(c) continuing its own exploration program in some of the areas not coveredunder the production sharing agreements.

1.19 In 1987 NRA entered into a technical cooperation agreement with PCIACfor the technical assistance to (a) shoot 6,000 line km seismic surveys in theRisha and Sirhan area and (b) reprocess and analyze about 8,000 km of seismicdata available with NRA with a view to preparing an exploration promotionpackage for the Risha area. NRA also hired a Canadian deep drilling rig totest the deeper horizons in the Risha area. The geological data obtained fromthe wells drilled in Risha is being evaluated by NRA.

Production Sharing Agreements (PSA)

1.20 In order to step up its exploration activities, in 1985 the Governmentinvited foreign oil companies to enter into a production-sharing agreementwith NRA on eight idontified sedimentary areas (IBRD Map: 21350). Under theBank financed Energy Development Project (Ln 2371-JO), technical assistancewas provided to NRA to prepare a Petroleum Promotion Package and to prepare amodel concessions agreement with less stringent financial commitments, in viewof the high risks involved. Based on such a model contract, NRA invitedforeign oil companies to participate in the production sharing agreements.

a) Amoco Jordan Petroleum

1.21 In March 1986, Amoco Jordan Petroleum, a subsidiary of Amoco (U.S.),signed an agreement covering 4,400 sq km in Jordan's Valley and Dead Seaareas, and 6,550 sq km in the Azraq area, excluding Hamza and the Wadi Rajilarea, which NRA is exploring itself. (IBRD Map: 21350). Over a 7-1/2 yearexploration period, Amoco is committed to carry out geological, geophysicaland geochemical surveys and drill five wells. Amoco started its operations inlate 1986 and has conducted gravity and magnetic surveys, as well as a landsetstudy of both blocks. Detailed geological and geochemical studies areunderway. Amoco spudded the first exploratory well in November 1988. InDecember 1988 OMV, Austria was formed with Amoco for a 30% interest in thecontract. So far Amoco has drilled two wells, which did not encounter anyhydrocarbon. Amoco has therefore terminated their activities and haveassigned their share to OMV. OMV is looking for other partners to continuewith PSA.

- 10 -

b) Jordan Hunt Oil Comnanv (USA)

1.22 Jordan Hunt Oil Company was awarded an exploration license over 8,806sq km in the southern area bordering Saudi Arabia in 1986 (IBRD Map: 21350).Hunt is committed to spend about US$20 million over a 7-1/2 year explorationperiod for geological, geophysical surveys and to drill four exploratory wellsto test deeper horizons (about 15,000 feet). Hunt started seismic surveys in1987 The first wildcat well was drilled to 13,360 feet. This well did notfind any hydrocarbons. In December 1988, BP farmed in with Hunt a 50%interest in the contract. Hunt/BP still find merit in the area and haveexpressed their desire to find a third partner before eirtering into a secondexploration phase under PSA.

c) Petrofina (Belgium)

1.23 Petrofina was awarded a seven-year exploration license covering anarea of 12,650 sq km in the Basalt plateau (IBRD MAP: 21350). It has afarm-in agreement with ARCO (Petrofina 50X, ARCO 50%). Petrofina is theoperator and is committed to spend $9 million in first three years and $6million in the subsequent two-year period. Petrofina is currently conductingseismic surveys. It is the first time that any company has undertaken such atask in the Basalt area. Petrofina expects to obtain good seismic resultsfrom the deeper horizons similar to those found in the Azraq area, which mayhave considerable oil potential.

(d) Japan National Oil Company (JNOC)

1.24 In November 1988, the Japanese National Oil Company (JNOC) signed anagreement with NRA to conduct extensive seismic surveys in the North SirhanConcession area. JNOC plans to complete these surveys within 18 months. Ifthe results are encouraging, JNOC expects to attract Japanese companies toenter into production sharing agreements for further exploration in theirarea.

(e) OKV (Austri-a)

1.25 OMV signed an assistance agreement with NRA to study the southwestSirhan area with an option to negotiate a PSA at the end of these studies,which are expected to be completed by March 1990. So far, OMV has done 750line kn seismic in the area.

The Government's Strategy for Oil and Gas Exnloration

1.26 Since the oil price increases of 1973 and 1979, the Government ofJordan has emphasised the exploration and development of domestic hydrocarbonresources. The Government's strategy is to attract international oilcompanies to join in the exploration effort, sharing the financial risks andbringing state-of-the-art exploration technology into Jordan, and, at the same

- 11 -

time, carrying on its own exploration program in open areas. This strategyhas so far proved to be successful in that production sharing agreements weresigned in the period 1986-8C with several internationally known oil companies.NRA has discovered modest oil reserves in the Azraq, and more recently in theSirhan areas, (para 1.22) and natural gas was discovered in the Risha area.Many international oil companies (over 40) have visited Jordan to review theavailable technical data with NRA.

1.27 The Government is continuing its strategy by vigorously implementingits exploration promotion program and the adoption of an open-door policy forthe international oil industry. Currently NRA, in cooperation with PCIAC, isundertaking an exploration promotion campaign by making presentations toAmerican and Canadian oil companies in Houston and Calgary, respectively.

1.28 Review of Current Status

(i) Incentives for Attracting Private ComRanies

The Government, through NRA, will continue the open-door policyfor the private oil companies, giving them free access to thelarge technical data bank now available with NRA. The wealth ofgeological and seismic data accumulated over the years proved tobe very useful in attracting many well-known companies in the oilindustry and provided more favorable understanding of the geologyof Jordan and its petroleum potential. Furthermore, NRA adopteda flexible attitude in its model contract; during actualnegotiations with the oil companies, it provided enoughincentives to attract investments in oil exploration in Jordan.NRA is continually reviewing its policies and is trying todevelop the most competitive position possible for Jordan tocontinue to encourage exploration.

(ii) Key Features of the Model Agreement

Jordan is currently using a model production-sharing agreement,which was originally based on the Egyptian model agreement. Itwas modified to suit the different geological, fiscal and legalconditions in Jordan. The model contract appears to besatisfactory for exploration and development in Jordan. However,NRA is continuing its efforts in updating and improving thismodel contract in all its aspects. Recently, NRA through theUnited Nations Aid Program (UNTDP) hired a consulting firm toreview the model agreement. This review was completed in October1988. Some of the recommendations for the improvements have been

accepted by NRA and will be incorporated in the existingmodel contract.

- 12 -

The key features of the Model Agreement are:

a. Fiscal Terms

- Production sharing based on a 40X cost-recovery limit and aprofit oil split with a sliding scale based on the levels ofproduction. In case of a gas discovery, the cost-recoverylimit is 501, and profit gas is split 70:30 in N.R.A's favorfor all levels of production.

- A signature bonus.

- Production bonuses.

- Payment for exploration data.

- Annual payments for the training of NRA professionals andthe transfer of technology.

- Corporate income taxes included in NRA's profit oil.

- Customs exemptions on all items used for petroleumoperations.

The cost-recovery limit, profit oil split, payment forexploration data and bonuses are all negotiable items.

b. Non-Fiscal Terms

- An exploration period of 7 to 8 years divided into threeexploration terms.

- A production period of 25 years, with possible extensions of5 years for oil and 10 years for gas.

- Relinquishments of parts of the original contract area atthe end of each exploration term and the relinquishment ofthe total area at the end of the exploration period, exceptthose areas designated as production areas.

- Right of Export: Contractors have the right to export allpetroleum to which they are entitled and are not required tosatisfy domestic consumption requirements.

Domestic Consumption: Contractors shall be paid in U.S.Dollars the current international market value for anypetroleum sold for domestic consumption.

- 13 -

- Foreign Exchange Control: None.

c. Legal Framework

- All petroleum resources belong to the Hashemite Kingdom ofJordan.

- Law No. 12 of 19t8 organized the Natural Resources Authorityand authorized it to enter into agreements, subject toGovernment approval, with the foreign investors for theexploration and exploitation of petroleum.

- Each negotiated agreement shall become law followingsignature and Government approval.

Future Strategy to Accelerate Exploration. Exploitation and DeveloRmentActivitles

1.29 In recent years considerable progress has been made by NRA inaccelerating exploration in Jordan through its own efforts and in attractingIOCs to explore for petroleum as well. However, considering the extent ofsedimentary basins with potential hydrocarbon prospects, detailed work usingstate-of-the-art seismic techniques is needed to identify deep Mesozoic andPaleozoic sediments and resolve geological complexities, followed by drillingor deep exploratory wells. This would require substantial high riskinvestments.

1.30 It would therefore be prudent for NRA/MEMR to follow a long-termstrategy to meet most of the energy needs of Jordan through finding anddeveloping indigenous hydrocarbon resources on the lines suggested below:

(i) To continue the "open door" policy for IOGs by offering themattractive incentives to participate in the explorationactivities, keeping in view the international petroleum scenario.

(ii) To provide incentives to IOCs in developing known oil and gasdiscoveries, e.g. the Hamza and Risha field, through mutuallybeneficial agreements with NRA in order to maximize theapplication of the latest state-of-the-art technologies; providetraining to the inexperienced Jordanian staff; and assist in thedevelopment of institutions to run oil and gas operationsefficiently.

- 14 -

(iii) To fully evaluate the Risha Gas potential prior to making long-term investment d:.cisions. If sufficient gas reserves areproven, then prepare gas development and utilization plan fornatural gas. All gas-related investments should be based on sucha plan.

(iv) To continue ongoing cooperation with the Petro-CanadaInternational Assistance Corporation (PCIAC), JNOC and similaragencies for the promotion of Sirhan, Risha and other areas.

(v) To continue NRA's own exploration activities in areas notcurrently under contract with IOCs.

(vi) To strengthen the technical expertise of NRA staff inexploration, production and reservoir engineering, gasdevelopment, transmission and distribution, by providing trainingin Jordan and abroad.

(vii) To establish facilities with NRA for advanced geological,geophysical, and geochemical reservoir engineering and gasengineering work by NRA staff.

(viii) To strengthen NRA's role in monitoring the act,v ,Ies of IOCsduring the exploration phase and later participate as partners inthe development of oil/gas production, transport and otheroperations.

(ix) To establish an autonomous national oil company, which could takeover oil/gas functions of NRA. This autonomous entity wouldperform the functions of a petroleum company on the industrystandards and interact with IOCs on an equal professional andinstitutional basis. It would plan for the future development ofhydrocarbon resources in an efficient manner and apply yardstickssimilar to other international petroleum companies for itsperformance.

(x) To change NRA's role to include monitoring and regulating of theactivities relating to geological surveys, mineral surveys, oilshale, and petroleum. NRA should continue with the scientificinvestigations, however, for the economic exploitation of mineralresources; it should also encourage commercially-orientedorganizations, both in public and private sectors. NRA shoulddevelop the capability to advise the Government in preparing andimplementing oil and gas rules and legislation. NRA should alsointegrate the planning of oil and gas resources along with othermineral resources of the country. It should develop the strategyfor strengthening technical expertise in Jordan by continuingresearch and development program and by interacting with otherinternational agencies (e.g. API, Institute of Petroleum,Institute France des Petrole USA, IFP, UK, and other similaragency.

- 15 -

Natural Gas

2.01 Geology and Risha Field Evaluation. The discovery of gas in Risha byNRA in 1987 has renewed the enthusiasm of the Government for finding andexploiting indigenous oil and gas resources. Risha Well No. 3 encounteredcommercial quantities of gas in an Upper Ordovician sandstone reservoir.Seismic data in the discovery area is of poor quality and the conventionalseismic interpretation does not help to define the areal extent of the gas-bearing sand body. Several sedimentological and reservoir geology studieswere carried out in an attempt to define the extent of these sands. Thesestudies indicated that the sandstones have complex distribution representingstacked submarine sand dunes deposited on a basal silstone sheet and orientedin a northeast-southwest direction. Several subsequent diagenetic processesadversely affected the reservoir quality. However, porosity was locallyenhanced by the dissolution of the cementing materials at a later stage.Since the discovery of natural gas in Well No. 3 at about 15 MMCFD ft. perday, NRA has drilled 12 appraisal and delineation wells. Of these, threewells have produced gas in commercial quantites.

Future Program

2.02 While the Government appreciates the need to fully evaluate the limitsof the Risha Gas field and determ'ne gas reserves, it has taken steps toutilize the producible gas from Risha by installing two 30 MW gas turbine-driven power units at Risha field and then transmitted the electricitygenerated through a 132 kV double circuit transmission line to Azraq. Thisline was commissioned in March 1989. The Government has prudently planned toutilize the gas produced during the long-term production tests of the twoproducing wells to determine gas deliverability in power generation, whichwould otherwise be flared during such tests. At the same time, the Governmentis planning to undertake studies for the evaluation of reserves and gasdeliverability from the Risha field in cooperation with PCIAC. The gasproduction data from the wells will be utilized to confirm the amount of thegas reserves. Meanwhile other geological, geophysical and engineering studieswill continue in an attempt to reach a better understanding of the possibleextent of the reservoir sands. If these studies prove the existence ofsizable gas reserves, then delineation wells will be drilled and a developmentplan will be formulated for the full development of the field.

Reserve Estimates and Factors Determining the Production Profile

.03 The preliminary reserve estimate of 58 BCF is calculated on the basisif production tests performed on Risha wells for relatively short periods.These data indicate that these wells could produce up to 20 MMCF/day. Severalhypothetical scenarios for gas reserves and production profiles are possible.These are based upon the assumptions concerning the size of reserves that

- 16 -

might be discovered at Risha. Starting with 58 BCF aa the base case, thefollowing are three possible scenarios:

Year of RecoverableScenario MMSCF/D Production Reserves BCF

I 200 10 730II 100 10 365III 20 3-4 42

2.04 It must be recognized that the above scenarios for the Risha field areconceptual in nature owing to the absence of the detailed geologicalinformation on which the estimates of possible reserves could be based. Ahypothetical rate of addition to the reserves and a rate of field developmentsufficient to support the indicated levels of production has been assumed.For case III, no transmission pipeline is contemplated. The gas produced isassumed to be supplied at the well head, i.e. used at the Risha field gasturbine driven power plant.

2.05 However, in order to establish the reliable gas deliverability of theRisha wells, long-term testing with careful monitoring by experts, preferablyindependent consultants, is needed. This data would be an important input inthe Risha Reservoir Study. Similar long-term tests are required for otherRisha wells which have shown some gas flows (e.g. Risha Well No. 8). Theheterogeneity of the gas sands and continuity of the reservoir would beimportant factors in preparing the production profile from the Risha field.

2.06 Further investigations are needed to determine the reservoircharacteristics, the limits of the reservoir, gas reserves and the factorswhich control gas deliverability. In the meantime, NRA's program for long-term tests would provide the production data for evaluating the reservoir.The data from the first six months of production tests will be crucial forrecalculating the reserves of this gas discovery. It would be prudent todrill only selected appraisals and, based on their results and the results ofthe proposed reservoir study, to make long-term gas utilization plans in orderto minimize the risks regarding the Risha Gas Reserves. It may take up to twoyears to get reliable gas reserves estimates. NRA/MEMR 's tnerefore advisedto set its investment priorities for gas utilization only after the gas supplysituation from the Risha field is determined with some confidence. Suchplanning could later be extended to other sources of gas supply which may bediscovered in the course of ongoing exploration activities in various areas ofJordan.

Estimation of Potential Demand for Gas

2.07 Jordan offers potentially very attractive markets for indigenousnatural gas. Recent sttudies commissioned by MEHR (Bechtel) have visualizedtotal gas demand for the power sector alone at about 347 MMCFD (based on

- 17 -

simultaneous full capacity operation at all the user plants). The Amman andAqaba areas are considered as centers for major gas demand. In addition,natural gas could be used in residential and commercial sectors primarilyreplacing kerosene, LPG and diesel in the major towns. Compressed natural gas(CNG) offers po2sibilities for use in the transport sector.

Institutional AsRects

3.01 Current Status of Natural Resources Authority. NRA was established asa Government agency entrusted to undertake all work related to geologicalsurveys, mineral and hydrocarbon exploration, and the exploration andmanagement of water resources, which in 1983 was handed over to the newly-formed Jordan Water Authority. Since 1978, NRA has been activelyparticipating in oil and and gas exploration activities. In addition to thepetroleum exploration, NRA also handles geological surveys, geologicalmapping, mining, laboratories, geochemicals and other laboratories andoilshale exploration. NRA's lead in the mining sector contributed to thefinding of potash and oilshale and other-minerals such as aluminum . In thesesectors NRA's research and development activities contributed valuablegeological data. NRA's role in mining exploration, scientific studies, andgeological mapping have been technically excellent and should continue tohandle these activities to encourage mineral development by the privatesector.

3.02 Chart: 43931C shows NRA's current petroleum orgauization. Thedirectorate of petroleum is one of eight directorates, each headed by adirector reporting to the Director General. Over the years, NRA has fulfilledan important role in initiating geological surveys and mapping, mineralexploration and exploitation, and in conducting geological, geophysical,geochemical and oil shale studies. During the last decade NRA's directexploration efforts have resulted in small oil and gas discoveries (para1.18). Additionally, NRA has collected useful subsurface data and preparedexploration promotion packages to successfully attract IOCs for petroleumexploration in Jordan.

Proposals to Improve Oil and Gas Sector Activities

3.03 In spite of the extensive exploration activities during the last twodecades, the success ratio of NRA's direct effort has been very low. NRAlacks the capability of a professional petroleum exploration company tocarefully evaluate the exploration risks in a prospective area. Although NRAhas highly qualified individuals among its staff members, NRA is still lackingthe professional, technical and managerial expertise to plan and implement theprograms according to industry standards. Such weaknesses exist in almost alldisciplines necessary to run an efficient operation. While expertise can behired or provided through a discreetly planned training program, by the verynature of its set up, NRA will still not develop into an entity responsiblefor efficient, cost effective and profit motivated planning, unless it is

- 18 -

reorganized as an autonomous commercially-oriented petroleum organization withfinancial independence and a goal-oriented strategy. Further, in order toachiave its goals, NRA should be able to attract the right talent withadequate incentives in its work force.

3.04 As mentioned above, with the expansion of oil and gas explorationactivities, the formulation of an independent national oil company is aprerequisite for effective petroleum operations. The shareholding of such acompany can initially be entirely with the Government, with a commitment fordivesting some of these holdings to the private sector, both national andforeign, in order to attract much needed capital. The newly restructuredcompany would operate with a commercial focus, like any other oil company inJordan, and would be subject to the same laws as other petroleum companies.

The major functions of this company are Eoreseen as:

(i) The exploration and development of oil and gas fields.

(ii) Production-sharing partnership with IOCs.

(iii) The promotion of acreage to IOC's for further exploration.

(iv) Natural gas operations and sales.

(v) Economic evaluation and corporate planning.

(vi) Financial control

(vii) Personnel management

(viii) The training and transfer of technology to Jordanians.

Revised Role of NRA

3.05 NRA should be reorganized to act as an arm of the Government to devisepolicies, forurjlate legislation and coordinate mining, geology and energysector work in Jordan. It should monitor the execution of the Government'spolicies. NRA should continue to perform its role in monitoring andregulating the oil and gas operations and should continue to advise theGovernment in formulating safety, environment and other codes relevant to theoil and gas industry.

Petroleum LaW

3.06 It is also necessary to examine the need for reformulating thePetroleum Law to improve the efficiency of the proposed organization, and itsrelations with the outside bodies instead of incorporating many details in thelaws of the organization itself. Nevertheless, it is of prime importance to

- 19 -

review on a regular basis the administrative, financial and legal status ofany organization to be able %vo cope with new tasks and to formui,ttestrategies.

Proposed Organizational Structur= of an Oil Com,anv

3.07 The proposed company should be set up as an autonorous organizationresponsible for managing its operations and should be accountable to itsshareholders. NRA and other organizations could be represented on its board.The participation of the private sector should be encouraged, and it shouldalso be represented on the board. This company should have strongprofessional management. The organizational set up should bo aimed atachieving maximum economy and efficiency in all operations. rhe companyshould be accountable for budgeting and expenditures to its board, who wouldapprove the budgets and plans before such expenditures were undertaken. Itshould be free to formulate its personnel policies to attract the best talent.

3.08 The management should be organized in such a manner that there shouldbe clear definition of responsibilities and functions at every level ofauthority. It is envisaged that the General Manager would be responsible forimplementing the board decisions and mrnnaging the company. Each manager wouldbe responsible for the budget allocated, and the tasks proposed to becompleted by his/her department. A conceptual organization chart of theproposed company is attached (Proposed Organization Chart for an Oil Company).It is based on the three levels of management with the authority and controlfunctions clearly defined at every level. The managers should be responsibleand accountable for the definition and achievement of their goals at apredetermined cost. The development of technical and management expertise atevery level woui.d be the task of the respective departmental manager.

3.09 Periodic review by senior management and close interaction would beneeded to ensure. that the objectives set out were being achieved with economyand efficiency. The proposed organization should provide the professionalenvironment for Jordanian professionals to freely apply their expertise toachieve the goals set for them. Additionally, training would be provided tothe younger Jordanian staff to keep them abreast of the latest state-of-the-art technology by interacting with specialized agencies both at home andabroad.

3.10 Prior to the formation of a new oil company, the structure, financialregulations, management and technical responsibilities of the proposedorganization should be studied carefully. It is suggested that a managementconsultant be hired to review the present organization of NRA and propose theorganizational setup, and formulate rules and regulations and job descriptionsfor running the proposed entity. The Government should review therecommendations regarding the proposed entity and prepare an implementationplan.

- 20 -

Natural Gas PricIns

4.01 Recommended Pricing Asp_pach. An appropriate strategy for natural gosdevelopment should have as its main objective the maximization of ret benefitsfrom the use of the country's exhaustible gas resources. This objestive hasthree important dimensions, each of which implies certain pricing principles.First, there must be incentives to promote the efficient use of gas. Gasprices must neither be so high as to inhibit consumption (especially where theusers must incur some cost to switch from other fuels) nor so low as toencourage wasteful use. Secondly, there must be adequate incentives toexplore for and produce the gas. Particularly in cases where the Governmentmay be able to attract foreign capital to assist in gas development, theprovision of an appropriate pricing and contractual framework is essential.Finally, the growth rates of both supply and demand for gas should be rapidand matched to speed up full development of gas resources.

Investment Strategy

5.01 Investment in Oil and Gas Exploration and Production between.19861990. In the National Five-"ear Plan for Economic and Social Development(1986-1990), estimated expenditures in oil and gas exploration are at aboutUS$86 million; however, actual expenditurs will be around US$100 million. Ir.addition to these planned expenditures related mainly to NRA's activities, theIOCs will spend about US$20 million for the same period. NRA's efforts andexpenditures have so far resulted in the oil discovery at Hamza and the recentdiscovery of light oil (43 degree API) in the Sirhan area and the gasdiscovery at Risha. It is anticipated that Risha gas production in 1989 willbe about 5,800 million SCF, which will give an income of more than US$6million per year.

5.02 Heaza field production and income are shown in the following table.These production levels are expected to continue in the nineties.

1986 1987 1988

Production (BBL) 110,661 162,968 109,884Income (J.D.) 414,247 888,520 502,800

Investment for Exploration and Development (1990-2000)

6.01 Based on the assumption that oil and gas exploration activities willcontinue at the current pace, the investment program is estimated to be around$35 million per year. Foreign oil companies' share of investment in oil andgas exploration activities is estimated to be about 50X of the investmentprogram. The investment program includes: (a) public investment by NRA in oil

- 21 -

and gas exploration, development and production activities in open areas; (b)Foreign National Oil Company investments by PCIAC and Japan National OilCompany (JNOC) in oil exploration activities in the Risha and Sirhan areas;and (c) private investment in oil exploration by IOCs in their respectiveconcession areas.

6.02 Public investment by NRA in the oil and gas sector includes: (a)expendit-ures for the continuation of oil production from the Hamza field; (b)the completion of long-term testing and the evaluation of the Risha gas fieldand expenditures on consultancy services for undertaking well services andtechnical studies; and (c) the continuation of NRA's seismic and explorationactivities in the ope. areas not under IOC's concession. NRA's plannedinvestment in seismic and drilling activities is estimated to be around US$15million per year. Seismic activities include use of one seismic crew fo:detailing features to find structures. NRA plans to carry out the drilling ofabout three to five exploration wells per year, with one rig purchased in1988, and a workover rig for servicing wells. NRA's plarned investment illdevelopment and production activivies are estimated to be around US$5.0million. The planned program includes: (a) $2.5 million investment ininfrastructure to build a small gathering station and a camp at the Hamza oilfield to continue oil production of about 500 bbl/day; (b) $2.5 million toconstruct gas gathering facilities and a gas treatment plant for the Rishaarea to supply gas from two production wells to the power station.

6.03 Overall, NRA's planned investment program is reasonable. The programaims to continue to undertake minimum efforts in exploration and drilling inopen areas while at the same time making efforts to attract foreigninvestments to accelerate oil exploration and development activities in theseareas. In this context, Jordan has already taken pioneering steps in theright direction by signing technical assistance contracts with foreignnational oil companies such as PCIAC and JNOC. PCIAC will provide technicalassistance to NRA in the evaluation of the Risha gas reservoir. In addition,PCIAC and JNOC plan to invest about US$30 million to undertake extensiveseismic surveys and evaluate both the Risha and Sirhan areas. Following thisevaluation, GOJ plans to promote these areas to international oil companies toaccelerate exploration activities. At present, IOC's (Amoco, Hunt andPetrofina) planned investments in oil exploration in their respectiveconcession areas in Jordan is estimated to be US$10 million per year over aperiod of seven years. Their exploration activities include geological,geophysical and geochemical surveys and the drilling of twelve exploratorywells between 1999-1995 in their respective concession areas. If ahydrocarbon discovery is made, plans for development will entail moreinvestment.

6.04 The investment program outlined above is based on the currentlyplanned program in seismic and exploratory drilling activities. Additionalnew investment requirements in oil and gas will depend on the acceleration ofexploration activities, the success rate of ongoing exploration, and new

- 22 -

discoveries and their development. Given the uncertainties about reserveassessments, the long lead times in project implementation compounded bydelays in the preparation of exploration and development programs, there couldhe changes both in the investment program and its priorities. Because ofinter-linkages of natural gas with coal, power, refining and other industrialactivities, it is essential that investment priorities are closely linked tohow much natural gas will become available and on what schedule. If there isno more gas than the present availability to fuel 2 x 3i MW gas turbines, noinvestment will be required for gas development. If natural gas reserveassessments from Risha and other potential discoveries show the availabilityof plentiful gas reserves, it would be economical to substitute natural gasfor fuel oil in power generation. If the present exploration efforts succeedin finding oil with associated gas or non-associated gas fields integrated gassupply and utilization studies should be undertaken to prepare a long-term gasdevelopment plan. The economic evaluation of the planrned investment should bemade, and related gas price and other issues should be addressed.

JORDANOIL AND GAS DEVELOPMENT

OF ~~~~~~~~~~~~~~~~~THEOLM Z lt E" S[ tMETR WICKS

L~~v

PRECAMBRIAe ROCKS

JOR A7', IN 4 GAS FIELD)

GULF OF SUEZ ~~~~~~~~~~~~~~~MAJOR BASIN 8(OJNL.Ahv

OF THE OIL AND SAS FIELD OF ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ CEA

THE MIDDLE EAST AND NORTH AFRICA

Source: NRA/MEMR

JORDONENERGY SECTOR STUDY

OIL AND GAS EXPLORATION AND DEVELOPMENT

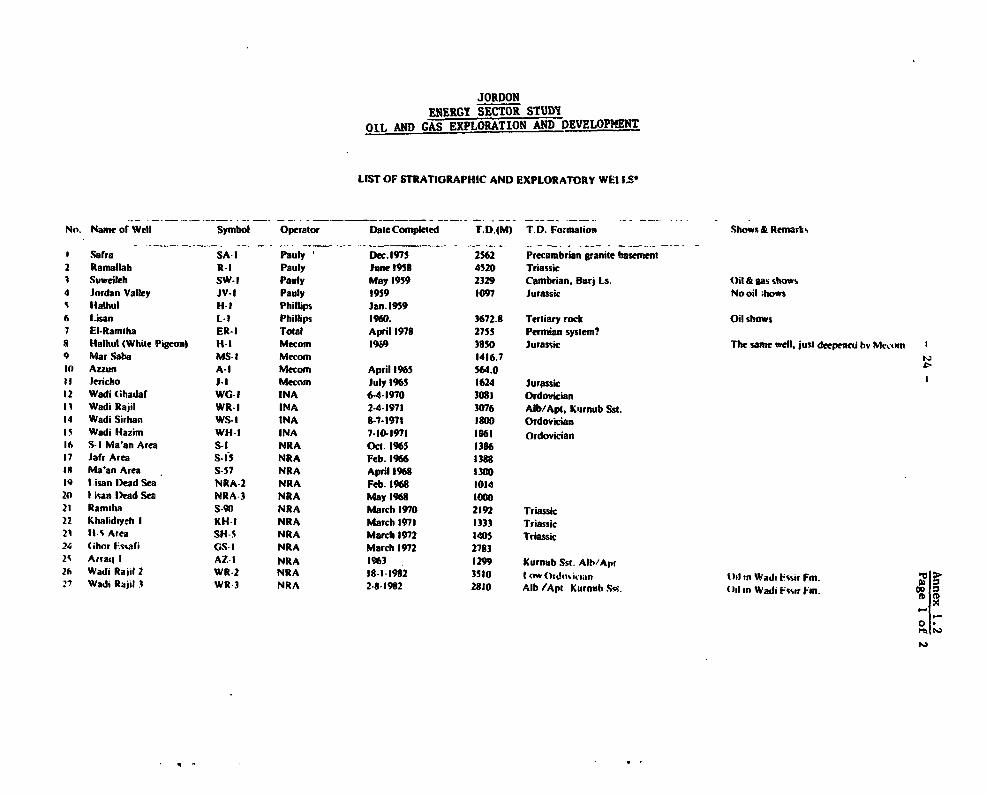

LIST OF STRATIGRAPHIC AND EXPLORATORY WEI IS

No. Name of Well Symbol Operator DaleCompleted T.D.gM) T.D. Formation Shows& Remark%

I .Safra SA-I Pauly Dec.1975 2562 Precambrian granite basement

2 Ramallabh R- Pauly June 1958 4520 Triassic1 Suweileh SW-I Pauly May 1959 2329 Cambrian, Burj Ls. Oil & gas shows

4 Jofdan Valley JV-I Pauly 1959 1097 Jurassk Nooil ;hows

S Hlalhul H-l Phillips Jan.19596 Lisan L-1 Phillips 1960. 3672.8 Tertiary rock Oil shows

7 El-Ramiha ER-I Total April 1978 2755 Permian system?a Halbul (White Pigeon) H- I Mecom 1969 3850 Jurassic The same well, just depenei bv Mctoun

9 Mar Saba MS-I Mecom 1416.710 Azzun A-1 Mecom April 1965 564.011 Jericho J-l Mecom July 1965 1624 Jurassic12 Wadi (Chadaf WG-I INA 6-4-1970 3081 OrdovkianI1 Wadi Raiil WR-I INA 24-1971 3076 Alb/Apt. Kurnub Ssit.

14 Wadi Sirhan WS-I INA 8-7-1971 1800 OrdovicianI5 Wadi Hazim WH-I INA 7-10-1971 1861 Ordovkian16 S-I Ma'an Area S-l NRA Oct. 1965 138617 Jafr Area s-IS NRA Feb. 1966 1388t# Ma-an Area S-57 NRA April 1%8 130019 I.isan D)ead Sea NRA-2 NRA Feb. 1968 101421t 1 isan l)ead Sea NRA-3 NRA May 1968 IC0021 Ramiha S-90 NRA March 1970 2192 Triassk22 Khalidiyrh I KH-I NRA March 1971 1333 Triassic21 lIs Area SH-5 NRA March 1972 1405 Triassic24 (ihor l.s%afi GS- I NRA March 1972 27832s Airaql I AZ-I NRA 1963 1299 Kurnub Ssit. Alb/Apt26 Wadi Rail 2 WR-2 NRA 18-1-1982 3510 I ow doviclam Oditn Wads sEsir Fm.

27 Wadi Rajil 3 WR3 NRA 2-8-1982 2810 Alb /Apt Kurnub Sst. Ill in Wadi jtsir Fm.

0*1i& N

Tahle I (Wontinmed)

No. Name (r Wcll Symbol Operator DateCompleted T.D.(M) T.D. Formation Sh&Remarks

2R Wadi Rajil 4 WR-4 NRA 8-2-1981 3103 Triassic ysten? Oil shows in W.Essir Fm.

29 Iahikiyeh I DH-I NRA 1-9-1983 4433 LOWdVCdoin OlsibwsinW.EsP Fm.

10 Wadi Al(haldaf WC-2 NRA 7-9-1983 3740 Cambrian System Oil show s in Cenomanin

It Ilam7ch I HZ-I NRA 22-1-1984 3216.5 Trlassic Ofl in Hunmur&NNaur Fs.

32 Risha I RH-I NRA 15-1-1984 3177 Ordovdatn

3. Risha 2 RH-2 NRA 21-7-1984 3314 Ordovidtn Gasdtows inPaloiozoCks.

34 Ilam7ch 200 HZ-2 NRA 30.7-1984 3257 AMb /Apt Kiurnub Sst OilIn Shib Fm.

35 Wadi Sirhan 2 WS-2 NRA 25-12-1984 3331 Ordovkia System

36 Ilam7ch 1 HZ-3 NRA 20-2-1985 3262 TUrotoa. W. Essir OCIinW.Es* FM.

37 Ilamich 4 HZ4 NRA 23-7-1915 3984 Paleo20ic Ordovian OuO"MsIWS2&ShwiF11a1s.

18 Ilam7ch 5 HZ-5 NRA 3-7-1985 3310 Alb /Apt Kurnub Sst. Oil shos In Shub FM.

19 Ham7ch 6 HZ-6 NRA 22-7-1985 3265 Kurnub Ssl. OidshwsInShfldbFm.

40 llam7ch 8 HZ-8 NRA 8-10-1985 3595 Triassk Oil dtosIn WS2 FM.

41 Ham7eh 7 HZ-7 NRA 26-10I'8S 2900 Kurnub Ssl. OR In WdiulErFtn.

42 Itam,ch 9 HZ-9 NRA 5-12-1985 3578 Jurassic

43 lIam7eh IOl HZ-10 NRA 15-11-198S 3199 KurnubSst. OildnowshiHumm rFm.

1 tsronian Wadi Essir Fm.WS2

hucib Fm.(r .accoln Senomanian Hummar Fm.

Fuheis Fm.Naur Fm.

Alhian / Aptian Kurnub FmvInra %ic .............. Huni Fm.

I *ija ic . .Main Fm.

Ihe wellR Imhown on figtire 9 are key stratigraphk and exploratory,11%; water wtlk are nol shown.

t11/ -2-1 Marc htotly spaced and considered to be delineation wells.

Ao0ua

o0.MFt'3

JORDANOIL AND GAS DEVELOPMENT

TABLE II

SEISMIC SURVEYS IN DIFFERENT EXPLORATION AREAS SEISMIC SURVEYSg@0 .- Se AREA COMPANY YE AR FOLD U)TAL Km

C-I IINA 1969 24 690

.- J , (C.G.G 1978/79 24 5t6

eo 0,, } _ . . . i _ _ ._ _ __ __ w . 6G.S.1 1981 224 1312

SYRIA C.6.G 1982/0 2 4 2435.5

1773km. ~ ~ ~~~~~~ -2 RA . -9 .64 24 27 OA~523I.".O.C 1964 46 56.1 TOTALs 67O9.6 km

loe / f->. ,. t C-2 C.G.C 1978 24 960.3

- C C 1 3522 km. C.G.G 1979 24 384

| i 5 1ll7t3W8t ..| § '' | |C-3 I N A 1969 24 630C C-I1~ ¶ C.G.G 197679 24 304

6709 km. .. cC.G 1991 24 1896

so t J w, | | __.G.G 1982/S 24 560 TOTALs 3390 kmU C-? C-4 C.G.G 1982 24/48 49i.4

J | 515 ken. \ C-S \ | s C~5 FI,NO.C 1965 4 437 1OTALs 926.4 km'a / 315km. ~~~~~~~~~~ ~~~~~~~~~~c-5 FILON I97I/1 It 270

kC-41 3390kmr. \ G.SJ 1981 48 773oo _K { * _I.#C 105/64 40 730 TOTALS 1773km

C-6 C.G.G 1962 24 751.9 TOTALs 751.9km

C-? I.N.o.C 19 24 3157 ,TOTAL315.Tkm

A- J/ , _ 9, _ r_o.

*00 Energy souhces io vibrosi in all weoso m . . ^ _. . , -o _ : OcoC old welS in Ataq and N.Jordan

Source: NRA/ME?

Annex 1.4- 27 -

JORDANOIL AND GAS DEVELOPMENT

' i00 150 a 0 250 oo zo50 400 450 Sao ySo 6 o

.. 3 t; I I;6 A . a t

as- a ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~50

- a"- NORTHERN ~~~~~~RISHA AREA

a R . . 00

sot E _. _ 1''--* ,~t '\- _

150 * :50

CENTRAL*TH HASHEMITE KGt4Om AN

PLATEAU N.R.A.-ENERGY nF.Pt. 'FNT

DeAD SEA SRNA AREARIO AN A A

?IRESSION~ ~ ~~~~~~~~~~~~~~~~~RIRT . COI TO R I NCRTHER II 0 . N

/ I~ ~ ~ ~~~~~~~~~~~~~~

201~~~~~~~~~~~~~~~~EIN AND(5 AREAS3' ._, Xc2\ 0

I*i ~~~~~~~~~~~~~~~A a ooiONOUS ROCKs REGION

QC/A 'REGION C0VEREO By BASALTIC RtOCKS .

~~~i A ~ C 19C4111OEM1ETARY ROCKS RE'.ION

0~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~6*x - -0 _ _ _ __ ---_ T___ - 850

,ol-~ IS ZO !250_.|

sets *ee,ws me te ggssgaoi s,,svSi sse t eve-go- *tsses s-me-* ae-Sol sees, sgomg *SStS on-to Mt. wS

4I is:,se1 %"III as e st Weg" 99m @ onws mo 8t F "et ee-IV sst etS _ 61*SC -.I,* assaet s*"Isu fes,u sInlet ones eet*se us*a now:~s, sr m ul11,o tat ' * enao :e:s oo,os w* - - --a - -

Sol* es lle t' FV* tl8'§88 _ _ _ _ _ _ _ _ _ |at se* sest,% m ae: staves onve:e -, - - - - - - e,w.saw os5is togIS" 69CS0t9 SI tiltS io3 3 * #t - - s 1 - - - - -S - SW W*D s19'@ sY Tn ltos seloll *n1311 1089031 90810 aslt ctl@v no-go: nwa 0 imatm ~w soo <@w glvo goolo * *e$, M,I l eR asel Mles poolRsfiS.0B atn "oelse n gi am "_@ mo l 01e 1ss: *iolo ss legg It -a - -e-,$ - - - - - - 53853wAsSt's sesose t nts*ss* M,Oet *l*wa :'s egeti iooest g9vo an -t - - - - mauiSt' 91928 l- " t *t'"ts @|§-§aE oeW-@@ SWISS Saf-B88 3"9-2 cmE n- ee 1-E "ZS" ZwoeSt zeeets*t Irm's Serowe l esse*w t s 9el ts *e o* u9a *ev:s set - - - - - - s,,lu.nh OW=1119s0 @e*ams sa,sse*u nutu es vufi 855*A *e6l1t 41163 sWSIbB Et*se* M,& 8sea' 2 eta :lE : Stiihm oa- -gg*i egagI- @ SuS5C-1 iss*et *sveam sect-C st*ei§ St*-lS 05- BlSf St5 ,l*:.' et:. gevs @gej*g -sj esaaaw

___~~~ ... .. .......... _............. ... .... _ ......... .......................................... . ......... ,,,,,,,,,,,,,,,,,,,,,,,,,,,_, nessas Me not t goofsg oal goal Mae eassse 541 Sit stvist 011111211

(aibu uuI8Wo( ul)g aaaaaBBsmm uou--3vumwes me te

cr etq')

uoe1j0oldx3 sv9 pue 110ApnIS J1o03S 46Jau3

NY0aIO(

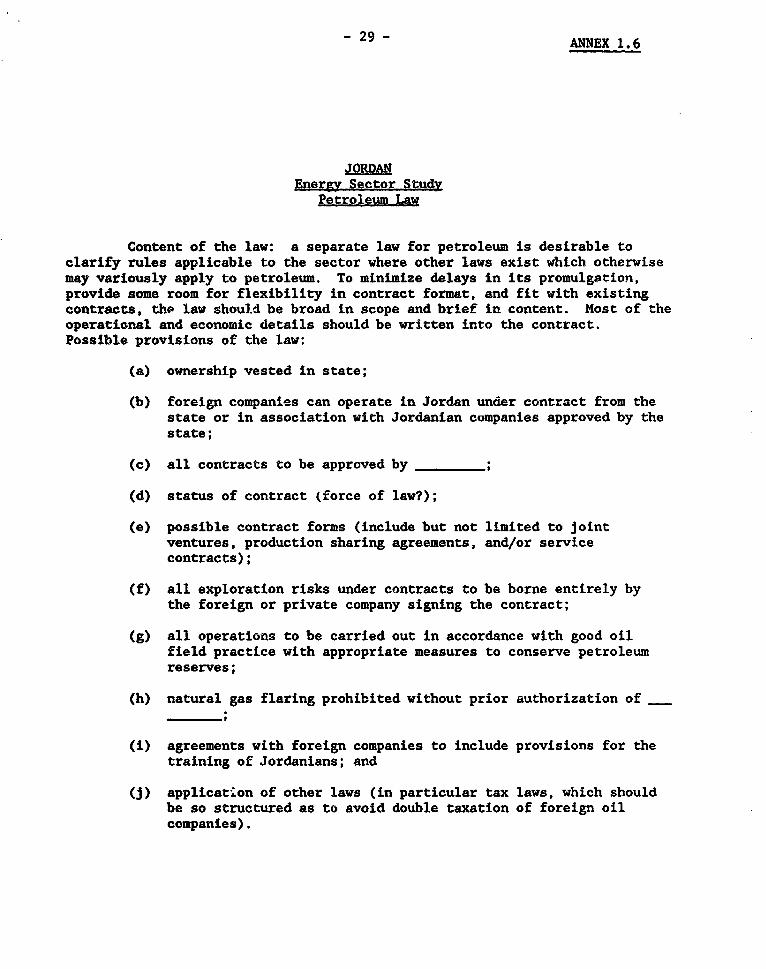

- 29 - ANNEX 1.6

JOR-DANEnergy Sector Study

Petroleum Law

Content of the law: a separate law for petroleum is desirable toclarify rules applicable to the sector where other laws exist which otherwisemay variously apply to petroleum. To minimize delays in its promulgation,provide some room for flexibility in contract format, and fit with existingcontracts, thp law should be broad in scope and brief in content. Most of theoperational and economic details should be written into the contract.Possible provisions of the law:

(a) ownership vested in state;

(b) foreign companies can operate in Jordan under contract from thestate or in association with Jordanian companies approved by thestate;

(c) all contracts to be approved by

(d) status of contract (force of law?);

(e) possible contract forms (include but not limited to jointventures, production sharing agreements, and/or servicecontracts);

(f) all exploration risks under contracts to be borne entirely bythe foreign or private company signing the contract;

(g) all operations to be carried out in accordance with good oilfield practice with appropriate measures to conserve petroleumreserves;

(h) natural gas flaring prohibited without prior authorization of

(i) agreements with foreign companies to include provisions for thetraining of Jordanians; and

(j) application of other laws (in particular tax laws, which shouldbe so structured as to avoid double taxation of foreign oilcompanies).

- 30 - ANNEX 1.7

JORDANEnergy Sector Study

Terms-of-Reference for a Diagnostic Study of the Risha Gas Reservoir

1. The consultant would study all available geological, geophysical,petrophysical, drilling, well test data and other studies performed on theRisha gas reservoir and prepare a geological model.

2. The consultant would digitize all well logs and correlate log anId coredata to determine reservoir rock properties. If necessary, detailed andspecial core analysis studies will be made to determine reservoir rockcharacteristics.

3. The consultant would determine gas reserves, both gas in place ardrecoverable reserves.

4. The consultant would perform reservoir simulation studiesincorporating the geology, well tcst and other data.

5. Based on these studies, the consultant would study reservoirproduction performance and develop gas production prediction cases.

6. The consultant will conduct stimulation studies on tight Risha gassands with a view to develop an optimal stimulation program to improve gaswell deliverability.

7. Based on the above studies, the consultant would recommend optimalfield development plans which would sustain gas deliverabilities over 10 and20 year periods.

8. The consultant would perform economic evaluations of variousproduction scenarios as recommended above.

9. The consultant would train NRA staff, both in Jordan and overseas, instate of the art technology, which would be applied in this study, and wouldcoordinate with NRA experts in various facets of this study.

- 31 -

Lil

4O Ig - 111Ii B I

i~~~~fs Js I1 I

!

JORDANENERGY SECTOR STUDY

Ministry of Energy and Mineral ResourcesProposed Organization Chart

Policy Co"Inat io

l Power | Pte || petroleum | | Eneokrgyhatloa | | Renewable T. | . lPetrolem imports Effiolenoya EIiONcouEvbato

EnErierxg |Energy Planig rI |Proeect lData Pocy and letment Opratnsand Demand Pricing PlForocoat

EK1w46343b

JORDAN - ENERGY STRATEGY REVIEW

Background Paper 2

Oil Shale Development

Page No.

Introduction ....................... . 33

Historical Background .33

Oil Shale Resources in Jordan .34

Characteristics of the Oil Shale Deposits . . . . . . . . . . 34

Review of Efforts in the Exploitation and Development of Oil Shale .. 35

A. The Study by the German Institute of GeologicalResearch . . . . . . . . . . . . . . . . . . . . 35

B. The Klockner-Lurgi Study . . . . . . . . . . . . . 3C. Combustion Engineering (CE)/Lummns Canada Inc. Study 38D. Bechtel/Byropower Study . . . . . . . . . . . . . . 40

Options for the Exploitation of Oil Shale . . . . . . . . . . 41

Strategy for Oil Shale Exploitation . . . . . . . . . . . . . 42

(a) Geological Assessment of Oil Shale . . . . . . . . 42(b) Evaluation of Water Resource Availability, Ash

Disposal, and Environmental Issues . . . . . . . 42(c) Technical Issues (Retorting) . . . . . . . . . . . 43(d) Technical Issues: Direct Combustion . . . . . . . 43

Conclusions . . . . . . . . . . . . . . . . . . . . . . . 44

Annex 2.1 Oil Shale Reserves

- 33 -

JORDAN - ENERGY STRATEGY REVIEW

Aackground Paper 2

Oil Shale Development

Introdiuctio

2.01 Jordan is dependent on imports of crude oil and petroleumproducts to meet virtually all its energy needs, which is a significantdrain of foreign exchange in Jordan's economy. One of the key elements ofJordan's energy strategy is to diversify its energy supply sources byeconomic exploitation of its domestic oil shale resources to meet theenergy needs in the next decade and beyond.

2.02 Extensive studies made by the Natural Resources Authority (NRA)of the Government of the Hashemite Kingdom of Jordan (GOJ) and severalbilateral/multilateral agencies have indicated large reserves of oil shalein Jordan with shallow overburden cover that could be exploited usingappropriate technology, both for extraction of synthetic crude (Syncrude)and for direct combustion utilizing state of art circulating fluidized bedcombustion (CFBC) technology for power generation. However, the mainconsideration is whether such projects could economically produce Syncrudeor generate power and contribute towards reducing Jordan's foreign exchangeburden by substituting imported petroleum or any future imported coal.

2.03 This background paper reviews the progress in oil shaletechnology, with particular emphasis on the studies made on Jordan's vastresources (over 40 billion tons) during the last decade, investigates thetechnical and economic feasibility of utilizing oil shale, the disposal ofresidual ash, and water requirements in the context of scarce nationalwater resources, and recommends a strategy for future exploitation of oilshale.

Historical Background

2.04 Oil shale is a source of energy of fossil origin with a highcontent of mineral matter called kerogen. Oil can be extracted from oilshale by destructive distillation (retorting) of the kerogen content.Crushed raw oil shale can also be considered as a high ash content fuel fordirect combustion in power generation. With appropriate technology, oilshale offers great promise as an indigenous fossil fuel resource that cansupport the growing energy needs of Jordan and other developing countries.

2.05 The development of shale oil began in Europe in 1830. However,with the discovery of petroleum in .870, commercial shale oil productiondeclined. After the 1973 "oil crisis" and steep rise in crude oil prices,the interest was renewed in the research and use of oil shales and tarsands in the United States, Europe, Brazil, China and the Soviet Union. InChina several hundred oil retorts produced up to 780,000 tons/year of shaleoil. The Soviet Union used oil shale for power generation (up to 3,000 MW)and for the production of resin for petrochemical industries.

- 34 -

2.06 Extensive research and advanced pilot projects were operated forthe production of oil from shale and tar sands in the USA and Canada inanticipation of oil price hikes to US$60/bbl. However, with the decline ofthe crude oil prices in the past few years to below US$20/bbl and thesurplus of crude supplies, the investment in large scale pilot projectsand, in some instances, in commercial production of syncrude was stopped.

2.07 The key to successful exploitation of the oil shale potential isthe use of appropriate technology that meets technical and economicrequirements. Until the early 1980s such technology was not commerciallyviable. In the last decade, new developments in direct burning, such asfluidized bed combustion (FBC) and, more recently, the second generation ofthis technology, i.e., circulating fluidized bed combustion (CFBC)utilizing low grade solid fuels, has been successfully developed andcommercially applied in power plants (over 60 units) in the USA, Canada,Finland, Sweden, Germany, Austria, Korea, and Japan. Such plants aregenerating power that is competitive with that from conventional powerplants.

Oil Shale Resources In Jordan

2.08 Jordan possesses a very large energy resource in its vastreserves of oil shale (over 40 billion tons of geological reserves). Thereare seventeen known surface and near surface occurrences of oil shale.Seven of the most important deposits are at El Lajjun, Sultani, Jurf edDarawish, Attarat Um Ghudran, Wadi Maghar, Siwaqa, and Khanez Zabib (seeMap: IBRD 21349). Their characteristics are given in Annex 2.2.

2.09 The major deposits of commercial scale interest are located southof Amman in Central Jordan and are easily accessible from the deserthighway from Amman to Aqaba. These are: (a) El Laii n, located about 100km south of Amman, about 15 km east of Karak and west of Qatrana;(b) Sultani, located at about 115 km south of Amman, just south ofQatrana; and (c) Jurf ed Darawish, located about 115 km south of Amman onthe desert highway near the town of Darawish.

2.10 So Ear. only the deposits at El Lajjun and Sultani have beengeologically investigated in detail. During the last decade, geological,techno-economic, and pre-feasibility studies for the exploitation of ElLajjun deposits for oil shale retorting and power generation, and ofSultani deposits for direct combustion in circulating fluidized bed thermalpower plants, have been undertaken by the Ministry of Energy and MineralResources (MEMR) and the Jordan Electricity Authority (JEA) incollaboration with American, Canadian and German consultants.

Characteristics of the Oil Shale DeRosits

2.11 Proven reserves at both El Lajjun and Sultani deposits areapproximately 2 billion tons, of which over 90X are exploitable by opencast mining. The reserves at Jurf ed Darawish are estimated at over 8billion tons. However, only 30X of these reserves may be exploitable. Themean oil content of El Lajjun, Sultani and Jurf ed Darawish are 10.5. 9.7,and 5.7 (wtX), respectively.

- 35 -

2.12 The deposits are shallow with essentially horizontal beds. Mheoverburden 's unconsolidated sedimentary rock consisting of gravels andsilt with some marl and limestone stringers. The thickness range of theoverburden is 15-62 meters at El Lajjun, 2-65 meters at Sultani, and 19-128meters at Jurf ed Darawish. At the Sultani and Jurf ed Darawish, the oilshale is underlain with phosphate beds whose thickness and quality are yetto be determined. So far, NRA has concentrated on the studies regardingthe exploitation of El Lajjun and Sultani oil shale deposits.

Review of Efforts in the Exploitation and Develooment of Oil Shale

A. The study by the German Federal Inscitute for Geological Research

2.13 NRA has done extensive geological studies to determine the oilshale reserves in the El Lajjun and Sultani areas. In 1979, NRAcommissioned a study by the German Federal Institute for GeologicalResearch (BGR) for the evaluation of El Lajjun deposits and atechno-economic pre-feasibility study for an oil shale retorting complexusing the Lurgi-Ruhrgas (LR) process. The results of these studiesindicated that the El Lajjun oil shale deposit shows continuous hydrocarbonimpregnations over an area of 18 sq km, with about 1 billion tons of oilshale reserves containing some 100 million tons of shale oil. It would besuitable for open cast mining and could support a 50,000 barrels/day (b/d)oil shale retorting complex for 30 years.

2.14 In October 1980, NRA commissioned Phase I of two pre-feasibilitystudies for (a) an oil shale retorting complex using the LR process forextracting 50,000 b/d shale oil; and (b) a power plant of 300 MW capacityutilizing El Lajjun oil shale by using Lurgi's CFBC process.

2.15 These studies were completed in 1982 and concluded that bothoptions were technically viable, although a stepwise approa:.h should betaken to (a) elaborate basic technical data; (b) investigate waterresources in view of their limited availability; and (c) undertake aneconomic assessment for the installation of a 50,000 b/d oil retortingcomplex and a 300-MW power generation complex.

B. The Klockner-Lurgi Study

2.16 In March 1986, NRA contracted with the West German consortiumKlockner-Lurgi for an update of the previous studies to assess thetechnical and economic feasibility of a large scale oil retorting complexfor the production of 50,000 b/d of shale oil. This study consisted of arevised geological study, updated pre-feasibility study, performance ofretorting pilot tests, CFB combustion tests with a 200-ton sample of ElLajjun oil shale in Germany, and hydrogeological studies for waterresources. In addition, Klockner-Lurgi also undertook an assessment of thepossibility of burning the spent shale in a 350-MW electric powergeneration plant by adopting Lurgi's CFB combustion process. The finalreport of the updated study was submitted to NRA in April 1988.

- 36 -