Embed Size (px)

Citation preview

<IR>: the big picture Jonathan Labrey, Chief Strategy Officer International Integrated Reporting Council

© Lorem ipsum delores septate atur vlore quires

IIRC Vision

The IIRC’s vision is to align capital allocation and corporate behaviour to wider goals of financial stability and sustainable development through the cycle of integrated reporting and thinking.

© Lorem ipsum delores septate atur vlore quires © International Integrated Reporting Council

The IIRC calls for

From

‘Silo Reporting’

to

‘Integrated Reporting’

From

‘Financial Capital Market System’

to

‘Inclusive Capital Market System ’

From

‘Short-term capital markets’

to

‘Sustainable capital markets’

© Lorem ipsum delores septate atur vlore quires © International Integrated Reporting Council

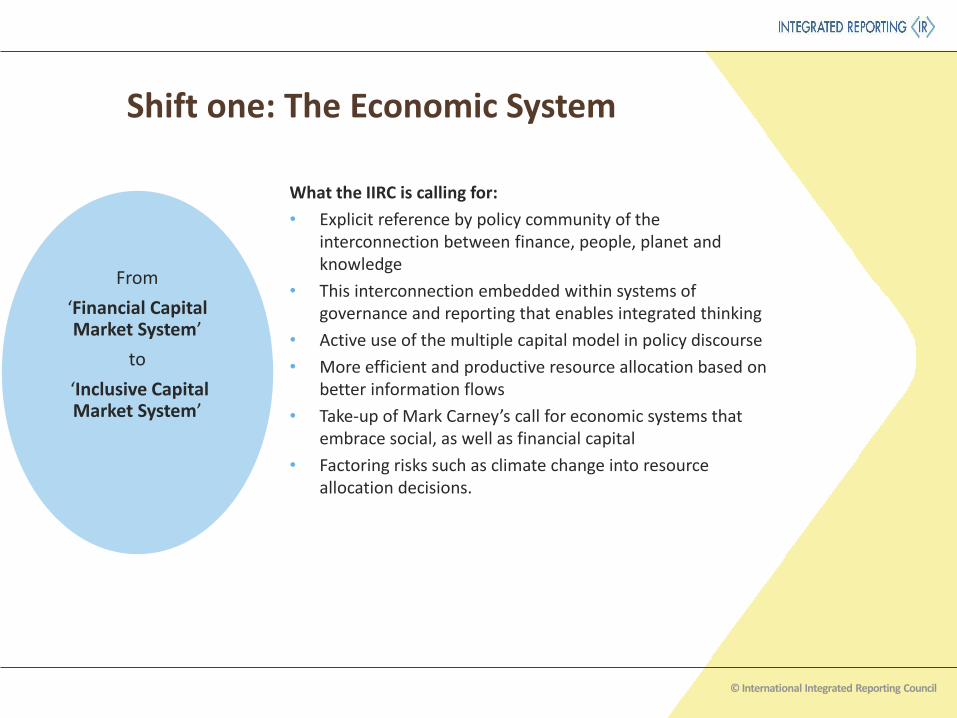

Shift one: The Economic System

What the IIRC is calling for:

• Explicit reference by policy community of the interconnection between finance, people, planet and knowledge

• This interconnection embedded within systems of governance and reporting that enables integrated thinking

• Active use of the multiple capital model in policy discourse

• More efficient and productive resource allocation based on better information flows

• Take-up of Mark Carney’s call for economic systems that embrace social, as well as financial capital

• Factoring risks such as climate change into resource allocation decisions.

From

‘Financial Capital Market System’

to

‘Inclusive Capital Market System’

© Lorem ipsum delores septate atur vlore quires © International Integrated Reporting Council

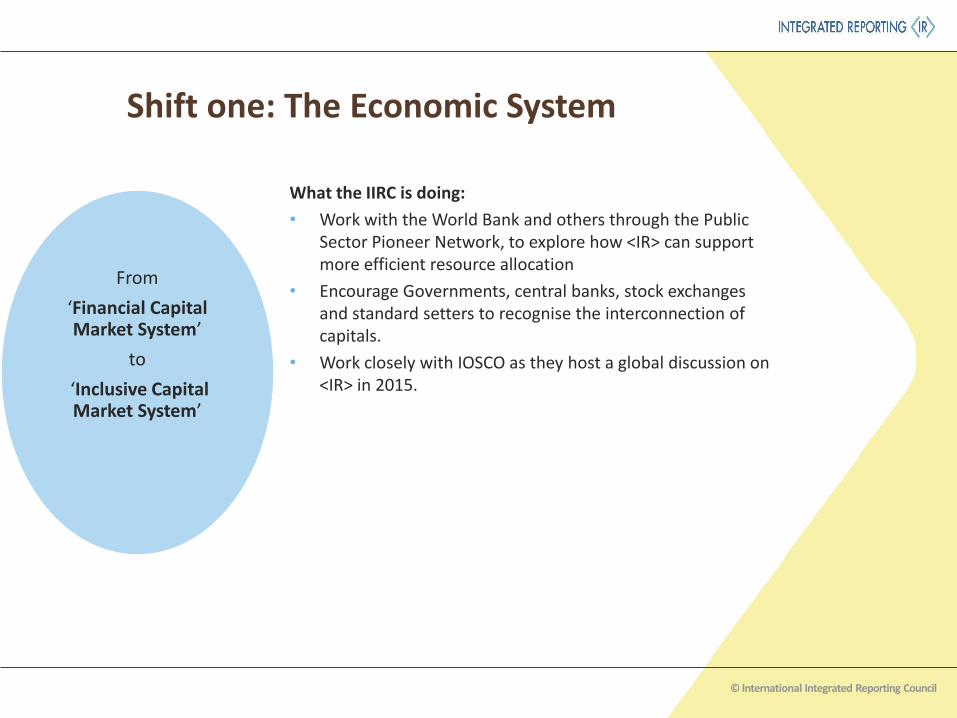

Shift one: The Economic System

What the IIRC is doing:

• Work with the World Bank and others through the Public Sector Pioneer Network, to explore how <IR> can support more efficient resource allocation

• Encourage Governments, central banks, stock exchanges and standard setters to recognise the interconnection of capitals.

• Work closely with IOSCO as they host a global discussion on <IR> in 2015.

From

‘Financial Capital Market System’

to

‘Inclusive Capital Market System’

© Lorem ipsum delores septate atur vlore quires © International Integrated Reporting Council

From

‘Short-term capital markets’

to

‘Sustainable capital markets’

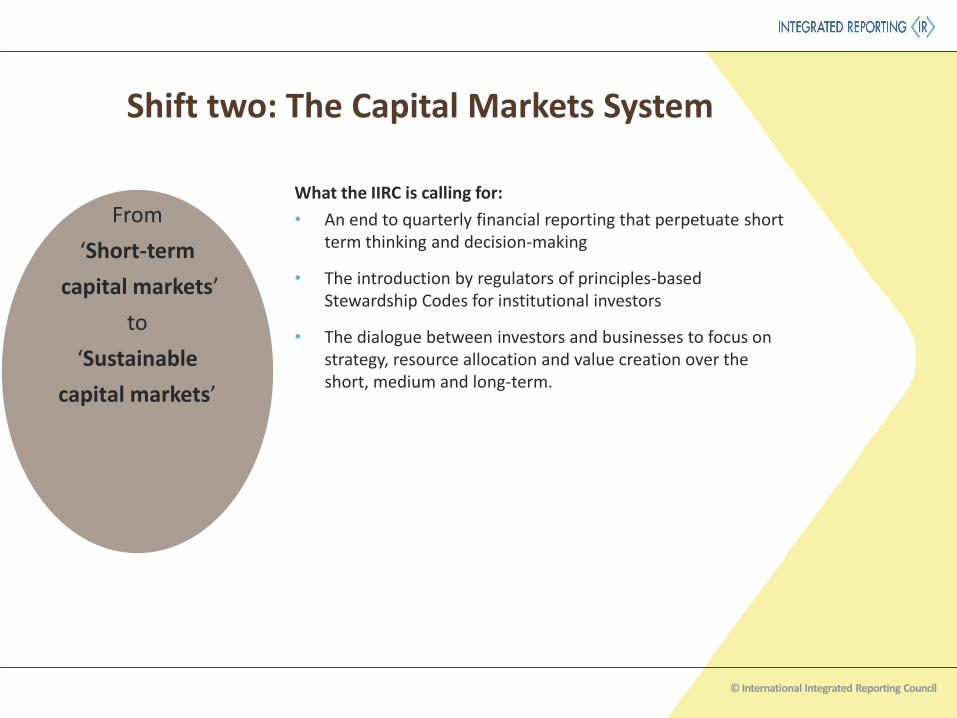

Shift two: The Capital Markets System

From

‘Short-term

capital markets’

to

‘Sustainable

capital markets’

What the IIRC is calling for:

• An end to quarterly financial reporting that perpetuate short term thinking and decision-making

• The introduction by regulators of principles-based Stewardship Codes for institutional investors

• The dialogue between investors and businesses to focus on strategy, resource allocation and value creation over the short, medium and long-term.

© Lorem ipsum delores septate atur vlore quires © International Integrated Reporting Council

Shift two: The Capital Markets System

What the IIRC is doing:

• Participate in the B20 process during Turkey’s Presidency of the G20 which will examine whether corporate reporting can become more conducive to long-term investment

• Continued participation post Davos on global climate change and financial stability discussions

• Promote academic evidence that <IR> attracts long-term investors.

From

‘Short-term capital markets’

to

‘Sustainable capital markets’

From

‘Short-term

capital markets’

to

‘Sustainable

capital markets’

© Lorem ipsum delores septate atur vlore quires © International Integrated Reporting Council

From

‘Silo Reporting’

to

‘Integrated Reporting’

Shift three: The Corporate Reporting System

From

‘Silo Reporting’

to

‘Integrated Reporting’

What the IIRC is calling for:

• <IR> underpins the shifts towards inclusive capitalism and sustainable capital markets

• An end to silo reporting that perpetuates short-term thinking

• A principles-based and cohesive reporting system, reflecting integrated thinking and resulting in a concise communication about value over time

• Mainstream adoption of <IR> will contribute towards financial stability and sustainable development.

© Lorem ipsum delores septate atur vlore quires © International Integrated Reporting Council

From

‘Silo Reporting’

to

‘Integrated Reporting’

Shift three: The Corporate Reporting System

From

‘Silo Reporting’

to

‘Integrated Reporting’

What the IIRC is doing:

• Call on Governments, regulators and standard setters to encourage innovation in corporate reporting

• Urge policy makers to remove regulatory barriers to <IR>

• Demonstrate that <IR> responds to challenges from IMF, Financial Stability Board and WEF.

© Lorem ipsum delores septate atur vlore quires

Why <IR>? More than financials

Source: OCEAN TOMO LLC January,1,2015

© Lorem ipsum delores septate atur vlore quires © International Integrated Reporting Council

Adoption Drivers

Policy alignment

Market innovation

Today’s business model

Stewardship: investor pull

Regulatory calls

<IR> adoption

© Lorem ipsum delores septate atur vlore quires

Where is financial value?

Trading risks and

opportunities

Brand value / reputation IT Systems

Natural resources: subject to

permits, levies, taxes, subsidies

Industry trends

Plant / Machinery

Stakeholder relations

Employee productivity

and retention

Social capital relations and

licence to operate

Land

Intellectual property: patents,

trademarks, copyright

Financial risks and

opportunities

Financial transactions

strategically relevant value needs strategically relevant information

© Lorem ipsum delores septate atur vlore quires

When Nikkei buys The Financial Times:

It is buying:

• technological innovation

• human and intellectual capital

• the history and the brand

• its reputation for journalistic excellence

© Lorem ipsum delores septate atur vlore quires

When Nikkei buys The Financial Times:

The price is not valued on:

• printing presses

• buildings and machinery

• the balance sheet

© Lorem ipsum delores septate atur vlore quires

“Ultimately, if we can change the structure of the system, the structure of incentives in banks and non-banks, that’s got to be better for everyone”

Andrew Haldane, Chief Economist, Bank of England speaking on 24 July 2015

© Lorem ipsum delores septate atur vlore quires

“Businesses need to break free from the tyranny of today’s earnings report so they can do what they do best: innovate, invest and build tomorrow’s prosperity”

Hilary Clinton, US Presidential candidate

© Lorem ipsum delores septate atur vlore quires

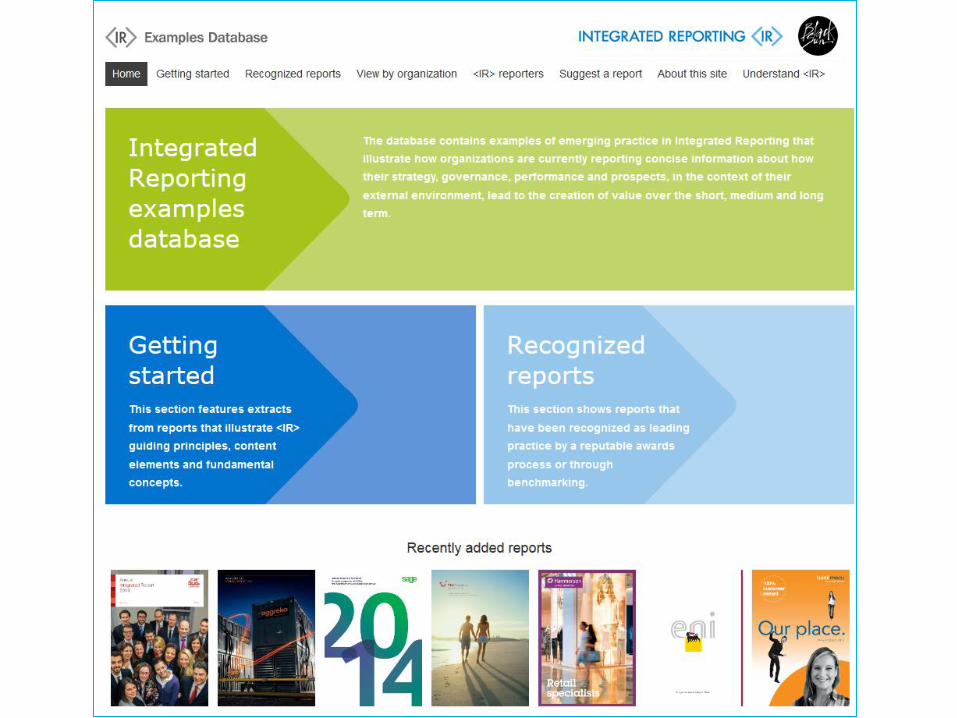

Resources Integrated Reporting Examples Database Sharing real examples of leading

practice in Integrated Reporting to help organisations on the <IR> journey

The International <IR> Framework Providing the principles and concepts

for organisations adopting <IR>

<IR> Network Bringing together organisations worldwide

to enhance the way they think, plan and report.

examples.integratedreporting.org www.integratedreporting.org

The key features of <IR> <IR>: Unlock Trust and Create Value Kuala Lumpur 6 August 2015

Michael Nugent

Technical Director, Framework Development

The Framework

Content Elements

Fundamental

Concepts

Guiding

Principles

19

Value is co-created

20

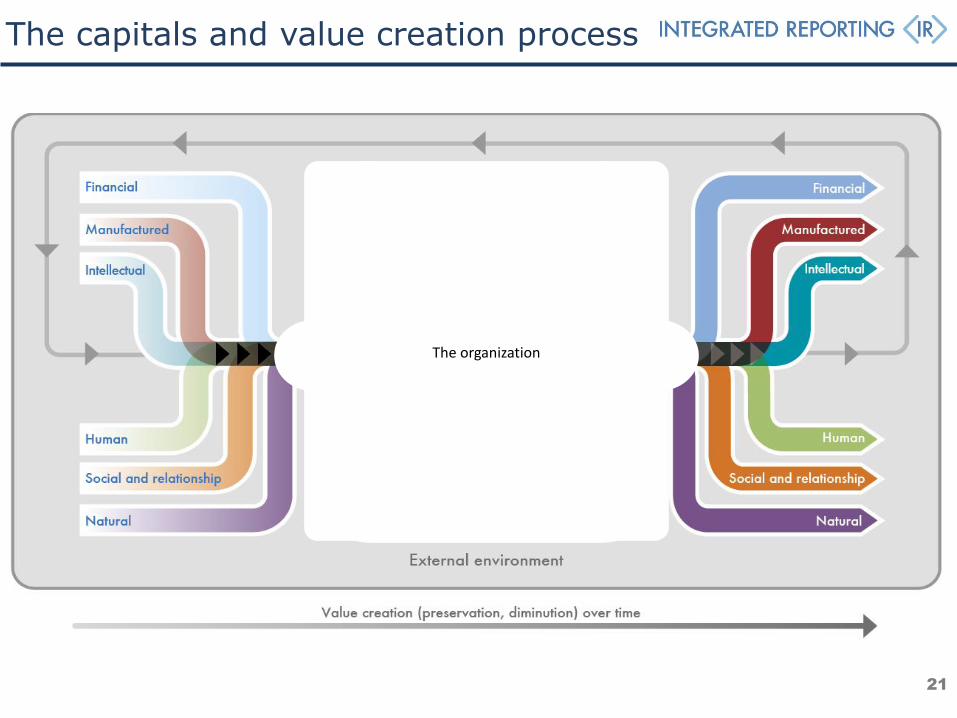

The capitals and value creation process

21

The organization

Inside the organization

22

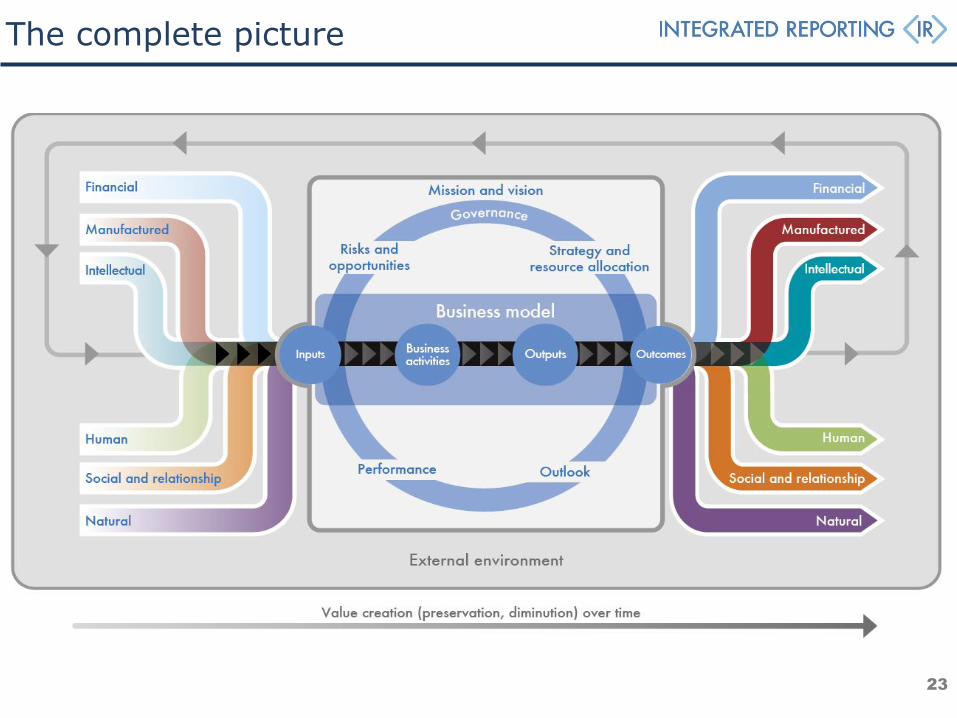

The complete picture

23

The Framework

Content Elements

Fundamental

Concepts

Guiding

Principles

24

Guiding Principles

• Strategic focus and future orientation

• Connectivity of

information • Stakeholder

relationships • Materiality • Conciseness • Reliability and

completeness • Consistency and

comparability

Underpin preparation

Inform content …

… and presentation of information

Judgement is needed

25

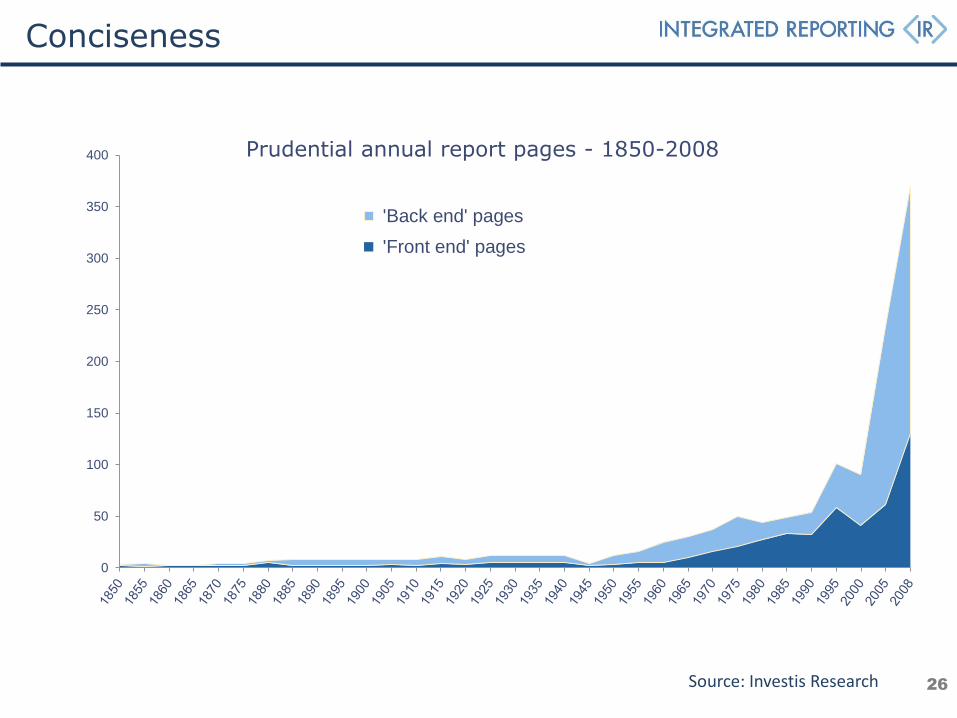

0

50

100

150

200

250

300

350

400 Prudential annual report pages - 1850-2008

'Back end' pages

'Front end' pages

Source: Investis Research

Conciseness

26

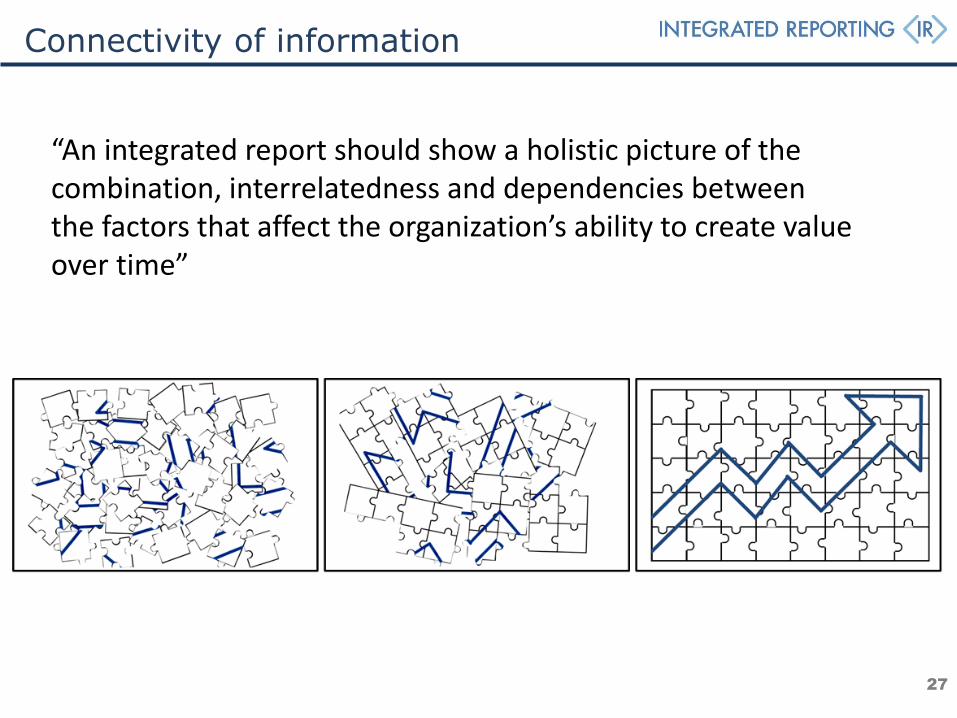

Connectivity of information

“An integrated report should show a holistic picture of the combination, interrelatedness and dependencies between the factors that affect the organization’s ability to create value over time”

27

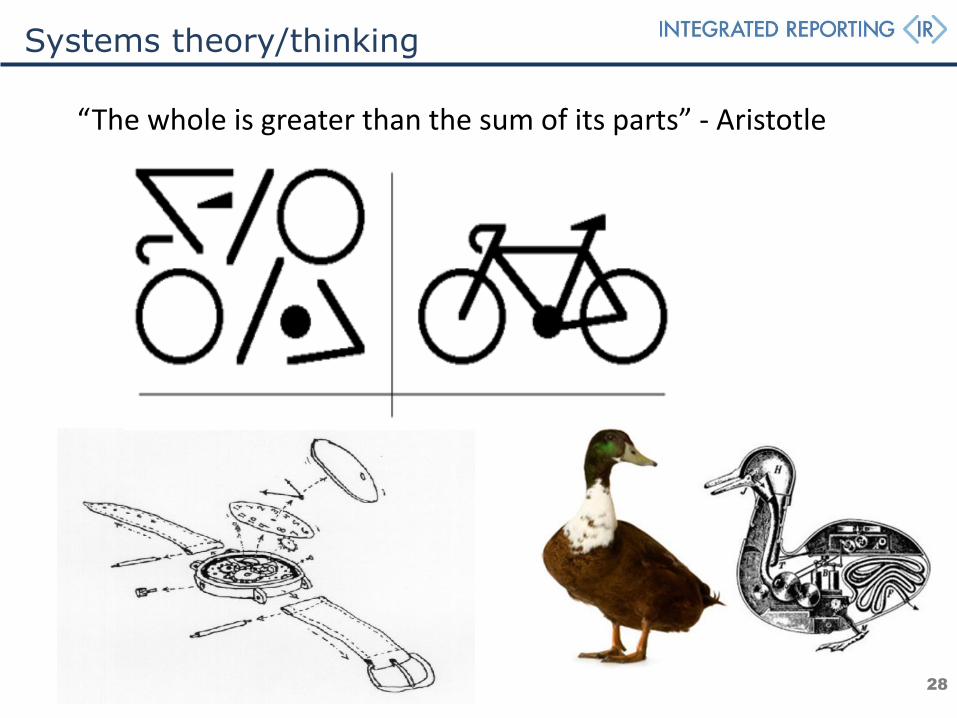

Systems theory/thinking

“The whole is greater than the sum of its parts” - Aristotle

28

Integrated thinking helps

Integrated thinking

Integrated report

Integrated thinking

Integrated report

Integrated thinking

Integrated report

Integrated thinking

29

The Framework

Content Elements

Fundamental

Concepts

Guiding

Principles

30

Questions to be answered

Not a set sequence

Not standalone sections

Connections apparent

Unique value creation story

Content Elements

• Organizational

overview and external

environment

• Governance

• Business model

• Risk and opportunities

• Strategy and resource

allocation

• Performance

• Outlook

31

Tell your own, unique story

32

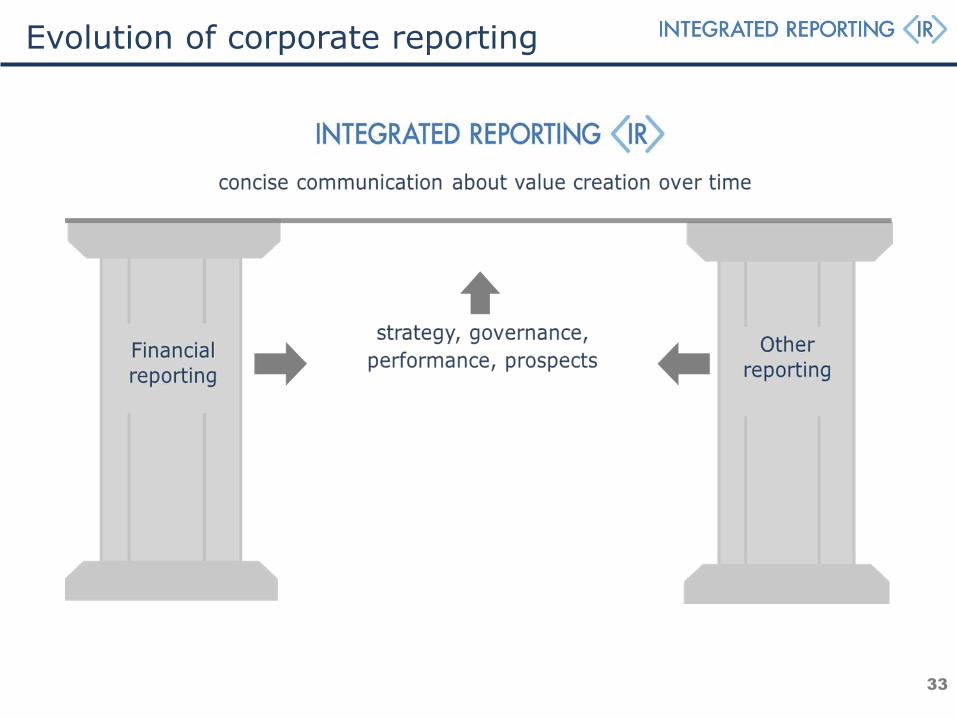

Evolution of corporate reporting

33

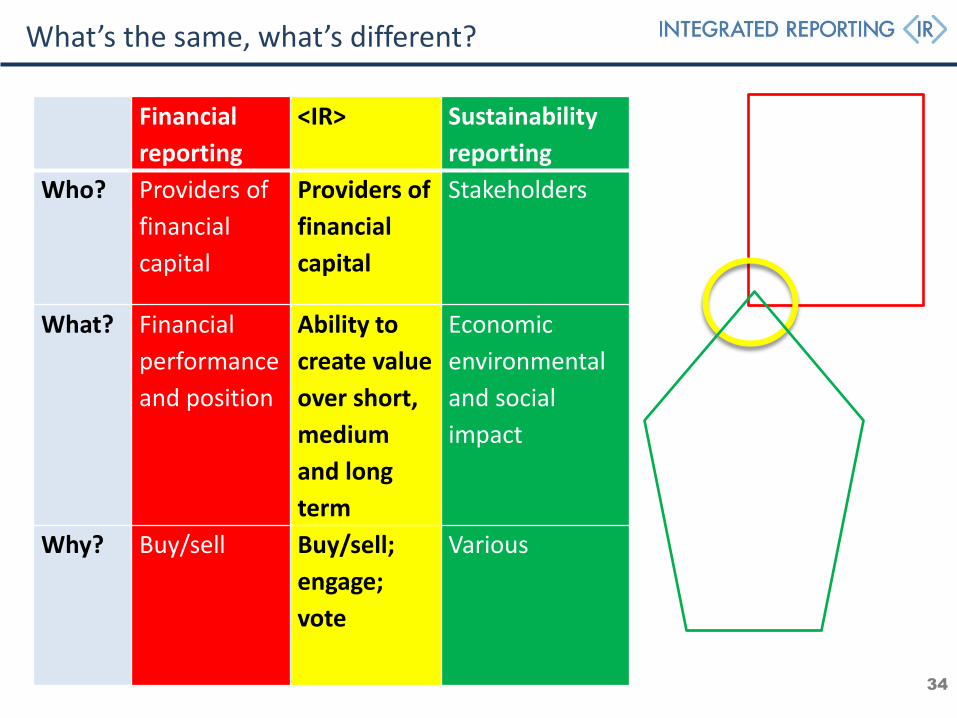

What’s the same, what’s different?

Financial

reporting

<IR> Sustainability

reporting

Who? Providers of

financial

capital

Providers of

financial

capital

Stakeholders

What? Financial

performance

and position

Ability to

create value

over short,

medium

and long

term

Economic

environmental

and social

impact

Why? Buy/sell Buy/sell;

engage;

vote

Various

34

The key features of <IR> <IR>: Unlock Trust and Create Value Kuala Lumpur 6 August 2015

Michael Nugent

Technical Director, Framework Development

<IR>: the emerging evidence Jonathan Labrey, Chief Strategy Officer International Integrated Reporting Council

© Lorem ipsum delores septate atur vlore quires

Why <IR>?

The development of <IR> is based on key insights:

• Increasing value in business is driven by a range of capitals

• Reporting is fragmented – the story is lost in detail

• Users want to read about value creation over time

• Reporting can influence better outcomes

• Not just financial but wider matters

• Better reporting can help to unlock long-term investment

© Lorem ipsum delores septate atur vlore quires

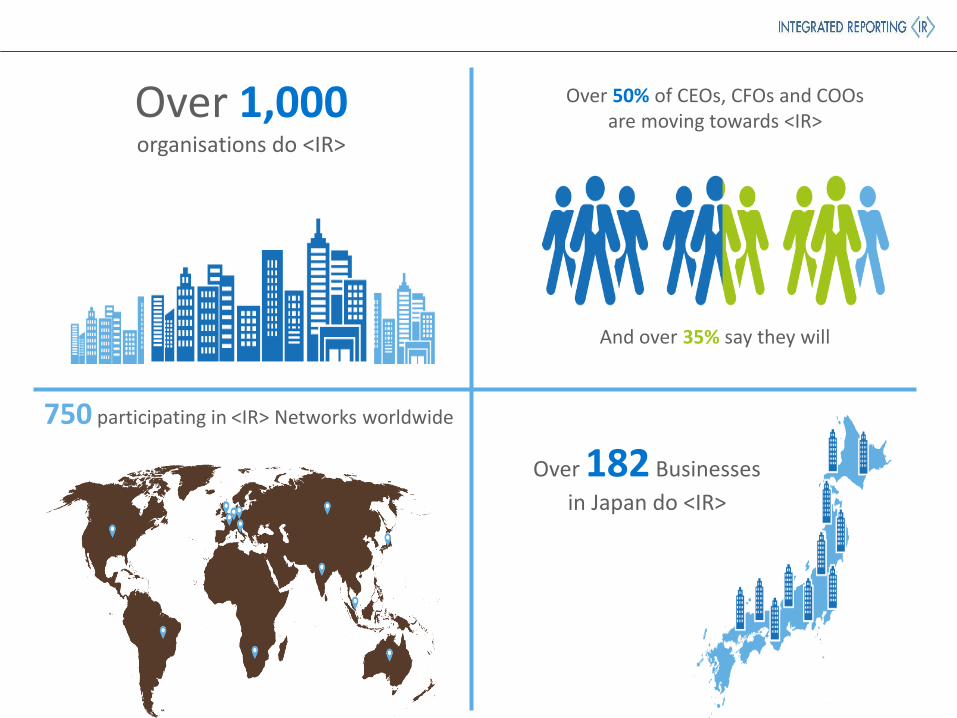

Over 1,000 organisations do <IR>

And over 35% say they will

750 participating in <IR> Networks worldwide

Over 50% of CEOs, CFOs and COOs are moving towards <IR>

Over 182 Businesses

in Japan do <IR>

© Lorem ipsum delores septate atur vlore quires

79%

Of SA Non-Executive Directors believe integrated thinking increases the quality

of organisations’ dialogue with shareholders other stakeholders

92%

Of people surveyed by Black Sun see increased understanding of value creation

87%

<IR> participants believe investors better understood their strategy

80%

Of investors believe quality of reporting affect professional

perception of management quality

© Lorem ipsum delores septate atur vlore quires © International Integrated Reporting Council

Harvard Business School research of 1,066 US companies concludes “more <IR> is associated with a more long-term investor base”

© Lorem ipsum delores septate atur vlore quires

“By improving reporting requirements for organisations <IR> will lead to better-informed and more sustainable long-term investment, for the benefit of society.”

Mark Carney, Governor Bank of England, Chairman, Financial Stability Board

© Lorem ipsum delores septate atur vlore quires

<IR> Benefits to Business

• Breakthroughs in understanding value creation

• Improving what is measured

• Improving management information and decision making

• A new approach to stakeholder relations

• Connecting departments and broadening perspectives

© Lorem ipsum delores septate atur vlore quires

Benefits to Investors

• Wider information on capitals for relevant investment decisions

• Greater confidence in the management of companies

• improved dialogue between investors and management

© Lorem ipsum delores septate atur vlore quires

Benefits to the Market and Society

Align capital allocation and corporate behaviour through integrated reporting and thinking to wider goals of financial stability and sustainable development

© Lorem ipsum delores septate atur vlore quires

Resources Integrated Reporting Examples Database Sharing real examples of leading

practice in Integrated Reporting to help organisations on the <IR> journey

The International <IR> Framework Providing the principles and concepts

for organisations adopting <IR>

<IR> Network Bringing together organisations worldwide

to enhance the way they think, plan and report.

examples.integratedreporting.org www.integratedreporting.org

Integrated Reporting

Better Alignment with Investor Decision Making

Pru Bennett

August 2015

For Institutional Investors Only, Not for Public Distribution (Please read important disclosure)

Agenda

48

Who is BlackRock?

Issues with current corporate reporting

Positive impacts of integrated reporting

Issues specific to Asia

Concerns regarding integrated reporting and potential solutions

For Institutional Investors Only, Not for Public Distribution (Please read important disclosure)

Who is BlackRock?

For Institutional Investors Only, Not for Public Distribution (Please read important disclosure)

The world’s largest investment management firm

US$4.721 trillion assets under management (AUM) as at June 30, 2015. US$1.5 trillion is actively managed while US$2.9 trillion is passive

12,400 employees in more than 30 countries serving clients in more than 100 countries (as of 06/30/15)

Clients include retail and institutional investors, which are comprised of pension funds, official institutions, endowments, insurance companies, corporations, financial institutions, central banks and sovereign wealth funds

Product range includes single- and multi-asset portfolios investing in equities, fixed income, alternatives and/or money market instruments

Our mission is to help our clients build better financial futures. Two-thirds of the assets that BlackRock manages support people in their retirement

50

Source: 2015 Q2 2015 Earnings Release, BlackRock Inc.

For Institutional Investors Only, Not for Public Distribution (Please read important disclosure)

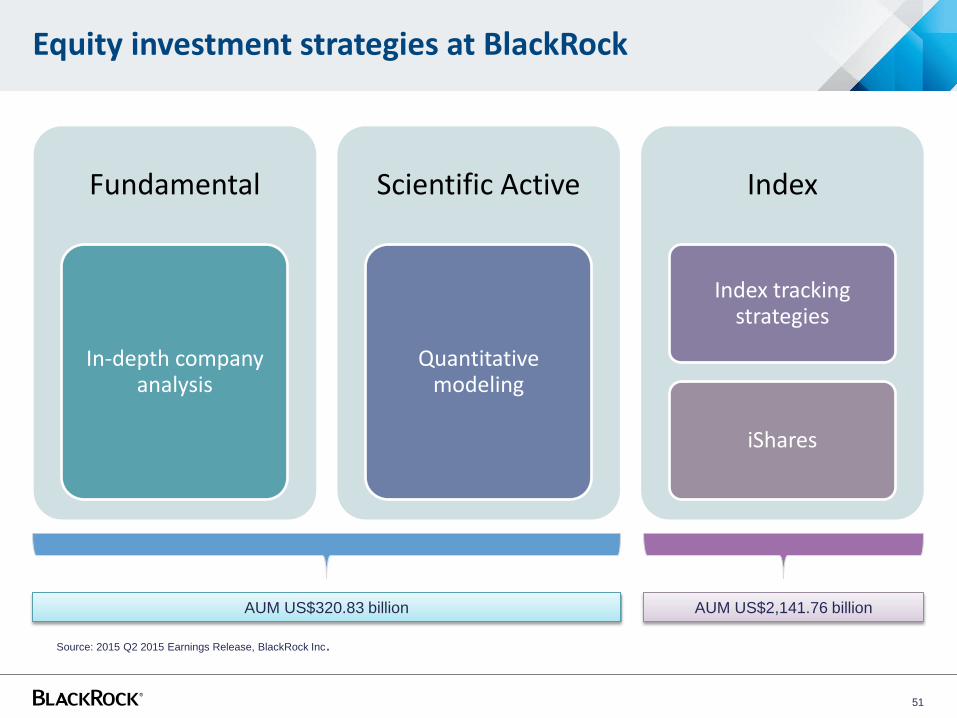

Equity investment strategies at BlackRock

Fundamental

In-depth company analysis

Scientific Active

Quantitative modeling

Index

Index tracking strategies

iShares

51

AUM US$320.83 billion AUM US$2,141.76 billion

Source: 2015 Q2 2015 Earnings Release, BlackRock Inc.

Issues with current corporate reporting

For Institutional Investors Only, Not for Public Distribution (Please read important disclosure)

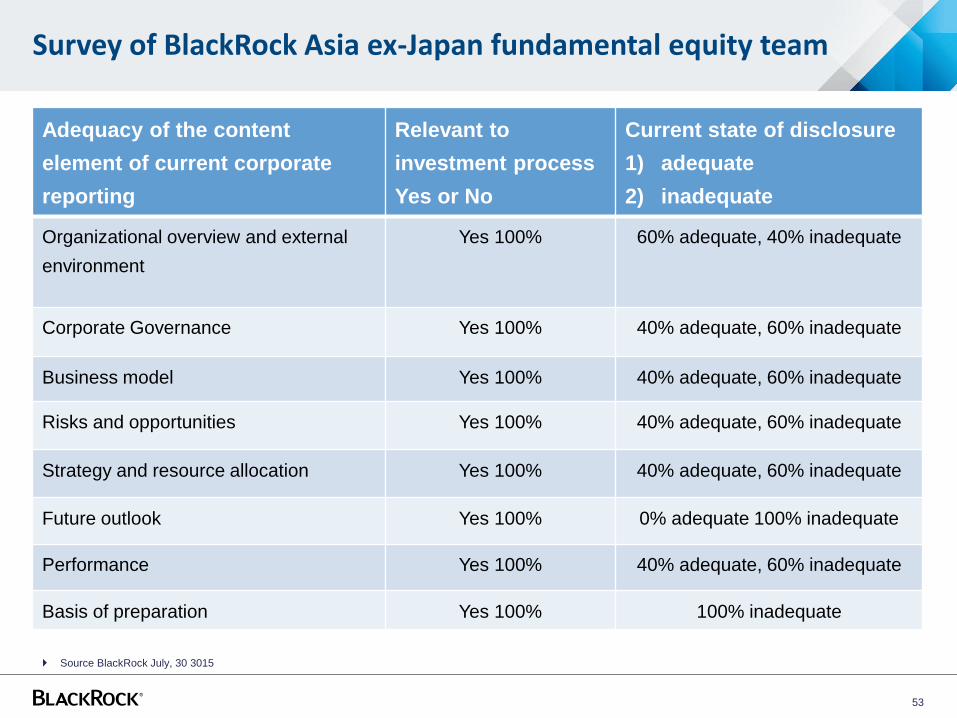

Adequacy of the content

element of current corporate

reporting

Relevant to

investment process

Yes or No

Current state of disclosure

1) adequate

2) inadequate

Organizational overview and external

environment

Yes 100% 60% adequate, 40% inadequate

Corporate Governance Yes 100% 40% adequate, 60% inadequate

Business model Yes 100% 40% adequate, 60% inadequate

Risks and opportunities Yes 100% 40% adequate, 60% inadequate

Strategy and resource allocation Yes 100% 40% adequate, 60% inadequate

Future outlook Yes 100% 0% adequate 100% inadequate

Performance Yes 100% 40% adequate, 60% inadequate

Basis of preparation Yes 100% 100% inadequate

53

Survey of BlackRock Asia ex-Japan fundamental equity team

Source BlackRock July, 30 3015

Issues with current reporting

• The primary source of information for investment decision making is from the

company itself

• Current corporate reporting focusses on the financial and manufactured capital

• Information on the “other capitals” can be found in various reports eg corporate

social responsibility reports but there is often no linkage of this information to

financial and manufactured capital and long term company value

• Current reporting is focused on the past. Companies are not encouraged to

report on future prospects

54

Positive impacts of integrated reporting

For Institutional Investors Only, Not for Public Distribution (Please read important disclosure)

Positive impacts of integrated reporting

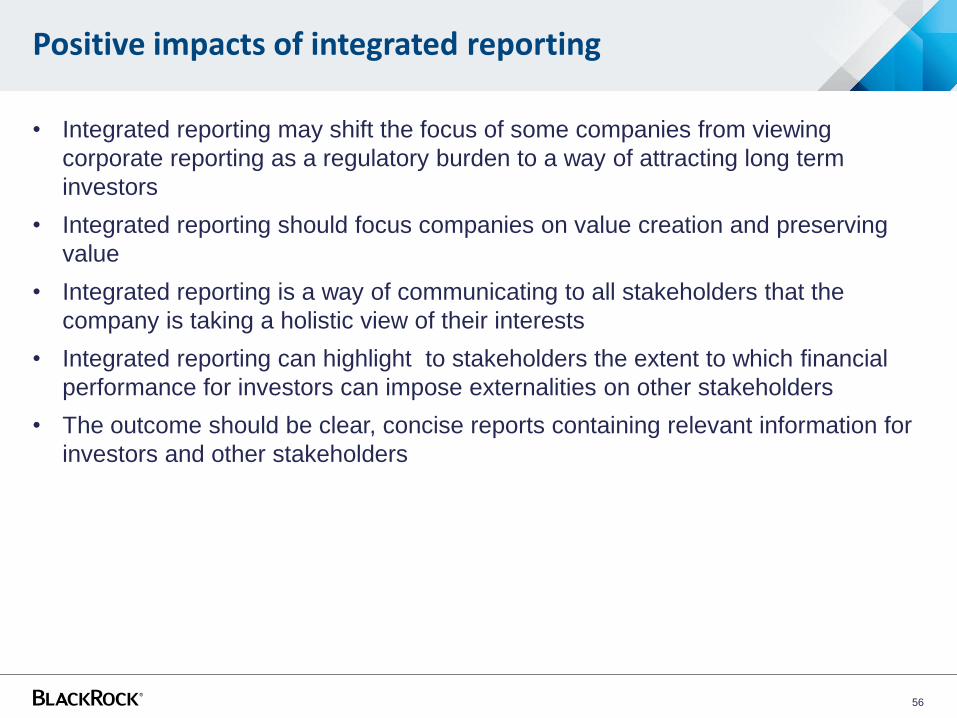

• Integrated reporting may shift the focus of some companies from viewing

corporate reporting as a regulatory burden to a way of attracting long term

investors

• Integrated reporting should focus companies on value creation and preserving

value

• Integrated reporting is a way of communicating to all stakeholders that the

company is taking a holistic view of their interests

• Integrated reporting can highlight to stakeholders the extent to which financial

performance for investors can impose externalities on other stakeholders

• The outcome should be clear, concise reports containing relevant information for

investors and other stakeholders

56

How integrated reporting will assist investors in decision making

• Integrated reporting should provide greater clarity around the value creation story

of a company and a link between sustainability and long term performance

• Integrated reporting should make clearer the links between a company’s strategy,

corporate governance, performance , risks and opportunities

• Integrated reporting provides a single source of qualitative and quantitative data

from a range of sources that impact organizational and financial success

• The disclosure of key risks and opportunities should assist in determining the

valuation of securities

• Integrated reporting provides greater efficiencies for the integration of ESG

factors into investment activities

57

Integrated reporting and investor valuation models

• The main determinants of value in a fundamental value approach are the

expected growth rate of earnings and the degree of risk in the investment.

• A risk analysis is run to determine the expected value and spread of the cash

flows in each period.

• Current reporting focuses on financial and manufactured capital. To ensure that

the risk analysis accurately reflects the risks faced by the company the other four

capitals are just as important.

58

Integrated reporting and investor valuation models

• Effective management of the other capitals should impact cash flows and hence

impact investor valuations

• Human capital – poor management of human capital impacts the ability to attract,

retain and develop the best people to implement and improve strategy (eg

discover a new mine, develop a commercial new product, manage capital

expenditure, manage operating expenditure)

• Natural capital –poor management of natural capital can result in regulatory

financial penalties and in extreme cases loss of licence to operate

• Social and relationship capital – poor management of social and relationship

capital for example supply chain management, bribery and corruption can lead to

reputational losses and competitive advantage

• Intellectual capital – poor management of intellectual capital could impair

competitive advantage

59

Client interest in a more holistic approach to valuation

• Increased attention by clients for asset managers to integrate environmental,

social and ethical (ESG) factors into the investment process

• Many asset managers are signatories to the UN Principles of Responsible

Investment which require signatories to incorporate ESG factors into their

investment processes and report how this is done

• Service providers such as MSCI, Asset4 and Bloomberg provide ESG data and

information to asset managers to assist ESG integration

• Clear, concise and accurate reporting of ESG issues mean that asset managers

can assess risk to be included in valuation models

• Integrated reporting should lead to better information from ESG service providers

60

Other investment strategies

Equity

Scientific Active Equity

• Integrated reporting will benefit SAE from a greater amount of information to

include in its models

Index tracking and iShares Strategies

• Integrated reporting will have no impact on portfolio construction

• Information provided in integrated reports could be used for thematic funds

• Integrated reporting will provide improved information for engagement and voting

activities

Fixed income

• Integrated reporting improved information regarding risks to allow better

assessment of overall credit risks

61

Issues specific to Asia

For Institutional Investors Only, Not for Public Distribution (Please read important disclosure)

Issues specific to Asia

• Generally a boiler plate compliance focus with respect to corporate reporting in

Asia

• A move to integrated reporting may help shift mindsets away from a pure regulatory

focus

• Corporate social responsibility (CSR) reports currently generally do not contain

information useful to investment managers

• CSR reports tend to be glossy marketing type documents. There is little focus on risks,

opportunities

• The move to integrated reporting will be a journey for the Asian region

• There is still a need for Asian companies to understand the needs of shareholders and

other stakeholders.

• Current disclosures on corporate governance issues are poor and provide shareholders

with little understanding of how a board operates

• Asset managers have a role to play in this journey

• Asset managers need to be involved in the discussion and debate on integrated

reporting

• Asset managers also need to articulate to companies why integrated reporting is

valued and how it potentially impacts investment decision making

63

Concerns with integrated reporting

For Institutional Investors Only, Not for Public Distribution (Please read important disclosure)

Concerns with integrated reporting

• Potential complexity due to the introduction of additional non-financial data into

corporate reporting

• Concerns from directors regarding exposure to liabilities with respect to future-

orientated information

• Difficulties with respect to providing assurance on some forms of information

which could impair reliability

• Getting the balance right between transparency and disclosure of commercially

sensitive information

65

Potential solutions

• Potential complexity – education about the framework and its use

• Director liability – legislation with a ‘better capital markets’ business case

• Assurance – the International Auditing and Assurance Standards Boards has

elevated integrated reporting assurance on its agenda

• Balancing the rewards from reporting competitive information – reporting strategy

to ensure that information is reliable, balanced and will produce “net reward” ie

NPV positive

66

Integrated reporting

67

This material is for distribution to institutional investors only and should not be relied upon by any other persons. This material is provided for

informational or educational purposes only and does not constitute a solicitation of any securities or BlackRock funds in any jurisdiction in

which such solicitation is unlawful or to any person to whom it is unlawful. Moreover, it neither constitutes an offer to enter into an investment

agreement with the recipient of this document nor an invitation to respond to it by making an offer to enter into an investment agreement.

This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other

things, projections, forecasts, estimates of yields or returns. This material is not intended to be relied upon as a forecast, research or

investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The

opinions expressed are as of [July 31, 2015 and may change as subsequent conditions vary. The information and opinions contained in this

material are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are

not guaranteed as to accuracy. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is

at the sole discretion of the reader. They do not necessarily reflect the views of any company in the BlackRock Group or any part thereof and

no assurances are made as to their accuracy.

Past performance is not a guide to future performance. The value of investments and the income from them can fall as well as rise and is not

guaranteed. You may not get back the amount originally invested. Changes in the rates of exchange between currencies may cause the value

of investments to fluctuate.

THIS MATERIAL IS HIGHLY CONFIDENTIAL AND IS NOT TO BE REPRODUCED OR DISTRIBUTED TO PERSONS OTHER THAN THE

RECIPIENT.

©2015 BlackRock, Inc., All Rights Reserved.

For Institutional Investors Only, Not for Public Distribution (Please read important disclosure)

S1214-43.

Some tips <IR>: Unlock trust … and create value Kuala Lumpur 6 August 2015

Michael Nugent

Technical Director, Framework Development

Overview

• <IR> is a journey

• First steps

• Some exercises

• Trust and credibility

• Getting help

• Examples

69

<IR> is a journey

70

Setting expectations

• <IR> is a journey; it will take more than one reporting cycle:

• Don’t try to do it all at once

• <IR> should not be seen as just additional reporting:

• Embed integrated thinking in the organization

• Don’t think of the Framework as a list of requirements:

• Tell your own, unique, value creation story

• You are probably doing some/a lot of this already:

• Build on what you’ve got

71

Stockland <IR> plan

Platform improvement

+ consolidation

Materiality + streamline

reporting + disclosure alignment

Materiality + strategy alignment

+ OFR

Internal engagement + test platform

Year 1 Year 2 Year 3 (now) Year 4

Continual focus on integrated thinking opportunities

STRATEGY AND GOVERNANCE

OUTLOOK / PROSPECTS

PAST PERFORMANCE

Value creation

STRATEGY AND GOVERNANCE

FORECASTS / PLANS

BUSINESS AS USUAL

Traditional reporting

Keep the end in mind

73

First steps

74

First steps

1. Top down or bottom up?

2. Those charged with governance (board) and senior management:

• clear understanding of what <IR> is

• clear understanding of why doing it

• agree on:

• objectives

• governance/oversight (including final approval)

• process (including timing and budget)

• communicate commitment:

• internally

• externally

First steps

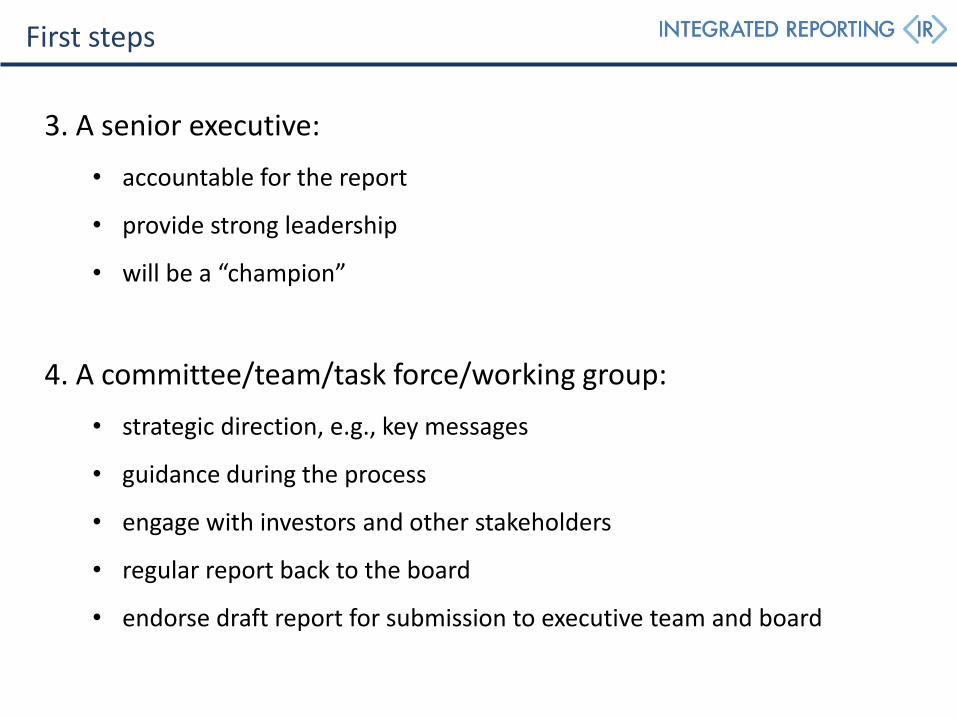

3. A senior executive:

• accountable for the report

• provide strong leadership

• will be a “champion”

4. A committee/team/task force/working group:

• strategic direction, e.g., key messages

• guidance during the process

• engage with investors and other stakeholders

• regular report back to the board

• endorse draft report for submission to executive team and board

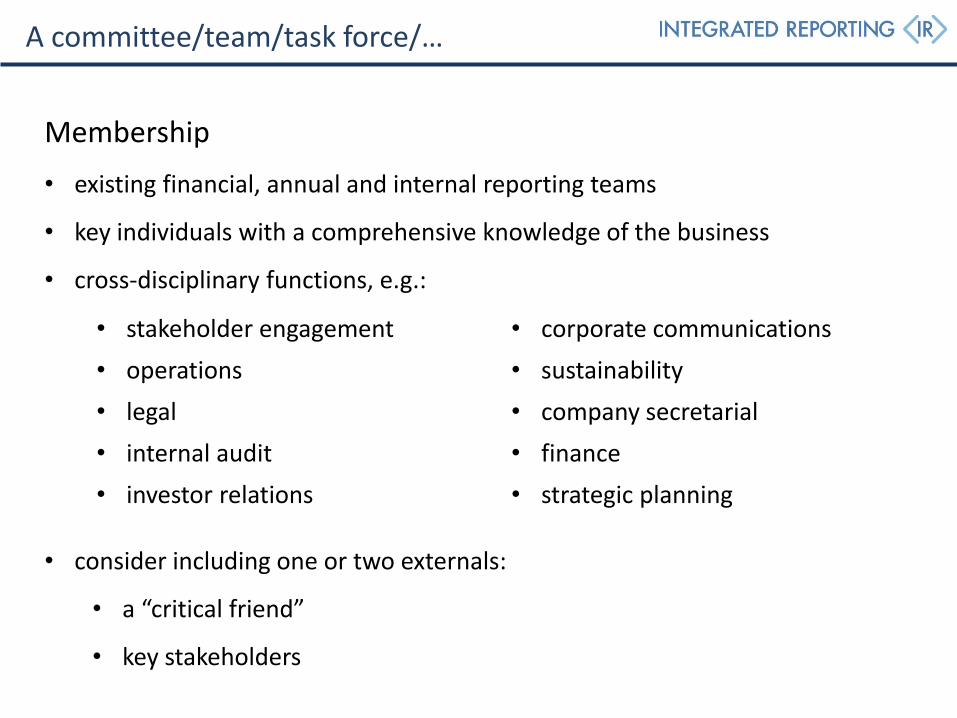

Membership

• existing financial, annual and internal reporting teams

• key individuals with a comprehensive knowledge of the business

• cross-disciplinary functions, e.g.:

A committee/team/task force/…

• stakeholder engagement • corporate communications

• operations • sustainability

• legal • company secretarial

• internal audit • finance

• investor relations • strategic planning

• consider including one or two externals:

• a “critical friend”

• key stakeholders

A committee/team/task force/…

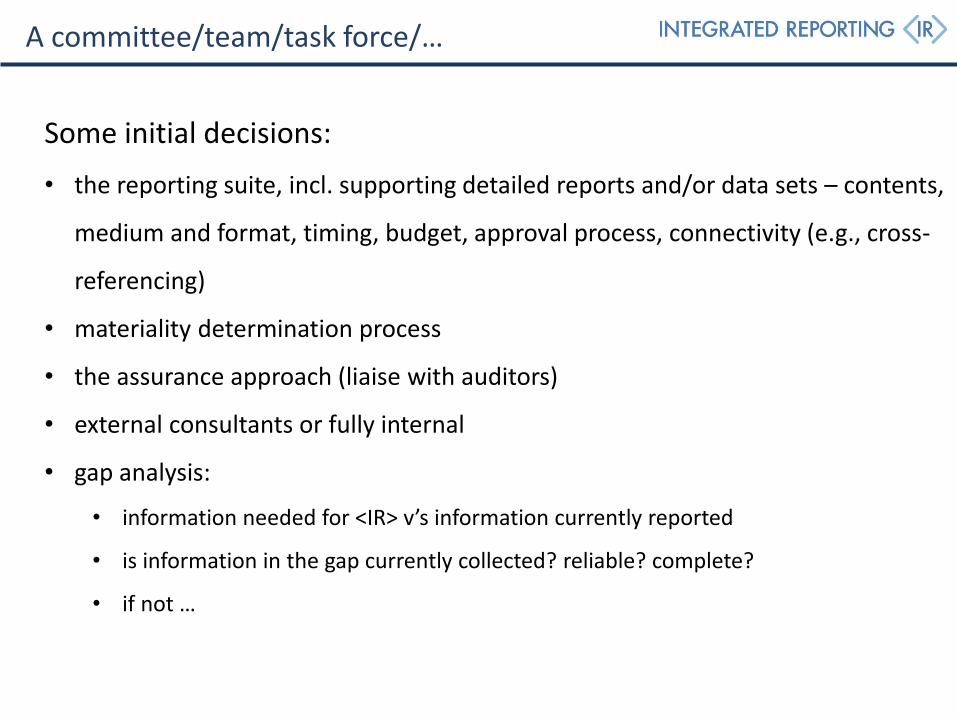

Some initial decisions:

• the reporting suite, incl. supporting detailed reports and/or data sets – contents,

medium and format, timing, budget, approval process, connectivity (e.g., cross-

referencing)

• materiality determination process

• the assurance approach (liaise with auditors)

• external consultants or fully internal

• gap analysis:

• information needed for <IR> v’s information currently reported

• is information in the gap currently collected? reliable? complete?

• if not …

Some exercises

79

Exercise: the capitals

• What, specifically, are your key capitals at each stage

• inputs, outputs and outcomes

• Are strategies around each key capital clearly articulated, communicated and

understood internally?

• Is information on each key capital:

• collected?

• used by line management? senior management? the board?

• reported to PoFC (e.g., annual report, investor briefings)?

• reported to others (e.g., sustainability report, website)?

• if not …

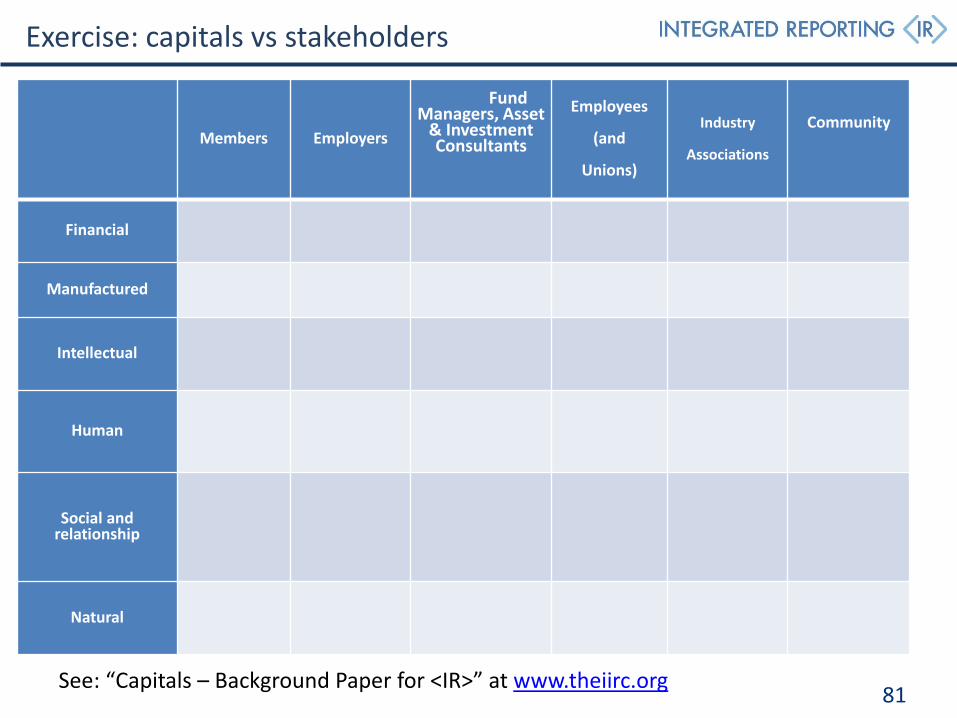

Exercise: capitals vs stakeholders

Members Employers

Fund Managers, Asset

& Investment Consultants

Employees

(and

Unions)

Industry

Associations

Community

Financial

Manufactured

Intellectual

Human

Social and relationship

Natural

See: “Capitals – Background Paper for <IR>” at www.theiirc.org 81

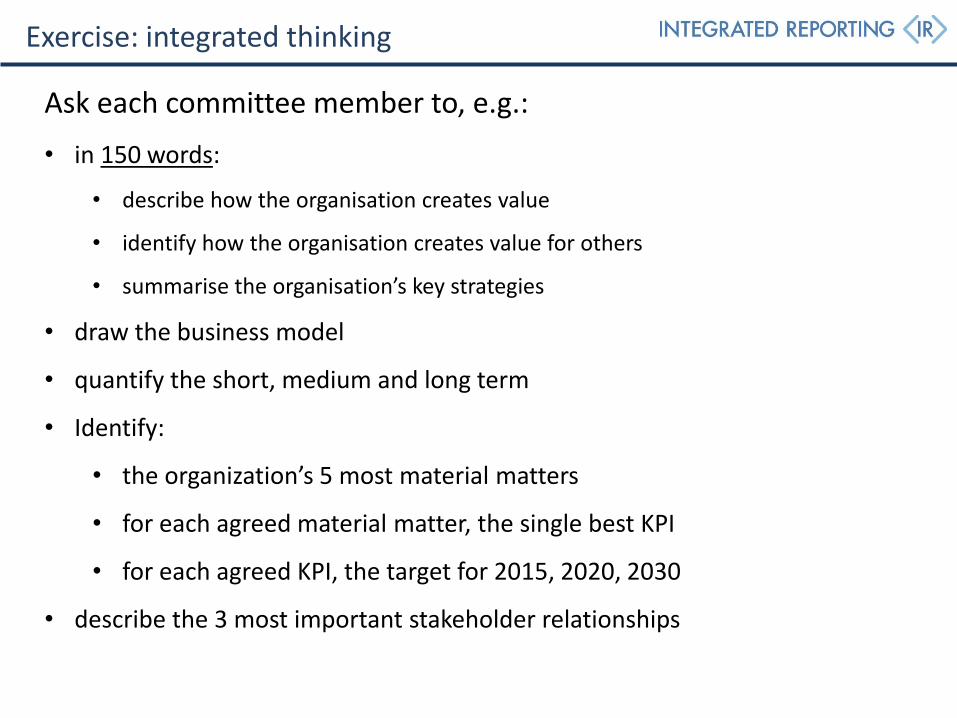

Exercise: integrated thinking

Ask each committee member to, e.g.:

• in 150 words:

• describe how the organisation creates value

• identify how the organisation creates value for others

• summarise the organisation’s key strategies

• draw the business model

• quantify the short, medium and long term

• Identify:

• the organization’s 5 most material matters

• for each agreed material matter, the single best KPI

• for each agreed KPI, the target for 2015, 2020, 2030

• describe the 3 most important stakeholder relationships

Trust and credibility

83

Trust and credibility

84

Internal systems and controls

85

■ “Financial” v “non-financial” systems

■ Less mature (may not even exist)

■ Internal controls need to catch up

■ Frameworks like COSO and CoCo

■ Iterative over time

■ Be transparent:

■ What is working and what is yet to be done

■ How did the board satisfy itself about integrity of the report?

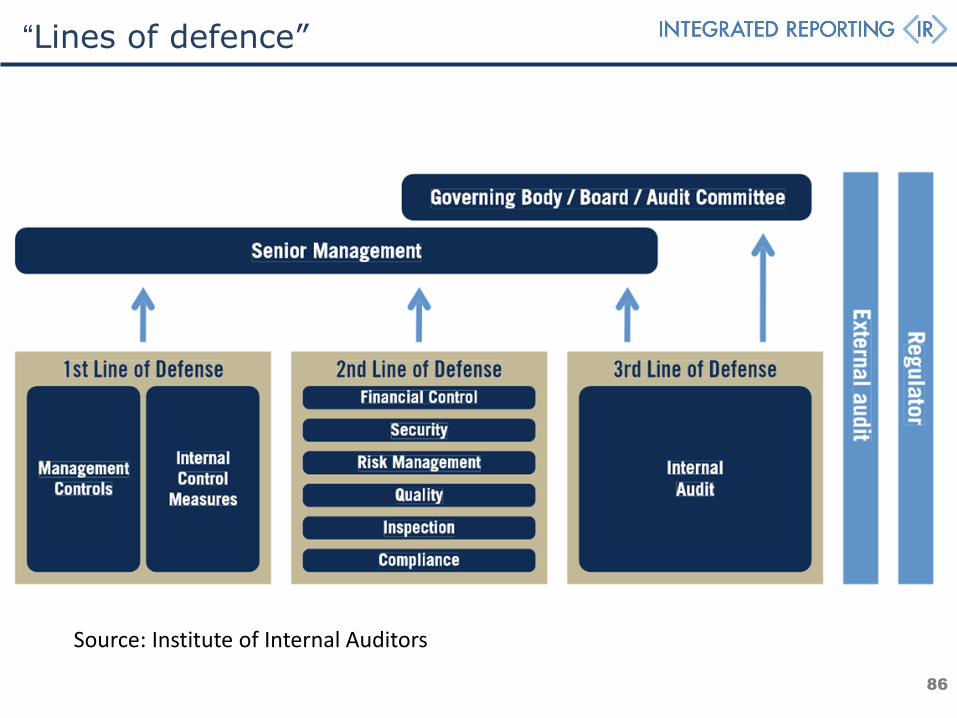

“Lines of defence”

86

Source: Institute of Internal Auditors

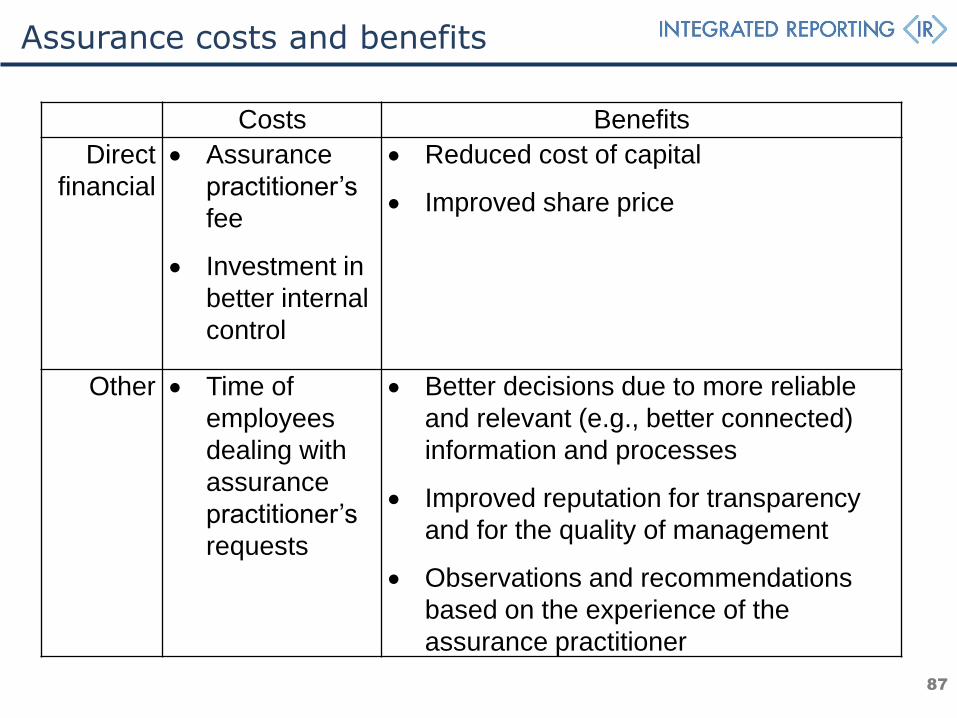

Assurance costs and benefits

87

Costs Benefits

Direct

financial

Assurance

practitioner’s

fee

Investment in

better internal

control

Reduced cost of capital

Improved share price

Other Time of

employees

dealing with

assurance

practitioner’s

requests

Better decisions due to more reliable

and relevant (e.g., better connected)

information and processes

Improved reputation for transparency

and for the quality of management

Observations and recommendations

based on the experience of the

assurance practitioner

Cost of capital – what investors say

88

The Short-listed Companies ‘Index’ - Long View

15.40%

86.23%

46.75%

27.81%

-40%

-20%

0%

20%

40%

60%

80%

100%

31-Mar-08 31-Mar-09 31-Mar-10 31-Mar-11 31-Mar-12 31-Mar-13

Time

Perc

enta

ge c

hange s

ince

1/4

/2008

FTSE350 Companies short-listed 3 years or more Companies short-listed 2 consecutive years All Companies short-listed each year

http://www.futurevalue.co.uk/future-value-strat-cap-index.html

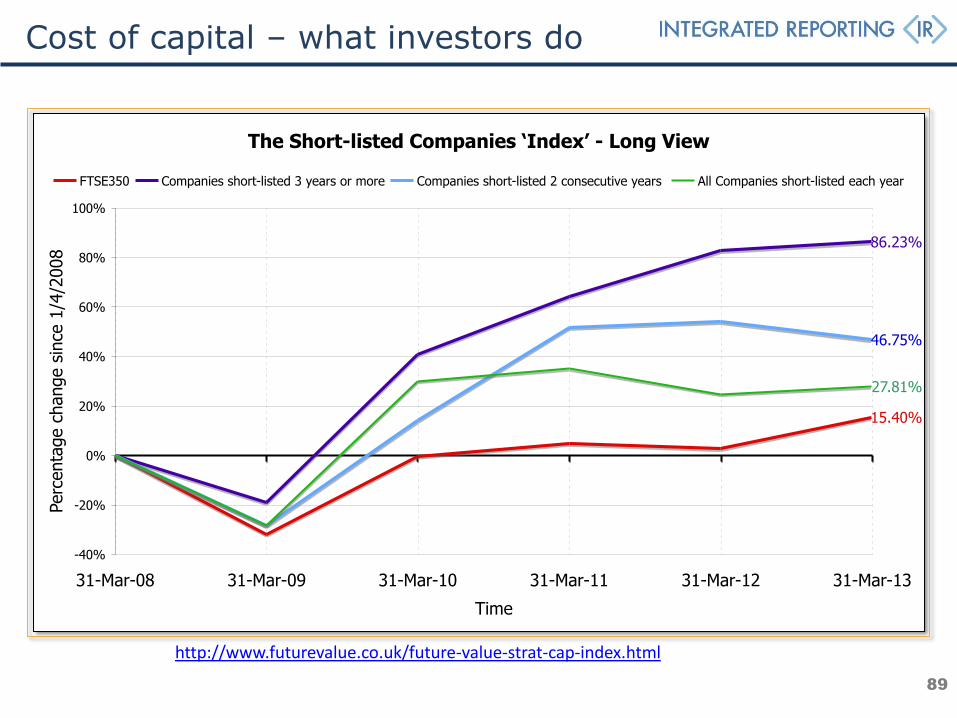

Cost of capital – what investors do

89

Assurance competencies and quality

90

Getting help

91

IIRC Pilot Programme Yearbooks and surveys Blogs, news and newsletters

www.integrtaedreporting.org

Creating Value series

92

Practical help

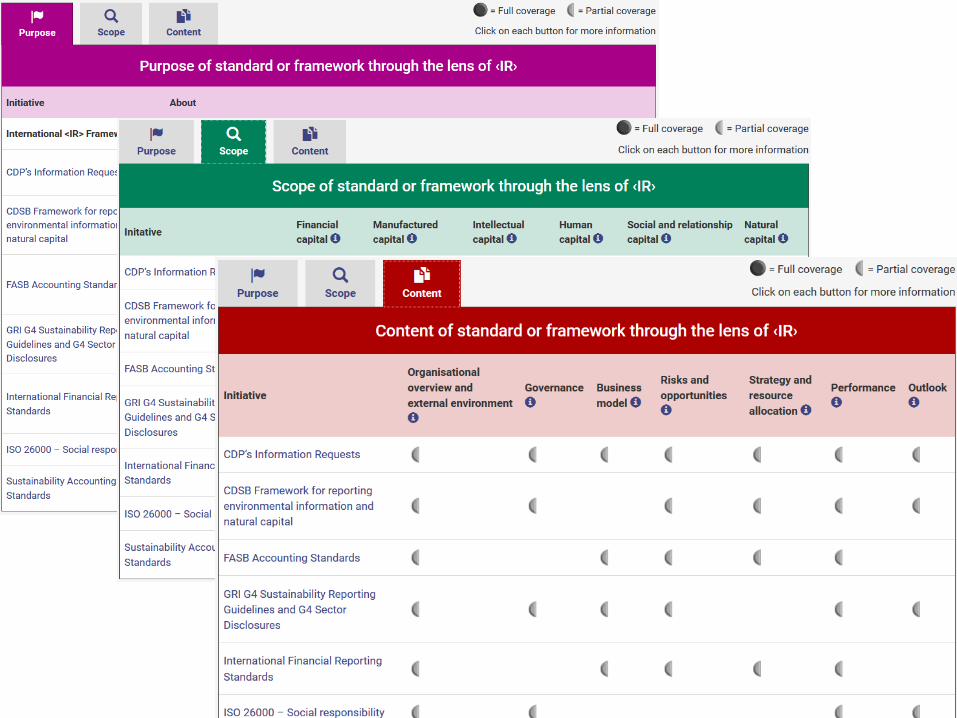

Corporate Reporting Landscape Map

Corporate Reporting Landscape Map

You’re not alone - Networks

• Countries/regions:

• Business Network

• Investor Network

• Regional Networks

• Pension Fund Network

• Banking Network

• Public Sector Pioneer Network

• Technology Initiative

• … Academic Network

• …… Accounting Bodies Network

97

What else is the IIC doing

• Framework revision

• … don’t wait

• Guidance

• Materiality

• Connectivity of information - megaforces

• Academic research

• Investor needs

• Materiality – completeness vs conciseness (UWA)

• Who reports and why

• Competency matrix

98

Examples (not templates)

99

Some tips <IR>: Unlock trust … and create value Kuala Lumpur 6 August 2015

Michael Nugent

Technical Director, Framework Development