Embed Size (px)

Citation preview

1 | P a g e

Financial Evaluation of The Cheesecake Factory Inc.

Joey Farquhar [email protected]

Tim Hipsher [email protected]

Trevor Rathbun [email protected]

Benjamin Johnson [email protected]

Charlie Horan [email protected]

2 | P a g e

TABLE OF CONTENTS

EXECUTIVE SUMMARY 6

INDUSTRY ANALYSIS 7

ACCOUNTING ANALYSIS 9

FINANCIAL ANALYSIS 10

VALUATION ANALYSIS 14

COMPANY/INDUSTRY OVERVIEW 15

COMPANY OVERVIEW 15

INDUSTRY OVERVIEW 15

FIVE FORCES ANALYSIS 18

RIVALRY AMONG EXISTING FIRMS 19

THREAT OF NEW ENTRANTS 31

THREAT OF SUBSTITUTION 32

BARGAINING POWER OF SUPPLIERS 32

BARGAINING POWER OF CUSTOMERS 33

KEY SUCCESS FACTOR ANALYSIS 34

COST LEADERSHIP 35

ECONOMIES OF SCALE 35

COST CONTROL 36

DIFFERENTIATION 36

SUPERIOR PRODUCT QUALITY 37

SUPERIOR CUSTOMER SERVICE 37

BRAND IMAGE 38

FIRM COMPETITIVE ADVANTAGE ANALYSIS 39

3 | P a g e

ACCOUNTING ANALYSIS 42

KEY ACCOUNTING POLICIES 44

TYPE I ACCOUNTING POLICIES 44

ECONOMIES OF SCALE 44

CUSTOMER SERVICE 46

PRODUCT QUALITY 47

TYPE II ACCOUNTING POLICIES 48

OPERATING LEASES 48

CONCLUSION 49

DEGREE OF ACCOUNTING FLEXIBILITY 50

OPERATING LEASES 50

GOODWILL 51

CONCLUSION 52

EVALUATION OF ACCOUNTING STRATEGY 52

OPERATING LEASES 53

GOODWILL 55

RESEARCH AND DEVELOPMENT 55

CONCLUSION 55

QUALITATIVE ANALYSIS 56

PRODUCT AND SERVICE QUALITY 57

OPERATING LEASES 58

RED FLAGS 58

ACCOUNTING DISTORTIONS 60

RESTATEMENT TABLE 61

DEPRECIATION TABLE 68

4 | P a g e

FINANCIAL ANALYSIS 69

LIQUIDITY RATIOS 69

CURRENT RATIO 70

QUICK RATIO 71

INVENTORY TURNOVER 72

INVENTORY DAYS OUTSTANDING 74

ACCOUNTS RECEIVABLE TURNOVER 76

ACCOUNTS REEIVABLE DAYS OUTSTANDING 77

CASH TO CASH 78

WORKING CAPITAL TURNOVER 80

CONCLUSION 81

PROFITABILITY RATIOS 82

SALES GROWTH 82

GROSS PROFIT MARGIN 83

OPERATING PROFIT MARGIN 85

NET PROFIT MARGIN 86

ASSET TURNOVER 88

RETURN ON ASSETS 89

RETURN ON EQUITY 90

CONCLUSION 92

CAPITAL STRUCTURE RATIOS 92

DEBT TO EQUITY RATIO 93

TIMES INTEREST EARNED RATIO 94

ALTMAN’S Z-SCORE 96

FINANCIAL FORECASTING 98

INCOME STATEMENT 98

DIVIDENDS FORECASTED 103

BALANCE SHEET 105

STATEMENT OF CASH FLOWS 111

5 | P a g e

RESTATED FINANCIALS 114

COST OF CAPITAL ESTIMATION 114

COST OF DEBT 115

COST OF EQUITY 117

BACKDOOR COST OF EQUITY 120

WEIGHTED AVERAGE COST OF CAPITAL 122

COMPARATIVE EVALUATION 125

INTRINSIC VALUATION 129

APPENDIX 145

6 | P a g e

Executive Summary

Analyst Recommendation: Sell (Overvalued)

52 Week Range 39.86-49.74 2008 2009 2010 2011 2012 2013

Revenue 1.9 Billion As stated 2.53 3.21 4.87 4.74 4.93 5.43

Market Cap 2.25 Billion Restated 2.38 3.11 3.61 3.64 3.7 3.74

Shares Outstanding 48.3 Million

Price

As Stated Restated Trailing P/E 39.42

Return on Equity 21.24 21.24 Forward P/E 34.79

Return on Assets 10.91 8.56 P/B 39.94

PEG 38.87

P/EBITDA 49.12

Estimated adj. r^2 Beta size adj. Ke EV/EBITDA 57.89

3 month 0.3687 0.915 0.1186

1 year 0.3688 0.915 0.1168 Price

2 year 0.369 0.915 0.1168 As Stated Re Stated

7 year 0.37 0.917 0.117 12.467 16.488

10 year 0.3702 0.917 0.117 91.62 115.74

16.6 19.64

As stated Restated 12.84 13.34

Backdoor Ke 10.81% 9.01%

BT WACC 11.59% 11.00%

Beta 1.637

Intrinsic Valuations

Discounted Dividends

Discounted Cash Flows

Residual Income

Long Run ROE Risidual Income

CAKE 6/1/2014- $45.87 Altman Z-Score

Market Valuations

Cost of Capital

7 | P a g e

Industry Analysis

The Cheesecake Factory is in the full service upscale-casual restaurant

industry. The Cheesecake Factory focuses on satisfying customers by delivering

quality meals from an innovative menu, and providing superior customer service.

Firms in this industry must possess value added business strategies to obtain a

competitive advantage over their competitors.

When analyzing the industry for it’s value added business strategies, we

used the Porters Five Forces Model. This can break the competitive forces down

by stating the level of competition from the rivalry among existing firms, threat

of new entrants, threat of substitute products, bargaining power of customers,

and bargaining power of suppliers. This tells us specifics about each firm within

the industry as well as data on the overall industry. It’s also important because it

gives potential investors and current shareholders an idea on how firms are

8 | P a g e

increasing shareholder wealth. Below is the summary table of Porters Five Forces

model for the upscale-casual restaurant industry.

Based on the five forces summary, we observed that rivalry among

existing firms is high. This high competition is likely caused from low

concentration in the industry, economies of scale, and a tight cost control

system. The threat of new entrants is low that is mostly due to high switching

cost and the need for high levels of economies of scale. The threat of substitute

products is high. Customers in this industry have many substitutable products.

There is the option of quick service as well as other available restaurants within

the industry. Our borrowing power from customers is high and suppliers is

opposite. Customers have bargaining power over firms, again, because of the

high threat of substitute products. The power of suppliers is low primarily due to

the high volume of suppliers. This allows firms to hedge prices and maintain

bargaining power over the suppliers.

After performing the five forces analysis, we now have a better

understanding of the upscale-casual restaurant industry. We were shown how

firms gain competitive advantages from a combination of cost control and

product differentiation business activities. These activities add value to the firm

and ultimately increase shareholder’s wealth.

Cheesecake Factory's Competitive Forces Level of CompetitionRivalry Among Existing Firms: High

Threat of New Entrants: Low

Threat of Substitute Products: High

Bargaining Power of Customers: High

Bargaining Power of Suppliers Low

9 | P a g e

Accounting Analysis

During the valuation process of Cheesecake Factory, it is important for us

to analyze the accounting policies and procedures presented within the recent

10-K. Companies have the ability to provide or distort certain information within

their annual and quarterly reports. It is our responsibility to seek out these

distortions and evaluate the quality of information given to us. Often, firms with

low quality of disclosure provide minimal details relating to their revenues,

expenses, and liabilities and vice versa for firms with high quality disclosure.

GAAP does require certain information to be placed in a company’s annual

report, but it is up to the management’s discretion to go beyond the requirement

and inform the reader more about their company.

To begin the accounting analysis, we determine what Cheesecake

Factory’s Type 1 and Type 2 key accounting policies. Type 1 accounting policies

can be linked to key success factors identified for Cheesecake Factory. We have

identified Cheesecake Factory’s type 1 accounting policies to be economies of

scale, superior customer service, and superior product quality. In Cheesecake’s

10-K they go in great detail about their key accounting policies but the remainder

of the annual report fails to be at the same level of disclosure as the competition

in the industry.

Type 2 accounting policies have more potential to distort information

provided to readers. We found that Cheesecake Factory’s type 2 policies to be

capital vs. operating leases and disclosure. Information regarding type 2

accounting policies clearly distorts Cheesecake Factory’s financial statements. For

example, the firm chooses to use only operating leases allowing Cheesecake to

leave a large portion of liabilities placed off the books. By capitalizing the leases

we are able to depict a more accurate picture of Cheesecake Factory’s liabilities

and obligations.

10 | P a g e

The quality of disclosure in Cheese Factory’s 10-K is poor. We determined

this analysis based on the amount of information presented in the report. Unlike

the competitors in the industry, Cheesecake Factory’s is below the industry

standard providing hardly any information relating to revenues, expenses, and

liabilities. The quality of disclosure present raises concerns in our valuation of the

company. We will have to identify all the red flags within the 10-K and possibly

restate the financial information to give us a more accurate description on the

operations of Cheesecake Factory.

Financial Analysis

The next thing we needed to look at to value The Cheesecake Factory was

to analyze the company’s financials through ratio analysis, forecasting financials,

and performing a regression study to determine cost of equity and backdoor cost

of equity. The first thing we had to do was perform a ratio analysis of The

Cheesecake Factory. The initial set of ratios we analyzed were the liquidity ratios

which include, current ratio, quick ratio, inventory turnover and days

outstanding, accounts receivable turnover and days outstanding, cash to cash

ratio, and working capital turnover. We analyzed these ratios to determine

health of the company and then compared the ratios to the industry.

Operating Lease Capital Lease

The Cheesecake Factory 100.00% 0.00%

BJ's Restaurants Inc. 100.00% 0.00%

Brinker Intl. 87.01% 12.99%

Darden Inc. 92.86% 7.14%

Percentage of Leases by Type 2013

11 | P a g e

Ratio Performance Comparison to

industry

Trend

Current Ratio Underperforming Over performing Downward

Quick Ratio Underperforming Over performing Downward

Inventory

Turnover

Over performing Average Downward

Inventory

Days

Over performing Average Upward

Accounts

Receivable

Turnover

Over performing Over performing Upward

Accounts

Receivable

Days

Over performing Over performing Upward

Cash to Cash Average Average Stable

Working

Capital

Turnover

Underperforming Underperforming Upward

Overall Underperforming Over performing Upward

The liquidity ratios show how easily a company can pay off their debt with

short term assets. After analyzing the liquidity ratios we saw that The

Cheesecake Factory underperforms overall but compared to the industry The

Cheesecake Factory generally outperforms the industry.

We analyzed the profitability ratios next. The profitability ratios tell us

how well a company retains income from sales as expenses are being taken out.

These ratios include sales growth ratio, gross profit margin, operating margin,

net profit margin, asset turnover, ROA, and ROE. We analyzed these ratios to

12 | P a g e

determine the health of The Cheesecake Factory and then compared the

company to the industry.

Ratios Performance Compare to

Industry

Trend

Sales growth Average Average Stable

Gross profit

margin

Average Average Stable

Operating margin Underperforming Average Stable

Net profit margin Underperforming Average Stable

Asset turnover Over performing Over performing Upward

ROA Underperforming Average Upward

ROE Over performing Average Upward

Overall average Average stable

After analyzing the profitability ratios we determined that The Cheesecake

Factory has generally healthy ratios and stay on par with the industry.

The last set of ratios we analyzed is the Capital Structure Ratios. These

ratios show us how a company funds itself and if it is headed for bankruptcy or

not. The capital structure ratios are debt to equity, times interest earned, and

Altman’s Z score. Again, we looked at these ratios to determine the health of

The Cheesecake Factory and then we compared to the industry.

Ratio Performance Industry compare Trend

Debt to equity Underperforming Underperforming Downward

Times interest

earned

Underperforming Underperforming Downward

Z score Over performing Over Performing Upward

overall Underperforming Underperforming Downward

13 | P a g e

After analysis of the capital structure ratios we determined that The

Cheesecake Factory has generally unhealthy ratios and are underperforming in

the industry. However, the Altman’s Z-Score which determines whether or not a

company is headed for bankruptcy was very high for The Cheesecake Factory

and tells us that the company is in no danger of going bankrupt.

The next step we took was to forecast the financials for the company over

the next 10 years. Forecasts are very volatile and prone to error but we

completed the forecasts as accurately as possible. When forecasting, our main

priority is to get a proper equity forecast, therefore, we do not care about the

liability forecast. The statement of cash flows is more volatile than the rest of

the forecast and is much more prone to error. The main focus of forecasting the

statement of cash flows is to get an accurate measurement on dividends so we

can get an accurate retained earnings forecast, and to get an accurate CAPEX

forecast. The rest of the statement is too prone to error and as such we did not

focus on it.

The final step in analyzing the financials is to run a regression test to

determine cost of capital. After running regressions with a 95% confidence

interval we decided on using the beta obtained through the 7 year treasury with

a 72 month horizon and got an adjusted beta of 1.637%. With this beta we

obtained a cost of equity of 17.46% which includes a size premium of 1.8%.

From there we used obtained an as stated backdoor cost of equity of 10.81%

and a restated backdoor cost of equity of 9.01% since we had to capitalize the

operating leases. We used these backdoor cost of equity rates to obtain an as

stated before tax weighted average cost of capital of 17.31% and a restated

before tax weighted average cost of capital of 15.69%.

14 | P a g e

Valuation Analysis

After the three prior analyses, we can now value Cheesecake Factory as

overvalued, undervalued, or fair. To begin the valuation process, we have

established ourselves as 10% analysts. Our results will be based on the

benchmark of the current price of $45.87 as of June 1st, 2014. Through this

comparison, we will come with a decision on the value of the company.

There are two methods for valuation. The first is the method of

comparable which uses industry prices as compared the company we are

valuing. The second method for valuation is the intrinsic valuation method. The

method for the valuation analysis we chose is the intrinsic valuation method. The

data for this method is purely based off Cheesecake Factory’s values rather than

the industries. The intrinsic valuation method consists of four valuation models

based off forecasted data; discounted dividends model, free cash flow model,

residual income, and long run residual income model.

The intrinsic method provides a more accurate and descriptive

interpretation on the future of the firm compared to other methods. To find

results from these models we take the forecasted data and put them into a

series of sensitivity analyses. The results from each model consistently interprets

that Cheesecake Factory is overvalued both as a stated and restated basis. The

residual income model is our best indicator of our recommendation because of its

dependency on the current situation of Cheesecake Factory. Through these

series of sensitive analyses, Cheesecake Factory’s model values fail to fall within

the lower and upper bounds limits of our 10% analysis. We conclude that

through our intrinsic valuation that Cheesecake Factory is currently overvalued.

15 | P a g e

Company Overview

The Cheesecake Factory, Inc. is an upscale casual, full service dining

establishment that competes in the food service industry and was incorporated in

Delaware in 1992. The company owns and operates 169 Cheesecake Factory

restaurants, 11 Grand Lux Café restaurants, and 1 RockSugar Pan Asian Kitchen

restaurant (Cheesecake 10-K). The Cheesecake Factory, Inc. also fully owns and

operates 2 bakery production facilities that are utilized to provide the desserts

the company is famous for to the restaurants and sell any excess capacity to

outside customers (Cheesecake 10-K).

The company utilizes a diversified menu to attract guests and fill the

restaurant at all hours of operation so they can stay competitive with the rival

companies. The great majority of Cheesecake Factories and Grand Lux Cafés are

located in the metropolitan areas of large cities or along the edge of metropolitan

areas where there are extremely high volumes of traffic per day at all times of

day from morning to late evening. The strategic advantage being that the larger

the volume of people moving past the restaurant during the day the more

opportunity there is for someone to stop in for a meal so that they can maintain

a full restaurant at all times of day.

Industry Overview

The Cheesecake Factory Inc. is a competitor in the restaurant industry in

the domestic United States as well as a future competitor in international

economies due to current licensing agreements. According to the National

Restaurant Association, restaurant sales “constitute 4 percent of the U.S. GDP”

with economic impact of an estimated $1.8 trillion. In billions of current dollars

restaurant industry sales have increased from $42.8 billion in 1970 to a projected

16 | P a g e

$683.4 billion in 2014. In 2010, during the middle of the recent economic

recession in the United States, restaurant sales were $586.7 billion. The

projected sales for 2014, which are $96.7 billion more than 2010, show an

increase in sales despite economic distress within consumer households in the

United States during this period.

Within the restaurant industry there are two primary divisions to

categorize establishments: quick service and full service restaurants. Differences

between these two categories involve service, quality, and time. Quick service

establishments involve fast-food and casual dining restaurants with no tableside

service. As the name suggests, quick service involves less waiting time on meals

17 | P a g e

than full service. Although there is a convenience factor for quick service

establishments, they also require the customers to self-serve themselves drinks

and other sides they may want or need. In contrast, full service establishments

employ waitresses and waiters to serve the guests, require guests to sit down for

an extended period of time, and also offer high quality food such as a prime

steak or a fresh water salmon made after ordering.

Companies in the restaurant industry compete on different levels based on

the type of establishment the restaurant is. Full service restaurants rely on high-

margin items and effective marketing of brand image in order to drive profits. In

contrast, quick service restaurants rely on high efficiency and high sales volume

in order to drive profits.

The demand in the industry is driven by factors that include

demographics, consumer tastes, and consumer income. In terms of

demographics and consumer income affecting demand in the industry, the lower

the consumer income the less disposable income customers have to spend on

dining out. Full service restaurants with higher menu prices target consumers

with a higher disposable income. Changing consumer tastes are also a driver of

demand in the restaurant industry. New flavors and awareness of ingredients

affect what product a company produces in order to gain more market share.

For analysis purposes we are defining the industry as upscale casual

dining. Upscale casual dining refers to full service establishments that compete

with a highly diverse menu selection, high quality service, prices that attempt to

target all socioeconomic classes, as well as presenting a décor and an ambiance

representative of a high quality establishment. The industry includes the

following firms: The Cheesecake Factory Inc., Brinker Intl., Darden Inc., and BJ’s

Restaurants Inc.

18 | P a g e

Porter’s Five Forces Model

Porter’s Five-Forces model aids financial analysts in answering questions

regarding the business strategy development of the company as well as an

overall industry analysis. This model also helps prospective and current investors

develop a better understanding of the industry in which the company operates as

well as the business strategy that the company implements in order to increase

shareholder wealth. The model consists of two factors, actual and potential

competition to a firm and bargaining power of customers and suppliers. The

competition factor of the model has three sub categories which include rivalry

amongst existing firms, the threat of new entrants, and the threat of substitute

product. These three sub categories along with the bargaining power of

customers and suppliers factor lead to industry profitability and help companies

decide how to operate the business activities and price products in order to

increase profit margins.

There are three levels of competition in an industry that the Five-Forces

model shows us: high competition, mixed competition, which consists of high

and low form of competition components, and low competition. High competition

does not allow firms room for variances in standard prices of products in an

industry while low competition allows firms to be able to specialize in a few

products, allowing control of prices and markets. All of the five aspects of the

model work together to help analyze the prospective profitability of an industry

as well as the firm in the industry.

19 | P a g e

Cheesecake Factory's Competitve

Forces Level of competition

Rivalry Among Existing Firms: High

Threat of New Entrants: Low

Threat of Substitute Products: High

Bargaining Power of Customers: High

Bargaining Power of Suppliers: Low

Rivalry Among Existing Firms

Rivalry among existing firms is a sub category of competition in the Five-

Forces model we are using for analysis. This category measures the competition

that is present in the upscale casual dining industry. When measuring the level of

competition of rivalries among existing firms, key success factors include:

Concentration of the industry

Product differentiation

Growth rate of specific firms and the industry as a whole

Scale and learning economies

Switching costs

Excess capacity

Utilizing these factors in the Five-Forces model can help firms improve and

maintain an efficient current business strategy in the industry in order to grow

profit margins.

20 | P a g e

Industry Concentration

The amount and size of the firms in an industry define the industry’s

degree of concentration. The degree of concentration determines whether firms

in an industry can be a price-taker or a price-setter. If the industry is dominated

by one firm it is considered a monopoly and the dominant firm will be the price-

setter, with less dominant firms using the prices as a benchmark. Industries that

have three or four equally sized firms cooperate in order to avoid price

competition that can become destructive to the industry as a whole, resulting in

a mix between price-setting and price-taking. Industries with fragmentation face

steep price competition between the firms involved. The degree of concentration

in the upscale casual dining industry in the United States is low due to existing

firms expanding their brands year to year. Shown below is the industries

concentration based on sales.

2009 2010 2011 2012 2013

Cheesecake Factory Inc. 12.79 13.66 13.91 13.56 13.36

BJ's Restaurants, Inc. 3.41 4.23 4.91 5.31 5.52

Darden Inc. 57.64 58.57 59.34 59.97 60.86

Brinker Intl. 26.16 23.54 21.85 21.15 20.26

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

% o

f S

har

e

Years

Industry Market Share (Sales)

21 | P a g e

The industry market share based on sales indicate that Darden Inc., holds the

majority of market share in the industry with Cheesecake Factory, Brinker Intl.,

and BJ’s Restaurants rounding out the bottom 40% of market share. One factor

behind the large market share of Darden Inc. is the number of restaurants the

company currently has in operation. Darden currently “[operates] 2,138

restaurants” that include 8 different brands (Darden 10K). Brinker Intl. operates

“more than 1,600 restaurants” with the brands being Chili’s and Maggiano’s

(Brinker 10-K). The Cheesecake Factory Inc. and BJ’s Restaurants operate on a

smaller scale than both Brinker and Darden. The Cheesecake Factory owns and

operates 181 restaurants with “169 under the Cheesecake Factory mark, 11

under the Grand Lux Café, and 1 under the RockSugar Pan Asian Kitchen mark”

(Cheesecake 10-K). BJ’s currently “owns and operates 150 restaurants as of May

2014” (BJ’s 10-K).

Although the firms in the industry vary in size, the “average check per

person was in the range of $16.25 to $16.75” for Darden Inc. during 2013

(Cornell). The average check per person for The Cheesecake Factory Inc. during

fiscal 2013 “was approximately $19.70” (Darden 10-K). BJ’s Restaurant has an

“average customer check of $11.00 to $17.00” during 2013 (BJ’s 10-K). The

similarity in price range for check per person within this industry despite the

differences in market share based on sales indicates that competition rivalry

amongst firms in the industry is high, thus leading to a mixture of price-setting

and price-taking within the industry.

22 | P a g e

Differentiation

Product differentiation creates a competitive advantage in price

competition in the upscale casual dining industry. Competitors producing similar

products in the industry allow consumers to switch firms on pure-price basis.

This factor leads to companies in the industry being price-takers in terms of the

similar products due to the high price competition present in an industry. In

contrast, when companies offer differing products than competitors, the firm

competes less on price and more on quality and service. This allows the

company to be price-setters in terms of the differing products.

For example, The Cheesecake Factory Inc. has product differentiation in

dessert products. The menu offers “approximately 50 varieties of cheesecake

and other quality baked deserts”. This product differentiation is a value driver

and allows the company to be a price-setter for the product by “offering high

quality deserts, [which] results in significant level of dessert sales, approximately

15% of The Cheesecake Factory restaurant sales for fiscal 2013, 2012, and

2011” (Cheesecake 10-K). BJ’s Restaurant’s use product differentiation by

“offering as many as 30 guest domestic and imported craft beers” with the

“[intent] to enhance BJ’s competitive position as the leading retailer of craft beer

in the casual dining segment.” BJ’s alcohol sales are a value driver of the firm in

the upscale casual dining industry and represent “approximately 22% of total

restaurant sales in 2013” (BJ’s 10-K).

“One of our competitive strengths is our ability to anticipate consumer

dining and taste preferences and adapt our menu to the latest trends in food

consumption” (Cheesecake 10-K). As an example, consumers are now more

concerned about what ingredients are in their food along with how “healthy”

their food is. As a response to this recent demand of healthy living, the

Cheesecake Factory has developed the SkinnyLicious® menu, “which offers

approximately 50 innovative items at 590 calories or less” (Cheesecake 10-K).

23 | P a g e

Darden Inc. offers items at its Seasons 52 restaurant that are “[no] more than

475 calories” (Darden 10-K), BJ’s restaurants offer “a lower calorie menu

category called Enlightened Entrées®” (BJ’s 10-K), and Brinker Intl. offers a

“lighter choices” menu that has items with less than 650 calories. These are

examples of companies responding to consumer tastes and preferences using

research and development as a means to differentiate products to drive value in

the industry.

Differentiation is also present in the firm’s atmosphere and services

offered. Companies in the upscale casual dining industry differentiate the

atmospheres of restaurants by using décor and designs that are parallel to the

firm’s business strategy. The Cheesecake Factory places “significant emphasis on

the unique, contemporary interior design and décor of [their] restaurants” in

order to create a “high-energy ambiance in a casual setting.” (Cheesecake 10-K).

Brinker Inc. differentiates their atmospheres of their restaurants based on the

brand. For example, Brinker Intl.’s Maggiano’s Little Italy restaurant’s interior

design “of all locations transport[s] [the] guests back to a classic Italian-

American restaurant in the style of New York’s Little Italy in the 1940s” (Brinker

10-K). The differentiation strategy in atmospheres of upscale casual dining

establishments are used as value drivers within the industry.

Conclusion

In the upscale casual dining industry differentiation of services and

products offered drive value for the firms. The degree of differentiation is a

mixture of highly differentiated and similar products and services. Companies in

the industry offer many of the same menu items such as steaks, pastas, and

salads. However, differentiation in specialty products such as The Cheesecake

Factory’s desserts and BJ’s Restaurants wide variety of beer on tap are product

differentiations that drive value for the companies. The service that firms provide

24 | P a g e

to customers in the industry is similar, with all company’s missions toward

hospitality ensuring that guest satisfaction is of “highest priority”. The

differentiation of concepts and atmospheres between restaurants in the industry

allow customers to differentiate between the firms based on consumer tastes

and preferences. Overall, differentiation of products, services, and atmospheres

are value drivers within the upscale casual dining industry and cause a mix of

Industry Growth Rate

Industry growth rate aids business analysts in determining if an industry is

either growing, declining, or is stagnate. The growth rate also helps indicate how

firms should revise current business plans in order to compete for market share

in the industry. When an industry is experiencing high growth companies can

gain a competitive advantage by developing new products in accordance with

current consumer tastes as a means to attract new consumers in order to gain

share of the growing market. In a low growth industry firms compete on price in

order to take business from the industry’s competitors.

The food service industry as a whole currently employs 13.5 million people

in the United States which consists of “10% of the overall U.S. workforce.” As of

2014, restaurant industry sales are projected to reach $683.4 billion,

experiencing an increase of “3.6% in nominal terms” (National Restaurant

Association). Firms in the overall restaurant industry expand by franchising or

opening more company owned stores.

For the purpose of analysis the industry we are valuing is consistent of

higher quality products and services, called the upscale casual dining industry.

25 | P a g e

With respect to sales revenues in the upscale casual dining industry

Darden Inc. holds the overall market share in comparison to other firms. The

average trend in sales revenues of the industry from 2010 to 2013 is increasing

for all firms in the industry. Between 2009 and 2010 however the trend in sales

revenue was decreasing. The decrease in sales revenue during this time period

can be attributed to the economic recession experienced in the United States.

Less consumer income means less disposable income to spend on dining out,

therefore leading to decreased sales in the upscale casual dining industry.

Annual sales growth, pictured below, is used to analyze the percentage of

sales growth that each firm experienced in the industry between 2009 and 2013.

Overall industry sales did not grow and instead shrank in terms of annual sales

growth between 2009 and 2010. However, between 2011 and 2013 the firms

and industry as a whole experienced annual sales growth, with the total sales

growth of the industry equaling 4.08%, 5.51%, and 5.36% for years 2011, 2012,

and 2013 respectively. The growth, steady and not increasing exponentially, is a

Sales Revenues (in thousands)

2009 2010 2011 2012 2013

Cheesecake

Factory Inc. $1,602,020.00 $1,659,404.00 $1,757,624.00 $1,809,017.00 $1,877,910.00

BJ's

Restaurants,

Inc. 426,707.00 513,860.00 620,943.00 708,325.00 775,125.00

Darden Inc. 7,217,700.00 7,113,100.00 7,500,200.00 7,998,700.00 8,551,900.00

Brinker Intl. 3,276,362.00 2,858,498.00 2,761,386.00 2,820,722.00 2,846,098.00

Total Industry

Sales 12,522,789.00 12,144,862.00 12,640,153.00 13,336,764.00 14,051,033.00

26 | P a g e

sign that the upscale casual dining industry has recovered from the economic

recession during 2009 and 2010. The consistent average increase in sales growth

for the industry is indicative of a high competition market within the industry,

thus leading to a mixture of price-setting and price-taking tendencies by firms

within the industry.

Conclusion

The upscale casual dining industry, consisting of The Cheesecake Factory

Inc., Brinker Intl., Darden Inc., and BJ’s Restaurants, Inc., shows to have

recovered from the economic recession taking place during 2009 and 2010 with

a positive and consistent growth rate in years 2011, 2012, and 2013. The

consistent average increase in sales growth of the industry as a whole indicates a

highly competitive market that is currently expanding, resulting in a mix of price-

taking and price-setting between the firms of the industry in order to increase

profitability.

27 | P a g e

Economies of Scale

In the upscale casual dining industry learning curves of products are

pivotal to being able to gain share of the market and increase sales. Steep

learning curves and the presence of other scale economies in the industry

require having enough capital and resources as a firm to achieve a learning

economy. Learning economies will result in quicker development of products that

target ever changing consumer tastes in an effort to gain a greater share of the

market. Below is the total assets of each firm in the upscale casual dining

industry we are valuing.

2009 2010 2011 2012 2013

Cheesecake Factory Inc. -0.27 3.58 5.92 2.92 3.81

BJ's Restaurants, Inc. 12.33 16.96 17.25 12.34 8.62

Darden Inc. 8.92 -1.45 5.44 6.65 6.92

Brinker Intl. -22.64 -12.75 -3.40 2.15 0.90

Total sales growth of industry -2.49 -3.02 4.08 5.51 5.36

-25.00

-20.00

-15.00

-10.00

-5.00

0.00

5.00

10.00

15.00

20.00

% o

f S

ale

s G

row

th

Annual Sales Growth %

28 | P a g e

In the industry that we are valuing the overall size of the firm in terms of

assets allows opportunities for more research and development of new ideas and

products due to having more capital. Darden Inc. captures approximately 60% of

sales revenue in the market for the industry and in correlation has the highest

amount of assets of any firm in the industry. By having more available assets to

use for capital Darden creates learning economies through product development,

thus capturing a greater share of the market in the upscale casual dining

industry. Another example of using assets to develop learning economies of scale

is vertical integration of inputs and outputs of a firm. For example, The

Cheesecake Factory Inc. vertically integrated its bakery production, “Vertical

integration of this vital part of our brand gives us control over the creativity and

quality of our deserts and is also more profitable than buying from a third party”

(Cheesecake 10-K). Vertical integration of bakery production creates an economy

of scale for The Cheesecake Factory in the industry. Controlling inputs and

outputs of the production process allows the firm to control costs of products

and has led dessert sales to account for “15% of restaurant sales.”

$-

$1,000,000

$2,000,000

$3,000,000

$4,000,000

$5,000,000

$6,000,000

$7,000,000

$8,000,000

2009 2010 2011 2012 2013

Total Assets (Thousands)

Cheesecake Factory BJ's Restaurants Brinker Intl. Darden Inc.

29 | P a g e

Conclusion

Economies of scale allow firms in the industry to control inputs and

outputs of production process, possibly lowering costs related to specific

products of a firm. Economies of scale are achieved in industries with steep

product learning curves by using capital as a means to develop learning

economies. Overall size of the firm in an industry affects the development of

learning economies and economies of scale due to the amount of assets a firm

has to put forth to product development. Economies of scale allow firms to

compete on costs and results in price-setting within the industry.

Switching Costs

When a firm is contemplating discontinuing operations in its current

industry and plans to enter another industry the firm will incur switching costs.

Switching costs in the restaurant industry are high, with property and equipment

specifically designed and produced for the purpose of restaurants. In the upscale

casual dining industry switching costs are high due to the “high quality” products

and services the firm offers. Ceasing operations in the industry would require

firms to sale supplies that are specific to the restaurant industry, thus having

little value to other industries. Kitchen supplies, décor, and fixtures within the

restaurant would be liquidated in order to exit the industry. Liquidating assets

can result in losses, thus increasing switching costs for the firm.

Along with costs to exit the industry a firm may incur costs to enter a new

industry. Purchasing of new assets related to the new industry, legal costs, as

well as a restructuring of business strategy are all factors associated with

switching costs for a firm.

30 | P a g e

Conclusion

Switching costs are costs that are related to ceasing operations in one

industry and beginning operations in a different industry. In the upscale

restaurant industry switching costs are high for firms due to the specialized

products used within the industry such as dining room furniture and heavy

kitchen appliances. Due to the high degree of switching costs firms are

discouraged from exiting the industry and thus create a highly competitive

market amongst firms in the industry.

Excess Capacity

Excess capacity occurs when the overall production is greater than the

consumers demand for products. High excess capacity results in increased

inventory expenses and unsold products increase the costs of goods sold.

In order to contain excess capacity to an acceptable level firms in the

upscale casual dining industry schedule inventory shipments based on current

demand of products. For example, The Cheesecake Factory Inc., “[negotiates]

short-term and long-term agreements” for the supply of inventory and

equipment requirements “depending on market conditions and expected

demand” (Cheesecake 10-K). By negotiating inventory shipment dates with

suppliers, firms in the industry control the level of excess capacity in the

company. The agreements help companies maintain stock and hedge against

over stocking in order to reduce costs related to inventory.

An industry’s excess capacity can be measured by dividing the total sales

by Plant, Property, and Equipment. The measure determines if the firms fixed

costs are producing profits for the company. The goal is to maintain a high sales

to plant, property, and equipment ratio in order to avoid pricing wars amongst

31 | P a g e

industry competitors. Below is the excess capacity ratios of the industry we are

valuing.

Threat of New Entrants

In the upscale casual dining industry the threat of new entrants is low due

to the market being relatively saturated. There are barriers to entry because

there are multiple firms that are established in the industry. Due to larger firms

being established, entering the industry is difficult due to market share already

being taken by other companies. A firm would have to compete on costs, which

is what the already established firms are already competing on. Also, a new firm

would have to compete against the brand value of the already established firms.

By entering a new market a new firm has to establish an economy of scale

to compete with the other firms. This can be difficult due to the new firm having

to create new relationships with their suppliers. Also, a new firm has little

negotiating power compared to firms that are already established and have been

in a relationship with their suppliers for an extended period of time.

-

0.50

1.00

1.50

2.00

2.50

3.00

2009 2010 2011 2012 2013

Excess Capacity (Sales/PPE)

Cheesecake Factory Inc. BJ's Restaurants, Inc. Darden Inc.

Brinker Intl. Industry

32 | P a g e

Threat of Substitute Products

Customers will think alternative products or services are substitutes based

on the price difference, how different a products function is, and how willing they

are to switch to another product. With such low concentration in the upscale

casual restaurant industry, the availability of substitutes is high. “Relevant

substitutes are not necessarily those that have the same form as the existing

products but those that perform the same function. For example, airlines and car

rental services might be substitutes for each other with it comes to travel over

medium distances.” (Palepu)

Because there are so many possible substitutes, we believe that it is

important to obtain differentiation. Offering customer satisfaction, superior

quality products, and a unique environment will help a company develop brand

loyalty and competitive advantage over competitors. By minimizing your product

cost and offering a reasonable price per plate allows you to compete on cost.

On the other hand, there will always be substitutes. Focusing on these

business operations can give you a competitive advantage. This reduces the

chance of customers going elsewhere and will potentially increase brand loyalty.

Bargaining Power of Suppliers

The bargaining power of suppliers in the upscale casual dining industry is

low. The companies in the industry mainly obtain their goods through suppliers

that they have negotiated long term contracts with (CAKE 10K) and therefore the

suppliers have very little control over who they supply to and by how much once

the contracts are signed. This results in very little bargaining power of suppliers

since the only chance they have to negotiate is during the contract negotiations

33 | P a g e

and even then the volume of suppliers in the industry is very large which creates

very little room for the suppliers to negotiate a price they want.

This method of contract negotiation allows the companies in the industry

to use a cost control method to keep the suppliers from changing prices on

them. Once the contracts are signed and the prices are negotiated, the supplier

has no ability to change their prices or stop supplying these companies. Because

of this the companies can maintain a consistent cost allocation to supplies that

allows them a high degree of flexibility with their other expenses.

Due to this the suppliers have very little bargaining power within the

upscale casual dining industry. A high volume of suppliers creates little room for

the suppliers to negotiate prices when writing up a long term contract with these

companies. This creates a large amount of flexibility for the companies and next

to nothing for the suppliers.

Bargaining Power of Customers

The bargaining power of customers is directly correlated to the threat of

substitute products and whether or not the product being supplied is a

commodity or a necessity. The upscale casual dining industry provides a

commodity service and there is a high threat of substitution within the industry

that creates a very high degree of bargaining power for the customers. As

evidenced by the financial statements from each company’s 10K, when the

economy crashes the upscale casual dining industry takes the crash very hard.

Sales decreased substantially across the board which ultimately negatively

affected net income and retained earnings.

This was all caused by the fact that the industry provides a commodity

service and the consumer base can substitute that product with cheaper

34 | P a g e

alternatives. This causes a massive backlash to the industry because the value

drivers that these companies use to obtain and retain business are rendered

useless because the customer has enough bargaining power that they can

choose to not utilize the product supplied whenever they want.

Because of these reasons we have concluded that the customers have a

very high degree of bargaining power within the upscale casual dining industry.

The ability for the customers to come and go as they please due to the high

availability of substitute products creates a very large amount of bargaining

power that the companies in the industry must follow. These companies do not

offer anything that the consumer needs to have that they cannot get anywhere

else.

Analysis of Key Success Factors for Value Creation in the

Industry

We have discussed how the five forces model can influence the

profitability of an industry as a whole. Now, we will express our analysis on the

industry's business activities that can add value and also create a competitive

advantage. There are two primary categories for achieving competitive

advantage – cost leadership and differentiation. After analyzing The Cheesecake

Factory and its competitors, we have determined our industry is primarily price

setters with a little price taking.

35 | P a g e

Cost Leadership

Cost leadership is “supplying the same product or service at a lower

cost.” (Palepu) It is possible to achieve a competitive advantage by cost

leadership from the following: economies of scale and scope, efficient

production, simple product designs, lower input costs, low-cost distribution, little

research and development or brand advertising, and also tight cost control

system. (Palepu) However, in the upscale casual restaurant industry, we think it’s

necessary to focus on achieving economies of scale and a tight cost control

system.

Economies of Scale

Economies of scale are a cost benefit a firm receives whenever they

buy, produce, or sell a large quantity of a product. The more the firm is able to

produce or sale, the more they fixed cost-per unit is going to decrease. In the

restaurant industry, with such a low concentration, it’s critical to the companies

in the industry to get inputs at a cheaper cost than competitors.

The Cheesecake Factory has 181 company restaurants and is also

currently expanding into the Middle East and Mexico. The firm has a bakery in

California and North Carolina. In this upscale casual industry firms are constantly

expanding not only nationally but also globally.

Based on the information above we’ve concluded that it’s important to

take advantage of the cost benefit from economies of scale. The more

restaurants a firm has the more inputs it will need. Having 2 bakeries makes it

possible for them to make their own products and offer a lower cost than their

competitors.

36 | P a g e

Tight Cost Control System

No matter the industry a company is in, every company is always seeking

to minimize cost. Obtaining a tight cost control system can be difficult to achieve

if a company’s budget is not tight. A way of cutting cost within a company can

be done by observing business operations over time and looking for possible

trends.

“Substantially all of our food and supplies are available from multiple

qualified suppliers, which helps to diversify our overall commodity availability and

cost risks. Independent foodservice distributors, including the largest foodservice

distributor in North America, deliver most items multiple times per week to our

restaurants. We attempt to negotiate short-term and long-term agreements for

our principal commodity, supply and equipment requirements, depending on

market conditions and expected demand.” (CAKE 10-K)

After analyzing the information above, we as a team of analyst have

determined that having multiple suppliers is beneficial because it ensures quality

products. It also prevents a company from putting all of its eggs in one basket.

Having high quality distribution is important because the firms in the industry

can’t sell something if they can’t make it. The Cheesecake Factory also hedges

for better prices by negotiating short and long term contracts with its suppliers.

Differentiation

We believe differentiation is the primary target for the upscale casual

restaurant industry. Specializing in differentiation, companies are able to set

prices for unique characteristics that they have. Differentiation is “supplying a

unique product or service at a cost lower than the price premium customers are

willing to pay.” (Palepu) The ways the industry achieves differentiation are by

having superior product quality, superior product variety, superior customer

37 | P a g e

service, more flexible delivery, quality investment in brand image, investment in

research and development, and control system focus on creativity and

innovation. In the upscale casual restaurant industry, we believe it’s important to

achieve product quality, customer service, and a brand image.

Superior Product Quality

Customers in the upscale casual restaurant industry pay the extra cost for

the high quality food. A superior product makes people not only remember the

company but also makes them want to return for more.

“As of February 27, 2014, we operated 181 Company-owned upscale,

casual, full-service dining restaurants.” (Cheesecake 10-k) The Cheesecake

Factory also prepares their menu items fresh from scratch daily, use all natural

chicken with no hormones, and premium beef that is Certified Angus, U.S.D.A.

(Cheesecake Investors)

Most chains in this industry have a lot of restaurants. We think it is

important that a guest can have a good quality meal in Texas and then goes to

California and have the same meal. The quality of the inputs should be equally

superior at all locations. In this upscale industry it only takes one mess up to lose

a customer, and providing superior quality products at all locations will prevent

this from happening. This will create a brand image and keep loyal customers

returning.

Superior Customer Service

When customers pay extra for a quality product they expect the service as

well. Service in the upscale casual industry is to be superior to the rest.

“Commitment to excellent service and hospitality through the selection, training

38 | P a g e

and retention of high quality staff members. Our mission is to create an

environment where absolute guest satisfaction is our highest priority. We strive

to consistently exceed the expectations of our guests in all aspects of their

experience in our restaurants and with our bakery products.” (Cheesecake 10-K)

As a team of analysts we think providing superior customer quality service

is one of the most critical factors in achieving a competitive advantage.

Employees must be experienced and knowledgeable in order to exceed guest

expectations. Also, employees need to dress professionally. Attire helps set the

more upscale atmosphere. Overall, employees should focus on doing whatever

necessary to have customers leave with the feeling of satisfaction.

Investment in Brand Image

Achieving a good brand image is necessary to gain people’s trust.

Whenever people talk about a company they should only say positive things by

the experiences they have had in the past. Having superior quality products and

superior quality customer service at one location is just as important as having

those at every other location. This comforts people in knowing that you’re going

to get the quality service you pay for everywhere you go and not just a specific

location.

“Our restaurants’ distinctive contemporary design and décor create a high

energy, non-chain image and upscale ambiance in a casual setting… We apply

high standards to the maintenance of our restaurants to keep them in “like new”

condition.”(Cheesecake 10-K)

The feeling you get whenever you go to a restaurant chain should be

unique to others. Having a clean and “like new” feeling impresses customers and

leads to improved customer satisfaction that leads to people talking about a

company which increases overall traffic.

39 | P a g e

Conclusion

Overall, in this upscale casual restaurant industry we think it’s important

to target differentiation with some cost control. This allows the companies to

develop superior business strategies that add value to their respective company

and help themselves stand out to competitors. All of these key success factors

assist the companies in gaining a competitive advantage over competition and

most importantly to increase shareholder’s wealth.

Firm Competitive Advantage Analysis

Superior Product Variety

At first glance, the Cheesecake Factory’s menu can be slightly

intimidating. It features over 200 items to choose from and a variety of food

types. Considering that you can get anything from a steak, to pasta, it seems to

us that the Cheesecake Factory is a great compromise to take a family that can’t

decide on a place to eat. The Cheesecake Factory’s menu serves pizzas, burgers,

sandwiches, pastas, seafood, steaks, and salads. Recently the Cheesecake

factory came out with their “Skinnylicious Menu”. It contains over 40 meals and 5

drinks that are healthier alternatives to the other options. The Cheesecake

Factory also features a diverse desert menu with over 50 different types of

cheesecakes. In addition to their food, the Cheesecake Factory has an abundant

drink menu featuring specialty drinks, cocktails, mojitos, margaritas, martinis,

and an impressive beer and wine selection. Their beer selection varies depending

on the location so they can offer local brews as well as the national know beers.

40 | P a g e

They offer wines from California, Washington, Europe, South America, and

Australia ranging from $7.95-$12.95 per glass. The selection of food and drink

show us that The Cheesecake Factory utilizes product differentiation as a major

value driver. In order to separate themselves in the industry they must use

product differentiation to maintain business.

Superior Product Quality

In our opinion, the fact that the cheesecake factory makes all of their

meals from scratch daily gives them a huge advantage over some of their other

competitor chains. They will also cater to every one of the diner’s needs. “We will

gladly honor requests to modify your order to suit specific health or dietary

needs” (Cheesecake Investors). The Cheesecake Factory also sells their famous

cheesecakes to other restaurants. To guarantee their superior food quality, the

Cheesecake Factory claims to use only the highest quality ingredients to produce

the best product. We believe that this product quality is leaps and bounds

beyond their industry competitors. The flexibility The Cheesecake Factory has

with its products and customer service represent a superior product quality,

another value driver for the company. In order to compete in the industry the

company must maintain this level of quality to pull business from the

competition.

Locations and Future Growth

The Cheesecake Factory has become an international brand name.

Cheesecake Factory has 169 locations in the United States including Puerto Rico.

In 2012, the Cheesecake Factory expanded its international boarders to the

United Arab Emirates, opening in the Dubai Mall, and in 2013, another location

41 | P a g e

opened in the Mall of the Emirates. The Cheesecake Factory also came out with

2 different restaurants, the Grand Lux Café and Rocksugar Pan Asian Kitchen.

The Grand Lux Café, which serves American, European, Thai, and Caribbean

cuisine, has 11 locations featured in the United States. The Cheesecake Factory

opened the Rocksugar Pan Asian Kitchen in 2008 with their only location in Los

Angeles. By the end of 2014, the Cheesecake Factory plans to open several more

locations in the U.S. and plans to have 3-5 locations in the Middle East

(thecheesecakefactory.com). We believe that with the amount of locations, both

nationally and abroad, and the plan for future growth gives the Cheesecake

Factory staying power. The way The Cheesecake Factory grows is by building

new restaurants. By showing us that they are aggressively expanding, not only in

the US, but in foreign countries as well, we see that The Cheesecake Factory

plans to stay competitive with its growth.

Strengthening Brand Image

The Cheesecake Factory’s community involvement and charitable giving’s

have helped strengthen the Cheesecake Factory’s brand name. They are involved

with several charities including: Feeding America, The Salvation Army, City of

Hope, and The Harvest Food Donation Program. On Thanksgiving Day, the

Cheesecake Factory’s staff members volunteer at their local Salvation Army.

They “prepare and serve an elaborate “Cheesecake Factory” traditional holiday

42 | P a g e

meal to thousands of disadvantaged individuals and families at Salvation Army

Community Centers across the country” (thecheesecakefactory.com). For City of

Hope, they host an annual golf tournament and auction fundraiser. Together

with their vendor partners, they have donated more than $2.1 million to City of

Hope. Through the Harvest Program, they donate all of their surplus food to local

soup kitchens, shelters, and after-school programs. Through this program, they

have donated more than 500,000 pounds of food each year. In addition to these

charities, they also contribute through their very own “Give back” Foundation

Team Sponsorship by getting involved with local communities and non-profit

organizations. In our opinion, all of their charitable donations and community

service have helped to improve their brand name. Now people don’t just like the

Cheesecake Factory for their cheesecakes, but they also like the fact that they

are getting involved in their community. This shows us that the Cheesecake

Factory isn’t only concerned with what’s going on inside their restaurant walls

and are focused on improving brand recognition nation-wide.

Accounting Analysis

After analyzing the business strategies, we’ve determined the key value

drivers, risks, and potential industry profitability by using Porters Five Forces

Analysis. We then used qualitative measures to determine whether a firm is able

to sustain a competitive advantage. Now, we will perform step three of analyzing

corporate financial statements, an accounting analysis. “Accounting analysis

evaluates accounting quality by assessing accounting policies and

estimates”…”The purpose of accounting analysis is to evaluate the degree to

which a firm’s accounting captures its underlying business economics.”(palepu)

We have performed an accounting analysis to potentially discover any

distortion and biased information in the financial statements. Distortion is caused

43 | P a g e

by the flexibility allowed to a firm’s management from the Generally Accepted

Accounting Principles. Management is given flexibility so they can show the

financial position of the firm. However, they can often be inclined to manipulate

and forecast their financials to benefit them personally. They could have a lot of

stock in the company, quarterly targets to hit, and questionable job security. It is

our job to undo any biased opinions or distortion.

In order to undo distortion and biased opinions from management we will

perform an accounting analysis that consists of 6 steps. First, we have to identify

the accounting policies. This involves the analyst identifying and analyzing the

firm’s policies and estimations. Next, we will assess the degree of flexibility given

to a firm. When management does the firm’s financials they have to make

estimations. They also might be inclined to make biased decisions for their

personal benefit. The third step is to evaluate the accounting strategy.

Evaluating the accounting strategy looks for possible causes of distortion and

biased opinion. The fourth step is to determine the degree of disclosure. If

management doesn’t disclose all the necessary information and make it easily

assessable, it can have a negative impact on the quality of the firms accounting.

This would lead to the firm presenting skewed information to potential investors

and stockholders giving them a misleading idea of what’s going on internally.

The fifth step of the analysis is to identify potential red flags. We will look for any

information presented that could point to any questionable accounting. Finally,

the last step of the analysis is to undo any accounting distortion by restating the

firm’s financials to eliminate any distortions in the financials.

44 | P a g e

Key Accounting Policies

After analyzing the firms within the industry, we have determined the key

accounting policies by focusing on success factors that will provide the company

with a competitive advantage. If key accounting policies can’t be linked to

success factors, it will possibly signal a red flag thus needing to be further

analyzed. The key accounting policies are important because estimations and

forecasting have to be done whenever the financials are created. There are two

types of accounting policies. Type I accounting policies can be directly linked to

the key success factors. In the upscale casual industry we believe economies of

scale, superior customer service, and superior product quality are critical

accounting policies. Type II accounting policies are policies that can potentially

distort our view of the financial position of the company. We feel capital vs.

operating leases, disclosure, and assumptions are the main type II policies.

Type I Accounting Policies

Type I accounting policies can be directly or indirectly related to the key

success factors of a firm. In the upscale casual restaurant industry we have

identified 3 main policies that are economies of scale, superior customer service,

and superior product quality.

Economies of Scale

Economies of scale play an important role in cost leadership. Economies of

scale can be achieved from lowering the fixed cost per unit by increasing output

or production. An idea is to grow a company’s locations. This will lead to larger

purchases from a company’s suppliers. With larger purchases a company can

negotiate short and long term contracts to hedge prices. The Cheesecake Factory

45 | P a g e

has many suppliers and hedges their prices by using contracts. In the

Cheesecake Factory’s 10K, it states how they use short term and long term

contracts for their main commodities. This enables them to get their inputs at a

lower cost and also ensures quality products.

The Cheesecake Factory also maximized economies of scale by using

vertical integration. “Vertical integration of this vital part of our brand gives us

control over the creativity and quality of our desserts and is also more profitable

than buying from a third party.” The Cheesecake Factory has a bakery in

California and North Carolina. We believe by being able to hedge input prices and

produce their own goods allows them to take advantage of economies of scale.

Fiscal Year

2009 2010 2011 2012 2013

Average sales per productive

square foot 830 850 885 887 913

By looking at the table above, we as a group of analysts have concluded

that The Cheesecake Factory is achieving economies of scale by increasing

average sales per square foot. The Cheesecake Factory targets total costs of

about $700-$800 per square foot. We believe by closing non-profitable locations,

increasing menu prices by 1-2% every year, and hedging input costs by

negotiating short and long term contracts have all attributed to increasing their

profits.

On May 19, 2014, The Cheesecake Factory Incorporated announced that

it was entering into an exclusive licensing agreement with an operator in Asia.

This agreement would provide for a minimum of 14 restaurants over the next 10

46 | P a g e

years in various countries. The first restaurant is expected to open sometime in

their fiscal year 2015. (investors.cheesecake.com) CAKE is showing future

expansion growth as well in the present. They’ve increase capital investment

about 38.5% since fiscal year 2011.

Fiscal

Year

2011 2012 2013

Additions to property

and equipment

-

76,746.00

-

86,442.00

-

106,289.00

Superior Customer Service

In the upscale casual restaurant industry, we believe superior customer

service and hospitality is extremely vital to success. Customers pay top dollar for

a meal and it is imperative that they are treated as so. In the Cheesecake

Factory 10-K it states “Our recruitment, selection, training and retention

programs are among the most comprehensive in the restaurant industry,

enabling us to attract and retain qualified staff members who are motivated to

consistently provide excellence in guest hospitality. This tells us they put a strong

emphasis on hiring good employees, training them to serve professionally,

focusing on customer retention, and offering customers a superior experience to

make guests return.

47 | P a g e

Superior Product Quality

Superior product quality is extremely important because customers go to a

upscale casual restaurant for the quality of the product and the experience. If

the quality of the product is sub-par then the customer is unlikely to return

because they will feel like they didn’t get their money’s worth. The Cheesecake

Factory makes their products handmade fresh daily using high quality products

and fresh ingredients using innovative and proprietary recipes. (CAKE 10k)

When analyzing information given within the 10k of a company, we can

determine the firm’s financial position among other things. Managers should

present both good and bad information that could help make a decision in the

company’s financial standing. However, what is presented might not be very

transparent. Good disclosure is when information represented in a firms

financials, estimations, and business activities are transparent. Financial

statements can also be misleading due to the amount of flexibility given to a

firm’s management by GAAP. Flexibility allows for estimations to be included and

also allows for management to manipulate certain things to portray a better

financial statement than they currently are in.

Fiscal Year

2009 2010 2011 2012 2013

Intangible assets, net N/A 14,482 14,674 17,829 18,647

Total Assets N/A 1,037,307 1,022,570 1,092,167 1,124,114

0.01396 0.01435 0.01632 0.01658

Goodwill isn’t directly stated in the 10k. As a team of analysts we’ve come

to the conclusion that goodwill is included in intangible assets. Intangible assets

are less than 2% and not at the threshold. Other relevant information that helps

investors make decisions such as discount rates and suppliers should give,

48 | P a g e

however, The Cheesecake Factory doesn’t think it’s too important. They aren’t

supplying enough material and transparent information and can prevent analyst

from being able to see the underlying economic value in business activities. This

is why we have decided the Cheesecake Factory has a low quality of disclosure.

Type II Accounting Policies

The Type II accounting policies lead to distortion. Distortion hides or

covers material information and can lead investors to believing a firm is doing

better or worse than it actually is. In the upscale casual restaurant industry we

believe leasing is the most important policy.

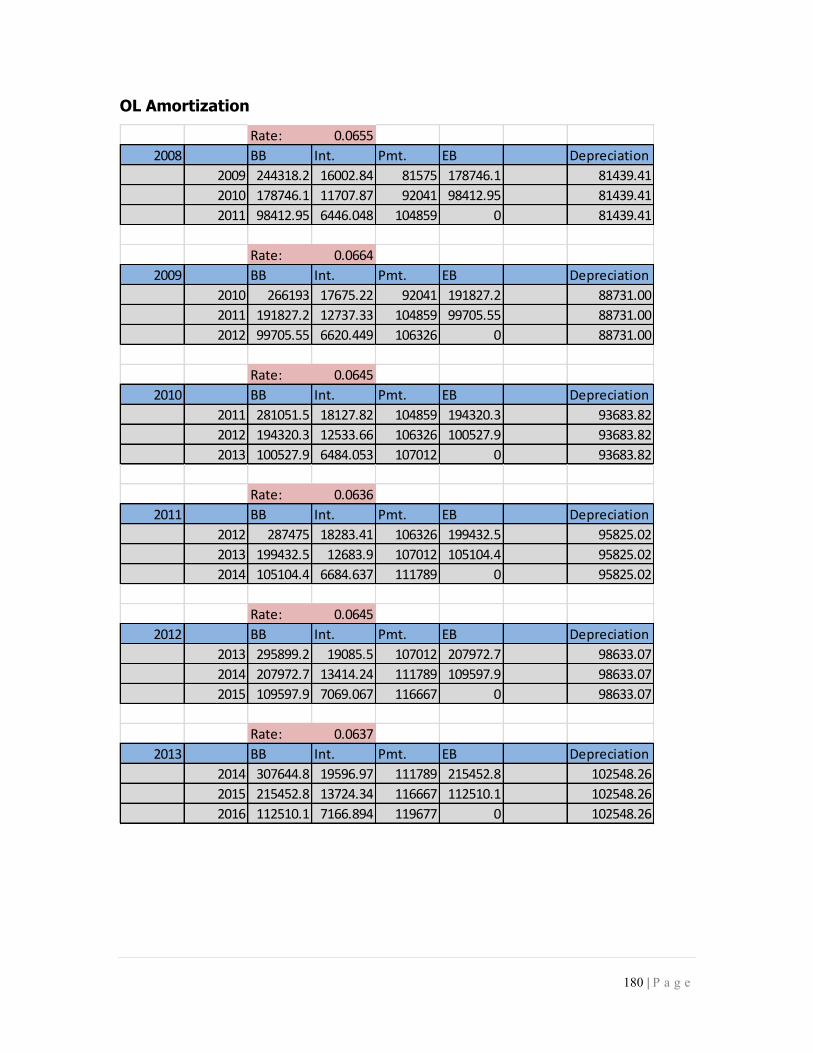

Operating Leases

A lease is an agreement between two parties that allows the usage of

land, buildings, property or equipment. There are two primary methods of

recording your lease. The first is a capital lease which recognized the asset and

liability on the balance sheet. The other method is an operating lease. The

operating lease does not claim the rights or ownership on the balance sheet and

just expenses the rent under operating expenses.

“Capital leases are considered equivalent to a purchase, while operating

leases cover the use of an asset for a period of time and are treated by the

lessee as periodic expenses.” (fasab.gov) A capital lease shows transfer of

ownership, rights, and liabilities when the lease is signed for. They are shown on

the balance sheet as an asset under PPE and a liability such as Capital Leasing

Liability. There are four main criteria that constitute a capital lease:

Ownership of Property – The lease will transfer ownership to the

person leasing at or before the ending lease date.

Bargaining Option – The lease allows for purchase of the lease

49 | P a g e

property at a discounted price.

Estimated Economic Life – The leasing term must be equal to or

greater than 75% of the estimated life of the property.

Fair Value – “The present value of rental and other minimum lease

payments, excluding that portion of the payments representing

executory costs, equals or exceeds 90% of the fair value of the

leased property.” (fasab.gov)

If the leasing term is after 75% of the estimated economic life then

the last two do not apply.

Operating leases are the only type of lease used by The Cheesecake

Factory. An operating lease “is an agreement conveying the right to use property

for a limited time in exchange for periodic rental payments.” (fasab.gov) They do

not assume the risk or ownership of PPE nor does it recognize the PPE on the

balance sheet. Rent payments are just expensed as an operating expense on the

income statement. Operating leases have less disclosure. By not having

operating leases on the balance sheet it also doesn’t show any type of A/D or

interest expenses for the capital. This can lead to understating expenses thus

overstating net income and retained earnings.

Conclusion

In conclusion, a firm can look at their key success factors and distortion

and then determine their type I and type II accounting policies. There will always

be estimations and distortion within financial statements due to flexibility. We

were able to identify firms with biased and misleading accounting. Because of

this we are able to look past the distortion and see the true value of the

financials.

50 | P a g e

Assess Degree of Accounting Flexibility

Accounting flexibility is the level at which managers can choose their

company's accounting policies. Accounting flexibility is dependent upon GAAP

and the other standards that financial filings must follow. Highly flexible

companies have more room to account in ways that the managers see fit. This

will generally result in the company looking much better than if the accounting

flexibility were lower. The accounting flexibility of the Cheesecake Factory, as

well as the industry, have been analyzed below by looking at three key business

activities that are affected by the accounting flexibility of the companies. The

two business activities that we have analyzed are Operating vs. Capital Leases

and Goodwill.

Operating vs. Capital Leases

The restaurants that make up this industry have a high amount of

flexibility with the decision to classify their leases as operating or capital leases.

Capital leases show up on the financial reports while operating leases do not.

Capital leases are accounted for as an asset and liability when the contract gets

finalized while operating leases get treated as rent expense to be recorded each

period as it gets paid. The problem with this is that the company makes a large

asset deposit in prepaid rent. Cheesecake Factory records each lease it signs as

an operating lease and the industry as a whole classifies almost all of their leases

as operating leases (CAKE 10-K, Darden 10-K, Brinker 10-K, BJ's 10-K). The high

degree of accounting flexibility that these companies have in their choice of lease

classification results in misstated financials. These misstatements will be

represented in the table below.

51 | P a g e

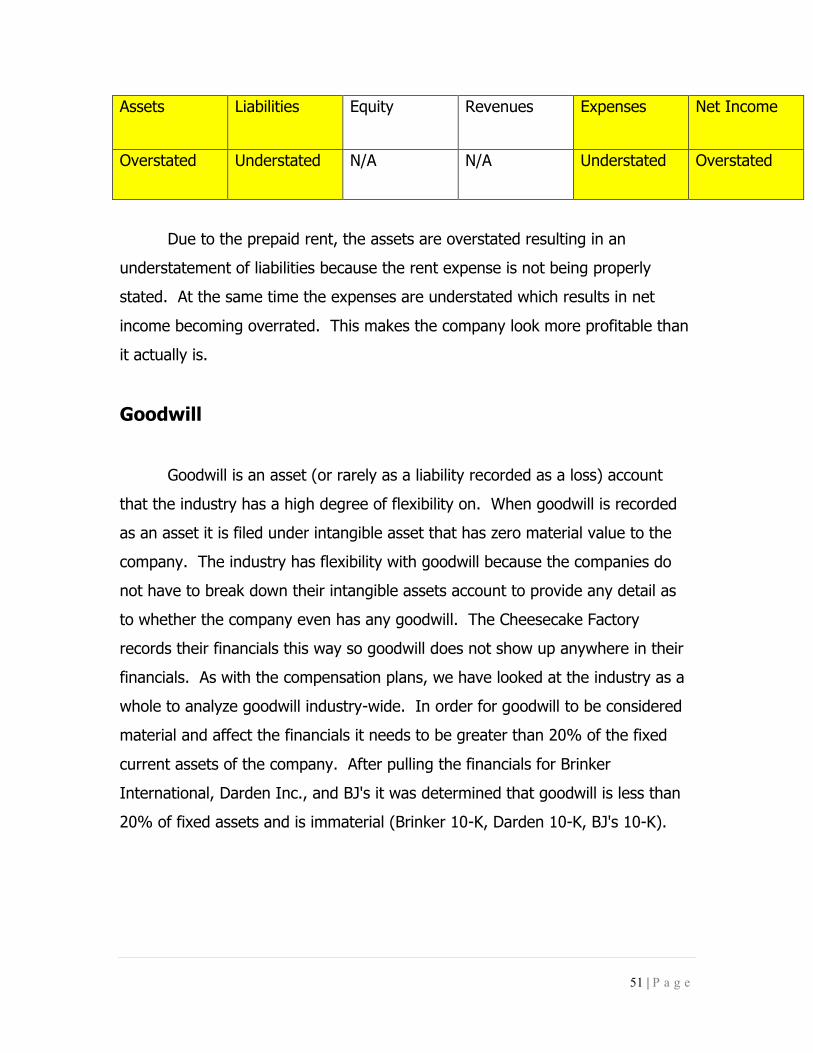

Assets Liabilities Equity Revenues Expenses Net Income

Overstated Understated N/A N/A Understated Overstated

Due to the prepaid rent, the assets are overstated resulting in an

understatement of liabilities because the rent expense is not being properly

stated. At the same time the expenses are understated which results in net

income becoming overrated. This makes the company look more profitable than

it actually is.

Goodwill

Goodwill is an asset (or rarely as a liability recorded as a loss) account

that the industry has a high degree of flexibility on. When goodwill is recorded

as an asset it is filed under intangible asset that has zero material value to the

company. The industry has flexibility with goodwill because the companies do

not have to break down their intangible assets account to provide any detail as

to whether the company even has any goodwill. The Cheesecake Factory