Embed Size (px)

Citation preview

JLL Breakfast Talk:

Top ASEAN markets for 2017

Jakarta 2017 OutlookTodd Lauchlan

Country Head, Indonesia

Economy Improving

Cyclical Recovery under the way

Will translate into increased demand

Politics stable / Ease of doing business improving

GDP growth in Indonesia

Source: Oxford Economics; Bank Indonesia; JLL Research

USD/IDR exchange rate

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017F

GD

P G

row

th

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

16,000

Dec-06

Dec-07

Dec-08

Dec-09

Dec-10

Dec-11

Dec-12

Dec-13

Dec-14

Dec-15

Dec-16

IDR

per

US

D

Office Supply Increasing

CBD supply, demand and occupancy

Source: JLL Research

70%

75%

80%

85%

90%

95%

100%

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Occupancy

Sqm

Net Absorption New Supply Occupancy

Flight to quality underway

Overall demand forecast to improve

Office Rents to continue falling in 2017

Cyclical Recovery under the way

Will translate into increased demand

Politics stable / Ease of doing business improving

Source: JLL Research

CBD Rents

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

IDR

per

sqm

per

mon

th

Premium Grade A

Office Projects

Capital Place IFC 2

Office Outlook

Demand to improve

Occupancy to fall

Rents to bottom 2018/2019 then recover

Older buildings to suffer

Residential Demand Forecast to Recover

Condominium Sales per annum

Market hit badly by luxury tax changes

Tax amnesty should bolster demand

Structural demand remains

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Uni

ts

Source: JLL Research

Residential Prices to remain flat as long as sales are low

Condominium prices by segment

Prices remain stable

Competition intense for limited buyers

Good projects selling well

Source: JLL Research

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

45,000,000

50,000,000

55,000,000

60,000,000

1Q

09

2Q

09

3Q

09

4Q

09

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

IDR

per

sqm

Lower middle Middle Upper High-end Luxury

Residential Projects

West Vista

Residential Outlook

Demand to improve

New Launches to achieve better absorption

Market has bottomed recovery on the way

Retail Demand likely to continue to be supply driven

Very limited Supply

Rising rents and occupancy

Food and Beverage / Cosmetics strong / luxury weak

Source: JLL Research

Retail supply, demand and occupancy

70%

75%

80%

85%

90%

95%

100%

0

50,000

100,000

150,000

200,000

250,000

300,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Occ

upan

cy

Sqm

New Supply Net absorption Occupancy rate

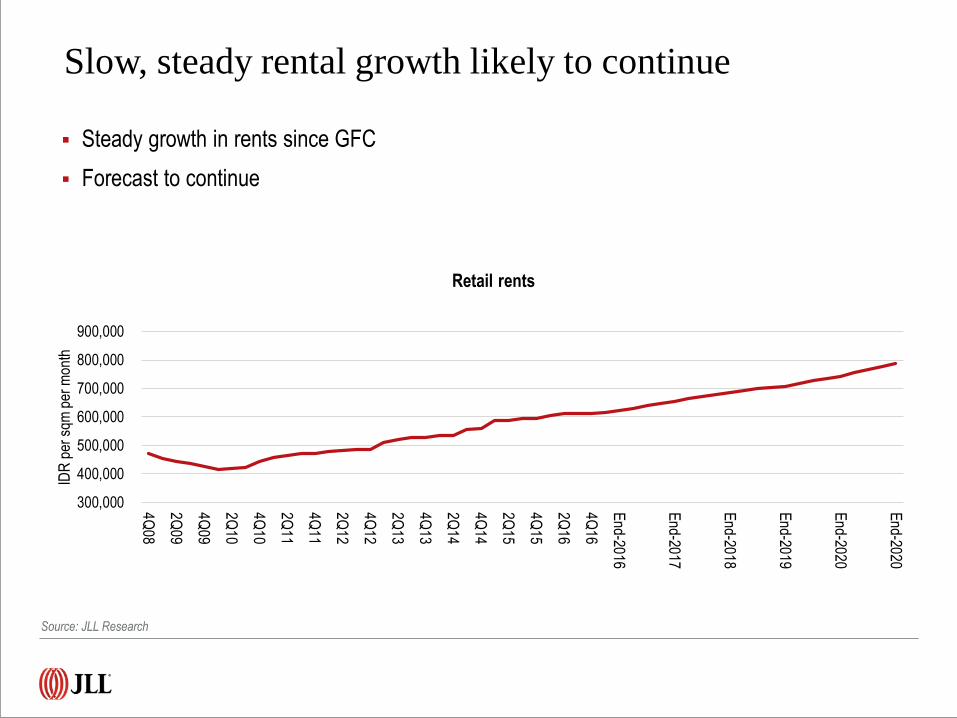

Slow, steady rental growth likely to continue

Steady growth in rents since GFC

Forecast to continue

Source: JLL Research

Retail rents

300,000

400,000

500,000

600,000

700,000

800,000

900,000

4Q08

2Q09

4Q09

2Q10

4Q10

2Q11

4Q11

2Q12

4Q12

2Q13

4Q13

2Q14

4Q14

2Q15

4Q15

2Q16

4Q16

End-2016

End-2017

End-2018

End-2019

End-2020

End-2020

IDR

per

sqm

per

mon

th

Retail Outlook

Supply Limited

High Occupancy

Rents to Grow

Logistics Market Evolving Rapidly

- Partnership announced in 2015;

- 500,000 sqm of space to be developed

- Three warehouse reportedly under

construction

In early 2016,

Alibaba

acquired a

controlling stake

in Lazada

Mitsui and other investors:

USD 100 million investment

in MatahariMall

Market entry expected in short-term

Also expanding…

Source: JLL

Jakarta Hotels: Upscale Trading Performance

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 YTD Oct2015

YTD Oct2016

Occ

up

ancy

(%

)

AD

R /

Rev

PA

R (I

DR

)

ADR (IDR) RevPAR (IDR) Occupancy (%)Source: STR Global

Note: Rates inclusive of Service Charge

Arrival numbers continue to grow, new visa rules providing support

50% overall occupancy forces rates down

Bali Hotels: Upscale Trading Performance

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

-

20

40

60

80

100

120

140

160

180

200

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 YTD Oct2015

YTD Oct2016

Occ

up

ancy

(%

)

AD

R /

Rev

PA

R (U

SD

)

ADR (USD) RevPAR (USD) Occupancy (%)

Source: STR Global

Note: Rates inclusive of Service Charge

Arrival numbers growing strongly .. up 23.5% YTD

Rates up but supply keeping rates increases in check

Summary

Huge Potential

Infrastructure / Investment driven growth

Urbanisation / Demographics

Logistic / Retail – Top Picks

Vietnam 2016 review and 2017 outlook:

Positive year aheadStephen Wyatt

Country Head, JLL Vietnam

Vietnam Economic Review

20

Source: GSO, Vietnam National Administration of Tourism.

FDI

▲7.1%y-o-y

▲

CPI Intl. Tourist

Credit Growth Interest Rate

y-o-y

6% - 9%9% - 11%

GDP

Vietnam Economic Review

21

South Korea Japan Singapore China

$1.52bnewly registered capital

Real Estate ranked #3

59 newly registered projectsTop FDI Countries

FDI in 2016 By Economic Activities64%

8%

Manufacturing

Retail and whole sale

7% Real estate

4% Technology

18% Others

Source: FIA Vietnam

Vietnam Economic Review

22

0

1

2

3

4

5

6

7

8

India Vietnam China Philippines Indonesia Malaysia Thailand NewZealand

SouthKorea

Singapore Hong Kong Australia Taiwan Japan

y-o-y (%)Real GDP Growth

-1

0

1

2

3

4

5

6

India Vietnam Indonesia Philippines Malaysia Hong Kong China Thailand Australia SouthKorea

NewZealand

Taiwan Singapore Japan

y-o-y (%)CPI Inflation

2016E 2017F

Source: Oxford Economics

Ho Chi Minh City Office Market Overview

‘000 sqm

1,748,843

Total Supply in 2012-2016 (NFA, Sqm)

Source: JLL Research

1,422,768 1,518,357 1,590,035

1,700,616

0

500

1,000

1,500

2,000

2012 2013 2014 2015 2016

. Grade A Grade B Grade C

45%

44%

11%

Ho Chi Minh City Office Market Overview

54 bps

468bps 121bps

211bps

Occupancy Rate

Grade A Grade B95.30%

93.60%

70%

75%

80%

85%

90%

95%

100%

2012 2013 2014 2015 Q1 Q2 Q3 Q4

2016

Grade A Grade B

Source: JLL Research

38.7

22.0

0

5

10

15

20

25

30

35

40

45

2012 2013 2014 2015 Q1 Q2 Q3 Q4

2016

Grade A Grade B

Ho Chi Minh City Office Market Overview

0.2%

1.9% 6.0%

0.8%

Average Rental Rate (US$/sm/month)

Grade A Grade B

Source: JLL Research

Ho Chi Minh City Office Market Overview

43%

50%

7%

Relocation New set-up transactions

Renewals and expansion

2016

Top 5 Industries

43%

50%

7%

201650%

30%

20%

2015

Finance Services

Law

Manufacturing

FMCG

IT

Source: JLL Research

Saigon Centre Phase IIDistrict 1

32,000 sqm

Deutsches HausDistrict 1

26,400 sqm

Etown CentralDistrict 4

35,000 sqm

Viettel CentreDistrict 10

49,500 sqm

Ho Chi Minh City Office Market Overview

127.0K 74.9K 160.0Ksqm (NFA) sqm (NFA) sqm (NFA)

2017 2018 2019 onward*

Grade A Grade B Grade C

Future Supply 2017-2019 Upcoming Projects

Source: JLL Research

*Future supply 2019 onward are tentative and may be subject to change depending on change in development plans.

Ho Chi Minh City Apartment Market Overview

28

35,928FY 2016

New Launches per Annum (Units)

FY 2015 24,5729,720

8,896

8,438

8,874

7,500

8,000

8,500

9,000

9,500

10,000

1Q16 2Q16 3Q16 4Q16

New Launches per quarter (units)

Source: JLL Research

Ho Chi Minh City Apartment Market Overview

33,996FY 2016

FY 2015 23,7938,974

7,798

8,438

9,091

7,000

7,500

8,000

8,500

9,000

9,500

1Q16 2Q16 3Q16 4Q16

Units Sold per quarter (units) Units Sold per annum (Units)

Source: JLL Research

Ho Chi Minh City Apartment Market Overview

1,527

1,228

500

700

900

1,100

1,300

1,500

1,700

2011 2012 2013 2014 2015 1Q16 2Q16 3Q16 4Q16

USD/sqm

Primary prices Secondary prices

1,527858

1,474

2,287

4,179

0

500

1000

1500

2000 2500 3000

3500

4000

4500

5000

1,228782

1,379

2,1074,200

0

500

1000

15002000 2500 3000

3500

4000

4500

5000

Average selling prices (US$/sqm) Primary Prices (USD/sqm)

Secondary Prices (USD/sqm)

Affordable Mid-end Premium Luxury

Source: JLL Research

26%

8%

6%28%

8%

20%

4%

13%

8%

14%

10%13%

6%

5%

19%

2015

2016

Ho Chi Minh City Apartment Market Overview

14%

40%

45%

2011 2012 2013 2014 2015 2016

Affordable Mid-end Premium Luxury - less than 1%

41.6K 52.8K 59.7K 67.1K 75.8K 94.1Kunits units units units units units

Total Stock, 2011-16 New launches by Districts

Source: JLL Research

Ho Chi Minh City Apartment Market Overview

D1MENSION - CAPITALAND

“ First residential project in

Vietnam to offer property

management and concierge

services by The Ascott Limited“

SERENITY SKY VILLAS – SONKIM LAND

“ New concept – “Sky Villa”

“ New direction for Elite lifestyle”

Ho Chi Minh City Retail Market Overview

418,350 445,350472,450

630,384

0

100

200

300

400

500

600

700

800

900

2012 2013 2014 2015 2016

. Non-CBD CBD

‘000 sqm

814,435

Total Supply in 2012-2016 (NFA, sqm)

Source: JLL Research

26%

74%

Ho Chi Minh City Retail Market Overview

100bps

250bps 120bps

70bps

Occupancy Rate

CBD Non-CBD

87.0%

92.6%

80%

84%

88%

92%

96%

2012 2013 2014 2015 Q1 Q2 Q3 Q4

2016

CBD Non-CBD

Source: JLL Research

Ho Chi Minh City Retail Market Overview

71.0

37.6

0

20

40

60

80

2012 2013 2014 2015 Q1 Q2 Q3 Q4

2016

CBD Non-CBD

Average Rental Rate (US$/sm/month)

0.7%

0.9% 3.8%

0.5%

CBD Non-CBD

Source: JLL Research

2017 2018 2019 onward *

CBD Shopping Centres Non-CBD Shopping Centres

Ho Chi Minh City Retail Market Overview

45.7K 83.6K 45.0Ksqm (GFA) sqm (GFA) sqm (GFA)

Léman C.T Plaza

Open in 2017

Vincom Landmark 81

Open 2018

12,000 sqm 46,345 sqm

Future supply in 2017-2019 Typical Future Shopping Centres

Source: JLL Research

*Future supply 2019 onward are tentative and may be subject to change depending on change in development plans.

Ho Chi Minh City Retail Market Overview

NEW LIFESTYLE SHOPPING MALLS & FOOD COURTS

Rubik Zoo @ Saigon Zoo

5,000 m2 & over 300 kiosksEco Box Mall @ Tan Phu

3,600 m2 & 300 kiosks

Taka Plaza - Sense Market @ 23/9 Park

2,000 m2 & 250 kiosks

Asiana Food Town

@ 23/9 Park

1,500 m2 & 100 food courts

Food Square

@ Near Big C Tan Phu

1,000 m2 & 70 food courts

Cocochin Food Court

@ Nguyen Hue Pedestrian Street

1,200 m2 & 15 food courts

Street Food Market

@ Ben Thanh Market

700m2 & 70 food courts

Source: JLL Research

INCREASING INTERNATIONAL TOURIST ARRIVALS INTO VIETNAM

affordability compared to other neighbouring destinations.

marketing campaigns to promote the country’s tourism since 2010.

rising disposable incomes.

Hotels: Vietnam International Visitor Arrivals

Source: Vietnam National Administration of Tourism Board

Hong Kong

▲ 67.5% y-o-y

South Korea

▲ 38.7% y-o-y

10,013

26.0%

0%

10%

20%

30%

40%

50%

60%

0

2,000

4,000

6,000

8,000

10,000

12,000

2009 2010 2011 2012 2013 2014 2015 2016

Foreign Visitors Growth Rate (%)

China

▲ 51.4% y-o-y

Ho Chi Minh City Hotel Market Overview

0%

20%

40%

60%

80%

100%

0

40

80

120

160

200

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 YTDOct

2015

YTDOct

2016

Occ

up

ancy

(%

)

AD

R /

Rev

PA

R (

US

D)

ADR (USD) RevPAR (USD) Occupancy (%)

Source: STR Global

Note: Rates inclusive of Service Charge, Marketwide number

Ho Chi Minh City Hotel Market Overview

MAJESTIC

(extension)

District 1

RITZ CARLTON

District 1

OKURA PRESTIGE

HOTEL

District 1

LAVENUE CROWN

District 1

353 Units 250 Units 250 Units 235 Units

Typical Future 5-STAR Hotels From 2017 ONWARD

Source: JLL Research

*Future supply 2019 onward are tentative and may be subject to change depending on change in development plans.

• Improving InfrastructureImprovements to the city’s infrastructure such as the new metro line and a proposed new airport in Long Thanh

will benefit the hotel and tourism market in the mid-to-long term when these infrastructure are completed.

• Slow SupplyThe supply pipeline for further hotel construction in HCMC has slowed, comprising 1,941 rooms from 2016 onwards. Continued FDI from Japan, China, and South Korea into the country should help to boost corporate demand.

We have identified 16 new hotel projects from 2017 to 2019, supplying approximately 3,500 rooms. More than 700 rooms from five existing three to four star hotels are also awaiting ratings approval

• Strong Growth in Number of TouristsThe country had 62 million domestic travelers in 2016 with total revenue at US 18 billion according to the Vietnam

National Administration of Tourism. Vietnam welcomed its 10 millionth annual foreign visitor on December 25th at

Phu Quoc International Airport, the first time the country has recorded 10 million international arrivals in a calendar

year, up 25% year on year.

Ho Chi Minh City Hotel Market Overview - Outlook

2016 M&A – Some Notable Transactions

A&B TOWER

GHOMES

DEVELOPMENT

D1 PRIME SITE

DUXTON

HOTEL

SAIGON

HCMC Hanoi

TNR TOWER

KEANGNAM

HANOI

LANDMARK TOWER

SEDONA SUITES

Source: RCA, retrieved at Jan 2017

Others

THE NAM HAI

RESORT &

SPA

Quang Nam

SIX SENSE

CON DAO - BR

- VT

SANCTUARY HO

TRAM - BR - VT

THE MANOR

CENTRAL PARK

INTERNATIONAL

CENTRE

BUILDING

KUMHO

ASIANA PLAZA

NOVOTEL

SAIGON CENTRE

EMPIRE CITYSOMERSET

VISTA

~$921mTotal Value Transactions In 2016

2016 M&A – Some Notable Transactions

BIG RETAIL M&A TRANSACTIONS 2016

NEW JVS/ FUNDS FORMED UP

Metro Group completes sale of Metro Cash & Carry Vietnam to TCC

Central Group announces the purchase of Zalora Thailand

French retailer Casino to sell Big C Vietnam

HK’s Sunwah to invest $100m in Vietnam, forms JV with Saigon Asset Management

VinaCapital & Warburg Pincus create $300 million JV

CapitaLand sets $500m target for follow-on Vietnam fund

Indochina Capital teams up with Kajima Corporation

Source: DealStreetAsia, VietnamEconomicTimes, Reuter, TheNation, AsiaProperty

Singapore 2017 outlook: Bottom fishingRegina Lim

Advisory and research, Capital Markets

Expect Singapore GDP to grow 2-3% in 2017-2018

GDP expected to grow c.2% in 2017, recovering slightly from the 1.8% in 2016. ASEAN growth on stronger domestic consumption is supportive. Sectors such as business services, IT and tourism-related services are expanding in Singapore.

While office, retail and F&B demand slowed in 2012-2015, we believe these bottomed in 2016 and we expect a modest recovery of 1-2% growth in 2017-2018.

GDP growth in Singapore and South East Asia

45

Source: Dept of statistics, URA, JLL Research estimates

Growth in office, retail, F&B demand

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

Office demand Retail sales F&B receipts

5.94.6 5 5

1.6 2.3 2.6

-4

-2

0

2

4

6

8

10

12

14

16

18

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

E

2018

E

ASEAN Singapore

Singapore consumer price index rose in 4Q16 after two years of deflation. Central Bank expects inflation of 0.5-1.5% in 2017.

This paves the way for MAS to maintain a zero SGD appreciation stance or allow slight appreciation. Consensus estimate 1.46 SGD/USD by end-2017 and end-2018

This should allow interest rates to rise slower than US rates, buffering companies from defaults. SGD 10Y govt bond yield is expected to remain stable at 2.4-2.5% till 2018.

46

Inflation returns, paving way for stable SGD and moderate rates

Inflation (CPI yoy change %) SGD/USD

Source: Dept of statistics, JLL Research

0.50

0.55

0.60

0.65

0.70

0.75

0.80

0.85

1Q95

1Q96

1Q97

1Q98

1Q99

1Q00

1Q01

1Q02

1Q03

1Q04

1Q05

1Q06

1Q07

1Q08

1Q09

1Q10

1Q11

1Q12

1Q13

1Q14

1Q15

1Q16

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

CPI MAS Core Inflation Measure

Foreign manpower policy is gradually loosening

In 2005-2011, Singapore attracted 50,000-80,000 skilled workers but the rapid increase in population and lack of infrastructure resulted in citizen discontent, and curbs in 2012-2015.

We expect a gradual relaxation on inflow of skilled workers, which increased from late 2015. This is expected to boost demand for office, retail and residential property.

47

Source: Dept of statistics, URA, JLL Research estimates

95

-3

4

1118

17 15

-1 -1 -23 2 2 1

82

(10)

(5)

-

5

10

15

20

25

30

35

1H08

2H08

1H09

2H09

1H10

2H10

1H11

2H11

1H12

2H12

1H13

2H13

1H14

2H14

1H15

2H15

1H16

'000

s

PRs Expats

Increase in permanent residents and expats Increase in residents and expats

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

New citizens Perm Residents Expats Total

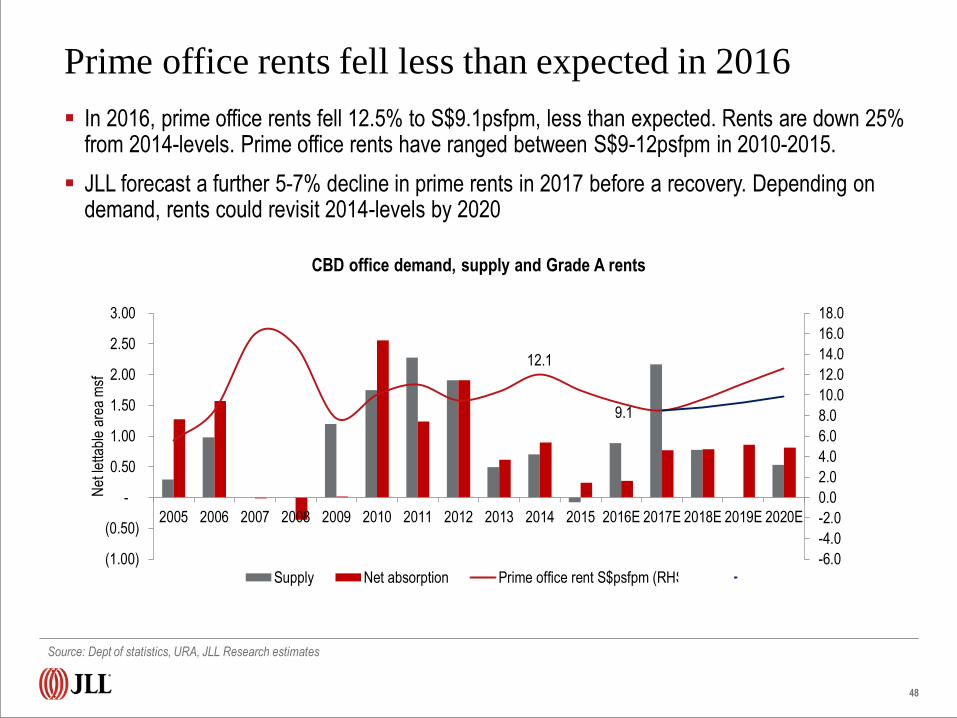

12.1

9.1

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

(1.00)

(0.50)

-

0.50

1.00

1.50

2.00

2.50

3.00

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E 2017E 2018E 2019E 2020E

Net

letta

ble

area

msf

Supply Net absorption Prime office rent S$psfpm (RHS)

Prime office rents fell less than expected in 2016

In 2016, prime office rents fell 12.5% to S$9.1psfpm, less than expected. Rents are down 25% from 2014-levels. Prime office rents have ranged between S$9-12psfpm in 2010-2015.

JLL forecast a further 5-7% decline in prime rents in 2017 before a recovery. Depending on demand, rents could revisit 2014-levels by 2020

CBD office demand, supply and Grade A rents

48

Source: Dept of statistics, URA, JLL Research estimates

Leasing of 2016-2017 completions healthy

In 2016, new office buildings attracted stronger than expected pre-commitments as tenants relocate from stock with smaller floor plates in a “flight to efficiency”

Overall, about 50% of the office space in buildings completing in 2016-2017 have been leased.

Pre-commitment rates of buildings completing in 2016-2017

49

Source: Dept of statistics, URA, JLL Research estimates

83%

34%

50%

40%

3% 0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

-

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

Tanjong Pagar Centre3Q16

DUO 4Q16 Marina One 1Q17 UIC Building 1Q17 Frasers Tower 2Q18

Net

letta

ble

area

(m

sf)

Net lettable area (sf) Precommitment %

Supply after 1H17 is low especially in CBD

In 2017-2020, office completions in the CBD is expected to be low at 0.95msf p.a., 40% lower than the supply in 2010-2016. The 5-year and 10-year average annual absorption rate for CBD office is 0.98msf and 0.87msf respectively.

50

Source: MAS, JLL Research estimates

Singapore office building completions

2010-16 avg CBD: 1.63msf

2017-2020E avg CBD: 0.95msf

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2010 2011 2012 2013 2014 2015 2016E 2017E 2018E 2019E 2020E

Offi

ce N

LA (

msf

)

CBD Strata Decentralised

Land prices rose sharply in 2H16, signalling optimism

Redevelopment schemes in 2H15-1H16 for CPF Building, Afro Asia Building and Park Mall pegged 99-year CBD commercial land prices at c.S$1,170-1,300psfppr.

In Nov 16, the Central Boulevard site was sold for S$1,690psfppr. The developers with the top 4 bids at S$1,400psfppr and above likely expect prime rents to rise 30% to S$12psfpm over the next 5 years.

51

Source: URA, JLL Research estimates

Govt land sale prices in Marina Bay area

Frasers Tower S$1,113psf

(4 bids)

SBF CentreS$ 882psf (3 bids)

Guoco Tower S$1,006psf

(6 bids)

Asia Square 2, Dec 07 S$ 780psf (2 bids)

Asia Square 1, Sep 07S$ 1,409psf (3 bids)

Mapletree Anson, Jul 07 S$ 1,022 psf (5 bids)

Twenty Anson, Aug 07S$ 941psf (3 bids)

MBFC S$405 psf (9 bids)

Sail@Marina BayS$ 227psf (2 bids)

ORQ S$290psf (2 bids)

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

07/1998 04/2001 01/2004 10/2006 07/2009 04/2012 12/2014 09/2017

South Beach, Jul 07

S$1,069 psf (2 designs)

Central Boulevard, Nov 16

S$1,690 psf (7 bids)

Buy office assets when sentiment, occupancy is weak

Given the cyclical market, buying assets when vacancy and pessimism is high has paid off.

In 2002-2004, buying an office building and selling it in 5 years would yield an average annual return of 18%. In 2009-1H2010, the same strategy would yield a 11% annual return.

We expect vacancy rate to rise above 12% in 2017, providing a buying opportunity.

52

Source: URA, JLL Research estimates

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

2000

2000

2001

2002

2003

2003

2004

2005

2006

2006

2007

2008

2009

2009

2010

2011

2012

2012

2013

2014

2015

2015

2016

E

2017

E

Vca

ncy

rate

Ann

ual r

etur

n ov

er 5

yea

rs

Annual return over 5 years Vacancy rate (RHS)

Prime office cap rates vs rent growth and 10y govt bonds

Counter-intuitively, buying assets make sense when yield spreads are low.

In 2002-2004, spread fell to 100-140 bps before rising to 250 bps in 2005-2008. In 2009-2010, when spread fell back to 180 bps, it was another buying opportunity.

We expect the yield spread to stay narrow at 100bps in 2017. Buying an asset at 3.3-3.9% yield in 2017 could provide 4.5-5.3% by 2020 if prime Grade A rents recover to 2014 levels.

53

Source: MAS, JLL Research estimates

Yoy rental growth 32% -13% -14% -18% -4% 28% 53% 89% -8% -48% 29% 10% -14% 9% 16% -14% -14%

4.96 5.22

4.92

4.07 4.23

5.13 5.25 5.52

5.87

4.34 4.17 4.03 3.56 3.65

4.15 3.83

3.50 3.40 4.37

3.56 3.53

2.92 3.23

2.92 3.36

2.88 2.78 2.37 2.40

2.09

1.46

2.06 2.36 2.44 2.50 2.50

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017E

Prime office yield 10Y Gov bond yield

Retail assets still sought after due to resilience

Singapore retail rents and occupancy (above 97%) are highly resilient amid recessions.

Further, asset yield spread above cost of debt is wide compared to other asset classes.

Retail caprates have compressed slightly in the last five years, as observed through retail REITs’ trading prices and recent transactions in 4Q16.

54

Source: Dept of statistics, URA, JLL Research

5.35%

5.79%

4.70%

4.00%

4.50%

5.00%

5.50%

6.00%

6.50%

2009 2010 2011 2012 2013 2014 2015 Dec2016

Valuation caprate Passing yield Implied cap for retail REITs

3.00% 3.0%

1.5%

4.5%

3.5%

2.0%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

5.00%

Retail Office Residential

Cost of debt Yield spread

Retail yields have compressed slightly over last 5 years Singapore asset yields and spread over cost of debt

Retail supply expected to be low in 2016-2020

Retail supply grew 1.7% CAGR in 1999-2005 as govt sought to increase efficiency of retail space. Supply rose at 7% CAGR in 2006-2014 as malls to attract tourists were built in Orchard Road, Marina Bay. Vacancy rate does not exceed 3%.

The government has disapproved initiation of new retail space since 2013 and capped retail space for new Govt Land Sale sites. Excluding Jewel@Changi, retail supply will grow at 1.4% CAGR in 2016-2020.

55

Source: Dept of statistics, URA, JLL Research

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

(0.50)

-

0.50

1.00

1.50

2.00

2.50

3.00

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

E

2017

E

2018

E

2019

E

2020

E

Vac

ancy

rat

e

Net

letta

ble

area

msf

Ch in stock Ch in demand Vacancy rate

Demand, supply and vacancy rate of retail space in Singapore

Retail and F&B sales recovered slightly in 2H16

After a gradual decline since 2011, retail and F&B sales recovered slightly in 2H16.

We expect stronger tourist arrivals and slightly higher economic growth to boost retail and F&B sales to grow 0-1% in 2017-2018.

Overall, Orchard Road and suburban retail rents have corrected 8% in 2016, but we expect a recovery in 2017-2018.

56

Source: Dept of statistics, URA, JLL Research estimates

Retail sales and F&B receipts

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

E

Retail sales F&B receipts

Prime Orchard and suburban retail rents fell 8% in 2016

15.0 17.0 19.0 21.0 23.0 25.0 27.0 29.0 31.0 33.0 35.0 37.0 39.0

S$p

sfpm

Prime suburban rent S$ psfpm Prime Orchard rent S$ psfpm

Well-positioned assets are gaining market share

While overall retail sales slowed since 2011 and average retail rents fell in 2016, well-positioned assets outperformed.

Larger malls with providing a wide range of retail, F&B, education and entertainment options gained market share and achieved positive rental reversions.

CapitaMall Trust mall traffic, sales and rental revenue Vivocity tenant sales and rental revenue (S$millions)

57

Source: CapitaLand Mall Trust, Mapletree Commercial Trust

180

190

200

210

220

230

240

250

30

32

34

36

38

40

42

44

46

48

50

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

1Q16

2Q16

Rent revenue Vivocity tenant sales (RHS)Singapore retail sales

98

100

102

104

106

108

110

112

2011 2012 2013 2014 2015 1H16

Traffic Tenant sales

Rent revenue Singapore retail sales

Singapore luxury home prices bottomed in 2016

Private luxury residential sale volume and prices

Source: URA, JLL Research

3,288

2,686

-

1,000

2,000

3,000

4,000

5,000

6,000

1,000

1,500

2,000

2,500

3,000

3,500

200

5Q

3200

6Q

1200

6Q

3200

7Q

1200

7Q

3200

8Q

1200

8Q

3200

9Q

1200

9Q

3201

0Q

1201

0Q

3201

1Q

1201

1Q

3201

2Q

1201

2Q

3201

3Q

1201

3Q

3201

4Q

1201

4Q

3201

5Q

1201

5Q

3201

6Q

1

Prime sales S$m (RHS) High-end residential price S$psf

-

1,000

2,000

3,000

4,000

5,000

6,000

2010 2011 2012 2013 2014 2015 2016

S$m

S$2500-3000psf S$3000-3500psf S$3500-4000psf Over S$4000psf

Transactions above S$2,500psf

Singapore luxury home prices have fallen c.20% in the last 3 years, but reached a turning point in 2016.

Transactions above S$2,500psf fell 67% in 2015 compared to 2010/11 after several rounds of property cooling measures. But in 2016, such transactions doubled yoy and recovered to 2011/12 levels

58

0

500

1000

1500

2000

2500

3000

3500

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Singapore PR Foreigner Company

Foreigner buying fell 80% since 2010 but recovered in 2016

Foreigner purchases of units above $2,000psf fell by 80% from 788 units p.a. in 2010-2011

to 160 units in 2015. In 2016, this doubled to 300 units.

Buyers from Indonesia, Malaysia, China, HK and Australia increased 3 times yoy.

Yearly transactions above $2000psf

Source: URA, JLL Research

59

Non-resident buyers of units above S$2,000psf

-

50

100

150

200

250

300

350

400

450

2010 2011 2012 2013 2014 2015 2016

Indonesia Hong Kong Malaysia China

Prime residential prices in London, New York, Hong Kong have continued to rise in the last 5 years. Hong Kong prices are 130% higher than Singapore. New York prices are now 62% higher.

Prime home prices in New York and London were within 10% of Singapore’s prices in 2010. In the last 5 years, these rose 20-25% while those in Singapore fell 20%.

60

Prime residential is compelling compared to other global cities

Source: JLL Research, Corcoran Report 2Q15

53%

Hong Kong, 126%

10%

London, 22%

New York, 62%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

140%

2010 2011 2012 2013 2014 2015 2016

Pric

e G

ap

Prime residential price gap between Singapore and other major cities in US dollars terms

Due to the correction in Singapore residential prices, home price to income ratio in Singapore has fallen from 7.3 in 2010 to 4.8 times in 2015.

In contrast, homes in London, San Francisco, Tokyo and Hong Kong have all become less affordable.

61

Housing affordability in Singapore improved, global prices soared

Source: demographia.com, JLL Research

Home price to income ratio from 2010-2016

7.3

4.8

7.2

8.5

7.2

9.2

7.1

10 9.6

12.211.4

18.1

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

2010 2016

Singapore

London

San Francisco

Tokyo

Sydney

Hong Kong

Cost of buying, holding and selling an USD2m residential property ranges from 15-33% in global cities such as London, New York, Hong Kong.

Cost including additional buyer stamp duty for Singapore is in the middle of the range.

Cost of buying in Singapore is much higher than holding costs.

62

Prime residential transaction costs in line with global cities

Source: JLL Research

Cost of buying, holding and selling a USD2m residential property

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

HongKong

Tokyo Sydney Singapore Paris New York London SanFrancisco

Dubai Shanghai

Cost of buying Holding (5 years) Cost of selling

Supply of luxury prime residential units in districts 9, 10, 11 is expected to grow by 0.5% p.a. in 2017-18

Supply via collective sale for larger redevelopment is unlikely until the current 15% ABSD on land purchases is amended

Completion of residential units in core central region

2280

2,823

1,899 2,043

4,046

2,281

1,300

600267

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

0

1000

2000

3000

4000

5000

2010 2011 2012 2013 2014 2015 2016E 2017E 2018E

Completed units Unsold as at 4Q15 %ch

7

Completions falling to 0.5% p.a.

in 2017-18

Upcoming supply in prime districts is limited

Residential block deals dominated in 2016, continue in 2017-18

64

Close to S$ 2bn of residential units were sold via block deals or structured vehicles in 2016 as developers rushed to meet the deadline to sell units within 2 years of completion (mandated by Residential Property Act). Over S$ 1bn of deals are under negotiation.

As the units that were completed in 2015-2016 and subject to these rules are still high, we expect more of such block deals in 2017-2018.

Unsold residential units in prime areas subject to extension charges

Source: Dept of statistics, JLL Research,

0

100

200

300

400

500

600

700

800

900

2013 2014 2015 2016 2017 2018

Res

iden

tial u

nits

Year of completion

Unsold units Subject to QC charges Seeking block deals

Hotels: Tourist arrivals recovered in 2016

YTD till Nov 2016, tourist arrivals rose 8% y-o-y to 14.9 million but still below the peak in 2013

Mainland China visitors rose by 32% y-o-y, due to improved flight connectivity between Singapore and second-tier Chinese cities.

9.7

11.6

13.2

14.515.6 15.1 15.2

13.814.9

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

0

4

8

12

16

2009 2010 2011 2012 2013 2014 2015 YTD Nov2015

YTDNov2016

Ann

ual G

row

th

Num

ber

of V

isito

rs (

Mill

ions

)

Visitor Arrivals (millions) Annual GrowthSource: Singapore Tourism Board (STB)

Singapore hotels: Upscale Trading Performance

As at YTD October 2016, upscale hotel RevPar fell 2.5%, while occupancy was stable, roomrates fell 3%.

Hotels found increasing room rates with their corporate accounts difficult as companies reduced travel budgets. In particular, the oil and gas industry has been significantly impacted.

New supply in the market has also given corporates more options in selecting where they place their business as new hotels are aggressive in building up their corporate clients.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

$0

$50

$100

$150

$200

$250

$300

2007 2008 2009 2010 2011 2012 2013 2014 2015 YTD Oct2015

YTD Oct2016

Occ

up

ancy

(%

)

AD

R /

Rev

PA

R (S

GD

)

ADR (SGD) RevPAR (SGD) Occupancy (%)Source: STR Global

Note: Rates inclusive of Service Charge

Singapore: Supply is low after 2017

In 2015-2017, hotel supply rose by 20%, resulting in falling room rates. The majority of the new supply are in the midscale and budget segments.

Hotel supply is expected to slow to c.1-2% in 2018-2020, as the government has reduced land release for hotels from 2013. This would be positive for hotel RevPar from 2018.

Singapore continues to grow the tourism sector by developing and investing in new initiatives, which makes it a compelling hotel investment market.

49,719 51,579 55,018 57,172 60,90865,627 69,078

1,2743,357 1,773

2,663 4,719

3,4511,284

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

2012 2013 2014 2015 2016 2017F 2018F

Num

ber

of R

oom

s

Existing Supply Completed Supply New/Future Rooms SupplySource: STB, JLL

Panel Discussion: Top ASEAN markets for 2017

Chris Fossick

Managing Director

Southeast Asia

Todd Lauchlan

Head

Indonesia

Stephen Wyatt

Head

Vietnam

Regina Lim

National Director

Research & Advisory

Mike Batchelor

Managing Director

Hotels & Hospitality

Dr Chua Yang Liang

Head of Research

Southeast Asia