Embed Size (px)

Citation preview

Jefferies 11th Annual Industrials Conference

August 10, 2015

Reliable power when and where you need it. Clean and simple.

2

Safe Harbor Statement This presentation contains “forward-looking statements” regarding future events or financial performance of the Company, within the meaning of the Safe Harbor provisions of the Private Securities Litigation Reform Act of 1995.

These statements relate to, among other things -- growth and diversification of our end markets; strengthened distribution channels; ongoing new order flow; reduced cash usage; growth in revenue, gross margin and backlog; attaining profitability; adequacy of liquidity and capital resources; improved operating leverage and organizational efficiency; new product development; product reliability; shifts to larger markets for our products; benefits from our cost reduction initiatives; performance in light of macroeconomic headwinds; advantages over competing technologies, continued Nasdaq listing; implementation of a new Capstone finance business; collection of reserved accounts receivable; continued opportunities in Russia; improved brand equity and product recognition; and leveraging of lean manufacturing practices. Forward-looking statements may be identified by words such as “expects," "objective," "intend," "targeted," "plan" and similar phrases.

These forward-looking statements are subject to numerous assumptions, risks and uncertainties described in Capstone's Form 10-K, Form 10-Q and other recent filings with the Securities and Exchange Commission that may cause Capstone's actual results to be materially different from any future results expressed or implied in such statements. Because of the risks and uncertainties, Capstone cautions you not to place undue reliance on these statements, which speak only as of today. We undertake no obligation, and specifically disclaim any obligation, to release any revision to any forward-looking statements to reflect events or circumstances after the date of this presentation or to reflect the occurrence of unanticipated events.

3

Why Capstone? Capstone Turbine is the world’s leading developer and manufacturer of

clean-and-green microturbine power generation systems. With over 100 patents and years of advanced engineering,

Capstone offers a comprehensive product line, providing scalable solutions from 30kW to 30MW. Capstone serves six major market

verticals, including Oil & Gas, Energy Efficiency, Renewable Energy, Critical Power Supply, Transportation and Marine.

These award-winning, low-emission energy systems operate on a variety of fuels and are compliant with all current emissions

regulations without after-treatment. Capstone microturbines provide reliable power when and where you

need it. Clean and Simple.

Capstone Investment Highlights

Large, Underpenetrated Vertical Markets and Geographies

Leading Manufacturer of Low Emission, Ultra Reliable, Highly Efficient, Electric/

Thermal Generators

• Microturbines are scalable from 30kW to 30MW and can operate on a variety of gaseous or liquid fuels: natural gas, propane, landfill gas, digester gas, diesel, aviation and kerosene

• Four major design features: advanced combustion technology, patented air-bearing technology, digital power electronics, remote monitoring and advanced control capability

• Optimized performance results in lower emissions, higher reliability and higher total system efficiency over a variable power range and harsh environmental conditions

• Annual addressable market of approximately $15 billion; potential capture of $1.5 billion • Diversified across end markets and geographies – currently in 73 countries, over 8,500 units shipped • Favorable macro trends such as corporate and regulatory trends towards energy efficiency and

stringent emission and fuel standards

Experienced, Proven Management Team

• 90 distributors and 9 OEMs reaching 152 market locations throughout the world • Built from the ground up over the last 8 years and the equivalent of 740 Capstone dedicated employees • As network continues to mature and grow, distributors become more productive and efficient

• Company has significant industry experience at senior leadership and operational levels • Leadership team has combined 113 years of energy industry experience

Growing Installed Base and Compelling Environmental and Value Proposition Enables Increased Market Penetration

• Microturbines are more environmentally friendly and offer lower total cost of ownership versus standard internal combustion engine solutions and lower cost than fuel cells without incentives

• Growing installed base helps drive new customer adoption across verticals and geographies • Broad and scalable product range supporting a number of end markets • Poised to penetrate new verticals (marine, transportation and critical power) and geographies (Middle

East and South America) • Market-leading service offering with 5 & 9 year contracts, provides recurring revenue

Future Revenue Growth, Continued Margin Expansion and Operating Leverage Drive

Path To Profitability

• Stronger, leaner, more flexible and better positioned for rapid growth than ever before • Projected revenue growth, steady margin improvements and positive operating leverage all support path

to profitability; balance sheet supports growth plans • Developing Capstone financial solutions business to leverage top line growth • Two manufacturing plants operating on a single shift, 5 days a week, 35% capacity

Maturing Distribution Network Lays Foundation for Long-Term Growth

4

INITIATIVE GOAL STATUS

Build the Highest Quality Product in the Distributed Energy Industry All Products 99% uptime – 14,000 hr. MTBF.

C30 & C65 currently meet goal. Flagship C200/C1000 Series MTBF improved from 6,500 hours to a projected 9,158 in July. This is from new improvements to the engine, filtration system, stator, electrical system and a new software release. Goal is to reach 14,000 hours by end of the fiscal year.

Increase Global Brand Equity and Product Recognition Drive global brand & product awareness

Recently launched new Capstone website. The intuitive platform is easy-to-use and features a more modern look, intended to serve as a primary resource for market, product and service information. The new design, content and features will help to facilitate a higher level of customer and distributor interaction with an increased use of marketing assets, project case studies and social media.

Improve Efficiency and Effectiveness of our Sales and Marketing Process

Improve project close rate from 11% to 20% of $1.5 billion in identified projects

Rolled out a new distributor key performance indicator (KPI) program to better measure and manage distributor performance and help focus on improving lead generation, project development, customer relationships and drive up order close rates. Conducted third party sales training in four different geographic locations around the world.

Leverage Lean Manufacturing and Organizational Practices

Keep operational costs flat while continuing to leverage the business with top line revenue growth

New leaner C200/C1000 Series manufacturing line with a new engine-building clean room, upgraded test cells, new emission testing equipment and improved manufacturing visual work instructions. These improvements have already led to higher engine yields and lower overtime expenses. Flattened our organizational structure to lower operating costs by eliminating three top-level executive positions that save the company an estimated $2 million dollars annually after severances and one-time termination expenses.

5

Business Strategy Update

6

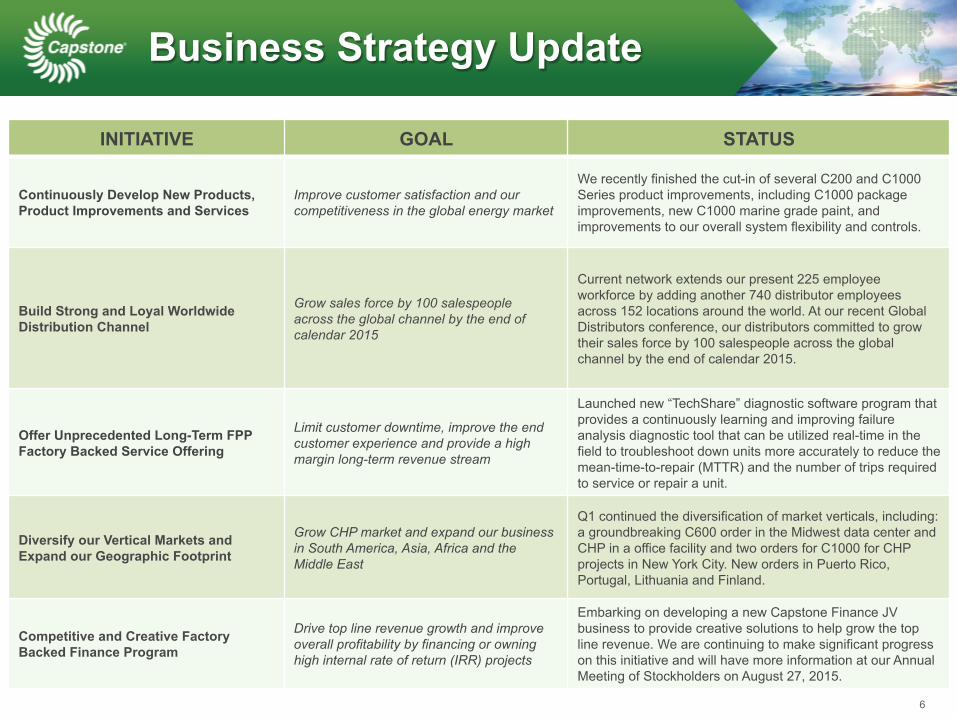

Business Strategy Update

INITIATIVE GOAL STATUS

Continuously Develop New Products, Product Improvements and Services

Improve customer satisfaction and our competitiveness in the global energy market

We recently finished the cut-in of several C200 and C1000 Series product improvements, including C1000 package improvements, new C1000 marine grade paint, and improvements to our overall system flexibility and controls.

Build Strong and Loyal Worldwide Distribution Channel

Grow sales force by 100 salespeople across the global channel by the end of calendar 2015

Current network extends our present 225 employee workforce by adding another 740 distributor employees across 152 locations around the world. At our recent Global Distributors conference, our distributors committed to grow their sales force by 100 salespeople across the global channel by the end of calendar 2015.

Offer Unprecedented Long-Term FPP Factory Backed Service Offering

Limit customer downtime, improve the end customer experience and provide a high margin long-term revenue stream

Launched new “TechShare” diagnostic software program that provides a continuously learning and improving failure analysis diagnostic tool that can be utilized real-time in the field to troubleshoot down units more accurately to reduce the mean-time-to-repair (MTTR) and the number of trips required to service or repair a unit.

Diversify our Vertical Markets and Expand our Geographic Footprint

Grow CHP market and expand our business in South America, Asia, Africa and the Middle East

Q1 continued the diversification of market verticals, including: a groundbreaking C600 order in the Midwest data center and CHP in a office facility and two orders for C1000 for CHP projects in New York City. New orders in Puerto Rico, Portugal, Lithuania and Finland.

Competitive and Creative Factory Backed Finance Program

Drive top line revenue growth and improve overall profitability by financing or owning high internal rate of return (IRR) projects

Embarking on developing a new Capstone Finance JV business to provide creative solutions to help grow the top line revenue. We are continuing to make significant progress on this initiative and will have more information at our Annual Meeting of Stockholders on August 27, 2015.

Product Competitive Advantages

7

Global Market Segments

8

DOWNTURN IN THE OIL MARKETS

CONTINUED STRENGTH OF

THE U.S. DOLLAR

ONGOING GEOPOLITICAL

TENSIONS

DELAYED ORDERS AND SHIPMENTS

RUSSIAN SANCTIONS AND RUBLE

CORPORATE FOCUS ON REDUCING

COSTS

SUSTAINED LOW COST GAS

ENVIRONMENT

DECLINING GRID

RELIABILITY

NEW GAS FLARING REGULATIONS

NEW TIER 4 EMISSIONS

REQUIREMENTS

47MW

2MW

7MW

12MW

2MW

5MW

9

<1MW

16MW

Macro Drivers and Headwinds

Note: The map above depicts megawatts of microturbines shipped for the fiscal year ended on March 31, 2015

Megawatts Shipped FY15 91MW

Historical Financial Results

$0

$25

$50

$75

$100

$125

$150

$82 FY 2011

$109 FY 2012

$128 FY 2013

$133 FY 2014

$116 FY2015

Revenue (in millions)

-5%

0%

5%

10%

15%

20%

-1% FY 2011

5% FY 2012

11% FY 2013

16% FY 2014

16% FY2015

Gross Margin

$0

$50

$100

$150

$200

$106 FY 2011

$139 FY 2012

$149 FY 2013

$172 FY 2014

$166 FY2015

Product Backlog (in millions)

0%

10%

20%

30%

40%

50%

41% FY 2011

34% FY 2012

28% FY 2013

28% FY 2014

43% FY2015

OpEx as % of Revenue

10

SOUTH AMERICA

NORTH AMERICA

EMEA ASIA

Distributor Employees

Distribution Locations

OEMs

Distributors 31

188

42

3

19

124

41

25

283

15

145

28

TOTAL

90

740

152 41

0 5 1 9

Growing Channel to Market

Note: The above employee and location figures are based on data provided by distributors and have not been independently verified.

11

Goal is to add 100 new sales people into our existing global distribution channel

• Contributing to overall gross margin

• Record FPP contract backlog

• 8,500 unit install base provides scalability

• C200/C1000 reliability improving

• Lower product warranty expense

• Improved reliability decreases FPP costs and increases customer satisfaction

Global Customer Footprint

Strengthening Aftermarket

• Supporting 90 Distributors/9 OEM partners in 73 countries

• 3 Capstone service centers globally

• 1,000+ units under FPP and growing

• Establishing regional remanufacturing centers to lower logistical costs and service

• Improved alignment with Sales and Aftermarket

FPP Contract Backlog ($M)

12

$0

$10

$20

$30

$40

$50

$60

$70

$29.7 FY 2011

$33.7 FY 2012

$35.0 FY 2013

$47.2 FY 2014

$61.2 FY 2015

Bearing Housings

Significant Operating Leverage

Operating expenses have remained stable over time despite significant revenue growth. 13

Long Term Goals

14

PAST FY15

PRESENT(1) 1-3

YEARS 3+

YEARS

Gross Margin -24% 17% 25% 35%

Operating Expenses 162% 34% 25% 20%

Operating Margin -185% -17% 5% 15%

Critical Power Market 0% 8% 12% 15%

Mobile Power Market 0% 1% 5% 10%

New Product Offerings C30 C65

C200 C1000 C250 C370

Financing Solutions None 3rd Party Capstone JV Capstone Finance

Positive operating margins driven by improved gross margins and operating leverage.

(1) Present margins for the fiscal year 2015 and exclude $1.2 million inventory charge, $0.7 million of product shipped to BPC and $9.9 million increase in bad debt reserves.

15

Buy – Price Target $1.00

First Revenue Beat In 12 Quarters. Looking For A Return To Double-Digit Revenue Growth In FY16 Despite Challenging Outlook

Accumulate – Price Target $1.00 CPST reports lower-than-expectation 4Q15 results

Outperform – Price Target $0.75 Coming Out of the Abyss; Strong Results and Diversification

Neutral – Price Target $0.33

CPST posted its first revenue beat in 12 quarters with improved gross margins as it navigates a still challenging environment (low oil prices, a strong USD, and a challenging market in Russia). Orders were up Q/Q on strength in CHP and follow-on orders in U.S. O&G, and CPST expects sequential order improvement for the rest of the FY, particularly as it makes progress on its CPST Finance vehicle.

Capstone's results came in better than expected and we believe we have hit a trough for the company as they have trimmed expenses and diversified their product line and geographic exposure. Strength in the CHP segment and decreased dependence on Russian revenue bode well for future revenue growth.

We are encouraged by CPST’s first revenue beat in more than two years, and with recent downside consensus estimate revisions, we see expectations as more reasonable going forward. We continue to remain on the sidelines, however, awaiting further fundamental improvement in CPST’s oil and gas end market. We would also prefer to see CPST make strong progress toward EBITDA breakeven given the company’s cash position.

A Positive Surprise in FQ1

Decreases in booking and backlog are the main causes that made us lower our FY16 sales estimates. Management expects double-digit y-o-y sales growth and strong recovery in 2H16, but, given its track record of guidance giving in the past two fiscal years, we are cautiously optimistic about sales recovery this year.

Eric Stine August 7, 2015

Jeffrey Osborne August 7, 2015

JinMing Liu June 17, 2015

Matt Koranda August 7, 2015

Capstone Analyst Coverage

NASDAQ: CPST

www.capstoneturbine.com